Small fibers Big difference Annual Report 2004 · Big difference. 2004 Annual Report Ahlstrom...

90

Small fibers. Big difference. 2004 Annual Report Annual Report 2004 Ahlstrom Corporation

Transcript of Small fibers Big difference Annual Report 2004 · Big difference. 2004 Annual Report Ahlstrom...

Small fibers. Big difference.2004

Annual Report

Ahlstrom CorporationP.O. Box 329 Eteläesplanadi 14 FI-00101 Helsinki, Finland www.ahlstrom.com

An

nu

al R

ep

ort 2

00

4A

hlstro

m Co

rpo

ratio

n

1Ahlstrom Corporation

Business review

Ahlstrom & society

Financial statements

2 Ahlstrom in brief

3 Financials 2004

4 Vision & strategy

6 Success factors

10 Main events in 2004

12 President’s review

14 Financial review

22 Introduction to business review

24 FiberComposites segment

30 Specialty Papers segment

37 Summary of the Code of Business Conduct

38 Sustainability reporting within Ahlstrom

39 Sustainability management

42 Human Resources

46 Occupational health & safety

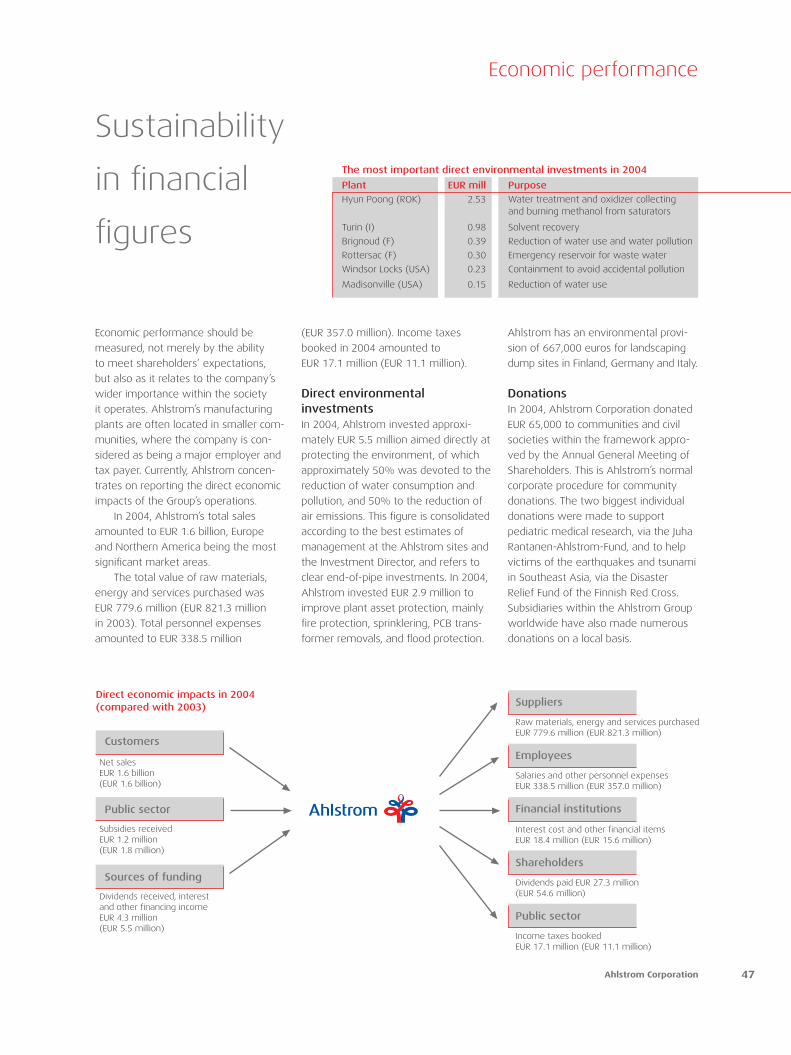

47 Economic performance

48 Environmental performance

52 Corporate governance

58 Report by the Board of Directors

62 Income statement

63 Statement of cash fl ows

64 Balance sheet

66 Notes to the fi nancial statements

78 Key fi gures

80 Shares and shareholders

81 Proposal for the distribution of profi ts

81 Auditor’s report

82 Board of Directors

84 Corporate Executive Team

86 Glossary

87 Locations & contact information

88 Financial information in 2005

Contents

2 Annual Report 2004

Nonwovens and specialty papers, made

by Ahlstrom, are used in a wide range

of everyday products, e.g. in fi lters,

wipes, fl ooring, labels, and tapes.

The company has a strong market

position in all its business areas, built

upon the company’s unique fi ber exper-

tise and innovative approach.

Ahlstrom in brief

Ahlstrom’s 5,800 employees serve

customers via sales offi ces and produc-

tion facilities in more than 20 countries

on fi ve continents.

In 2004, Ahlstrom’s net sales

amounted to EUR 1.6 billion. Half of the

net sales originates from products that

are market leaders in their respective

fi elds. Furthermore, approximately one

third of net sales comes from products

where the company is the second or

third largest market player.

Ahlstrom’s objective is for one-third

of the company’s annual growth to

come from new products.

Ahlstrom is the global leader in the development, manufacture

and marketing of high performance fi ber-based materials.

Segment FiberComposites Specialty Papers *

Net sales in 2004 EUR 664 million EUR 813 million

Share of Group’s net sales** 45% 55%

Employees 2,858 2,520

Key customer industries Filtration and automotive, Packaging & labeling industry, furniture &

consumer products, healthcare, building building, consumer products & food

Production units Belgium, Brazil, Finland, France, Italy, Finland, France, Germany, Italy

South Korea, Spain, Sweden, UK, USA

Business areas and Nonwovens Label & Packaging Papers

main applications Wipes Self-adhesive labels

Medical gowns and drapes Food packaging:

Wallcoverings coffee, dairy products, pet food

Teabags Labels for beverage bottles

Fibrous meat casings

Technical Papers

Filtration Furniture foils, abrasive paper,

Air, fuel and oil engine fi lters masking tape, engine gaskets, posters,

Industrial and laboratory fi ltration wallpaper, processing paper

Glass Nonwovens

Windmill blades, fl ooring, boat hulls

* This organizational structure has been effective as of January 1, 2005. The fi gures for the Specialty Papers segment have been calculated pro forma based on the former LabelPack and Specialties divisions. ** Excluding discontinued operations.

3Ahlstrom Corporation

Financials 2004

Key fi gures, EUR million 2004 2003

Net sales 1,567.8 1,556.4

Operating profi t 51.0 48.5

Profi t before extraordinary items and taxes 34.8 33.7

Net profi t 17.5 22.4

Balance sheet, total 1,399.8 1,425.5

Capital expenditure (incl. acquisitions) 167.0 93.1

Net cash fl ow from operations 128.0 202.0

Gearing ratio (%) 53.9 42.3

Return on capital employed (ROCE) (%) 5.3 4.6

Earnings per share (EUR) 0.48 0.61

• Ahlstrom completed its structural

change from multi-business company

to a focused fi ber-based materials

supplier

• Ahlstrom’s business environment

remained challenging and the

company was faced by weak demand

in Europe

• The Specialties division improved its

fi nancial performance signifi cantly

• Healthy operating cash fl ow

Year 2004 in brief

Financial targets

1. Profi tability:

– operating profi t (EBIT) of 10%

– return on capital employed (ROCE)

of 13%

2. Financial strength: gearing ratio of

50–80% (may temporarily be

exceeded for strategic acquisitions)

3. Growth: both organically and through

acquisitions in higher value-added

businesses. Organic growth should

exceed the market average.

4. Dividends: dividend averaging

30–40% of the net profi t

04

0 5 10

03

02

%15

Target level 13%

Return on capital employed(ROCE)

04

0 20

03

02

%100

Target level 50–80%

Gearing

40 60 80

04

0 5

03

02

Target level 10%

Operating profit (EBIT)

15 %10

4 Annual Report 2004

Ahlstrom manufactures high-quality

fi ber materials of synthetic and natural

fi bers. The company supplies these

materials to its customers as roll goods

for further processing. Converters,

such as printers or automotive industry

suppliers, deliver the products to a

marketer or seller serving consumers

or industrial customers worldwide.

Ahlstrom’s vision is

to be the global source

for fi ber-based materials

Ahlstrom in the value chain

• Natural fibers

(wood, cotton, hemp)

• Oil/petrochemicals

• Pulp producers

• Synthetic fiber

producers

(PET, PP)

• Chemical suppliers

Ahlstrom • Printers

(label, decor, poster,

wallcover...)

• Label metalizers

• Siliconizers

• Automotive industry

suppliers (filter, gasket)

• World class consumer

or industrial brands

Consumers

Industrialcustomers

Primaryproduction

Raw materialsupplier

Roll goodsproducer

Converter Marketer /seller

5Ahlstrom Corporation

Vision & strategy

Strategy based on

four cornerstones

Long-term customer relationships

We focus on customer needs and work

in partnership with customers to develop

new products and improved product

features. Innovations are essential to

our long-term success and competitive

position. Our customers are signifi cant

players in their industries and, as they

develop and expand their businesses,

Ahlstrom is ready to serve their fi ber

materials needs on a global basis.

Ahlstrom Expertise

Ahlstrom’s Expertise lies in our know-

ledge of fi bers and fi ber processing.

Our teams work with a large number

of customers and with numerous

applications, products and supporting

technologies. This wide scope gives

us a unique knowledge base, which

we combine with developed market

insight, to create and manufacture

competitive fi ber materials.

Expansion in high value-added

and growth segments

We aim to serve high value-added and high

growth fi ber materials segments. We seek

to expand our operations by organic growth

to increase production capabilities

at existing sites and by acquisitions.

Competitive operations

We continuously improve our operations to

strengthen our competitiveness as a supplier

and to meet our fi nancial targets. Key elements

in competitive operations include cost effi ciency,

increased productivity, as well as streamlined

operations and support functions.

6 Annual Report 2004

Unique fi ber expertiseAhlstrom’s business is high-quality fi ber-

based materials. Unlike most of its

competitors, Ahlstrom utilizes natural

fi bers, synthetic fi bers and various

combinations of these in its production,

whereas most manufacturers use either

natural or synthetic fi bers.

Many of Ahlstrom’s customer

relationships have lasted for decades.

Long-term cooperation is benefi cial to

both the company and its customers,

as new products and product features

are developed jointly.

Ahlstrom’s long-term

success is based on

long-lasting customer

relationships, unique

know-how of fi bers,

innovative products

and technologies, and

the continuous focus

on improving the

company’s performance.

Ensuring Ahlstrom’s

long-term success

Ahlstrom is a global company with

multi-cultural teams. They work in

close cooperation with customers, and

evaluate customer needs and market

development, understand market

trends, and adjust production

capabilities to meet the changes in

demand. Teams representing different

business operations also benefi t from

being able to utilize each other’s

competencies in, for example,

investments and innovation activities.

100% synthetic fibers100% natural fibers

Product value added

Integratedforestproducts

Polymers/textiles

Fiber based materials

Ahlstrom No. 1

• World leader in fiber based materials

• The broadest range of product offerings, utilizing fibers that vary from 100% synthetic to 100% natural, with multiplecombinations of both.

• Versatile production capability

7Ahlstrom Corporation

Innovations to benefi t customers

Success factors

Ahlstrom’s innovations are strongly

customer-driven, and the actual

development work is done in close

cooperation with customers. Innovative

products are essential to Ahlstrom’s

long-term success and competitiveness.

Ahlstrom aims to effi ciently develop

new, value-adding products, product

features, and technologies. The result

of this work has created entirely new

sales possibilities both for Ahlstrom and

its customers.

Highlights in 2004The long-running competition between

paper and fi lm as packaging material

started to turn gradually to paper’s

advantage. Thanks to the ambitious

R&D work done by Ahlstrom and

within the industry new, fi lm-like but

recyclable paper products have been

developed for food packaging and

other applications.

Development work with new tech-

nologies continued in 2004. For photo

catalysis Ahlstrom has pioneered a new

and interesting end-use application for

waste treatment in paper mills. This

patented solution eliminates the odor

from paper mill sludge and will create

new sales opportunities for Ahlstrom.

Several trials conducted with

Ahlstrom’s pilot coater resulted in new

products and product features to the

company’s range. Specialty coating is

a key focus area for Ahlstrom’s innova-

tion activities, because many customer

applications require excellent printing

qualities and smooth surface facilities

for roll goods.

R&D resources in 2004Ahlstrom’s global innovation function is

organized at three levels. The Ahlstrom

Research Corporate Center, ARCC, is

based in Pont-Evêque, France. There

are also seven R&D facilities, located in

Finland, France, Germany, Italy, and in

the United States. All Ahlstrom product

line teams around the world are

Several leading companies worldwide,

such as banks, insurance companies,

and telecommunication companies, use

Ahlstrom’s Cristal Evolution windows in

their envelopes. This technical paper is

constantly gaining new market share

against polystyrene fi lms, demon-

strating that the marketing and promo-

tion efforts Ahlstrom has undertaken

are paying back.

Cristal Evolution for window envelopes

Cristal Evolution is a transparent

paper produced from wood fi bers, a

fully renewable resource. It is com-

pletely recyclable and biodegradable.

Using Cristal Evolution in the windows

of window envelopes makes the enve-

lope an all-paper product, contributing

effi ciently to sustainable development.

As environmental concern becomes

more and more part of the strategies

of Ahlstrom’s customers, the highly

technical Cristal Evolution becomes

the perfect solution for ecological

envelopes. In addition, the use of

Cristal Evolution windows allows cus-

tomers in France and Japan to print

the offi cial eco-label on the envelope.

capable of providing their customers

with day-to-day research and develop-

ment services.

At year-end, Ahlstrom had a total

of 192 (208) employees working on

its research and development activities.

The company’s expenditure on R&D

was EUR 27.6 million (EUR 32.9 million

in 2003). This fi gure equates to 1.8%

of net sales (2.2%). The decline in

fi gures is mainly attributable to the

creation of Sonoco-Alcore joint venture,

as Ahlstrom’s cores & board businesses

were excluded from corporate account-

ing as of November, 2004.

8 Annual Report 2004

Ahlstrom’s performance improvement

program, “a plus”, aims to consolidate

the know-how and experience of

Ahlstrom employees, and to incorpo-

rate these best practices into daily

routines.

All sites now on boardWhen launched, the program involved

three selected pilot sites. Their role was

to customize the methodology to fi t

Ahlstrom’s businesses and cultures. The

success of this phase made it possible

to further develop the tool and to

expand it progressively to all Ahlstrom’s

sites.

Since then, Ahlstrom’s employees

worldwide have discovered the value

of “a plus” and adapted its tools for

”a plus” expands to all Ahlstrom sitesuse as part of their everyday working

procedures. The enthusiasm shown

by more than 1,000 employees (16%

of Ahlstrom’s total headcount) who

have so far been involved in one or

more of the program’s project teams,

gives great hope for the future of the

program.

The early starters are now well

advanced with the process and are

able to make full use of the program.

At these sites, the level of employee

involvement now exceeds 45% of

the staff.

Turnaround to Performance Excellence2004 was also a year of consolidation

at Ahlstrom’s sites. Major improve-

ments were made in the way business

is conducted and in how the company

serves its customers. At the same time,

there has been an ongoing effort both

to continue the process of improve-

ment and to consolidate the gains

resulting from earlier projects.

Ahlstrom has also developed its

own training program to strengthen

the leadership and problem solving

skills of its managers. This effort will

be intensifi ed in 2005, as will the

‘cross-fertilization’ between sites to

ensure that the benefi ts and best

practices created through “a plus”

will be shared by all. This will further

emphasize the commitment to better

serve the customers, Ahlstrom’s top

priority.

If you are a tea drinker, there’s a good

chance that Ahlstrom (formerly

Dexter) and Unilever (today under

the brand Lipton, formerly T J Lipton)

have contributed to both the quality

and taste of your last cup. In 1938,

when it was discovered that Ahlstrom’s

porous yet strong and lightweight

nonwoven material could be used to

hold tea leaves, a great idea was born:

the modern teabag. This was quite a

change from early 20th century tea

bags, made of gauze and stitched.

Over the years, a close working

relationship has resulted in further

Ahlstrom & Lipton:

Inventors of the modern teabag

developments. In 1952, Lipton launched

the fi rst ‘fl o-thru’ tea bag – a double

chambered bag allowing for more area

to be exposed to hot water. Then, in

the 1990’s a revolution: the invention

of leak proof teabags. No longer would

consumers complain of leaky bags or

tealeaves in their cup of tea! Compa-

nies’ desire to brand their teabags is

the most recent development, and

now specially developed nonwoven

materials allow teabag companies to

bear their logo directly on the bag.

Today, Ahlstrom remains one of

Unilever’s main nonwoven suppliers.

The teabags are a strategic product

for Ahlstrom, and the company cur-

rently holds a signifi cant market share

globally. The fabrication of nonwoven

materials for teabags at Ahlstrom’s

Windsor Locks, US plant currently

supplies the US and worldwide market,

while the Chirnside, Scotland plant

focuses mainly on Europe.

A long history of the two compa-

nies, and their desire to meet chal-

lenges with innovative new products,

has meant that they have been respon-

sible for producing great cups of tea for

almost 70 years.

9Ahlstrom Corporation

Success factors

Ahlstrom & Voith have a lot in common.

Both are longstanding businesses with

a passion for papermaking, and they

are also suppliers to each other.

In 1957, Ahlstrom began supplying

Voith (previously Kleinewefers), a world

leader in paper machine technology,

with fi ber material used in calender

bowls. Calender bowls are made out

of cotton paper sheets stacked on

a steel shaft. The bowl is fi nished

after pressing and turning. During the

fi nishing phase of papermaking called

“supercalendering”, paper passes over

Ahlstrom & Voith:

A mutual passion for papermaking

the cylinders enhancing its surface

properties, such as glossiness and

smoothness.

Today, Ahlstrom’s material is used

in 70% of the calender bowls world-

wide. Specifi cally, Ahlstrom continues

to be Voith’s largest supplier, while

primarily serving paper mills involved in

the fi nishing of printing or high density

papers. Calender bowls are used also

to fi nish textiles, as well as in the pro-

duction of audio and video tapes.

Passionate about paper and under-

standing customer needs, Ahlstrom

strives to provide fl exible service and

quality in its products and operations.

Research and development has

enhanced Ahlstrom’s fi ller materials to

ameliorate gloss and smoothness of

printing papers plus mark resistance

or durability of the bowls.

In 1994, the relationship came full

circle when Ahlstrom purchased Voith’s

mixing and twisting machine for its

Altenkirchen, Germany plant, to fi nish

calender bowl papers in order to run in

Voith’s (Kleinewefers) calenders.

Ahlstrom & 3M: Long-lasting innovative cooperation

Ahlstrom’s relationship with 3M, one of

the world’s most diversifi ed and innova-

tive technology companies specializing

in, among other areas, consumer offi ce

products, began almost 40 years ago

at Ahlstrom’s Rottersac, France plant.

During this time, Ahlstrom’s activity has

mainly centered around two types of

products: paper used in photocopiers

and calendered paper used in the now

famous Post-it® note product.

As far back as 1966, Ahlstrom

began supplying 3M with copy and

transfer paper for photocopy machines.

However, as photocopying technology

advanced, these types of paper became

obsolete.

A turning point in the relationship

was in fact in 1980, when Ahlstrom

performed the fi rst trials for the paper

used in what is now a widely used

offi ce staple: the yellow Post-it® note.

The immense popularity of the product

led to a close cooperation between

Ahlstrom and 3M to ensure a reliable

supply and continual innovation.

Among other characteristics, the

selection of dyes and the way in which

they are incorporated into the paper

is of prime importance to ensure color

consistency and longevity. To this end,

since the launching of the original

yellow Post-it® note, Ahlstrom has been

involved in many innovative develop-

ments: white for personalization, and

multicoloured, including pastels, fl uores-

cent and other intense colors.

Today the relationship remains

strong, and regular meetings keep both

sides apprised of new objectives and

future developments.

10 Annual Report 2004

February 12

Ahlstrom streamlines French

operationsThe Specialties division of Ahlstrom announced

plans to restructure its coreboard and crepe

paper facility in Pont-Audemer, France. The

restructuring measures included the closing

of its coreboard production line. As a result,

the headcount of Pont-Audemer plant was

reduced by 70 employees. The plant now

focuses entirely on the production of crepe

papers.

April 19

Ahlstrom and Sonoco build leading

European cores and tubes companyAhlstrom and Sonoco, a global packaging

company, signed an agreement to combine

their European paper-based core, tube and

coreboard operations. Ahlstrom will hold

35.5% and Sonoco 64.5% of the shares in

the new entity named Sonoco-Alcore.

Sonoco-Alcore is the largest European

producer of cores and tubes.

May 25

Investigation by the EU

competition authoritiesThe European Commission competition

authorities investigated Ahlstrom’s

premises at various locations. The

investigations were related to alleged

anti-competitive practices between

competitors within the release liners

and face stock product segments.

June 23

Ahlstrom acquires North American

filtration materials producerAhlstrom acquired Hollinee, L.L.C.'s US-

based filtration division that manufactures

mainly nonwoven filtration materials for

Heating, Ventilation, and Air-Conditioning

(HVAC) applications. The transaction

expands Ahlstrom's product offering

to the HVAC filtration media business,

offering promising global growth

opportunities. The acquired business

employs approximately 200 people at

two US sites.

June 24

New production line inaugurated

at Windsor Locks, USA plantAn investment of EUR 38 million was

made at Ahlstrom’s Windsor Locks plant.

The new production line serves mainly

the growing North American wipes

market, and offers more innovative

products and economies of scale.

January February March April May June

April 2

Modification of a production line

in Turin completedA production line at the Turin, Italy plant

was reconfigured in order to increase the

breadth of product offering available. In

addition to the specialty paper products the

line was previously dedicated to, it is now

capable of supporting the fast growing

nonwovens market with products designed

specifically for the engine filtration market

and for medical, wipes and general industrial

applications. The investment was valued at

EUR 11 million.

Main events

11Ahlstrom Corporation

2004 in brief

July 22

Juha Rantanen appointed CEO

of Outokumpu Group Juha Rantanen, President and CEO of Ahlstrom

Corporation, was appointed CEO of the

Outokumpu Group, effective January 1, 2005.

Juha Rantanen had worked for Ahlstrom

since 1997.

July 29

Jukka Moisio appointed President

& CEO of Ahlstrom CorporationAhlstrom’s Board of Directors appointed

Jukka Moisio as President and CEO, effective

September 1, 2004. Previously, he was

President of the FiberComposites division,

Executive Vice President, and deputy

to the President & CEO of Ahlstrom

Corporation. He joined Ahlstrom in 1991.

October 1

Ahlstrom divested its remaining

packaging manufacturingTecno Jolly (Akerlund & Rausing SpA) in Italy

was sold to the Italian flexible packaging

company Sacchital SpA, and Russian ZAO

Akerlund & Rausing Kuban to Kuban AB. The

divested entities employ in total approximately

300 persons. These transactions complete

Ahlstrom’s exit from the packaging manu-

facturing business.

October 4

Ahlstrom acquired US-based Green

Bay NonwovensThe transaction strengthened Ahlstrom's

position in the wipes market and

complemented its product offering with

the addition of specialty spunlace and resin

bond technologies. The acquired business

employs 75 people at its Green Bay, Wisconsin

facility.

November 9

Ahlstrom and Sonoco complete

the creation of a European cores

and tubes companyAhlstrom announced that the conditions

set by the European Commission for the

creation of the joint venture Sonoco-

Alcore had been fulfilled. Following this

transaction, Ahlstrom’s entire focus is

now on high-performance nonwovens

and specialty papers.

July August September October November December

October 6

Organizational changesAhlstrom announced a flattening of its

organization to be more customer driven.

The new organization helps Ahlstrom

recognize customer needs more rapidly,

bringing a considerable competitive edge

to its operations.

As of January 1, 2005, Ahlstrom’s

FiberComposites division was divided into

three business areas: Nonwovens, Filtration

and Glass Nonwovens. These three areas

make up the FiberComposites segment.

Together, the LabelPack and Specialties

divisions formed the new Specialty Papers

segment as of the same date. The segment

includes both the Label & Packaging Papers

and the Technical Papers business areas.

October 21

EUR 28 million investments at

the South Korea plant completedA second production line and a new

impregnation line were inaugurated at

the Hyun Poong, South Korea plant.

These investments enable the facility to

manufacture both filtration media and

nonwovens for the growing Asian market.

12 Annual Report 2004

Ahlstrom completed its structural

change process to become a focused

fi ber materials company in 2004. In

October, we divested the remaining

two packaging manufacturing units and

in November a joint venture for cores

and coreboard production started its

operations. This has taken six years,

with two parallel agendas: fi rst, we sold

several non-core businesses and units

to more dedicated future owners and

secondly, we invested in fi ber materi-

als know-how, trained our teams and

developed the business through organic

growth and acquisitions.

On behalf of all employees and

shareholders, I would like to take this

opportunity to thank my predecessor

Juha Rantanen for his signifi cant contri-

bution in steering Ahlstrom towards a

one focus company.

Profi tability improvement In 2004, Ahlstrom’s profi tability

remained well below our target level

for a variety of reasons. In 2005, our

major target is to deliver improved

fi nancial performance.

We made some progress over the

previous year with our operating profi t

amounting to EUR 51.0 million (EUR 48.5

million in 2003) and return on capital

employed (ROCE) to 5.3% (4.6%).

Our operating cash fl ow remained at a

good level despite two acquisitions and

several investments in new manufac-

turing lines. However, we fell short of

our group level target of 13% for ROCE.

The main reasons for the profi tability

gap were weak demand in Europe,

currency changes and low utilization of

certain assets.

Our long-term success requires a

solid foundation. We will enhance our

performance orientation and foster

“One Ahlstrom” thinking to advance

a more cohesive company culture

– a signifi cant change compared

with our multi-business history. One

Ahlstrom will enhance our team’s ability

to serve our customers, represent

Ahlstrom worldwide, and to leverage

our expertise. It will further facilitate

a dedication to serving customers

with specialty papers and nonwoven

products.

Business strategy fi ne-tunedIn order to achieve improved fi nancial

performance and to become a more

unifi ed company, we explored and fi ne-

tuned our strategic priorities in 2004.

Long-term customer

relationships

The most signifi cant element in our

business strategy is our much valued,

long-term customer relationships

encompassing often several products

and product generations sold to

one customer. We value highly our

access to leading fi ber materials roll

goods users and we will ensure that

Ahlstrom’s innovation expertise and

manufacturing capabilities meet the

expectations of our world class custom-

ers. Our customer interface consists

of product line teams serving specifi c

13Ahlstrom Corporation

President’s review

customer end uses. The teams are

complemented by our own sales offi ces

or carefully chosen partners.

In 2004, we developed our sales

teams with an aim to upgrade their

skills to meet future customer expecta-

tions. At the same time, we decided to

open new sales offi ces in Poland and

India to increase our sales in emerging

markets. Currently, our products are

sold to 112 countries served by 23

Ahlstrom teams (sales offi ces or

product lines) or by 20 agents. The geo-

graphic breadth of our commercial front

line brings us closer to our customers

worldwide.

Ahlstrom Expertise

Every day, we work with a variety of

natural and synthetic fi bers, as well as

chemicals. Not only do we produce

100% natural or 100% synthetic

fi ber roll goods, but we manufacture

products with many combinations of

both in one product. The unique know-

how in applying a multitude of raw

materials, combined with versatile roll

goods manufacturing, makes Ahlstrom

an innovative partner to leading cus-

tomers worldwide. This knowledge is

our value added to customers – we call

it “Ahlstrom Expertise”.

In 2004, we continued to advance

Ahlstrom Expertise. Our research

team tested fi bers and their features

to design the most suitable products

to meet ever changing quality and

performance criteria. Operations and

engineering professionals worked

to advance proprietary manufactur-

ing solutions. Our product line teams

combine breadth of knowledge into

customer products and solutions to

meet quality and competitiveness

expectations. The dedication behind

Ahlstrom Expertise manifests itself in

initiatives such as training of our teams,

research and innovation and the Perfor-

mance Excellence (“a plus”) program,

to name just a few.

Seeking to grow

The journey from multi-business to

focused fi ber materials company has

decreased the group net sales by

divestments during the past years.

However, our fi ber materials business

has been able to grow approximately

10% annually. We aim to develop and

successfully implement attractive new

ideas, products and technologies.

In 2004, our investments in new

manufacturing capabilities and acquisi-

tions amounted to more than EUR 160

million and we allocated 1.8% of our

net sales to research and innovations.

With these actions we want to ensure

that we have our required number of

new products in the market and a full

pipeline of new ideas approaching

commercialization.

We expect these investments

to deliver growth and improve our

fi nancial performance in 2005 and

beyond. Our growth ideas are targeted

to strengthen our customer relation-

ships and to serve geographically wider

market areas.

Competitive operations

A high level of innovation and new

products characterize our business

environment. Consequently, we face

and accept the risk of product and

product line obsolescence every day.

In order to remain successful and

maintain our competitiveness we

monitor our businesses continuously

and act with determination on under-

performing businesses.

During the past several years, we

have closed down some non-compet-

itive assets. In addition, we aim to keep

costs low and our operating model lean

and effi cient. Our “a plus” program and

its success have established a solid

foundation to strive for cost effi ciency

and increased productivity.

Ahlstrom experienced challenging

structural change as it transitioned to a

dedicated fi ber materials company. In

2005, we are well positioned to deliver

improved fi nancial results with a lean

organization, a determination to better

serve our customers, and to become an

even more successful supplier of fi ber

materials.

I would like to thank our employ-

ees, customers, shareholders and other

stakeholders for their continued support

and commitment during 2004. I invite

you to join our current journey in the

fi ber materials business, where we aim

to be the world leader.

Jukka Moisio

President and CEO

In 2005, we are well positioned to deliver improved

fi nancial results with a lean organization, a determination

to better serve our customers, and to become an even

more successful supplier of fi ber materials.

14 Annual Report 2004

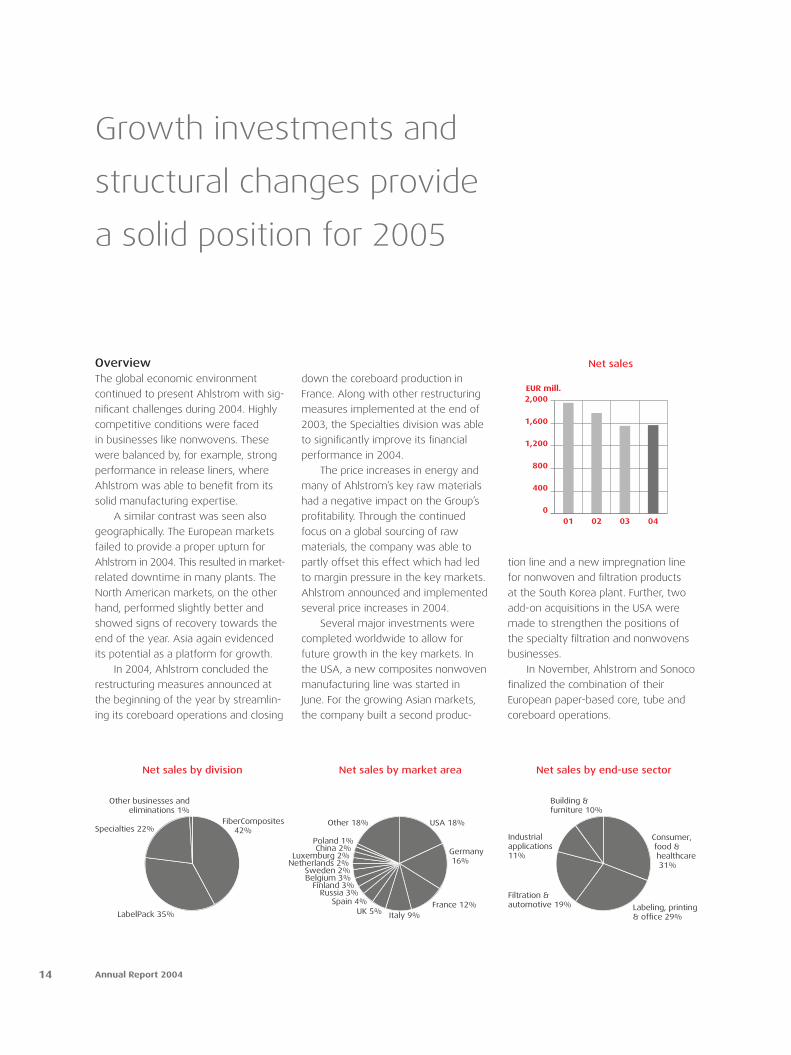

Growth investments and

structural changes provide

a solid position for 2005

OverviewThe global economic environment

continued to present Ahlstrom with sig-

nifi cant challenges during 2004. Highly

competitive conditions were faced

in businesses like nonwovens. These

were balanced by, for example, strong

performance in release liners, where

Ahlstrom was able to benefi t from its

solid manufacturing expertise.

A similar contrast was seen also

geographically. The European markets

failed to provide a proper upturn for

Ahlstrom in 2004. This resulted in market-

related downtime in many plants. The

North American markets, on the other

hand, performed slightly better and

showed signs of recovery towards the

end of the year. Asia again evidenced

its potential as a platform for growth.

In 2004, Ahlstrom concluded the

restructuring measures announced at

the beginning of the year by streamlin-

ing its coreboard operations and closing

tion line and a new impregnation line

for nonwoven and fi ltration products

at the South Korea plant. Further, two

add-on acquisitions in the USA were

made to strengthen the positions of

the specialty fi ltration and nonwovens

businesses.

In November, Ahlstrom and Sonoco

fi nalized the combination of their

European paper-based core, tube and

coreboard operations.

down the coreboard production in

France. Along with other restructuring

measures implemented at the end of

2003, the Specialties division was able

to signifi cantly improve its fi nancial

performance in 2004.

The price increases in energy and

many of Ahlstrom’s key raw materials

had a negative impact on the Group’s

profi tability. Through the continued

focus on a global sourcing of raw

materials, the company was able to

partly offset this effect which had led

to margin pressure in the key markets.

Ahlstrom announced and implemented

several price increases in 2004.

Several major investments were

completed worldwide to allow for

future growth in the key markets. In

the USA, a new composites nonwoven

manufacturing line was started in

June. For the growing Asian markets,

the company built a second produc-

Net sales

2,000

1,600

1,200

800

400

0

EUR mill.

02 03 0401

Net sales by division

LabelPack 35%

Specialties 22%

Other businesses andeliminations 1%

FiberComposites 42%

Net sales by market area

USA 18%

Germany 16%

Italy 9%France 12%

UK 5%Spain 4%

Russia 3%Finland 3%

Belgium 3%Sweden 2%

Netherlands 2% Luxemburg 2%

China 2%Poland 1%

Other 18%

Industrialapplications11%

Net sales by end-use sector

Labeling, printing& office 29%

Building &furniture 10%

Filtration &automotive 19%

Consumer, food & healthcare 31%

15Ahlstrom Corporation

The tough market environment

contributed to the Group making an

unsatisfying 7.1% return on capital

employed (excluding non-recurring

items) which, however, represents

improved profi tability over the previous

year. Cash fl ow remained satisfactory

and the Group’s gearing was 53.9%,

well within the target of 50–80%.

DeliveriesVolumes delivered to customers grew

by 5.1% on a comparable basis. The

increase in volumes was due to the

market growth as well as businesses

acquired and investments made by the

FiberComposites division. In addition,

the Specialties division’s pre-impreg-

nated decor papers increased their

deliveries substantially.

Sluggish demand in certain product

lines led to machine downtime. For the

whole year, market-related downtime

was 3.7% and capacity utilization 86%

of total capacity. However, the capacity

utilization rate improved towards the

end of the year.

Net sales unchangedConsolidated net sales amounted to

EUR 1,568 million (EUR 1,556 million).

The increase of EUR 12 million broke

down to the following factors:

EUR mill.

Volumes + 68

Sales prices + 6

Foreign currency - 41

Other (e.g. structural changes) - 21

+ 12

Net sales were adversely impacted by

the unfavorable currency development.

Further, the sale of the cores and core-

board operations, the Tecno Jolly and

Kuban plants, as well as the closure of

the coreboard production line in France

decreased net sales in 2004. Adjusted

for the structural changes, comparative

Financial review

net sales in fi scal year 2004 were 2%

higher than in the previous year.

Geographically, net sales looked

similar to last year. Europe remains

the Group’s most important market

area, accounting for 62% of total sales

in 2004 (62%). Net sales in North

America increased slightly to 19%,

compared to 18% a year ago, while

Asia’s share remained approximately

the same at 8% (8%). Ahlstrom’s

sales to the domestic Finnish market

accounted for 3% (3%) in 2004.

Slight improvement in profi tabilityThe Group’s operating profi t increased

to EUR 51.0 million (EUR 48.5 million),

representing a 3.3% margin (3.1%).

The operating profi t includes certain

exceptional transactions, which are not

related to normal business operations

and which are reported as non-recur-

ring items, shown below.

Operating profit

100

80

60

40

20

0

EUR mill.

02 03 0401

(excluding non-recurring items)

Profit before extraordinary items

75

60

45

30

15

0

EUR mill.

02 03 0401

(excluding non-recurring items)

Net profit

60

48

36

24

12

0

EUR mill.

02 03 0401

(excluding non-recurring items)

16 Annual Report 2004

EUR mill. 2004 2003

Operating profi t (EBIT) 51.0 48.5

Non-recurring items:

- asset sales 5.3 - 4.6

- restructuring costs 11.5 21.7

- other non-recurring items 3.5 - 0.2

EBIT w/o non-recurring items 71.3 65.4

The sales of the Tecno Jolly and

Kuban plants (loss of EUR 10.6 million)

as well as the forming of the Sonoco-

Alcore joint venture (gain of EUR 4.3

million) are shown as asset sales.

Restructuring costs relate to write

downs of assets and provision charges

for personnel reductions in underper-

forming units.

Operating profi t excluding non-

recurring items increased by EUR 5.9

million. The change was attributable

to the divisions as follows:

EUR mill.

FiberComposites - 11

LabelPack - 5

Specialties + 16

Other units + 6

+ 6

The biggest achievement in 2004

was the solid turnaround of the

Specialties division. The result of the

FiberComposites division was hit mainly

due to the weak demand in Europe,

as well as the restructuring costs and

write-downs across the division.

The share of profi ts from opera-

tive associated companies, in particular

Jujo Thermal Oy, amounted to EUR 2.8

million (EUR 3.4 million). From 2005

onwards, Sonoco-Alcore will also be

reported as an associated company.

Profi t before extraordinary items

and taxes was EUR 34.8 million (EUR

33.7 million). Net interest expenses

increased to EUR 12.0 million (EUR 10.4

million). The increase was mainly due

to higher interest-bearing debt. The

foreign exchange loss, arising from the

conversion of foreign currency denomi-

nated assets and liabilities, was EUR

2.1 million (EUR 4.7 million). Other net

fi nancial expenses were EUR 2.8 million

(EUR 0.2 million), partly due to

fees related to the new fi nancing facilities.

Net profi t was EUR 17.5 million (EUR

22.4 million). Income taxes amounted

to EUR 17.1 million (EUR 11.1 million).

Non-recurring tax refunds lowered the

income taxes in 2003. High effective

tax rate in 2004 is partly a result of

the non-deductible divestments. The

EPS (earnings per share) decreased to

EUR 0.48, compared to EUR 0.61 a year

earlier.

Return on capital employed (ROCE)

was 5.3% (4.6%) and return on equity

(ROE) 2.7% (3.2%). As total invest-

ments more than compensated the

effects of divestments and the reduc-

tion of working capital in 2004, capital

employed increased slightly to EUR

1,009 million at December 31 (EUR

994 million).

To achieve improvements in

operating performance at our plants,

Ahlstrom continued its “a plus” perfor-

mance excellence program in 2004.

By the end of 2004, “a plus” had been

introduced in all Ahlstrom’s plants. To

learn more about “a plus”, see page 8.

Cash fl ow remained healthyAhlstrom continued to generate healthy

operating cash fl ow. Net cash from

operating activities, namely the cash

fl ow after net interest expenses, taxes

paid, and the change in working capital,

amounted to EUR 128.0 million (EUR

202.0 million) and developed positively

during the second half of the year. In

2003, the decrease in working capital

had a positive effect on the cash fl ow.

The same effect was not seen in 2004.

Interest-bearing net debt increased

by EUR 56.0 million to EUR 341.8 million

(EUR 285.8 million) mainly due to the

acquisition of Hollinee L.L.C.’s Filtration

Division and Green Bay Nonwovens, Inc.

A dividend of EUR 1.50 per share was

paid to the shareholders in 2004, total-

ling EUR 54.6 million. The strengthening

of the euro decreased the debt in the

balance sheet by approximately EUR

7 million.

Ahlstrom’s gearing (ratio of interest-

bearing net debt to equity) was 53.9%

at year-end (42.3%). Equity ratio dec-

lined to 45.3% (47.4%).

The Group’s liquidity remained

good throughout the year. At year-end,

cash and marketable securities were

EUR 19.6 million (EUR 24.1 million).

In addition, committed credit facilities

available to the Group amounted to

EUR 764 million, including a new 5-year

EUR 400 million syndicated revolving

credit facility raised in November 2004.

Return on capitalemployed (ROCE)

10

8

6

4

2

0

%

03 0402

Return on equity(ROE)

10

8

6

4

2

0

%

03 0402

Earnings per share

2.0

1.5

1.0

0.5

0

-0.5

EUR

02 03 0401

17Ahlstrom Corporation

Focused capital expenditureCapital expenditure for the year

exceeded the level of depreciation and

excluding acquisitions amounted to

EUR 101.0 million (EUR 92.5 million).

The biggest investments were the EUR

38 million new composites nonwoven

manufacturing line built at Windsor

Locks, USA, and the EUR 28 million

investment in a second production line

for nonwoven and fi ltration products in

South Korea.

In addition, two production lines

were rebuilt at the Turin plant in Italy

for engine fi ltration products, medical

and general industrial applications, and

wipes, totaling EUR 17 million.

Ahlstrom will lower its capital

spending for 2005 due to a decrease

in the number of large investment

projects.

Acquisitions and divestmentsThe total acquisition costs for the year

amounted to EUR 66.0 million (EUR 0.7

million).

During 2004, the FiberComposites

division completed two add-on acquisi-

tions in the USA to strengthen its

position in the fi ltration and nonwovens

businesses. In June, the Hollinee Filtra-

tion Division was acquired to expand

Ahlstrom’s air and heating fi ltration

product range. The business was sub-

sequently named Ahlstrom Air Media.

In October, Green Bay Nonwovens

was acquired to strengthen Ahlstrom’s

wipes product line.

In October 2004, Ahlstrom

completed the sale of its packaging

business, which consisted of one

production facility in Italy (Tecno Jolly)

and one production facility in Russia

(Kuban). The combined net sales

of these businesses were EUR 30

million in 2003. In the fourth quarter,

Ahlstrom recognized a EUR 10.6 million

loss related to these sales. Ahlstrom

continues to produce base materials

for fl exible packaging: calendered and

one-side coated papers, as an integral

part of its Label & Packaging Papers

business area.

Ahlstrom and Sonoco combined

their European paper-based core, tube

and coreboard operations in 2004. The

joint venture, Sonoco-Alcore, began

operations in November, 2004. Sonoco-

Alcore employs 1,800 people and its

annual net sales amount to approxi-

mately EUR 300 million, making the

company the largest European producer

of cores and tubes. Ahlstrom holds

35.5% of the shares in the new entity.

Cores and board business contributed

net sales of EUR 71 million to Ahlstrom

Group in January–October 2004.

Financial performance by divisionFiberComposites

The division’s net sales increased to

EUR 663.8 million (EUR 644.7 million)

refl ecting higher delivery volumes,

mainly due to the acquired businesses

and investments made in 2003 and

2004. Volumes grew by 11% over the

previous year. The net sales were nega-

Financial review

Interest-bearing net debtand gearing ratio %

100

80

60

40

20

0

%

02 03 0401

750

600

450

300

150

0

EUR mill.

Capital expenditure

225

180

135

90

45

0

EUR mill.

02 03 0401

(including acquisitions)

Net cash from operating activities

225

180

135

90

45

0

EUR mill.

02 03 0401

18 Annual Report 2004

tively impacted by the strengthening

of the euro against other currencies, as

over 60% of the divisions net sales are

non-euro denominated.

The division’s result was hit by a

weak demand in Europe, price increases

in oil-based raw materials, restructuring

costs for personnel reductions, and

write-downs in several plants. The

operating profi t was EUR 33.9 million

(EUR 57.2 million), representing a 5.1%

margin (8.9%). The operating profi t for

2003 included a EUR 4.6 million gain on

the sale of the power generating facility

in the USA. Return on net assets was

6.2% (10.8%).

LabelPack

Volumes grew by 1.3% over the

previous year. The division’s net sales

remained at the level of 2003 and

totaled EUR 542.0 million (EUR 541.5

million). The lack of growth in net sales

was due to the Italian production line

being transferred from the LabelPack

division to the FiberComposites division

as of January 1, 2004. Furthermore, the

decline in the US dollar exchange rate

had a negative impact on the division’s

overseas sales. The division imple-

mented several price increases during

the year.

The capacity utilization rate of the

division was good (96%), mainly due

to the favorable market conditions

for release base papers. The division’s

profi tability was, however, affected by

the increased raw material and energy

prices as well as the higher fi xed costs

mainly due to one-time charges, result-

ing in a decline in the operating profi t

to EUR 17.1 million (EUR 24.9 million).

Return on net assets for the division

was 6.2% (8.3%).

Specialties

The division’s net sales remained nearly

unchanged compared to the previous

year and were EUR 343.9 million (EUR

344.7 million). Excluding the Cores &

Board business, volumes sold increased

by 13% compared with 2003, and net

sales totaled EUR 270.9 million, repre-

senting an increase of 5.4%.

Improved market conditions in

most product lines boosted the deliv-

eries and the fi nancial performance

improved considerably compared to the

previous year. The restructuring projects

in France and Germany continued to

drive reductions in fi xed costs.

The division reported a complete

turnaround, resulting in an increase

in oper ating profi t to EUR 10.8 million

(loss of EUR 23.7 million), correspond-

ing to a 3.1% (-6.9%) margin. The

result for 2003 includes non-recurring

costs of EUR 19.1 million related to the

restructuring of operations. The return

on net assets was 7.9% (-13.8%). The

improvement is attributable to higher

volumes, improved plant performance

and cost reductions.

Other operations

The major part of other operations

business relates to the Tecno Jolly

plant in Italy and the Kuban plant in

Russia, both of which were sold in

November 2004. Net sales of other

operations were EUR 27.1 million (EUR

36.2 million). Operating profi t together

with the associated company Jujo

Thermal Ltd was EUR 2.0 million (EUR

1.7 million).

Other operations include also

corporate units in Finland, France and

the USA as well as the sales offi ces

serving the customers of all businesses

through Ahlstrom’s own global sales

and marketing network, bringing the

total operating loss of other operations

to EUR 10.9 million (a loss of EUR 10.0

million). The loss is mainly due to the

loss of the sales of the Tecno Jolly and

Kuban plants.

The associated company Sonoco-

Alcore will be reported under other

operations.

Change in business structureIn October, Ahlstrom announced a

change in the external reporting

structure to refl ect the realignment of

the business. The new structure, which

took effect on January 1, 2005, is based

on two segments, FiberComposites

and Specialty Papers. The Specialty

Papers segment consists of the former

LabelPack and Specialties divisions

with annual net sales of approximately

EUR 810 million. The FiberComposites

segment, continuing with the same

lines of business as earlier, reported

annual net sales of EUR 664 million

in 2004.

19Ahlstrom Corporation

Financial review

Quarterly data by division

EUR million Q1/2003 Q2/2003 Q3/2003 Q4/2003 Q1/2004 Q2/2004 Q3/2004 Q4/2004

Net sales

FiberComposites 172 166 157 151 164 166 165 169

LabelPack 147 138 132 124 138 141 133 131

Specialties (excl. Cores & Board) 71 64 62 60 69 70 68 66

Other operations and eliminations -3 -2 -3 2 -3 -2 -2 -1

Continuing operations total 387 366 348 337 368 375 364 365

Discontinued operations 30 30 29 29 29 30 29 7

Group total 417 396 377 366 397 405 393 372

Operating profi t

FiberComposites 21.7 14.5 11.6 9.4 10.9 11.8 7.3 4.0

LabelPack 11.2 4.8 5.0 3.9 3.2 3.2 5.5 5.2

Specialties (excl. Cores & Board) 2.4 -0.5 -4.8 -23.5 1.6 1.7 1.0 2.7

Other operations and eliminations -3.7 -3.0 -0.6 -1.2 -0.4 -0.4 -0.8 -2.5

Continuing operations total 31.6 15.8 11.2 -11.4 15.3 16.3 13.0 9.4

Discontinued operations 0.1 0.7 0.1 0.4 0.3 0.8 1.7 -5.8

Group total 31.7 16.5 11.3 -11.0 15.6 17.1 14.7 3.6

Quarterly income statement

EUR million Q1/2003 Q2/2003 Q3/2003 Q4/2003 Q1/2004 Q2/2004 Q3/2004 Q4/2004

Net sales 417 396 377 366 397 405 393 372

Expenses 1) -364 -354 -341 -330 -358 -363 -351 -328

Other income and expense 1) 1 1 2 1 3 3 1 -1

Depreciation and amortization 1) -27 -26 -26 -27 -25 -25 -26 -25

Non-recurring items 5 0 -1 -21 -1 -3 -2 -14

Operating profi t 32 17 11 -11 16 17 15 4

Net fi nancial items -6 -3 -2 -4 -3 -3 -4 -7

Profi t before extraordinary items 26 13 9 -15 13 14 11 -3

and taxes

Income taxes 2) -11 -7 -3 9 -6 -6 -4 -1

Minority interests 0 0 0 0 0 0 0 0

Net profi t 15 6 6 -5 7 8 7 -4

Operating profi t 1) 27 17 12 10 17 20 17 18

Operating profi t, % 1) 6.5 4.2 3.3 2.7 4.1 4.9 4.3 4.9

1) Excluding non-recurring items.

2) Taxes are stated as the tax corresponding to the result for the reported period.

20 Annual Report 2004

Foreign currencies

A large part of the Group’s cash fl ows,

receivables, payables and loans are

denominated in currencies other than

the euro. Internationally traded pulp,

which at present is Ahlstrom’s main

raw material, is generally priced in US

dollars. In contrast, products sold are

mostly priced in local currencies.

Consequently, fl uctuations in the

US dollar and the euro have an impact

on Ahlstrom as they affect not only

the Group’s result, but also its fi nancial

development and competitiveness.

The strengthening of the euro has

had a signifi cant impact on the

FiberComposites division’s sales and

profi tability, as over 60% of the sales

are denominated in non-euro curren-

cies. Similarly, the non-euro based sales

of the other divisions were affected by

the stronger euro. In order to mitigate

this risk at Group level, Ahlstrom

operates a currency hedging policy

which is explained in the Financial Risk

Management section, on page 76.

Fibers

The main raw materials for Ahlstrom

are various wood pulps and other

natural fi bers (cotton, abaca etc.) as

well as synthetic fi bers. The Group’s

total fi ber costs in 2004 were EUR 429

million, with wood pulp accounting for

the biggest share of the total. The costs

of other natural, synthetic and glass

fi bers increased by more than 15%.

Ahlstrom does not produce wood

pulp and therefore purchases 100%

of its pulp needs. The Group’s profi t-

ability is thus exposed to variations in

pulp prices, with certain exceptions

for specialty pulps. Although the price

variations are partly passed on to

customers, Ahlstrom is sensitive to

quick changes in the highly volatile pulp

markets. Ahlstrom’s goal is to limit the

price sensitivity by setting fi rm prices,

or by agreeing fl oor and cap price level

contracts.

Chemicals

Ahlstrom uses a wide variety of chemi-

cals (latex binders, fi llers and pigments,

resins, etc) in production. The total

costs of chemicals in 2004 amounted

to EUR 179 million. Latex binders, being

the biggest single type of chemicals,

represented more than 25% of these

costs. There is high volatility in the

price of latex due to its strong histori-

cal correlation with the crude oil and

petrochemicals derivatives prices. The

target is to reach agreements based on

the lowest possible guaranteed annual

prices for each chemical.

Energy

The Group’s total energy costs in 2004

amounted to EUR 110 million, with

electricity, gas and steam constituting

more than 90% of the total.

In 2004, the European market faced

electricity price increases, and the

electricity price is expected to remain

high in 2005. However, more than half

of Ahlstrom’s electricity needs in Europe

(and some in the USA) are covered by

fi rm price purchase contracts for 2005.

The target is to further decrease price

sensitivity through coordinated purchas-

ing and fi rm price contracts, as well as

with total consumption optimization.

The CO2 emissions trading within

the EU starts in 2005. In most of the EU

countries where Ahlstrom has produc-

tion, the emission rights have already

been allocated and distributed to the

industries. However, Italy and Spain had

not announced their allocation deci-

sions by the end of 2004. Ahlstrom has

suffi cient rights to cover the present

CO2 emissions, and thus the emission

trading scheme is not expected to have

a fi nancial impact on the Group in 2005.

Capacity utilization rate

Capacity utilization has a major impact

on Ahlstrom’s profi tability. Production

volumes depend on demand and

products are manufactured mainly

against orders. In addition, the margins

vary from one product to the other,

and therefore the product mix also

has an effect on profi tability.

Factors affecting Ahlstrom’s profi tability

Invoicing by currency

EUR 65%

USD 28%

GBP 4%Other 3%

Raw material and energy costs

Fibers 57%

Chemicals 24%

Energy 15%

Others 4%

Total costs EUR 745 million

EUR/USD Exchange rate

1.40

1.30

1.20

1.10

1.00

1/03 6/03 1/04 6/04 12/04

21Ahlstrom Corporation

Financial review

Adoption and effects of the IFRS

Ahlstrom begins to apply International

Financial Reporting Standards (IFRS)

in its fi rst-quarter interim report 2005,

which will be published on April 27,

2005. Prior to the publishing of the Q1,

2005 results, Ahlstrom will publish its

comparative 2004 (Q1-Q4) fi nancial

statements in order to communicate

the effects of the adoption of IFRS.

In the transition to IFRS, Ahlstrom

will apply the First-Time Adoption

standard that allows exceptions to

some of the specifi c standards at the

time of transition. January 1, 2004 is

used as the transition date to IFRS. As

for the fi nancial instruments, Ahlstrom

utilizes the exemption for a fi rst-time

adopter of IFRS not to restate compara-

tive information for 2004.

The most signifi cant effects of the

transition to IFRS relate to the treat-

ment of goodwill, pension and impair-

ment of assets. The other changes

relate mainly to the fair value mea-

surement and recognition of fi nancial

instruments as well as the reporting of

fi nance leases. The transition to IFRS

does not affect the Group’s cash fl ow.

Adoption of IFRS will have a

positive effect on the Group’s operating

profi t due to the abolition of goodwill

amortization, amounting to EUR 12

million in 2004. At the IFRS opening

balance sheet as per January 1, 2004,

Ahlstrom’s shareholders’ equity will

decrease by approximately EUR 55

million mainly due to increases in

pension obligations and impairment

write-downs of assets. The Group’s

balance sheet structure and the

gearing ratio will be slightly weakened

as a result of the IFRS transition.

Employee benefi ts

Ahlstrom has various pension and other

postretirement plans in accordance with

local practices in the countries where

it operates. Under FAS, the pension

liabilities are reported according to

local regulations. Under IFRS, all plans

are classifi ed as being either defi ned

contribution plans or defi ned benefi t

plans. The obligations of defi ned benefi t

plans are charged to income based on

the calculations made by authorized

actuaries.

At the date of transition to IFRS,

the Group’s pension obligations will

increase by approximately EUR 25

million. The largest increases by country

are as follows: EUR 14 million in UK,

EUR 8 million in Germany and EUR 4

million in Finland.

The change to the principle for

calculating disability pension liabilities

under the Finnish statutory employ-

ment pension scheme (TEL) will not

have a major effect for Ahlstrom.

The change will release the previously

made provision and enter a positive

item of approximately EUR 3 million

in operating profi t.

Business combinations

and impairment of assets

Business combinations before the date

of transition to IFRS are reported in

accordance with the same principles as

under FAS. Acquisitions after January 1,

2004 are reported in accordance with

IFRS 3. Hence, part of the goodwill rec-

ognized from the acquisitions in 2004

may be reclassifi ed as intangible assets.

Goodwill is no longer amortized

but will instead be tested periodically

for impairment. In the IFRS opening

balance sheet the total amount of

goodwill is EUR 74 million.

Ahlstrom periodically evaluates

the carrying amounts of assets to

determine whether there is any indica-

tion of impairment. If such indication

exists, the assets are written down to

a recoverable amount which is esti-

mated as being the higher of the net

selling price and the value in use.

As a result of impairment tests

performed at the date of transition to

IFRS, a total amount of approximately

EUR 60 million of impairment losses are

recognized in the IFRS opening balance

sheet.

Inventory

Changes in inventory may arise from

the reclassifi cation of spare parts.

Income taxes

Deferred taxes are entered in accor-

dance with IAS 12 for IFRS adjustments

causing temporary differences.

Consequently, deferred taxes are not

recognized for permanent differences

and non-deductible goodwill.

As a result of the transition to IFRS,

the change in Ahlstrom’s deferred

taxes are mainly a consequence of

the changes in pension obligations and

impairment write-downs of assets.

The increase in deferred tax assets on

IFRS adjustments at the date of transi-

tion amounts to approximately EUR

20 million.

Business review

FiberComposites• Nonwovens

• Filtration

• Glass Nonwovens

Specialty Papers• Label & Packaging Papers

• Technical Papers

Fiber-Composites45%

Net sales by segment

Specialty Papers 55%

23Ahlstrom Corporation

Business review

The FiberComposites segment com-

prises three business areas: Nonwo-

vens, Filtration and Glass Nonwovens.

The Specialty Papers segment consists

of the former LabelPack and Specialties

divisions and is divided into the busi-

ness areas of Label & Packaging Papers

and Technical Papers.

Ahlstrom’s operations will become

even more customer-driven under

As of January 1, 2005, Ahlstrom was divided into two segments:

FiberComposites and Specialty Papers. Ahlstrom will report

its activities and performance by segment, but operatively

the segments consist of fi ve business areas.

the new organization, in which the

directors of all fi ve business areas are

members of the Corporate Executive

Team. This enables the company to

identify and respond more swiftly to

customer needs and ensures that all

business areas contribute their specifi c

expertise to decision making. The new

organization is also leaner and more

cost effective.

Financial performanceThe new organizational structure

became effective as of January 1, 2005.

The fi nancial performance of Ahlstrom

in 2004 is therefore reported in the

Report by the Board of Directors,

pages 58–61, following the earlier

divisional structure.

Other 6%

Fiber- Composites 50%

Employees by segment

SpecialtyPapers 44%

Other 7%

Fiber- Composites 56%

Capital employed by segment

SpecialtyPapers 37%

Investments and acquisitions

supported growth ambition

<< Ahlstrom’s fi ltration media is an integral component in these air fi lters. In 2004, Ahlstrom expanded its

fi ltration material product offering to the heating, ventilation and air-conditioning (HVAC) applications

through the acquisition of Hollinee, L.L.C’s Filtration Division in the USA. This transaction supports

Ahlstrom’s dedication to being a leading global supplier to fi ltration markets.

25Ahlstrom Corporation

The segment consists of a worldwide

network of development, sales, and

marketing resources with manufactur-

ing assets on four continents. It aims to

strengthen its position among leading

nonwoven producers by offering

innovative products to customers. The

segment uses a large range of syn-

thetic and natural fi bers in its products,

which makes it possible to develop and

customize the product features and

performance to meet customer needs

and pricing expectations.

Market reviewThe business environment remained

challenging in 2004. The demand for

main products was weak in Europe

because of the slow growth in various

industrial sectors – primarily automo-

tive, windmill, building & construction

– which are the segment’s key markets

in Europe. The North American market

started slowly but improved towards

the year-end. Demand in both Asia and

South America was good.

Filtration volumes grew as a

result of investments and acquisitions,

although the automotive industry in

Europe experienced diffi culties due to

moderate growth and rising oil prices.

Nonwovens started the year slowly

but the demand improved towards

the year-end, mainly driven by the

North American market. Demand for

glass nonwovens was weak through-

out the year with the exception of

CV fl ooring tissue.

Profi tability was affected by rapidly

increasing costs of oil-based raw

materials such as synthetic fi bers and

binders, and by increased price compe-

tition. Despite the challenging business

environment, Ahlstrom succeeded

in increasing its volumes through

organic growth investments and two

add-on acquisitions. Its position as a

key supplier in the industry improved

during 2004. New production facilities

for wiping and medical fabrics, engine

fi ltration, and air fi ltration have been

added. In addition, FiberComposites

announced a line extension for glass

nonwovens.

Development measuresFiberComposites completed three major

growth investments in 2004. In Italy, a

new fi ltration materials line came

on-line in April, while in the USA,

a wiping fabrics line for the North

American market was inaugurated

in June. Similarly, a production line

for fi ltration materials and nonwovens

was started in South Korea in October.

These major investments were techni-

cally successful and completed on

schedule to serve growing customer

needs in their respective geographic

regions. Two signifi cant growth invest-

ments are on-going, namely a fi ne

fi bers production line in Italy and a

glass tissue line expansion in Finland.

These will serve customers with new

and improved products during 2005.

In addition, FiberComposites

completed two add-on acquisitions

to strengthen its positions in fi ltration

and nonwovens. Hollinee’s Filtration

Division, subsequently renamed

Ahlstrom Air Media, was acquired

in June 2004 in order to expand

Ahlstrom’s air fi ltration product range.

Green Bay Nonwovens was acquired

in October 2004 to expand Ahlstrom’s

wipes product line.

FiberComposites

Ahlstrom’s FiberComposites is one of the leading nonwoven roll

goods producers in the world, manufacturing and selling fi ltration

materials, nonwoven fabrics and glass nonwovens.

26 Annual Report 2004

R & D activitiesIn 2004, FiberComposites launched

several new and improved products,

including dispersible wiping materials,

composite spunlace fabrics for wiping,

and new fi ltration materials. The rate

of innovation is expected to increase

in 2005 as the new lines manufacture

more advanced products.

OutlookThe business environment continues

to be challenging. North American

demand improved towards the end

of 2004 and seems likely to remain at

a good level in early 2005. European

economic growth is expected to

continue at 2004 level. Asia seems

likely to have another year of growth

ahead. Sales prices will remain under

pressure in 2005 and this, combined

with expected raw material price

increases, will make 2005 a challeng-

ing year. FiberComposites will keep its

operating costs under tight control in

2005 while seeking to benefi t from

the new production line start-ups and

acquisitions made during 2004.

FiberComposites

Business area Nonwovens Filtration Glass Nonwovens

Product line Building Food Technical Medical Wipes Engine Filtration Glass- Glassfi bre Specialty nonwovens fi ltration appli- fi bre reinforce- reinforce- cations tissues ments ments

Plants

Barcelona (E) • • Brignoud (F) • • •

Chirnside (UK) • • • •

Green Bay (USA) • • Groesbeck (USA) • Hyun Poong (ROK) • • •

Karhula (FIN) • • Louveira (BR) •

Madisonville (USA) •

Malmédy (B) • • Mikkeli (FIN) • Mt. Holly Springs (USA) •

New Windsor (USA) • Ställdalen (S) • • • Tampere (FIN) • •

Taylorville (USA) • Turin (I) • • Windsor Locks (USA) • • • • •

Other 1%

Consumer &healthcare 32%

Industrialapplications17%

Net sales by customer industry

Filtration & automotive 40%

Building 10%

Top 10 in nonwovens

300MUSD 600 900 1,200 1,500

2. DuPont

5. Ahlstrom*

3. Kimberly-Clark

6. PGI

4. BBA

7. Johns Manville8. Colbond

9. Buckeye Technologies

1. Freudenberg

10. Japan Vilene

* Including net sales of USD 70 million from Green Bay Nonwovens andHollinee L.L.C’s filtration division, both acquired in 2004.Source: Nonwovens Industry 9/2004, Ahlstrom

27Ahlstrom Corporation

FiberComposites

Breathable Viral Barrier:

Better protection and comfort for medical personnel

Ahlstrom has introduced a breakthrough

fabric for medical gowns. The new

material, called Breathable Viral Barrier

(BVB), not only protects medical per-

sonnel from viral exposures but also

maintains a high level of breathability

and comfort, even as the wearer’s

temperature rises e.g. due to working

stress in the operating theater.

This unique triple-layered fabric

features a responsive, monolithic

membrane sandwiched between inner

and outer fabrics made of a continuous

fi ne fi lament nonwoven. The inner layer

provides a soft touch to the wearer’s

skin while the outer layer provides

additional repellency and strength.

The monolithic technology of the BVB

fabric has passed the American ASTM

F1671 viral penetration test for resis-

tance to bloodborne pathogens and

complies with the performance charac-

teristics of a Level 4 device as classifi ed

by AAMI and the FDA. It provides the

maximum viral protection available in

the market today.

The protection of medical person-

nel, particularly in surgery settings, from

viral exposure has never been more

important. The incidents of viruses

and contagious diseases such as HIV,

Hepatitis and SARS are increasing

throughout the world.

Ahlstrom has launched a new Web

site designed to provide information

to the medical industry about infec-

tion control and the fabrics that help

keep medical personnel safe. This new

Internet resource provides up-to-date

information on key advancements in

viral barrier protection.

For more information, please visit

www.viralbarrier.com.

ASTM: American Society for Testing and Materials

AAMI: Association for the Advancement of Medical

Instrumentation

FDA: Federal Drug Association (US)

The restructuring measures taken

at the end of 2004 will reduce fi xed

costs in 2005.

Nonwovens is well positioned for

2005 to benefi t from new capabilities

arising from organic growth investments

and by the Green Bay Nonwovens add-

on acquisition.

Additional expansion ideas are

being assessed with a view to secure

Ahlstrom’s leading position in fi ltration

media supply.

Glass Nonwovens will expand its

manufacturing capacity in the glass

tissue line and make several investments

to boost capacity and productivity.

Business area reviewsNonwovens

Ahlstrom’s nonwovens business area

serves customers in the food packag-

ing, medical, wiping, wallcover, auto-

motive, and technical nonwoven goods

sectors. The product line teams operate

globally and the business runs 15 pro-

duction lines. In 2004, the business area

completed two expansions in North

America by starting a new production

line in Windsor Locks and by acquiring

Green Bay Nonwovens. The new line

in South Korea is used for both fi ltra-

tion materials and nonwoven fabrics

production.