Saurashtra Universityetheses.saurashtrauniversity.edu/650/1/vora_ap_thesis...IMPACT OF SELECTED...

268

Saurashtra University Re – Accredited Grade ‘B’ by NAAC (CGPA 2.93) Vora, Ashish P., 2008, “Impact of Selected Banking System on Small Scale Industries with Special Reference to Gujarat”, thesis PhD, Saurashtra University http://etheses.saurashtrauniversity.edu/id/eprint/650 Copyright and moral rights for this thesis are retained by the author A copy can be downloaded for personal non-commercial research or study, without prior permission or charge. This thesis cannot be reproduced or quoted extensively from without first obtaining permission in writing from the Author. The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the Author When referring to this work, full bibliographic details including the author, title, awarding institution and date of the thesis must be given. Saurashtra University Theses Service http://etheses.saurashtrauniversity.edu [email protected] © The Author

Transcript of Saurashtra Universityetheses.saurashtrauniversity.edu/650/1/vora_ap_thesis...IMPACT OF SELECTED...

Saurashtra University Re – Accredited Grade ‘B’ by NAAC (CGPA 2.93)

Vora, Ashish P., 2008, “Impact of Selected Banking System on Small Scale

Industries with Special Reference to Gujarat”, thesis PhD, Saurashtra

University

http://etheses.saurashtrauniversity.edu/id/eprint/650 Copyright and moral rights for this thesis are retained by the author A copy can be downloaded for personal non-commercial research or study, without prior permission or charge. This thesis cannot be reproduced or quoted extensively from without first obtaining permission in writing from the Author. The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the Author When referring to this work, full bibliographic details including the author, title, awarding institution and date of the thesis must be given.

Saurashtra University Theses Service http://etheses.saurashtrauniversity.edu

© The Author

IMPACT OF SELECTED BANKING SYSTEM ON SMALL SCALE NDUSTRIES WITH SPECIAL REFERENCE TO GUJARAT

A THESIS SUBMITTED TO

SAURASTRA UNIVERSITY IN PARTIAL FULFILMENT OF THE REQUIREMENT FOR THE

DEGREE OF DOCTOR OF PHILOSPOHY

IN ECONOMICS

By ASHISH P. VORA Lecturer in Economics

C. Z. Patel College of Business and Management, Vallabh Vidyanagar.

Research Supervisor DR. VIBHA BHATT

Lecturer and Head , Economics Department,

P D M Commerce College, Rajkot.

November, 2008.

Ashish Pravinchandra Vora,

Lecturer: Economics,

C Z Patel College of Business & Management,

Sardar Patel University,

Vallabh Vidyanagar – 388 120.

CERTIFICATE

I hereby declare that the research work on “ Impact of selected banking

system on small scale industries with special reference to Gujarat” is

carried out by me individually this is my original work and it is not

submitted to any other universities for any other degree.

Ashish P Vora

Dr. Vibha Bhatt,

Lecturer & Head,

Economics Department,

P D M Commerce College,

Rajkot.

CERTIFICATE

This is to certify that the thesis entitled “Impact of selected banking

system on small scale industries with special reference to Gujarat” is a

bonafide research work carried out independently by Mr. Ashish

Pravinchandra Vora, Lecturer, C Z Patel College of Business &

Management, Vallabh Vidyanagar under my supervision during 2005 -

2008 in partial fulfillment of the requirement of the award of the degree

of Doctor of Philosophy and the thsis has not formed the basis for the

award previously of any degree, diploma, associateship, fellowship or

any other similar titles.

Dr. Vibha Bhatt

ACKNOWLEDGEMENT

I am highly indebted to my supervisor and guide Dr. Vibha Bhatt, Professor, P D M

Commerce College, Rajkot for without her help and constant guidance I would have

accomplished nothing.

I would like to offer my deepest gratitude to my younger brother Mr. Jayesh Vora for his

support and assistance, without his help this mammoth task would not have been

possible.

I offer my humble pranams to my Dada - Dadi, Nana – Nani, my mother Vijayagauri P.

Vora & my father Pravinchandra T Vora for being there always when I needed their

blessing and support. They are the source of my inspiration and strength. I am special

thankful to my younger brother Jayesh Vora for he has been with me in all my

endeavours, motivating me to march ahead and also thankful to my brother Subodh Vora,

Mr. Sureshbhai Yagnik, Mrs. Chandrika Yagnik, Ms Abhaya and Mr. Sagar for showing

keen interest in my work.

I express my sincere thanks to my well wishers Dr. Sonalde Desai and Dr. Smita Zala for

keeping me steady on my work track with their inspiring words and good wishes.

My special thanks are due to the following bank officials who supplied me adequate data

and the necessary information for my research. They are

Mr. V R Pandey, Asst. Manager, Union Bank of India, Ahmedabad.

Mr. D M Patel, Chief Manager, Union Bank, Main Branch, Ahmedabad.

Mr. D T Nathan, Senior Manager, Dena Bank, Ahmedabad.

Mr. R J Patel, Lead District Manager, SLBC Dena Bank, Surat.

Mr. Anil Purohit, Lead District Manager, Dena Bank, Mehsana.

Mr. Bhagwati Patel, Lead Bank Manager, Surat.

Mr. Mahesh Patel, Lead District Manager, Godhra.

Mr. Arvind S Patel, Senior Manager, Bank of Baroda, Ahmedabad.

Mr. Yagnik, Lead District Manager, Rankot.

I take this opportunity to express my sincerest gratitude to the authorities of Charutar

Vidya Mandal, Dr. Nikhil Zaveri and Principal Dr. Atul Bansal for providing me

facilities and help to carry out my research work.

I am also thankful to Mrs. Niranjanaben and Mr. Navalsinh Chauhan, Reference

Department, Gujarat Vidyapith Library, Ahmedabad for their valuable service.

I also acknowledge the help by Dr. Ketki Nagar, Dr. Dhavla Ketan Diwan,

Mrs. Shehnaz Shaikh, Ms. Rakhi Thakur, Mr. Sanjiv Sharma, Ms. Sudhadhara Shamal,

Mr. Devranjan Hota, Mr. Jayesh Mehta, Mrs. Preeti Mehta, Mrs. Bhavna Padhya, Mrs.

Malini Sukesh Shah, Dr. Nayanjeet Chaudhary, Mrs. Reema Chaudhary, Mr. Kamyadeep

Chaudhary, Mr. Hiren Unadakat Mr. Rajiv Patel, Mr. Mehul Parmar and Dr. Raju

Chaudhury, And last but not list my dear and darling students.

TABLE OF CONTENTS

Sr. No Title

Pate No.

1 Sectoral Credit Concepts and Overview 1

2 Research Frame Work 21

3 Small Scale Industries: An Introductory Framework 28

4 Sub Regional Analysis 71

5 Finding, Suggestions and Conclusions 246

1

Chapter 1

Sectoral Credit-Concepts & Overview

Sr. No Title

1.1 Introduction

1.2 Characteristics of Credit

1.3 Kinds of Credit

1.4 Importance of Credit

1.5 Need of Credit

1.6 Financing of Small & Medium Enterprises (SMEs): Indian &

Global Scenario

2

1.1 Introduction:

Credit has assumed wide significance as an important instrument of promoting

and sustaining economic growth of modern economies. It constitutes the foundation upon

which the financial and through it the real investment in the economy is determined we

have transcended the narrow confines of money economy and we enjoy the vast horizon

of credit money economy. Although money is the basis of credit creation by the banks in

the economy, on account of the increasing importance of credit in modern tome it is held

by many that man today is living in a credit money economy. This aspect of the

contemporary economics life has been discussed by many economists, such as Willis and

Hawtrey. These economists regard money as a substitute for credit, rather than regard

credit as substitute for money. According to them, credit is characteristics of a system

whereby exchanges are normally effected. There are other who regard credit as a means

of transferring capital. John Stuart Mill wrote that from the point of view of society credit

merely transfers capital that is already in existence. Of itself it is not capital any more

than it is not capital any more than if is money, all it does is to put the present capital in

to the productive hands.

The word credit has been derived from the Latin word Credo, meaning “I

believe”. Credo, however, is a combination of the Sanskrit word Cred, meaning “trust”

and the Latin meaning “I place” according to Wingfield Stratford, credit is “nothing more

or less on the stock exchange than before the alter, is the substance of things hoped for,

the evidence of things not seen”. According to William Stanley Jevons, credit is ‘nothing

but the deffering of payment’. According to Cole, “Credit is purchasing power not

derived from income, but created by financial institutions either as an offset to idle

incomes held by depositors in the banks, or as a net addition to the total amount of

purchasing power”. It is in this sense that the term credit is used in current monetary

discussion.

3

1.2 Characteristics of Credit

When credit to an individual or business enterprise is provided the credit has

some salient features which are important. These characteristics of credit are being

discussed as given under:-

(1) Confidence

The basis of credit is confidence. No person will part with his goods in exchange

for a provide to pay money unless he has trust or confidence in the ability and will of the

debtor to make payment when it becomes due.

(2) Capacity

The paying capacity of the borrower affects the credit. Creditor must satisfy

himself with regard to the ability and paying capacity of the borrower before making

loans and advances. The reputation of the borrower and ability to repay is based on

certain personal qualities, training and successful experience. He gives reasonable

assurance to repay the advances in time.

(3) Goodwill

Goodwill of debtor is another salient feature of credit. It also affects the amount of credit

to be extended by the creditor. If a person has a goodwill that he will repay its out

standing credit in time then he will get the credit without any difficulty. The goodwill is

based on the character of the borrowers.

(4) Securities

General credit is provided by banks. Before granting credit bank has to see

whether the debtor has proper securities or not. If the debtor or borrow has adequate

property and assets at his disposal, then he will be given loan by the bank.

4

(5) Size of Credit

Availability of credit is also depends on the amount of credit generally credit of

small size is easily available but the sanction of large amount of credit taken time and

various formalities are to be completed.

(6) Period of credit

The period of credit also affects the availability of credit. Short period and

medium period credit is easily sanctioned by banks and other financial institution. But the

long term credit is not easily available as it involves risk because future is uncertain and

repayment requires more time.

Thus we can say that credit is affected by the various factors. The relations

between creditor and debtor are more important. Besides these factors goodwill of the

borrower, period of credit and amount of credit are taken into consideration by creditor

before sanctioning the amount of credit.

1.3 Kinds of credit

In modern times credit is required for many purposes and is employed by almost

every sector of the economy. Indeed the demand for credit is ubiquitous in the economy.

In the developed countries of the west the purchases of most customer durables – cars we

see on the roads, refrigerators used in the kitchen, the T.V. sets in the drawing rooms and

the like – are all financed by banks and other financial intermediaries. Producers

undertake production on a large scale by depending upon the banks to finance the

purchases of raw materials, wage payment by seeking overdraft and cash credit since it

permeates throughout the economy, but as a rough approximation to classification, on the

basis of the use to which it is put credit can be classified into industrial credit,

commercial credit, agriculture credit, etc. according as it is used to finance the

development of industry, commerce, agriculture etc. On the basis of the period for which

credit is repaid advanced we have short period credit which is replying after the period of

few days or a few months, and long period credit which is repayable after a period of few

years. We may also have productive credit advanced by the banks to the entrepreneurs to

5

finance their business development plans in the form of undertaking new investment

activity or extension of existing plant capacity and the consumer credit advanced to the

consumers to the finance purchases of consumer durables. When credit helps in

increasing the productive capacity in the economy, it is called productive credit or

investment. While the industrial credit is taken and advanced for long period to finance

the purchase of fixed capital goods, the commercial credit is given and taken for a short

period of few months to finance trade and commerce or to finance the working capital

requirement of the industrial units. The difference between the commercial and industrial

credit is important for no company can safely use funds for fixed investment which it

obtains for short term because long term assets cannot pay of short term debts. The

German standstill agreements, for instance, had their origin in such a situation. For a

decade prior to 1931 German banks had obtained short term credit from abroad which

had been used to acquire long term asset at home.

Beside long and short period credit, there is the medium-term and demand credit.

Medium-term credit stands midway the long and short term credit. It has a maturity

extending over year but less than five years. Thus it follows that a long term credit is

generally that which matures after five years while short term credit is extended for less

then a year. Demand credit is a loan which is payable to the creditor on demand. The

example of a demand credit is call loan which can be asked to be repaid at any time. A

demand credit can only be utilized for the financing of such assets which can be readily

converted in to cash at any tome the call is received from the creditor.

Loans are generally granted by the banks and other financial agencies against the

security of tangible assets pledged by the borrower in favor of the lender bank. The goods

or bond etc. so pledged are known as collateral securities. Loans may however, be

granted without requiting the borrower to furnish any collateral security. The first

category of loans are known as secured loans while the second category of loans are

called unsecured loans.

On the basis of the type of the borrower credit can be classified as individual

credit, business credit and government credit. Government credit is used by the central,

state and local governments. The following table summaries the kinds of credit.

6

Kinds of Credit

Purpose Maturity Borrower Security

1. Industrial 1. Long-term 1. Individual 1. Secured

2. Agriculture 2. Medium-term 2. Business 2. Unsecured

3. Commercial 3. Short-term 3. Government

4. Consumption 4. Demand or call

1.4 Importance of credit

Credit has become so important in modern society that to imagine of a modern

economy without credit is a misnomer. Today almost all bullk economic transaction are

settled by means of credit instruments. By a mere stroke of pen on a bank cheque

transaction involving large sums of money are settled without involving any money

payment. Credit is frequently called “the life-blood of business” and it true if we ponder

over the function performed by credit in modern times.

The credit system, embracing the instruments, agencies, customs and laws

concerned with the granting of credit and the collection of obligations, has developed

rapidly in extent and technique during the last hundred years. Deniel Webster has

described the significance of credit for a modern economy in most forceful words. He

says that “credit has done more-a thousand times more-to enrich nations than all the

mines of the world. It has excited labor, stimulated manufactures, pushed commerce on

every son, and brought every nation, every kingdom and every small tribe the races of

man to be know to all the rest “

Explaining the importance of credit the well-know classical economist, john

Stuart mill writes: “….though credit is but a transfer of capital from hand to hand, it is

generally, and naturally a transfer to hands more competent to employ the capital, more

efficiently in production. If there were no such thing credit, or if from general insecurity

or want of confidence, it were scantily practiced, many persons who possess more or less

capital, but who from their occupations, or for want of the necessary skill and knowledge,

cannot personally superintend its employment would no benefit it; their funds would

either be idle, or would be perhaps wasted and annihilated in unskillful attempts to make

7

them yield a profit. All this capital is now lent at unskillful and made available for

production. Capital thus circumstanced forms a large portion of the productive resources

of any commercial country; and is naturally attracted to those producers or traders who

being in the greatest business, have the means of employing it most advantage; because

such are both the most desirous to obtain it and able to give best security. Although

therefore, the productive funds of the country are not increased by credit, they are called

into a more complete state of productive activity. As the confidence on which credit is

grounded extends itself means are developed by which even the smallest portions of

capital, the sums which each person keeps by him to meet contingencies, are made

available for productive uses.

Credit serves the economy in many ways which may be summarized as following.

1. Credit provides a convenient and economical medium of exchange by

supplementing or superseding other forms of money. It saves the community the

cost of acquiring large sums of standard money, the labor and cost involved in

handing metals, and the loss through were and tear incidental to the use of

precious metals. It renders the monetary system of the country elastic by

permitting expansion and contraction of the fiduciary money supply based on the

metallic reserves.

2. Credit facilitates the production and exchange of goods and services in the

economy. It enables the state to finance its expenditure for routine and socialized

activities far in excess of its immediate revenues. It enables honest person with

business managers to adjust the volume of capital employed to the changing

requirement of their enterprises. It increases the scope of sales of goods and

services. It makes the expansion of markets and productive activities possible.

3. Credit also increases consumption. Through installment credit consumers are

enabled to enjoy consumption of a large range of goods. With the increase in

demand consequent upon the extension of credit facilities the commodity market

becomes broad enough to warrant the large scale production with consequent

upon the extension of credit facilities the commodity market becomes broad

enough to warrant the large scale production with consequent in costs. This result

8

in raising the standard of living and converting future income into the present

purchasing power.

4. Credit promotes thrift by productive employment for saving. Thus by promoting

saving, credit encourages capital formation in the economy which is essential for

the economic development of the economy.

5. Credit facilitates development of large scale enterprises and specialized industry

by encouraging the assembling of substantial amount of capital. The corporate

from of business organization whose security issues are handled through

specialized credit institutions like the bank, insurance companies, investment

trusts etc, have become outstanding features of modern capitalist society.

6. Credit makes the optimum use of economy’s capital resources possible. Trough

the use of credit not only are the funds formed together; they are also apportioned

between the different competing uses in the most efficient manner. The borrower

is a more efficient producer then the lender because had the latter been more

efficient he could use capital formed as result of saving in his own productive

activities. When by means of credit the funds are given to those who pay the

highest price in the form of interest control of the productive capital is entrusted

to those who are most likely to provide additional consumer commodities for the

community at low cost of production.

7. By influencing the rate of capital formation credit influences output and

employment in the economy. Expansion of credit helps to pull the economy out of

depression while a restriction of it may exercise a restraining influence upon

boom. A cyclical expansion of credit by the banks and other credit institutions

may accelerate the employment of unused factors and thus help in increasing the

output which may stimulate spending and saving and vice versa.

8. Credit enables the financial system to render its two-fold service by providing a

system of exchange and a system of capital supply. It enables the debtor use

something which he does not yet own completely i.e. it enable him to extend

control as distinct from economic ownership over goods.

9. Credits benefit lenders in at least two ways. Firstly it enables them to earn income

on their saving. Apart from benefiting the individual sever lender it also benefits

9

the society in as much as by stimulating saving it promotes capital formation

which is vital for economy’s growth. Secondly, it helps the saver-lender to get

greeter total utility or satisfaction from his life-time income by deferring

consumption from a time when it would yield him less satisfaction to a time when

it would him more satisfaction. He first sacrifices some consumption and saves

and lends; later he dissaves by selling his debt clam and uses the proceeds for

consumption securing satisfaction.

1.5 Need of Credit

On the demand side of the economy are the consumers of goods and service who

require funds basically for acquiring certain consumer durables. The credit facility

offered to the households will generally be in the form of auto- finance, education loans,

credit card loans housing loans, and for the purpose of other consumer durable items.

Loans will also be provided to individuals against other financial and real assets. Except

for the housing loans all the other types of individual loans range bound in short term.

Similarly, on the supply side also, the credit market provides funds to the

corporate though for entirely different purposes. Corporate basically fonds for project

finance while initiating investment plan and working capital finance for their day-to-day

operations.

Credit extended for project finance would enable the corporate to acquire real

assets, plant and machinery, technological expertise, etc require for expansion /

modernization / diversification purposes. In certain cases, where the project is very large

and the funds can not be provided by a single situation, consortium lending will be

resorted to in this facility, two more intermediaries will join together to finance large

project proposals. Such funding requirements will generally arise while financing large

infrastructure project, petroleum projects etc.

In addition to long-term requirement, firms would also require short-term funds

for meeting their working capital requirements. Firm require these funds. To meet their

day-to-day operational requirements and for maintaining adequate levels of current assets

since these funds support the daily operations of the firm, they are required on a

continuous basis. The financial assistance for the working capital requirements is

10

generally provided by banks in the form of cash credit (cc). overdraft facilities (od) and

bill finance

1.6 Financing of small and medium enterprises (SMEs): Indian and global

scenario

Overview

SMEs globally, have been recognized as a vital component of the domestic

economy and employment generation of a country, disregard of the geographical barriers.

According to a report by the World Bank, in low-income countries with GNP per capita

between $100 and $500, SMEs account for over 60% of GDP and 70% of total

employment. In the middle-income countries, they produce close to 70% of GDP and

95% of total employment. However, even in the era of globalization and liberalization,

SMEs continue to face increased challenges across the globe.

In the Indian scenario, small enterprises’ contribution to economy is 40% of the

country’s domestic production, about 50% of total exports and 45% of industrial

employment. The achievements and contributions of SME sector can be attributed to the

positive response and support of the Indian banking system to SME sector since early

seventies till 1991. Despite these positive features, SMEs are not able to exploit their full

potential. One reason for this is considered to be low credit penetration into the segment

caused by sub-optimal delivery of credit and services to the sector.

With the advent of economic reforms, the compelling statutory regulations and

compliance requirements against risk weighted assets, have forced the commercial banks

to change their direction in approaches to lending, which has resulted in a reduced

institutional credit flow to the SME sector. Thanks to the initiative of GOI through the

setting up of microfinance institutions like SIDBI and comprehensive policy package for

SMEs al along. The recent enactment in 2005 for the development of the SME sector is

another long-term measure, whereby GOI defined small and medium enterprises and

taken several initiatives for assisting the SMEs. The government of India has set an

ambitious target of doubling the institutional credit to SMEs by 2010. RBI has also put in

place several measures encouraging banks to step up their lending to SME sector

11

considerably. Realizing the importance of the sector for its contribution to domestic

economy and going by the policy initiatives of the government and directives of RBI, the

globalizes markets prompting banks to look for new business opportunities, have all

made the banks to take a re-look in financing SMEs. The markets for industrial products

and services and technological advancements across the globe also demand a better

performance on the part of the SMEs, to which the sector has started responding

positively.

Apart from institutional funding support at macro level reforms are also

considered essential, to usher in the growth of SME sector through intense financing by

banks and FIS. One of the present barriers is the 150% risk weight assigned to loans to

SMEs prescribed under the basal norms. There exists an urgent need for rationalizing

these norms to promote liberal financing of SMEs. RBI has already laid down guidelines

to classify loans to SMEs as retail loans, which attract only 75% risk weight, subject to

fulfillment of a certain criteria. In advanced countries like USA also, Basel II norms have

had their adverse impact on the promotion and prosperity of SMEs and there the

government is actively considering alternatives to overcome the barriers. Many other

countries like Sri Lanka, Bangladesh, and Korea also face new challenges in the wake of

the Basel II Norms and these countries seem to be exploring alternative bailout measures

for sustaining the development of SMEs.

Visionaries of economy advocate and stress the urgent need to regenerate SME

financing. According to World Bank study of “Firm Size and Business Environment in

SME Financing” ,SMEs across the world do face more or less common or similar

problems, due to inversely related factors, the problem areas being financing and

regulatory policies.

Financing agencies are focusing on new approaches like cluster approach to

achieve the twin objective of their own business growth and development of SME sector.

The objective is to ensure that the fruits of development are spread across a vast majority

of entrepreneurs and community and balanced regional development.

This book is an attempt to capture all relevant and contemporary issues and challenges

relating to SME financing, given its potential for employment generation and high

12

contribution to the economy, in Indian context as also in the developed, developing and

under developed economies. The contents of the book are divided into two sections

consisting of eight articals each.

Section I: Indian Perspective

The first article “SME Financing: The Indian Scenario” by Chakravati Anand,

mainly focuses on the financial help SME sector is receiving with the support of the

World Bank, besides explaining the characteristics unique to Indian SMEs.A loan of

$120 recently approved by the World Bank to the SIDBI is aims at improving SME

access to finance and business development services, thereby fostering SME growth.

Regenerating SME financing in India is essential as the sector serves as a Greenfield for

nurturing entrepreneurial talent. The setting up of Small Industries Development Bank Of

India (SIDBI) in April 1990 as the principal financial institution for financing and

developing SSIs , was a major step initiated by GOI towards promotion of the SMEs in

India.

Some of the instruments of financing that have been introduced to support SME

sector include Credit Guarantee Fund Trust for small industries, Micro Credit Capital

Funding, ME Fund, etc.The article concludes that an increased focus by Indian Banks and

financial institutions on providing micro finance, factoring assistance, etc., at reasonable

costs would go a long way in making SMEs domestically as well as globally competitive,

leading to economic growth.

“Policy Initiatives for Financing Small and Medium Enterprises”, the second

article by Garimella G K Murthy, focuses on the various policy initiatives for the

development and financing of small and medium enterprises the world over. In this

context ,the article discusses the defecations of and approaches to SMEs in a cross

section of countries in the world. The article also throws light on the various policy

initiatives on the part of the Government, RBI and banks in extending financial support

to SME sector on liberalized terms and thus indirectly contributing to the robustness of

the Indian economy. RBI has asked the banks to adopt the new definition of SME as

contained the SME Bill-2005.The enactment of the SME Bill in 2005 by government of

India, besides providing a thrust for intensifying the financing of SME Sector by Banks

13

and financial institutions, has also spelt out other measures to empower the SME sector

which is the progressive contributor to the economy. In a competitive environment, with

better management attributes being displayed by the entrepreneurs, banks, of late, have

started responding more positively to the financial needs of the SME sectors, which is a

redeeming feature.

The next article “Role Of The Government Agencies in the Development &

Financing of Small & Medium Enterprises” is by P Uday Shankar.It focuses on

government agencies involved in the promotion, financing and development of SMEs and

their functional areas ,highlighting the role played by them. The Government of India has

promoted a number of agencies for financing and development of SMEs ,like the

SIDO,NIESBUD,IIE,NSIC,NISIET and state level organization like DICs ,IIC,SC,BC

corporations, etc. ,each playing a distinct role. Apart from providing extension services

,some agencies ,are involved in the identification of entrepreneur specific projects vis-à-

vis business opportunities and prospects and also in the section of beneficiaries for

finance by banks/financial institutions ,for taking up various productive activities as wel

as support services like project implementation ;post project implementation assistance

;hand-holding ;monitoring and guidance and follow up .Agencies like SIDCO offer many

schemes for financing the entrepreneurs.

The fourth article “Role of Banks in the Development of SMEs”is by S Murli

and A Lakshminarsimha.It gives an overview of SME sector and analyzes the role played

by Indian Banks in its development. The perception of the SME clients and the bankers

about one another is not fully true and hence, it is important to bring about a change in

the mindset of both. Bankers should look beyond financing or lending and aim at

efficient and quick ‘customer service’ in serving SME clients. It is suggested that the

bankers hold clients’ meet regularly, in order to understand the needs and grievances of

SMEs and offer tailor- made products that would help in removing the bottlenecks in

their growth to a great extent. The later part of the article explains various strategies by

banks such as advisory services, KPO receivables finance etc., that can be extremely

useful for providing financial support to the SMEs.

14

The fifth article “Marketing Strategies of Banks to Foster Financing of SMEs

in India” by chakravarthi Anand and A Srikant, focuses on the marketing strategies of

banks to promote financing of Small and Medium Enterprises (SMEs)in India .It

explains, in detail, various marketing strategies including the communication options

being adopted by major Indian private banks like ICICI and HDFC as well as foreign

banks like Cities and HSBC, to shore up financing of SMEs. The article also highlights

the promotion of SME business and finance through innovation, specialization and e-

services, besides other financing methods. The article concludes on the note that

development of right strategies for marketing and measurement of performances are vital

for the success of any organization engaged in the SME financing activity.

Seok-Dong Wang in the sixth article titled The Development of E-Financing:

Implications for SMEs”, focuses on the recent trends in financial markets and the

implications of development in financial services for SMEs, across the globe, particularly

with regards to ICT, and provides some useful policy recommendations. With the rapid

globalization and emerging technologies, the potential contribution of SMEs has also

increased. However, many of the problems traditionally facing SMEs have become more

acute in a globalize environment. The spread of e-finance ranging from the basic to fully

integrated Internet Services, that has accompanied growing integration of financial

market, has also been highlighted in the article. While suggesting that a supportive policy

environment and better coordination can foster the adoption of Internet technologies to

promote SMEs and develop E-finance, the article concludes by stating that the advances

in ICT and low costs of the internet have made e-finance an ideal tool for SMEs across

the Globe, for seeking information and financing for growth.

The next article by S K Kar titled “SME Sector Needs Innovative Lending

Approach Under Basel II”, highlights the modifications carried out by Basel II ,in order

to focus on the market and operational risk exposures of banks and their implications for

SMEs in India. The article also explores the possibility of the SSIs being deprived of the

benefits of bank lending, in case the bank in India adopt the Internal Rating Based

Approach (IRB Approach) to measure and mitigate credit risk under Basel I.E. points out

that the fundamental flaw in Basel I was, that it was only dealing with the credit risk and

knowingly ignored the market and operational risk exposure of banks. Under the Basel

15

Capital Accord, loans to SMEs generally fall in the 100% risk –weight category.

If Banks prefer to rate these with the help of credit rating agencies, the maximum risk

weight for a highly risky SSI could be 150 %.However, in the above case, it is possible

that the banks have the option of not rating them and assigning to them a maximum risk

weight of 100% meant for unrated category.

The eighth article titled “SMEs in India: Future Perfect” by Amit Singh

Sisodiya, attempts to throw light on the tremendous challenges faced by SMEs to survive

and sustain, as the process of globalization and liberalization gathers momentum across

the globe. Small and Medium Enterprises (SMEs)have played an Important role in the

growth of economy for long. Some of the major challenges faced by SMEs include lack

of access to finance, low R&D investment, lack of access to technology, lack of product

innovation, increasing competition, etc. Earlier, banks were not showing showing interest

in financing SMEs due to problems attendant on them. Nowadays, though bankers are

wiling to extend loans to SMEs, efforts are still needed to improve cooperation between

SMEs and lenders. SMEs too ,on their part are gearing up to meet the challenges arising

out of the changing business environment. The article concludes on the note that the

above efforts have proved to be extremely promising for the SME sectors, which aims to

make it big in the realm of domestic as well as international business arena.

Section II: Global Perspectives

The ninth article “Informally financed SMEs” by Allan riding and brad belanger,

attempts to capture a crisp view of the financial support measures for SMEs that are in

vogue in Canada. Among the various sources of risk capital informal investments are the

single largest source of external equity capital for candian SMEs. This article focuses on

the small and medium-sized Enterprises (SMEs) that received financing fir risk capital

through the information markeeplase in Canada. The informal marplots in Canada are

composed of two types of investors; family or friends, and business angle (individuals

who invest their personal funds at arm’s length in businesses owned and operated by

individuals unrelated to them). It also discusses the differences between these two types

of investors and the impact of their investments on SMEs. The study concludes by stating

that firms financed by angles are considerably larger (suggesting higher levels of

16

historical growth) then other firms and are more likely to seek and receive other more

forms of financing including commercial loans. Firms financed by friend and family on

the other hand are less likely to have loan applications approved and are more likely to

resort to personal loans rather then commercial loans to finance their firms.

The tenth article “Securitization as a means to Enhance SME Financing and the

EIF’s Role as a Guarantor” by Allessandro tappi and pre-Erik Eriksson provides an in-

depth view of SME securitization in the context of application of securitization in the

area of SME financing and the advantages of securitization to SMEs. Securitization of

SME loans is the most efficient means of enhancing their access to debt finance as banks

achieve capital relief and free up capacity for new loans to SMEs by transferring their

credit risk to the capital markets in an effective manner. The successful SME lones

securitization programmed lunched in 1985 by the small business administration in the

US, can be regarded as a forerunner to European SME Securitization The potential for

securitization transactions of SME financing in the European countries by new

originators is huge and as securitized loans are standardized and liquid they are easily

marketable to a variety of investors. The article also explains the role of European

Investment fund in securitization transactions for supporting enhanced debt finance to

SMEs by facilitating the SME risk transfer from the originating banks to the capital

market.

The eleventh article “SME Financing in Japan: what we have found” by usages

lichiro while dealing with various perspectives relating to SME financing in Japan

provides an analysis of the behavior of SMEs particularly in financing activates, by using

a recently developed set of micro data on SMEs and examining statically regularities

observed in various aspects of SME financing Success or failure in obtaining finance

exerts a far greater and more direct impact on the fate of SMEs in Japan which are

primarily dependent on loans from financial institutions An observation of the selection

channel has found that companies with low return on assets (ROA) and equity ratios are

paying high interest rates and eventually defaulting This indicates that the mechanism of

natural selection works properly for SMEs Another important finding of the analysis is

that the effect of adaptation is a greater contributing factor then the effect of selection in

improving the financing environment for SMEs The article concludes on the note that the

17

current state of SME financing in Japan based on factors such as the availability of

collateral and / or personal guarantee and presence of the public credit guarantee systemic

generally conducive to improving the efficiency of credit allocation.

“Supporting SMEs in the pacific Region “ is the twelfth article contributed by

Stephen McCarthy. Most of the pacific region countries are classified as small vulnerable

Economies (SVEs) nevertheless they do have economic opportunities for growth and

development The main constraint for SME development in the pacific region is the

limited human resource skill and entrepreneurship and limited capacity for financial risk

taking arising from traditional land tenure and property rights systems which have been

explained in detail in the article An SME loan guarantee scheme has also been proposed

whish would allow existing banks in the region to guarantee a part of their risk of SME

lending in the expectation that it would increase the volume of such leading this article

discusses the common interest of the European investment bank (EIB) and the

commonwealth secretariat in supporting the growth of the private sector in particular

SMEs in the commonwealth small vulnerable Economies A more pro-active approach

involving Diaspora citizens in the economic development of their native country has also

been suggested as an effective tool towards promoting SME in the pacific region.

The thirteenth article “Problems of SME Financing in Russia” by Xavier bare is

based on a survey of 4350 SMEs in 80 subjects of the Russian federation in February-

April 2005 It revealed that financing rank third in the list of problems SMEs are facing

immediately after administrative barriers and problems related to real estate This article

discusses the market of SME financing in Russia resistance and problems involved in

extending credit to SME and also highlights the progress achieved due to SME lending.

Three banks KMB and vneshtorg bank which are aggressively expanding their

activities nationwide dominate the SME market Although every Russian banks a

potential lender to SMEs and most banks have even very limited experience in crediting

to small business the majority of Russian banks do not favor crediting to small size

enterprises for both cultural and regulatory reasons. The most notable working initiatives

in Russia are the regional authority’s initiative that provides guarantees to the SMEs the

USAID loan portfolio guarantee initiative started by Swiss contract. The article concludes

by stating that for many years the main source of SME finance came from international

18

finance institutions and donors and therefore the challenge before the Russian

government now is to increase capital flows commercial banks to the SME sector.

The fourteenth article “(small and medium enterprises ) financing in southeast

Asian nation” is by garimella G K Murthy and usha n raghunandan financing of small

and Medium Enterprises pose perennial challenges in ASEAN (Association of south east

Asian Nations) for want of financial measures both in terms of number and quality.

Having realized the contribution of SMEs to the economy the Governments in these

nations have of late put in place several initiatives to promote the SME to the economy

the Governments in these nation have of late put in place several initiatives to promote

the SME financing . Within ASEAN there is a wide gap in major sources of financing

between the Asian -6 and asian-4 countries. In asian-6 nations SMEs mostly rely on

formal channels of finances such as banks financial institution and non-banking finance

companies whereas in asian-4 countries the reliance is on non formal channels. This

article presents an overview of various challenges for SMEs pattern of government

assistance as also sources of finances available in AS EAN. The role of development

financial institutions as well as the capital markets in these two categories of nation to

support SMEs has also been discussed in the article.

The next article “SME financing in turkey “by usha N Raghunadan presents a

comprehensive view of the SME financing and related issued pertaining to Turkey. Small

and medium sized enterprises in turkey account for 99 percent of all enterprises about 75

percent of employment and more then 25 percent of value added. nevertheless their share

of bank loans is less then 5 percent The reasons are an inflationary economic climate and

increasing public sector debt leading to a lack confidence a series of financial crises a

sharp rise in real interest rates and marked deprecation of the Turkish lira.

This article attempts to explore the challenges facing the small and medium

Enterprises (SMEs) in Turkey and the initiatives undertaken by the government to

promote their development a range of policy initiatives included in the 8th five year

Development plan (2001-05) aimed at improving the productivity of Turkish SMEs and

enhancing their international competitiveness. Policies and strategies for SMEs such as

those forth in the “SME strategy and action plan” essentially seek to correct the

19

fundamental weaknesses of Turkey’s industrial SMEs but could place grater emphasis on

their existing and potential strengths.

The last article which is a summary of the research paper titled “potential

competitive effects of Basel II on banks in SME credit markets in the united state”

examines the likely competitive effects of the proposed implementation of the Basel II

capital requirements on bank in the market for credit to SMEs in the United States. Under

Basel II proposal the required capital for an SME loan would depend on a number of

factors include ding the probability of default (PD) and loss given default (LGD)

assigned by the bank whether the loan is classified as retail or corporate and the size of

the borrowing firm. It address in detail issues like how reduced risk weights for SME

credit extended by large banking organization that adopt the adman cede internal ratings

based (A-IRB) approach of Basel II could significantly affect the competitive position of

organizations that do not adopt A-IRB. The analysis also suggests that there will be only

a relatively minor competitive effect on the majority of community banks primarily

because the organization that are likely to adopt A-IRB tend to make different types of

SME loans to different types of borrowers then community banks The possibilities of

significant adverse effects on the competitive positions of large banking organizations

that do not adopt-A-IRB have also been discussed in the article.

This book has thus covered the current Indian and global perspective of SME

financing capturing the relevant futures and it hope that the readers will find it

informative and resourceful.

Conclusion on financing of small scale industries

Because of the significant place the SS1 sector occupies in our economy an

appropriate environment needs to be created for the growth and substance of the small

scale units. This call for steps to build on faming strength of small units. Overcome their

weakness. Availability of timely and adequate financial assistance is vital for the growth

of SS1 units. A multi-agency credit structure to fill the financial needs of small scale

units has evolved over the year.

20

References :

1. The economics of money and banking – L V Chandler.

2. Central banking – M H De Kock

3. Money, Credit and commerce – Alfrade Marshall.

4. Monetary theory – M C Vaish.

5. The wealth of nations – Adams Smith.

6. Economics of money and banking – G N Halm.

7. Modern Banking – R S Sayers.

8. Banking by 2000 AD – N Vinayakan.

9. Indian financial system – H R Machiraju.

10. Indian Financial policy – S S Tarapor.

11. Monetary planning in India – S B Gupta.

12. Indian banking systems – Board of Editors ICFAI University.

13. Schrader, H 1994 Formal and informal finance in contemporary India: Working

paper No 215, Sociology of development research centre.

14. Seibel, H D. 1989 Finance with the poor, by the poor, fore poor. Financial

technologies for the informal sector. With case studies form Indonesia K M,

Leisinger, P Trappe (ed.) Social strategies for chungsberichte 3, 2.

15. Kropp, E et al. 1989. Linking self help groups and banks in developing countries

Eschborn, GTZ – Verlag.

16. Germidis, D 1990 interlinking the formal and informal financial sectors in

developing countries. Saving and development.

21

Chapter 2

Research Framework

Sr No Title

2.1 The Research Problem

2.2 Objective of the Study

2.3 Research Methodology

2.4 Hypothesis

2.5 Significance of the Study

2.6 Limitations of the Study

22

2.1. The Research Problem:

The statement of the problem is "Impact /finances of selected Banking system on

small scale industries".

The small scale industries (SSIs) have a place of pride in our economy. They have

a high potential among others, for generating employment, dispersal of semi-urban and

rural areas, promoting entrepreneurship and earning foreign exchange.

Inadequate access to credit both short term and long term remains a perennial problem

facing the small scale sector. Finance has been a bug bear. Commercial banks have been

fulfilling only partially their commitments to the SSI sector. Even while assessing small

units, banks play safe by using conventional, objective yardsticks without appreciating

the owner-entrepreneur his enthusiasm, dynamism and innovative ability.

State finance corporations (SFCs), which lend long term funds, have also become

strict about lending particularly since many are deeply troubled by their own profitability

concerns. Small units can not access capital market because of their size and costs

involved the over the counter exchange of India (OTCET) promoted as the small

company's options, still excludes most of the small sector. There are endless hassles from

lending agencies while evaluation methods and in extending credit to small scale units.

2.2. Objective of the Study:

The broad objective of the research study is to analyse impact of selected banking

system on small scale industries. However, objectives of the study are as under:

1. To study Bank-wise allocation of credit plan for small scale industries.

2. To study importance of credit for SSIs.

3. To study Bank-wise achievement of credit of selected nationalized banks for SSIs.

4. To study the trend of finances of nationalized banks towards SSIs.

5. To study inter banking issues on evaluation and grant of credit to SSIs.

23

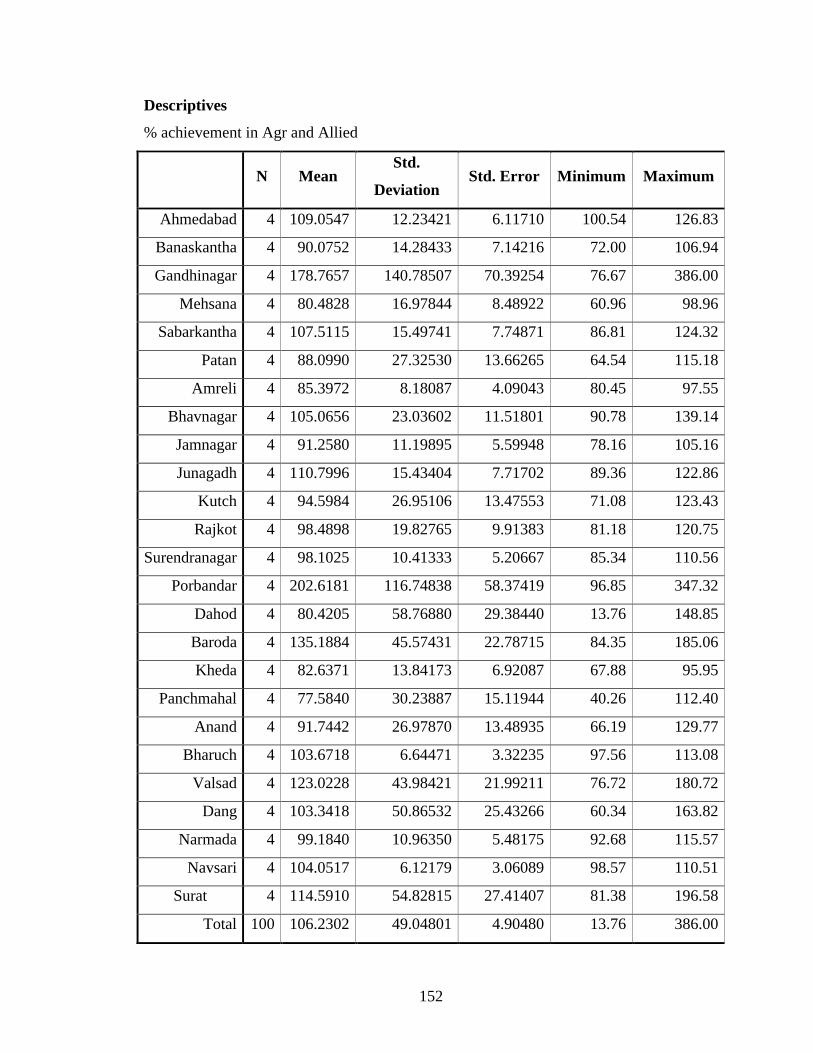

2.3. Research Methodology:

Research methodology is a way to systematically solve the research problem. It is

a science of studying how research is done scientifically. Research methodology includes

the following steps :

? Research Design

? Data Collection

? Tools and Techniques

? Limitations

? Chapter Plan

? Bibliography

? References/ Journals / Newspaper / Websites etc.

Research Design:

Research design is a conceptual structure within which research would be

conducted. It is a blue print of research work.

So far as this research concerns, the data on allocation and achievement of annual

credit plan of selected nationalized banks for small-scale industries should be taken. The

research work is done for the Gujarat state only. We have divided five regions and take

necessary data of the said five regions.

The tools and techniques of the research is the comparison of the data.

Data Collection:

The main source of the data collection is primary, secondary data. Secondary data

is collected from annual credit plan of five district bank report and state level banking

review reports.

For research purpose, 10 years data of nationalized banks viz., from 1997 to 2006

collected and analyzed as per various tools and techniques.

24

Tools and Techniques:

From the data about Target amount credit and achievement amount credit, we

have calculated the percentage achievements for agricultural and allied as well as smalls

scale industries.

For the region-wise and district-wise comparison of percentage achievement in

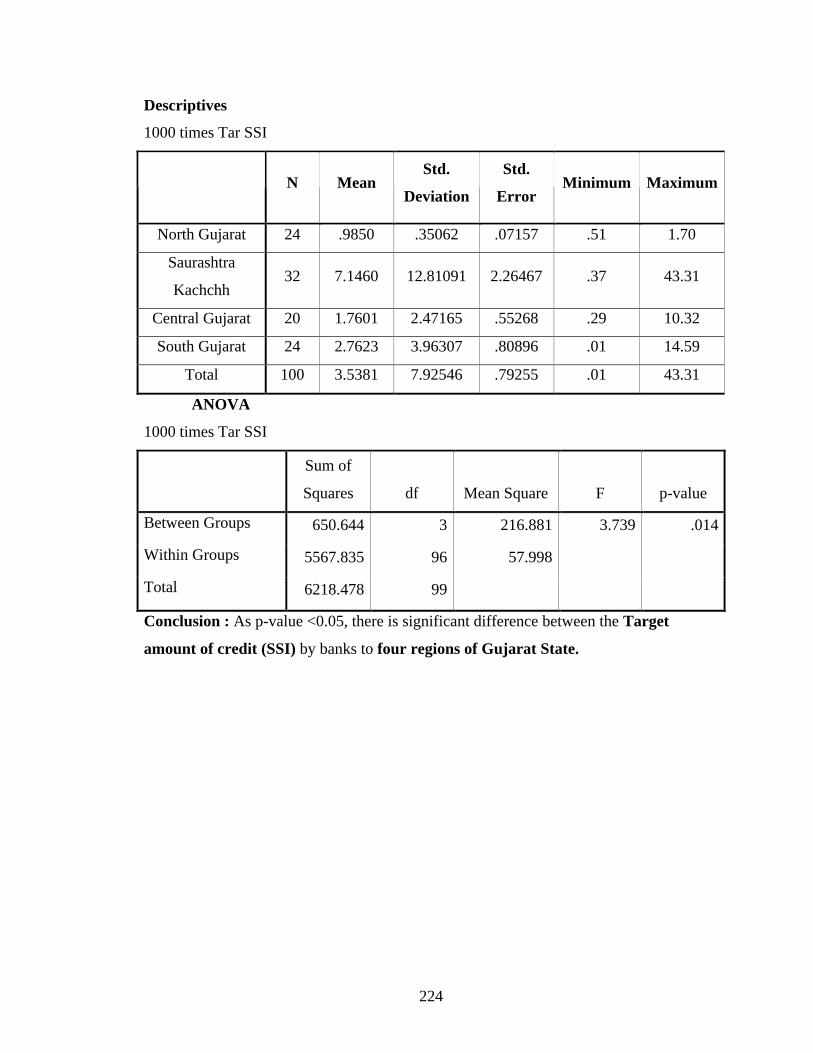

agricultural and allied industries as well as percentage achievement in SSIs, Analysis of

variance (ANOVA) technique is used.

2.4. Hypothesis:

Broader hypothesis of the study would be as under:

1) There is no significant difference between the target amount (Agri. and Allied)

credit to four different regions of Gujarat state.

2) There is no significant difference between the target amount (SSIs) credit to four

different regions of Gujarat state.

3) There is no significant difference between the percentage target amount (Agri.

and Allied) credit to four different regions of Gujarat state.

4) There is no significant difference between the percentage target amount (SSIs)

credit to four different regions of Gujarat state.

Universe of the study and sample design:

The universe of study consists of all nationalized banks working in Gujarat. We

have divided four region is Gujarat. The data should be collected from the nationalized

banks of all districts of Gujarat. Researcher has selected nationalized banks working in

the all districts of Gujarat.

Sample has been selected considering the following factors.

Data for the entire period of study i.e., from 1997to 2006 were collected from

nationalized banks of Ahmedabad, Mehsana, Panchmahal, Rajkot and Surat.

The nationalized banks should be managed by government of India.

25

2.5. Significance of the Study:

The topic for research has been selected in view of the following due

consideration:

1) The small-scale sector has a high potential for providing employment, dispersal of

industries, promoting entrepreneurship and earning foreign exchange to the

country. The above points demonstrate the importance of small-scale industries in

our economy. So small scale sector can not be ignore for the growth of Indian

economy.

2) Poor financing is the major drawback issues towards small scale industries.

Nationalized/commercial banks, state finance corporations (SFCs) co-operative

and Rural banks are strict about lending particularly small scale sectors.

3) There are endless hassles from private banks, lending agencies to finance, who are

otherwise meant for discouraging the development of small scale sector.

2.6. Limitations of the Study:

The limitation of the research study are as follows :

(A) The study should be based on secondary data collected from various reports of

leading nationalized banks and RBI bulletin. The limitation of secondary data, if

any, will also influence the study.

(B) The study should be based on nationalized bank belonging to Gujarat state only.

(C) The study relates to industrial credit issues of small scale sector only. Study

exceeds from its other financial area like dividend distribution, capital structure,

fixed assets, management of nationalized banks etc.

(D) The study also exceeds from other problems of SSIs, like marketing problem,

technology modernization, hassles from government and other agencies, sickness

of SSIs. etc.

26

Chapter Plan:

The present study is divided into five chapters which are outlined as here under:

Chapter 1: Research Framework

This chapter deals with the research problem, objective, significance of the

research, universe of the study and sample design, hypothesis of the problem and

research methodology.

Chapter 2: Sectoral Credit Concepts and Overview

This is an introductory chapter. It deals with introduction, concepts and

importance of credit need for credit, kinds of credit, global and Indian credit scenario.

Chapter 3: Small Scale Industries: An Introductory Framework

This chapter mainly concentrates on the meaning of SSI units, significance of

SSIs, growth of SSIs, problems facing by SSIs, institutional framework of SSI in India

and Gujarat, importance of SSI in Gujarat economy, SSI in India and Gujarat.

Chapter 4: Sub Regional Analysis

This chapter includes introduction to Gujarat economy, analysis of north, south,

central, East and west Gujarat.

Chapter 5: Finding, Suggestions and Conclusions

This chapter gives its emerging conclusions based on analysis carried out,

suggestions, findings, scope for further research.

27

References :

1. Fundamentals of applied statistics – S C Gupta and V K Kapoor.

2. Statistics for management – Levin and Rudin.

28

Chapter 3

An Introduction of Small Scale Industries

Sr No Title

3.1 Definition

3.2 Characteristics

3.3 Relation between Small & Large Units

3.4 Rationale

3.5 Objectives

3.6 Scope

3.7 Opportunities for an Entrepreneurial Career

3.8 Role of Small Enterprise in Economic Development

3.9 Problems of small scale Industries

3.10 Institutional Framework for Small Scale Industries in India

3.11 Literature Review

29

3.1. Definition

What is a small-scale industry? In fact, small-scale industry comprises of a variety

of undertakings. The definition of small scale industry (SSI) varies from one country to

another and from one time to another in the same country depending upon the pattern and

stage of development, Government policy and administrative set up of the particular

country. As a result, there are at least 50 different definitions of SSIs found and used in

75 countries. All these definitions either relate to capital or employment of both or any

other criteria. We trace here the evolution of the legal concept of small-scale industry in

India.

The Fiscal Commission, 1950, for the first time, defined a small-scale industry as

one which is operated mainly with hired labour usually 10 to 50 hands. In order to

promote small-scale industries in the country, the government of India set up the Central

Small-Scale industries Organization and the small-scale Industries Board in 1954-55. The

SSI board at its first meeting held on January 5th and 6th, 1955, defined small-scale

industry as a unit employing less than 50 employees, if using power, and less than 100

employees without the use of power and with a capital asset not exceeding Rs. 5 lakhs.

The definitional change of small-scale industry over the period in India is

resumed in below Table.

30

TABLE Definition of Small Scale Industry: An overview.

Investment criterion Year

SSI units Ancillary units Employment Criterion

Up to 1958 Fixed capital investment up

to Rs. 5 Lakhs

Same as SSI

unit

Employment up to 50 workers if using

power or up to 100 if not using power.

1959

The value of machine was

taken as the original price

paid irrespective of new or

old machinery

Same as SSI

unit

Employment up to 50 workers if using

power or up to 100 if not using power.

1960

Gross value of fixed asset

up to

Rs. 5 Lakhs

Gross value of

fixed asset up

to

Rs. 10 Lakhs

Employment criterion dropped

1966* Rs. 7.5 Lakhs Rs. 10 Lakhs Employment criterion dropped

1975 Rs. 10 Lakhs Rs. 15 Lakhs Employment criterion dropped

1980 Rs.20 Lakhs Rs. 25 Lakhs Employment criterion dropped

1985 Rs. 35 Lakhs Rs. 45 Lakhs Employment criterion dropped

1991 Rs.60 Lakhs Rs. 75 Lakhs Employment criterion dropped

As the Abid Hussain Committee’s recommendations on small-scale industries, the

government of India has, in March 1997, further raised investment ceiling to RS. 3 crores

for small-scale industries and to rs. 50 lakhs for tiny units.

The new policy initiatives in 1990-2000 for the small scale sector has reduced the

investment limit for small scale and ancillary undertakings from existing Rs. 3 crore to

Rs. 1 crore.

An ancillary unit is one which sells not less than 50 % of its manufacturers to one

or more industrial units.

For small-scale industries, the planning commission of India uses terms village

and small-scale industries. These includes modern small-scale industry and the traditional

cottage and household industries. This is depicted in the following chart:

31

Small-Scale Industry

Types of Small-Scale Industries

Small-Scale Industries can be classified in to five main types as follows:

(1) Manufacturing industries, i.e. industries producing complete articles for direct

consumption and also processing industries;

(2) Feeder industries specializing in certain types of products and services, e.g.

casting, electro-plating, welding, etc.

(3) Serving industries covering light, repair, shops necessary to maintain mechanical

equipment;

(4) Ancillary to large industries, producing parts and components and rendering

services; and

(5) Mining of quarrying.

3. 2. Characteristics

“Small-Scale industry is beautiful” because of its following important

characteristics:

(1) A small scale unit is generally a one-man show. Even the small units which run

by a partnership firm or company, the activities are mainly carried out by one of

the partner or directors. In practice, the others are simply as sleeping partners or

directors who mainly assist in providing funds.

(2) In case of small-scale industries, the owner himself/herself is a manager also.

Thus, these units are managed in a personalized fashion. The owner has first hand

Modern Small Scale Industry Cottage Industry Village Industry Ancillary Industry

32

knowledge of what is actually going on in the business. He takes effective

participation in all matters of business decision taking.

(3) Compared to large units, a small-scale industrial unit has a lesser gestation period,

i.e. the period after which the return on investment starts.

(4) The scope of operation of small industrial undertaking is generally localized

catering to the local and regional demands.

(5) Small units use indigenous resources and, therefore, can be located anywhere

subject to the availability of these resources like raw materials, labour etc.

(6) Small industries are fairly labour intensive with comparatively smaller capital

investment than the larger units. Let the facts speak. According to P.C.

Mahalnobis, small scale units require very little capital. About six or seven

hundred rupees would get an artisan family started. With any given investment,

employment possibilities would be ten of fifteen or even twenty times greater in

comparison with corresponding factory system.

(7) Using local resources, small units are decentralized and dispersed to rural areas.

Thus, the development of small-scale industries in rural areas promotes more

balanced regional development, on the one hand, and prevents the influx of job

seekers from rural areas to cities and urbanizing centers, on the other.

(8) Last but not the least, compared to large scale units, small scale units are more

change susceptible and highly reactive and respective to socio-economic

conditions. They are more flexible to adapt changes like introduction on new

products, new method of production, new materials and new markets, new forms

of organization etc.

3.3. Relation between Small & Large Units

Going through the distinct characteristics of small-scale industries, one should not

assume that the both small and large, are antithetic to each other. In other words, the both

cannot sustain in an economy. It is, in fact, true the other way round, and to a great

extent, one is often ancillary or complementary to the other.

The relationship between the small and the large industrial units can be seen in

various respects. Yet, the following are the importance ones:

33

1. Competitive: Small-scale industry can not compete with large industry in certain

circumstances and in selected products. Examples of such industries are bricks

and tiles, fresh baked goods and perishable edibles, preserved fruits, goods

requiring small engineering skills, items demanding craftsmanship and artistry.

2. Supplementary: Small industry can fill in the gaps between large scale

production and standard outputs caused by large scale units. This id due to this

supplementary role of small units, a small tricycle factory sustained and

flourished alongside a large cycle factory in Chennai city.

3. Complementary: Apart from supplementary relationship, small industry has

been a complementary to its large counterparts. In the real world, many small

units produce intermediate products for large units. Such subcontracting

relationship between the small and large was particularly marked in the economic

history of today’s industrially developed Japan. As industrialization proceeds,

small firms seem naturally to shift from activities that complete with large firms

to complementary ones. Similarly, China too continues to relay on Mao’s

aphorism of “walking on two legs”- one being small and the other large.

Under complementary relationship, small units function under the tutelage

of the large units and enjoy the advantage of protected market for their products.

Then, the flourishment of such small units remains beyond doubt.

4. Initiative: Attracted by the high profits of large units, small units can also take

initiative to produce the particular product. If succeed, the small unit grows to

large over a period of rime. Staley quotes such initiative that many of the

automobile factories started this way in the United States of America. In our

country too, the electronic industry looks like following to this initiative pattern of

development.

5. Servicing: Small industries do also install servicing and repairing shops for the

products of large units. In the case of India, such small servicing units can be seen

proliferating in respect of large industries like refrigerators, radio and relevision

sets, watches and clocks, cycles and motor vehicles.

34

3. 4. Rationale

Having discussed the distinct characteristics of small-scale industry as also its

relationship with large scale units, we now discuss the rationale of small-scale industry

development in India.

Emphasizing the very rational of small-scale industry in the Indian economy, the

Industrial Policy Resolution (IPR), 1956 stated:

“They provide immediate large scale employment, they offer a method of

ensuring a more equitable distribution of the national income and they facilitate an

effective mobilization of resources of capital and skill which might otherwise remain

unutilized. Some of the problems that unplanned urbanization tends to create will be

avoided by the establishment of small centres of industrial production all over the

country.”

The rationale of small-scale industries so established can broadly be classified

into four arguments, viz., (1) Employment argument (2) Equality argument, (3)

Decentralization argument, and (4) Latent resources argument. Let us discuss these in

more detail one by one.

1. Employment Argument:

In view of India’s scarce capital resources and abundant labour, the most

important argument advanced in facour of the SSIs that they have a potential to create

immediate large-scale employment opportunities. The increasing emphasis on SSIs in

developing countries like India stems largely from the widespread concern over

unemployment hovering in the country. There are many research findings available

which well establish that small-scale units are more labour intensive than large units. In

other words, small units use more of labour per unit of output than investment.

According to a study, while the output-employment ratio is the lowest in the

small-scale sector, employment-generating capacity of small sector is eight time that of

the large scale sector. As mentioned earlier, P.C Mahalnobis also support the view that

small industries are fairly labour intensive. He mentions that with any given investment,

employment possibilities would be ten of fifteen or even twenty times greater in

comparison with factory system.

35

There are some scholars like Dhar and Lydall who oppose to this employment

argument of small-scale industries. They hold the view that employment should the view

that employment should not be created for the sake of employment. The important

problem, according to them, is not how to absorb surplus resources, but how to make the

best use of scare resources. Then, the employment-argument becomes and output

argument.

2. Equality Argument:

One of the main argument put foreword in favour of the small-scale industries is

that they ensure a more equitable distribution of national income and wealth. This is

accomplished because of the two major considerations: (i) compared to the ownership of

large scale units, the ownership pattern in S S I is more widespread. (ii) their more labour

intensive nature, on the one hand, and their decentralization and dispersal to rural and

backward areas, on the other, provide more employment opportunities to the

unemployed. This result in more equitable distribution of the produce of the small-scale

units. It also held that as most of the small enterprises are either proprietary or partnership

concerns, the relations between the workers and the employers are more harmonious in

small enterprises than in the large enterprises.

Here, again Dhar and Lydall have pointed out this equality arguments as

fallacious. Giving statistical evidence, they established the fact that wages paid to

workers are much less in small enterprises than the wages paid to the workers in large

industries. In India, wages in small industries are about half the wages paid in large

industries. The reason is not difficult to seek. Workers in small enterprises, due to virtual

non existence of trade unions, are unorganized and, therefore, are easily exploited by the

employers.

There is no doubt that the argument of Dhar and Lydall does have some force. But

in an under –developed country like India, the workers have choice not between a high

paid job and low paid job but between a low paid job and no job at all. Then, even if

small scale units provide low paid jobs, they would be of virtual importance in an

economy like ours where millions are already in search of employment to eke-out their

livelihood.

36

3. Decentralization Argument:

Decentralization argument emphasis the necessity of regional dispersal of

industries to promote balanced regional development in the country. Big industries are

concentrated everywhere in urban areas. But, small industries can be located in rural and

semi-urban areas to use local resources and to cater to the local demand admittedly, it

will not be possible to start small enterprises in every village, but it is quite possible to

start small enterprises in a group of villages. The international perspective planning team

also rightly stressed that the focused for industrial development under a dispersal policy

should be neither the metropolis nor the village, but rather the large range of potentially

attractive cities and towns between these two extremes.

Decentralization of industrial enterprises will help tap local resources search as

raw materials, idle savings, local talents and ultimately improves the standards of leaving

even in erstwhile backward areas. The most glaring example of this phenomenon is the

economy of Punjab which has more small scale units, then even the industrially

developed state of Maharashtra.

4. Latent Resources Argument:

This argument suggests that small enterprises are capable of mopping of latent

and unutilized resources like hoarded wealth and ideal entrepreneurial ability, etc.

however, Dhar and Lydall feel that the real force of talent resources argument lies in the

existence of entrepreneurial skill. They argue that there is no evidence of an overall

shortage of small entrepreneurs in India. Hence, they doubt the force of this latent

resources argument. Their assertion does not appear to be very sound simply because of

the fact that if small entrepreneurs were present in abundance, then what obstructed the

growth of small enterprises?

The emergence of entrepreneurial class requires a conductive environment. The

fact remains that small enterprises provide such environment in which the latent talents of

entrepreneurs find self-expression. Our economic history of bears this evidence. The

impressive growth in the number of small enterprises in the post-independence period

highlights the same fact that providing the necessary conditions such as power and credit

37

facilities, the latent resources of entrepreneurship can be tapped by the growth of small

enterprises only.

3. 5. Objectives:

The various objectives of developing small industries are, in fact, implied in one

way or other, in its rationale itself, just discussed in the preceding section. Nonetheless,

an attempt has been made in this section to list the main objectives of developing small

enterprises in India in a more orderly manner. These are:

(1) To generate immediate and large scale employment opportunities with relatively

low investment.

(2) To eradicate unemployment problem form the country.

(3) To encourage dispersal of industries to all over country covering small towns,

villages and economically lagging regions.

(4) To bring backward areas too in the mainstream of national development

(5) To promote balanced regional development in the whole country.

(6) To ensure more equitable distribution of national income.

(7) To encourage effective mobilization of country’s untapped resources.

(8) To improve the level of living of people in the country.

3. 6. Scope: