Smart Phone Industry Note

19

www.morganmarkets.com Global Equity Research 22 April 2012 Smartphone industry Qualcomm 28nm shortage - Largest Smartphone Supply Hiccup Yet Asian Technology Alvin Kwock AC (852) 2800-8533 [email protected] J.P. Morgan Securities (Asia Pacific) Limited Rick Hsu AC (886-2) 2725-9874 [email protected] J.P. Morgan Securities (Taiwan) Limited. Rod Hall, CFA AC (1-415) 315-6713 [email protected] J.P. Morgan Securities LLC JJ Park AC (822) 758-5717 [email protected] J.P. Morgan Securities (Far East) Ltd, Seoul Branch Yoshiharu Izumi AC (81-3) 6736-8637 [email protected] JPMorgan Securities Japan Co., Ltd. Mark Moskowitz AC (1-415) 315-6704 [email protected] J.P. Morgan Securities LLC Gokul Hariharan AC (852) 2800-8564 [email protected] J.P. Morgan Securities (Asia Pacific) Limited Masashi Itaya AC (81-3) 6736 8633 [email protected] JPMorgan Securities Japan Co., Ltd. Ashish Gupta (91-22) 6157-3284 [email protected] J.P. Morgan India Private Limited Ashwin Kesireddy (1-415) 315-6756 [email protected] J.P. Morgan Securities LLC See page 16 for analyst certification and important disclosures, including non-US analyst disclosures. J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. This note is collaboration among JPM global analysts covering Foundry/ Handset brands & chipsets. Our demand/ supply model suggests shortages are likely to persist at least through Q3 with the worst shortage materializing in Q3– supply will increase sharply by 4Q but demand supply balance at that point will depend on the ramp in iPhone5 volume which could be substantial. We believe QCOM may prioritize for modem-only customers (Apple, Samsung) to maximize unit output and keep larger customers happy which can be bad news for brands without in-house AP who are more reliant on QCOM’s 8960 Snapdragon chip (HTC, LG, Sony, Moto, Pantech, etc). We think QCOM and TSMC are in a very good position in terms of pricing power and we expect unit volume upside in Q4. We also believe the shortage in LTE capable chips may boost demand for Renesas LTE chips in Q4. The bottom line is that severe capacity shortages in Q3, just when supply is needed for holiday manufacturing, may have material impact on overall smartphone supply in H2, in our view. QCOM a victim of its own success: QCOM’s first-ever integrated LTE/ 3G chipsets on 28nm has won ~150 designs (so S4 chips) across many major smartphone brands. We believe this is due to 1) lower power consumption due to higher levels of integration; 2) smaller overall footprint allowing slimmer designs, 3) ability to use the same chip across all major regions/ operators due to multi-standard baseband (lowers R&D cost). Our proprietary analysis suggests that supply shortages will peak in CQ3 and likely cap smartphone production – particularly for smaller vendors. Root cause: Yield, capacity or design flaw? We believe the cause of the trouble is a combination of these issues: 1) 28nm yield at TSMC is lower than other nodes due to initial ramp, but is ramping faster than 40nm on a comparable timeframe; 2) Qualcomm, due to unexpectedly strong demand for the 8960, may have overpromised what could be supplied for 3G parts; 3) we believe the integrated 3G/ LTE/ AP (8960) has poorer yields than the high end modem (9x15), so it is possible that design flaws are also to blame. Second quarter shortage or longer: Depends on iPhone: We estimate 62mn handsets demanding Qualcomm 28nm parts in 2Q/3Q, vs. supply at 40mn. This assumes QCOM prioritizes its 9x15 (modem-only), then 8x60, then 8x30 (integrated AP/ modem for latter 2). We expect supply to increase sharply in 4Q as TSMC adds 28nm capacity ahead of plan. Yet, the iPhone 5’s autumn launch is the big swing factor here – its LTE version will likely use the 9x15, and if the 3G market version also uses the same 28nm parts, then supply is likely to be very tight even into early 2013. Switch chipset? More plausible for 3G than LTE: We believe that several brands will diversify chip supply to address the shortage though for LTE devices we think this is more difficult. As an example, Samsung may use a 2- chip solution on 45nm parts in some LTE models, and HTC is switching chipsets for its One S product (3G model) due to low 8260a supply. LTE supply swaps are more difficult due to higher power consumption on older chips and larger footprint. A swap down to a 3G chipset is possible but would tend to create design delays at this stage given H2 is not far away.

Transcript of Smart Phone Industry Note

www.morganmarkets.com

Global Equity Research22 April 2012

Smartphone industryQualcomm 28nm shortage - Largest Smartphone Supply Hiccup Yet

Asian Technology

Alvin Kwock AC

(852) 2800-8533

J.P. Morgan Securities (Asia Pacific) Limited

Rick Hsu AC

(886-2) 2725-9874

J.P. Morgan Securities (Taiwan) Limited.

Rod Hall, CFA AC

(1-415) 315-6713

J.P. Morgan Securities LLC

JJ Park AC

(822) 758-5717

J.P. Morgan Securities (Far East) Ltd, Seoul Branch

Yoshiharu Izumi AC

(81-3) 6736-8637

JPMorgan Securities Japan Co., Ltd.

Mark Moskowitz AC

(1-415) 315-6704

J.P. Morgan Securities LLC

Gokul Hariharan AC

(852) 2800-8564

J.P. Morgan Securities (Asia Pacific) Limited

Masashi Itaya AC

(81-3) 6736 8633

JPMorgan Securities Japan Co., Ltd.

Ashish Gupta

(91-22) 6157-3284

J.P. Morgan India Private Limited

Ashwin Kesireddy

(1-415) 315-6756

J.P. Morgan Securities LLC

See page 16 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

This note is collaboration among JPM global analysts covering Foundry/ Handset brands & chipsets. Our demand/ supply model suggests shortages are likely to persist at least through Q3 with the worst shortage materializing in Q3– supply will increase sharply by 4Q but demand supply balance at that point will depend on the ramp in iPhone5 volume which could be substantial. We believe QCOM may prioritize for modem-only customers (Apple, Samsung) to maximize unit output and keep larger customers happy which can be bad news for brands without in-house AP who are more reliant on QCOM’s 8960 Snapdragon chip (HTC, LG, Sony, Moto, Pantech, etc). We think QCOM and TSMC are in a very good position in terms of pricing power and we expect unit volume upside in Q4. We also believe the shortage in LTE capable chips may boost demand for Renesas LTE chips in Q4. The bottom line is that severe capacity shortages in Q3, just when supply is needed for holiday manufacturing, may have material impact on overall smartphone supply in H2, in our view.

QCOM a victim of its own success: QCOM’s first-ever integrated LTE/ 3G chipsets on 28nm has won ~150 designs (so S4 chips) across many major smartphone brands. We believe this is due to 1) lower power consumption due to higher levels of integration; 2) smaller overall footprint allowing slimmer designs, 3) ability to use the same chip across all major regions/ operators due to multi-standard baseband (lowers R&D cost). Our proprietary analysis suggests that supply shortages will peak in CQ3 and likely cap smartphone production – particularly for smaller vendors.

Root cause: Yield, capacity or design flaw? We believe the cause of the trouble is a combination of these issues: 1) 28nm yield at TSMC is lower than other nodes due to initial ramp, but is ramping faster than 40nm on a comparable timeframe; 2) Qualcomm, due to unexpectedly strong demand for the 8960, may have overpromised what could be supplied for 3G parts; 3) we believe the integrated 3G/ LTE/ AP (8960) has poorer yields than the high end modem (9x15), so it is possible that design flaws are also to blame.

Second quarter shortage or longer: Depends on iPhone: We estimate 62mn handsets demanding Qualcomm 28nm parts in 2Q/3Q, vs. supply at 40mn. This assumes QCOM prioritizes its 9x15 (modem-only), then 8x60, then 8x30 (integrated AP/ modem for latter 2). We expect supply to increase sharply in 4Q as TSMC adds 28nm capacity ahead of plan. Yet, the iPhone 5’s autumn launch is the big swing factor here – its LTE version will likely use the 9x15, and if the 3G market version also uses the same 28nm parts, then supply is likely to be very tight even into early 2013.

Switch chipset? More plausible for 3G than LTE: We believe that several brands will diversify chip supply to address the shortage though for LTE devices we think this is more difficult. As an example, Samsung may use a 2-chip solution on 45nm parts in some LTE models, and HTC is switching chipsets for its One S product (3G model) due to low 8260a supply. LTE supply swaps are more difficult due to higher power consumption on older chips and larger footprint. A swap down to a 3G chipset is possible but would tend to create design delays at this stage given H2 is not far away.

2

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

Table of ContentsAnalysis of 28nm Shortfall ......................................................3

28nm Supply...........................................................................................................4

28nm Demand.........................................................................................................5

Bringing it all together ............................................................................................6

Root cause – 28nm yield, capacity or design? ......................7

Production yield ......................................................................................................8

Insufficient capacity ................................................................................................8

Circuitry design.......................................................................................................9

Switch chipset? More difficult for LTE ...................................9

28nm demand by smartphone brands .......................................................................9

LTE: Board space & power consumption limitations..............................................10

3G: Possible but take time to re-design ..................................................................11

Impact triggering down the value chain ...............................11

TSMC...................................................................................................................11

Apple supply chain................................................................................................12

Samsung Electronics .............................................................................................12

HTC......................................................................................................................13

LG Electronics ......................................................................................................13

Renesas Mobile (100% subsidiary of Renesas electronics) .....................................13

QCOM S4/ 28nm Product Roadmap......................................14

3

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

Analysis of 28nm Shortfall

We believe there will be a shortage of around 17m chips in CQ3 as a result of demand exceeding 28nm capacity at TSMC. The absolute unit shortfall depends largely on which chips Qualcomm chooses to produce since smaller die chips like the 9x15 modem can be produced in larger quantities with the same fab capacity.

There are many variables going into our analysis so it is difficult to say for sure but we currently believe both Apple and Samsung will experience some 9x15 supply shortages in CQ2 and CQ3 with fairly material shortages possible in CQ3. Our model actually shows that QCOM could serve all projected 9x15 demand if other chips were put into severe shortage – something we doubt Qualcomm will do. As a result our base case assumes that both Apple and Samsung will get less supply than needed in CQ3 and then, depending on iPhone5 demand, CQ4 may be better.

We calculate that the 8960 and related chips will be in shortage to the tune of 10.8m chips in CQ2 and then 9.3m in CQ3 even if QCOM shortchanges Apple and Samsung somewhat. This creates serious problems for vendors like HTC and LG who we believe have used the 8960/8260a/8660 in several designs. For the 8630 and 8x27 we estimate a combined shortfall of 4.6m units in CQ3 and then a smaller 1.5m unit shortfall in CQ4. The fate of these two chips probably rests on how large the iPhone5 ramp turns out to be. If the iPhone5 volumes outpace current forecasts we believe both he 8630 and the 8x27 could be delayed until early 2013.

As TSMC brings the third 15P2 fab online in CQ4 (QCOM’s FQ1) we believe 28nm shortages rapidly abate. At this point we forecast a total shortfall in CQ4 of just 1.5m units and no shortfall for either the 9x15 or the 8960 family. The outcome in CQ4 and even CQ3 depends largely, in our opinion, on the speed of the ramp in the iPhone5. The product will likely see a major redesign along with the addition of LTE - the combination of these changes could spur a demand spike even more substantial than what was seen with the iPhone4S in 2011 and lead to further shortages.

Table 1: Demand vs. Supply for 28nm QCOM Chips

Units in millions

Q2'12E Q3'12E Q4'12E Q1'13E

Time shift supply for Chips- 8960/8260a/ 8660 8.3 7.1 8.9 12.2- 8930/ 8230a/ 8630/ 8227 0.0 0.0 1.9 5.5- 9x15 3.1 21.0 34.4 33.2

Estimated Demand by Chip- 8960/8260a/ 8660 11.55 17.92 18.23 12.23- 8930/ 8230a/ 8630/ 8227 0.81 2.80 6.56 7.06- 9x15 4.5 24.7 34.8 33.2

Difference- 8960/8260a/ 8660 (3.27) (10.80) (9.32) -- 8930/ 8230a/ 8630/ 8227 (0.81) (2.80) (4.61) (1.53)- 9x15 (1.42) (3.68) (0.32) (0.00)Total (5.50) (17.28) (14.26) (1.53)

Source: J.P. Morgan estimates.

Global Communication analysts:

Rod Hall/ Ashwin Kesireddy

Asia Tech Hardware analysts:

Alvin Kwock/ Ashish Gupta

Asia Foundry analyst: Rick Hsu

4

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

28nm Supply

We utilize input from Asian industry sources to estimate TSMC's wafer output capacity at 28nm. Although Qualcomm indicated that the problem is due to increaseddemand we don't believe that is completely the case. We see a slower ramp of 28nm production as the main problem in CQ2 but then excess demand becomes the problem as we move into CQ3 and CQ4.

In Table 2 below you can see our estimates for TSMC 28nm wafer output by fab. The imbalance between supply and demand only begins to clear as the third 15P2 fab comes online in late CQ3 to help alleviate shortages. As QCOM indicated on their earnings call that they expect to incur additional opex to spin this capacity up sooner than was originally planned.

Table 2: TSMC 28nm Capacity

units in '000s (300mm)

Q2'12E Q3'12E Q4'12E Q1'13EFab12P5 45 45 45 45Fab15P1 35 60 75 75Fab15P2 0 5 30 60Total 28nm capacity 80 110 150 180

Source: J.P. Morgan estimates.

After estimating wafer output capability things get more complicated. We first have to make an assumption about the proportion of TSMC 28nm capacity that will be allocated to Qualcomm. We believe the maximum allocation will be around 1/3 of total capacity so assume that for our calculations. Other major users of TSMC’s supply include AMD for its APUs (we believe as order shift from Global foundries) and new Radeon HD-7000 GPU series, Fujitsu for server CPUs, ALTR and XLNX for their FPGA and likely Renesas for its LTE chips.

We next estimate the die size for major groupings of chips and the resulting gross dies/wafer. For the 8960 family we are assuming about 600 gross dies/wafer. For the 9x15 multi standard LTE modem we assume 1,300 gross dies/wafer. Finally, we assume 800 gross dies/wafer for the 8930, 8230a, 8630 and the 8x27 as a group. One interesting takeaway from this is that, should QCOM decide to do so, they can produce over twice the 9x15s per wafer compared to larger parts like the Snapdragon 8960s.

To arrive at actual chip output numbers we also need to assume yields for each chip by quarter. Our estimates are again based on industry conversations we have had and a bigger picture assumption that higher levels of integration such as exist on the 8960 will lead to lower yields. Figure 1 below summarizes our yield assumptions for each chip type.

5

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

Figure 1: TSMC Yield Assumptions

Source: J.P. Morgan estimates.

The last step in estimating supply is to allocate capacity by chip type. However, since we believe this allocation decision will be based on demand for the various chips we move on to discuss our demand calculations and then, in the "Bringing it all together" section after our Demand discussion we describe how we believe Qualcomm will match capacity with demand.

28nm Demand

Based on our bottoms-up model, we estimate demand of 17m units for the 28nm chipsets in CQ2’12 for QCOM (FQ3). We believe demand will increase to ~45m in CQ3 and ~60m in CQ4’12 (FQ1’13). Our model utilizes ship-in estimates from individual handset company analyst’s for LTE/3G smartphones as well as our best guess regarding the proportion of chip types that will be used/needed. We adjust our analyst’s estimates for Qualcomm’s market share and timing effects.

Figure 2: QCOM 28nm DemandUnits in millions

Source: J.P. Morgan estimates.

We believe that demand will be initially skewed toward 8xxx series products and then will shift toward the 9x15 LTE modem as iPhone5 production ramps in CQ3. We outline our proportionate chip demand estimates in Figure 3 below.

85%90%

95%

Q1'12E Q2'12E Q3'12E Q4'12E Q1'13E

- 8960/8930 - 8x60A/8x25/8x27/8630 - 9x15

-

10.00

20.00

30.00

40.00

50.00

60.00

70.00

Q2'12E Q3'12E Q4'12E Q1'13E

Total 28nm Demand

6

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

Figure 3: QCOM's 28nm Demand Skew

Source: J.P. Morgan estimates.

Known handsets with 28nm QCOM chips

Qualcomm announced that there are now more than 370 announced Snapdragon-based devices and 400 more in design of which over 150 are S4 designs. We don’t know exactly what subset of these design wins are on 28nm though we do know that at least the 150 S4s are 28nm Snapdragon based handsets. In addition to this we believe that QCOM's 9x15 LTE modem is very attractive to designers due to its ability to handle multiple coding technologies and likely power efficiency gains from a higher level of integration. We also believe that the dual core 8960 with the same multi standard baseband capability that the 9x15 has is proving very popular with designers. In the table below, we show a list of announced smartphones based on Qualcomm’s 28nm chipsets. This is incomplete due to the fact that most of the devices based on the new 28nm chips have yet to be announced. We do note, however, a preponderance of HTC products on this initial list – consistent with the particular concerns HTC is believed to have with 8960 supply.

Table 3: Announced smartphone based on Qualcomm 28nm parts

OEM Model Expected Availability OS 28nm ComponentAsus PadFone Apr-12 ICS Qualcomm MSM8260AAsus Transformer Pad Infinity Q2'12 ICS Qualcomm MSM8960HTC One XL (for AT&T) Apr 12 ICS Qualcomm MSM8960HTC Evo One LTE (for Sprint) Jun 12 ICS Qualcomm MSM8960HTC One S Q2'12 ICS Qualcomm MSM8260APansonic Eluga Power NA ICS Qualcomm MSM8660ALG D1L NA ICS Qualcomm MSM8960ZTE V96 NA ICS Qualcomm MSM8660APantech Vega Racer II Apr-12 ICS Qualcomm MSM8960

Source: Company data and J.P Morgan

Bringing it all together

To match supply with demand we have made the simplifying assumption that Qualcomm will initially give preference to the 8960/8260A, 9x15 and then other 28nm chips in CQ2, in that order. This is somewhat complicated by checks which suggest that the 9x15 is in shortage at Samsung. In our supply/demand matching exercise below we have therefore prioritized as indicated but shifted some supply away from 9x15s assuming QCOM may be doing the same thing to keep major customers using the8960/8260a happy. Beginning in CQ3 we assume Qualcomm will prioritize 9x15 over other chips to accommodate demand related to the iPhone5

69%

39%31% 23%

5%

6%11%

13%

27%

54% 58% 63%

0%10%20%30%40%50%60%70%80%90%

100%

Q2'12E Q3'12E Q4'12E Q1'13E

8960/8260a/ 8660 8930/ 8230a/ 8630/ 8227 9x15

7

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

and new Samsung products. Table 4 details our estimates, shortfall by chip in each quarter and then total unit shortfall. Note that total unit shortfall depends on what type of chip Qualcomm decides to produce given the large variation in die size between the 9x15 and the integrated Snapdragon chips like the 8960.

Table 4: Demand vs. Supply for 28nm QCOM Chips

Units in millions

Q2'12E Q3'12E Q4'12E Q1'13ETime shift supply for Chips- 8960/8260a/ 8660 8.3 7.1 8.9 12.2- 8930/ 8230a/ 8630/ 8227 0.0 0.0 1.9 5.5- 9x15 3.1 21.0 34.4 33.2

Estimated Demand by Chip- 8960/8260a/ 8660 11.55 17.92 18.23 12.23- 8930/ 8230a/ 8630/ 8227 0.81 2.80 6.56 7.06- 9x15 4.5 24.7 34.8 33.2

Difference- 8960/8260a/ 8660 (3.27) (10.80) (9.32) -- 8930/ 8230a/ 8630/ 8227 (0.81) (2.80) (4.61) (1.53)- 9x15 (1.42) (3.68) (0.32) (0.00)Total (5.50) (17.28) (14.26) (1.53)

Source: J.P. Morgan estimates.

Our modeling assumes key timing delays from wafer start to finished product. These assumption are depicted graphically below. If you would like to tweak our supply/demand model yourself please request a copy by email.

Figure 4: Time Line of a Chip

Source: J.P. Morgan estimates.

Root cause – 28nm yield, capacity or design?

There are talks in the market about the severe LTE chipset supply shortage (likely well below 50% sufficiency) since this is the first smartphone chipset using the most cutting-edge 28nm as the foundry work. While some look to have blamed yields or insufficient capacity, others have blamed circuitry designs. Based on our conversations with supply-chain players, we believe the root cause is a combination of all. However, in our opinion, while yields are arguably normal and satisfactory during the ramp, we believe the shortage issue will likely ease in 4Q as TSMC looks to be adding 28nm capacity ahead of the original plan.

Asia Foundry analyst: Rick Hsu

8

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

Production yield

Though yield satisfaction is somewhat subjective during initial ramps of a new technology node, we believe the 28nm yield ramps at TSMC, which only have proceeded for two quarters in terms of commercialization, are comparable to 65nm-and-above nodes (if not better) and faster than 40nm which faced difficulties during initial ramp due to a so-called "chamber mismatch" issue. Illustrated by a Figure below, if we use 20% of revenue contribution as a threshold, it took an average of 7 quarters for the previous nodes (except 40nm) and 9 quarters for 40nm. This time, we expect TSMC to take 7-8 quarters for 28nm to reach the 20% level. The ramp looks to be on track to meet our target of 5% revenue contribution in 1Q, 9% in 2Q and over 15% by end-2012, on our observation.

Figure 5: TSMC's tech ramp (as % of revenue)

xx

Source: Company, J.P. Morgan estimates.

As we discussed in our TSMC note, 28nm production ceased? Not really we say (8 March), TSMC’s overall production yields for its 28nm were 50-60%, which we believe is rising to 55-65% currently suggesting a steady improvement to its optimal range of 80%+ to 90%+ level in 4Q. This, together with the revenue contribution comparison aforementioned, further supports our view that TSMC’s 28nm yield ramp is faster than 40nm during the same comparable timeframe. Thus we can hardly fault TSMC on yield, in our opinion.

Insufficient capacity

We’ve been flagging the issue of likely insufficient capacity build for 28nm in the foundry space as TSMC appears to be the only pure foundry operating but the demand is broad based (not only from handset baseband and AP from the likes of QCOM, but from other applications such as graphics, CPU and FPGA). Spending has been cautious due to the macro overhang, resulting in capacity constraint, and this comes further with Qualcomm being aggressive in pushing 3G chips at 28nm,combined with strong demand for these chips that QCOM may have over-promised, thus causing the chip shortage, in our opinion. TSMC’s 28nm has been over-booked as per our observation.

0%

10%

20%

30%

40%

50%

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

E

3Q12

E

1Q13

E

3Q13

E

130nm 90nm 65nm 40nm 28nm

We can hardly fault TSMC on

yields, as we see the ramp as

normal and satisfactory

28nnm capacity is overbooked

9

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

Figure 6: TSMC's 28nm capacity ramp (input base)

'000 wpm/300mm

Source: J.P. Morgan estimates.

But we believe TSMC will soon announce to raise capex with focus on building more 28nm capacity, as on our observation, TSMC is pulling in machine installation for its Fab15P1 ahead of schedule and meanwhile initiating Fab15P2 right after Fab15P1 installation completes. This may lift its 28nm capacity to around 30-35k wpm (wafers per month, 300mm) by June and 50-55k wpm by end-2012, about 35-40% higher than its original plan on annual installation base. Therefore, we believe the shortage issue will be eased in 4Q. Note: Fab15P1, Fab15P2 and Fab12P5 are TSMC's focus fabs for 28nm expansion.

Circuitry design

LTE appears to be a milestone in circuitry designs for handset baseband chip application, and integration of LTE with 3G/AP further complicates the design flows, in our opinion, which could create challenges to chip designers. We get feedback from the supply chain that the integrated 3G/LTE/AP chip (8960) has poorer yields than the 3G parts (8260a) or 3G/LTE modem (9x15), thus we do not rule out some design issues associated with silicon integration, which goes beyond TSMC’s controls, to be fair.

Switch chipset? More difficult for LTE

28nm demand by smartphone brands

Based on our demand model, we note that Samsung and Apple are the largest vendors for 9x15 chip, which we anticipate to have only minor supply issues given Qualcomm may prioritize supply here.

For Snapdragon, HTC has the largest exposure, followed by LG. Based on our calculation, 8960/8930 will remain in shortage supply even in 1Q13, unless Apple decides to use chipsets other than 9x15 for the 3G models, which may not necessarily be Apple’s style who used to embrace global model approach. Our calculations in the model are based on an assumption that all iPhone 5 would be using 9x15.

0

20

40

60

80

100

120

140

160

1Q11 2Q11 3Q11 4Q11 1Q12E 2Q12E 3Q12E 4Q12E 1Q13E 2Q13E 3Q13E 4Q13E

New Original

LTE design is a milestone that

could create challenges

10

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

Table 5: 28nm demand model

2Q12 3Q12 4Q12 1Q139x15 DemandApple 3.60 23.68 33.71 32.25 Samsung 0.89 1.04 1.05 0.99 Total 9x15 Demand 4.49 24.72 34.76 33.24

8960/8930 DemandHTC 2.75 4.33 5.69 4.26 LG 0.50 1.17 1.65 1.11 Pantech 0.79 1.04 1.21 1.01 Others 0.20 0.20 0.20 0.20 Total 8960/8930 Demand 4.25 6.74 8.75 6.58 Of which 8930 0% 0% 20% 30%8930 Demand - - 1.75 1.97 8960 Demand 4.25 6.74 7.00 4.61

8x60A/8x25/8x27/8630Samsung 2.66 5.66 7.48 5.26 HTC 4.71 5.51 5.30 5.18 LG 0.46 1.06 1.50 1.01 Others 0.29 1.74 1.76 1.26 Total 8x60A/8x25/8x27/8630 Demand 8.12 13.98 16.03 12.71 % of 8260A/8660 90% 80% 70% 60%8260A/8660 7.30 11.18 11.22 7.63 Others 3G 28nm 0.81 2.80 4.81 5.08

Total 28nm Demand 16.85 45.44 59.55 52.53

Vendor SummaryApple (9x15) 3.60 23.68 33.71 32.25 Samsung (9x15) 0.89 1.04 1.05 0.99 Samsung (8x60A/8x25/8x27/8630) 2.7 5.7 7.5 5.3 HTC (8960/8930) 2.75 4.33 5.69 4.26 HTC (8x60A/8x25/8x27/8630) 4.7 5.5 5.3 5.2 LG (8960/8930) 0.50 1.17 1.65 1.11 LG (8x60A/8x25/8x27/8630) 0.5 1.1 1.5 1.0 Pantech (8960/8930) 0.79 1.04 1.21 1.01 Others (8960/8930) 0.20 0.20 0.20 0.20 Others (8x60A/8x25/8x27/8630) 0.3 1.7 1.8 1.3 Total 28nm Demand 16.85 45.44 59.55 52.53

Source: J.P. Morgan estimates.

LTE: Board space & power consumption limitations

For LTE phones using dual baseband/ RF structure, they would require higher power consumption and thus larger form factor and usually shorter battery life. This is clearly demonstrated in the case between Galaxy S II LTE & 3G versions, as the specifications are mostly identical other than a slightly bigger display.

We believe integrated chipsets like MSM8960 have better power performance over discrete chips. Using integrated chips will reduce the power consumption between handoffs when compared to using discrete chips, in our opinion. Also, Qualcomm claims that using its integrated solution will eliminate the need for additional multimedia processor and memory sub-systems. We believe lowering number of components will also help batter life of the device. Plus, the power leakage is lower on 28nm. HTC One XL using MSM8960 is a clear demonstration – there is no compromise in form factor and battery life any more.

Asia Tech Hardware analyst:

Alvin Kwock/ Ashish Gupta

11

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

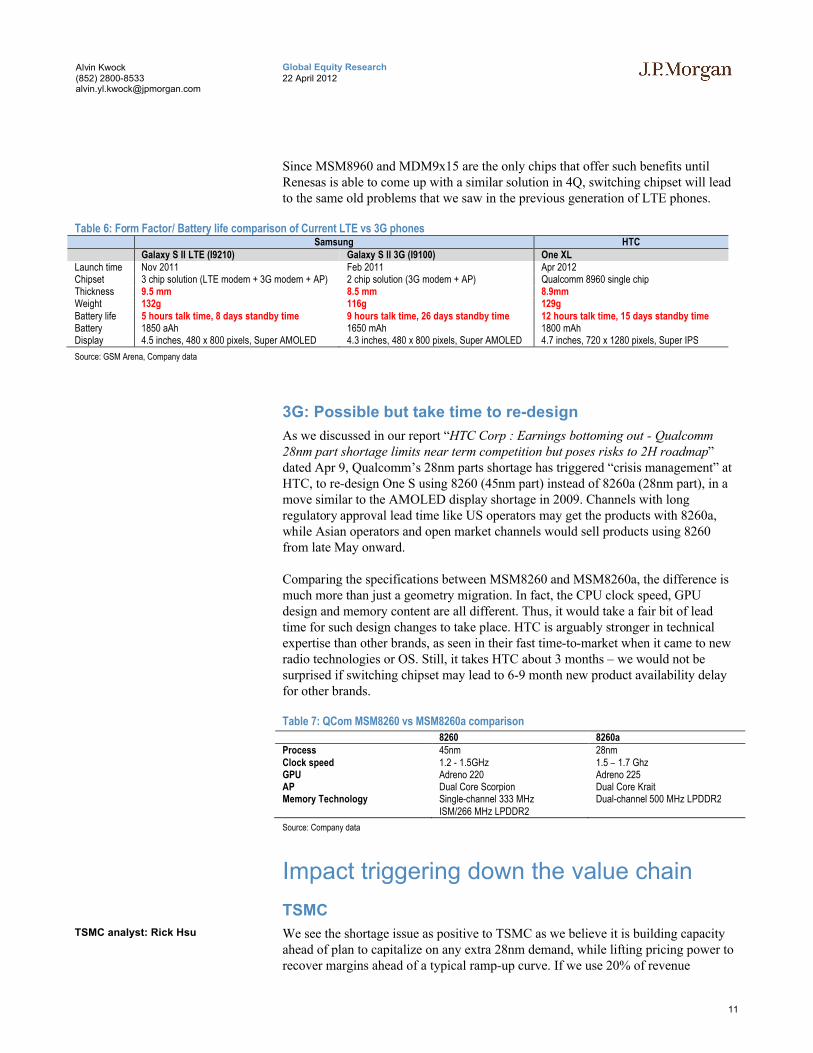

Since MSM8960 and MDM9x15 are the only chips that offer such benefits until Renesas is able to come up with a similar solution in 4Q, switching chipset will lead to the same old problems that we saw in the previous generation of LTE phones.

Table 6: Form Factor/ Battery life comparison of Current LTE vs 3G phonesSamsung HTC

Galaxy S II LTE (I9210) Galaxy S II 3G (I9100) One XLLaunch time Nov 2011 Feb 2011 Apr 2012Chipset 3 chip solution (LTE modem + 3G modem + AP) 2 chip solution (3G modem + AP) Qualcomm 8960 single chipThickness 9.5 mm 8.5 mm 8.9mmWeight 132g 116g 129gBattery life 5 hours talk time, 8 days standby time 9 hours talk time, 26 days standby time 12 hours talk time, 15 days standby timeBattery 1850 aAh 1650 mAh 1800 mAhDisplay 4.5 inches, 480 x 800 pixels, Super AMOLED 4.3 inches, 480 x 800 pixels, Super AMOLED 4.7 inches, 720 x 1280 pixels, Super IPS

Source: GSM Arena, Company data

3G: Possible but take time to re-design

As we discussed in our report “HTC Corp : Earnings bottoming out - Qualcomm 28nm part shortage limits near term competition but poses risks to 2H roadmap” dated Apr 9, Qualcomm’s 28nm parts shortage has triggered “crisis management” at HTC, to re-design One S using 8260 (45nm part) instead of 8260a (28nm part), in a move similar to the AMOLED display shortage in 2009. Channels with long regulatory approval lead time like US operators may get the products with 8260a, while Asian operators and open market channels would sell products using 8260 from late May onward.

Comparing the specifications between MSM8260 and MSM8260a, the difference is much more than just a geometry migration. In fact, the CPU clock speed, GPU design and memory content are all different. Thus, it would take a fair bit of lead time for such design changes to take place. HTC is arguably stronger in technical expertise than other brands, as seen in their fast time-to-market when it came to new radio technologies or OS. Still, it takes HTC about 3 months – we would not be surprised if switching chipset may lead to 6-9 month new product availability delay for other brands.

Table 7: QCom MSM8260 vs MSM8260a comparison

8260 8260aProcess 45nm 28nmClock speed 1.2 - 1.5GHz 1.5 – 1.7 GhzGPU Adreno 220 Adreno 225AP Dual Core Scorpion Dual Core KraitMemory Technology Single-channel 333 MHz

ISM/266 MHz LPDDR2Dual-channel 500 MHz LPDDR2

Source: Company data

Impact triggering down the value chain

TSMC

We see the shortage issue as positive to TSMC as we believe it is building capacity ahead of plan to capitalize on any extra 28nm demand, while lifting pricing power to recover margins ahead of a typical ramp-up curve. If we use 20% of revenue

TSMC analyst: Rick Hsu

12

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

contribution as a threshold, it took TSMC an average of 7 quarters for the previous nodes (except 40nm) and 9 quarters for 40nm. This time, we expect TSMC to take 7-8 quarters for 28nm to reach the 20% level. The ramp looks to be on track to meet our target of 5% revenue contribution in 1Q, 9% in 2Q and over 15% by end-2012, on our observation. We see potential upside surprise on margins to catalyze the stock further.

Apple supply chain

As related to the current 28nm supply constraints, we are not too concerned about any deep or lasting impact on Apple’s smartphone business. Despite our sanguine view, in coming months, we look to leverage the insights of our J.P. Morgan global technology research colleagues, focusing on 28nm capacity and yield improvements. At this point, we are not changing our estimates for Apple’s iPhone unit shipments for C2012 or C2013 due to the 28nm constraints.

In our view, Apple’s stature and influence over the tech supply chain should mitigate any lingering effects of the 28nm supply constraints on its business. For Apple, we think downside risks are limited. We do not expect the company to launch its next smartphone (i.e., iPhone 5) until C3Q 12. By then, there stands to be more clarity on the improvements in 28nm supply, in our view. In any case, we would expect Apple to negotiate supply agreements ahead of any pending product ramp. As for the iPhone 5 launch, we expect the device to be 4G LTE-capable, thinner, and offer good battery life, which should help Apple capture market share from the early 4G LTE entrants, in our view.

As for the adoption rate of 4G LTE-capable iPhones, we estimate that the devices could represent close to 30% of iPhone shipments in C2013. To put this into perspective, our total C2013 iPhone estimate is 156 million units, and we estimate that approximately 44 million units will be 4G LTE-capable. In geographic regions where 4G LTE is not available, we think that Apple has the option to source other baseband modem components not impacted by the 28nm constraints.

Currently, the U.S. carrier networks seem to be advancing faster than international peers in deploying 4G LTE. Indeed, we think that China wireless carriers are a year or two behind the curve, but that is ok. The slower ramp in China provides a long-term runway of growth for Apple and other smartphone vendors. As for the U.S., we point out that Apple has increasing share at the three major U.S. carriers deploying 4G LTE (AT&T, Verizon, and Sprint), putting Apple in the pole position with the iPhone 5 launch later this year.

Samsung Electronics

As SEC is using its own in-house Application Processor (AP, Exynos) for flagship smartphones (Galaxy S series) with either Qualcomm’s 9x15 or two chip solution from other model chip makers (i.e. STE), the impact would be marginal in our view. We estimate about 18M units of SEC smartphones (approx. 10% of annual shipment) to adopt Qualcomm chips. Additionally, we don’t expect SEC to incrementally benefit from prevalent shortage from 28nm capacity at TSMC, given it is yet to commercialize 28nm node production.

Apple analyst: Mark Moskowitz

Samsung analyst: JJ Park

13

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

HTC

Even though HTC may be able to switch chipset faster than the other brands thanks to its stronger technical expertise, it is still one of the most impacted brands in this 28nm part shortage, as its products are more geared towards high-end, and its dependency on Qualcomm is higher than most other brands.

There are 2 fold impact for HTC: 1) HTC is likely to get priority supply for 8960 given they are the largest chipset customer for Qualcomm in revenue terms, yet the 2H roadmap would likely be delayed if 8930 gets postponed; 2) For 3G models, HTC is re-designing One S using 8260 (45nm part) instead of 8260a (28nm part) –Channels with long regulatory approval lead time like US operators may get the products with 8260a, while Asian operators and open market channels would sell products using 8260 from late May onward.

While strong One X demand may offset some of the shipment impact and bring up total ASP, overall we still expect almost 2mn shortfall in 2Q12 due to the 28nm shortage. The impact in 2H could be even more profound based on our proprietary analysis of demand/ supply situation.

LG Electronics

LGE has also diversified its AP chips into other companies. We estimate +6M units of LGE's 3G & LTE smartphones to adopt Qualcomm 28nm chips and expect supply shortage to impact its LTE phones in short-term. LGE is currently in talk with several other chip makers to diversify its supply and plan to increase independency from Qualcomm. Of note, LGE announced to launch new LTE model (code name: D1L) in mid-May, which uses Qualcomm Snapdragon S4 series one-chip solution.

Renesas Mobile (100% subsidiary of Renesas electronics)

Currently, Only Qualcomm and Renesas can provide LTE modem (MP2531) commercially. And their modem is CAT 4 spec (150mbps ). Regarding LTE triple mode mobile phone platform (MP5232, Modem and AP combined 1 chip solution), they plan to ship from the end of 2012.CPU is ARM Coretex-A9 dual core and using 28nm process (TSMC).

HTC analyst: Alvin Kwock

LG analyst: JJ Park

Renesas analyst: Yoshiharu

Izumi

14

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

QCOM S4/ 28nm Product Roadmap

We think Qualcomm is already sampling or is planning to sample S4 based MSM8625, MSM8225, APQ8064, MSM8960, MSM8260A, MSM8660A and APQ8060A chipsets in H1’12. Of these chipsets, we expect smartphones based on only the 8960 to be available in H1’12 and rest of the chipsets could appear in smartphones in H2’12. Among the chipsets that are sampling or planned to sample in H1’12, the 8960 and 8260A support TD-SCDMA and HSPA standards, with the 8960 offering additional support for LTE TDD/FDD and EV-DO Rev. A/B. On the baseband front, Qualcomm said that it has moved LTE products on to 28nm technology. We believe that the MDM 9615 is largely sampling baseband product now.

Qualcomm’s roadmap reveals as many as seven additional S4 chips lined up for sampling in H2’12. Qualcomm said that 28nm will only be a relatively small part of their portfolio for 2Q, and expected that to account for 1/3 of its total chipset volume by end of its fiscal year.

Figure 7: QCOM Chip Roadmap

Source: Company. * - Expected

Type of

Processor

Addressable

Products

APTablets

8060 (S3)

8064 (S4)

8060A (S4)

8030 (S4)

MPQ TVs*8064 (S4)

Premium

Smartphones

8x50 (S1)

8x55 (S2)

8055 (S2)

8x60 (S3)

8960 (S4)

8660A(S4)

8260A(S4)

8625(S4)

8225(S4)

8960 Pro(S4)

First 28nm,

First integrated

3G/LTE (World

Mode) + AP,

First Integrated

quad combo

connectivity,

1.5-1.7GHz

Dual Krait,

Adreno 225

21 HSPA+/

1x Adv./1x

EV-DO

Rev. A/B,

1.5-

1.7GHz

Dual Krait

DC-

HSPA+/

TD-

SCDMA,

1.5-

1.7GHz

Dual Krait

HSPA/EDG

E/1x Rev.

A, 1xEV-

DO Rev.

A/B, 1GHz

Dual ARM

Cortex A5

HSPA/

EDGE,

1GHz

Dual

ARM

Cortex

A5

3G/LTE

(World

Mode) + AP,

Integrated

quad

combo, 1.5-

1.7GHz Dual

Krait,

Adreno 320

Mass Market

Smartphones

7x27 (S1)

7x25 (S1)

7x27A (S1)

7x25A (S1)

7x30 (S2)

8930 (S4)

8630 (S4)

8230 (S4)

8627(S4)

8227(S4)

8227(S4)

integrated

3G/LTE

(World

Mode),

1.2GHz Dual

Krait

21 HSPA+/

1x

Adv./DOr0/

A/B, SVDO-

DB,

1.2GHz

Dual Krait

DC-

HSPA+/T

D-

SCDMA,

1.2GHz

Dual Krait

21 HSPA+/

1x

Adv./DOr0/

A/B, SVDO-

DB, 1GHz

Dual Krait

DC-

HSPA+/TD-

SCDMA,

1GHz Dual

Krait

DC-

HSPA+/

TD-

SCDMA,

1GHz

Dual

Krait

QSCFeature

Phones

11x0 (1x)

60x5 (1x/DO

rA)

61x5 (DOrB/

1xAdv)

6295(HSPA+)

62xx(HSDP

A)

6xxx

MDM

Modems and

Data Cards

8200A (HSPA+)

6x00 (DOrB/

HSPA+

)

9200(LTE/D

C-

HSPA+)

8220(DC-

HSPA+)

9600(LTE/D

OrB/DC-

HSPA+

)

9x15(LTE/DOrB

/DC-

HSPA+/TD-

SCDMA in

Q2'12)

8215(DC-

HSPA+)

9x25LTE/DOrB/

DC-

HSPA+/TD-

SCDMA in

Q2'13)

8225 (DC-

HSPA+)

In-Production H2'12 and Beyond

MSM

H1'12

15

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

Figure 8: Qualcomm MSM8960 Chipset Architecture

Source: Company data

Figure 9: Qualcomm MSM8260a Chipset Architecture

Source: Company data

Figure 10: Qualcomm MDM9x15 Chipset Architecture

Source: Company data

LTE

TD-LTE FD-LTE

3G Backward Compatibility

WCDMA TDSCDMACDMA 2000

Dual Core Krait AP

1.5 – 1.7 GHz

1.5 – 1.7 GHz

GPU

Adreno 225

Connectivity

WiFi GPS

Bluetooth FM

LTE Disabled

TD-LTE FD-LTE

3G Backward Compatibility

WCDMA TDSCDMACDMA 2000

Dual Core Krait AP

1.5 – 1.7 GHz

1.5 – 1.7 GHz

GPU

Adreno 225

Connectivity

WiFi GPS

Bluetooth FM

16

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

Companies Recommended in This Report (all prices in this report as of market close on 20 April 2012)Apple Inc. (AAPL/$572.98/Overweight), HTC Corp (2498.TW/NT$462.00/Overweight), LG Electronics (066570.KS/W74400/Overweight), QUALCOMM (QCOM/$62.25/Overweight), Renesas Electronics (6723) (6723.T/¥480/Overweight), Samsung Electronics (005930.KS/W1282000/Overweight), TSMC (2330.TW/NT$84.30/Overweight)

Analyst Certification: The research analyst(s) denoted by an “AC” on the cover of this report certifies (or, where multiple research analysts are primarily responsible for this report, the research analyst denoted by an “AC” on the cover or within the document individually certifies, with respect to each security or issuer that the research analyst covers in this research) that: (1) all of the views expressed in this report accurately reflect his or her personal views about any and all of the subject securities or issuers; and (2) no part of any of the research analyst's compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analyst(s) in this report.

Important Disclosures

Market Maker: JPMS makes a market in the stock of QUALCOMM, Apple Inc..

Lead or Co-manager: J.P. Morgan acted as lead or co-manager in a public offering of equity and/or debt securities for Samsung Electronics within the past 12 months.

Client: J.P. Morgan currently has, or had within the past 12 months, the following company(ies) as clients: QUALCOMM, TSMC, LG Electronics, Samsung Electronics, Apple Inc., Renesas Electronics (6723).

Client/Investment Banking: J.P. Morgan currently has, or had within the past 12 months, the following company(ies) as investment banking clients: LG Electronics, Samsung Electronics.

Client/Non-Investment Banking, Securities-Related: J.P. Morgan currently has, or had within the past 12 months, the following company(ies) as clients, and the services provided were non-investment-banking, securities-related: QUALCOMM, TSMC, LG Electronics, Samsung Electronics, Apple Inc., Renesas Electronics (6723).

Client/Non-Securities-Related: J.P. Morgan currently has, or had within the past 12 months, the following company(ies) as clients, and the services provided were non-securities-related: QUALCOMM, TSMC, LG Electronics, Samsung Electronics.

Investment Banking (past 12 months): J.P. Morgan received in the past 12 months compensation for investment banking LG Electronics, Samsung Electronics.

Investment Banking (next 3 months): J.P. Morgan expects to receive, or intends to seek, compensation for investment banking services in the next three months from TSMC, LG Electronics, Samsung Electronics.

Non-Investment Banking Compensation: J.P. Morgan has received compensation in the past 12 months for products or services other than investment banking from QUALCOMM, TSMC, LG Electronics, Samsung Electronics, Apple Inc., Renesas Electronics (6723).

J.P. Morgan Securities (Far East) Ltd, Seoul branch is acting as a Market Maker (Liquidity Provider) for the Equity Linked Warrants of LG Electronics and owns 15,605,860 as of 20-Apr-12.

J.P. Morgan Securities (Far East) Ltd, Seoul branch is acting as a Market Maker (Liquidity Provider) for the Equity Linked Warrants of Samsung Electronics and owns 45,937,040 as of 20-Apr-12.

Analyst Position: The following analysts (and/or their associates or household members) own a long position in the shares of Apple Inc.: Richard Wright

Company-Specific Disclosures: Important disclosures, including price charts, are available for compendium reports and all J.P. Morgan–covered companies by visiting https://mm.jpmorgan.com/disclosures/company, calling 1-800-477-0406, or emailing [email protected] with your request.

Explanation of Equity Research Ratings and Analyst(s) Coverage Universe: J.P. Morgan uses the following rating system: Overweight [Over the next six to twelve months, we expect this stock will outperform the average total return of the stocks in the analyst's (or the analyst's team's) coverage universe.] Neutral [Over the next six to twelve months, we expect this stock will perform in line with the average total return of the stocks in the analyst's (or the analyst's team's) coverage universe.] Underweight [Over the next six to twelve months, we expect this stock will underperform the average total return of the stocks in the analyst's (or the analyst's team's) coverage universe.] In our Asia (ex-Australia) and UK small- and mid-cap equity research, each stock’s expected total return is compared to the expected total return of a benchmark country market index, not to those analysts’ coverage universe. If it does not appear in the Important Disclosures section of this report, the certifying analyst’s coverage universe can be found on J.P. Morgan’s research website, www.morganmarkets.com.

17

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

Coverage Universe: Kwock, Alvin YL: ASM Pacific (0522.HK), BYD (1211.HK), Erajaya Swasembada Tbk PT (ERAA.JK), Foxconn Int'l Holdings (2038.HK), HTC Corp (2498.TW), MediaTek Inc. (2454.TW), Synnex (2347.TW), TPV Technology (0903.HK), Wistron Corporation (3231.TW)

Hsu, Rick: ASE (2311.TW), Novatek Microelectronics Corp. (3034.TW), Powertech Technology Inc (6239.TW), Richtek Technology Corporation (6286.TW), SMIC (0981.HK), SPIL (2325.TW), TSMC (2330.TW), UMC (2303.TW), Vanguard International Semiconductor Corporation (5347.TWO)

Hall, Roderick B: Acme Packet (APKT), Ciena Corp. (CIEN), Cisco Systems (CSCO), Corning (GLW), F5 Networks (FFIV), Infinera (INFN), Juniper Networks (JNPR), Mitel Networks (MITL), Motorola Mobility (MMI), QUALCOMM (QCOM), Research in Motion (RIMM), Riverbed (RVBD), Tellabs (TLAB)

Park, JJ: LG Display (034220.KS), LG Electronics (066570.KS), SK Hynix (000660.KS), Samsung Electronics (005930.KS)

Moskowitz, Mark: Aeroflex (ARX), Apple Inc. (AAPL), Brocade (BRCD), Dell Inc. (DELL), EMC (EMC), Emulex Corp. (ELX), Fusion-io (FIO), Hewlett-Packard (HPQ), IBM (IBM), Lexmark International (LXK), NetApp (NTAP), Orbotech (ORBK), QLogic Corporation (QLGC), STEC (STEC), Seagate Technology (STX), Western Digital (WDC), Xerox Corporation (XRX)

Zhang, Qin: AsiaInfo-Linkage Inc. (ASIA), Digital China (0861.HK), Spreadtrum Communications (SPRD), ZTE Corp (0763.HK)

Hariharan, Gokul: ASUSTek Computer (2357.TW), Acer Inc (2353.TW), Catcher Technology (2474.TW), Compal Electronics, Inc. (2324.TW), Delta Electronics, Inc. (2308.TW), Foxconn Technology (2354.TW), Hon Hai Precision (2317.TW), Lenovo Group Limited(0992.HK), Lite-On Technology Corporation (2301.TW), Pegatron Corp (4938.TW), Quanta Computer Inc. (2382.TW)

Izumi, Yoshiharu: Fuji Electric (6504) (6504.T), Fujitsu (6702) (6702.T), Hitachi (6501) (6501.T), Mitsubishi Electric (6503) (6503.T), NEC (6701) (6701.T), Nissin Electric (6641) (6641.T), Oki Electric Industry (6703) (6703.T), Omron (6645) (6645.OS), Panasonic (6752) (6752.T), Renesas Electronics (6723) (6723.T), Sharp (6753) (6753.T), Sony (6758) (6758.T), Toshiba (6502) (6502.T)

J.P. Morgan Equity Research Ratings Distribution, as of April 3, 2012

Overweight(buy)

Neutral(hold)

Underweight(sell)

J.P. Morgan Global Equity Research Coverage 45% 43% 12%IB clients* 51% 45% 34%

JPMS Equity Research Coverage 43% 48% 9%IB clients* 70% 61% 53%

*Percentage of investment banking clients in each rating category.For purposes only of FINRA/NYSE ratings distribution rules, our Overweight rating falls into a buy rating category; our Neutral rating falls into a hold rating category; and our Underweight rating falls into a sell rating category.

Equity Valuation and Risks: For valuation methodology and risks associated with covered companies or price targets for covered companies, please see the most recent company-specific research report at http://www.morganmarkets.com , contact the primary analyst or your J.P. Morgan representative, or email [email protected].

Equity Analysts' Compensation: The equity research analysts responsible for the preparation of this report receive compensation based upon various factors, including the quality and accuracy of research, client feedback, competitive factors, and overall firm revenues, which include revenues from, among other business units, Institutional Equities and Investment Banking.

Registration of non-US Analysts: Unless otherwise noted, the non-US analysts listed on the front of this report are employees of non-US affiliates of JPMS, are not registered/qualified as research analysts under NASD/NYSE rules, may not be associated persons of JPMS, and may not be subject to FINRA Rule 2711 and NYSE Rule 472 restrictions on communications with covered companies, public appearances, and trading securities held by a research analyst account.

Other Disclosures

J.P. Morgan ("JPM") is the global brand name for J.P. Morgan Securities LLC ("JPMS") and its affiliates worldwide. J.P. Morgan Cazenove is a marketing name for the U.K. investment banking businesses and EMEA cash equities and equity research businesses of JPMorgan Chase & Co. and its subsidiaries.

Options related research: If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the Option Clearing Corporation's Characteristics and Risks of Standardized Options, please contact your J.P. Morgan Representative or visit the OCC's website at http://www.optionsclearing.com/publications/risks/riskstoc.pdf

Legal Entities Disclosures U.S.: JPMS is a member of NYSE, FINRA, SIPC and the NFA. JPMorgan Chase Bank, N.A. is a member of FDIC and is authorized and regulated in the UK by the Financial Services Authority. U.K.: J.P. Morgan Securities Ltd. (JPMSL) is a member of the London Stock Exchange and is authorized and regulated by the Financial Services Authority. Registered in England & Wales No. 2711006. Registered Office 125 London Wall, London EC2Y 5AJ.

18

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

South Africa: J.P. Morgan Equities Limited is a member of the Johannesburg Securities Exchange and is regulated by the FSB. Hong Kong: J.P. Morgan Securities (Asia Pacific) Limited (CE number AAJ321) is regulated by the Hong Kong Monetary Authority and the Securities and Futures Commission in Hong Kong. Korea: J.P. Morgan Securities (Far East) Ltd, Seoul Branch, is regulated by the Korea Financial Supervisory Service. Australia: J.P. Morgan Australia Limited (ABN 52 002 888 011/AFS Licence No: 238188) is regulated by ASIC and J.P. Morgan Securities Australia Limited (ABN 61 003 245 234/AFS Licence No: 238066) is a Market Participant with the ASX and regulated by ASIC. Taiwan: J.P.Morgan Securities (Taiwan) Limited is a participant of the Taiwan Stock Exchange (company-type) and regulated by the Taiwan Securities and Futures Bureau. India: J.P. Morgan India Private Limited, having its registered office at J.P. Morgan Tower, Off. C.S.T. Road, Kalina, Santacruz East, Mumbai - 400098, is a member of the National Stock Exchange of India Limited (SEBI Registration Number - INB 230675231/INF 230675231/INE 230675231) and Bombay Stock Exchange Limited (SEBI Registration Number - INB 010675237/INF 010675237) and is regulated by Securities and Exchange Board of India. Thailand: JPMorgan Securities (Thailand) Limited is a member of the Stock Exchange of Thailand and is regulated by the Ministry of Finance and the Securities and Exchange Commission. Indonesia: PT J.P. Morgan Securities Indonesia is a member of the Indonesia Stock Exchange and is regulated by the BAPEPAM LK. Philippines: J.P. Morgan Securities Philippines Inc. is a member of the Philippine Stock Exchange and is regulated by the Securities and Exchange Commission. Brazil: Banco J.P. Morgan S.A. is regulated by the Comissao de Valores Mobiliarios (CVM) and by the Central Bank of Brazil. Mexico: J.P. Morgan Casa de Bolsa, S.A. de C.V., J.P. Morgan Grupo Financiero is a member of the Mexican Stock Exchange and authorized to act as a broker dealer by the National Banking and Securities Exchange Commission. Singapore: This material is issued and distributed in Singapore by J.P. Morgan Securities Singapore Private Limited (JPMSS) [MICA (P) 088/04/2012 and Co. Reg. No.: 199405335R] which is a member of the Singapore Exchange Securities Trading Limited and is regulated by the Monetary Authority of Singapore (MAS) and/or JPMorgan Chase Bank, N.A., Singapore branch (JPMCB Singapore) which is regulated by the MAS. Malaysia: This material is issued and distributed in Malaysia by JPMorgan Securities (Malaysia) Sdn Bhd (18146-X) which is a Participating Organization of Bursa Malaysia Berhad and a holder of Capital Markets Services License issued by the Securities Commission in Malaysia. Pakistan: J. P. Morgan Pakistan Broking (Pvt.) Ltd is a member of the Karachi Stock Exchange and regulated by the Securities and Exchange Commission of Pakistan. Saudi Arabia: J.P. Morgan Saudi Arabia Ltd. is authorized by the Capital Market Authority of the Kingdom of Saudi Arabia (CMA) to carry out dealing as an agent, arranging, advising and custody, with respect to securities business under licence number 35-07079 and its registered address is at 8th Floor, Al-Faisaliyah Tower, King Fahad Road, P.O. Box 51907, Riyadh 11553, Kingdom of Saudi Arabia. Dubai: JPMorgan Chase Bank, N.A., Dubai Branch is regulated by the Dubai Financial Services Authority (DFSA) and its registered address is Dubai International Financial Centre - Building 3, Level 7, PO Box 506551, Dubai, UAE.

Country and Region Specific Disclosures U.K. and European Economic Area (EEA): Unless specified to the contrary, issued and approved for distribution in the U.K. and the EEA by JPMSL. Investment research issued by JPMSL has been prepared in accordance with JPMSL's policies for managing conflicts of interest arising as a result of publication and distribution of investment research. Many European regulators require a firm to establish, implement and maintain such a policy. This report has been issued in the U.K. only to persons of a kind described in Article 19 (5), 38, 47 and 49 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (all such persons being referred to as "relevant persons"). This document must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this document relates is only available to relevant persons and will be engaged in only with relevant persons. In other EEA countries, the report has been issued to persons regarded as professional investors (or equivalent) in their home jurisdiction. Australia: This material is issued and distributed by JPMSAL in Australia to "wholesale clients" only. JPMSAL does not issue or distribute this material to "retail clients". The recipient of this material must not distribute it to any third party or outside Australia without the prior written consent of JPMSAL. For the purposes of this paragraph the terms "wholesale client" and "retail client" have the meanings given to them in section 761G ofthe Corporations Act 2001. Germany: This material is distributed in Germany by J.P. Morgan Securities Ltd., Frankfurt Branch and J.P.Morgan Chase Bank, N.A., Frankfurt Branch which are regulated by the Bundesanstalt für Finanzdienstleistungsaufsicht. Hong Kong: The 1% ownership disclosure as of the previous month end satisfies the requirements under Paragraph 16.5(a) of the Hong Kong Code of Conduct for Persons Licensed by or Registered with the Securities and Futures Commission. (For research published within the first ten days of the month, the disclosure may be based on the month end data from two months prior.) J.P. Morgan Broking (Hong Kong) Limited is the liquidity provider/market maker for derivative warrants, callable bull bear contracts and stock options listed on the Stock Exchange of Hong Kong Limited. An updated list can be found on HKEx website: http://www.hkex.com.hk. Japan: There is a risk that a loss may occur due to a change in the price of the shares in the case of share trading, and that a loss may occur due to the exchange rate in the case of foreign share trading. In the case of share trading, JPMorgan Securities Japan Co., Ltd., will be receiving a brokerage fee and consumption tax (shouhizei) calculated by multiplying the executed price by the commission rate which was individually agreed between JPMorgan Securities Japan Co., Ltd., and the customer in advance. Financial Instruments Firms: JPMorgan Securities Japan Co., Ltd., Kanto Local Finance Bureau (kinsho) No. 82 Participating Association / Japan Securities Dealers Association, The Financial Futures Association of Japan, Type II Financial Instruments Firms Association and Japan Securities Investment Advisers Association. Korea: This report may have been edited or contributed to from time to time by affiliates of J.P. Morgan Securities (Far East) Ltd, Seoul Branch. Singapore: JPMSS and/or its affiliates may have a holding in any of the securities discussed in this report; for securities where the holding is 1% or greater, the specific holding is disclosed in the Important Disclosures section above. India: For private circulation only, not for sale. Pakistan: For private circulation only, not for sale. New Zealand: This material is issued and distributed by JPMSAL in New Zealand only to persons whose principal business is the investment of money or who, in the course of and for the purposes of their business, habitually invest money. JPMSAL does not issue or distribute this material to members of "the public" as determined in accordance with section 3 of the Securities Act 1978. The recipient of this material must not distribute it to any third party or outside New Zealand without the prior written consent of JPMSAL. Canada: The information contained herein is not, and under no circumstances is to be construed as, a prospectus, an advertisement, a public offering, an offer to sell securities described herein, or solicitation of an offer to buy securities described herein, in Canada or any province or territory thereof. Any offer or sale of the securities described herein in Canada will be made only under an exemption from the requirements to file a prospectus with the relevant Canadian securities regulators and only by a dealer properly registered under applicable securities laws or, alternatively, pursuant to an exemption from the dealer registration requirement in the relevant province or territory of Canada in which such offer or sale is made. The information contained herein is under no circumstances to be construed as investment advice in any province or territory of Canada and is not tailored to the needs of the recipient. To the extent that the information contained herein references securities of an issuer incorporated, formed or created under the laws of Canada or a province or territory of Canada, any trades in such securities must be conducted through a dealer registered in Canada. No securities commission or similar regulatory authority in Canada has reviewed or in any way passed judgment upon these materials, the information contained herein or the merits of the securities described herein, and any representation to the contrary is an offence. Dubai: This report has been issued to persons regarded as professional clients as defined under the DFSA rules.

19

Global Equity Research22 April 2012

Alvin Kwock(852) [email protected]

General: Additional information is available upon request. Information has been obtained from sources believed to be reliable but JPMorgan Chase & Co. or its affiliates and/or subsidiaries (collectively J.P. Morgan) do not warrant its completeness or accuracy except with respect to any disclosures relative to JPMS and/or its affiliates and the analyst's involvement with the issuer that is the subject of the research. All pricing is as of the close of market for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipient of this report must make its own independent decisions regarding any securities or financial instruments mentioned herein. JPMS distributes in the U.S. research published by non-U.S. affiliates and accepts responsibility for its contents. Periodic updates may be provided on companies/industries based on company specific developments or announcements, market conditions or any other publicly available information. Clients should contact analysts and execute transactions through a J.P. Morgan subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

"Other Disclosures" last revised April 18, 2012.

Copyright 2012 JPMorgan Chase & Co. All rights reserved. This report or any portion hereof may not be reprinted, sold or redistributed without the written consent of J.P. Morgan. #$J&098$#*P