Whidbey General Hospital Provider Clinics & Rural Health Clinics

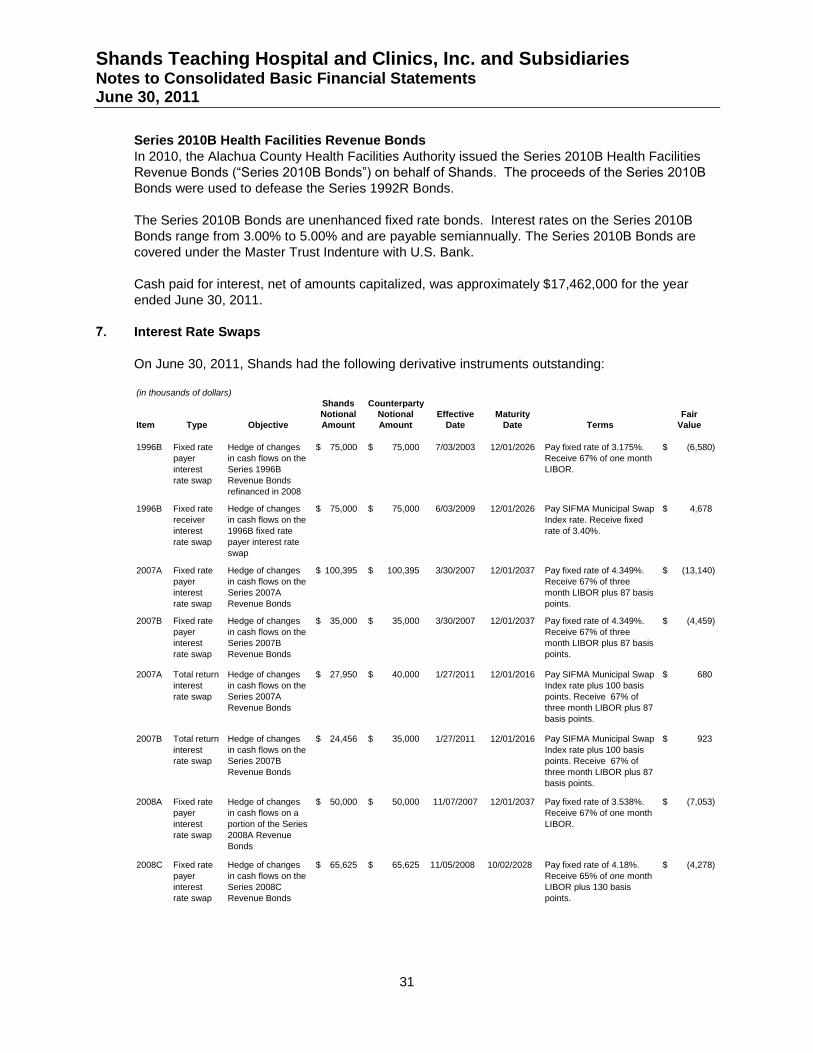

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Consolidated Basic Financial Statements, Required Supplementary Information and Supplemental Consolidating Information June 30, 2011

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Index June 30, 2011

Page(s)

Management's Discussion and Analysis (Unaudited) ................................................................................ 1-7

Report of Independent Certified Public Accountants .......................................................................... 8-9

Consolidated Basic Financial Statements

Consolidated Basic Statement of Net Assets ............................................................................................. 10

Consolidated Basic Statement of Revenues, Expenses and Changes in Net Assets ........................... 11-12

Consolidated Basic Statement of Cash Flows ....................................................................................... 13-14

Notes to Consolidated Basic Financial Statements ............................................................................... 15-43

Required Supplementary Information

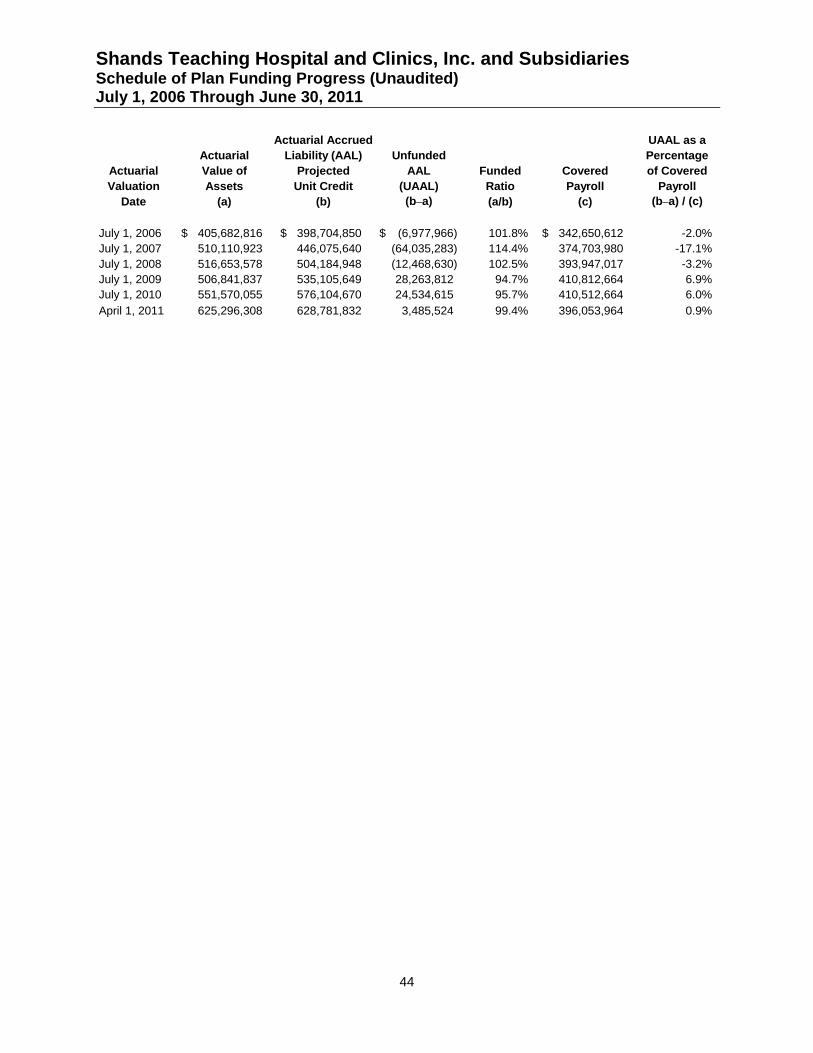

Schedule of Plan Funding Progress (Unaudited) ....................................................................................... 44

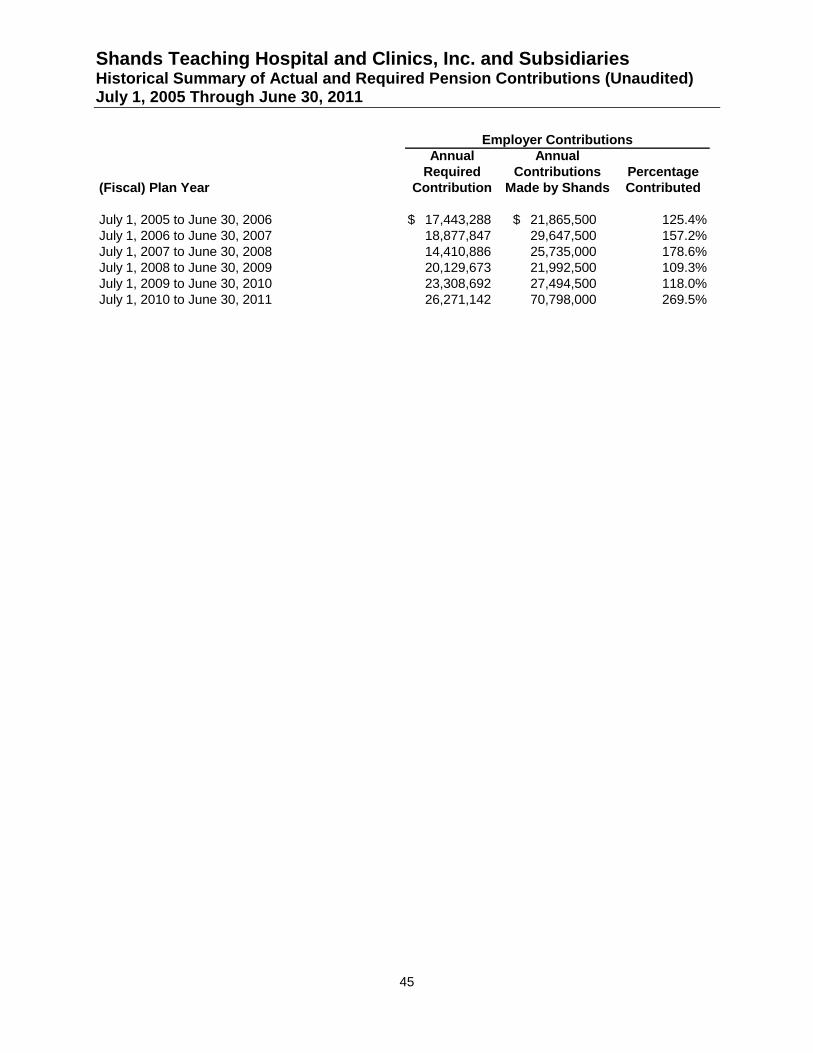

Historical Summary of Actual and Required Pension Contributions (Unaudited) ....................................... 45

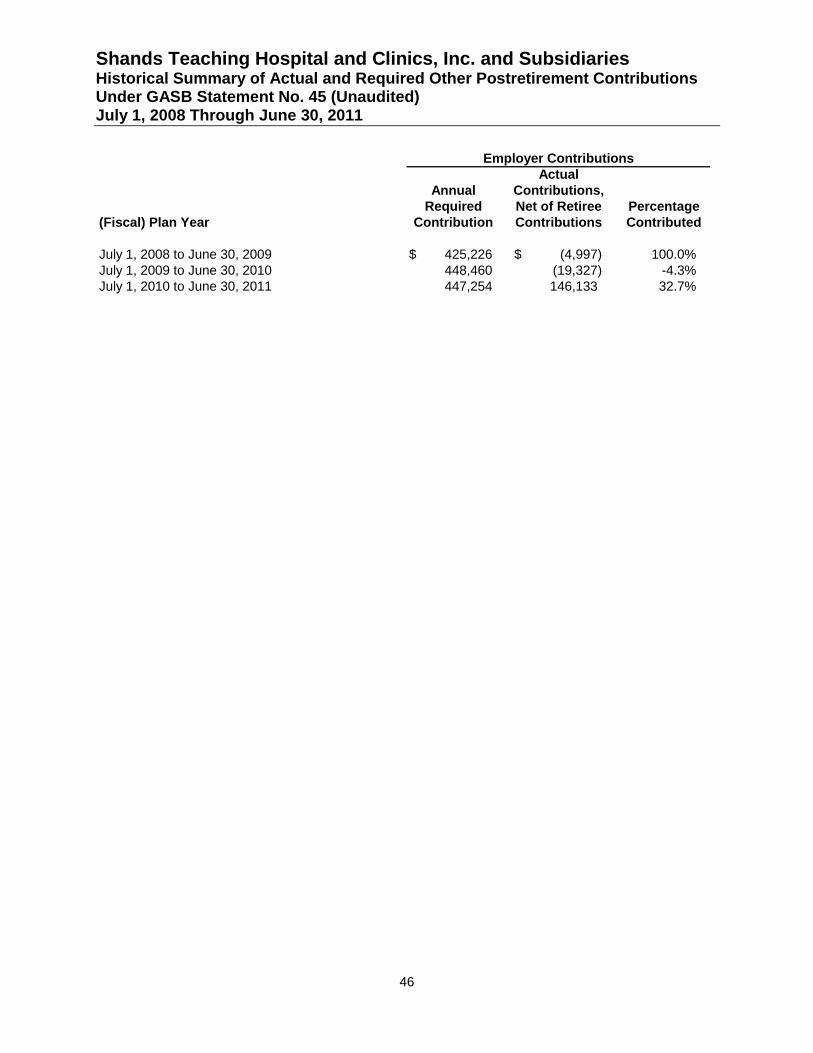

Historical Summary of Actual and Required Other Postretirement Contributions Under GASB Statement No. 45 (Unaudited) ............................................................................................ 46

Supplemental Consolidating Information

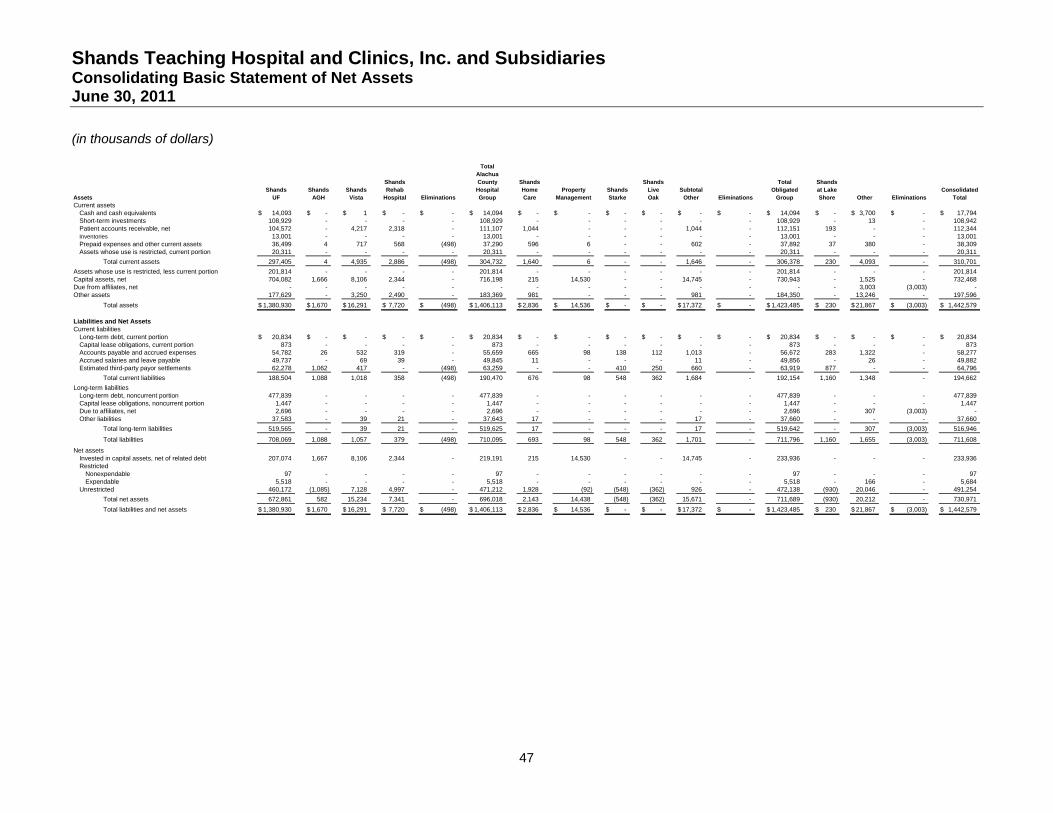

Consolidating Basic Statement of Net Assets............................................................................................. 47

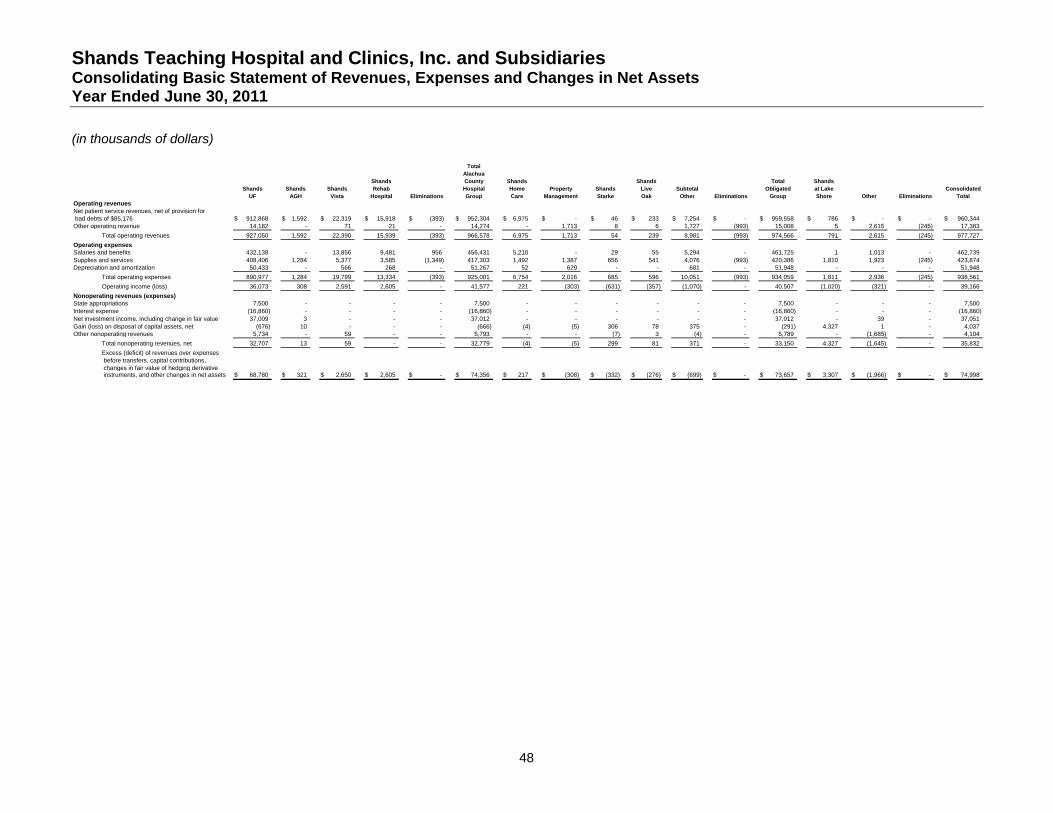

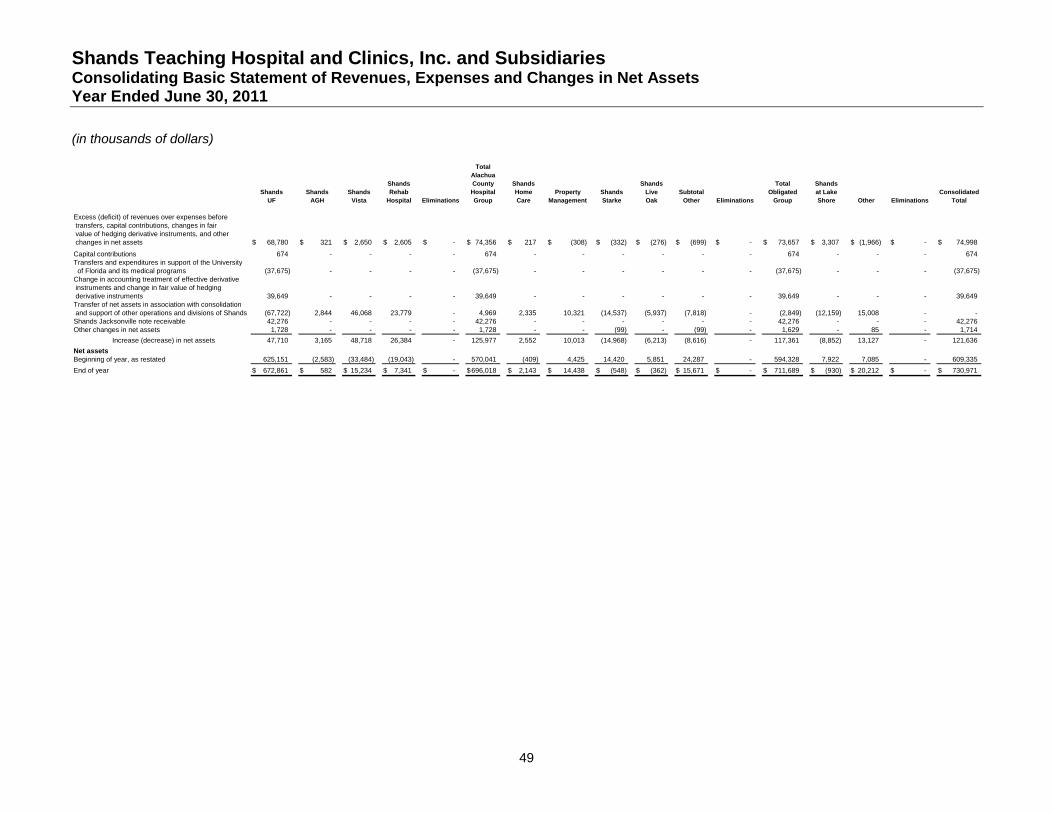

Consolidating Basic Statement of Revenues, Expenses and Changes in Net Assets .......................... 48-49

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Management's Discussion and Analysis (Unaudited) June 30, 2011

1

This section of the Shands Teaching Hospital and Clinics, Inc. and Subsidiaries’ (“Shands”) annual

financial report presents Shands' analysis of its financial performance as of June 30, 2011, and for the

fiscal year then ended. Please read this analysis in conjunction with the consolidated basic financial

statements, which follow this section.

Introduction

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries includes the following:

Shands UF, a major tertiary care teaching institution licensed to operate an 852-bed teaching hospital

which provides clinical settings for medical education programs at the University of Florida.

Shands Vista, an inpatient psychiatric and substance abuse facility licensed to operate 81 beds, of which

57 are psychiatric and 24 are substance abuse.

Shands Rehab Hospital, a 40-bed inpatient rehabilitation hospital located on the same campus as

Shands Vista.

Shands HomeCare is a hospital-based home care agency providing home care services to the citizens

of north central Florida.

Property Management leases properties including a condominium medical office building and

nonmedical buildings.

ElderCare of Alachua County, Inc. provides social and health care support to the elderly in Alachua

County, Florida.

Southeastern HealthCare Foundation, Inc. provides charitable aid to the University of Florida and to

Shands and owns and leases various rental properties in Florida.

First Coast Advantage Central, LLC is a provider service network ("PSN") established to administer

Medicaid in Alachua County and certain contiguous counties.

In November 2009, Shands AGH, an acute care community hospital located in Gainesville, Florida, was

closed and its services consolidated into Shands UF.

On July 1, 2010, Shands sold the operating assets and certain liabilities of three rural hospitals (Shands

at Lake Shore, Shands Starke, and Shands Live Oak) to Health Management Associates, Inc. (“HMA”).

Shands then entered into a partnership agreement with HMA for a 40% minority interest in Lake Shore

HMA, LLC, Starke HMA, LLC, and Live Oak HMA, LLC and HMA manages the operations of the three

facilities. Shands also has an equal partnership interest with Solantic of Orlando, LLC for a walk-in urgent

care center.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Management's Discussion and Analysis (Unaudited) June 30, 2011

2

Effective September 8, 2010, the Board of Directors of Shands approved a motion to reorganize its

corporate structure. Under the reorganization, Shands will no longer be the sole corporate member of

Shands Jacksonville HealthCare, Inc. (“Shands Jacksonville”), but will continue as an affiliated entity

under common control of the University of Florida. Effective September 27, 2010, the Board of Directors

of Shands Jacksonville approved the motion for Shands to no longer be the sole corporate member of

Shands Jacksonville. The reorganization is being accounted for under the de-pooling method of

accounting, and, as such, Shands Jacksonville is no longer consolidated with Shands effective July 1,

2010. Therefore, the financial position and results of operations and changes in net assets of Shands

Jacksonville are not included in these consolidated basic financial statements.

After reassessing its articles of incorporation and bylaws, Shands determined that it meets the definition

of a governmental entity and thus adopted Governmental Accounting Standards Board (“GASB”) financial

reporting. Previously, Shands utilized Financial Accounting Standards Board (“FASB”) financial reporting.

The primary consolidated basic financial statement items affected by the change in accounting treatment

are derivatives, pension liabilities, postemployment benefits, and related effects to net assets. Due to the

differences in accounting treatment and presentation of results, it is management’s determination that it is

not practical to present the consolidated basic financial statements reflecting prior year comparative

information.

As such, Shands is presenting financial results as of June 30, 2011 and the fiscal year then ended in

single-year format. Management will make reference in its discussion and analysis to certain financial

results and statistics from the prior year not impacted by the GASB to FASB conversion. Comparative

analysis will be presented in future years’ consolidated basic financial statements.

This section of Shands’ financial statements presents analysis of the financial condition, the results of

operations and cash flows of Shands as of June 30, 2011 and for the fiscal year then ended. Along with

the information in this report, the notes to the consolidated basic financial statements should be used to

provide additional information that is essential for a full understanding of the consolidated basic financial

statements.

Overview of the Financial Statements

Along with management’s discussion and analysis, the annual financial report includes the independent

certified public accountants’ report, and the consolidated basic financial statements of Shands. The

consolidated basic financial statements also include notes that explain in more detail some of the

information in the consolidated basic financial statements. By referring to the accompanying notes to the

consolidated basic financial statements, a broader understanding of issues impacting financial

performance can be realized.

Statement of Net Assets

The consolidated basic statement of net assets presents the financial position of Shands as of June 30,

2011 and includes all assets and liabilities of Shands. Shands’ net assets, or the difference between total

assets and total liabilities, are one indicator of the current financial condition of Shands. Changes in net

assets are an indicator of whether the overall financial condition of the organization has improved or

worsened over a period of time. Assets and liabilities are generally measured using current values, with

the exception of capital assets, which are stated at historical cost less allowances for depreciation.

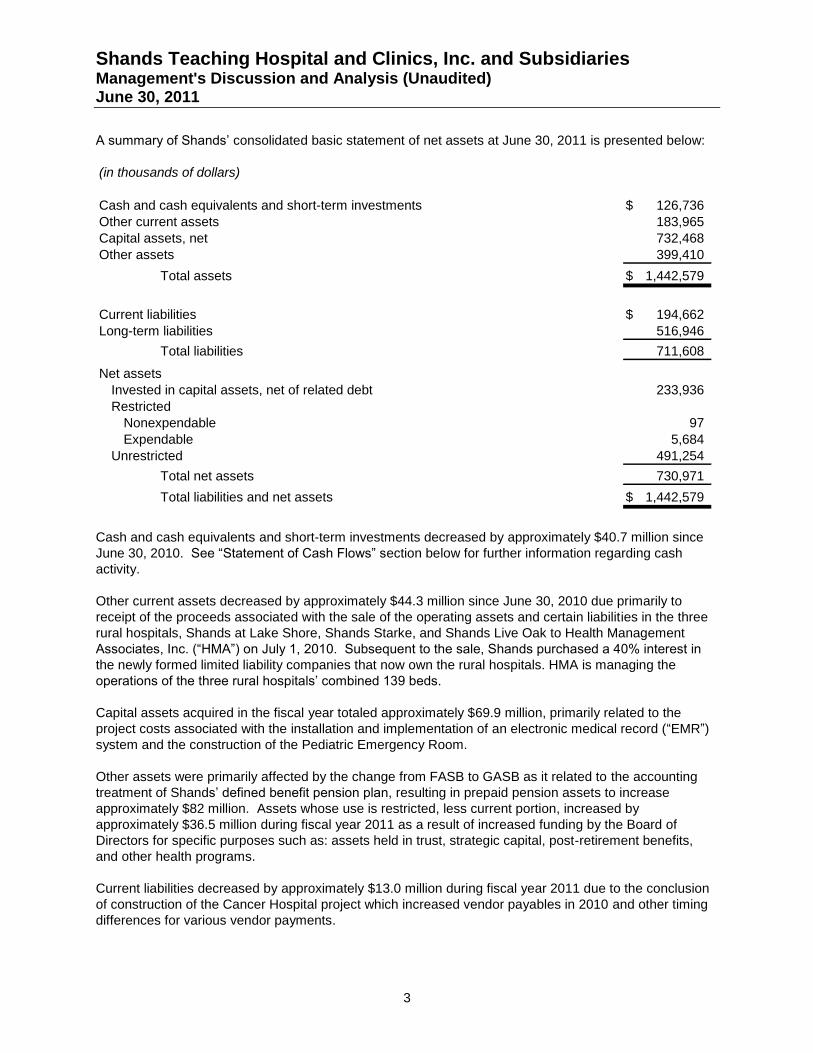

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Management's Discussion and Analysis (Unaudited) June 30, 2011

3

A summary of Shands’ consolidated basic statement of net assets at June 30, 2011 is presented below:

(in thousands of dollars)

Cash and cash equivalents and short-term investments 126,736$

Other current assets 183,965

Capital assets, net 732,468

Other assets 399,410

Total assets 1,442,579$

Current liabilities 194,662$

Long-term liabilities 516,946

Total liabilities 711,608

Net assets

Invested in capital assets, net of related debt 233,936

Restricted

Nonexpendable 97

Expendable 5,684

Unrestricted 491,254

Total net assets 730,971

Total liabilities and net assets 1,442,579$

Cash and cash equivalents and short-term investments decreased by approximately $40.7 million since

June 30, 2010. See “Statement of Cash Flows” section below for further information regarding cash

activity.

Other current assets decreased by approximately $44.3 million since June 30, 2010 due primarily to

receipt of the proceeds associated with the sale of the operating assets and certain liabilities in the three

rural hospitals, Shands at Lake Shore, Shands Starke, and Shands Live Oak to Health Management

Associates, Inc. (“HMA”) on July 1, 2010. Subsequent to the sale, Shands purchased a 40% interest in

the newly formed limited liability companies that now own the rural hospitals. HMA is managing the

operations of the three rural hospitals’ combined 139 beds.

Capital assets acquired in the fiscal year totaled approximately $69.9 million, primarily related to the

project costs associated with the installation and implementation of an electronic medical record (“EMR”)

system and the construction of the Pediatric Emergency Room.

Other assets were primarily affected by the change from FASB to GASB as it related to the accounting

treatment of Shands’ defined benefit pension plan, resulting in prepaid pension assets to increase

approximately $82 million. Assets whose use is restricted, less current portion, increased by

approximately $36.5 million during fiscal year 2011 as a result of increased funding by the Board of

Directors for specific purposes such as: assets held in trust, strategic capital, post-retirement benefits,

and other health programs.

Current liabilities decreased by approximately $13.0 million during fiscal year 2011 due to the conclusion

of construction of the Cancer Hospital project which increased vendor payables in 2010 and other timing

differences for various vendor payments.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Management's Discussion and Analysis (Unaudited) June 30, 2011

4

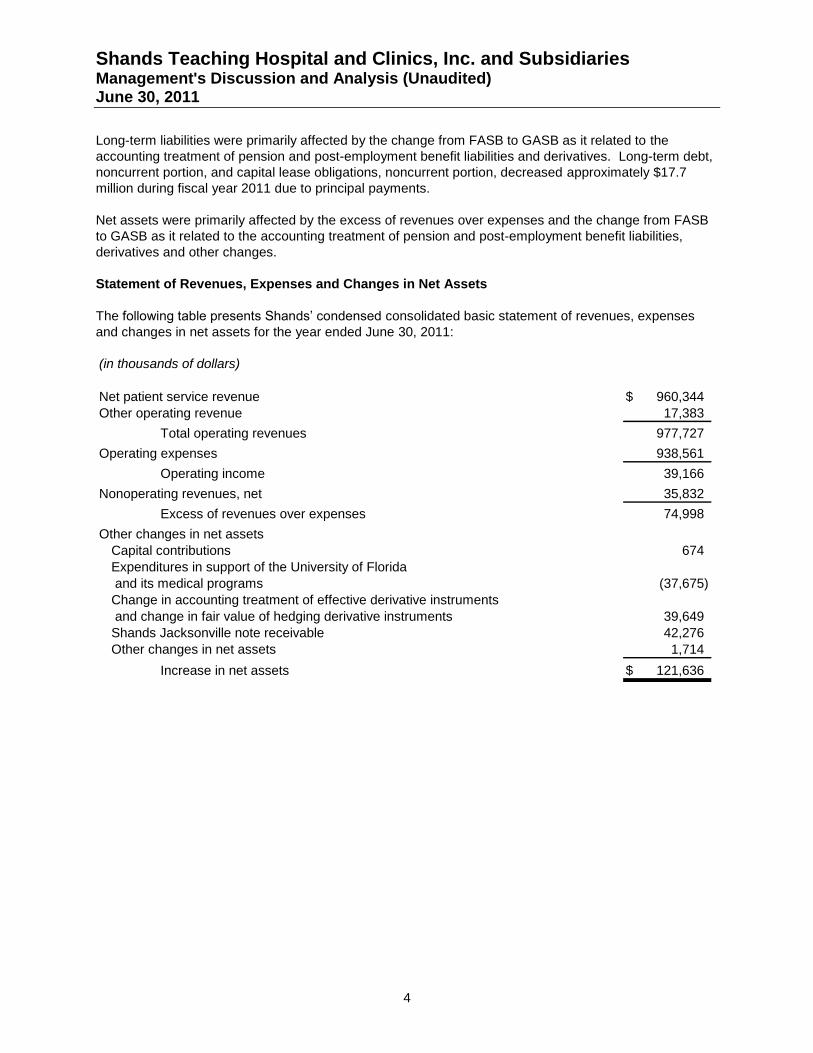

Long-term liabilities were primarily affected by the change from FASB to GASB as it related to the

accounting treatment of pension and post-employment benefit liabilities and derivatives. Long-term debt,

noncurrent portion, and capital lease obligations, noncurrent portion, decreased approximately $17.7

million during fiscal year 2011 due to principal payments.

Net assets were primarily affected by the excess of revenues over expenses and the change from FASB

to GASB as it related to the accounting treatment of pension and post-employment benefit liabilities,

derivatives and other changes.

Statement of Revenues, Expenses and Changes in Net Assets

The following table presents Shands’ condensed consolidated basic statement of revenues, expenses

and changes in net assets for the year ended June 30, 2011:

(in thousands of dollars)

Net patient service revenue 960,344$

Other operating revenue 17,383

Total operating revenues 977,727

Operating expenses 938,561

Operating income 39,166

Nonoperating revenues, net 35,832

Excess of revenues over expenses 74,998

Other changes in net assets

Capital contributions 674

Expenditures in support of the University of Florida

and its medical programs (37,675)

Change in accounting treatment of effective derivative instruments

and change in fair value of hedging derivative instruments 39,649

Shands Jacksonville note receivable 42,276

Other changes in net assets 1,714

Increase in net assets 121,636$

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Management's Discussion and Analysis (Unaudited) June 30, 2011

5

Patient Volumes

Compared to the prior year, inpatient and outpatient volumes decreased primarily as a result of the

closure of Shands AGH in November 2009, and the sale of the three rural hospitals to HMA in July 2010.

The following tables reflect the associated volumes of each facility on a comparative basis to the prior

year.

Net %

2011 2010 Change Change

In-Patient Admissions

Shands UF 36,150 34,026 2,124 6.2%

Shands Vista 3,009 2,768 241 8.7%

Shands Rehab Hospital 808 753 55 7.3%

Subtotal 39,967 37,547 2,420 6.4%

Shands AGH - 1,995 (1,995) -100.0%

Lake Shore, Starke, and Live Oak - 5,963 (5,963) -100.0%

Total 39,967 45,505 (5,538) -12.2%

Net %

2011 2010 Change Change

Out-Patient Visits

Shands UF 707,271 667,399 39,872 6.0%

Shands Vista 20,930 18,487 2,443 13.2%

Shands Rehab Hospital 1,343 1,073 270 25.2%

Subtotal 729,544 686,959 42,585 6.2%

Shands AGH - 25,152 (25,152) -100.0%

Lake Shore, Starke, and Live Oak - 303,786 (303,786) -100.0%

Total 729,544 1,015,897 (286,353) -28.2%

In-patient admissions compared to the prior year were lower by 12.2%. Over the same period, the

admission levels for Shands UF, Vista and Rehab increased 6.4% compared to their prior year volumes

primarily related to the closure of Shands AGH. Out-patient visits compared to the prior year were lower

by 28.2%. Over the same period, the out-patient visit levels for Shands UF, Vista and Rehab increased

6.2% compared to their prior year volumes primarily related to the closure of Shands AGH.

Operating Revenues

Patient service revenue, net of allowances for contractual discounts, charity care and bad debt expense,

was approximately $960.3 million, a decrease of approximately $56.6 million, or 5.6% from fiscal year

2010. The primary factor for the decrease was the sale of the three rural hospitals in July 2010. Other

operating revenues of approximately $17.4 million were approximately $1.0 million lower than the prior

year primarily related to the closure of Shands AGH.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Management's Discussion and Analysis (Unaudited) June 30, 2011

6

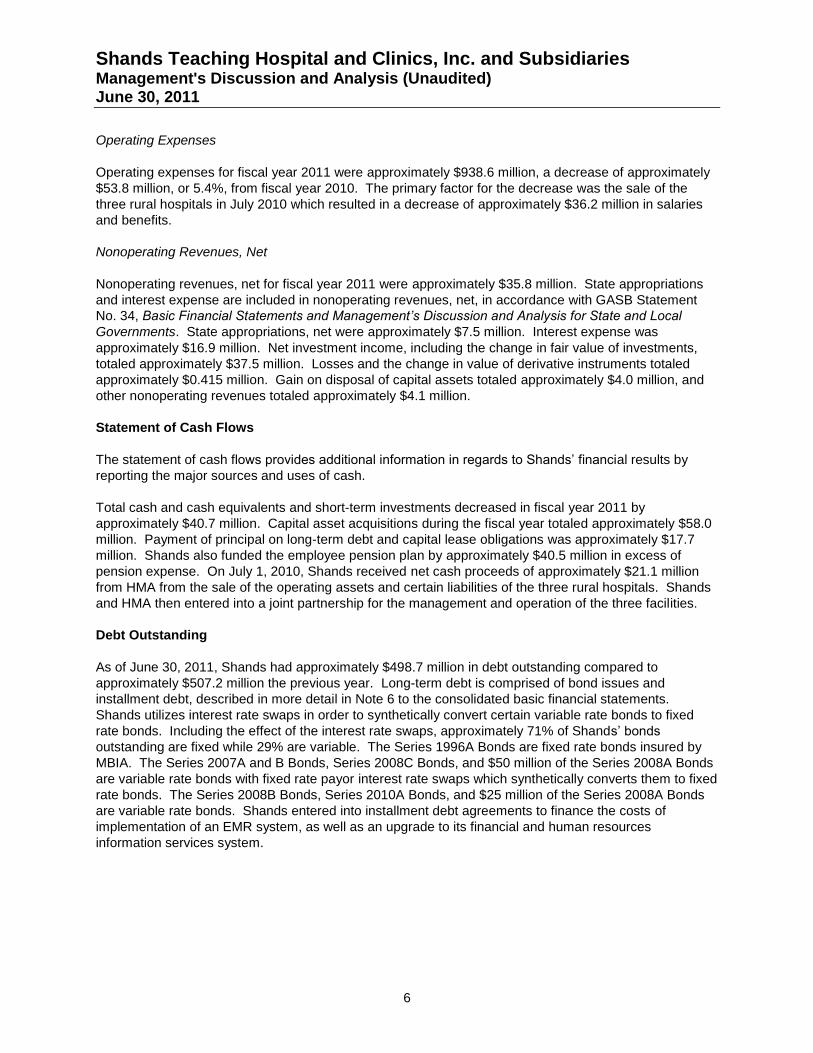

Operating Expenses

Operating expenses for fiscal year 2011 were approximately $938.6 million, a decrease of approximately

$53.8 million, or 5.4%, from fiscal year 2010. The primary factor for the decrease was the sale of the

three rural hospitals in July 2010 which resulted in a decrease of approximately $36.2 million in salaries

and benefits.

Nonoperating Revenues, Net

Nonoperating revenues, net for fiscal year 2011 were approximately $35.8 million. State appropriations

and interest expense are included in nonoperating revenues, net, in accordance with GASB Statement

No. 34, Basic Financial Statements and Management’s Discussion and Analysis for State and Local

Governments. State appropriations, net were approximately $7.5 million. Interest expense was

approximately $16.9 million. Net investment income, including the change in fair value of investments,

totaled approximately $37.5 million. Losses and the change in value of derivative instruments totaled

approximately $0.415 million. Gain on disposal of capital assets totaled approximately $4.0 million, and

other nonoperating revenues totaled approximately $4.1 million.

Statement of Cash Flows

The statement of cash flows provides additional information in regards to Shands’ financial results by

reporting the major sources and uses of cash.

Total cash and cash equivalents and short-term investments decreased in fiscal year 2011 by

approximately $40.7 million. Capital asset acquisitions during the fiscal year totaled approximately $58.0

million. Payment of principal on long-term debt and capital lease obligations was approximately $17.7

million. Shands also funded the employee pension plan by approximately $40.5 million in excess of

pension expense. On July 1, 2010, Shands received net cash proceeds of approximately $21.1 million

from HMA from the sale of the operating assets and certain liabilities of the three rural hospitals. Shands

and HMA then entered into a joint partnership for the management and operation of the three facilities.

Debt Outstanding

As of June 30, 2011, Shands had approximately $498.7 million in debt outstanding compared to

approximately $507.2 million the previous year. Long-term debt is comprised of bond issues and

installment debt, described in more detail in Note 6 to the consolidated basic financial statements.

Shands utilizes interest rate swaps in order to synthetically convert certain variable rate bonds to fixed

rate bonds. Including the effect of the interest rate swaps, approximately 71% of Shands’ bonds

outstanding are fixed while 29% are variable. The Series 1996A Bonds are fixed rate bonds insured by

MBIA. The Series 2007A and B Bonds, Series 2008C Bonds, and $50 million of the Series 2008A Bonds

are variable rate bonds with fixed rate payor interest rate swaps which synthetically converts them to fixed

rate bonds. The Series 2008B Bonds, Series 2010A Bonds, and $25 million of the Series 2008A Bonds

are variable rate bonds. Shands entered into installment debt agreements to finance the costs of

implementation of an EMR system, as well as an upgrade to its financial and human resources

information services system.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Management's Discussion and Analysis (Unaudited) June 30, 2011

7

Capital Assets

At June 30, 2011, Shands had approximately $233.9 million invested in net capital assets. A breakdown

of these assets can be found in Note 5 to the consolidated basic financial statements. This represents a

decrease of approximately $8.0 million from the previous year. Shands expects to make total capital

expenditures of approximately $81.9 million in fiscal year 2012 primarily on expenditures for the EMR

project, facility upgrades, information systems and patient care equipment. These capital purchases are

expected to be funded directly from operations.

Credit Ratings

Shands has received underlying credit ratings of A2 and A from Moody’s Investor Services and Standard

& Poor’s, respectively. Both firms have assigned an outlook of “Stable”. The Moody’s rating was affirmed

in June 2010 and the Standard & Poor’s rating was affirmed in August 2011.

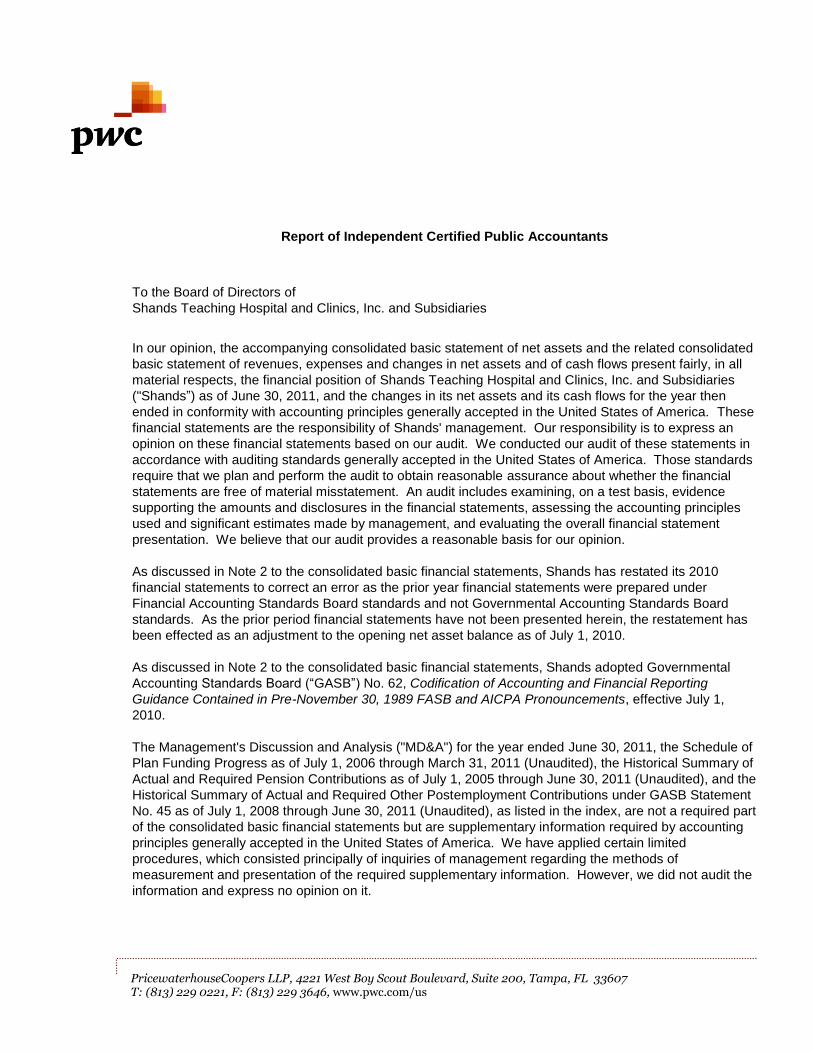

Report of Independent Certified Public Accountants

To the Board of Directors of

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries

In our opinion, the accompanying consolidated basic statement of net assets and the related consolidated

basic statement of revenues, expenses and changes in net assets and of cash flows present fairly, in all

material respects, the financial position of Shands Teaching Hospital and Clinics, Inc. and Subsidiaries

("Shands”) as of June 30, 2011, and the changes in its net assets and its cash flows for the year then

ended in conformity with accounting principles generally accepted in the United States of America. These

financial statements are the responsibility of Shands' management. Our responsibility is to express an

opinion on these financial statements based on our audit. We conducted our audit of these statements in

accordance with auditing standards generally accepted in the United States of America. Those standards

require that we plan and perform the audit to obtain reasonable assurance about whether the financial

statements are free of material misstatement. An audit includes examining, on a test basis, evidence

supporting the amounts and disclosures in the financial statements, assessing the accounting principles

used and significant estimates made by management, and evaluating the overall financial statement

presentation. We believe that our audit provides a reasonable basis for our opinion.

As discussed in Note 2 to the consolidated basic financial statements, Shands has restated its 2010

financial statements to correct an error as the prior year financial statements were prepared under

Financial Accounting Standards Board standards and not Governmental Accounting Standards Board

standards. As the prior period financial statements have not been presented herein, the restatement has

been effected as an adjustment to the opening net asset balance as of July 1, 2010.

As discussed in Note 2 to the consolidated basic financial statements, Shands adopted Governmental

Accounting Standards Board (“GASB”) No. 62, Codification of Accounting and Financial Reporting

Guidance Contained in Pre-November 30, 1989 FASB and AICPA Pronouncements, effective July 1,

2010.

The Management's Discussion and Analysis ("MD&A") for the year ended June 30, 2011, the Schedule of

Plan Funding Progress as of July 1, 2006 through March 31, 2011 (Unaudited), the Historical Summary of

Actual and Required Pension Contributions as of July 1, 2005 through June 30, 2011 (Unaudited), and the

Historical Summary of Actual and Required Other Postemployment Contributions under GASB Statement

No. 45 as of July 1, 2008 through June 30, 2011 (Unaudited), as listed in the index, are not a required part

of the consolidated basic financial statements but are supplementary information required by accounting

principles generally accepted in the United States of America. We have applied certain limited

procedures, which consisted principally of inquiries of management regarding the methods of

measurement and presentation of the required supplementary information. However, we did not audit the

information and express no opinion on it.

PricewaterhouseCoopers LLP, 4221 West Boy Scout Boulevard, Suite 200, Tampa, FL 33607 T: (813) 229 0221, F: (813) 229 3646, www.pwc.com/us

9

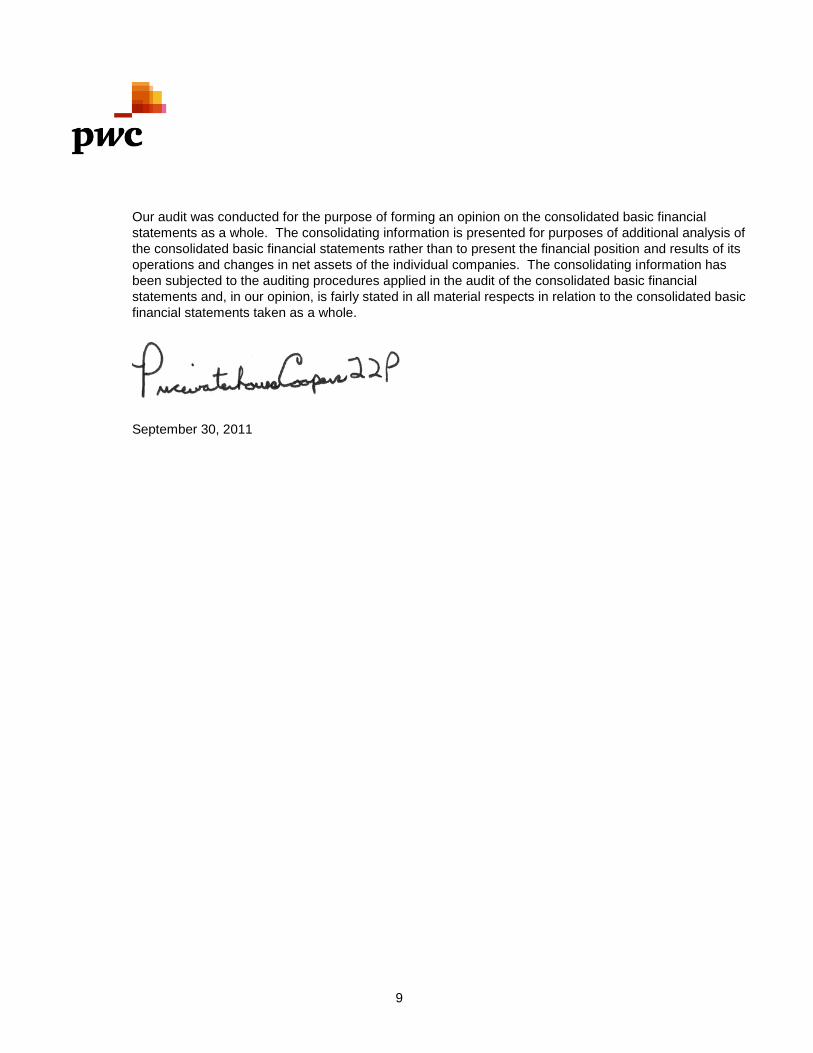

Our audit was conducted for the purpose of forming an opinion on the consolidated basic financial

statements as a whole. The consolidating information is presented for purposes of additional analysis of

the consolidated basic financial statements rather than to present the financial position and results of its

operations and changes in net assets of the individual companies. The consolidating information has

been subjected to the auditing procedures applied in the audit of the consolidated basic financial

statements and, in our opinion, is fairly stated in all material respects in relation to the consolidated basic

financial statements taken as a whole.

September 30, 2011

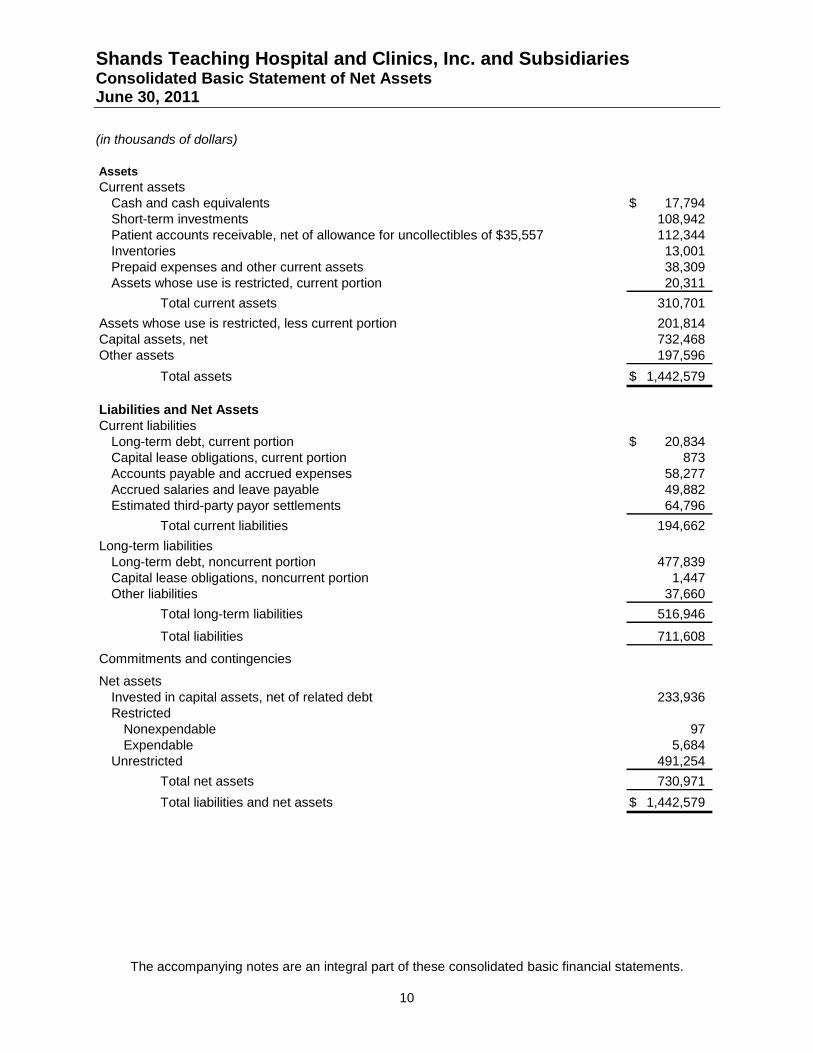

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Consolidated Basic Statement of Net Assets June 30, 2011

(in thousands of dollars)

The accompanying notes are an integral part of these consolidated basic financial statements.

10

Assets

Current assets

Cash and cash equivalents 17,794$

Short-term investments 108,942

Patient accounts receivable, net of allowance for uncollectibles of $35,557 112,344

Inventories 13,001

Prepaid expenses and other current assets 38,309

Assets whose use is restricted, current portion 20,311

Total current assets 310,701

Assets whose use is restricted, less current portion 201,814

Capital assets, net 732,468

Other assets 197,596

Total assets 1,442,579$

Liabilities and Net Assets

Current liabilities

Long-term debt, current portion 20,834$

Capital lease obligations, current portion 873

Accounts payable and accrued expenses 58,277

Accrued salaries and leave payable 49,882

Estimated third-party payor settlements 64,796

Total current liabilities 194,662

Long-term liabilities

Long-term debt, noncurrent portion 477,839

Capital lease obligations, noncurrent portion 1,447

Other liabilities 37,660

Total long-term liabilities 516,946

Total liabilities 711,608

Commitments and contingencies

Net assets

Invested in capital assets, net of related debt 233,936

Restricted

Nonexpendable 97

Expendable 5,684

Unrestricted 491,254

Total net assets 730,971

Total liabilities and net assets 1,442,579$

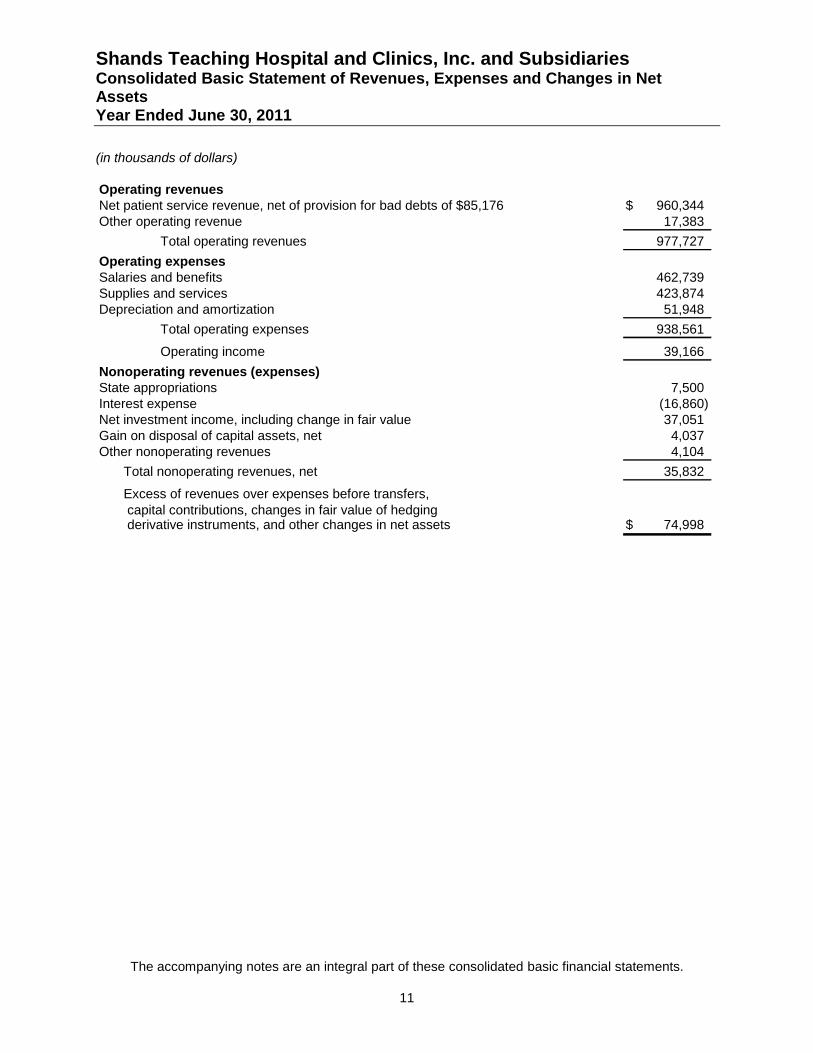

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Consolidated Basic Statement of Revenues, Expenses and Changes in Net Assets Year Ended June 30, 2011

(in thousands of dollars)

The accompanying notes are an integral part of these consolidated basic financial statements.

11

Operating revenues

Net patient service revenue, net of provision for bad debts of $85,176 960,344$

Other operating revenue 17,383

Total operating revenues 977,727

Operating expenses

Salaries and benefits 462,739

Supplies and services 423,874

Depreciation and amortization 51,948

Total operating expenses 938,561

Operating income 39,166

Nonoperating revenues (expenses)

State appropriations 7,500

Interest expense (16,860)

Net investment income, including change in fair value 37,051

Gain on disposal of capital assets, net 4,037

Other nonoperating revenues 4,104

Total nonoperating revenues, net 35,832

Excess of revenues over expenses before transfers,

capital contributions, changes in fair value of hedging derivative instruments, and other changes in net assets 74,998$

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Consolidated Basic Statement of Revenues, Expenses and Changes in Net Assets Year Ended June 30, 2011

(in thousands of dollars)

The accompanying notes are an integral part of these consolidated basic financial statements.

12

Excess of revenues over expenses before transfers, capital contributions,

changes in fair value of hedging derivative instruments, and

other changes in net assets 74,998$

Capital contributions 674

Transfers and expenditures in support of the University of Florida and its

medical programs (37,675)

Change in accounting treatment of effective derivative instruments

and change in fair value of hedging derivative instruments 39,649

Shands Jacksonville note receivable 42,276

Other changes in net assets 1,714

Increase in net assets 121,636

Net assets

Beginning of year, as restated (Note 2) 609,335

End of year 730,971$

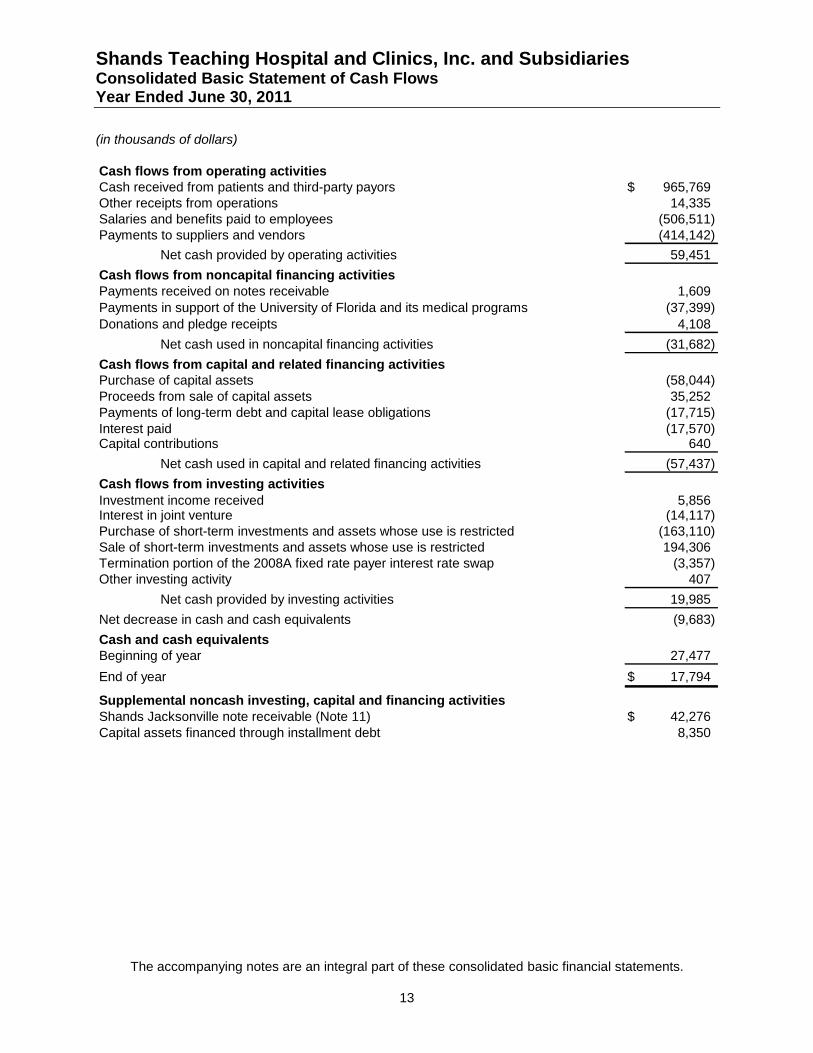

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Consolidated Basic Statement of Cash Flows Year Ended June 30, 2011

(in thousands of dollars)

The accompanying notes are an integral part of these consolidated basic financial statements.

13

Cash flows from operating activities

Cash received from patients and third-party payors 965,769$

Other receipts from operations 14,335

Salaries and benefits paid to employees (506,511)

Payments to suppliers and vendors (414,142)

Net cash provided by operating activities 59,451

Cash flows from noncapital financing activities

Payments received on notes receivable 1,609

Payments in support of the University of Florida and its medical programs (37,399)

Donations and pledge receipts 4,108

Net cash used in noncapital financing activities (31,682)

Cash flows from capital and related financing activities

Purchase of capital assets (58,044)

Proceeds from sale of capital assets 35,252

Payments of long-term debt and capital lease obligations (17,715)

Interest paid (17,570)Capital contributions 640

Net cash used in capital and related financing activities (57,437)

Cash flows from investing activities

Investment income received 5,856Interest in joint venture (14,117)

Purchase of short-term investments and assets whose use is restricted (163,110)

Sale of short-term investments and assets whose use is restricted 194,306

Termination portion of the 2008A fixed rate payer interest rate swap (3,357)

Other investing activity 407

Net cash provided by investing activities 19,985

Net decrease in cash and cash equivalents (9,683)

Cash and cash equivalents

Beginning of year 27,477

End of year 17,794$

Supplemental noncash investing, capital and financing activities

Shands Jacksonville note receivable (Note 11) 42,276$

Capital assets financed through installment debt 8,350

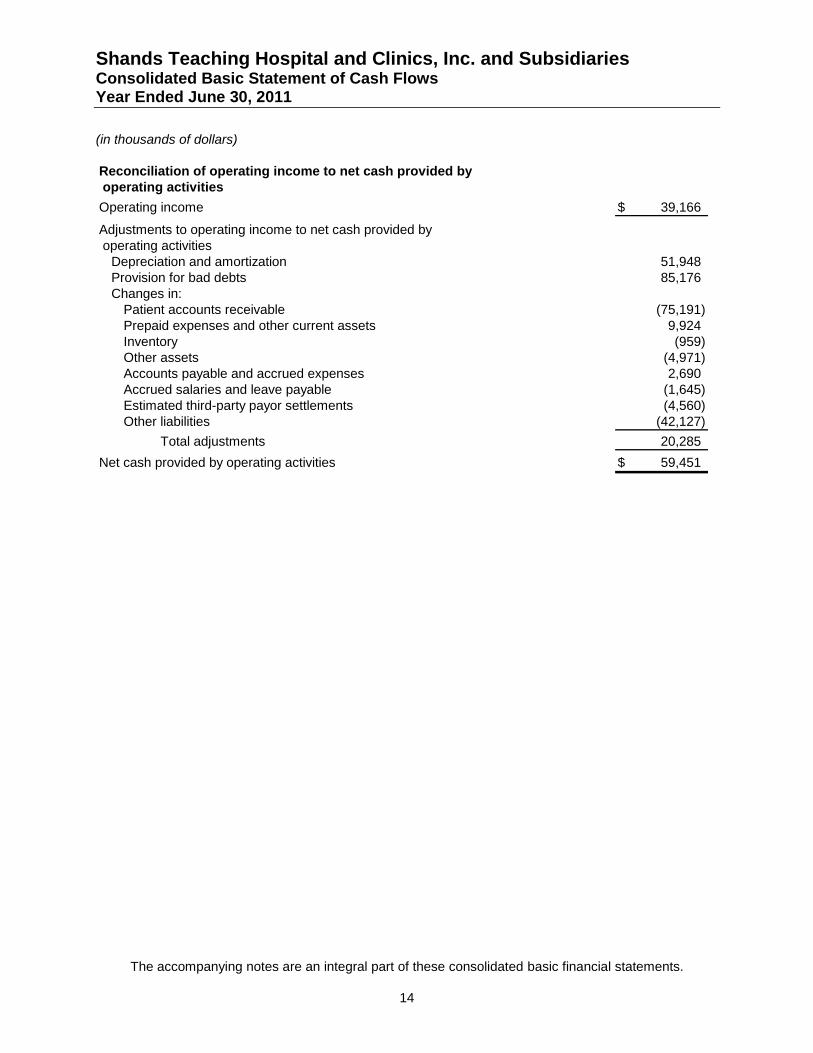

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Consolidated Basic Statement of Cash Flows Year Ended June 30, 2011

(in thousands of dollars)

The accompanying notes are an integral part of these consolidated basic financial statements.

14

Reconciliation of operating income to net cash provided by

operating activities

Operating income 39,166$

Adjustments to operating income to net cash provided by

operating activities

Depreciation and amortization 51,948

Provision for bad debts 85,176

Changes in:

Patient accounts receivable (75,191)

Prepaid expenses and other current assets 9,924

Inventory (959)

Other assets (4,971)

Accounts payable and accrued expenses 2,690

Accrued salaries and leave payable (1,645)

Estimated third-party payor settlements (4,560)

Other liabilities (42,127)

Total adjustments 20,285

Net cash provided by operating activities 59,451$

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

15

1. Organization

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries (“Shands”) was incorporated on

October 15, 1979 as a Florida not-for-profit corporation. The President of the University of Florida

("UF"), or his designee, serves as the President of Shands’ Board of Directors and retains

appointment and termination rights over a majority of the members of Shands’ Board of Directors.

The President of UF is deemed a state official as the position is appointed by a Board of Trustees

that govern UF (the "UF Board"), and the members of the UF Board are appointed by the Governor

and the Board of Governors of the state of Florida.

Shands operates a multi-hospital system. The accompanying consolidated basic financial

statements consolidate the accounts of Shands and its subsidiaries, as described below:

Shands UF, a division of Shands, is a major tertiary care teaching institution located in

Gainesville, Florida, licensed to operate an 852-bed teaching hospital. Shands UF is a

leading referral center in the State of Florida and provides clinical settings for medical

education programs at the University of Florida.

Shands Vista, a division of Shands, is an inpatient psychiatric and substance abuse facility

located in Gainesville, Florida, licensed to operate 81 beds, of which 57 are psychiatric and 24

are substance abuse.

Shands Rehab Hospital, a division of Shands, is a 40-bed inpatient rehabilitation hospital

located on the same campus as Shands Vista.

Shands HomeCare, a division of Shands, is a hospital-based home care agency providing

home care services to the citizens of north central Florida.

Property Management, a division of Shands, leases properties in Gainesville including a

condominium medical office building and nonmedical buildings.

ElderCare of Alachua County, Inc. (“ElderCare”), a Florida not-for-profit corporation,

provides social and health care support to the elderly in Alachua County, Florida, through

programs such as Meals on Wheels and an Alzheimer’s Day Care Center. Shands is the sole

corporate member of ElderCare.

Southeastern HealthCare Foundation, Inc. (“Foundation”), a Florida not-for-profit

corporation, provides charitable aid to the University of Florida and to Shands and owns and

leases various rental properties in Florida. Shands is the sole corporate member of the

Foundation.

First Coast Advantage Central, LLC is a provider service network (“PSN”) established to

administer Medicaid in Alachua and certain contiguous counties.

In November 2009, Shands AGH, an acute care community hospital located in Gainesville, Florida,

was closed and its services consolidated into Shands UF.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

16

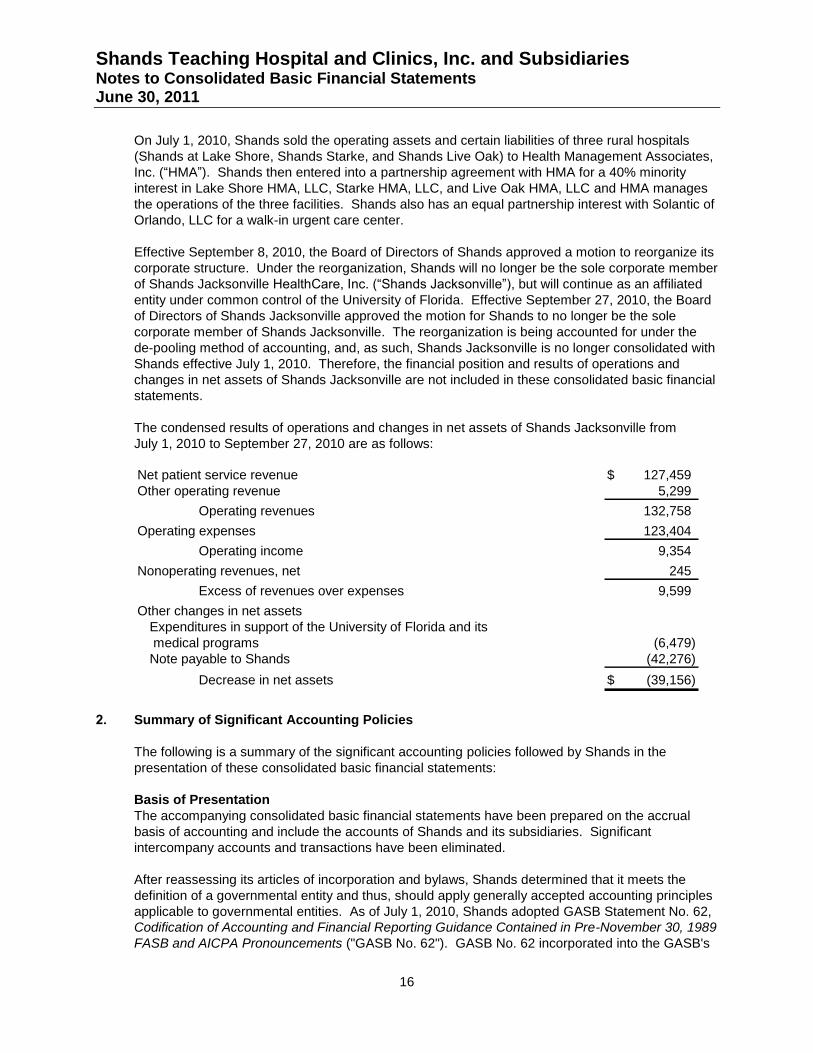

On July 1, 2010, Shands sold the operating assets and certain liabilities of three rural hospitals

(Shands at Lake Shore, Shands Starke, and Shands Live Oak) to Health Management Associates,

Inc. (“HMA”). Shands then entered into a partnership agreement with HMA for a 40% minority

interest in Lake Shore HMA, LLC, Starke HMA, LLC, and Live Oak HMA, LLC and HMA manages

the operations of the three facilities. Shands also has an equal partnership interest with Solantic of

Orlando, LLC for a walk-in urgent care center.

Effective September 8, 2010, the Board of Directors of Shands approved a motion to reorganize its

corporate structure. Under the reorganization, Shands will no longer be the sole corporate member

of Shands Jacksonville HealthCare, Inc. (“Shands Jacksonville”), but will continue as an affiliated

entity under common control of the University of Florida. Effective September 27, 2010, the Board

of Directors of Shands Jacksonville approved the motion for Shands to no longer be the sole

corporate member of Shands Jacksonville. The reorganization is being accounted for under the

de-pooling method of accounting, and, as such, Shands Jacksonville is no longer consolidated with

Shands effective July 1, 2010. Therefore, the financial position and results of operations and

changes in net assets of Shands Jacksonville are not included in these consolidated basic financial

statements.

The condensed results of operations and changes in net assets of Shands Jacksonville from

July 1, 2010 to September 27, 2010 are as follows:

Net patient service revenue 127,459$

Other operating revenue 5,299

Operating revenues 132,758

Operating expenses 123,404

Operating income 9,354

Nonoperating revenues, net 245

Excess of revenues over expenses 9,599

Other changes in net assets

Expenditures in support of the University of Florida and its

medical programs (6,479)

Note payable to Shands (42,276)

Decrease in net assets (39,156)$

2. Summary of Significant Accounting Policies

The following is a summary of the significant accounting policies followed by Shands in the

presentation of these consolidated basic financial statements:

Basis of Presentation

The accompanying consolidated basic financial statements have been prepared on the accrual

basis of accounting and include the accounts of Shands and its subsidiaries. Significant

intercompany accounts and transactions have been eliminated.

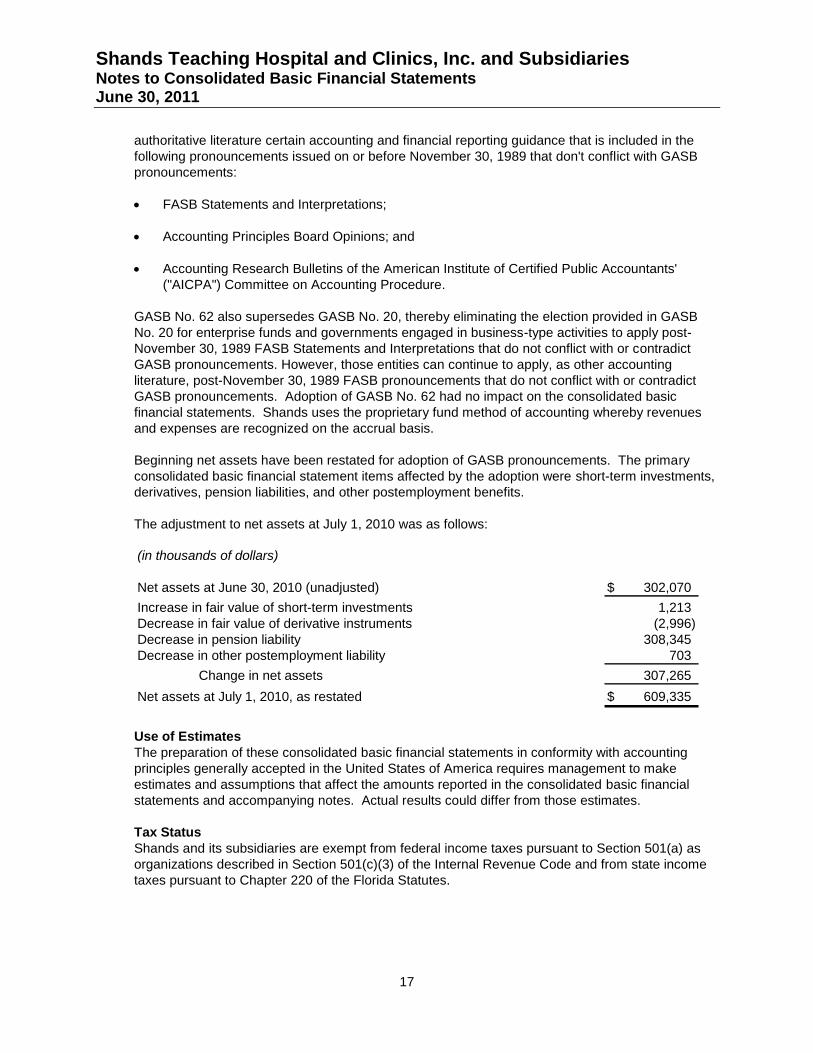

After reassessing its articles of incorporation and bylaws, Shands determined that it meets the

definition of a governmental entity and thus, should apply generally accepted accounting principles

applicable to governmental entities. As of July 1, 2010, Shands adopted GASB Statement No. 62,

Codification of Accounting and Financial Reporting Guidance Contained in Pre-November 30, 1989

FASB and AICPA Pronouncements ("GASB No. 62"). GASB No. 62 incorporated into the GASB's

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

17

authoritative literature certain accounting and financial reporting guidance that is included in the

following pronouncements issued on or before November 30, 1989 that don't conflict with GASB

pronouncements:

FASB Statements and Interpretations;

Accounting Principles Board Opinions; and

Accounting Research Bulletins of the American Institute of Certified Public Accountants'

("AICPA") Committee on Accounting Procedure.

GASB No. 62 also supersedes GASB No. 20, thereby eliminating the election provided in GASB

No. 20 for enterprise funds and governments engaged in business-type activities to apply post-

November 30, 1989 FASB Statements and Interpretations that do not conflict with or contradict

GASB pronouncements. However, those entities can continue to apply, as other accounting

literature, post-November 30, 1989 FASB pronouncements that do not conflict with or contradict

GASB pronouncements. Adoption of GASB No. 62 had no impact on the consolidated basic

financial statements. Shands uses the proprietary fund method of accounting whereby revenues

and expenses are recognized on the accrual basis.

Beginning net assets have been restated for adoption of GASB pronouncements. The primary

consolidated basic financial statement items affected by the adoption were short-term investments,

derivatives, pension liabilities, and other postemployment benefits.

The adjustment to net assets at July 1, 2010 was as follows:

(in thousands of dollars)

Net assets at June 30, 2010 (unadjusted) 302,070$

Increase in fair value of short-term investments 1,213

Decrease in fair value of derivative instruments (2,996)

Decrease in pension liability 308,345

Decrease in other postemployment liability 703

Change in net assets 307,265

Net assets at July 1, 2010, as restated 609,335$

Use of Estimates

The preparation of these consolidated basic financial statements in conformity with accounting

principles generally accepted in the United States of America requires management to make

estimates and assumptions that affect the amounts reported in the consolidated basic financial

statements and accompanying notes. Actual results could differ from those estimates.

Tax Status

Shands and its subsidiaries are exempt from federal income taxes pursuant to Section 501(a) as

organizations described in Section 501(c)(3) of the Internal Revenue Code and from state income

taxes pursuant to Chapter 220 of the Florida Statutes.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

18

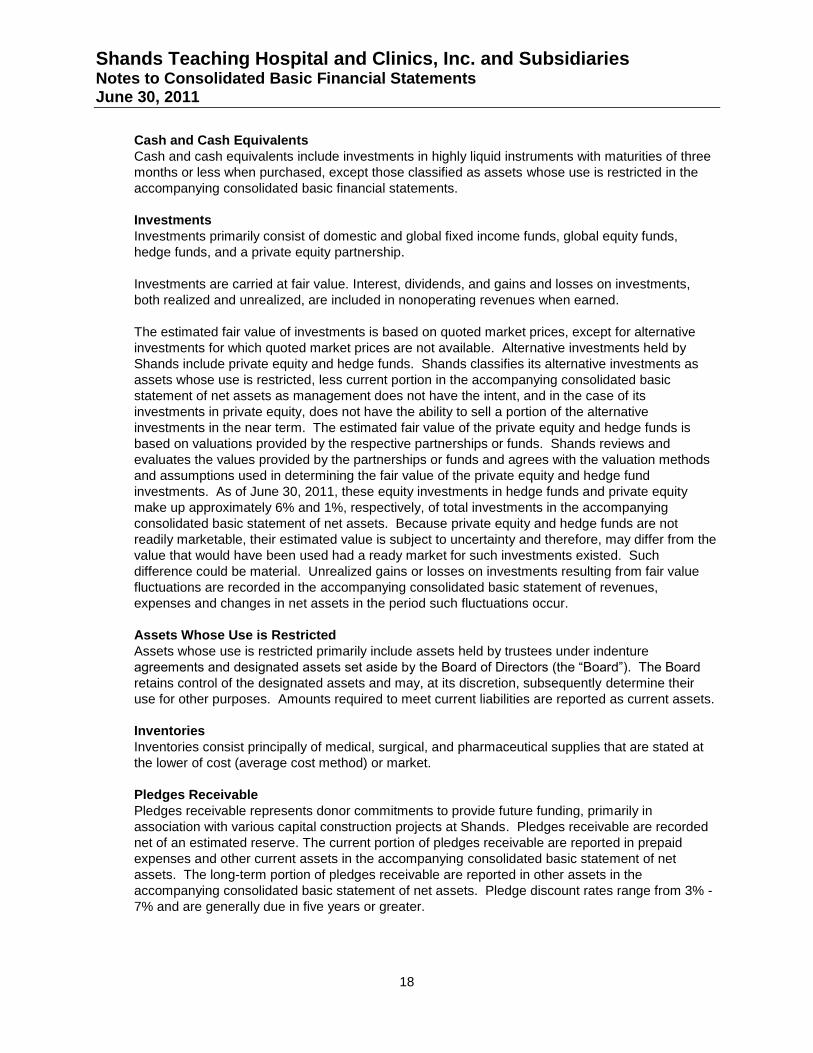

Cash and Cash Equivalents

Cash and cash equivalents include investments in highly liquid instruments with maturities of three

months or less when purchased, except those classified as assets whose use is restricted in the

accompanying consolidated basic financial statements.

Investments

Investments primarily consist of domestic and global fixed income funds, global equity funds,

hedge funds, and a private equity partnership.

Investments are carried at fair value. Interest, dividends, and gains and losses on investments,

both realized and unrealized, are included in nonoperating revenues when earned.

The estimated fair value of investments is based on quoted market prices, except for alternative

investments for which quoted market prices are not available. Alternative investments held by

Shands include private equity and hedge funds. Shands classifies its alternative investments as

assets whose use is restricted, less current portion in the accompanying consolidated basic

statement of net assets as management does not have the intent, and in the case of its

investments in private equity, does not have the ability to sell a portion of the alternative

investments in the near term. The estimated fair value of the private equity and hedge funds is

based on valuations provided by the respective partnerships or funds. Shands reviews and

evaluates the values provided by the partnerships or funds and agrees with the valuation methods

and assumptions used in determining the fair value of the private equity and hedge fund

investments. As of June 30, 2011, these equity investments in hedge funds and private equity

make up approximately 6% and 1%, respectively, of total investments in the accompanying

consolidated basic statement of net assets. Because private equity and hedge funds are not

readily marketable, their estimated value is subject to uncertainty and therefore, may differ from the

value that would have been used had a ready market for such investments existed. Such

difference could be material. Unrealized gains or losses on investments resulting from fair value

fluctuations are recorded in the accompanying consolidated basic statement of revenues,

expenses and changes in net assets in the period such fluctuations occur.

Assets Whose Use is Restricted

Assets whose use is restricted primarily include assets held by trustees under indenture

agreements and designated assets set aside by the Board of Directors (the “Board”). The Board

retains control of the designated assets and may, at its discretion, subsequently determine their

use for other purposes. Amounts required to meet current liabilities are reported as current assets.

Inventories

Inventories consist principally of medical, surgical, and pharmaceutical supplies that are stated at

the lower of cost (average cost method) or market.

Pledges Receivable

Pledges receivable represents donor commitments to provide future funding, primarily in

association with various capital construction projects at Shands. Pledges receivable are recorded

net of an estimated reserve. The current portion of pledges receivable are reported in prepaid

expenses and other current assets in the accompanying consolidated basic statement of net

assets. The long-term portion of pledges receivable are reported in other assets in the

accompanying consolidated basic statement of net assets. Pledge discount rates range from 3% -

7% and are generally due in five years or greater.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

19

Capital Assets

Capital assets have been recorded at historical cost or fair market value at date of purchase or

donation, respectively. Equipment under capital leases is stated at the present value of minimum

lease payments at the inception of the lease. Routine maintenance and repairs are expensed

when incurred. Expenditures that materially increase the value, change the capacity or extend the

useful life of an asset are capitalized. Interest costs incurred on borrowed funds during the period

of construction of capital assets are capitalized as a component of the cost of acquiring those

assets. Depreciation for financial reporting purposes is computed using the straight-line method

over the estimated useful lives of the related depreciable assets as recommended by the American

Hospital Association. Capital assets under capital leases are amortized using the straight-line

method over the shorter period of the lease term or the estimated useful life of the related assets.

Such amortization is included in depreciation and amortization expense in the accompanying

consolidated basic statement of revenues, expenses and changes in net assets. Gains and losses

on dispositions are recorded in the year of disposal.

Goodwill

Goodwill represents the excess of the acquisition cost over the fair value of the net assets of

businesses acquired. Goodwill was approximately $2,982,000 at June 30, 2011, and is included in

other assets in the accompanying consolidated basic statement of net assets. Goodwill is

evaluated for impairment annually. Management evaluated goodwill and based on the analysis

performed, no impairment loss was recorded for the year ended June 30, 2011.

Joint Ventures

In May 2010, Shands entered into an agreement to sell a 60% controlling interest in its three rural

hospitals, Shands at Lake Shore, Shands Starke, and Shands Live Oak to Health Management

Associates, Inc. (“HMA”). The closing date of the sale was July 1, 2010. Shands recognized a gain

on disposal of capital assets of approximately $4,711,000 which is included in gain on disposal of

capital assets in the accompanying consolidated basic statement of revenues, expenses and

changes in net assets. Shands accounts for the investment under the equity method of accounting.

The investment was approximately $12,823,000, which was recorded in other assets in the

accompanying consolidated basic statement of net assets at June 30, 2011. The investment loss

of approximately $1,545,000 was recorded in other nonoperating revenues in the accompanying

consolidated basic statement of revenues, expenses and changes in net assets for the year ended

June 30, 2011.

Bond Issuance Costs and Bond Premium and Discounts

Bond issuance costs and bond premiums and discounts are amortized over the period the bonds

are outstanding using the effective interest method. Amortization of bond issuance costs of

approximately $320,000 was recorded for the year ending June 30, 2011 and unamortized bond

costs at June 30, 2011 of approximately $2,461,000 was recorded in other assets in the

accompanying consolidated basic statement of net assets.

Accrued Personal Leave

Shands provides accrued time off to eligible employees for vacations, holidays, and short-term

illness dependent on their years of continuous service and their payroll classification. Shands

accrues the estimated expense related to personal leave based on pay rates currently in effect.

Upon termination of employment, employees will have their eligible accrued personal leave paid in

full.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

20

Long-Term Debt

The fair value of fixed rate debt is estimated based on dealer quotes for hospital tax-exempt debt

with similar terms and maturities and using discounted cash flow analyses based on current

interest rates for similar types of borrowing arrangements. The fair value of variable rate debt

approximates its carrying value. The carrying value of Shands’ long-term debt is approximately

$498,673,000 at June 30, 2011. The fair value is approximately $461,280,000 at June 30, 2011.

Net Assets

Net assets are categorized as “invested in capital assets, net of related debt,” “restricted -

expendable,” “restricted - nonexpendable,” and “unrestricted.” Invested in capital assets, net of

related debt is intended to reflect the portion of net assets that are associated with non liquid

capital assets, less outstanding balances due on borrowings used to finance the purchase or

construction of those assets. Restricted net assets have restrictions placed on the use of net

assets through external constraints imposed by contributors. Restricted – nonexpendable net

assets are those that have been restricted by donors to be maintained by Shands in perpetuity.

Restricted – expendable net assets are those whose use by Shands has been limited by donors to

a specific time period or purpose. Unrestricted net assets are net assets that do not meet the

definition of invested in capital assets, net of related debt and have no third-party restrictions on

use.

Operating Revenues and Expenses

Shands' consolidated basic statement of revenues, expenses and changes in net assets

distinguishes between operating and nonoperating revenues and expenses. Operating revenues

result from exchange transactions associated with providing health care services, Shands' principal

activity. State appropriations, net investment income, interest expense, and gain on disposal of

assets are reported as nonoperating revenues (expenses). Donations received for the purpose of

acquiring or constructing capital assets are recorded below nonoperating revenues as capital

contributions. Operating expenses are all expenses incurred to provide health care services,

excluding financing costs.

Net Patient Service Revenue and Patient Accounts Receivable

Shands has agreements with third-party payors that provide for payments to Shands at amounts

different from its established rates. Payment arrangements include prospectively determined rates

per discharge, reimbursed costs, discounted charges, and per diem payments. Net patient service

revenue and patient accounts receivable are reported at estimated net realizable amounts from

patients, third-party payors, and others for services rendered and include estimated retroactive

revenue adjustments due to future audits, reviews, and investigations. Retroactive adjustments are

considered in the recognition of revenue on an estimated basis in the period the related services

are rendered, and such amounts are adjusted in future periods as adjustments become known or

as years are no longer subject to such audits, reviews, and investigations. For the year ended

June 30, 2011, net patient service revenue increased approximately $13,676,000 due to such

adjustments.

Laws and regulations governing the Medicare and Medicaid programs are extremely complex and

subject to interpretation. As a result, there is at least a reasonable possibility that recorded

estimates will change by a material amount in the near term.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

21

Medicare

Shands participates in the federal Medicare program ("Medicare"). Approximately 31% of Shands’

net patient service revenue in fiscal year 2011 was derived from services to Medicare beneficiaries.

Inpatient acute care services rendered to Medicare beneficiaries are reimbursed at prospectively

determined rates per discharge. These rates vary according to a patient classification system that

is based on clinical, diagnostic, and other factors.

Inpatient non-acute services, outpatient services, and defined capital costs related to Medicare

beneficiaries are reimbursed based upon a prospective reimbursement methodology. Shands is

paid for cost-reimbursable items at a tentative rate with final settlement determined after

submission of annual cost reports by Shands and audits by the Medicare fiscal intermediary.

Shands' classification of patients under the Medicare program and the appropriateness of their

admission are subject to an independent review. As of June 30, 2011, the Medicare cost reports

were final settled by Shands' Medicare fiscal intermediary through June 30, 2006.

It is management’s opinion that settlements of outstanding Medicare cost reports, when received,

will not vary materially from the estimated amounts, which are recorded as current liabilities in the

accompanying consolidated basic statement of net assets.

Medicaid

Approximately 22% of Shands' net patient service revenue for fiscal year 2011 was derived under

the Medicaid program. Inpatient and outpatient services rendered to Medicaid program

beneficiaries are paid based upon a cost reimbursement methodology subject to certain ceilings.

Shands is reimbursed at a tentative rate with final settlement determined after submission of

annual cost reports by Shands, and audits by the Medicaid fiscal intermediary. The Medicaid cost

reports have been audited by the Medicaid fiscal intermediary through June 30, 2005. In addition

to the tentative payments received by Shands for the provision of health care services to Medicaid

beneficiaries, the State of Florida provides supplemental Medicaid and disproportionate share

payments to reflect the additional costs associated with treating the Medicaid population in Florida.

These amounts are reflected in net patient service revenue in the accompanying consolidated

basic statement of revenue, expenses and changes in net assets.

Shands Medicaid interim rates are based on the most recent “as filed” Medicare/Medicaid cost

report. The rates used in 2011 were based on the unaudited cost report for 2009.

It is management’s opinion that settlements of outstanding Medicaid cost reports, when received,

will not vary materially from the estimated amounts, which are recorded as current liabilities in the

accompanying consolidated basic statement of net assets.

Other Third-Party Payors

Shands has also entered into reimbursement agreements with certain commercial insurance

carriers, health maintenance organizations, and preferred provider organizations. The basis for

reimbursement under these agreements includes prospectively determined rates per discharge,

discounts from established charges and prospectively determined per diem rates.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

22

Provision for Bad Debts and Allowance for Uncollectible Accounts

The provision for bad debts is based on management’s assessment of historical and expected net

collections, considering business and economic conditions, trends in federal and state

governmental health care coverage, and other collection indicators. Throughout the year,

management assesses the adequacy of the allowance for uncollectible accounts based upon these

trends. The results of this review are then used to make any modification to the provision for bad

debts to establish an appropriate allowance for uncollectible accounts. Patient accounts receivable

are written off after collection efforts have been followed under Shands’ policies.

Risk Management

Shands is exposed to various risks of loss from torts; theft of, damage to, and destruction of assets;

business interruption; errors and omissions; employee injuries and illnesses; natural disasters;

medical malpractice; and employee health, dental, and accident benefits. Commercial insurance

coverage is purchased for claims arising from such matters in excess of self-insured limits. Settled

claims have not exceeded this commercial coverage in 2011.

Effective July 1, 2011, Shands was granted sovereign immunity under the provision of Chapter

2011-114, Laws of Florida. As such, recovery in tort actions arising subsequent to June 30, 2011

will be limited to $100,000 for any one person for one incident and all recovery related to one

incident is limited to a total of $200,000. Effective October 1, 2011, the limits increase to $200,000

for any one person for one incident and $300,000 in total for one incident.

Derivative Financial Instruments

Shands’ derivative financial instruments consist of interest rate swaps, which are utilized by

Shands to manage net exposure to interest rate changes associated with its variable rate debt and

to lower its overall borrowing costs. Shands accounts for its derivative financial instruments under

GASB Statement No. 53, Accounting and Financial Reporting for Derivative Instruments (“GASB

No. 53”). GASB No. 53 addresses the recognition, measurement, and disclosure of information

regarding derivative instruments entered into by state and local governments (Note 7). Shands

entered into the floating to fixed interest rate swap agreements to reduce the market risk

associated with the changes in interest rates related to Shands' revenue bonds. For those interest

rate swaps that qualify for hedge accounting, as they are highly effective in offsetting changes to

expected future cash flows on interest payments, changes in the fair value of the interest rate swap

agreement are considered to be deferred inflows or outflows. Deferred outflows related to hedging

instruments are recorded in other assets while deferred inflows related to hedging instruments are

recorded in other liabilities within the consolidated basic statement of net assets. Changes in fair

value of interest rate swaps that do not qualify for hedge accounting are included within net

investment income in the accompanying consolidated basic statement of revenues, expenses and

changes in net assets.

Future Accounting Pronouncements

In June 2011, the GASB issued GASB Statement No. 63, Financial Reporting of Deferred Outflows

of Resources, Deferred Inflows of Resources, and Net Position ("GASB No. 63"). GASB No. 63

improves financial reporting by standardizing the presentation of deferred outflows of resources

and deferred inflows of resources and their effects on a government’s net position. It alleviates

uncertainty about reporting those financial statement elements by providing guidance where none

previously existed. The provisions of GASB No. 63 are effective for financial statements for periods

beginning after December 15, 2011. Shands did not adopt GASB No. 63 for the year ended

June 30, 2011.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

23

In June 2011, the GASB issued GASB Statement No. 64, Derivative Instruments: Application of

Hedge Accounting Termination Provisions ("GASB No. 64"), an amendment of GASB No. 53.

GASB No. 64 clarifies whether an effective hedging relationship continues after the replacement of

a swap counterparty or a swap counterparty’s credit support provider. GASB No. 64 sets forth

criteria that establish when the effective hedging relationship continues and hedge accounting

should continue to be applied. The provisions of GASB No. 64 are effective for financial statements

for periods beginning after June 15, 2011. Shands did not adopt GASB No. 64 for the year ended

June 30, 2011.

3. Unsponsored Community Benefit

Community benefit is a planned, managed, organized, and measured approach to a health care

organization’s participation in meeting identified community health needs. It implies collaboration

with a “community” to “benefit” its residents, particularly the poor and other underserved groups, by

improving health status and quality of life. Community benefit projects and services are identified

by health care organizations in response to findings of a community health assessment, strategic

and/or clinical priorities, and partnership areas of attention.

Community benefit categories include financial assistance, community health services, health

professions education, research, and donations. Shands has a long history of providing community

benefits and has quantified these benefits using national guidelines developed by the Catholic

Health Association in collaboration with the Voluntary Hospital Association.

Shands has policies providing financial assistance for patients requiring care but who have limited

or no means to pay for that care. These policies provide free or discounted health and health-

related services to persons who qualify under certain income and asset criteria. Because Shands

does not pursue collection of amounts determined to qualify for financial assistance, they are not

reported as net patient service revenue. Shands maintains records to identify and monitor the level

of financial assistance it provides. Charges foregone for services provided under Shands’ financial

assistance policy as a percentage of total charges for the year ended June 30, 2011 was

approximately 5.2%.

In addition to financial assistance, Shands provides benefits for the broader community. The cost

of providing these community benefits can exceed the revenue sources available. Examples of the

benefits provided by Shands and general definitions regarding those benefits are described below:

Community health services include activities carried out to improve community health. They

extend beyond patient care activities and are usually subsidized by the health care

organization. Examples include community health education, counseling and support

services, and health care screenings.

Health professions education includes education provided in clinical settings such as

internships and programs for physicians, nurses, and allied health professionals. It also

includes scholarships for health professional education related to providing community health

improvement services and specialty in-service programs to professionals in the community.

Research includes studies on health care delivery, unreimbursed studies on therapeutic

protocols, evaluation of innovative treatments, and research papers prepared for professional

journals.

Donations include funds and in-kind services benefiting the community-at-large.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

24

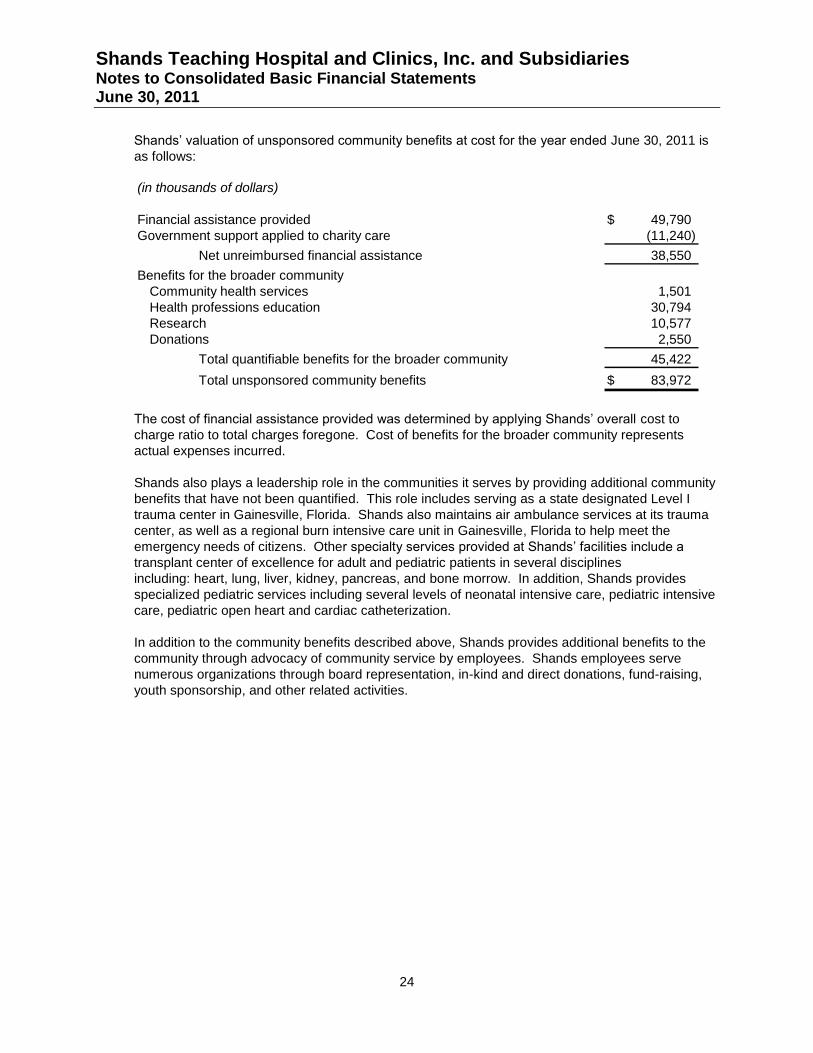

Shands’ valuation of unsponsored community benefits at cost for the year ended June 30, 2011 is

as follows:

(in thousands of dollars)

Financial assistance provided 49,790$

Government support applied to charity care (11,240)

Net unreimbursed financial assistance 38,550

Benefits for the broader community

Community health services 1,501

Health professions education 30,794

Research 10,577

Donations 2,550

Total quantifiable benefits for the broader community 45,422

Total unsponsored community benefits 83,972$

The cost of financial assistance provided was determined by applying Shands’ overall cost to

charge ratio to total charges foregone. Cost of benefits for the broader community represents

actual expenses incurred.

Shands also plays a leadership role in the communities it serves by providing additional community

benefits that have not been quantified. This role includes serving as a state designated Level I

trauma center in Gainesville, Florida. Shands also maintains air ambulance services at its trauma

center, as well as a regional burn intensive care unit in Gainesville, Florida to help meet the

emergency needs of citizens. Other specialty services provided at Shands’ facilities include a

transplant center of excellence for adult and pediatric patients in several disciplines

including: heart, lung, liver, kidney, pancreas, and bone morrow. In addition, Shands provides

specialized pediatric services including several levels of neonatal intensive care, pediatric intensive

care, pediatric open heart and cardiac catheterization.

In addition to the community benefits described above, Shands provides additional benefits to the

community through advocacy of community service by employees. Shands employees serve

numerous organizations through board representation, in-kind and direct donations, fund-raising,

youth sponsorship, and other related activities.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

25

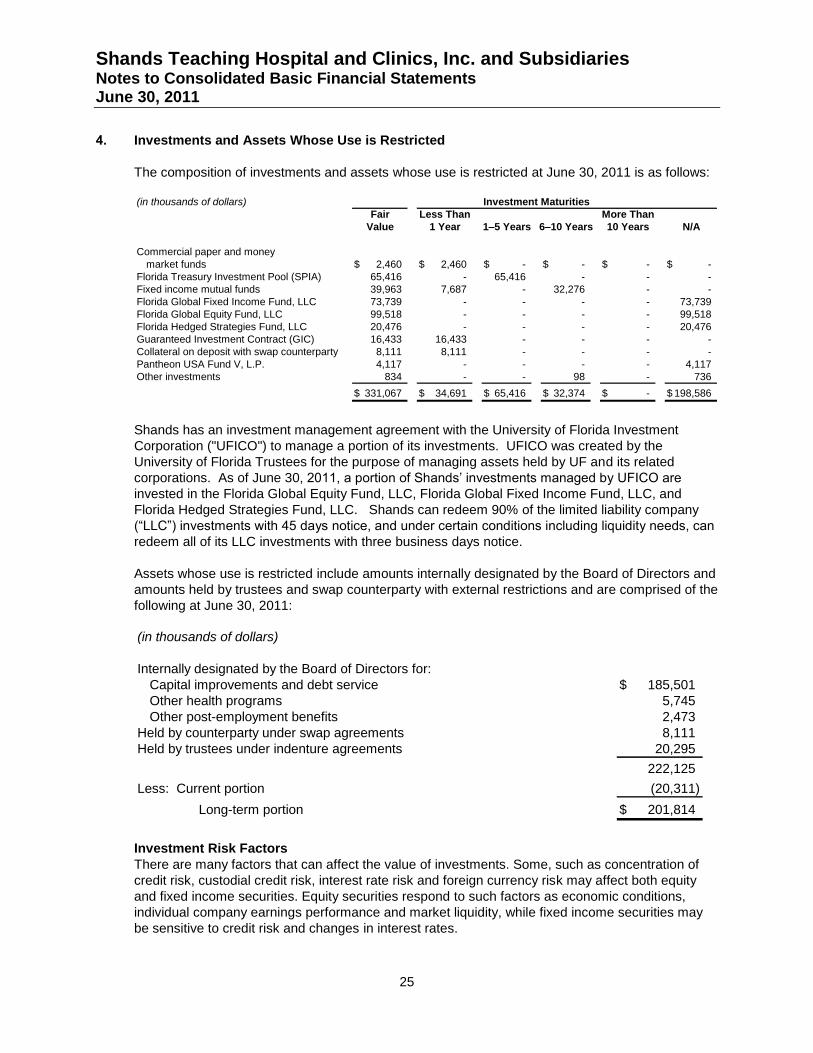

4. Investments and Assets Whose Use is Restricted

The composition of investments and assets whose use is restricted at June 30, 2011 is as follows:

(in thousands of dollars)

Fair Less Than More Than

Value 1 Year 1–5 Years 6–10 Years 10 Years N/A

Commercial paper and money

market funds 2,460$ 2,460$ -$ -$ -$ -$

Florida Treasury Investment Pool (SPIA) 65,416 - 65,416 - - -

Fixed income mutual funds 39,963 7,687 - 32,276 - -

Florida Global Fixed Income Fund, LLC 73,739 - - - - 73,739

Florida Global Equity Fund, LLC 99,518 - - - - 99,518

Florida Hedged Strategies Fund, LLC 20,476 - - - - 20,476

Guaranteed Investment Contract (GIC) 16,433 16,433 - - - -

Collateral on deposit with swap counterparty 8,111 8,111 - - - -

Pantheon USA Fund V, L.P. 4,117 - - - - 4,117

Other investments 834 - - 98 - 736

331,067$ 34,691$ 65,416$ 32,374$ -$ 198,586$

Investment Maturities

Shands has an investment management agreement with the University of Florida Investment

Corporation ("UFICO") to manage a portion of its investments. UFICO was created by the

University of Florida Trustees for the purpose of managing assets held by UF and its related

corporations. As of June 30, 2011, a portion of Shands’ investments managed by UFICO are

invested in the Florida Global Equity Fund, LLC, Florida Global Fixed Income Fund, LLC, and

Florida Hedged Strategies Fund, LLC. Shands can redeem 90% of the limited liability company

(“LLC”) investments with 45 days notice, and under certain conditions including liquidity needs, can

redeem all of its LLC investments with three business days notice.

Assets whose use is restricted include amounts internally designated by the Board of Directors and

amounts held by trustees and swap counterparty with external restrictions and are comprised of the

following at June 30, 2011:

(in thousands of dollars)

Internally designated by the Board of Directors for:

Capital improvements and debt service 185,501$

Other health programs 5,745

Other post-employment benefits 2,473

Held by counterparty under swap agreements 8,111

Held by trustees under indenture agreements 20,295

222,125

Less: Current portion (20,311)

Long-term portion 201,814$

Investment Risk Factors

There are many factors that can affect the value of investments. Some, such as concentration of

credit risk, custodial credit risk, interest rate risk and foreign currency risk may affect both equity

and fixed income securities. Equity securities respond to such factors as economic conditions,

individual company earnings performance and market liquidity, while fixed income securities may

be sensitive to credit risk and changes in interest rates.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

26

Credit Risk

This is the risk that an issuer or other counterparty to an investment will not fulfill its obligations.

Shands investment policy provides guidelines for its fund managers and lists specific allowable

investments. The policy provides for the utilization of varying styles of managers so that portfolio

diversification is maximized and total portfolio efficiency is enhanced.

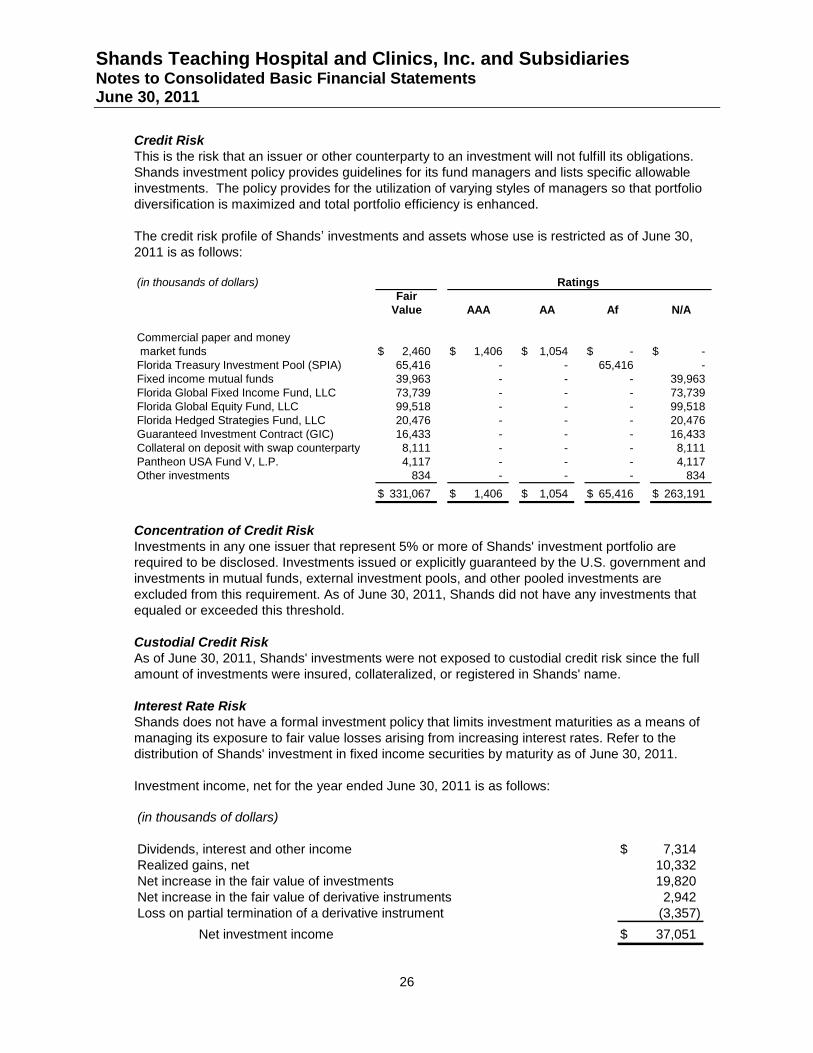

The credit risk profile of Shands’ investments and assets whose use is restricted as of June 30,

2011 is as follows:

(in thousands of dollars)

Fair

Value AAA AA Af N/A

Commercial paper and money

market funds 2,460$ 1,406$ 1,054$ -$ -$

Florida Treasury Investment Pool (SPIA) 65,416 - - 65,416 -

Fixed income mutual funds 39,963 - - - 39,963

Florida Global Fixed Income Fund, LLC 73,739 - - - 73,739

Florida Global Equity Fund, LLC 99,518 - - - 99,518

Florida Hedged Strategies Fund, LLC 20,476 - - - 20,476

Guaranteed Investment Contract (GIC) 16,433 - - - 16,433

Collateral on deposit with swap counterparty 8,111 - - - 8,111

Pantheon USA Fund V, L.P. 4,117 - - - 4,117

Other investments 834 - - - 834

331,067$ 1,406$ 1,054$ 65,416$ 263,191$

Ratings

Concentration of Credit Risk

Investments in any one issuer that represent 5% or more of Shands' investment portfolio are

required to be disclosed. Investments issued or explicitly guaranteed by the U.S. government and

investments in mutual funds, external investment pools, and other pooled investments are

excluded from this requirement. As of June 30, 2011, Shands did not have any investments that

equaled or exceeded this threshold.

Custodial Credit Risk

As of June 30, 2011, Shands' investments were not exposed to custodial credit risk since the full

amount of investments were insured, collateralized, or registered in Shands' name.

Interest Rate Risk

Shands does not have a formal investment policy that limits investment maturities as a means of

managing its exposure to fair value losses arising from increasing interest rates. Refer to the

distribution of Shands' investment in fixed income securities by maturity as of June 30, 2011.

Investment income, net for the year ended June 30, 2011 is as follows:

(in thousands of dollars)

Dividends, interest and other income 7,314$

Realized gains, net 10,332

Net increase in the fair value of investments 19,820

Net increase in the fair value of derivative instruments 2,942

Loss on partial termination of a derivative instrument (3,357)

Net investment income 37,051$

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

27

5. Capital Assets

A summary of changes in capital assets during fiscal year 2011 is as follows:

(in thousands of dollars) Balance at Disposals Balance at

June 30, and June 30,

2010 Additions Transfers 2011

Land 43,829$ 1,749$ -$ 45,578$

Buildings and leasehold improvements 760,663 4,588 (129) 765,122

Equipment 373,361 36,380 (12,892) 396,849

Totals at historical cost 1,177,853 42,717 (13,021) 1,207,549

Less: Accumulated depreciation for

Buildings and leasehold improvements (206,011) (22,748) 108 (228,651)

Equipment (257,203) (29,200) 11,788 (274,615)

(463,214) (51,948) 11,896 (503,266)

Construction-in-progress 9,849 27,211 (8,875) 28,185

Capital assets, net 724,488$ 17,980$ (10,000)$ 732,468$

Depreciation and amortization expense was approximately $51,948,000 for the year ended

June 30, 2011. Amortization expense on equipment held under capital lease which is included

within depreciation and amortization in the accompanying consolidated basic statement of

revenues, expenses and changes in net assets was approximately $877,000 for the year ended

June 30, 2011. Interest costs capitalized were approximately $638,000 for the year ended June 30,

2011. Construction-in-progress at June 30, 2011 mainly related to costs incurred for a new

electronic medical records system. Shands has contracts for the construction and remodeling of

facilities and equipment purchases. Estimated costs to complete the installation of the projects

was approximately $51,167,000 at June 30, 2011.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

28

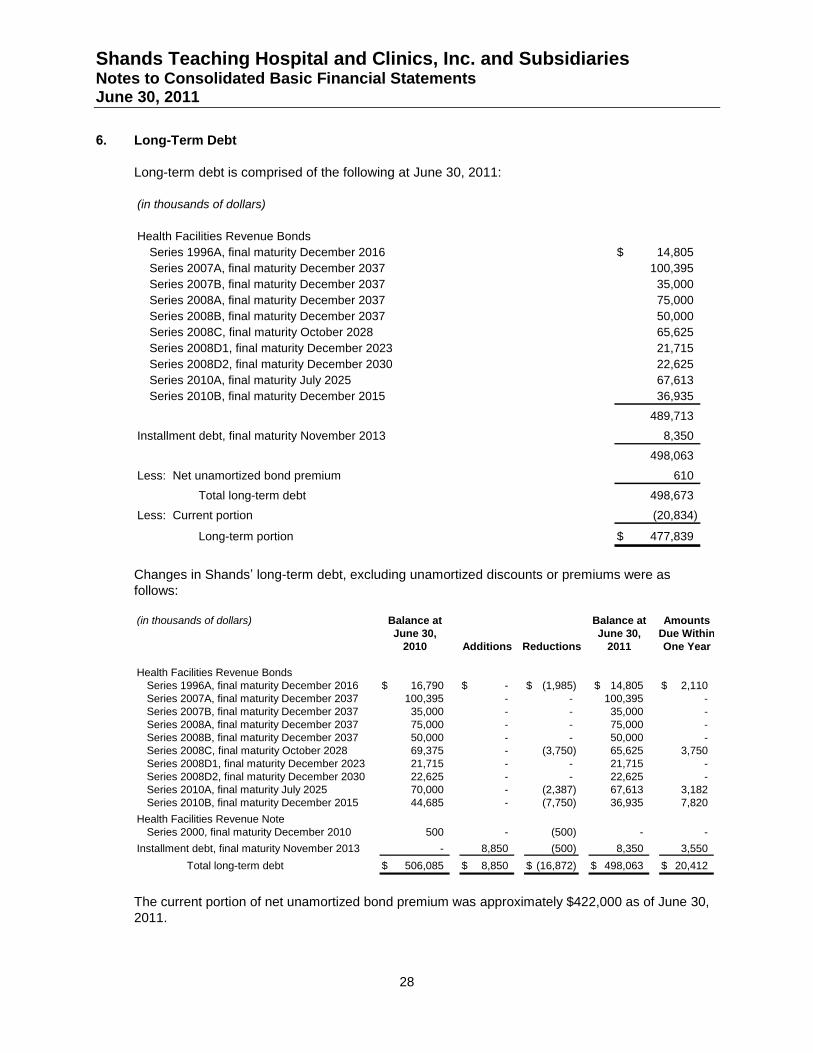

6. Long-Term Debt

Long-term debt is comprised of the following at June 30, 2011:

(in thousands of dollars)

Health Facilities Revenue Bonds

Series 1996A, final maturity December 2016 14,805$

Series 2007A, final maturity December 2037 100,395

Series 2007B, final maturity December 2037 35,000

Series 2008A, final maturity December 2037 75,000

Series 2008B, final maturity December 2037 50,000

Series 2008C, final maturity October 2028 65,625

Series 2008D1, final maturity December 2023 21,715

Series 2008D2, final maturity December 2030 22,625

Series 2010A, final maturity July 2025 67,613

Series 2010B, final maturity December 2015 36,935

489,713

Installment debt, final maturity November 2013 8,350

498,063

Less: Net unamortized bond premium 610

Total long-term debt 498,673

Less: Current portion (20,834)

Long-term portion 477,839$

Changes in Shands’ long-term debt, excluding unamortized discounts or premiums were as

follows:

(in thousands of dollars) Balance at Balance at Amounts

June 30, June 30, Due Within

2010 Additions Reductions 2011 One Year

Health Facilities Revenue Bonds

Series 1996A, final maturity December 2016 16,790$ -$ (1,985)$ 14,805$ 2,110$

Series 2007A, final maturity December 2037 100,395 - - 100,395 -

Series 2007B, final maturity December 2037 35,000 - - 35,000 -

Series 2008A, final maturity December 2037 75,000 - - 75,000 -

Series 2008B, final maturity December 2037 50,000 - - 50,000 -

Series 2008C, final maturity October 2028 69,375 - (3,750) 65,625 3,750

Series 2008D1, final maturity December 2023 21,715 - - 21,715 -

Series 2008D2, final maturity December 2030 22,625 - - 22,625 -

Series 2010A, final maturity July 2025 70,000 - (2,387) 67,613 3,182

Series 2010B, final maturity December 2015 44,685 - (7,750) 36,935 7,820

Health Facilities Revenue Note

Series 2000, final maturity December 2010 500 - (500) - -

Installment debt, final maturity November 2013 - 8,850 (500) 8,350 3,550

Total long-term debt 506,085$ 8,850$ (16,872)$ 498,063$ 20,412$

The current portion of net unamortized bond premium was approximately $422,000 as of June 30,

2011.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

29

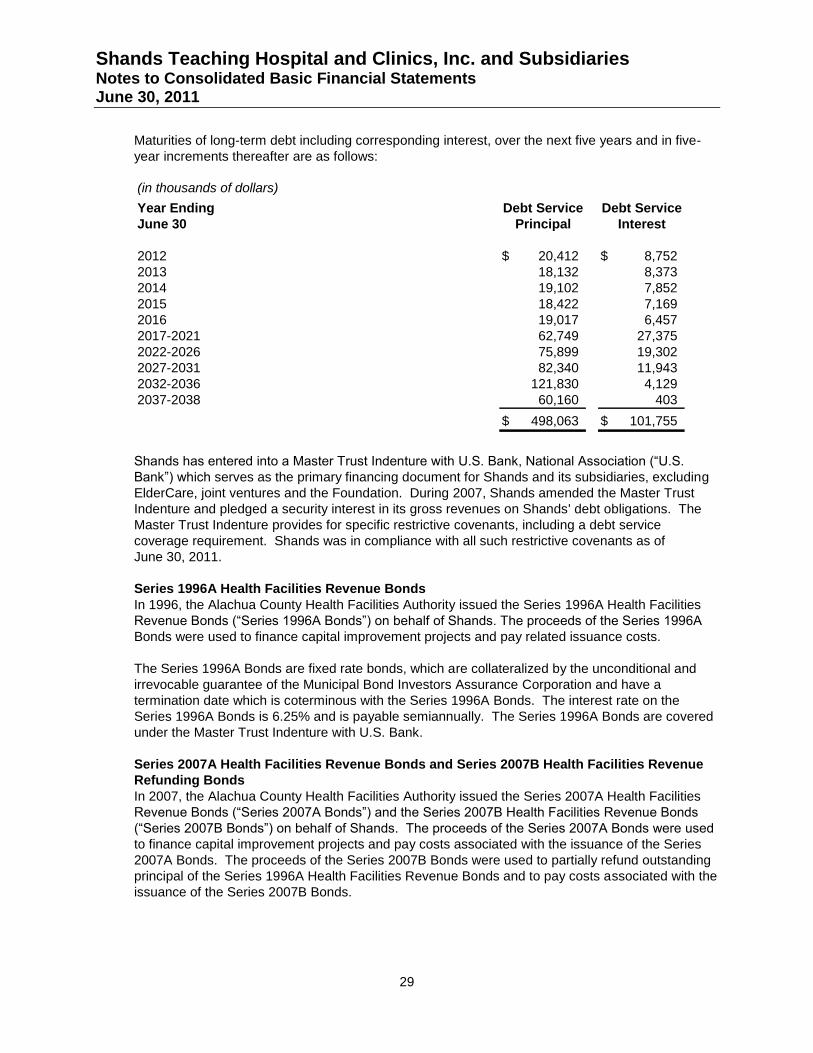

Maturities of long-term debt including corresponding interest, over the next five years and in five-

year increments thereafter are as follows:

(in thousands of dollars)

Year Ending Debt Service Debt Service

June 30 Principal Interest

2012 20,412$ 8,752$

2013 18,132 8,373

2014 19,102 7,852

2015 18,422 7,169

2016 19,017 6,457

2017-2021 62,749 27,375

2022-2026 75,899 19,302

2027-2031 82,340 11,943

2032-2036 121,830 4,129

2037-2038 60,160 403

498,063$ 101,755$

Shands has entered into a Master Trust Indenture with U.S. Bank, National Association (“U.S.

Bank”) which serves as the primary financing document for Shands and its subsidiaries, excluding

ElderCare, joint ventures and the Foundation. During 2007, Shands amended the Master Trust

Indenture and pledged a security interest in its gross revenues on Shands' debt obligations. The

Master Trust Indenture provides for specific restrictive covenants, including a debt service

coverage requirement. Shands was in compliance with all such restrictive covenants as of

June 30, 2011.

Series 1996A Health Facilities Revenue Bonds

In 1996, the Alachua County Health Facilities Authority issued the Series 1996A Health Facilities

Revenue Bonds (“Series 1996A Bonds”) on behalf of Shands. The proceeds of the Series 1996A

Bonds were used to finance capital improvement projects and pay related issuance costs.

The Series 1996A Bonds are fixed rate bonds, which are collateralized by the unconditional and

irrevocable guarantee of the Municipal Bond Investors Assurance Corporation and have a

termination date which is coterminous with the Series 1996A Bonds. The interest rate on the

Series 1996A Bonds is 6.25% and is payable semiannually. The Series 1996A Bonds are covered

under the Master Trust Indenture with U.S. Bank.

Series 2007A Health Facilities Revenue Bonds and Series 2007B Health Facilities Revenue

Refunding Bonds

In 2007, the Alachua County Health Facilities Authority issued the Series 2007A Health Facilities

Revenue Bonds (“Series 2007A Bonds”) and the Series 2007B Health Facilities Revenue Bonds

(“Series 2007B Bonds”) on behalf of Shands. The proceeds of the Series 2007A Bonds were used

to finance capital improvement projects and pay costs associated with the issuance of the Series

2007A Bonds. The proceeds of the Series 2007B Bonds were used to partially refund outstanding

principal of the Series 1996A Health Facilities Revenue Bonds and to pay costs associated with the

issuance of the Series 2007B Bonds.

Shands Teaching Hospital and Clinics, Inc. and Subsidiaries Notes to Consolidated Basic Financial Statements June 30, 2011

30

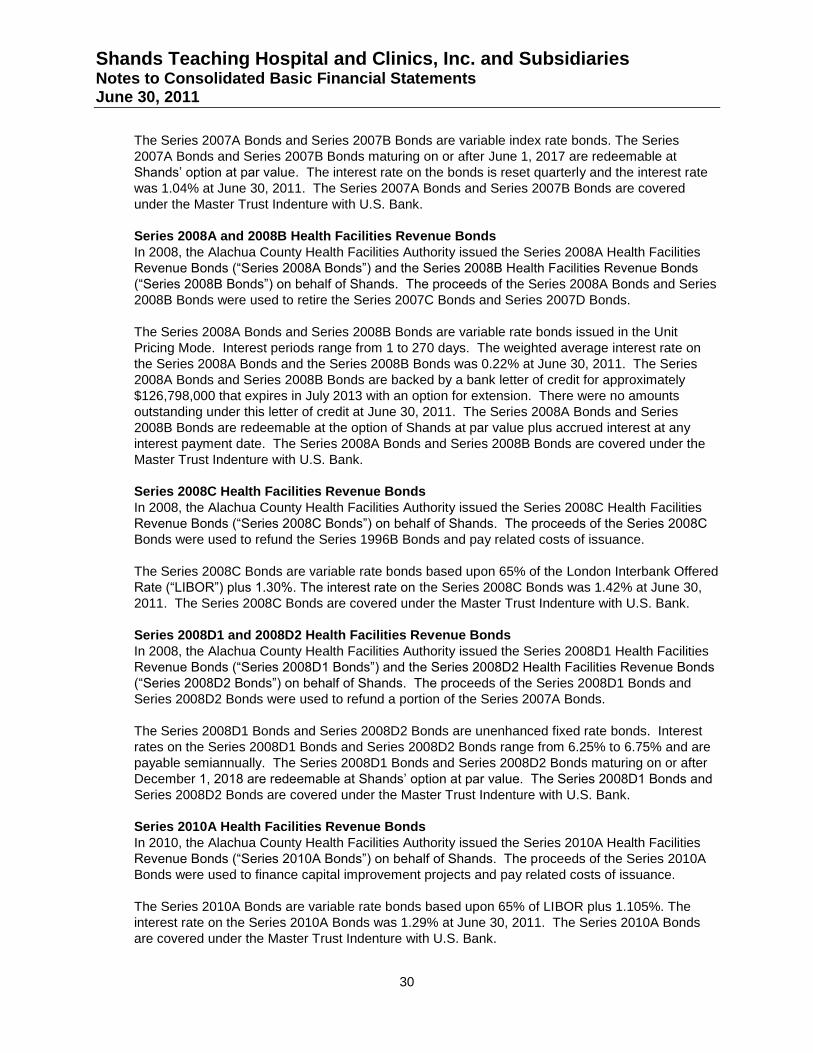

The Series 2007A Bonds and Series 2007B Bonds are variable index rate bonds. The Series

2007A Bonds and Series 2007B Bonds maturing on or after June 1, 2017 are redeemable at

Shands’ option at par value. The interest rate on the bonds is reset quarterly and the interest rate

was 1.04% at June 30, 2011. The Series 2007A Bonds and Series 2007B Bonds are covered

under the Master Trust Indenture with U.S. Bank.

Series 2008A and 2008B Health Facilities Revenue Bonds

In 2008, the Alachua County Health Facilities Authority issued the Series 2008A Health Facilities

Revenue Bonds (“Series 2008A Bonds”) and the Series 2008B Health Facilities Revenue Bonds

(“Series 2008B Bonds”) on behalf of Shands. The proceeds of the Series 2008A Bonds and Series