SME FINANCING : DEMAND SIDEssadmin.bibm.org.bd/notice/02-07-19/Monograph 03.pdfBSCIC Bangladesh...

72

Transcript of SME FINANCING : DEMAND SIDEssadmin.bibm.org.bd/notice/02-07-19/Monograph 03.pdfBSCIC Bangladesh...

RESEARCH MONOGRAPH 003

SME FINANCING : DEMAND SIDE

PROBLEMS AND SUPPLY SIDE RESPONSES

Ashraf Al Mamun

Md. Mosharref Hossain

A. N. K. Mizan

Associate Professor, BIBM

Lecturer, BIBM

Lecturer, BIBM

BANGLADESH INSTITUTE OF BANK MANAGEMENTMirpur, Dhaka

SME Financing : Demand Side Problems and Supply Side Responses

Ashraf Al MamunMd. Mosharref HossainA. N. K. Mizan

Published: November, 2012

Bangladesh Institute of Bank Management (BIBM)Plot No. 4, Main Road No. 1 (South), Section No. 2Mirpur, Dhaka-1216, BangladeshPABX : 9003031-5, 9003051-2Fax : 88-02-9006756E-mail : [email protected] : www.bibm.org.bd

Printed by Olympic Products Printing & Packaging, Dhaka, Bangladesh

The views in this publication are those of authors only and do not necessarily reflect theviews of the institution involved in this publication.

Published by

ii

Forewords

As part of the ongoing dissemination of BIBM research outputs, the presentresearch monograph contains the findings of the research project: “

The SME sector remainsone of the key policy focus areas of the Bangladesh Government as well as theBangladesh Bank.

This publication examines the problems of the demand side as well as the responses ofthe supply side while financing SMEs. It also

It gives me great pleasure, on behalf of BIBM, to offer this important resource to thepractitioners of the financial institutions, as well as to the academics and commonreaders.

I hope this monograph will be a useful reference point for financial institutionsinvolved in providing financial services to small and medium enterprises inBangladesh.

We do encourage feedback from our esteemed readers on this issue which certainlywould help us to improve upon our research activities in the years to come.

Director General

SMEFinancing: Demand Side Problems and Supply Side Responses”.

highlights on the current status of SMEs inBangladesh, issues of the small enterprises' access to formal credit, the stakeholder's roles insmall enterprise financing and finally, analyzes the gap between demand and supply side.

Dr. Toufic Ahmad Choudhury

iii

Acknowledgments

This research project has been completed with great support from manypersons and organizations.

We would like to specially thank Dr. Toufic Ahmad Choudhury, honorableDirector General, BIBM for his valuable advice, comments and innovative ideas toimprove our work throughout the year.

We are really thankful to Dr. Shah Md. Ahsan Habib, Professor and Director(Training), BIBM; Dr. Prashanta Kumar Banerjee, Professor & Director (Research,Development & Consultancy), BIBM; Mr. Habibullah Bahar, Agrani Bank ChairProfessor, BIBM; Mr. Abed Ali, Faculty Member, BIBM and Mr. Leif Andersen,Consultant, INSPIRED Project, European Union for their thoughtful contributionand comment on drafting and finalizing the report.

We are also verygrateful to all of our facultycolleagues for theirvaluableobservationsand constructivesuggestions whichhelpedusin completingthe report.

Bangladesh Bank, different financial institutions, SME Foundation, NASCIB andmany other organizations extended their support for completing the report. We dohighly recognize their contribution in fulfilling our objectives.

Our sincere appreciation goes to our field assistants for helping us in obtaining awide range of information from the field level. We are also thankful to Ms. PaponTabassum, Research Officer, BIBM; Mr. Sarder Aktaruzzaman, Proof Reader, BIBMand Mr. Md. Awalad Hossain, Computer Operator, BIBM for their support.

Finally, we would like to extend our gratitude to those who, directly and indirectly,extended their cooperation in our endeavor.

Ashraf Al MamunMd. Mosharref HossainA. N. K. Mizan

iv

RESEARCH MONOGRAPH 003

SME FINANCING : DEMAND SIDEPROBLEMS AND SUPPLY SIDE RESPONSES

Contents

Sl.No. Title Page

No.List of Abbreviations

Executive Summary

ix

x

1 Introduction

1.1 Objective of the Study

1.2 Data and Methodology

1

5

5

2 Current Status of SME Financing in Bangladesh and Role of Financial

Institutions7

3 Small Enterprises’ Access to Formal Credit 124 Stakeholders’ Roles and their Initiatives for Financing Small Enterprises

in Bangladesh

4.1 Government

4.2 Central Bank

4.3 SME Foundation

4.4 NASCIB

4.5 NGO/MFI

4.6 Business Bodies

16

16

17

19

19

20

20

5 Major Problems Faced by Small Enterprises in Bangladesh 20

6 Responses of Supply Side against the Problems Raised by the Demand Side 30

7 Gap Analysis between Demand Side and Supply Side and Some

Observations37

8 Recommendations 43

References 47

Appendix Table 49

Appendix Questionnaire 50

vii

List of Tables

List of Figures

List of Boxes

List of Appendix Tables

TableNo. Title Page

No.Table-1 Current Status of SME Loan Compared to Total Loan 7Table-2 Targeted SME Loan and Achievement 8Table-3 Segregation of SME Loan in Small and Medium Enterprises 9Table-4 Sector-wise Disbursement of SME Loan 10Table-5 Disbursement of SME Loan to the Women Entrepreneur 11Table-6 Summary Information on SME Refinancing (up to April 2011) 18Table 7 Main Obstacles Cited by Entrepreneurs for Accessing Formal Financial Sector 21Table-8 Barriers to Access of Credit: Overall Perception of Demand Side 21Table-9 Gap Analysis between Demand Side Problems and Supply Side Responses 41

viii

FigureNo. Title Page

No.Figure-1 Survey Results on Access to Formal Credit from Banks & NBFIs 13Figure-2 Reasons for Dissatisfaction with Bank Loan 14Figure-3 Reasons for not Obtaining Loan from Formal Sector: Entrepreneurs’ Perception 15Figure-4 Current Practices of Recording the Financial Information by the Entrepreneurs 28Figure-5 Responses of FIs against High Interest Rate 30Figure-6 Reasons for Charging High Interest Rate 31Figure-7 Responses of FIs against Excessive Security and Guarantee Requirement 32Figure-8 Responses of FIs Whether Security and Guarantee is Mandatory or Not 32Figure-9 Problems Faced by FIs Regarding Unstructured Financial Information 35

BoxNo. Title Page

No.Box-1 High Interest Rate and High Sunk Cost 24Box-2 Long Loan Processing Time 26Box-3 Insufficient Working Capital Loan, Long Loan Processing Time and Malpractice 27

Appendix TableNo. Title Page

No.Appendix Table 1 Descriptive Statistics of Major Demand Side Problems 49Appendix Table-2 One way ANOVA of Ranking 49Appendix Table-3 Questionnaire for the Survey of Small Enterprises 50Appendix Table 4 Questionnaire for the Survey of Banks/NBFIs 53

List of Abbreviations

Abbreviation Elaboration

ADB Asian Development Bank

ANOVA Analysis of Variance

BB Bangladesh Bank

BBS Bangladesh Bureau of Statistics

BIBM Bangladesh Institute of Bank Management

BSCIC Bangladesh Small and Cottage Industries Corporation

CIB Credit Information Bureau

FCB Foreign Commercial Bank

FI Financial Institution

FY Financial Year

GDP Gross Domestic Product

IDA International Development Association

MFI Microfinance Institute

MIDAS Micro Industry Development Assistance and Services

MoF Ministry of Finance

NASCIB National Association of Small and Cottage Industries of Bangladesh

NBFI Non-bank Financial Institution

NGO Non-government Organization

OECD Organization for Economic Co-operation and Development

PCB Private Commercial Bank

SAPRI Structural Adjustment Participatory Review Initiative

SB Specialized Bank

SE Small Enterprise

SCB State-owned Commercial Bank

SMCI Small, Medium and Cottage Industries

SME Small and Medium Enterprise

SMESPD SME & Special Programmes Department

TIN Tax Identification Number

VAT Value Added Tax

WB World Bank

ix

The economic and social importance of the Small and Medium Enterprise (SME) sector iswell recognized in academic and policy literature. SMEs play a very significant role in theeconomy in terms of balanced and sustainable growth, employment generation,development of entrepreneurial skills and contribution to export earnings. Although the termSME is widely used in different literatures and studies, the present study focuses on smallenterprises (SEs) only. Therefore, throughout the report the term small enterprises (SEs)have been used. Basically the specific objectives of the paper are: i) to identify the problemsfaced by small enterprises in obtaining loans from financial institutions in Bangladesh, ii) topoint out the responses and initiatives of the supply side to address the problems faced by thedemand side and iii) to identify and analyze the gap between demand side expectations andthe supply side responses and finally to formulate suggestions for policy initiatives.

To achieve the objectives of the study, data has been collected both from primary andsecondary sources. Primary data have been collected through interview and questionnairesurvey from both the demand side and supply side stakeholders. For this purpose, two sets ofquestionnaires (Appendices 3 & 4) were developed; one set for demand side and the otherone for supply side. For collecting the information from the demand side, as many as twelvedistricts have been selected on the basis of the concentration of small enterprises mentionedin the 'SME Credit Policies and Programmes 2010' by Bangladesh Bank. However, thecurrent study does not extensively cover the small businesses in rural areas and moreemphasis is given to the urban and semi-urban areas of the twelve districts where smallenterprises are concentrated. From these districts, 509 small enterprises were interviewedthrough the questionnaire. Among 509 small enterprises, 96 (18.86%) from manufacturing,335 (65.81%) from trading and 78 (15.33%) from the service sector were randomly selected.

As one of the main objectives of the study was to identify the major problems of the demandside, the entrepreneurs were selected from both the group of existing and potential (who areyet to get any financing facilities) borrowers of the formal financial institutions. The existingborrowers identied the problems related to SME financing by the formal financialinstitutions. On the other hand, the other group provided good insights regarding access toformal finance. For better understanding the ranks of the demand side problems, descriptivestatistics (Appendix-1) have been used and to judge the significance of the data set, one wayANOVA(Appendix-2) has been performed.

x

Executive Summary

For collecting the supply side information, a sample survey was conducted on 26 financialinstitutions consisting of state-owned commercial banks, private commercial banks,development financial institutions, foreign banks operating in Bangladesh and some non-bank financial institutions. To highlight the problems of the demand side, both the acceptedand rejected loan proposals of some particular banks and financial institutions were alsoreviewed.

The current status of the SME financing has been analyzed in terms of SME loan comparedto total loan, targeted SME loan and achievement, segregation of SME loan in small andmedium enterprises, sector-wise disbursement of SME loans by the financial institutions anddisbursement of SME loan to the women entrepreneurs.

Small enterprises' access to formal credit has been highlighted in the study. Access tosufficient and adequate capital to grow and further develop their activities is one of the mostimportant problems faced by many small businesses in our country. This is because most ofthe financial institutions considered that this sector characterizes high risk, involve hightransaction costs and provide low returns on investment. Choudhury and Raihan (2000)conducted a survey on SME access to credit under SAPRI study where they found that, “theaccess to formal credit is not available at all to 50.53 percent of the stakeholders. Only 35.79percent of SME stakeholders enjoy unrestricted access to the formal credit. The rest (13.68percent) of them have restricted access to the formal credit”. However, our study found that60.31% of the small enterprises got the access into the formal credit while the other 10. 41%enterprises did not have their access at all. On the other hand, 29.27% of enterprises did notapply for formal credit as they managed their funds by themselves.

The study explores main obstacles cited by the entrepreneurs for accessing formal financialsector and the major problems were ranked according to the responses of the entrepreneurs.The problems are listed here according to the ranking start from high interest rate,excessive security and guarantee requirement, insufficient working capital loan,ccomplexity of documentation, long loan processing time, unstructured financialinformation, financial institutions' negligence, high sunk cost for obtaining loan,malpractices in sanctioning loan, and lack of managerial capacity. ChoudhuryRaihan (2000) identified collateral as the prime barrier followed by bribe, delays, highinterest rate, banker's disinterest etc. On the other hand, our survey (2011) result showedhigh interest rate as the prime barrier. So it is evident that the factors acting as the primebarrier(s) have changed significantly.

ing

However, and

,

xi

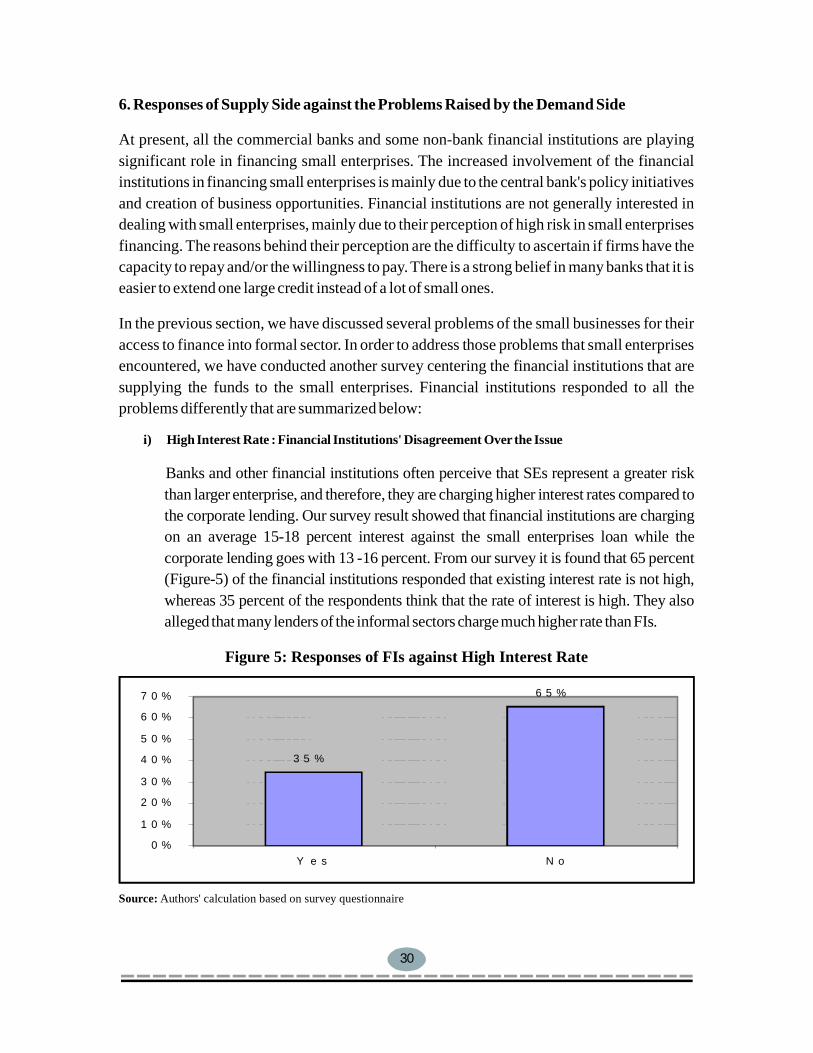

The study pointed out several problems of the small businesses (demand side) for theiraccess to finance into formal sector. In order to address those problems that small enterprisesencountered, we have conducted another survey centering the financial institutions that aresupplying the funds to the small enterprises. Financial institutions responded to all theproblems differently. Financial institutions had strong disagreement over the issue ofcharging high interest rate. Survey result shows that 65 percent of the financial institutionsresponded that existing interest rate is not high, whereas 35 percent of the respondents thinkthat the rate of interest is high. The reasons for charging high interest are: high monitoringand recovery cost, smaller range of credit limit, higher rate of provision, required collateral isnot available, high cost of maintaining relationship, risk is high, high cost of fund.

Financial institutions showed mixed response about the excessive security and guaranteerequirements. The survey results show that 58% of the respondents think security andguarantee is the real problem for providing loan to this sector. On the other hand, 42% of thefinancial institutions do not consider it as a problem.

Regarding complexity of documentation the financial institutions' responses were mixed.46% of the respondents do not think that complexity of documentation is the barrier foraccessing finance from their institutions. However, 54% respondents complained thatdocumentation really create some problems while taking their credit decision. In response tothe claim of the entrepreneurs that the financial institutions' documentation requirement isvery rigid, most of the respondents answered that they do not have any other alternativeswithout maintaining such documentation. Some of the respondents mentioned that, as perthe regulatory guidelines, they must follow the documentary requirement. But, dependingon the nature of their relationship and future business prospect sometimes they mayminimize the documentation requirements

The common perception of the demand side indicates that financial institutions take muchtime for processing the loan. But our survey result shows that, supply side does not supportthe perception of demand side, rather all the financial institutions in our sample stronglystated that their loan processing time is not high. Their responses range from 12-25 dayswhich is on an average 15.13 days. Whereas the demand side expected to have the loanwithin 10.61 days (on an average), supply side required 15.13 days (on an average) todisburse the loan.

In response to the issue of the availability of insufficient working capital most of the financialinstitutions explained that they are providing working capital loan to the small enterprisesprovided that the borrower fulfill their requirements.

.

xii

The FIs (supply side) opined that small businesses do not maintain good record of theirtransactions as per their requirement and most of the small business have unstructuredfinancial information. The supply side respondents cited that they are facing severeproblems while assessing the financial risk of the borrower due to unstructured financialinformation.

Besides, FIs may offerlower interest rate to the borrowers who have willingness to accept a collateralized loancontract relative to unsecured loans.

In response to Bankers' Negligence about small enterprise financing, banks and otherfinancial institutions strongly opposed the demand side claim and mentioned that, as it is thegovernment's priority sector and central bank's regulatory requirement as well as their owninterest, they do not show their negligence in this respect.

From the survey result it is evident that, high sunk cost is regarded as a relativelyinsignificant problem in obtaining loan from the FIs. In response to this problem, financialinstitutions mentioned that to some extent it is true but it does not mean that FIs themselvesare responsible for such cost.

Financial institutions did not agree at all against the complaint of demand side regardingtheir malpractices in sanctioning loan. Although the respondents do not take this complainton their own shoulders, a few of them mentioned that it may be true for some other FIs.

The study analyzed the prevailing gap between demand side and supply side problems.The gap exists between the two sides mainly due to perceptional and procedural differences.Finally, based on the observations and findings, to minimize the gaps and to reduce theproblems of demand side in getting finance from the financial institutions, the studyrecommends the following actions:

In regard to high interest rate, FIs have the scope to reduce such rate by searching for low costfunds. Bangladesh Bank and SME Foundation should intensify their efforts (refinancing andpre-financing) to provide low cost funds to the commercial banks.

In relation to excessive security and guarantee requirement, the financial institutions maytake care for the collateral free loan where personal guarantee is strong and the project hasgood future prospects. Moreover, FIs can concentrate on finding collateral substitute such ascash flow based lending, extensive monitoring, social security, etc.

To minimize the problems related with the insufficient working capital loan, FIs should notconsider the prior relationship with the borrower only rather they should also put emphasis

xiii

on the business prospects of the borrowers. Besides, FIs should make them understand aboutthe process of working capital assessment and the minimum time required for the approval ofsuch capital.

To eliminate the problem of unstructured financial information of borrowers, the businessowners should be encouraged to use proper accounting records on their businesstransactions. Moreover, they should be educated about the benefit of accounting andfinancial information to avail incentives such as tax holidays and easier access to bank loans.

To overcome the issue of financial institutions' negligence in dealing with the SE clients,banker should have good customer relationship, positive and caring attitude towards thesmall entrepreneurs. To address the issue, lack of managerial capacity of the smallentrepreneurs, government as well as the other stakeholders can take capacity buildingprojects and impart quality training to the small entrepreneurs.

To reduce the sunk costs of the borrowers in terms of money, energy and time, therelationship official should provide the prospective borrower a so that the borrowermight visualize al the requirements of the loan clearly. Long loan processing time may bereduced by adopting standard loan approving procedures based on information technologyand maintaining better information management.

To address the issue of malpractices (taking bribe, nepotism etc.) in sanctioning loan tosmall enterprises, the FIs have to adopt better internal control and governance mechanism toidentify such activities, and if found, involved officials must get exemplary punishment.

There is an urgent need to adopt a new business model for financing SEs. Thus, FIs shouldre-engineer (business process re-engineering) their existing financing process of SEs to takespecial care for them.

The local government bodies can operate the rural information centers in a better way toprovide information to the small entrepreneurs about the different sources of refinancing orpre-financing schemes available in our country. To address the problems of gettingdocuments from different issuing authorities, government and other relevant authorities canease the documents-obtaining process by establishing separate counter for the SE clients invarious departments across the country.

To enhance their effective contribution in the sector NASCIB can organize more effectivetraining for the skill development of the entrepreneurs, can take initiatives to establish

,

check list

xiv

business links of the small businesses with large corporations for better marketing of Small,Medium and Cottage Industries (SMCI) products. Government and trade associations mayinitiate building a good relationship between businessmen and bankers by participating indiscussions, seminars, and symposiums to reduce lack of understanding of bankingprocedures by the businessmen.

In order toidentify thepotential suppliers of financial services

and evaluate the cost of the financial. In order to ensure access to finance for the SEs, the FIs canestablish branches in the rural areas. If it is not possible, they may establish extensive creditlinkage programswith the NGO/MFIsof the country for covering larger area.

NBFIs may also diversify their SE financing portfolio by offering more innovative financingproducts throughout the country such as small lease, micro lease, seed money, factoring,invoice financing, venture capital, investment funding etc. NGO/MFIs can extend financingfacilities for the small enterprises because it can reduce their administrative costs andenhance the quality of their portfolio. They can also enter in the small enterprise financingmarket by forming strategic partnerships with the FIs.

1

reduce the information asymmetry, a very good relationship between the FIs and itsSEs should be established by whichSEs can

xv

1Since administrative cost of microfinance is higher than the SE financing.

SME Financing : Demand Side Problems and Supply Side Responses

1. Introduction

The economic and social importance of the Small and Medium Enterprise (SME) sector iswell recognized in academic and policy literature. SMEs play a very significant role in theeconomy in terms of contribution toward balanced and sustainable growth, employmentgeneration, development of entrepreneurial skills and export earnings. Bangladesh economyis characterized by low per capita income, high level of unemployment, mass poverty andsocial deprivation. In these circumstances, higher growth of SMEs can reduce poverty to asatisfactory level by creating jobs for the skilled and unskilled manpower in this sector.Cross country study (Ayyagari et al. 2003) shows that SMEs account for over 51 percent ofGDP and 57 percent of employment in high income countries while the correspondingfigures for low income countries are only16 and 18 percent respectively. It is recognized thatSME sectors in developing economies are underserved, especially in terms of finance.

Prior to a discussion on the problems of SME financing in Bangladesh, the definition of thesesmall and medium enterprises should be cleared. Throughout the world, there are a lot ofdefinitions of SME and the researchers and policy makers are far away from a unanimousdefinition. In Bangladesh, two definitions exist regarding SMEs; one is given in 'SME CreditPolicies & Programmes 2010' published by Bangladesh Bank and other is in the 'IndustrialPolicy 2010' published by the Ministry of Industry. Recently Bangladesh Bank has issued acircular (SMESPD, Circular No-1, 19 June, 2011) to determine the size of the SMEs in order2

1

2According to Bangladesh Bank Circular, means an entity, ideally not a public limited

company, which complies with the following criteria:A with total assets at cost including installation of fixed asset and excluding

land and building from Tk. 50 lac to 10 crore and/or number of employee ranges from 25 to 99. A with totalassets at cost including installation of fixed asset and excluding land and building from Tk. 5 lac to Tk 1 crore and/or numberof employees ranges from 10 to 25. A with total assets at cost including installation of fixed asset andexcluding land and building from Tk. 5 lac toTk 1 crore and/or number of employees ranges from 10 to 25.

A with total assets at cost including installation of fixed asset and excludingland andbuilding from Tk. 10 crore to 30 crore and/or number of employee ranges from 100 to 250.A with totalassets at cost including installation of fixed asset and excluding land and building from Tk. 1 crore to 15 crore and/or number ofemployees ranges from 50 to 100. A with total assets at cost including installation of fixed asset and excludingland and building from Tk. 1 crore to15 crore and/or number of employees ranges from 50 to 100.

If on one criterion, a firm falls into the 'small' category, while it falls into 'medium' category based on the othercriterion, the firm will be deemed as in the 'medium' category. On the other hand, if on one criterion, a firm falls into the'medium' category, while it falls into 'large' category based on the other criterion, the firm will be deemed as in the 'large'category.

Small and Medium Enterprise

Small Enterprise-

Medium Enterprise-

Note:

manufacturing concernservice concern

trading concern

manufacturing concernservice concern

trading concern

2

to harmonize the definition with the industrial policy. It is important to note that industrialpolicy does not cover the definition for trading concerns.

Although the term SME is widely used in different literatures and studies, the present studyfocuses on small enterprises (SEs) only. Therefore, throughout the report the term smallenterprises (SEs) have been used.

The main characteristics of small business are: (i) they are operated by a family or closegroup; (ii) business owner is the day-to-day decision maker; (iii) formal business records arenot widely available and even if some formal records are available, information may not beaccurate and are rarely audited. Small enterprises are labor intensive businesses and in mostcases they are able to serve niche market segments that are not covered by the largerbusinesses. It makes innovative use of knowledge, experience, resources and simpletechnologies to turn local market conditions into business opportunities. In many developingcountries, 95% of all companies have less than 50 employees (NCDO 2005). If the aim is tostimulate private sector development, there is a clear demand to cater for specific needs ofsmall businesses. Every dollar invested in a small enterprise generated an average ten dollarsof economic activity in the local economy (SEAF 2005).

For most of the developing and transition economies, the common challenges that SEstypically confront include barriers related with access to finance in the formal financialsector, institutional, legal and administrative barriers. Small enterprises, throughout theworld, for their heterogeneous characteristics face severe problems. In this regard Levy(1991) highlighted some of the common problems faced by most developing countries, viz.,the financing constraints; regulatory constraints; technical, marketing and other non-financial input constraints; and cost constraints.

Identifying problems related to small enterprise financing is a much-debated issue. Differentliteratures give deeper insight into the problems of the demand side and the activities of thefinancial institutions (supply side) in coping with the problems. Most of the small businessesare family-based and lack appropriate financing for their start- up and maintaining theoperations. Their access to formal credit is not easier compared to the medium and largeenterprises. Some studies (EBRD 2004; Hossain 1998; PECC 2003) concluded that theinability to access to credit is one of the major bottlenecks of SME, as almost all ofthese economies have poorly developed banking sectors. Thus, this financing problemhinders their normal business operations that result in the lack of potentiality for futuregrowth. Empirically, it has been tested and found (Beck et al. 2005) that lack of access to

3

external finance is a key obstacle to firm growth, especially for SMEs. A number of studies(Schiffer and Weder 2001; Beck et al. 2005; and Beck and Demirgüç-Kunt 2006) usingfirm-level survey data have shown that SMEs not only perceive access to finance and thecost of credit to be greater obstacles than large firms, but see these factors as constrainingSMEs (i.e., affect their performance) more than large firms.

Small entrepreneurs face several difficulties in obtaining finance from the formal sector.Interest rate and collateral requirement are among the major problems inhibiting their accessto finance from the formal financial institutions. Haque and Mahmud (2003) reveals that,high interest rate, collateral requirement and lack of skills and attitude of bankers are amongthe most significant problems for small and medium entrepreneurs in availing of financefrom the formal financial institutions. Quader and Abdullah (2008) ranked high lending rateand collateral requirement as the most significant financing problem for the demand side.On the other hand, financial institutions also encounter several problems while financingsmall enterprises. A report revealed that collateralrequirements, weak credit skills and practices, cumbersome loan processing anddocumentation were the major supply side problems in most of the Asian countriesspecifically in the ASEAN countries for financing SMEs. In addition, Beck (2008)revealed that banks in developing countries are less exposed to SMEs, tend to providea smaller share of investment loans, and charge higher fees and interest rates to SMEsrelative to banks in developed countries.

Availability of required working capital at appropriate time is another significant problemfor most of the small businesses. For the day to day business operation, timely availability ofworking capital and its utilization is required. This kind of problem arises mainly due todelay in payments made by the debtors. The funds of many small enterprises in industrialunits are blocked in receivables. As a result, recycling of funds is affected and productionsuffers. In his study, Hossain (1998) revealed that SMEs encounter great difficulties whileraising fixed and working capital because of the reluctance of banks to provide loans toSMEs. In many cases, it is found that financial institutions take long time for processing theworking capital loan even after taking the positive credit decision.

Low quality financial statements, lack of quality information, and lack of adequateguarantees often hinder small enterprises to have access into the formal financial sector.Most of the literatures (Demirgüç-Kunt and Maksimovic 1998; Beck 2005, andBeck Demirgüç-Kunt 2006) showed that around the world informality and low qualitybalance sheets, lack of quality information and lack of adequate guarantees stand out as

RAM Consultancy Services (2005)

et al.

et al.and

4

SME-specific factors that banks perceive as obstacles in serving these firms. Using a surveyof banks in Argentina and Chile, Torre (2008) showed that, informality and low qualitybalance sheets in Argentina, lack of quality information in Chile, and lack of adequateguarantees in both countries stand out as SME-specific factors that banks perceive asobstacles in serving these firms. Similarly, Stephanou and Rodriguez (2008) pointed outsome problems related with the demand side as informality, unavailability and unreliabilityof financial statements, low managerial capacity of owners, their family-owned nature andcredit worthiness. (2005) depicts that lack of information about the SMEs tothe lending institutions is also a great problem to ensure access to finance.

Most of the entrepreneurs in our country are illiterate and are unable to prepare properbusiness plan that may help them to achieve their goal easily. Proper documentation, on theother hand, creates major problems for obtaining funds from the formal sources. Many SMElinked products and services are available in different financial institutions but in many casessmall businesses are not aware about these products and services. These problems are alsosupported by empirical evidence. (2005) report identified some problemsfrom the demand side as lack of well-developed business plan, problems related todocumentation, lack of knowledge about the available SME financing products provided bydifferent financial institutions.

OECD (2006) study pointed out several problems on both the demand side and supply side asthe difficulties that SMEs encounter when trying to access to financing. These are:incomplete range of financial products and services, regulatory rigidities or gaps in the legalframework, lack of information on both the bank's and the SME's side. In the same paper, thestudy also focused on the problems relating to the attitude of the banks, in particular, start upsand very young firms that typically lack sufficient collateral, or firms whose activities offerthe possibilities of high returns but at a substantial risk of loss.Along with the finance relatedproblems, there are some non financial problems like managerial capacity, willingness topay, lack of motivation to grow, lack of using money efficiently etc. are associated with thesmall businesses. In this context, Brkanovic (2005) provides insights about the non-financialobstacles of SME financing in Serbia, like lack of modern mechanisms in deploying financefor the SMEs.

After reviewing different literatures and studies, it is evident that the small enterprises(the demand side) are encountering multidimensional problems while obtaining financefrom the formal financial sector. Moreover, there exist many barriers in this sector in theform of underdeveloped or inefficient legal and administrative framework.

et al.

RAM Consultant

RAM Consultant's

5

Bakht (1998) and Ahmad et al. (1998) revealed in their study that the policy environmentwithin which SMEs in Bangladesh operate imposes legal, regulatory and administrativeconstraints. Sometimes the entrepreneurs need to procure various papers and documents tobe eligible for loan and therefore they need the support from the different regulators andadministrators. But in many cases they face difficulties in this regard.

This paper examines the present scenario of financing problems identified by the demandside and the responses of the supply side. Thus the specific objectives of the paper are:

(i) To identify the problems faced by small enterprises in obtaining loans fromfinancial institutions in Bangladesh.

(ii) To point out the responses and initiatives of the supply side to address the problemsfaced by the demand side and

(iii) To identify and analyze the gap between demand side expectations and the supplyside responses and finally to formulate suggestions for policy initiatives.

To achieve the objectives of the study, data has been collected both from primary andsecondary sources. Primary data have been collected through interview and questionnairesurvey from both the demand side and supply side stakeholders. For this purpose, two sets ofquestionnaires (Appendices 3 & 4) were developed; one set for demand side and the otherone for supply side. For collecting the information from the demand side, as many as twelvedistricts have been selected on the basis of the concentration of small enterprises mentionedin the 'SME Credit Policies and Programme 2010' by Bangladesh Bank. However, thecurrent study does not extensively cover the small businesses in rural areas and moreemphasis is given to the urban and semi-urban areas of the twelve districts where smallenterprises are concentrated. From these districts, 509 small enterprises were interviewedthrough the questionnaire. Among 509 small enterprises, 96 (18.86%) from manufacturing,335 (65.81%) from trading and 78 (15.33%) from the service sector were randomly selected.

As one of the main objectives of the study is to identify the major problems of the demandside, the entrepreneurs were selected from both the group of existing and potential (who areyet to get any financing facilities) borrowers of the formal financial institutions. The existing

1.1 Objective of the Study

1.2 Data and Methodology

3

3Dhaka, Narayang nj, Chittagong, Comilla, Noakhali, Barisal, Narsingdi, Gazipur, Rajshahi, Nilphamar , Dinajpur and

Rangpur.a i

6

borrowers identify the problems related to SME financing by the formal financialinstitutions. On the other hand, the other group provides good insights regarding access toformal finance. For better understanding the ranks of the demand side problems, descriptivestatistics (Appendix-1) have been used and to judge the significance of the data set, one wayANOVA(Appendix-2) has been performed.

For collecting the supply side information, a sample survey was conducted on 26 financialinstitutions consisting of State-owned Commercial Banks (SCBs) , Private CommercialBanks (PCBs) , development financial institutions , foreign banks operating in Bangladeshand some non-bank financial institutions . To justify the problems of the demand side, boththe accepted and rejected loan proposals of some particular banks and financial institutionswere also reviewed. While selecting the sample of small enterprises and banks/FIs,the following factors were considered:

i) Different sectors of small enterprises such as manufacturing, trading and servicewere considered.

ii) Financial institutions having extensive involvement in SME financing wereconsidered.

iii) The number of SME linked products offered by banks and NBFIs to respond to thecustomer needs.

Published literature, research papers, different books were reviewed to complete thetheoretical background and relevant websites were visited to collect secondary information.

This paper is divided into eight sections. After a brief background as part of introduction(Section-1), Section-2 highlights the current status of SMEs in Bangladesh. Section-3reveals small enterprises' access to formal credit. Section-4 represents the stakeholder's rolesin small enterprise financing in Bangladesh. Section-5 presents the major problems faced bysmall enterprises in Bangladesh. Section-6 focuses on the responses of supply side againstthe problems raised by the demand side. Section-7 analyzes the gap between demand andsupply side and, finally, Section-8 represents the recommendations.

4

5 6 7

8

4

5

6

7

8

Sonali Bank Ltd., Janata Bank Ltd., Agrani Bank Ltd., Rupali Bank Ltd.Uttara Bank Ltd., Pubali Bank Ltd., AB Bank Ltd., National Bank Ltd., Eastern Bank Ltd., Islami Bank Bangladesh

Ltd., IFIC Bank Ltd., NCC Bank Ltd., EXIM Bank Ltd., BRAC Bank Ltd., Bank Asia Ltd., Mutual Trust Bank Ltd.,The City Bank Ltd., Social Islami Bank Ltd.

Bangladesh Krishi Bank, BASIC Bank Ltd., Rajshahi Krishi Unnayan Bank.HSBC, Commercial Bank of Ceylon PLC.IDLC Ltd., ULC Ltd., IPDC Ltd.

7

2. Current Status of SME Financing in Bangladesh and Role of Financial Institutions

Table 1: Current Status of SME Loan Compared to Total Loan

The current status of the SME financing has been analyzed in terms of SME loan comparedto total loan, targeted SME loan and achievement, segregation of SME loan in small andmedium enterprises, sector-wise disbursement of SME loans by the financial institutionsand disbursement of SME loan to the women entrepreneurs.

Table 1 highlights the current status of the SME outstanding loan compared to the total loanprovided by the banks and non-bank financial institutions operating in Bangladesh. In 2010(Jan Dec), the share of SME loan in total outstanding loan on the part of State-ownedCommercial Banks (SCBs) was the highest 31.79% compared to Specialized Banks (SBs)20.64%, Foreign Commercial Banks (FCBs) 10.21%, and Private Commercial Banks(PCB) 19.12% in the banking sector. The average of all banks showed that the totaloutstanding loan in the SME sector was 21.48%. It was observed that the FCB's outstandingloan in this sector was the lowest, only 10.21%. In case of the Non Bank FinancialInstitutions (NBFI) the share of SME loan compared to total outstanding loan and advanceswas The average of all banks and NBFIs was only 21.07%.

In 2011 (January-June), the Table shows that SCBs' share of SME sector in total loan was27.81%, while the shares of SBs, FCBs, PCBs and NBFIs were 20.22%, 9.30%, 18.81% and15.22%, respectively. The average share of all banks and NBFIs in SME sector was only20.12%. While the survey conducted by Beck et al. (2009) found that the average share ofSME sector in total loan is 41%, 69%, 14% and 8%, respectively in India, Sri Lanka,Pakistan and Nepal. Therefore, SME Financing by the FIs in Bangladesh is lagging far fromIndia and Sri Lanka. But it is ahead of Pakistan and Nepal.

-

-

13.91%.

(Tk. in Crore)

Source: Bangladesh Bank, SME & Special Programmes Department

Name ofBanks/NBFIs

2010 2011 ( January-June)

Total Loans&

Advances

BalanceOutstandingof SME Loan

% of SMEOutstanding

to TotalLoans

Total Loans&

Advances

BalanceOutstandingof SME Loan

% of SMEOutstanding

to TotalLoans

SCB 68702.48 21839.54 31.79 78557.74 21845.81 27.81SB 20578.15 4247.31 20.64 22462.76 4541.94 20.22

FCB 18486.44 1887.54 10.21 20812.24 1936.08 9.30PCB 204442.22 39083.85 19.12 219788.24 41332.98 18.81

Total Banks 312209.29 67058.24 21.48 341620.98 69656.81 20.39NBFIs 17741.02 2468.34 13.91 18943.22 2883.44 15.22

Total Banks& NBFIs 329950.31 69526.58 21.07 360564.20 72540.25 20.12

8

Table-2 is concerned with the overall status of total target, total disbursement, achievementof target and percentage of SME disbursement by banks and NBFIs'. In 2010 (Jan-Dec), allthe banks and NBFIs surpassed their respective targets. The highest target achievers(222.70%) in that year were the SBs and the lowest target achiever (100.48%) were theNBFIs. It may be mentioned here that the targets were jointly set by the individual banks inconsultation with the SME & Special Programmes Department of Bangladesh Bank.

In terms of disbursement of SME financing by group of institutions, Table-2 shows that, in2010 the share of PCBs' disbursement in total SME loan was the highest at 75.63% andFCBs' disbursement was the lowest at 2.12%. The share of SCBs' and SBs' disbursement intotal SME loan was 14.05% and 5.03%, respectively. The disbursement status of SME loanof PCBs is very significant compared to the share of SCBs'. In Bangladesh, mainly thebanking system contributes towards SME financing. The share of SME loan disbursementby the banking system was 96.83% whereas the contribution of NBFIs was only 3.17%.

In 2011 (January-June) compared to 2010, the Table-2 shows that there was a significantdecline in the share of target achievement for SME loan in relation to total target indisbursing SME loan. The share of PCBs' SME loan disbursement was highest (81.42%)among all the group of financial sector (total banks and NBFIs). The total SME disbursementby the banking sector was 96.42% while for the NBFIs it was only 3.58%.

Table-3 shows the segregation of SME loan into small and medium enterprises on the basisof the total SME loans disbursed by the banks and NBFIs in Bangladesh. In 2010,

Table 2: Targeted SME Loan and Achievement

(Tk. in Crore)

Source: Bangladesh Bank, SME & Special Programmes Department

Banks/NBFIs

2010 2011 ( January-June)

TotalTarget

TotalDisburse-

ment

% ofAchieve-ment toTarget

% of SMEto Total

SME Dis-bursement

TotalTarget

TotalDisburse-

ment

% ofAchievement toTarget

% of SMEto Total

SME Dis-bursement

SCB 5083.10 7523.98 148.02 14.05 7668.00 2107.98 27.49 8.06SB 1210.00 2694.66 222.70 5.03 3365.00 1225.89 36.43 4.69

FCB 731.69 1133.93 154.97 2.12 1197.43 592.12 49.45 2.26PCB 30144.6 40494.57 134.33 75.63 42325.9 21302.00 50.33 81.42

Total Banks 37169.4 51847.14 139.49 96.83 54556.3 25227.99 46.24 96.42NBFIs 1688.66 1696.79 100.48 3.17 2393.80 935.35 39.07 3.58

Total Banks& NBFIs 38858.1 53543.93 137.79 100 56950.1 26163.34 45.94 100

9

the percentage of small enterprises loan compared to total SME disbursement ranges from34.25% to 47.39% among the SCBs, SBs, FCBs and PCBs. The aggregate disbursement insmall enterprises by all banks was 42.82% and by NBFIs was 49.17%. The totaldisbursement by the financial sector in small enterprises was 43.02%.

In 2010, the share of medium enterprises' loan to total SME disbursement ranges from52.61% to 65.75% among the SCBs, SBs, FCBs and PCBs. The aggregate disbursement inmedium enterprises by all banks was 57.18% and by NBFIs was 50.83%. The totaldisbursement by all banks and NBFIs was 56.98%. Therefore, the banks' and NBFIs' totalSME loan disbursement was concentrated more in medium enterprise sector (56.98%) andless in small enterprises sector (43.02%).

Although, in 2011 (January-June) the concentration of total SME disbursement in smallenterprises (44.66) and medium enterprises (55.34) remained almost similar to those in theprevious year, but there was a significant shift in disbursement by the SCBs, SBs and NBFIsfrom medium enterprises to small enterprises. The SCBs' share in small enterprisesfinancing was 58.95% and 41.05% in medium enterprises. The SBs' concentration in smallenterprises was 42.92% and in medium enterprises it was 57.08%.

The share of NBFIs' was 62.91% and 37.09%, respectively in small enterprises and mediumenterprises. If the focus for concentration in small enterprises continues by all the banks andNBFIs then the small enterprises will be able to be benefited and they will be able to graduatefrom small to medium enterprises category.

Table 3: Segregation of SME Loan in Small and Medium Enterprises

(Tk. in Crore)

Source: Bangladesh Bank, SME & Special Programmes Department

Banks/NBFIs

2010 2011 ( January-June)

Small% of TotalDisburse-

mentMedium

% of TotalDisburse-

mentSmall

% of TotalDisburse-

mentMedium

% of TotalDisburse-

ment

SCB 3458.23 45.96 4065.75 54.04 1242.64 58.95 865.34 41.05SB 923.01 34.25 1771.65 65.75 526.18 42.92 699.71 57.08

FCB 537.40 47.39 596.53 52.61 274.17 46.20 317.95 53.8PCB 17281.86 42.68 23212.71 57.32 9053.66 42.50 12248.34 57.5

Total Banks 22200.50 42.82 29646.64 57.18 11096.65 43.99 14131.34 56.01NBFIs 834.39 49.17 862.40 50.83 588.39 62.91 346.96 37.09

Total Banks& NBFIs 23034.89 43.02 30509.04 56.98 11685.04 44.66 14478.3 55.34

10

Table- 4 highlights on the sector-wise disbursement of SME loan by the banks and NBFIs inBangladesh. The disbursement of SME loan was categorized as service sector, trading sectorand manufacturing sector. In 2010, disbursement of SME loans by all banks was 67.35% intrading, 27.72% in manufacturing and only 4.94% in service sector. On the other hand, theNBFIs concentration for trading, manufacturing and service sectors were 47.92%, 28.01%and 24.07%, respectively.

Here it is evident that banking sector disbursed SME loan largely in the trading sector andleast in the service sector, while NBFIs maintained more or less balanced approachcompared to the banking sector in disbursing their SME loan. The aggregate average of SMEloan disbursement by the banks and NBFIs was 66.69% in trading sector, 27.73%manufacturing sector and 5.59% in service sector.

The 2011 (January-June) figures revealed that 63.51%, 30.14% and 6.35% were disbursed intrading, manufacturing and services sectors respectively by the banks and NBFIs. 2011(January-June) experienced a little increase of SME loan disbursement in the trading,manufacturing and service sector compared to 2010. It is evident that, trading sector isgetting more finance from the banks and NBFIs. If the banks and NBFIs do not reallocatetheir funds for the manufacturing sector then the productive sector would not develop.Bangladesh is at present largely engaged in the manufacturing of common consumer goods,requiring rather simple technologies that are predominantly labor-intensive and that do notrequire a very high degree of skills to produce. Thus, increasing financial access to SMEmanufacturing can ensure the better growth for future.

Table 4: Sector-wise Disbursement of SME Loan

(Tk. In Crore)

Source: Bangladesh Bank, SME & Special Programmes Department

Name ofBanks/NBFIs

2010 2011 ( January-June)Total

Disburse-ment

% toServiceSector

% toTradingSector

% toMfg.

Sector

TotalDisburse-

ment

% toServiceSector

% toTradingSector

% to Mfg.Sector

SCB 7523.98 3.05 61.50 35.45 2107.98 3.37 55.24 41.39SB 2694.66 1.65 49.86 48.49 1225.89 2.04 52.16 45.79

FCB 1133.93 12.81 47.93 39.27 592.12 12.05 49.22 38.73PCB 40494.57 5.11 69.59 25.30 21302.00 6.08 66.12 27.80

Total Banks 51847.14 4.94 67.35 27.72 25227.99 5.80 64.13 30.07NBFIs 1696.79 24.07 47.92 28.01 935.35 21.12 46.80 32.07

Total Banks &NBFIs 53543.93 5.59 66.69 27.73 26163.34 6.35 63.51 30.14

11

The women entrepreneurs are contributing to our national economy and they are creatingjobs as well. Therefore, women entrepreneurs are coming forward by establishing SMEs andthey are desperately seeking financial assistance from the formal financial institutions.But the contribution of formal financial institutions in financing women entrepreneurs arenot that much significant. Table-5 shows the status of SME loan disbursement to the womenentrepreneurs by the banks and NBFIs in Bangladesh. In 2010, the average disbursement ofSME loan for women entrepreneurs to total SME loan disbursement was 3.73% by all banksand 4.29% by NBFIs. The aggregate disbursement by all banks and NBFIs was only 3.75%in 2010.

In 2011 (January-June) the aggregate disbursement to women entrepreneurs by all banksand NBFIs was 3.66%. It would be a worthy contribution to the society and to womenentrepreneurs if the banks and NBFIs can disburse more SME loan to them.

Banks and NBFIs are very important stakeholders in the field of small enterprise financing.They are playing an important role in ensuring access to finance for the small enterprises.The FIs are trying to align their businesses by developing small enterprise based products.The NBFIs are offering factoring (Receivable Financing), a very good product for workingcapital financing for their clients. This is definitely a good initiative by the NBFIs in thecontext of Bangladesh.

Although financing of SEs in off-farm rural economic activities are largely dependent onequity financing from personal and family savings, currently banks and financial institutions

Table 5: Disbursement of SME Loan to the Women Entrepreneur

(Tk. in Crore)

Source: Bangladesh Bank, SME & Special Programmes Department

Banks/NBFIs

2010 2011 ( January-June)

TotalDisburse-

ment

Disbursementto Women

% to Dis-bursement

TotalDisburse-

ment

Disbursementto Women

% to Dis-bursement

SCB 7523.98 73.89 3.51 2107.98 31.73 3.38SB 2694.66 58.03 4.73 1225.89 43.98 6.72

FCB 1133.93 2.88 0.49 592.12 1.28 0.46PCB 40494.57 806.81 3.79 21302.00 348.32 3.51

Total Banks 51847.14 941.61 3.73 25227.99 425.31 3.61NBFIs 1696.79 40.12 4.29 935.35 21.89 5.27

Total Banks &NBFIs 53543.93 981.73 3.75 26163.34 447.20 3.66

12

are also coming forward to provide finance to this sector. Different initiatives have alreadybeen taken and practiced by the financial institutions in order to facilitate the smallenterprise financing mostly at the behest of Bangladesh Bank. Some of those initiatives areas follows:

- Separate SME division, SME units/centers and dedicated desk.- Separate SME dedicated desk for women entrepreneurs.- Separate monitoring team for SME.- Separate team for selling loan and collecting deposit through SME products.- Special credit risk management team for SME banking.- Different trainings for SME officials as well as for entrepreneurs.- Commission/incentives based on the performances of direct sales team.- Dedicated collection team for SME loan.- Customized products and services for SME.- Establishment of SME/Krishi Branch.- Delegate loan authority to the branch managers and head of SME up to a certain limit

for quicker decision.- 24 hours call center and doorstep banking.- Organizing SME service fortnight in every years.- Develop clusters under area approach etc.

Beck et al. (2002) clarify how financial constraints affect firms of different sizes. Their studyof 4,000 firms in 54 countries offers evidence that large firms internalize many of the capitalallocation functions carried out by financial markets and financial intermediaries. Theyconclude that financial constraints affect the smallest firms most adversely and that anincremental improvement of the financial system that helps relax these constraints will bemost beneficial for SMEs.

Choudhury Raihan (2000) conducted a survey on SME access to credit under(SAPRI) study where they found that, “the access to

formal credit is not available at all to 50.53 percent of the stakeholders. Only 35.79 percent ofSME stakeholders enjoy unrestricted access to the formal credit. The rest (13.68 percent) ofthem have restricted access to the formal credit”.

9

3. Small Enterprises'Access to Formal Credit

and StructuralAdjustment Participatory Review Initiative

9Every initiative may not applicable for all FIs

13

10As the survey emphasizes more on the urban and semi-urban areas, the results shows better access to formal credit.

However, it might show different result if the enterprises of the rural areas could be covered.

Willing to take furtherloan 167 (88.83%)

Total Sample 509

Manufacturing 96

Trading 335

Service 78Not received

202 (39.69%)

Loan received

307 (60.31%)Not satisfied

119 (38.76%)

Satisfied

188 (61.24%)

Not Applied

149 (73.76%)

Applied but notreceived 53 (26.24%)

Not willing to take furtherloan 21 (11.17%)

Willing to take further loan 85(71.43%)

Not willing to take furtherloan 34 (28.57%)

Reason:

Doing business with their ownmoney or borrowing from family/relatives/

friendsReasons:

- Lack of collateral

In this study, a sample survey was conducted on 509 small enterprises of which 18.86% werefrom manufacturing concerns, 65.81% were from trading concerns and 15.33% from theservice concerns. The survey result (Figure-1) showed that 60.31% enterprises receivedloans from banks and other financial institutions, while 39.69% enterprises did not receiveany loan from the formal financial institutions. Out of those enterprises who received loan,46.11% enterprises received the full amount they had applied for and the other 53.89%enterprises received a part of their total requirement.

10

Figure 1: Survey Results on Access to Formal Credit from Banks and NBFIs

Source: Authors' analysis based on survey questionnaire

Total Sample 509Manufacturing 96

Trading 335Service 78

Loan received307(60.31%)

Not Received202 (39.69%)

Applied but notreceived 53(26.24%)

Not Applied149 (73.76%)

Not satisfied119 (38.76%)

Satisfied188 (61.24%)

Willing to take further loan167 (88.83%)

Not willing to take further loan21 (11.17%)

Not willing to take further loan85 (71.43%)

Not willing to take further loan34 (28.57%)

Reason:

Doing business with their ownmoney or borrowing fromfamily/relitives/friends

Reasons:

- Lack of collateral- Un-registered business- New business- Lack of managerial and

technical expertise- Poor business condition- Non-fulfillment of loan

conditions- High documentation- Non-availability of guarantor

14

In comparison to the previous study (Choudhury and Raihan 2000), our study found that60.31% of the small enterprises got the access into the formal credit while the other 10. 41%enterprises did not have their access at all. On the other hand, 29.27% of enterprises did notapply for formal credit as they managed their funds by themselves.

Among the enterprises who received loans (Fig -1) from the formal financial institutions,61.24% enterprises were satisfied in terms of loan covenants and, of them, 88.83%enterprises were willing to take further loan. But 11.17% enterprises were not willing to takefurther loan from the financial institutions mainly due to the fact that the requirement ofborrowing was over.

Again, among the enterprises who received loan (Fig -1) banks and financialinstitutions, 38.76% enterprises were not satisfied with the loan covenants and requirements.From the questionnaire survey and interview of different entrepreneurs we found thatinterest rate is the major reason for their dissatisfaction. About 76.51 per cent of thedissatisfied respondents claimed and gave the priority on interest rate. Complex and longprocessing, deposit of blank cheque against loan, too much paper work were also highlyemphasized by them. Total survey results are shown in igure-2.

11

12

ure

ure from

F

Figure 2: Reasons for Dissatisfaction with Bank Loan

Source: Authors' calculation based on survey questionnaire (Multiple responses)

11

12

Out of 509 enterprises 53 enterprises applied for loan but did not get the loan. Therefore, 10.41% of total sample didnot have their access at all from formal financial institutions

Out of 509 enterprises 149 enterprises did not apply for loan

Deposit blank cheque against loan

Bankers' negligence

Interest rate is high

Too much paper work

Sanctioned less than required amount

Profit goes to the bank for high interest

Repayment schedule is not in favour

Process is complex and long

No response

15

It is important to note that from the dissatisfied enterprises, 71.43% enterprises were willingto take further loans from banks and financial institutions and 28.57% enterprises were notwilling to take further loan. Again, from the satisfied respondents 11.17% enterprises werenot willing to take further loan. Thus, 10.81% enterprises showed their unwillingness to takefurther loan from the formal sector and the reasons they identified are:

.

From the survey it is found that 39.69% enterprises did not receive any loan from banks andfinancial institutions. Out of the total enterprises who did not receive loan, 73.76%enterprises did not apply for any loan as they were carrying on their business with their ownfinance and borrowing from other informal sources like family, relatives and friends. In ourquestionnaire survey we tried to identify the general perceptions of the entrepreneurs abouttheir reluctance in applying for loan form formal sector by asking the question “why are younot willing to borrow from banks/FIs?” with a detailed list. The responses of the question areexhibited in Figure-3.

On the other hand, 26.24% enterprises applied for the loan but they were rejected.The reasons behind the rejection were lack of collateral, un-registered business, newbusiness, lack of managerial and technical expertise, poor business condition,non-fulfillment of loan conditions, high documentation, and non-availability of guarantor.

business is notprofitable, negative attitude of bankers, harassment by the financial institutions, interestrate and service charge is high, obtaining loan from informal sector is easy, security andguarantee requirement is high

Figure 3: Reasons for not Obtaining Loan from Formal Sector: Entrepreneurs' Perception

Source: Authors' calculation based on survey questionnaire (Multiple responses)

44%

67%

31%

77%

49%

21%

13%

86%

41%

Could not fulfill the loan conditions

Complicated loan procedures

Bank’s negligence or lack of interest

Lack of collateral security

Easy availability of funds from other sources

Borrowing is disgraceful

High interest rate

High sunk cost for obtaining loan

Being afraid to involve with fin institution

16

4. Stakeholders' Roles and their Initiatives for Financing Small Enterprises inBangladesh

A large number of stakeholders are involved in developing SEs in Bangladesh. They havealready taken several initiatives from their end to facilitate the small enterprises for theirsuccess. Some of the stakeholders' roles and initiatives are discussed below:

Among the different ministries of the Government of Bangladesh, the Ministry of Industrytakes different initiatives to create better environment for the financial institutions to takepart in the SME financing activities. Bangladesh Government has already felt theimportance of SMEs in the economic development of the country. This is why thegovernment has developed a SME policy in the year 2005. In continuation to that, in 2007,the ministry of industry undertook SME sector development program with the objective tosupport government efforts to expedite the development of the SME sector throughstrengthening the policy environment for SMEs and improving SMEs access to credit andrelated services. As a part of the continuing efforts of the government to develop the SMEsector, the Industrial Policy 2010 has greatly emphasized for the growth and balancedexpansion of this sector. The industrial policy 2010 states the role of the government asfollows:

(a) Government will accentuate and sustain SME activities through motivation, loanallocation and training of the entrepreneurs.

(b) Refinancing the SME sector through the 3 (three) funds created by Bangladesh Bankwill continue.

(c) Women Entrepreneurs will be given priority in the SME sector. At least 15% of totalsanction will be held in reserve in favour of the women entrepreneurs and the interestrate will be 10% only.

(d) Special preferences will be provided to the development of the industries dealing withInformation and CommunicationTechnology.

Besides, the Ministry of Industry through BSCIC (Bangladesh Small and Cottage IndustriesCorporation) is identifying small entrepreneurs all over the country and providing themfinance, training and other related services. One of the important services that are providedby the BSCIC is that it arranges fairs to ensure selling of the products produced by theirregistered organizations. So the government through its different organs is trying to creategood business environment for the small entrepreneurs of the country.

4.1 Government

17

4.2 Central Bank

Bangladesh Bank, the central bank of Bangladesh, is very much proactive in takingfavorable policy decision and providing guidelines related to small enterprise financing forthe banks and non-bank financial institutions. For example, the Bangladesh Bank hasdeveloped and

: two important documents for enabling the banks to takeactive part in the small enterprise financing activities. Besides, Bangladesh Bank arrangesroad show, SME center/branch monitoring etc.

The Prudential Regulations for Small Enterprise Financing (2004) include 13 prudentialregulations. These regulations cover sources and capacity of repayment and cashflow-backed lending, personal guarantees, per party exposure limit, aggregate exposure of abank/ NBFI on SE sector, limit on clean facilities, securities, loan documentation, marginrequirement, Credit Information Bureau (CIB) clearance, minimum condition for takingexposure, proper utilization of loan, restriction on facilities to related parties, classificationand provisioning for assets. Besides these regulations it also stipulated developmentguidelines which consists of policy guidelines (product program guidelines, segregation ofduties, credit approval, credit approval authority), procedural guidelines (approval process,maintenance of negative files), credit administration (credit documentation, disbursement,custodial duties, compliance requirements), risk management (credit risk, third party risk,fraud risk, liquidity & funding risk, political & economic risk, operational risk, maintenanceof documents & securities, internal audit), collection and remedial measures (monitoring,recovery, collection objective, identification & allocation of accounts, collection steps,productivity tracking, agency arrangement) and preferred organogram and responsibilities.The central bank has developed this comprehensive guideline for enabling the formalfinancial institutions to carry on financing the small enterprises of the country. Afteranalyzing the policy guidelines of Bangladesh Bank, we have found that there is nopolicy- induced barrier in small enterprise financing.

In addition to Prudential Regulations 2004, Bangladesh Bank has developed the '' which is a further policy initiative for the financial

institutions to participate in small enterprise financing. This document focuses ons

Prudential Regulations for Small Enterprise Financing 2004 SME CreditPolicies & Programmes 2010

,

SME CreditPolicies and Programmes 2010

teps/measures taken by Bangladesh Bank for SME development, target for SME credit,area approach method, cluster development policy, priority to the small entrepreneurs,

18

priority to refinance in industry (manufacturing) and service sector, special arrangement forwomen entrepreneurs, identification of the real women entrepreneurs, eligibility of theborrower, training programmes, monitoring of SME credit, methods of monitoring of SMEcredit, SME service centre, clusters of SME.

The major success of this policy publication is the identification of potential SME clusters ofBangladesh across industries. This is very much helpful for the financial institution toundertake the cluster approach and area approach for financing the small enterprises.

The Bangladesh Bank has initiated refinancing facilities for providing low cost fund forfinancing small enterprises by the financial institutions. Bangladesh Bank has beencontinuing its refinancing scheme in 2010-2011 against the disbursed loan in SME sector bythe banks and financial institutions. The amount of the disbursed loan in SME sector wasTk. 29092.61 crore in December 2010 of 2010-2011( ). Table-6reveals that, during 2010-2011(uptoApril 2011), twenty one banks and twenty two financialinstitutions received Tk. 1806.00 crore from the refinance scheme as against 19,339enterprises. The refinance scheme included Tk. 1185.88 from Bangladesh Bank fund(number of enterprises 13,146 of which 2,554 are women entrepreneurs with Tk. 182.77crore), Tk. 284.92 from IDA fund (number of enterprises 2929) and Tk. 334.94 from ADBfund (number of enterprises 3264).

It is important to note that most of refinanced funds go to the trading purpose whileBangladesh Bank has given the priority to the industry and service sector as mentioned in the'SME Credit Policies and Programmes 2010'. This policy also indicates that 100% claims inindustry and service sector is being refinanced in order to create a friendly environment for

SMESPD, Bangladesh Bank

Table 6: Summary Information on SME Refinancing (up to April 2011)

Source: Bangladesh Bank, SME & Special Programmes Department

Name ofBanks/FIs

Refinanced

Amount Refinanced (In crore Taka) No. of Beneficiary Enterprises (sector wise)

WorkingCapital

Mid TermLoan

Long TermLoan

TotalLoan

IndustrialLoan

CommercialLoan

Service Total

BangladeshBank

266.99 638.40 280.49 1185.88 3600 7616 1930 13146

IDA 69.09 119.15 96.67 284.92 1137 1306 486 2929

ADB 144.48 132.27 58.19 334.94 800 2096 368 3264

Total 480.56 889.83 435.36 1805.74 5537 11018 2784 19339

19

employment generation and higher production. The amount disbursed among the 19,339enterprises included Tk. 480.56 as working capital loan, Tk. 889.83 as medium term loan andTk. 435.36 as long term loan.

Small and Medium Enterprise Foundation got registration from the Ministry of Commerceon 12 November 2006 and from the Registrar of Joint Stock Companies and Firms on 26November 2006 under the Companies Act (Act XXVIII), 1994 . It is an independent andunique non-profit organization. It has been established with the objective of developing theentrepreneurship by reducing information asymmetry, proper training and education,targeted credit wholesaling and easing the distribution mechanism of SME products.The SME Foundation provides low cost funds to the financial institutions, which are used tofinance the small enterprises. By this credit wholesaling operation, the SME Foundationprovides low cost fund to the financial institutions which enable them to finance the smallenterprises at a lower interest rate. This is a pre-finance facility at the rate of 4% interest rate.Till date, SME Foundation has disbursed Tk. 7.75 crore to different financial institutions forlending to specific clusters especially in the manufacturing sectors. The financial institutionsusing this facility are EBL, MIDAS, NCCBL, and MTBL.Among the other initiatives, it hasundertaken projects for developing SME database, SME cluster mapping etc. So SMEFoundation can play a very important role for the development of SME sector of the country.SME Foundation should take proper initiative to collect low cost fund and let the financialinstitution use it for financing small enterprises. In addition to that it can undertake extensiveresearch initiatives to provide better policy advocacy for formulating dynamic SMEpolicies.

National Association of Small and Cottage Industries of Bangladesh (NASCIB) is a tradeassociation established in 1984 to highlight SMCI issues and work for the development ofsmall and cottage industries of Bangladesh. It organizes SMCI fairs for the marketing oftheir products produced by the indigenous raw materials, conducts research for thedevelopment of the sector, provide consultancy to the entrepreneurs country-wide andconducts training for the skill development of the entrepreneurs. NASCIB often, incollaboration with the banks and non-bank financial institutions, organizes events(e.g. Bank-SME beach festival at Cox's Bazar) to disseminate information about the bankingproducts available for the small enterprises. But the efforts are not sufficient enough againstthe desired need of the sector.

4.3 SME Foundation

4.4 NASCIB

20

4.5 NGO/MFI

4.6 Business Bodies

These institutions in the financial system of Bangladesh are called the semi-formal financialinstitutions. These are meeting the demand of financial services of the greater rural area ofthe country where the banks and other formal financial institutions have limited or no access.So they are playing a pivotal role in financing the rural small enterprises and contribute in abetter fashion to the economic development of the country.

Local business associations, such as, chambers of commerce and women entrepreneurs'associations play very important role in creating better environment for the smallenterprises. These organizations are working as bargaining institutions to ensure betterpolicy initiatives by the government, Bangladesh Bank and other regulators.

From the literature review, it has been observed that both demand side and supply sideencountered several problems such as, high interest rate and fees, collateral and guaranteerequirements, negative attitude of bankers, cumbersome loan processing anddocumentation, lack of quality information, lack of well developed business plan,ascertainment of capacity or willingness to pay, working capital requirements, informalityand low quality financial data, low managerial capacity of owners, high transaction cost,capital shortage, high administrative costs etc. Keeping these constraints in mind, the studyhas examined the current scenario regarding the problems faced by small enterprises inBangladesh.

In our questionnaire survey we provided a list of tentative problems faced by our smallbusinesses to rank them according to their merit as per the entrepreneurs' real experiences.In our list we also provided one option for 'other problems- if any' and in this regard theypointed out three other problems which are high sunk cost for obtaining loan, malpractices insanctioning loan and lack of managerial capacity. The detailed descriptive statistics of theproblems stated by the entrepreneurs are shown in appendix-1 and the list is exhibited inTable-7 according to their importance.

5. Major Problems Faced by Small Enterprises in Bangladesh

13

13The merit was justified by the rating scale starting from 'not significant' to 'most significant' ranked from 0 to 4 with

0 bearing not significant and 4 bearing most significant.

21

From Table-7, it is clear that high interest rate is the most significant problem according tothe perception of the entrepreneurs followed by security and guarantee, working capitalrequirement, complexity of documentation etc. However, Choudhury and Raihan (2000)conducted a similar survey on SME access to credit and found some different results asbarriers for access to credit which are shown in Table-8.

In their survey they identified collateral as the prime barrier followed by bribe, delays, highinterest rate, banker's disinterest etc. On the other hand, our survey (2011) result showedhigh interest rate as the prime barrier. So it is evident that the factors acting are the primebarrier(s) has been changed significantly. The reasons for their perception may be due to thelower interest rate charged for corporate loan compared to SE loan, lower return from thebusiness compared to the borrowing rate, lower bargaining capacity, etc. Moreover,nowadays the borrower is more conscious about the rate of interest than before. Inconnection with the collateral, both the studies found approximately similar result. But incase of bribe, previous study found it as the second most significant barrier while the currentstudy found it as a very insignificant barrier of access to credit. Our study found workingcapital as the third important problem although the previous study did not recognize it as aproblem at all. Both the studies have identified some other common barriers (such as longloan processing time, sunk cost, malpractice, and negligence of FIs, etc.) that are illustratedinTable 7 & 8.

Table 7: Main Obstacles Cited by Entrepreneurs forAccessing Formal Financial Sector

Authors' calculation based on survey questionnaire

* Importance is ranked from 0 to 4, with 4 being the most significant

Source:

Sl No. Obstacle Importance*1 High Interest Rate 3.692 Excessive Security and Guarantee Requirement 2.913 Insufficient Working Capital Loan 2.814 Complexity of Documentation 2.465 Long Loan Processing Time 2.15

6 Unstructured Financial Information 1.857 Financial Institutions’ Negligence 1.738 High Sunk Cost for Obtaining Loan 1.589 Malpractices in Sanctioning Loan 1.4010 Lack of Managerial Capacity 1.23

22

Among the problems high interest rate has the highest mean 3.69 (Table-7) signifying themajor obstacle in the opinion of the respondents. The values against high interest rate havethe lowest standard deviation which indicates consistency in ranking the problem.The second highest mean is 2.91 (Table-7) with the excessive security and guaranteerequirement.

Although it has been repeatedly emphasized by the central bank to lend money to the smallenterprises with little or no collateral, financial institutions are reluctant to lend withoutcollateral securities which is observed from the table where the respondents put higher values inregard to the security and guarantee. The third highest mean (2.81) is associated with theproblem of working capital which is consistent with the prior researches in the field. The smallentrepreneurs suffer a lotdue to lack of available working capital.The fourth important problemis documentation (2.46). As evident in earlier literatures, small entrepreneurs cannot approachtheformal financial institutionsdue to rigiddocumentation requirement.

t[In Descending Order]

The next important problem we identified is the long processing time (2.15) required todisburse the credit. The respondents opined that the average loan processing time should bearound 10 days. Although during the survey we have found that a few of the financialinstitutions are taking as little as 5 working days to disburse the credit but most of theinstitutions, due to lack of their internal capacity, cannot deliver the services so promptly. In afew instances, we have found some of the institutions are taking even more than a month todisburse their credit. In case of PCBs, loan processing time is much shorter than the SOBsand SBs. The reality is that if the institutions take longer time for loan processing, it would

Table-8: Barriers o Access of Credit: Overall Perception of Demand Side

Source: Choudhury and Raihan (2000), SAPRI SME Survey

Sl No. Barrier Percentage of Respondents1 Collateral 79.42 Bribe 66.03 Delays 54.64 High Interest Rate 39.25 Banker's Disinterest 27.86 Guarantees Required 27.87 Inadequate Volume of Credit 22.78 Harassment 11.39 High Sunk Cost 8.2

10 Lack of Information 6.2

23