RPC Group Plc Proposed Acquisition of British Polythene .../media/Files/R/RPC-Group/documents... ·...

16

RPC Group Plc Proposed Acquisition of BPI 101 RPC Group Plc Proposed Acquisition of British Polythene Industries PLC June 2016

Transcript of RPC Group Plc Proposed Acquisition of British Polythene .../media/Files/R/RPC-Group/documents... ·...

RPC Group Plc

Proposed Acquisition of BPI

101

RPC Group Plc Proposed Acquisition of British Polythene Industries PLC

June 2016

RPC Group Plc

Proposed Acquisition of BPI

102

Disclaimer Important Notice THIS PRESENTATION (AND THE INFORMATION CONTAINED HEREIN) IS NOT FOR RELEASE, PUBLICATION, DISTRIBUTION OR FORWARDING, DIRECTL Y OR INDIRECTLY, IN WHOLE OR IN PART, IN, INTO OR FROM AUSTRALIA, CANADA, JAPAN, THE REPUBLIC OF SOUTH AFRICA, THE UNITED STATES OF AMERICA OR ANY OTHER JURISDICTION WHERE TO DO SO WOULD CONSTITUTE A VIOLATION OF THE RELEVANT LAWS OF SUCH JURISDICTION. This presentation has been prepared and issued by, and is the sole responsibility of, RPC Group Plc (the “Company” or “RPC”) and is being delivered in connection with the proposed offer by the Company for the entire issued and to be issued share capital of British Polythene Industries PLC (“BPI”) (the “Transaction”). For the purposes of this notice, the presentation that follows shall mean and include the slides that follow, the oral presentation of the slides by the Company, the question-and-answer session that follows that oral presentation, hard copies of this document

and any materials distributed at, or in connection with, that presentation. Terms defined in the announcement of the Transact ion dated 9 June 2016 shall have the same meaning when used in this notice. This presentation is being supplied to you solely for your information and does not constitute or form part of, and should not be construed as, any offer for sale or subscription of, or solicitation or any offer to buy or subscribe for or otherwise acquire, any securities of the Company in any

jurisdiction pursuant to the Transaction or otherwise. This presentation does not constitute a prospectus or prospectus equivalent document. This presentation and the materials distributed in connection with this presentation are not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, country or other jurisdiction in which such distribution, publication,

availability or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction, including, but not limited to, the United States, Canada, Australia, Japan or South Africa. Any failure to comply with these restrictions may constitute a violation of the securities laws of any such jurisdiction. Any person into whose possession this presentation comes should inform themselves about, and observe, any such restrictions. The Company does not intend to make any public offering of securities in the United States.

In the United States, this presentation is directed only at persons who are qualified institutional buyers (“QIBs”) as defined in Rule 144A of the US Securities Act of 1933 (the “US Securities Act”). In the United Kingdom, this presentation is directed only at (i) persons who have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”); or (ii) high net worth entities falling within Article 49(2)(a) to (d) of the Order or to those persons to whom it can ot herwise

lawfully be distributed (each a “Relevant Person”). This presentation must not be acted or relied upon by persons other than Relevant Persons. In member states of the European Economic Area (the “EEA”) other than the United Kingdom, this presentation is directly only at “qualified investors” within the meaning of Article 2(1)(e) of the Prospectus Directive (Directive 2003/71/EC as amended, including by EU Directive 2010/73/EU to the extent implemented in the relevant member state (the “Prospectus Directive”)).

This presentation is confidential and may not be reproduced, redistributed or forwarded, directly or indirectly, to any other person or published, in whole or in part, for any purpose. The information contained in this presentation has not been independently verified. Neither the Company nor, N M Rothschild & Sons Limited (“Rothschild”), Deutsche Bank AG, London Branch (“Deutsche Bank”) or Panmure Gordon (UK) Limited (“Panmure Gordon”) (Rothschild, Deutsche Bank and Panmure Gordon collectively, the “Banks”) nor any of their parent or subsidiary undertakings, or the

subsidiary undertaking of any such parent undertakings, or any of such person’s respective partners, shareholders, directors, officers, affiliates, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any information or opinions presented or contained in this presentation nor shall they accept any responsibility whatsoever for, or make any representation or warranty, express or implied, as to the truth, fullness, accuracy or completeness of the information in this presentation (or whether any information has

been omitted from the presentation) or any other information relating to the Company, its subsidiaries or associated companies, in any form whatsoever, howsoever transmitted or made available or for any loss howsoever arising from any use of this presentation or its contents or otherwise

arising in connection therewith.

The information and opinions presented or contained in this presentation (including forward-looking statements) speak as of the date hereof (unless otherwise stated) and are subject to updating, revision, verification and amendment without notice and such information may change materially. Neither the Company nor the Banks nor their affiliates nor their advisers are under an obligation to correct, update or keep current the information contained in this presentation or to publicly announce or inform you of the result of any revision to the statements made herein except where they

would be required to do so under applicable law. This presentation is made on the express understanding that it does not cont ain all information that may be required to evaluable the Company. No part of this presentation, nor the fact of its distribution, should form the basis of, or be relied on

in connection with, any contract or commitment or investment decision relating thereto, nor does it constitute a recommendation regarding the securities of the Company. The information and opinions in this presentation are not based upon a consideration of your particular investment

objectives, financial situation or needs. This presentation does not constitute an audit or due diligence review and should not be construed as such nor has it been approved by any regulatory or supervisory body. You must make y our own independent assessment and investigations as you deem necessary. You may wish to seek independent legal, regulatory, accounting, tax and such professional advice as appropriate with regards to the contents of this presentation.

Matters discussed in this presentation may constitute forward-looking statements that reflect management’s current views with respect to future events and financial and operational performance. Forward-looking statements include statements concerning plans, object ives, goals, strategies,

future events or performance and underlying assumptions and other statements which are other than statements of historical facts. The words “believe”, “expect”, “anticipate”, “intend”, “estimate”, “forecast”, “project”, “will”, “may”, “should” and similar expressions identify forward-looking

statements. Others can be identified from the context in which they are made. These forward-looking statements involve various assumptions, known and unknown risks, uncertainties, estimates and other factors which are beyond the Company's control and which may cause actual results or performance to differ materially from those expressed or implied from such forward-looking statements, whether as a result of new information, future events or results or otherwise. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and

future events could differ materially from those anticipated in such statements. Past performance of the Company cannot be relied on as a guide to future performance. Accordingly, you should not place undue reliance on forward-looking statements due to the inherent uncertainty therein.

Other than the Quantified Financial Benefits Statement, no statement in this presentation is intended as a profit forecast or estimate for any period and no statement in this presentation should be interpreted to mean that earnings or earnings per ordinary share for RPC or BPI respectively for

the current or future financial years would necessarily match or exceed the historical published earnings or earnings per ordinary share for RPC or BPI respectively. To the extent available, the industry, market and competitive position data contained in this presentation come from official or third party sources. The Company has not independently verified the data contained therein and there is no guarantee of the accuracy or completeness of such data.

In addition, certain of the industry, market and competitive position data contained in this presentation come from the Company's own internal research and estimates based on the knowledge and experience of the Company's management in the markets in which the Company operates.

While the Company believes, acting in good faith, that such research and estimates are reasonable and reliable, they, and their underlying methodology and assumptions, have not been verified by any independent source for accuracy or completeness and are subject to change. Accordingly,

you should not place reliance on any of the industry, market or competitive position data contained in this presentation. The statements in the Quantified Financial Benefits Statement relate to future actions and circumstances which, by their nature, involve risks, uncertainties and contingencies. As a result, the synergies and cost savings referred to may not be achieved, or may be achieved later or sooner than

estimated, or those achieved could be materially different from those estimated. Neither these statements nor any other statement in this presentation should be construed as a profit forecast or interpreted to mean that the Combined Group's earnings in the first full year following implementation of the Transaction, or in any subsequent period, would necessarily match or be greater than or be less than those of RPC and/or BPI for the relevant preceding financial period or any other period. For the purposes of Rule 28 of the Takeover Code, the Quantified Financial

Benefits Statement contained in this presentation is the responsibility of RPC and the RPC Directors. Deutsche Bank AG is authorised under German Banking Law (competent authority: BaFIN – Federal Financial Supervisory Authority). Deutsche Bank AG, London Branch is further authorised by the Prudential Regulation Authority (the “PRA”) and is subject to limited regulation by the FCA

and PRA. Rothschild is authorised and regulated in the United Kingdom by the Financial Conduct Authority (the “FCA”) and the PRA. Panmure Gordon is regulated in the United Kingdom by the FCA. The Banks, are acting exclusively for the Company and no one else. None of the Banks will regard any other person (whether or not a recipient of this presentation) as a client and will not be responsible to anyone other than the Company for providing the protections afforded to their respective clients nor for providing advice in relation to this presentation or any transaction,

arrangement or other matter referred to in this presentation. Apart from the responsibilities and liabilities, if any, which may be imposed on the Banks by the Financial Services and Markets Act 2000 (as amended) or the regulatory regime established thereunder, or under the regulatory regime of any jurisdiction where exclusion of liability under the relevant regulatory regime would be illegal, void or unenforceable, the Banks disclaim all and any responsibility or liability, whether arising in tort, contract or otherwise, which they might otherwise have in respect of this presentation.

Note to US investors The Offer relates to the shares of a UK company and it is proposed to be made by means of a scheme of arrangement provided for under the laws of England and Wales. The Scheme will relate to the shares of a UK company that is a “foreign private issuer” as def ined under Rule 3b-4 under

the US Exchange Act. A transaction effected by means of a scheme of arrangement is not subject to the shareholder vote, proxy solicitation and tender offer rules under the US Exchange Act. Accordingly, the Scheme is subject to the disclosure requirement s and practices applicable in the UK to schemes of arrangement, which differ from the disclosure requirements and practices of US shareholder vote, proxy solic itation and tender offer rules.

By attending and otherwise accessing this presentation, you warrant, represent, undertake and acknowledge that ( i) you have read and agree to comply with the foregoing limitations and restrictions including, without limitation, the obligation to keep this presentation and its contents confidential, (ii) you are able to receive this presentation without contravention of any applicable legal or regulatory rest rictions, (iii) if you are in the United States, you are a QIB, (iv) if you are in a member state of the EEA (other than the United Kingdom), you are a “qualified investor” and (v)

if you are in the United Kingdom, you are a Relevant Person. Further information, including all documents related to the proposed Transaction, can be found at: www.rpc-group.com.

RPC Group Plc

Proposed Acquisition of BPI

103

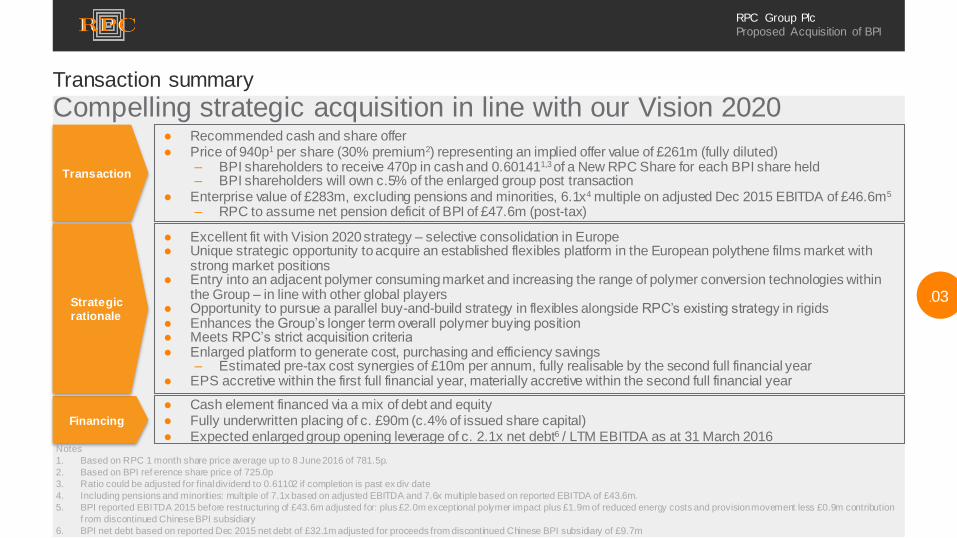

Compelling strategic acquisition in line with our Vision 2020 Transaction summary

Transaction

Financing

Strategic

rationale

● Recommended cash and share offer ● Price of 940p1 per share (30% premium2) representing an implied offer value of £261m (fully diluted)

– BPI shareholders to receive 470p in cash and 0.601411,3 of a New RPC Share for each BPI share held – BPI shareholders will own c.5% of the enlarged group post transaction

● Enterprise value of £283m, excluding pensions and minorities, 6.1x4 multiple on adjusted Dec 2015 EBITDA of £46.6m5 – RPC to assume net pension deficit of BPI of £47.6m (post-tax)

● Cash element financed via a mix of debt and equity ● Fully underwritten placing of c. £90m (c.4% of issued share capital) ● Expected enlarged group opening leverage of c. 2.1x net debt6 / LTM EBITDA as at 31 March 2016

● Excellent fit with Vision 2020 strategy – selective consolidation in Europe ● Unique strategic opportunity to acquire an established flexibles platform in the European polythene films market with

strong market positions ● Entry into an adjacent polymer consuming market and increasing the range of polymer conversion technologies within

the Group – in line with other global players ● Opportunity to pursue a parallel buy-and-build strategy in flexibles alongside RPC’s existing strategy in rigids ● Enhances the Group’s longer term overall polymer buying position ● Meets RPC’s strict acquisition criteria ● Enlarged platform to generate cost, purchasing and efficiency savings

– Estimated pre-tax cost synergies of £10m per annum, fully realisable by the second full financial year ● EPS accretive within the first full financial year, materially accretive within the second full financial year

Notes

1. Based on RPC 1 month share price average up to 8 June 2016 of 781.5p.

2. Based on BPI ref erence share price of 725.0p

3. Ratio could be adjusted for final dividend to 0.61102 if completion is past ex div date

4. Including pensions and minorities: multiple of 7.1x based on adjusted EBITDA and 7.6x multiple based on reported EBITDA of £43.6m.

5. BPI reported EBITDA 2015 before restructuring of £43.6m adjusted for: plus £2.0m exceptional polymer impact plus £1.9m of reduced energy costs and provision movement less £0.9m contribution

f rom discontinued Chinese BPI subsidiary

6. BPI net debt based on reported Dec 2015 net debt of £32.1m adjusted for proceeds from discontinued Chinese BPI subsidiary of £9.7m

RPC Group Plc

Proposed Acquisition of BPI

104

Profile of BPI BPI is a leading manufacturer and supplier of polythene films for a diverse range of end

markets, including agriculture and horticulture, construction, industrial, healthcare and waste services and food & non-food retail

● Leading brands based upon innovative multi-layer films

● Global leader in silage stretch films, strong positions in the industrial and consumer films market

● Proven ability to innovate through development of new, added value products

● Supplies c. 275,000 tonnes of polythene films each year for a diverse range of everyday

applications

● One of the largest recyclers of waste polythene films in Europe; recycling c. 65,000 tonnes

annually

● Operates through 19 manufacturing facilities across the UK, Europe and North America − 55% of 2015 sales by destination were in the UK

● As of December 2015 the company employed c. 2,000 people

● Listed on the main market of the London Stock Exchange

● Headquartered in Greenock (Scotland), UK

● Adjusted sales of £464m1 and adjusted EBITDA of £46.6m1 in 2015

Business overview BPI

Source: Company information

Notes

1. BPI reported sales 2015 of £468.3m less £4.7m sales from discontinued Chinese BPI subsidiary . BPI reported EBITDA 2015 before restructuring of £43.6m adjusted for: plus £2.0m exceptional

poly mer impact plus £1.9m of reduced energy costs and provision movement less £0.9m contribution from discontinued Chinese BPI subsidiary

RPC Group Plc

Proposed Acquisition of BPI

105

£150m £126m

Overview of end market sectors

• Container liners • Heavy duty sacks • Pallet protection • Form fill seal films

Group

Share of sales1 FY2015 Total reported sales: £468m

Products

Brands

Retail Food

Chain Industrial

Agriculture and

Horticulture Construction

Sample products

• Silage products • Greenhouse films • Polytunnel covers • Consumer packaging for

retail horticulture • Animal feed packaging • Fertiliser packaging

• Gas protection systems • Structural waterproofing • Protection films • Ventilated cement sacks • Overwrap films for insulation • Packaging for aggregate,

bricks and blocks

• Bakery packaging • Frozen food packaging • Shrink film for cans and

bottles • Fresh produce packaging • Refuse sacks • Transit packaging

Healthcare and

Waste Serv ices

• Refuse sacks • Clinical waste sacks • Recycling bags • Caddy liners • Aprons

• Mailing bags and garment film

• Mailing film • Transit packaging • Protective films • Heavy duty refuse sacks

£66m £61m £37m £28m

Selected customers

Business overview BPI

Non-Food Retail

Source: Company information

Notes

1 Includes revenues from BPI China subsidiary (disposed of in April 2016, £4.7m external sales)

32% 27% 14% 13% 8% 6%

RPC Group Plc

Proposed Acquisition of BPI

106

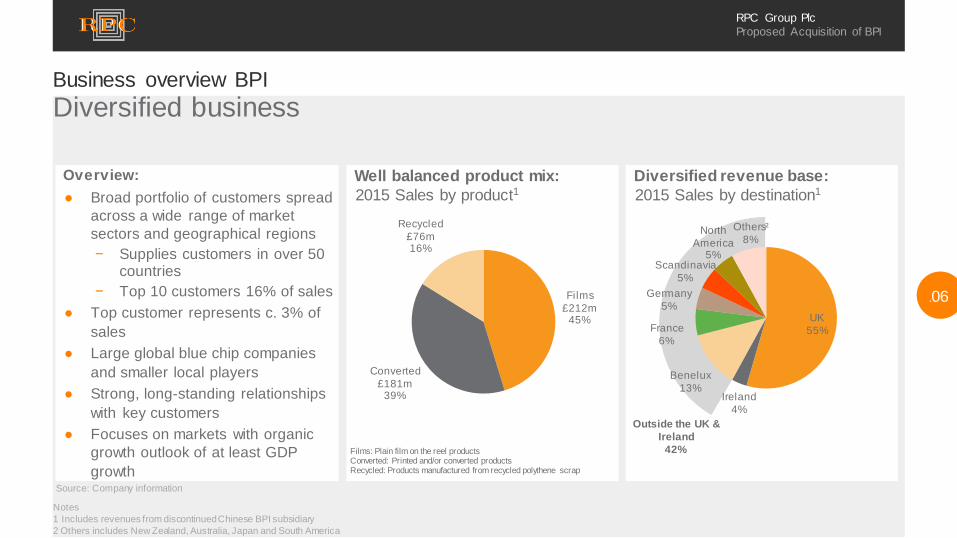

Well balanced product mix:

2015 Sales by product1

Films

£212m 45%

Converted

£181m 39%

Recycled

£76m 16%

Diversified revenue base:

2015 Sales by destination1

Overview:

● Broad portfolio of customers spread

across a wide range of market

sectors and geographical regions

− Supplies customers in over 50 countries

− Top 10 customers 16% of sales

● Top customer represents c. 3% of

sales

● Large global blue chip companies

and smaller local players

● Strong, long-standing relationships

with key customers

● Focuses on markets with organic

growth outlook of at least GDP

growth

Diversified business Business overview BPI

Source: Company information

Outside the UK &

Ireland

42%

Notes

1 Includes revenues from discontinued Chinese BPI subsidiary

2 Others includes New Zealand, Australia, Japan and South America

Films: Plain film on the reel products Converted: Printed and/or converted products Recycled: Products manufactured from recycled polythene scrap

UK

55%

Ireland

4%

Benelux

13%

France

6%

Germany

5%

Scandinavia

5%

North

America 5%

Others²

8%

RPC Group Plc

Proposed Acquisition of BPI

107

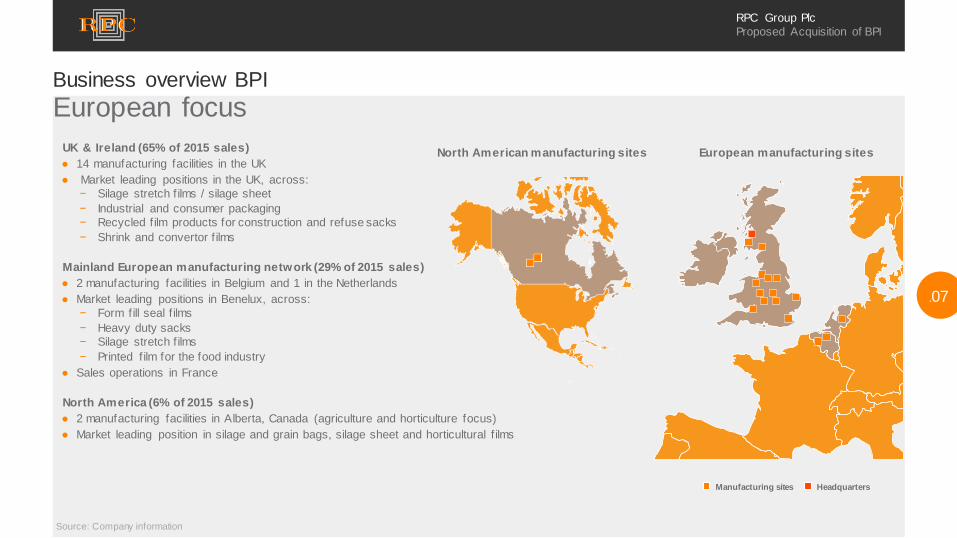

European focus Business overview BPI

Source: Company information

UK & Ireland (65% of 2015 sales)

● 14 manufacturing facilities in the UK

● Market leading positions in the UK, across:

− Silage stretch f ilms / silage sheet

− Industrial and consumer packaging

− Recycled f ilm products for construction and refuse sacks

− Shrink and convertor f ilms

Mainland European manufacturing network (29% of 2015 sales)

● 2 manufacturing facilities in Belgium and 1 in the Netherlands

● Market leading positions in Benelux, across:

− Form fill seal f ilms

− Heavy duty sacks

− Silage stretch f ilms

− Printed f ilm for the food industry

● Sales operations in France

North America (6% of 2015 sales)

● 2 manufacturing facilities in Alberta, Canada (agriculture and horticulture focus)

● Market leading position in silage and grain bags, silage sheet and horticultural f ilms

Manufacturing sites Headquarters

European manufacturing sites North American manufacturing sites

RPC Group Plc

Proposed Acquisition of BPI

108

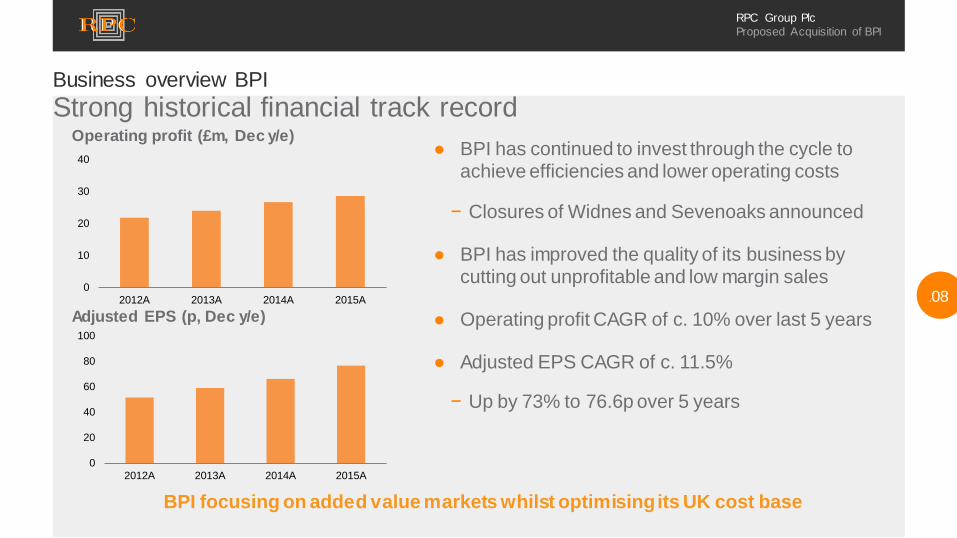

Operating profit (£m, Dec y/e)

Strong historical financial track record Business overview BPI

● BPI has continued to invest through the cycle to achieve efficiencies and lower operating costs

− Closures of Widnes and Sevenoaks announced

● BPI has improved the quality of its business by cutting out unprofitable and low margin sales

● Operating profit CAGR of c. 10% over last 5 years

● Adjusted EPS CAGR of c. 11.5%

− Up by 73% to 76.6p over 5 years

Adjusted EPS (p, Dec y/e)

0

10

20

30

40

2012A 2013A 2014A 2015A

0

20

40

60

80

100

2012A 2013A 2014A 2015A

BPI focusing on added value markets whilst optimising its UK cost base

RPC Group Plc

Proposed Acquisition of BPI

109

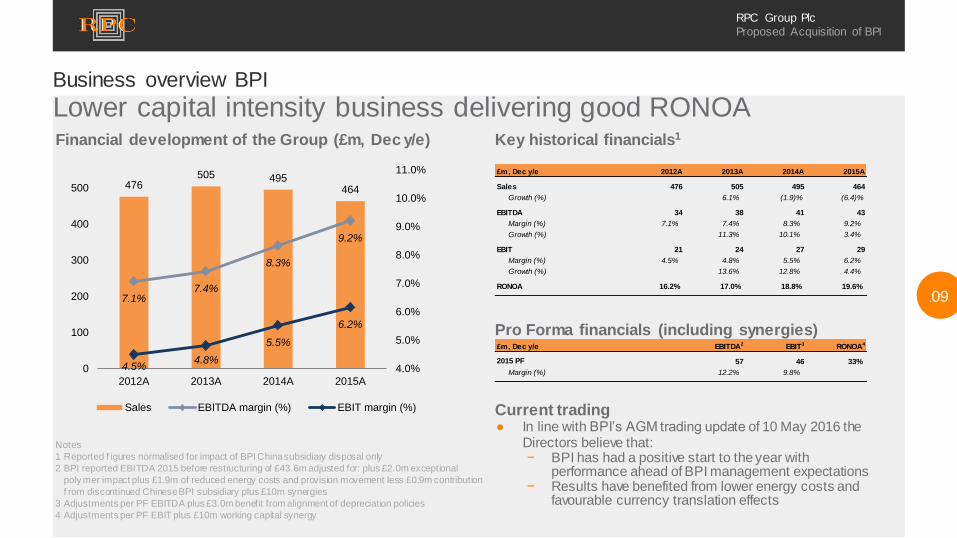

Financial development of the Group (£m, Dec y/e)

Lower capital intensity business delivering good RONOA Key historical financials1

Business overview BPI

Notes

1 Reported f igures normalised for impact of BPI China subsidiary disposal only

2 BPI reported EBITDA 2015 before restructuring of £43.6m adjusted for: plus £2.0m exceptional

poly mer impact plus £1.9m of reduced energy costs and provision movement less £0.9m contribution

f rom discontinued Chinese BPI subsidiary plus £10m synergies

3 Adjustments per PF EBITDA plus £3.0m benefit from alignment of depreciation policies

4 Adjustments per PF EBIT plus £10m working capital synergy

Current trading ● In line with BPI’s AGM trading update of 10 May 2016 the

Directors believe that: − BPI has had a positive start to the year with

performance ahead of BPI management expectations − Results have benefited from lower energy costs and

favourable currency translation effects

Pro Forma financials (including synergies)

£m, Dec y/e 2012A 2013A 2014A 2015A

Sales 476 505 495 464

Growth (%) 6.1% (1.9)% (6.4)%

EBITDA 34 38 41 43

Margin (%) 7.1% 7.4% 8.3% 9.2%

Growth (%) 11.3% 10.1% 3.4%

EBIT 21 24 27 29

Margin (%) 4.5% 4.8% 5.5% 6.2%

Growth (%) 13.6% 12.8% 4.4%

RONOA 16.2% 17.0% 18.8% 19.6%

£m, Dec y/e EBITDA2 EBIT3 RONOA4

2015 PF 57 46 33%

Margin (%) 12.2% 9.8%

476505 495

464

7.1%7.4%

8.3%

9.2%

4.5% 4.8%

5.5%

6.2%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

0

100

200

300

400

500

2012A 2013A 2014A 2015A

Sales EBITDA margin (%) EBIT margin (%)

RPC Group Plc

Proposed Acquisition of BPI

110

Excellent fit with Vision 2020 strategy – selective consolidation in Europe

Strong market positions,

differentiated by engineering

capabilities

● Entry into high added value segments in a fragmented polymer consuming market ● Leading positions in its markets, supported by industry recognised, branded products ● BPI’s strong focus on innovation fits well with RPC’s focus on product development

● Opportunity to extend RPC’s European consolidation strategy into polythene films

● Identified pipeline of potential strategic acquisition targets that would enhance BPI’s existing product segments and further consolidate polymer procurement

Access to a European

polythene films platform

enabling a parallel buy-and-

build strategy

Enhancing the Group’s overall

longer term polymer buying

position

● RPC currently buys c. 600kt of polymer, mainly in Western Europe

● BPI buys c. 200kt of polymer, mainly in Western Europe

Group strategy and acquisition rationale

Entry to an adjacent polymer

consuming market

● Complementary parallel addition to RPC’s existing strategy in rigid technologies ● Majority of larger packaging groups operate in both rigid and flexible plastic market segments

RPC Group Plc

Proposed Acquisition of BPI

111

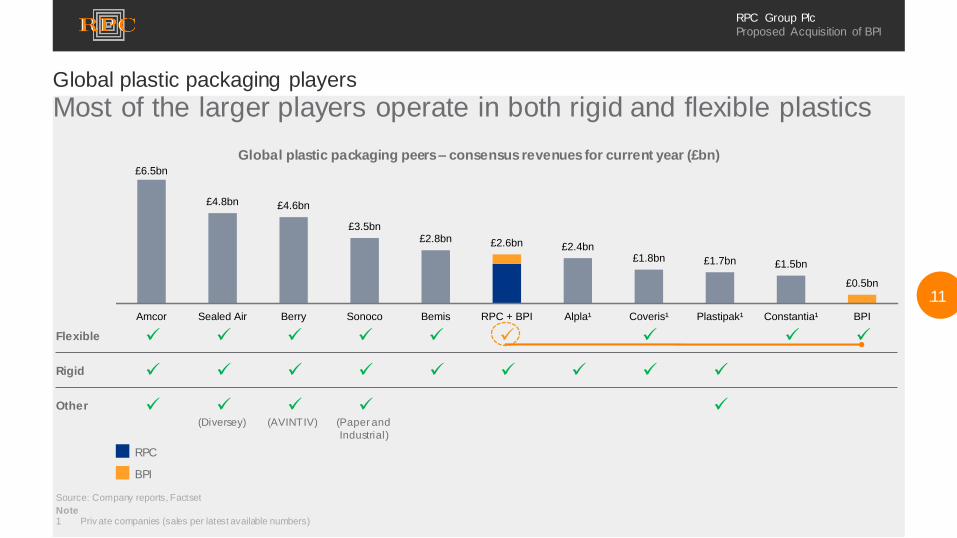

Most of the larger players operate in both rigid and flexible plastics Global plastic packaging players

Global plastic packaging peers – consensus revenues for current year (£bn)

Flexible

Rigid

Other

(Diversey) (AVINTIV) (Paper and

Industrial)

Source: Company reports, Factset

Note 1 Priv ate companies (sales per latest available numbers)

£6.5bn

£4.8bn £4.6bn

£3.5bn £2.8bn £2.6bn £2.4bn

£1.8bn £1.7bn £1.5bn

£0.5bn

Amcor Sealed Air Berry Sonoco Bemis RPC + BPI Alpla¹ Coveris¹ Plastipak¹ Constantia¹ BPI

RPC

BPI

RPC Group Plc

Proposed Acquisition of BPI

112

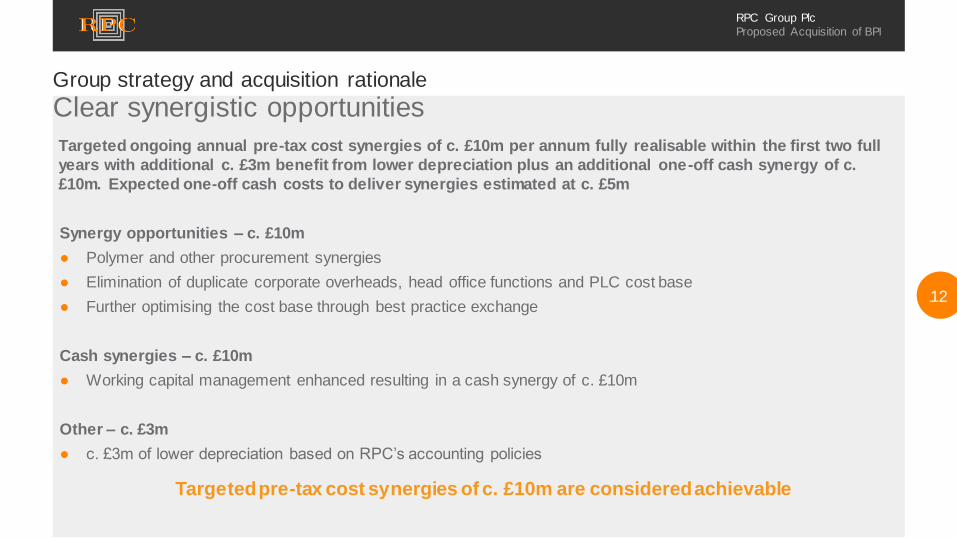

Clear synergistic opportunities

Targeted ongoing annual pre-tax cost synergies of c. £10m per annum fully realisable within the first two full

years with additional c. £3m benefit from lower depreciation plus an additional one-off cash synergy of c.

£10m. Expected one-off cash costs to deliver synergies estimated at c. £5m

Synergy opportunities – c. £10m

● Polymer and other procurement synergies

● Elimination of duplicate corporate overheads, head office functions and PLC cost base

● Further optimising the cost base through best practice exchange

Cash synergies – c. £10m

● Working capital management enhanced resulting in a cash synergy of c. £10m

Other – c. £3m

● c. £3m of lower depreciation based on RPC’s accounting policies

Targeted pre-tax cost synergies of c. £10m are considered achievable

Group strategy and acquisition rationale

RPC Group Plc

Proposed Acquisition of BPI

113

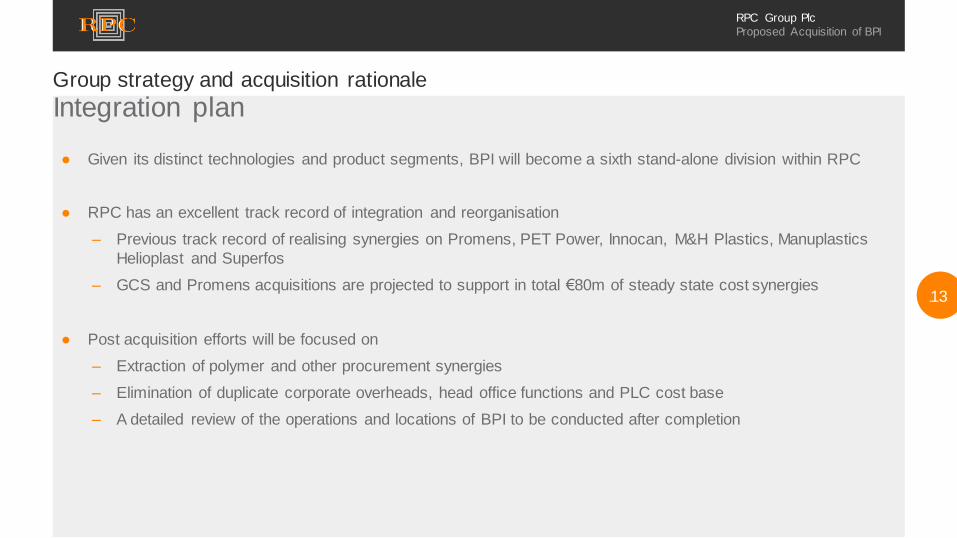

Integration plan

● Given its distinct technologies and product segments, BPI will become a sixth stand-alone division within RPC

● RPC has an excellent track record of integration and reorganisation

– Previous track record of realising synergies on Promens, PET Power, Innocan, M&H Plastics, Manuplastics

Helioplast and Superfos

– GCS and Promens acquisitions are projected to support in total €80m of steady state cost synergies

● Post acquisition efforts will be focused on

– Extraction of polymer and other procurement synergies

– Elimination of duplicate corporate overheads, head office functions and PLC cost base

– A detailed review of the operations and locations of BPI to be conducted after completion

Group strategy and acquisition rationale

RPC Group Plc

Proposed Acquisition of BPI

114

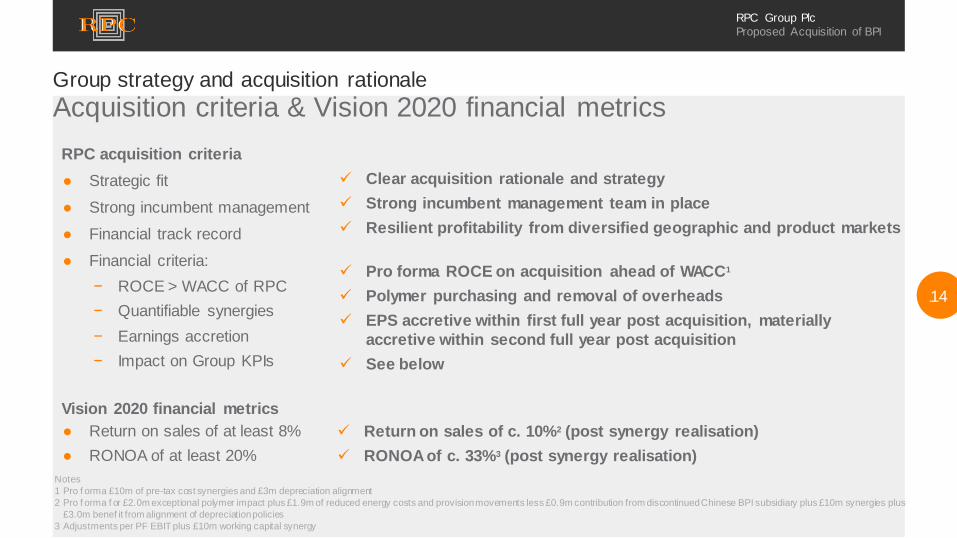

Acquisition criteria & Vision 2020 financial metrics

RPC acquisition criteria

● Strategic fit

● Strong incumbent management

● Financial track record

● Financial criteria:

− ROCE > WACC of RPC

− Quantifiable synergies

− Earnings accretion

− Impact on Group KPIs

Vision 2020 financial metrics

● Return on sales of at least 8%

● RONOA of at least 20%

Clear acquisition rationale and strategy

Strong incumbent management team in place

Resilient profitability from diversified geographic and product markets

Group strategy and acquisition rationale

Pro forma ROCE on acquisition ahead of WACC1

Polymer purchasing and removal of overheads

EPS accretive within first full year post acquisition, materially

accretive within second full year post acquisition

See below

Return on sales of c. 10%2 (post synergy realisation)

RONOA of c. 33%3 (post synergy realisation)

Notes

1 Pro f orma £10m of pre-tax cost synergies and £3m depreciation alignment

2 Pro f orma f or £2.0m exceptional polymer impact plus £1.9m of reduced energy costs and provision movements less £0.9m contribution from discontinued Chinese BPI subsidiary plus £10m synergies plus

£3.0m benef it from alignment of depreciation policies

3 Adjustments per PF EBIT plus £10m working capital synergy

RPC Group Plc

Proposed Acquisition of BPI

115

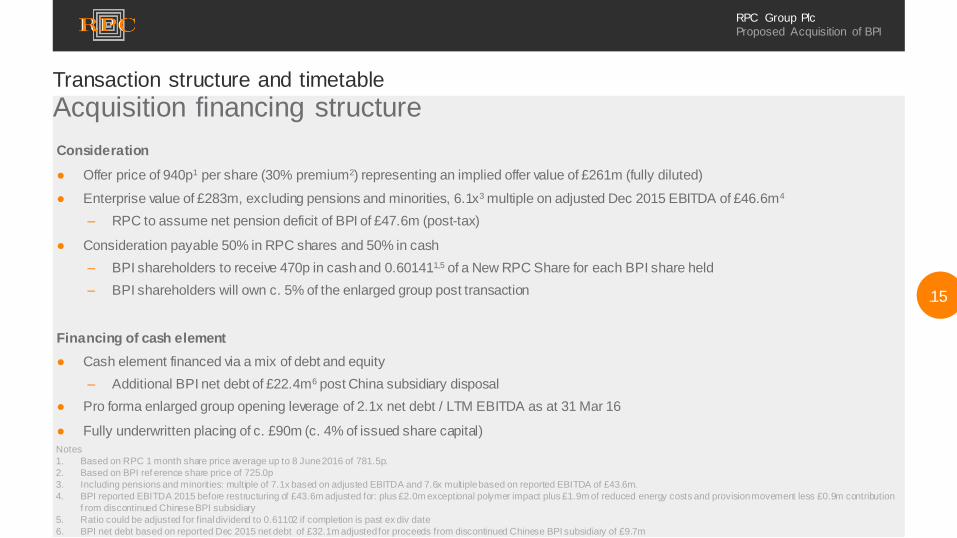

Acquisition financing structure

Consideration

● Offer price of 940p1 per share (30% premium2) representing an implied offer value of £261m (fully diluted)

● Enterprise value of £283m, excluding pensions and minorities, 6.1x3 multiple on adjusted Dec 2015 EBITDA of £46.6m4

– RPC to assume net pension deficit of BPI of £47.6m (post-tax)

● Consideration payable 50% in RPC shares and 50% in cash

– BPI shareholders to receive 470p in cash and 0.601411,5 of a New RPC Share for each BPI share held

– BPI shareholders will own c. 5% of the enlarged group post transaction

Financing of cash element

● Cash element financed via a mix of debt and equity

– Additional BPI net debt of £22.4m6 post China subsidiary disposal

● Pro forma enlarged group opening leverage of 2.1x net debt / LTM EBITDA as at 31 Mar 16

● Fully underwritten placing of c. £90m (c. 4% of issued share capital)

Notes

1. Based on RPC 1 month share price average up to 8 June 2016 of 781.5p.

2. Based on BPI ref erence share price of 725.0p

3. Including pensions and minorities: multiple of 7.1x based on adjusted EBITDA and 7.6x multiple based on reported EBITDA of £43.6m.

4. BPI reported EBITDA 2015 before restructuring of £43.6m adjusted for: plus £2.0m exceptional polymer impact plus £1.9m of reduced energy costs and provision movement less £0.9m contribution

f rom discontinued Chinese BPI subsidiary

5. Ratio could be adjusted for final dividend to 0.61102 if completion is past ex div date

6. BPI net debt based on reported Dec 2015 net debt of £32.1m adjusted for proceeds from discontinued Chinese BPI subsidiary of £9.7m

Transaction structure and timetable

RPC Group Plc

Proposed Acquisition of BPI

116

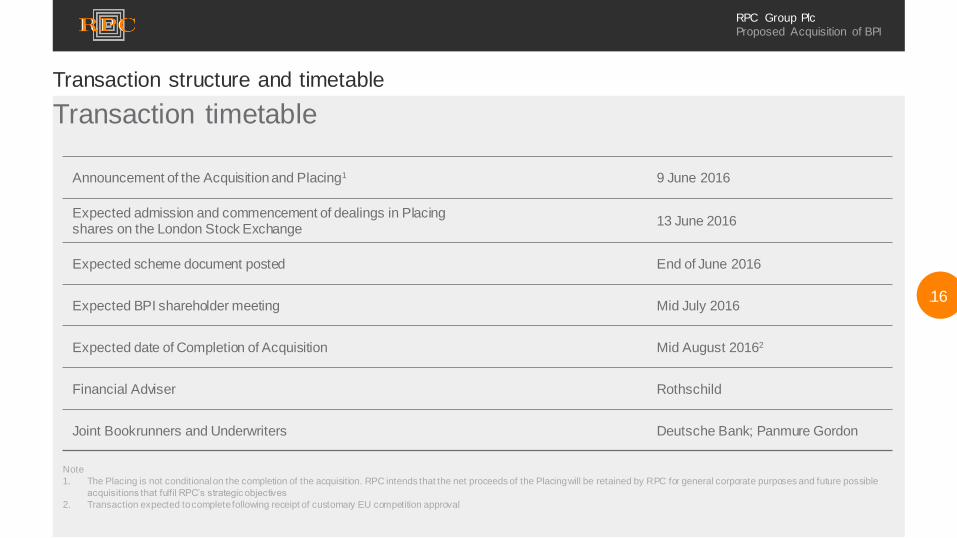

Transaction timetable

Transaction structure and timetable

Announcement of the Acquisition and Placing1 9 June 2016

Expected admission and commencement of dealings in Placing shares on the London Stock Exchange

13 June 2016

Expected scheme document posted End of June 2016

Expected BPI shareholder meeting Mid July 2016

Expected date of Completion of Acquisition Mid August 20162

Financial Adviser Rothschild

Joint Bookrunners and Underwriters Deutsche Bank; Panmure Gordon

Note

1. The Placing is not conditional on the completion of the acquisition. RPC intends that the net proceeds of the Placing will be retained by RPC for general corporate purposes and future possible

acquisitions that fulfil RPC’s strategic objectives

2. Transaction expected to complete following receipt of customary EU competition approval

![The Sage Group plc Acquisition of Intacct Corporation[Draft] The Sage Group plc Acquisition of Intacct Corporation Stephen Kelly, CEO Steve Hare, CFO [x] July 2017 The Sage Group Plc](https://static.fdocuments.in/doc/165x107/5e8d33fbc95aac529244a94b/the-sage-group-plc-acquisition-of-intacct-corporation-draft-the-sage-group-plc.jpg)