Sap Cloud Strategy 2014sap.lianacms.com/.../sap-cloud-strategy-by-anoop-srivastava.pdf · • SAP...

14

SAP Cloud Strategy Anoop Srivastava Director (Energy & Natural Resources) MENA ENR Forum, Al Khobar

Transcript of Sap Cloud Strategy 2014sap.lianacms.com/.../sap-cloud-strategy-by-anoop-srivastava.pdf · • SAP...

SAP Cloud Strategy

Anoop SrivastavaDirector (Energy & Natural Resources)

MENA ENR Forum, Al Khobar

© 2014 SAP SE. All rights reserved. 2

Disclaimer

This presentation outlines our general product direction and should not be relied on in

making a purchase decision. This presentation is not subject to your license

agreement or any other agreement with SAP. SAP has no obligation to pursue any

course of business outlined in this presentation or to develop or release any

functionality mentioned in this presentation. This presentation and SAP's strategy and

possible future developments are subject to change and may be changed by SAP at

any time for any reason without notice. This document is provided without a warranty

of any kind, either express or implied, including but not limited to, the implied

warranties of merchantability, fitness for a particular purpose, or non-infringement.

SAP assumes no responsibility for errors or omissions in this document, except if

such damages were caused by SAP intentionally or grossly negligent.

© 2014 SAP SE. All rights reserved. 3© 2014 SAP SE. All rights reserved. 3

Agenda

SAP Cloud:

• Market Trends

• SAP Cloud Strategy

• Portfolio

• Cloud Deployment and Migration Models

© 2014 SAP SE. All rights reserved. 4© 2014 SAP SE. All rights reserved. 4

Cloud Mobile Networks Big Data

More than 60% of CEOs expect 15-50% of their

earnings growth in the next 5 years to come from

technology-enabled business innovations.

– McKinsey study, 2013 ”“

Simplicity, time to

value, speed to

innovation, and

extensible platform

Adaptability for the 21st

century workforce,

everything doable from

anywhere

Hyper-connectivity fueled

by digital communities and

social collaboration

Predictive insight driven

by business strategy,

new product strategies,

new customer

relationships

Transformational technologies have converged to drive business innovation like never before

© 2014 SAP SE. All rights reserved. 5© 2014 SAP SE. All rights reserved. 5

Cloud is where the market is going

75%New enterprise IT spend

Will be cloud-based or hybrid by 2016

Source: IDC 2013 Report:

“New Enterprise IT Spend”

60%Cloud Spending

Will be for Cloud apps (SaaS)

Source: IDC 2013 Report:

“New Enterprise IT Growth”

$200B+ Greater cloud market

growth by 2018including cloud services and the technology to enable cloud servicesSource: IDC Predictions 2015

80%New IT purchases

Will be made byLine of Business

Source: IDC 2013 Report:

“Line of Business IT Purchases”

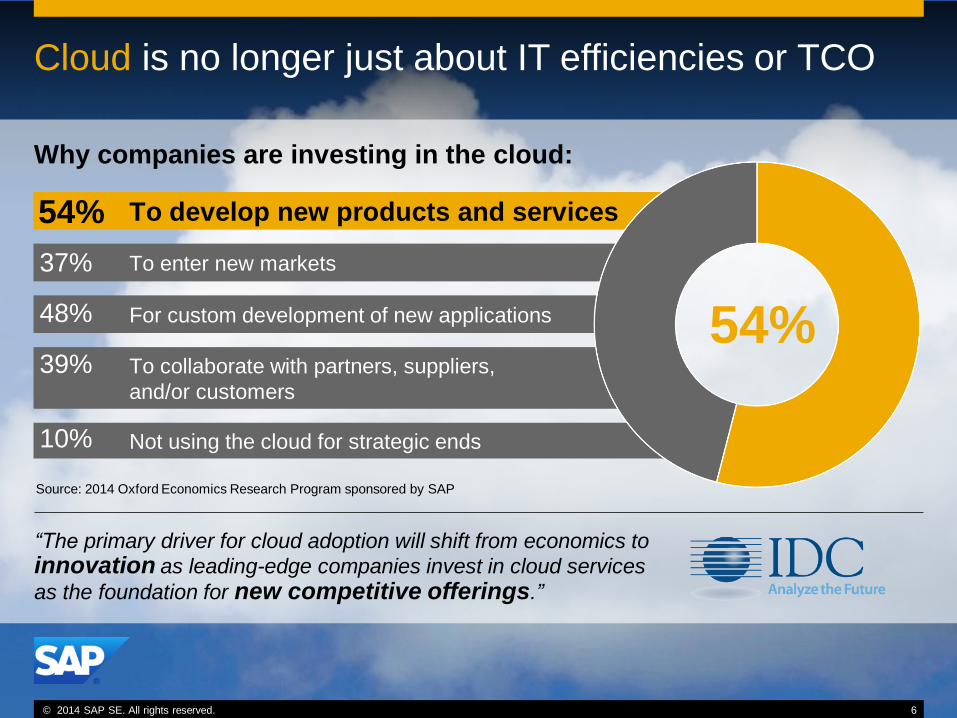

© 2014 SAP SE. All rights reserved. 6© 2014 SAP SE. All rights reserved. 6

To collaborate with partners, suppliers,

and/or customers

To enter new markets

For custom development of new applications

Not using the cloud for strategic ends

To develop new products and services54%

37%

48%

39%

10%

“The primary driver for cloud adoption will shift from economics to

innovation as leading-edge companies invest in cloud services

as the foundation for new competitive offerings.”

Source: 2014 Oxford Economics Research Program sponsored by SAP

54%

Cloud is no longer just about IT efficiencies or TCO

Why companies are investing in the cloud:

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 7

• Full deployment

in weeks

• Mobile grade

user experience

= less training

• Multiple

innovation

releases per year

• Customer

feedback a

cornerstone of

updates

• Rapid process

configuration

• Faster adoption

• No lengthy

upgrade cycles

• Packaged

integration

Lower CapEx &

faster Time to

Value

Faster

deployment

More frequent

innovation

updates

Agile deployment,

configuration and

integration

• Lower initial solution

and deployment

fees

• No maintenance or

upgrade costs

• Prepackaged

integrations

Cloud is about innovation and new engagement models

© 2014 SAP SE. All rights reserved. 8© 2014 SAP SE. All rights reserved. 88

THE cloud company,

powered by SAP HANA

Cloud is at the center of SAP’s strategy

Run Simple = Cloud + SAP HANA

© 2014 SAP SE. All rights reserved. 9

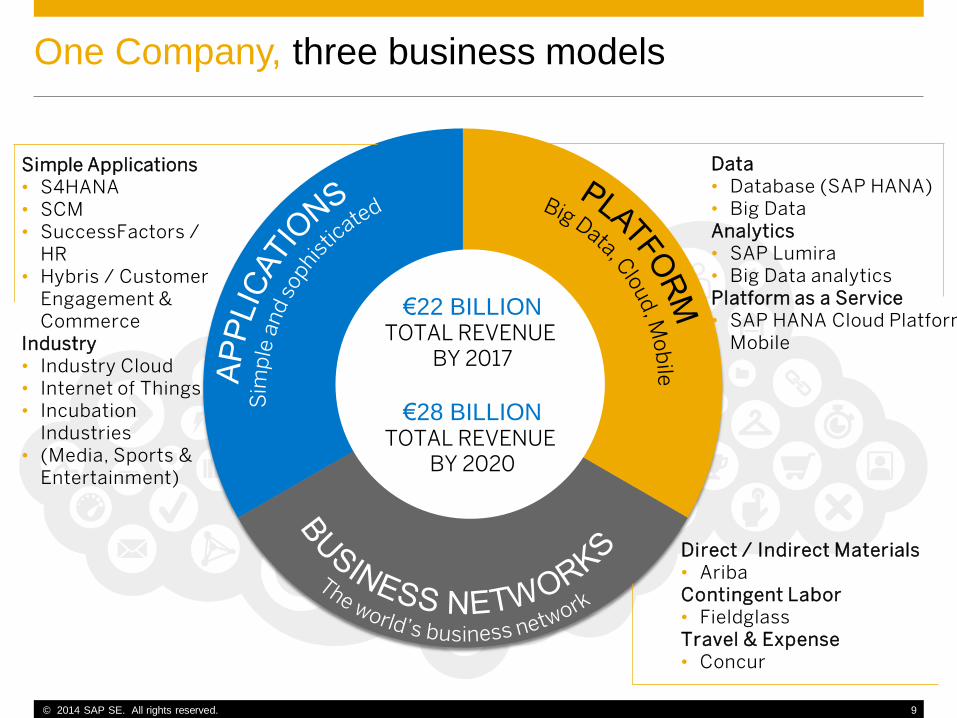

One Company, three business models

Direct / Indirect Materials• AribaContingent Labor• FieldglassTravel & Expense• Concur

Simple Applications• S4HANA• SCM• SuccessFactors /

HR• Hybris / Customer

Engagement & Commerce

Industry• Industry Cloud• Internet of Things• Incubation

Industries• (Media, Sports &

Entertainment)

Data• Database (SAP HANA)• Big DataAnalytics• SAP Lumira• Big Data analyticsPlatform as a Service• SAP HANA Cloud Platform• Mobile

PLATFOR

M

€22 BILLIONTOTAL REVENUE

BY 2017

€28 BILLIONTOTAL REVENUE

BY 2020

© 2014 SAP SE. All rights reserved. 10

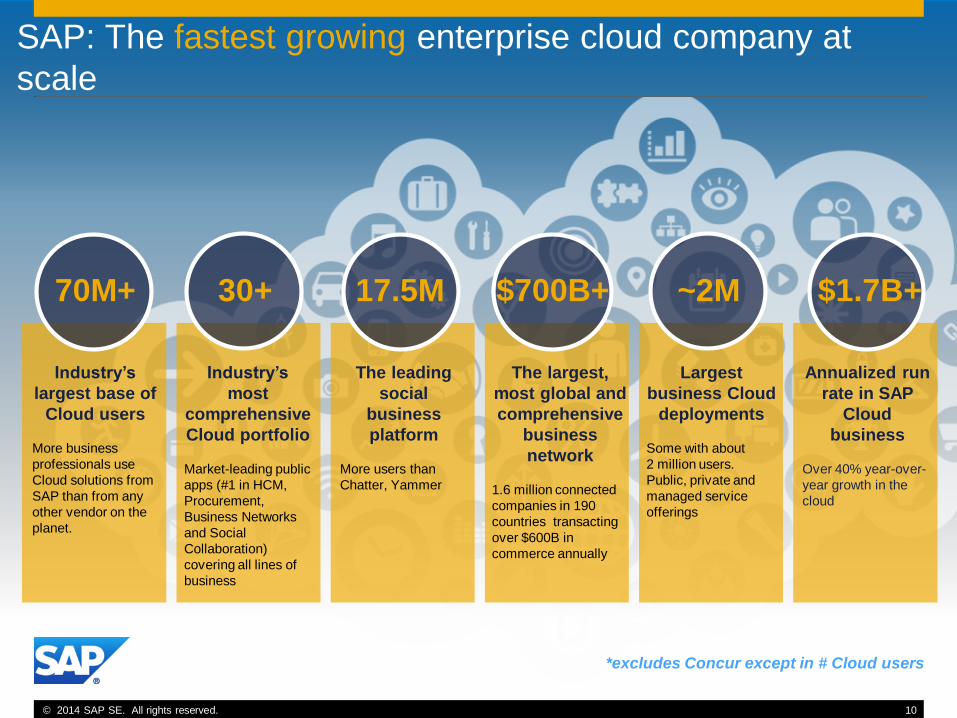

Industry’s

most

comprehensive

Cloud portfolio

Market-leading public

apps (#1 in HCM,

Procurement,

Business Networks

and Social

Collaboration)

covering all lines of

business

Industry’s

largest base of

Cloud users

More business

professionals use

Cloud solutions from

SAP than from any

other vendor on the

planet.

The leading

social

business

platform

More users than

Chatter, Yammer

The largest,

most global and

comprehensive

business

network

1.6 million connected

companies in 190

countries transacting

over $600B in

commerce annually

Largest

business Cloud

deployments

Some with about

2 million users.

Public, private and

managed service

offerings

Annualized run

rate in SAP

Cloud

business

Over 40% year-over-

year growth in the

cloud

SAP: The fastest growing enterprise cloud company at

scale

70M+ 30+ 17.5M $700B+ ~2M $1.7B+

*excludes Concur except in # Cloud users

© 2014 SAP SE. All rights reserved. 11© 2014 SAP AG. All rights reserved. 11Internal

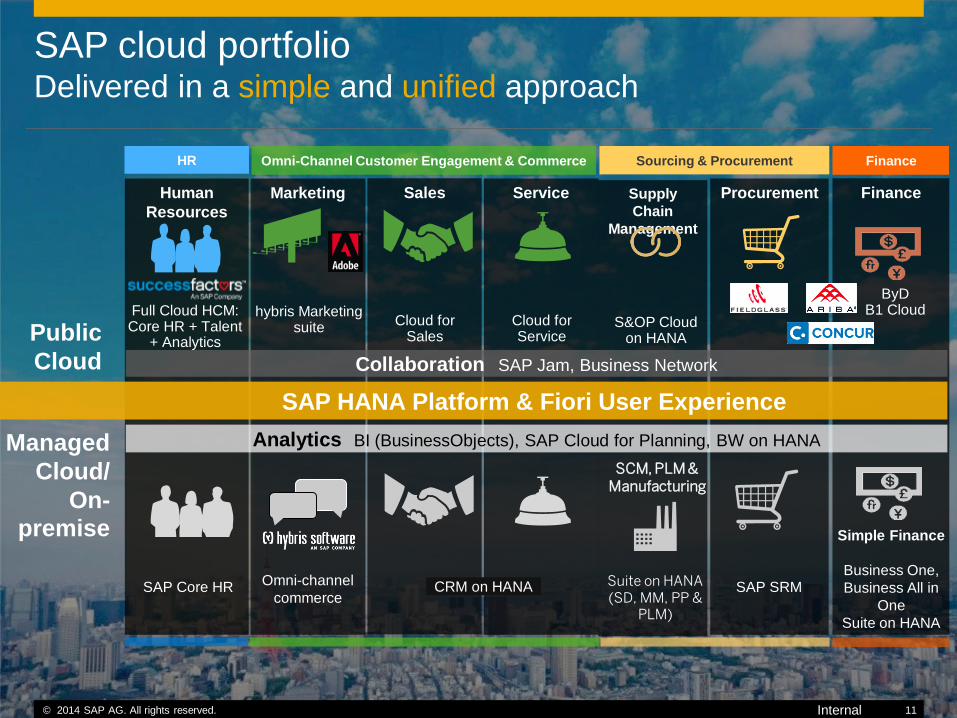

Marketing

hybris Marketing suite

Omni-channel

commerce

Sales Service

Cloud forSales

Cloud forService

CRM on HANA

Human

Resources

ProcurementSupply

Chain

Management

S&OP Cloudon HANA

Suite on HANA (SD, MM, PP &

PLM)

Finance

ByDB1 Cloud

Simple Finance

Business One,

Business All in

One

Suite on HANA

SCM, PLM & Manufacturing

Managed

Cloud/

On-

premise

Public

Cloud

Omni-Channel Customer Engagement & Commerce

Collaboration SAP Jam, Business Network

SAP HANA Platform & Fiori User Experience

Analytics BI (BusinessObjects), SAP Cloud for Planning, BW on HANA

SAP Core HR SAP SRM

Sourcing & ProcurementHR Finance

SAP cloud portfolioDelivered in a simple and unified approach

Full Cloud HCM:Core HR + Talent

+ Analytics

© 2014 SAP SE. All rights reserved. 12

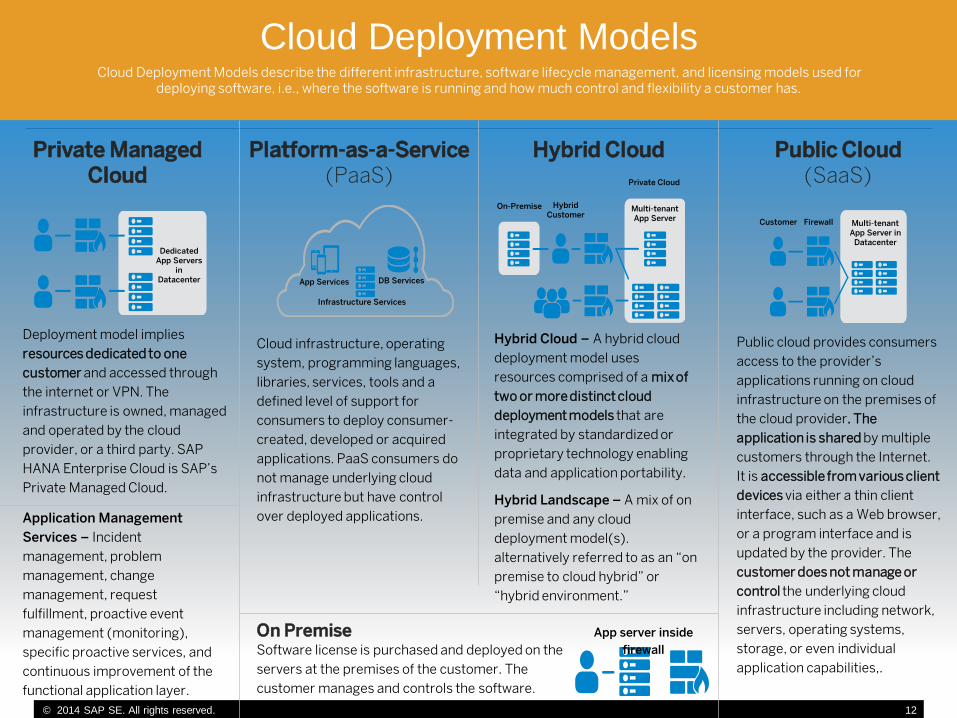

Cloud Deployment ModelsCloud Deployment Models describe the different infrastructure, software lifecycle management, and licensing models used for

deploying software, i.e., where the software is running and how much control and flexibility a customer has.

Private Managed Cloud

Platform-as-a-Service (PaaS)

Hybrid Cloud Public Cloud(SaaS)

Deployment model implies

resources dedicated to one

customer and accessed through

the internet or VPN. The

infrastructure is owned, managed

and operated by the cloud

provider, or a third party. SAP

HANA Enterprise Cloud is SAP’s

Private Managed Cloud.

Cloud infrastructure, operating

system, programming languages,

libraries, services, tools and a

defined level of support for

consumers to deploy consumer-

created, developed or acquired

applications. PaaS consumers do

not manage underlying cloud

infrastructure but have control

over deployed applications.

Hybrid Cloud – A hybrid cloud

deployment model uses

resources comprised of a mix of

two or more distinct cloud

deployment models that are

integrated by standardized or

proprietary technology enabling

data and application portability.

Hybrid Landscape – A mix of on

premise and any cloud

deployment model(s).

alternatively referred to as an “on

premise to cloud hybrid” or

“hybrid environment.”

Public cloud provides consumers

access to the provider’s

applications running on cloud

infrastructure on the premises of

the cloud provider. The

application is shared by multiple

customers through the Internet.

It is accessible from various client

devices via either a thin client

interface, such as a Web browser,

or a program interface and is

updated by the provider. The

customer does not manage or

control the underlying cloud

infrastructure including network,

servers, operating systems,

storage, or even individual

application capabilities,.

On PremiseSoftware license is purchased and deployed on the

servers at the premises of the customer. The

customer manages and controls the software.

Application Management

Services – Incident

management, problem

management, change

management, request

fulfillment, proactive event

management (monitoring),

specific proactive services, and

continuous improvement of the

functional application layer.

App Services DB Services

Infrastructure Services

Dedicated App Servers

in Datacenter

On-Premise Hybrid Customer

Private Cloud

Multi-tenantApp Server Customer Firewall Multi-tenant

App Server in Datacenter

App server inside

firewall

© 2014 SAP AG or an SAP affiliate company. All rights reserved.13

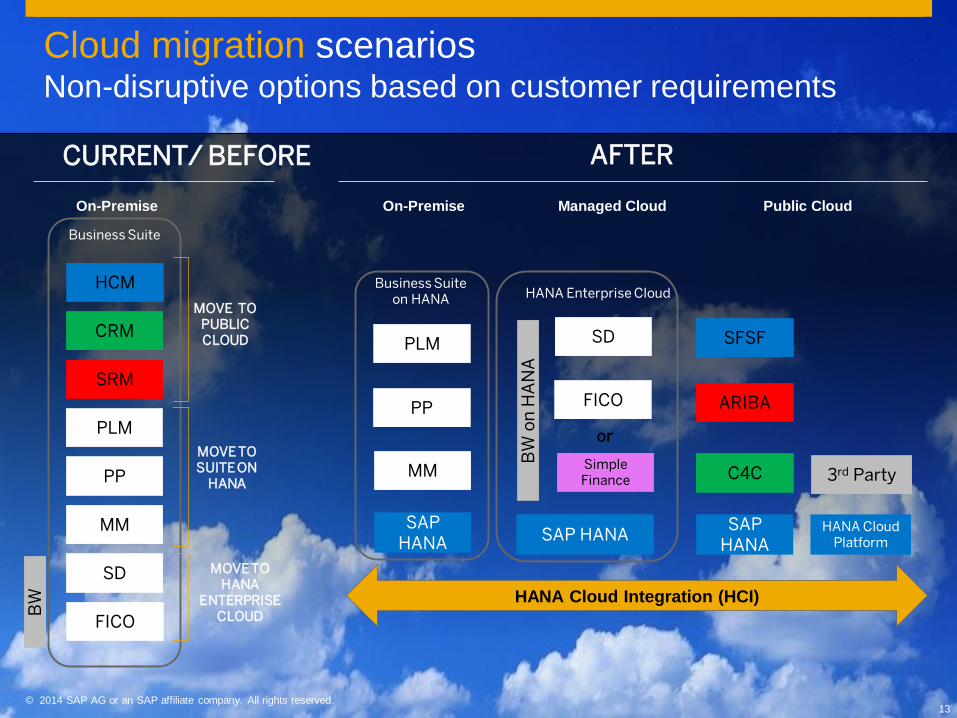

MOVE TO PUBLIC CLOUD

HANA Cloud Integration (HCI)

HCM

CRM

SRM

PLM

MM

FICO

SFSF

C4C

ARIBA

MOVE TO HANA

ENTERPRISE CLOUD

Business Suite

On-Premise

CURRENT/ BEFORE

PLM

PP

MM

Business Suiteon HANA

SAP HANA

SAP HANASAP

HANAHANA Cloud

Platform

3rd PartyPP

SD

MOVE TO SUITE ON

HANA

BW

SD

FICO

HANA Enterprise Cloud

Simple Finance

or

BW

on

HA

NA

Public CloudManaged CloudOn-Premise

AFTER

Cloud migration scenariosNon-disruptive options based on customer requirements

Thank you