Savings Capacity of the Vulnerable Groups

4

Savings capacity of the vulnerable groups One of the indicators of economic buoyancy is the savings capacities of the vulne rable groups . The analyses of the vulnerabl e groups abili ty to sav e are made for the period of before and after micro credit use and the result portrayed by figure 5:10. FIGURE 5:10, SAVINGS CAPACITIES 0 10 20 30 40 50 60 70 80 90 79.27 0 81.71 77.44 12.19 24.39 13.41 12.19 8.54 34.15 4.88 9.15 0 26.83 0 1.22 0 14.43 0 0 PERCENTAGE SAVINGS CAPACITY (=N= 000) None (0) 1 to 50 51 to 100 101 to 150 151 to > 200 Source: Data analyses 2013 Figure 5:10 shows that the pattern of borrowers saving capacities after micro loans use is diff erent from the other three categori es. The borrowers savings capacity after using the micro loans have all gone above the amount of =N=25,000.00 and

Transcript of Savings Capacity of the Vulnerable Groups

7/29/2019 Savings Capacity of the Vulnerable Groups

http://slidepdf.com/reader/full/savings-capacity-of-the-vulnerable-groups 1/4

Savings capacity of the vulnerable groups

One of the indicators of economic buoyancy is the savings capacities of the

vulnerable groups. The analyses of the vulnerable groups ability to save are made

for the period of before and after micro credit use and the result portrayed by

figure 5:10.

FIGURE 5:10, SAVINGS CAPACITIES

0

10

20

30

40

50

60

70

80

9079.27

0

81.71

77.44

12.1924.39

13.41

12.19

8.54

34.15

4.889.15

0

26.83

0

1.22

014.43

0

0

PERCENTAGE SAVINGS CAPACITY (=N= 000)

None (0)

1 to 50

51 to 100

101 to 150

151 to > 200

Source: Data analyses 2013

Figure 5:10 shows that the pattern of borrowers saving capacities after micro loans

use is different from the other three categories. The borrowers savings capacity

after using the micro loans have all gone above the amount of =N=25,000.00 and

7/29/2019 Savings Capacity of the Vulnerable Groups

http://slidepdf.com/reader/full/savings-capacity-of-the-vulnerable-groups 2/4

moved to fall within =N=26,000.00 to =N=201,000.00. Whereas, the borrowers

before, the non-borrowers before and the non-borrowers after portray similar trend

of savings capacity where savings capacities within the low range of =N=1,000.00

to =N=25,000.00 remind very high and higher amount savings of =N=51,000.00

to =N=100,000.00 has gone low. Among these three groups savings from

=N=101,000.00 and above all remained zero.

5.10. Side Effects of Micro Credit scheme analyses

Side effects of the NACRDB micro credit scheme in Borno State were assessed on

both the beneficiary and non-beneficiary vulnerable groups. The data obtained are

analyzed by figure 5:11.

FIGURE 5:11. SIDE EFFECTS OF MICRO CREDIT

7/29/2019 Savings Capacity of the Vulnerable Groups

http://slidepdf.com/reader/full/savings-capacity-of-the-vulnerable-groups 3/4

14.41

6.69

5.5 5.675.99

13.51

7.86

13.22

4.56

5.96

16.64

0

2

4

6

8

10

12

14

16

18

SIDE EFFECTS OF MICRO CREDIT %

Figure 5:11 shows that over-proud by the micro loan borrowers have been the

greatest side effects of micro credit impacts. This is followed by too dependence

on the micro loan as a development variable. Increased land dispute, corruption

and bribery are also significant side effects. The other side effects are moderately

adverse, while rubbery cases take the least side effect but the most dangerous

among all.

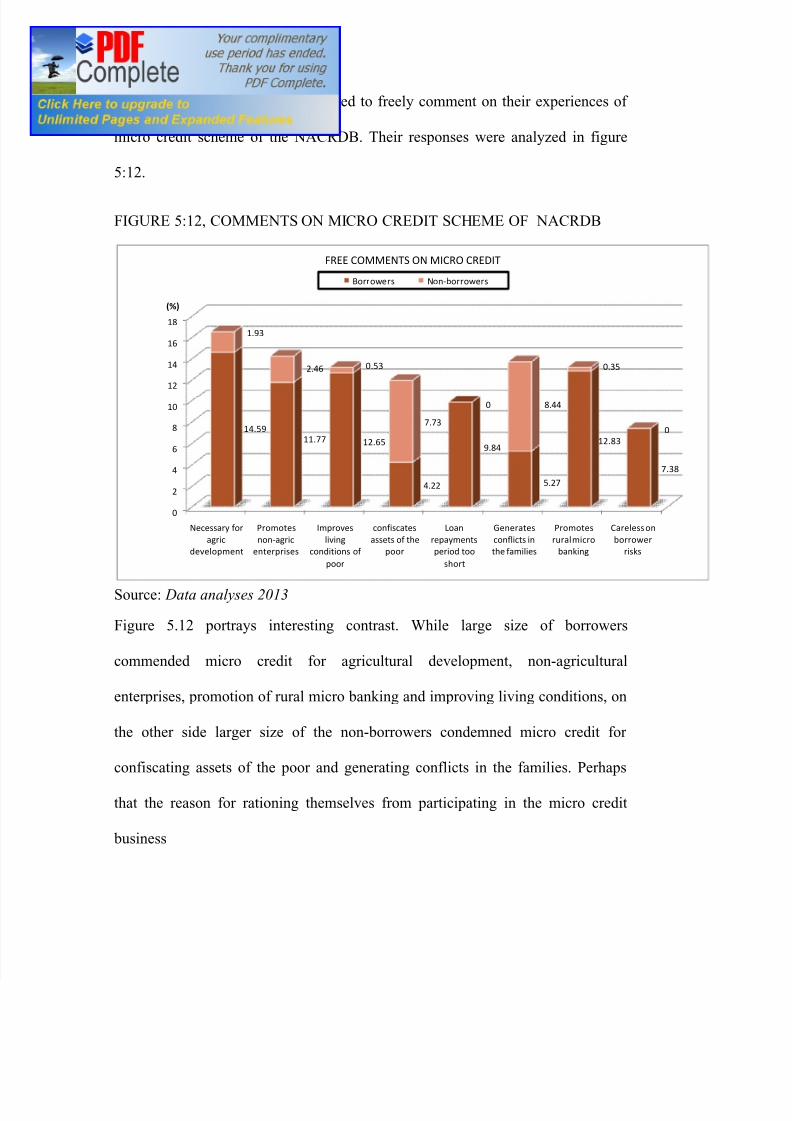

5.11. Free Comments on Micro Credit Scheme Analysis

7/29/2019 Savings Capacity of the Vulnerable Groups

http://slidepdf.com/reader/full/savings-capacity-of-the-vulnerable-groups 4/4

The vulnerable groups were requested to freely comment on their experiences of

micro credit scheme of the NACRDB. Their responses were analyzed in figure

5:12.

FIGURE 5:12, COMMENTS ON MICRO CREDIT SCHEME OF NACRDB

0

2

4

6

8

10

12

14

16

18

Necessary for

agric

development

Promotes

non-agric

enterprises

Improves

living

conditions of

poor

confiscates

assets of the

poor

Loan

repayments

period too

short

Generates

conflicts in

the families

Promotes

rural micro

banking

Careless on

borrower

risks

14.59

11.77 12.65

4.22

9.84

5.27

12.83

7.38

1.93

2.46 0.53

7.73

0 8.44

0.35

0

(%)

FREE COMMENTS ON MICRO CREDIT

Borrowers Non-borrowers

Source: Data analyses 2013

Figure 5.12 portrays interesting contrast. While large size of borrowers

commended micro credit for agricultural development, non-agricultural

enterprises, promotion of rural micro banking and improving living conditions, on

the other side larger size of the non-borrowers condemned micro credit for

confiscating assets of the poor and generating conflicts in the families. Perhaps

that the reason for rationing themselves from participating in the micro credit

business