Second Quarter 2004 Results En

15

Slide 1 2Q04 Results 2Q04 Results July 22, 2004

description

Transcript of Second Quarter 2004 Results En

Slide 1

2Q04 Results2Q04 Results

July 22, 2004

Slide 2

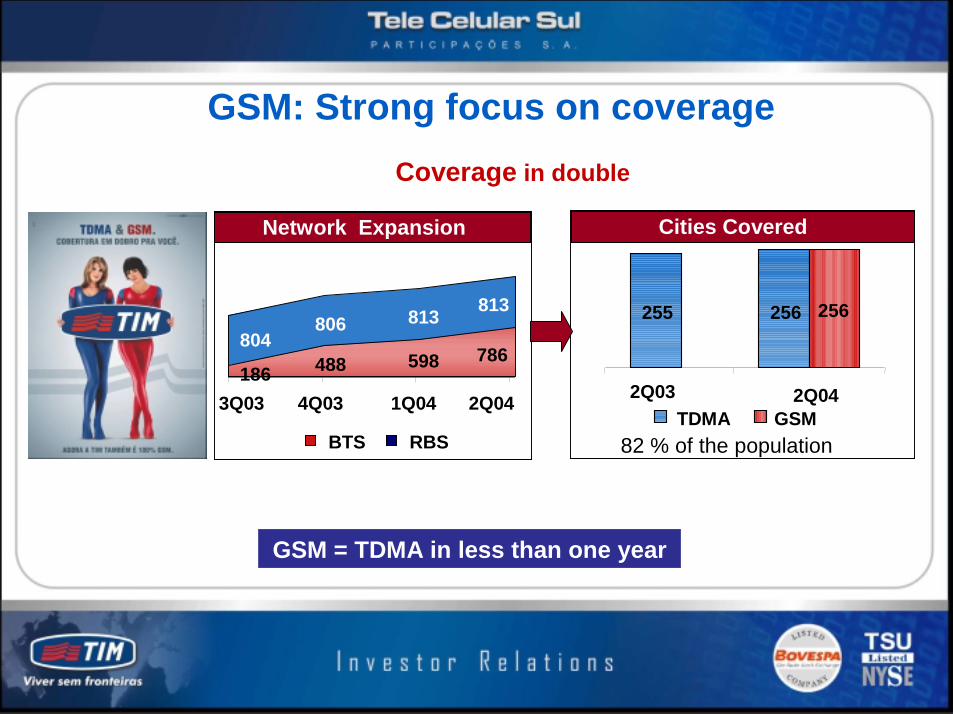

GSM: Strong focus on coverage

488 598

806 813

786186

813

804

3Q03 4Q03 1Q04 2Q04

BTS RBS

255 256 256

2Q03TDMA

2Q04GSM

Cities CoveredNetwork Expansion

82 % of the population

GSM = TDMA in less than one year

Coverage in double

Slide 3

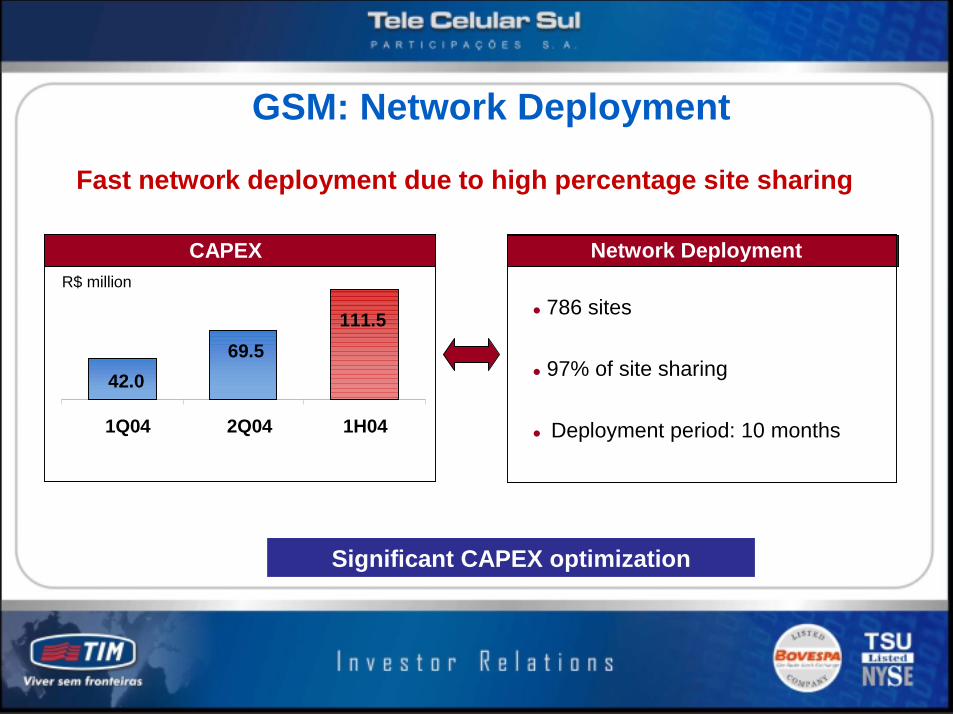

GSM: Network Deployment

CAPEX

Significant CAPEX optimization

42.0

111.569.5

1Q04 2Q04 1H04

Network Deployment

Fast network deployment due to high percentage site sharing

R$ million

� 786 sites

� 97% of site sharing

� Deployment period: 10 months

Slide 4

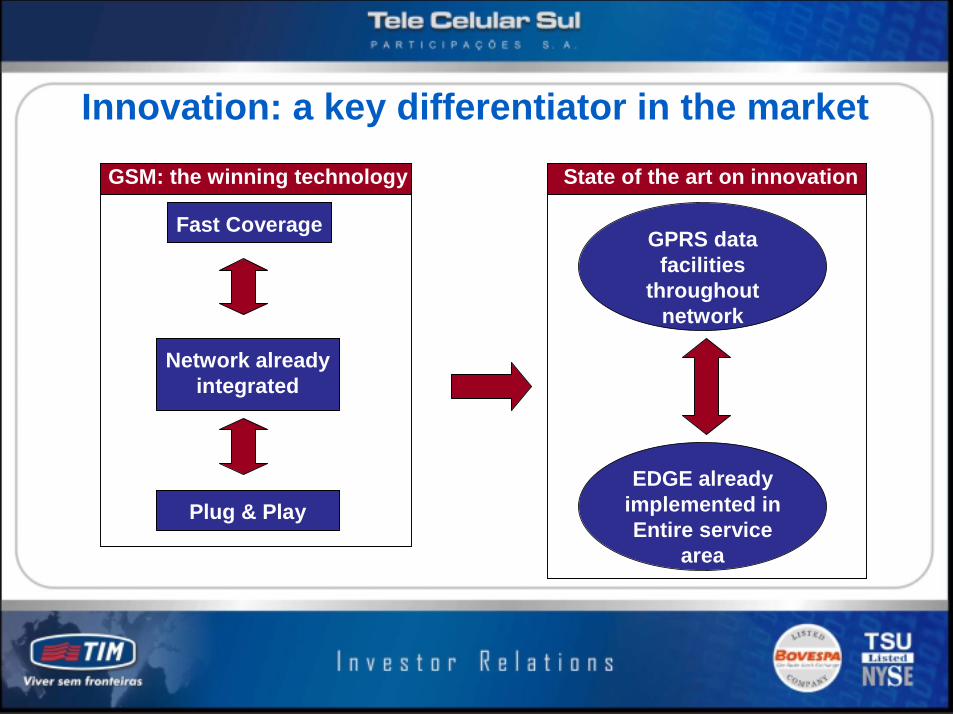

Innovation: a key differentiator in the market

GPRS data facilities

throughout network

EDGE already implemented inEntire service

area

Fast Coverage

Network alreadyintegrated

State of the art on innovationGSM: the winning technology

Fast Coverage

Plug & Play

Slide 5

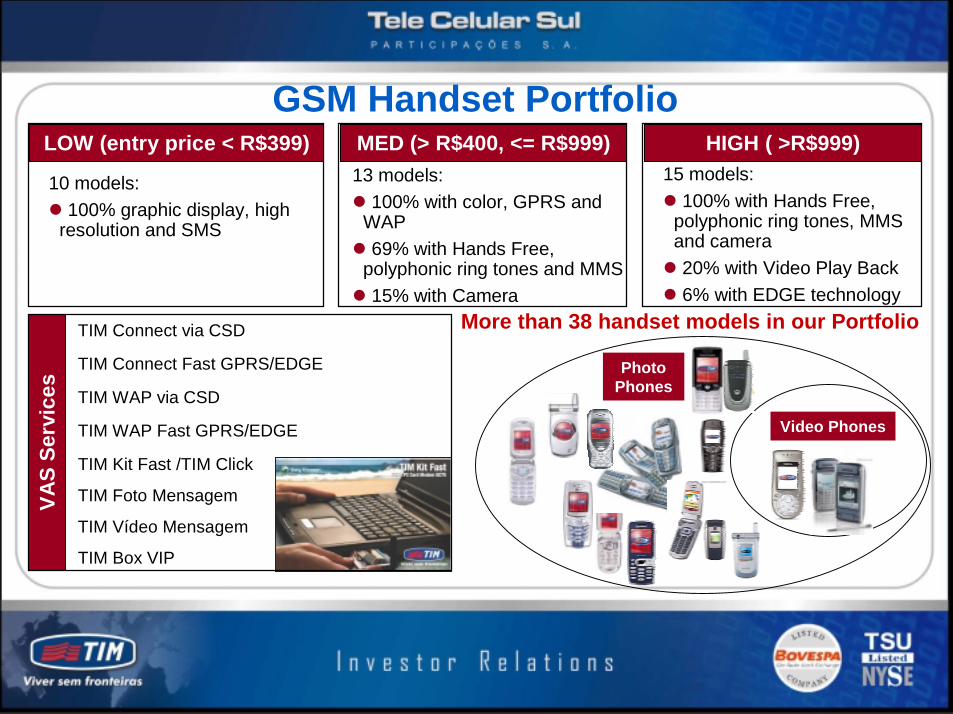

13 models: � 100% with color, GPRS and

WAP� 69% with Hands Free,

polyphonic ring tones and MMS� 15% with Camera

15 models: � 100% with Hands Free,

polyphonic ring tones, MMS and camera

� 20% with Video Play Back� 6% with EDGE technology

GSM Handset Portfolio

More than 38 handset models in our Portfolio

Photo Phones

LOW (entry price < R$399)

10 models: � 100% graphic display, high

resolution and SMS

MED (> R$400, <= R$999) HIGH ( >R$999)

Video Phones

TIM Connect via CSD

TIM Connect Fast GPRS/EDGE

TIM WAP via CSD

TIM WAP Fast GPRS/EDGE

TIM Kit Fast /TIM Click

TIM Foto Mensagem

TIM Vídeo Mensagem

TIM Box VIP

VAS

Serv

ices

Slide 6

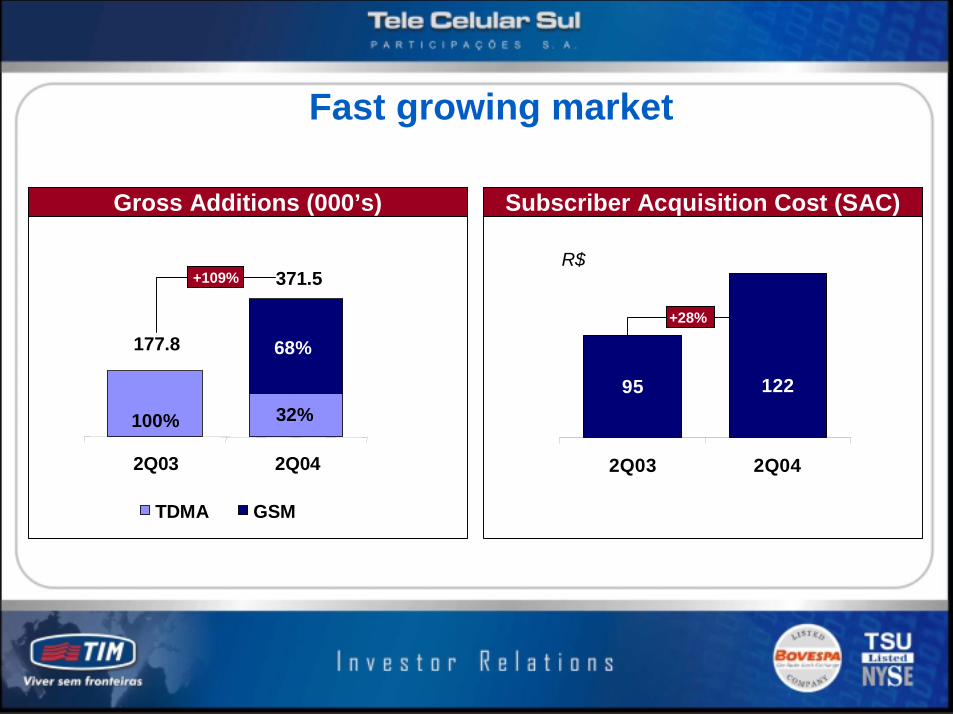

+28%

95 122

2Q03 2Q04

Fast growing market

R$

68%

100% 32%

2Q03 2Q04

TDMA GSM

Gross Additions (000’s) Subscriber Acquisition Cost (SAC)

177.8

371.5+109%

Slide 7

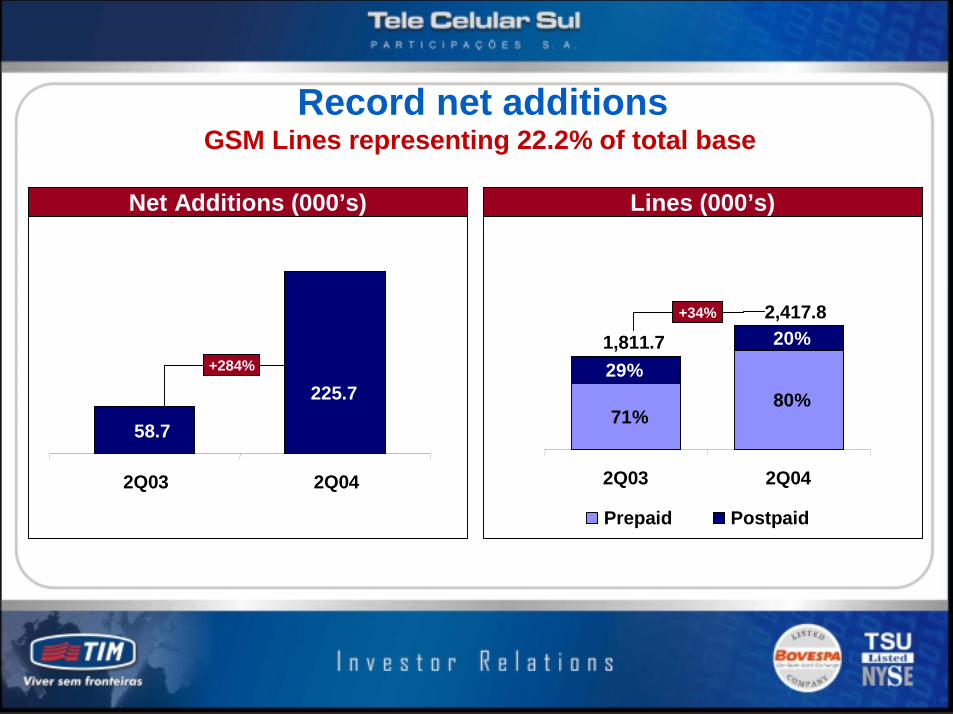

+284%

225.7

58.7

2Q03 2Q04

Record net additions

Net Additions (000’s) Lines (000’s)

71%80%

29%20%

2Q03 2Q04

Prepaid Postpaid

1,811.72,417.8+34%

GSM Lines representing 22.2% of total base

Slide 8

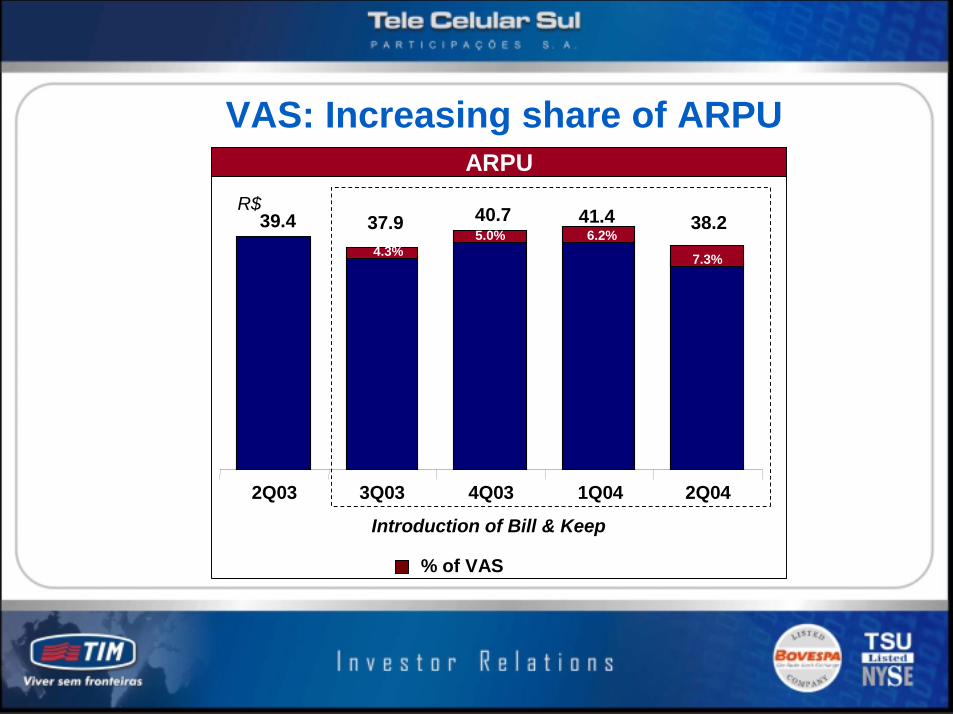

2Q03 3Q03 4Q03 1Q04 2Q04

VAS: Increasing share of ARPU

R$ 40.7 41.4 38.239.4 37.9

ARPU

% of VAS

Introduction of Bill & Keep

7.3%

6.2%5.0%4.3%

Slide 9

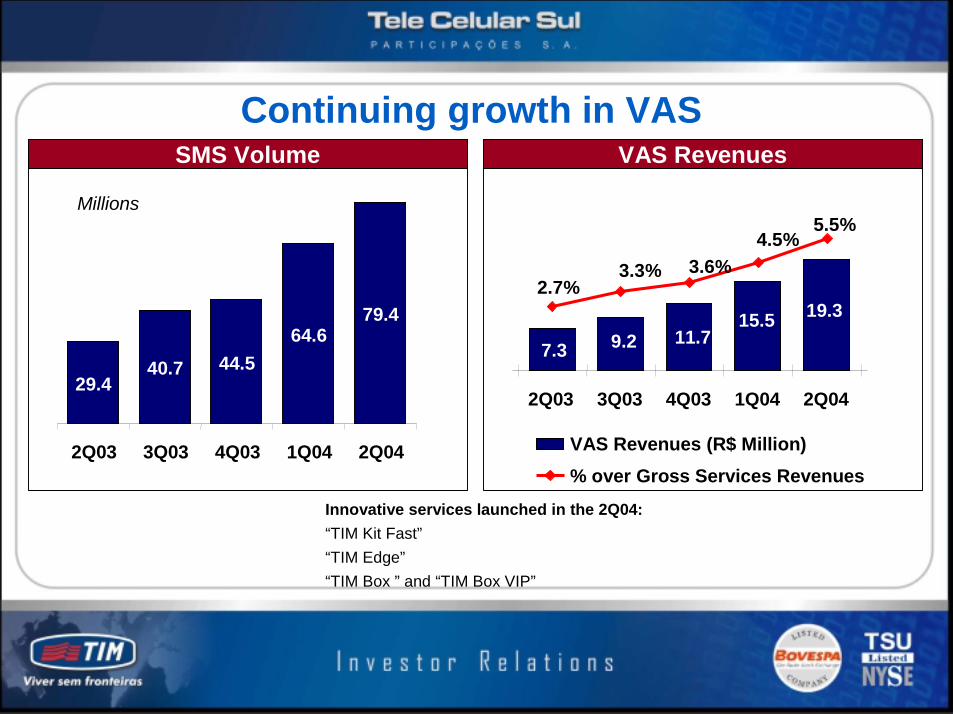

Continuing growth in VASSMS Volume VAS Revenues

29.440.7 44.5

64.679.4

2Q03 3Q03 4Q03 1Q04 2Q04

19.315.511.79.27.3

5.5%4.5%

3.6%3.3%2.7%

2Q03 3Q03 4Q03 1Q04 2Q04

VAS Revenues (R$ Million)% over Gross Services Revenues

Innovative services launched in the 2Q04:“TIM Kit Fast”“TIM Edge”“TIM Box ” and “TIM Box VIP”

Millions

Slide 10

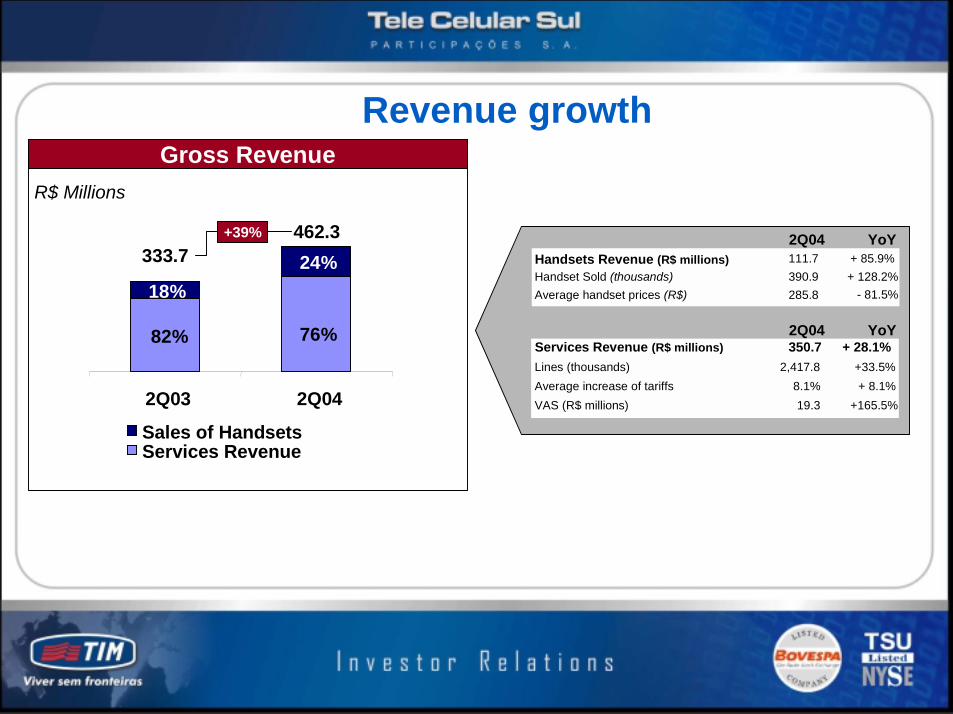

Revenue growth

R$ Millions

2Q04 YoY

Handset Sold (thousands) 390.9 + 128.2%Average handset prices (R$) 285.8

2Q04 YoY

Lines (thousands) 2,417.8 +33.5%Average increase of tariffs 8.1% + 8.1%VAS (R$ millions) 19.3 +165.5%

- 81.5%

Handsets Revenue (R$ millions) 111.7 + 85.9%

Services Revenue (R$ millions) 350.7 + 28.1%

Gross Revenue

82%

24%18%

76%

2Q03 2Q04

Sales of HandsetsServices Revenue

462.3333.7

+39%

Slide 11

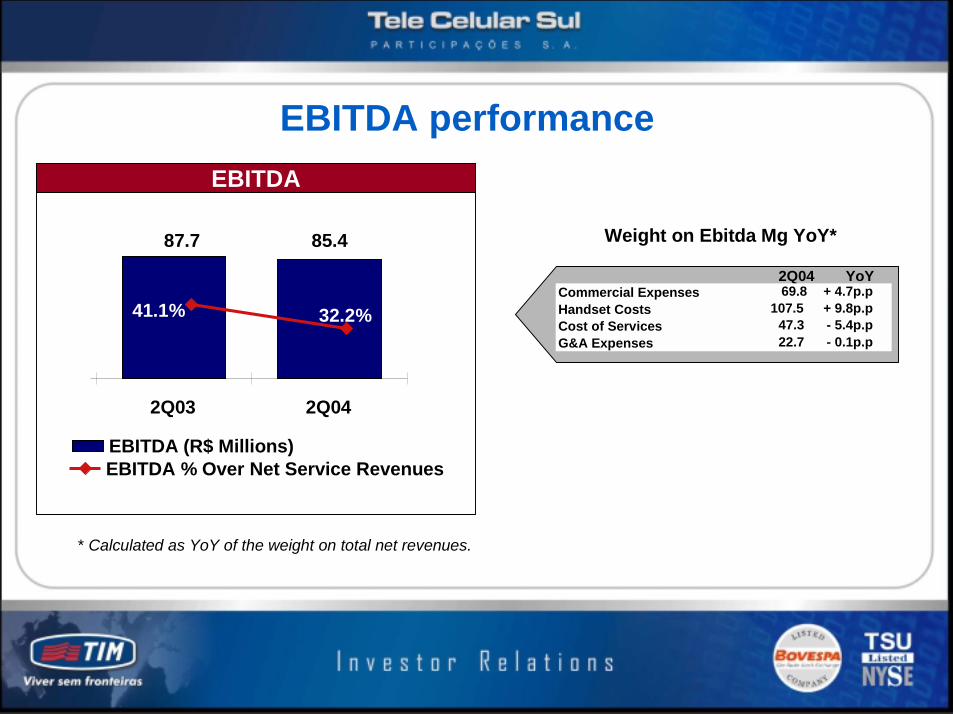

EBITDA performance

Weight on Ebitda Mg YoY*

* Calculated as YoY of the weight on total net revenues.

2Q04 YoYCommercial ExpensesHandset CostsCost of ServicesG&A Expenses

69.8 + 4.7p.p107.5 + 9.8p.p

47.3 - 5.4p.p22.7 - 0.1p.p

EBITDA

87.7 85.4

41.1% 32.2%

2Q03 2Q04

EBITDA (R$ Millions)EBITDA % Over Net Service Revenues

Slide 12

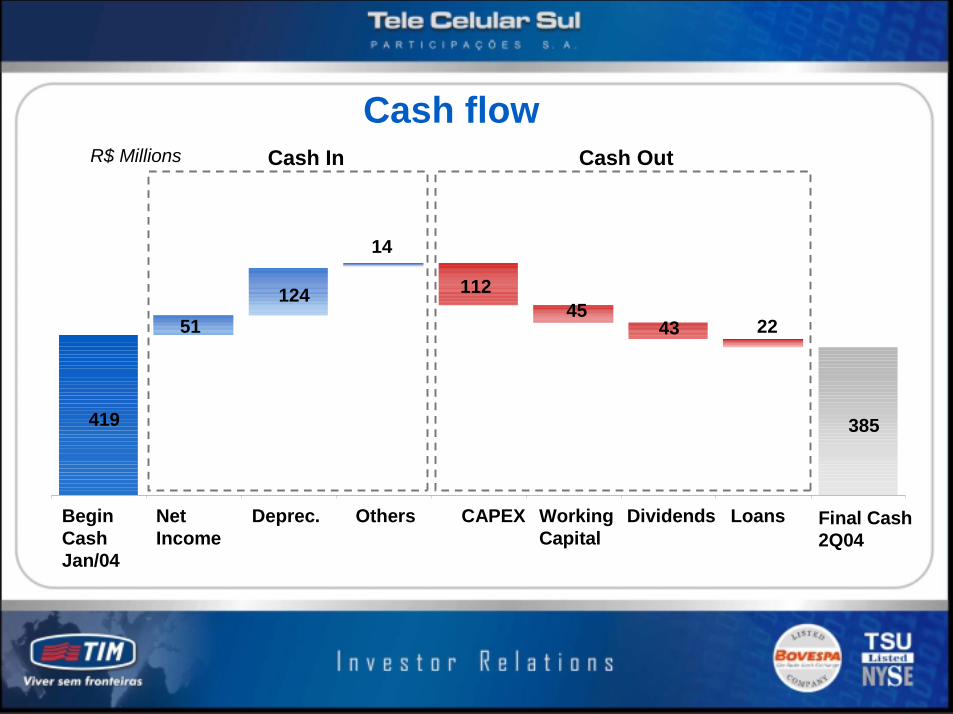

Cash flowR$ Millions Cash In Cash Out

385

112

419

51124

14

224345

Begin CashJan/04

Net Income

Deprec. Others CAPEX WorkingCapital

Dividends Loans Final Cash2Q04

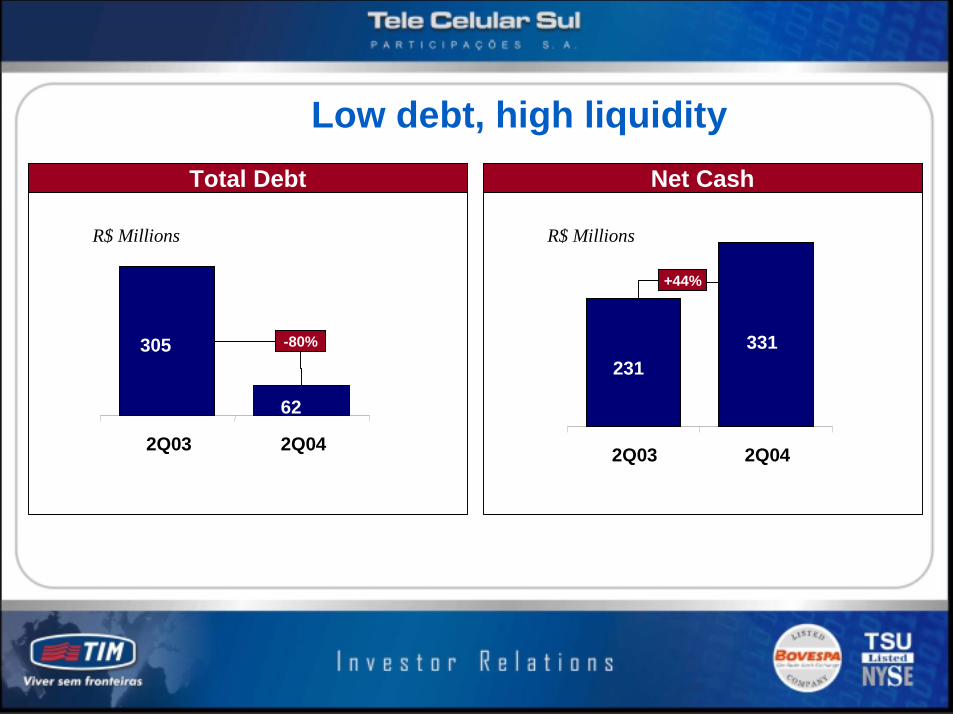

Slide 13

Low debt, high liquidity

R$ Millions R$ Millions

62

305

2Q03 2Q04

Total Debt

-80%

Net Cash

+44%

231331

2Q03 2Q04

Slide 14

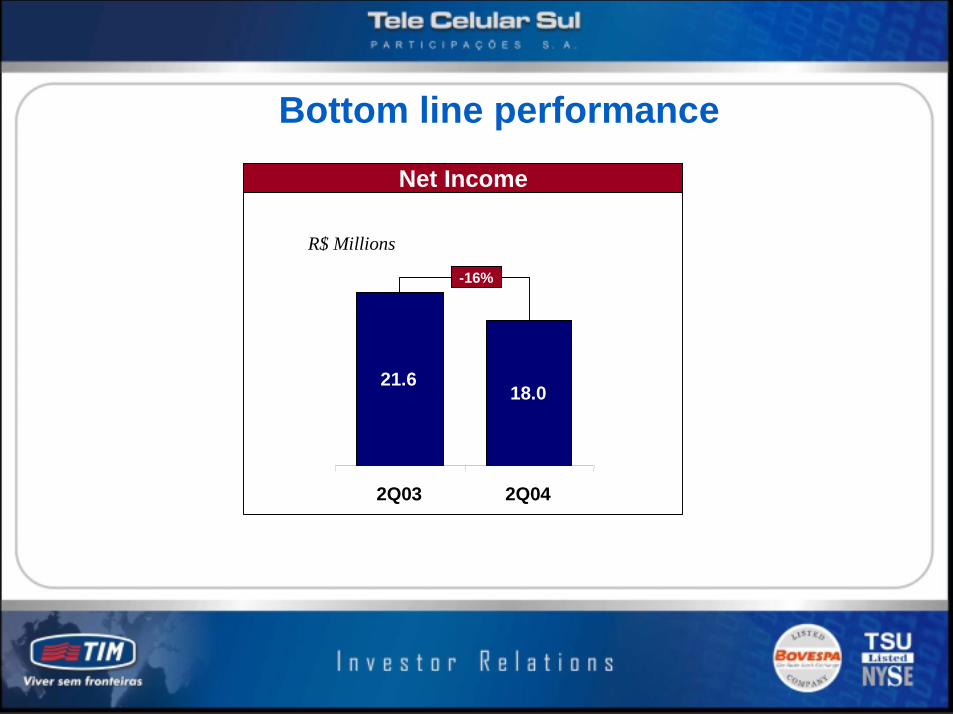

Bottom line performance

R$ Millions

Net Income

21.618.0

2Q03 2Q04

-16%

Slide 15

For further information, please contact:

Tele Celular Sul Participações S.A.R. Comendador Araújo. 299 – Cep 80.420-000Curitiba – PR – Brasil�: (+ 55) 41 312-6862http://timsulri.com.br/

Investor Relations Department:Joana SerafimCell: (+ 55) 41 [email protected]

Rafael BósioCell: (+ 55) 41 [email protected]