Self Driving Vehicles and Transport Forecasting Futura October13

29

FORECASTING THE IMPACT OF SELF-DRIVING-CARS What to do about them in our models and forecasts

-

Upload

luis-willumsen -

Category

Business

-

view

290 -

download

0

Transcript of Self Driving Vehicles and Transport Forecasting Futura October13

FORECASTING THE IMPACT OF SELF-DRIVING-CARSWhat to do about them in our models and forecasts

MO

TIVATION

Motivation

Cars have been cars for quite a long time We know how to model assignment, capacities, traffic

management Mode choice between car and other modes is reasonably

well known Public Transport policies are known (and stable)

It became clear during 2013 that we will be facing a new disruptive technology in the Self Driving Car or Autonomous Vehicles

THE D

ESIGN

OF CARS

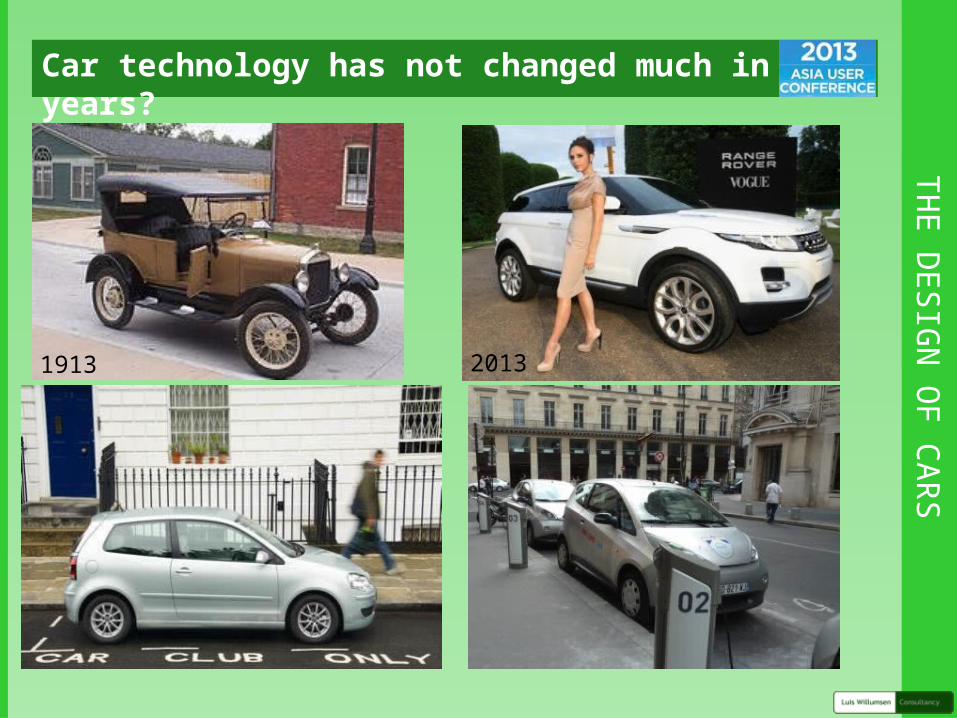

Car technology has not changed much in 100 years?

1913 2013

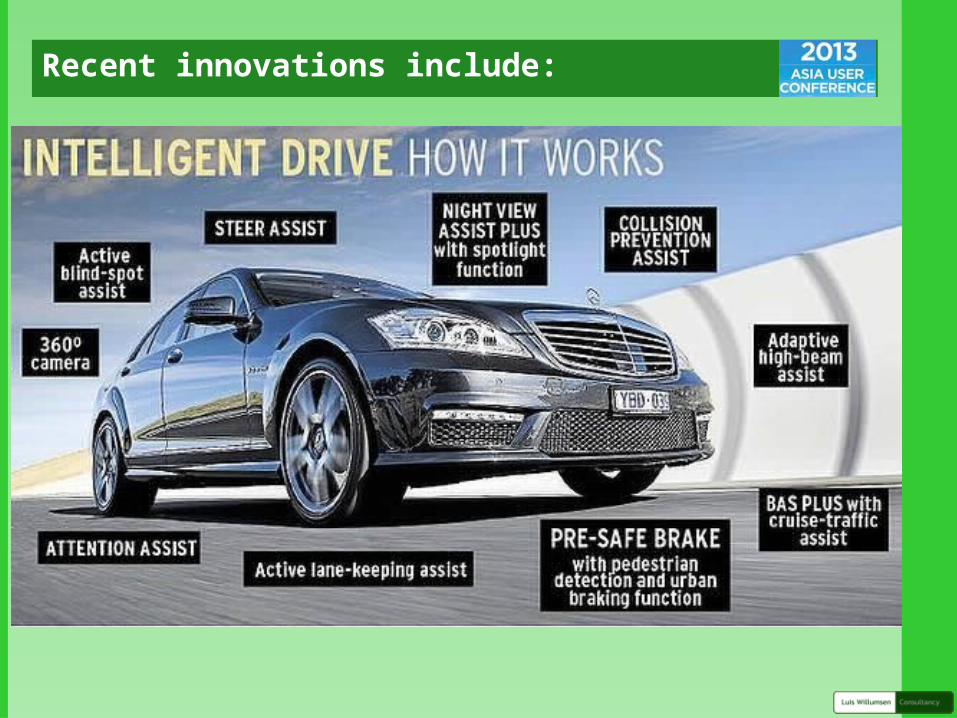

Recent innovations include:

DREAM

ING

ABOU

T THE FU

TURE

The unrealised dream

Origins

Autonomous vehicles have been a dream solution for some time

Japan (starting in 1977), Germany (Ernst Dickmanns and VaMP), Italy (the ARGO Project), European Union (EUREKA Prometheus Project), In the United States of America the main driver was military

The Defense Advanced Research Projects Agency (DARPA) launched in 2004 a challenge to complete a 150 mile off-road route: $ 1 and then $2 million

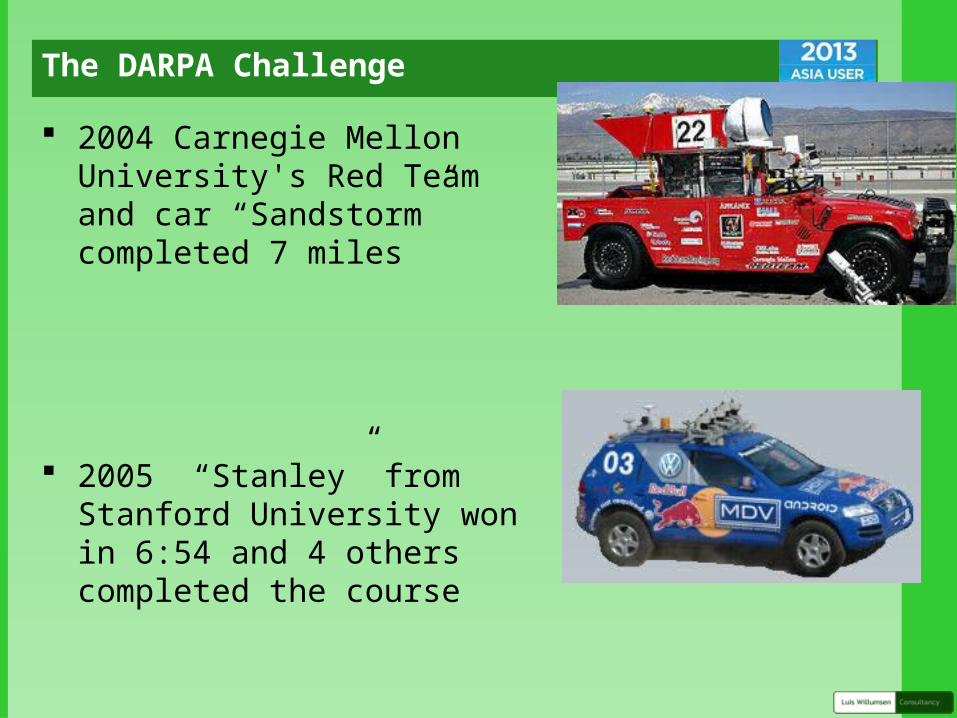

The DARPA Challenge

2004 Carnegie Mellon University's Red Team and car “Sandstorm” completed 7 miles

2005 “Stanley” from Stanford University won in 6:54 and 4 others completed the course

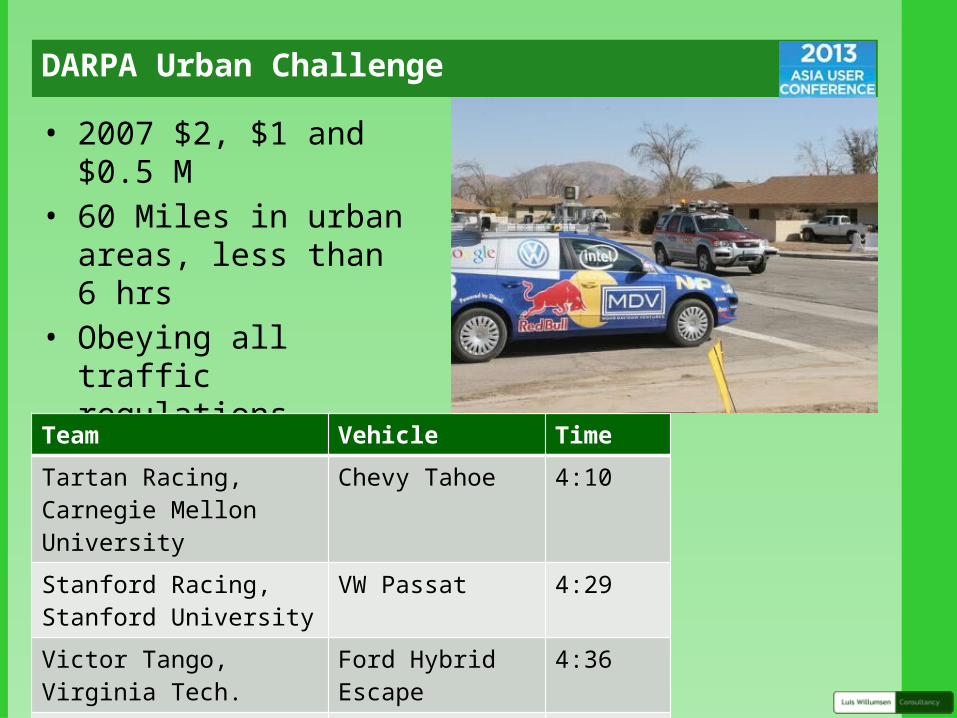

DARPA Urban Challenge

• 2007 $2, $1 and $0.5 M• 60 Miles in urban areas,

less than 6 hrs• Obeying all traffic

regulations

Team Vehicle Time

Tartan Racing, Carnegie Mellon University

Chevy Tahoe 4:10

Stanford Racing, Stanford University

VW Passat 4:29

Victor Tango, Virginia Tech. Ford Hybrid Escape 4:36

7 other teams finished the course

6 hours +

U.S. National Highway Traffic Safety Administration (NHTSA)

Defined Vehicle Automation levelsLevel 1 – Function-specific Automation: e.g. cruise control, lane guidance and automated parallel parking. Level 2 - Combined Function Automation: e.g. adaptive cruise control with lane centering. Drivers are responsible for monitoring the roadway. Level 3 - Limited Self-Driving Automation: Drivers can cede all safety-critical functions under certain conditions and rely on the vehicle to monitor for changes in those conditions that will require transition back to driver control. Level 4 - Full Self-Driving Automation: Vehicles can perform all driving functions and monitor roadway conditions for an entire trip, and so may operate with occupants who cannot drive and without human occupants.

GO

OG

LEAutonomous, self-driving-vehicles are coming!

360 VISION

360° vision and perception

ADVANTAG

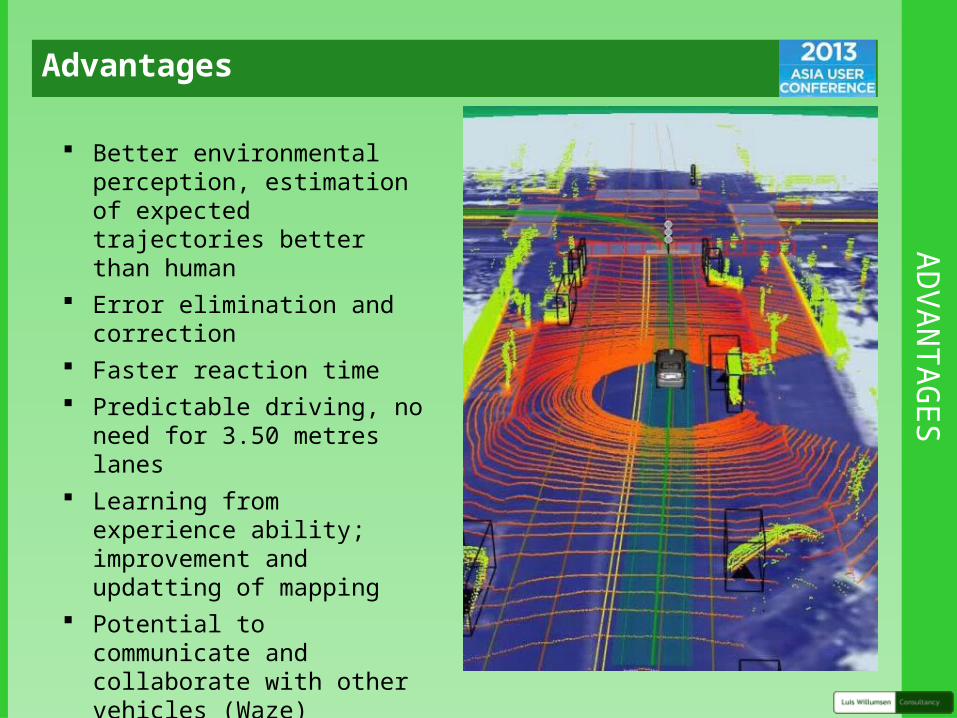

ESAdvantages

Better environmental perception, estimation of expected trajectories better than human

Error elimination and correction Faster reaction time Predictable driving, no need for

3.50 metres lanes Learning from experience ability;

improvement and updatting of mapping

Potential to communicate and collaborate with other vehicles (Waze)

No need to own it Civil responsibilty, insurance Changes in legislation

BMW

There are many initiatives under way e.g. BMW

AUD

I VOLKSW

AGEN

Audi

PLATOO

NS

Volvo

OTH

ERSGeneral Motors – Renault – Nissan-Oxford University

IMPACTS

Possible Impacts (with SDVs as 90% of the fleet)

95% reduction in traffic accidents Road capacities are doubled (without any investment in

them) All speeds and manoeuvres are legal Travel time available for other uses SDVs rented by the minute rather than owned, thus

Smaller fleet Use the right vehicle for each journey Parking problems eliminated

Fewer emissions and lower energy consumption per trip Better driving patterns More one way trips (no escort trips)

But some trip induction: more vehicle-miles

CON

GESTIO

N EFFECTS

Impact on roads

Highway Capacity Benefits from Using Vehicle-to-Vehicle Communication and Sensors for Collision Avoidance, by Patcharinee Tientrakool, Ya-Chi Ho, and Nicholas F. Maxemchuk from Columbia University

CON

GESTIO

N EFFECTS

Impact on roads

Highway Capacity Benefits from Using Vehicle-to-Vehicle Communication and Sensors for Collision Avoidance, by Patcharinee Tientrakool, Ya-Chi Ho, and Nicholas F. Maxemchuk from Columbia University

2018? 2020? 2025?How soon?

• When available at the showrooms?• How expensive?• Would we buy or rent them, or prefer to drive ourselves?

• When are we going to feel the impact on our roads?• How will they affect our Transport Plans?• Public Transport Modes?• Toll Roads?• Policies?

Timeline according to General Motors & Google

• 2014 some self-parking cars. Automatic emergency stops in several contexts. LEVEL 2

• 2015, cars change lanes as requested by driver. Stop automatically at STOP signs and red lights.

• 2016 cars merge and leave motorways automatically. Emergency stop in all cases. LEVEL 3

• 2018 Autonomous vehicles completing journeys without human driving, including unpaved roads. LEVEL 4

• Most observes agree Level 4 will be available commercially 2018-2020.

NAVIG

ANT RESEARCH

Recent Research Report on SDVs Navigant Research

Level 4 commercially available by 2020

SDVs will be 4% of fleet by 2025

Compound Annual Growth Rate 2025-2030 for main markets:

North America, Western Europe and Asia Pacific = 85%

Market penetration 41% in 2030 and 75% in 2035

NAVIG

ANT RESEARCH

Recent Research Report on SDVs Navigant Research

UN

IVERSITY OF TEXAS AT AU

STINENO Center for Transportation

Fagnant, D. and Kockelman, K. (2013) Preparing the Nation for Autonomous Vehicles; Opportunities, Barriers and Policy Recommendations.

https://www.enotrans.org/store/research-papers/preparing-a-nation-for-autonomous-vehicles-opportunities-barriers-and-policy-recommendations

UN

IVERSITY OF TEXAS AT AU

STINENO Center Report

Accepts estimate of incremental costs reducing from $10,000 to $3,000 in a few years

Very significant savings in accidents and their cost Reduced congestion: doubling capacity at 90% penetration Expect vehicle sharing, car clubs, short term rentals: each SDV

to replace 4-5 cars Induced traffic will increase Vehicle Miles Travelled up to 37%

off-setting fuel/emission savings off-peak Benefits also to non-SDVs (smoothing traffic, following SDV)

CBA for US market 10% 50% 90%

Additional cost for SDVs $ 10,000 $ 5,000 $ 3,000

Net discounted annual benefits $ per SDV $12,590 $ 23,070 $ 33,200

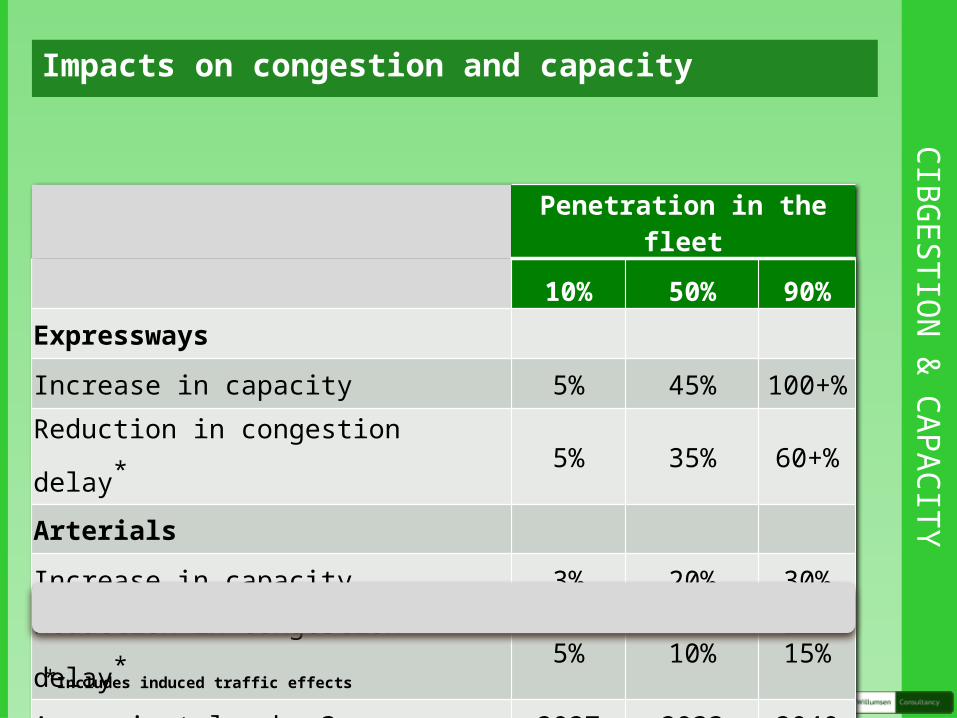

CIBGESTIO

N &

CAPACITYImpacts on congestion and capacity

Penetration in the fleet

10% 50% 90%Expressways

Increase in capacity 5% 45% 100+%

Reduction in congestion delay* 5% 35% 60+%

Arterials

Increase in capacity 3% 20% 30%

Reduction in congestion delay* 5% 10% 15%

Approximately when? 2027 2033 2040

*Includes induced traffic effects

LIKE THEM

?Apparently we are happy to use them: CISCO

Discussion topic: how do we incorporate SDV in our forecasts?

We can no longer ignore them if planning horizon is 10+ years

At least a source of uncertainty and part of Risk Analysis Assumptions about freeway capacity enhancements

10% a 2025? 50% a 2033? 100% a 2040?

Impact on Public Transport services and subsidies; which buses will survive? Would they become driver-less?

Sell any shares in Taxi and Limousine companies and consider divesting in rural and low frequency bus

Thanks … let’s discuss what we think we should do in our forecasts