S+B

108

www.strategy-business.com strategy+business Autumn 2010 15 YEARS OF BEST BUSINESS THINKING DON TAPSCOTT • C. K. PRAHALAD • MARSHALL GOLDSMITH • GARY NEILSON • A. G. LAFLEY • DAVID ROCK S P E C I A L ANNIVERSARY I S S U E Special Issue CELEBRATING 15 YEARS OF THE BEST BUSINESS THINKING Special Issue, Autumn 2010 US $12.95 Canada C$12.95

Transcript of S+B

0 74851 08213 3

0 5

$12.95

www.strategy-business.com

strategy+businessA

utumn 2010

15

YE

AR

SO

FB

ES

TB

US

INE

SS

TH

INK

ING

DON TAPSCOTT • C.K. PRAHALAD • MARSHALL GOLDSMITH • GARY NEILSON • A.G. LAFLEY • DAVID ROCK

SP

ECIAL

ANNIVERSARY

I S S U

E

Special Issue

CELEBRATING15 YEARSOFTHE BESTBUSINESSTHINKING

Special Issue, Autumn 2010US $12.95 Canada C$12.95

ed

itor’s

lette

r

1

a sound federal budget headingtoward surplus, and strong businessconfidence. How could anythingpublished in those years matter toanyone in 2010?

Yet despite all the turbulencesince then, there has been a slow butsteady increase in knowledge abouteconomic value and organizationaleffectiveness. The importance ofman agerial capability has been dis-counted by economists (and others)for years, but it is now becomingincreasingly apparent. Variance inmanagerial prowess explains whysome companies weathered the eco-nomic storm and others did not,and why some new CEOs succeedwhile others crash and burn. That’swhy, at s+b — through the editor-ships of Kurtzman (1995–1999),Randall Rothenberg (2000–2005),and me (since 2005) — our primaryeditorial mission has been to helpreaders find the most profound andmost pragmatic business insight,and put it to use.

Consider, for instance, “WhyCEOs Succeed (and Why TheyFail): Hunters and Gatherers in theCorporate Life” (page 8), written in 1996 by an innovative venturecapitalist (Edward F. Tuck) and a prominent anthropologist (Timo-

thy Earle). They show how theCEO and the board of a major com-pany play out the same roles in ourtime that the chiefs and elders ofprehistoric tribes established manythousands of years ago. In that con-text, the passage of 15 years is al -most nothing.

Similarly, the 1997 article “10XValue: The Engine Powering Long-term Shareholder Returns” (page16) anticipates many of the ideasemerging now about the value ofcoherence. Leslie Moeller (now aBooz & Company partner) andBooz alumni Charles E. Lucier andRaymond Held studied 30-yeargrowth patterns of 1,300 publiclytraded companies in the U.S., andfound it is possible to raise a com -pany’s value 10-fold in that time, ifyou know how to muster the rightkind of innovation.

Don Tapscott’s 2001 article,“Rethinking Strategy in a Net-worked World (or Why MichaelPorter Is Wrong about the Inter-net)” (page 24) remains currentbecause the controversy it raised stillendures: Does the Internet makecorporate boundaries obsolete?Should companies emulate Apple,which retains tight control overevery aspect of its enterprise, or

Since its inception, strategy+businesshas focused on the value of manage-ment thinking and practice. Be -cause business knowledge is a mov-ing target, in which there is alwayssomething to learn from practiceand reflection, the best insightsabout management often seem coun-terintuitive at first. But they canmake a significant difference in youreffectiveness and the per for mance of your enterprise — whether you’rea CEO, a student, an entrepreneur,or anyone else in business. This year,we celebrate the magazine’s 15thanniversary by looking back at thewisdom we have published in ourpages. Much of it is still worth read-ing now.

When s+b was founded in 1995by former Harvard Business Revieweditor Joel Kurtzman and a group offarsighted partners at Booz & Com-pany (then part of Booz AllenHamilton), the dot-com era was justbeginning, and the shape of theworld economy was very differentthan it is today. Amazon andGoogle did not yet exist; neitherChina nor India was seen as a globaleconomic force. The United States,where the magazine’s focus was cen-tered at the time, was at a peak ofprosperity, with rising equity prices,

15 YEARS OF SIGNIFICANCE

ed

itor’s

lette

r

2

stra

tegy

+bu

sine

sssp

ecia

l iss

ue, a

utum

n 20

10

terns of CEO succession and thequalities of effective CEOs — con-tinues to appear in s+b.

Another author who has be -come more prominent while writ-ing for s+b is Marshall Goldsmith,the executive coach’s executivecoach, now known for his bestsellersWhat Got You Here Won’t Get YouThere: How Successful People BecomeEven More Successful (with MarkReiter; Hyperion, 2007) and Mojo:How to Get It, How to Keep It, Howto Get It Back if You Lose It (withMark Reiter; Hyperion, 2009). In2004’s “Leadership Is a ContactSport: The ‘Follow-up Factor’ inManagement Development” (page56), Goldsmith and his coauthorHoward Morgan reveal the mostimportant factor in helping leadersbecome capable: following up withother people about their own im -provement. The Ed Koch “How’m Idoing?” style of leadership may havebeen right all along.

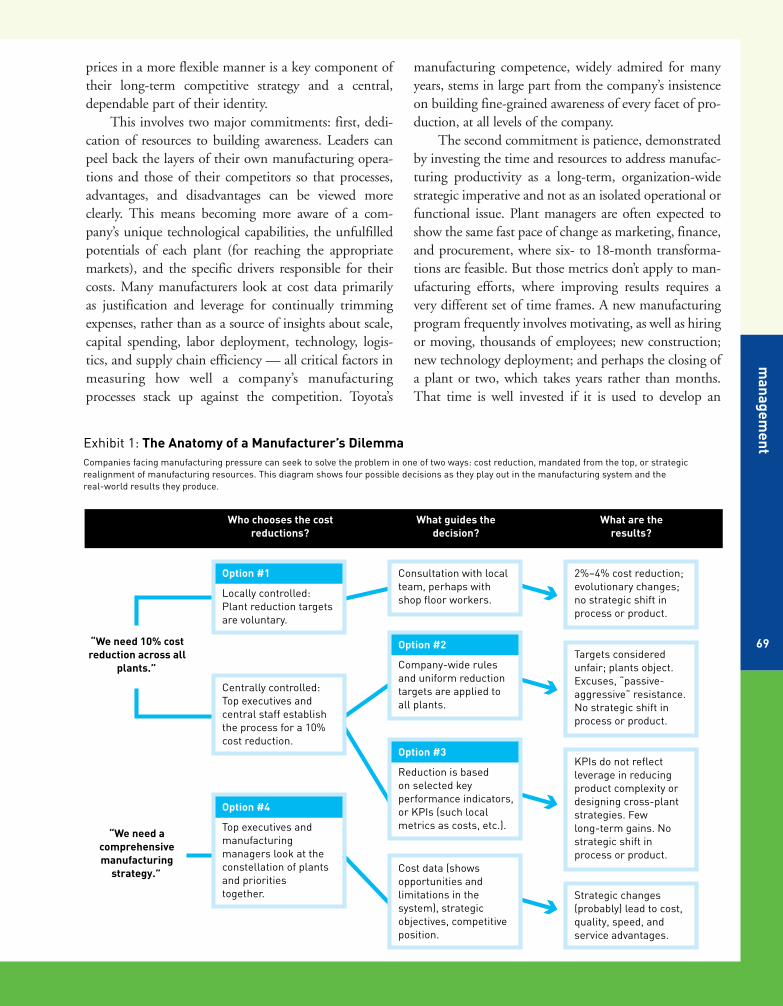

“Manufacturing Myopia” (page66), published in 2006, describes aperennial affliction that is demand-ing more attention now as produc-ers of goods wonder where theirindustries went. Authors Kaj Grich-nik, Conrad Winkler, and Peter vonHochberg posit a culprit differentfrom the usual suspects (China andoutsourcing): the conventionallyfragmented approach to manufac-turing management. Competitive-ness, on both a corporate and anational level, depends on takingthis kind of guidance seriously.

One of the great executives ofour time is Procter & Gamble’s for-mer CEO A.G. Lafley, the author of “P&G’s Innovation Culture”(page 78), published in 2008. Heand noted management writer RamCharan (who introduces the article)conceived of it as a follow-up to

or “missing chapter” of their best-selling book, The Game-Changer:How You Can Drive Revenue andProfit Growth with Innovation(Crown Business, 2008), which dis-cussed the human changes neededto foster Procter & Gamble’s re -markable strategic renaissance dur-ing the 2000s.

This special issue also includes2009’s “Managing with the Brain inMind” (page 88) by David Rock,founder of the NeuroLeadershipInstitute and one of the first writersto explore the relationship betweenneuroscience and organizationallead ership. Change efforts can takehold only when leaders recognizethe deep, brain-based needs peoplehave for status, certainty, autonomy,relationships, and fairness.

These articles are classics; theywill always be relevant. (For a list ofother classics we’ve published, seepage 104.) In this special issue, wealso celebrate some of the great busi-ness books we have reviewed overthe years; see the survey by SeniorEditor Theodore Kinni, an experton business books, on page 98.

Society’s growth curve is drivenby the quality of its ideas, particular-ly those about management. That isthe real engine behind increases inwealth and productivity at manycompanies, and it represents a pri-mary source of strength in dealingwith today’s immense social andenvironmental issues. We (and Booz& Company, the firm that publish-es s+b) are proud of our track recordin bringing this type of knowledgeto you. +

Art Kleiner

IBM, which thrives by providing itscustomers access to an open sourceworld of software, services, anddevices? The debate is far from set-tled (especially with Apple ascen-dant right now), but Tapscott laysout a compelling case for opensource enthusiasm.

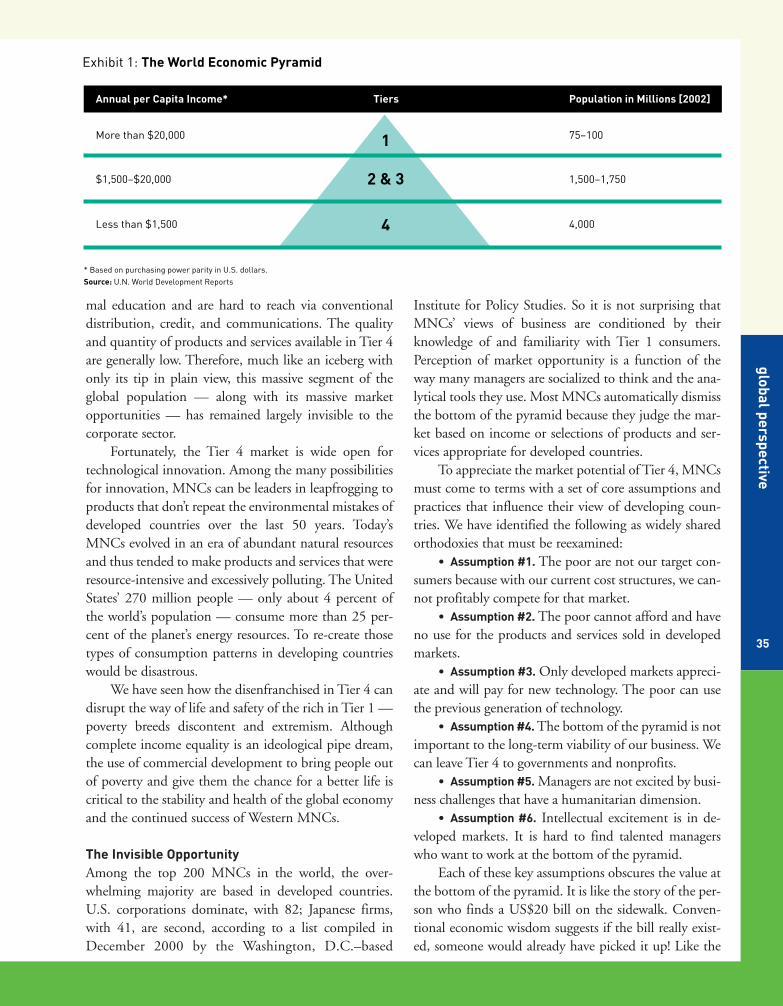

Perhaps the most prescientwork that s+b has published to datewas “The Fortune at the Bottom ofthe Pyramid,” by C.K. Prahalad andStuart L. Hart (page 32). This arti-cle, published in 2002, foresawbusiness models targeteted at thebillions of “aspiring poor” in emerg-ing markets. To reach them, multi -national companies would need tocreate low-margin, low-cost goodsin “culturally sensitive, environmen-t ally sustainable, and economicallyprofitable” ways. Prahalad, whopassed away in April 2010 after asud den illness, lived to see this seem -ingly outlandish concept be comepart of the strategy of com paniesaround the world. (See the discus-sion of his book in “Essential Read-ing: Highlights from 15 Years of s+bBook Reviews,” by s+b Senior Edi-tor Theodore Kinni, on page 98.)

The concept of organizationalDNA began life in our pages as“The Four Bases of OrganizationalDNA” (page 46), published in 2003as an effort to isolate the factors thatshape a company’s culture. As au -thors Gary Neilson, Bruce A. Paster-nack, and Decio Mendes describe it,company be havior is influenced bythe design of structures (reportingrelationships and hierarchy), deci-sion rights, motivators (incentivesand career options), and informa-tion flow (the informal networks bywhich people share knowledge).Neilson’s ongoing work — on bol-stering organizational capabilitiesfor better execution, and on the pat-

8

MANAGEMENT

Why CEOs Succeed (and Why They Fail):Hunters and Gatherers in the Corporate LifeEdward F. Tuck and Timothy Earle In the corporate world, the laws of the jungle still rule.CEOs and boards fall prey to the habits and practices ofprehistoric hunters and gatherers.

STRATEGY & COMPETITION

10X Value: The EnginePowering Long-termShareholder ReturnsCharles E. Lucier, Leslie Moeller, and Raymond HeldYour company can pursue 10-fold growth over 15 yearsthrough strategic innovation: changing the rules of thegame for your industry.

STRATEGY & COMPETITION

Rethinking Strategy in a Networked World Don Tapscott The original manifesto for open source, Internet-conscious competitive advantage argued that MichaelPorter was wrong about partnerships and alliances.Here’s why working outside your boundaries is centralto business success.

Six Reasons There Is a New Economy

GLOBAL PERSPECTIVE

The Fortune at the Bottomof the PyramidC.K. Prahalad and Stuart L. HartLow-income markets present a prodigious opportunityfor the world’s largest companies to seek their fortunesand bring prosperity to the billions of aspiring poor whoare joining the market economy for the first time.

16

24

28

32

features

66

16

8

featuresMANAGEMENT

The Four Bases ofOrganizational DNAGary Neilson, Bruce A. Pasternack, and Decio MendesHow does a company design its organization toexecute its strategy and successfully adapt whencircumstances change? The first step is to under-stand how four key traits of an organization influ-ence each individual’s behavior: the organizationalstructure, the decision rights for processes, themotivators, and the flow of information.

Focus: Testing Quest Diagnostics’ DNA

MANAGEMENT

Leadership Is a ContactSport: The “Follow-upFactor” in ManagementDevelopmentMarshall Goldsmith and Howard MorganA review of leadership development programs ateight major corporations reveals that nothingworks better than interaction with colleagues.Executives who follow up their training by discussing their improvement plans and progresswith co-workers become the best leaders.

MANAGEMENT

Manufacturing MyopiaKaj Grichnik, Conrad Winkler, and Peter von HochbergWhy do manufacturers lose relevance and competi-tiveness? Because their operations strategies areoften the same as they were 10 or 20 years ago.Instead of drifting into decline, producers of goodshave a chance to seize the future by cultivating bet-ter awareness about manufacturing costs andmeans: learning to see their operations moreclearly and redesign them more flexibly.

The Roots of Myopia

STRATEGY & COMPETITION

P&G’s InnovationCultureA.G. Lafley, with an introduction by Ram CharanLafley, the CEO of Procter & Gamble, explains howhis company built a world-class organic growthengine by investing in people. Going beyond theirbook, The Game-Changer, the authors explore therole of social systems in turning new ideas into commercial success.

Becoming a Great Innovation Team LeaderRam Charan

MANAGEMENT

Managing with the Brain in MindDavid Rock Neuroscience research is revealing the social nature of the workplace and its implications formanagement. The brain’s social needs — for status, cer tainty, autonomy, relatedness, and fairness —matter more than money.

BEST BUSINESS BOOKS 1995–2010

Essential Reading:Highlights from 15 Years of s+b Book Reviews Theodore Kinni Our all-time favorite business books.

ENDPAGE

Articles of SignificanceOf s+b’s many classic articles over the years, hereare a few of the editor’s favorites.

Cover illustration by Opto

Special Issue, Autumn 2010

50

46

66

72

56

84

78

98

88

104

EDITORIAL

Editor-in-Chief Art Kleinerkleiner_art@ strategy-business.com

Executive EditorRob Nortonnorton_rob@ strategy-business.com

Managing Editor Elizabeth [email protected]

Senior EditorKaren Henriehenrie_karen@ strategy-business.com

Senior EditorJeffrey Rothfederrothfeder_jeffrey@ strategy-business.com

Senior Editor, s+b BooksTheodore Kinnieditors@ strategy-business.com

Art DirectorJohn [email protected]

Associate Art DirectorJessie [email protected]

DesignerMika [email protected]

Contributing Editors Edward H. BakerNicholas G. CarrDenise CarusoMelissa Master

CavanaughMichael V. Copeland

Stuart CrainerDes DearloveTom EhrenfeldBruce FeirsteinLawrence M. Fisher Ann Graham

Sally HelgesenWilliam J. HolsteinDavid K. HurstJon KatzenbachTim LaseterChuck Lucier

Gary L. NeilsonJustin PettitRandall RothenbergMichael SchrageMark StahlmanChristopher Vollmer

Editorial and Business Offices101 Park Avenue New York, NY 10178 Tel: +1 212 551 6222Fax: +1 212 551 6363 [email protected]

Design ServicesOpto Design Inc.153 W. 27th Street, 1201New York, NY 10001Tel: +1 212 254 4470 Fax: +1 212 254 5266 [email protected]

PermissionsDoreen Annette GanttTel: +1 212 551 6022Fax: +1 212 551 6363 [email protected]

Retail Comag Customer Service Tel: +1 800 223 0860

SubscriptionsCustomer Servicestrategy+business P.O. Box 1724 Sandusky, OH44871-1724www.strategy-business.com/subscriber Tel: +1 877 829 9108 Outside the U.S., call +1 429 626 8934E-mail: [email protected]

Back Issues Tel: +1 800 810 1404Outside the U.S., call +1 817 685 5626

Reprints www.strategy-business.com/reprints Tel: +1 703 787 8044

strategy+business www.strategy-business.com

strategy+business (ISSN 1083-706X) is published quarterly by Booz & Company Inc., 101 Park Avenue, New York, NY 10178. ©2010 Booz & Company Inc.All rights reserved. “strategy+business,” “Booz & Company,” and “booz&co.” are trademarks of Booz & Company Inc. No reproduction is permitted inwhole or part without written permission from Booz & Company Inc. Postmaster: send changes of address to strategy+business, P.O. Box 1724, Sandusky,OH 44871-1724. Annual subscription rates: United States $38, Canada and elsewhere $48. Single copies $12.95. Canada Post Publications Mail SalesAgreement No. 1381237. Canadian Return Address: P.O. Box 1632, Windsor, ON, N9A 7C9. Printed in the U.S.A.

Deputy Managing Editor Laura W. [email protected]

Web EditorBridget [email protected]

Chief Copy EditorVictoria [email protected]

Information GraphicsLinda [email protected]

Assistant to the Editorsand PublisherDoreen Annette Gantt [email protected]

ChairmanJoe Saddi

Chief Executive OfficerShumeet Banerji

Chief Marketing andKnowledge OfficerThomas A. Stewart

Marketing AdvisoryCouncilPaul LeinwandNiko CannerKlaus-Peter GushurstBarry JaruzelskiKarim Sabbagh

BOOZ & COMPANY INC.

PUBLISHING

Publisher and BusinessDevelopment DirectorJonathan GageTel: +1 212 551 6681Fax: +1 212 551 [email protected]

InternCharity Delich

Advertising DirectorJudith Russo Tel: +1 212 551 6250 Fax: +1 212 551 [email protected]

European AdvertisingRepresentativeMichael WeatherallTel: +44 7770 [email protected]

PUBLISHING

Marketing ManagerAlan Shapiro Tel: +1 212 551 [email protected]

Financial ReportingTaryn Grace Diaz-Harrison

Business DevelopmentGretchen [email protected]

Production DirectorCatherine FickPublishing Experts [email protected]

Circulation DirectorBeverly Chaloux Circulation Specialists Inc. [email protected]

PUBLISHING

Business OperationsAnalystChristian [email protected]

Cert no. SCS-COC-00648

strategy+business magazine contains only paper products that the Forest Stewardship Council certifieshave come from well-managed forests that contributeto conservation and responsible management.

ma

na

ge

me

nt

8

Illu

str

ati

on

by

Elw

oo

d S

mit

h

It is enormously destructive and expensive tochange the chief executive of a growth company whostumbles in office. The human cost is high, as well: competent executives, used to success, fail withoutunderstanding why. They are branded with their failure.Some succumb to bitterness and despair; a few are suicides.

Why do these otherwise successful, competent,well-trained people fail? Why, in the face of good advice,do they do things that bring about their ruin? Why, afterthey fail, can people of less training, skill, and intelli-gence turn their failures into successes?

The authors of this article are an early-stage ventureseed capitalist and an anthropologist who specializes inleadership. We have examined the most common waysthat CEOs fail by applying the findings and techniques

of anthropology to business organizations. We havefound that the cause of these systematic failures is notthe CEO’s lack of skill, nor even his or her psychology;it is the changing institutional context in which theCEO must perform.

A chief executive officer will fail most often in thesethree situations:

• He or she has moved to a much smaller company,either as an entrepreneur or to take over a startup orearly-stage company.

• The CEO’s small company has grown into a mid-sized company.

• The CEO has been a successful vice president orchief operating officer and has been promoted to chiefexecutive, or has been recruited as chief executive foranother company.

BY EDWARD F. TUCK AND TIMOTHY EARLE

WHY CEOS SUCCEED (AND WHY THEY FAIL)

HUNTERSAND

GATHERERS IN THE

CORPORATE LIFEWhat are the factors that determine

which CEOs succeed and which fail? Even in the high-tech world,

the laws of the jungle still rule.

ma

na

ge

me

nt

9

10

stra

tegy

+bu

sine

sssp

ecia

l iss

ue, a

utum

n 20

10

These three modes of failure seem unrelated; theyare not. Something changes when a company reaches acertain size that makes it somehow different to manage;also, running an independent company is different fromrunning a division of a large company. In short, small-company CEOs fail in large companies, large-companyCEOs fail in small companies, and CEOs who haverisen through the ranks can’t work with their boards.

Camp, Corporation, and Community

Every company is a polity: a politically organized com-munity. Even though employees may be hired and firedat will, and may be called “resources,” “heads,” “directs,”or some other impersonal term, each director, officer,manager, and employee of a company is a functioningmember of the polity. This is true regardless of thedegree of democracy that exists in the company, regard-less of an employee’s position and regardless of whetherhe or she or the company’s management wants it to betrue. Everybody in a company is part of a politicallyorganized community, a polity, and each person’s roleand behavior in that polity is determined by his or herinherited nature, upbringing, and training. In a com -pany, as in any polity, each person behaves according tohis or her rules about behavior in groups. Some of theserules come from upbringing and training. According toanthropologists L.J. Eaves, H.J. Eysenck, and N.G.Martin (Genes, Culture and Personality: An EmpiricalApproach, Academic Press, 1989), half of this behavior is inherited.

These rules come from our ancestors, and to a greatdegree they are shared among the other members of our species. When we are born we are humans, and weknow how to behave with other humans. When we try

to succeed in a group, we unconsciously call on thoseprim itive patterns of behavior that have evolved overmillions of years of living and working in groups; andthe structure of our groups comes from the way webehave together.

Anthropologists have found patterns in these“primitive,” isolated human polities that will help CEOsunderstand and solve difficulties in their relationshipswith their boards and their employees. We have foundthat corporations and their boards have strong parallelsin primitive polities, and that boards are therefore orga-nizationally different from the corporations to whichthey are attached. We learned that the founder who isruined by his or her company’s success, the captain ofindustry who cannot run a small company, and the sea-soned executive who cannot be promoted are all victimsof the same simple and ancient effect, and we propose areason for that effect. First, let’s compare organizations.

Inside Primitive Organizations

Three primitive organizations have counterparts inmod ern companies: the working group, camp, and hier-archy. A fourth organization, the state, evolved later —and it, too, has counterparts in modern companies.

1. The working group. A “working group” is foundin all cultures. It is a temporary association of two to sixpeople with useful skills, and it has a specific purpose: tohunt, to lay a section of railroad track, to right an over-turned car, to catch a criminal. Working groups are vari-ously called “hunting parties,” “task forces,” “work par-ties,” “posses,” and “patrols”: names fitting the purposeof the group and the group’s societal context. They existonly for the purpose at hand, and they are organizedquickly and informally.

Edward F. Tuck

[email protected] is the principal of Falcon Fund,

a venture capital and private

equity fund for seed and early-

stage investments, and CEO of

Social Fabric Corporation, a

relationship-prediction service

that uses DNA samples. At the

time of publication, he was a

general partner of Kinship

Partners II, a venture capital

fund. He has also been the

founder or cofounder of

sev eral companies, including

Magellan (the GPS pioneer)

and Teledesic Corporation.

Timothy Earle

[email protected] is professor and chair of the

department of anthropology at

Northwestern University, posi-

tions he held at the time of

this article’s original publica-

tion. Formerly, he was a pro-

fessor of anthropology at the

University of California at Los

Angeles and director of its

Institute of Anthropology.

Originally published Fourth

Quarter 1996.

ma

na

ge

me

nt

ma

na

ge

me

nt

11

When a hierarchical organization like a corporationor an army sets up a working group, a leader is namedby the hierarchy (“chairman” or “squad leader”),although the real leader of the group emerges inform ally.Sometimes the group chooses its own leader by accla-mation (“team captain”) or by lottery (“straw boss”);usually, the leader arises without any special action as thework progresses, and leadership passes from one personto another smoothly as the nature of the work changes.A working group has a problem to solve and works dem-ocratically, accepting suggestions from any memberregardless of his or her status outside the working group. When the problem is solved or abandoned, thegroup disbands.

The result of the group’s work has a strong effect onthe mood of its members. If the work is successful, theyare elated and often celebrate. If the work is a failure, itsmembers are depressed and uncommunicative for atime. Working groups are short-lived, have only a fewmembers, and are re-formed as needed.

2. The camp. Hunting and gathering “camps” usu al-ly comprise about 30 people, from up to six families.The business of the camp — hunting, gathering, cook-ing, building — is done by temporary working groupsas defined above. Though many jobs in a camp are sepa-rated by sex, little other specialization exists; today’shunter may be tomorrow’s gatherer or hut-builder,although special skills such as stone tool making are rec-ognized by all.

The hunting–gathering camp does not admit tohaving a leader; in fact, members of the camp will denythere is a leader. They will say, “We’re all leaders.”Nonetheless, a member of a nearby camp will say,“That’s Joe’s camp.”

The camp thus does have a person who facilitatesdecisions. He or she does not command, but is respect-ed because of knowledge, judgment, and skill in orga-nizing opinion. As Andrew Schmookler has noted, thisperson does not give orders, but focuses the decision-making process. Decision making in a camp is a politi-cal, deliberative, consensual process. The camp’s eldersare expected to choose courses of action that are accept-able to the camp, and to accept suggestions from every-

one. The whole camp behaves in a consensual manner,and there is strong social pressure to conform. (In func-tioning camps, all members are interested in the facts,are fully informed of them, continuously discuss them,and are aware of the alternatives being considered.) Atno time are the people in the camp invited to solve aproblem as a group, nor do they wish or expect to do so.

Where a consensus is not found and distrust anddisagreement linger, the usual solution is for the smallerfaction to leave, striking off on its own. This is a fairlynormal event, as families frequently move from camp tocamp; but it is not without risk. The faction that takesoff risks its very survival if a new camp receptive to itcannot be found.

When a camp grows to about 50 people, it becomesunstable and splits into two or more camps. This patternof size-related instability is repeated in organizations ofall kinds across human society.

3. The hierarchy. The tribe, which may encompassseveral camp-sized groups, is a hierarchy. Hierarchicalorganizations have a clearly defined leader and oftenmany strata of authority. They have clear lines of author-ity, and no inherent means to achieve consensus. Theyevolved as a means of providing a mechanism for rela-tions with other tribes (including commerce and war),for conducting religious observances, and to allow occu-pational specialization. But they had the fortuitousresult of solving the problem of instability in largeorganizations. The tribal hierarchy made it possible formore than 50 people to live and work together, at thecost of personal and group autonomy.

Simple tribes are organized into local groups of afew hundred, each with its own leadership. More com-plex tribes are organized into regional chiefdoms ofseveral thousand, each with a hierarchy of leaders. At thetop of every stable hierarchy there is a camplike consen-sual group. Even in outright dictatorships there must bean egalitarian council, as Machiavelli advised in ThePrince 500 years ago: “A prudent prince must…[choose]for his council wise men.… He must ask them abouteverything and hear their opinion, and afterwards de lib-erate by himself and in his own way, and in these coun-cils and with each of these men comport himself so that

12

stra

tegy

+bu

sine

sssp

ecia

l iss

ue, a

utum

n 20

10

everyone may see that the more freely he speaks, themore he will be acceptable.”

4. The state. Eventually, in the archaic world, statesevolved to organize much larger populations, whichwere often living together in cities and relying on marketexchange. It was at this time that real bureaucraciesemerged, both to solve efficiently the problems of largegroups and to control those groups for the will of dicta-torial rulers.

In the 18th and 19th centuries, with industrializa-tion and the introduction of cheap transportation, peo-ple began to live together in even larger groups. Thebureaucratic state then developed fully and became thepreferred method of managing any continuing enter-prise employing more than a handful of people. At first,these were outright dictatorships, but improvements incommunication, education, and the economy led to arevision of societal values so that now all members ofhierarchical societies have some voice. This voice variesfrom union grievance procedures through election ofleaders and managers through public approval of certainactions to formal consensus meetings; however, thestructure of any stable organization of more than 50 to100 people is some form of hierarchy.

Size Determines Structure

Why are human organizations of different sizes struc-turally different? Why does a small organization becomeunstable as it grows? Why is the triggering size the samein different cultures? It appears that six or seven is thelargest number of relationships that one person can dealwith continuously. We need the hierarchy, with its well-defined roles and patterns of behavior, to allow largenumbers of people to work together without overload.

A study by anthropologist Gregory Johnson at theCity University of New York has shown that decision-making performance in egalitarian groups falls off rap-idly as the group size grows beyond six. This is a resultof a well-documented limitation of the human brain,which cannot simultaneously retain and process morethan about seven “information chunks” at once. (Onesuch study by the Bell System set the size of local tele-phone numbers at seven digits.)

To make larger groups work while still retainingtheir egalitarian nature, six or seven groups form a“sequential hierarchy.” In this structure, consensus isachieved first within small units — for example, nuclearfamilies — and then is attempted among the formativegroups themselves, with full consensus finally reached

after a lengthy process of referring the issue back andforth from the smaller to the larger entities. The largeststable group in which this process has been observedcontains about 100 people, and involves three levels ofconsensus; the usual maximum is about 50 people (7times 7), and uses two levels of consensus.

Two points to hold in mind are: 1) As group sizechanges, so must its organizational structure. This is astrue for the long-term evolution of human society as itis for the short-term evolution of a company; 2) Withina single social system, groups of different scale exist andrequire different organizational structures. A major dys-function occurs when an organizational structure appro-priate for one scale is used for groups of other sizes.

The Modern Organization

Thus, four types of organization have arisen when peo-ple live together and try to do something in common:the working group, the camp, the general hierarchy, andthe state bureaucracy.

The most primitive of these is the working group,up to six people. It is also the one that elicits the mostprofound emotional response. The camp, up to 30 to 50people, is the next most primitive, and is also a very oldstructure.

The most modern organizations, and therefore theones for which we are by nature least adapted, are thehierarchy and the bureaucracy. Behavior in a tribe, acompany, or a nation is not innate: It is learned, in con-trast to behavior in camps and working groups. An indi-vidual’s success in a hierarchy depends on how well he orshe has learned its rules, and to what extent his or herinnate behavior allows that person to conform to thoserules. A modern corporation employing more than 100people is a hierarchy; a company of more than 1,000 isa bureaucracy. A camplike board of directors is at thetop, to offer guidance by diverse experience and to pro-vide intercorporate information. The corporation’s bestwork is done by working groups.

The advantages and satisfactions of recognizing theegalitarian nature of the working group are now under-stood; most traditional companies attempt to exploitthis. Very little analysis in a similar vein has been donewith boards of directors. Yet in corporations, the camp-like consensual group, the prince’s council, is the board.

Since today’s boards are like the camps of primitivesocieties, a successful CEO must remember how campsbehave.

A board is not a working party. It cannot solve

ma

na

ge

me

nt

ma

na

ge

me

nt

13

problems, it can only approve or disapprove courses ofaction proposed by its leader. If it is forced to choosebetween alternatives, a crisis of leadership often arises.

The CEO’s leadership role is not openly acknowl-edged by outside board members, who strongly asserttheir equality. The CEO thus must reach consensusamong board members before proposing importantissues. This process is called “keeping in touch.”

The CEO is the natural leader of the board. Evenwhen a board has a chairman who is not the CEO, aperson close to the company will refer to “Joe’s [theCEO’s] board.” If the chief executive refuses to lead,then the CEO and board will flounder or another indi-vidual member will assume leadership. In either case, theCEO must be replaced. This is because the surrogateleader cannot lead well unless he or she assumes theCEO’s role inside the organization and on the board.

Board members expect the CEO to be their leaderand will treat him or her as such until they decide to firethe person. Anything the CEO says or does will be dealtwith by experienced board members in the context ofCEO-as-leader. If an act or utterance of the CEO isunreasonable in this leadership context, the other mem-bers will believe at a deep, unconscious level that he orshe is incompetent or even insane. Since in either ofthese cases the CEO must be replaced, an extremelyunpleasant and difficult task, a member will sometimesopt for denial by assuming that a chief executive whoexhibits such behavior is manipulative or evil, either ofwhich is a disquieting but acceptable alternative.

The Ways CEOs Fail

We can now examine CEO failure modes by comparingmodern companies with polities in primitive cultures,

and by recognizing that much of our behavior is geneti-cally determined and will be similar when working with-in groups of the same size. Our understanding of theshort-term development of companies can thus be aidedby knowing the long-term evolution of human society.

These comparisons confirm anecdotal evidence thatsuccessful management techniques are fundamentallydifferent for companies above and below a critical size,and that techniques that succeed in a company abovethe critical size will fail below it, and vice versa. Thecomparisons also explain why CEOs who are successfulas division or subsidiary managers in large companies areunable to run independent companies. These failures arerelated to their inability to deal with their camplikeboards of directors.

Consider the following scenarios:Problems with the board: the new CEO’s surprise.

Those few extraordinary individuals who succeed byclimbing to the top of a hierarchy are surprised andsometimes quickly fail when faced with the need toimmediately lead the board. The new CEO is in thesame position as a camp leader, but without the usefulexperience of having lived in a camp.

The result is that the CEO often arrives at his or herposition as head of the board without realizing that therole has fundamentally changed.

A CEO in this position assumes that the wholeorganization is simply like his or her old division orfunction. If his or her whole experience has been in hier-archies, the CEO may define the role as giving or receiv-ing orders; he or she has always been told what to do orhas told others what to do. If the CEO has had no expe-rience with boards of directors, he or she may make thefatal error of regarding the board as a new boss, as a

Since today’s boards are like the camps of primitive societies,

a successful CEO must remember how camps behave.

14

stra

tegy

+bu

sine

sssp

ecia

l iss

ue, a

utum

n 20

10

working group to solve the company’s problems, or as apart of the organization that he or she must supervise. Ifthe CEO is told to lead the board but not command it,and to work by consensus, he or she may find this guid-ance incomprehensible. Denying the realities of the newsituation, the CEO may either actively avoid assumingleadership of the board or try to manipulate it or dictateto it. He or she can be further confused by fellow boardmembers, who may insist either that the board has noleader or that the leader is the aging chairman.

If, in fact, the CEO does not lead the board, theboard’s other members, who are operating out of theirprimitive, innate rule book, have little conscious insightinto the situation. They are confused and become un -ruly. The CEO and sometimes the organization it selfthen fail. Often, neither the board members nor theCEO can explain the failure. They then go on to repeatthe pattern until the board gets a CEO who will lead oruntil the CEO accepts his or her leadership role or re -turns to a subsidiary role in another company.

Problems with becoming big: the faltering founder.

Unless he or she has access to an enormous amount ofmoney, the founder of a company must first found acamp. In a camp, as we have seen, there is little special-ization; in a new company, it is common to hear, “I weara lot of hats.” It is also common to operate by consen-sus: Members marvel at the speed with which decisionsare made, and at their feeling of mutual support, clearobjectives, and clean, unambiguous communication.Employees at all levels speak as though they know whatis going on throughout the company. Most of the com-pany’s people work far more hours than a normal work-day; they enjoy their work.

If the company succeeds, it grows. At first, the com-

pany’s members are elated with the growth, and point tothe company’s new people as evidence of its success.Soon, however, typically when the company reaches 25people, a few dissonant voices are heard: “She’s trying todo my job,” “I don’t know what’s going on anymore,”and, as the company continues to grow beyond the sizeof a camp, “We’ve lost something important. I don’tknow what it is, but it’s gone. It isn’t fun anymore.” Atthis point, one or two key employees decide to leave, orsimply begin to work 40-hour weeks.

If an insensitive CEO doesn’t understand what ishappening, he or she will say that the people areungrateful and will withdraw; a more sensitive CEO willredouble efforts to communicate. Both will fail.

The appropriate action is to assemble a hierarchy,using experienced people, when the staff numbers morethan 20. Some key people will be dissatisfied and leave,because they left a hierarchy for the camplike feeling ofthe small company; some will feel betrayed. Others willadjust. The CEO must gradually abandon his or her roleas consensus leader and take on the role of chief.

This is a difficult transition even for CEOs whounderstand the problem. Often, founders have chosentheir role because of difficulties in the hierarchy of a pre-vious company; they see the transformation of theircompany to a hierarchy as a personal failure. At best,they must deal with alienation and feelings of betrayal inpeople with whom they have worked closely, and withwhom they shared the bonding and elation of a success-ful working party. Sometimes, even if their companiessucceed, they are unhappy and unfulfilled.

Problems with going small: a chief without a tribe.

The opposite occurs when a CEO is recruited from alarge company to run a young one. Such people often

ma

na

ge

me

nt

As the company continues to grow beyond the size of a camp, people say,

“We’ve lost something important. It isn’t fun anymore.”

ma

na

ge

me

nt

15

time, and whose work has largely been in hierarchies,would be wise to find an insightful friend who has suc-cessfully run a small company, or a person with exten-sive board experience, to act as an advisor.

Venture capitalists, executive recruiters, and boardmembers of young companies who have a stake in thesuccess of the people they fund or recruit can reducetheir risks considerably by discussing consensual organi-zations with their candidates.

One of the authors of this article has made a recenthabit of exploring the central issues that have been dis-cussed here with company founders (who are frequentlypro-consensus and anti-hierarchy) and with experiencedcandidates for top management jobs (who are dramati-cally the reverse). In two cases, after such a discussion, afounder suggested that he take the role of a functionmanager in the new company rather than be its CEO,and that he and the investors go out together to recruitan experienced hierarchical CEO to run the new enter-prise when it grew to an appropriate size.

In both cases, the company was unusually suc cess-ful. Perhaps more important, the founder happilyremained with the company in a productive and reward-ing role. +

Reprint No. 96402

Resources

Timothy Earle, “Chiefdoms in Archaeological and EthnohistoricalPerspective,” Annual Review of Anthropology (Annual Reviews, 1987): Asource of the insights in this article.

Eric Flamholtz, How to Make the Transition from Entrepreneurship to aProfessionally Managed Firm (Jossey-Bass, 1986): Describes what happenswhen a camplike company must become a hierarchy.

Allen W. Johnson and Timothy Earle, The Evolution of Human Societies(Stanford University Press, 1987): Includes observations on the structureand leadership of primitive polities. Insights from this book have beenused throughout this article.

Gregory A. Johnson, “Organizational Structure and Scalar Stress,” inTheory and Explanation in Archaeology, edited by C.A. Renfrew, M.J.Rowlend, and D.A. Segraves (Academic Press, 1982): Why consensusdoesn’t work in groups larger than six people.

Niccolò Machiavelli, The Prince, translated by Luigi Ricci (New AmericanLibrary, 1952): The classic for leaders of a state — or a hierarchy.

Andrew Bard Schmookler, The Parable of the Tribes (University ofCalifornia Press, 1984): This work, subtitled The Problem of Power inSocial Evolution, contains many strong parallels to modern corporatebehavior.

For more thought leadership on this topic, see the s+b website at: www.strategy-business.com/organizations_and_people.

have no experience with consensus-based groups.When the CEO arrives at his or her new company

and finds that everyone has a title and a place in anorganization chart, he or she is pleased, and often beginsthe process of interviewing people to see if they are wellqualified for their positions.

The CEO is then usually dismayed. If he or sheconcludes that the staff is incompetent, however, thatconclusion will be wrong. If, on the other hand, he orshe believes that the titles and the organization chartdescribe the real organization, and then attempts tooperate the company accordingly, the CEO will failimmediately. There is no hierarchical organization; it isa camp. The CEO cannot delegate; he or she must workby consensus.

Gaining Anthropological Guidance

The literature and techniques of anthropology and cul-tural evolution can be used to understand businessorganizations at different scales. We have explained threefamiliar failure modes of chief executive officers, derivedfrom studies of primitive societies and their leadership.We have shown that these failure modes can be avoidedif the CEO and the company’s employees understandand conform to the deep structure of their organization.

We have also shown that the board of directors of amodern corporation is a more primitive and intrinsic allydifferent structure from the organization it serves, andthat CEOs must use fundamentally different techniquesto work with their boards and with their companies.

Many failures of companies and their chief execu-tives can be avoided by supplementing graduate businesstraining, which now deals largely with the structure andmanagement of hierarchies, with training in consensualorganizations such as boards, skunkworks, and smallcompanies. The goal is for the new CEO to have thetraining to understand the differences between theorganization he or she is entering and the one he or sheis leaving.

In the absence of knowledge, people do the thingsthat have worked for them in the past. When thesethings fail to work, people simply do them more inten-sively, like a tourist in a foreign country who just shoutslouder if he or she is not understood.

But new CEOs have staked everything on their newjobs and they desperately want to succeed. When theyarrive in an unfamiliar organization, they are receptive toguidance they believe may keep them from failing. Aperson who is entering a small company for the first

stra

teg

y &

com

pe

tition

16

Illu

str

ati

on

by

Da

n P

ag

e

The question of how to achieve long-term sustain-able growth in shareholder value is at the top of theCEO agenda. Many companies have successfullyfocused their efforts on cost reduction through increasedlabor and asset productivity, and have achieved short-term increases in shareholder value as a reward. Withtheir businesses running efficiently, these companieshave refocused their energies into developing long-termgrowth strategies.

Aggressive revenue-oriented strategies are the mostcommon approach to creating long-term value forshareholders. These strategies typically include acquisi-tions, new products that extend the line, and marketingprograms to improve customer loyalty and retention.

Unfortunately, our research indicates that thesestrategies can cause more harm than good. Superior

long-term value for shareholders is derived only from aspecific type of revenue growth: growth that resultswhen a company delivers an order-of-magnitudeincrease in value to its customers, which we call “10Xvalue.” An order-of-magnitude improvement in thevalue proposition — obtained through a mixture ofproduct, image, service, and price — not only stimulatesgrowth by compelling customers to purchase, but alsoenables a company to earn superior profitability. A 10Xvalue innovation changes the industry’s basis of compe-tition and forces competitors to react, often by trying tocopy the innovation.

We find that attempts to grow revenue rapidly with-out a 10X improvement in value are seldom successfuland often counterproductive. They involve either costlyacquisitions that are subsequently divested, “renting”

BY CHARLES E. LUCIER, LESLIE MOELLER, AND RAYMOND HELD

10X ValueTHE ENGINE POWERING LONG-TERM SHAREHOLDER RETURNS

What does it take to grow shareholder value at world-class rates? More than profit and

revenue increases. It takes strategic innovation to make it into the top tier.

stra

teg

y &

com

pe

tition

17

18

stra

tegy

+bu

sine

sssp

ecia

l iss

ue, a

utum

n 20

10

new customers with the latest promotion, or the exten-sion of product lines at the expense of the long-term loy-alties of current customers. The only reliable way to earnreturns for shareholders in the top 10 percent over aperiod of 10 to 15 years is through a 10X value innova-tion. Of course, our findings do not invalidate theimportance of rapid productivity improvements andrevenue growth in all businesses. To sustain even averagereturns for its shareholders, a company must achievecontinual improvements in its productivity and targetincreases in market share.

This article relates our findings on 10X value as acause of shareholder value growth and discusses theimplications for senior managers. These findings resultfrom an ongoing effort to uncover the dynamics ofgrowth. They are based on an assessment of the creationof long-term shareholder value by more than 1,300 largecompanies publicly traded in the United States between1967 and 1997, supplemented by case studies of 65companies in the top 10 percent of shareholder valuecreation for at least a decade. Although the quantitativeresearch that underlies this article focuses on UnitedStates companies, our subsequent research suggests thatthe conclusions are equally valid in other countries.Indeed, many top-performing U.S. companies (forexample, the Coca-Cola Company) achieved much oftheir growth by replicating their 10X value in othercountries.

Several findings from this research contradict con-ventional wisdom. First, the relationship between rev-enue growth and growth in shareholder value — definedas increases in stock price plus dividends, adjusted forstock splits — is not close in either the short term or thelong term. For example, despite significant growth in

revenue between 1985 and 1994, USAir, Fleming, andBlack & Decker had a modest or negative growth inshareholder value.

Additionally, industry growth rates are almost com-pletely unrelated to the likelihood that a company willcreate superior shareholder value over the long term.Contrary to prevailing strategic thinking, companies inslow-growth, mature markets are somewhat more likelyto create superior returns for shareholders than compa-nies in fast-growth industries.

Finally, the tactics implied by traditional strategicplanning — which focuses on achieving better marketand cost positions than competitors through superiorplanning and management — results, at best, in growthrates a few points faster than average and significantlyless than the top-performing companies.

Innovation: The Value Multiplier

What then are the drivers of sustained superior long-term growth in shareholder value? More than 90 percentof the companies we studied that achieved top-decilereturns for at least 10 years have been able to sustainrapid increases in operating earnings through the con-tinual creation of 10X value for customers. They thenachieved top-line growth by replicating the 10X value toattract new segments of customers (what we call a“growth superhighway”).

To accomplish this, they relied on continual, high-ly productive innovation: developing and constantlyenhancing unique approaches to serve customers moreeffectively and sharing the value with customers. Thisoften resulted in value propositions that offered bothbetter differentiation and lower pricing. Although theresult of innovation is often a breakthrough that changes

Charles E. Lucier

[email protected] is a writer and contributing

editor to strategy+business.

He was instrumental in the

founding of this magazine.

At the time of this article’s

publication, he was a senior

vice president at Booz Allen

Hamilton (whose commercial

business later became Booz &

Company), and the managing

partner of its Cleveland office.

Leslie Moeller

[email protected] is a partner with Booz &

Company in Cleveland. He

leads the firm’s North

American work in the con-

sumer, media, and retail

industries. He is the coauthor

of The Four Pillars of Profit-Driven Marketing: How toMaximize Creativity,Profitability, and ROI (McGraw-

Hill, 2009).

Raymond Held

is the chief financial officer

of Kellogg de Mexico. At the

time of this article’s pub lica-

tion, he was a senior associate

in the engineering and manu-

facturing group at Booz Allen

Hamilton.

Originally published Third

Quarter 1997.

stra

teg

y &

com

pe

tition

stra

teg

y &

com

pe

tition

19

the rules of the game, all of the companies we studiedrelied on a series of innovations, not a single “big idea.”

The highest-performing companies were dividedinto two types of innovators. Strategic innovations —dramatic improvements in the entire business systemthat deliver value to customers — powered about half ofthem. For this group of “strategic innovators,” willing-ness to share the benefits with customers was an essen-tial factor — to drive top-line growth, and to stimulateadditional improvements in the business system andremain ahead of competitors. Innovation in products orservices that create 10X value for customers powered theother half of the top-performing companies.

• Strategic innovators. Although it is not surprisingthat a successful strategic innovator creates extraordinaryvalue for its shareholders, we were surprised to discoverthat nearly half of the top decile of companies for each ofthe three decades we studied fall into this category.Strategic innovation is unusual in any one industry: inthe 75 industries in the United States that we investi -gated, we found an average of 0.6 successful strategicinnovations per industry per decade. Nonetheless, 5 per-cent of all large publicly traded companies are strategicinnovators, which is a significant number.

Because strategic innovators change the rules of thegame in their industries, most of their stories are wellknown. Nevertheless, three findings common to all ofthe strategic innovators deserve mention.

First, strategic innovations are not brainstorms orconcepts that emerge fully formed: The initial concept isdifferent from the typical game-changing innovation.Strategic innovation requires not only a breakthroughidea, but also the commitment and the feedbackprocesses to refine the idea until it is successful. For

example, FedEx Corporation was founded to provideguaranteed overnight delivery, which was a break-through idea. However, the initial target market waspurveyors of critical supplies, such as medical suppliesand parts. It was the later discovery that most of the vol-ume of material sent was paper, and the subsequentpositioning of FedEx to provide the reliable delivery ofimportant business material, that really drove growth.Innovations that in retrospect may appear to be a singleidea were in fact the result of a series of linked innova-tions and adaptations.

Second, strategic innovation is difficult and time-consuming to put into practice. Home Depot Inc., forexample, was a strategic innovator in its transformingthe category of home improvement retailing. An in di -cation of the magnitude of the difficulty is the 15 yearsrequired for any of its competitors to create an equallysuccessful format — even though they could build uponHome Depot’s experience. A strategic innovator’s com-petitive advantage is not the breakthrough idea, butrather the myriad details of the successful business sys-tem and the ability to adapt rapidly and improve.

Finally, to create superior value for shareholders,strategic innovators don’t need to start in a large marketsegment. In fact, the companies that created the high estrate of return for their shareholders over a decade weresomewhat smaller (in revenue) than the average largepublicly traded company at the beginning of the decadeand larger than the average large publicly traded com -pany at the end of the decade. Strategic innovators aremuch more likely to succeed when they initially focuson a peripheral segment. The innovator can learn howto make its breakthrough idea really work to deliver 10Xvalue in the periphery, often without reaction from the

The initial target market was purveyors of medical supplies and parts.

Then FedEx discovered that most ofthe material sent was paper.

20

stra

tegy

+bu

sine

sssp

ecia

l iss

ue, a

utum

n 20

10

dominant competitors focused on the core markets. Nucor Corporation illustrates the pattern. Nucor

began as a manufacturer of steel joists and a regionalmanufacturer of reinforcing bars — the lowest-qualitysteel, of least interest to the major integrated mills. Overtime, it moved into light structural shapes, mediumstructural shapes, and finally, flat rolled steel. By themid-1990s, Nucor had become the second-largest steelproducer in North America.

• Product and service innovators. These companiesbring a series of successful “new to the world” productsto market. Their success lies in coupling an effectiveinnovation process with a superior product concept, andrepeating this success time after time. Just one newproduct is no longer enough to power superior share-holder value; top-decile growth in shareholder valuerequires getting new products right consistently.

Although the most successful product innovatorsare effective throughout the innovation stream of activi-ties, it is excellence in one of four activities that powerssuccess. These are market understanding (defining cus-tomer and channel needs and opportunities ahead ofcompetitors); technology management (ensuring thatthe correct high-impact technologies are available whenneeded); product planning (integrating market needswith product architecture to enable competitive specifi-cation, development, and delivery of products); andproduct development (translating a product line orprocess specification into an engineered design that canbe competitively delivered to customers).

For instance, Nike Inc.’s success comes from anunderstanding of its customers’ total experience with itsproduct, including intensive managerial experience withthe products and a special panel of athletes to providefeedback on designs and trends. Leading-edge productscombine with powerful advertising campaigns using rolemodels to enhance the customer’s athletic shoe experi-ence. Intel Corporation, on the other hand, creates valuefrom a focus on maintaining market leadership by usingtechnology to constantly improve physical product per-formance. Before a new product is launched, a designteam is working on the next-generation technology thatwill make the new product obsolete — bringing a con-tinuous stream of higher-powered chips to the market.

In capital-intensive industries, driving valuethrough continual product innovation often requires“new to the world” innovations that “bet the company.”For the Boeing Company, the development of each newaircraft is a major decision, one that could permanently

damage the company if it fails. For instance, from thelate 1980s to the early ’90s Boeing spent US$4.5 billionto develop the 777 aircraft, at a time when the compa-ny’s equity was $8 billion. The success of this aircraft wasinstrumental in helping the company turn its sales num-bers around during the industry rebound of the late1990s. Intel has to make similarly risky bets on eachnext wave of microprocessor technology. Although mak-ing these bets can be frightening for all involved, theymust enable the stream of continual product innovationrequired to deliver 10X value. In addition, big bets cre-ate a barrier to entry by less-experienced companies, andthis helps to maintain the product innovator’s superiorvalue over its competitors.

The Growth Superhighway

To earn superior returns for shareholders, a companymust effectively exploit its 10X value to sustain annualtop-line growth of 15 to 25 percent without mistakesthat negatively impact earnings. Whatever the source oftheir 10X value, the companies that created the greatestlong-term value for their shareholders all created agrowth superhighway — that is, the capability to repli-cate revenue growth along one targeted path.

All companies seek growth through some mix ofmarket share gains within current segments, new seg-ments, new geographies, and acquisitions. Most compa-nies try to generate growth through most of these paths.The companies that create the most long-term value fortheir shareholders are unusual in that they focus on oneprimary path. For example, Walmart and Home Depothave grown primarily through geographic expansion,the Shaw Group and WMX Technologies (formerlyWaste Management Inc.) expanded by acquisition;

stra

teg

y &

com

pe

tition

stra

teg

y &

com

pe

tition

21

Nucor and Rubbermaid pursued adjacent segments; andIntel has primarily focused on rapid rollout within itscurrent segments.

Global expansion is an increasingly importantgrowth superhighway. Coke’s ability to replicate its 10Xvalue proposition overseas — especially in developingand supporting the local bottlers who sell and distributethe product — has been the principal driver of itsgrowth. Similarly, Carrefour SA, the leading Frenchhypermarket retailer, has had tremendous success inexpanding its format in Latin America. In Carrefour’scase, international expansion into less-developed mar-kets has been especially effective because the hypermar-ket value proposition is more than a 10X improvementover the small local supermarkets and general merchan-dise retailers.

The best-performing companies invest in routiniz-ing expansion along the targeted growth path. For exam-ple, Walmart has a standard, very efficient process tobuild a new store, Home Depot excels in quickly pene-trating a new metropolitan area with a critical mass ofstores, and Shaw and WMX learned to install their 10Xvalue-creating system quickly in the companies theyacquired. Once these companies stray from their growthsuperhighway, their performance can become highlyvariable. For example, Home Depot’s entry into Canadaby acquisition and its formats targeted at other customersegments (for example, Expo) have not really panned out.

It appears that more than one growth superhighwaymay be viable in an industry. For example, between1972 and 1985, WMX and Browning-Ferris Industrieseach created 10X value for customers and top-decilereturns for their shareholders, even though WMX grewprimarily by acquisition and Browning-Ferris mainly by

geographic expansion. Hence, the imperative appears tobe less to select the correct growth path than to focus onone path and invest in building the capability to make ita superhighway.

Implications for Management

Our findings demonstrate that creation of 10X value forcustomers along a growth superhighway leads to superi-or long-term value for shareholders. The four impera-tives top management must heed to develop and exploita 10X value proposition are: challenge; focus; differenti-ate your management approach; and lead, don’t follow.

• Challenge. Companies that create superior long-term returns for their shareholders have financial per-formance that is significantly — not incrementally —better than average. Increasing the rate of growth inearnings and revenue of an average company by two orthree points will not result in 80th or 90th percentilereturns to shareholders.

By setting the strategic long-term challenge ofachieving dramatically higher financial goals, a CEO canhelp stimulate a fundamental rethinking of the businessthat might yield 10X value for customers.

• Focus. The best-performing companies that wehave studied all prospered by creating 10X value for cus-tomers in one business and by exploiting their advantagedown one growth superhighway. Focus enables a com-pany to continue to innovate, to gain leverage from scaleas it grows, and to sustain its advantage over competi-tors. Companies that lose their focus on one growthsuperhighway often falter in creating superior long-termreturns to shareholders.

The multibusiness corporations like GeneralElectric Company and PepsiCo that have created 10X

22

stra

tegy

+bu

sine

sssp

ecia

l iss

ue, a

utum

n 20

10

value have done so in only one business unit at a time(specifically, GE Capital and Frito-Lay). In part, this factmay merely reflect the inherent difficulty of creating10X value. However, we believe that it will be very difficult for any corporation to create and exploit 10Xvalue in two distinct business units simultaneously. 10X value creation is simply too demanding in terms ofmanagement talent, investment to finance rapid growth,and the attention of the CEO.

One principal reason that large multibusiness com-panies have been less likely to create 10X value than single-business companies may have been an unwilling-ness to focus on a single business unit as the driver ofsupe rior long-term shareholder value creation.

The good news is that even in a corporation as largeand diverse as GE, one division that creates 10X valueand exploits the advantage along a growth superhighwaycan yield excellent long-term results to shareholders. Forexample, GE is an extremely well-managed companywith returns to shareholders in the 75th percentilebetween 1985 and 1994. However, without GECapital’s 23 percent annual earnings growth, the corpo-ration’s earnings would have grown at only 6 percentinstead of 9 percent, and returns to shareholders proba-bly would have been only average.

• Differentiate your management approach. Cre-ation of 10X value for customers requires a distinctivemanagement model. This involves the rapid incorpora-tion of feedback from customers into the evolving valueproposition; investment in rapid growth, often before acompelling case can be made that the investment will payoff; an entrepreneurial culture with rapid decision mak-ing; and compensation heavily incentivized toward bot-tom-line growth or superior returns to shareholders.

Although single-business companies can embracethis model, multidivision corporations face a formidablechallenge. The usual multidivision corporate planningand budgeting processes, culture, and compensation sys-tems are inconsistent with the 10X value creationmodel. For example, traditional strategic planning usu-ally focuses on what is and what has been, whereas 10Xvalue creation involves “new to the world” innovation.An analytical demonstration that something that hasnever been done will prove to be a superior investmentis very difficult.

The solution for a large multidivision company thatwants to create 10X value in a business is to differentiateits management systems. That is, it can use differentplanning, budgeting, and compensation systems in thedivision targeting 10X value and allow that business’sculture to diverge somewhat. More traditional planningand budgeting systems are better adapted to businessesthat are not trying to create 10X value. These systemscan stimulate productivity improvements, target oppor-tunities for profitability increases and market sharegains, quickly match successful initiatives by competi-tors, and ensure that business units create and executenear-term plans consistent with a long-term strategicdirection.

• Lead, don’t follow. 10X value creation requiressenior management leadership. There are two key rolesto be played: a senior champion who makes the refine-ment and success of the 10X value innovation his or hersole objective, and a CEO who decides which bets tomake and who creates the environment for success.

Creating 10X value starts with the conviction that amarket is ready for value innovation, like that shown bySam Walton in leaving Ben Franklin stores when that

stra

teg

y &

com

pe

tition

It will be very difficult for any corporation to create and exploit

10X value in two distinct business units simultaneously.

stra

teg

y &

com

pe

tition

23

improve products significantly (its R&D spending isabout 4 percent of sales whereas Unilever’s is about 2percent) and has developed the ability to globalize theproducts rapidly. Although P&G cannot claim everybreakthrough — indeed, it missed such product ideas as pull-up diapers and peroxide and baking soda intoothpaste — it creates a sufficient stream of global win-ners, such as two-in-one shampoo and compact deter-gents, to fuel returns to shareholders, as of 1997, in the81st percentile.

CEOs of companies with successful 10X value cre-ation strategies consider them to be low risk: As long asthey can sustain the 10X advantage, there is no need toworry about the actions of competitors or the cyclicalityof the underlying market.

Superior long-term growth in shareholder value isfeasible only with creation of 10X value for customersthrough strategic or product innovation, sharing part of the value with customers and capturing part of thevalue in attractive profitability. Ultimately, 10X valuecreation is strategically liberating: Virtually all compa-nies, even large corporations in mature industries, havethe potential of creating superior long-term returns fortheir shareholders. +

Reprint No. 97302

Resources

Paul Leinwand and Cesare Mainardi, “The Coherence Premium,”Harvard Business Review, June 2010, Reprint R1006F,www.booz.com/global/home/what_we_think/capabilities_driven_strategy/hbr_article: Takes the concept of focus further by showing howaligning strategy, capabilities, and products and services leads to a long-term “right to win” in the market.

Charles E. Lucier and Amy Asin, “Toward a New Theory of Growth,”s+b, Winter 1996, www.strategy-business.com/article/8660: Paved the wayfor this article by asserting that increasing revenue is not enough; 10Xshareholder-value growth requires strategic innovation.

Kenichi Ohmae, “The Godzilla of the New Economy,” s+b, First Quarter2000, www.strategy-business.com/article/10401: A prescient look at therapidly growing 10X-value companies of the turn of the century: Amazon,Nokia, eBay, Docomo, Cisco Systems, and more.

For more thought leadership on this topic, see the s+b website at:www.strategy-business.com/strategy_and_leadership.

company rejected the idea of a “Walmart” or by GaryWendt and Larry Bossidy in building GE Capital acqui-sition by acquisition during the 1990s. We are not say-ing these leaders had a vision that popped fully formedinto their minds, but they did have the commitment torefine the idea until it succeeded, the willingness tomake mid-course corrections, and the ruthless executionto make the financials attractive while evolving along agrowth superhighway. Although the CEO usually playsthe champion’s role in small entrepreneurial companies,in large companies the role does not have to be playedby the CEO (for example, at GE Capital it was playedby the head of the business).

The CEO plays three critical roles in the creation ofsuperior value for shareholders. He or she sets the objec-tive of truly superior (top 10th or 20th percentile) long-term returns to shareholders. He or she evaluates theopportunities for 10X value creation across the businessunits, betting on no more than one or two prospectivegrowth engines and adjusting the bets as new informa-tion comes to light. Finally, the CEO ensures that man-agement processes, incentives, and leadership of the tar-geted bets support 10X value creation.

In our discussions with CEOs of large companies,their major concern is risk: How likely is an innovativegrowth strategy to succeed? What is the downside if itfails? Our response is that if the CEO’s objective is top10th or 20th percentile long-term returns to sharehold-ers, then there is no real alternative to a 10X value cre-ation strategy.

Because 10X value creation strategies typicallyinvolve pilot programs to refine the concept, signifi cantfinancial commitments may not be required initially.The downside of the pursuit of an innovative strategythat is ultimately unsuccessful is less the financial lossthan the loss of time and management attention thatwould have been used more productively elsewhere.Partially successful 10X value creation strategies can stillproduce excellent returns for shareholders, albeit returnssustained for a shorter period of time (because competi-tors can match the innovation quickly) or fall “only” inthe 70th or 80th percentile. For example, Procter &Gamble Company spends heavily on tech nology to

Illu

str

ati

on

by

Jo

hn

He

rse

y

BY DON TAPSCOTT

stra

teg

y &

com

pe

tition

24

Rethinking

(or Why Michael Porter Is Wrong about the Internet) in a Netw

stra

teg

y &

com

pe

tition

25

For decades, the starting point for strategic think-ing has been the stand-alone, vertically integrated cor-poration. These powerful companies do everything fromsoup to nuts and dominate the competitive landscape. Wethink of them as intrinsic to the economy, and they pro-vide the context for theories about competitive strategy.

Companies prospered with this model of produc-tion because it was cheaper and simpler for them to per-form the maximum number of functions in-house,

rather than incurring the high cost, hassle, and risk of part-nering with outsiders to execute vital business activities.

This is no longer true.The CEO of Boeing Company says his company is

no longer an aircraft manufacturer; it has become a sys-tems integrator. Mercedes-Benz doesn’t build its own E-Class cars; the Magna Corporation does the work,including final assembly. IBM has become a computercompany that doesn’t really make its computers; its part-

Strategy

The Harvard strategy guru errs when he says partnerships erode competitive

advantage. Instead, they are now central to business success.

orked World

stra

teg

y &

com

pe

tition

26

stra

tegy

+bu

sine

sssp

ecia

l iss

ue, a

utum

n 20

10

ner network does. Indeed, we are seeing spectacular growth in contract

manufacturing — with companies such as Celestica,Flextronics, and Solectron partnering with computerand telecommunications vendors to provide core elec-tronics manufacturing services. Virtually overnight, thetop five contract manufacturing firms have achievedaggregate revenues of more than US$50 billion, averag-ing return on invested capital of more than 25 percent.

All of this is possible because of networking —specifically, the Internet. This deep, rich, publicly avail-able communications technology is enabling a new busi-ness architecture that challenges the industrial-age cor-porate structure as the basis for competitive strategy. Mycolleagues at Digital 4Sight and I have studied hundredsof different examples of this architecture, what we call abusiness web, or b-web. We define it as any system com-posed of suppliers, distributors, service providers, infra-structure providers, and customers that uses the Internetfor business communications and transactions. B-websacross industries, in which each business focuses on itscore competence, are proving to be more supple, inno-vative, cost-efficient, and profitable than traditional ver-tically integrated competitors.

Established companies, not dot-coms, are the mainbeneficiaries of b-web thinking. Successful businessessuch as Citibank, Herman Miller, Dow Chemical,American Airlines, Nortel Networks, and Schwab arenow transforming themselves by partnering in areas thatwere previously unthinkable. The perfor mance advan-tages of a b-web also explain why new Internet-basedcompanies such as eBay, Travelocity, E-Trade, andAmazon are growing dramatically and competing welldespite volatility in their stock prices. And b-webs ex -

Don Tapscott

[email protected] is president of the New

Paradigm Learning

Corporation and cofounder of

Digital 4Sight, a company that

designs and implements new

business models for corpora-

tions. He is the coauthor, with

David Ticoll and Alex Lowy, of

Digital Capital: Harnessing the

Power of Business Webs

(Harvard Business School

Press, 2000).

Originally published Third

Quarter 2001.

plain why an upstart e-business entity like Napster iswreaking havoc in the music industry, and why opensource software such as Linux poses a huge threat toMicrosoft.

Profound changes to the deep structures of the cor-poration are under way. Yet most of this underlyingrestructuring has been either unnoticed or underappre-ciated by the financial media and business schools. Theyremain shell-shocked at the rise and collapse of theNasdaq. And since “Nasdaq” and “New Economy” areso frequently (but incorrectly) used interchangeably, the Nasdaq collapse is often cited as proof that the NewEconomy is a bogus notion. (See “Six Reasons There Is a New Economy,” page 28.) As for eBay, Amazon,Linux, Napster, and others, they are dismissed asInternet aberrations.

Michael Porter’s obituary for the New Economy,“Strategy and the Internet,” published in the March2001 Harvard Business Review, is typical of this think-ing. In it, Porter exhorts business leaders to “return tofundamentals” and abandon thoughts of “new businessmodels” or “e-business strategies” that he says encouragemanagers “to view their Internet operations in isolationfrom the rest of the business.”

When a politician makes a motherhood statementthat receives wide support, pollsters say it “resonateswith” the voters (i.e., it’s considered credible and is con-sistent with citizens’ values). Such is the appeal ofPorter’s article. Profitability still counts. True economicvalue, measured by sustained profits, is the arbiter ofbusiness success — not eyeballs, stickiness, hits, or evenmarket share. To compete, companies must operate at alower cost and/or command a premium price, eitherthrough operational effectiveness or by creating unique

stra

teg

y &

com

pe

tition

27

value for customers. Being a first mover does not guaran-tee competitive advantage over the long haul.

Unfortunately, he uses these truths to prop up afalse thesis. Because corporate objectives remainunchanged by the Net, Porter argues, the best methodsof achieving these goals, including operating within avertically integrated structure, must be unchanged, too.