RUCHI SOYA INDUSTRIES LIMITED · Ruchi Soya Industries Limited (the "Company“ or “Ruchi...

24

RUCHI SOYA INDUSTRIES LIMITED CORPORATE PRESENTATION August 2013

Transcript of RUCHI SOYA INDUSTRIES LIMITED · Ruchi Soya Industries Limited (the "Company“ or “Ruchi...

RUCHI SOYA

INDUSTRIES LIMITED

CORPORATE PRESENTATION

August 2013

Disclaimer

By attending the meeting where this presentation is made, or by reading the presentation slides, you agree to be bound by the following limitations: • This document has been prepared for information purposes only and is not an offer or invitation or recommendation to buy or sell any securities of

Ruchi Soya Industries Limited (the "Company“ or “Ruchi Soya”), nor shall part, or all, of this document form the basis of, or be relied on in connection with, any contract or investment decision in relation to any securities of the Company.

• This document is strictly confidential and may not be copied, published, distributed or transmitted to any person, in whole or in part, by any medium or in any form for any purpose. The information in this document is being provided by the Company and is subject to change without notice. The Company relies on information obtained from sources believed to be reliable but does not guarantee its accuracy or completeness.

• This document contains statements about future events and expectations that are forward-looking statements. These statements typically contain

words such as "expects" and "anticipates" and words of similar import. Any statement in this document that is not a statement of historical fact is a forward-looking statement that involves known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. None of the future projections, expectations, estimates or prospects in this document should be taken as forecasts or promises nor should they be taken as implying any indication, assurance or guarantee that the assumptions on which such future projections, expectations, estimates or prospects have been prepared are correct or exhaustive or, in the case of the assumptions, fully stated in the document. The Company assumes no obligations to update the forward-looking statements contained herein to reflect actual results, changes in assumptions or changes in factors affecting these statements.

• You acknowledge that you will be solely responsible for your own assessment of the market and the market position of the Company and that you will

conduct your own analysis and be solely responsible for forming your own view of the potential future performance of the business of the Company. • Neither the delivery of this document nor any further discussions of the Company with any of the recipients shall, under any circumstances, create

any implication that there has been no change in the affairs of the Company since that date.

Page 1

INDEX

pg.

Company Overview 2

Key Highlights 7

Financial Performance 16

Appendix 20

Page 2

COMPANY OVERVIEW

1st

1st

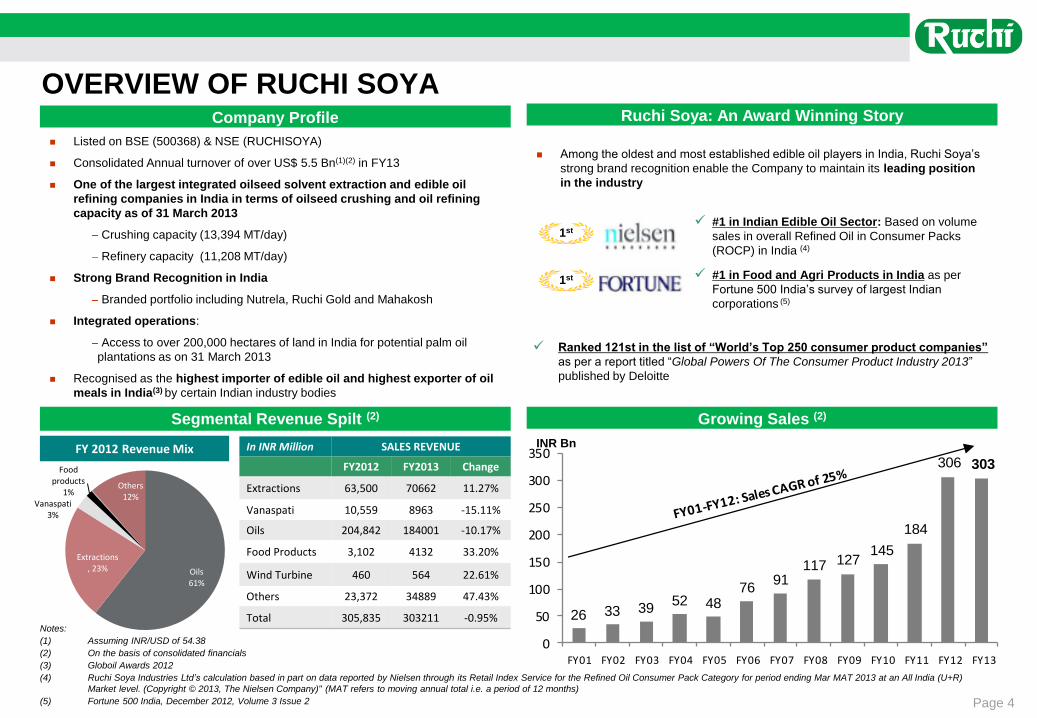

OVERVIEW OF RUCHI SOYA Company Profile

Listed on BSE (500368) & NSE (RUCHISOYA)

Consolidated Annual turnover of over US$ 5.5 Bn(1)(2) in FY13

One of the largest integrated oilseed solvent extraction and edible oil

refining companies in India in terms of oilseed crushing and oil refining

capacity as of 31 March 2013

Crushing capacity (13,394 MT/day)

Refinery capacity (11,208 MT/day)

Strong Brand Recognition in India

Branded portfolio including Nutrela, Ruchi Gold and Mahakosh

Integrated operations:

Access to over 200,000 hectares of land in India for potential palm oil

plantations as on 31 March 2013

Recognised as the highest importer of edible oil and highest exporter of oil

meals in India(3) by certain Indian industry bodies

Segmental Revenue Spilt (2)

In INR Million SALES REVENUE

FY2012 FY2013 Change

Extractions 63,500 70662 11.27%

Vanaspati 10,559 8963 -15.11%

Oils 204,842 184001 -10.17%

Food Products 3,102 4132 33.20%

Wind Turbine 460 564 22.61%

Others 23,372 34889 47.43%

Total 305,835 303211 -0.95%

FY 2012 Revenue Mix

Page 4

Notes:

(1) Assuming INR/USD of 54.38

(2) On the basis of consolidated financials

(3) Globoil Awards 2012

(4) Ruchi Soya Industries Ltd’s calculation based in part on data reported by Nielsen through its Retail Index Service for the Refined Oil Consumer Pack Category for period ending Mar MAT 2013 at an All India (U+R)

Market level. (Copyright © 2013, The Nielsen Company)" (MAT refers to moving annual total i.e. a period of 12 months)

(5) Fortune 500 India, December 2012, Volume 3 Issue 2

Ruchi Soya: An Award Winning Story

Among the oldest and most established edible oil players in India, Ruchi Soya’s

strong brand recognition enable the Company to maintain its leading position

in the industry

#1 in Indian Edible Oil Sector: Based on volume

sales in overall Refined Oil in Consumer Packs

(ROCP) in India (4)

#1 in Food and Agri Products in India as per

Fortune 500 India’s survey of largest Indian

corporations (5)

Ranked 121st in the list of “World’s Top 250 consumer product companies”

as per a report titled “Global Powers Of The Consumer Product Industry 2013”

published by Deloitte

Growing Sales (2)

26 33 3952 48

7691

117 127145

184

306 303

0

50

100

150

200

250

300

350

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

INR Bn

Oils 61%

Extractions, 23%

Vanaspati 3%

Food products

1% Others

12%

ORGANIZATIONAL CHART(1)

(1) Shareholding pattern as of 31 Mar 2013

Page 5

Group companies outside India

Group companies within India

Indian Oil

Ruchi Bio

Fuels LLP

(50%)

GHI Energy

Private Limited

(48.96%)

RSIL

Beneficiary

Trust

(100%)

Mrig Trading

Private Limited

(100%)

Gemini Edible

& Fats India

Private Limited

(50%)

Ruchi

Worldwide Limited

(52.48%)

Ruchi Agri PLC

(100%)

Ruchi Ethiopia

Holding Limited

(100%)

Ruchi Industries

Pte Ltd

(100%)

Ruchi Agri

Plantation

(Cambodia)

Pte. Limited

(100%)

Palmolein

Industries Pte.

Limited

(100%)

Ruchi

Agri Trading

Pte. Limited

(100%)

Ruchi Soya Industries

Limited

(Parent)

Ruchi Agri

SARL.

(100%)

Page 6

LEADING POSITION IN EDIBLE OIL SEGMENT The Company has an estimated market share of ~15% in the edible oil segment in India. In terms of ROCP category, the Company has

attained leadership position with market share of ~ 17% as per a recent survey(1)

1,243

1,535 1,598

2,380 2,398

3,095

2,697

0

500

1,000

1,500

2,000

2,500

3,000

3,500

FY07 FY08 FY09 FY10 FY11 FY12 FY13

Qu

anti

ty (0

00

'MT)

10.5%

11.8%11.0%

15.6%14.9%

18.3%

14.7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

FY07 FY08 FY09 FY10 FY 11 FY12 FY13M

ark

et

Sh

are

(%

)

Ruchi Soya edible oil sales(2)

Ruchi soya edible oil segment:

CAGR FY07–FY13: 14%

Indian edible oil:

CAGR FY07–FY13: 8%

(000’MT) 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13

Industry edible oil consumption 11,807 12,989 14,508 15,247 16,052 16,901 18312

Ruchi Soya edible oil market share (estimated) (3)

Source: USDA FAS

Notes: (1) Ruchi Soya Industries Ltd’s calculation based in part on data reported by Nielsen through its Retail Index Service for the Refined Oil Consumer Pack Category for period ending March MAT 2013 at an All India (U+R)

Market level. (Copyright © 2013, The Nielsen Company)" (MAT refers to moving annual total i.e. a period of 12 months) (2) Company Filings. Standalone sales of edible oil segment of Ruchi Soya Industries Ltd.; excludes the sales for captive consumption (3) Market share estimated based on edible oil sales of Ruchi Soya and Industry edible oil consumption data based on USDA FAS data, prepared by Ruchi Soya

BUSINESS STRATEGIES

Page 7

To capitalize on the supply and demand gap in the edible oil industry in India

To increase market share in branded edible oil products and food products in India

To continue focus on backward integration

To have a global footprint

To focus on innovation in our product range to deliver differentiated products

KEY HIGHLIGHTS

KEY HIGHLIGHTS

Page 9

Our brand portfolio includes brands such as Nutrela, Mahakosh and Ruchi Gold, which enjoy strong brand recognition in the Indian market

India is one of the leading consumers of edible oil

Significant room for growth in domestic production expected given that the increasing consumption of edible oil has been primarily met through imports as domestic production is not able to keep pace

One of the few companies in this industry operating across the value chain from origination, supply chain, manufacturing to branding, which enable us to manage costs more effectively than several of our competitors

Experienced management team with over four decades of industry experience

Key members have served or are currently serving as officers of various industry bodies, recognizing their standing in this sector

Favourable Industry Dynamics

Strong Brand Recognition in

India

Fully Integrated Operations

Extensive Distribution Network

in India

1

2

3

4

Experienced Management 5

Pan-India presence with strategically located manufacturing facilities striking the right balance between proximity to raw materials and markets

Extensive distribution network in India and a large sales force

46% 16% 13% 6% 7% 8% 4%

Palm Soyabean Rapeseed Peanut Cottonseed Sunflower seed Other

FAVOURABLE INDUSTRY DYNAMICS GLOBAL EDIBLE OIL INDUSTRY OVERVIEW

World Edible Oil Consumption (FY13) World Edible Oil Production (FY13)

India is the leading consumer of edible oil with high growth expectation

Palm and Soyabean oil constitute ~61% of the Global Edible Oil Demand

Page 10 Source: Global Edible Oil Demand as per USDA FAS

Source: USDA FAS

Source: USDA FAS

Indonesia

37 41 44 45 47 49 54

36 38 36 38 41 42 4217 18 20 22 23 24 2411 10 12 11 11 13 1420 21 21 21 23 23 24

0

20

40

60

80

100

120

140

160

180

FY07 FY08 FY09 FY10 FY11 FY12 FY13

(MnT)

Palm oil Soyabean oil Rapeseed oil Sunflowerseed oil Others

FY07-FY13

CAGR

Argentina

6%

3%

5%

4%

3%

Indonesia

20%

Malaysia

13%

China 14%

Europe

10%

United States

6%

Argentina

5%

India 5%

Other 26%

Brazil, 4%

China, 20%

Argentina,

2%

Europe, 15%India, 12%

US, 8%

Others, 39%

1

Edible Oil63%Pulses

12%

Cashew Nuts7%

Spices3%

Fruits & Nuts6%

Sugar4%

Cotton1%

Others2%

Indian Edible oil demand being substantially met by imports as domestic

production has lagged

Oil Consumption In India growing inline with growth

in population …

…getting turbo charged by growing per capita

income

Edible oils have a significant share in Indian agricultural imports

Source: Ministry of Agriculture (GOI) and DGCI&S) Page 11

Source: USDA FAS, IMF

Source: USDA FAS

Significant growth in per capita consumption can be

expected as Indian per capita GDP continues to grow

Source: USDA FAS, IMF

Robust growth in consumption of edible oil .... Rising deficit with domestic production not being able to keep pace

6 7 6 7 6 6 7 7 7

5 5 56 9 9

9 1011

0

4

8

12

16

20

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

Mn MT

India Production India Imports

CAGR 2005-2012 Imports: 10%

CAGR 2005-2012Production : 1%

USD

Source: USDA FAS, IMF

FAVOURABLE INDUSTRY DYNAMICS INDIA EDIBLE OIL INDUSTRY - HIGH GROWTH POTENTIAL

1

Per capita oil consumption (Ltr) Million Mn MT MT

0

5

10

15

20

25

30

35

402008-09 2009-10 2010-11 2011-12 2012-13

467

481

549

630

729

807

1009

1081

1068

1342

1389

1455

1583

0

2

4

6

8

10

12

14

16

0

200

400

600

800

1000

1200

1400

1600

1800

GDP / capita Per capita consumption

0

5

10

15

20

200

700

1200

1700

Population Total oil consumption

947 1,054 1,038 1,060 1,116 1,214 1,238

3,6715,075

6,230 6,4407,080 7,425

8,4251,433

1,582

1,455 1,3201,256

1,160

1,189

2,133

1,967

2,097 2,0962,318

2,433

2,425

2,500

2,330

2,300 2,7602,640

2,750

3,000

600

398

733912

9911280

1380

523

574

655659

651

639

655

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

FY07 FY08 FY09 FY10 FY11 FY12 FY13

Cottonseed Palm PeanutRapeseed Soybean SunflowerseedOther

India Edible Oil Imports

Page 12

Source: USDA FAS (Office of Global Analysis)

India Edible Oil Consumption

Palm oil consumption in India has seen significant growth, and is primarily met through imports, leaving significant room

for growth in domestic production

Source: USDA FAS (Office of Global Analysis)

11,807

8%

15%

FY07-FY13 CAGR

‘000 MT

12,970

14,508

15,247

16,052

16,901

15%

FAVOURABLE INDUSTRY DYNAMICS INDIA EDIBLE OIL INDUSTRY - HIGH GROWTH POTENTIAL

1

18,312

3,650

5,013

6,867 6,603 6,661

7,473

8,500 1,447

733

1,060 1,598 945

1,174

1,150

203

18

583 611

776

1114

1150

140

143

278 256

200

266

248

0

1,500

3,000

4,500

6,000

7,500

9,000

10,500

FY07 FY08 FY09 FY10 FY11 FY12 FY13

Palm Soybean Sunflowerseed Other

13% FY07-FY13 CAGR

Nutrela – Food products/ Refined Oils (Soyabean,

Groundnut, Cottonseed, Sunflower , Mustard ,

Ricebran)

Nutri Gold – Vanaspati

Mahakosh – Refined Oils (Soyabean, Groundnut,

Cottonseed and Ricebran) & Vanaspati

Sunrich – Refined Sunflower Oil

Ruchi Gold – Refined Oils (Mustard and Palmolein)

Ruchi Star – Refined Soyabean Oil

Ruchi No. 1 – Vanaspati

STRONG BRAND RECOGNITION IN INDIA P

rem

ium

Page 13

Track record of creating successful brands in a highly commoditized industry. Company has multiple brands for several of

their products to cater to different income segments of the Indian retail market

Key Brands

Va

lue

M

as

s

2

FULLY INTEGRATED OPERATIONS Healthy mix of midstream and downstream, and well on its way to develop an upstream business

Origination

– Palm plantations across Andhra Pradesh, Karnataka, Mizoram, Gujarat, Orissa and Tamil Nadu

– Access to total agricultural land of 2,00,000 hectares for potential oil palm procurement

Processing

– Daily capacity (MT)(Mar - 2013):

– Crushing:13,394

– Crude Oil: 2,411

– Soya Meal: 10,983

– Refining: 11,208

– Vanaspati & bakery fats: 2,118

– Textured soya protein: 467

– Edible soya flour: 300

Products

– Key products

– Edible oil

– Seed extractions,

– Vanaspati

– Food productions

– Key brands include Nutrela, Ruchi Gold, Ruchi Star, Sunrich and Mahakosh

Merchandising and distribution

– As of 31 March 2013, 106 company depots through India with storage and logistical facilities

– As of 31 March 2013, pan-India non-exclusive distribution network covering 5,642 distributors reaching over 725,000 retail outlets

Origination Customer Processing Products

Merchandising

and

distribution

Finance / Risk management / Logistics coordination

Information flows / Visibility across value chain

Page 14

One Of The Few Edible Oil Companies in India with Integrated Operations

3

EXTENSIVE DISTRIBUTION NETWORK IN INDIA

Page 15

Processing plants across 22 locations in India, giving access to markets across India

106 company depots (with storage and other logistical facilities) which serve 5,642 distributors across the country reaching over 725,000 retail outlets

All refining plants located near ports, providing easier access to imported edible oil

Distribution through pipes at ports saves transport cost and time

Inland crushing plants located in key soya bean and mustard producing states

Crushing in

Soya bowl of

India

Proximity to

Ports

Pan India

Footprint

We have a large distribution presence in India. As of March 31, 2013, we have 22 manufacturing locations, 11 wind power generating

locations and 106 company depots across India. In terms of distribution, we have 5,642 non-exclusive distributors in India, covering

over 2,210 towns and over 725,000 retail outlets.

Strategic Manufacturing locations

Note: Manufacturing and other locations as on March 2012

Map for representation purpose only - Not to scale

Strategically located facilities striking the right balance between proximity to

raw materials (cultivating states and ports) and proximity to markets.

4

Pan India Presence

2

3

16

17

18

11

6 13

14

12

4

7

15

10

8

9

Plant location

Jammu

Haldia Gaderwada

Nagpur

Vijaywada

Kakinada

Guna

Piparia

Shujalpur

Manglia

Sriganganagar

Baran

Kota

Kandla

Patalganga

Manglore

Chennai

19

1

Washim

Daloda

5

Krishnapatnam

Durgawati 20

21 22

Cities Activity Access to

Ports Crushing Refining Vanaspati Soya food 1 Jammu 2 Ganganagar 3 Baran 4 Kota 5 Guna 6 Kandla 7 Shujalpur 8 Piparia 9 Gadarwara 10 Haldia 11 Manglia 12 Nagpur 13 Washim 14 Daloda 15 Patalganga 16 Mangalore 17 Chennai 18 Kakinada (A.P) palm mill 19 Vijaywada (A.P) palm mill 20 Durgawati (Bihar) 21 Mysore (Palm Crushing) 22 Krishnapatnam

Mysore

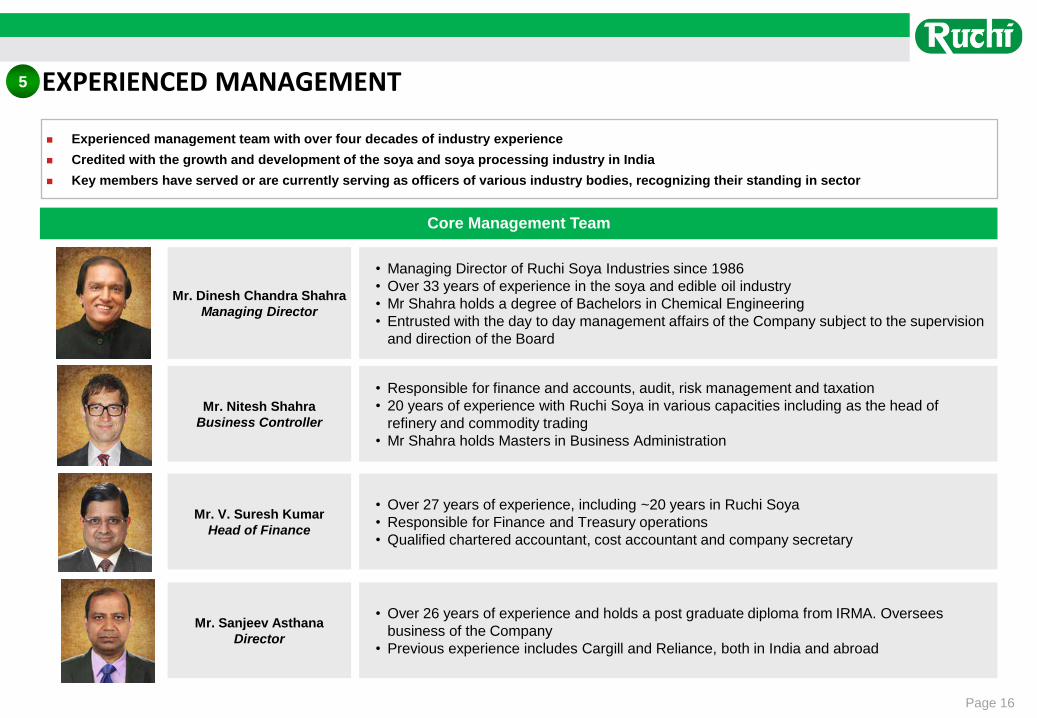

• Over 26 years of experience and holds a post graduate diploma from IRMA. Oversees

business of the Company

• Previous experience includes Cargill and Reliance, both in India and abroad

• Over 27 years of experience, including ~20 years in Ruchi Soya

• Responsible for Finance and Treasury operations

• Qualified chartered accountant, cost accountant and company secretary

• Responsible for finance and accounts, audit, risk management and taxation

• 20 years of experience with Ruchi Soya in various capacities including as the head of

refinery and commodity trading

• Mr Shahra holds Masters in Business Administration

• Managing Director of Ruchi Soya Industries since 1986

• Over 33 years of experience in the soya and edible oil industry

• Mr Shahra holds a degree of Bachelors in Chemical Engineering

• Entrusted with the day to day management affairs of the Company subject to the supervision

and direction of the Board

EXPERIENCED MANAGEMENT

Experienced management team with over four decades of industry experience

Credited with the growth and development of the soya and soya processing industry in India

Key members have served or are currently serving as officers of various industry bodies, recognizing their standing in sector

5

Core Management Team

Mr. Sanjeev Asthana

Director

Mr. V. Suresh Kumar

Head of Finance

Mr. Nitesh Shahra

Business Controller

Mr. Dinesh Chandra Shahra

Managing Director

Page 16

FINANCIAL PERFORMANCE

CONSOLIDATED FINANCIAL PERFORMANCE

Page 18

INR Million FYE MAR 10 FYE MAR 11 FYE MAR 12 FYE MAR 13

Total Revenue 145,333 183,729 305,835 303211

EBITDA(1) 5,316 7,173 10,080 9750

EBITDA (% of gross revenues) 3.7% 3.9% 3.3% 3.21%

Finance Cost(2) 1,537 2,550 6,625 4482

Depreciation & Amortisation 1,203 1,458 1,729 1869

Profit Before Tax 2,809 3,381 1,957 3610

Profit after Tax(3) 1,749 2,252 869 2732

Source: Company Filings.

(1) EBITDA = Total Revenue – Total Expenses

(2) Finance cost = Interest expense + Other Borrowing Costs + Net Loss of Foreign Currency Transactions

(3) Profit after tax excludes profit attributable to Minority Interest

CONSOLIDATED BALANCE SHEET

Page 19

INR Million FYE MAR 10 FYE MAR 11 FYE MAR 12 FYE MAR 13

Net Fixed Assets Incl. CWIP 20,942 24,165 27,375 28,743

Cash and Cash balances 15,997 19,547 33,151 42,962

Inventories 16,184 32,045 41,614 35,628

Total Assets 80,070 111,460 146,142 168,222

Long-term Borrowings 7,053 7,426 8,753 11,226

Short-term Borrowings 17,508 37,699 53,431 62,540

Gross Borrowings 24,561 45,125 62,184 73,766

Net Borrowings(1) 8,564 25,578 29,033 30,804

Shareholders’ Funds(2) 19,678 22,375 22,499 24,719

Total Capitalization(3) 28,242 47,953 51,532 55,523

Source: Company filings

(1) Net Borrowings = Gross Borrowings – Cash and cash balances

(2) Shareholders’ funds = Paid up Capital + Retained Earnings + Minority Interest

(3) Total Capitalization = Consolidated Net Borrowings + Shareholders’ Funds

SUMMARY CONSOLIDATED FINANCIALS AND RATIOS

Page 20

Revenues EBITDA

Total Assets Net Leverage (1)

INR Bn INR Bn

INR Bn

Shareholders’ Funds

Net Borrowings / Total Capitalization (2)

INR Bn

Source:

(1) Net Leverage = Net Borrowings / EBITDA

(2) Net Borrowings = Gross Borrowings – Cash and cash balances; Total Capitalization = Consolidated Net Borrowings + Shareholders’ Fund

CAGR 2010- 2012: 28.3% CAGR 2010- 2012: 23.8% CAGR 2010- 2012: 4.6%

CAGR 2010- 2012: 22.2%

0

50

100

150

200

250

300

350

FY10 FY11 FY12 FY13

145

184

306 303

0

2

4

6

8

10

12

FY10 FY11 FY12 FY13

5.31

7.17

10.08 9.75

0

10

20

30

FY10 FY11 FY12 FY13

19.6 22.3 22.5

24.7

0

20

40

60

80

100

120

140

160

180

FY10 FY11 FY12 FY13

80

111

146

168

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FY10 FY11 FY12 FY13

1.61

3.57

2.88 3.16

0.0

0.1

0.2

0.3

0.4

0.5

0.6

FY10 FY11 FY12 FY13

0.30

0.53 0.56 0.55

APPENDIX

ABBREVIATIONS

Page 22

Abbreviations Used Description

FY / FYE Financial Year

9ME 9 Months Ending

Mn Million

Bn Billion

yr Year

MT Metric Tonnes

MTPA Metric Tonnes per annum

BSE BSE Limited

NSE National Stock Exchange of India Limited

INR Indian Rupee

US$ United States Dollar

USDA FAS United States Department of Agriculture Foreign Agricultural Service

IMF International Monetary Fund

THANK YOU!