Snuil Bharti Mittal - Rajesh Goli€¦ · PPT file · Web view · 2009-10-10SUNIL BHARTI MITTAL...

72

SUNIL BHARTI MITTAL Pratap Vijay Simha 200604 5 Mayur Wadhwa 200702 9 Rajesh Goli 200704 4 K Md Feroz Irfan 200708 8 Dipankar Datta 200411 9 Ramesh Shanbhag 200604 8 Sudhir Chandrappa 200605 7

-

Upload

trinhthien -

Category

Documents

-

view

236 -

download

0

Transcript of Snuil Bharti Mittal - Rajesh Goli€¦ · PPT file · Web view · 2009-10-10SUNIL BHARTI MITTAL...

SUNIL BHARTI MITTAL

Pratap Vijay Simha 2006045

Mayur Wadhwa 2007029

Rajesh Goli 2007044

K Md Feroz Irfan 2007088

Dipankar Datta 2004119

Ramesh Shanbhag 2006048

Sudhir Chandrappa 2006057

BHARTI INTO RETAIL WITH WAL-MART

WHY RETAIL?

Late mover

Very limited front end retail stores

Currently, focused on cash & carry

IS THIS HOW SUNIL MITTAL OPERATES?

His approach towards Airtel

Choose speed over perfection

First mover

“Get big fast”

The strategy in retail seems to be different!

ABOUT THE INDIAN RETAIL INDUSTRY

Largest industry in India – employment of 8% and contributing to around 10% of the GDP. Currently at $500 billion

The organized retailing sector in India is about 4-5% and growing.

Next wave of growth expected to be driven by semi-urban and rural India

Large number of retail players

Weak and fragmented suppliers

Regulation –

100% FDI is allowed in cash-and-carry wholesale formats

51% FDI is allowed in single-brand retailing

CRITICAL SUCCESS FACTORS

What are the critical success factors in retail?

Low cost

Scale

Location(s)

Ability to navigate through the system

Regional and cultural differences

WHAT'S THE RATIONALE?

Achieve low cost via

Develop ecosystem of suppliers

Better supply chain management

Logistics

Bargaining power with FMCG manufacturers

Scale

Leverage JV partner

Location

Bharti Realty

Acquisition of 10 million sqft by 2015

Low-key entry in a small way in Ludhiana, Punjab

WHAT'S THE RATIONALE?

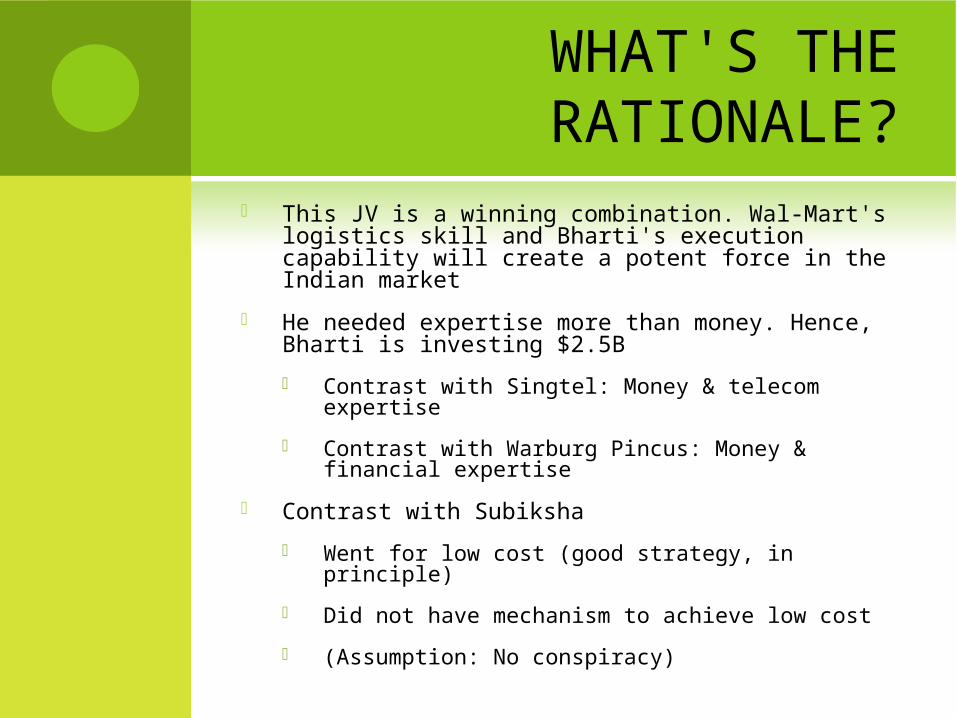

This JV is a winning combination. Wal-Mart's logistics skill and Bharti's execution capability will create a potent force in the Indian market

He needed expertise more than money. Hence, Bharti is investing $2.5B

Contrast with Singtel: Money & telecom expertise

Contrast with Warburg Pincus: Money & financial expertise

Contrast with Subiksha

Went for low cost (good strategy, in principle)

Did not have mechanism to achieve low cost

(Assumption: No conspiracy)

AIRTEL DTH

AGAIN, NOT TYPICAL

Last mover in DTH.

DTH has adoption problems

Unrelated to Airtel’s existing businesses

What has GSM in common with Satellite DTH from an infrastructure point of view?

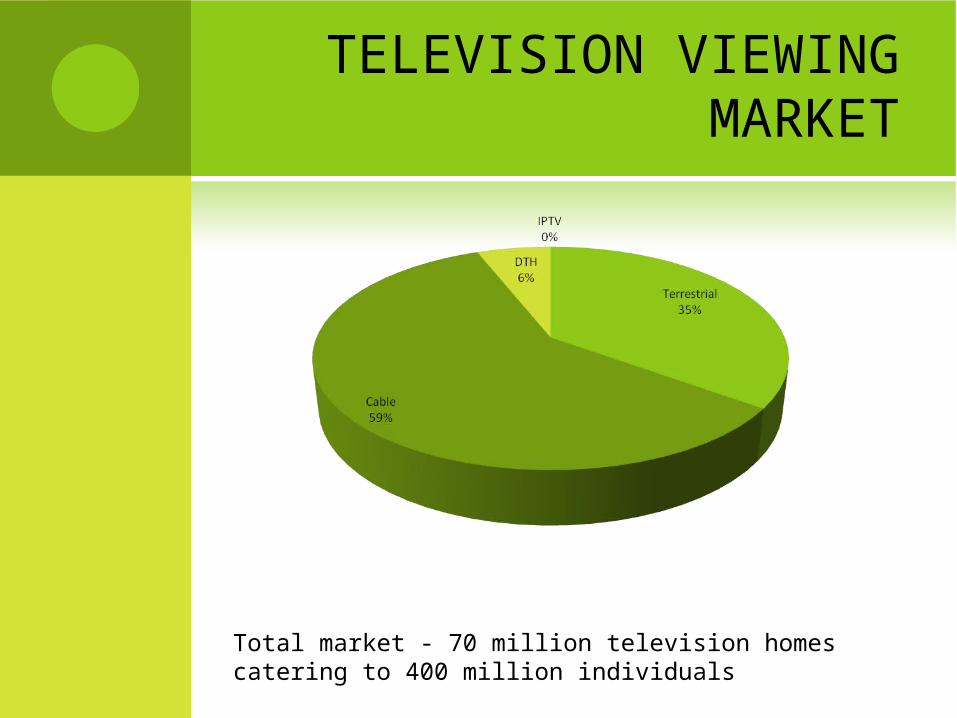

TELEVISION VIEWING MARKET

Total market - 70 million television homes catering to 400 million individuals

DTH INDUSTRY Big four private DTH players has made a head-start. DishTV, TataSky,

Big TV and Sun Direct

Intense price war

Weak financials (all are in loss)

Lack of exclusive content issue

Foreign Investment cap –

DTH: Foreign equity cap of 49% and within that FDI component cannot exceed 20%

Cable: Foreign equity cap on cable industry is at 74% with no limit on FDI

Satellite transponder capacity

Quality of service issue

THE LOGIC Current DTH market is 8 million subscribers and expected to

grow to 40 million by 2015

The industry is evolving

Airtel’s DTH strategy

Integrate its operations with mobile phone, internet and TV and bundle these services

Leverage existing distribution channels and customer service

Provide larger dish antenna to provide higher QoS

Customer switching from existing provider might be difficult

But, what about rural market?

Is it a strong logic for being a late entrant in DTH market? Did he miss the opportunity at the beginning?

THE RHETORIC

Airtel wants to be in all three screens

Mobile

PC

TV

Is it strategic or motto driven?

Or is it the market potential (just as in retail)?

FORMATIVE BUSINESS YEARS

1976 TO 1984 Very complex import and export policies, industrial licensing regime.

Licenses were required right from manufacturing a pin to manufacturing a car

People who found favor with the government could get industrial licenses. The entrepreneurs had to find out small openings in various government policies and move ahead, every now and then turn lucky.

In 1976, Sunil at age of 18, with a capital of 20K, started making Bicycle parts. From 1981 to 1984 he took an agency of Suzuki to import portable generators. Imports became very successful. Made a lot of money and more importantly, set up a large distribution system across the country

In 1984 due to lobbying two business houses(who managed to get licenses to manufacture generators) the government decided to ban import of generators. No amount of pleading or lobbying by a young entrepreneur would have made any difference. So overnight there was no business.

VALUABLE LESSONS LEARNT ?

Did Sunil learnt his valuable lessons from his initial ventures ?

“These were the times when entrepreneurs were at the mercy of government policy, and you always had to be prepared, sitting in your hot seat, to take a jump and plunge into something else as soon as the government hit you with a change in policy.”

ENTRY INTO TELECOM

WHY TELECOM? Mittal saw the huge gap between potential demand &

supply from state run telecom companies

Reforms in telecom sector began in 1980 followed by national telecom policy in 1994 & 1999

Technology advances in 1990s led to better quality of service at lower tariff rates – beginning of a service which could be marketed to the Indian urban masses, and then rural masses

NTP 1994 attempted to provide telephone on demand & telecom services at affordable prices to the Indian populace, and this policy further encouraged Mittal to get into telephony.

WHY TELECOM?

NTP 1999 further reformed the telecom sector with guidelines for internet telephony & broadband

Booming industry in India required high end services like leased lines, ISDN & videoconferencing

OUTSOURCING OF NETWORK AND IT BY BHARTI AIRTEL

UNCONVENTIONAL WISDOM ?

OUTSOURCING OF NETWORK

When every one said network is the critical factor to a telecom service provider Bharti decides to outsource its networks

Do reverse of conventional Wisdom

Does Sunil know the Telecom Business like Baba Kalyani knew Forging ?

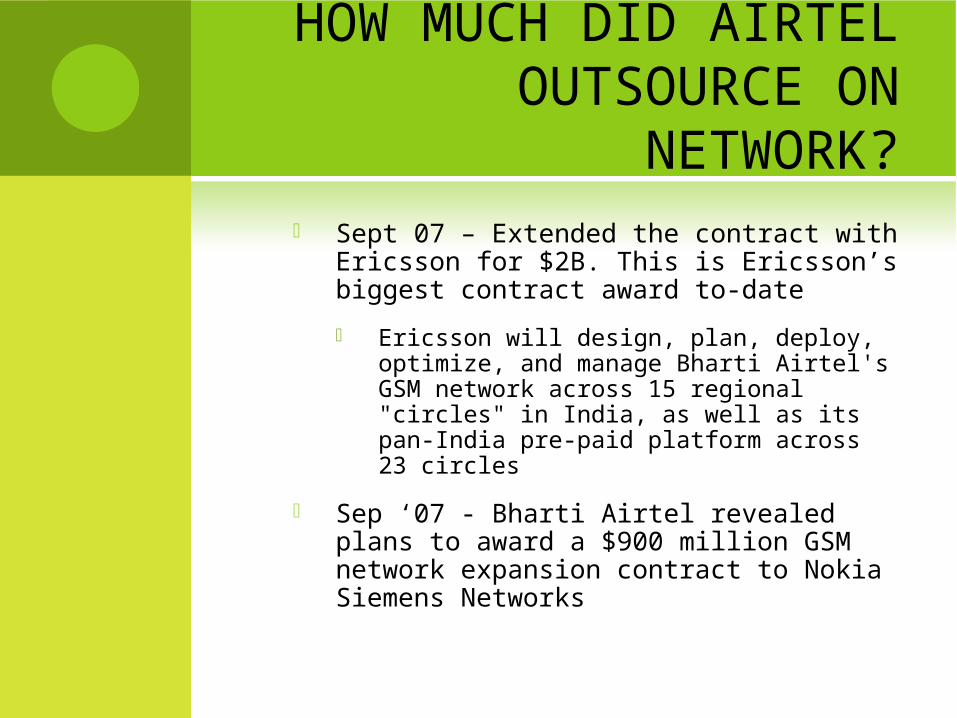

HOW MUCH DID AIRTEL OUTSOURCE ON

NETWORK? Sept 07 – Extended the contract with Ericsson

for $2B. This is Ericsson’s biggest contract award to-date

Ericsson will design, plan, deploy, optimize, and manage Bharti Airtel's GSM network across 15 regional "circles" in India, as well as its pan-India pre-paid platform across 23 circles

Sep ‘07 - Bharti Airtel revealed plans to award a $900 million GSM network expansion contract to Nokia Siemens Networks

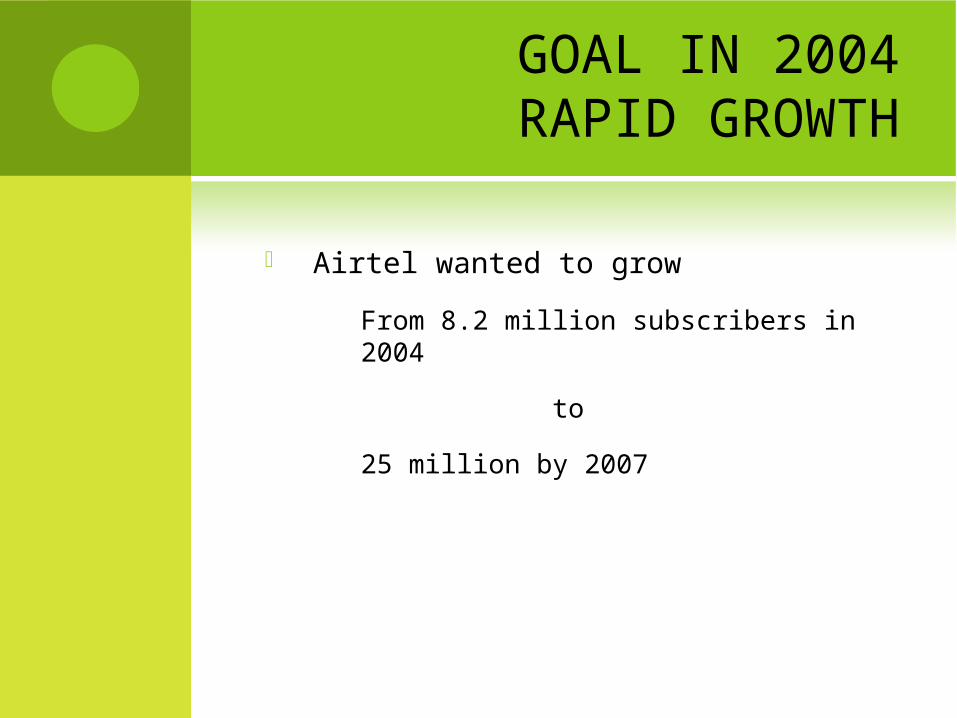

GOAL IN 2004RAPID GROWTH

Airtel wanted to grow

From 8.2 million subscribers in 2004

to

25 million by 2007

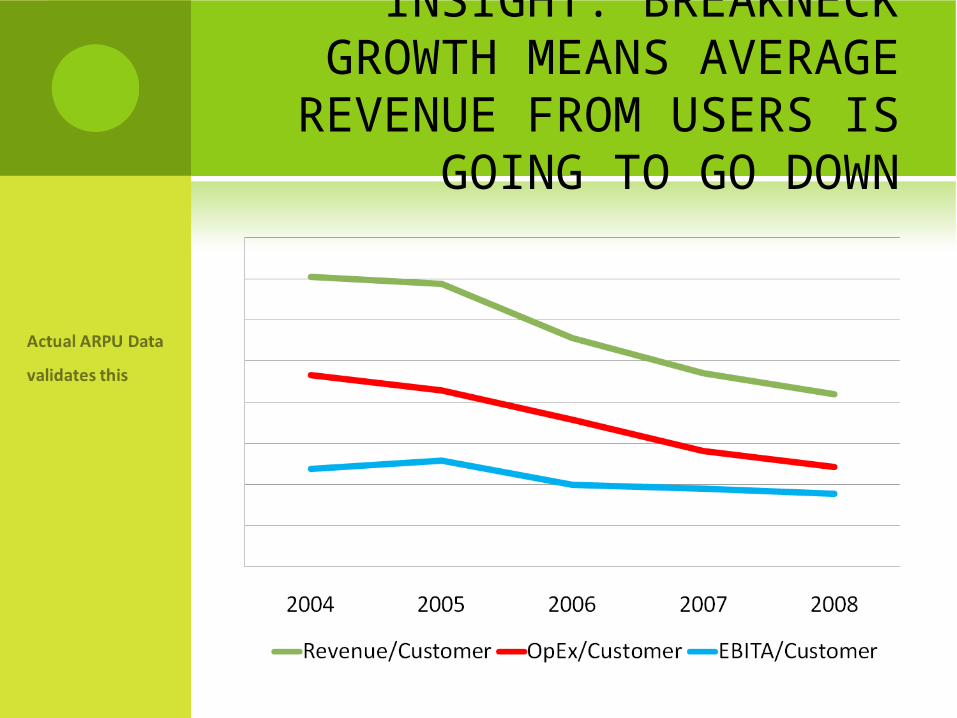

INSIGHT: BREAKNECK GROWTH MEANS

AVERAGE REVENUE FROM USERS IS GOING TO GO

DOWN

QUESTION SET#1

How to drive down operating costs faster than rate at which ARPU will go down?

Can Bharti Airtel run the network and IT and still drive down costs?

Should they outsource? What are the risks? Is this core, non-core or something else?

QUESTION SET#2

If AirTel keeps Network in house, can it deploy and grow fast enough to keep pace?

Is outsourcing better suited for Growth?

OUTSOURCING: PRACTICE IN SEARCH OF THEORY

It is not about “core” vs “non-core”

Rationale

Cost minimization

Resource access

Resource leverage

Risk diversification

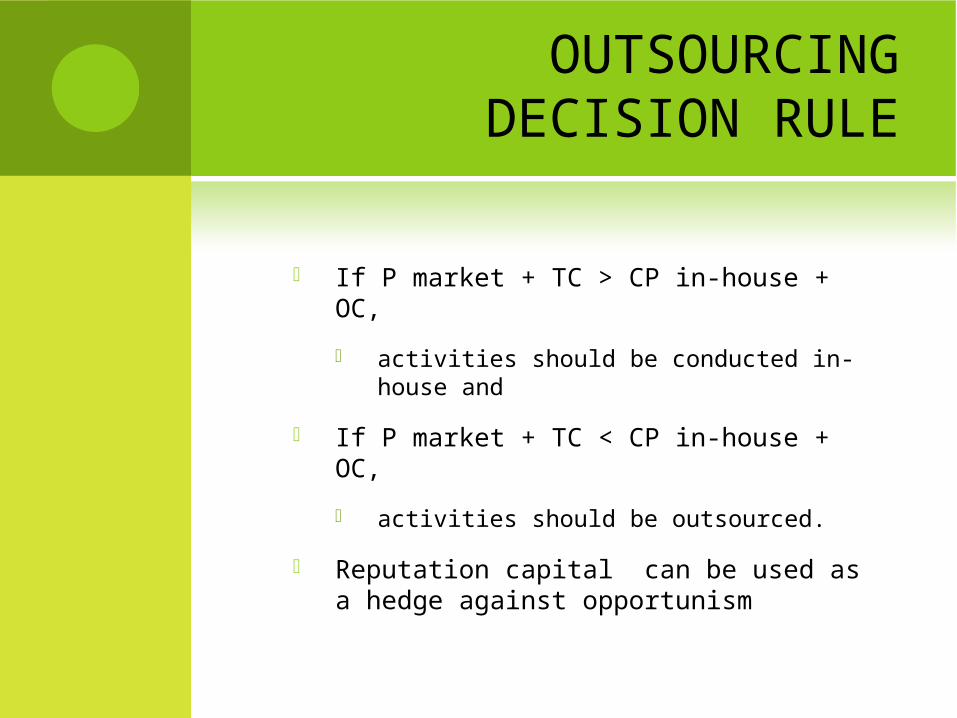

OUTSOURCINGDECISION RULE

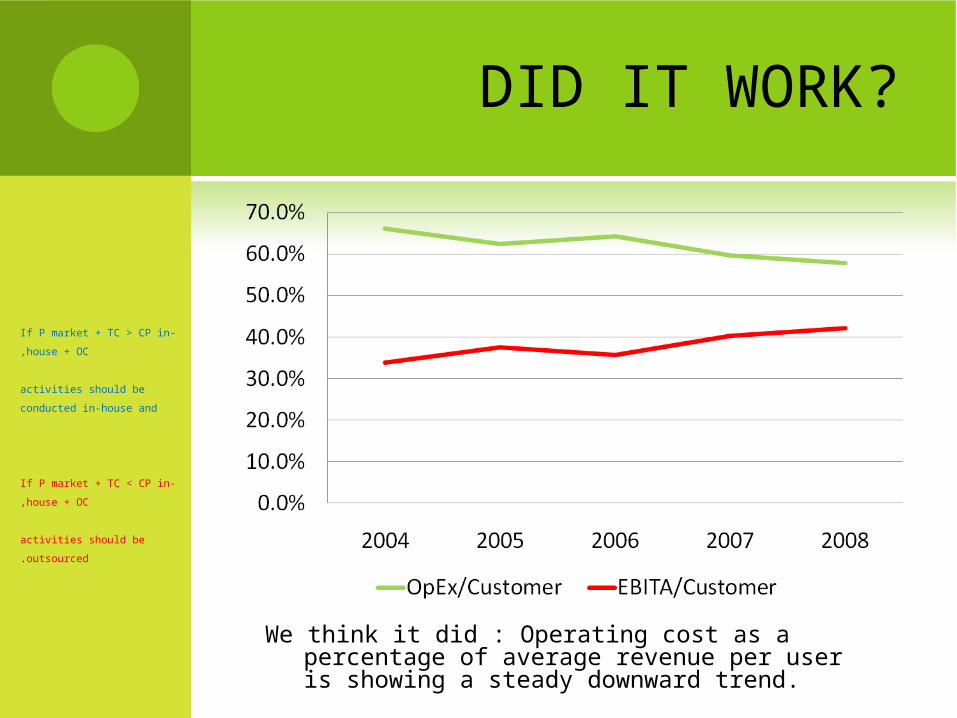

If P market + TC > CP in-house + OC,

activities should be conducted in-house and

If P market + TC < CP in-house + OC,

activities should be outsourced.

Reputation capital can be used as a hedge against opportunism

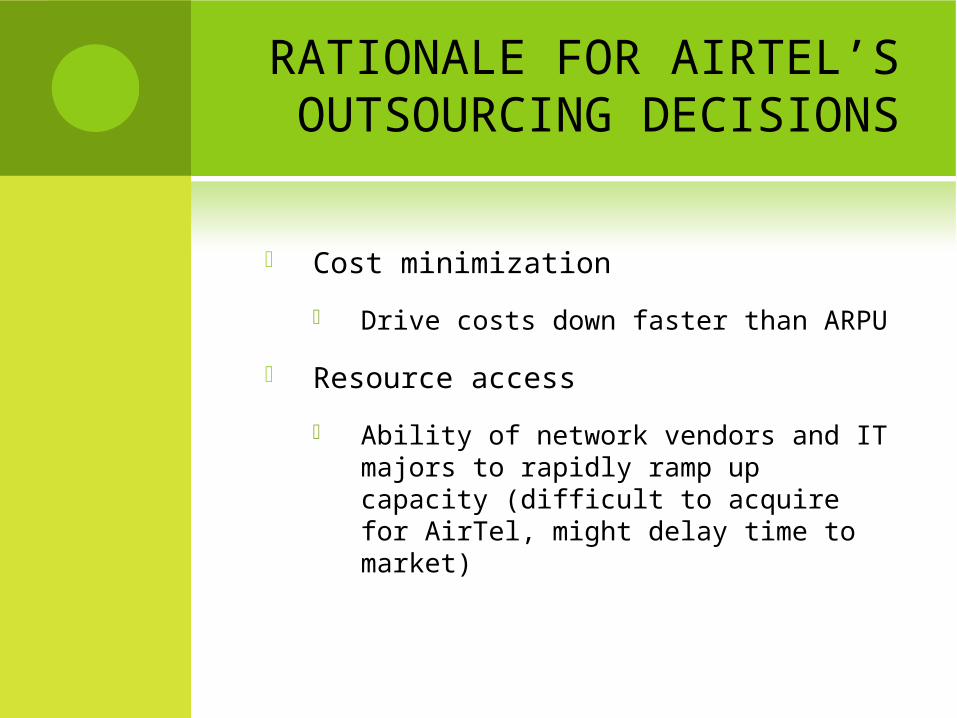

RATIONALE FOR AIRTEL’S OUTSOURCING

DECISIONS

Cost minimization

Drive costs down faster than ARPU

Resource access

Ability of network vendors and IT majors to rapidly ramp up capacity (difficult to acquire for AirTel, might delay time to market)

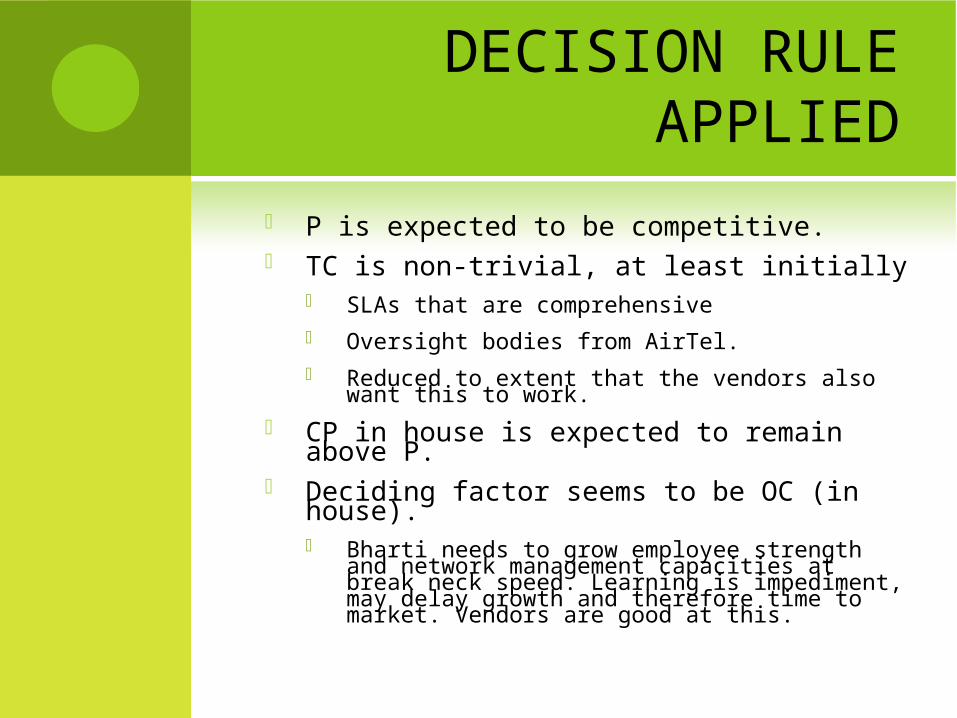

DECISION RULE APPLIED

P is expected to be competitive. TC is non-trivial, at least initially

SLAs that are comprehensive Oversight bodies from AirTel. Reduced to extent that the vendors also want this

to work. CP in house is expected to remain above P. Deciding factor seems to be OC (in house).

Bharti needs to grow employee strength and network management capacities at break neck speed. Learning is impediment, may delay growth and therefore time to market. Vendors are good at this.

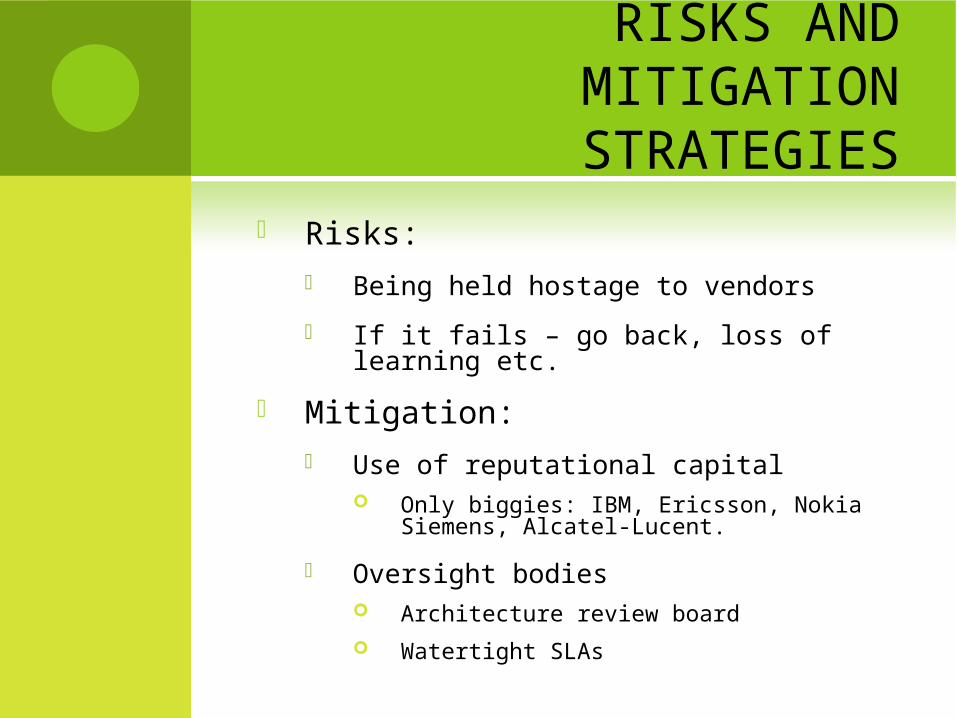

RISKS AND MITIGATION STRATEGIES

Risks: Being held hostage to vendors

If it fails – go back, loss of learning etc.

Mitigation: Use of reputational capital

Only biggies: IBM, Ericsson, Nokia Siemens, Alcatel-Lucent.

Oversight bodies Architecture review board Watertight SLAs

DID IT WORK?

We think it did : Operating cost as a percentage of average revenue per user is showing a steady downward trend.

If P market + TC > CP in-house

+ OC,

activities should be conducted

in-house and

If P market + TC < CP in-house

+ OC,

activities should be outsourced.

MTN DEAL

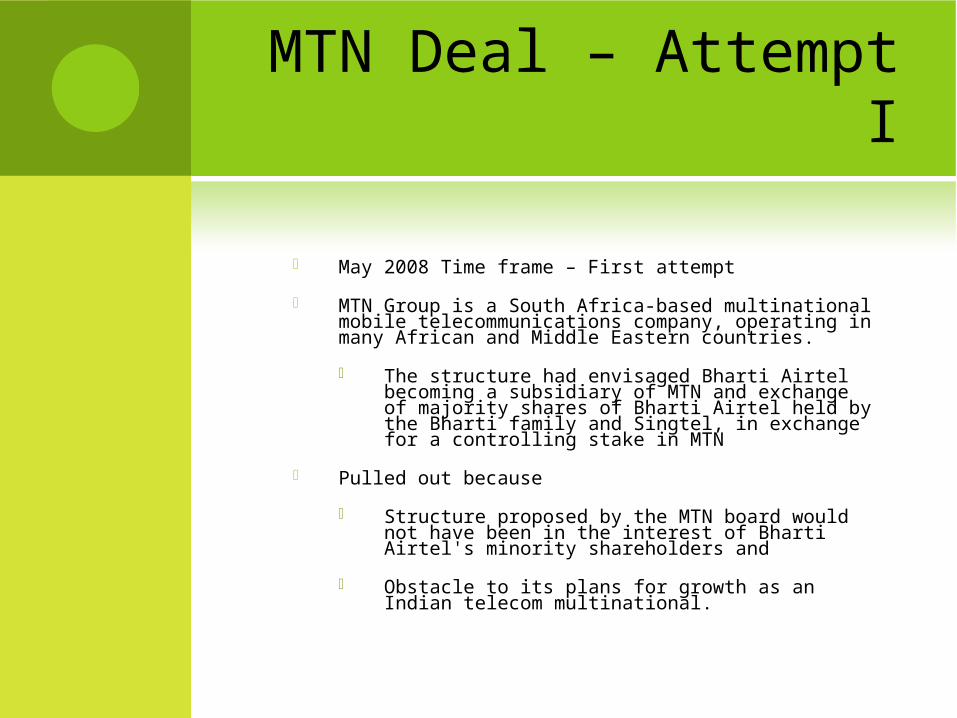

MTN Deal – Attempt I

May 2008 Time frame – First attempt

MTN Group is a South Africa-based multinational mobile telecommunications company, operating in many African and Middle Eastern countries.

The structure had envisaged Bharti Airtel becoming a subsidiary of MTN and exchange of majority shares of Bharti Airtel held by the Bharti family and Singtel, in exchange for a controlling stake in MTN

Pulled out because

Structure proposed by the MTN board would not have been in the interest of Bharti Airtel's minority shareholders and

Obstacle to its plans for growth as an Indian telecom multinational.

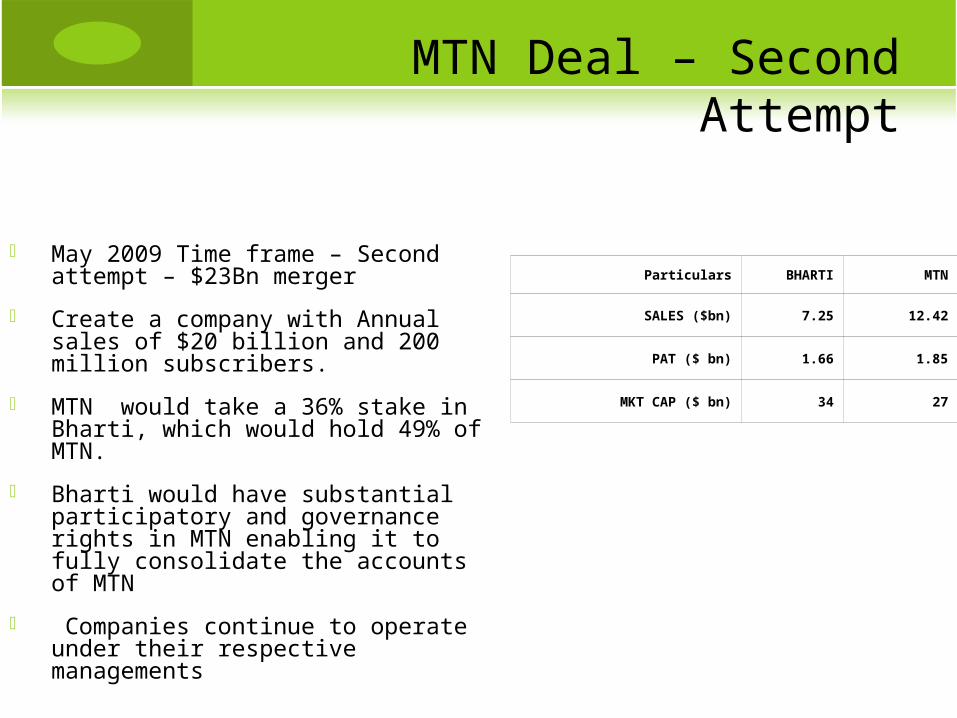

MTN Deal – Second Attempt

Particulars BHARTI MTN

SALES ($bn) 7.25 12.42

PAT ($ bn) 1.66 1.85

MKT CAP ($ bn) 34 27

May 2009 Time frame – Second attempt – $23Bn merger

Create a company with Annual sales of $20 billion and 200 million subscribers.

MTN would take a 36% stake in Bharti, which would hold 49% of MTN.

Bharti would have substantial participatory and governance rights in MTN enabling it to fully consolidate the accounts of MTN

Companies continue to operate under their respective managements

MTN Deal - Structure

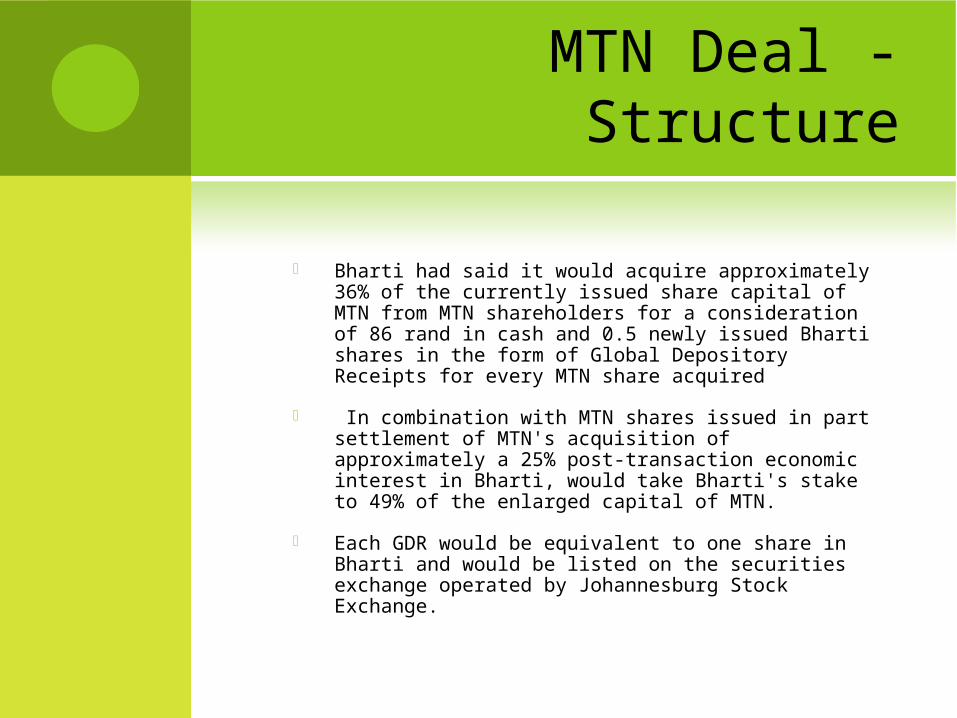

Bharti had said it would acquire approximately 36% of the currently issued share capital of MTN from MTN shareholders for a consideration of 86 rand in cash and 0.5 newly issued Bharti shares in the form of Global Depository Receipts for every MTN share acquired

In combination with MTN shares issued in part settlement of MTN's acquisition of approximately a 25% post-transaction economic interest in Bharti, would take Bharti's stake to 49% of the enlarged capital of MTN.

Each GDR would be equivalent to one share in Bharti and would be listed on the securities exchange operated by Johannesburg Stock Exchange.

MTN Deal – Going Global

Indian market at its peak, Boom in telecom sector but perceived to decline in 2-3 years

BAL as the Indian leader wants to continue to grow

Emerging S Africa Markets very similar to India 6-7 years back. Mobile telephony is in nascent stage. ARPU Higher.

So, great potential to grow into S Africa and the Middle east. MTN in 21 countries.

Increase the reach. Be the Biggest telco in the world.

Limited integration risk as the two companies have almost no overlapping operations

Bharti - Synergies

Combined Co to benefit from economies of scale as it would become a leading emerging market telecom operator

MTN's operating experience in 3G and

Number portability

Help him avoid the clutches of Indian telecom regulators Rows over the matter of spectrum allocation remain

unresolved and the rollout of 3G services is long delayed. MTN would benefit from Bharti's experience of growing

market Share and maintaining operating margins in a highly competitive environment – cost efficiencies

MTN Deal – Going Global - Hurdles

Counter Offers by Competition.

RCom was also bidding for Merger with MTN.

Similar deal in Vodacom, which is owned by Vodafone

Unions against it in S Africa

Foreign holding stake is 65+% Limit is 75%

$4Bn for the deal. 3G bid also needs this much

Debt Pressures in short term

KEY DATA ABOUT BHARTI

1985 TO 1991 – TELEPHONE

MANUFACTURING 1985 - Entered into technical tie-up with Siemens AG of

Germany for manufacture of electronic push button telephones 'Beetel‘ and reached a peak sales of 5 million

1989 - Tied-up with Takacom Corporation, Japan, for manufacture of telephone answering machines

1990 - Tied-up with Lucky Gold Star International Corporation of South Korea for manufacture of cordless telephones

1991 - OEM Contract with Sprint, USA for manufacture and export of telephone sets

1992 TO 2001 – FORMATIVE YEARS OF

TELECOM MAJOR 1992 - Formed a consortium with SFR-France, Emtel-

Mauritius and MSI-UK, to bid for cellular licenses for metropolitan circles under Bharti Cellular.

1994 - Cellular license for Delhi circle obtained. Launched AirTel next year. Launched cellular services in Himachal Pradesh in 1996

1995 - Formed a consortium with Telecom Italia-Italy to bid for cellular and fixed-line services under Bharti Telenet.

1996 - Telecom Italia, Italy acquired 20% equity interest in Bharti Tele-Ventures.

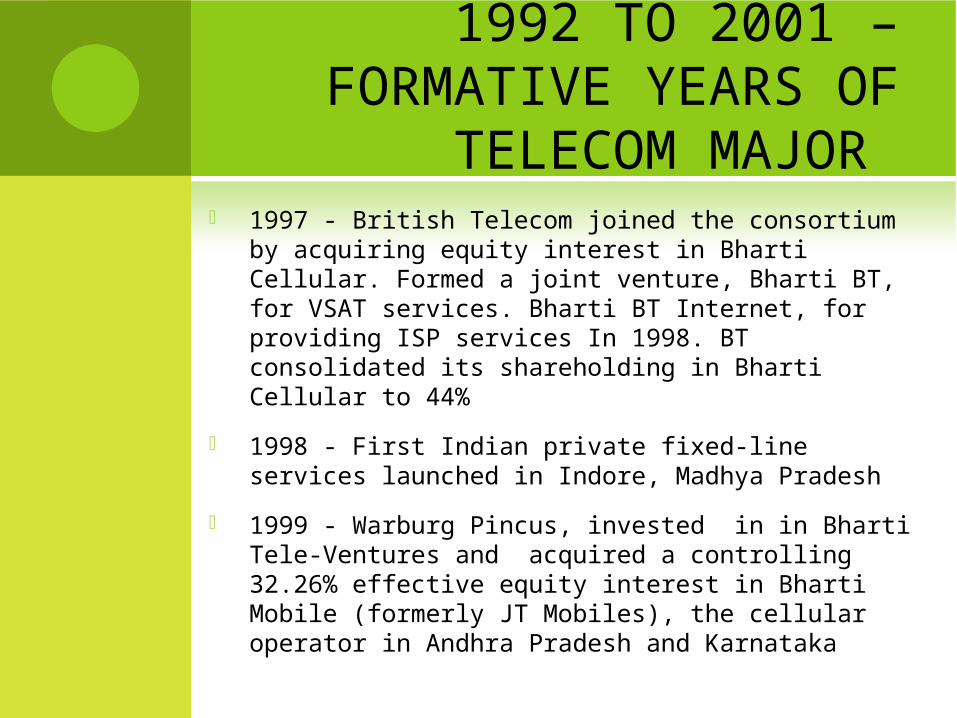

1992 TO 2001 – FORMATIVE YEARS OF

TELECOM MAJOR 1997 - British Telecom joined the consortium by

acquiring equity interest in Bharti Cellular. Formed a joint venture, Bharti BT, for VSAT services. Bharti BT Internet, for providing ISP services In 1998. BT consolidated its shareholding in Bharti Cellular to 44%

1998 - First Indian private fixed-line services launched in Indore, Madhya Pradesh

1999 - Warburg Pincus, invested in in Bharti Tele-Ventures and acquired a controlling 32.26% effective equity interest in Bharti Mobile (formerly JT Mobiles), the cellular operator in Andhra Pradesh and Karnataka

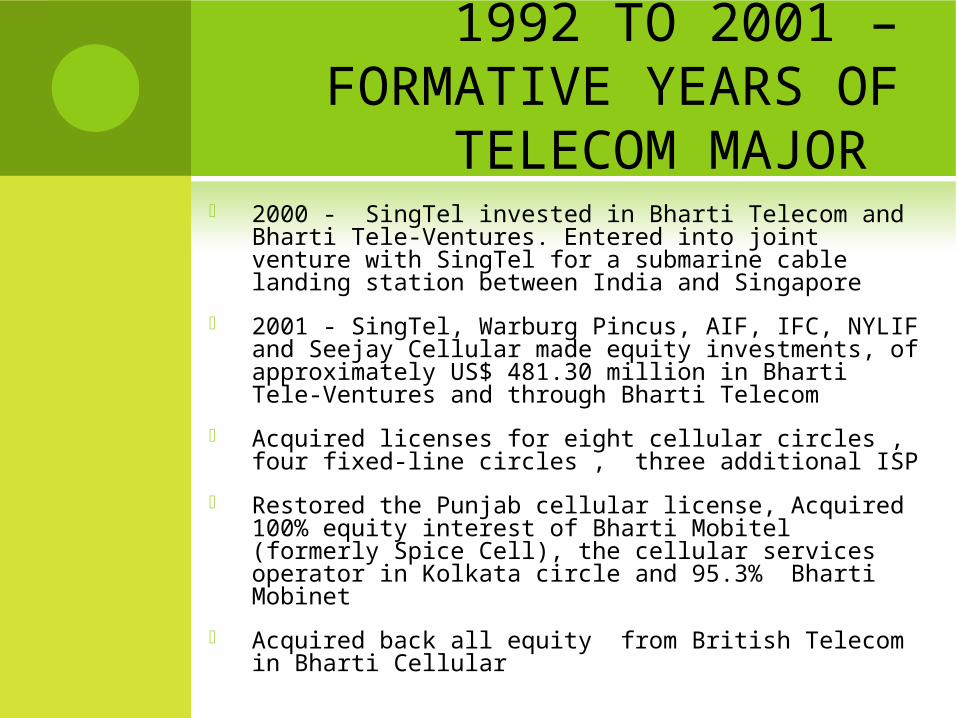

1992 TO 2001 – FORMATIVE YEARS OF

TELECOM MAJOR 2000 - SingTel invested in Bharti Telecom and Bharti Tele-

Ventures. Entered into joint venture with SingTel for a submarine cable landing station between India and Singapore

2001 - SingTel, Warburg Pincus, AIF, IFC, NYLIF and Seejay Cellular made equity investments, of approximately US$ 481.30 million in Bharti Tele-Ventures and through Bharti Telecom

Acquired licenses for eight cellular circles , four fixed-line circles , three additional ISP

Restored the Punjab cellular license, Acquired 100% equity interest of Bharti Mobitel (formerly Spice Cell), the cellular services operator in Kolkata circle and 95.3% Bharti Mobinet

Acquired back all equity from British Telecom in Bharti Cellular

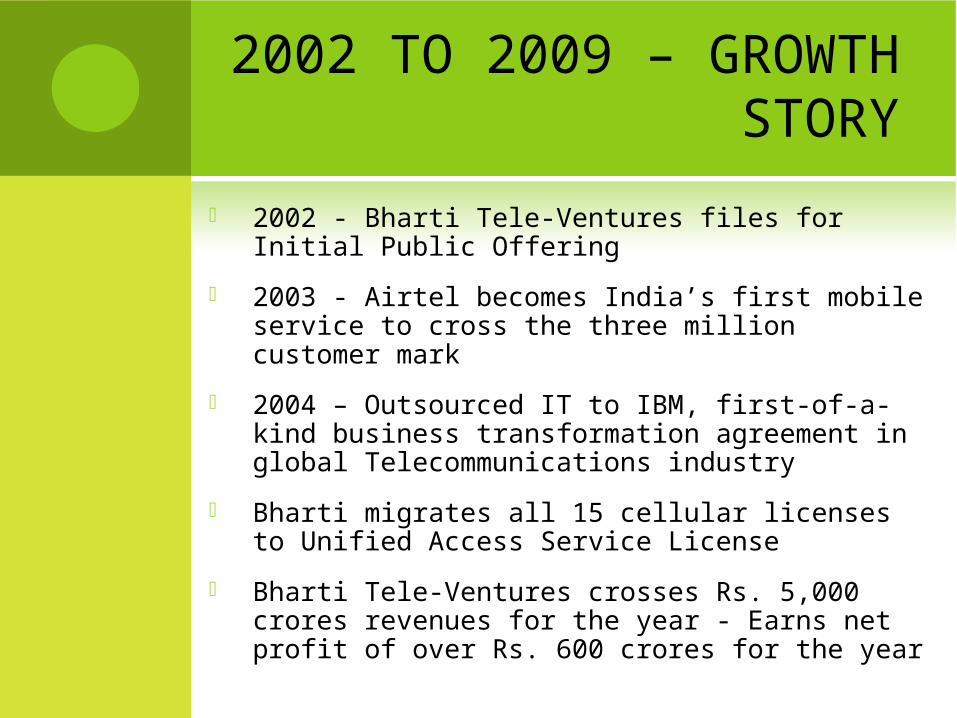

2002 TO 2009 – GROWTH STORY

2002 - Bharti Tele-Ventures files for Initial Public Offering

2003 - Airtel becomes India’s first mobile service to cross the three million customer mark

2004 – Outsourced IT to IBM, first-of-a-kind business transformation agreement in global Telecommunications industry

Bharti migrates all 15 cellular licenses to Unified Access Service License

Bharti Tele-Ventures crosses Rs. 5,000 crores revenues for the year - Earns net profit of over Rs. 600 crores for the year

2002 TO 2009 – GROWTH STORY

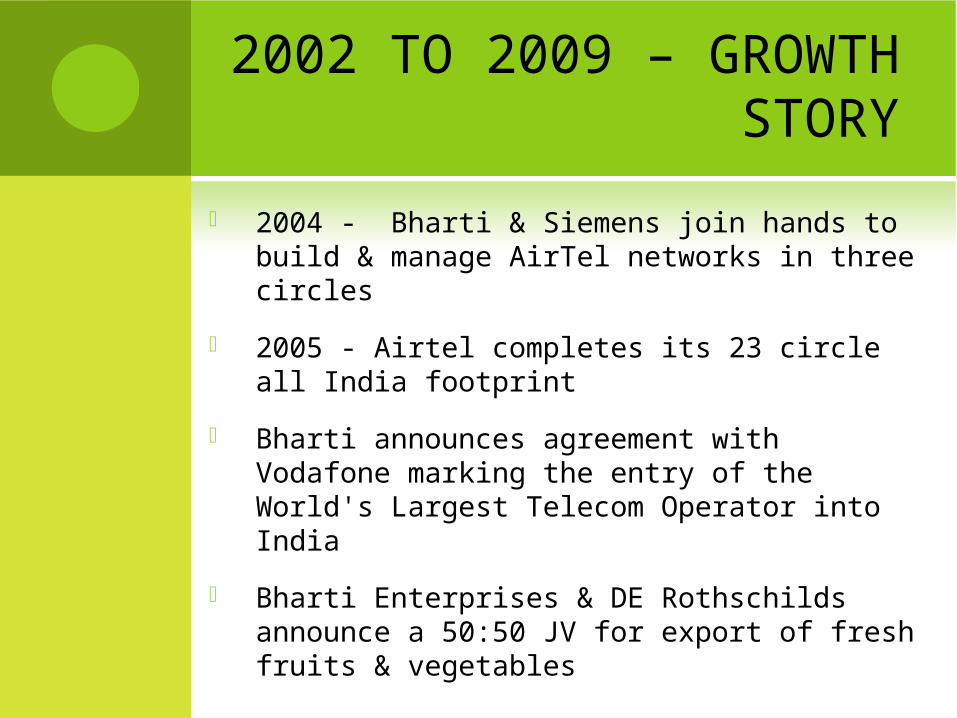

2004 - Bharti & Siemens join hands to build & manage AirTel networks in three circles

2005 - Airtel completes its 23 circle all India footprint

Bharti announces agreement with Vodafone marking the entry of the World's Largest Telecom Operator into India

Bharti Enterprises & DE Rothschilds announce a 50:50 JV for export of fresh fruits & vegetables

2002 TO 2009 – GROWTH STORY

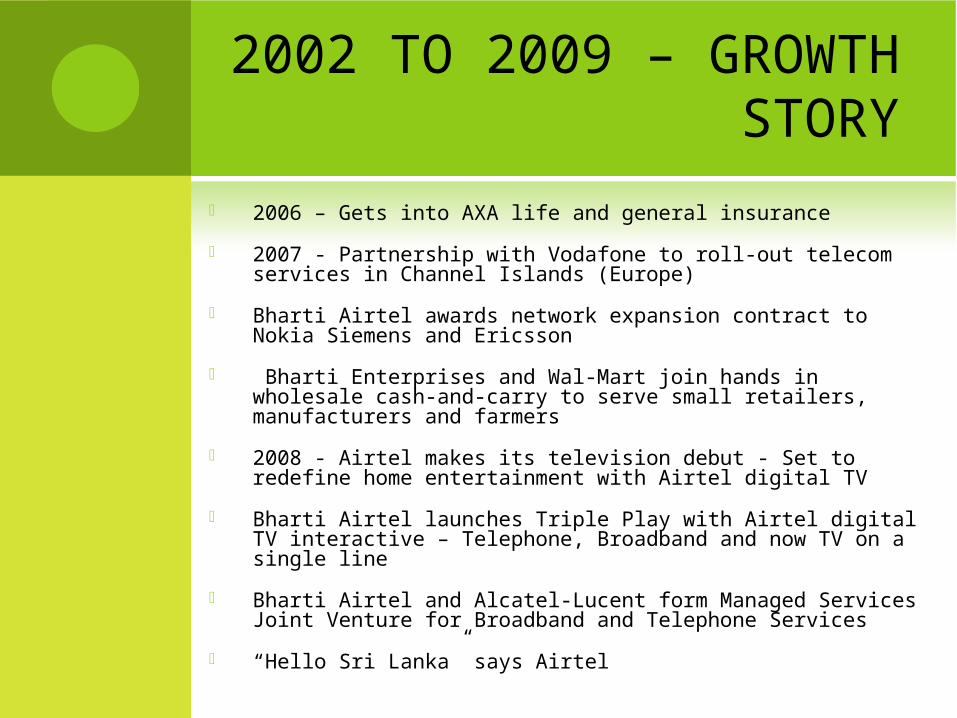

2006 – Gets into AXA life and general insurance

2007 - Partnership with Vodafone to roll-out telecom services in Channel Islands (Europe)

Bharti Airtel awards network expansion contract to Nokia Siemens and Ericsson

Bharti Enterprises and Wal-Mart join hands in wholesale cash-and-carry to serve small retailers, manufacturers and farmers

2008 - Airtel makes its television debut - Set to redefine home entertainment with Airtel digital TV

Bharti Airtel launches Triple Play with Airtel digital TV interactive – Telephone, Broadband and now TV on a single line

Bharti Airtel and Alcatel-Lucent form Managed Services Joint Venture for Broadband and Telephone Services

“Hello Sri Lanka” says Airtel

2002 TO 2009 – GROWTH STORY

2009 - Bharti Airtel launches Triple Play with Airtel digital TV interactive – Telephone, Broadband and now TV on a single line

Bharti Airtel and Alcatel-Lucent form Managed Services Joint Venture for Broadband and Telephone Services

Bharti Group Companies

Bharti Airtel

Bharti Teletech

Telecom Seychelles

Comviva Technologies Ltd

FieldFresh Foods Pvt. Ltd

Bharti Retail

Bharti AXA General Insurance

Bharti Group Companies

Bharti AXA Life Insurance

Bharti AXA Investment Managers

Centum Learning Limited

Jersey Airtel

Guernsey Airtel

Bharti Foundation

Bharti Realty

Bharti Infratel

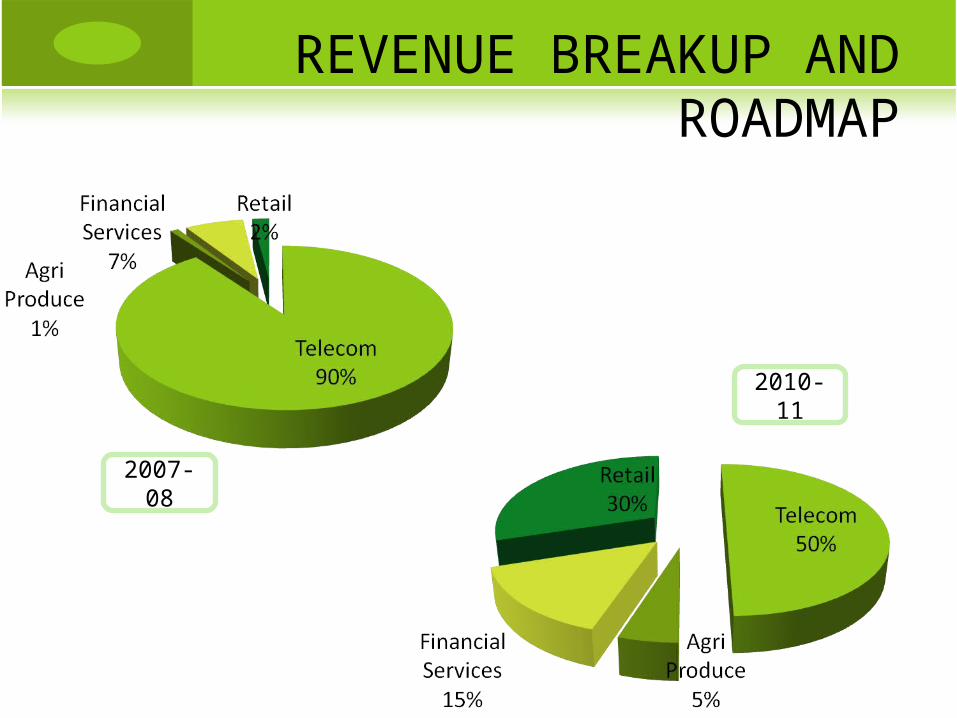

REVENUE BREAKUP AND ROADMAP

2007-08

2010-11

Bharti Airtel Ltd Bharti Airtel is India's largest telecommunications company by subscriber

base, which stood at 85.7 million in December 2008, and total revenues, which were Rs. 270 billion in 2007/08

Started July 07, 1995, as a Public Limited Company

Globally, Bharti Airtel is the 3rd largest in-country mobile operator by subscriber base, behind China Mobile and China Unicom

In India, the company has a 24.6% share of the wireless services market, followed by 17.7% for Reliance Communications and 17.4% for Vodafone Essar.[4]

Bharti Airtel has 5 business segments:

(i) Mobile Services; (ii) Telemedia Services; (iii) Enterprise Services - Carriers; (iv) Enterprise Services - Coprorates; and (v) Passive Infrastructure Services.

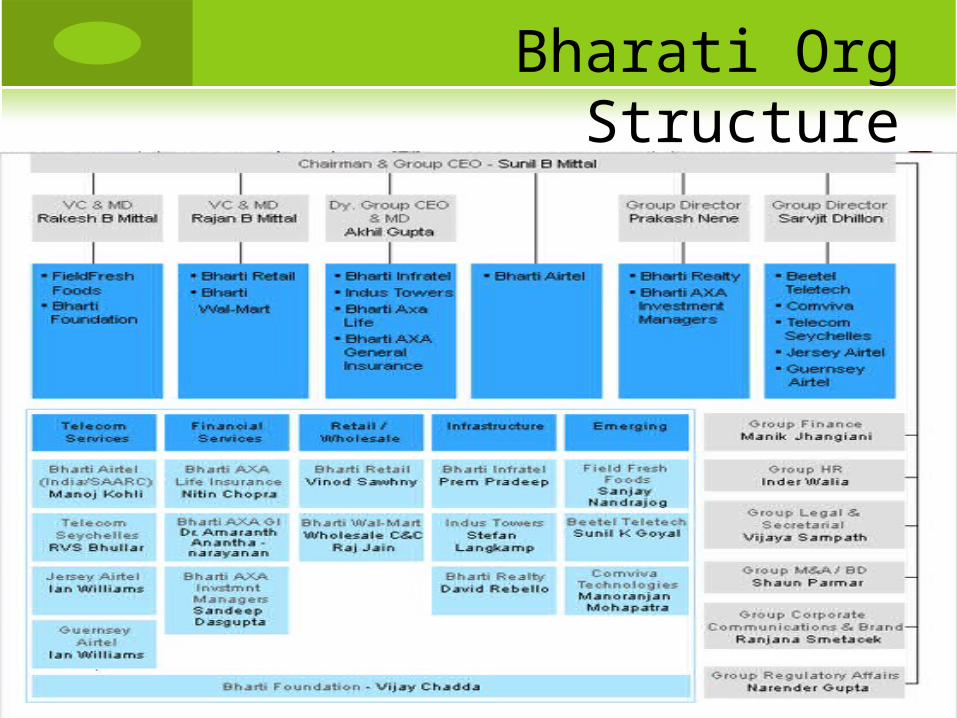

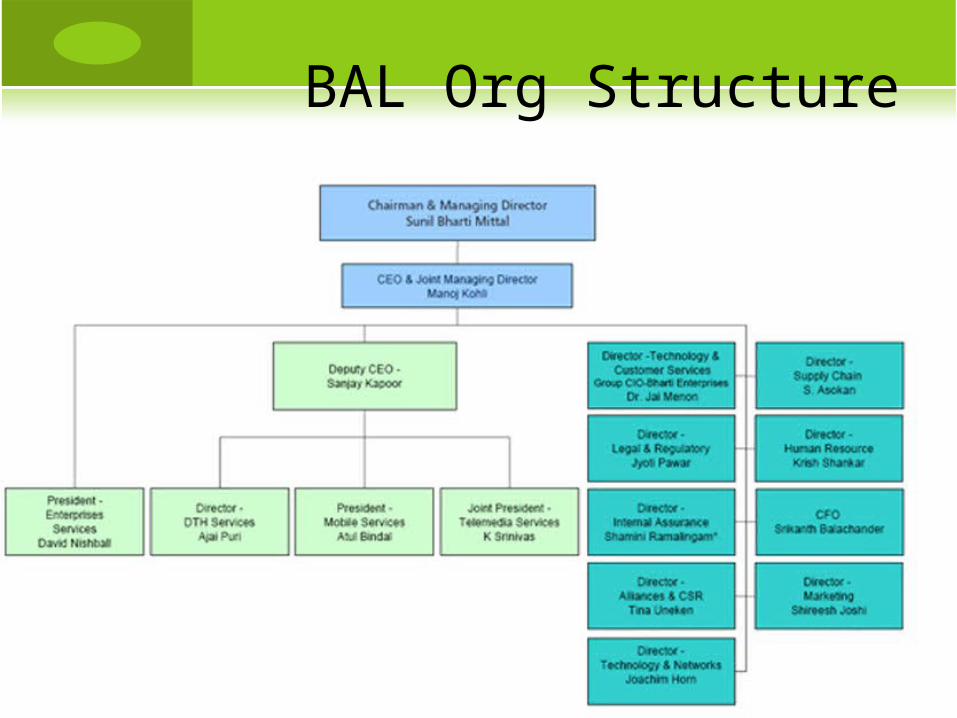

Bharati Org Structure

BAL Org Structure

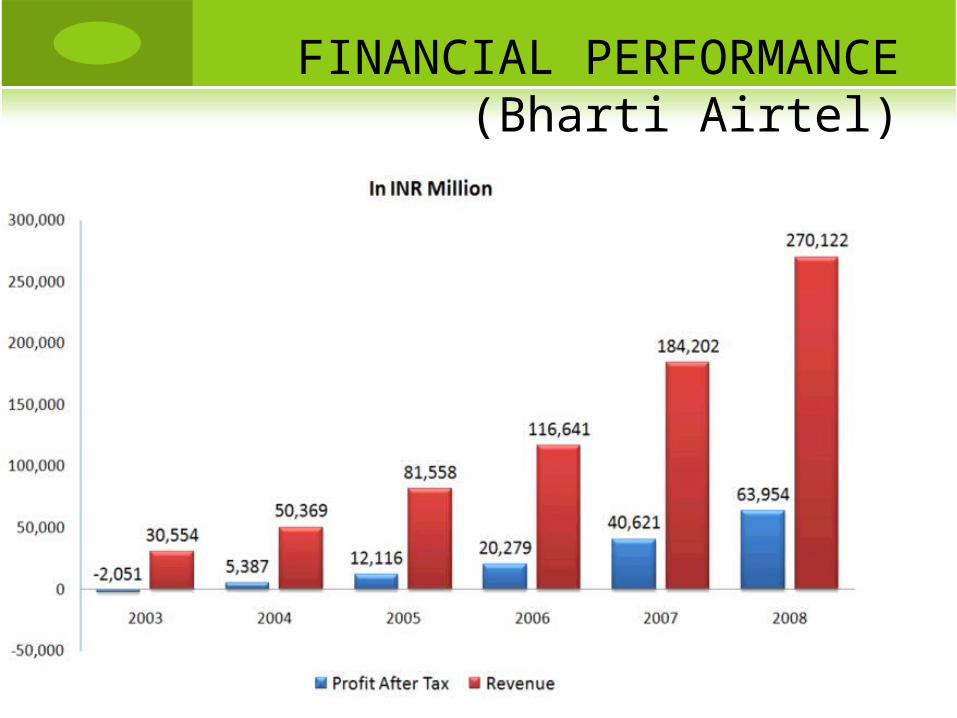

FINANCIAL PERFORMANCE (Bharti Airtel)

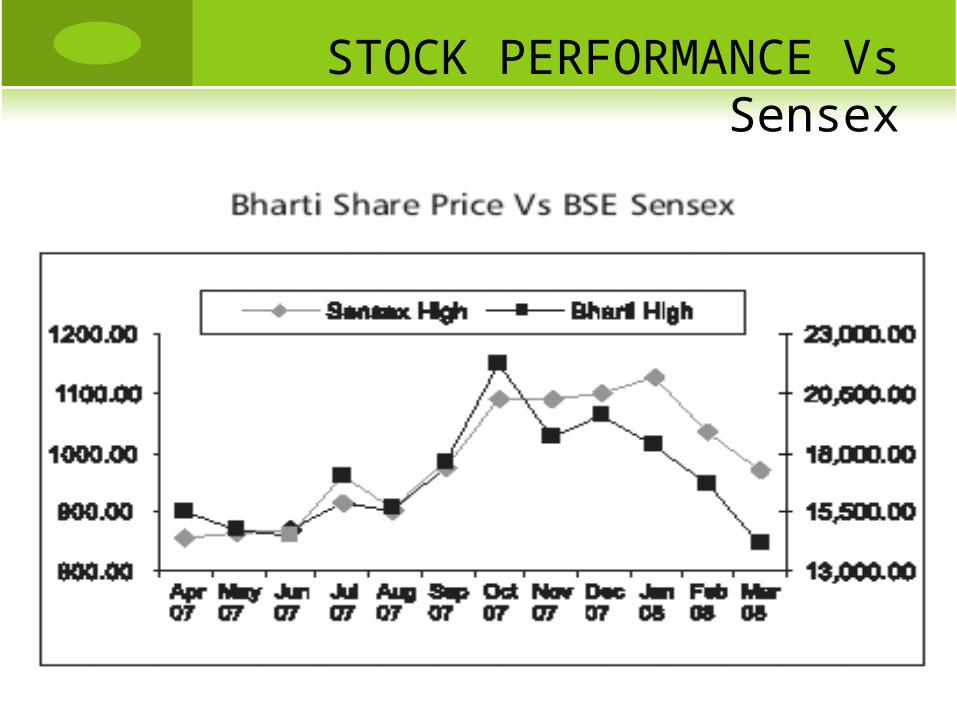

Stock Perforarmce

BAL has been growing at an exponential rate in terms of subscriber base, revenues and Net profits

STOCK PERFORMANCE Vs Sensex

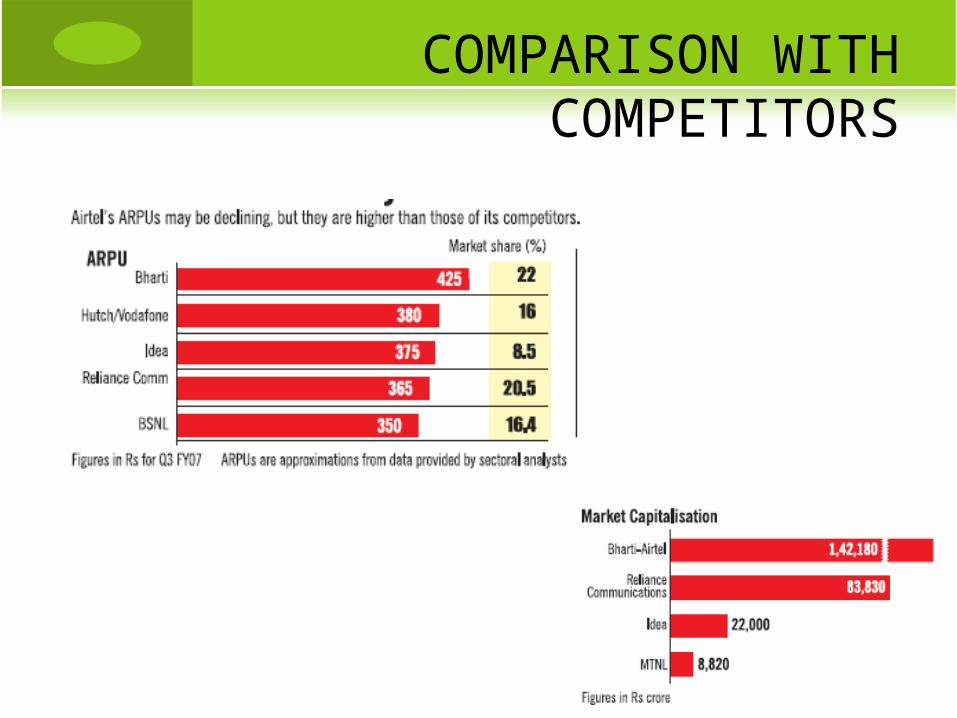

COMPARISON WITH COMPETITORS

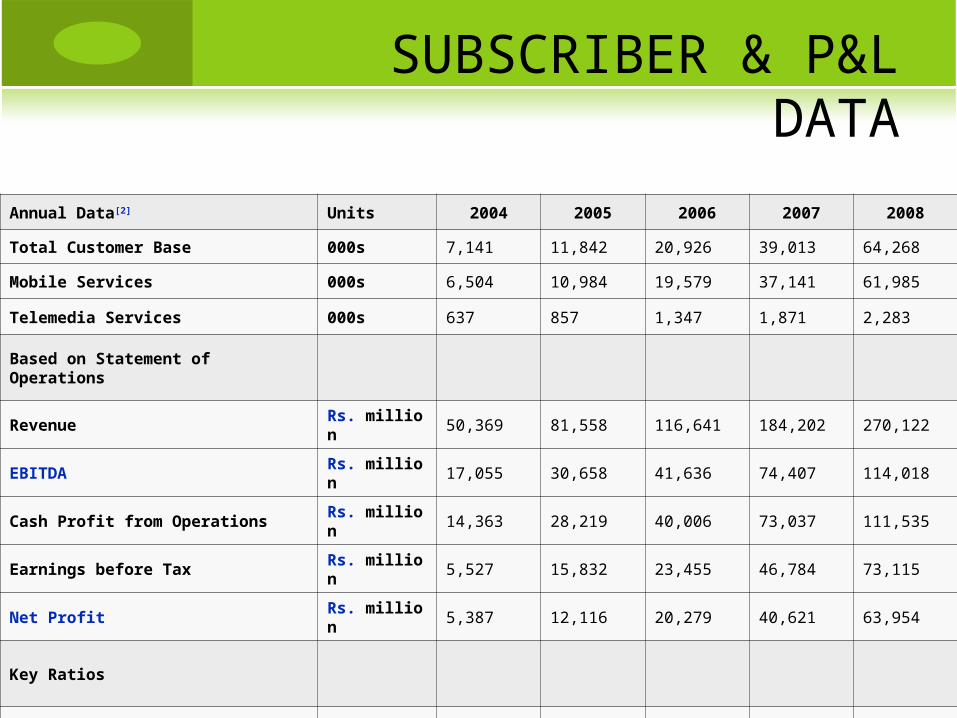

SUBSCRIBER & P&L DATA

Annual Data[2] Units 2004 2005 2006 2007 2008

Total Customer Base 000s 7,141 11,842 20,926 39,013 64,268

Mobile Services 000s 6,504 10,984 19,579 37,141 61,985

Telemedia Services 000s 637 857 1,347 1,871 2,283

Based on Statement of Operations

Revenue Rs. million 50,369 81,558 116,641 184,202 270,122

EBITDA Rs. million 17,055 30,658 41,636 74,407 114,018

Cash Profit from Operations Rs. million 14,363 28,219 40,006 73,037 111,535

Earnings before Tax Rs. million 5,527 15,832 23,455 46,784 73,115

Net Profit Rs. million 5,387 12,116 20,279 40,621 63,954

Key Ratios

Return on Equity (ROE) % 12.00% 23.70% 32.00% 43.10% 38.50%

Earnings per Share (EPS) Rs. million 3.15 6.53 10.78 21.43 34.23

BHARTI AS AN EMPLOYER

In 2004, Bharti Airtel was ranked the No. 2 best employer in India by Hewitt Associates; in 2006 it was ranked No. 10 in BusinessWeek's IT 100 list.

The company's other benefits include half days on birthdays, gifts for anniversaries, no meetings on weekends, flexible work time, gym, yoga classes and regular health checks on campus

FRAMEWORKS AND CONCLUSIONS

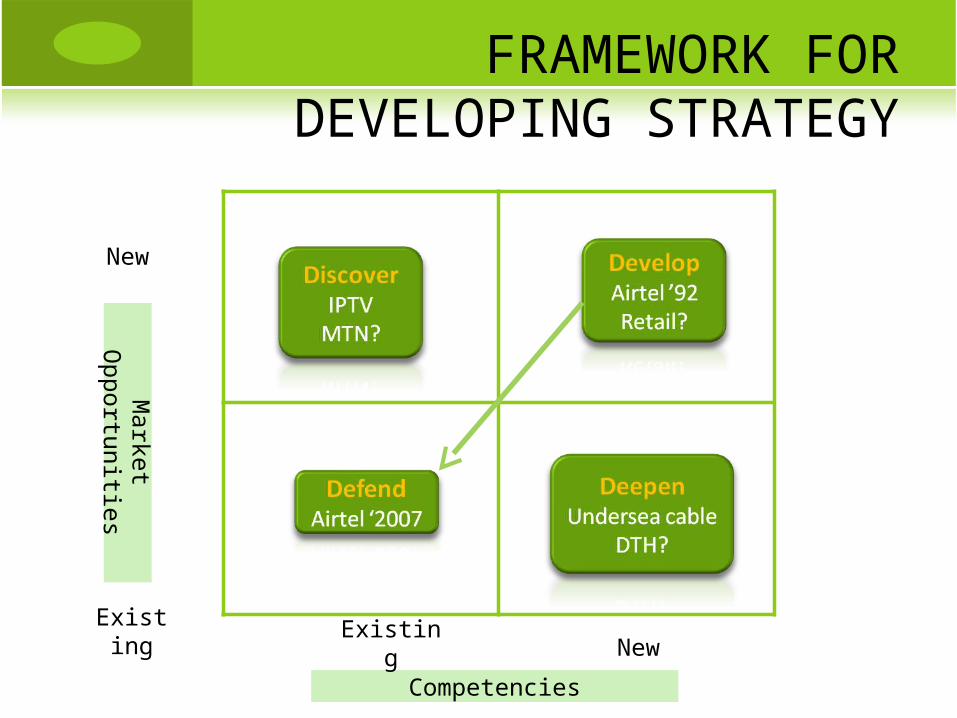

FRAMEWORK FOR DEVELOPING STRATEGY

Market O

pportunities

Competencies

New

Existing Existing New

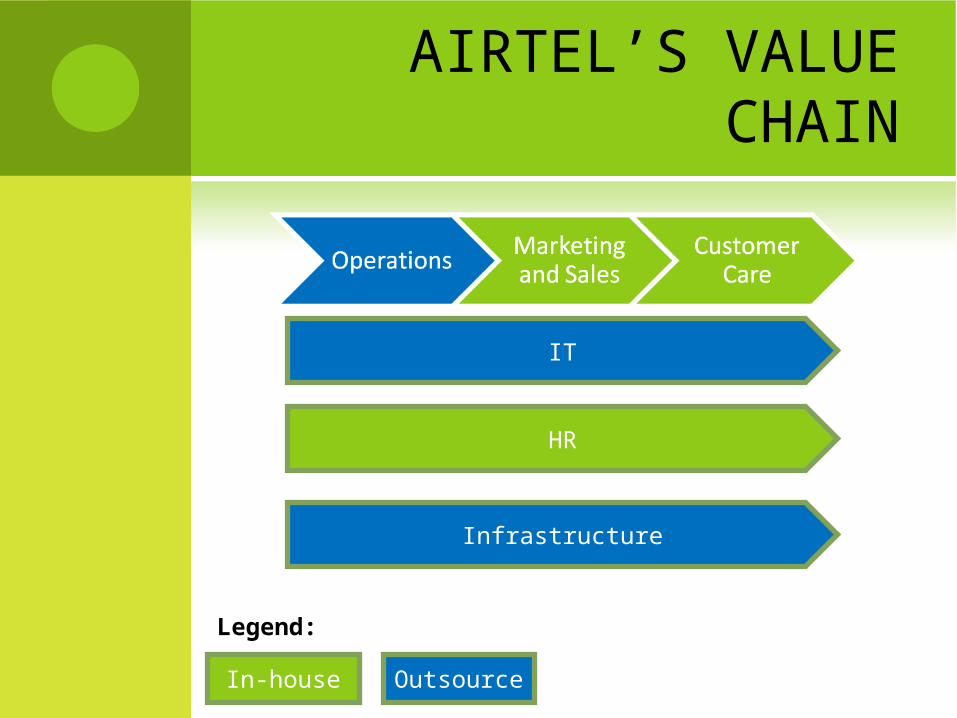

AIRTEL’S VALUE CHAIN

IT

HR

Infrastructure

In-house Outsource

Legend:

SUNIL MITTAL: MANAGEMENT STYLE

Ability to navigate through the socio, legal processes

Entrepreneur style at the early stages and then evolved to professional management style

Ability to convince lenders to provide him capital

Hands-on – himself tests out Airtel’s IPTV

Known to routinely travel to remote areas around India to boost the morale of his sales troops as well as to experience firsthand how good or poor his company’s telecom services are

SUNIL MITTAL: MANAGEMENT STYLE

Agile decisions: “Speed over perfection”

Sets clear and bold targets for the organization

His ability to rope in big players with deep pockets (like SingTel, Vodafone, Warburg Pincus & Siemens)

Ability to collaborate - sharing towers, network with competitors

At the age of 50, he stepped back to delegate operational control to the professional Managers to lead the various entities

Ability to attract and retain the best management team

His ability to think big and execute it flawlessl

INFLEXION POINTS

BAL has been growing at an exponential rate in terms of subscriber base, revenues and Net profits

Outsourcing

MTN

Pan India presence

FUTURE OF BHARTI

FUTURE

Enter into Education. Mittal’s vision of building a knowledgeable society in India

Advocates CSR

Seeking reforms in Insurance and Retail sectors

Grow the diversified businesses

Protect Airtel’s market share

Foray into Global markets

Wants to be the most respected conglomerate by 2020

THANK YOU

APPENDIX

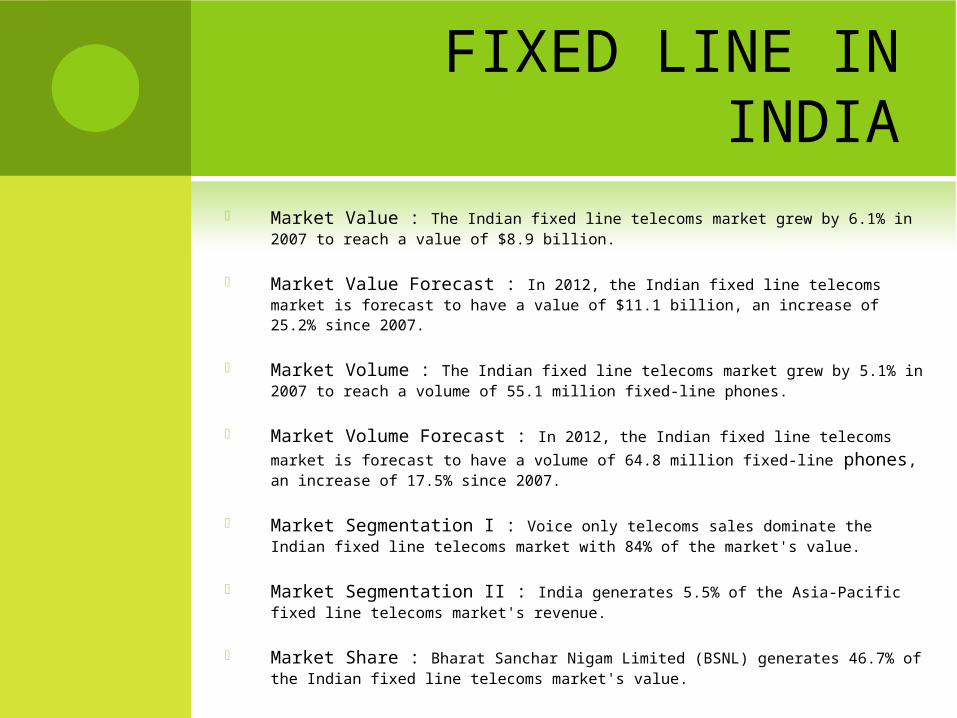

FIXED LINE IN INDIA Market Value : The Indian fixed line telecoms market grew by 6.1% in 2007 to reach a value of

$8.9 billion.

Market Value Forecast : In 2012, the Indian fixed line telecoms market is forecast to have a value of $11.1 billion, an increase of 25.2% since 2007.

Market Volume : The Indian fixed line telecoms market grew by 5.1% in 2007 to reach a volume of 55.1 million fixed-line phones.

Market Volume Forecast : In 2012, the Indian fixed line telecoms market is forecast to have a volume of 64.8 million fixed-line phones, an increase of 17.5% since 2007.

Market Segmentation I : Voice only telecoms sales dominate the Indian fixed line telecoms market with 84% of the market's value.

Market Segmentation II : India generates 5.5% of the Asia-Pacific fixed line telecoms market's revenue.

Market Share : Bharat Sanchar Nigam Limited (BSNL) generates 46.7% of the Indian fixed line telecoms market's value.