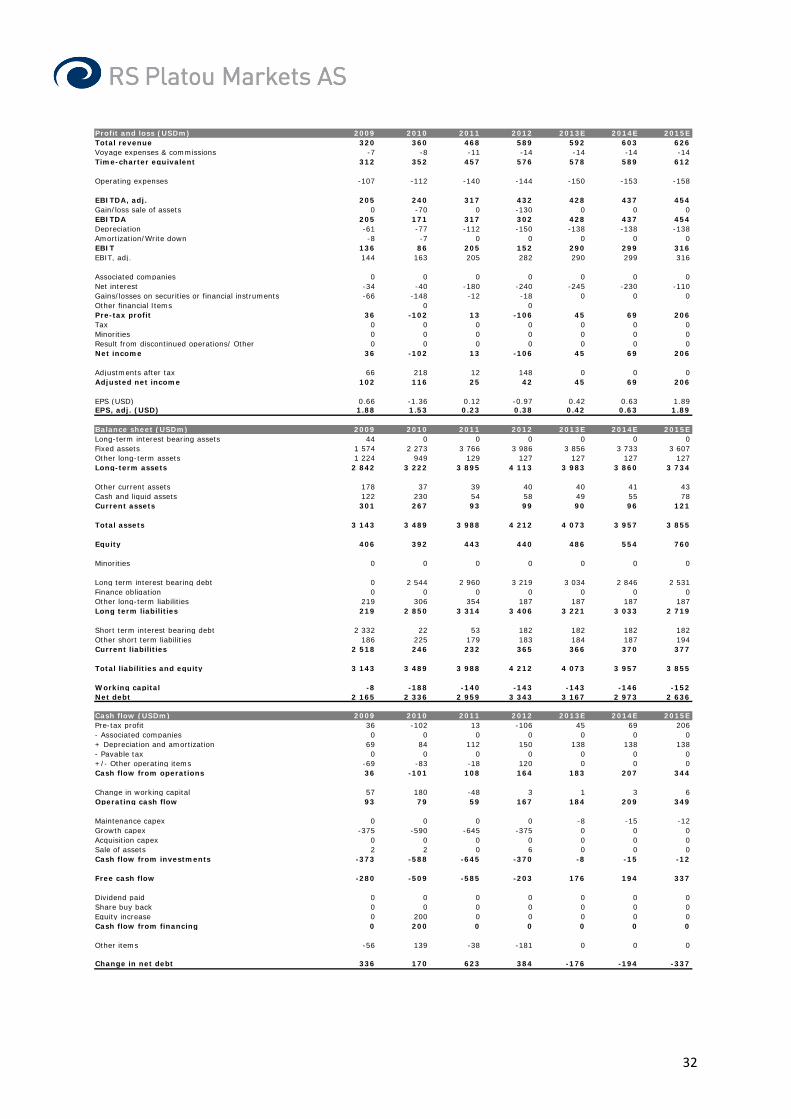

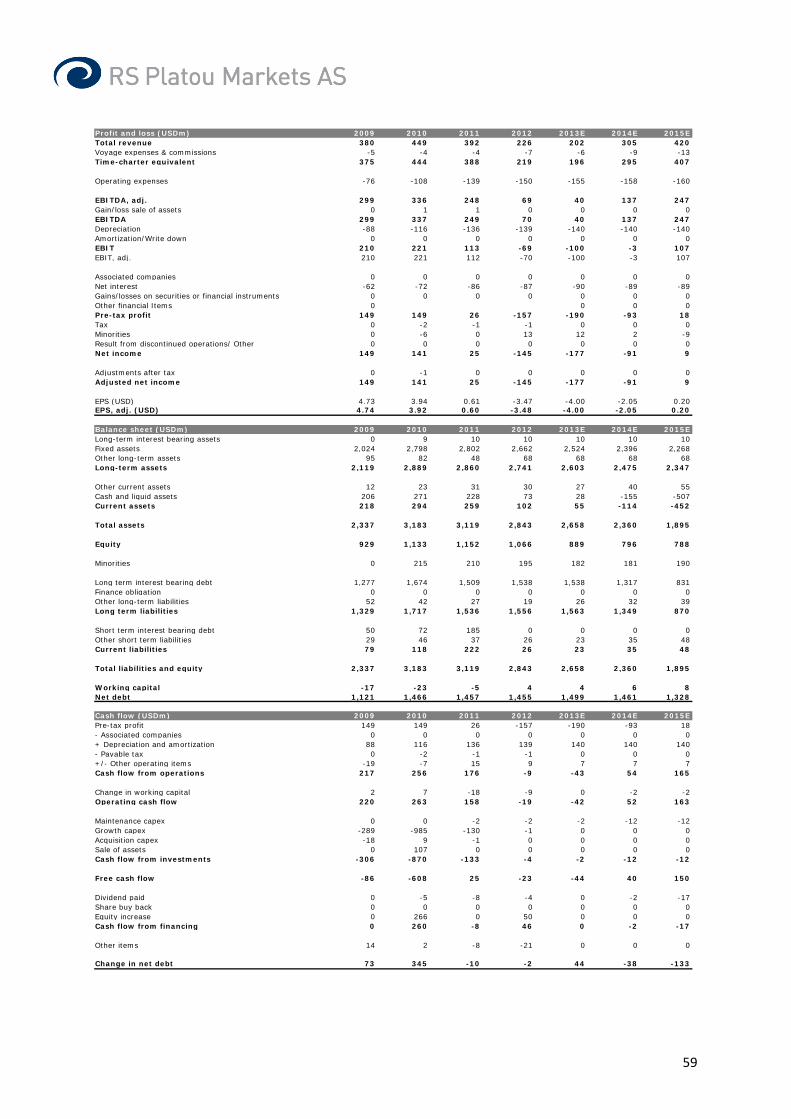

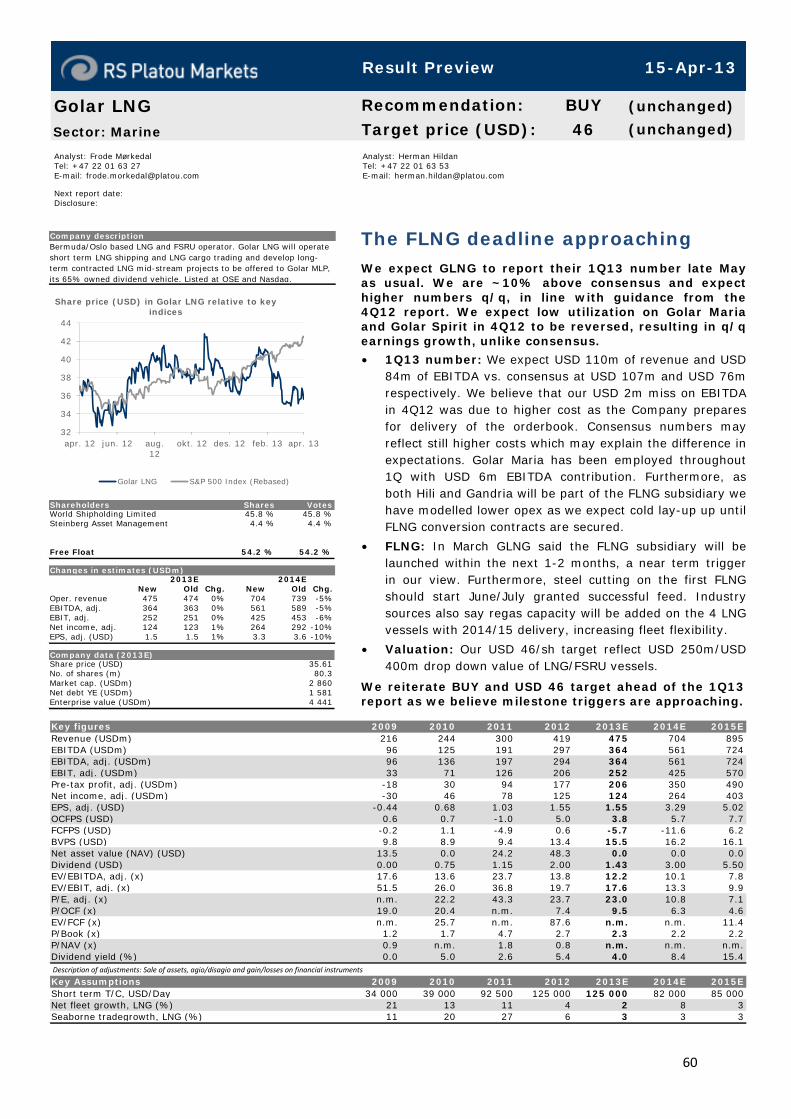

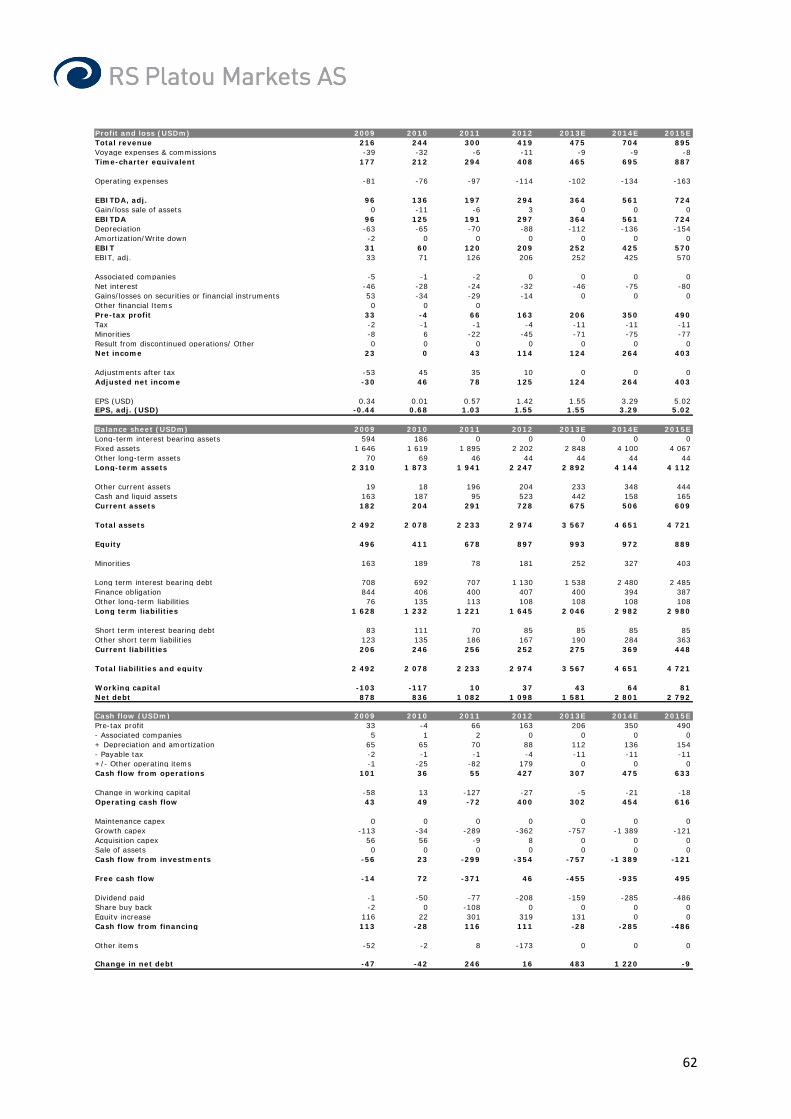

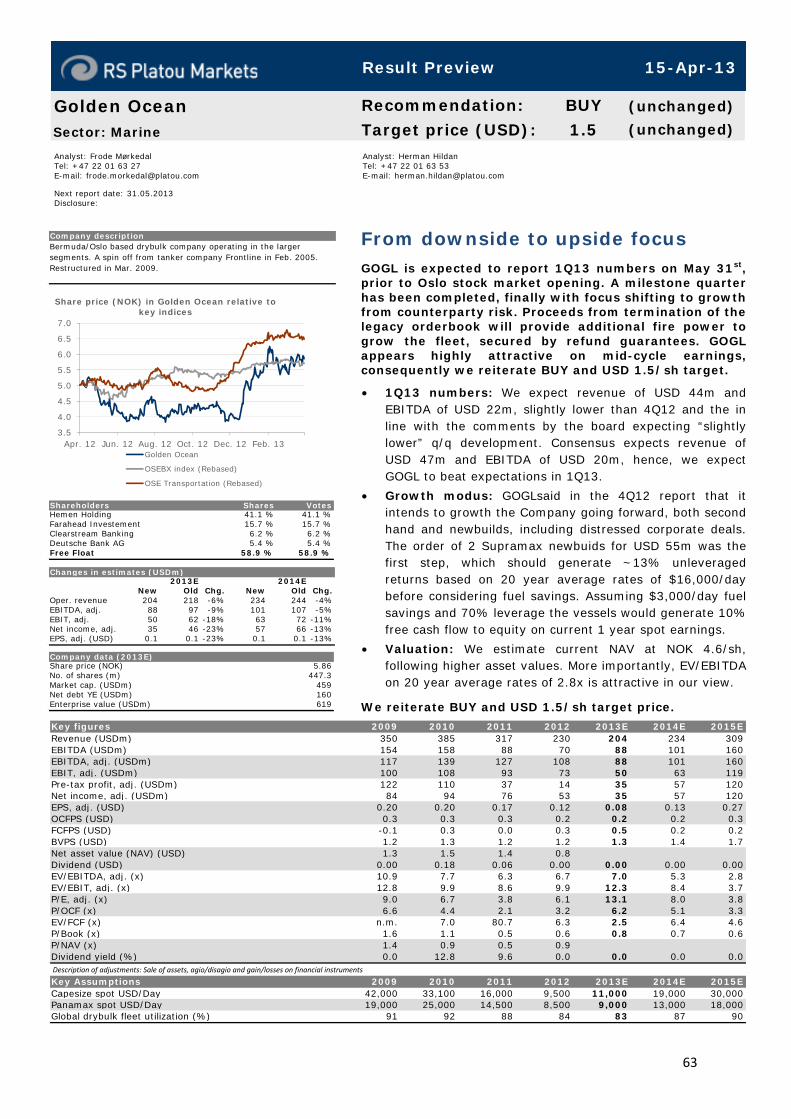

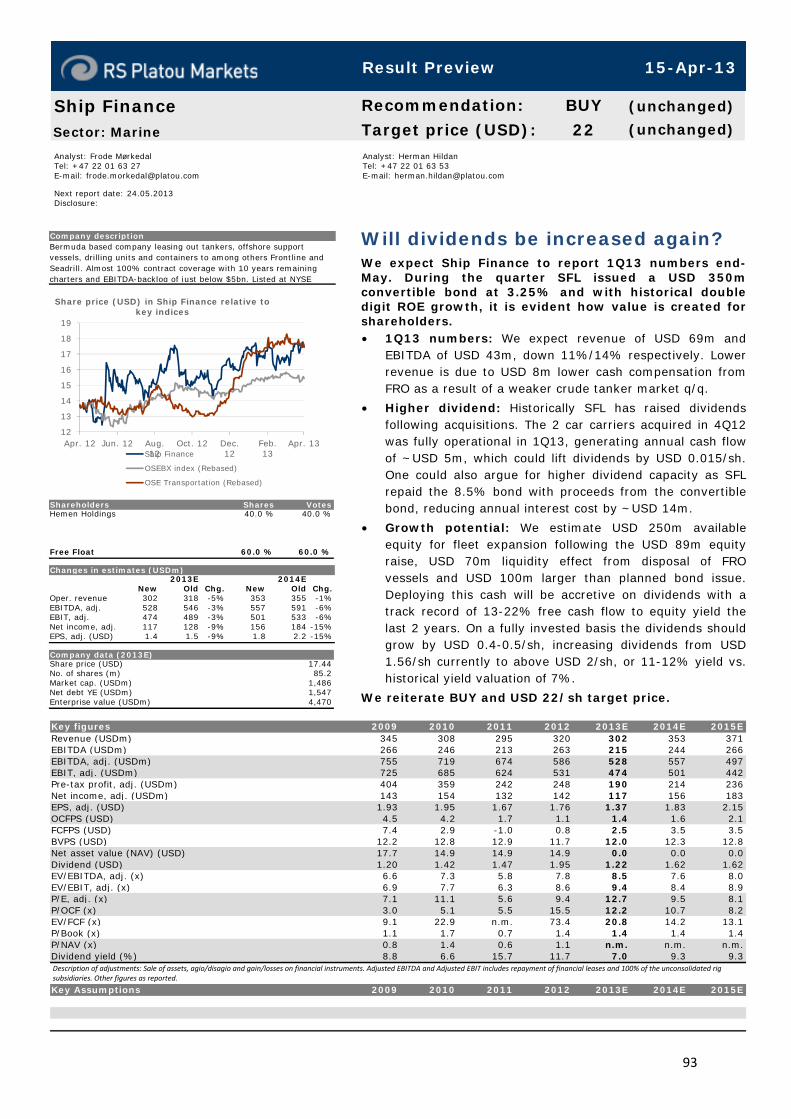

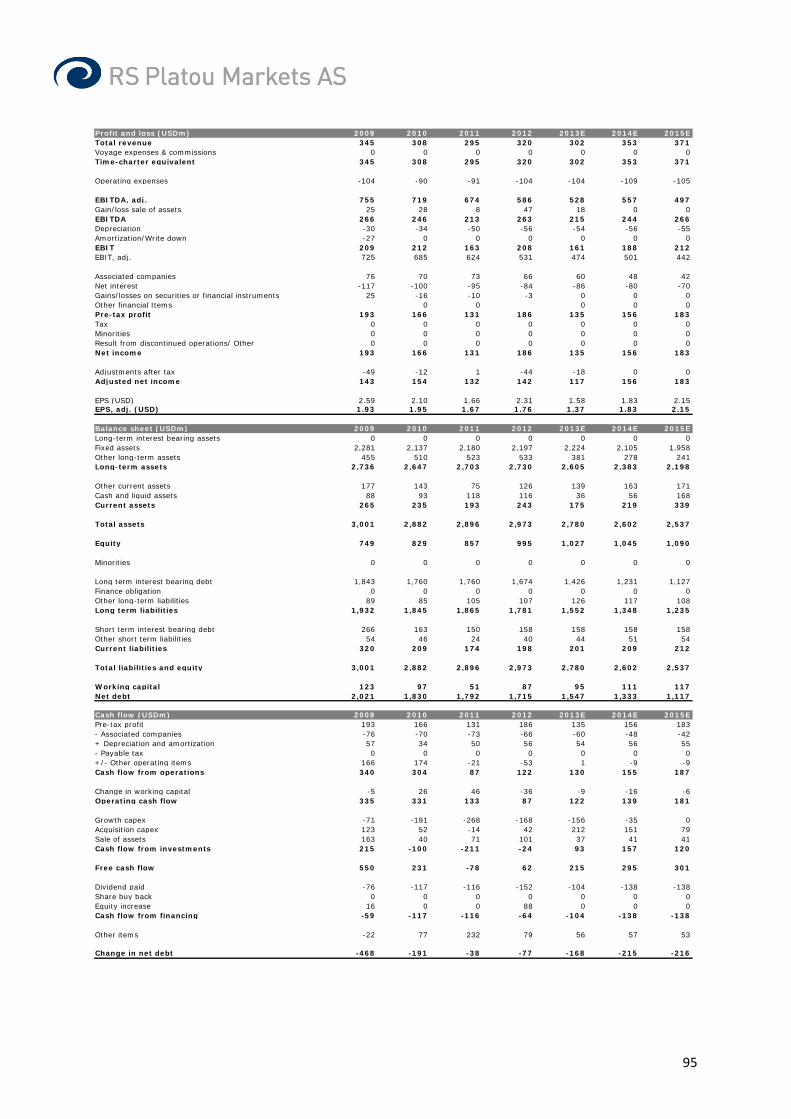

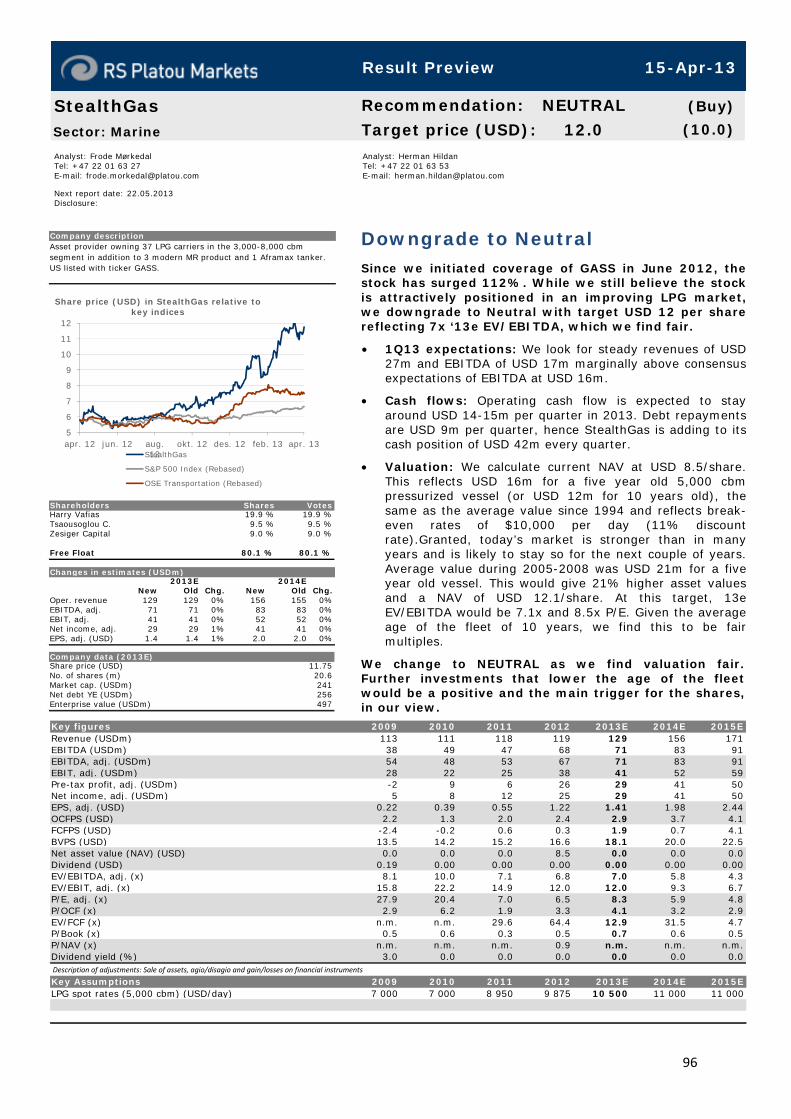

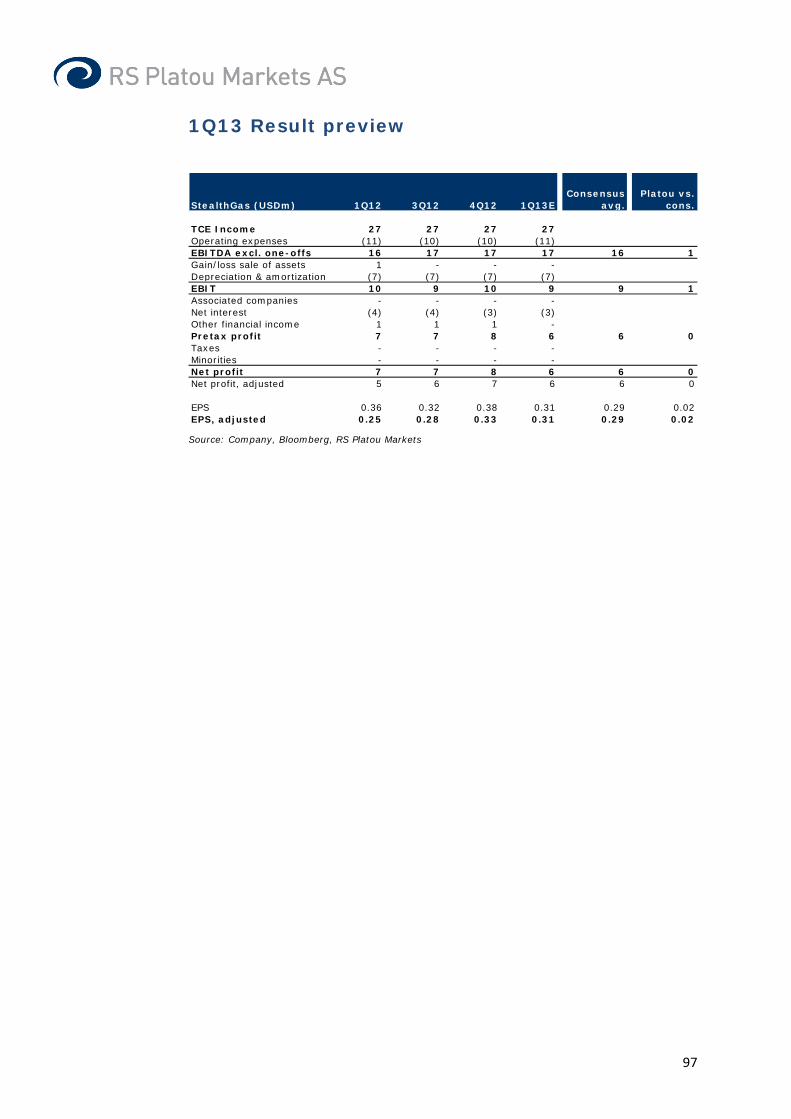

Shipping 1Q13 Previews -...

114

Sector Report 15-Apr-13 RS PLATOU MARKETS AS Haakon VII’s gate 10 P.O. BOX 1474 Vika N-0116 Oslo, Norway Telephone +47 22 01 63 00 Telefax +47 22 01 63 10 [email protected] www.platoumarkets.com NO 942 274 238 MVA Shipping 1Q13 Previews Analyst: Frode Mørkedal Tel: +47 22 01 63 27 E-mail: [email protected] Analyst: Herman Hildan Tel: +47 22 01 63 53 E-mail: [email protected] Shipping 1Q13 Previews Investing in shipping stocks today is a bet on a cyclical recovery of freight rates over the next two years. Given the sharply lower fleet growth in most segments during the forecast period, we believe such a bet is attractive. The stocks that have done well the last months have been able to tie a story around acquisition of ships at historically low asset values, and we expect the winners this year will remain growth-oriented companies. We continue to favour product tankers and dry bulk shipping where demand growth is high and therefore should be able to absorb the overcapacity of ships faster than in other segment. Closures of refinery capacity in mature markets means trading distances for product tankers will increase, while China will be increasingly reliant on dry bulk imports because of constrained local production of iron ore and coal with new low-cost supply from Australia and Brazil opening up arbitrage opportunities. • 1Q13 market review:Product tankers enjoyed much better rates in 1Q, particularly for MRs that averaged $18,000 per day. We believe this reflects that US product exports are driving up trading distances, although seasonal refinery turnarounds helped as well. Dry bulk earnings remained at operating cost levels, although we have seen improved freight rates for the smaller Handysize, Supramax and Panamax vessels during March on the back of a strong South American grain season and rising port congestion. In the crude tanker sector, rates have struggled due to reduced OPEC production and declining crude imports to both USA and China. However, we expect the end of a heavy refinery maintenance period to lift Saudi crude exports in coming months, provided oil prices do not drop much further. The container shipping market saw flat box rates q/q but 16% higher y-y, which should help the container operators to avoid the dramatic losses seen during 1Q12. However, box rates have underperformed last year’s level during April. In our view this is due to too high fleet growth and still struggling volumes and demand from Europe. LPG and LNG carriers saw rates slip in the first quarter due to lower export volumes whereas chemical tanker earnings were up 4% y-y. • Recommendation changes:We have lifted our rating for Nordic American Tankers from Sell to Neutral following the recent equity raise, the alignment of management’s incentives with other shareholders, and growth clearly on the agenda with recent investments. We have also lifted Diana Containerships from Sell to Neutral after the recent stock price decline. We have changed StealthGas from Buy to Neutral following the strong share price performance. • Valuation: Tanker stocks (both crude and clean) today trade 1.4x NAV (simple peer group average) which we find implies around 16% higher asset values compared with broker quotes. Dry bulk stocks on the other hand trade on average 1.03x NAV. Since we are at the trough of the shipping cycle (with ship values historically low when inflation adjusted), we find that today’s NAV is not very meaningful to base an investment on since it is fair to price in a recovery of asset values. Based on EV/EBITDA, the tanker peer group trades at 7x ‘15e while dry bulk on average trades at 3.5x ‘15e (both sectors based on mid-cycle rates of $30,000/day for Capesize and $43,000/day for VLCC). We reiterate our view from our Shipping Quarterly February 2013 that we believe both dry bulk and tankers will bottom out in 2013 and see a gradual recovery towards mid-cycle rates in 2015. Our top picks include d’Amico Shipping, Frontline 2012, Golden Ocean, Navios Acquisition, Scorpio Tankers and Ship Finance. 80 85 90 95 100 105 110 115 120 apr. 12 jun. 12 aug. 12 okt. 12 des. 12 feb. 13 apr. 13 Platou Shipping index relative to key indices, rebased Platou Shipping (Rebased) OSEBX index (Rebased) Company Share Share price perf. Target price* 3m 6m 12m price Rec. AP Moller-Maersk 41760 - 14 % 0 % -8 % 50 000 NEUTRAL Awilco LNG 14.50 -20 % -29 % -53 % 4.0 BUY Baltic Trading 3.66 4 % 7 % - 19 % 6.0 BUY Capital Product Partners 8.55 7 % 0 % -1% 10.0 BUY Cost amare 15.80 3 % -2 % 7 % 16.0 NEUTRAL d'Amico International Shipping 0.44 3 % 36 % - 12 % 0.70 BUY D/S Norden 182.60 5 % 14 % 11% 39.0 BUY Danaos 3.84 7 % 24 % -5 % 3.5 NEUTRAL DHT Holdings 4.75 1% -25 % 431% 7.0 BUY Diana Cont ainerships 5.29 -24 % - 12 % - 19 % 6.0 NEUTRAL Diana Shipping 9.79 11% 39 % 17 % 15.0 BUY Dryships 1.88 - 15 % -22 % -48 % 3.5 BUY Euronav 3.24 -38 % -38 % -54 % 3.0 SELL Frontline 11.95 -43 % -46 % -71% 2.5 NEUTRAL Front line 2012 45.75 31% 69 % 85 % 10.0 BUY GasLog 12.69 1% -1% 6 % 14.0 NEUTRAL Genco Shipping 2.29 -43 % -41% -61% 1.0 SELL Golar LNG 35.61 - 10 % - 11% - 10 % 46.0 BUY Golden Ocean 5.86 9 % 29 % 9 % 1.5 BUY Hoegh LNG 49.00 -9 % 11% -7 % 12.0 NEUTRAL Navios Maritime Acquisition 3.38 27 % 22 % -4 % 5.0 BUY Nept une Orient Lines 1.16 - 16 % -1% - 19 % 1.2 NEUTRAL Nordic American Tankers 9.73 2 % -1% -37 % 10.0 NEUTRAL Norwegian Car Carriers 1.60 -24 % -25 % - 18 % 2.5 BUY Odfjell 27.80 -8 % 30 % -26 % 6.0 BUY Orient Overseas 48.55 - 16 % 2 % -21% 54.0 NEUTRAL Pacific Basin 4.62 -6 % 12 % 4 % 5.0 NEUTRAL Scorpio Tankers 8.49 10 % 39 % 15 % 13.0 BUY Ship Finance 17.44 -3 % 10 % 19 % 22.0 BUY StealthGas 11.69 24 % 63 % 89 % 12.0 NEUTRAL Stolt-Nielsen 116.50 -9 % 5 % 6 % 24.0 NEUTRAL Teekay Tankers 2.60 -26 % -31% -57 % 4.0 BUY Thoresen Thai Agencies 18.20 0 % 0 % 0 % 18.0 NEUTRAL Wilh. Wilhelmsen ASA 49.50 - 13 % 21% 25 % 10.0 NEUTRAL Wilh. Wilhelmsen Holding 165.00 - 12 % 20 % 6 % 37.0 BUY 12 % 12 % * The share price is in local currency, Target price is in USD except for d'Amico, Euronav, Maersk, Nept une Orient Lines, Norwegian Car Carriers, Orient Overseas, Pacif ic Basin and Thoresen Thai.

Transcript of Shipping 1Q13 Previews -...

Sector Report 15-Apr-13

RS PLATOU MARKETS AS Haakon VII’s gate 10 P.O. BOX 1474 Vika N-0116 Oslo, Norway

Telephone +47 22 01 63 00 Telefax +47 22 01 63 10

[email protected] www.platoumarkets.com

NO 942 274 238 MVA

Shipping 1Q13 Previews

Analyst: Frode Mørkedal Tel: +47 22 01 63 27 E-mail: [email protected] Analyst: Herman Hildan Tel: +47 22 01 63 53 E-mail: [email protected]

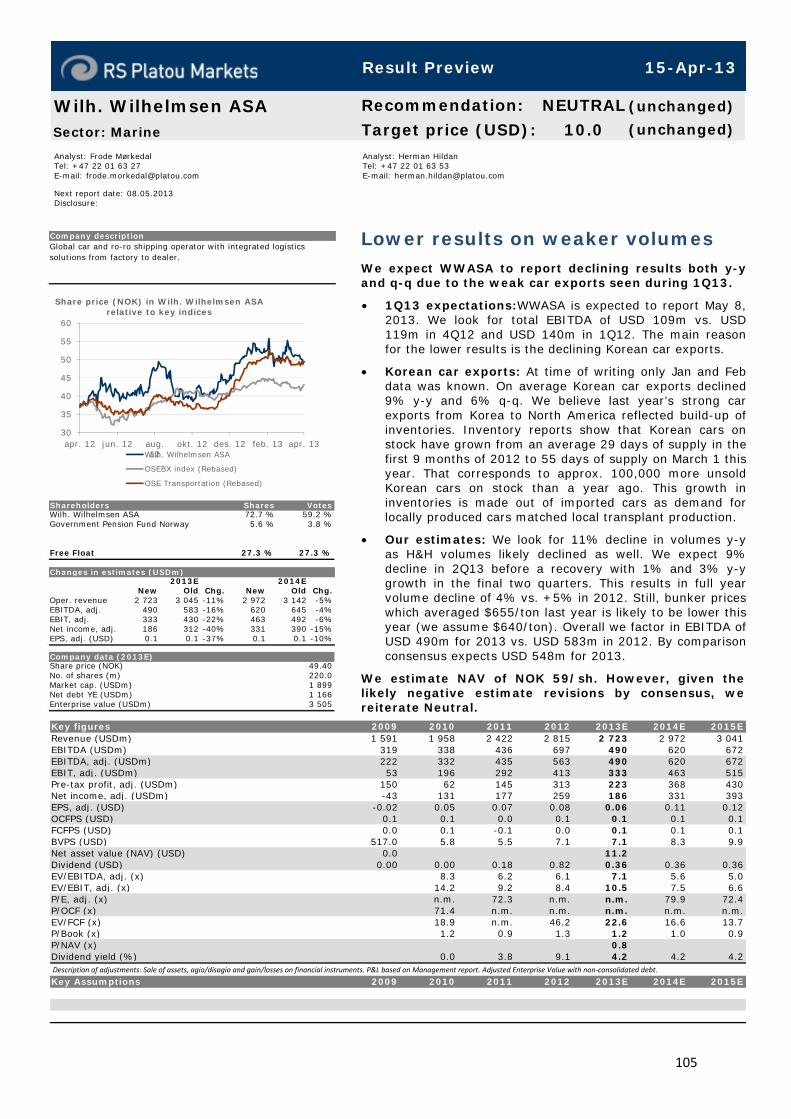

Shipping 1Q13 Previews Investing in shipping stocks today is a bet on a cyclical recovery offreight rates over the next two years. Given the sharply lower fleetgrowth in most segments during the forecast period, we believesuch a bet is attractive. The stocks that have done well the last months have been able to tie a story around acquisition of ships athistorically low asset values, and we expect the winners this yearwill remain growth-oriented companies. We continue to favour product tankers and dry bulk shipping where demand growth is high and therefore should be able to absorb the overcapacity of shipsfaster than in other segment. Closures of refinery capacity inmature markets means trading distances for product tankers willincrease, while China will be increasingly reliant on dry bulk imports because of constrained local production of iron ore and coal withnew low-cost supply from Australia and Brazil opening up arbitrageopportunities.

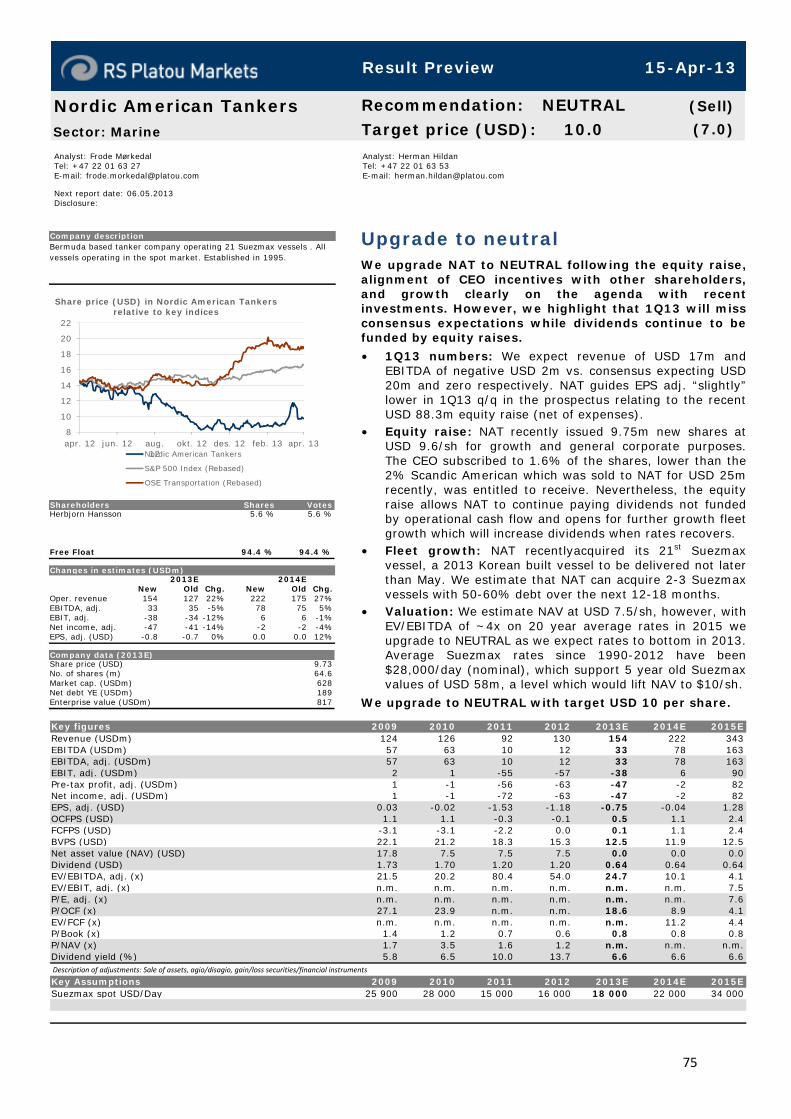

• 1Q13 market review:Product tankers enjoyed much better rates in 1Q, particularly for MRs that averaged $18,000 per day. We believethis reflects that US product exports are driving up trading distances,although seasonal refinery turnarounds helped as well. Dry bulkearnings remained at operating cost levels, although we have seen improved freight rates for the smaller Handysize, Supramax andPanamax vessels during March on the back of a strong South Americangrain season and rising port congestion. In the crude tanker sector,rates have struggled due to reduced OPEC production and declining crude imports to both USA and China. However, we expect the end of aheavy refinery maintenance period to lift Saudi crude exports incoming months, provided oil prices do not drop much further. Thecontainer shipping market saw flat box rates q/q but 16% higher y-y, which should help the container operators to avoid the dramatic lossesseen during 1Q12. However, box rates have underperformed lastyear’s level during April. In our view this is due to too high fleet growthand still struggling volumes and demand from Europe. LPG and LNGcarriers saw rates slip in the first quarter due to lower export volumeswhereas chemical tanker earnings were up 4% y-y.

• Recommendation changes:We have lifted our rating for Nordic American Tankers from Sell to Neutral following the recent equity raise, the alignment of management’s incentives with other shareholders,and growth clearly on the agenda with recent investments. We havealso lifted Diana Containerships from Sell to Neutral after the recent stock price decline. We have changed StealthGas from Buy to Neutralfollowing the strong share price performance.

• Valuation: Tanker stocks (both crude and clean) today trade 1.4x NAV (simple peer group average) which we find implies around 16% higher asset values compared with broker quotes. Dry bulk stocks on theother hand trade on average 1.03x NAV. Since we are at the trough ofthe shipping cycle (with ship values historically low when inflationadjusted), we find that today’s NAV is not very meaningful to base an investment on since it is fair to price in a recovery of asset values.Based on EV/EBITDA, the tanker peer group trades at 7x ‘15e while drybulk on average trades at 3.5x ‘15e (both sectors based on mid-cycle rates of $30,000/day for Capesize and $43,000/day for VLCC).

We reiterate our view from our Shipping Quarterly February 2013 that we believe both dry bulk and tankers will bottom out in 2013 and see a gradual recovery towards mid-cycle rates in 2015. Our top picks include d’Amico Shipping, Frontline 2012, Golden Ocean, Navios Acquisition, Scorpio Tankers and Ship Finance.

80

85

90

95

100

105

110

115

120

apr. 12 jun. 12 aug.12

okt. 12 des. 12 feb. 13 apr. 13

Platou Shipping index relative to key indices, rebased

Platou Shipping (Rebased) OSEBX index (Rebased)

Compa ny S ha r e S ha r e pr i c e pe r f . Ta r ge t

pr i c e * 3 m 6 m 12 m pr i c e R e c .

AP Moller-Maersk 41 760 -14 % 0 % -8 % 50 000 NEUTRAL

Awilco LNG 14.50 -20 % -29 % -53 % 4.0 BUY

Balt ic Trading 3.66 4 % 7 % -19 % 6.0 BUY

Capit al Product Part ners 8.55 7 % 0 % -1 % 10.0 BUY

Cost amare 15.80 3 % -2 % 7 % 16.0 NEUTRAL

d'Amico Int ernat ional Shipping 0.44 3 % 36 % -12 % 0.70 BUY

D/ S Norden 182.60 5 % 14 % 11 % 39.0 BUY

Danaos 3.84 7 % 24 % -5 % 3.5 NEUTRAL

DHT Holdings 4.75 1 % -25 % 431 % 7.0 BUY

Diana Cont ainerships 5.29 -24 % -12 % -19 % 6.0 NEUTRAL

Diana Shipping 9.79 11 % 39 % 17 % 15.0 BUY

Dryships 1.88 -15 % -22 % -48 % 3.5 BUY

Euronav 3.24 -38 % -38 % -54 % 3.0 SELL

Front line 11.95 -43 % -46 % -71 % 2.5 NEUTRAL

Front line 2012 45.75 31 % 69 % 85 % 10.0 BUY

GasLog 12.69 1 % -1 % 6 % 14.0 NEUTRAL

Genco Shipping 2.29 -43 % -41 % -61 % 1.0 SELL

Golar LNG 35.61 -10 % -11 % -10 % 46.0 BUY

Golden Ocean 5.86 9 % 29 % 9 % 1.5 BUY

Hoegh LNG 49.00 -9 % 11 % -7 % 12.0 NEUTRAL

Navios Marit ime Acquisit ion 3.38 27 % 22 % -4 % 5.0 BUY

Nept une Orient Lines 1.16 -16 % -1 % -19 % 1.2 NEUTRAL

Nordic American Tankers 9.73 2 % -1 % -37 % 10.0 NEUTRAL

Norwegian Car Carr iers 1.60 -24 % -25 % -18 % 2.5 BUY

Odf jell 27.80 -8 % 30 % -26 % 6.0 BUY

Orient Overseas 48.55 -16 % 2 % -21 % 54.0 NEUTRAL

Pacif ic Basin 4.62 -6 % 12 % 4 % 5.0 NEUTRAL

Scorpio Tankers 8.49 10 % 39 % 15 % 13.0 BUY

Ship Finance 17.44 -3 % 10 % 19 % 22.0 BUY

St ealt hGas 11.69 24 % 63 % 89 % 12.0 NEUTRAL

St olt -Nielsen 116.50 -9 % 5 % 6 % 24.0 NEUTRAL

Teekay Tankers 2.60 -26 % -31 % -57 % 4.0 BUY

Thoresen Thai Agencies 18.20 0 % 0 % 0 % 18.0 NEUTRAL

Wilh. Wilhelmsen ASA 49.50 -13 % 21 % 25 % 10.0 NEUTRAL

Wilh. Wilhelmsen Holding 165.00 -12 % 20 % 6 % 37.0 BUY12 % 12 %

* The share pr ice is in local currency, Target pr ice is in USD except f or d'Amico,

Euronav, Maersk, Nept une Orient Lines, Norwegian Car Carr iers,

Orient Overseas, Pacif ic Basin and Thoresen Thai.

2

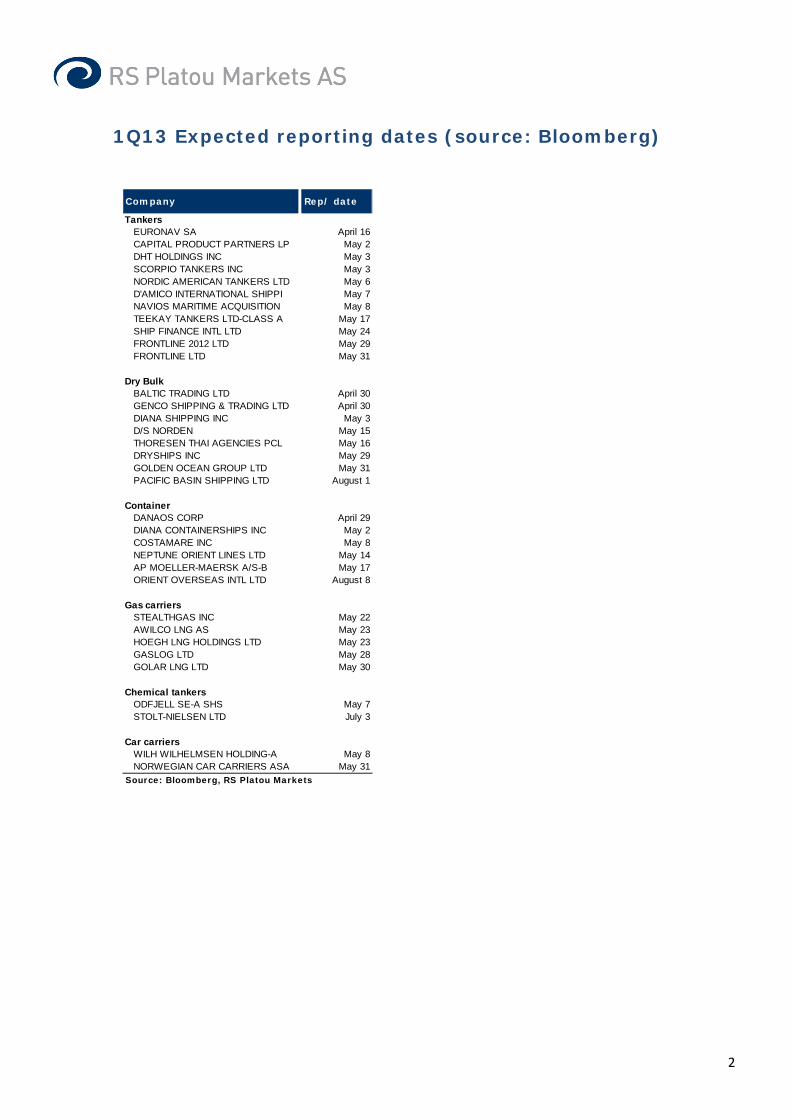

1Q13 Expected reporting dates (source: Bloomberg)

TankersEURONAV SA April 16CAPITAL PRODUCT PARTNERS LP May 2DHT HOLDINGS INC May 3SCORPIO TANKERS INC May 3NORDIC AMERICAN TANKERS LTD May 6D'AMICO INTERNATIONAL SHIPPI May 7NAVIOS MARITIME ACQUISITION May 8TEEKAY TANKERS LTD-CLASS A May 17SHIP FINANCE INTL LTD May 24FRONTLINE 2012 LTD May 29FRONTLINE LTD May 31

Dry BulkBALTIC TRADING LTD April 30GENCO SHIPPING & TRADING LTD April 30DIANA SHIPPING INC May 3D/S NORDEN May 15THORESEN THAI AGENCIES PCL May 16DRYSHIPS INC May 29GOLDEN OCEAN GROUP LTD May 31PACIFIC BASIN SHIPPING LTD August 1

ContainerDANAOS CORP April 29DIANA CONTAINERSHIPS INC May 2COSTAMARE INC May 8NEPTUNE ORIENT LINES LTD May 14AP MOELLER-MAERSK A/S-B May 17ORIENT OVERSEAS INTL LTD August 8

Gas carriersSTEALTHGAS INC May 22AWILCO LNG AS May 23HOEGH LNG HOLDINGS LTD May 23GASLOG LTD May 28GOLAR LNG LTD May 30

Chemical tankersODFJELL SE-A SHS May 7STOLT-NIELSEN LTD July 3

Car carriersWILH WILHELMSEN HOLDING-A May 8NORWEGIAN CAR CARRIERS ASA May 31

Source: Bloomberg, RS Platou Markets

Company Rep/ date

3

Crude tanker market graphs

Source: LoneStar, Baltic Exchange, RS Platou Markets

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

USD

/day

VLCC spot earnings (USD/day)

Avg. 2008-2012 2012 2013

0

10 000

20 000

30 000

40 000

50 000

60 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecU

SD/d

ay

Suezmax spot earnings (USD/day)

Avg. 2008-2012 2012 2013

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

USD

/day

Aframax spot earnings (USD/day)

Avg. 2008-2012 2012 2013

25

29

13

1617

22

19

1211

131311

1213

11

0

5

10

15

20

25

30

35

Q1'12 Q2'12 Q3'12 Q4'12 Q1'13

'000

USD

/day

Crude tanker earnings, quarterly

VLCC Suezmax Aframax

4

Product tanker market graphs

Source: Baltic Exchange, RS Platou Markets

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

USD

/day

LR2 spot earnings (USD/day)

Avg. 2008-2012 2012 2013

0

5 000

10 000

15 000

20 000

25 000

30 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecU

SD/d

ay

LR1 spot earnings (USD/day)

Avg. 2008-2012 2012 2013

5 000

7 000

9 000

11 000

13 000

15 000

17 000

19 000

21 000

23 000

25 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

USD

/day

MR spot earnings (USD/day)

2011 2012 2013e

1211

14

12

14

13

14

12

1415

14

12 11

14

18

0

2

4

6

8

10

12

14

16

18

20

Q1'12 Q2'12 Q3'12 Q4'12 Q1'13

'000

USD

/day

Product tanker earnings, quarterly

LR2 LR1 MR

5

Dry bulk market graphs

Source: Baltic Exchange, RS Platou, RS Platou Markets

2 000

2 100

2 200

2 300

2 400

2 500

500

700

900

1 100

1 300

1 500

1 700

Jan FebMar Apr May Jun Jul Aug Sep Oct Nov Dec

Ave

rage

Bal

tic D

ry In

dex

1990

-201

2

Balti

c D

ry In

dex

2012

/201

3

Baltic Dry Index

Avg. 1990-2012 2012 2013 ytd

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecU

SD/d

ay

Capesize spot earnings (USD/day)

Avg. 2009-2012 2012 2013

0

5 000

10 000

15 000

20 000

25 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

USD

/day

Panamax spot earnings (USD/day)

Avg. 2009-2012 2012 2013

9

65

16

89

10

76

89

9 9

78

7

99

77

0

2

4

6

8

10

12

14

16

18

Q1'12 Q2'12 Q3'12 Q4'12 Q1'13

'000

USD

/day

Dry bulk earnings, quarterly

Capesize Panamax Supramax Handysize

6

Container market graphs

Source: Shanghai Shipping Exchange, RS Platou Markets

500

700

900

1 100

1 300

1 500

1 700

1 900

2 100

Sep07

Feb08

Jul08

Dec08

May09

Oct09

Mar10

Aug10

Jan11

Jun11

Nov11

Apr12

Sep12

Feb13

USD

/TEU

Box rates per major trade lanes

Intra-Asia CCFI Asia-Europe CCFI Transpacific CCFI

900

950

1 000

1 050

1 100

1 150

700

800

900

1 000

1 100

1 200

1 300

1 400

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ave

rage

200

8-20

12 ($

/TEU

)

2012

/201

3 ($

/TEU

)

China Containerized Freight Index ($/TEU)

Avg. 2008-2012 2012 2013

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

USD

/TEU

Asia-Europe rates (spot)

2011 2012 2013

1 000

1 200

1 400

1 600

1 800

2 000

2 200

2 400

2 600

2 800

3 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

USD

/FEU

Asia-USWC rates (spot)

Avg. 2010-2012 2012 2013

7

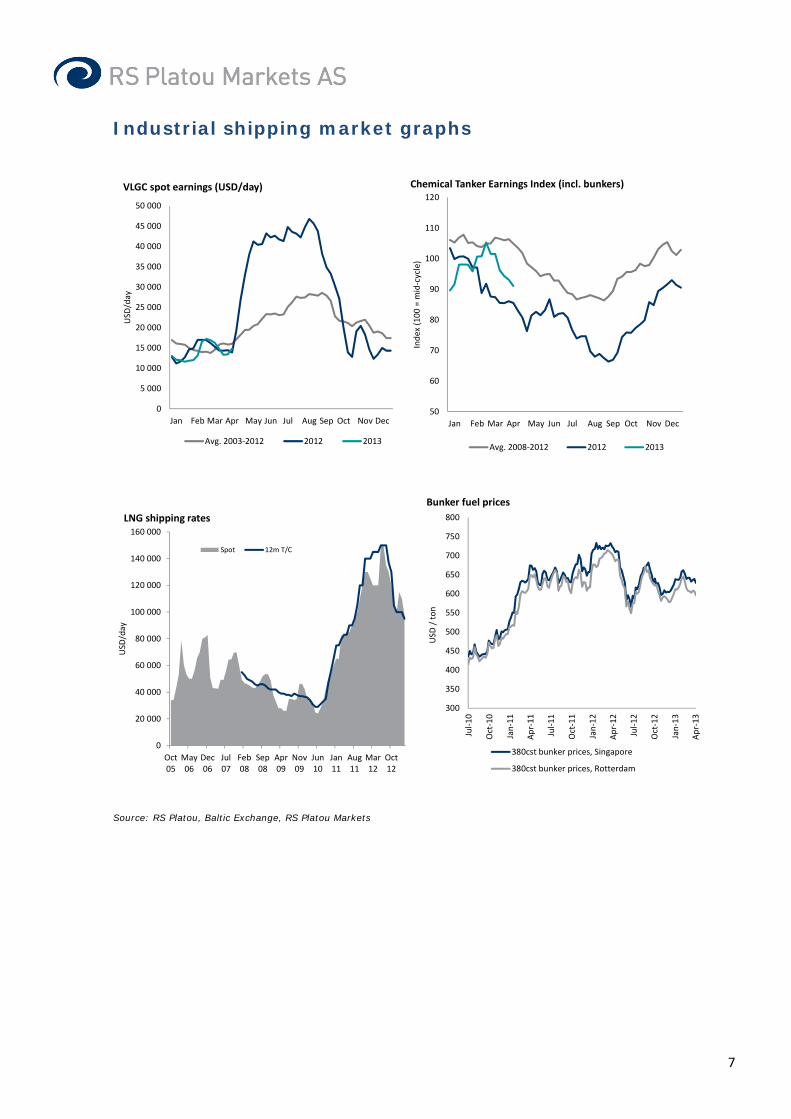

Industrial shipping market graphs

Source: RS Platou, Baltic Exchange, RS Platou Markets

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

50 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

USD

/day

VLGC spot earnings (USD/day)

Avg. 2003-2012 2012 2013

50

60

70

80

90

100

110

120

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecIn

dex

(100

= m

id-c

ycle

)

Chemical Tanker Earnings Index (incl. bunkers)

Avg. 2008-2012 2012 2013

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

Oct05

May06

Dec06

Jul07

Feb08

Sep08

Apr09

Nov09

Jun10

Jan11

Aug11

Mar12

Oct12

USD

/day

LNG shipping rates

Spot 12m T/C

300

350

400

450

500

550

600

650

700

750

800

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

USD

/ to

n

Bunker fuel prices

380cst bunker prices, Singapore

380cst bunker prices, Rotterdam

8

RS Platou Markets peer group

TP Last M.Cap EV NAV P/ EV/ Yield %Rating USD* local USDm USDm USD* NAV ASSETS 2013 2014 2015 2013

TankersCapital Product Partners Buy 10.0 8.6 794 1 195 4.1 2.10 1.53 10.8 10.3 7.9 10.9d'Amico International Shipping Buy 0.7 0.4 158 353 0.5 0.80 0.90 11.3 9.0 3.7 0.0DHT Holdings Buy 7.0 4.8 73 214 7.7 0.62 0.83 12.2 6.7 2.1 1.7Euronav Sell 3.0 3.2 212 1 401 1.8 2.39 1.10 9.3 7.3 3.0 0.0Frontline Neutral 2.5 12.0 162 1 372 -3.1 nmf 1.17 29.0 21.3 5.7 0.0Frontline 2012 Buy 10.0 45.8 1 714 2 157 4.1 1.93 1.62 nmf 24.0 9.4 0.0Navios Maritime Acquisition Buy 5.0 3.4 265 1 195 2.4 1.42 1.07 10.0 8.1 5.3 5.9Nordic American Tankers Neutral 10.0 9.7 628 823 7.5 1.30 1.22 24.7 10.1 4.1 6.6Scorpio Tankers Buy 13.0 8.5 1 049 1 104 7.0 1.21 1.19 38.9 19.9 6.1 0.0Ship Finance Buy 22.0 17.4 1 486 4 476 14.9 1.17 1.05 8.5 7.6 8.0 7.0Teekay Tankers Buy 4.0 2.6 217 927 1.8 1.47 1.08 10.7 8.8 4.2 4.6Weighted average 1.51 1.29 13.6 14.6 7.1 3.8

Dry bulkBaltic Trading Buy 6.0 3.7 82 180 4.9 0.75 0.87 nmf 10.2 5.0 0.0Diana Shipping Buy 15.0 9.8 792 806 8.0 1.22 1.21 16.2 11.8 4.6 0.0Dryships Buy 3.5 1.9 799 4 465 2.8 0.67 0.92 10.2 4.7 3.4 0.0D/S Norden Buy 39.0 182.6 1 319 951 39.1 0.82 0.77 16.2 7.9 3.2 2.3Genco Shipping Sell 1.0 2.3 101 1 556 -8.2 nmf 1.43 nmf 11.4 5.8 0.0Golden Ocean Buy 1.5 5.9 457 862 1.0 1.05 1.03 7.0 5.3 2.7 0.0Pacific Basin Neutral 5.0 4.4 1 104 1 286 3.8 1.18 1.15 15.0 8.9 4.3 0.0Thoresen Thai Neutral 18.0 18.2 621 952 12.7 1.44 1.25 7.7 3.0 1.4 0.0Weighted average 1.01 1.03 12.7 7.5 3.5 0.6

ContainerAP Moller-Maersk Neutral 50 000 41 760 31 949 48 756 70 300 0.59 0.69 3.9 3.5 3.0 3.1Costamare Neutral 16.0 15.8 1 182 2 429 10.9 1.45 1.18 10.4 8.1 7.5 7.0Danaos Neutral 3.5 3.8 421 3 764 2.3 1.67 1.05 8.4 7.8 6.7 0.0Diana Containerships Neutral 6.0 5.3 170 230 5.7 0.92 0.94 17.9 20.2 11.7 11.3Neptune Orient Lines Neutral 1.2 1.1 2 392 5 471 1.1 1.08 1.03 18.5 7.2 6.0 0.0Orient Overseas Neutral 54.0 48.5 3 906 5 078 69.8 0.69 0.75 8.9 4.7 3.5 1.9Weighted average (excl. Maersk) 0.98 0.91 12.1 6.4 5.2 2.2

Gas carriersAwilco LNG Buy 4.0 14.5 171 169 4.1 0.62 0.62 12.0 5.9 5.9 0.0Hoegh LNG Neutral 12.0 49.0 597 1 102 11.0 0.78 0.87 25.5 16.7 7.5 0.0GasLog Neutral 14.0 12.7 797 820 11.2 1.14 1.13 17.0 11.9 9.5 4.1Golar LNG Buy 46.0 35.6 2 860 3 959 48.3 0.74 0.79 12.2 10.1 7.8 4.0StealthGas Neutral 12.0 11.7 240 535 8.5 1.37 1.14 7.0 5.8 4.3 0.0Weighted average 0.84 0.87 14.5 10.9 7.8 3.2

Chemical tankersOdfjell Buy 6.0 27.8 416 1 593 7.0 0.69 0.90 10.5 7.3 6.3 0.0Stolt-Nielsen Neutral 24.0 116.5 1 178 2 769 22.8 0.89 0.95 8.7 7.0 6.4 4.9Weighted average 0.84 0.94 9.2 7.1 6.4 3.6

Car carriersNorwegian Car Carriers Buy 2.5 1.6 68 283 1.9 0.84 0.96 7.1 6.6 5.6 0.0Wilh. Wilhelmsen ASA Neutral 10.0 49.5 1 897 3 397 10.3 0.84 0.90 7.1 5.6 5.0 4.2W.Wilhelmsen Holding Buy 37.0 165.0 1 337 2 994 42.9 0.67 0.82 4.9 3.8 3.2 3.5Weighted average 0.77 0.87 6.2 4.9 4.3 3.8

* NAV and TP in local currencies for Maersk, d'Amico, Euronav, Neptune Orient Lines, Norwegian Car Carriers, Orient Overseas, Pacific Basin and Thoresen Thai.

Source: RS Platou Markets estimates

EV/EBITDA

9

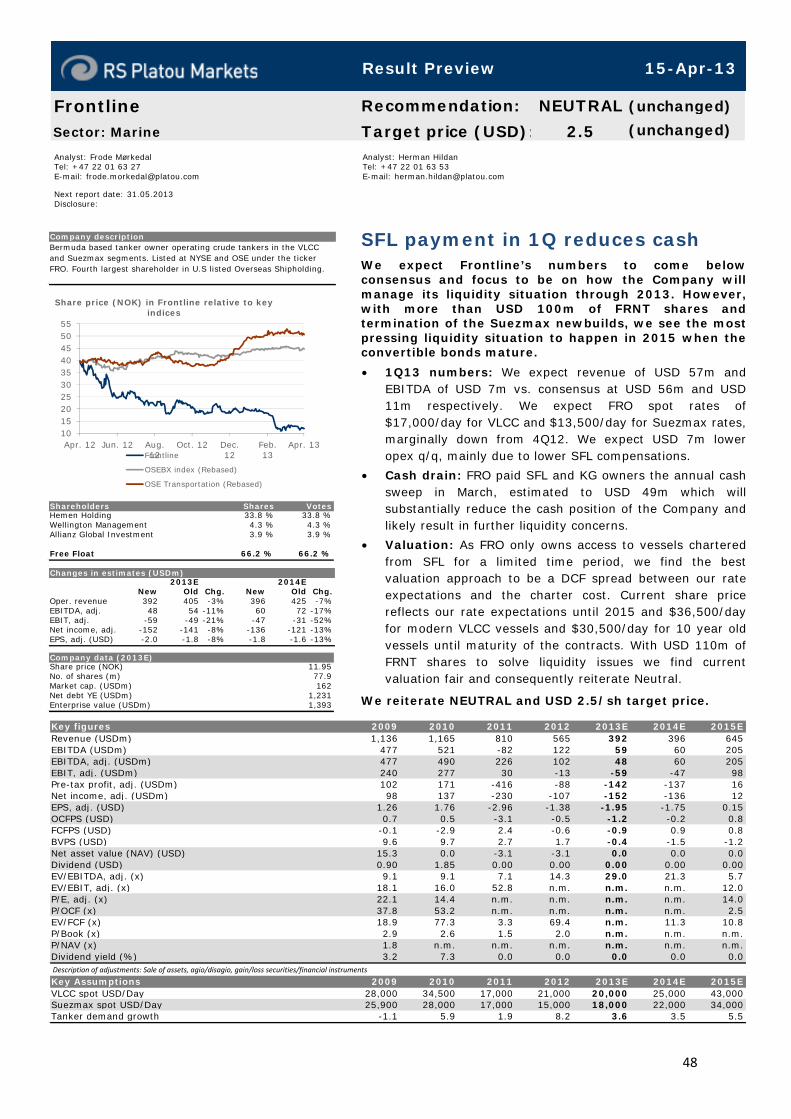

Analyst: Frode Mørkedal Tel: +47 22 01 63 27 E-mail: [email protected] Next report date: 17.05.2013 Disclosure:

Analyst: Herman Hildan Tel: +47 22 01 63 53 E-mail: [email protected] Analyst: Alex Gheorghe Tel: +47 22 01 63 47 E-mail: [email protected]

Weak container results – focus on Oil reserves update AP Moller-Maersk will report 1Q13 results on May 17.We expect focus to be on updated resource estimatesfor Maersk Oil and as always, the near term outlook forthe struggling container market. We remain NEUTRAL.

• 1Q13 expectations: We look for EBITDA of DKK 16bndown from DKK 18bn in 4Q12 due to lower results fromMaersk Line. Compared to preliminary Bloombergconsensus we are DKK 2bn lower on EBITDA level.

• Maersk Line: The container market in 1Q13 was muchbetter than 1Q12 when Maersk Line posted a negative DKK3.4bn net loss. Still, we look for a slightly negative resultof DKK -0.13bn. We factor in 6% lower volumes y-y but6% higher rates y-y (but flat rates vs. 4Q12). Comparedwith 4Q12 the result is negatively impacted by higherbunker costs.

• Maersk Oil: Updated reserves figures along withresources, perhaps with more granularity than previouslydisclosed, will be the focus with 1Q13 results. Whileproduction is expected to be weak at 232 mbbl/d, weforecast a rebound settling by 3Q13. More importantly, wewill be watching for changes in pace and costs indevelopments going forward.

Our 2013e EPS is maintained at DKK 4,380 for now. However, given the weaker than expected container market we see downside risk on our estimates should the May 1 container surcharges not be successful. We therefore maintain our Neutral recommendation.

AP Moller-MaerskSector: Marine

Recommendation: NEUTRAL (unchanged)

Target price (DKK): 50000 (unchanged)

Company descriptionDanish conglomerate with diversification across a broad range of businesses including world-leading positions in container shipping, tankers, terminals, tugs and niche offshore supply services. Comprehensive oil & gas activities. Listed at OMX Copenhagen.

35 000

40 000

45 000

50 000

55 000

60 000

apr. 12 jun. 12 aug. 12 okt. 12 des. 12 feb. 13

Share price (DKK) in AP Moller-Maersk relative to key indices

AP Moller-Maersk

OMX Copenhagen 20 (Rebased)

OSE Transportation (Rebased)

Shareholders Shares VotesA.P. Møller and Hustru 51.1 % 64.1 %Franklin Resources INC 4.2 % 6.5 %MC-Kinney Moeller Maersk 3.7 % 5.9 %

Free Float 41.0 % 41.0 %

Changes in estimates (DKKm)2013E 2014E

New Old Chg. New Old Chg.Oper. revenue 325 738 325 738 0% 335 302 335 302 0%EBITDA, adj. 70 821 70 821 0% 76 581 76 581 0%EBIT, adj. 42 853 42 853 0% 46 228 46 228 0%Net income, adj. 19 132 19 132 0% 25 181 25 181 0%EPS, adj. (DKK) 4 383.1 4 383.1 0% 5 768.8 5 768.8 0%

Company data (2013E)Share price (DKK) 41 760.00No. of shares (m) 4.4Market cap. (DKKm) 182 282Net debt YE (DKKm) 95 266Enterprise value (DKKm) 277 548

Description of adjustments: Sale of assets, agio/disagio and gain/losses on financial instruments.

Key figures 2009 2010 2011 2012 2013E 2014E 2015ERevenue (DKKm) 261 532 315 831 324 172 344 782 325 738 335 302 348 076EBITDA (DKKm) 50 124 93 010 83 254 76 593 70 821 76 581 81 780EBITDA, adj. (DKKm) 49 262 89 218 78 506 72 910 70 821 76 581 81 780EBIT, adj. (DKKm) 21 854 59 474 51 251 41 937 42 853 46 228 48 234Pre-tax profit, adj. (DKKm) 17 543 58 705 53 174 43 264 41 365 45 540 48 546Net income, adj. (DKKm) -9 034 22 901 13 085 13 625 19 132 25 181 29 129EPS, adj. (DKK) -2 152.65 5 246.53 2 997.63 3 121.54 4 383.06 5 768.84 6 673.37OCFPS (DKK) 5 980.4 13 052.1 8 908.6 10 126.5 10 771.9 12 444.9 14 001.2FCFPS (DKK) -3 391.7 7 077.7 -3 063.7 1 737.2 1 343.6 2 831.3 8 085.8BVPS (DKK) 37 855.5 44 206.8 47 637.1 50 984.0 54 566.6 59 434.9 65 107.9Net asset value (NAV) (DKK) 0.0 0.0 70 100.0 70 100.0 0.0 0.0 0.0Dividend (DKK) 325.00 1 000.00 1 000.00 1 200.00 1 300.00 1 400.00 1 400.00EV/EBITDA, adj. (x) 5.2 3.3 3.3 3.9 3.9 3.5 3.0EV/EBIT, adj. (x) 11.6 5.0 5.1 6.7 6.5 5.9 5.0P/E, adj. (x) n.m. 9.6 12.6 13.6 9.5 7.2 6.3P/OCF (x) 6.1 3.9 4.3 4.2 3.9 3.4 3.0EV/FCF (x) n.m. 9.6 n.m. 37.2 47.3 21.9 6.8P/Book (x) 1.0 1.1 0.8 0.8 0.8 0.7 0.6P/NAV (x) n.m. n.m. 0.5 0.6 n.m. n.m. n.m.Dividend yield (%) 0.9 2.0 2.6 2.8 3.1 3.4 3.4

Key Assumptions 2009 2010 2011 2012 2013E 2014E 2015EOil price (Brent USD/bbl) 62 80 111 113 107 100 100Asia-Europe spot rates $/TEU 1 720 883 1 362 1 300 1 365 1 365Maersk Line achieved box rates $/FEU 2 370 3 062 2 833 2 881 2 842 2 871 2 871

Result Preview 15-Apr-13

10

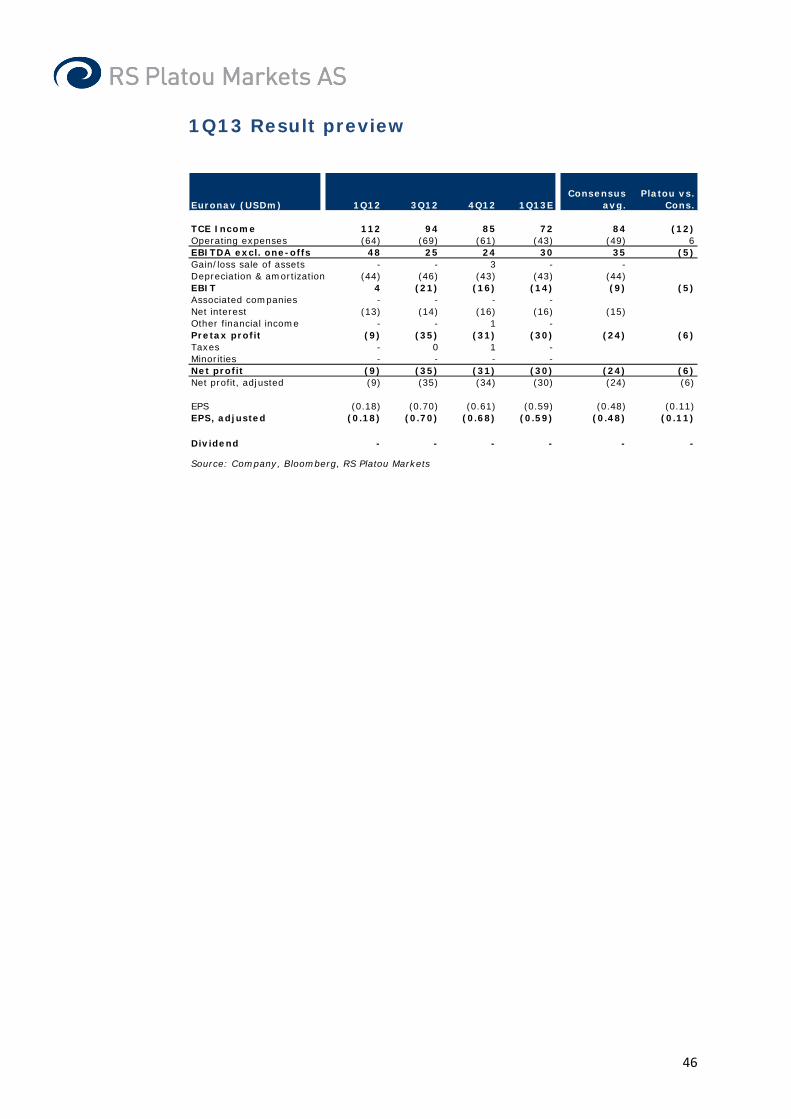

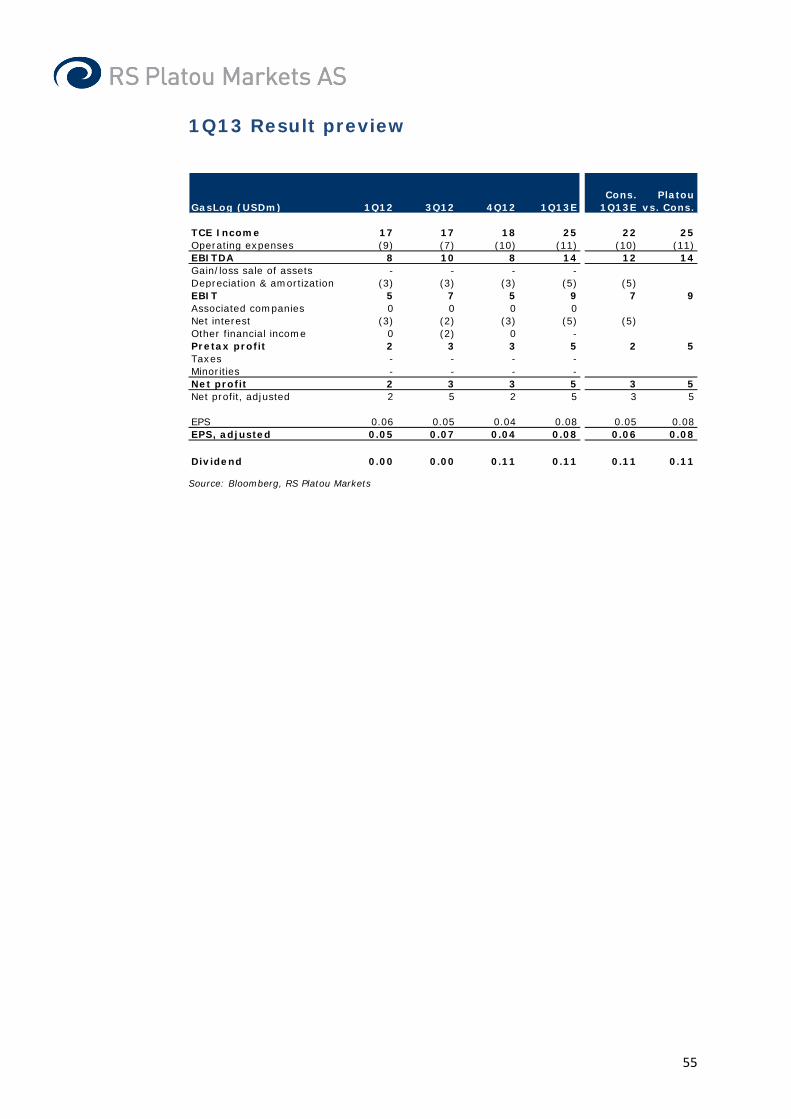

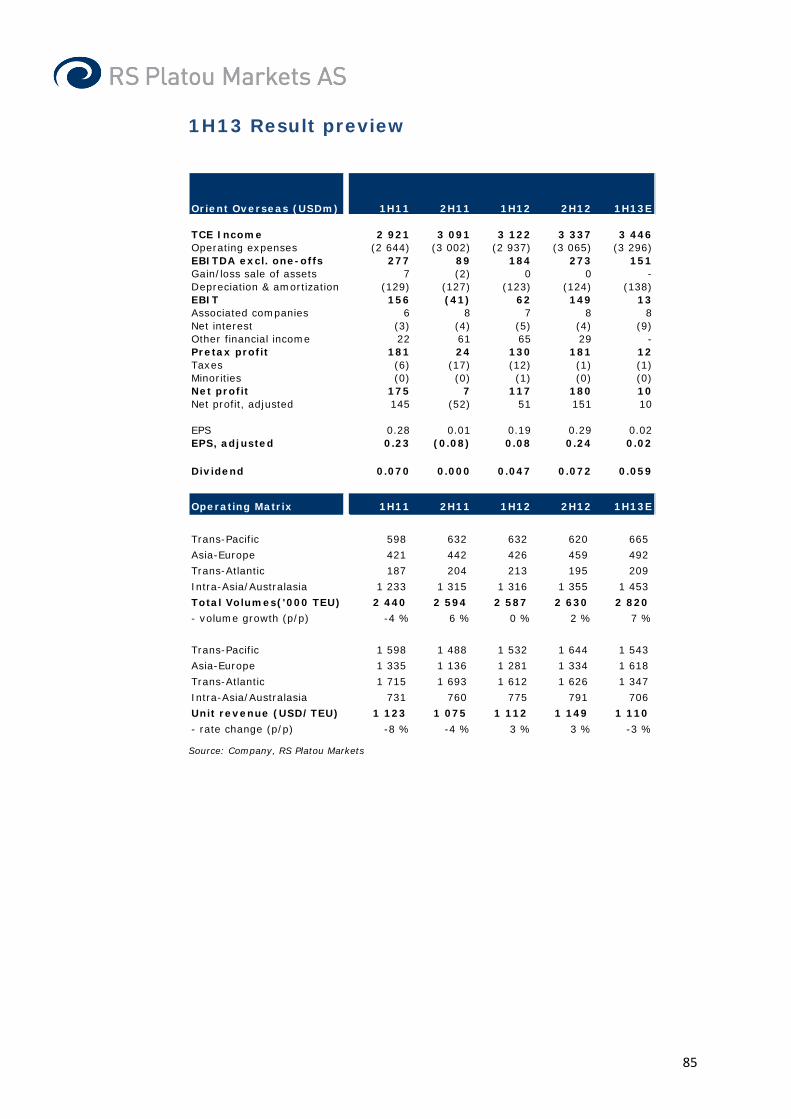

1Q13 Result preview

AP Moller-Maersk(DKK bn) 1Q12 2Q12 3Q12 4Q12 1Q13E

Consensus avg.

Platou vs. Cons.

TCE Income 81 89 87 85 80 82 (2)Operating expenses (67) (68) (67) (67) (64)EBITDA excl. one-offs 14 21 20 18 16 18 (2)Gain/loss sale of assets 2 0 1 0 -Depreciation & amortization (7) (7) (9) (8) (7)EBIT 9 14 12 11 9 11 (2)Associated companies 0 0 0 0 0Net interest (1) (1) (1) (1) (1)Other financial income - - - - -Pretax profit 8 13 12 10 9 10 (2)Taxes (2) (7) (6) (4) (5)Minorities (1) (0) (0) (0) (0)Net profit 6 5 5 5 3 4 (1)Net profit, adjusted (1) 5 5 6 3 4

EPS 1 399 1 197 1 172 1 158 718 849EPS, adjusted (171) 1 124 1 242 1 271 718 849 (131)

CurrencyUSD/DKK 5.67 5.79 5.95 5.75 5.65

Net profit per segmentMaersk Line (3.4) 1.3 2.9 1.9 (0.1)Maersk Oil 7.3 2.8 1.5 2.5 1.9APM Terminals 1.3 0.9 1.0 1.0 0.8Maersk Drilling 0.7 0.6 0.5 0.3 0.7Maersk Supply Service 0.2 0.2 0.3 0.1 0.3Maersk Tankers (0.2) (0.0) (1.6) 0.0 (0.0)Damco 0.0 0.2 0.1 0.0 0.1SVITZER 0.2 0.2 0.2 (0.5) 0.1Maersk FPSOs and Maersk LNG 0.6 0.2 0.9 0.2 0.0Dansk Supermarked 0.3 0.3 0.2 0.5 0.4Other industrial 0.5 0.5 0.2 0.3 0.2Other/consolidation eliminations (1.0) (1.4) (0.6) (0.8) (0.8)Total net profit (before minority) 6.7 5.6 5.6 5.5 3.6

Key value drivers Transported volumes (mill FEU) 2.2 2.1 2.0 2.1 Average container freight rate (USD per FEU) 3 152 3 022 2 842 2 816 Entitlement oil production (bpd ´000) 288 240 242 232 Oil price (USD/bbl) 104 108 113 104 APM Terminals equity throughput (mill TEU) 9.1 9.0 8.8 9.1

Source: Company, Bloomberg, RS Platou Markets

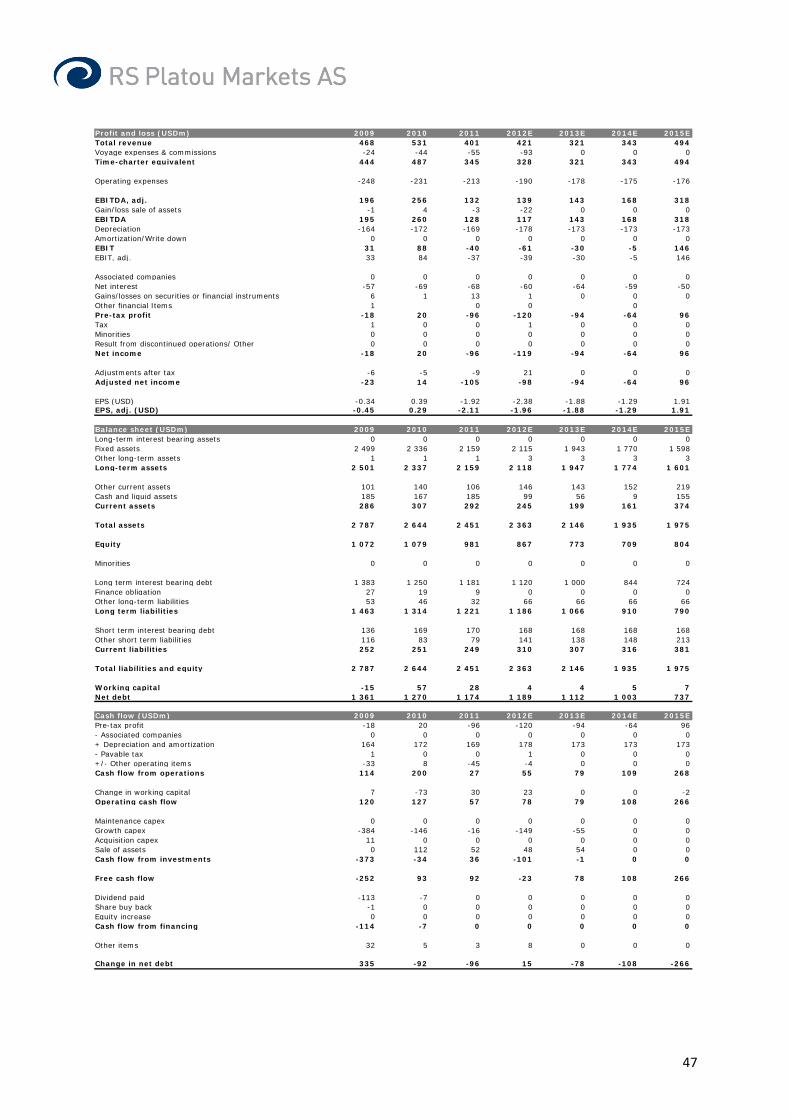

11

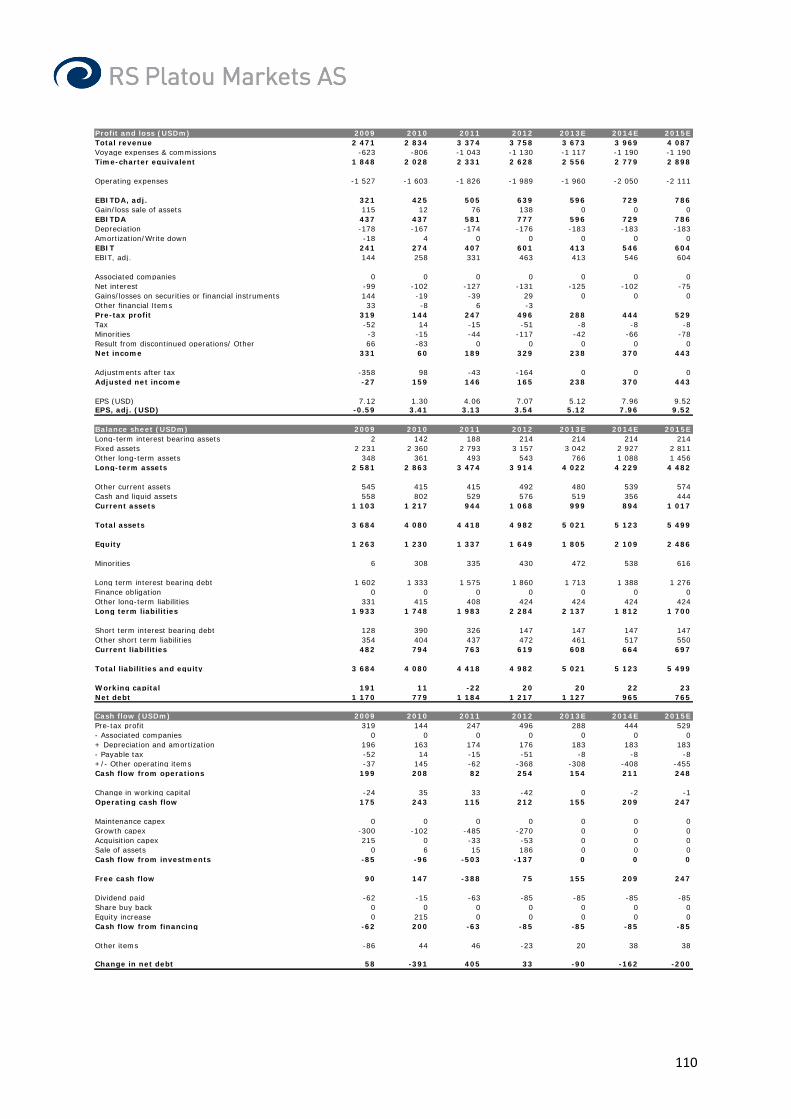

Profit and loss (DKKm) 2009 2010 2011 2012 2013E 2014E 2015ETotal revenue 261 532 315 831 324 172 344 782 325 738 335 302 348 076Voyage expenses & commissions 0 0 0 0 0 0 0Time-charter equivalent 261 532 315 831 324 172 344 782 325 738 335 302 348 076

Operating expenses -212 270 -226 613 -245 666 -271 872 -254 917 -258 721 -266 296

EBITDA, adj. 49 262 89 218 78 506 72 910 70 821 76 581 81 780Gain/loss sale of assets 862 3 792 4 748 3 683 0 0 0EBITDA 50 124 93 010 83 254 76 593 70 821 76 581 81 780Depreciation -27 408 -29 744 -27 255 -30 973 -27 968 -30 353 -33 546Amortization/Write down -3 784 -4 078 -1 634 -2 369 0 0 0EBIT 18 932 59 188 54 365 43 251 42 853 46 228 48 234EBIT, adj. 21 854 59 474 51 251 41 937 42 853 46 228 48 234

Associated companies 360 461 651 1 286 2 112 2 812 3 112Net interest -5 533 -5 022 -3 476 -3 642 -3 600 -3 500 -2 800Gains/losses on securities or financial instruments 270 -241 -1 088 -734 0 0 0Other financial ItemsPre-tax profit 14 029 54 386 50 452 40 161 41 365 45 540 48 546Tax -20 393 -26 174 -32 447 -19 138 -20 489 -18 615 -17 673Minorities -1 538 -1 760 -2 894 -1 722 -1 744 -1 744 -1 744Result from discontinued operations/ Other 0 3 78 16 0 0 0Net income -7 902 26 455 15 189 19 317 19 132 25 181 29 129

Adjustments after tax -1 132 -3 554 -2 104 -596 0 0 0Adjusted net income -9 034 22 901 13 085 13 625 19 132 25 181 29 129

EPS (DKK) -1 882.91 6 060.74 3 479.74 4 425.45 4 383.06 5 768.84 6 673.37EPS, adj. (DKK) -2 152.65 5 246.53 2 997.63 3 121.54 4 383.06 5 768.84 6 673.37

Balance sheet (DKKm) 2009 2010 2011 2012 2013E 2014E 2015ELong-term interest bearing assets 2 966 711 87 0 0 0 0Fixed assets 244 995 249 007 265 180 264 425 277 611 289 222 281 496Other long-term assets 46 292 50 347 71 390 80 386 82 498 85 310 88 422Long-term assets 294 253 300 065 336 657 344 811 360 109 374 531 369 918

Other current assets 40 233 48 776 52 839 60 709 57 356 59 040 61 289Cash and liquid assets 10 713 25 882 15 247 15 171 26 631 23 119 9 324Current assets 50 946 74 658 68 086 75 880 83 987 82 158 70 613

Total assets 345 199 374 723 404 743 420 691 444 096 456 690 440 531

Equity 148 779 181 556 194 157 208 800 222 694 242 200 265 219

Minorities 10 089 11 406 13 778 13 744 15 488 17 232 18 976

Long term interest bearing debt 98 158 88 421 96 884 98 112 108 945 98 749 55 771Other long-term liabilities 25 557 24 591 29 888 31 568 31 568 31 568 31 568Long term liabilities 123 715 113 012 126 772 129 680 140 513 130 317 87 339

Short term interest bearing debt 16 300 14 610 14 571 12 952 12 952 12 952 12 952Other short term liabilities 46 316 54 139 55 465 55 515 52 449 53 989 56 045Current liabilities 62 616 68 749 70 036 68 467 65 401 66 941 68 997

Total liabilities and equity 345 199 374 723 404 743 420 691 444 096 456 690 440 531

Working capital -6 083 -5 363 -2 626 5 194 4 907 5 051 5 244Net debt 100 779 76 438 96 121 95 893 95 266 88 582 59 399

Cash flow (DKKm) 2009 2010 2011 2012 2013E 2014E 2015EPre-tax profit 14 029 54 386 50 452 40 161 41 365 45 540 48 546- Associated companies -360 -461 -651 -1 286 -2 112 -2 812 -3 112+ Depreciation and amortization 31 192 33 822 28 889 33 342 27 968 30 353 33 546- Payable tax -20 393 -26 174 -32 447 -19 138 -20 489 -18 615 -17 673+/- Other operating items 1 815 -3 881 -4 620 -1 057 0 0 0Cash flow from operations 26 283 57 692 41 623 52 022 46 732 54 466 61 307

Change in working capital -1 185 -720 -2 737 -7 820 287 -144 -192Operating cash flow 25 098 56 972 38 886 44 202 47 019 54 322 61 115

Maintenance capex 0 0 0 0 0 0 0Growth capex -43 822 -30 958 -42 058 -47 108 -43 810 -41 963 -25 821Acquisition capex 2 267 1 533 -12 456 368 0 0 0Sale of assets 2 223 3 347 2 255 10 121 2 656 0 0Cash flow from investments -39 332 -26 078 -52 259 -36 619 -41 154 -41 963 -25 821

Free cash flow -14 234 30 894 -13 373 7 583 5 865 12 358 35 294

Dividend paid -3 082 -2 104 -4 947 -5 475 -5 238 -5 674 -6 111Share buy back 0 0 61 -1 514 0 0 0Equity increase 8 177 153 0 0 0 0 0Cash flow from financing 5 095 -1 951 -4 886 -6 989 -5 238 -5 674 -6 111

Other items -8 883 -4 602 -1 424 -366 0 0 0

Change in net debt 18 022 -24 341 19 683 -228 -627 -6 684 -29 183

12

Analyst: Frode Mørkedal Tel: +47 22 01 63 27 E-mail: [email protected] Next report date: 30.05.2013 Disclosure:

Analyst: Herman Hildan Tel: +47 22 01 63 53 E-mail: [email protected]

Waiting for contracts and financing Awilco LNG will report their 1Q13 figures on May 5th. Weare in line with consensus on estimates and expect mainfocus to be the newbuilds with 2H13 delivery.

• 1Q13 figures: We expect revenue of USD 10m andEBITDA of USD 5m, in line with consensus at USD 11mand USD 5m respectively. Only WillGas is on long termcontract while WilEnergy is reported by brokers to havefixed two spot voyages, to Brunei and West Australia. Weexpect $40,000/day, hence, lower earnings for theCompany q/q. WilPower is idle and will likely remain idle aswe enter into the seasonally slow period over the summer.Consequently 2013 estimates are lowered as we model inWilPower being idle going forward.

• Newbuildings and financing: Management has guidednewbuild contracts 3-6 months prior to vessel delivery,consequently we expect the first contract prior to summer.Duration and rate level will determine financing, but 70%debt financing should be achievable either fully throughbank debt or in combination with bonds.

• Valuation: With at least $80,000/day on the newbuildsone could argue for USD 225m value of the newbuilds.With scrap value of USD 20m on the remaining 3 vesselsand USD 36m contract value for WilGas we arrive at USD4/share after USD 280m of capex. Furthermore, the 2xnewbuilds alone should be able to provide USD 15m ofdividend capacity, assuming 15 year debt profile.

We lower target to USD 4/sh, but reiterate BUY.

Awilco LNGSector: Marine

Recommendation: BUY (unchanged)

Target price (USD): 4.0 (5.0)

Company descriptionOwns 3 LNG carriers built in 1983-84 and two newbuilds for 2013 delivery marketed for spot and term chartering in the LNG shipping market.

10

15

20

25

30

35

40

45

apr. 12 jun. 12 aug.12

okt. 12 des. 12 feb. 13 apr. 13

Share price (NOK) in Awilco LNG relative to key indices

Awilco LNG

OSEBX index (Rebased)

OSE Transportation (Rebased)

Shareholders Shares VotesAwilco AS 33.7 % 33.7 %Home Capital AS 7.9 % 7.9 %Astrup Fearnley AS 7.6 % 7.6 %Uthalden A/S 7.6 % 7.6 %Free Float 66.3 % 66.3 %

Changes in estimates (USDm)2013E 2014E

New Old Chg. New Old Chg.Oper. revenue 57 76 -25% 94 117 -20%EBITDA, adj. 35 51 -30% 64 82 -23%EBIT, adj. 26 41 -37% 47 65 -29%Net income, adj. 19 34 -45% 36 54 -34%EPS, adj. (USD) 0.3 0.5 -45% 0.5 0.8 -34%

Company data (2013E)Share price (NOK) 15.00No. of shares (m) 67.8Market cap. (USDm) 178Net debt YE (USDm) 254Enterprise value (USDm) 431

Description of adjustments: Sale of assets, agio/disagio and gain/losses on financial instruments

Key figures 2011 2012 2013E 2014E 2015ERevenue (USDm) 31 57 57 94 88EBITDA (USDm) 5 29 35 64 57EBITDA, adj. (USDm) 5 29 35 64 57EBIT, adj. (USDm) 1 22 26 47 38Pre-tax profit, adj. (USDm) 2 21 23 40 32Net income, adj. (USDm) -1 22 19 36 28EPS, adj. (USD) -0.02 0.32 0.28 0.53 0.41OCFPS (USD) 0.1 0.4 0.4 0.8 0.7FCFPS (USD) -2.5 -0.4 -3.8 0.7 0.6BVPS (USD) 2.5 2.9 3.1 3.6 4.1Net asset value (NAV) (USD) 4.1 4.1 0.0 0.0 0.0Dividend (USD) 0.00 0.00 0.00 0.00 0.00EV/EBITDA, adj. (x) 56.2 8.1 12.2 6.0 6.0EV/EBIT, adj. (x) n.m. 10.9 16.8 8.2 9.1P/E, adj. (x) n.m. 10.9 9.5 5.0 6.3P/OCF (x) 48.8 8.4 6.7 3.3 3.8EV/FCF (x) n.m. n.m. n.m. 8.2 8.5P/Book (x) 1.9 1.2 0.8 0.7 0.6P/NAV (x) 1.2 0.9 n.m. n.m. n.m.Dividend yield (%) 0.0 0.0 0.0 0.0 0.0

Key Assumptions 2011 2012 2013E 2014E 2015EShort term T/C, USD/Day 95 500 125 000 82 000 85 000Short term T/C, USD/Day old tonnage 51 000 36 000 40 000 40 000

Result Preview 15-Apr-13

13

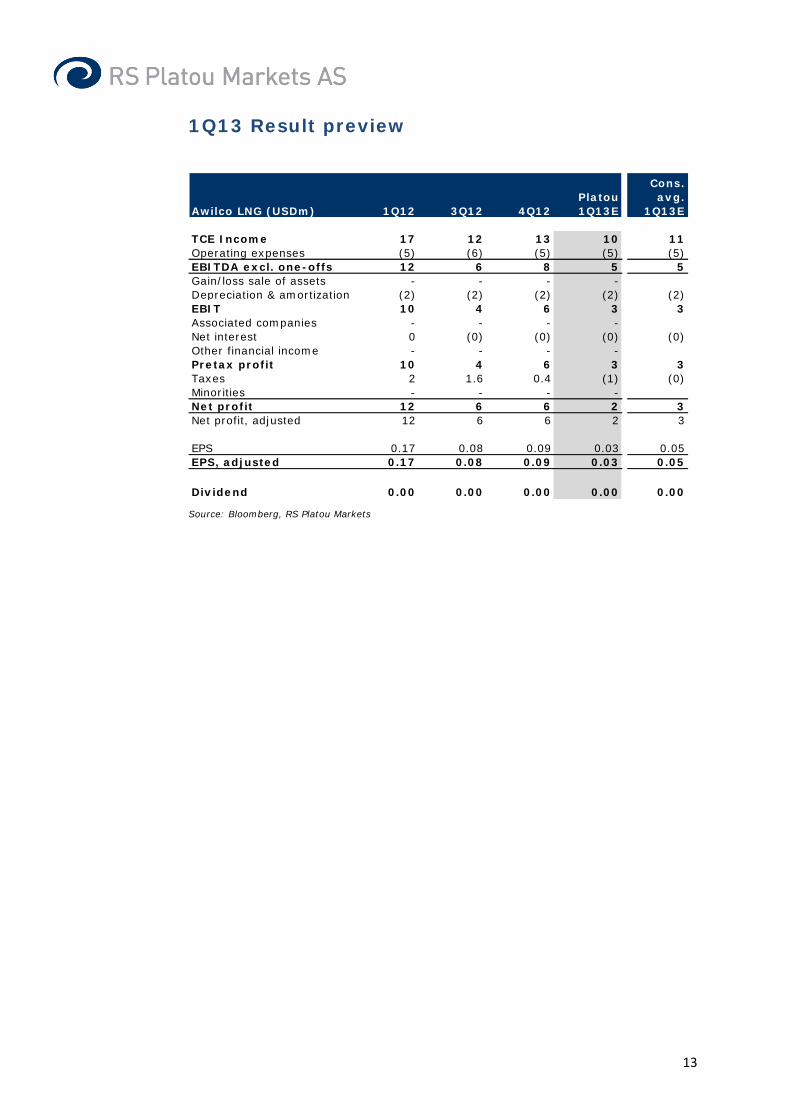

1Q13 Result preview

Source: Bloomberg, RS Platou Markets

Awilco LNG (USDm) 1Q12 3Q12 4Q12Platou 1Q13E

Cons. avg.

1Q13E

TCE Income 17 12 13 10 11Operating expenses (5) (6) (5) (5) (5)EBITDA excl. one-offs 12 6 8 5 5Gain/loss sale of assets - - - -Depreciation & amortization (2) (2) (2) (2) (2)EBIT 10 4 6 3 3Associated companies - - - -Net interest 0 (0) (0) (0) (0)Other financial income - - - -Pretax profit 10 4 6 3 3Taxes 2 1.6 0.4 (1) (0)Minorities - - - -Net profit 12 6 6 2 3Net profit, adjusted 12 6 6 2 3

EPS 0.17 0.08 0.09 0.03 0.05EPS, adjusted 0.17 0.08 0.09 0.03 0.05

Dividend 0.00 0.00 0.00 0.00 0.00

14

Profit and loss (USDm) 2011 2012 2013E 2014E 2015ETotal revenue 31 57 57 94 88Voyage expenses & commissions -10 -4 -2 -2 -2Time-charter equivalent 21 52 55 92 86

Operating expenses -15 -23 -20 -28 -28

EBITDA, adj. 5 29 35 64 57Gain/loss sale of assets 0 0 0 0 0EBITDA 5 29 35 64 57Depreciation -4 -8 -10 -17 -19Amortization/Write down 0 -1 0 0 0EBIT 1 20 26 47 38EBIT, adj. 1 22 26 47 38

Associated companies 0 0 0 0 0Net interest 0 0 -3 -7 -6Gains/losses on securities or financial instruments 0 0 0 0 0Other financial Items -1Pre-tax profit 0 20 23 40 32Tax -3 2 -4 -4 -4Minorities 0 0 0 0 0Result from discontinued operations/ Other 0 0 0 0 0Net income -2 22 19 36 28

Adjustments after tax 1 0 0 0 0Adjusted net income -1 22 19 36 28

EPS (USD) -0.04 0.32 0.28 0.53 0.41EPS, adj. (USD) -0.02 0.32 0.28 0.53 0.41

Balance sheet (USDm) 2011 2012 2013E 2014E 2015ELong-term interest bearing assets 0 0 0 0 0Fixed assets 149 196 467 456 444Other long-term assets 0 0 0 0Long-term assets 149 196 467 457 444

Other current assets 5 5 4 7 6Cash and liquid assets 28 3 26 57 81Current assets 33 7 30 64 88

Total assets 182 203 497 521 532

Equity 172 193 212 247 275

Minorities 0 0 0 0 0

Long term interest bearing debt 0 0 280 264 248Finance obligation 0 0 0 0 0Other long-term liabilities 2 0 0 0 0Long term liabilities 2 0 280 264 248

Short term interest bearing debt 0 2 0 0 0Other short term liabilities 9 8 5 9 8Current liabilities 9 9 5 9 8

Total liabilities and equity 182 203 497 521 532

Working capital -4 -3 -1 -2 -2Net debt -28 -1 254 207 167

Cash flow (USDm) 2011 2012 2013E 2014E 2015EPre-tax profit 0 20 23 40 32- Associated companies 0 0 0 0 0+ Depreciation and amortization 4 9 10 17 19- Payable tax -3 2 -4 -4 -4+/- Other operating items 0 -2 0 0 0Cash flow from operations 2 29 28 53 47

Change in working capital 4 -1 -2 1 0Operating cash flow 6 28 26 53 47

Maintenance capex 0 -13 -1 -7 -7Growth capex -151 -43 -280 0 0Acquisition capex 0 0 0 0 0Sale of assets 0 0 0 0 0Cash flow from investments -151 -56 -281 -7 -7

Free cash flow -145 -27 -255 47 40

Dividend paid 0 0 0 0 0Share buy back 0 0 0 0 0Equity increase 132 0 0 0 0Cash flow from financing 132 0 0 0 0

Other items 42 0 0 0 0

Change in net debt -28 28 255 -47 -40

15

Analyst: Frode Mørkedal Tel: +47 22 01 63 27 E-mail: [email protected] Next report date: 30.04.2013 Disclosure:

Analyst: Herman Hildan Tel: +47 22 01 63 53 E-mail: [email protected]

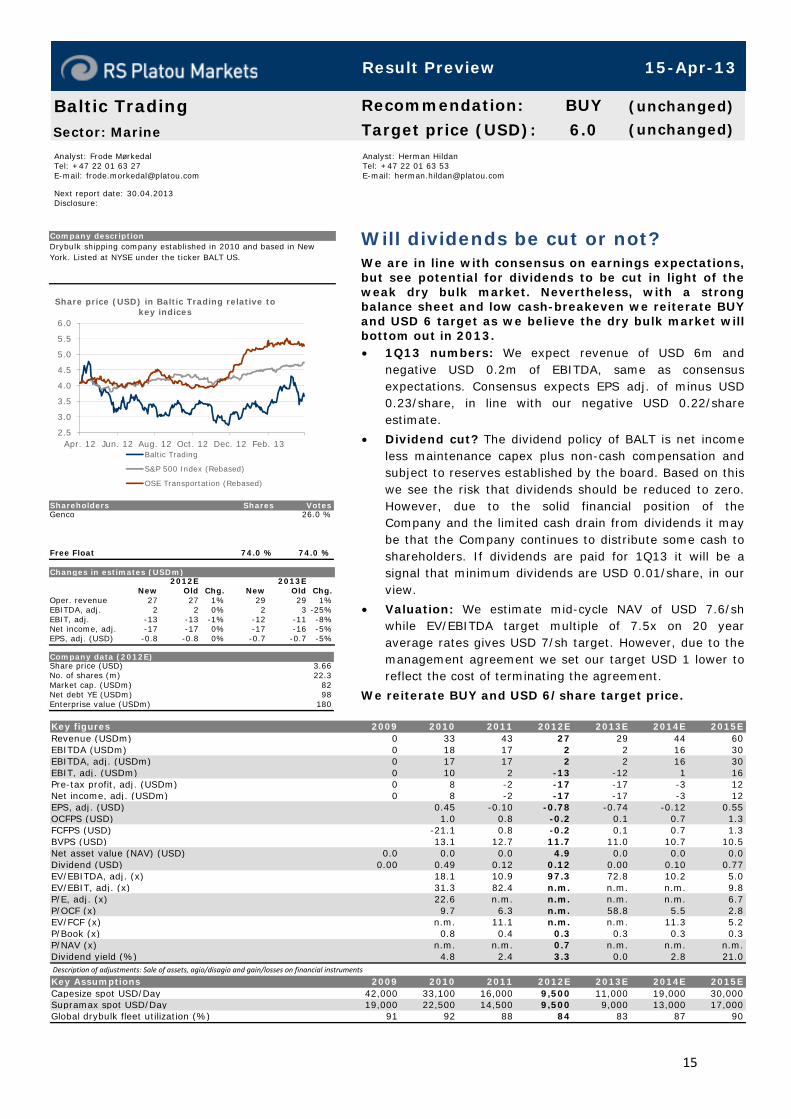

Will dividends be cut or not? We are in line with consensus on earnings expectations,but see potential for dividends to be cut in light of theweak dry bulk market. Nevertheless, with a strongbalance sheet and low cash-breakeven we reiterate BUYand USD 6 target as we believe the dry bulk market willbottom out in 2013. • 1Q13 numbers: We expect revenue of USD 6m and

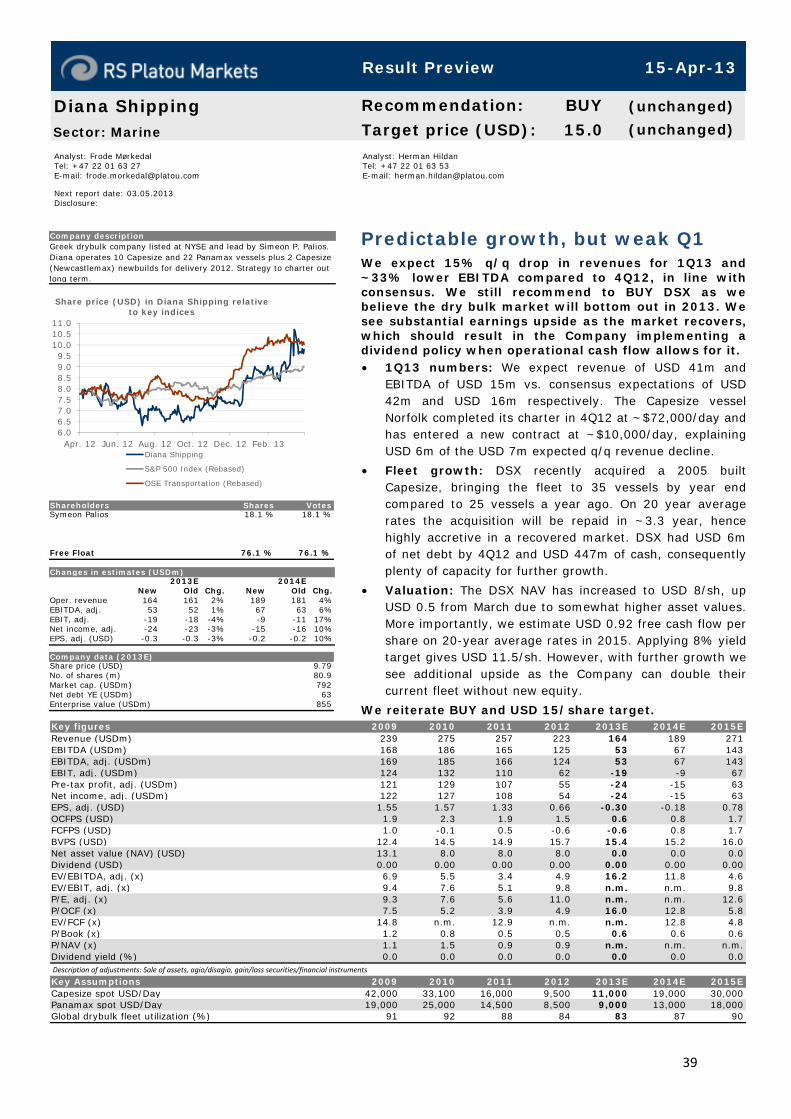

negative USD 0.2m of EBITDA, same as consensusexpectations. Consensus expects EPS adj. of minus USD0.23/share, in line with our negative USD 0.22/shareestimate.

• Dividend cut? The dividend policy of BALT is net incomeless maintenance capex plus non-cash compensation andsubject to reserves established by the board. Based on thiswe see the risk that dividends should be reduced to zero.However, due to the solid financial position of theCompany and the limited cash drain from dividends it maybe that the Company continues to distribute some cash toshareholders. If dividends are paid for 1Q13 it will be asignal that minimum dividends are USD 0.01/share, in ourview.

• Valuation: We estimate mid-cycle NAV of USD 7.6/shwhile EV/EBITDA target multiple of 7.5x on 20 yearaverage rates gives USD 7/sh target. However, due to themanagement agreement we set our target USD 1 lower toreflect the cost of terminating the agreement.

We reiterate BUY and USD 6/share target price.

Baltic TradingSector: Marine

Recommendation: BUY (unchanged)

Target price (USD): 6.0 (unchanged)

Company descriptionDrybulk shipping company established in 2010 and based in New York. Listed at NYSE under the ticker BALT US.

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Apr. 12 Jun. 12 Aug. 12 Oct. 12 Dec. 12 Feb. 13

Share price (USD) in Baltic Trading relative to key indices

Baltic Trading

S&P 500 Index (Rebased)

OSE Transportation (Rebased)

Shareholders Shares VotesGenco 26.0 %

Free Float 74.0 % 74.0 %

Changes in estimates (USDm)2012E 2013E

New Old Chg. New Old Chg.Oper. revenue 27 27 1% 29 29 1%EBITDA, adj. 2 2 0% 2 3 -25%EBIT, adj. -13 -13 -1% -12 -11 -8%Net income, adj. -17 -17 0% -17 -16 -5%EPS, adj. (USD) -0.8 -0.8 0% -0.7 -0.7 -5%

Company data (2012E)Share price (USD) 3.66No. of shares (m) 22.3Market cap. (USDm) 82Net debt YE (USDm) 98Enterprise value (USDm) 180

Description of adjustments: Sale of assets, agio/disagio and gain/losses on financial instruments

Key figures 2009 2010 2011 2012E 2013E 2014E 2015ERevenue (USDm) 0 33 43 27 29 44 60EBITDA (USDm) 0 18 17 2 2 16 30EBITDA, adj. (USDm) 0 17 17 2 2 16 30EBIT, adj. (USDm) 0 10 2 -13 -12 1 16Pre-tax profit, adj. (USDm) 0 8 -2 -17 -17 -3 12Net income, adj. (USDm) 0 8 -2 -17 -17 -3 12EPS, adj. (USD) 0.45 -0.10 -0.78 -0.74 -0.12 0.55OCFPS (USD) 1.0 0.8 -0.2 0.1 0.7 1.3FCFPS (USD) -21.1 0.8 -0.2 0.1 0.7 1.3BVPS (USD) 13.1 12.7 11.7 11.0 10.7 10.5Net asset value (NAV) (USD) 0.0 0.0 0.0 4.9 0.0 0.0 0.0Dividend (USD) 0.00 0.49 0.12 0.12 0.00 0.10 0.77EV/EBITDA, adj. (x) 18.1 10.9 97.3 72.8 10.2 5.0EV/EBIT, adj. (x) 31.3 82.4 n.m. n.m. n.m. 9.8P/E, adj. (x) 22.6 n.m. n.m. n.m. n.m. 6.7P/OCF (x) 9.7 6.3 n.m. 58.8 5.5 2.8EV/FCF (x) n.m. 11.1 n.m. n.m. 11.3 5.2P/Book (x) 0.8 0.4 0.3 0.3 0.3 0.3P/NAV (x) n.m. n.m. 0.7 n.m. n.m. n.m.Dividend yield (%) 4.8 2.4 3.3 0.0 2.8 21.0

Key Assumptions 2009 2010 2011 2012E 2013E 2014E 2015ECapesize spot USD/Day 42,000 33,100 16,000 9,500 11,000 19,000 30,000Supramax spot USD/Day 19,000 22,500 14,500 9,500 9,000 13,000 17,000Global drybulk fleet utilization (%) 91 92 88 84 83 87 90

Result Preview 15-Apr-13

16

1Q13 Result preview

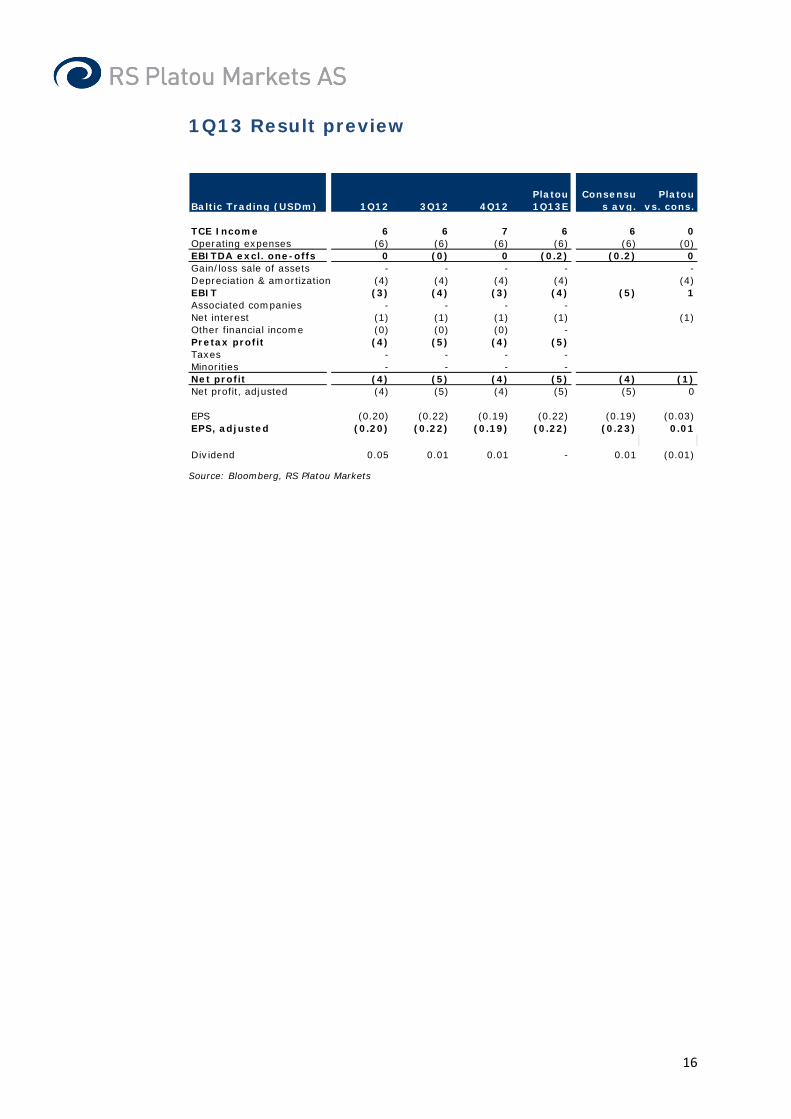

Source: Bloomberg, RS Platou Markets

Baltic Trading (USDm) 1Q12 3Q12 4Q12Platou 1Q13E

Consensus avg.

Platou vs. cons.

TCE Income 6 6 7 6 6 0Operating expenses (6) (6) (6) (6) (6) (0)EBITDA excl. one-offs 0 (0) 0 (0.2) (0.2) 0Gain/loss sale of assets - - - - -Depreciation & amortization (4) (4) (4) (4) (4)EBIT (3) (4) (3) (4) (5) 1Associated companies - - - -Net interest (1) (1) (1) (1) (1)Other financial income (0) (0) (0) -Pretax profit (4) (5) (4) (5)Taxes - - - -Minorities - - - -Net profit (4) (5) (4) (5) (4) (1)Net profit, adjusted (4) (5) (4) (5) (5) 0

EPS (0.20) (0.22) (0.19) (0.22) (0.19) (0.03)EPS, adjusted (0.20) (0.22) (0.19) (0.22) (0.23) 0.01

Dividend 0.05 0.01 0.01 - 0.01 (0.01)

17

Profit and loss (USDm) 2009 2010 2011 2012E 2013E 2014E 2015ETotal revenue 0 33 43 27 29 44 60Voyage expenses & commissions 0 -1 -1 -1 -2 -2 -3Time-charter equivalent 0 32 42 26 28 42 57

Operating expenses 0 -14 -25 -24 -25 -26 -26

EBITDA, adj. 0 17 17 2 2 16 30Gain/loss sale of assets 0 0 0 0 0 0 0EBITDA 0 18 17 2 2 16 30Depreciation 0 -7 -15 -15 -15 -15 -15Amortization/Write down 0 0 0 0 0 0 0EBIT 0 10 2 -13 -12 1 16EBIT, adj. 0 10 2 -13 -12 1 16

Associated companies 0 0 0 0 0 0 0Net interest 0 -2 -5 -4 -4 -4 -3Gains/losses on securities or financial instruments 0 0 0 0 0 0 0Other financial Items 0 0Pre-tax profit 0 8 -2 -17 -17 -3 12Tax 0 0 0 0 0 0 0Minorities 0 0 0 0 0 0 0Result from discontinued operations/ Other 0 0 0 0 0 0 0Net income 0 8 -2 -17 -17 -3 12

Adjustments after tax 0 0 0 0 0 0 0Adjusted net income 0 8 -2 -17 -17 -3 12

EPS (USD) 0.46 -0.10 -0.78 -0.74 -0.12 0.55EPS, adj. (USD) 0.45 -0.10 -0.78 -0.74 -0.12 0.55

Balance sheet (USDm) 2009 2010 2011 2012E 2013E 2014E 2015ELong-term interest bearing assets 0 0 0 0 0 0 0Fixed assets 0 382 367 355 340 326 311Other long-term assets 1 1 2 2 2 2Long-term assets 0 383 368 357 342 328 313

Other current assets 4 5 4 4 6 8Cash and liquid assets 0 8 10 3 5 17 28Current assets 0 12 15 7 9 23 37

Total assets 0 395 383 364 351 351 350

Equity 0 289 281 261 244 239 234

Minorities 0 0 0 0 0 0 0

Long term interest bearing debt 0 92 82 101 101 101 100Finance obligation 0 0 0 0 0 0 0Other long-term liabilities 3 3 7 10Long term liabilities 0 92 86 101 105 108 110

Short term interest bearing debt 0 7 7 0 0 0 0Other short term liabilities 0 7 9 2 3 4 5Current liabilities 0 14 17 2 3 4 5

Total liabilities and equity 0 395 383 364 351 351 350

Working capital 0 -3 -4 1 1 2 3Net debt 0 92 80 98 97 84 72

Cash flow (USDm) 2009 2010 2011 2012E 2013E 2014E 2015EPre-tax profit 0 8 -2 -17 -17 -3 12- Associated companies 0 0 0 0 0 0 0+ Depreciation and amortization 0 7 15 15 15 15 15- Payable tax 0 0 0 0 0 0 0+/- Other operating items 0 0 3 3 3 3 3Cash flow from operations 0 16 16 1 1 15 30

Change in working capital 0 3 1 -5 0 -1 -1Operating cash flow 0 19 17 -4 1 15 30

Maintenance capex 0 0 0 0 0 0 0Growth capex 0 -387 0 0 0 0 0Acquisition capex 0 -12 0 0 0 0 0Sale of assets 0 0 0 0 0 0 0Cash flow from investments 0 -399 0 0 0 0 0

Free cash flow 0 -380 17 -4 1 15 30

Dividend paid 0 -7 -5 -5 0 -2 -17Share buy back 0 0 0 0 0 0 0Equity increase 0 285 0 0 0 0 0Cash flow from financing 0 278 -5 -5 0 -2 -17

Other items 0 10 0 -8 0 0 0

Change in net debt 0 92 -12 18 -1 -12 -12

18

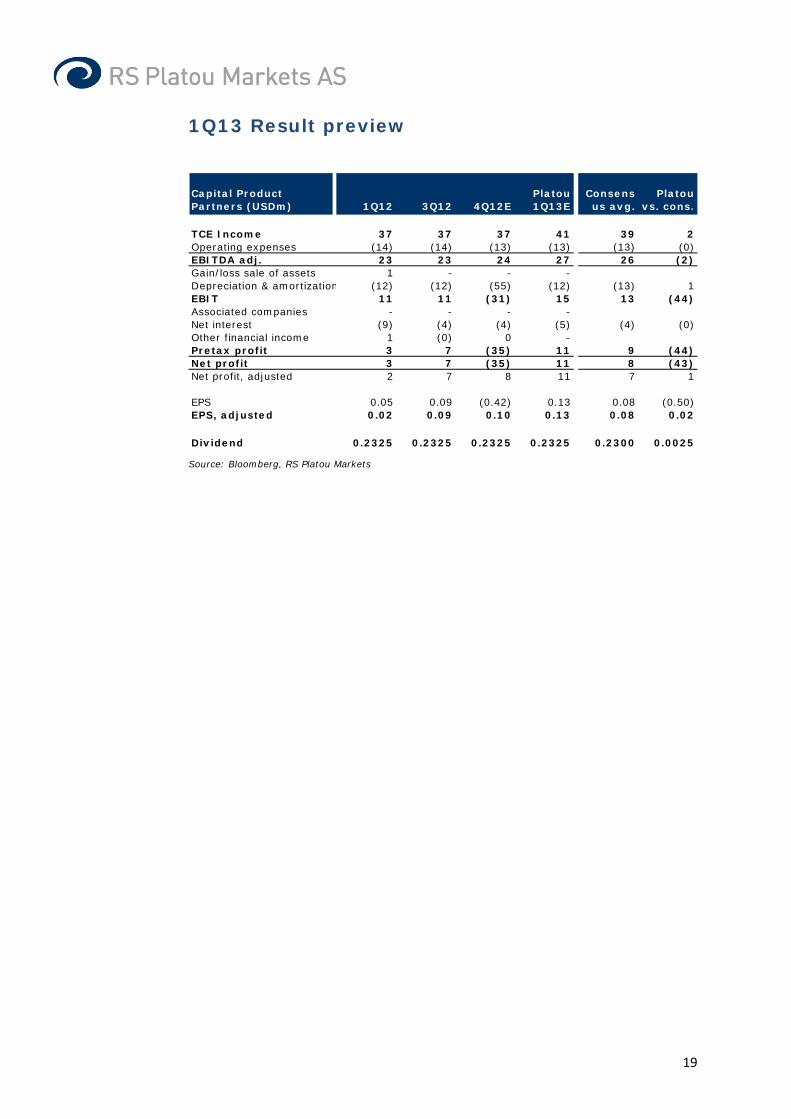

Analyst: Frode Mørkedal Tel: +47 22 01 63 27 E-mail: [email protected] Next report date: 02.05.2013 Disclosure:

Analyst: Herman Hildan Tel: +47 22 01 63 53 E-mail: [email protected]

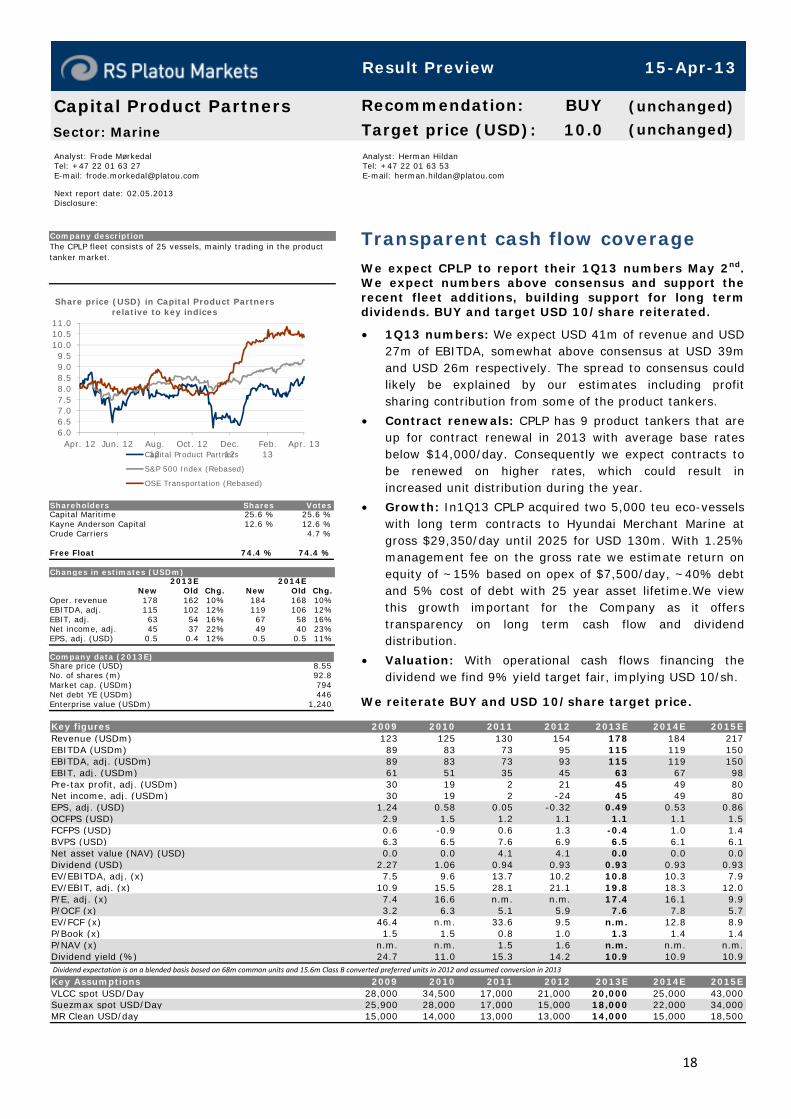

Transparent cash flow coverage We expect CPLP to report their 1Q13 numbers May 2nd.We expect numbers above consensus and support therecent fleet additions, building support for long termdividends. BUY and target USD 10/share reiterated.

• 1Q13 numbers: We expect USD 41m of revenue and USD27m of EBITDA, somewhat above consensus at USD 39mand USD 26m respectively. The spread to consensus couldlikely be explained by our estimates including profitsharing contribution from some of the product tankers.

• Contract renewals: CPLP has 9 product tankers that areup for contract renewal in 2013 with average base ratesbelow $14,000/day. Consequently we expect contracts tobe renewed on higher rates, which could result inincreased unit distribution during the year.

• Growth: In1Q13 CPLP acquired two 5,000 teu eco-vesselswith long term contracts to Hyundai Merchant Marine atgross $29,350/day until 2025 for USD 130m. With 1.25%management fee on the gross rate we estimate return onequity of ~15% based on opex of $7,500/day, ~40% debtand 5% cost of debt with 25 year asset lifetime.We viewthis growth important for the Company as it offerstransparency on long term cash flow and dividenddistribution.

• Valuation: With operational cash flows financing thedividend we find 9% yield target fair, implying USD 10/sh.

We reiterate BUY and USD 10/share target price.

Capital Product PartnersSector: Marine

Recommendation: BUY (unchanged)

Target price (USD): 10.0 (unchanged)

Company descriptionThe CPLP fleet consists of 25 vessels, mainly trading in the product tanker market.

6.06.57.07.58.08.59.09.5

10.010.511.0

Apr. 12 Jun. 12 Aug.12

Oct. 12 Dec.12

Feb.13

Apr. 13

Share price (USD) in Capital Product Partners relative to key indices

Capital Product Partners

S&P 500 Index (Rebased)

OSE Transportation (Rebased)

Shareholders Shares VotesCapital Maritime 25.6 % 25.6 %Kayne Anderson Capital 12.6 % 12.6 %Crude Carriers 4.7 %

Free Float 74.4 % 74.4 %

Changes in estimates (USDm)2013E 2014E

New Old Chg. New Old Chg.Oper. revenue 178 162 10% 184 168 10%EBITDA, adj. 115 102 12% 119 106 12%EBIT, adj. 63 54 16% 67 58 16%Net income, adj. 45 37 22% 49 40 23%EPS, adj. (USD) 0.5 0.4 12% 0.5 0.5 11%

Company data (2013E)Share price (USD) 8.55No. of shares (m) 92.8Market cap. (USDm) 794Net debt YE (USDm) 446Enterprise value (USDm) 1,240

Dividend expectation is on a blended basis based on 68m common units and 15.6m Class B converted preferred units in 2012 and assumed conversion in 2013

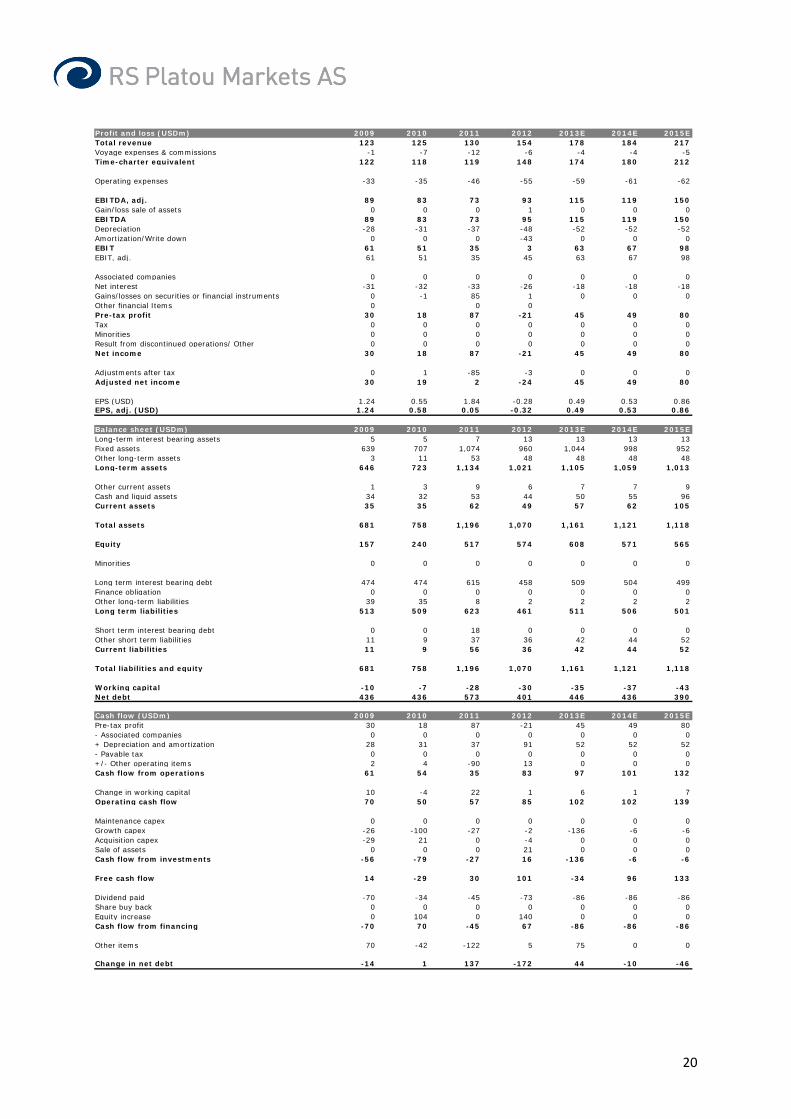

Key figures 2009 2010 2011 2012 2013E 2014E 2015ERevenue (USDm) 123 125 130 154 178 184 217EBITDA (USDm) 89 83 73 95 115 119 150EBITDA, adj. (USDm) 89 83 73 93 115 119 150EBIT, adj. (USDm) 61 51 35 45 63 67 98Pre-tax profit, adj. (USDm) 30 19 2 21 45 49 80Net income, adj. (USDm) 30 19 2 -24 45 49 80EPS, adj. (USD) 1.24 0.58 0.05 -0.32 0.49 0.53 0.86OCFPS (USD) 2.9 1.5 1.2 1.1 1.1 1.1 1.5FCFPS (USD) 0.6 -0.9 0.6 1.3 -0.4 1.0 1.4BVPS (USD) 6.3 6.5 7.6 6.9 6.5 6.1 6.1Net asset value (NAV) (USD) 0.0 0.0 4.1 4.1 0.0 0.0 0.0Dividend (USD) 2.27 1.06 0.94 0.93 0.93 0.93 0.93EV/EBITDA, adj. (x) 7.5 9.6 13.7 10.2 10.8 10.3 7.9EV/EBIT, adj. (x) 10.9 15.5 28.1 21.1 19.8 18.3 12.0P/E, adj. (x) 7.4 16.6 n.m. n.m. 17.4 16.1 9.9P/OCF (x) 3.2 6.3 5.1 5.9 7.6 7.8 5.7EV/FCF (x) 46.4 n.m. 33.6 9.5 n.m. 12.8 8.9P/Book (x) 1.5 1.5 0.8 1.0 1.3 1.4 1.4P/NAV (x) n.m. n.m. 1.5 1.6 n.m. n.m. n.m.Dividend yield (%) 24.7 11.0 15.3 14.2 10.9 10.9 10.9

Key Assumptions 2009 2010 2011 2012 2013E 2014E 2015EVLCC spot USD/Day 28,000 34,500 17,000 21,000 20,000 25,000 43,000Suezmax spot USD/Day 25,900 28,000 17,000 15,000 18,000 22,000 34,000MR Clean USD/day 15,000 14,000 13,000 13,000 14,000 15,000 18,500

Result Preview 15-Apr-13

19

1Q13 Result preview

Source: Bloomberg, RS Platou Markets

Capital Product Partners (USDm) 1Q12 3Q12 4Q12E

Platou 1Q13E

Consensus avg.

Platou vs. cons.

TCE Income 37 37 37 41 39 2Operating expenses (14) (14) (13) (13) (13) (0)EBITDA adj. 23 23 24 27 26 (2)Gain/loss sale of assets 1 - - -Depreciation & amortization (12) (12) (55) (12) (13) 1EBIT 11 11 (31) 15 13 (44)Associated companies - - - -Net interest (9) (4) (4) (5) (4) (0)Other financial income 1 (0) 0 -Pretax profit 3 7 (35) 11 9 (44)Net profit 3 7 (35) 11 8 (43)Net profit, adjusted 2 7 8 11 7 1

EPS 0.05 0.09 (0.42) 0.13 0.08 (0.50)EPS, adjusted 0.02 0.09 0.10 0.13 0.08 0.02

Dividend 0.2325 0.2325 0.2325 0.2325 0.2300 0.0025

20

Profit and loss (USDm) 2009 2010 2011 2012 2013E 2014E 2015ETotal revenue 123 125 130 154 178 184 217Voyage expenses & commissions -1 -7 -12 -6 -4 -4 -5Time-charter equivalent 122 118 119 148 174 180 212

Operating expenses -33 -35 -46 -55 -59 -61 -62

EBITDA, adj. 89 83 73 93 115 119 150Gain/loss sale of assets 0 0 0 1 0 0 0EBITDA 89 83 73 95 115 119 150Depreciation -28 -31 -37 -48 -52 -52 -52Amortization/Write down 0 0 0 -43 0 0 0EBIT 61 51 35 3 63 67 98EBIT, adj. 61 51 35 45 63 67 98

Associated companies 0 0 0 0 0 0 0Net interest -31 -32 -33 -26 -18 -18 -18Gains/losses on securities or financial instruments 0 -1 85 1 0 0 0Other financial Items 0 0 0Pre-tax profit 30 18 87 -21 45 49 80Tax 0 0 0 0 0 0 0Minorities 0 0 0 0 0 0 0Result from discontinued operations/ Other 0 0 0 0 0 0 0Net income 30 18 87 -21 45 49 80

Adjustments after tax 0 1 -85 -3 0 0 0Adjusted net income 30 19 2 -24 45 49 80

EPS (USD) 1.24 0.55 1.84 -0.28 0.49 0.53 0.86EPS, adj. (USD) 1.24 0.58 0.05 -0.32 0.49 0.53 0.86

Balance sheet (USDm) 2009 2010 2011 2012 2013E 2014E 2015ELong-term interest bearing assets 5 5 7 13 13 13 13Fixed assets 639 707 1,074 960 1,044 998 952Other long-term assets 3 11 53 48 48 48 48Long-term assets 646 723 1,134 1,021 1,105 1,059 1,013

Other current assets 1 3 9 6 7 7 9Cash and liquid assets 34 32 53 44 50 55 96Current assets 35 35 62 49 57 62 105

Total assets 681 758 1,196 1,070 1,161 1,121 1,118

Equity 157 240 517 574 608 571 565

Minorities 0 0 0 0 0 0 0

Long term interest bearing debt 474 474 615 458 509 504 499Finance obligation 0 0 0 0 0 0 0Other long-term liabilities 39 35 8 2 2 2 2Long term liabilities 513 509 623 461 511 506 501

Short term interest bearing debt 0 0 18 0 0 0 0Other short term liabilities 11 9 37 36 42 44 52Current liabilities 11 9 56 36 42 44 52

Total liabilities and equity 681 758 1,196 1,070 1,161 1,121 1,118

Working capital -10 -7 -28 -30 -35 -37 -43Net debt 436 436 573 401 446 436 390

Cash flow (USDm) 2009 2010 2011 2012 2013E 2014E 2015EPre-tax profit 30 18 87 -21 45 49 80- Associated companies 0 0 0 0 0 0 0+ Depreciation and amortization 28 31 37 91 52 52 52- Payable tax 0 0 0 0 0 0 0+/- Other operating items 2 4 -90 13 0 0 0Cash flow from operations 61 54 35 83 97 101 132

Change in working capital 10 -4 22 1 6 1 7Operating cash flow 70 50 57 85 102 102 139

Maintenance capex 0 0 0 0 0 0 0Growth capex -26 -100 -27 -2 -136 -6 -6Acquisition capex -29 21 0 -4 0 0 0Sale of assets 0 0 0 21 0 0 0Cash flow from investments -56 -79 -27 16 -136 -6 -6

Free cash flow 14 -29 30 101 -34 96 133

Dividend paid -70 -34 -45 -73 -86 -86 -86Share buy back 0 0 0 0 0 0 0Equity increase 0 104 0 140 0 0 0Cash flow from financing -70 70 -45 67 -86 -86 -86

Other items 70 -42 -122 5 75 0 0

Change in net debt -14 1 137 -172 44 -10 -46

21

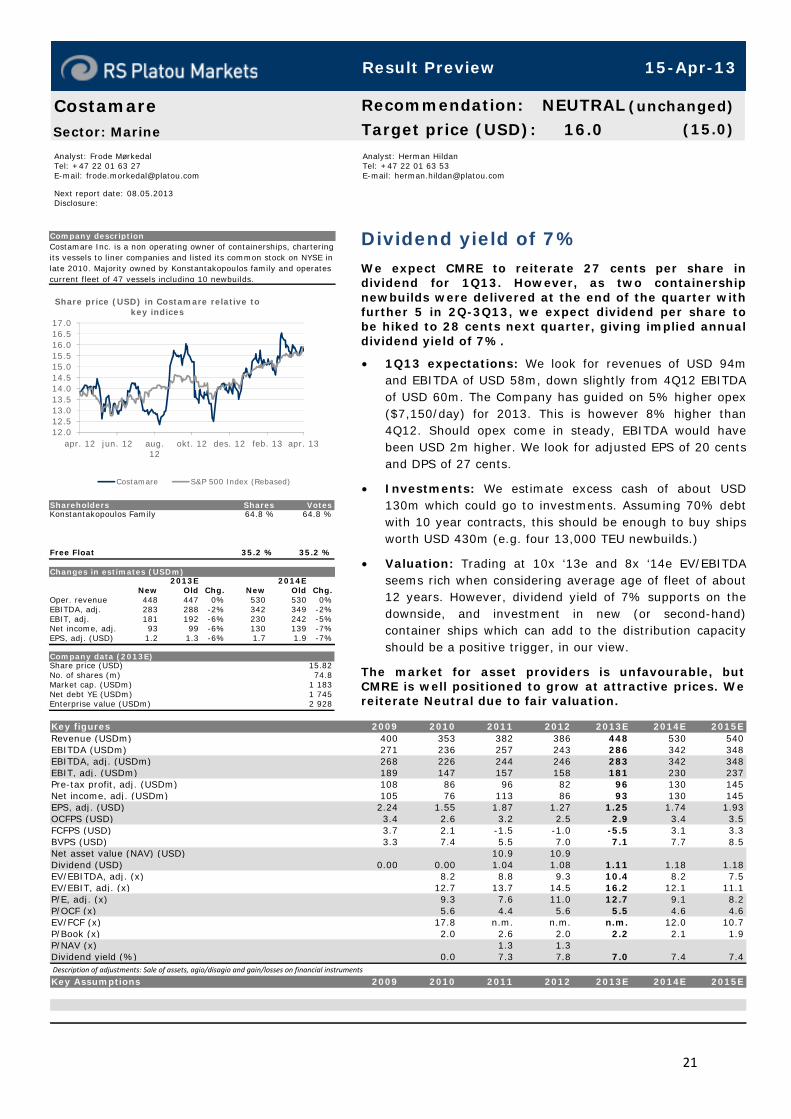

Analyst: Frode Mørkedal Tel: +47 22 01 63 27 E-mail: [email protected] Next report date: 08.05.2013 Disclosure:

Analyst: Herman Hildan Tel: +47 22 01 63 53 E-mail: [email protected]

Dividend yield of 7% We expect CMRE to reiterate 27 cents per share individend for 1Q13. However, as two containershipnewbuilds were delivered at the end of the quarter withfurther 5 in 2Q-3Q13, we expect dividend per share to be hiked to 28 cents next quarter, giving implied annual dividend yield of 7%.

• 1Q13 expectations: We look for revenues of USD 94m and EBITDA of USD 58m, down slightly from 4Q12 EBITDAof USD 60m. The Company has guided on 5% higher opex($7,150/day) for 2013. This is however 8% higher than4Q12. Should opex come in steady, EBITDA would have been USD 2m higher. We look for adjusted EPS of 20 centsand DPS of 27 cents.

• Investments: We estimate excess cash of about USD 130m which could go to investments. Assuming 70% debtwith 10 year contracts, this should be enough to buy ships worth USD 430m (e.g. four 13,000 TEU newbuilds.)

• Valuation: Trading at 10x ‘13e and 8x ‘14e EV/EBITDA seems rich when considering average age of fleet of about12 years. However, dividend yield of 7% supports on thedownside, and investment in new (or second-hand) container ships which can add to the distribution capacityshould be a positive trigger, in our view.

The market for asset providers is unfavourable, but CMRE is well positioned to grow at attractive prices. We reiterate Neutral due to fair valuation.

CostamareSector: Marine

Recommendation: NEUTRAL (unchanged)

Target price (USD): 16.0 (15.0)

Company descriptionCostamare Inc. is a non operating owner of containerships, chartering its vessels to liner companies and listed its common stock on NYSE in late 2010. Majority owned by Konstantakopoulos family and operates current fleet of 47 vessels including 10 newbuilds.

12.012.513.013.514.014.515.015.516.016.517.0

apr. 12 jun. 12 aug.12

okt. 12 des. 12 feb. 13 apr. 13

Share price (USD) in Costamare relative to key indices

Costamare S&P 500 Index (Rebased)

Shareholders Shares VotesKonstantakopoulos Family 64.8 % 64.8 %

Free Float 35.2 % 35.2 %

Changes in estimates (USDm)2013E 2014E

New Old Chg. New Old Chg.Oper. revenue 448 447 0% 530 530 0%EBITDA, adj. 283 288 -2% 342 349 -2%EBIT, adj. 181 192 -6% 230 242 -5%Net income, adj. 93 99 -6% 130 139 -7%EPS, adj. (USD) 1.2 1.3 -6% 1.7 1.9 -7%

Company data (2013E)Share price (USD) 15.82No. of shares (m) 74.8Market cap. (USDm) 1 183Net debt YE (USDm) 1 745Enterprise value (USDm) 2 928

Description of adjustments: Sale of assets, agio/disagio and gain/losses on financial instruments

Key figures 2009 2010 2011 2012 2013E 2014E 2015ERevenue (USDm) 400 353 382 386 448 530 540EBITDA (USDm) 271 236 257 243 286 342 348EBITDA, adj. (USDm) 268 226 244 246 283 342 348EBIT, adj. (USDm) 189 147 157 158 181 230 237Pre-tax profit, adj. (USDm) 108 86 96 82 96 130 145Net income, adj. (USDm) 105 76 113 86 93 130 145EPS, adj. (USD) 2.24 1.55 1.87 1.27 1.25 1.74 1.93OCFPS (USD) 3.4 2.6 3.2 2.5 2.9 3.4 3.5FCFPS (USD) 3.7 2.1 -1.5 -1.0 -5.5 3.1 3.3BVPS (USD) 3.3 7.4 5.5 7.0 7.1 7.7 8.5Net asset value (NAV) (USD) 10.9 10.9Dividend (USD) 0.00 0.00 1.04 1.08 1.11 1.18 1.18EV/EBITDA, adj. (x) 8.2 8.8 9.3 10.4 8.2 7.5EV/EBIT, adj. (x) 12.7 13.7 14.5 16.2 12.1 11.1P/E, adj. (x) 9.3 7.6 11.0 12.7 9.1 8.2P/OCF (x) 5.6 4.4 5.6 5.5 4.6 4.6EV/FCF (x) 17.8 n.m. n.m. n.m. 12.0 10.7P/Book (x) 2.0 2.6 2.0 2.2 2.1 1.9P/NAV (x) 1.3 1.3Dividend yield (%) 0.0 7.3 7.8 7.0 7.4 7.4

Key Assumptions 2009 2010 2011 2012 2013E 2014E 2015E

Result Preview 15-Apr-13

22

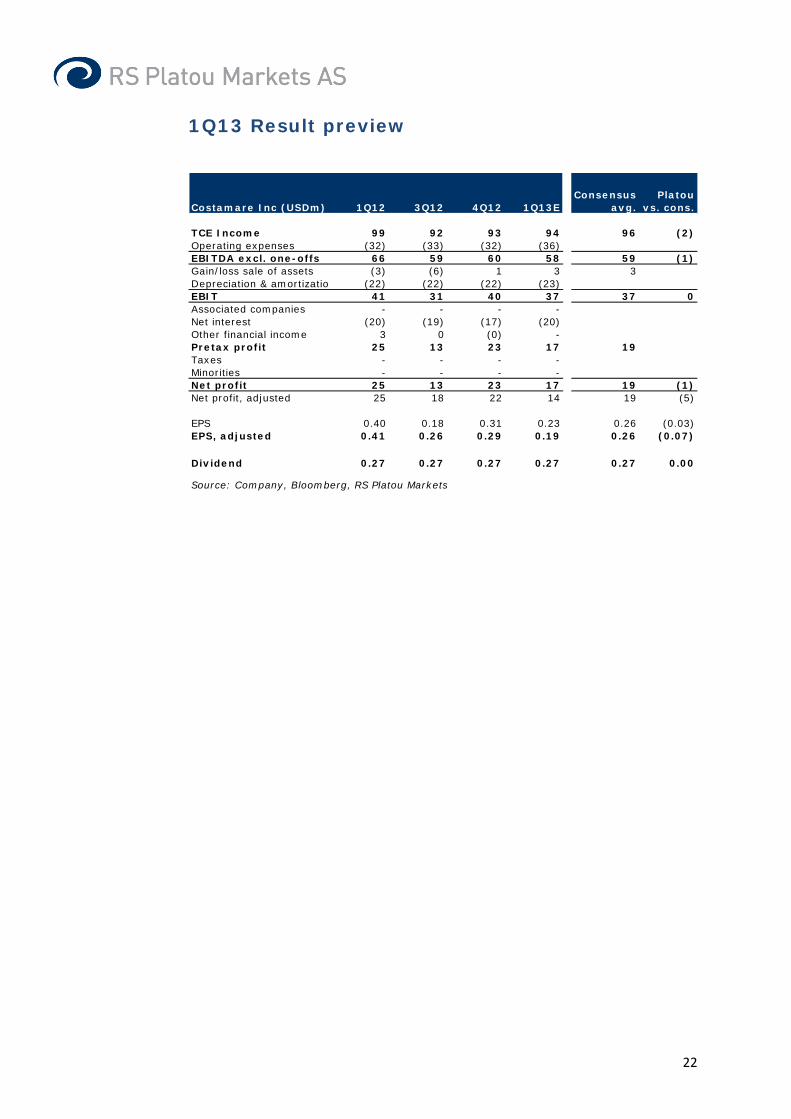

1Q13 Result preview

Costamare Inc (USDm) 1Q12 3Q12 4Q12 1Q13EConsensus

avg.Platou

vs. cons.

TCE Income 99 92 93 94 96 (2)Operating expenses (32) (33) (32) (36)EBITDA excl. one-offs 66 59 60 58 59 (1)Gain/loss sale of assets (3) (6) 1 3 3Depreciation & amortizatio (22) (22) (22) (23)EBIT 41 31 40 37 37 0Associated companies - - - -Net interest (20) (19) (17) (20)Other financial income 3 0 (0) -Pretax profit 25 13 23 17 19Taxes - - - -Minorities - - - -Net profit 25 13 23 17 19 (1)Net profit, adjusted 25 18 22 14 19 (5)

EPS 0.40 0.18 0.31 0.23 0.26 (0.03)EPS, adjusted 0.41 0.26 0.29 0.19 0.26 (0.07)

Dividend 0.27 0.27 0.27 0.27 0.27 0.00

Source: Company, Bloomberg, RS Platou Markets

23

Profit and loss (USDm) 2009 2010 2011 2012 2013E 2014E 2015ETotal revenue 400 353 382 386 448 530 540Voyage expenses & commissions -3 -2 -7 -8 -7 -8 -8Time-charter equivalent 397 351 375 378 441 522 532

Operating expenses -128 -125 -131 -132 -158 -180 -183

EBITDA, adj. 268 226 244 246 283 342 348Gain/loss sale of assets 3 10 13 -3 3 0 0EBITDA 271 236 257 243 286 342 348Depreciation -71 -71 -79 -80 -93 -103 -104Amortization/Write down -8 -8 -8 -8 -8 -8 -8EBIT 192 156 171 155 184 230 237EBIT, adj. 189 147 157 158 181 230 237

Associated companies 0 0 0 0 0 0 0Net interest -84 -71 -75 -73 -88 -100 -92Gains/losses on securities or financial instruments 9 -4 -8 -1 0 0 0Other financial ItemsPre-tax profit 117 81 88 81 96 130 145Tax 0 0 0 0 0 0 0Minorities 0 0 0 0 0 0 0Result from discontinued operations/ Other 0 0 0 0 0 0 0Net income 117 81 88 81 96 130 145

Adjustments after tax -12 -5 -5 3 -3 0 0Adjusted net income 105 76 113 86 93 130 145

EPS (USD) 2.49 1.65 1.45 1.20 1.29 1.74 1.93EPS, adj. (USD) 2.24 1.55 1.87 1.27 1.25 1.74 1.93

Balance sheet (USDm) 2009 2010 2011 2012 2013E 2014E 2015ELong-term interest bearing assets 40 37 39 42 42 42 42Fixed assets 1 560 1 535 1 767 1 922 2 453 2 366 2 266Other long-term assets 62 45 38 48 48 48 48Long-term assets 1 662 1 618 1 844 2 011 2 542 2 456 2 356

Other current assets 36 51 41 27 36 43 44Cash and liquid assets 12 160 98 273 241 194 192Current assets 48 211 139 300 277 236 235

Total assets 1 710 1 829 1 983 2 311 2 819 2 692 2 591

Equity 155 362 330 520 535 577 633

Minorities 0 0 0 0 0 0 0

Long term interest bearing debt 1 342 1 227 1 290 1 400 1 865 1 675 1 515Finance obligation 29 54 125 0 0 0 0Other long-term liabilities 1 1 11 142 142 142 142Long term liabilities 1 372 1 282 1 426 1 541 2 007 1 817 1 656

Short term interest bearing debt 94 115 153 162 162 162 162Other short term liabilities 89 70 73 87 116 137 139Current liabilities 183 185 227 249 278 299 302

Total liabilities and equity 1 710 1 829 1 983 2 311 2 819 2 692 2 591

Working capital -53 -19 -33 -60 -79 -94 -96Net debt 1 383 1 145 1 307 1 247 1 745 1 601 1 443

Cash flow (USDm) 2009 2010 2011 2012 2013E 2014E 2015EPre-tax profit 117 81 88 81 96 130 145- Associated companies 0 0 0 0 0 0 0+ Depreciation and amortization 79 79 87 89 101 112 112- Payable tax 0 0 0 0 0 0 0+/- Other operating items -11 -4 17 -29 -3 0 0Cash flow from operations 185 156 192 141 195 242 256

Change in working capital -23 -29 4 27 20 15 2Operating cash flow 162 128 195 168 214 256 258

Maintenance capex 0 0 0 0 -10 -6 -12Growth capex -57 -55 -341 -200 -628 -19 0Acquisition capex 0 0 0 0 0 0 0Sale of assets 70 31 57 -37 8 0 0Cash flow from investments 13 -24 -284 -237 -629 -25 -12

Free cash flow 175 104 -89 -68 -415 231 246

Dividend paid -30 -10 -62 -71 -83 -88 -88Share buy back 0 0 0 0 0 0 0Equity increase 0 148 0 194 0 0 0Cash flow from financing -30 138 -62 123 -83 -88 -88

Other items -1 528 -4 -11 5 1 0 0

Change in net debt 1 383 -238 162 -59 497 -143 -158

24

Analyst: Frode Mørkedal Tel: +47 22 01 63 27 E-mail: [email protected] Next report date: 07.05.2013 Disclosure:

Analyst: Herman Hildan Tel: +47 22 01 63 53 E-mail: [email protected]

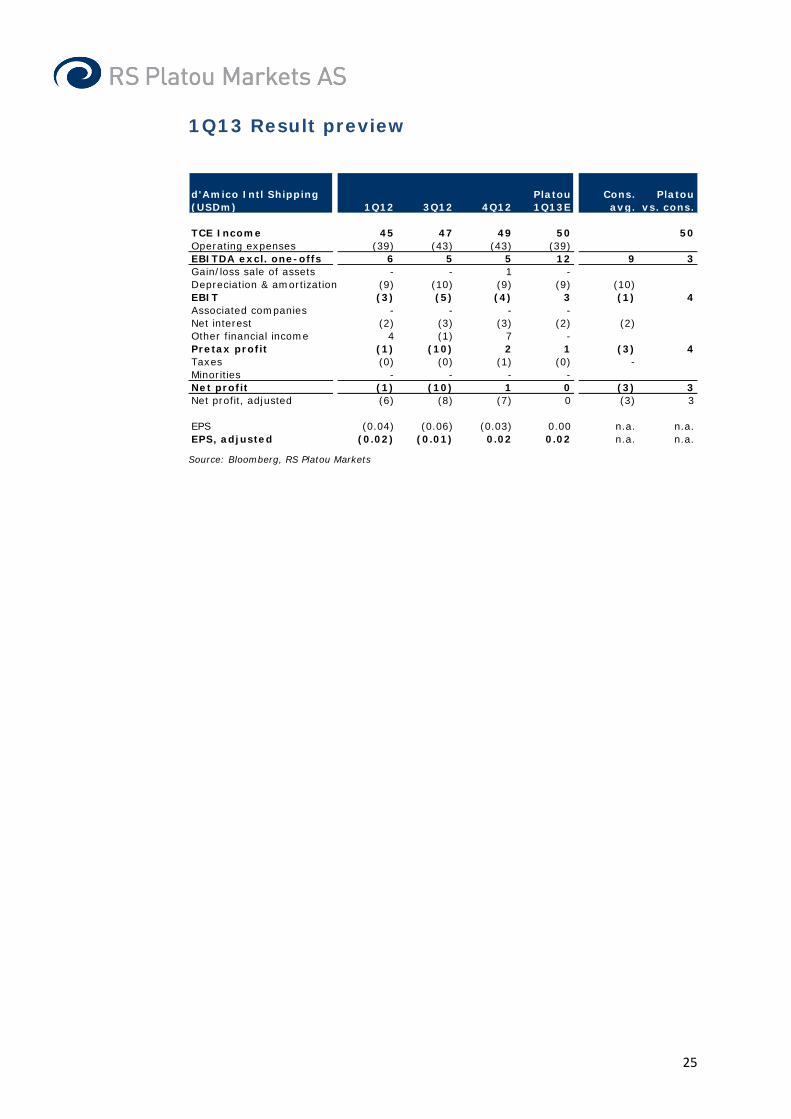

Continued fleet expansion d’Amico International Shipping (DIS IM) continued itsfleet expansion during the quarter by adding another 2newbuilds to the orderbook with 2014 delivery at highlyattractive prices.

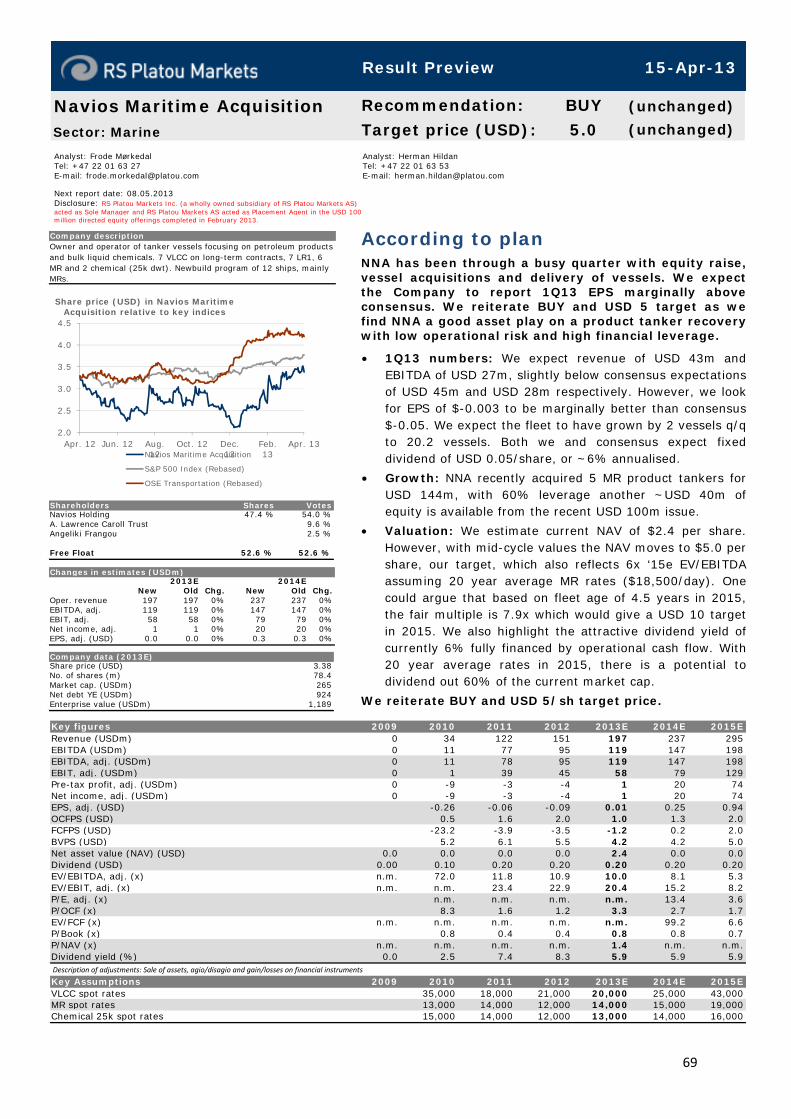

• 1Q13 numbers: We expect USD 50m of revenue and EBITDA of USD 12m vs. consensus EBITDA expectation ofUSD 9m. Management was bullish on the 4Q12 conferencecall, citing low fleet growth on the back of the changingrefinery landscape, likely to be repeated on the 1Q13 call. However, we expect somewhat lower DIS spot rates as theCompany said on the last conference call that Januaryaverage earnings were $14,000/day. This is below ourestimated average 1Q13 MR earnings of $18,000/day. Weexpect average fleet earnings of $15,100/day for 1Q13.

• Fleet expansion: DIS added another 2 MR newbuilds to their orderbook in March, to be built in Vietnam butdelivered by Hyundai Mipo (Korea). Industry sources saythe technical management of DIS holds unique quality,hence we see limited quality risk for the newbuilds.

• Valuation: We estimate current NAV of EUR 0.55/sh, increasing to EUR 0.7/sh with newbuild parity. At EUR0.7/sh EV/EBITDA is 6x while the theoretically fair targetmultiple indicates EUR 1/sh target in 2015 on 20 yearaverage rate of $18,500/day. However, due to low freefloat and Italy listing a discount seems likely.

We reiterate BUY and EUR 0.7/sh target.

d'Amico International ShippingSector: Marine

Recommendation: BUY (unchanged)

Target price (EUR): 0.70 (unchanged)

Company descriptionItalian pure play product tanker company focused on MRs, current fleet of 25 owned and 6 eco newbuilds. Listed on the Milan Stock Exchange.

0.25

0.30

0.35

0.40

0.45

0.50

0.55

0.60

0.65

Apr. 12 Jun. 12 Aug.12

Oct. 12 Dec.12

Feb.13

Apr. 13

Share price (EUR) in d'Amico International Shipping relative to key indices

d'Amico International Shipping

S&P 500 Index (Rebased)

OSE Transportation (Rebased)

Shareholders Shares VotesD'AMICO Intl SA 74.1 % 74.1 %

Free Float 25.9 % 25.9 %

Changes in estimates (USDm)2013E 2014E

New Old Chg. New Old Chg.Oper. revenue 327 327 0% 349 343 2%EBITDA, adj. 33 33 0% 52 51 3%EBIT, adj. -2 -2 0% 9 9 6%Net income, adj. -12 -12 0% -2 -3 19%EPS, adj. (USD) 0.0 0.0 0% 0.0 0.0 19%

Company data (2013E)Share price (EUR) 0.44No. of shares (m) 429.9Market cap. (USDm) 248Net debt YE (USDm) 215Enterprise value (USDm) 462

d’Amico International Shipping S.A. (DIS) is one of the ten world main owners in its industry segment with a long history of over 60 years, and one of the few pure Product Tankers players

Key figures 2010 2011 2012 2013E 2014E 2015ERevenue (USDm) 311 295 327 327 349 470EBITDA (USDm) 30 31 20 33 52 110EBITDA, adj. (USDm) 30 28 19 33 52 110EBIT, adj. (USDm) -2 -9 -20 -2 9 62Pre-tax profit, adj. (USDm) -12 -17 -29 -11 -1 51Net income, adj. (USDm) -11 -21 -116 -12 -2 50EPS, adj. (USD) -0.08 -0.14 -0.69 -0.03 0.00 0.12OCFPS (USD) 0.0 0.2 0.0 0.1 0.1 0.2FCFPS (USD) -0.3 -0.1 -0.4 0.0 -0.3 0.1BVPS (USD) 2.2 2.1 0.7 0.7 0.7 0.8Net asset value (NAV) (USD) 0.0 0.0 0.7 0.0 0.0 0.0Dividend (USD) 0.00 0.00 0.00 0.00 0.00 0.00EV/EBITDA, adj. (x) 13.8 12.0 20.1 14.0 10.8 4.5EV/EBIT, adj. (x) n.m. n.m. n.m. n.m. 59.2 8.0P/E, adj. (x) n.m. n.m. n.m. n.m. n.m. 4.9P/OCF (x) 79.4 2.9 29.9 10.9 6.1 2.5EV/FCF (x) n.m. n.m. n.m. n.m. n.m. 8.8P/Book (x) 0.6 0.3 0.6 0.9 0.9 0.7P/NAV (x) n.m. n.m. 0.6 n.m. n.m. n.m.Dividend yield (%) 0.0 0.0 0.0 0.0 0.0 0.0

Key Assumptions 2010 2011 2012 2013E 2014E 2015EMR spot rates (USD/day) 14,000 13,000 13,000 14,000 15,000 18,500

Result Preview 15-Apr-13

25

1Q13 Result preview

Source: Bloomberg, RS Platou Markets

d'Amico Intl Shipping (USDm) 1Q12 3Q12 4Q12

Platou 1Q13E

Cons. avg.

Platou vs. cons.

TCE Income 45 47 49 50 50Operating expenses (39) (43) (43) (39)EBITDA excl. one-offs 6 5 5 12 9 3Gain/loss sale of assets - - 1 -Depreciation & amortization (9) (10) (9) (9) (10)EBIT (3) (5) (4) 3 (1) 4Associated companies - - - -Net interest (2) (3) (3) (2) (2)Other financial income 4 (1) 7 -Pretax profit (1) (10) 2 1 (3) 4Taxes (0) (0) (1) (0) -Minorities - - - -Net profit (1) (10) 1 0 (3) 3Net profit, adjusted (6) (8) (7) 0 (3) 3

EPS (0.04) (0.06) (0.03) 0.00 n.a. n.a.EPS, adjusted (0.02) (0.01) 0.02 0.02 n.a. n.a.

26

Profit and loss (USDm) 2010 2011 2012 2013E 2014E 2015ETotal revenue 311 295 327 327 349 470Voyage expenses & commissions -106 -105 -142 -140 -149 -201Time-charter equivalent 205 190 185 187 200 269

Operating expenses -174 -162 -167 -154 -147 -159

EBITDA, adj. 30 28 19 33 52 110Gain/loss sale of assets 0 3 1 0 0 0EBITDA 30 31 20 33 52 110Depreciation -32 -37 -38 -35 -43 -48Amortization/Write down 0 0 -85 0 0 0EBIT -2 -6 -103 -2 9 62EBIT, adj. -2 -9 -20 -2 9 62

Associated companies 0 0 0 0 0 0Net interest -10 -11 -10 -9 -11 -11Gains/losses on securities or financial instruments -9 -4 9 0 0 0Other financial Items 0Pre-tax profit -21 -20 -105 -11 -1 51Tax 1 -1 -1 -1 -1 -1Minorities 0 0 0 0 0 0Result from discontinued operations/ Other 0 0 0 0 0 0Net income -21 -21 -106 -12 -2 50

Adjustments after tax 9 0 -10 0 0 0Adjusted net income -11 -21 -116 -12 -2 50

EPS (USD) -0.14 -0.14 -0.63 -0.03 0.00 0.12EPS, adj. (USD) -0.08 -0.14 -0.69 -0.03 0.00 0.12

Balance sheet (USDm) 2010 2011 2012 2013E 2014E 2015ELong-term interest bearing assets 0 0 0 0 0 0Fixed assets 544 548 499 507 613 610Other long-term assetsLong-term assets 544 548 499 507 613 610

Other current assets 97 72 60 61 65 88Cash and liquid assets 68 51 118 68 33 85Current assets 165 123 178 129 98 172

Total assets 710 670 677 635 712 782

Equity 333 315 294 282 291 353

Minorities 0 0 0 0 0 0

Long term interest bearing debt 285 282 284 254 317 301Finance obligation 0 0 0 0 0 0Other long-term liabilities 5 5 5 5Long term liabilities 285 282 289 259 322 305

Short term interest bearing debt 11 15 28 28 28 28Other short term liabilities 81 57 66 67 71 96Current liabilities 92 72 94 95 99 124

Total liabilities and equity 710 670 677 635 712 782

Working capital 16 14 -5 -5 -6 -8Net debt 227 246 195 215 312 244

Cash flow (USDm) 2010 2011 2012 2013E 2014E 2015EPre-tax profit -21 -20 -105 -11 -1 51- Associated companies 0 0 0 0 0 0+ Depreciation and amortization 32 37 123 35 43 48- Payable tax 1 -1 -1 -1 -1 -1+/- Other operating items 7 11 -35 0 0 0Cash flow from operations 19 27 -17 23 40 99

Change in working capital -16 2 20 0 0 2Operating cash flow 2 29 2 23 41 101

Maintenance capex 0 0 0 0 0 0Growth capex -57 -65 -85 -43 -149 -45Acquisition capex 0 0 0 0 0 0Sale of assets 3 27 12 0 0 0Cash flow from investments -54 -37 -73 -43 -149 -45

Free cash flow -52 -8 -71 -20 -108 56

Dividend paid 0 0 0 0 0 0Share buy back 0 0 0 0 0 0Equity increase 0 -1 84 0 11 12Cash flow from financing 0 -1 84 0 11 12

Other items -176 -10 39 0 0 0

Change in net debt 227 19 -51 20 97 -68

27

Analyst: Frode Mørkedal Tel: +47 22 01 63 27 E-mail: [email protected] Next report date: 15.05.2013 Disclosure:

Analyst: Herman Hildan Tel: +47 22 01 63 53 E-mail: [email protected]

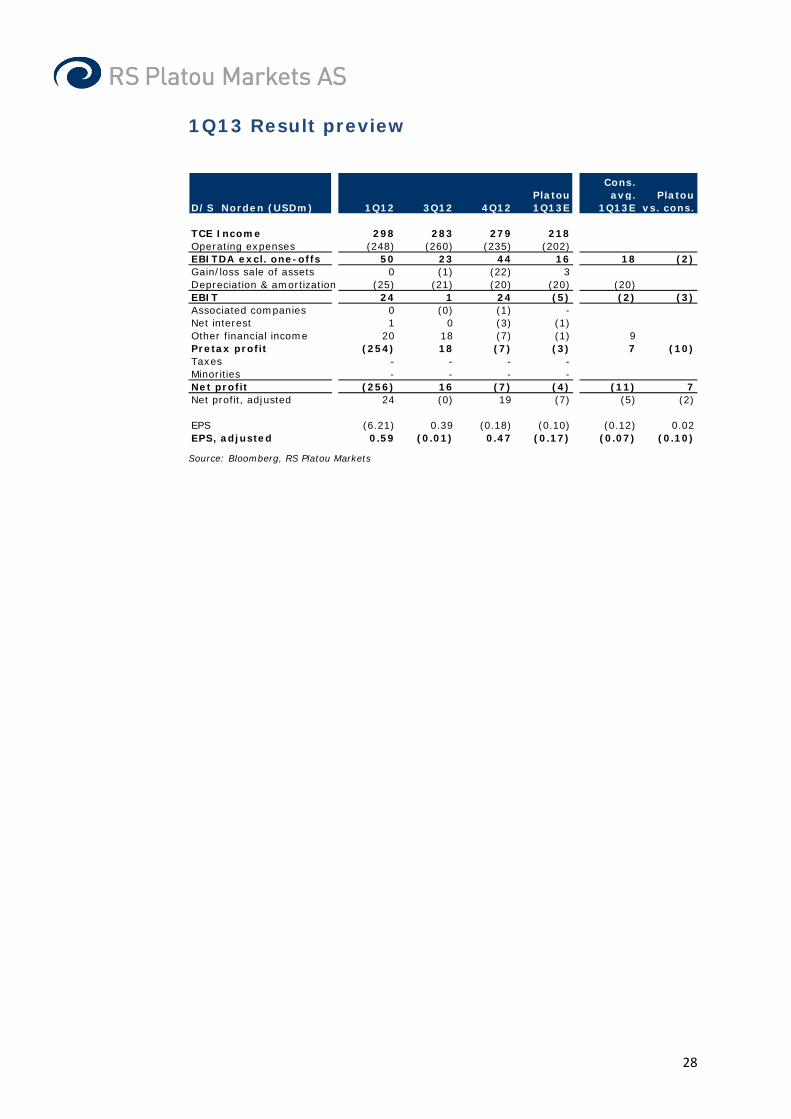

Expect higher full year guidance DS Norden is expected to report 1Q13 numbers on May15th. We expect the low 2013 guidance from the last report to be upgraded and see high upside potential forDNORD as the market is expected to bottom in 2013. Weexpect management comments to be bullish in terms ofbuilding upside for a recovery, in line with the signals at a lunch presentation in our offices during the quarter.

• 1Q13 numbers: We expect TCE income of USD 218m and EBITDA of USD 16m, in line with consensus expecting USD18m of EBITDA.

• 2013 guidance: Management guided USD 0m EBITDA for Dry Cargo and USD 25-45m for Product tankers and Group EBITDA of USD 15-45m on the 4Q12 presentation. Management told us at a lunch presentation that theguidance was based on a depressed FFA market inFebruary, on the back of a recovery since then we find itlikely that the guiding will be upgraded in 1Q13.

• Valuation: We estimate DNORD NAV at DKK 223/sh, up from DKK 214/sh a month ago due to higher asset values.Management said in the last report that they believed assetvalues have bottomed out and implemented a sharebuyback program of USD 30m as long as the share price is below NAV (DKK 213/sh at 4Q12 report). Regardless, wefind earnings more important and find EV/EBITDA of 3.2x‘15e as attractive in light of the strong balance sheet. OurUSD 39/sh target implies EV/EBTIDA of ~4.5x.

We reiterate BUY and USD 39/sh target.

D/S NordenSector: Marine

Recommendation: BUY (unchanged)

Target price (USD): 39 (unchanged)

Company descriptionDanish dry bulk major founded in 1871 that operates more than 100 bulk vessels including long-term charters. Has a large newbuild orderbook in addition to a product tanker exposure . Listed in Copenhagen under the ticker DNORD.

140

150

160

170

180

190

200

210

220

Apr. 12 Jun. 12 Aug. 12 Oct. 12 Dec. 12 Feb. 13

Share price (DKK) in D/S Norden relative to key indices

D/S Norden

OSEBX index (Rebased)

OSE Transportation (Rebased)

Shareholders Shares VotesA/S Motortramp 26.6 % 26.6 %Kristiansand Tankrederi (Rasmussengrupp 10.9 % 10.9 %D/S Norden (treasury shares) 5.7 % 5.7 %

Free Float 56.8 % 56.8 %

Changes in estimates (USDm)2013E 2014E

New Old Chg. New Old Chg.Oper. revenue 1,622 1,622 0% 1,899 1,899 0%EBITDA, adj. 60 60 0% 119 119 0%EBIT, adj. -22 -22 0% 30 30 0%Net income, adj. -31 -31 0% 21 21 0%EPS, adj. (USD) -0.8 -0.8 0% 0.5 0.5 0%

Company data (2013E)Share price (DKK) 182.60No. of shares (m) 41.2Market cap. (USDm) 1,321Net debt YE (USDm) -343Enterprise value (USDm) 979

Description of adjustments: Sale of assets, agio/disagio and gain/losses on financial instruments

Key figures 2009 2010 2011 2012 2013E 2014E 2015ERevenue (USDm) 1,676 2,190 2,273 2,131 1,622 1,899 2,461EBITDA (USDm) 195 268 186 124 63 119 239EBITDA, adj. (USDm) 126 240 186 148 60 119 239EBIT, adj. (USDm) 90 190 105 59 -22 30 149Pre-tax profit, adj. (USDm) 167 220 108 33 -23 26 145Net income, adj. (USDm) 87 186 103 -249 -31 21 139EPS, adj. (USD) 2.06 4.42 2.49 -6.03 -0.76 0.50 3.38OCFPS (USD) 3.8 7.1 1.5 3.0 1.9 2.3 4.8FCFPS (USD) 1.9 -1.9 -7.5 3.1 0.1 1.7 4.8BVPS (USD) 42.8 47.4 48.4 40.9 39.5 39.3 42.0Net asset value (NAV) (USD) 51.2 39.1 39.1 39.1 0.0 0.0 0.0Dividend (USD) 1.29 1.43 0.73 0.73 0.73 0.73 0.73EV/EBITDA, adj. (x) 8.5 4.0 3.9 5.6 16.2 7.9 3.2EV/EBIT, adj. (x) 11.9 5.1 6.9 13.9 n.m. 31.1 5.2P/E, adj. (x) 19.6 8.1 9.4 n.m. n.m. 64.1 9.5P/OCF (x) 10.6 5.1 15.5 9.8 16.6 14.2 6.7EV/FCF (x) 13.2 n.m. n.m. 6.4 n.m. 13.7 3.9P/Book (x) 0.9 0.8 0.5 0.7 0.8 0.8 0.8P/NAV (x) 0.8 0.9 0.6 0.7 n.m. n.m. n.m.Dividend yield (%) 3.2 4.0 3.1 2.5 2.3 2.3 2.3

Key Assumptions 2009 2010 2011 2012 2013E 2014E 2015EPanamax USD/day 19,000 25,000 14,500 8,500 9,000 13,000 18,000Supramax USD/day 17,100 22,500 14,500 9,500 9,000 13,000 17,000Handysize USD/day 11,200 16,500 10,500 7,500 7,000 10,000 13,000

Result Preview 15-Apr-13

28

1Q13 Result preview

Source: Bloomberg, RS Platou Markets

D/S Norden (USDm) 1Q12 3Q12 4Q12Platou 1Q13E

Cons. avg.

1Q13EPlatou

vs. cons.

TCE Income 298 283 279 218Operating expenses (248) (260) (235) (202)EBITDA excl. one-offs 50 23 44 16 18 (2)Gain/loss sale of assets 0 (1) (22) 3Depreciation & amortization (25) (21) (20) (20) (20)EBIT 24 1 24 (5) (2) (3)Associated companies 0 (0) (1) -Net interest 1 0 (3) (1)Other financial income 20 18 (7) (1) 9Pretax profit (254) 18 (7) (3) 7 (10)Taxes - - - -Minorities - - - -Net profit (256) 16 (7) (4) (11) 7Net profit, adjusted 24 (0) 19 (7) (5) (2)

EPS (6.21) 0.39 (0.18) (0.10) (0.12) 0.02EPS, adjusted 0.59 (0.01) 0.47 (0.17) (0.07) (0.10)

29

Profit and loss (USDm) 2009 2010 2011 2012 2013E 2014E 2015ETotal revenue 1,676 2,190 2,273 2,131 1,622 1,899 2,461Voyage expenses & commissions -451 -617 -900 -997 -751 -880 -1,142Time-charter equivalent 1,225 1,572 1,373 1,134 871 1,019 1,319

Operating expenses -1,100 -1,333 -1,187 -986 -810 -900 -1,080

EBITDA, adj. 126 240 186 148 60 119 239Gain/loss sale of assets 70 28 0 -24 3 0 0EBITDA 195 268 186 124 63 119 239Depreciation -36 -50 -81 -89 -82 -88 -91Amortization/Write down -3 0 0 -300 0 0 0EBIT 156 218 105 -265 -19 30 149EBIT, adj. 90 190 105 59 -22 30 149

Associated companies 1 4 -1 -1 0 0 0Net interest 7 -2 4 -2 -4 -4 -4Gains/losses on securities or financial instruments 61 30 -15 -6 0 0 0Other financial Items 0Pre-tax profit 225 251 93 -274 -23 26 145Tax -7 -6 -6 -5 -6 -6 -6Minorities 0 0 0 0 0 0 0Result from discontinued operations/ Other 0 0 0 0 0 0 0Net income 217 245 88 -279 -28 21 139

Adjustments after tax -130 -59 15 30 -3 0 0Adjusted net income 87 186 103 -249 -31 21 139

EPS (USD) 5.16 5.80 2.12 -6.77 -0.69 0.50 3.38EPS, adj. (USD) 2.06 4.42 2.49 -6.03 -0.76 0.50 3.38

Balance sheet (USDm) 2009 2010 2011 2012 2013E 2014E 2015ELong-term interest bearing assets 0 0 0 0 0 0 0Fixed assets 996 1,373 1,613 1,183 1,179 1,114 1,024Other long-term assets 32 35 21 13 13 13 13Long-term assets 1,028 1,408 1,634 1,196 1,192 1,127 1,037

Other current assets 293 229 309 309 237 278 360Cash and liquid assets 711 613 407 529 481 502 651Current assets 1,004 842 716 838 718 779 1,011

Total assets 2,032 2,250 2,350 2,033 1,909 1,907 2,047

Equity 1,805 1,998 1,994 1,687 1,629 1,620 1,729

Minorities 0 0 0 0 0 0 0

Long term interest bearing debt 58 22 135 138 116 98 80Finance obligation 0 0 0 0 0 0 0Other long-term liabilitiesLong term liabilities 58 22 135 138 116 98 80

Short term interest bearing debt 5 44 30 22 22 22 22Other short term liabilities 163 187 191 186 143 167 216Current liabilities 168 230 221 208 165 189 238

Total liabilities and equity 2,032 2,250 2,350 2,033 1,909 1,907 2,047

Working capital 130 43 118 123 95 111 144Net debt -647 -547 -242 -368 -343 -381 -549

Cash flow (USDm) 2009 2010 2011 2012 2013E 2014E 2015EPre-tax profit 225 251 93 -274 -23 26 145- Associated companies -1 -4 1 1 0 0 0+ Depreciation and amortization 39 50 81 389 82 88 91- Payable tax -7 -6 -6 -5 -6 -6 -6+/- Other operating items 13 -79 -32 17 -3 0 0Cash flow from operations 269 211 138 128 51 109 230

Change in working capital -109 87 -75 -6 29 -16 -33Operating cash flow 160 298 62 122 79 93 197

Maintenance capex 0 0 0 0 0 0 0Growth capex -533 -660 -383 -150 -124 -24 0Acquisition capex 2 -39 -25 -12 0 0 0Sale of assets 451 319 35 169 49 0 0Cash flow from investments -80 -380 -373 7 -75 -24 0

Free cash flow 80 -82 -310 129 4 69 197

Dividend paid -98 -53 -60 -29 -30 -30 -30Share buy back -10 -8 -32 0 0 0 0Equity increase 0 0 0 0 0 0 0Cash flow from financing -107 -60 -92 -29 -30 -30 -30

Other items -63 42 97 26 0 0 0

Change in net debt 91 100 305 -126 26 -39 -167

30

Analyst: Frode Mørkedal Tel: +47 22 01 63 27 E-mail: [email protected] Next report date: 29.04.2013 Disclosure:

Analyst: Herman Hildan Tel: +47 22 01 63 53 E-mail: [email protected]

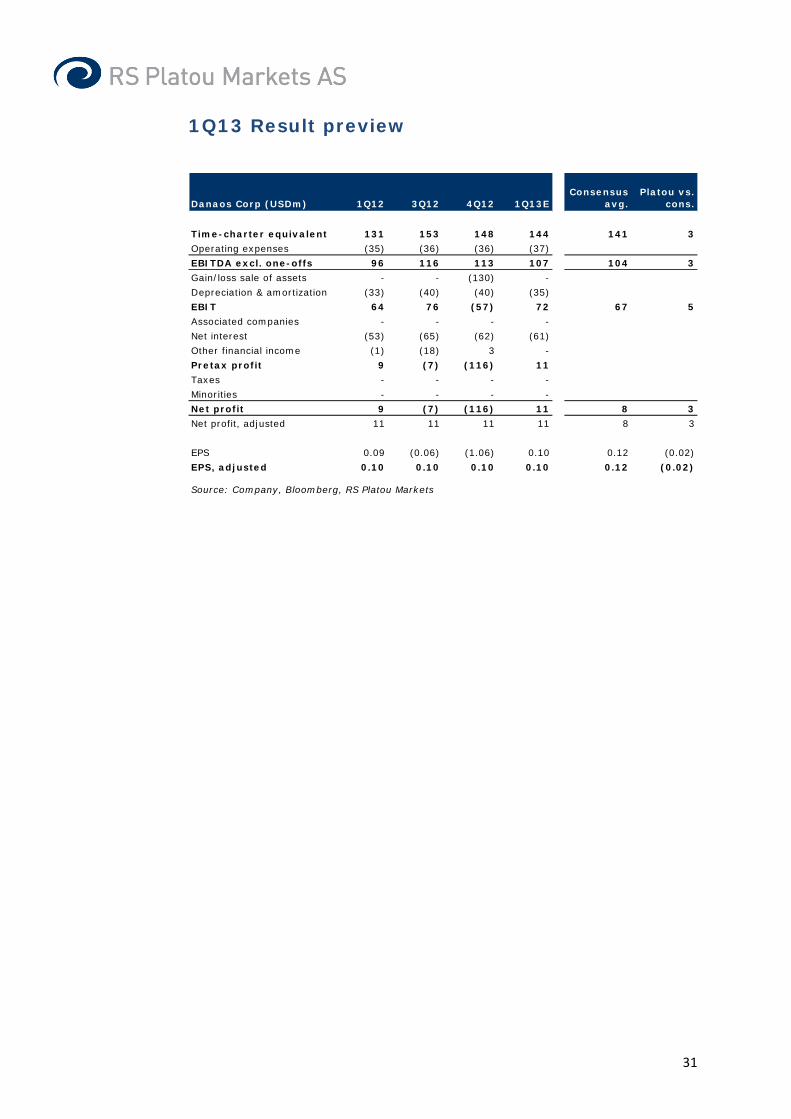

Little happening while deleveragingDanaos is expected to report 1Q13 figures April 29th. We expect somewhat lower results quarter on quarter dueto idle vessels. The problem for the stock is that theCompany is unable to grow unless new equity is raised. Lacking company specific triggers, the share needsmarket momentum to lift the price, which is unlikely tohappen in 2013 given the poor supply-demand balance.