Search - January 2012 - Top 500 Manufacturing Companies: Listing & Analysis

108

-

Upload

infomedia18 -

Category

Documents

-

view

289 -

download

23

description

‘SEARCH’, India’s leading B2B magazine on general engineering and manufacturing, is aimed to equip its readers with latest business trends, news, views and insights. A ready-reckoner for all techno-commercial information, it is a sumptuous source of business trends and growth opportunities. Encompassing all the segments of manufacturing along with sourcing solutions, this monthly presentation is a unique platform for SMEs as well. With multitude of dedicated readers patronising this flagship magazine, launched in 1998, SEARCH has retained the leadership position in its domain.

Transcript of Search - January 2012 - Top 500 Manufacturing Companies: Listing & Analysis

Search Jan 2012 Ad Name: JYOTI CNC Pg. 7

Search Jan 2012 Ad Name: Riat Pg. 8

J A N U A R Y 2 0 1 2 | SEARCH - THE INDUSTRIAL SOURCEBOOK 11

EDITORIAL

new economic order is taking shape in front of our eyes, as the old Western powers and the emerging world’s major new players converge. But the forces driving this convergence are not those that generations of economists envisaged, but the new best strategies are the ones that have never been thought of by anybody else, this is to say that for all the old, new and the next generation companies to stay ahead, you need to think ahead.

Think ‘ahead’ of your perceived and hidden competitors and think ‘for’ your customers, a strategy which sounds simple, but has many layers and hidden insights concerning all

things important for companies to win. It is very important to accept and acknowledge that a company does not gain at the expense of its competitors or by limiting or cloning its competitor’s strategy, but rather, by crafting or deploying a distinctive strategy that changes the rules of the game in its favour. What wins in the business is not trying to out muscle your competitors with brawn, but rather to outthink those competitors with some serious brain power.

This will enable you to produce a distinctive strategy. Then again there is a need for strategic thinking, which sets out a vision of where your company is going. Use this as your basis for making appropriate choices and plans. Clarify what your company is, and is not, to avoid becoming scattered and overextended. Every leader of a company must carefully choose what game to play, and how to craft a strategy to make and shape the rules. How to use strategic thinking is today’s most important management tool, to put your company on a growth-oriented path to the future.

It is very important to find out how to overcome the key obstacles to strategic thinking; craft a future profile for your organisation; articulate a meaningful business concept; utilise strategic leverage; make competition practically irrelevant; benefit from product innovation & market fragmentation and avoid mistakes when making alliances and acquisitions, all this will help you outthink, outsmart & outpace your competitors.

In the automated world, it’s still the human angle that dominates the thought process and strategies for success. In the race to win customer confidence, companies must ensure that they make the customer come back for more. Focus on delivering high-quality services that meet the needs of key customers is critical. Producing innovative solutions comes from a number of actions — closer relationships with supply chain partners, making corporate acquisitions relevant to better meeting the needs of customers and investing in & developing relationships with existing and new generation of consumers for your product or service, all underpin a commitment to innovation. Another critical human angle is the workforce that has the potential to make or mar the fortunes of a company. Building the right leadership and creating the best team is fundamental to success.

All this and more will help you position yourself among the best in class, if you are already doing these things, chances are that you are a part of this envious listing of Top 500 Manufacturing Companies, if not, the analysis of what makes these winning companies tick will get you there.

So read on and go ahead… Outthink, Outsmart, Outpace your competitor!

AOUTTHINK, OUTSMART, OUTPACE

Archana [email protected]

J A N U A R Y 2 0 1 2 | SEARCH - THE INDUSTRIAL SOURCEBOOK 13

CARE RESEARCH & Information Services is an independent division of CARE. CARE Research services a variety of business research needs with credible, high quality research and analysis on various facets of the Indian Economy and Industries. The research division has a two pronged objective of providing an in-house research to the ratings division as also high quality sectoral research to fi nancial intermediaries, corporate, analysts, policy makers, etc., as an aid to their decision making process. CARE Research draws its strengths from CARE’s decade long experience and in-depth understanding of the Indian economy/industries, use of rigorous analytical methods and its knowledge team. It has an in-house team of qualifi ed, experienced analysts and is committed to provide accurate, reliable research to its clients with consistent updates in time frame.

CARE RESEARCH has established a network of primary and secondary sources, which enable the team of analysts to form unbiased opinions on industry segments. It has also developed different methodologies for forecasting the future demand-supply situation in a particular industry.

CARE RESEARCH produces Industry Research Reports, Industry Risk Evaluation Reports and undertakes customised assignments on request basis.

Industry Research: CARE Research is a leading provider of value research. Investors, corporates, bankers, analysts, etc use the sector reports for in-depth understanding of present situation, issues, outlook, etc., to arrive at opinion. The reports contain latest available data on capacity utilisation, consumption, prices, domestic and global trends, raw material scenario, and outlook. Further CARE Research also provides updates on monthly/quarterly /half-yearly basis as well as impact notes on policy changes. Subscription is made available though CARE online research distribution systems and all the reports can be accessed online from anywhere. The Industry Research Report services are today subscribed by vast number of clients. At present, we cover 30 industries.

Industry Risk Evaluation: Industry Risk Evaluation Reports offer industry specifi c risk scores which capture the infl uence of industry variables on various critical parameters which can impact cash fl ow and debt servicing capabilities of the industry for the next 2-3 years. The risks on various parameters are quantifi ed by assigning a score to each parameter. Some of the key parameters used for scoring are demand, supply, competition, factors of production, government policies and regulations and the fi nancial structure of the industry. The risk scores are useful tools for quantifying industry risk and are used in credit assessment of companies. At present, evaluation reports are available on 84 sectors.

Customised Research: The rising level of volatility in complex markets with lots of opportunities to tap necessitates a thorough understanding and guidance provided by a well known research fi rm. To address such needs, CARE Research offers need-based solutions by completely checking the facts, market scenario, past trends, etc., to help clients realise their futuristic goals and transform their businesses. Some of the areas in which we offer customised research are market sizing, demand estimation, demand-gap analysis, cost-benefi t analysis, cost indexation, product segmentation, business analysis, competitive intelligence, etc. We also prepare industry overviews for clients in connection with their capital markets offerings.

FOREWORD

DR DograMD & CEO, CARE Ltd.

he World Economic Outlook suggests moderation in global growth to about 4% through CY2012 from over 5% in CY2010. Th e real GDP in developed economies is anticipated to expand at about 1.9% in CY2012, while emerging/developing ones are anticipated to expand at 6.1%. Th e macroeconomic situation in India is currently subdued as refl ected by the decline in various indicators like GDP, IIP, export trends, etc. Th e Indian manufacturing sector grew at 3.7% in April-October, 2011, as compared to 9.4% in the last year. Hence, for the current fi scal, CARE estimates the GDP growth would be in the range of 7.1% to 7.4%, lower than 8.6% clocked in the previous fi scal.

IIP capital goods have registered a sharp drop of 25.5% in October, 2011, on the back of a slowdown in investments because of rising interest rates and slowdown in demand. Th ese factors have inevitably dragged down production in the manufacturing sector and are expected to have an impact in the coming months as well. Further, FY12 continues to be marked by concerns such as those emanating from the European debt crisis, global currency wars, etc. However, resilient domestic consumption followed by diversifi cation of businesses to new geographical areas would help India arrest the decline to some extent. India, with its vast domestic consumption, remains a more resilient economy and one of the fastest growing economies in the world.

CARE Research, as the Ratings Partner for SEARCH magazine, has developed a comprehensive methodology to bring out the leaders and rank the ‘Top-500 Indian Manufacturing Companies’ for the third consecutive year. Th e various parameters on which the companies were assessed on included: size of the company, profi tability, capital structure and return to the investor community. Th e research methodology is explained in detail in this issue and reinforces the fact that the companies, which strategically tackled the tidal waves of economic uncertainty, also paced faster than others to gain from the economic growth and achieved a higher rank than the rest in the rankings.

Going forward, apart from scalability, sustainability would be the mantra for success for the Indian manufacturing industry.

T

RATINGS PARTNER

Scalability & Sustainability: Key To Manufacturing Growth

J A N U A R Y 2 0 1 2 | SEARCH - THE INDUSTRIAL SOURCEBOOK 15

CONT

ENTSEditorial11

Foreword13

18

RANKING METHODOLOGYDeciphering The Top 500 Manufacturing Companies

30

Top 500 Manufacturing Companies - Listing34

ANALYSING THE TOP 14

54

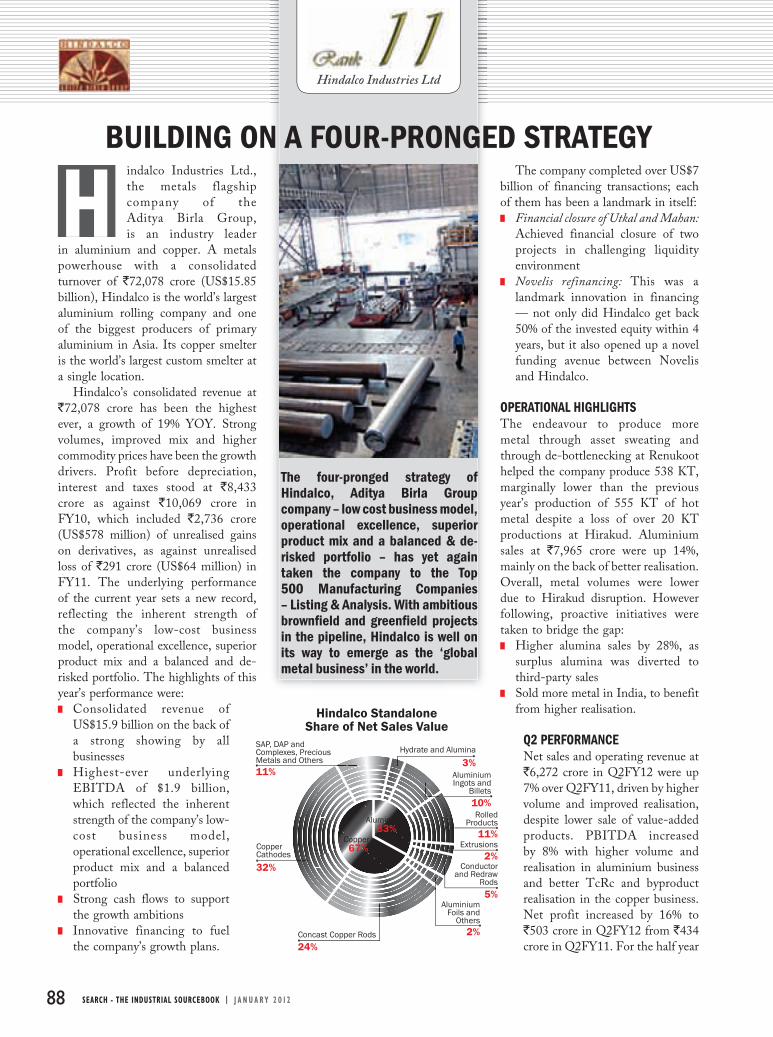

HINDALCO INDUSTRIES LTDBuilding On A Four-pronged Strategy

STEEL AUTHORITY OF INDIA LTD (SAIL)Growing From Strength-to-strength

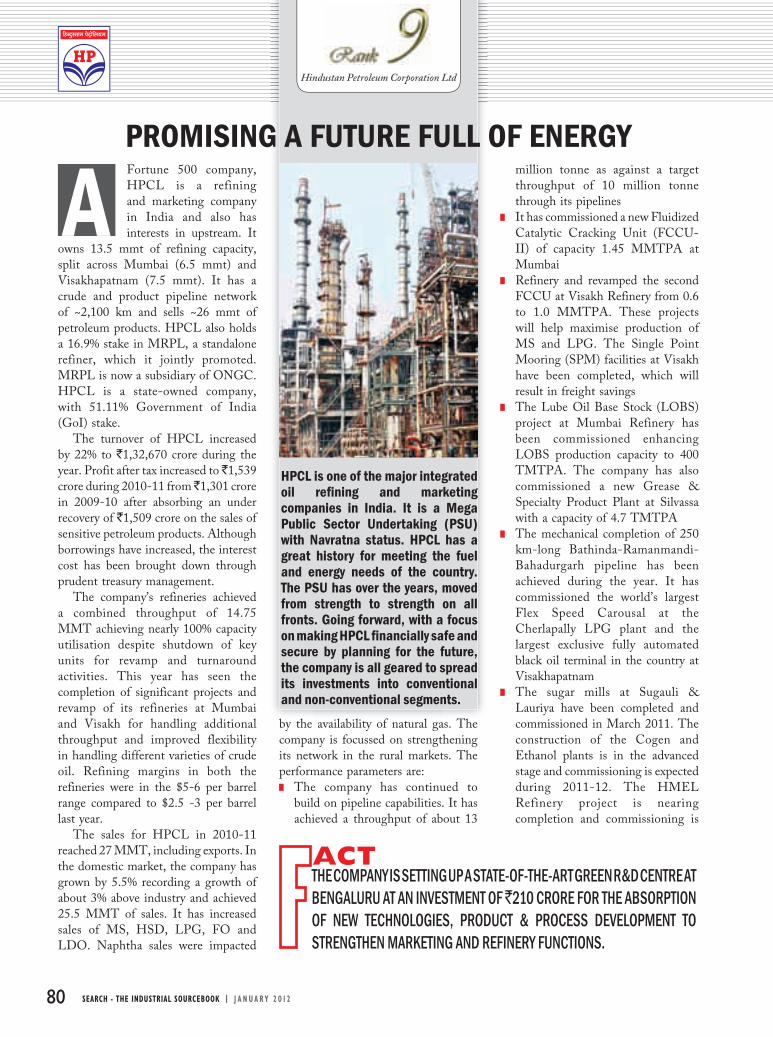

HINDUSTAN PETROLEUM CORPORATION LTD (HPCL)Promising A Future Full Of Energy

BHARAT PETROLEUM CORPORATION LTD (BPCL)Securing India’s Future Energy Needs

TATA MOTORSCapitalising On Product Innovation

ITCBuilding on Green GDP & Inclusive Growth

INDIAN OIL CORPORATION (IOC)On A Strong Tech & Marketing Footing

OIL & NATURAL GAS CORPORATION (ONGC)Moving Towards Hydrocarbon Assets

RELIANCE INDUSTRIES LTD (RIL)The Pole Star

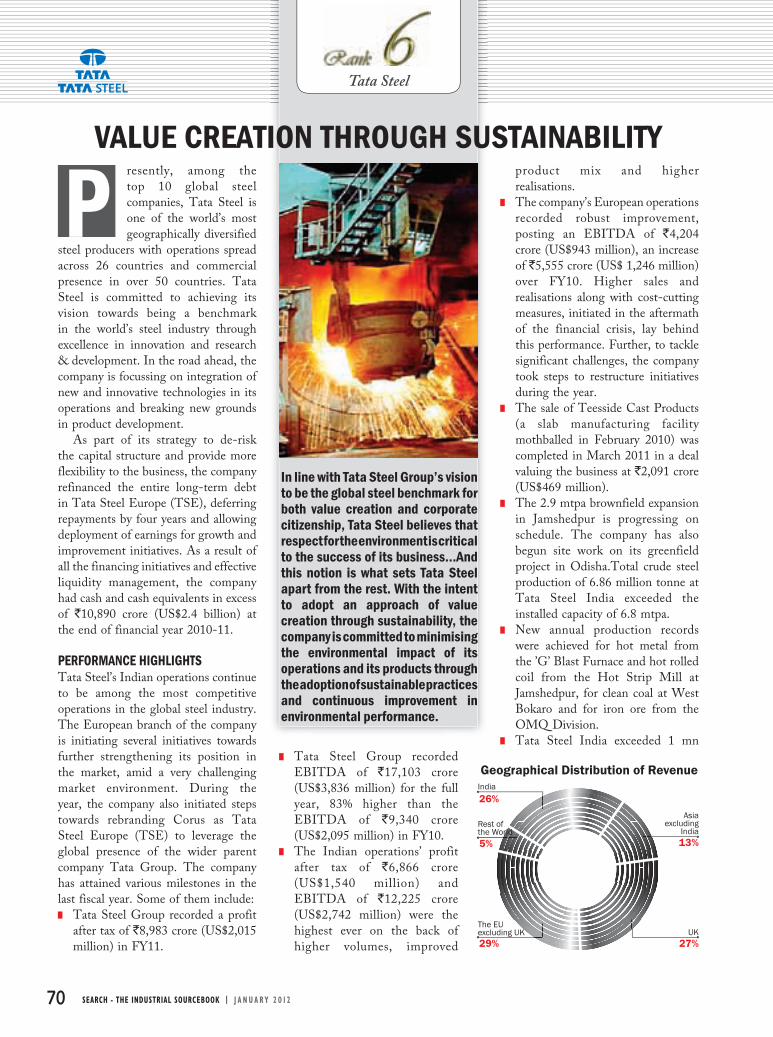

TATA STEELValue Creation Through Sustainability

BHARAT HEAVY ELECTRICALS LTD (BHEL)Of Envious Order Books & Potential Profi ts

STERLITE INDUSTRIES (INDIA) LTDFocussing On Organic Growth Projects

56

60

63

67

70

74

78

80

84

88

92

HINDUSTAN UNILEVER LTD (HUL)Winning With Brands & Innovations 96

Glossary102 Product Index103

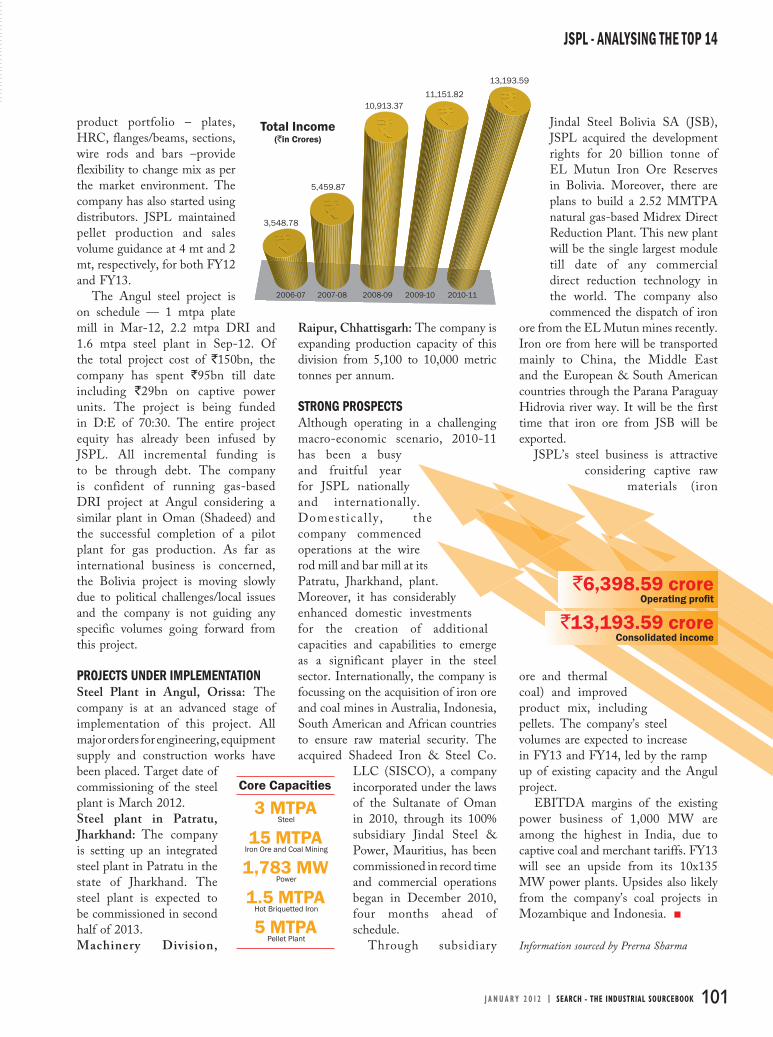

JINDAL STEEL & POWER LTDTreading Along The Success Path 100

Advertisers’ List104

GLOBAL ECONOMIC OUTLOOKProspects Constrained, Yet Sturdy

24 China: Slower Growth, Longer-term Risks

27 Japan: On The Bright Side…

28 India: Trudging Along, For Now

FOUNDER & EDITOR, NETWORK 18Raghav Bahl

PRESIDENT & EDITORIAL DIRECTOR, TV 18Senthil Chengalvarayan

EXECUTIVE EDITORArchana Tiwari-Nayudu

ASSISTANT EDITORPrerna Sharma

EDITORIAL TEAMSumedha Mahorey, Kimberley D’Mello, Nishi Rath, Michael Anthony,

Arindam Ghosh (Delhi), Abha Mishra, Paskaline L Sebastian

ASSISTANT ART DIRECTORVaruna Naik

DESIGN TEAMSanjay Dalvi, Uttam Rane

CHIEF PHOTOGRAPHERMexy Xavier

PHOTOGRAPHYNeha Mithbawkar, Joshua Navalkar

BUSINESS CONTROLLERSPukha Dhawan, Lovey Fernandes, Akshata Rane, Deepak Bhatia,

Shwetha ME, Jayashree N, Sugandha Kulkarni, Shefali Mahant

PRINTINGEXECUTIVE VICE PRESIDENT

Ananth R Iyer

ASSISTANT GENERAL MANAGER - PPCShekhar Khot

PRODUCTION TEAMDnyaneshwar Goythale, Surekha Karmarkar, Ravikumar Potdar, Ravi Salian, Sanjay Shelar

OVERSEAS CONTACTRingier Trade Media Ltd CHINA

1001 Tower 3, Donghai Plaza, 1486 Nanjing Road, West, Shanghai 200040, China Tel: +86-21 6289 – 5533 Ext. 368, Fax: +86-21 6247 – 4855

(Craig Shibinsky) Email: [email protected] Trade Media Ltd HONG KONG

9/F, Cheong Sun Tower, 118 Wing Lok Street, Sheung Wan, Hong Kong Tel: +852 2369 – 8788 Ext. 21, Fax: +852 2869 – 5919

(Octavia Au-Yeung) Email: [email protected] Trade Media Ltd TAIWAN

Room 3, Fl. 12, No. 303, Chung Ming S. Rd., Taichung, TaiwanTel: +886-4 2329 – 7318 Ext. 16, Fax: +886-4 2310 – 7167

(Sydney La) Email: [email protected] Trade Media Ltd GERMANY, AUSTRIA, SWITZERLAND

Tel: +41-44 734 0472, Fax: +41 44 734 0680Email: [email protected]

USA Tel: (513) 527-8800 Fax: (513) 527-8801

Email: [email protected]

USA Alfredo Domador, 6505 Blue Lagoon Drive, Suite 430 Miami, FL. 33126, USA

Tel: (305) 448-6875, Fax: (305) 448-9942

GROUP CEO, NETWORK 18Haresh Chawla

GROUP COO, NETWORK 18B Sai Kumar

CEO-PUBLISHING, INFOMEDIA 18Sandeep Khosla

EVP-HUMAN RESOURCESSanjeev Kumar Singh

ASSOCIATE VICE PRESIDENTSudhanva Jategaonkar

ADVERTISING SALESShashin Bhagat (Ahmedabad)[email protected]

Mahadev B (Bengaluru)[email protected]

Hari Hara Subramaniam (Chennai)[email protected]

Prakash N (Coimbatore)[email protected]

Rahul Hanchate (Hyderabad)[email protected]

Ameya Gokhale (Indore)[email protected]

Durgesh Grover (Jaipur)[email protected]

Inder Dhingra (Ludhiana)[email protected]

Mukesh Yadav (New Delhi)[email protected]

Rohit Dass (Pune)[email protected]

Chirag Pathak (Vadodara)[email protected]

MARKETING TEAMGanesh Mahale, Prachi Mutha, Varsha Nawathe, Abhay Borkar

NEWSSTAND AND SUBSCRIPTIONSDISTRIBUTION HEADSunil Nair

DEPUTY GENERAL MANAGERManoj Palsay

SENIOR MANAGER - SUBSCRIPTIONSSheetal Kotawdekar

CO-ORDINATORSRahul Mankar, Anant Shirke, Sarita Quadros,Chaitali Parkar, Kamlesh Mathkar, Vaibhav Ghavale

SERVICESSUBSCRIPTION SERVICES For subscription queries, write [email protected] or call +91 22 30034631-34 or toll free 1800 200 1021

PERMISSIONS For subscription to copy or reuse material from SEARCH,Write to [email protected]

Views and opinions expressed in this magazine are not necessarily those of Infomedia18 Ltd, its publisher and/or editors. We at Infomedia 18 Ltd do our best to verify the information published but do not take any responsibility for the absolute accuracy of the information. Infomedia 18 Ltd does not accept the responsibility for any investment or other decision taken by readers on the basis of information provided herein. Infomedia 18 Ltd does not take responsibility for returning unsolicited material sent without due postal stamps for return postage. No part of this magazine can be reproduced without the prior written permission of the publisher. Infomedia18 Ltd reserves the right to use the information published herein in any manner whatsoever.

Infomedia 18 Ltd is the publishing arm of Network 18.

Printed by Mohan Gajria and published by Lakshmi Narasimhan on behalf of Infomedia 18 Ltd.Executive Editor: Archana Tiwari-NayuduPrinted at Infomedia 18 Ltd, Plot no.3, Sector 7, off Sion-Panvel Road, Nerul, Navi Mumbai 400 706, and published at Infomedia 18 Ltd, ‘A’ Wing, Ruby House, J K Sawant Marg, Dadar (W), Mumbai - 400 028. SEARCH is registered with the Registrar of Newspapers of India under No. 67827/98. Infomedia 18 Ltd does not take any responsibility for loss or damage incurred or suffered by any subscriber of this magazine as a result of his/her accepting any invitation/offer published in this edition.

18 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

UROZONELast quarter, the biggest issues facing the global economy were the crisis in the Eurozone and uncertainty about the path of US monetary and fiscal policy. Well, nothing seems to have changed. These remain the big issues. And yet,

much has indeed changed. In Europe, the members of the Eurozone agreed on a new package for assisting Greece, only to find that financial market stress kept getting worse as market participants doubted the

package would be sufficient. The fortune of the Eurozone depends crucially on whether -

and how fast - a convincing solution to the debt crisis can be found and implemented. Fears of a Greek default

and its contagion effect, including the possibility of an ensuing banking crisis, hang over the economy

like the sword of Damocles. Leaders are currently trying to solve three key issues: Dealing decisively with Greece while

firewalling other, less-affected fringe nations Establishing a mechanism for a functioning European bond market by giving the European Financial Stability Facility (EFSF) more money and more power Putting the announced plans on fiscal and

macroeconomic surveillance and enforcement into action. Eurozone growth is slowing. Sentiment has

deteriorated over the summer amid signs of weakening global demand and disappointed hopes of solving the

sovereign debt crisis. This is a crucial time for Europe. If Eurozone leaders act decisively to stabilise financial markets and turn

their plans for closer cooperation into action, it could halt the downward spiral of deteriorating confidence and weakening activity. Real economic

Global economic activity weakened in the fi rst half of 2011. In advanced economies, the recovery was dragged down by the continued fragility in private sector balance sheets, as fi nancial markets were buffeted by a series of shocks, including greater Euro area sovereign risks and the credit downgrade of the US. Tracking the impact of these on the emerging economies, here’s analysing the prospects that the global economy holds...

ProspectsConstrained,

SturdyYetYet

E

18 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

J A N U A R Y 2 0 1 2 | SEARCH - THE INDUSTRIAL SOURCEBOOK 19

GLOBAL ECONOMIC OUTLOOK

indicators are not yet indicating a recession, but markets remain unsettled by deteriorating sentiment and speculation about the future of the monetary union.

THE UNITED STATESIn the United States, it is likely that job growth failed to materialise, in part, because the private sector faced increased costs associated with regulatory oversight in health care, financial services, and energy. Add to this, the increase in government spending that was used to fund short-term consumption, shifting wealth from the future into the present. And finally, the Federal Reserve’s high-risk but ultimately unsuccessful second round of quantitative easing increased oil and food prices but did little to stimulate real growth.

The first piece of hard data that argues in favor of a recession can be found in the most recent readings on US Gross Domestic Product (GDP). While the 2007–2009 recession was more severe than previously advertised, the new data also showed that real GDP growth in the second quarter was up just 1.5% from a year ago. Since 1947, there have been 14 occasions when real GDP growth slowed below 2%. In 11 of those cases, the economy fell into a recession, which puts the historical probability at 78%.

The second development that raises the risk of a recession in the United States is the European debt crisis and a corresponding recession that would follow it. A recession in Europe would wash back into the US economy in several ways, including trade, industrial production, corporate profitability, and banking. The European Union is a major trading partner for the United States, accounting for $259 billion in exports, which is roughly 12% of the $1.9 trillion in total US exports. During the 2008–2009 recession, exports to the EU fell sharply from a peak of $272 billion to $220 billion, a peak-to-trough decline of 19.1% over a fifteen month period. Even with a recovery, the US exports to the EU are still 4.9% below their mid-2008 peak.

Another recession in Europe would have a comparable drag on US exports. A comparable decline to what happened in 2008–2009 would bring US exports down to $210 billion. Since Europe would not be the only place from which US exports would decline, the trade sector would become a drag on growth.

US businesses are going into this recession with much stronger balance sheets and much leaner operations than in 2008. Cash levels and productivity are substantially higher. With leaner operations, layoffs and inventory reduction will not create the kind of downdraft for the broader macro economy that they did in 2008. On the downside, the policy options available to address the recession are much more limited today than they were in 2008. Back-to-back stimulus programs in 2009 and 2010 in excess of $800 billion are unthinkable today. A third round of quantitative

easing is possible, but it will be controversial and given the effectiveness of the previous round, may be of limited value. Weaker exports, a decline in business investment, and contracting manufacturing will likely combine to push an economy that is operating at stall speed into a recession.

UNITED KINGDOMConsistent with the other large industrialised countries, UK growth slowed sharply in the second quarter (although, in the case of the UK, activity was somewhat depressed by timing effects and by the impact of Japan’s tsunami and earthquake). UK domestic fundamentals have weakened, but the big change has been in the global environment. The Eurozone debt crisis created fears of a vicious spiral of sovereign and bank defaults. One consequence has been the virtual closure of corporate bond and bank term funding markets to new issuance.

Confidence about global growth has waned. Consensus forecasts for GDP growth have declined across the industrialised world. The UK consumer sector remains weak with spending under pressure from a severe squeeze on real incomes. Over the last year, real personal disposable incomes have fallen by almost 3%, the fastest rate of decline in this indicator of consumer spending power since 1976. With consumer borrowing growing at single-digit rates, credit has been unable to fill the gap. Over the last year, retail spending has hardly increased, and house prices have fallen. Mortgage approvals, a key leading indicator for housing activity, remain at historically low levels.

Much will hinge on the speed and effectiveness of the response from European policymakers to the crisis in the Euro area. A combination of monetary ease in the UK and abroad should help bolster growth next year. So, too, will sharply lower inflation; UK inflation is widely expected to almost halve over the next 12 months, and this will support consumer spending power. But the UK’s fortunes are heavily dependent on events in the Euro area. Financial stress, as Lehman’s failure demonstrated, can spread contagiously. Disruption to demand in the Euro area would hit the UK’s largest export market. Introducing another round of quantitative easing in the UK is politically and technically straightforward, but finding a solution to the problems of the Euro area is precisely the opposite.

RUSSIAAt long last, the political situation in Russia has clarity. It was announced that Prime Minister Putin will return as president in March 2012, exchanging jobs with President Medvedev. This means that, in theory, Putin could be president for the next 12 years since the constitution would allow this. Yet, clarity about who occupies which chair does not imply clarity about the policy outlook, which remains uncertain. And it could be that uncertainty pertaining to

20 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

GLOBAL ECONOMIC OUTLOOK

policy has contributed to a declining value of the ruble. In the past few years, Russia has experienced almost $250 billion in capital flight, given the weak global economy and a perception of poor investment opportunities at home. Such flight puts downward pressure on the currency.

Unfortunately, a slowing global economy and dampening oil prices will not be helpful. Instead, the economy will mostly have to rely on domestic demand. While consumer spending is doing well, fixed asset investment is not growing at a speed that would offset a slowdown in exports. On the positive side, consumer spending continues to rise, given rising real wages and greater access to consumer credit. Also, it is widely expected that fiscal policy will be more expansive in the months leading up to the election in March. This expectation is based on the fact that similar policy shifts have taken place in the past. Fiscal expansion will likely have a positive impact on economic activity.

Also on the positive side is the fact that inflation is not accelerating. The central bank tightened monetary policy during the first half of 2011, but it left policy unchanged since May. This tightening, combined with declining global food and energy prices, has caused inflation to peak below 10%. In addition, it is expected that inflation will gradually decline in the coming year. However, a steep drop in the value of the ruble could have an inflationary impact.

As for monetary policy, the deceleration of inflation provides the central bank room for engaging in more aggressive policy, should the economic slowdown become onerous. On the other hand, while the central bank does not explicitly target the exchange rate, a declining ruble could restrain the bank from cutting interest rates.

BRAZILBrazil’s central bank has chosen a new path. After a two year period of raising interest rates in order to fight rising inflation, the bank suddenly and unexpectedly cut the critical Selic rate in August. The changing fortunes of the global economy have caused the central bank to rethink its policy in light of a new outlook.

Going forward, it seems likely that interest rates will be cut further. After all, the inflation-adjusted interest rate remains fairly high by global standards. A lower rate will help maintain a satisfactory level of business investment. In addition, the rate of inflation is expected to decline as the economy slows and, especially, as commodity prices stabilize. Thus, a looser monetary policy is likely to be beneficial.

The Brazilian economy will probably grow more slowly in the coming year than it did recently. The lagged effect of tight monetary policy and a high valued currency will take its toll on growth. Yet the new policy of lower rates, combined with a declining currency, will help boost investment and exports. Foreign direct investment is likely to be strong given expectations about Brazil’s long-term future.

The big uncertainty concerns the impact of the global economy on Brazil. A severe recession in Europe emanating from a partial collapse of the Eurozone would certainly have a negative impact on Brazil. Moreover, a global slowdown could have a significantly negative impact on commodity prices, which in turn, would hurt Brazil’s export revenue.

MEXICOAt the turn of this century, Mexico was Latin America’s largest economy. Its prospects were akin to those of the BRIC nations. However, as the BRICs’ marched ahead, Mexico, it seems, lost its way. Despite being an uppermiddle-income nation, Mexico continues to grapple with widespread income inequality and poverty. Between 2000 and 2010, Brazil’s economy grew at an average rate of 3.7% compared to Mexico’s 2%. Today, Brazil’s economy is larger than Mexico and growing at a faster pace. While the outlook for China, India, and Russia is much more favorable, Mexico finds itself caught in the crossfire of violent drug cartels and the prospect of an economic slowdown for its major trading partner, the United States. Yet, Mexico has tremendous potential and if policymakers tackle the country’s challenges effectively, the economy could blossom once again.

The economy will be constrained by declining oil output (due to underinvestment), poor business investment, and the likelihood of an unstable environment due to widespread violence. If remittances continue to increase, it could potentially boost domestic demand and positively impact the local economy. Higher consumer spending will likely benefit the retail industry as more people transition into the middle class. If demand from the United States strengthens, the export sector will be boosted. With elections due this year, tackling security concerns and making Mexico’s economic environment conducive for large-scale foreign and domestic investment will be high on the agenda.

ASIAThe increased uncertainty over the global outlook and greater risk aversion in financial markets spilled over to Asia in August and September 2011, with leveraged investors liquidating profitable positions in the region to cover their losses elsewhere. As a result, many Asian financial and currency markets experienced declines of magnitudes similar to those experienced in mid 2010.

After a strong start in the first quarter of 2011, economic activity in Asia has also moderated (Figure 1.1). Sluggish demand in advanced economies and supply chain disruptions after the tragic March 2011 earthquake and tsunami in Japan led to a broad-based decline in industrial production and export growth across Asia. High frequency indicators, including manufacturing purchasing managers’ indices (PMI) and export orders, suggest that the moderation of activity continued in the third quarter of 2011.

22 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

GLOBAL ECONOMIC OUTLOOK

By contrast, Asian domestic demand has proven generally resilient in 2011. Employment gains and real wage growth supported private consumption, and high capacity utilisation boosted private investment. Financial conditions have remained accommodative in most of Asia, as increases in interest rates were offset partly by higher inflation in some economies (such as Korea, Malaysia, and Thailand), and real effective exchange rates have generally not strengthened during 2011, except in a few commodity exporters, including Indonesia, Australia and New Zealand, as well as in Korea & Singapore. By contrast, monetary policy normalisation and slowing credit growth have contributed to tighter financial conditions in China and India.

Notwithstanding the moderation in growth, inflationary pressures across the Asia-Pacific region remain elevated. Headline inflation continued to increase in most economies and averaged 5.5% (year over year) in July 2011, as compared

with 4.6% in January. In particular, inflation has continued to rise in China, Hong Kong SAR, Korea & Vietnam, and remains above central banks’ explicit or implicit targets in many cases. Inflation has been driven by commodity prices, but also in many economies by sustained demand pressures. Indeed, core inflation has increased in Hong Kong SAR, India, Indonesia, Korea, Malaysia and Thailand, as second-round effects of previous commodity price rises have fed through to generalised inflationary pressures.

Inflation expectations have also risen since the first quarter of 2011 in a number of economies. In contrast to the rest of the region, Japan’s deflationary pressures persisted, with core inflation that excludes food and energy prices still in negative territory as of July 2011.

DYNAMICS AND COMPOSITION OF GROWTHThe dynamics and composition of growth in 2011 have

varied across Asia: In much of industrial Asia, economic activity has been

significantly influenced by natural disasters. In Japan, the earthquake and tsunami led to a sharp contraction in domestic demand. In Australia, cyclones and flooding disrupted mineral output, although strong global demand for coal and iron pushed the terms of trade to 60-year highs and supported private investment. New Zealand’s economy, however, continued to expand despite the impact of the January 2011 earthquake.

In East Asia, growth has been held up by strong domestic demand. In China, gains in wages employment supported private consumption, whereas strong private investment, including real estate investment, offset a slowdown in public investment. Growing financial and economic integration with the mainland helped cushion Hong Kong SAR and Taiwan Province of China against weaker

external demand from advanced economies. In Korea, continuing easy financial conditions and wage growth supported private domestic demand. In several ASEAN economies, strong domestic

demand, particularly investment, helped mitigate the slowdown in export growth. In addition, commodity exporters, such as Indonesia and Malaysia, benefitted from the rise in commodity prices through mid-2011. Inflation concerns have persisted in Vietnam. In South Asia, private consumption remained

robust in India on account of rising disposable income, but investment was subdued partly on concerns over governance and the global outlook. In Bangladesh, buoyant credit growth amid a still-accommodative monetary stance continued to fuel domestic demand, while in Sri Lanka activity benefitted from greater political stability. In Nepal, domestic demand was subdued on investor concerns

over banking system fragilities and a decline in remittances from the Middle East.

In other low-income countries and Pacific Island economies, commodity exporters such as Mongolia and Papua New Guinea benefitted from high mineral prices in the first half of 2011, and new garment quotas in European markets contributed to buoyant exports in Cambodia. In Mongolia, growth has also been fuelled by expansionary macroeconomic policies, which boosted underlying inflation above the authorities’ target. However, in a number of Pacific Island economies, high commodity prices continued to weigh on growth, although the strong Australian dollar boosted tourism flows.Net capital flows into emerging Asia have moderated

so far in 2011 relative to 2010, following the sharp rise in global risk aversion. Within the region, however, there are large disparities — in the first half of 2011, capital

30

25

20

15

10

5

0

-5

-10

Sing

apor

e

Japa

n

Thai

land

Phili

ppin

es

New

Zea

land

Taiw

an P

rovi

nce

of C

hina

Hong

Kon

g SA

R

Mal

aysi

a

Kore

a

Indi

a

Aust

ralia

Indo

nesi

a

Chin

a

2011:01 2011:02

Sources: CEIC Data Company Ltd.; Haver Analytics; and IMF staff calculations.

Figure 1: Selected Asia: Real GDP at Market Prices(Quarter-over-quarter% change; SAAR)

24 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

GLOBAL ECONOMIC OUTLOOK

China’s economic growth is decelerating because of the weakening global economy and tightened monetary policy. Overall debt has nearly tripled in the last fi ve years and signifi cant investments in fi xed assets may loom heavily over China’s longer term.

hina’s economy is decelerating. In September, the purchasing managers’ indices for output

and exports were below 50 for a third month in a row, which has not happened since 2009. Still, the indices

barely slipped below 50, indicating that the decline in manufacturing is moderate. Moreover, China’s central bank has stopped tightening policy given the latest global slowdown. Therefore, although China’s economy

will slow down, deceleration will likely be less-than-dramatic. On the other hand, it is notable that a senior Chinese official recently predicted that growth in 2012 would be below 9%. If this prediction materialises, it would be the

China:Slower growth,

longer-term risks

C

inflows remained strong in China, thus reflecting increased borrowing by mainland firms from Hong Kong SAR, and in India & Indonesia, where strong growth prospects and interest rate differentials attracted large equity and bond inflows, respectively. In East Asia (excluding China) and Singapore, however, concerns about slowing growth led to net capital outflows. Although direct investment and banking inflows to Asia have been relatively resilient, equity and bond inflows have been volatile, with equity recording sharp outflows since August 2011.

GROWTH FORECAST Looking ahead, for the region, growth is forecast to average 6¼% in 2011 and 6¾% in 2012. The somewhat weaker growth forecast for Asia mainly reflects the deteriorating outlook for exports to advanced economies. The impact would be smaller for domestic demand-based economies, such as China, India & Indonesia and larger for highly open economies that specialise in income-sensitive, high-tech consumer and investment goods, such as Korea, Singapore and Taiwan Province of China. Adverse regional supply chain disruptions are not expected to play a major role in the future, as Japanese production in key sectors returned to normal levels.

The fundamentals for domestic demand in the region remain strong and are expected to cushion the impact of weaker external demand on overall growth in 2012: In Industrial Asia, reconstruction investment will be the

main driver of domestic demand growth in Japan, while investment in mining will propel growth in Australia.

In East Asia, more spending on social housing is expected to support investment in China. Moreover, accommodative

financial conditions and high capacity utilisation should boost private investment in Korea, while strong employment is expected to sustain private consumption in Hong Kong SAR.

In more advanced ASEAN economies, in addition to favourable labour market conditions and high capacity utilisation, greater public investment projects will provide an additional boost to domestic demand in Indonesia, Malaysia, the Philippines and Singapore. In Thailand, the new government is seeking to stimulate domestic demand through measures to increase disposable income and private investment.

In India, robust disposable income growth (including from high agricultural prices) and accommodative financial conditions are expected to support private consumption and investment.Headline inflation is expected to decelerate gradually in

2012. But inflation is expected to remain above the midpoint of the target range in most Asian economies, as commodity prices fall only slightly, domestic demand pressures persist and inflation spillovers from key regional economies remain elevated. The September 2011 World Economic Outlook, (WEO) projects fuel and nonfuel commodity price inflation in 2012 to recede by 3.5% and 4.5%, respectively – a mild deceleration relative to the sharp run up in 2010-11.

Moreover, output gaps in many Asian economies will remain positive in 2012. Finally, inflation in China is expected to settle at levels that, while lower than the peak in 2011, are higher than in the recent past – with spillovers to inflation in the rest of Asia.

Let’s take a look at the fortunes of major Asian economies in the near-term:

26 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

GLOBAL ECONOMIC OUTLOOK

first year since 2001 that growth falls below 9%. These comments reflect a belief that a combination of monetary policy tightening and reduced global growth will cause the Chinese economy to grow more slowly.

Interestingly, there is an evidence that the economic slowdown is being experienced principally by small- to medium-sized private businesses and not by the large, state-run enterprises that retain favourable access to credit. After all, imports of oil and iron ore rose significantly in August. The biggest source of recent growth has been fixed asset investment, especially construction. The importation of iron ore, used to make steel, indicates ongoing strength in construction. Meanwhile, a deceleration in exports is the prime cause of the economic slowdown. While the strength of construction is good in the short term, it means that China continues to over-build.

EXCESSIVE DEBT China’s officials have complained about the rapid expansion of US Government debt. This reflects fear that the massive stock of foreign currency reserves held by China’s Government could lose value. Less attention, however, has been paid to the big increase in overall debt in China itself. Yet, that is likely to change soon, given the fact that overall debt has nearly tripled in the past five years.

HOW DID IT COME TO THIS?When the global economic crisis began in 2008 and China’s exports suddenly dropped, the government implemented a vast stimulus programme to boost domestic demand and offset the drop in exports. Part of this involved extending credit to provincial and local governments to engage in infrastructure development. In the short run, this policy was successful in boosting growth and preventing a general recession. The problem, however, is that many such investments have failed

to generate adequate returns. The Chinese Government estimates that little more than one quarter of local government investment has produced a return adequate to service the debts.

Furthermore, local government borrowing is not the entire problem. During the global crisis, the government injected capital into state-run banks so that they could lend to state-run companies. The result was an investment boom. Yet this also involved many investments that are not producing an adequate return. The result was that investment in fixed assets surged, reaching almost 50% of last year’s GDP.

WHAT EXACTLY IS THE RISK?Is China at risk of having a financial crisis? On one hand, there is a danger that a new round of defaults will damage the solvency of China’s state-run banking system. Yet, it is likely that the government would bail out such banks and thereby prevent a larger financial crisis. Moreover, due to capital controls, China’s financial system is not integrated into the global economy. Therefore, a problem in China’s banks would not lead to problems outside China.

On the other hand, China does face a risk. Specifically, if the government were compelled to bail out troubled financial institutions, it would probably not support continued lending for the purpose of poorly conceived investments. Consequently, investment would likely fall considerably. Given that investment is now close to 50% of GDP, such a fall could have serious consequences for GDP without an offsetting increase in something else. What could that something else be?

Exports are not likely to take up slack. With a rising currency, slower growth overseas, and rising wages at China’s factories, it seems likely that export growth will be slow in the next few years. In this scenario, China will likely look towards a boost in consumer spending to offset a decline

in investment, but it would have to grow rapidly to make a difference and avoid a significant slowdown, given that consumer spending is now only 35% of GDP.

WHAT COULD GO RIGHT?There are some positive signs concerning the prospect for boosting consumer spending. First, wages have been rising, adding to real, disposable incomes. This reflects a shortage of labour as demographic trends limit the labour force’s growth and as internal migration slows. In addition, provincial and local governments have been increasing their minimum wages. Second, the government intends to have state-run companies pay higher dividends to shareholders. In doing so, this will reduce retained earnings and therefore, the impetus to invest. Third, higher inflation will help reduce some of the real value of the debts in question. On the other hand, high inflation means that real interest rates are largely negative, thereby fuelling continued borrowing. Also, high inflation means that the real value of the currency is rising quickly, thereby hurting export competitiveness. So, a slowdown in exports could become more pronounced.

WHAT HAPPENS NEXT?It is safe to say that China is slowing down. In addition, the excessive debt-financed investment of recent years will likely lead to challenges somewhere down the road. In that situation, economic growth will decelerate. How much it slows will depend on a variety of factors, including how the government responds to such an event. In any event, an economic slowdown in China will have global ramifications. A Chinese slowdown will remove pressure on global commodity prices and reduce export growth for China’s major trading partners. Domestically, slower growth could remove some of the upward pressure on wages and prices.

J A N U A R Y 2 0 1 2 | SEARCH - THE INDUSTRIAL SOURCEBOOK 27

GLOBAL ECONOMIC OUTLOOK

n a world of slowing economic growth, Japan is the exception. In fact, the country can

reasonably expect that growth will soon accelerate — at least for a while. The silver lining of a natural disaster is the extra spending that boosts economic growth, but the positive impact of reconstruction spending has not met expectations. Challenges remain for the Japanese economy.

In the second quarter of 2011, the economy contracted at a rate of 2%. This third consecutive quarter of declining GDP was, in part, due to the negative impact of the earthquake and tsunami. While many analysts anticipated a strong boost to economic growth in the second half of 2011, the latest numbers suggest slower growth than expected. The Tankan index of sentiment at large manufacturing companies rose from -9 in the second quarter to +2 in the third quarter. A positive reading means that there are more optimists than pessimists among the surveyed executives. The current reading is still lower than in March, just before the earthquake. Japan is recovering, but the pace is underwhelming. This is likely due to slower overseas growth, a high-valued yen and slower than expected reconstruction spending.

The rising value of the yen is taking its toll on the industrial sector. While the automotive sector is recovering from damage to its supply chain, the major players are planning to

shift production capacity offshore in order to avoid the impact of an overvalued currency. The strong yen reflects several factors, including the repatriation of overseas funds for the purpose of reconstruction. It is also due to the perception of Japan as a safe haven for financial assets in a time of global turmoil. Although the return on Japanese assets is very low, global investors do not perceive them to be at risk of outright failure.

Still, despite troubles in Japan’s export sector, the country will probably grow faster in 2012 than either Europe or the US. This case would be different sans the earthquake or tsunami; reconstruction spending will make a significant difference.

In September, the Japanese Government proposed its third reconstruction budget of 12 trillion yen — roughly $160 billion, which is about twice of what has already been budgeted. This brings the total to about $240 billion. The big debate has been over how to finance this expenditure. The current government has indicated a preference for tax increases so as to not substantially increase the already large debt. As such, it is likely that there will be an increase in the consumption tax. This will have some negative impact on consumer spending. In addition to increasing the consumption tax, the government plans to sell assets such as shares in Japan Tobacco to fund reconstruction.

Interestingly, the government’s

deficit was already projected to be 8% of the GDP even before the earthquake. Reconstruction costs, by adding an estimated 4% of GDP, will not have a big impact on overall debt, even if it is financed by borrowing. Meanwhile, despite the government’s plans for fiscal rectitude, Moody’s has again downgraded Japan’s sovereign debt. This action had little impact on the market for Japanese Government bonds, which continue to offer among the lowest rates of return in the world. While Moody’s was evidently concerned about the fact that government debt has reached 200% of GDP, there are other mitigating factors. For example, 95% of that debt is held domestically. In addition, Japan continues to have a very high rate of savings, so financing government deficits is not a problem.

Interestingly, Japanese monetary policy has been relatively aggressive this year; the Bank of Japan is engaged in quantitative easing on a surprisingly large scale, but perhaps it has not been large enough. The currency continues to rise, and inflation continues to be very low. One of the purposes of a round of quantitative easing is to boost expectations of inflation. Higher inflation can have the effect of boosting spending, reducing real interest rates and reducing the real value of debts. However, retail sales are declining, business investment fell in the second quarter and inflation remains close to zero. Thus, the real level of debt has

Japan: On theBright side…

The Japanese economy is one of the few economic bright spots in a world that is experiencing slower growth. Japan is recovering from a natural disaster and additional spending will likely accelerate the Japanese economy next year. However, slower overseas growth, a high-valued yen and slower than expected reconstruction spending, are introducing obstacles to the country’s economic prospects.

I

28 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

GLOBAL ECONOMIC OUTLOOK

Indian policymakers are trying to curb the rapidly rising infl ation and simultaneously sustain growth despite a weakening global economy. GDP growth may continue to hover around 7.5% for the current fi scal year.

ver the past two years, India has experienced one of the highest inflation rates in major

emerging markets. High food inflation and fears of a lack of meaningful fiscal intervention have compelled the central bank to increase interest rates in order to pursue lower prices at the expense of growth. The central bank’s latest tightening in September – the 12th since March 2010 – comes in the wake of fears of a global recession and the possibility of debt defaults in some Eurozone countries. While some critics of the central bank say that the bank has been too slow in reacting to inflation and has not been bold enough with its rate increases, several others lament the rising cost of capital and falling domestic demand. While the debate regarding India’s monetary policy rages on, it is becoming increasingly likely that the Indian Government will not meet its fiscal deficit target for the year. While policymakers tinker with policy tools, the Indian economy is on course to achieve over 7% growth this fiscal year.

INFLATION STAYS HIGHInflation continues to be the key issue

for Indian policymakers. In a bold move to curb inflation, the central bank raised interest rates by 50 bps in July and by another 25 bps in September. Despite recent rate increases, inflation came in at over 9% in July and hit a 13-month high of 9.8% in August. Food inflation, despite hitting a 20-month low of 7.3% in July, settled at 9.1% in September. That food inflation continues to be an issue, despite a good harvest in the 2010-11 season and normal rainfall this year, is a clear indication that structural issues and supply-side bottlenecks that plague the Indian agricultural sector will remain for some time to come. Fuel inflation is beginning to exert upward pressure on headline inflation as well. While the inflationary impact of the rise in fuel prices is worrisome, what is interesting is the fact that the latest price increase was the result of the depreciating rupee against the dollar on imports of crude oil.

THE EXTERNAL SECTOR With policymakers wrestling to control inflation and sustain growth in the context of a weak global

economy, the rupee hit new lows as global funds chase better prospects for growth. The falling rupee is a serious cause of consternation for importers, oil companies included. At the same time, while one would normally expect a weaker rupee to benefit exporters, a shaky global recovery means exporters may not be able to take advantage of the opportunity for cost arbitrage in the coming months.

CONSUMPTION IS BAD, BUT INDUSTRY IS WORSEInterest rate hikes have finally begun to put the brakes on GDP growth in India. GDP growth for the first three months of 2011 came in at 7.8%, as compared to a growth of 9.4% in the corresponding quarter of 2010. Figures for the quarter that ended July further corroborate the slowdown in growth. GDP grew at 7.7% as compared to 8.8% the previous year. What is

surprising about

India:Trudging along,

for Now

O

not improved.Going forward, Japan continues to

face several downside risks despite the anticipated boost from reconstruction spending. The global economic

slowdown is the first among these risks as it will have a negative impact on export growth. Domestically, major challenges include a slower than expected revival of electricity generating

capacity, uncertainty about the future of Japan’s nuclear programme, political uncertainty, a continued high rate of savings, and long-term problems related to demographics.

J A N U A R Y 2 0 1 2 | SEARCH - THE INDUSTRIAL SOURCEBOOK 29

GLOBAL ECONOMIC OUTLOOK

data from the recent quarter is that investment increased almost 8%.

High interest rates, combined with a potential liquidity challenge in the second half of the year, could ensure that investment drops off once again as the year progresses. The Central Government recently announced that it will need to borrow 13% more than what it budgeted for the current fiscal year primarily due to a reduction in funds available through national savings accounts; there has been an exodus of funds from national saving accounts toward accounts in banks as they offer higher interest rates. This mopping up of funds from the market, although unlikely to add to the fiscal deficit, could crowd out investment from the private sector and increase the cost of borrowing for both government as well as private sector borrowers. However, the central bank is likely to be called upon to buy government bonds from the market in order to infuse

liquidity and this could, in turn, add to inflation.

Consumer demand has taken a hit, and growth in rate sensitive sectors has been weak in the last two quarters. Still, relatively speaking, domestic consumption is robust and is likely to act as a buffer for the economy in the event of further global economic turbulence. However, it is important to note that policymakers are currently grappling with high inflation.

Both the finance minister and the head of the central bank believe that current levels of food inflation are a matter of grave concern, and another hike in interest rates is a possibility. That being said, we could also be very close to the end of the rate increases. Until there is a clear indication that interest rates will stabilise, business confidence is likely to continue to drop. Private investment is expected to slow down in the coming months as well.

A LOOK AHEADThe challenges that face Indian policymakers are, to a large extent, the same as they were a year ago. Inflation shows no signs of abating, and another interest rate hike is a possibility, but the end of the cycle of rate increases is probably very close. Consumer demand is likely to continue to slow down as monetary policy kicks in with some lag. Consequently, GDP growth may slow down further and may hover around 7.5% for the current fiscal year. The fiscal deficit is unlikely to meet the target level of 4.6% of GDP. Since a significant portion of the deficit is funded through funds from the central bank, money supply in the economy will continue to increase and exert upward pressure on inflation.

The article is an excerpt from ‘Navigating An

Uncertain Global Environment’ by IMF &

Deloitte Global Economic Outlook, 4th Quarter

2011.

30 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

RANKING METHODOLOGY

TOP 500TOP 500Uncertain global economic conditions coupled with rising infl ationary trends are posing a threat to India Inc.’s stupendous growth journey. Withstanding such external as well as internal shocks is our pack of Top 500 Manufacturing Companies who have demonstrated to the world their mettle & might in true sense & spirit. Notably so, ranking these companies while taking all the fundamental aspects into consideration can never be an easy feat. Carefully crafting the most transparent methodology, we trace the inspirational journey of India Inc.’s most sought after manufacturing companies…

he l ist ing and analysis of the Top 500 Manufacturing Companies is an ode to those, who, by virtue of

their grit & determination, have set enviable benchmarks when it comes to not only the financial performance, but also imbibing societal values and ethics. These are the companies who believe in leading by examples and setting milestones for emerging companies. In order to ensure a just & fair ranking, utmost care was taken while developing a step-by-step approach by taking each and every parameter into consideration. The process is as follows:

SELECTION CRITERIAThe classification of manufacturing companies from non-manufacturing companies is based on “The Central Excise Tariff Act 1985”. Also, companies wherein their core business activities do not contribute to excise payments have been excluded. However, the manufacturing companies with operation set up in excise exemption zones like SEZs and EPZs have been considered. Only the entities listed on BSE or NSE have been considered.

CLASSIFICATION & ASSUMPTIONSThe ranking is based on the consolidated results of the company. In cases, where the company does not have any subsidiary or latest data for consolidated results are not available,

the standalone results are assumed as consolidated results. The listed subsidiaries of the company qualifying the ranking criteria as detailed above have been excluded. Those companies having negative shareholder’s funds have also been excluded. The ratios as well as other company financials in absolute terms have been sourced through the database – CMIE Prowess. For the purpose of ranking, the annual financials of the companies has been sourced as available in the said database uptill December 4, 2011.

A STEP-WISE APPROACHStep 1: A two-tier weighting methodology was used to rank the companies. Step 2: Based on parameters selected and weightage specified for the same, ranking for each group was arrived at.Step 3: Each group was assigned a specific weightage to arrive at a weighted value for consolidating said values from all four groups.Step 4: The summation of weighted values for all four groups was then sorted in descending order to arrive at the final ranking.

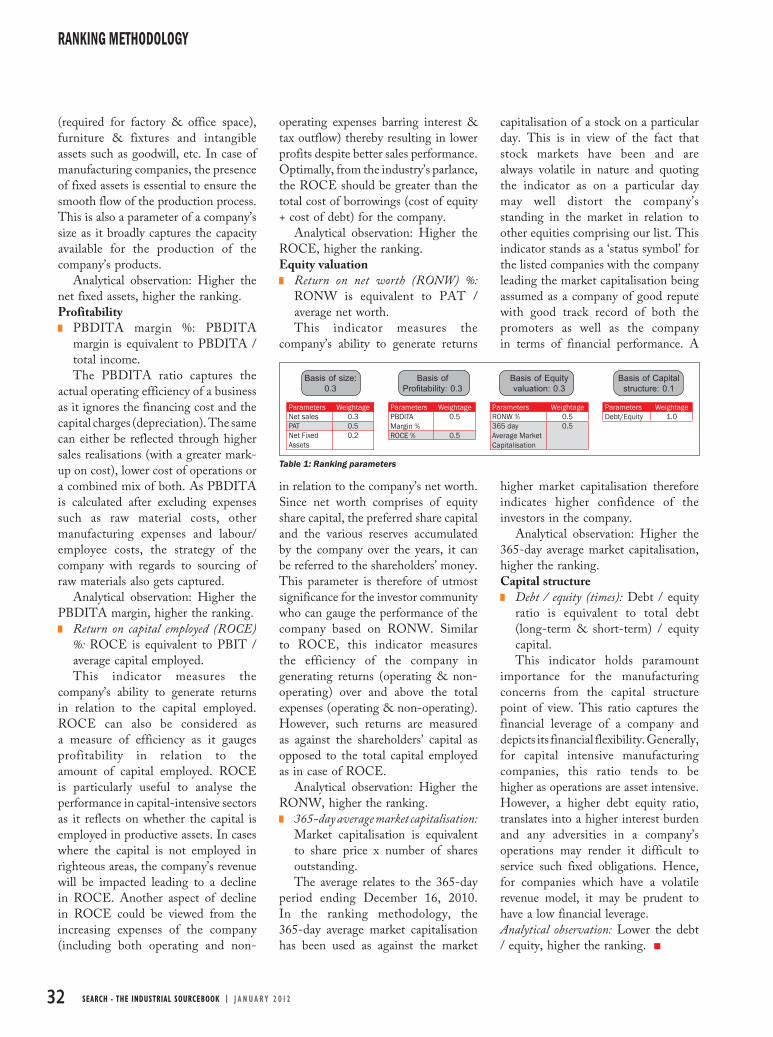

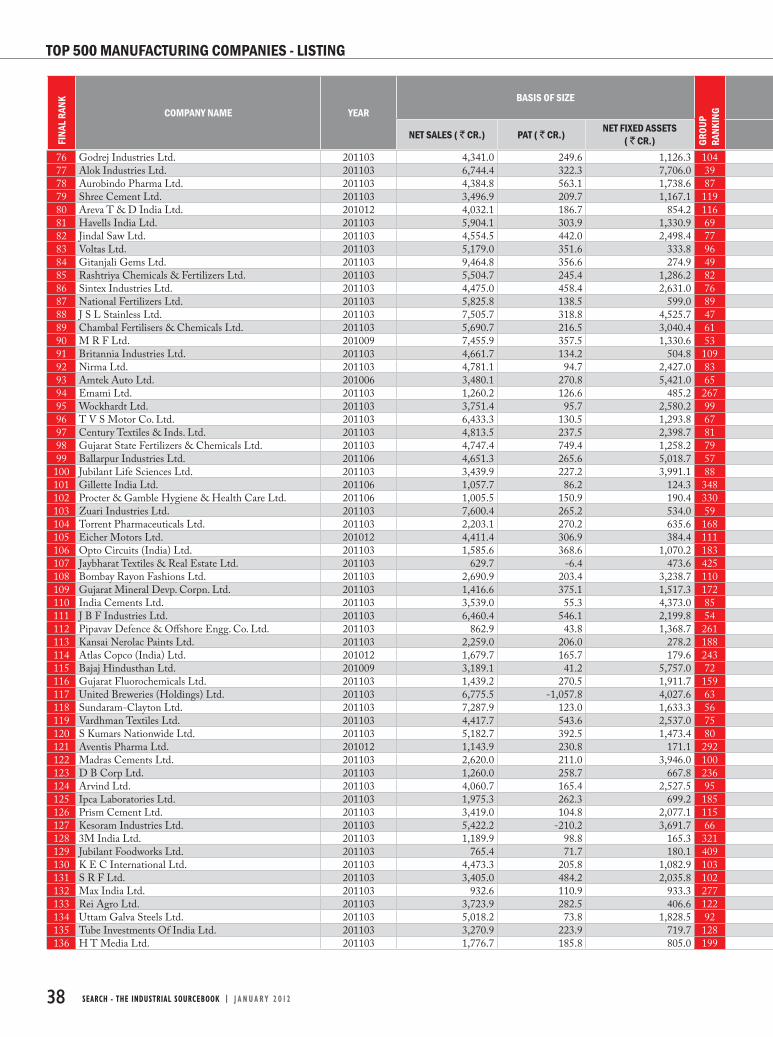

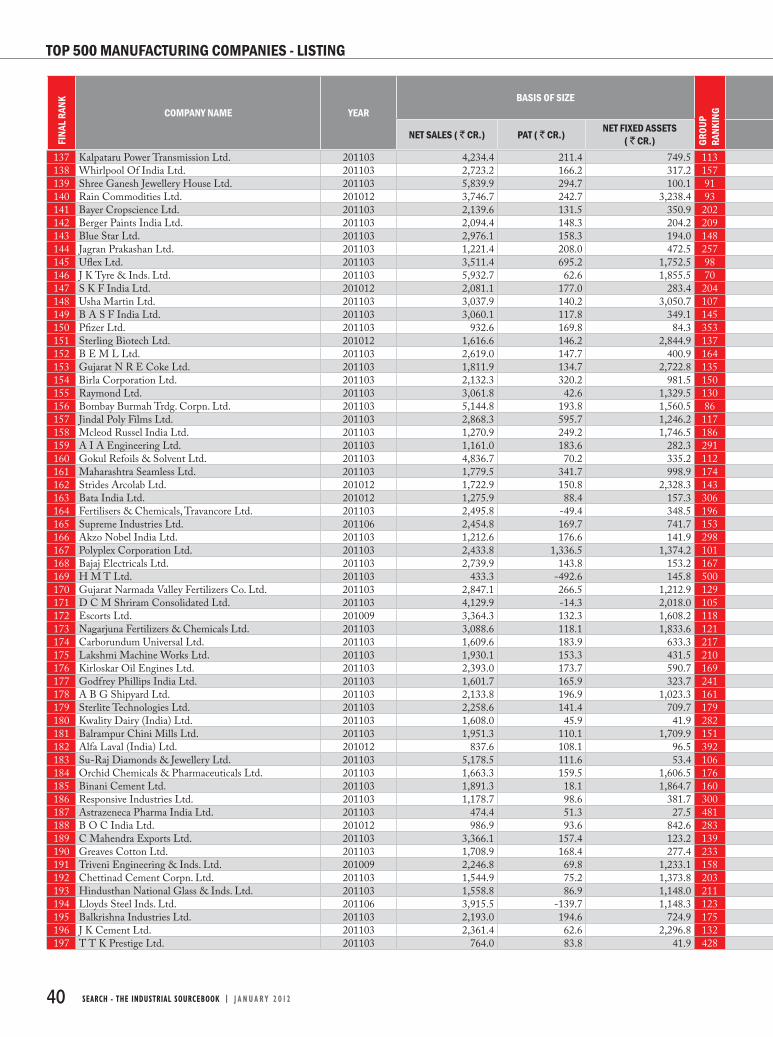

The relevance of selection of the parameters with the weightage so appropriated has been detailed below. Size Net sales: Net sales is equivalent to

the sales of goods – excise duty paid. Any manufacturing concern is

primarily recognised by its size and the same can well be reflected through the company’s sales activity. Herein, ‘net sales’ has been preferred over ‘gross sales’ as the latter includes collection of excise duty from customers as applicable to the company’s products. Thus, a higher levy of excise duty for the company’s products would inflate the company’s gross sales. The net sales figure ignores the levy of excise and reflects the value of goods sold with a mark-up on cost.

Analytical observation: Higher the sales, higher the ranking. Profit after tax (PAT): PAT is

equivalent to PBDITA – Depreciation – Interest – Tax paid.PAT value determines earnings of

the company post operating expenses, interest, depreciation, other non-operating expenses & tax. It reflects the company’s ability to recover its overall expenses (operating as well as non-operating) through a mark-up on the cost of goods manufactured. A company registering high sales, but still recording negative PAT figures is probably not prospering as the expenses are still left unrecovered.

Analytical observation: Higher the PAT, higher the ranking. Net Fixed Assets: Net fixed assets is

equivalent to gross fixed assets – depreciation. This reflects the book value of assets

owned by the company in the form of plants & equipment, land & buildings

T

Deciphering the

Manufacturing CompaniesManufacturing CompaniesTOP 500TOP 500

32 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

RANKING METHODOLOGY

(required for factory & office space), furniture & fixtures and intangible assets such as goodwill, etc. In case of manufacturing companies, the presence of fixed assets is essential to ensure the smooth flow of the production process. This is also a parameter of a company’s size as it broadly captures the capacity available for the production of the company’s products.

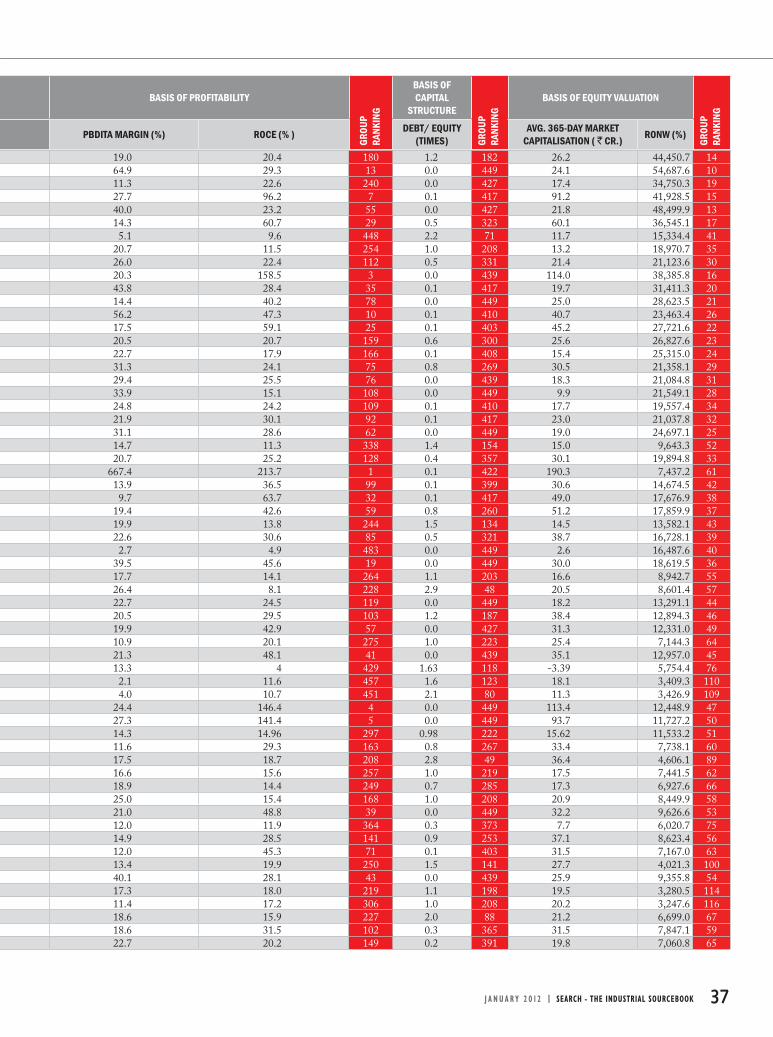

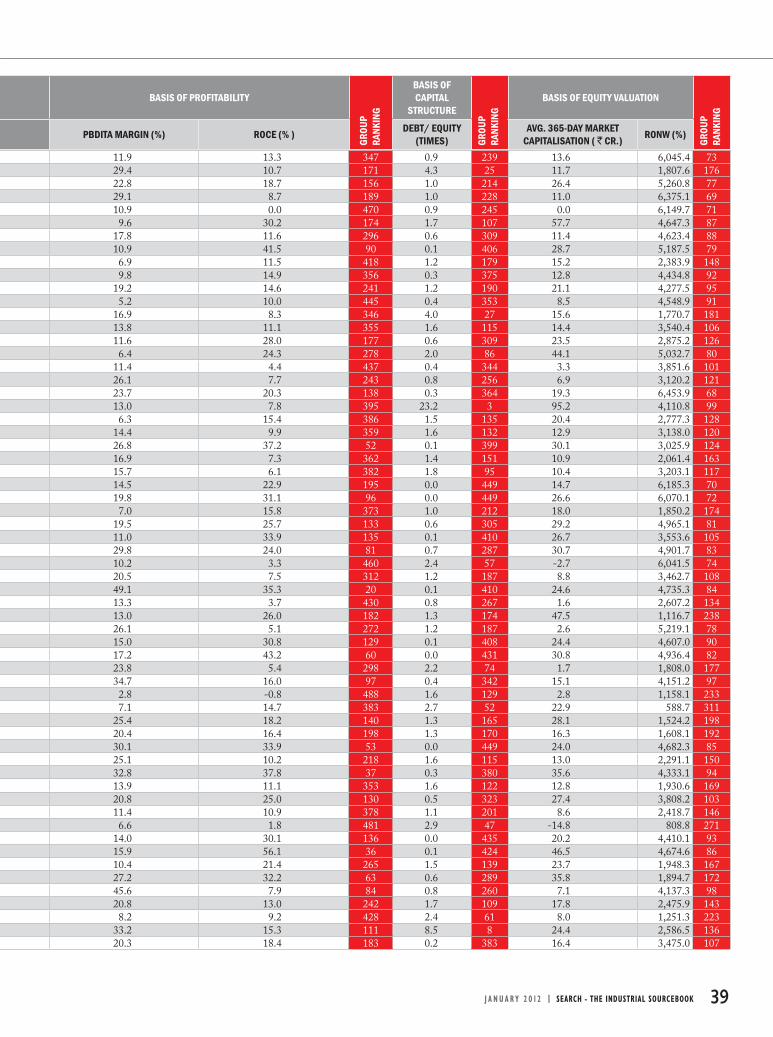

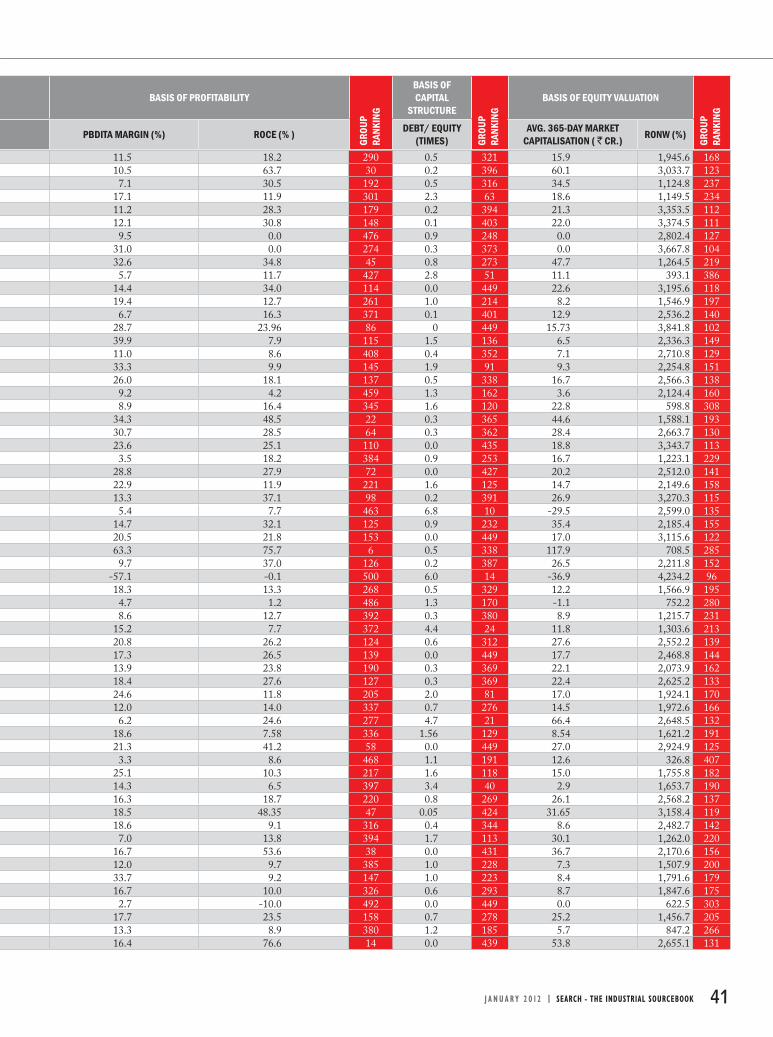

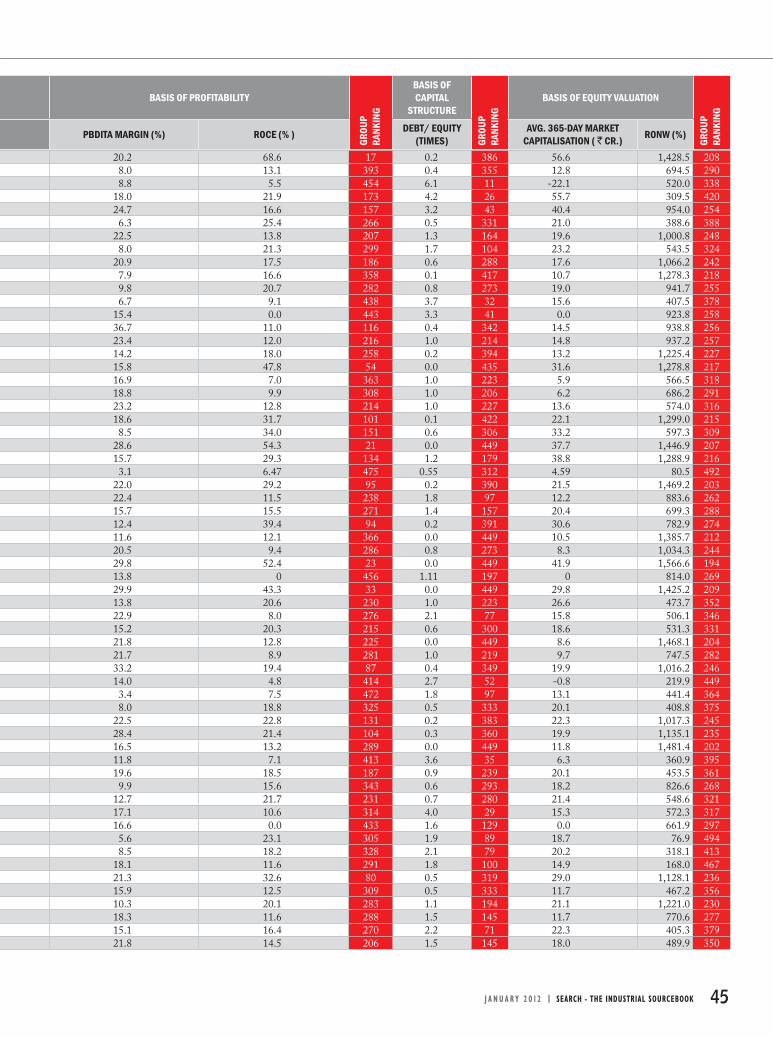

Analytical observation: Higher the net fixed assets, higher the ranking.Profitability PBDITA margin %: PBDITA

margin is equivalent to PBDITA / total income. The PBDITA ratio captures the

actual operating efficiency of a business as it ignores the financing cost and the capital charges (depreciation). The same can either be reflected through higher sales realisations (with a greater mark-up on cost), lower cost of operations or a combined mix of both. As PBDITA is calculated after excluding expenses such as raw material costs, other manufacturing expenses and labour/employee costs, the strategy of the company with regards to sourcing of raw materials also gets captured.

Analytical observation: Higher the PBDITA margin, higher the ranking. Return on capital employed (ROCE)

%: ROCE is equivalent to PBIT / average capital employed. This indicator measures the

company’s ability to generate returns in relation to the capital employed. ROCE can also be considered as a measure of efficiency as it gauges profitability in relation to the amount of capital employed. ROCE is particularly useful to analyse the performance in capital-intensive sectors as it reflects on whether the capital is employed in productive assets. In cases where the capital is not employed in righteous areas, the company’s revenue will be impacted leading to a decline in ROCE. Another aspect of decline in ROCE could be viewed from the increasing expenses of the company (including both operating and non-

operating expenses barring interest & tax outflow) thereby resulting in lower profits despite better sales performance. Optimally, from the industry’s parlance, the ROCE should be greater than the total cost of borrowings (cost of equity + cost of debt) for the company.

Analytical observation: Higher the ROCE, higher the ranking.Equity valuation Return on net worth (RONW) %:

RONW is equivalent to PAT / average net worth. This indicator measures the

company’s ability to generate returns

in relation to the company’s net worth. Since net worth comprises of equity share capital, the preferred share capital and the various reserves accumulated by the company over the years, it can be referred to the shareholders’ money. This parameter is therefore of utmost significance for the investor community who can gauge the performance of the company based on RONW. Similar to ROCE, this indicator measures the efficiency of the company in generating returns (operating & non-operating) over and above the total expenses (operating & non-operating). However, such returns are measured as against the shareholders’ capital as opposed to the total capital employed as in case of ROCE.

Analytical observation: Higher the RONW, higher the ranking. 365-day average market capitalisation:

Market capitalisation is equivalent to share price x number of shares outstanding.The average relates to the 365-day

period ending December 16, 2010. In the ranking methodology, the 365-day average market capitalisation has been used as against the market

capitalisation of a stock on a particular day. This is in view of the fact that stock markets have been and are always volatile in nature and quoting the indicator as on a particular day may well distort the company’s standing in the market in relation to other equities comprising our list. This indicator stands as a ‘status symbol’ for the listed companies with the company leading the market capitalisation being assumed as a company of good repute with good track record of both the promoters as well as the company in terms of financial performance. A

higher market capitalisation therefore indicates higher confidence of the investors in the company.

Analytical observation: Higher the 365-day average market capitalisation, higher the ranking.Capital structure Debt / equity (times): Debt / equity

ratio is equivalent to total debt (long-term & short-term) / equity capital. This indicator holds paramount

importance for the manufacturing concerns from the capital structure point of view. This ratio captures the financial leverage of a company and depicts its financial flexibility. Generally, for capital intensive manufacturing companies, this ratio tends to be higher as operations are asset intensive. However, a higher debt equity ratio, translates into a higher interest burden and any adversities in a company’s operations may render it difficult to service such fixed obligations. Hence, for companies which have a volatile revenue model, it may be prudent to have a low financial leverage. Analytical observation: Lower the debt / equity, higher the ranking.

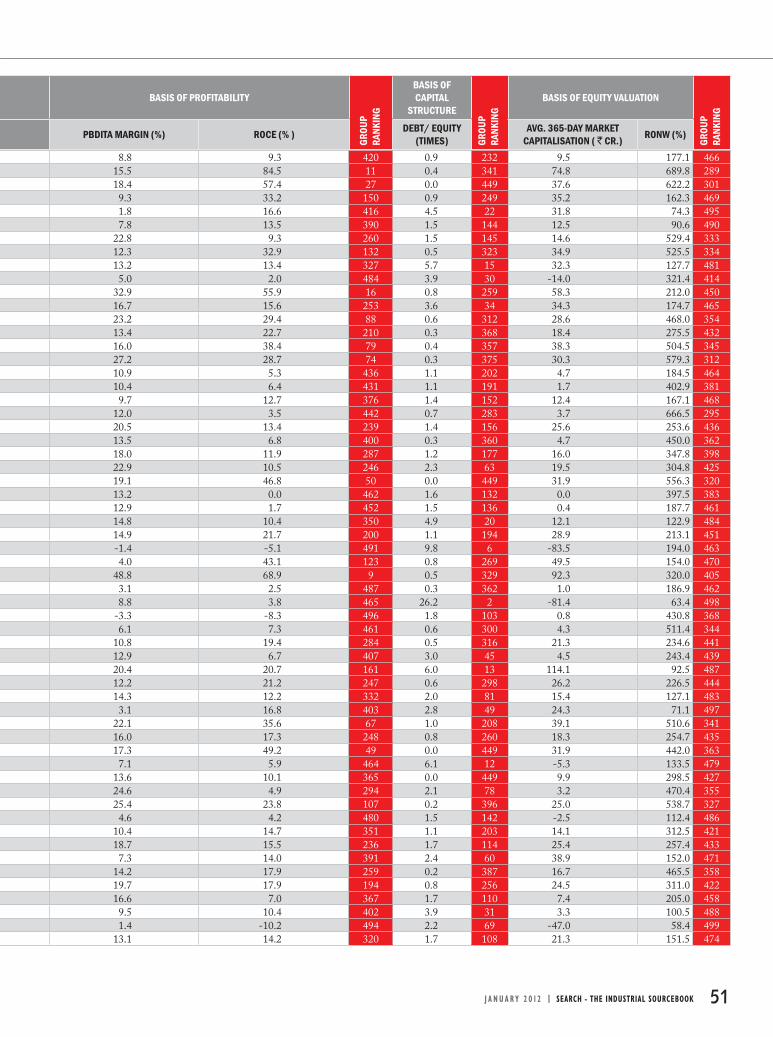

Basis of size: 0.3

Basis of Profitability: 0.3

Basis of Equity valuation: 0.3

Basis of Capital structure: 0.1

Parameters WeightageNet sales 0.3PAT 0.5Net Fixed Assets

0.2

Parameters WeightagePBDITA Margin %

0.5

ROCE % 0.5

Parameters WeightageRONW % 0.5365 day Average Market Capitalisation

0.5

Parameters WeightageDebt/Equity 1.0

Table 1: Ranking parameters

34 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

Disclaimer:This ranking is prepared by CARE Research, a division of Credit Analysis & REsearch (CARE). CARE Research has taken utmost care to ensure accuracy and objectivity while developing this ranking based on information available in public domain. The data pertaining to the companies so ranked has been sourced through Prowess database. However, neither the accuracy nor completeness of information contained in this ranking is guaranteed. CARE Research operates independently of ratings division and this ranking does not contain any confi dential information obtained by ratings division, which they may have obtained in the regular course of operations. The opinion expressed in this ranking cannot be compared to the rating assigned to the company within this industry by the ratings division. The opinion expressed is also not a

14TOP

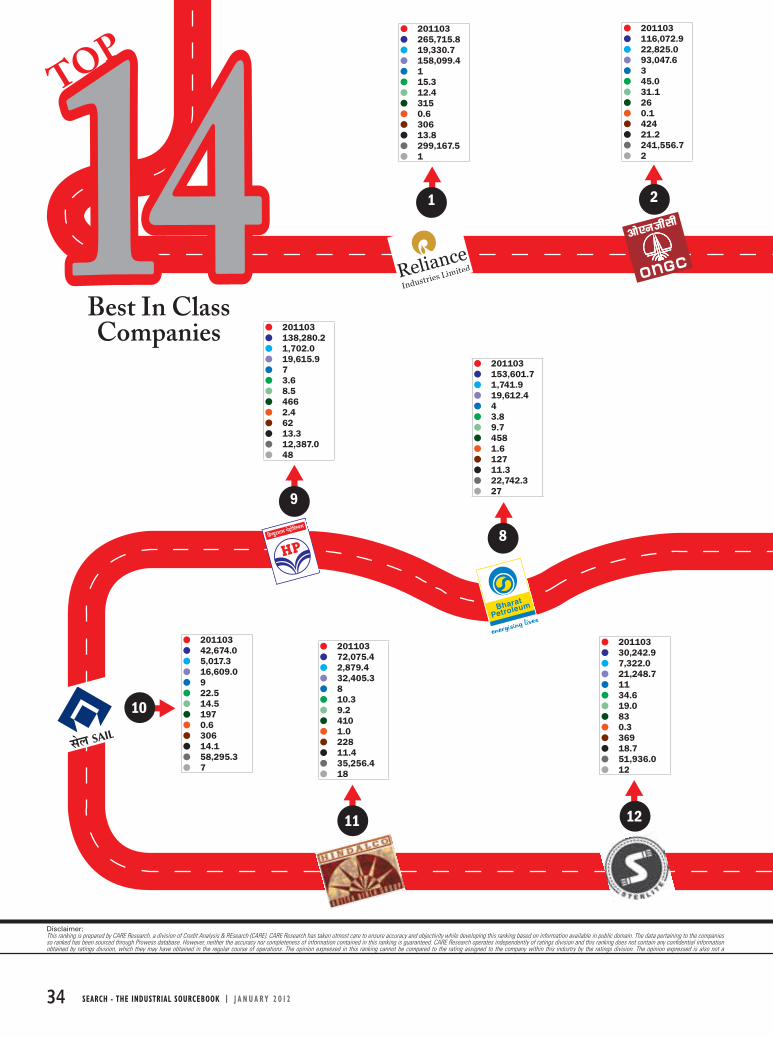

Best In Class Companies

201103265,715.819,330.7158,099.4115.312.43150.630613.8299,167.51

201103116,072.922,825.093,047.6345.031.1260.142421.2241,556.72

201103 153,601.7 1,741.9 19,612.4 4 3.8 9.7 458 1.6 127 11.3 22,742.3 27

201103 138,280.2 1,702.0 19,615.9 7 3.6 8.5 466 2.4 62 13.3 12,387.0 48

201103 42,674.0 5,017.3 16,609.0 9 22.5 14.5 197 0.6 306 14.1 58,295.3 7

201103 72,075.4 2,879.4 32,405.3 8 10.3 9.2 410 1.0 228 11.4 35,256.4 18

201103 30,242.9 7,322.0 21,248.7 11 34.6 19.0 83 0.3 369 18.7 51,936.0 12

2

8

9

10

11 12

1414 1

J A N U A R Y 2 0 1 2 | SEARCH - THE INDUSTRIAL SOURCEBOOK 35

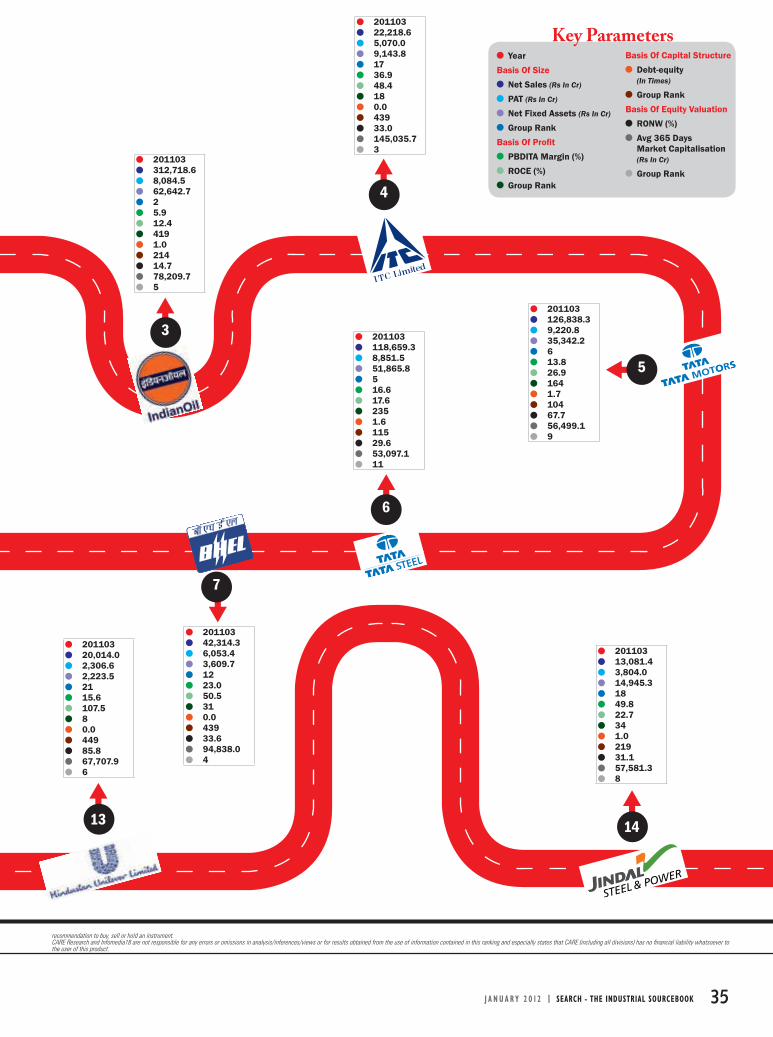

recommendation to buy, sell or hold an instrument.CARE Research and Infomedia18 are not responsible for any errors or omissions in analysis/inferences/views or for results obtained from the use of information contained in this ranking and especially states that CARE (including all divisions) has no fi nancial liability whatsoever to the user of this product.

201103 312,718.6 8,084.5 62,642.7 2 5.9 12.4 419 1.0 214 14.7 78,209.7 5

201103 22,218.6 5,070.0 9,143.8 17 36.9 48.4 18 0.0 439 33.0 145,035.7 3

201103 126,838.3 9,220.8 35,342.2 6 13.8 26.9 164 1.7 104 67.7 56,499.1 9

201103 118,659.3 8,851.5 51,865.8 5 16.6 17.6 235 1.6 115 29.6 53,097.1 11

201103 42,314.3 6,053.4 3,609.7 12 23.0 50.5 31 0.0 439 33.6 94,838.0 4

201103 13,081.4 3,804.0 14,945.3 18 49.8 22.7 34 1.0 219 31.1 57,581.3 8

Year

Basis Of Size

Net Sales (Rs In Cr)

PAT (Rs In Cr)

Net Fixed Assets (Rs In Cr)

Group Rank

Basis Of Profi t

PBDITA Margin (%)

ROCE (%)

Group Rank

Basis Of Capital Structure

Debt-equity (In Times)

Group Rank

Basis Of Equity Valuation

RONW (%)

Avg 365 Days Market Capitalisation (Rs In Cr)

Group Rank

Key Parameters

201103 20,014.0 2,306.6 2,223.5 21 15.6 107.5 8 0.0 449 85.8 67,707.9 6

3

4

6

7

13 14

5

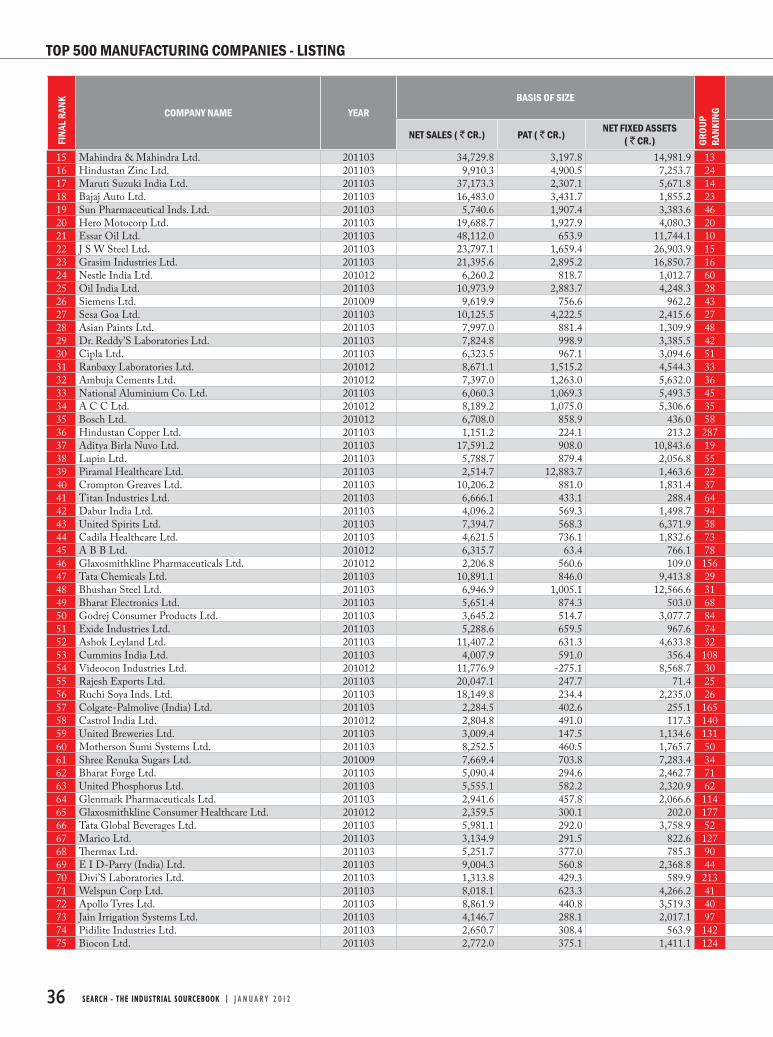

COMPANY NAME YEARBASIS OF SIZE

NET SALES ( ` CR.) PAT ( ` CR.) NET FIXED ASSETS( ` CR.)

36 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

FINA

L RAN

K

GROU

P RA

NKIN

G

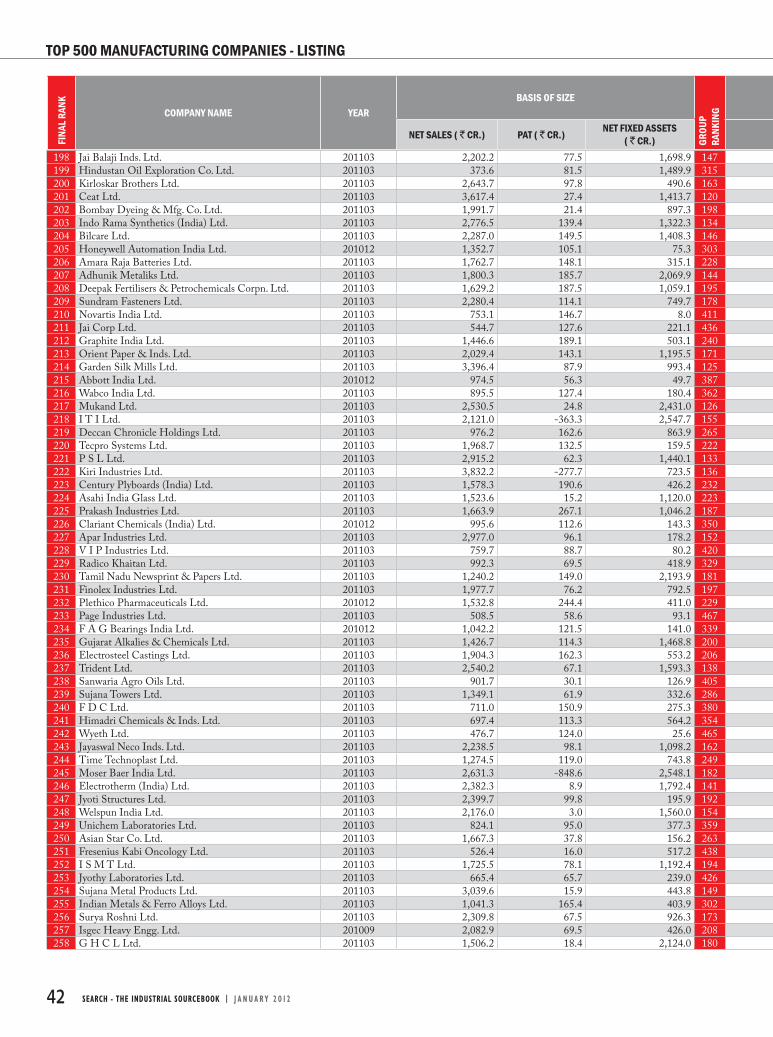

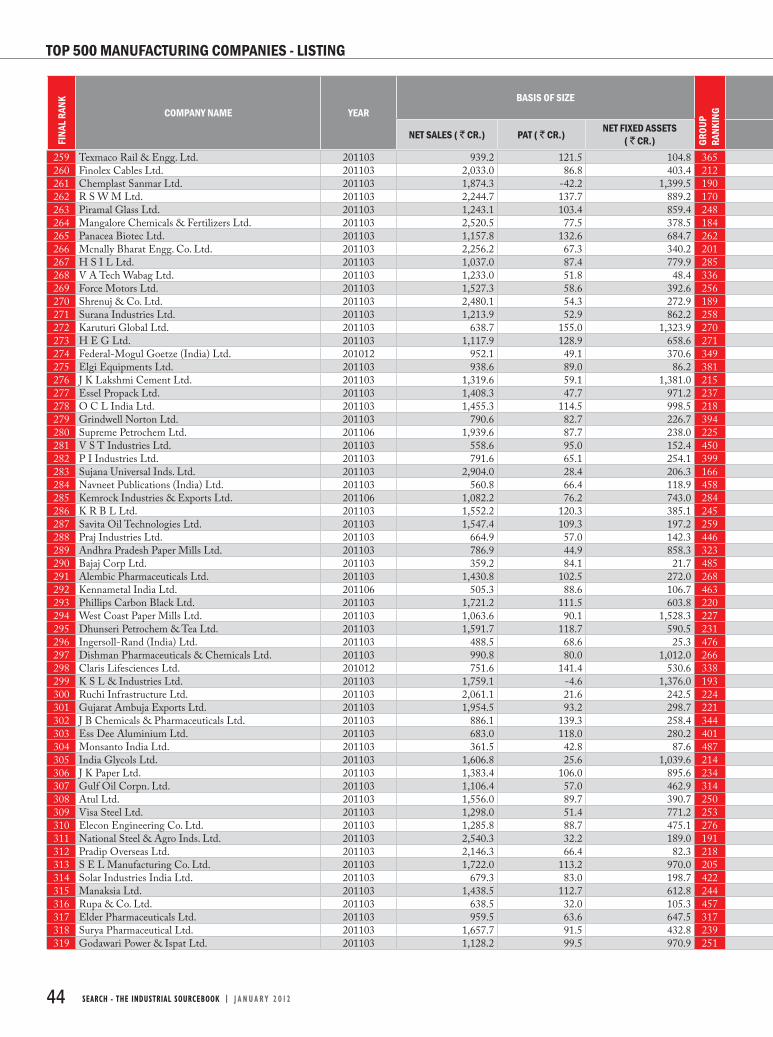

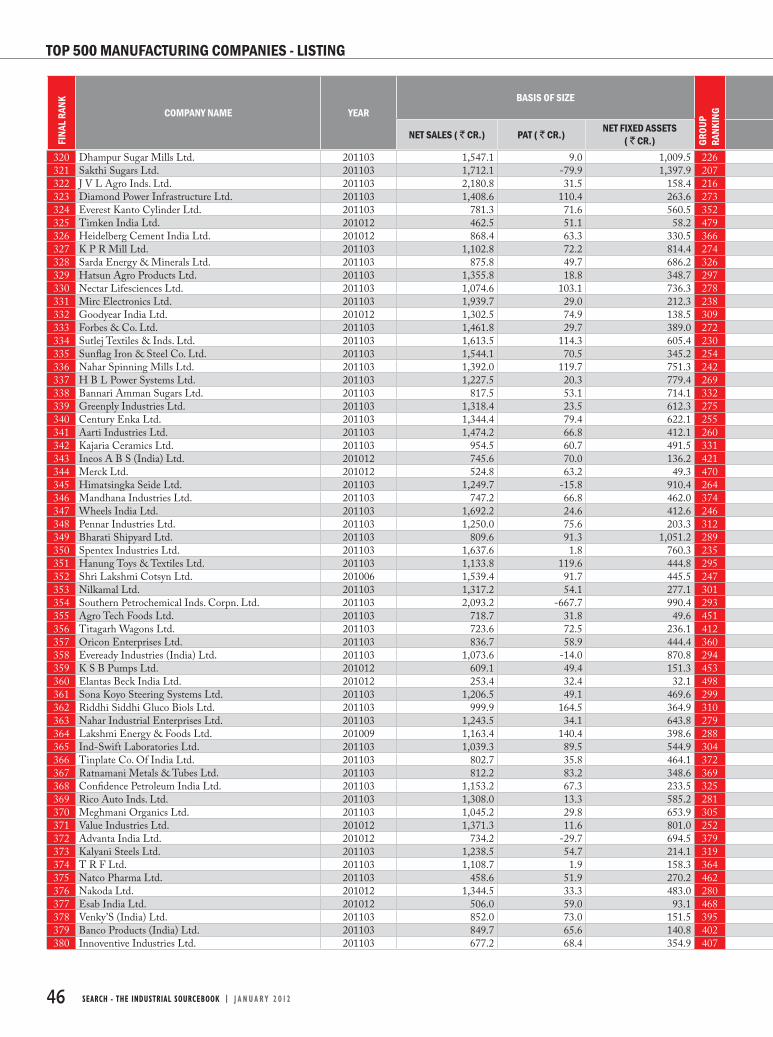

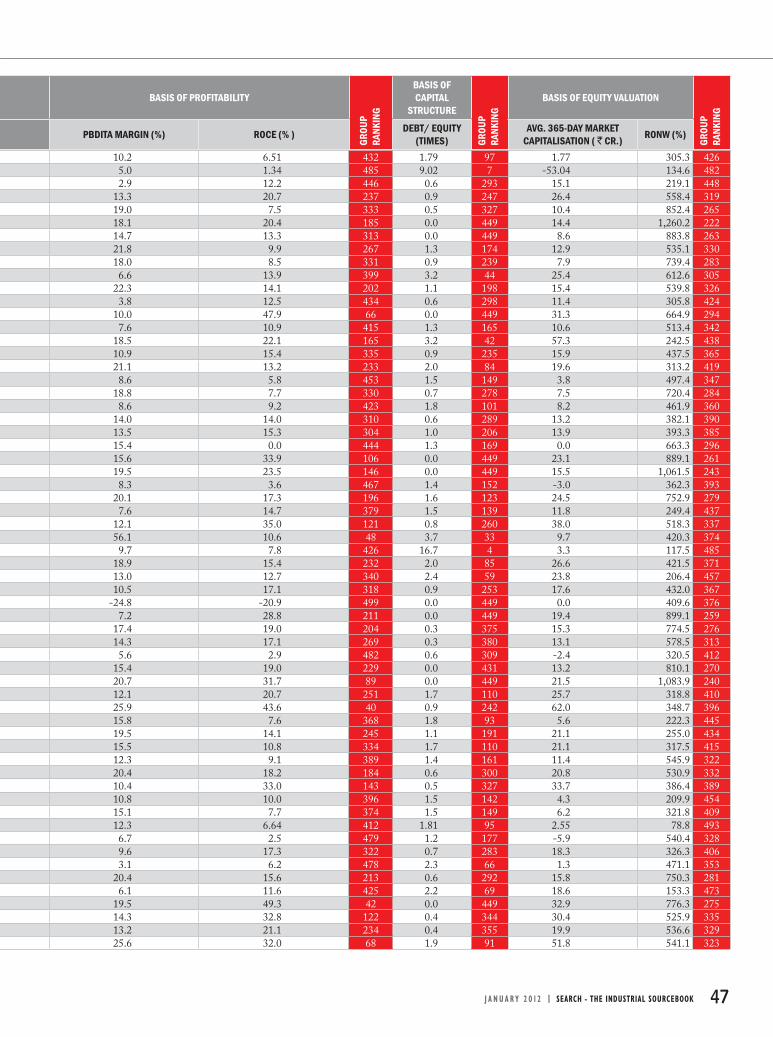

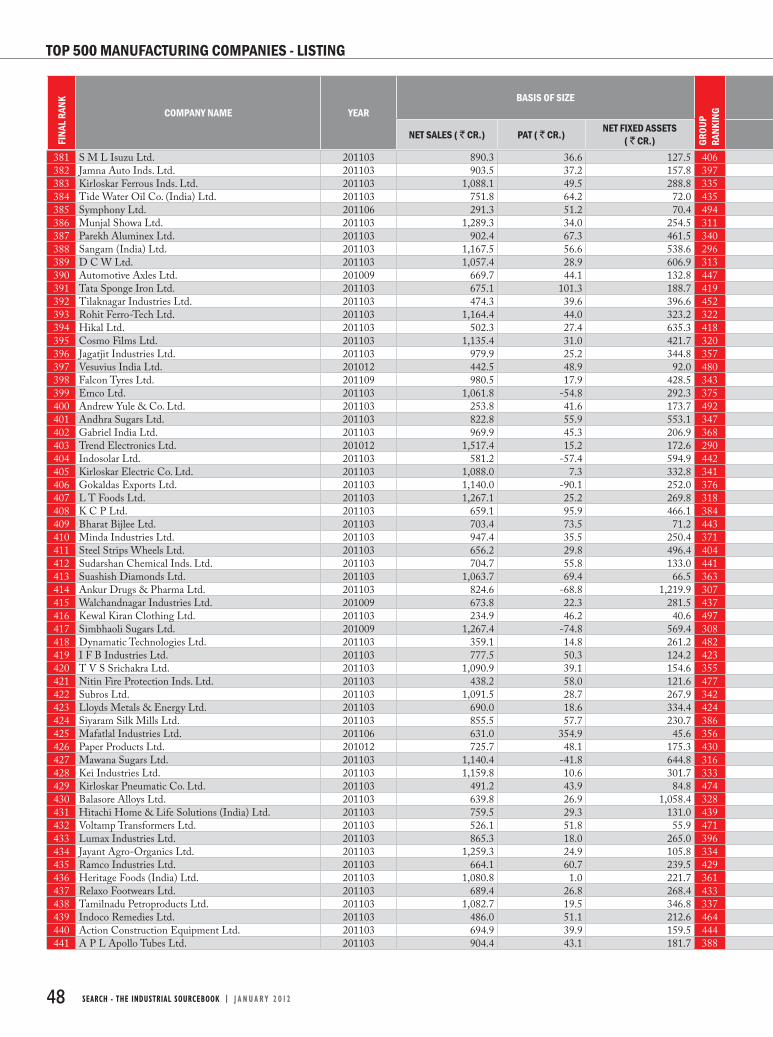

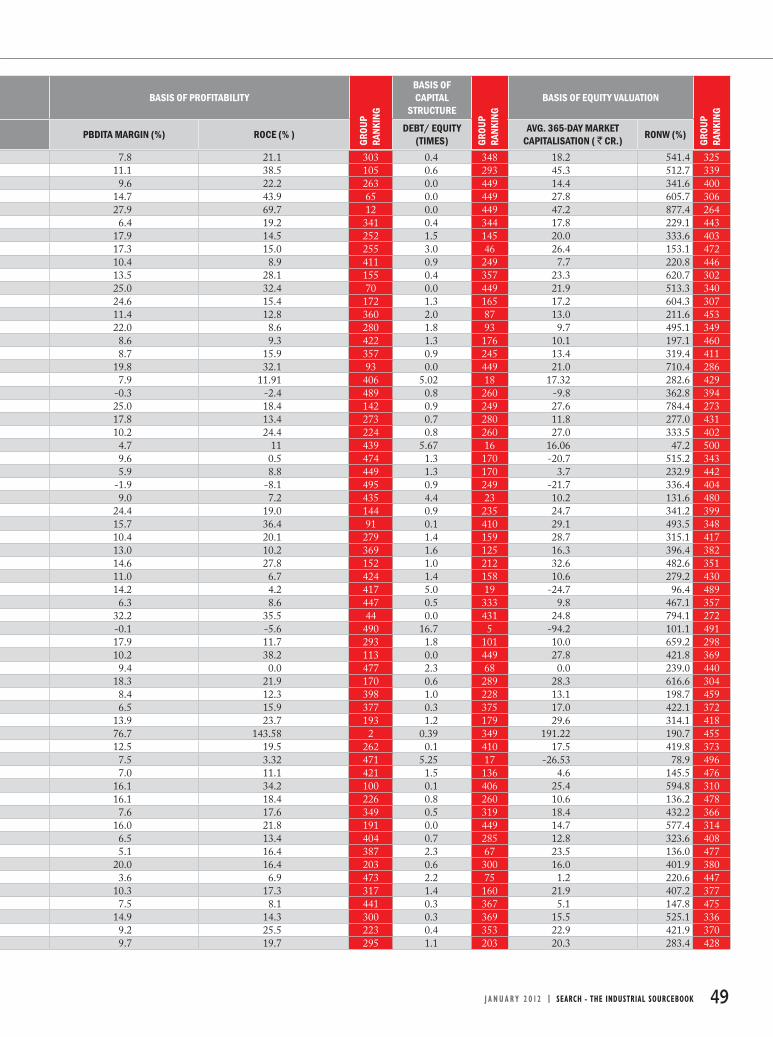

TOP 500 MANUFACTURING COMPANIES - LISTING

15 Mahindra & Mahindra Ltd. 201103 34,729.8 3,197.8 14,981.9 1316 Hindustan Zinc Ltd. 201103 9,910.3 4,900.5 7,253.7 2417 Maruti Suzuki India Ltd. 201103 37,173.3 2,307.1 5,671.8 1418 Bajaj Auto Ltd. 201103 16,483.0 3,431.7 1,855.2 2319 Sun Pharmaceutical Inds. Ltd. 201103 5,740.6 1,907.4 3,383.6 4620 Hero Motocorp Ltd. 201103 19,688.7 1,927.9 4,080.3 2021 Essar Oil Ltd. 201103 48,112.0 653.9 11,744.1 1022 J S W Steel Ltd. 201103 23,797.1 1,659.4 26,903.9 1523 Grasim Industries Ltd. 201103 21,395.6 2,895.2 16,850.7 1624 Nestle India Ltd. 201012 6,260.2 818.7 1,012.7 6025 Oil India Ltd. 201103 10,973.9 2,883.7 4,248.3 2826 Siemens Ltd. 201009 9,619.9 756.6 962.2 4327 Sesa Goa Ltd. 201103 10,125.5 4,222.5 2,415.6 2728 Asian Paints Ltd. 201103 7,997.0 881.4 1,309.9 4829 Dr. Reddy’S Laboratories Ltd. 201103 7,824.8 998.9 3,385.5 4230 Cipla Ltd. 201103 6,323.5 967.1 3,094.6 5131 Ranbaxy Laboratories Ltd. 201012 8,671.1 1,515.2 4,544.3 3332 Ambuja Cements Ltd. 201012 7,397.0 1,263.0 5,632.0 3633 National Aluminium Co. Ltd. 201103 6,060.3 1,069.3 5,493.5 4534 A C C Ltd. 201012 8,189.2 1,075.0 5,306.6 3535 Bosch Ltd. 201012 6,708.0 858.9 436.0 5836 Hindustan Copper Ltd. 201103 1,151.2 224.1 213.2 28737 Aditya Birla Nuvo Ltd. 201103 17,591.2 908.0 10,843.6 1938 Lupin Ltd. 201103 5,788.7 879.4 2,056.8 5539 Piramal Healthcare Ltd. 201103 2,514.7 12,883.7 1,463.6 2240 Crompton Greaves Ltd. 201103 10,206.2 881.0 1,831.4 3741 Titan Industries Ltd. 201103 6,666.1 433.1 288.4 6442 Dabur India Ltd. 201103 4,096.2 569.3 1,498.7 9443 United Spirits Ltd. 201103 7,394.7 568.3 6,371.9 3844 Cadila Healthcare Ltd. 201103 4,621.5 736.1 1,832.6 7345 A B B Ltd. 201012 6,315.7 63.4 766.1 7846 Glaxosmithkline Pharmaceuticals Ltd. 201012 2,206.8 560.6 109.0 15647 Tata Chemicals Ltd. 201103 10,891.1 846.0 9,413.8 2948 Bhushan Steel Ltd. 201103 6,946.9 1,005.1 12,566.6 3149 Bharat Electronics Ltd. 201103 5,651.4 874.3 503.0 6850 Godrej Consumer Products Ltd. 201103 3,645.2 514.7 3,077.7 8451 Exide Industries Ltd. 201103 5,288.6 659.5 967.6 7452 Ashok Leyland Ltd. 201103 11,407.2 631.3 4,633.8 3253 Cummins India Ltd. 201103 4,007.9 591.0 356.4 10854 Videocon Industries Ltd. 201012 11,776.9 -275.1 8,568.7 3055 Rajesh Exports Ltd. 201103 20,047.1 247.7 71.4 2556 Ruchi Soya Inds. Ltd. 201103 18,149.8 234.4 2,235.0 2657 Colgate-Palmolive (India) Ltd. 201103 2,284.5 402.6 255.1 16558 Castrol India Ltd. 201012 2,804.8 491.0 117.3 14059 United Breweries Ltd. 201103 3,009.4 147.5 1,134.6 13160 Motherson Sumi Systems Ltd. 201103 8,252.5 460.5 1,765.7 5061 Shree Renuka Sugars Ltd. 201009 7,669.4 703.8 7,283.4 3462 Bharat Forge Ltd. 201103 5,090.4 294.6 2,462.7 7163 United Phosphorus Ltd. 201103 5,555.1 582.2 2,320.9 6264 Glenmark Pharmaceuticals Ltd. 201103 2,941.6 457.8 2,066.6 11465 Glaxosmithkline Consumer Healthcare Ltd. 201012 2,359.5 300.1 202.0 17766 Tata Global Beverages Ltd. 201103 5,981.1 292.0 3,758.9 5267 Marico Ltd. 201103 3,134.9 291.5 822.6 12768 Th ermax Ltd. 201103 5,251.7 377.0 785.3 9069 E I D-Parry (India) Ltd. 201103 9,004.3 560.8 2,368.8 4470 Divi’S Laboratories Ltd. 201103 1,313.8 429.3 589.9 21371 Welspun Corp Ltd. 201103 8,018.1 623.3 4,266.2 4172 Apollo Tyres Ltd. 201103 8,861.9 440.8 3,519.3 4073 Jain Irrigation Systems Ltd. 201103 4,146.7 288.1 2,017.1 9774 Pidilite Industries Ltd. 201103 2,650.7 308.4 563.9 14275 Biocon Ltd. 201103 2,772.0 375.1 1,411.1 124

BASIS OF PROFITABILITYBASIS OF CAPITAL

STRUCTUREBASIS OF EQUITY VALUATION

PBDITA MARGIN (%) ROCE (% ) DEBT/ EQUITY (TIMES)

AVG. 365-DAY MARKET CAPITALISATION ( ` CR.) RONW (%)

J A N U A R Y 2 0 1 2 | SEARCH - THE INDUSTRIAL SOURCEBOOK 37

GROU

P RA

NKIN

G

GROU

P RA

NKIN

G

GROU

P RA

NKIN

G

19.0 20.4 180 1.2 182 26.2 44,450.7 1464.9 29.3 13 0.0 449 24.1 54,687.6 1011.3 22.6 240 0.0 427 17.4 34,750.3 1927.7 96.2 7 0.1 417 91.2 41,928.5 1540.0 23.2 55 0.0 427 21.8 48,499.9 1314.3 60.7 29 0.5 323 60.1 36,545.1 175.1 9.6 448 2.2 71 11.7 15,334.4 41

20.7 11.5 254 1.0 208 13.2 18,970.7 3526.0 22.4 112 0.5 331 21.4 21,123.6 3020.3 158.5 3 0.0 439 114.0 38,385.8 1643.8 28.4 35 0.1 417 19.7 31,411.3 2014.4 40.2 78 0.0 449 25.0 28,623.5 2156.2 47.3 10 0.1 410 40.7 23,463.4 2617.5 59.1 25 0.1 403 45.2 27,721.6 2220.5 20.7 159 0.6 300 25.6 26,827.6 2322.7 17.9 166 0.1 408 15.4 25,315.0 2431.3 24.1 75 0.8 269 30.5 21,358.1 2929.4 25.5 76 0.0 439 18.3 21,084.8 3133.9 15.1 108 0.0 449 9.9 21,549.1 2824.8 24.2 109 0.1 410 17.7 19,557.4 3421.9 30.1 92 0.1 417 23.0 21,037.8 3231.1 28.6 62 0.0 449 19.0 24,697.1 2514.7 11.3 338 1.4 154 15.0 9,643.3 5220.7 25.2 128 0.4 357 30.1 19,894.8 33

667.4 213.7 1 0.1 422 190.3 7,437.2 6113.9 36.5 99 0.1 399 30.6 14,674.5 429.7 63.7 32 0.1 417 49.0 17,676.9 38

19.4 42.6 59 0.8 260 51.2 17,859.9 3719.9 13.8 244 1.5 134 14.5 13,582.1 4322.6 30.6 85 0.5 321 38.7 16,728.1 392.7 4.9 483 0.0 449 2.6 16,487.6 40

39.5 45.6 19 0.0 449 30.0 18,619.5 3617.7 14.1 264 1.1 203 16.6 8,942.7 5526.4 8.1 228 2.9 48 20.5 8,601.4 5722.7 24.5 119 0.0 449 18.2 13,291.1 4420.5 29.5 103 1.2 187 38.4 12,894.3 4619.9 42.9 57 0.0 427 31.3 12,331.0 4910.9 20.1 275 1.0 223 25.4 7,144.3 6421.3 48.1 41 0.0 439 35.1 12,957.0 4513.3 4 429 1.63 118 -3.39 5,754.4 762.1 11.6 457 1.6 123 18.1 3,409.3 1104.0 10.7 451 2.1 80 11.3 3,426.9 109

24.4 146.4 4 0.0 449 113.4 12,448.9 4727.3 141.4 5 0.0 449 93.7 11,727.2 5014.3 14.96 297 0.98 222 15.62 11,533.2 5111.6 29.3 163 0.8 267 33.4 7,738.1 6017.5 18.7 208 2.8 49 36.4 4,606.1 8916.6 15.6 257 1.0 219 17.5 7,441.5 6218.9 14.4 249 0.7 285 17.3 6,927.6 6625.0 15.4 168 1.0 208 20.9 8,449.9 5821.0 48.8 39 0.0 449 32.2 9,626.6 5312.0 11.9 364 0.3 373 7.7 6,020.7 7514.9 28.5 141 0.9 253 37.1 8,623.4 5612.0 45.3 71 0.1 403 31.5 7,167.0 6313.4 19.9 250 1.5 141 27.7 4,021.3 10040.1 28.1 43 0.0 439 25.9 9,355.8 5417.3 18.0 219 1.1 198 19.5 3,280.5 11411.4 17.2 306 1.0 208 20.2 3,247.6 11618.6 15.9 227 2.0 88 21.2 6,699.0 6718.6 31.5 102 0.3 365 31.5 7,847.1 5922.7 20.2 149 0.2 391 19.8 7,060.8 65

COMPANY NAME YEARBASIS OF SIZE

NET SALES ( ` CR.) PAT ( ` CR.) NET FIXED ASSETS( ` CR.)

38 SEARCH - THE INDUSTRIAL SOURCEBOOK | J A N U A R Y 2 0 1 2

FINA

L RAN

K

GROU

P RA

NKIN

G

TOP 500 MANUFACTURING COMPANIES - LISTING