Sme Aug Oct2010

15

AUGUST -OCTOBER 2010 COMPLIMENTARY WITH THE FINANCIAL EXPRESS READ TO LEAD FOCUSON EMERGING ENTERPRISES CL US T ER S AC RO SS I ND IA COVER STORY CL US T ER S AC RO SS I ND IA Exclusive interview Unido representative in India Ayumi Fujino Focus Gujarat industries Special Tec h solutions Exclusive interview Unido representative in India Ayumi Fujino Focus Gujarat industries Special Tech solutions

-

Upload

rohit-behl -

Category

Documents

-

view

230 -

download

0

Transcript of Sme Aug Oct2010

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 1/19

AUGUST-OCTOBER 2010 COMPLIMENTARY WITH THE FINANCIAL EXPRESS

READ TO LEAD

FOCUSON

EMERGING

ENTERPRISES

CLUSTERS ACROSS INDIA

COVER STORY

CLUSTERS ACROSS INDIA

Exclusive interview

Unido representativein India Ayumi Fujino

FocusGujarat industries

SpecialTech solutions

Exclusive interview

Unido representativein India Ayumi Fujino

FocusGujarat industries

SpecialTech solutions

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 2/19

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 3/19

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD August-October 20104 SMALL AND MEDIUM ENTERPRISE WORLD5

EDITORIAL SUPPORTVERGHIS CHANDY

MONALISA SEN

DESIGNSANTOSH PL

SPECIAL PROJECTS TEAMG. SUBRAMANIAN

Mumbai Space Marketing

g.subramanian@expressindia .com

POOJA RANA

Delhi Space Marketing

pooja .rana@expressindia .com

RATISH NAIR

Chennai Space Marketing

ra tish.nair@expressindia .com

JAMEEL ADWAN & JUGAL MIRANI

Gujarat Space Marketing

jugal.mirani@expressindia .com

PRODUCTIONB.R. TIPNIS

General Manager

Copyright:The Indian Express Limited.All

r ights reserved.Reproduction in any

manner,e lec tronic or otherwise ,in wh ole or

in part ,with out prior written permission is

prohibited

A SPECIAL PROJECTS INITIATIVEHOW TO REACH US

We prefer to receive letters via email,wi thout

attachments.Writers should disclose any connection

or r e la t ionship with the subjec t of the ir com m ents .

All le t te r s m ust inc lude an addre ss and dayt im e and

evening phone numb ers.We reserve the right to edit

letters for clarity and space

monalisa .sen@expressindia .com

Email: sme@expressindia .com

The Indian Express Limited

2nd floor,Expr ess Towers,

Narim an Point, Mumba i - 400 021

Tel: 022-22022627 Ext n: 389 Fa x:022-22022139

FOCUSON

EMERGINGENTERPRISES

C o n t e n t s

Public procurement

preferences for SMEs■ P RAGHAVAN POLICY P4

MRP-based valuation andbulk industrial sales■ SALONI ROY & JAYANTA KALITA

TAXATION P2 0

Where small industriesbloom■ JYOTSNA BHATNAGAR

FOCUS: GUJARAT P21

Customer satisfaction islinked to relevant data■MAHESH KIRAN

VIEW P31

Optimum investment forstart-up enterprises■ SANJAY ANANDARAM

INDIPRENEUR P32

“Nokia Tej offers businesses a speedyonline order management system”■ ANTTI-JUSSI SUOMINEN

Head of commerce in corporate development, Nokia P2 6

‘Cisco Capital enables our customersto spread out their payments’■ PATRICK MATHIAS

Vice-president, sales-west, Cisco India & Saarc P2 7

‘Data storage is no longer a backroom

IT issue’■ SATYEN VYAS

Director ASG in SMB division, Dell India P2 9

‘Internet is a great medium to buildvisibility for business’■MANISH DALAL P30

T E C H S O L U T I O N S

COVER STORY

‘SMEs areunable to

understand orabsorb manyincentives’■ AYUMI FUJINO

Unido representative in India and head of the

South Asia regional office INTERVIEW P8

Drivers of Indianmanufacturing■ COVER STORY CLUSTERS P13

COVER PHOTOGRAPH BYOINAM ANAND

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 4/19

■ P RAGHAVAN

A

KEY FEATURE of the MSME Development

Act of 2006 has been the preferentia l t reat-

ment given to small units in public procure-

me nt . The Ac t s t i pul a t ed t ha t gove r nme nt

and pu blic sector un its wil l give preference

to goods and services from the SSI sector.Th ough provi-

s ions regarding this ar e s t i l l to be formu lated, the gov-

ernment has recently said the Cabinet wil l c lear the

policy, which wil l make i t binding on governm ent de-

partments and PSUs to source at least 20% of their pur-

chases from small-scale units.

Public procurement can lend vita l demand support

to specific segments ofin dustry,whether they are pub-

l ic sector or small-scale units . This is because of the

large share of public procurement in GDP.In developed

countr ies public procurement accounts for about 20% of

GDP, a nd in I ndi a t he s ha r e i s a vi s i bly muc h highe r

30%.

I n I ndi a t he us e of publ i c pr ocur e me nt a s a pol i cy

tool to support specific segments of industry h as been

largely restr ic ted to a 10% price preference for public

s e c tor u ni t s . Howeve r, a dva nc e d e c onomie s l i ke t he

United States and the European Union, and some devel-

oping countr ies l ike Mexico,have used public procure-

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD 6

Public procurementpreferences for SMEsLegal provisions alone cannot ensure that the small-scale industrybenefits from government procurement

P o l i c y

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 5/19

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD 8

ment as a tool to support small busi-

ness units .

Though th ere are no common defi-

ni t i ons of the s ma l l i ndus t r y i n t he

United States and the European

Union,the available information sug-

gests that small businesses supplied

23% of the federal pr ime contracts in

the US in 2005 while they accoun ted

for half of the private sector employ-

ment and the value-add in the economy.In contrast , the

s ha r e of the s ma l l bus ine ss i n Eur ope a n publ i c pr o-

curement is est imated to be a much higher 42%.

But these figures relate only to public contr acts above

the thresholds set by the public procurement direct ives

and do not count subcontracts of al l s izes awarded to

SMEs .Howe ve r t he SMEs ’ s ha r e s of publ i c pr oc ur e -

ment above the EU thresholds varied sharply,r angingfrom a high 78% and 77 % in Slovenia and Slovakia to a

low of35% and 31% in Fran ce and the UK.

In the developing world, the m ost recent example of

gove r nme nt ba c king t o s ma l l uni t s t hr ough pr oc ur e -

ment polices comes from Mexico,where the s t imulu s

package to combat the recession required that a t least

20% of government purchases be made from small and

medium companies .

Publ i c pr oc ur e me nt i n I ndi a i s

highly decentral ised with purchases

being made by the Centre , the s ta tes

a nd publ i c s e c tor uni t s . Howeve r,

there are n o national-level legal provi-

s ions on public procurement and the

quantum is general ly decided by pub-

l ic policy.However, the ministry of f i-

na nc e pr e pa r e s a ma nua l on pur -

c ha s e of goods , s e r vi c es a nd wor ks , a n d t hi s a c t s a s a

guideline to the central government.Other ar ms of the

government, l ike the Central Vigilance Commissioner

and th e Directorate General of Supplies and Disposals,

have also issued guidelines,w hich are followed by other

departments .

Some sta tes l ike Tamil Nadu and Kar nataka have re-

cently enacted legis la t ion to ensure transparency inpr oc ur e me nt .Howe ve r, t he Ta mi l Na du gover nme nt

has taken a s tep forward and extended ma rketing sup-

port to micro and small manu facturing enterprises by

giving domestic enterprises a 15% price preference in

pur c ha s e of goods, a s pr ovided i n t he Ta mi l Na du

Transparen cy in Tenders Act , 1998.

However, legal provisions a lone cannot ensu re that

the small-scale industry benefi ts f rom government pro-

curement. Globally public procurement has been asso-

ciated with corruption an d the World Bank est imates

that br ibes paid on th is count wil l add up to $1 tr i l l ion

each year.

India’s governm ent procurem ent practices and proce-

dures are not very condu cive for the small industr y as

they lack transparency.India is s t i l l not a s ignatory to

the WTO Agr e e me nt on Gove r nme nt Pr oc ur e me nt

(GPA) but the country has obtained an “observer” status

in the WTO Committee on Government Procu remen

in Februar y 2010.One way to curb th e malpractices

publ i c s e ctor pr oc ur e me nt i s t he u s e of inf or ma t io

technology.Th e govern ment has fol lowed up on thi

front and asked al l procurers to switch to th e e-procur

ment regime.

But a small or medium un it has to overcome variou

other generic constraints i f i t is to act ively gain frothe new procurement polic ies .A recurr in g complai

from small units involved with government procur

ment is that their small s ize itself is a handicap as th

large s ize of the government or ders de facto exclude

them from part ic ipation s in ce they are unable to te

der for the whole contract . This handicap can be ove

come only if the government direct ives a l low contrac

to be awarded in separate lots .France has adopted thi

method to overcome the s ize constraints of small unit

Ye t a nothe r ma jor ha n dic a p of s ma l l uni t s i s t he

l imited access to information on governm ent procur

ment. This can be overcome to a large extent throug

e -pr oc ur e me nt .Howe ve r ,wi th a va s t numbe r of We

por t a l s c a te r i ng t o t he gove r nme nt , only s ome uni

wil l be able to tap the ful l potentia l of the policy eve

a f t er t he i n t r oduc t ion of e -pr oc ur e me nt on a l a r g

scale.

A suggest ion made in this context is the use of ce

tral ised Websites for e-procurement in federal or larg

countr ies .Electronic tenderin g faci l i t ies ,which al lo

author i t ies to invite bids online,wou ld also improv

small units’access to government pr ocurement.

At the more general level , the introdu ction of a 20%

reservation for small units has to be accompanied b

guida nc e on t e nde r pr oc e dur e s .Unt i l t ha t h a ppe n

MSME units wil l f ind i t hard to ful ly tap the public pr

curement opportunit ies . ●

Size remains ahandicap for SSIs.The large size of

government ordersde facto excludes

them fromparticipation

August-October 2010 SMALL AND MEDIUM ENTERPRISE WORLD9

P o l i c y

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 6/19

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD 10

Ms Ayumi Fujino has taken charge as the Unido repre-

sen t a t i ve i n Indi a and head of t he Sout h Asi a re-

gional office in July this year.Before this,Fu jino was the

Unido representat ive in Th ailand and head of the re-

giona l office from 2006.

Fujino began h er career with Unido in th e 1980s, serv-

ing in various capacit ies.While at the Unido h eadquar-

ters in Vienna from 1997 to 2006,Fujin o designed and im-

plemented various technical cooperation projects for the

development of MSM Es,especially in rural areas in select

industria l sector clusters like food processing,textiles and

leather, with the geographical focus on countries in Sub -

Saharan Africa,South Asia and Central America.

She was also closely involved in Unido program mes for

the promotion of entrepreneurship through local produc-

tion networks and mark et facilitation by linking rural/ lo-

cal products with urban and export mark ets.

Throughout h er career with Unido,Fujino has been in-

volved in inter-agency collaboration in programm es and

projects with organisat ions l ike the World Bank , ADB,

African Development Bank, Islamic Development Bank ,

IFAD, UNDP, UNFPA,Unifem, UNHCR, FAO, ILO,Un-

esco,W HO as well as internationa l NGOs like CARE and

World Vision.

Fujino shared,in an email interview,her vision for India

with FE SME World’s Monalisa Sen .Excerpts:

As a Uni do representat ive i n Indi a , wh at are your

immediate priorities?

The United Nations Industr ia l Development Organisa-

t ion (Unido) aspires to reduce poverty through sustain-

able industr ia l development. To this end, i t focuses i ts

expertise and resources to support developing countries

and economies in tran si t ion in their efforts to promote

their in dustr ies---- especial ly their micro, small and

medium enterprises (MSMEs)---so that they h ave the

fullest opportunity to develop a f lourishing productive

sector, to increase their part ic ipation in inter national

trade and to safeguard their environmen t. Hence,my

priori ty as the Unido r epresentat ive here wil l be to pur-

sue our essentia l long-term objectives of promoting the

growth of industry, in part icular in the SME sector,and

combatin g climate chan ge in the fight again st poverty.

This core agenda will continu e to drive our efforts to cre-

ate jobs,ra ise incomes and l if t people out of poverty

through th e sustainable development ofindu str ies .

I t may be relevant to mention here a m ajor new flag-

ship project–the integrated cluster development pro-

gramme (ICDP)–a five-year programme 2009-2014 --that

we will be implementing in cooperation with th e depart-

ment of industr ia l policy and promotion (DIPP),m in-

i s t r y of c ommer c e a nd i ndus t r y,gove r nme nt of I ndi a.

This is intended to provide integrated,tu rn key solutions

to a host of constraints affect ing the performa nce of

SMEs in pre-selected clusters in several sectors by ad-

dressing their technology,qu ali ty and environment-re-

la ted needs.The programme wil l complement the assis-

tance to the same clusters a lready being extended to

them un der DIPP’s industr ia l infrastructure upgrada-

t ion scheme (IIUS).The progr amme is designed to im -

prove resource productivi ty and environmental perfor-

ma nc e of SMEs, in pa r t i c ula r i n a uto c ompone nt s ,

leather,chemical and other sectors ,and in doing so, i t is

expected that it will help tackle poverty issues and con-

tr ibute to environmental sustainabil i ty.

What do you see as the m ajor chal l enges fac i ng

SMEs in India?

As you know,small and medium enterpr ises play a key

role in th e growth process,as they collectively account for

a substantia l share of the country’s industr ia l employ-

ment,outpu t and exports.

‘SMEs are unable to

understand or absorbmany incentives’

Ayumi Fujino, Unido India representative

C o v e r s t o r y

I n t e r v i e w

August-October 2010 SMALL AND MEDIUM ENTERPRISE WORLD11

PHOTOGRAPH BYOINAM ANAND

Unido’s newprojects areventuring intoinnovative aspectsof clusterdevelopment suchas CSR, energyefficiency andtwinning amongclusters inadvanced anddeveloping

countries

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 7/19

The constraints impeding their development are a lso

well known,such as:access to factors (finance, technol-

ogy,skil ls ,and support ing man agement processes) and

access to mark ets (logistics,compliance with standa rds,

access to quali ty cert if ication services ,design,product

range,packaging,branding, marketing and so on).

The vast majori ty ofSMEs are in the lower end of sup-

ply chain.In the case of India ,despite the fact that vari-ous polic ies and economic in centive schemes exis t ,

SMEs are in general not able to reach th e schemes due

to their l imited capacity for un derstanding and absorb-

ing such benefits.A lack of policy coherence for SME de-

velopment at the central and regional levels also poses

the challenge to many SMEs.

What are the Uni do act i v i t i es and

program m es i n Indi a i n re l at i on to

SMEs?

Currently, the for Unido operat ions

in India is set by ‘the five-year countr y

pr ogr a mme of c oope r a t ion be twee n

the Republic of India and Unido 2008-

2012.’to SMEs through cluster-based

approaches constitu tes a cross-cutting

the me of the count r y pr ogr a mme.

I n a ddi t i on t o t he SME s uppor t , we

also address the issues ofrais ing com-

peti t iveness through th e introduction

of environment-fr iendly technologies

and faci l i ta t ing the part ic ipation

of developing countr ies in the global

economy through south-south cooper-

at ion.Unido offers a r ange of services

to private and public sector institutions enga ged in SME

cluster development wh ich include:technical coopera-

t ion in the formulat ion and implementat ion of cluster

development pr ojects;and institutional capacity building

and policy advice for the dissemina tion of cluster devel-

opment polic ies a t regional and national scale.In addi-

t ion, i t offers tools such as c luster mapping; awareness

rais ing ini t ia t ives; tra ining for policy makers ,pr oject

managers and policy advisers involved in cluster develop-

ment; c luster twinnin g ini t ia t ives , including business-to-business networks, inter- inst i tut ional partn erships

and alliances between cluster associations;development

of horizontal and vertical networks and export consortia,

and monitoring and evaluation of cluster development

programmes.

Unido has been at the forefront of the SME cluster de-

velopment in India and has implemented a large num-

ber of projects since 1996.Wh ile the earlier cluster pro-

jects focused on economic issues – that is,en han cing the

competi tiveness of under-performing clusters , the la ter

projects are ventur ing into innovative aspects of cluster

development such as corporate social responsibil i ty

(CSR) in MSME practices, impr oved energy efficiency

and twinn ing among clusters in advanced and developing

countr ies as well as trade facilitation.Unido c lus t e r pr ogr a mme s i nc lude : the Cha nde r i

handloom and Sindhudurg food processing clusters ;

SME cluster development and CSR in the Jalandhar

sports goods cluster;and th e MSME cluster development

program me in Orissa---Barpall i (handlooms),Konark

and Pur i (stone carving),Rourkela (fabrication),and the

Sal leaves non-timber forest produ cts

clusters in Baripada.

The cluster development approach

is applied also to the national

programm e for technology upgrada-

t ion of brass and bell metal industry

a nd a r t i s a na l e nt e r pr i s e s i n

Khagra and other ar eas ofWest Ben-

ga l a nd ne ighbour ing s t a t e s a s

well as the cane and bamboo net-

working pr oject .

On the trade capacity building

s ide, t he pr oj ec t , “ Suppor t i ng s ma l l

and medium sized manu facturers in

the automotive component indu stry

in I ndi a –Unido pa r tne r s hip pr o-

gramm e phase-II” ,w as successfully

completed in 2009.Th is project aimed

at s trengthening the Indian SME au-

tomotive component suppliers to meet the require-

me nt s of ve hi c le a nd t i e r -1 a utomot ive c ompone nt

manufacturers and faci l i ta te their integrat ion in the

global supply chain.

Another imp ortant ongoin g project is the “consoli-

dated project for the development of SMEs in India”

which focuses on the “twinnin g”clusters as a new area

of int e r ve nt ion. The pr oj e ct , l a unc he d i n 2007, i s t he

largest c luster development programme in India and is

f inanced by the I ta l ian governmen t and working withthe development commissioner of MSMEs,ministry of

MSMEs,as i ts counterpar t .

Fina l ly, i n t he a r e a of e ne r gy a nd e nvi r onme nt , t he

project on energy eff iciency and qua li ty s tandards in

the cerami c industr y in India---coverin g ceramics clus-

ters in Morbi and Thangadh in Gujarat and Khu rja in

Uttar Pradesh– has been completed in J une th is year.

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD 12

Thai authoritieshave provided manysupport measures toSMEs in recent years.The One Tambon OneProduct initiative has

reached great

success. Theinitiative showcasestraditional products

for the local andinternational markets

C o v e r s t o r y

I n t e r v i e w

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 8/19

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD 14

What were Unido’s major contributions to SMEs in

Indi a i n the spheres of trade, technol ogy, pol i cy, f i -

nance and value -add ?

In keeping with i ts a ims,s trengthening of the compet-

i t iveness of SMEs through technology-led intervention

has often been cited as one of the most successful compo-

nents of Unido programmes so far. As an evaluation of

the ‘country service framework ’(2007) noted: “The clus-

ter development programm e (CDP),developed over the

past decade,is Unido’s flagship programm e in India ,

which has also significantly shaped the policy environ-

ment towards the MSMEs”.

I ts contr ibution has evolved over a period of t ime –

from ini t ia l ly awareness ra is ing of the potentia l and

structuring of the methods and tools ,

then policy advice and now,interven-

t ions in several new areas wh ere clus-

ter ing also becomes a tool to achieve

other object ives such as poverty re-

duction, CSR,ener gy eff ic iency and

be t t er c oor dina t ion of va r ious s e r -

vices offered to the SME clusters like

finance, investment and trade promo-

tion etc. Programmes in Tamil Nadu,

Maharashtra , NCR,West Bengal and

Karnatak a have been using the clus-

ter methodologies for the furth er de-

velopment of Indian companies .

As a n e xa mple of c oncr e t e out -

comes for t r ade promotion for Indian

SMEs,Unido has created subcontract ing and partner-

ship exchange (SPX) centres in Delhi ,Pun e and Chen-

nai in the footwear, leather and automotive sectors for

connecting mainly small enterprises to the foreign mar-

kets . Actions have been taken at the inter nal level

through the development of their competi t iveness and

quality up gradation an d at the external level by enhan c-

ing their possibi l i t ies to be included in global value

chain and as main suppliers for big players in India and

abroad.

Another tangible intervention of Unido cluster devel-

opme nt pr ogr a mme s i s t he de ve lopme nt of a mutua l

credit guara ntee (MCG) in order to add ress the issue of limited access to finan ce for SMEs due to the lack of col-

la teral . This is based on the mechanism being estab-

lished based on th e best practices from Italy,by r eplicat-

i ng t he s uc c es s ful I t a l ia n e xpe r i e nce of mutua l

guarantee associat ions into the Indian context .Unido,

together with th e Indian Venture Capita l Associat ion

(IVCA) and Indian An gel Network (IAN),is orga nising a

series of awareness-rais ing workshops on equity in-

vestors , including private equity funds and an gel in-

vestors.

What’s the SME scenario in Thailand? How it is dif-

ferent from Indi a , especi a l l y i n term s of technol -

ogy, scal e and governm ent support?

As in many countr ies , in Th ailand too SMEs play a

cri t ical role in economic development. In fact ,accord-

ing to est imates ,SMEs account for a lmost 95% of indus-

tr ia l enti t ies in the country and over 20% of the coun-

try’s total in dustr ia l workforce. The constraints facing

the SMEs in Thailan d are similar to those faced by SMEs

in most other developin g countries---nam ely, issues re-

la t ing to ut i l isat ion of advanced tech-

nologies in production pr ocesses;ac-

cess to credit especially access to

formal sector f inancing;quali ty s tan-

da r ds ;ma r ke t i ng; a nd ma na ge me nt

related constraints,particularly in the

context of the need to enhan ce com-

peti t iveness of the enterprises .

In recent years these constraints

have been exacerbated by the global

economic downturn ,creat ing a tough

business c l imate . In order to help

SMEs,the Thai auth ori t ies have pro-

vided many support measures for the

promotion and development of SMEs,

includin g a ‘prom otion plan for SMEs

in Thailan d’ coinciding with the five-year ‘national eco-

nomic and social development plan,’an Office of Small

and Medium Enterpr ises Promotion and also a national

competi t iveness committee.F urth er , the One Tambon

One Produ ct (OTOP) initiative,based on Japan’s One Vil-

lage One Product (OVOP), has reach ed great success in

Thailand. The ini t ia t ive showcases local t radit ional

products for the local and intern ational markets throu gh

clever packaging and marketin g strategies coupled with

effect ive government faci l i ta t ion of the buy an d sel l

process.OTOP also faci l i ta tes the exchange of informa-

t ion and ideas for innovation at the r ural level ensuring

improved communication across various Tambons inThailand. While the cluster development approach per se

does not yet find the n iche in the SME sector in Thailand,

unlike in India ,vi l lage/commun ity-level business ini-

t ia t ives are being integrated into th e regional and na-

t ional supply chain through a very vibrant promotion of

produce- and sector-based associations nationwide,led by

both government and pr ivate sector associat ions. ●

August-October 2010 SMALL AND MEDIUM ENTERPRISE WORLD15

■ GOPAKUMAR WARRIER

INDIA ha s ove r 1 .55 mi l l i on MSME u ni t s .Of the s e ,

micro un its comprise 95.05% and sm all-scale units

4.74%.On ly 0.21% falls in th e mediu m-sized category.

Among the MSME units , 66.67% is categorised as

ma nuf a c tur ing e nt e r pr i s e s , a c c or ding t o qui c k r e -

sults of the fourth a l l-India census of MSMEs,2006-07.

With a c ont r i but ion of 50% to t he c ount r y’s i ndus -

tr ia l output an d 35% to direct exports , the SME sector

has achieved s ignif icant milestones for India’s indus-

tr ia l development.Within the SME sector,a key role is

played by clusters that have come up across th e coun-

try,some of which have been in exis tence for decades

and sometimes even centuries .

Ac cor ding t o a s t udy of the I ndi a n I ns t it u t e of Pu

lic Administr a t ion, there are 388 documen ted SM

clusters in India . Besides that , there are about 2,00

rur al- and ar t isan -based clusters .I t is est imated tha

these clusters contr ibute 60% of the manu factured e

ports from India . The SME clusters in India are est

mated to have a s ignif icantly high share in employme

generat ion compared to c lusters in other countr ies .

Some Indian SSE clusters are so big that they accoun

for 90% of India’s total production ou tput in selecte

products .For example, the knitwear cluster of Ludh

ana. Almost the entire gems & jewellery exports ar

from the clusters of Surat and Mumbai. Similar ly, th

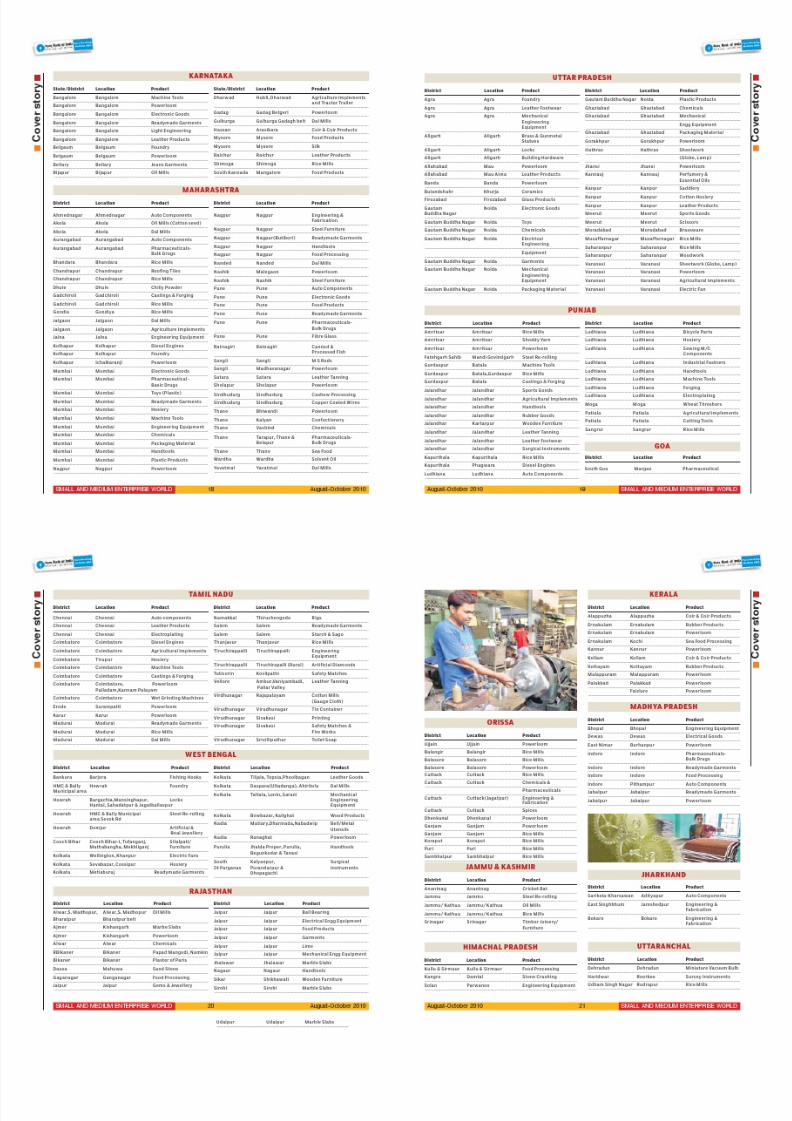

Drivers of Indian manufacturingIndia has 388 documented SME clusters, besides about

2,000 rural- and artisan-based clusters

Clusters

Anantpur Rayadurg Readymade Garments

Anantpur Chitradurg Jeans Garments

Chittoor Nagari Powerloom

Chittoor Ventimalta, Brass UtensilsSrikalahasti, Chundur

East Godavari East Godavari Rice Mills

East Godavari Rajahmundry Graphite Crucibles

East Godavari East Godavari Coir & Coir Products

East Godavari Rajahmundry Aluminium Utensils

East Godavari & East Godavari(EG) &West Godavari West Godavari Refractory Products

Guntur Guntur Powerloom

Guntur Guntur Lime Calcination

Guntur Macherla Wooden Furniture

Hyderabad Hyderabad Ceilling Fan

Hyderabad Hyderabad Electronic Goods

Hyderabad Hyderabad Pharmaceuticals

Hyderabad Musheerabad Leather Tanning

Hyderabad Hyderabad Hand Pumpsets

Hyderabad Hyderabad Foundry

Karimnagar Sirsilla Powerloom

Krishna Machilipatnam Gold Plating & Imitation

Jewellery

Krishna Vijayawada Rice Mills

Krishna Chundur, Kavadiguda, Steel FurnitureCharminar,Vijayawada

Kurnool Adoni Oil Mills

Kurnool Kurnool Artificial Diamonds

Kurnool & Kurnool Polished SlabsC ud da pa h ( Ba na ga na pa lle ,

Bethamcheria,Kolimigundla)Cuddapah

Prakasam Markapuram Stone Slate

Ranga Reddy Balanagar, Jeedimetla Machine Tools& Kukatpally

Srikakulam Palasa Cashew Processing

Visakhapatnam & Visakhapatnam, Marine FoodsEast Godavari Kakinada

Warangal Warangal Powerloom

Warangal Warangal Brassware

West Godavari West Godavari Rice Mills

District Location Product District Location Product

ANDHRA PRADESH

C o v e r s t o r y

I n t e r v i e w

SME CLUSTERS ACROSS INDI A

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 9/19

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 10/19

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 11/19

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 12/19

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD August-October 201022 SMALL AND MEDIUM ENTERPRISE WORLD23

■ JYOTSNA BHATNAGAR

IN GUJARAT, arguably the country’s most industr i-

a l ised s ta te ,small is beautiful . That’s evident from

the fact that i t ’s not only the Goliaths of corporate In-

di a , i nc luding Re l i a nce ,Es s a r ,Ada ni a n d Tor r e nt ,

which are prospering but thousands of Davids ofth e

indus t r i a l s e ctor, t oo, a r e t hr iving a nd mus hr ooming

in al l parts of th e s ta te.

Ac cor ding t o l a t e s t i ndus t r i a l s ur ve ys, Guja r a t i s

home to ove r t hr e e l akh mic r o, s ma l l a nd me dium

units .Some important SME clusters in Gujarat include

readymade garments , drugs & phar maceuticals ,dyes

& int e r me dia t es a t Ahme da ba d; s hip-br e a king

Alang;re-rol ling mil ls a t Bhavnagar/ Shior;plast ic i

dustry a t Dhoraji ;brass parts a t Jam nagar; wall c lock

at Morbi;chemicals a t Nandesari ,Vapi & Ankleshwa

diesel engines, e lectr ic motors , ferrous cast ings,gol

& si lver ornam ents ,machin e tools,wr is t watch & com

ponents a t Rajkot;Powerlooms,diamonds,gems & jew

ellery, jar i a t Surat ;pottery & ceramics a t Surendra n

gar (Than) & Wankaner;ceramic products a t Than gad

and petrochemicals a t Vadodara.

While SMEs are spread al l over the s ta te , i t is Ahmed

abad that tops the MSME sweepstakes,accounting fo

21% of the total MSMEs followed by Surat and Rajko

Where small industries bloomThe state, home to over three lakh MSMEs, boasts of more than50 thriving industrial clusters T

a x a t i o n

■ SALONI ROY & JAYANTA KALITA

Our com pany i s based outs i de Indi a . We recentl y

set up a paint unit in India and we sel l our products

i n the reta i l m arket . We understand that we are re-

quired to adopt MRP-based valuation for the pay-

m ent of exci se duty on our products . Very often we

get orders from industrial buyers,who buy in bulk.

We were to l d the duty com putati on on M RP i s not

appl i cabl e for i ndustr i a l sa l es . P l ease advi se .

MRP-based valuation for levy of excise duty is gov-

ern ed by Section 4A of the Central Excise Act,1944.Th e

primary requirement for a t tract ing MRP-based valua-

t ion of goods is that the goods should be notif ied under

Section 4A ofth e Excise Act and on wh ich the retail sale

price should be declared under the Standards of

Weights & Measures Act (SWMA).Th e requirement to

declare the retail price on goods is governed by the provi-

s ions of SWMA and the Standards of Weights & Mea-

sures (Packa ged Commodit ies) Rules,1977 (PCR) and is

applicable on pr oducts intended for re ta i l sa le

Under the PCR,certa in exemptions have been made.

One is that ‘any pr oduct special ly packed for exclusive

use of any industry as raw materia l shall or for the pur-

pos e of s e r vi c ing a ny i ndus t r y’ would not be c ons id-

ered as product intended for re ta i l sa le.Th erefore, th e

sale ofbulk products to any indu str ia l consumer that is

not intended for re ta i l sa le should be outside

the pur vi e w of the PCR a nd s hould not a t t r a c t MRP-

based valuation.

O u r s i s a n e w l y s e t u p c o m p a n y c o n s t r u c t in g a

m anufacturi ng faci l i ty. We pay servi ce tax to ou r

v e n d o r s o n v a r i o u s s e r v i c e s i n t h i s c o n n e c t i o n .

Can we take credi t for the servi ce tax pai d?As per Cenvat Credit Rules , the prim ary condit ion for

availing of credit is that the service for which the credit

is sought should qu alify as an ‘input service’.The defin-

i t i on of input s e r vi c e i nc lude s s er vi c e s us e d by t he

manufacturer in re la t ion to set t ing up,m odernisat ion,

renovation or repairs ofa factory. Therefore ,you may

avail of Cenvat credit for the service tax paid on ‘ input

services’used for set t ing up the factory.

However,we would l ike to highlight th at in Circular

No 98/1/2008-ST dated Ja nuar y 4, 2008,the CBEC has

clar if ied that Cenvat credit of input services (such as

‘commercial or industr ia l construction service’and

‘works contract service’) used in th e construction of

immovable property cannot be availed of. The reason-

ing given is that those services are in the n ature of input

services towards the creat ion of an immovable prop-

erty,wh ich is subject to neither central excise duty n or

service tax.Th ough the circular was issued in the con-

t e xt of c ons tr uc t i on of a n immova ble pr oper ty t ha t i s

rented out , the author i t ies could use this for restr ic t-

ing Cenvat credit of services used for construction of

factories also.

In our view,the circular seeks to lay down a pr ovision

that is clearly contra dictory to the law as enum erated in

the c r e di t r ul es . I n t he pr e s e nce of a c l e ar l a w on t he

subject matter,a contrar y provision (by way of a c ircu-

lar) would clearly be inapplicable. However, the view

expressed in the c ircular does create a dispute and m ay

entai l l i t igat ion.

We are an EPC contractor and have recentl y been

awarded a contract for the construct i on of an SEZ

uni t . We understand that suppl y of goods and ser-

v i ces to an SEZ uni t i s exem pt from taxes and du-

t i e s . W i ll s u c h e x e m p t i on b e a v a i l ab l e i f w e p r o -

cure goods from thi rd part i es?

Rule 27 of the SEZ Rules ,2006 provides that exemp-

tions,drawbacks and concessions and other benefi ts on

goods and services a l lowed to a SEZ unit for set t ing up

and main tenance of factory building is a lso al lowed to

the c ont r a c tor s a ppoint e d by suc h a uni t . To e njoy

these benefi ts,procurements should be m ade joint ly bythe contractor and the unit . All documents should bear

the na me of the uni t a nd t he c ont r a c tor a nd s hould be

filed jointly in their nam e.Hence, the benefits shall also

be available to you if they are pr ocured joint ly.

The au thors work with Ern st & Young.Replies here

do not constitute professional advice

MRP-based valuation andbulk industrial sales

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 13/19

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD August-October 201024 SMALL AND MEDIUM ENTERPRISE WORLD25

The 2003 industr ia l policy also

made it easy for MSMEs to avail of fi-

nancial assis tance for quali ty u pgra-

dation, including obtaining ISO 9000

and ISO 14000 cert if icat ion, as a lso

assis tance for f i l ing patents .

The 2003 policy was followed up by

the Gujarat governm ent with yet an-

other water-shed step–the enactment

of the the Micro,Sm all and Medium

Enterprises Development Bil l in

2006.The Act aim ed to facilitate promotion an d develop-

ment of micro,small and medium enterprises in a sus-

ta inable way.Fu rtherm ore, i t a lso empowered the s ta te

governm ent with several discret ionary measures to fa-

ci l i ta te and h elp such enterprises gradu ate themselves

to new levels of growth. One of i ts pr imary object ives

was to make pr ovisions for ensuring t imely and smooth

flow of credit to SMEs and to help them mitigate busi-

ness risk s to effectively achieve a greater su ccess rate.

Gujarat has been reviewing the industr ial policy period-

ical ly and has been making al te

a t i ons i n vi e w of the c ha nging ma

ket paradigm. Only recently, th e po

icy has once again b een re- touche

Terming the SME sectors as th

ba c kbone of indus t r i e s i n Guja r a

the government is a lso draf t ing a r

habil i ta t ion package that would i

c lude revival of or a l lowance of ex

f or s i c k un i t s .Suppor t wi l l a l so b

given f or m a r ke t de ve lopme nt , i

c luding ini t ia t ives for creat ing the ‘Made in Gujara

brand by th e SMEs.

Industr y observers say the policy and the Act hav

largely been instru mental in the exponentia l growth o

the SME sector. Between 1996 to 2006,th e MSME secto

has seen an average investment of Rs 500 crore annu

ally and has led to the creat ion of over 7 lakh jobs.SME

ha ve a vibr a nt ma nu f a ctur ing ba s e i n Guja r a t . He r

again, th e s ta te governmen t is taking ini t ia t ives to em

power industr ia l c lusters to take on the challenges

Between them, the three ci t ies account for 51% of the

MSMEs . I n t e r ms of inves tme nt , t he MSMEs a c c ount

for over Rs 80 million wh ile production is pegged at well

over Rs 100 million.

The bur ge oning numbe r of SMEs in Guja r a t i s a

te l l ing test imony of the innate entrepreneurial spir i t

of the Gujarat is .SMEs in Gujarat have been on a rol l,

part icular ly in the past few years , than ks largely to the

pr oa c t ive s uppor t of t he s t a t e gove r nme nt .Re a l i si ng

the immense potentia l of the SME sector in contr ibut-

ing to the overal l growth of the s ta te , the Gujarat gov-

ernm ent has put in place a game-changer Gujarat In-

dustr ia l Policy in 2003, which focused special ly on

promoting the growth of MSMEs.

The policy was comprehensive in i ts reach and gave

top priori ty to labour r eform s in a bid to faci l i ta te in-

dustr ia l investment both for employment generat ion

and produ ctivi ty.I t a lso gave an impetus to creat ion of ur ba n a n d i ndus t r i a l i nf r a s t r uc tur e a nd s imul t a ne -

ously ushered in power reforms and port- led develop-

ment.But most importantly, the policy gave tangible in-

centives for set t ing up MSMEs, including interest

subsidies a t 5% for set t ing up n ew units as well as ex-

pansion and modernisat ion of exis t ing ones,and an in-

terest subsidy of 3% for technological upgradation.

While SMEsare spread allover the state,three cities—

Ahmedabad, Suratand Rajkot—

account for 51%of the units

Ahmedabad : Readymade garments, drugs &pharmaceuticals, dyes & intermediates

Surat: Powerlooms, diamonds, gems& jewellery, jari

Rajkot: Diesel engines, electric motors, ferrouscastings, gold & silver ornaments, machine tools,wrist watch & components

Vadodara: Petrochemicals

Alang: Ship-breaking

Bhavnagar/ Shior: Re-rolling mills

Dhoraji: Plastic industry

Jamnagar: Brass partsMorbi: Wall clocks

Nandesari, Vapi & Ankleshwar: Chemicals

Surendranagar (Than) & Wankaner: Pottery &ceramics

Thangadh: Ceramic products

Major SME clustersin Gujarat

f o c u s : G u j a r a t

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 14/19

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD August-October 201026 SMALL AND MEDIUM ENTERPRISE WORLD27

partment of one of the largest public sector banks,“The

MSME sector in Gujarat is extremely robust , owing

largely to the environment of the s ta te , the absence of

labour unrest and government suppor t and incentives.In

the last fiscal itself,th e sector posted a growth of 20-25%

in non-seasonal segments.”

The banker , however, gives much credit to the s ta te

government’s biennial Vibrant Gujarat investment

melas for the spurt in investment in Gujarat. So success-

ful has the hardsell of the s ta te by the Gujarat govern-

ment been that countr ies like Seoul and Japan are evin

ing interest in mak ing forays into the MSME sector o

the s ta te .Recently, South Korea h as expressed intere

in involving i tself with the SME sector of Gujarat in

major way and has plans to set up a world class innov

tion centre in th e s ta te .

e c onomies of s c a le a nd qua l i t y i n t he i nt e r na t i ona l

markets .Equal considerat ion is being given to man age-

r ia l and f inancial aspects by the s ta te while support ing

the m. I n a ma jor i n i t i a t i ve t o che c k c los ur e of s ma l l

units , the Gujarat governmen t has drawn up a “credit

against performance” scheme,wh ich is el ic i t ing rave

reviews from the indu stry.

The s ta te government has a lso decided to recognise

c lus t er s wi th a c r i t i c a l ma s s of minimum 50 uni t s

within a 10-km rad ius and is providin g common facility

centres and assis tance to c luster associat ions for act iv-

i t ies leading to s trengthening of clusters .

Today, Gujarat has several inst i tut ions th at are en-

gaged in cater ing for the growing demands and chal-lenges of the SME sector given the fact that with r apid

globalisat ion, i t has become crucial for SMEs to mit i-

gate business r isks and acquire a nimble outlook.In the

wa ke of e c onomic s lowdown in t he US a nd t he Eur o-

pean Union,coupled with severe man ufacturing compe-

t i t ion from China,SMEs in Gujarat are quickly adapt-

i ng t o t he c ha nging e nvi r onme nt wi th c a pa c i t y

building, infrastructur e augmentat ion , innovative f i-

nancing options, technology upgradation,investment in

research & development,enh anced quali ty s tandards,

and by f ine tuning mar keting s tra tegies .

Notable among the institu tions doing a sterling job for

the empowerment of the SME sector is Small Industr ies

Service Institute (Sisi).In Gujar at,Sisi h elps small-scale

industr ies meet various needs of planning,assessment

and imp lementat ion by offer ing services in technical

consultancy,industr ia l m anagement, tra ining and work-

s hops . Guja r a t I ns ti t u t e of De ve lopme nt Re s ea r c h

(GIDR),an autonom ous research body,u ndertak es study

on sectoral development. Most s tudies undertaken by

the inst i tute have focused on the development of small-scale rural industr ies .

Further , th e Industr ies Commissionerate ,a long with

the District Industr ies Centres (DICs),implements state-

level schemes for SMEs on an on going basis.

In the backdrop of such impressive growth,industry

watchers are bull ish about the prospects of MSME

growth in Gujarat .Says a ban ker heading the MSME de-

f o c u s : G u j a r a t

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 15/19

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD August-October 201028 SMALL AND MEDIUM ENTERPRISE WORLD29

Antti -Juss i Suom i nen ,head of commerce in corporate

development , Nokia, tel ls SME World’s M onal i sa Sen

about the concept of Nokia’s new service for small and

medium bu sinesses in India, cal led Nokia T ej .

Can you elaborate how Nok ia Tej works for SMBs?

Nokia Tej is a unique mobile productivity service.It is

a hosted mobile order management service that le ts

small and m edium bu sinesses (SMBs)

place orders and access order-rela ted

information via their Nokia han dsets .

Nokia Tej offers businesses an online

or de r ma na ge me nt s ys t e m tha t c a n

process nearly a l l business proce-

dures ,an d provide their supply chain

pa r tne r s r e l e va nt i nf or ma t ion r e -

mote ly a nd i ns t a nt l y. I t c a n be de -

ployed on m obile handsets ofusers ,a l-

lowing them to send and receive

or de r s , c onfi r m a nd r e vi e w or de r s ,

di s pa t ch de t a i ls , v i e w s a l e s r e por t s

and inventory s ta tus ,among others .

Nokia Tej can be integrated to the

user’s back-end system for invoicing an d accounting;

and by integrat ing the mobile payment solut ion for

business paymen ts and rela ted inform ation f low,al-

most the whole business process can be automated andmade mu ch more eff icient .

Nokia Tej is simple to configure,easy to u se.It is com-

patible with a l l GPRS-enabled Nokia d evices and does

not require addit ional investment in expensive and

cumbersome IT systems,and can be customised as per

the organisat ion’s requirement.

Can you m enti on speci f i c i ndustr i es that woul d

benefi t from thi s servi ce?

We believe that Nokia Tej is the idea l service for any

SMBs owner who wants to improve his /her produ ctiv-

ity and profitab ility.It is par ticularly effective for busi-

nesses with complex supply chains, such as manu fac-

turing,texti les or fast moving consumer goods.Nokia is

currently offer ing Nokia Tej services commercial ly to

various FMCG,texti le/appar el ,con-

s ume r dur a bl e s , r e a dy-ma de ga r -ments as well as pharmaceutical

companies with sales and dis tr ibu-

t i on c ha nne l s s pr e a d a c r os s t he

country.

What woul d be the average cost of

adopti ng Noki a Tej , i ncl udi ng the

handset cost per em pl oyee?

Nokia charges a nominal fee of Rs

1,250 per month for por tal access and

Rs 550 per user per month for en-

hanced productivi ty and automation

o f a n S MB . T h e co s t o f t h e No k i a

han dset & data cost (dependent on the operator/ net-

wor k pr ovide r of c hoice ) i s s e pa r a t e a nd i s only r e -

quired if the employees don’t already have a compatible

Nokia GPRS enabled handset .

How safe i s the data transm i tted through Noki a

Tej from vi rus and abuse s?

Nokia Tej is a secure hosted service.I t ensu res that

only an SMB and i ts defined network have access to or-

der re la ted data . ●

“Nokia Tej offers businesses

a speedy onlineorder management system”

Antti-Jussi Suominen,Head of commerce in corporate development, Nokia

T e c h

s o l u t i o n s

Patri ck M athi as , vice-president , sales-west ,Cisco In

dia & Saarc, tel ls SME World’s M onal i sa Sen abo

the company’s technology solut ions for SMB s and the f

nancing scheme i t has to mak e the products af fordable

What are the so l ut i ons Ci sco has for SM Bs?

Cisco now has the complete range of products to o

fer end-to-end techn ology solutions for SMBs.Compl

me nt ing t he e xi s t i ng r a nge of ‘plug & pl a y’ pr oduc

like the UC500 and ISR series for SMBs, WebEx and th

managed services offer ings, our new stora ge solutio

makes Cisco a one-stop-shop for SMB-targeted tech no

ogy infrastructure .

What is the latest offering ? How different is i t from

the earl i er one?

The most r ecent addit ion to the SMB portfol io from

Cisco is the Smart Storage solution, which significantl

expands the por tfol io and addr esses the specific co

cern area of storage.Th e Cisco NSS 300 Series Smar

Storage is a new family of affordable ,easy-to-use desktop network s torage solutions,which al lows small bus

nesses to secure and s tore cr i t ical business data ,sh ar

information and ru n their business better. This is th

first SMB-focused stor age solution from Cisco.

How affordabl e i s the product for Indi an SM Es?

‘Cisco Capitalenables ourcustomers tospread outtheir payments’

Patrick M athias,Vice-president, sales-west,Cisco India & Saarc

Nokia Tej isparticularly effectivefor businesses with

complex supplychains, such asmanufacturing,textiles or fast

moving consumergoods

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 16/19

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD August-October 201030 SMALL AND MEDIUM ENTERPRISE WORLD31

Indian SMBs,while price-sensi t ive,are a lso aware of

the value an d competi t ive advantage that good technol-

ogy infrastructure can bring to their business .Cisco’s

small business products We also have support mecha-

nisms through ou r f inancing arm, Cisco Capita l,which

e na bles our c us tome r s t o s pr e a d out t he i r pa yme nt s

over a certa in t ime-frame wh en choosing Cisco gear .

How do you just i fy the i nvestm ent i n th i s product

by an SM E?

Technology infrastructure is a core business require-

ment for many SMBs today.Ou r s torage solution is de-

signed so that businesses that invest in the technology

not only have their s torage n eeds fulfi l led,but they are

also able to enjoy a wide range of features that make i t

easy to insta l l and maintain .Our s torage solution cus-

tomers can also tap into a range of add-on applicat ions

l ike an integrated WordPress publishing platform,

iTunes server ,and FTP server .

What are the m ajor chal l enges that the SM B m ar-

ket faces i n Indi a?

The most s ignif icant challenge that SMBs face in In-

dia is to do with f inances available for investments in

technology. They also often have to make-do with

scaled-down versions of enterprise-c l a ss pr oduc t s, whic h me a n tha t

they probably pay for features that

they may never use.The propensity

of I ndi a n SMEs being i n c lus te r s

also proves challenging,especial ly

f or t he ve ndor or i n t e gr a tor who i s

tasked with instal l ing and maintain-

ing the SMBs infrastructure .

W h a t i s t h e l e v e l o f I T a d op t i o n

i n Indi an SM Es?

This is h ighly subject ive based on

the i ndus t r y ve r t i c al wi thin whic h

the bus ine s s ope r a t es . Typic a ll y,

businesses with the need for more

connectivi ty would have s l ightly more advanced IT re-

quirements than a business that uses basic IT for officeautomation.However,on a global scale ,when compared

alongside s imilar economies,In dian SMBs defini te ly

are c lose to the median.

What are the h i ndrances to IT adopti on?

The pr ima r y hindr a nc e i s t he minds e t .Ma ny bus i -

ness owners may feel that investing

in technology is n on-essentia l and

so delay i t unti l a l l other expendi-

tures are covered.

However, more technological ly

aware individuals an d process-ori-

ented organisat ions would quickly

realise the value added to the

business through an effect ive

IT network.

What i s your advi ce to Indi an

SM Bs?

Our advice to SMBs would be

that for every business , there is an ideal technology so-

lut ion just wait ing to be tapped.We recommend that a l lSMBs evaluate every aspect of th eir business ,with ex-

perts i f necessary,an d identify areas that could be im-

pr oved t hr ough a u toma t ion.The r e s ul ti ng huma n r e -

source bandwidth that is f reed up can be direct ly

ploughed back into the busin ess , leading to break-out

growth for the business . ●

For every business,there is an ideal

technology solution justwaiting to be tapped.We recommend thatSMBs evaluate every

aspect of their businessand identify areas that

could be improvedthrough automation

T e c h s o l u t i o n s

Satyen Vyas, director ASG in SMB division, Dell India

As technology adoption and data storage emerge as new

challenges for small an d m edium-sized businesses (SMBs)

of the country,Dell India sees opportunities for it to help the

segment and thr ive in the mark etplace.Satyen Vyas , d i -

rector,Adva nced Solutions Group in the SMB division of

Dell India, who ma nages the Dell enterprise products and

solutions business,shared his thoughts on th e subject with

SME World’s Monalisa Sen .Excerpts:

Data storage has becom e an i ssue of concern for i n-

dustry today.What are your views on i t?

One of the biggest challenges faced by companies today

is the exponential growt h in data an d the most effective

ways of managing that data .Given issues such as data

archiving, data security,disaster recovery & storing and

managing the information continuously s treaming in,companies recognise that this is no longer just a back-

room IT issue but real ly among the key CXO

concerns–the way this information is used makes i t a

business-driver.

At Dell ,a key focus ar ea for is Intel l igent Data Man-

agement solut ions, that is ,automated data management

of predictable ,scalable open data s torage. Dell is a lso

among th e leaders on the iSCSI s torage – the r ise of

10GbE is changing the dynam ics of storage systems,al-

lowing companies to have robust yet affordable, highly

scalable storage systems on the IP SAN protocol.ISCSI

SAN is of part icular interest to medium-sized busi-

nesses that require the f lexibili ty of larger enterprises ,

but h ave limited IT resources to deploy.

How is the storage m arket placed now? What is the

s i ze of the SM B segm ent?According to AMI-Partner s , the s torage hardware

market is estimated at Rs 1,583 crore–31% of this shar e

this a t tr ibuted to SMBs.Th e s torage hardware market

for SMBs is Rs 484.80 crore--SAN constitu tes 55% of the

market, Tape 17%,DAS 18% and NAS 10%.

W h a t a r e t h e c h a l l e n g e s S M B s f a c e i n t e c h n o l -

o g y a d o p t i o n ?

The ch allenge most SMBs face is access to sk ills–fo

instan ce,Gartn er says that Asia-Pacific mid-sized bus

nesses are s lower to adopt server vir tua l isat ion tech

nologies compared to their European and North Amer

can counterparts , and i t c i tes t ra ining and skil ls as th

reason. This is a challenge that we,at Dell , look to ad

dress. We believe technology mu st be affordable,sim pl

to buy an d easy to use.With s implici ty designed withi

our offerings,we believe we can help Indian SMBs adop

technology easily.

Lastly, in the comin g years,h ow do you see the stor

age market developing for SMBs?

SMBs are steadily realising the power of technology iboosting their enterprise.Mor e and more businesses ar

using technology in inn ovative ways to enhan ce thei

competi t iveness .Technology is being seen m ore as an

enabler ra ther than as a cost. India is one of the grow

ing markets for s torage and Indian SMBs represent a

at tract ive opportunity for s torage hardware, softwar

and services vendors . ●

‘Data storage is no longer

a backroom IT issue’

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 17/19

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD August-October 201032 SMALL AND MEDIUM ENTERPRISE WORLD33

■MANISH DALAL

GLOBALISATION has changed the way

business is condu cted the world over.Its ef-

fect can be seen in how businesses, big and

small,comp ete with each other in the local

and global markets .Th e Internet has fu-

elled and enabled this chan ge by making access to infor-

mation and services easy and communication instant .

The web offers a wealth ofoppor tunities to businesses

irrespective of size. Over 81 mill ion Indians now h ave

access to the Internet and over 1.73 billion Intern et users

exist worldwide,making i t a r ich and

powerful media to create awareness of

your business . While creat ing aware-

ness is one of the key benefi ts ,an In-

ternet presence when used s tra tegi-

cal ly can help a business increaseinquir ies for its products an d services.

To be present on the web,an impor-

tant first step for a business is to select

and register a domain name.Selecting

the r ight domain name increases a

business’s visibility on the net.A .com

domain nam e is appropriate for busi-

nesses ofa ll sizes and it is one ofth e most widely used do-

main nam e extensions around the world.

While i t is key to pay at tention to the design of one’s

website, i t is perhaps more important to m ake the web-

site searchable.Her e are a few practical tips to help you

reach m ore potent ial customer s cost-effectively.

■ Promote your domain nam e on al l commu nicat ion

and m arketing collaterals:Put your web address on busi-

ness cards and al l your s ta t ionery to make customers

aware ofwh ere they can f ind you on the Internet .Notifyyour c ur r e nt c us tome r s of your ne w we bs i t e.Us e t he

phrase-vis it our website a t www.yourbusin ess .com on

your advert isements and pu blic ity materia ls .Use an e-

ma i l s i gna tur e of your we bs it e doma in na me on a l l

email correspondence.

■Use search engine optimisation:Search engine optimi-

sation,or SEO,is the process ofr esearching and selecting

keywords that your potentia l customers would u se to

f ind what you offer .By using SEO, businesses can help

improve their chances ofbeing found on the Internet .

■ List your compan y on local web directories: Web di-

rectories are websites on which compa nies can get their

nam es listed for free.

■Choose a simple domain n ame: Select a domain na me

with care ,one that direct ly refers to your l ine of busi-

ness.Registering multiple domain nam es increases your

chances ofbeing found on the Internet .

■ Use a business email address: Your bu siness email

address can serve as a powerful tool to dr ive traff ic to

your website.It serves as a constant re-

minder of who you are whenever you

send anyone an e-mail f rom your pro-

fessional email id.

■ Make regular updates: Consider

making frequent chan ges to the con-tent posted on your website (once a

quarter can be a good star t) and pro-

vide recent updates on information or

services re la ted to your l ine of busi-

ness to encourage vis i tors to come

back rep eatedly.

■ Build traffic by exchanging links:

Increasing your vis ibi l i ty in a crowded online mar ket

may be achieved by building partnerships to gain refer-

rals .Working with other websites to place l inks to your

website can bring in more traff ic to you.Doing so,m ay

also increase your page ranking with search engines.

■ Acquire on-line advertising space: Aim to be visible in

the places where people look for the services you pro-

vide.For example if you supply handicraf ts i t may be

useful to buy online bann er advertisements on appropri-

ate websites that will link to your website.The Internet is a great m edium to build vis ibi l i ty for

your busin ess.For a small business it could be a powerful

and cost-effective marketing tool. With a little strategic

planning,you can help boost your bu siness inquir ies .

Welcome to the In tern et World!

Th e author is vice-president-Apac,VeriSign

‘Internet is a great medium tobuild visibility for business’

Over 81 millionIndians now have

access to theInternet, makingit a powerful media

to createawareness of one s

business

T e c h s o l u t i o n s Customer satisfaction is

linked to relevant data■MAHESH KIRAN

MI CR O, s m al l a n d

medium enterprises

are categorised ac-

cording investments

ma de i n pl a nt a nd

ma c hine r y. The c ur r e nt i nve s t -

ment l imits ar e Rs 25 lakh for mi-

cro,Rs 5 crore for small an d Rs 10

crore for medium enterprises .If an

enterprise is engaged in providing

s e r vi ce s , t he i nve s tme nt l imi t i n

plant and machin ery is re laxed to

Rs 10 lakh, Rs 2 crore and Rs 5

crore,respectively.

SMEs currently contr ibutes to

around 8% to Indian GDP.This ra-t io is projected to touch 10% in th e

near future .

Every SME is aware th at ‘ to suc-

c e ed i n a n e nvi r onme nt of e ve r -

growing competi t ion coupled with severe margin pres-

sure’i t has to fol low the dictum,cu stomer comes f irs t .

And an SME shou ld ensure that the customer is a lways

happy doing business with i t . However,customer sat is-

fact ion is a product of r ight mana gement decis ions.To

arr ive at the r ight decisions, th e management must be

provided with updated relevant data from t ime to t ime

for analysis .

Let’s take some common issues--most SMEs are bat-

tling ‘cash flow.’SMEs operate with limi ted liquid capi-

ta l with the customer always wanting the materia l on

credit but the supplier is a lways demanding advance or

on-delivery payments for supplies .So i t’s cr i t ical thatSMEs plan and en sure materia ls are available just-in-

t ime, so no excess s tock is s tored blocking the capita l

and at the same t ime production does not suffer for

wa nt of r a w ma te r i a ls .Th i s r e qui r e s a c le a r unde r -

s t a nding of the or de r s i n h a nd, t he s t oc k pos i ti on a nd

the re-order level.

Another cr i t ical requirement is s ta tutory compli-

ance--- mult iple government depar tments r equire dat

on regular in tervals.Be it VAT / service tax / excise / in

come tax.

To manage these challenges,SMEs need to ensur

that t imely data is captured in the r ight format. Var

ous surveys show when computers are put in use,mo

SMEs begin by computeris ing their accounting data .

The curr ent IT adaptat ion level in SMEs is very e

couraging,with maximum penetrat ion in terms ofpe

sonal computers and laptops, followed by printer an

accounting applicat ions ( l ike Tally).IT adoption is e

pected to grow at a very rapi d pace in the next two-thre

years . Another revolution in SMEs is the adoption I nt e r ne t a s t he i r de fa ul t me a ns of c ommunic a t i o

This wil l s ignif icantly change the way SMEs carry ou

their business .Sti l l very negligible part of transaction

takes place online.This wil l a lso change over t ime.

The author w orks with Tally Solut ions.He can be

reached at [email protected]

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 18/19

August-October 2010SMALL AND MEDIUM ENTERPRISE WORLD 34

Optimum investment forstart-up enterprisesEvery business needs a threshold level of investment in talent

■ SANJAY ANANDARAM

IDON’T think we can afford him” is what I heard the

founder and CEO of a s tar t-up say last week.He was

referr ing to a potentia l head of engineering’s resume

that had been sent across by a fr iend.The profi le was

terr if ic and seemed l ike the s tar t-up could certa inly

benefi t enormously from having the individual on

board.The CEO,though,was very apprehensive that the

candidate would be unaffordable.Bein g cost conscious

and frugal was a pract iced way with this CEO and his

founding team.So,wh at is the CEO to do when he now

needs experienced an d specialised talent to help the or-

ganisat ion grow? While i t is extremely hard to f ind a

company th at collapsed because it cut too much cost toofast,it is also hard to find a company that starved itself to

anorexic success.

Every business needs a certa in threshold level of in-

vestment to f irs t es tablish i tself ( these could include

building technology,acquir ing facilities and infrastruc-

ture ,acquir ing customer,a certa in market presence and

so on) and then another inject ion ofinvestment to grow

and scale .The ini t ia l threshold level required by a com-

pa ny i s a f unc t i on of the ma r ke t , c ompe ti t i on a nd t he

quali ty of the ini t ia l team.To establish the in i t ia l value

proposit ion in th e market , th e company has to be care-

ful with i ts money and smart about how to deploy i t . I t

must be frugal and leverage i ts re la t ionships and r e-

sources to the maximum . As the company establishes

i ts value proposit ion, th e technology and infrastructure

need revamping to handle growth, addit ions have to be

made to the management team,in crease in marketingspends and so on.

I t is a t this s tage that the mindset of the CEO has to ad-

just to the changed circumstances of his /h er company.

“Do I continue with th e frugal approach and work my r e-

sources to the bone or do I spend money on aspects of my

business that affect growth?” “Do I spend money an d

make that business tr ip to meet customers and business

partners or do I s tay with email?”“Do I spend money on

hirin g the best or do I make do with the less than satisfac-

tory senior management?”“Do I spend money on a mar-

keting campaign or do I hope for ‘viral’messaging to

take place?”Investors do not invest in a company so th at

you can return th eir money unspent af ter two years .In-

vestors invest because they want to extract value out of

the company they’ve invested in. Value is created

through value-generat ing act ivi t ies .Value-generat ing

activities include first and foremost,pr ofitable sales and

an increasing number of such sales .Whatever is neces-

sary to achieve this end r esult must be invested in.

For example, invest ing in creat ing a top-notch sales

team but being smar t in their in centives is cer ta inly a

good idea.Being generous with s tock options coupledwith operat ional freedom and involvement in company

decision-making can h elp at tract a c lass of executives.

In some cases,top-class talent can be lured by th e vision of

creating (without interference) the next great company ;

The CEO’s passion,ab ility and vision t o get the best for

his company is put to test in such cases.

Sometimes, i t becomes imperat ive to pay the individ-

ua l h ighe r t ha n m a r ke t r a t e s. I n s uc h c a s es , t he r e a r e

trade-offs to be considered.What would be the in cremen-

tal gain to the company by having such individuals on

board? What would be the downside of not having heavy

hittin g talent on your side? What is gained as sales,mar-

ket presence,abil i ty to hire others , t ime and so on?

If the incremental gains are more than incremental

costs , then the decis ion must be taken in favour of in-

vest ing.Mistakes wil l happen but the decis ion-making

process must not change.Th ere are far more examples of companies, especially in India,th at have und er-invested

themselves to oblivion than th ere are of companies that

have splurged and collapsed.What do you think?

Sanjay An andaram is an advocate of entrepreneurship.

He’s involved with Nasscom,TiE, IIM-B and INS EAD

business school

I n d i p r e n e u r

8/8/2019 Sme Aug Oct2010

http://slidepdf.com/reader/full/sme-aug-oct2010 19/19

![Ruff Newsletter Oct2010[1]](https://static.fdocuments.in/doc/165x107/577d35991a28ab3a6b90e32e/ruff-newsletter-oct20101.jpg)