Shell Exploration

19

Shell Exploration & Production 06/ 08/ 1 0 File Title Copyright: Shell Exploration & Production Ltd. Gas Development and Commercialization Corporate Council on Africa Africa Oil & Gas Forum– Houston, Texas November 30 th 2004 ‘Demola Adeyem i-Bero New Business Development Director – Africa

Transcript of Shell Exploration

Shell Exploration &Production

06/0

8/1

0Fi

le T

itle

Copyr

ight

: Sh

ell E

xplo

ratio

n &

Pro

duc

tion

Ltd.

Gas Development and Commercialization

Corporate Council on AfricaAfrica Oil & Gas Forum – Houston, TexasNovember 30th 2004

‘Demola Adeyemi-BeroNew Business Development Director – Africa

. Gas Touches Our Lives In So Many Ways . Gas Touches Our Lives In So Many Ways

Electricity Fertilizers

Fuel Industrial Feedstock

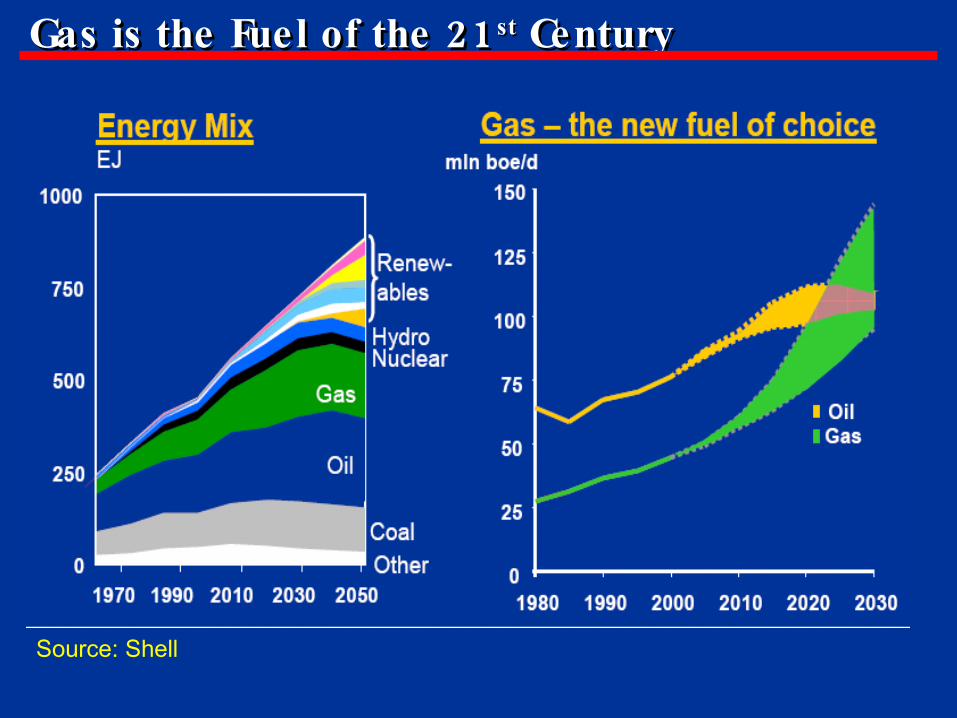

21Gas is the Fuel of the 21Gas is the Fuel of the stst Century Century

Source: Shell

S. & Cent. America7.19

North America7.31

Asia Pacific13.47

Africa13.78

Europe & Eurasia62.30

Middle East71.72

Trillion Cubic Meters

Major Gas Resource – Major Gas Resource – Africa has significant reservesAfrica has significant reserves

… .Proximity to the key markets

Source: bp statistical review 2004, Cedigazs, Shell estimates)

The increasing role of African LNG in the Atlantic Basin

Source: bp statistical review 2004, Cedigaz , Shell estimates

1659

910

176

(Nigeria Reserves tcf )*

268

(N Africa Reserves tcf )*

236

942

* (2003 Proved Gas Reserves tcf )

0

10

20

2003 2010 2020

/Bcf d

8%

17%

0

10

20

2003 2010 2020

/Bcf d

8%14%

17%

/Bcf d

0

10

20

2003 2010 2020

2%

9%14%

/Bcf d

0

10

20

2003 2010 2020

2%

9%14%

. N America LNG Demand( )and LNG share of supply Europe LNG Demand

( )and LNG share of supply

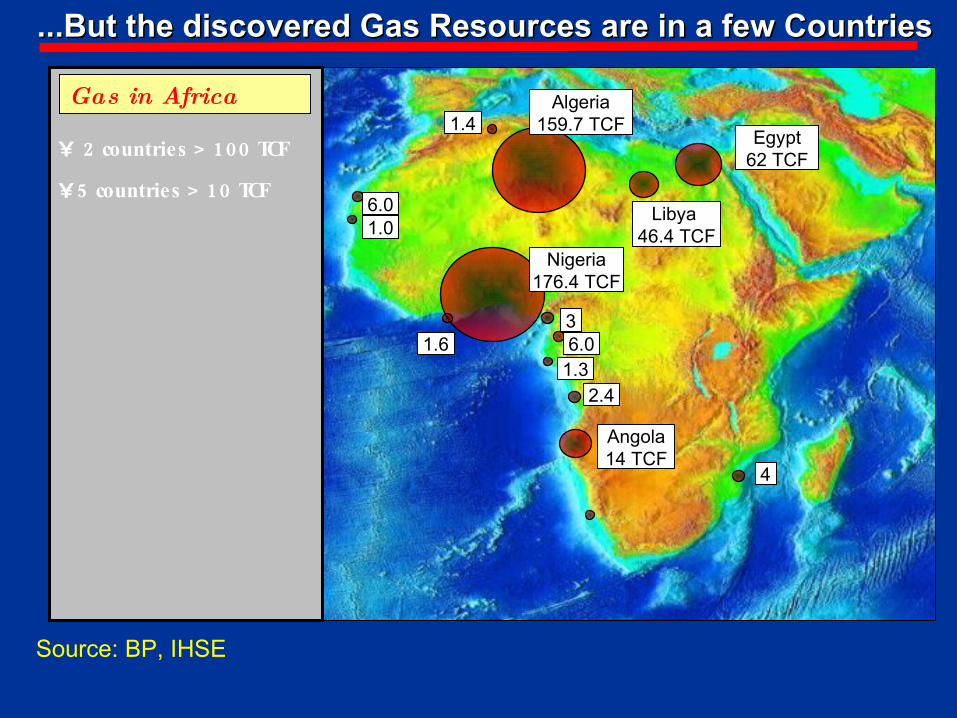

Continent’s Gas Are Concentrated In Few countriesContinent’s Gas Are Concentrated In Few countriesGas in Africa

• 2 > 100 countries TCF

•5 > 10 countries TCF

Nigeria176.4 TCF

Libya 46.4 TCF

Angola14 TCF

Egypt62 TCF

2.4

6.0 1.6

1.4 Algeria

159.7 TCF

4

3

1.3

...But the discovered Gas Resources are in a few Countries...But the discovered Gas Resources are in a few Countries

Source: BP, IHSE

6.0 1.0

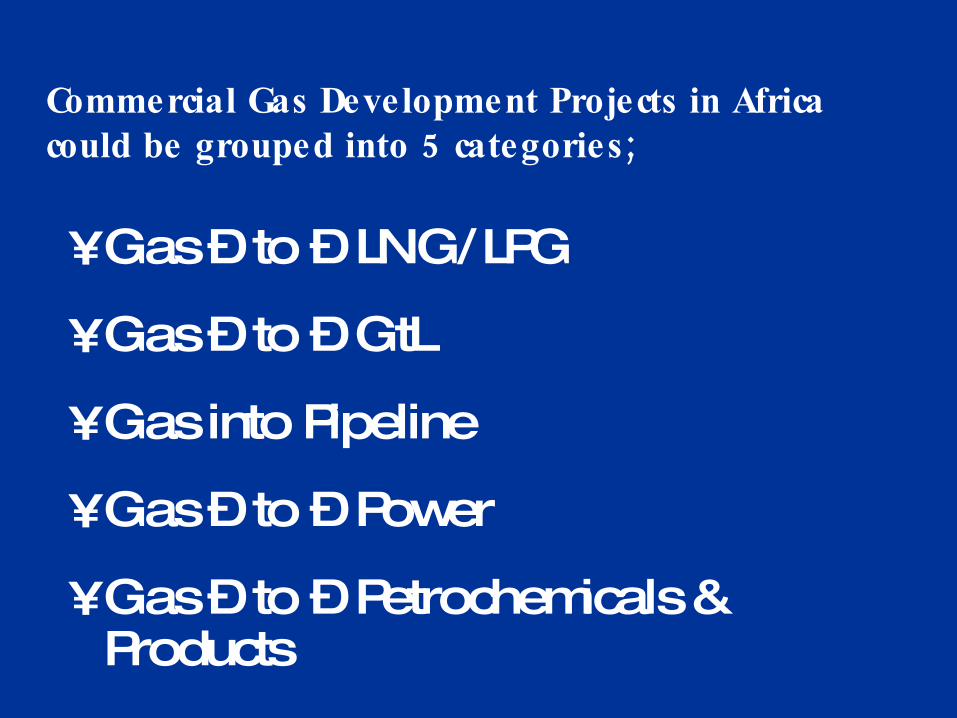

Commercial Gas Development Projects in Africa 5 ;could be grouped into categories

•Gas – to – LNG/LPG

•Gas – to – GtL

•Gas into Pipeline

•Gas – to – Power

•Gas – to – Petrochemicals & Products

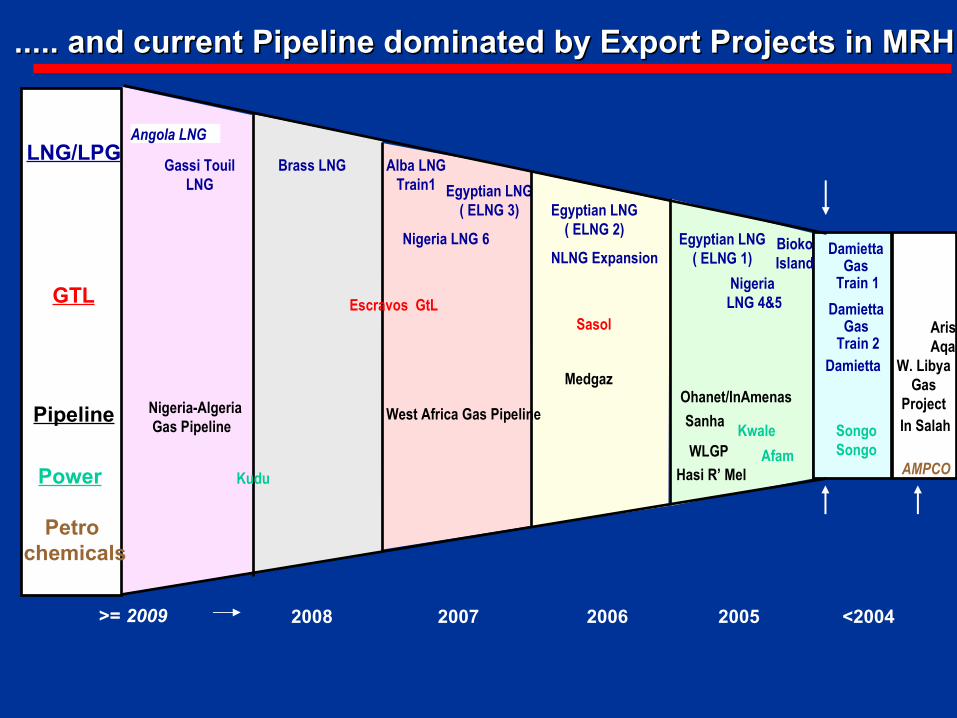

..... and current Pipeline dominated by Export Projects in MRH..... and current Pipeline dominated by Export Projects in MRH

LNG/LPG

200520062007

GTL

Pipeline

<20042008

Alba LNGTrain1

Angola LNG

>= 2009

Brass LNG

Damietta Gas

Train 1

Damietta Gas

Train 2

Egyptian LNG( ELNG 1)

Egyptian LNG( ELNG 2)

Egyptian LNG( ELNG 3)

Gassi TouilLNG

Nigeria LNG 4&5

Nigeria LNG 6

Damietta

Ohanet/InAmenas

Sanha

WLGP

BiokoIslandNLNG Expansion

Escravos GtLSasol

Petro chemicals

AMPCOHasi R’ Mel

ArishAqaba

W. LibyaGas

ProjectIn Salah

Medgaz

West Africa Gas PipelineNigeria-Algeria Gas Pipeline

Power KuduAfam

SongoSongo

Kwale

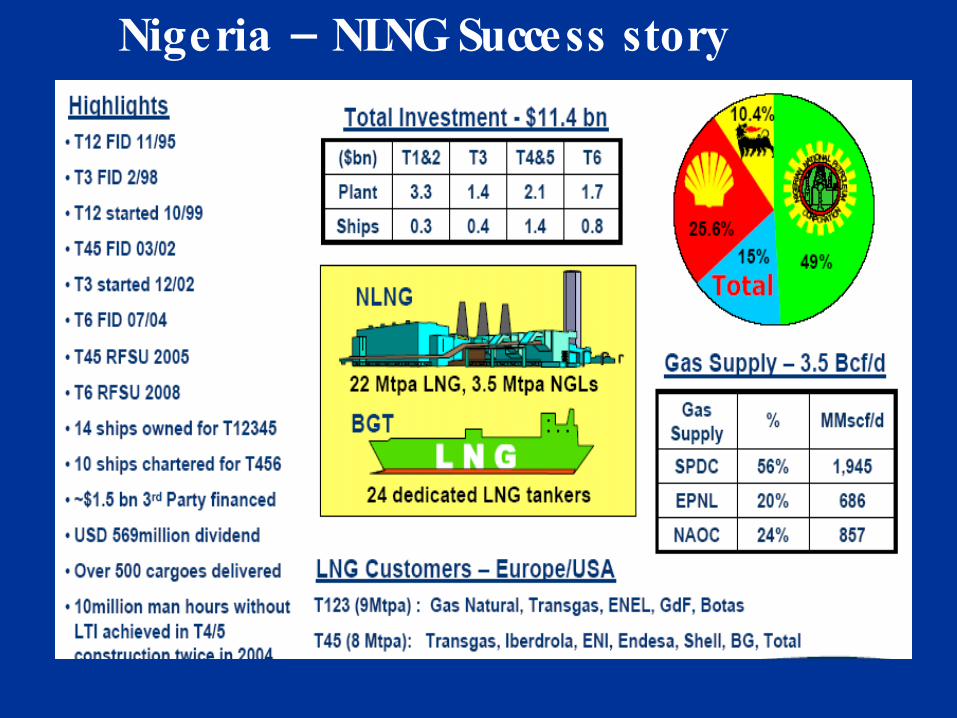

– Shell Global leader in LNG

Gas production LNG supplyLNG marketsGTL plantOther Africa LNG Development

• 2nd largest producer• Positioned in key

markets– #1 in Asia Pacific– #2 in Europe– #3 in North America

• Largest supplier of equity LNG

• GTL leader

– Nigeria NLNGSuccess story

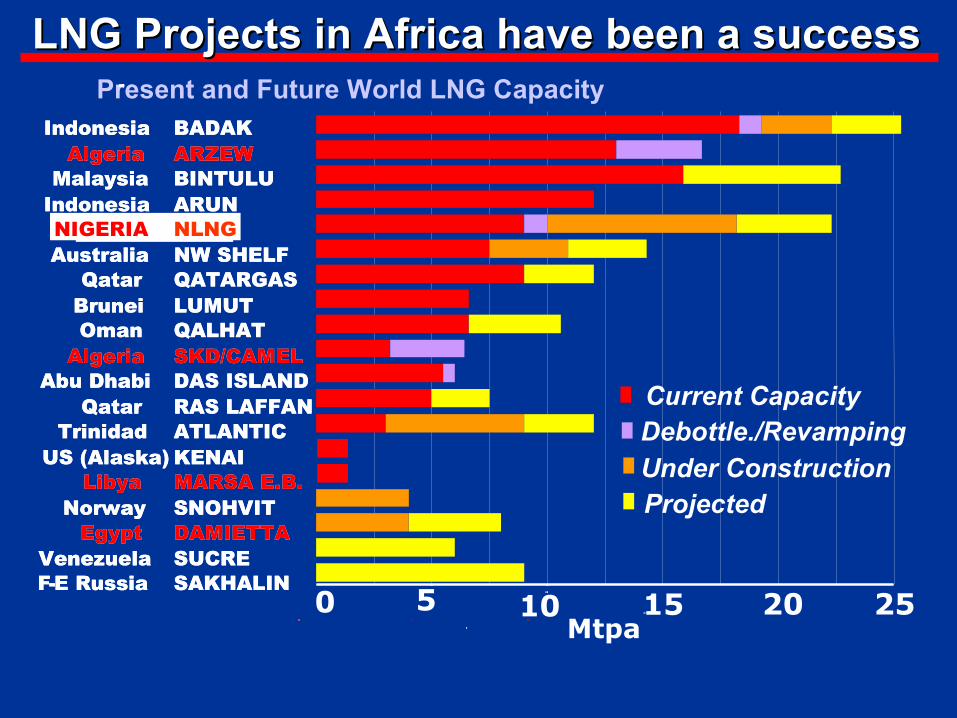

LNG Projects in Africa have been a successLNG Projects in Africa have been a successPresent and Future World LNG Capacity

Mtpa

-

IndonesiaAlgeria

MalaysiaIndonesiaNIGERIA NIGERIA Australia

QatarBruneiOman

AlgeriaAbu Dhabi

QatarTrinidad

US (Alaska)Libya

NorwayEgypt

VenezuelaF-E Russia

BADAKARZEW BINTULUARUNNLNGNLNGNW SHELFQATARGASLUMUTQALHATSKD/CAMELDAS ISLAND RAS LAFFANATLANTICKENAIMARSA E.B.SNOHVITDAMIETTASUCRESAKHALIN

IndonesiaAlgeria

MalaysiaIndonesiaNIGERIA NIGERIA Australia

QatarBruneiOman

AlgeriaAbu Dhabi

QatarTrinidad

US (Alaska)Libya

NorwayEgypt

VenezuelaF-E Russia

BADAKARZEW BINTULUARUNNLNGNLNGNW SHELFQATARGASLUMUTQALHATSKD/CAMELDAS ISLAND RAS LAFFANATLANTICKENAIMARSA E.B.SNOHVITDAMIETTASUCRESAKHALIN

15 20 250

5

10

0

5

10

Current CapacityDebottle./RevampingUnder ConstructionProjected

0 5 100 10

0 5 10

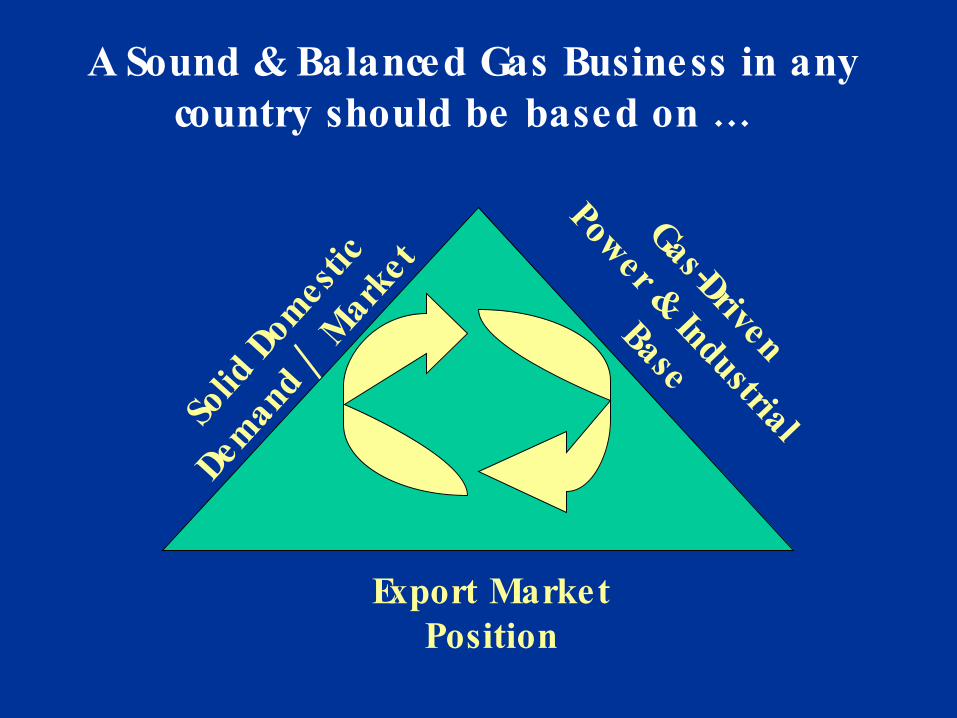

ASound &Balanced Gas Business in any … country should be based on

SolidDomestic

/

DemandMarket

Export MarketPosition

-Gas Driven

Power &Industrial

Base

A successful Gas Business that fosters economic & industrial

6 ;growth requires key e lements

• Major Gas Resource Base

• Sustained Market Demand Growth (Domestic & Global)

• Attractive (Stable) Gas Price (Domestic & International)

• Attractive & competitive Investment Business environment (Fiscal & Legislative)

• Capable of Sustainable Development– (People, Planet & Profit)

• Participation of all the key stakeholders

… ..Peer Comparison

Hence a view of Africa against the key elements… …

• Major Gas Resource Base

• Sustained Market Demand Growth (Domestic & Global)

• Attractive (Stable) Gas Price (Domestic & International)

• Investment friendly Business environment (Fiscal & Legislative)

• Sustainable Development –(People, Planet & Profit)

• Participation of all key Stakeholders

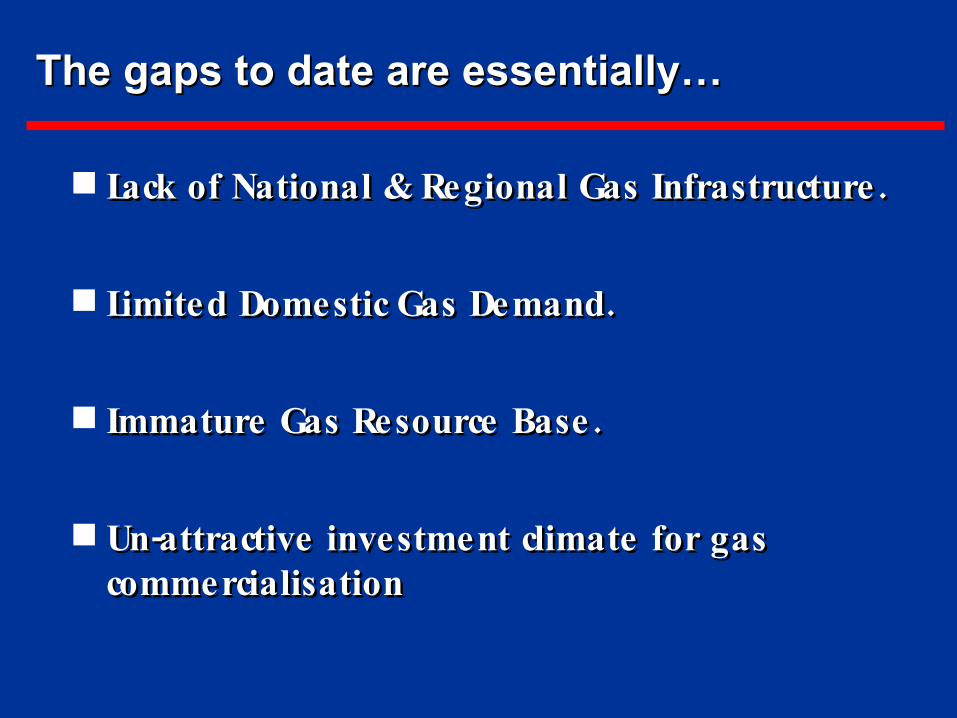

.Lack of National &Regional Gas Infrastructure .Lack of National &Regional Gas Infrastructure

.Limited Domestic Gas Demand .Limited Domestic Gas Demand

.Immature Gas Resource Base .Immature Gas Resource Base

- Un attractive investment climate for gas- Un attractive investment climate for gascommercialisationcommercialisation

The gaps to date are essentially…The gaps to date are essentially…

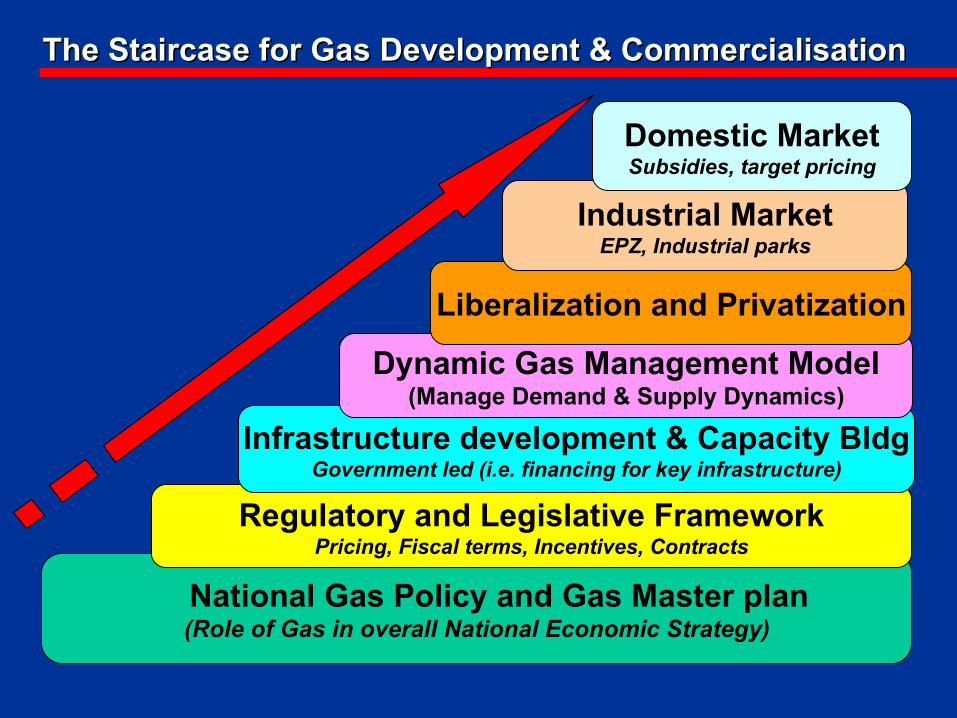

The Staircase for Gas Development & CommercialisationThe Staircase for Gas Development & Commercialisation

National Gas Policy and Gas Master plan(Role of Gas in overall National Economic Strategy)

Regulatory and Legislative FrameworkPricing, Fiscal terms, Incentives, Contracts

Infrastructure development & Capacity BldgGovernment led (i.e. financing for key infrastructure)

Dynamic Gas Management Model(Manage Demand & Supply Dynamics)

Liberalization and Privatization

Industrial MarketEPZ, Industrial parks

Domestic MarketSubsidies, target pricing

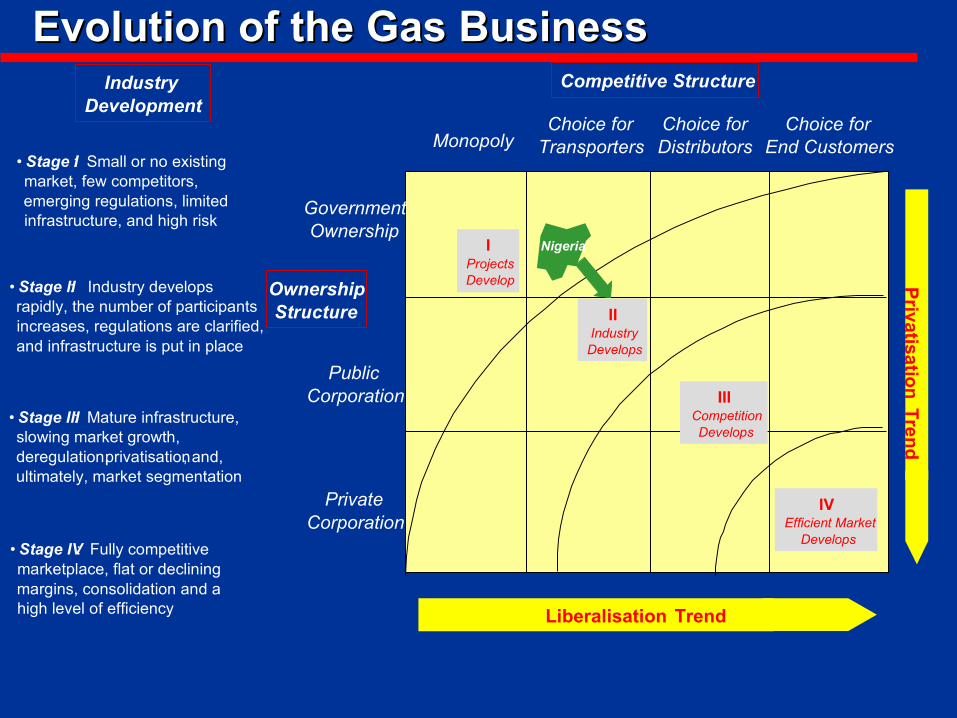

Evolution of the Gas BusinessEvolution of the Gas BusinessCompetitive Structure

OwnershipStructure

MonopolyChoice for

TransportersChoice forDistributors

Choice forEnd Customers

GovernmentOwnership

PublicCorporation

PrivateCorporation

Liberalisation Trend

Privatisatio

nT

rend

IProjectsDevelop

• Stage I: Small or no existingmarket, few competitors,emerging regulations, limitedinfrastructure, and high risk

• Stage II: Industry developsrapidly, the number of participantsincreases, regulations are clarified,and infrastructure is put in place

• Stage III: Mature infrastructure,slowing market growth,deregulation, privatisation, and,ultimately, market segmentation

• Stage IV: Fully competitivemarketplace, flat or decliningmargins, consolidation and ahigh level of efficiency

IndustryDevelopment

IIIndustryDevelops

IIICompetitionDevelops

IVEfficient Market

Develops

Nigeria

Shell Exploration &Production

06/0

8/1

0Fi

le T

itle

Copyr

ight

: Sh

ell E

xplo

ratio

n &

Pro

duc

tion

Ltd. Thank You