Show-Me Guide - Home | UnitedHealthcare Community … educational resource developed and published...

28

An educational resource developed and published by UnitedHealth Group Introduction to Part D: Medicare’s New Prescription Drug Coverage Show-Me Guide

Transcript of Show-Me Guide - Home | UnitedHealthcare Community … educational resource developed and published...

An educational resourcedeveloped and published by

UnitedHealth Group

Introduction to Part D:Medicare’s New Prescription Drug Coverage

Show-Me Guide

100-D4111 6/05

7482 Covers04 5/20/05 4:13 PM Page i

Contents

What are the big ideas? 2

Is a Part D plan for me? 4

What to do 5

How Part D plans will share costs 6

A sample plan 7

Examples 8

What is a formulary? 10

Help for people with lower incomes 12

Next steps

What’s your current coverage? 13

What are my choices? 14

What to do and when to do it 16

Frequently asked questions 18

Glossary 21

Not sure what some of the words mean?You may not be familiar with some words usedin this book, like “formulary,” or “deductible.” To help you, there’s a Glossary that explainsthe meaning of some of these words.cSee Glossary, page 21

7482 Covers04 5/20/05 4:13 PM Page ii

You’ve probably heard about Medicare’s new prescription drug

coverage. It’s sometimes called Medicare Part D, and it starts

January 1, 2006.

If you’re like most people, you know the cost of prescription drugs has been

rising. The U.S. Congress developed Part D to help Medicare participants

with the cost of their prescription drugs. It will offer most people who are

eligible for Medicare a significant opportunity to save. Some may say it’s not

a perfect solution, but others believe it’s a good start toward affordable

drugs.

The Part D prescription drug coverage will work differently from Medicare

Part A and Part B. To get the coverage, you’ll choose a plan from a private

company. Each plan may be a little different.

If you already have prescription drug coverage, you’ll want to compare the

plan you have now with the new plans that are being offered under Part D.

If you don’t have coverage now, it’s important for you to look at Part D

plans.

This guide is an introduction to how Part D plans will work. It explains the

decisions you’ll need to make in the next few months, and offers some advice

on what you should do next. It is not intended to help you choose a specific

plan right now. Under the timeline set by the federal government, you will

receive detailed information about plans available in your area this fall.

Let’s get started.

© 2005 United HealthCare Services, Inc. 1

If you only have time for a quick introduction to Part D prescription drug

plans, read this list. These are the big ideasyou need to know. Later, if you want, youcan dig deeper into these topics.

1Open to all people with Medicare Part D plans are open to everyone who’s eligible for Medicare in the U.S. and U.S. territories. Generally, that means people whoare 65 years old or older, and some youngerpeople with certain disabilities. You cannot be denied coverage for health reasons.Participation is voluntary. You get to decide if you want to enroll or not. If you haveMedicare and Medicaid, you will be enrolledautomatically, so there is no lapse in yourMedicaid prescription drug coverage. The firstenrollment period starts November 15, 2005,for coverage beginning January 1, 2006. Therewill be annual enrollment periods from then on.If you decide to join later, your monthlypremiums may be higher because there’s an additional fee for late enrollment.

2Pay to participateParticipation has a cost and you will pay aportion. However, much of the cost is paid bythe government. Typically, the government paysabout 75 percent of the enrollment costs of theplan. You pay the rest.

What are the big ideas?Top 10 things to know about Part D plans

2 © 2005 United HealthCare Services, Inc.

3Safety net and peace of mindAll of the Part D plans are private insuranceplans. Most participants will pay monthlypremiums. That premium buys you the peace ofmind of knowing that if your drug costs becomevery high, you will be protected.

4Discounted prices If you join a Part D plan, and use the plan’snetwork pharmacies, you’ll have access todiscounted prices. Plans will negotiate lowerprices with drug companies and pass thosesavings along to you. So when you pay fordrugs within the plan, you’ll have access todiscounted prices even when you areresponsible for 100 percent of the payment.

5Choices in plansYou’ll have choices in plans. All plans will berun by private companies. Companies willrelease details of their plans after October 1,2005. Although all plans must meet thegovernment’s requirements, there will bedifferences between plans, including whatdrugs are covered and what pharmacies youcan use. Some plans may offer mail-orderservice. You will want to see which one is bestfor you. You’ll be able to change plans once ayear.

© 2005 United HealthCare Services, Inc. 3

6Two kinds of plansPlans will come in two basic types. The mostsimple is a prescription drug plan (sometimescalled a PDP), which covers only drugs and canbe used with your traditional Medicare and/or a Medicare supplement plan. The other typecombines a prescription drug plan with aMedicare Advantage plan that includes medicalcoverage for doctor visits and hospitalexpenses. This kind of plan is called aMedicare Advantage plus Prescription Drug, or MA-PD.

7Enroll late, pay moreYou can choose to enroll beginning November15. Just like other types of insurance plans,the longer you wait, the higher your premiummay be. If you are eligible, and don’t sign up bythe end of the initial enrollment period, whichends on May 15, 2006, you may pay more ifyou sign up later. The late enrollment fee isapproximately one percent of your premium foreach month you delay, and you’ll pay it for aslong as you stay in a Part D plan. If you’re latebecause you were participating in a qualifiedprescription drug plan, such as a plan fromyour former employer, the fees may not apply to you.

8Choose drugs from a formularyEach Part D drug plan will have a government-approved list of drugs it covers—called aformulary, or a preferred-drug list. Theformulary may vary from plan to plan, but youand your doctor will have choices. Before youchoose a plan, you’ll probably want to compareplan formularies to see which one fits yourneeds best. cSee What is a formulary? on page 10.

9No free drugsDon’t expect free drugs. For each prescription, you’ll pay a portion of the cost. The plan willhelp you with some of the costs. How much you pay and how much the plan pays varies. cSee A sample plan, page 7 for an example of how cost sharing will work in a typical plan.

10Extra help for people who need itPeople with lower incomes get extra help.Premiums may be reduced or eliminated, andother payments may be less. cSee Help for people with lower incomes, page 12.

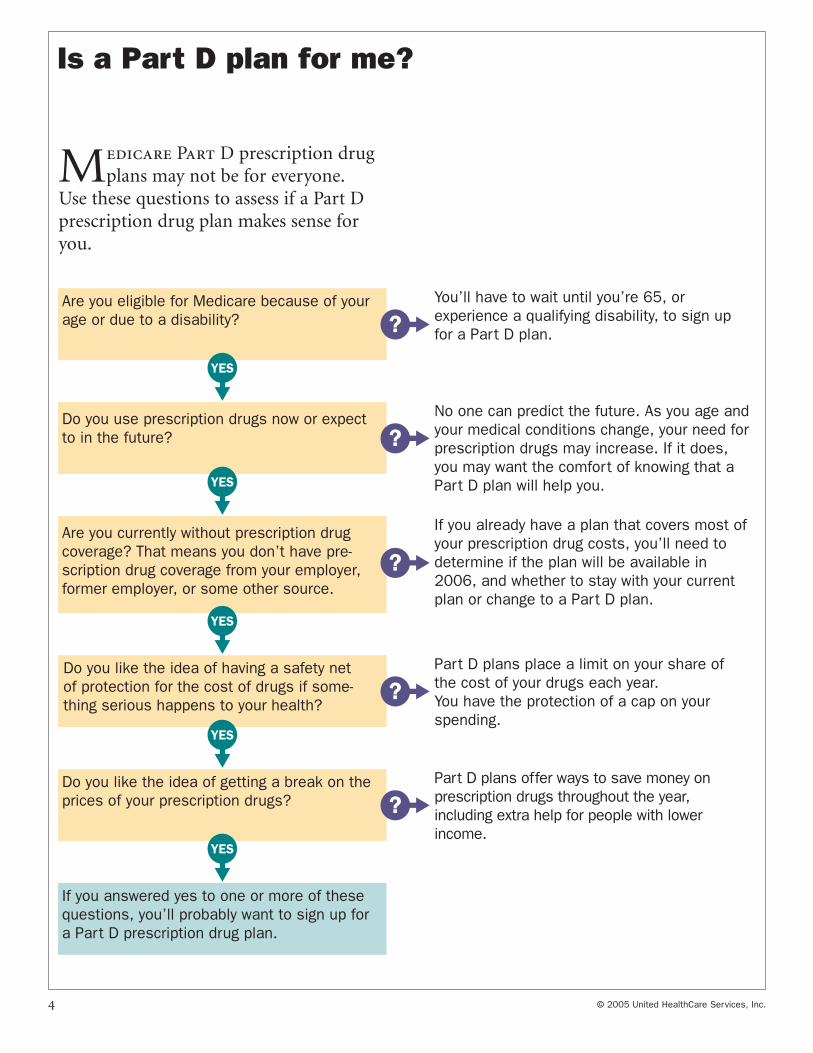

Is a Part D plan for me?

4 © 2005 United HealthCare Services, Inc.

Medicare Part D prescription drugplans may not be for everyone.

Use these questions to assess if a Part D prescription drug plan makes sense foryou.

You’ll have to wait until you’re 65, or experience a qualifying disability, to sign up for a Part D plan.

Are you eligible for Medicare because of your age or due to a disability?

YES

?

No one can predict the future. As you age and your medical conditions change, your need for prescription drugs may increase. If it does, you may want the comfort of knowing that a Part D plan will help you.

Do you use prescription drugs now or expect to in the future?

YES

?

If you already have a plan that covers most of your prescription drug costs, you’ll need to determine if the plan will be available in 2006, and whether to stay with your current plan or change to a Part D plan.

Are you currently without prescription drug coverage? That means you don’t have pre-scription drug coverage from your employer, former employer, or some other source.

YES

?

Part D plans place a limit on your share of the cost of your drugs each year. You have the protection of a cap on your spending.

Do you like the idea of having a safety net of protection for the cost of drugs if some-thing serious happens to your health?

YES

?

Part D plans offer ways to save money on prescription drugs throughout the year, including extra help for people with lower income.

Do you like the idea of getting a break on the prices of your prescription drugs?

YES

?

If you answered yes to one or more of these questions, you’ll probably want to sign up for a Part D prescription drug plan.

Get ready. You won’t be able to finish your decision-making process until this fall, when private companies release the details of theplans they’re offering. But you’ll have a headstart if you learn about Part D plans now.

Read this book carefully. It’s a good way to get the big picture. It explains the “big ideas”behind Part D prescription drug coverage, and it explains how the insurance plans willwork. If you have prescription drug coveragenow, it tells you a little about what will happento that coverage and what your choices will be.

Figure out what kind of health care coverageyou have now, and whether it will be availablein 2006. The choices you have for prescriptiondrug coverage will partly depend on what kindof health care coverage you have today. cSee page 13 for help in identifying your current coverage.

Collect current information. In the fall of 2005,collect information you will need to help in making your decision. cSee page 16 for somesuggestions about what you’ll need. And if youreceive any letters from your former employeror insurance plan about your current prescrip-tion drug coverage, be sure to save them.

© 2005 United HealthCare Services, Inc. 5

What to do

Part D prescription drug coverage is a new program, so you’ll probably see

and hear a lot about it in the comingmonths. One important thing to know is

that you’ll have some choices to make. Andbefore you decide what’s best for you, you’llprobably want to do some comparisonshopping.

Compare choices. When details of specific PartD plans are available, you’ll want to compareyour choices before you decide what’s best foryou. If you have prescription drug coveragenow, you’ll want to compare it to the coverageavailable in a Part D plan. And if you don’t havecoverage now, it’s still up to you to decide whatis best for you.

Decide what’s right for you. This book describessome of the general features of Part D pre-scription drug coverage. When you add thisinformation to the information about specificplans, you’ll be able to make your choice.

Important datesOctober 1, 2005 First day for private companies to releasedetails of their individual plans.

November 15, 2005 First day you can enroll in an individual Part Dprescription drug plan.

January 1, 2006First day you can use your Part D prescriptiondrug coverage (if you enrolled prior toDecember 31, 2005).

May 15, 2006If you’re eligible for Medicare, last day you canenroll in a Part D prescription drug plan withouta late enrollment fee, unless you qualify for anexception.cSee page 16.

6 © 2005 United HealthCare Services, Inc.

Like all insurance plans, Part D plansspread the cost of coverage across

everyone who joins the plan. Part D plansmay use four types of cost sharing. Howmuch you pay will depend on how many

How Part D plans will share costs

drugs you use during the year. Here is howthe cost-sharing will work in the standardPart D plan. The details of individual plansmay vary.

Premiums are the monthly chargesyou pay to participate in the plan.For most plans, your premium pay-ments will be about $37 per month(about $445 per year). In addition,the government contributes about$1,600 per year towards the cost ofyour premium. In future years, costsmay go up. For your convenience,you can have your premiums deduct-ed automatically from your monthlySocial Security check or you can bebilled by the plan.

1Deductible is the term for theamount you pay before your insur-ance starts. In the standardMedicare plan, Step 1 ends whenthe total you’ve paid for eligibledrugs reaches $250.

drugs reaches $250.

3Coverage gap describes when theplan makes no contribution to drugcosts and you must pay 100 percentfor drugs out of your pocket until youreach a pre-set maximum. You’llhear some people call this step “thedoughnut hole,” or “gap.” You’ll stillhave access to discounts on theprice of your drugs.

2Co-insurance is the term for splittingcosts on a percentage basis. Forexample, in Step 2 of the standardplan designed by Congress, you pay 25 percent of the drug cost andthe plan pays 75 percent until thecombined total reaches $2,000.Some plans may have flat co-paysfor each prescription instead of apercentage.

4Catastrophic coverage applies whenyour drug costs are very high. Itbegins after you’ve paid $3,600 outof your own pocket for drugs in ayear. In this step the plan pays mostcosts with no upper limit. You pay asmall portion, such as five percent,or a small flat amount for each pre-scription.

4

FE

DE

RA

L R

ESE

RV

E N

OT

E

D0

73

95

98

3A

D0

73

95

98

3A

FE

DE

RA

L R

ESE

RV

E N

OT

E

D0

73

95

98

3A

D0

73

95

98

3A

FE

DE

RA

L R

ESE

RV

E N

OT

E

D0

73

95

98

3A

D0

73

95

98

3A

2

You pay 25%Plan pays 75%

F

D 0 7 3 9

FEDERAL RESERVE NOTE

5 9 8 3 A

D 0 7 3 9 5 9 8 3 A

3

1PREMIUM

APRILMARCH

FEBRUARYJANUARY

© 2005 United HealthCare Services, Inc. 7

A sample plan

This is the standard plan passed byCongress. Individual plans offered by

private companies may vary. Details will bereleased after October 1, 2005. Not all planswill include all of the features described

below. As the total amount you spend onprescription drugs grows during the year,you will move through some or all the foursteps of coverage. Here’s an example of howcosts would be shared at each step.

43

12

STEP 3*You pay all costs up to$2,850Plan pays$0Receive drugs worth$2,850

STEP 4You pay very little,approximately 5%Plan pays 95%Receive drugs worthUnlimited to end of the calendar year

STEP 2You pay co-insurance up to$500Plan pays up to$1,500Receive drugs worth$2,000

STEP 1You pay your deductible$250Plan pays$0Receive drugs worth$250

STARTYou pay about$37 per month premium(about $445 annually) to participate in the plan

PREMIUM

F

D 0 7 3 9

FEDERAL RESERVE NOTE

D 0 7 3 9 5 9 8 3 A

D 0 7 3 9 5 9 8 3 A

FEDERAL RESERVE NOTE

D 0 7 3 9 5 9 8 3 A

D 0 7 3 9 5 9 8 3 A

FEDERAL RESERVE NOTE

9 5 9 8 3 A

D 0 7 3 9 5 9 8 3 A

FEDERAL RESERVE NOTE

D 0 7 3 9 5 9 8 3 A

D 0 7 3 9 5 9 8 3 A

Plan pays 95%You pay 5%

Plan pays 0%You pay 100%

Plan pays 75%You pay 25%

Plan pays 0%You pay 100%

*Total costs at the end of Step 3 are $3,600 not counting your premium ($250 + $500 + $2,850). Total value of drugs received is $5,100 ($250 + $2,000 + $2,850).

Catastrophic

Gap

Co-insurance

Deductible

During Step 4 the plancomes to your rescue and pays approximately 95percent of all eligible drugcosts until the end of thecalendar year. No limit. Youpay whichever is greater—five percent of the cost ofthe prescription, or $2 foreach prescription of ageneric drug and $5 foreach brand drug.

A person who takes very few drugsmay not move beyond Step 1. Someone

who takes several drugs for chronic condi-tions, or who has a major illness during the year, may easily reach Step 4. Theseexamples are based on the standard Part Dplan on the previous page.

Amounts shown are for one person. Ifyou’re married, you’ll each need your ownplan.

If you use a lot of drugs, you’ll save a lotof money. But Part D plans offer anotherbenefit that’s hard to calculate in a simplestudy of savings. How much is it worth tohave a safety net that picks up almost allthe costs if you develop a serious medicalcondition that pushes your drug costs tothe catastrophic level?

Examples

8 © 2005 United HealthCare Services, Inc.

JeromeJerome, age 45, has diabetes and is disabled. He spends more than $950 per month on prescrip-tion drugs. Part D prescription drug coverage is amajor financial benefit to him.

Space

Annual drug costs $11,500Total out-of-pocket spending with Part D $4,365

Annual premium $445Step 1 deductible $250Step 2 co-insurance (25%) $500Step 3 coverage gap $2,850Step 4 catastrophic coverage (5%) $320

Savings $7,135

AgnesAgnes, age 67, has had a major illness this year.Her drug spending has averaged more than $700per month for nine prescriptions. With a Part D plan,Agnes saves a lot of money.

Space

Annual drug costs $8,800Total out-of-pocket spending with Part D $4,230

Annual premium $445Step 1 deductible $250Step 2 co-insurance (25%) $500Step 3 coverage gap $2,850Step 4 catastrophic coverage (5%) $185

Savings $4,570

43

21

PREMIUM

43

21

PREMIUM

More savingsMost drug costs paid under Part D plans arediscounted prices negotiated by the privatecompanies with drug companies. Thoseadditional savings are not reflected in thesecalculations. Discounts could be as much as 5 to 40 percent.

© 2005 United HealthCare Services, Inc. 9

Examplescontinued

CarlosCarlos, age 77, has several chronic conditions,including asthma. He spends nearly $400 permonth for seven prescriptions. Carlos saves a signif-icant amount with a Part D plan, even though hepays all of his own costs in the coverage gap.

Space

Annual drug costs $4,570Total out-of-pocket spending with Part D $3,515

Annual premium $445Step 1 deductible $250Step 2 co-insurance (25%) $500Step 3 coverage gap $2,320Step 4 catastrophic coverage $0

Savings $1,055

WilliamWilliam, age 88, has high blood pressure and cholesterol problems. He spends less than $200per month for prescriptions. With a Part D plan,William reaches the Step 2 co-insurance phase, butstill saves money.

Space

Annual drug costs $2,250Total out-of-pocket spending with Part D $1,195

Annual premium $445Step 1 deductible $250Step 2 co-insurance (25%) $500Step 3 coverage gap $0Step 4 catastrophic coverage $0

Savings $1,055

21

PREMIUM

32

1PREMIUM

HelenHelen, age 71, is generally in good health. Shespends less than $100 each month for two prescriptions for osteoporosis drugs. With a Part Dplan, Helen saves a modest amount but she alsohas the comfort of knowing drugs will be covered ifshe is ill.

Space

Annual drug costs $870Total out-of-pocket spending with Part D $850

Annual premium $445Step 1 deductible $250Step 2 co-insurance (25%) $155Step 3 coverage gap $0Step 4 catastrophic coverage $0

Savings $20

LouiseLouise, age 73, spends about $300 each month onprescription drugs. Louise enrolled in a MedicareAdvantage plan that includes Part D prescription drugcoverage. Since her health plan has no monthly premi-um, she saves significantly on her prescription drugs.

Space

Annual drug costs $3,500Total out-of-pocket spending with Part D $2,000

Annual premium $0Step 1 deductible $250Step 2 co-insurance (25%) $500Step 3 coverage gap $1,250

Step 4 catastrophic coverage $0Savings $1,500

32

1PREMIUM

21

PREMIUM

10 © 2005 United HealthCare Services, Inc.

Aformulary is a list of the drugs thata plan covers. Each plan has its own

formulary. All formularies are similarbecause they’re based on federal guidelines,but they may not include exactly the samedrugs. The differences may be important toyou. You’ll want to compare formularieswhen you select a plan. You’ll be able to seea plan’s specific formulary after October 1,2005.

1 Different drugs, different pricesSome plans may offer abroader formulary thanother plans. Plans may alsohave different cost sharingfor a particular drug.

What’s this mean to me? Safe and effective drugs willalways be available. Youand your doctor will alwayshave a choice.

3 Discounted pricesA plan will be able to negoti-ate special prices with drugcompanies and these sav-ings will be passed along toyou.

What’s this mean to me? Prices you pay as a plan member will probably belower than the prices youwould pay on your own.Your dollars go further.

2 Additional choicesPlan formularies willinclude both generic andbrand name drugs.Generic drugs are lower-cost alternatives to brandname drugs. You can savemoney by switching to thegeneric version.

What’s this mean to me? Stretch your dollars furtherby choosing generic drugswhenever you can.

4 Drug advancesFormularies probably won’tchange very often, butwhen research reveals newtreatments, or new genericdrugs are launched, thatmay trigger changes toplan formularies. Your planwill tell you of changes soyou and your doctor canconsider your options.

What’s this mean to me? As formularies evolve, youmay occasionally need tohave your doctor adjustyour prescriptions to ensurethey are covered. Your plan’scurrent list will usually beavailable on a Web site orby mail.

What is a formulary?

All FDA-approved drugs

Drugs in thesame group

treat thesame conditions.

Discount pricesapply to

most drugsin the formulary.

In the future,improved drugs

will lead toformulary updates.

Formulariesgroup drugs

by whatthe drugs do.

P L A N ’ S F O R M U L A R Y

10 things to know about formularies

Other namesA formulary may also bereferred to as a preferreddrug list (PDL), or a selectdrug list.

© 2005 United HealthCare Services, Inc. 11

What is a formulary?continued

5 Match your drugs to the formularyWhen choosing a plan,compare the drugs on theplan’s formulary with thedrugs you currently take.Discuss the drug optionswith your doctor.

What’s this mean to me? If you take multiple drugs,you probably won’t findevery one of them on a sin-gle formulary. If a drug youtake isn’t on the formulary,talk to your doctor aboutupdating your prescriptionto a drug on the list.

6 ExceptionsFormularies are designedto meet the needs of mostpeople. No formulary canmeet everyone’s needs. Aformulary-exceptionsprocess will be available ifyour doctor determines thatno substitute drug worksfor you.

What’s this mean to me? You probably won’t bedenied coverage for a drugin the rare cases where noother drug can be used.

8 PharmaciesPlans will usually requireparticipants to get theirdrugs from specific pharm-acies within a network ofpharmacies that haveagreed to special low prices.

What’s this mean to me? Most pharmacy networksinclude many locations, butcheck to see what local phar-macies are included beforeyou select a plan.

10 Drug safetyA plan will have systemsset up to alert your phar-macist of potential interac-tions between different pre-scription drugs you may be taking. When you obtainyour drugs through yourplan, your pharmacist willget these messages whilehe or she is filling your pre-scription, even if you filledother prescriptions atanother network pharmacy.

What’s this mean to me? You’ll get help to avoid drug interactions that could decrease medication effectiveness or make you ill.

9 Drugs at lower costIf needed, your doctor canhelp you switch your pre-scriptions to drugs that arecovered by your plan’s for-mulary. Your doctor can alsohelp you lower costs byswitching your prescriptionsto drugs with lower co-pay-ments or to lower-costgenerics.

What’s this mean to me? You will pay less money foryour drugs.

7 Outside the planFederal law has excludedsome drugs from the list. cSee page 19.

What’s this mean to me? For drugs that are not covered by any plan, youalways have the option topay the full cost out of yourown pocket. Whatever youspend in this way doesn’tcount toward any deductibleor out-of-pocket costs.

MyPrescriptions

P L A N ’ S F O R M U L A R Y

Substitution drugis on formulary

Drug is on formularyYES

YESNO

DRUG SAFETYALERT

Help is available for people withlower incomes and few savings or

other assets. If you think you can’t afford aPart D plan, find out if you qualify for help.

What kind of help?Depending on the level of need:• Your premiums may be reduced or eliminated.• Your deductibles may be reduced or

eliminated.• Your co-insurance and co-pay amounts may

be reduced.• Your coverage gap may be eliminated.

*Example of 2005 figures; figures will also vary in Alaska andHawaii.

Couples

Singles

For coupleshelp may start when income is less than $19,245*

For singleshelp may start when income is less than $14,355*

Help for people with lower incomes

12 © 2005 United HealthCare Services, Inc.

Who’s eligible?Eligibility depends on your income (money youreceive from retirement benefits or other moneythat you would report for tax purposes). Insome cases, the government also reviews yourassets (for example, property besides yourhouse that you own). cSee Glossary, page 21,for a definition of assets.

How to applyYou will need to fill out an application form toapply for assistance. You may have receivedthis form in the mail, or you may contact yourlocal Social Security Administration office.

ExampleAndrew is a single person with an annualincome of $8,700. At this income level, the gov-ernment does not consider assets. Andrew iseligible for the maximum amount of help. Hereis what he would pay for a Part D plan.*

Premium Pay no premium

Step 1 Deductible Pay no deductible, and move directly to Step 2

Step 2 Co-insurance Pay $1 (generic) or $3(brand) per prescription

Step 3 Coverage gap No coverage gap, continue paying at Step 2 levels

Step 4 Catastrophic Pay nothingcoverage

*Low-income programs will vary in the U.S. territories.

© 2005 United HealthCare Services, Inc. 13

Next stepsWhat’s your current coverage?

Your choices for Part D plans dependon what kind of health care coverage

you have now. Not sure what type of cover-age you have? Think about what kind ofidentification card you show to your doctoror hospital when you need care.

If you only use your Medicarecard issued by the federal government, you probably havetraditional Medicare (Part Aand B) coverage.

If you use your Medicare card,plus a second card that paysfor expenses Medicare doesn’tcover, then you probably havea Medicare supplement policywhich you purchased on yourown, or which may be providedthrough your former employer.

If you use a different card from your Medicare card foryour costs, then you probablyhave a Medicare Advantageplan which you purchased onyour own, or which is providedby your former employer.

Drug discount cards are not the same as Part D prescription drugplans. They are not insurance plans. Medicare-approved discount drugcards (which have the Medicare-approved seal on them) will end whenyou sign up for a Part D plan, or onMay 15, 2006, whichever is earlier.

Other discount drug cards (non-Medicare approved) may continue toexist. If you join a Part D plan, youcan keep your non-Medicare-approveddiscount drug card. If you stay with a discount drug card only, you’ll haveto pay a late-enrollment fee if you join a Part D plan later. cSee page 15.

If you still have questionsabout the type of insur-ance you have, call thecustomer service numberon your card.

Once you know what type of currenthealth care coverage you have, it’s easier

to determine what your choices are.

14 © 2005 United HealthCare Services, Inc.

Next stepsWhat are my choices?

You can enroll in a stand-alone Part D prescription drug plan (PDP)that only covers drugs. Or you can enroll in a Medicare Advantageplan with prescription drugs (MA-PD) that combines coverage for doctor and hospital care with a prescription drug plan. MedicareAdvantage plans are not available in every part of the country.

Traditional Medicareonly(Parts A & B)

In 2006, all Medicare Advantage plans will offer Part D prescriptiondrug coverage. Some may also offer plans without drug coverage.Your plan will tell you about changes in your coverage and what yourchoices are. If you choose to stay in a Medicare Advantage plan thatdoesn’t offer drug coverage, you will not be allowed to enroll in astand-alone Part D plan.

Medicare Advantageplan (with or withoutdrug coverage)

You can get Part D prescription drug coverage by enrolling in a stand-alone Part D drug plan to complement your Medicare and Medicaresupplement policy.

Traditional Medicare plus a Medicare supplement policy(for example, plans Athrough G, no drugs)

You must decide whether you want to keep your supplemental drug coverage or enroll in a Part D plan. If you enroll in a Part D plan, youmust change your supplement policy to exclude drugs. You cannothave both a supplemental plan with drug coverage and a Part D plan.If you decide to stay in a plan with drug coverage and later decide tojoin a Part D plan, you’ll face a late enrollment fee.

Traditional Medicare plus a Medicare sup-plement policy (for example, plan H, I,or J, with drugs)

What you have now What your choices are

© 2005 United HealthCare Services, Inc. 15

Next steps—What are my choices?continued

Late enrollment feeIf you choose not to enroll in a Part D plan now and later change yourmind, you may have to pay higher premiums because there is a lateenrollment fee of about one percent per month, or 12 percent per year.

Example: Edward is 68 years old and has no prescription drug cover-age. He doesn’t join a Part D plan in 2006. Three years later, hedecides to join a plan. Because of the late enrollment fee, Edward’spremiums will be about 36 percent higher (1 percent per month x 36months) and they will remain higher for as long as he stays in a Part Dplan. Instead of paying about $450 for premiums, Edward will payaround $600 a year ($450 plus 36 percent).

In 2006, your drug coverage will be provided by a Part D plan. Youcan choose your own Part D plan. If you don’t choose a plan andenroll by December 31, 2005, you’ll be assigned to a plan at ran-dom. You’ll have an opportunity to switch to another plan. Your cur-rent drug coverage may change. Contact your state Medicaid orMedical Assistance office with questions.

Medicaid

Your state will determine if you will receive additional help with yourcosts for a Part D plan. If you think that you might qualify for help,contact your local Social Security office or your state Medicaid orMedical Assistance office to determine if you are eligible.

State pharmacyassistance program

Many employers who provide drug benefits may continue their drugcoverage. Others may choose to help employees or retirees whoenroll in a Part D plan by paying some of the costs. Before the endof 2005, ask your former employer what you can expect. If your for-mer employer continues a plan that meets or exceeds the govern-ment standards, you won’t have to worry about a late enrollment fee if you decide to join a Part D plan in the future.

Employer drugcoverage

What you have now What your choices are

Now that you know the basics about new Part D prescription drug cover-

age, it’s clear that you’ll need to do somepreparation before you choose a plan. Hereare some suggestions about what to do andwhen.

Important dates

October 1, 2005Private companies can begin to release detailsabout what they have to offer, costs, and thespecific drugs in their formularies.

November 15, 2005First day you can enroll in a Part D plan.

January 1, 2006First day you can use your Part D prescriptiondrug coverage (if you enrolled prior to December31, 2005).

May 15, 2006If you are eligible for Medicare, this is the lastday you can enroll in a Part D prescription drugplan without a late enrollment fee, unless youqualify for an exception. After this date, youmust wait until the next open-enrollment period(November 15–December 31) to enroll, unlessyou have special circumstances.

Next stepsWhat to do and when to do it

16 © 2005 United HealthCare Services, Inc.

What to do now

1 Apply for financial help if you need it. If you think you can’t afford a Part D plan, or if you’re already having trouble paying for yourdrugs, take advantage of programs that are available to help you. Based on your income andassets, you may be eligible for help that lets youpay a much smaller share of the costs than otherparticipants, or pay nothing at all. cSee page 24 forresources.

The first step in qualifying for financial help is applying for help. Contact your local SocialSecurity Administration for help with this application. Make this application right away.

2 Gather information about your current healthcare and drug coverage. Make sure you know what kind of health care coverage you have now. cSee page 13. Find outwhether you currently have any prescription drugcoverage, what kind it is, and whether it will beavailable after January 1, 2006. You’ll use thisinformation to help you decide whether to keepthe plan you have, or move to a Part D plan. Callthe customer service number on your identifica-tion card for more information about the type ofcoverage you have.

3 Gather information about the drugs you use. Begin making a list of the drugs you regularly take, including their names, and your dosage (for example, 20 milligrams), how much it costseach time you refill the prescription, and howmany times a year you refill the prescription. You’llneed this list to help you compare plans later.

© 2005 United HealthCare Services, Inc. 17

Next stepscontinued

What to do next

4Gather information about the Part D plans in your area. In October, 2005, Medicare will send you the 2006edition of its annual booklet, Medicare & You.This booklet will give you information about thePart D plans available in your area. You will also be able to find information about Part D plans atwww.medicare.gov, the Medicare Web site. Youmay also receive information in the mail from private companies about their plans.

5Compare plans.Once you have information about the plans avail-able to you, compare plans. Making a simple chartcan help you compare one plan to another. Hereare some of the items you may want to compare.

• Monthly premium• Deductible• What percentage you pay for co-insurance• What amount you pay for co-payments

You also will want to compare formularies to seewhether the drugs you take are covered by theplan.

And check to see where the plan’s networkpharmacies are located.

6Find out whether you have “creditable coverage.”If you are currently enrolled in a plan that offerscoverage equal to a Part D plan, you have what iscalled “creditable coverage.” If you have drug cov-erage now, ask your plan if you have “creditablecoverage.” If you do have creditable coverage, youwon’t be charged a late enrollment fee if you moveto a Part D plan after the initial enrollment period.

Why is there a late enrollment fee?Congress believes that unless you already havecreditable prescription drug coverage, Part D plansare a great way for you to get help with the cost ofprescription drugs. They crafted the rules toencourage people to enroll in the beginninginstead of waiting to join only when health prob-lems develop and drug costs rise. The late enroll-ment fee gives people a reason not to postpone thedecision to join.

Who is eligible for Medicare Part D prescriptiondrug coverage?All individuals with Medicare Part A or MedicarePart B are eligible to enroll regardless of age,income or health conditions.

Do I have to participate in a Part D plan? No, you do not have to participate. It is yourchoice. However, similar to other types ofinsurance, the longer you wait, the higher your premium will be.

How do I know if I should sign up?You will need to review your options carefully to see if a Part D plan is right for you. Part D plansare designed to provide financial savings to most people with Medicare. As insurance plans, theyprovide protection against future, unexpectedcosts. They also provide additional financial assis-tance for people with lower incomes.

Frequently asked questions

18 © 2005 United HealthCare Services, Inc.

This book is a good start, but how do I get thespecific information I need to make a decision? In October 2005, you will begin to receive specificinformation about the options available to you.First, you will receive the 2006 Medicare & Youhandbook, which will include all of the plansavailable in your area. Second, in October, 2005,the plans will begin releasing specific plan infor-mation, including plan costs, the list of covereddrugs (formulary), and the list of network pharmacies. Information will also be available atwww.medicare.gov, the Medicare Web site.

How do I find out if I qualify for help? If you have both Medicare and Medicaid, youalready qualify for low-income assistance. If youdon’t qualify for Medicaid, you may still qualify forsome assistance if your income is below $14,355*for an individual, or $19,245* for a couple. In somecases, the government will also review how manyassets you own. If you think you might qualify,contact your local Social Security Administrationoffice. You have nothing to lose by applying.

What assets will be counted to determine if I am eligible for help? The assets that will be counted include cash or anyproperty that can be converted to cash within 20days. This includes checking accounts, savingsaccounts, certificates of deposit, retirementaccounts (like IRAs or 401ks), stocks, bonds,mutual fund shares, promissory notes, mortgages,and life insurance policies. Property that is notcounted includes your primary home, burial plots,or burial agreements. Certain funds set aside forburial expenses, up to $1,500, will also not becounted. cSee Help for people with lower incomes,page 12.

*Example of 2005 figures; figures will also vary inAlaska and Hawaii.

© 2005 United HealthCare Services, Inc. 19

Frequently asked questionscontinued

Can I change Part D plans once I have enrolled? Yes, you can change your Part D plan. The oppor-tunities to switch are:Annual enrollment: Each year, you will be able tochoose a different Part D prescription drug plan orMedicare Advantage plan during an annual enroll-ment period that lasts from November 15 throughDecember 31. Coverage under the new plan willbegin the following January 1.Other exceptions: There are other limited excep-tions that may give you the right to switch plansduring a year. For example, if you move out of theservice area of your current plan, you will have anopportunity to choose another plan that servesyour new area.

How will I know if the drugs I currently take willbe covered? Each Part D plan will provide its own formularyor list of covered drugs. This information will beavailable through the plan’s Web site, customerservice center, and through marketing materials.

Who decides which drugs will be covered on aformulary? All Part D plans must meet formulary require-ments set by Medicare. The formulary will includeboth generic and brand name drugs. Each planmust use a Pharmacy and Therapeutic Committee,which includes doctors and pharmacists, to establish its formulary. This process assures youthat you’ll have access to a number of drugs,although not necessarily all drugs.

What drugs are excluded from Part D plans? The drugs that are excluded from Part D byMedicare are:1 Drugs used for anorexia, weight loss, or weight

gain2 Drugs used to promote fertility3 Drugs used for cosmetic purposes or hair

growth4 Drugs used for the symptomatic relief of cough

and colds5 Prescription vitamins and mineral products,

except prenatal vitamins and fluoride prepara-tions

6 Non-prescription drugs7 Inpatient drugs 8 Barbiturates (sleeping pills) 9 Benzodiazepines (central nervous system

depressants)

In addition, a drug cannot be covered under a Part D plan if payment for that drug is availableunder Parts A or B of Medicare, such as drugsadministered in a hospital or a physician’s office.Also, each Part D prescription drug plan may haveits own specific exclusions.

Will Part D cover drugs purchased fromCanada?No. Only drugs sold in the United States are eligible for Part D coverage.

Can premiums be deducted from Social Securitychecks? Yes, you will have the option to have the premiumdeducted from your Social Security check (just likeyour Part B premium), or you or your formeremployer can pay your premium directly to theprivate company.

What is creditable coverage? Creditable coverage is coverage, from a plan otherthan a Part D plan, that meets certain Medicarestandards. If you currently have prescription drugcoverage that is considered creditable coverage,you may keep that coverage and wait to enroll in aPart D plan. If you later decide to enroll in a PartD plan, you will not have to pay a late enrollmentfee.

Will Part D coverage only be available through aprivate company, or will I be able to get cover-age directly from Medicare, the same way that Iget Part A and Part B coverage?No, Part D coverage will not be available directlyfrom Medicare. Although you will be able to haveyour premium deducted from your Social Securitycheck, you must purchase Part D coverage from aprivate company that has been approved byMedicare to offer coverage.

I have drug coverage through the Veterans’Administration (VA). Can I continue to get myprescriptions through the VA in 2006? The introduction of Part D prescription drugplans in January 2006 will have no impact onVeterans’ Administration benefits. Medicare beneficiaries who currently have prescription drugbenefits through the VA will be able to continue toobtain their prescriptions through the VA.

If I live in the U.S. territories, will I have accessto a Medicare Part D plan?Yes, Medicare Part D plans will be available in theU.S. territories.

Frequently asked questionscontinued

20 © 2005 United HealthCare Services, Inc.

I take several different prescription drugs. Will there be help with managing all my medications?Yes, one of the advantages of Medicare Part Dplans is that there will be help managing drugs forpeople who take multiple medications, havechronic diseases, such as diabetes or heart diseaseand high drug costs. The help is designed to makesure that your medications work well together andreduces the risk of a bad reaction. You might alsohear this called medication therapy management.

© 2005 United HealthCare Services, Inc. 21

Glossary

assetsProperty you own that the government mayreview when you apply for assistance. For helpwith a Part D plan’s costs, the government countscash or any property that can be turned into cashwithin 20 days. This includes checking and savingsaccounts, certificates of deposit, IRAs and 401(k)s,stocks, bonds, and similar items. It does notinclude your primary home, or certain propertyrelated to burial expenses.

benefitAnother name for coverage.See coverage.

brand name drugs Prescription drugs that are sold under a trade-marked brand name.

catastrophic coverageA name for the step of a Part D plan in which theplan pays nearly all of your drug expenses until theend of the year, with no upper limit. In this step,you pay only a small share of your drug expenses(approximately five percent).

Centers for Medicare and Medicaid Services(CMS)The federal agency that runs the Medicare pro-gram, and works with the states to manage theMedicaid program. CMS sets standards for Part Dinsurance plans.

co-insuranceA kind of cost sharing where costs are split on apercentage basis. For example, a plan might pay 75percent and you would pay 25 percent.See cost sharing.

co-paymentA kind of cost sharing where you pay a pre-set, flatamount for each service. In a Part D plan, forexample, you might pay $10 for each prescriptionyou receive and the plan would pay the remainingcost of the drug.See cost sharing.

cost sharingA term for the way an insurance plan shares itscosts with someone. The most common types ofcost sharing are co-insurance and co-payments.See co-insurance and co-payments.

coverageThe benefits you receive from an insurance plan.In a Part D plan, the prescription drug costs thatare paid by the insurance plan are your benefits, orcoverage.

coverage gapA name for the step in a Part D plan in which youpay all of your expenses for eligible drugs, untilyou have spent $2,850. Some people call this stepthe doughnut hole.

creditable coveragePrescription drug coverage, from a plan other thana Part D plan, which meets certain Medicare standards. If you are currently enrolled in a drugplan that gives you prescription drug coverage,your plan will tell you if it meets the Medicarestandards for creditable coverage.See late enrollment fee.

deductibleIn an insurance plan, the term for an amount youpay first, before your plan starts to pay. In a Part Dplan, you may have to pay the first $250 of youreligible drug expenses for the year as yourdeductible.

doughnut hole Another name for the step in a Part D plan inwhich you pay all of your expenses for eligibledrugs, until you have spent $2,850.See coverage gap.

dual eligiblesPeople who are eligible for both Medicare andMedicaid.

eligible drugsDrugs that are covered by a prescription drugplan. In a Part D plan, eligible drugs are listed onthe plan’s formulary.See formulary.

exclusionsItems that are not covered by an insurance policy.Part D drug plans have two types of exclusions.The first type is drugs that Medicare has excludedfrom coverage under Part D, such as weight-lossdrugs. The second type is drugs that are excludedfrom a plan’s list of covered drugs, or formulary.See eligible drugs and formulary.

formularyA list of prescription drugs that are covered by aPart D plan. Drugs listed on the formulary are alsocalled eligible drugs in this book. Some people calla formulary a preferred-drug list (PDL), or a selectdrug list.

generic drugsPrescription drugs that have the same active ingre-dient formula as a brand name drug. Genericdrugs usually cost less than brand name drugs andare rated by the Food and Drug Administration(FDA) to be as safe and effective as brand namedrugs.

Glossary

22 © 2005 United HealthCare Services, Inc.

late enrollment fee Congress wants to encourage as many eligible peo-ple as possible to enroll in a Part D prescriptiondrug plan before the first enrollment period endsin May 2006, or to enroll as soon as they are eligi-ble for Medicare. To do this, it has created a lateenrollment fee to discourage putting off enroll-ment. This fee is approximately one percent ofyour premium cost per month (or 12 percent peryear) that you delay enrolling. There is no limit tothe percentage, and it lasts as long as you areenrolled in a Part D prescription drug plan. Thefee won’t apply if you move from an insuranceplan that offers creditable coverage to a Part Dprescription drug plan.See creditable coverage.

MedicaidA program that pays for medical assistance for certain individuals and families with low incomesand resources. Medicaid is jointly funded by thefederal and state governments to assist states inproviding long-term care assistance to people whomeet certain eligibility criteria.

Medicare Advantage PlansHealth plans offered by private insurance compa-nies that contract with Medicare to provideMedicare coverage. Depending on where you live,Medicare Advantage Plans may be available bothwith and without Part D plans. You may also hearMedicare Advantage Plans referred to as MedicareHealth Plans. The Medicare Advantage Plans usedto be called the Medicare+Choice plans.

© 2005 United HealthCare Services, Inc. 23

Glossary

MedicareA federal government health insurance programfor

• people age 65 and older,• people with certain disabilities, and• people of all ages with End-Stage Renal Disease

(permanent kidney failure requiring dialysis orkidney transplant).

Medicare Part D prescription drug plansInsurance plans offering prescription drug cover-age that meets the standards established byMedicare. Other names for these plans includePart D prescription drug plans, PDPs, or MA-PDs.However, not all private insurance plans offeringprescription drug coverage are Part D plans. You’llwant to pay close attention to whether a plan is aPart D plan.

Medicare supplement policyThe traditional federal Medicare insurance program doesn’t pay the total amount of medicalexpenses. Expenses that are not covered are called“gaps” in Medicare coverage. Private insurancecompanies sell insurance policies that fill some ofthese gaps and pay for some of these expenses.These policies are known as Medicare supplementpolicies.

MedigapSee Medicare supplement policy.

Medication therapy managementThe term used to describe the type of help thatpeople with multiple prescriptions, chronic diseases, and high drug costs receive to help themmanage all of their medications. The purpose ofthe help is to make sure that all of their drugswork well together.

networkThe group of doctors, hospitals, and pharmacieswho have contracts with an insurance plan to provide care to the plan’s members. You shoulduse your Part D prescription drug plan’s networkof pharmacies to save money on your drugs.

out-of-pocket costsThe amounts you pay as your share of your prescription drug costs in a Part D plan.Out-of-pocket costs include deductibles,co-insurance, and the amounts you pay in the coverage gap.

In a Part D plan, any amounts you pay, but forwhich you are later reimbursed by someone else,such as an employer’s insurance plan, do notcount as part of your out-of-pocket costs. Theout-of-pocket costs you pay for which you are notreimbursed are called your “true out-of-pocketcosts,” or “TROOP.”

When your “true out-of-pocket costs” exceed$3,600, you are eligible for the catastrophic cover-age step of a Part D plan.See catastrophic coverage.

premiumThe money you pay to have an insurance plan.In a Part D plan, this is usually a monthly fee.

RxA symbol that means “prescription drugs.”

Medicare HelplineFor help with choosing Part D prescription drugcoverage, and for questions about Medicare:1-800-MEDICARE (1-800-633-4227)TTY 1-877-486-2048

Social Security AdministrationFor help with questions about eligibility for andenrolling in Medicare, Social Security retirementbenefits, and disability benefits, and for questionsabout eligibility for help with costs of a Part Dplan:1-800-772-1213TTY 1-800-325-0778

Your health plan’s customer service centerFor questions about your existing health coverage, call the telephone number on youridentification card.

Your state’s Medical Assistance or MedicaidofficeFor questions about your state’s Medicaid program, call the Medicare Helpline (1-800-MEDICARE) and ask the operator for the telephone number for your state’s MedicalAssistance or Medicaid office.

Your state’s Health Insurance AssistanceProgram For help with questions about buying insurance,choosing a health plan, buying a Medicare supplement policy, and your rights and protec-tions under Medicare, call the Medicare Helpline(1-800-MEDICARE) and ask the operator for thetelephone number for your state’s HealthInsurance Assistance Program office.

Medicare & YouOfficial Medicare handbook for Medicare pro-grams, including Part D prescription drug plans(2006 edition available in October 2005).

AARP Web site For information about Medicare and other programs for seniors:www.aarp.org

Medicare Web site For help with choosing Part D prescription drugcoverage, and for questions about Medicare:www.medicare.gov

Resources

24 © 2005 United HealthCare Services, Inc.

Contents

What are the big ideas? 2

Is a Part D plan for me? 4

What to do 5

How Part D plans will share costs 6

A sample plan 7

Examples 8

What is a formulary? 10

Help for people with lower incomes 12

Next steps

What’s your current coverage? 13

What are my choices? 14

What to do and when to do it 16

Frequently asked questions 18

Glossary 21

Not sure what some of the words mean?You may not be familiar with some words usedin this book, like “formulary,” or “deductible.” To help you, there’s a Glossary that explainsthe meaning of some of these words.cSee Glossary, page 21

7482 Covers04 5/20/05 4:13 PM Page ii

An educational resourcedeveloped and published by

UnitedHealth Group

Introduction to Part D:Medicare’s New Prescription Drug Coverage

Show-Me Guide

100-D4111 6/05

7482 Covers04 5/20/05 4:13 PM Page i