Roger Moser: Thailand 2022

57

The THAILAND Automotive Industry 2022 A Preliminary Report on the Thailand Automotive 2022 Study A collaboration between the ASIA CONNECT Center, University of St.Gallen, the Thai Automotive Focus Group and the Thai-European Business Association. Dr. Roger Moser Director ASIA CONNECT Center University of St.Gallen St.Gallen/Bangkok, 2012 Uli Kaiser President Automotive Focus Group

-

Upload

uli-kaiser -

Category

Automotive

-

view

689 -

download

1

Transcript of Roger Moser: Thailand 2022

The THAILAND Automotive Industry 2022

A Preliminary Report on the Thailand Automotive 2022 Study

A collaboration between the ASIA CONNECT Center, University of St.Gallen, the Thai Automotive

Focus Group and the Thai-European Business Association.

Dr. Roger Moser

Director ASIA CONNECT Center

University of St.Gallen

St.Gallen/Bangkok, 2012

Uli Kaiser

President

Automotive Focus Group

1 Setting the Stage: Why a Thailand Automotive 2022 Study?

2 The Industry Intelligence Approach applied for Thailand 2022

3 Summary and Outlook

STARTING POINT: Local as well as Expat and Western managers in Asian

countries face uncertainty and ambiguity regarding future institutional change.

Uncertainty & Ambiguity as Challenges

The dynamics of institutions in emerging markets can cause frequent

changes in governmental regulations, tax laws, foreign direct investment

(FDI) regulations, business practices, competition, or market conditions,

etc..

Yet, changes in environmental conditions are difficult to identify and

interpret and, subsequently, the complexity of their development and

interrelatedness are difficult to understand for local as well as foreign

senior executives.

Insights on the Future Industry Context to

Improve Strategic Flexibility

In order to successfully deal with the increased

complexity, interdependencies and dynamics that are

inherent in emerging markets’ institutional context,

senior executives require not only an accurate picture

of today’s market situation but also information about

the potential future business environment(s).

PROPOSAL: We have developed an INDUSTRY INTELLIGENCE APPROACH to

better understand potential changes in the industry environment of Asian

markets.

Industry Intelligence Approach

抛砖引玉 / Tossing out a brick to get a jade gem

The Industry Intelligence approach of the ASIA CONNECT Center-HSG can be used to serve local

as well as Expat and Western managers to better understand the dynamic context of their focal

industry. The approach enables decision-makers to reduce uncertainty about impactful future

developments as well as ambiguity about the institutional context based on a structured, practice-

oriented research methodology. The approach also allows to transform insights on potential futures

into functional consequences today.

APPROACH: The INDUSTRY INTELLIGENCE APPROACH builds on quantitative

and qualitative data from a diverse range of local industry experts as well as

onsite discussions (analysis workshops).

Exchanging Viewpoints in (Workshops)

Onsite expert workshops on the campus of business schools or

in collaboration with industry associations allow for even more

detailed insights on the consequences of the evaluated

projections and scenarios for industry stakeholders as well

as the institutional interdependencies in the focal industry.

Looking into the Minds of Local Experts (Online Delphi Study)

First, we evaluate projections about future industry developments or

strategic group behavior with respect to their probability of occurrence as

well as impact on the industry/competitors and evaluate consensus

among the participating industry experts (e.g. online and real-time).

Moreover, participating experts are encouraged to explain the reasons for a

high/low assessment of a projection.

This approach allows for a unique understanding based on the different

perspectives and opinions of a wide range of local industry experts

a unique combination of qualitative and quantitative data!

OVERALL OBJECTIVE OF THE APPROACH : Uncertainty and ambiguity

reduction for senior executives .

UNDERSTANDING YOUR INDUSTRY

ENVIRONMENT

STEP 1: Real-time Delphi

Online study with local industry experts to gather distinct

perspectives on ‘hot topics’ (e.g. PEST, Value Chain, Markets) .

STEP 2: Workshop

to develop scenarios of the future political, socio-cultural, value chain and

infrastructure environment for your focal industry, (e.g. for the year

2022).

Which changes might occur in the

institutional environment? How changes might interrelate and

what does it mean for a firm?

Challenge 1:

Uncertainty

about future institutional developments

Challenge 2:

Ambiguity about

institutional interdependences

INDUSTRY SEGMENT STUDY EXAMPLE from CHINA – There is moderate

consensus and probability that the majority of Chinese car buyers prefer green

power train technologies in 2020.

Probability Low Probability High

…China is too far away to prioritize environment and health

considerations.

…price sensitivity of the end user

…large vehicles will remain more popular

…running costs will compensate the high tag price in the long run.

…be careful what is regarded as green energies…all OEMs will

offer low-energy consumption vehicles.

…pollution and restrictions in urban areas drive this development.

Impact Low Impact High

… all cars will be complying with emission requirements … pushes the industry towards more R&D investments.

Desirability Low Desirability High

…this will drive up costs … continuous improvement of technologies.

Industry Stakeholder Projection: Customers Probability * Impact* Desirability* Consensus**

“Green Focus”: In 2020, more than 90% of China’s car buyers

prefer cars that utilize the most environment-friendly power

train technologies available.

53% 4.1 3.9 20

Likely Very

High High

Moderate

Consensus

* Probability (0-100%); Impact on Chinese automotive industry (low (1) –(5) high); Desirability for Chinese automotive industry (low (1) – (5) high)

* * Consensus (Level of agreement between 80 Delphi study participants measured as Interquartile Distance)

SP1: Private Transportation

SP

2:

“S

tatu

s S

ym

bo

ls”

INDUSTRY SEGMENT STUDY EXAMPLE from China – Distinct

characteristics, implications for the industry's

stakeholders and probability of occurrence.

INDUSTRY SEGMENT STUDY EXAMPLE from China – Understanding the

“institutional dynamics” (reducing ambiguity).

EXTENSION OF THE APPROACH: Identifying future market and value chain

investment behaviors of strategic groups.

Understanding the Future Behavior of

STRATEGIC GROUPS

STEP 1: Real-time Delphi

Online real-time Delphi study with local industry experts to

gather distinct perspectives on ‘hot topics’.

STEP 2: Expert Interviews

to further investigate differences within strategic groups and

differentiate more specifically the interrelations between single

resource investments

Which geographical markets do the

strategic groups focus on?

Where do the strategic groups focus their

investments along the value chain?

Question 1:

Future Geographical

Market Focus

Question 2:

Future Value Chain

Investments

STRATEGIC GROUP STUDY EXAMPLE from China – Dependent & Independent

Chinese OEMs:.

*

* Dependent = e.g. SAIC, FAW;

Independent = e.g. Chery, Geely;

Chinese

Market

Government

Intervention

Projections

35 40 45 50 55 60 65 70

Impact1-5

4.0

3.5

3.0

Probabilityin %

3.8

3.2

3.1

3.9

3.3

3.4

3.6

3.7

Probability vs. Impact

1010 Dep. OEMs produce their brands only in China

11 Chinese OEMs reach 40% market share

22 Indep. OEMs grow stronger than dep. OEMs

33 Consolidation takes place

44 Government support will be reduced

55 Enforcement of IPR1 will improve

66 Dep. OEMs heavily depend on tech. transfer

77 Indep. OEMs are successful innovators

88 Indep. OEMs invest 10% of revenues in R&D

99 10% of indep. OEMs‘ hires are “experienced“

1111 Quality gap of dep. OEMs has been narrowed

1212 Indep. OEMs follow multi-location strategy

1313 Quality gap of indep. OEMs has been narrowed

1414 Dep. OEMs will double marketing spending

1515 3 indep. OEMs among most valuable brands

1616 Indep. OEMs will double marketing spending

1717 Dep. OEMs sell 98% of own brands in China

1818 3 indep. OEMs sell 5% of cars in dev. markets

1919 Indep. OEMs positioned as budget brands in EU

2020 Indep. OEMs invest heavily in local suppliers

2121 Sourcing engineering services will be critical

VC

Evo

lutio

n

R&D

Pro-

duc-

tion

Mar-

ke-

ting

Dis-

tribu-

tion

Sour-

cing

1010

11

22

334455

66

7788 99

1111

1212

1313

14141515

1616

1717

1818

1919

2020

2121

Value Chain Evolution – Marketing/Branding

1414In 2020, dependent Chinese OEMs will have at least doubled the marketing spending for their own brands,

compared to the level in 2011.

Key Insights Results (Statistical Group)

Probability (Detailed)

• During the past few years, the Chinese government has

been pushing dependent Chinese OEMs to develop

their own brands, independent of the activities with their

JV partners

• So far the success of these initiatives has been

limited, with notable first achievements only by SAIC and

FAW

• One of the reasons for the slow development of own

brands is the limited focus on marketing

• Dependent Chinese OEMs have simply given much more

attention to the development of technological

capabilities than to the development of marketing and

branding know-how

• There is moderate consensus among the panel that this

situation is going to change. The experts rate the

probability that dependent Chinese OEMs will at least

double the marketing spending for their own brands within

the next decade as 68%

• 2 out of 3 respondents actually estimate the probability

above 60%

Probability

in %

Con-

sensus Impact

Desi-

rability

6868 2020 3,63,6 3,73,7

9

59

1913

00

10

20

30

40

50

60

0-20 41-6021-40

Share of expert panelin %

61-80 81-100

Probability, in %

Likely High HighModerate

Consensus

STRATEGIC GROUP STUDY EXAMPLE from China: Dependent OEMs likely to

increase the marketing spending for their own brands significantly.

1 Setting the Stage: Why a Thailand Automotive 2022 Study?

2 The Industry Intelligence Approach applied

3 Summary and Outlook

Definition of

relevant projections

Reconsideration of initial

assessment

Initial assessment of

projections

Online Delphi Study with experts for Thailand’s automotive industry

• Development of

projections for Thailand’s

2022 vision based on

extensive desktop

research and interviews

with industry experts

• Finalization of

projections in major

categories:

PEST

Markets

Value chain

evolution

• Industry experts assess

projections on Delphi

online platform

• Every expert gives

quantitative estimates

for each projections with

regard to

Probability

• In addition experts can

add qualitative

arguments for their

probability ratings

• After the first round,

each expert is able to

see assessment and

arguments of the other

participants

• Experts are able to

reconsider their own

assessment based on

the reasoning of the rest

of the group

• Iterative process until

each participant has

reached his final

assessment

THAILAND 2022: Development of projections for Thailand’s automotive industry

and their assessment through online survey with local industry experts.

THAILAND 2022 – STEP 1: Conducting an online study with local industry

experts.

Online Delphi platform

Probability

Degree of

Consensus

• Measured using the

interquartile range (IQR)

• The IQR is the measure of

dispersion for the median and

consists of the middle 50% of

the observations

Terminology

• Measures the expected

probability of each projection

to come true

• Metric scale (0-100%)

THAILAND 2022: Research Frame Overview

THAILAND 2022: Research Frame Overview

Politics: There is strong consensus for a 50/50 probability that the Thai

government will have given up local standards and implemented international

UNECE-based standards in 2022.

Probability Low Probability High

…It depends on OEM’s whether they are ready or not, not only on

the government policy.

…The Thai automotive industry will not be able to meet the

requirements of the international UNECE-based standards in

terms of quality.

…Thai government basically follows OEM's intention and

investment plans, whereby if Thailand becomes more export

oriented, it must implement international standards within 10

years.

…All car makers in key part suppliers are strongly pushing.

Projection for political environment Probability * Consensus**

“UNECE-based standards”: In 2022, the Thai government has given up local

standards and implemented international UNECE-based standards.

53% 10

Likely Strong Consensus

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

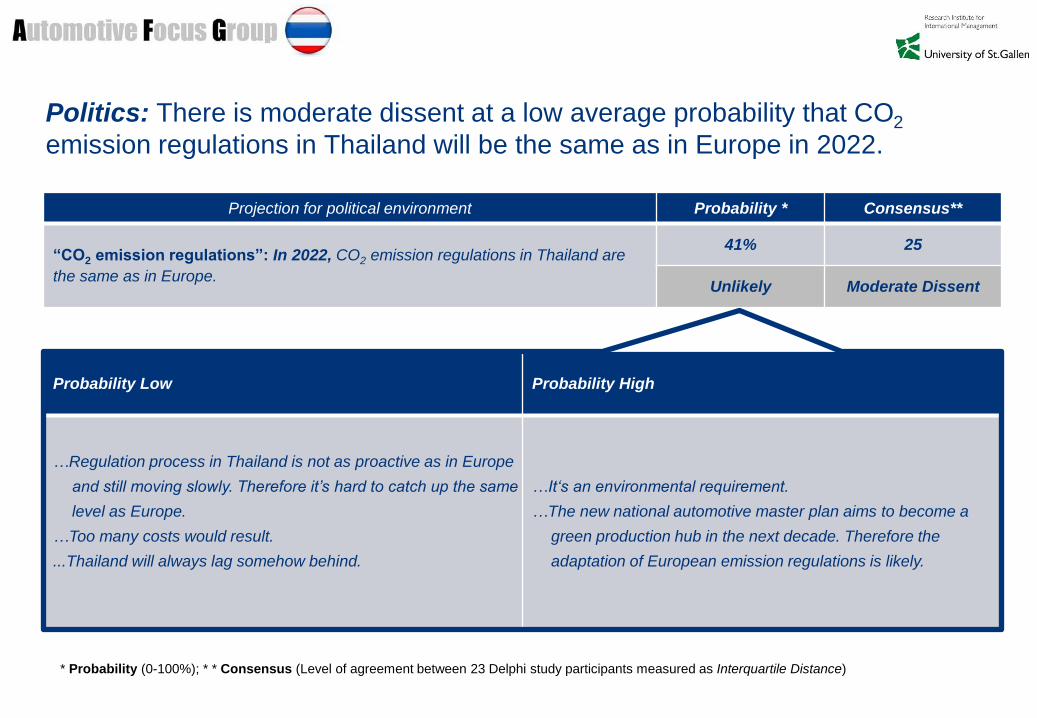

Politics: There is moderate dissent at a low average probability that CO2

emission regulations in Thailand will be the same as in Europe in 2022.

Probability Low Probability High

…Regulation process in Thailand is not as proactive as in Europe

and still moving slowly. Therefore it’s hard to catch up the same

level as Europe.

…Too many costs would result.

...Thailand will always lag somehow behind.

…It‘s an environmental requirement.

…The new national automotive master plan aims to become a

green production hub in the next decade. Therefore the

adaptation of European emission regulations is likely.

Projection for political environment Probability * Consensus**

“CO2 emission regulations”: In 2022, CO2 emission regulations in Thailand are

the same as in Europe.

41% 25

Unlikely Moderate Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Politics: There is moderate dissent at a relatively high probability that Free

Trade Agreements will be in place between Thailand / AEC and Europe / EC in

2022.

Probability Low Probability High

...No one can answer this question.

…Pressure from Europe and at the same time benefits for

Thailand.

…in capitalistic perspective, it will be a MUST happening case but

not fully in 2022. It needs to be more effective for ASEAN first.

…Thailand’s government and private sector are aiming to settle a

FTA Thai-EU in quick if EU will keep sensitive list to work in

second stage FTA.

Projection for political environment Probability * Consensus**

“Free trade Agreements”: In 2022, Free Trade Agreements are in place between

Thailand / AEC and Europe / EC.

58% 25

Likely Moderate Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Supplier: There is strong dissent at a high average probability

that local manufacturers will supply more than 85% of the parts used in local

assemblies of OEM’s for passenger cars in 2022.

Probability Low Probability High

…ASEAN has allowed for free trade in between all member

countries; localization in Thailand will not be driven by

government incentives but by scale effects and TOCO

considerations of the OEM when sourcing.

…Free trade will be facilitated through the introduction of AEC. As

a result Thailand will as well import some auto parts instead of

producing most of them.

…Increasing foreign demand for auto parts and components from

Thailand will strengthen the local industry.

…There is already a trend to have more local supply for significant

components.

Projection for (economic) value chain environment / Supplier: Probability * Consensus**

“Local value creation”: In 2022, local manufacturers supply more than 85% of the

parts used in local assemblies of OEM’s for passenger cars.

63% 30

Very Likely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Supplier: There is strong dissent at a 50/50 probability whether

all major global automotive suppliers will have set up production plants in

Thailand in 2022.

Probability Low Probability High

…Many alternatives. Why cluster in Thailand? Costs rising. Labor

short. Engineering schools sub-par.

…related to FTA effectiveness, but most will rely on India and

export to Thailand.

...Automotive Know How will be concentrated in Thailand and will

play a major factor for automotive OEMs in location decisions;

however, this does not necessarily mean that TIER1/2 will have

plants only in Thailand and not in other ASEAN countries. Other

strategies come into play here.

Projection for (economic) value chain environment / Supplier: Probability * Consensus**

“Global automotive suppliers”: In 2022, all major global automotive suppliers

have set up production plants in Thailand.

53% 30

Likely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / R&D: There is strong dissent at a low average probability that

Thailand will be the only relevant R&D hub in South-East Asia in 2022.

Probability Low Probability High

…Only if Singapore, Malaysia and Indonesia disappear from the

map.

…Japan will still be strong in R&D.

…still difficult to have good solid R&D center in SE Asia, more in

India and China, then SEA is used for production.

…Malaysia has the same industrial attitude as Thailand.

…It should have developed by then.

…Investors will chose Thailand as R&D center because of it's

relatively cheap but well educated engineers.

Projection for (economic) value chain environment / R&D: Probability * Consensus**

“Automotive R&D hub”: In 2022, the only relevant automotive R&D hub in South-

East Asia is Thailand.

41% 30

Unlikely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between X Delphi study participants measured as Interquartile Distance)

Value Chain / R&D: There is strong consensus at a low probability that all

major international Tier 1 suppliers have serious R&D facilities in Thailand in

2022.

Probability Low Probability High

…What would the rationale be? Application engineering yes, but

not R&D. Also, look at how Thai universities rate in the global

context; maybe one in the top 200.

…In India and China, not much in Thailand.

…This will be the last bastion to fall. Although Thailand will lead

automotive R&D in the region, many Tier 1 suppliers will keep

their R&D in their own countries - close to the OEM R&D.

…They will need to have a base in Thailand.

…With the introduction of the AEC high skilled labour can migrate

to Thailand and compensate the shortfall.

Projection for (economic) value chain environment / R&D: Probability * Consensus**

“Serious R&D facilities”: In 2022, all major international Tier 1 suppliers have

serious R&D facilities in Thailand.

44% 10

Unlikely Strong Consensus

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Sourcing: There is strong dissent at a relatively high probability

whether Japanese suppliers in OEM’s and car parts in Thailand have a market

share less than 65% in 2022.

Probability Low Probability High

…Hard to be possible when Japanese is fully dominated and able

to control this market. Other change ranger such as US and

European car makers are very much far behind.

…Cannot see the major investment Japan has diminishing.

…More mix with Korean, Chinese and others. More strong

suppliers develop similar level of quality to support non-

Japanese OEM as well, which helps good bland in market.

…It is possibility that more Europe brands will set production

bases in Thailand to survive in the buying power shift of the

world.

…Suppliers will avoid cluster risk.

…VW, Ford and GM will increase presence.

Projection for (economic) value chain environment / Sourcing: Probability * Consensus**

“Japanese suppliers market share”: In 2022, the market share of Japanese

suppliers in OEM’s and car parts in Thailand is less than 65%.

56% 35

Likely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Sourcing: There is strong dissent at a 50/50 probability whether

the quality of suppliers in Thailand is comparable to those in EU and Japan in

2022.

Probability Low Probability High

…This is related to people's mentality. Thai need more flexibility of

quality in terms of delivery and time R&D management, which

will be still critical.

…Culturally based, the tendency for compromises, not clearly

addressing and not sustainably solving issues as well as not

executing consistency in management practices is relatively

higher pronounced than in European countries and will hinder

the overall quality level.

…Most multi nationals will be present in Thailand.

…Most of mechanical parts will be very competitive except for

electronically part where part makers in Thailand still have no

competitive technology.

…Already Thai production quality is nearly the same as in Japan.

…It must to meet market demand.

Projection for (economic) value chain environment / Sourcing: Probability * Consensus**

“Quality of suppliers ”: In 2022, the quality of suppliers in Thailand is comparable

to those in EU and Japan.

54% 30

Likely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Production: There is strong dissent at very high average

probability that Thailand is the largest automotive production base in South-East

Asia in 2022.

Probability Low Probability High

...Indonesia will overtake Thailand.

…As a consequence of the Thai flood crisis several companies

are diversifying their operations to other countries and thereby

weaken Thailand’s current leader position.

…Diversification will take place, low cost cars will be produced in

Indonesia, while higher priced cars will be produced in Thailand

and Thailand will emerge as the clear winner.

…Auto infrastructure needs some time to establish, in Thailand it

is already built up.

…Automotive OEMs need component parts, and Thailand is the

biggest parts production cluster, new OEMs will move in and

then bring more part suppliers.

Projection for (economic) value chain environment / Production: Probability * Consensus**

“Largest automotive production base”: In 2022, Thailand is the largest

automotive production base in South-East Asia.

69% 38

Likely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Production: There is strong dissent at a 50/50 probability that

the total car production volume in Thailand is more than 5 million units per year

in 2022.

Probability Low Probability High

…If the world economic do not return back to normal within 5

years we might be unable to achieve that number.

…OEM’s have choice of production site in other countries always,

and speed of increase is not that high in my smell.

…Thailand has high costs compared to Indonesia.

…Thailand will export more vehicles.

…Most of Japanese car makers are under process to transfer

capacity from Japan to Thailand and Indonesia.It will make

Thailand become major exporting hub of Japanese.

…An adjusted gi = annual growth rate (2013 to 2022) = 0.03, 0.1,

0.09, 0.07, 0.05, 0.03, .01, 0.2, 0.1, 0.1 (with 2 economic

downturns) could bring the 2022 volume up to 5 Mio.

Projection for (economic) value chain environment / Production: Probability * Consensus**

“5 million units production”: In 2022, the total car production volume in Thailand

is more than 5 million units per year.

46% 30%

Unlikely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Production: There is strong dissent at a 50/50 probability that

labour costs in the automotive industry are lower in Thailand than in China in

2022.

Probability Low Probability High

…China is a big country which doesn't use all of it’s labor yet, but

Thailand is going to reach the maximum level of labor use

already.

…Thailand does everything to impede migration of labor from

neighboring countries while at the same time forcing increases

in labor cost.

…Costs are continuing to increase in Thailand, inflation will hinder

the industry.

…They are lower now and costs in China will rise stronger than

Thai cost.

…Labor cost in China is increasing rapidly due to high inflation

and fast growth in the automotive industry. It will pass Thailand

very soon.

…Could come down from AEC.

Projection for (economic) value chain environment / Production: Probability * Consensus**

“Labour costs”: In 2022, labour costs in the automotive industry are lower in

Thailand than in China.

50% 36

Likely / Unlikely Strong dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Production: There is strong dissent at a 50/50 probability that

car and component production in Thailand is mostly automated in 2022.

Probability Low Probability High

…Not much of a pay-back. If investment in automation is required,

other countries like Malaysia with better skill base will be more

attractive.

…More customers are adding robots today.

…Already some level of automation has been successful in

Thailand. In process, it will be more automated but not as

significant as you would imagine.

…Automation will increase, but not to that extent.

...Labour shortage will drive automation.

…Cost of labor will drive this.

…It's already mostly automated.

Projection for (economic) value chain environment / Production: Probability * Consensus**

“Automated production”: In 2022, car and component production is mostly

automated.

52% 35

Likely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Marketing: There is VERY strong dissent at relatively high

probability that the most important marketing channel for the automotive industry

in Thailand in 2022 is Social Media.

Probability Low Probability High

...Social media is just a hype and not a long term trend.

…There will always be a need for the conventional.

…Social Media is growing up its importance, but it might not reach

Thai rural area and not cover to all ones who have power of

buying cars.

…Communication is becoming more and more digitalized.

Therefore social media is highly relevant in the future.

…Some influence but more from actual hearing from peers.

…As everywhere in the world – unfortunately.

Projection for (economic) value chain environment / Marketing: Probability * Consensus**

“Social Media”: In 2022, the most important marketing channel for the automotive

industry in Thailand is Social Media.

56% 51

Likely Strong dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Marketing: There is moderate consensus at 50/50 probability

that Thailand’s motor shows in 2022 are as significant for global automotive

OEM’s as the shows in Europe, US and Japan.

Probability Low Probability High

…Two current shows need to merge into one to be able to hold

the most relevant show in 2022 as Jakarta will be catching up

very fast.

…Thailand‘s relevance in the automotive industry is as a sourcing

and production market rather an end-consumer market.

Therefore its motor shows will not become globally relevant.

…In Thailand all is related to R&D and trend impact rather than

selling shows.

…Thailand as the automotive hub in ASEAN provides access to a

market of about 600 Million people. Therefore Thai motor

shows gain relevance.

Projection for (economic) value chain environment / Marketing: Probability * Consensus**

“Motor Shows”: In 2022, Thailand’s motor shows are as significant for global

automotive OEM’s as the shows in Europe, US and Japan.

46% 15

Unlikely Moderate

Consensus

* Probability (0-100%); * * Consensus (Level of agreement between X Delphi study participants measured as Interquartile Distance)

Value Chain / Distribution: There is strong dissent at a 50/50 probability that

75% of all vehicles manufactured in Thailand are exported in 2022.

Probability Low Probability High

…Investors will derisk and hedge export bases.

…May be 50%.

…There will be growth of the local market as more eco cars are

produced here.

…The realization of the DAWEI deep seaport project reduces

logistic cost for exporting Thai made vehicles and therefore

boosts Thai automotive exports.

…The realization of the DAWEI deep seaport project reduces

logistic cost for exporting Thai made vehicles and therefore

boosts Thai automotive exports.

…That is the direction that I can see considering investment and

market domestic demand.

Projection for (economic) value chain environment / Distribution: Probability * Consensus**

“Export ratio”: In 2022, 75% of all vehicles manufactured in Thailand are exported.

54% 30

Likely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Consumers: There is strong dissent at a 50/50 probability that

car density in Thailand is 200 cars per 1000 people in 2022.

Probability Low Probability High

... Macroeconomics don't support this number. Plus infrastructure

will collapse at that level.

…Too many cars to imagine, no infrastructure to support.

…Only in BKK area, others still primitive.

…It's already at >160.

…Average personal income will grow accordingly.

…More developed road infrastructure will lead to higher car

density.

Projection for (economic) value chain environment / Consumers: Probability * Consensus**

“Car density”: In 2022, car density in Thailand is 200 cars per 1000 people.

47% 35

Unlikely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Consumers: There is moderate consensus at a very low

probability that the motorcycle has replaced small cars for personal transport

and is only be used for recreational transport in 2022.

Probability Low Probability High

…Motor cycles will remain a flexible low cost means of

transportation. The importance of low cost cars however has

increased.

…Still act as one of major transporting method, all related to city

development and rail / road infrastructure but there is not much

improvement in last 10 years.

…Small cars flopped even in India.

... Motor cycles will be used in rural areas.

…As cars get cheaper and salaries go up this will happen. It has

already happened to a significant extent.

…GDP in Thailand grows fast and therefore gives people more

purchasing power. If affordable Thai people will always prefer a

car over a motorbike.

Projection for (economic) value chain environment / Consumers: Probability * Consensus**

“Motorbikes for recreational transport”: In 2022, the motorcycle has been

replaced by small cars for personal transport and is only used for recreational

transport.

28% 20

Unlikely Moderate

Consensus

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Consumers: There is moderate dissent at a rather high

probability that public transportation is the only efficient mode of transportation

throughout the metropolis in 2022.

Probability Low Probability High

…Thai likes to drive and private feeling among friends.

…Since cars will remain a very important status symbol in

Thailand, public transportation will never be the most preferred

means of transportation.

…It already is.

…If emphasis is on "efficient" then yes, all other means of

transportation will not be providing adequate ratios of

1) Resources per person per kilometer

2) Time per person per kilometer

…The transport system will be improved.

…It is already.

Projection for (economic) value chain environment / Consumers: Probability * Consensus**

“Public transportation”: In 2022, public transportation is the only efficient mode of

transportation throughout the metropolis.

58% 25

Likely Moderate Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Value Chain / Consumers: There is strong dissent at a very low probability that

Bangkok has introduced car-sharing (i.e. fractional car ownership / pay per use

vehicles) throughout the metropolis in 2022.

Probability Low Probability High

…Sharing a meal: yes. Sharing cars, no.

…People want ownership

…It’s too risky for cars being stolen and deceit.

…Additional rise in traffic volume will bock the metropolis seriously

and make parking space really expensive. Therefore people will

consider car-sharing as a convenient alternative.

…Low vehicle-ownership rates due to low incomes will boost car-

sharing in Bangkok.

Projection for (economic) value chain environment / Consumers: Probability * Consensus**

“Car-sharing”: In 2022, Bangkok has introduced car-sharing (i.e. fractional car

ownership / pay per use vehicles) throughout the metropolis.

27% 30

Unlikely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Society: There is VERY strong dissent at a 50/50 probability that there is an

annual demand for one million low-emission vehicles per year in Thailand in

2022.

Probability Low Probability High

…no incentives (government driven) in sight and unlikely to be

done unless government becomes more focused on the issue

and implements real policies rather than face saving, false

compromises.

…Thai people will not relief on low-emission yet but price only.

…cost of technology are too high.

... In terms of capacity, there is obligation for OEM to produce in

given years, but mainly it will be used for export base.

…Thailand has a new green Automotive Master Plan.

…there might be a chance when the Thai government sees

possibilities to gain profit from it by implementing charges on

car manufacturers which doesn’t provide low-emission vehicles.

…Thailand has strong views on the environment.

…trends will change due to pressure from ASEAN for low

emission vehicles and overall pollution reductions.

Society Projection Probability * Consensus**

“Demand for low emission vehicles”: In 2022, there is an annual demand for one

million low-emission vehicles per year in Thailand.

50% 45

Unlikely Strong dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Society: There is very strong dissent at a 50/50 probability that total cost of

ownership of a car is the most important factor for a purchase decision of an

average Thai car buyer in 2022.

Probability Low Probability High

…Status of "owning a car" is more important than TOCO; this is

embedded in the national culture and requires significant

external triggers to start shifting towards a more cost oriented

view (e.g. fuel prices increase ten fold, taxes etc.)

…One of the most important, yes, but the most important, no.

Practicality for intended purpose (e.g. truck)and overall appeal

(e.g. design)are likely to supersede cost of ownership.

…Thailand will have more disposable income by 2022

…Total cost will be key criteria for purchasing intention when most

of people are the mid income and debt will be national issue to

control.

…Small car segment is growing and these buyers are more

budget conscious.

…Another big financial crisis which forces Thais to reduce their

cost and save for the future.

…Thai\'s hire purchase and image is important so cost still

important but other factors too.

Projection for social environment: Probability * Consensus**

“TCOO for purchase decision”: In 2022, total cost of ownership of a car is the

most important factor for a purchase decision of an average Thai car buyer.

51% 41

Likely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Society: There is VERY strong dissent at a low probability that 100% Biodiesel

is the most popular fuel in the rural areas of Thailand in 2022.

Probability Low Probability High

…Hard to be possible when palm oil shall supply to food sector

too.

…Not in the next 10 years. The government has given so much

program to promote investors to come based on usual fuel,

adapting Biodiesel requires additional structure change for

OEM, which is being studied but not in next 10 years.

…It is a profit maximizing question. Therefore the government

plays an important role in this question.

...When the price of the world diesel oil is too high, people in rural

area will do save their cost by using more Biodiesel.

…Thailand can produce Biodiesel locally.

…Biodiesel is economical and environmentally friendly.

Projection for social environment: Probability * Consensus**

“Biodiesel”: In 2022, 100% Biodiesel is the most popular fuel in the rural areas of

Thailand.

38% 50

Unlikely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Technology: There is VERY strong dissent and at a relatively high probability

that roads are the only relevant mass transportation infrastructure in Thailand in

2022.

Probability Low Probability High

…True for upcountry while Bangkok will see a significant improve

in mass transportation in order to prevent a total collapse of the

infrastructure.

…Thailand will have a developed high speed train system by then

because the government planes to spend more than 1 trillion

THB to develop rail infrastructure.

…Thai government provides more and better infrastructure on

rails since the traffic on the roads will increase dramatically and

is not controllable anymore.

…Inaptitude to manage large mass-transport projects.

…Thailand seems to lack vision and will to develop a

comprehensive rail network for example.

…Yes, still if you say only in next 10 years, however, in the longer

term Rail transport and Vessel transport will be examined

effectively.

…Though many new sky train lines will have been finished before

2022 but that for Bangkok Metropolitan, Thailand is not merely

Bangkok.

Projection for (soft/hard technological) infrastructure environment: Probability * Consensus**

“Roads for mass transportation”: In 2022, roads are the only relevant mass

transportation infrastructure in Thailand.

56% 50

Likely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

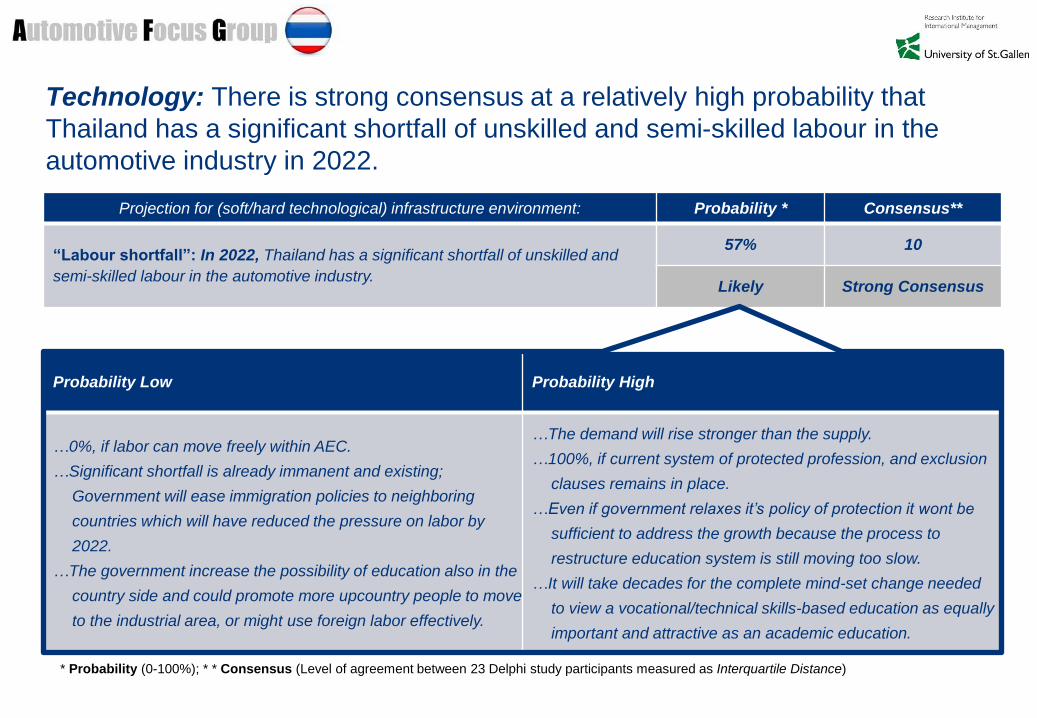

Technology: There is strong consensus at a relatively high probability that

Thailand has a significant shortfall of unskilled and semi-skilled labour in the

automotive industry in 2022.

Probability Low Probability High

…0%, if labor can move freely within AEC.

…Significant shortfall is already immanent and existing;

Government will ease immigration policies to neighboring

countries which will have reduced the pressure on labor by

2022.

…The government increase the possibility of education also in the

country side and could promote more upcountry people to move

to the industrial area, or might use foreign labor effectively.

…The demand will rise stronger than the supply.

…100%, if current system of protected profession, and exclusion

clauses remains in place.

…Even if government relaxes it’s policy of protection it wont be

sufficient to address the growth because the process to

restructure education system is still moving too slow.

…It will take decades for the complete mind-set change needed

to view a vocational/technical skills-based education as equally

important and attractive as an academic education.

Projection for (soft/hard technological) infrastructure environment: Probability * Consensus**

“Labour shortfall”: In 2022, Thailand has a significant shortfall of unskilled and

semi-skilled labour in the automotive industry.

57% 10

Likely Strong Consensus

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Technology: There is strong dissent at 50/50 probability that most high skilled

automotive engineers from ASEAN area are working in Thailand in 2022.

Probability Low Probability High

…Thailand has faced a “brain drain” in recent years, with its skilled

students and workers migrating in search of better opportunities

and pay.

…Indo and others are not far behind.

…Indonesia is catching up, with macroeconomics and

demographics in their favor.

…Thailand is the center of SE Asia and have the biggest

automotive parts production cluster in the region with a good rate

of growing up.

…Especially, Chinese and Indian will be present with experienced

skills to fulfill the gap since skilled Thai workers will be still short.

…Thailand will maintain it's status as Automotive hub.

……Competition with neighboring countries such as Indonesia and

Malaysia is significant. However, Thailand will come up as the

manufacturing hub for ASEAN.

Projection for (soft/hard technological) infrastructure environment: Probability * Consensus**

“ASEAN’s engineers in Thailand”: In 2022, most high skilled automotive

engineers from ASEAN area are working in Thailand.

53% 36

Likely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

THAILAND 2022: Research Frame Overview

Malaysia: There is moderate consensus at a low probability that Malaysia has

found a JV Partner for Proton and has become a serious player with more than

1’000’000 vehicles produced per year and 30% export ratio in 2022.

Probability Low Probability High

…Quality and design is still not that shiny, additionally they have

their own management problem.

…So many engagements, but never a wedding.

…Proton will vanish.

…Proton always has difficulty on improving technology in order to

match the world standard.

…Unlikely. Many have looked, but few have continued with Proton.

…Local value creation requirements in Malaysia boost its exports.

…Chines brands will enter the Malaysian market and therefore

help the industry growing.

…Looks like Honda is the enabler, if one can trust the newspaper

reports.

Projection for ASEAN environment: Probability * Consensus**

“Malaysia”: In 2022, Malaysia has found a JV Partner for Proton and becomes a

serious player with more than 1’000’000 vehicles produced per year and 30% export

ratio.

42% 20

Unlikely Moderate

Consensus

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Indonesia: There is moderate consensus at a low probability that Indonesia has

increased its automotive export to 50% and has overtaken Thailand as the

leading automotive production hub in South-East Asia in 2022.

Probability Low Probability High

…Indonesia supports mainly domestic demand.

…Indonesia cannot build up a component parts cluster within 10

years and labour cost are the same as in Thailand.

…Indonesia is politically too unstable.

…It is depending on car makers policy from which base they

export, but from Japanese point of view Thailand will be main

exporting base because Thailand’s supply chain is more

competitive.

…Macroeconomics and demographics favour Indonesia.

…Many companies will continue to invest in Indonesia and by this

help bringing it to the top in South-East Asia.

Projection for ASEAN environment: Probability * Consensus**

“Indonesia”: In 2022, Indonesia has increased their automotive export to 50% and

has overtaken Thailand as the leading automotive production hub in South-East

Asia.

41% 20

Unlikely Moderate

Consensus

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

Myanmar: There is strong dissent at a low probability that Myanmar has an

automotive industry with more than 1’000’000 car capacity per annum strongly

dominated by Chinese manufacturers in 2022.

Probability Low Probability High

... Automotive industry will be set up in Myanmar but development

in all aspects need more than 10 years.

…Maybe 500’000 but not dominated by Chinese.

…Myanmar needs more time to develop the infrastructure.

…Hard for such fast capacity building unless the market grows

significantly.

…Myanmar is still far from being en enticing market for industrial

investment. In order to get to that scale, projects would have to

be starting now.

…China is developing Myanmar as logistics gateway and

production will follow.

.. Yes, some chance and Chinese will be major player followed by

Japanese.

Projection for ASEAN environment: Probability * Consensus**

“Chinese Domination in Myanmar”: In 2022, Myanmar has an automotive

industry with more than 1’000’000 car capacity per annum strongly dominated by

Chinese manufacturers.

38% 40

Unlikely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

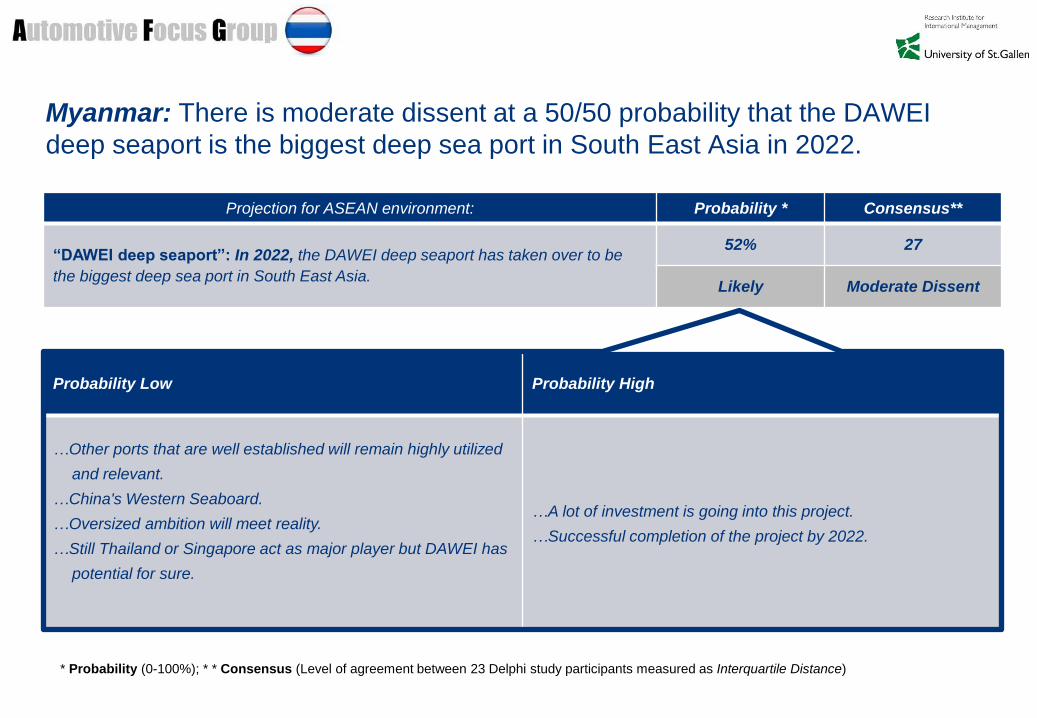

Myanmar: There is moderate dissent at a 50/50 probability that the DAWEI

deep seaport is the biggest deep sea port in South East Asia in 2022.

Probability Low Probability High

…Other ports that are well established will remain highly utilized

and relevant.

…China's Western Seaboard.

…Oversized ambition will meet reality.

…Still Thailand or Singapore act as major player but DAWEI has

potential for sure.

…A lot of investment is going into this project.

…Successful completion of the project by 2022.

Projection for ASEAN environment: Probability * Consensus**

“DAWEI deep seaport”: In 2022, the DAWEI deep seaport has taken over to be

the biggest deep sea port in South East Asia.

52% 27

Likely Moderate Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

THAILAND 2022: Research Frame Overview

China: There is moderate dissent at low probability that Thai automotive exports

to China account for 30 per cent of the Thai automotive exports to global

markets in 2022.

Probability Low Probability High

…China will not import but produce domestically.

…Chinese still consider automotive as sensitive list. So they will

block them out.

…China will still have their own OEM’s domestically, no need to

rely on other countries much (except high end).

…Unlikely, as OEM will build in China for local market and in

Thailand for the rest of the world.

…Only Thailand can produce the luxury class cars.

Projection for global environment: Probability * Consensus**

“Exports to China”: In 2022, the Thai automotive exports to China account for 30

per cent of the Thai automotive exports to global markets.

32% 25

Unlikely Moderate Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

China / Japan: There is strong dissent at a rather low probability that China is

the second largest foreign automotive investor in Thailand after Japan in 2022.

Probability Low Probability High

... Myanmar is the target for China.

…Chinese investments will go to Indonesia because it’s a larger

market.

…It’s hard for Chinese car to find acceptance in Thailand or in

ASEAN by culture whereas US cars are still competitive and

more accepted.

…China will increase investment in Thailand but not within next 10

years.

…China will strongly engage in ASEAN.

…Chinese OEM and suppliers need other place like Thailand to

invest in order to support not much Yuan appreciation as well as

duty exemption in importing countries.

Projection for global environment: Probability * Consensus**

“Investments from China and Japan”: In 2022, China is the second largest

foreign automotive investor in Thailand after Japan.

44% 30

Unlikely Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23 Delphi study participants measured as Interquartile Distance)

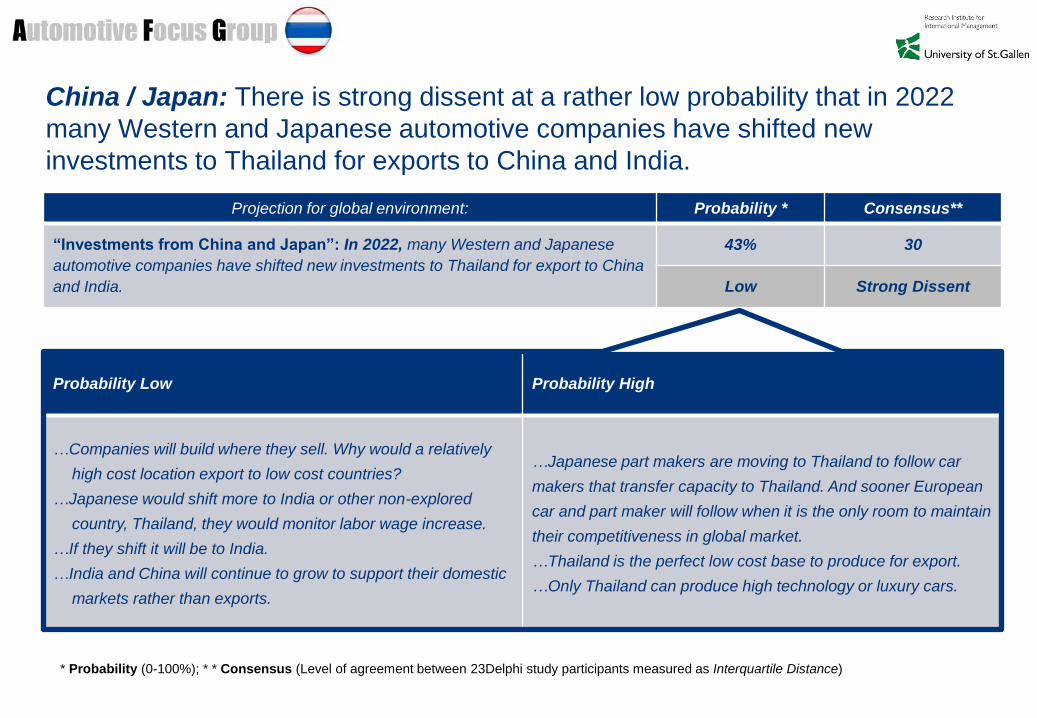

China / Japan: There is strong dissent at a rather low probability that in 2022

many Western and Japanese automotive companies have shifted new

investments to Thailand for exports to China and India.

Probability Low Probability High

…Companies will build where they sell. Why would a relatively

high cost location export to low cost countries?

…Japanese would shift more to India or other non-explored

country, Thailand, they would monitor labor wage increase.

…If they shift it will be to India.

…India and China will continue to grow to support their domestic

markets rather than exports.

…Japanese part makers are moving to Thailand to follow car

makers that transfer capacity to Thailand. And sooner European

car and part maker will follow when it is the only room to maintain

their competitiveness in global market.

…Thailand is the perfect low cost base to produce for export.

…Only Thailand can produce high technology or luxury cars.

Projection for global environment: Probability * Consensus**

“Investments from China and Japan”: In 2022, many Western and Japanese

automotive companies have shifted new investments to Thailand for export to China

and India.

43% 30

Low Strong Dissent

* Probability (0-100%); * * Consensus (Level of agreement between 23Delphi study participants measured as Interquartile Distance)

1 Setting the Stage: Why a Thailand Automotive 2022 Study

2 The Industry Intelligence Approach applied

3 Summary and Outlook

THAILAND 2022 – (Outlook): Conducting a “scenario development” workshop

(reducing uncertainty).

THAILAND 2022 – (Outlook): Turning scenario insights into functional

consequences today through the “Institutions-Resource Matrix” (Example).

Political Value Chain

Socio-cultural Technological Infrastructure

Scenario Development

Probability Impact

Desirability Roadmap

Industry Environment P-S-T

Projection 1 Projection 2

Probability Impact

Desirability

Industry Value Chain

Projection 1 Projection …

Institutional

Dynamics

Effects on Department's Strategic Plans

Organizational(Structures, Processes, Leadership Style etc.)

Technological(IP Rights, Production

Technologies, Tacit Knowledge etc.)

Human(Executives, Employees

etc.)

Physical(Plants, Machinery etc.)

Relationships(within company,

functions, customer or suppliers etc.)

R&D

Procurement

Production

Marketing

Distribution

After Sales

Modification of Local Operations

CONTACT: The ACC-HSG / AFG research team can be contacted to further

discuss your interests and answer your questions.

ASIA CONNECT Center-HSG

Dr. Roger Moser, Director

University of St.Gallen

Dufourstrasse 40a

CH-9000 St.Gallen, Switzerland

Tel: +41 71 224 73 54

E-mail: [email protected]

Web: www.acc.unisg.ch

Paolodal Pozzo Toscanelli, 1457

Automotive Focus Group

Uli Kaiser