5 - 1 © 2005 Accounting 1/e, Terrell/Terrell Recording Accounting Data Chapter 5.

Upload

isabel-parksCategory

view

213download

0

Robert N. West © VEMBA Accounting

Revenue and Monetary Assets

© The McGraw-Hill Companies, Inc., 1999

5Part One: Financial Accounting

Robert N. West © VEMBA Accounting

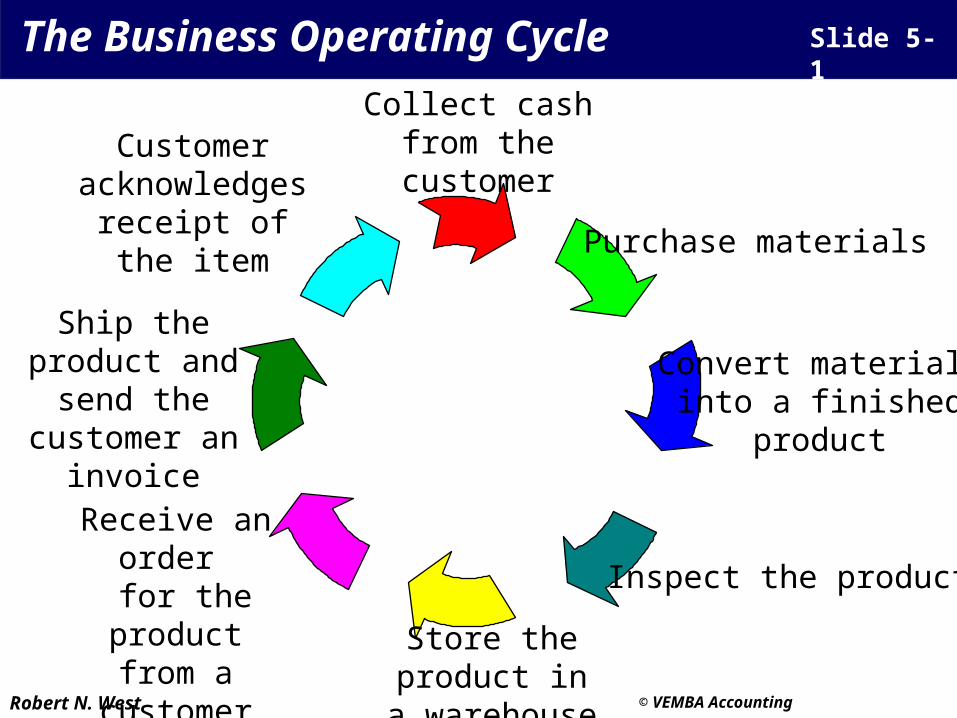

The Business Operating Cycle Slide 5-1

Purchase materials

Convert materialsinto a finished

product

Inspect the productReceive an order for the productfrom a customer

Ship the product and send the customer an

invoice

Customer acknowledges

receipt of the item

Store the product ina warehouse

Collect cash from the customer

Robert N. West © VEMBA Accounting

1. Sales order received no none2. Deposit or advance no nonepayment received3. Goods being produced For certain long- percentage of

term contracts completion4. Production completed; For precious metals productiongoods stored and certain agri-

cultural products5. Goods shipped or usually delivery6. Customer pays account collection is installmentreceivable uncertain

Timing of Revenue Recognition Slide 5-2

Typical

Revenue Recognition Revenue Recognition Event at This Time Method

Robert N. West © VEMBA Accounting

dr. Inventory on consignment 1,000

cr. Merchandise inventory 1,000

Consignment Shipments Slide 5-3

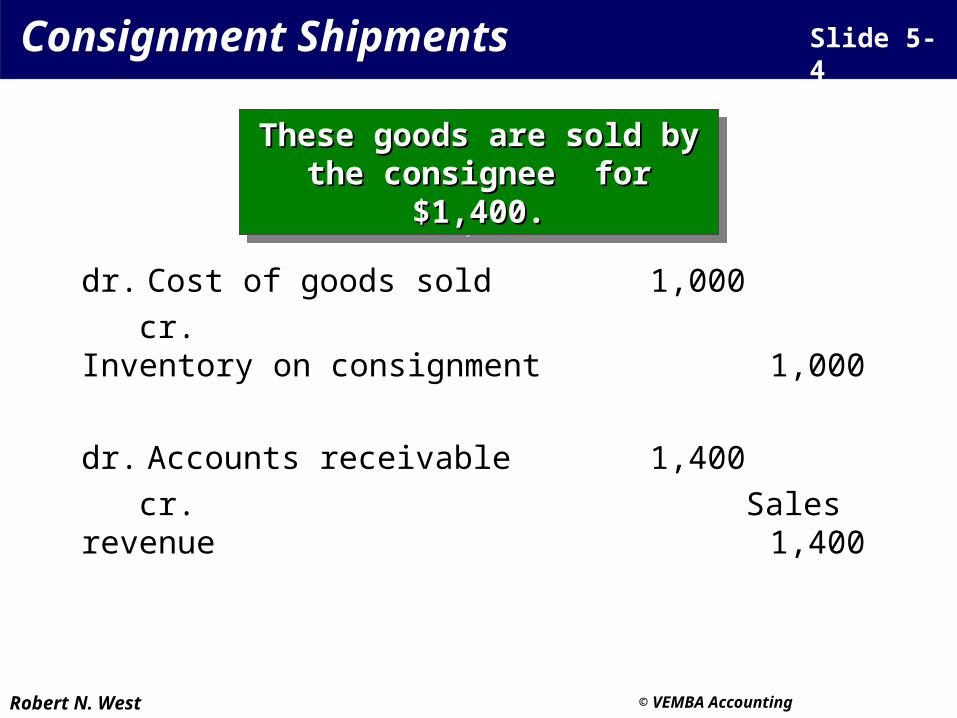

Goods costing $1,000 were Goods costing $1,000 were shipped out on consignment.shipped out on consignment.

Goods costing $1,000 were Goods costing $1,000 were shipped out on consignment.shipped out on consignment.

Robert N. West © VEMBA Accounting

dr. Cost of goods sold 1,000

cr. Inventory on consignment 1,000

dr. Accounts receivable 1,400

cr. Sales revenue 1,400

Consignment Shipments Slide 5-4

These goods are sold by the These goods are sold by the consignee for $1,400.consignee for $1,400.

These goods are sold by the These goods are sold by the consignee for $1,400.consignee for $1,400.

Robert N. West © VEMBA Accounting

Customer Project Year-End Payments Costs Percent Year Received Incurred Complete Revenues Expenses Income

1 $120,000 $160,000 20 $ 0 $ 0 $ 0

2 410,000 400,000 70 0 0 0

3 370,000 240,000 100 900,000 800,000 100,000

Total $900,000 $800,000 $900,000 $800,000 $100,000

Completed-Contract Method Slide 5-5

If the amount of income to be earned on the contract cannot be reliably estimated, then

revenue is to be recognized only when the project has been completed.

If the amount of income to be earned on the contract cannot be reliably estimated, then

revenue is to be recognized only when the project has been completed.

Robert N. West © VEMBA Accounting

1 $120,000 $160,000 20 $180,000 $160,000 $ 20,000

2 410,000 400,000 70 450,000 400,000 50,000

3 370,000 240,000 100 270,000 240,000 30,000

Total $900,000 $800,000 $900,000 $800,000 $100,000

Customer Project Year-End Payments Costs PercentYear Received Incurred Complete Revenues Expenses Income

Percentage-of-Completion Method Slide 5-6

GAAP assumes that the percentage-of-completion method will be used to account for

long-term contracts.

GAAP assumes that the percentage-of-completion method will be used to account for

long-term contracts.

Robert N. West © VEMBA Accounting

Bad Debts Slide 5-7

Check out the aging schedule in

Illustration 5-4.

Check out the aging schedule in

Illustration 5-4.

The firm expectsbad debts of

$7,132 .

The firm expectsbad debts of

$7,132 .

Robert N. West © VEMBA Accounting

The accounts receivable section of the December 31, 1997 balance sheet would appear as follows:

Accounts receivable $262,250 less: allowance for doubtful accounts 7,132 accounts receivable, net $255,118

dr. Bad Debts Expense 7,132

cr. Allowance for Doubtful 7,132

Bad Debts Slide 5-8

The adjusting entry would be:

Robert N. West © VEMBA Accounting

Bad Debts Slide 5-9

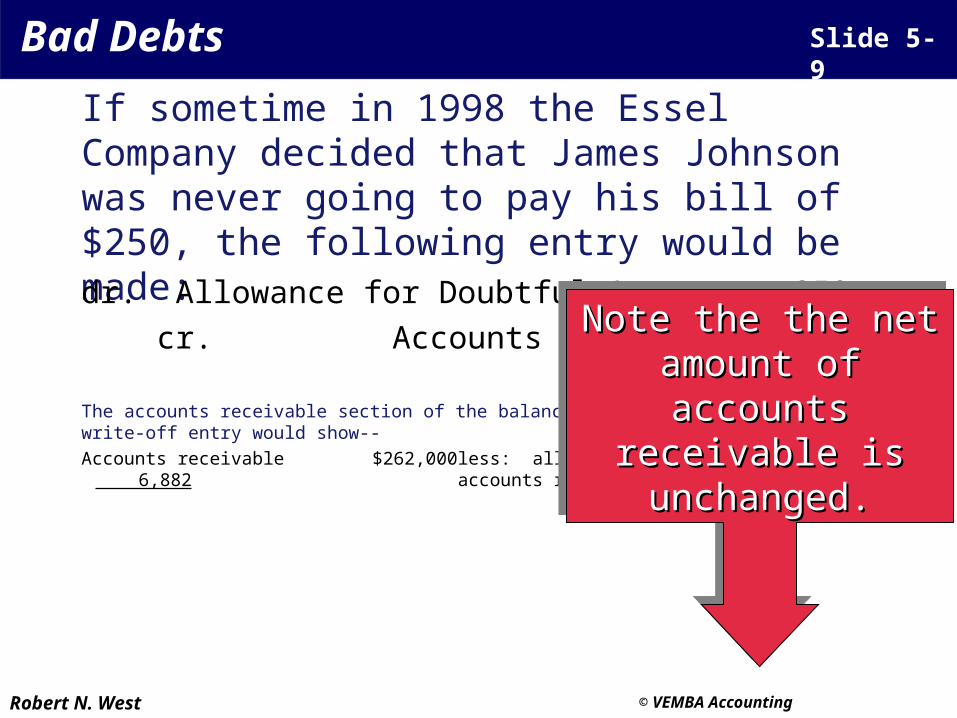

If sometime in 1998 the Essel Company decided that James Johnson was never going to pay his bill of $250, the following entry would be made:dr. Allowance for Doubtful Accounts 250

cr. Accounts Receivable 250

The accounts receivable section of the balance sheet immediately after the write-off entry would show--

Accounts receivable $262,000 less: allowance for doubtful accounts 6,882 accounts receivable, net $255,118

Note the the net Note the the net amount of accountsamount of accounts

receivable is unchanged.receivable is unchanged.

Note the the net Note the the net amount of accountsamount of accounts

receivable is unchanged.receivable is unchanged.

Robert N. West © VEMBA Accounting

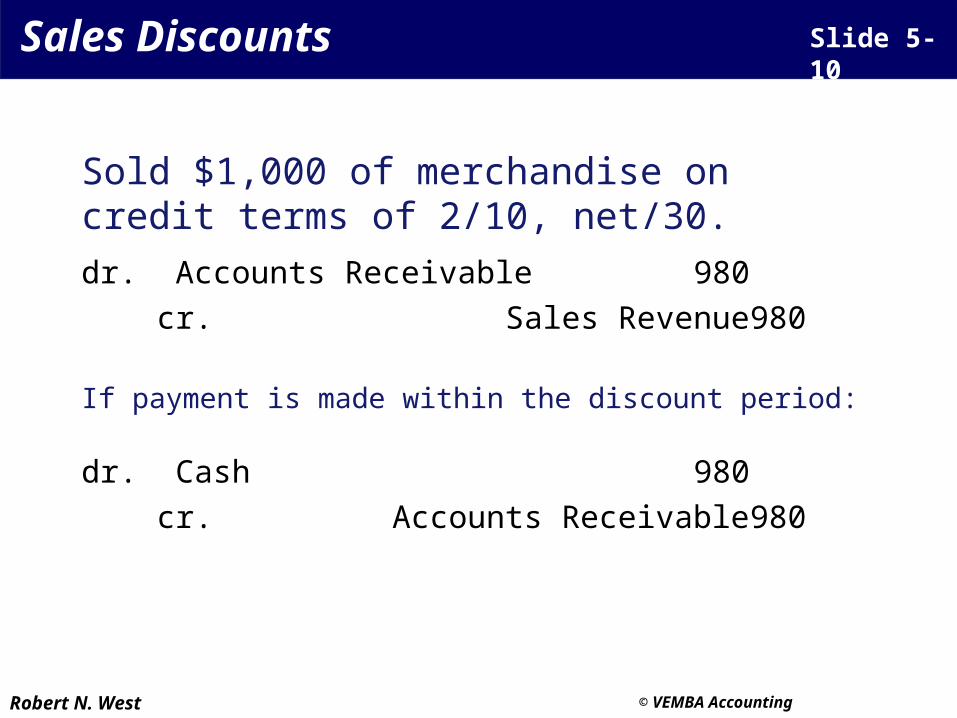

Sales Discounts Slide 5-10

Sold $1,000 of merchandise on credit terms of 2/10, net/30.

Robert N. West © VEMBA Accounting

Sales Discounts Slide 5-10

Sold $1,000 of merchandise on credit terms of 2/10, net/30.

dr. Accounts Receivable 980

cr. Sales Revenue 980

If payment is made within the discount period:

dr. Cash 980

cr. Accounts Receivable 980

Robert N. West © VEMBA Accounting

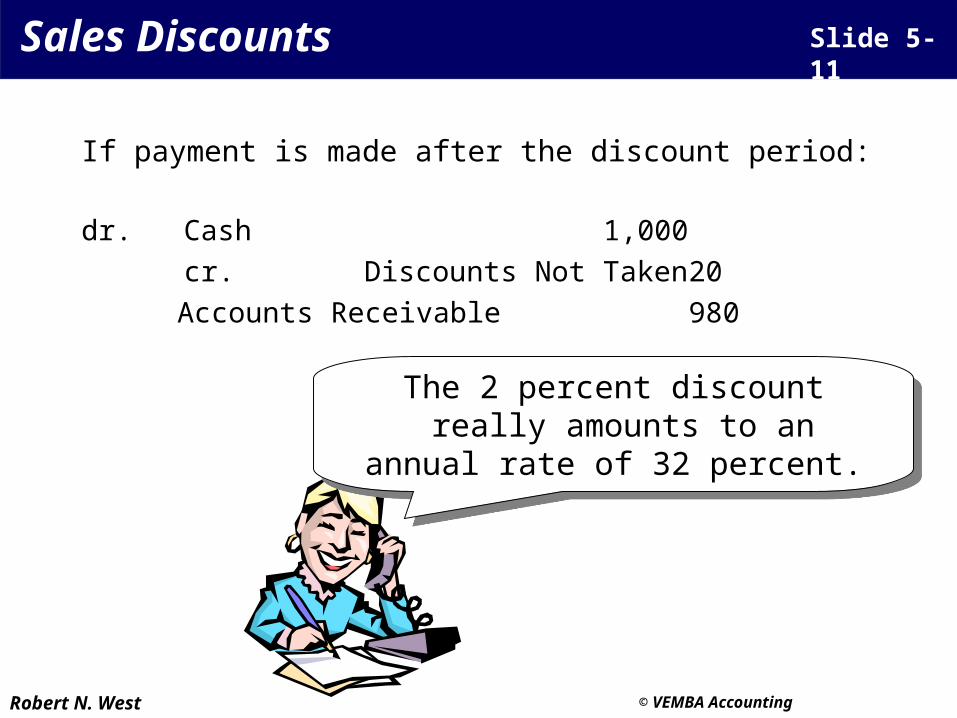

Sales Discounts Slide 5-11

If payment is made after the discount period:

dr. Cash 1,000

cr. Discounts Not Taken 20

Accounts Receivable 980

The 2 percent discount really amounts to an

annual rate of 32 percent.

The 2 percent discount really amounts to an

annual rate of 32 percent.

Robert N. West © VEMBA Accounting

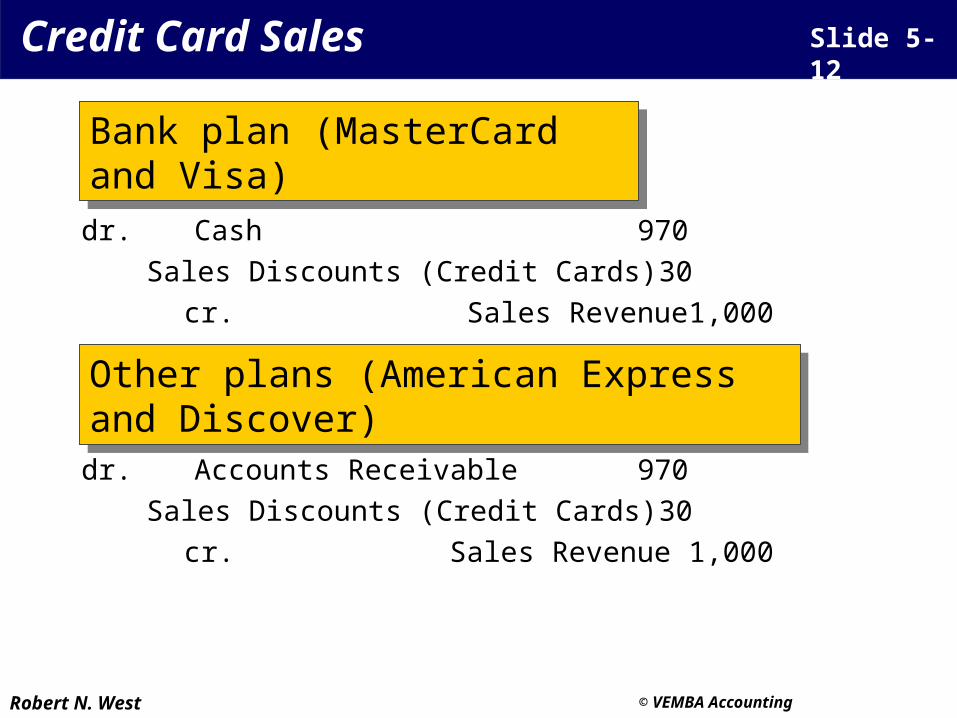

Credit Card Sales Slide 5-12

Bank plan (MasterCard and Visa)Bank plan (MasterCard and Visa)

dr. Cash 970

Sales Discounts (Credit Cards) 30

cr. Sales Revenue 1,000

Other plans (American Express and Discover)Other plans (American Express and Discover)

dr. Accounts Receivable 970

Sales Discounts (Credit Cards) 30

cr. Sales Revenue 1,000

Robert N. West © VEMBA Accounting

Interest Revenue Slide 5-13

On September 1, 1997, a bank loaned $10,000 for one year at 9 percent interest, the interest and principal to be paid on August 31, 1998. The bank’s entry on September 1, 1997 is:dr. Loan Receivable 10,000

cr. Cash 10,000

On December 31, 1997, an adjusting entry is made to record the fact that interest for one-third of a year, $300, was earned in 1997:

dr. Loan Interest Receivable 300

cr. Interest Revenue 300

Robert N. West © VEMBA Accounting

Interest Revenue Slide 5-14

On September 1, 1997, a bank loaned $10,000 for one year at 9 percent discounted.dr. Loan Receivable 10,000

cr. Cash 9,100

Unearned Interest Revenue 900

On December 31, 1997, an adjusting entry is made to record the fact that $300 of interest was earned in 1997.

dr. Unearned Interest Revenue 300

cr. Interest Revenue 300

Robert N. West © VEMBA Accounting

Interest Revenue Slide 5-15

On August 31, 1998, when the loan is repaid, the entry is:dr. Cash 10,000

cr. Loans Receivable 10,000

After repayment by the borrower, an adjusting entry is also made by the bank to record the fact that $600 interest was earned in 1998.

dr. Unearned Interest Revenue 600

cr. Interest Revenue 600

Robert N. West © VEMBA Accounting

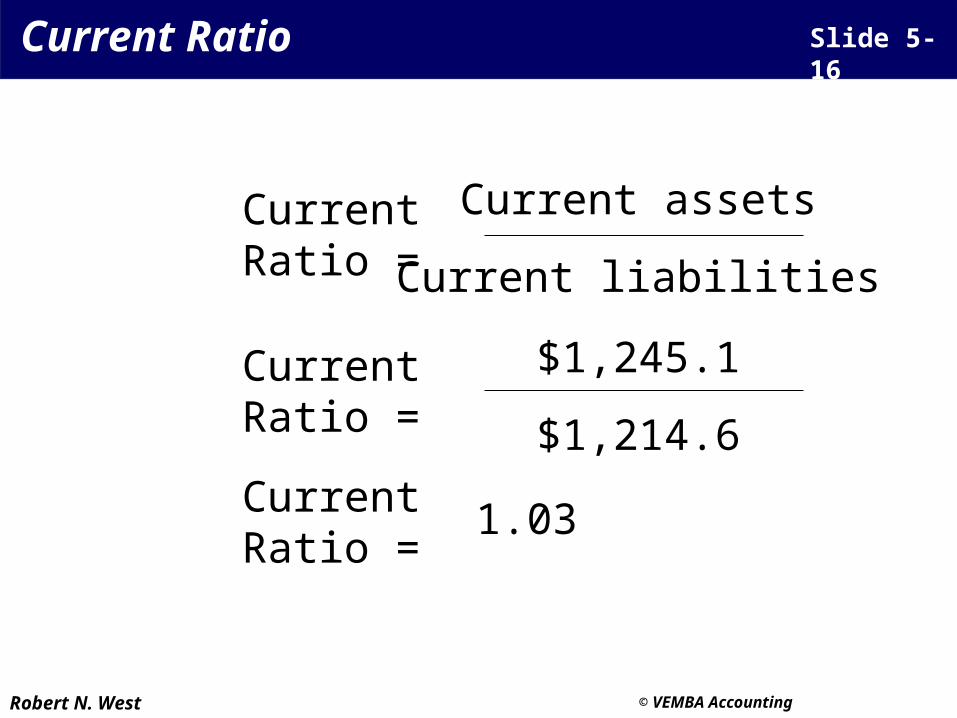

Current Ratio Slide 5-16

Current assets

Current liabilitiesCurrent Ratio =

$1,245.1

$1,214.6Current Ratio =

1.03Current Ratio =

Robert N. West © VEMBA Accounting

Slide 5-17 Acid-Test Ratio

Cash, temporary

investments, and accounts

receivable (net)

Monetary Current assets

Current liabilities

Acid-Test Ratio =

$634.9

$1,214.6

Acid-Test Ratio =

0.52Acid-Test

Ratio =

Robert N. West © VEMBA Accounting

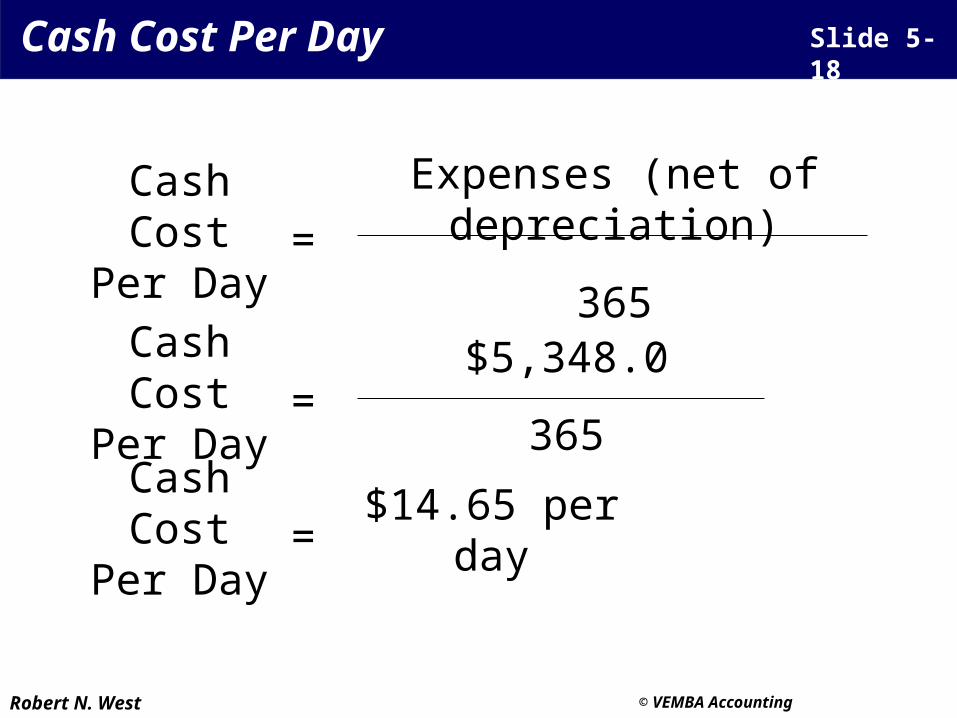

Slide 5-18 Cash Cost Per Day

Expenses (net of depreciation)

365

Cash Cost Per Day =

$5,348.0

365

Cash Cost Per Day =

$14.65 per dayCash Cost Per Day =

Robert N. West © VEMBA Accounting

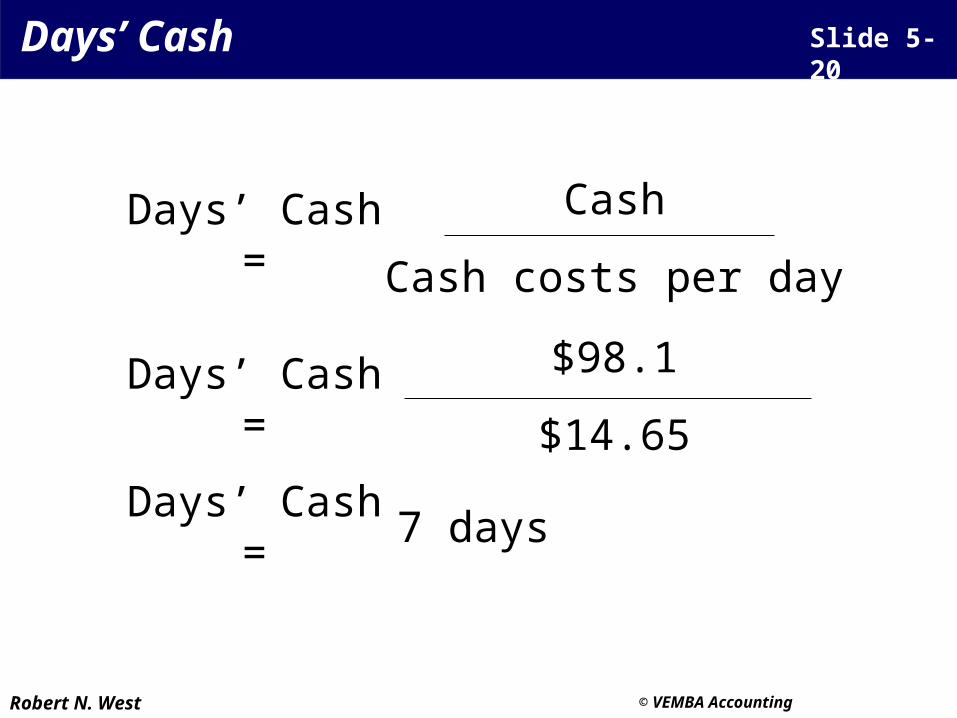

Slide 5-20 Days’ Cash

Cash

Cash costs per dayDays’ Cash =

$98.1

$14.65Days’ Cash =

7 daysDays’ Cash =

Robert N. West © VEMBA Accounting

Chapter 5

The End

Robert N. West © VEMBA Accounting

Remaining Slides

• You can browse through the remaining slides at your own discretion. Most of these slides show the journal entries underlying bad debt accounting. I will not test this material, but you may find it useful to give it a quick look.

Robert N. West © VEMBA Accounting

Trade ReceivablesArise from the sale of services or

products on credit

Robert N. West © VEMBA Accounting

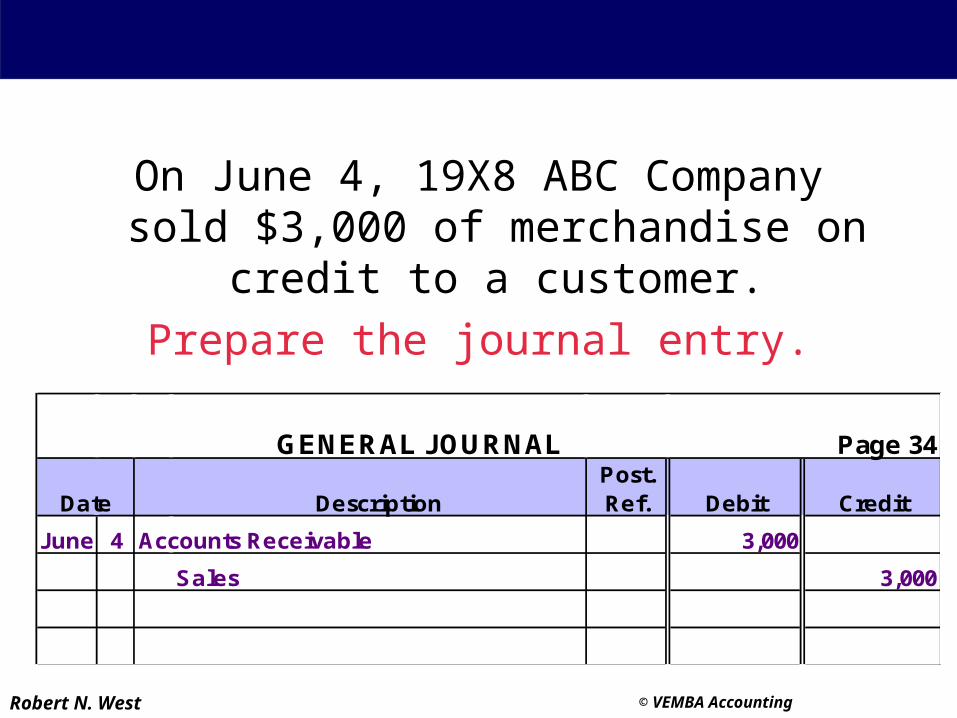

Trade ReceivablesOn June 4, 19X8 ABC Company sold $3,000

of merchandise on credit to a customer.

Prepare the journal entry.

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

June 4 Accounts Receivable 3,000

Sales 3,000

Robert N. West © VEMBA Accounting

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

June 4 Accounts Receivable 3,000

Sales 3,000

Trade Receivables Even though cash was not received, the

revenue is still considered earned at this point because the earnings process is

assumed to be complete.

Robert N. West © VEMBA Accounting

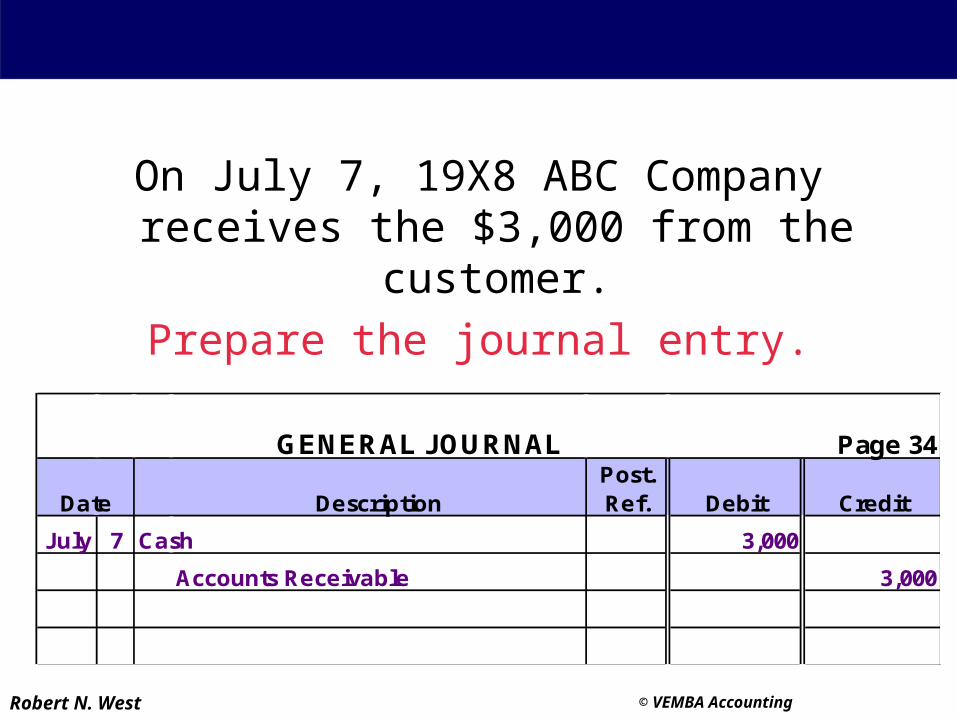

Trade ReceivablesOn July 7, 19X8 ABC Company receives the

$3,000 from the customer.

Prepare the journal entry.

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

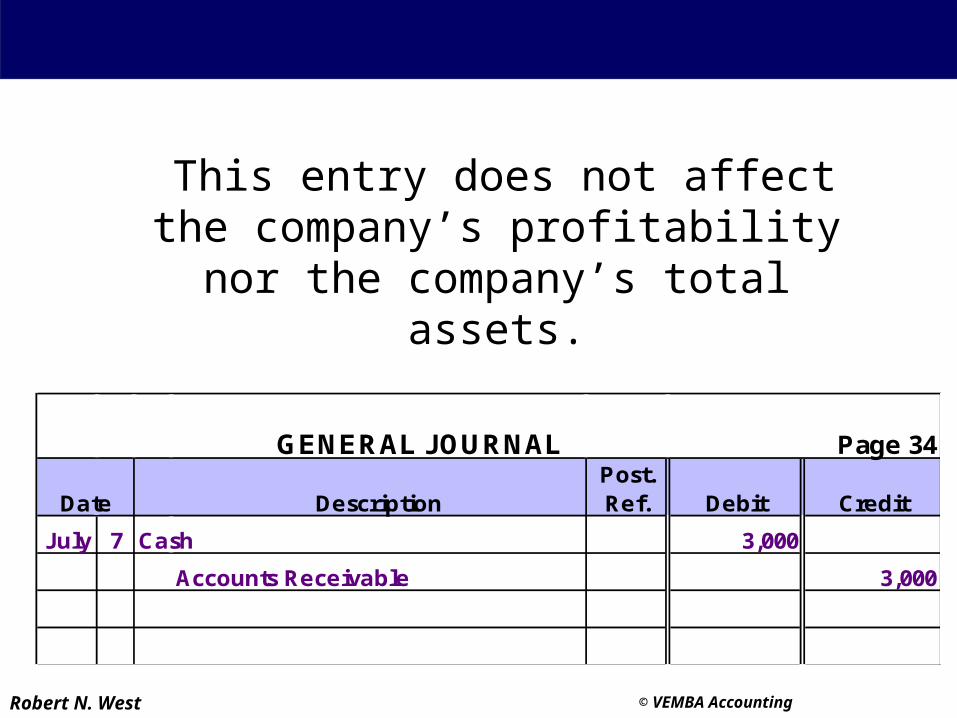

July 7 Cash 3,000

Accounts Receivable 3,000

Robert N. West © VEMBA Accounting

Trade Receivables This entry does not affect the company’s profitability nor the company’s total assets.

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

July 7 Cash 3,000

Accounts Receivable 3,000

Robert N. West © VEMBA Accounting

Management IssuesSelling merchandise on

credit helps to increase my sales, but it also delays the

receipt of cash!

Wow! Buying merchandise on credit let’s me hold on to my

cash longer!!

Robert N. West © VEMBA Accounting

Management IssuesMaybe I can offer a discount to credit

customers to entice them to pay sooner . . .

Robert N. West © VEMBA Accounting

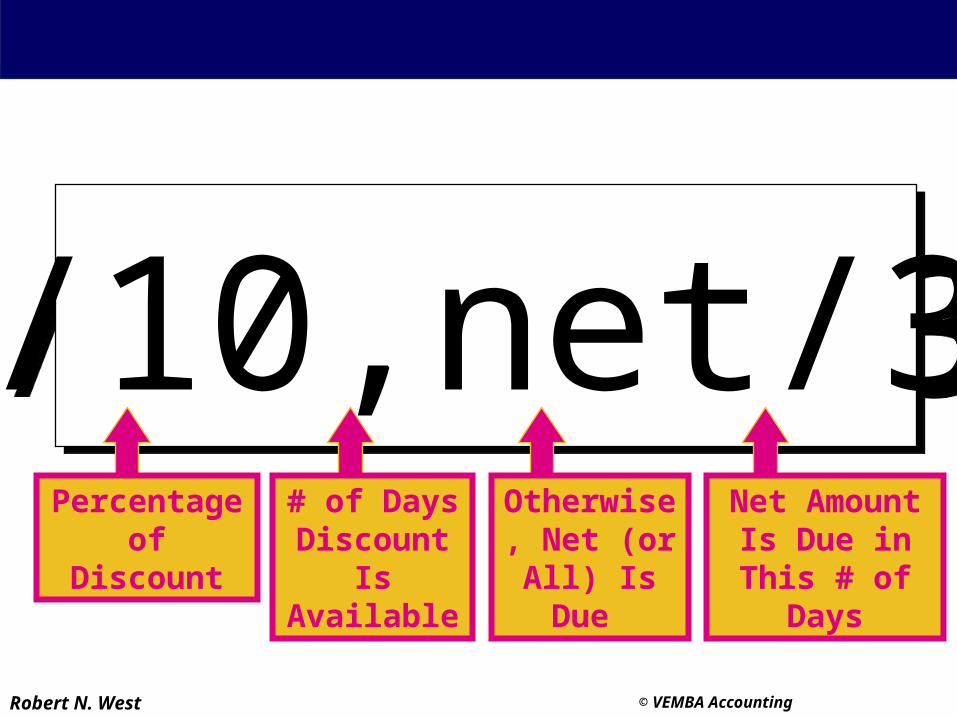

Management Issues

2/10,net/302/10,net/30Percentage of Discount

Net Amount Is Due in This #

of Days

Otherwise, Net (or All)

Is Due

# of Days Discount Is Available

Robert N. West © VEMBA Accounting

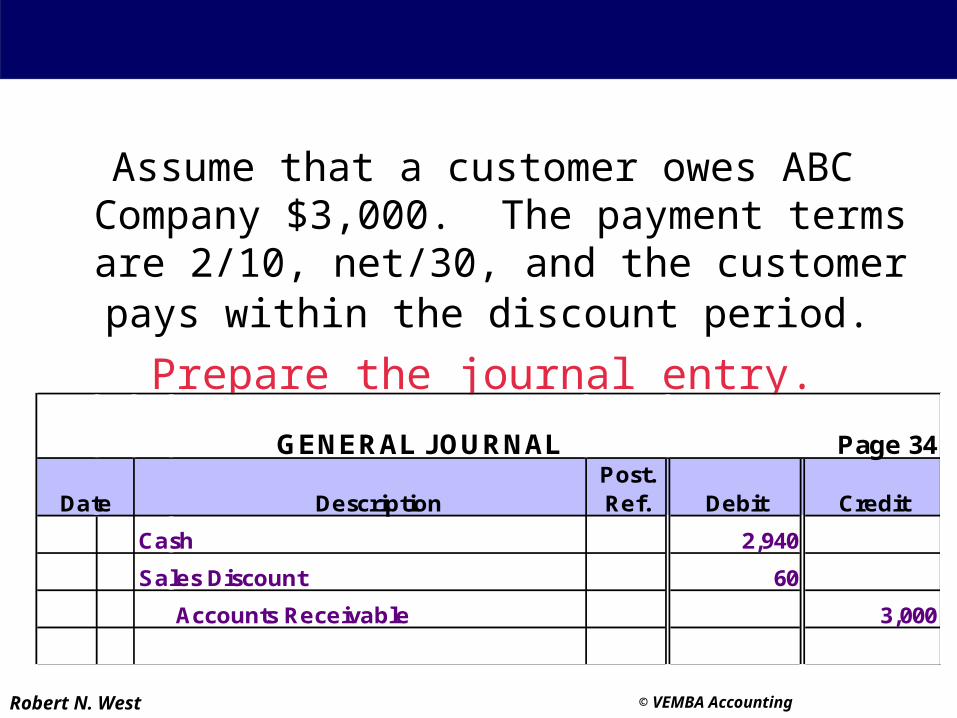

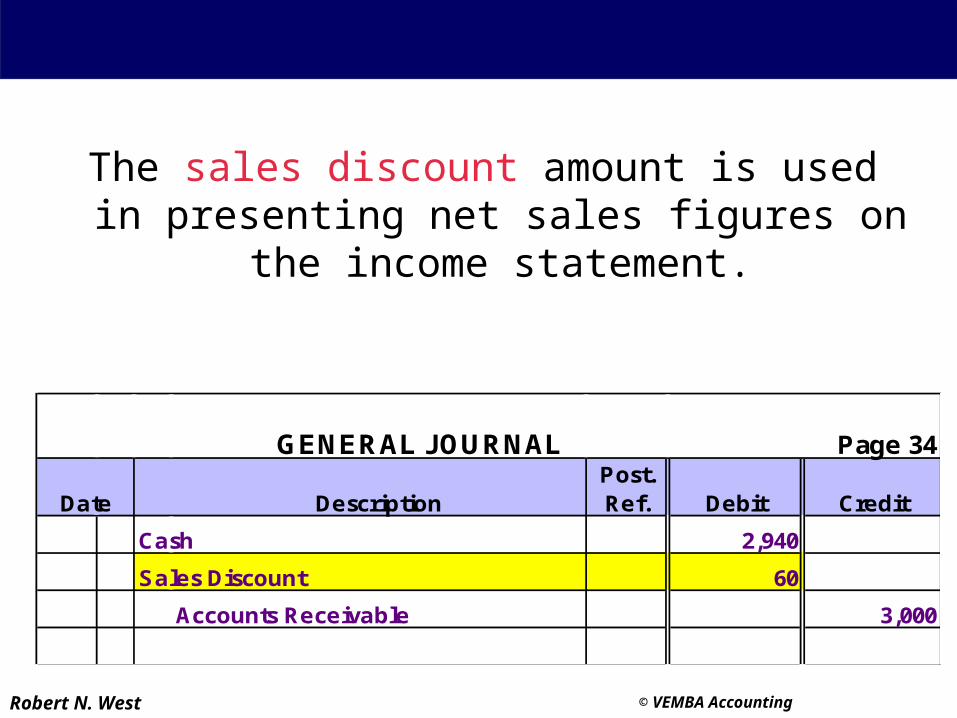

Management IssuesAssume that a customer owes ABC Company $3,000. The payment terms are 2/10, net/30, and

the customer pays within the discount period.

Prepare the journal entry.

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

Cash 2,940

Sales Discount 60

Accounts Receivable 3,000

Robert N. West © VEMBA Accounting

Management IssuesThe sales discount amount is used in presenting net

sales figures on the income statement.

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

Cash 2,940

Sales Discount 60

Accounts Receivable 3,000

Robert N. West © VEMBA Accounting

Management IssuesI wonder if this will be one

of my credit customers who ends up not paying the

balance owed to me?

Robert N. West © VEMBA Accounting

Net Realizable ValuePat's PlaceBalance Sheet

December 31, 19X3

Assets Cash 100,000$Accounts receivable, net 25,000 Inventory 65,000 Total assets 190,000$

Liabilities and Shareholders' EquityLiabilitiesAccounts Payable 95,000$

Shareholders' EquityCapital stock 50,000$Paid-in capital in excess of par value 20,000 70,000 Retained earnings 25,000 Total liabilities and shareholders' equity 190,000$

Net realizable value is the amount expected to be

collected.

Robert N. West © VEMBA Accounting

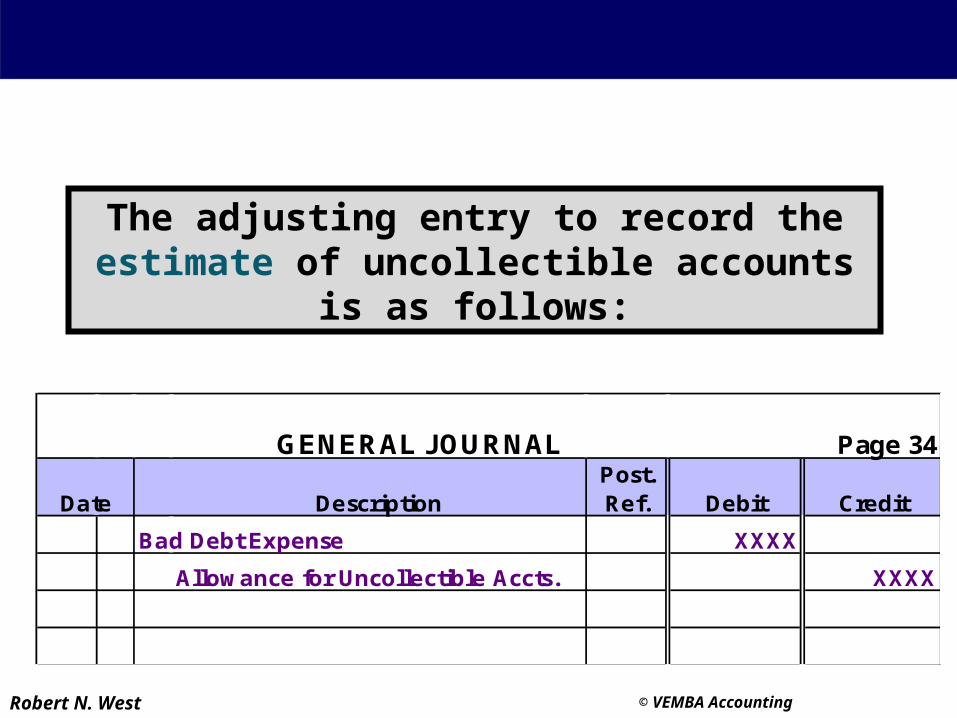

Uncollectible Accounts

Matching Principle

An estimate of the expense relating to

selling goods on credit should be recorded in the period when the revenue is earned.

We must use an estimate because we do not know

which specific customers will

default.

Robert N. West © VEMBA Accounting

Uncollectible Accounts

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

Bad Debt Expense XXXX

Allowance for Uncollectible Accts. XXXX

The adjusting entry to record the estimate of uncollectible accounts is as follows:

Robert N. West © VEMBA Accounting

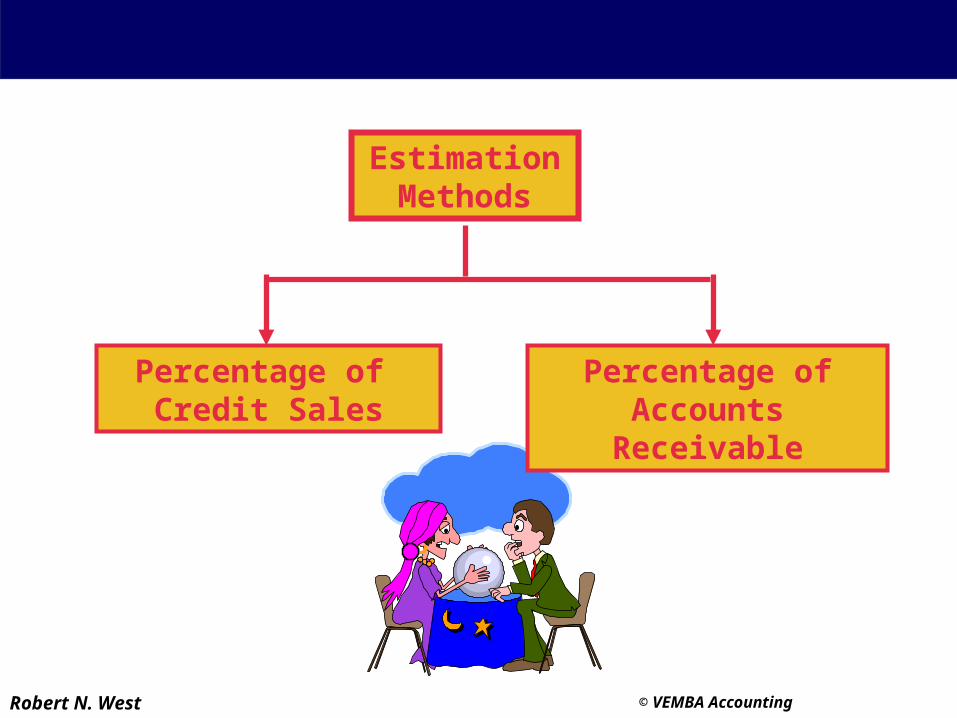

Uncollectible AccountsEstimationMethods

Percentage of Credit Sales

Percentage of Accounts Receivable

Robert N. West © VEMBA Accounting

Percentage of Credit Sales

Based on past history, I can determine the

percentage of credit sales that I never collected.

Then, the amount of my adjusting entry could be

determined as:

Current Year Credit Sales

× Bad Debt%

Estimated Bad Debt Expense

Robert N. West © VEMBA Accounting

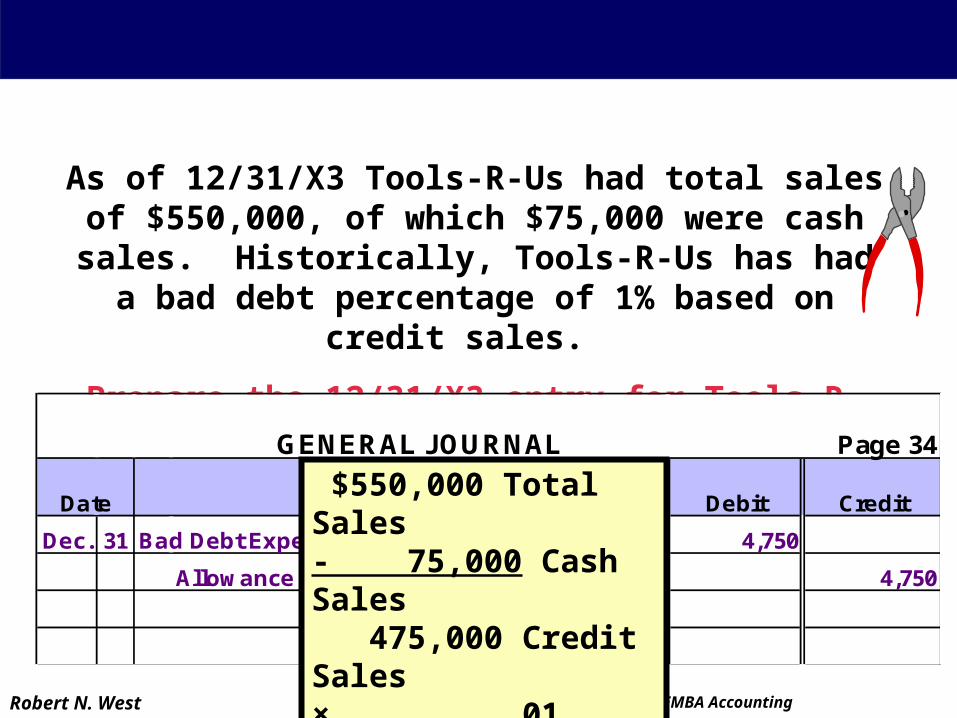

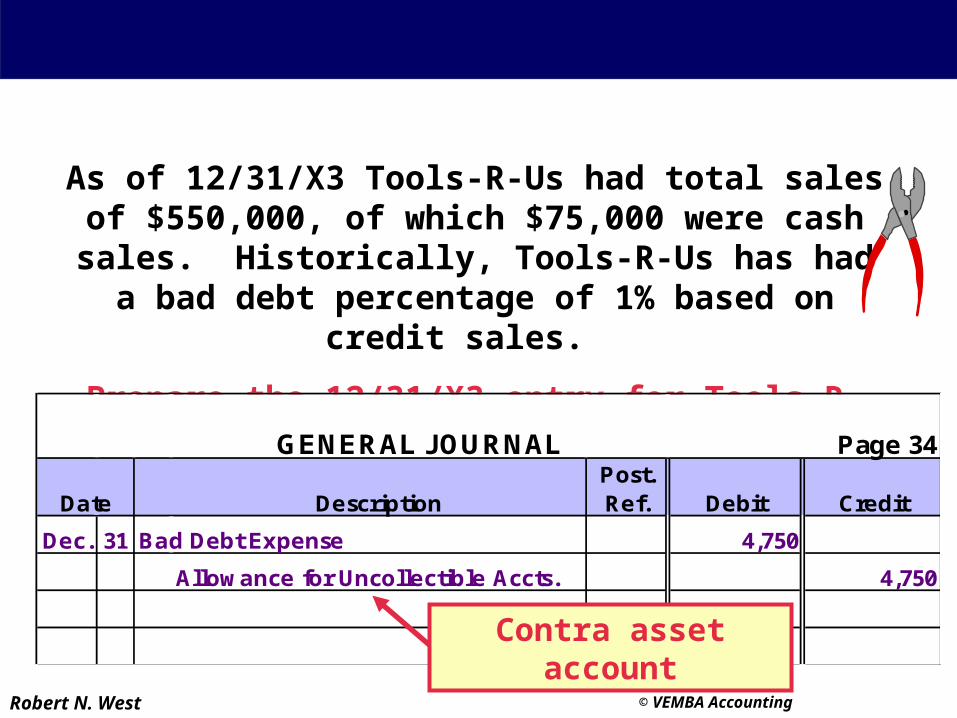

Percentage of Credit SalesAs of 12/31/X3 Tools-R-Us had total sales of $550,000, of which $75,000 were cash sales. Historically, Tools-R-Us has had a bad debt percentage of 1% based on credit sales.

Prepare the 12/31/X3 entry for Tools-R-Us.

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

Dec. 31 Bad Debt Expense 4,750

Allowance for Uncollectible Accts. 4,750

$550,000 Total Sales- 75,000 Cash Sales 475,000 Credit Sales× .01 $ 4,750

Robert N. West © VEMBA Accounting

Percentage of Credit SalesAs of 12/31/X3 Tools-R-Us had total sales of $550,000, of which $75,000 were cash sales. Historically, Tools-R-Us has had a bad debt percentage of 1% based on credit sales.

Prepare the 12/31/X3 entry for Tools-R-Us.

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

Dec. 31 Bad Debt Expense 4,750

Allowance for Uncollectible Accts. 4,750

Contra asset account

Robert N. West © VEMBA Accounting

Percentage of Credit SalesIf Tools-R-Us had accounts receivable of

$100,000 at 12/31/X3, what amount should be reported on the 12/31/X3 balance sheet?

Accounts receivable 100,000$Less allowance 4,750 Net realizable value 95,250$

Robert N. West © VEMBA Accounting

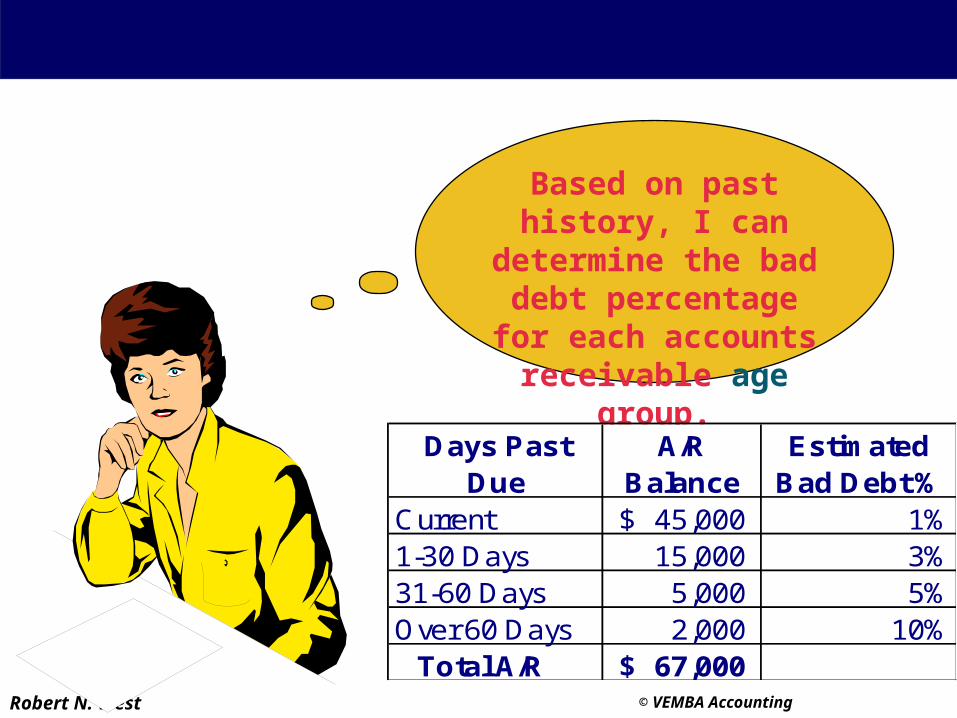

Percentage of Accounts ReceivableBased on past history, I can determine the bad

debt percentage for each accounts

receivable age group.

Days Past Due

A/R Balance

Estimated Bad Debt %

Current 45,000$ 1%1-30 Days 15,000 3%31-60 Days 5,000 5%Over 60 Days 2,000 10% Total A/R 67,000$

Robert N. West © VEMBA Accounting

Percentage of Accounts Receivable

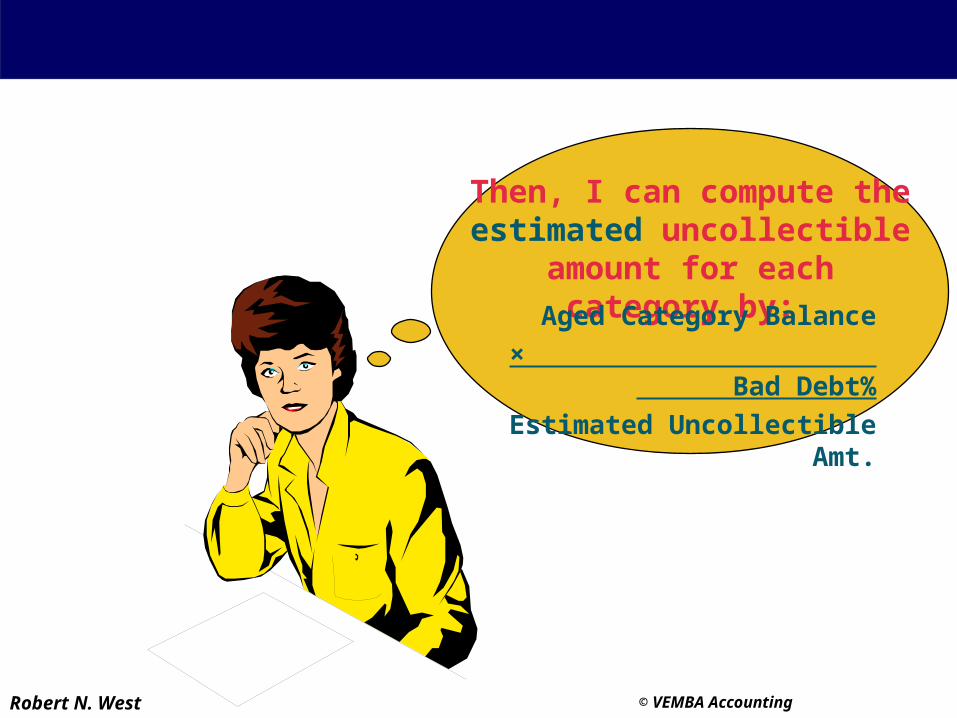

Then, I can compute the estimated uncollectible

amount for each category by:

Aged Category Balance

× Bad Debt%

Estimated Uncollectible Amt.

Robert N. West © VEMBA Accounting

Percentage of Accounts Receivable

Robert N. West © VEMBA Accounting

Percentage of Accounts Receivable

By adding the estimated uncollectible total for

each aged category, I can determine the desired

balance for the allowance for uncollectible

accounts.

Robert N. West © VEMBA Accounting

Percentage of Accounts Receivable

Robert N. West © VEMBA Accounting

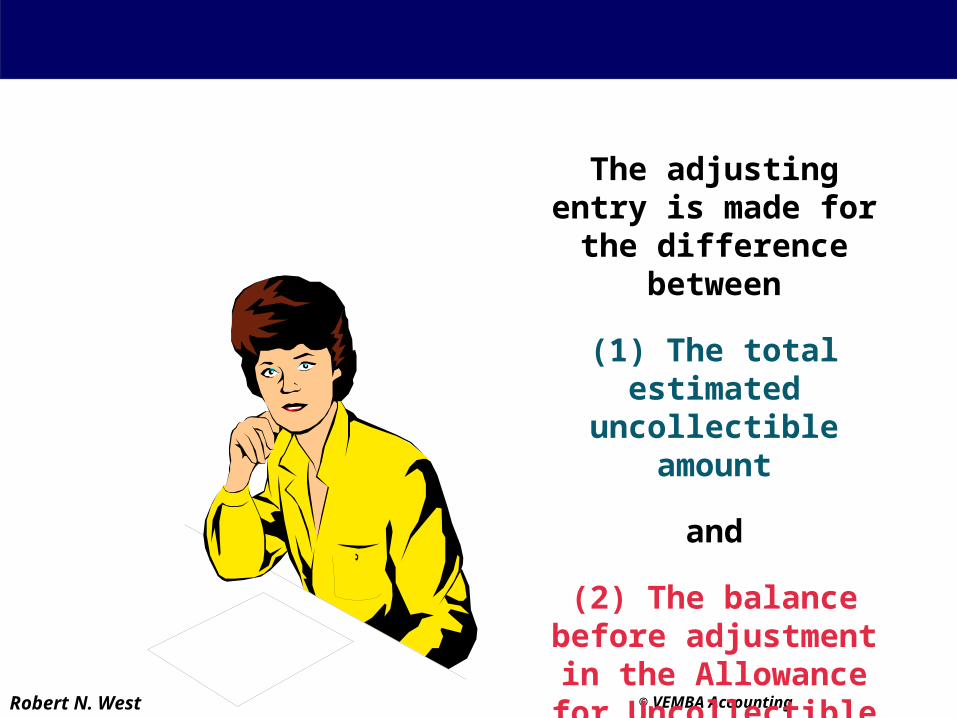

Percentage of Accounts ReceivableThe adjusting entry is

made for the difference between

(1) The total estimated uncollectible amount

and

(2) The balance before adjustment in the

Allowance for Uncollectible Accounts

Robert N. West © VEMBA Accounting

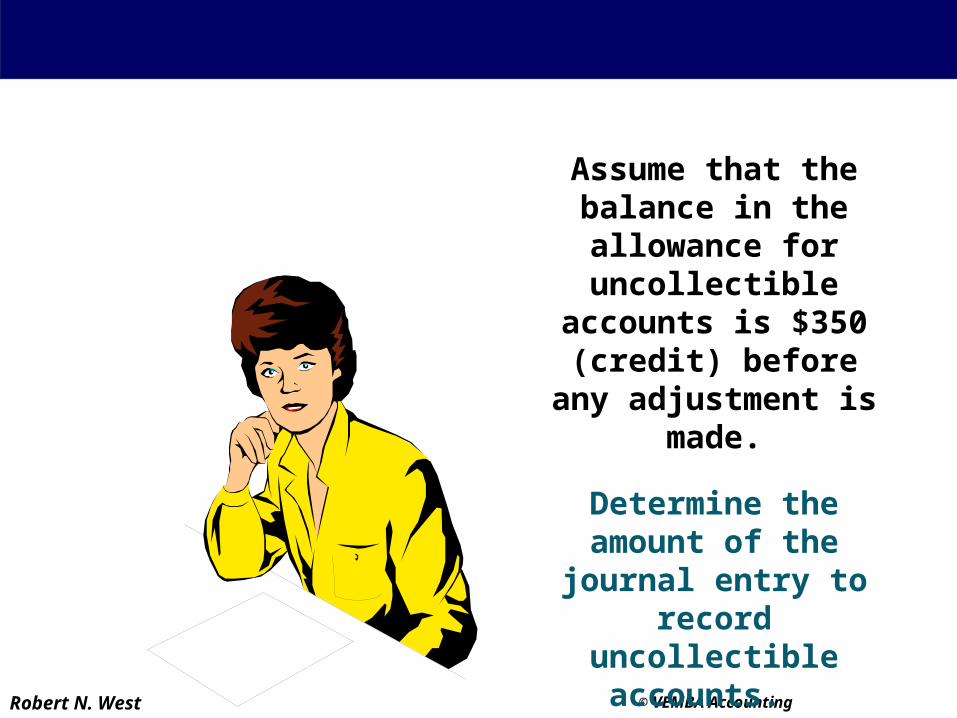

Percentage of Accounts ReceivableAssume that the

balance in the allowance for

uncollectible accounts is $350 (credit) before

any adjustment is made.

Determine the amount of the journal entry to record uncollectible

accounts.

Robert N. West © VEMBA Accounting

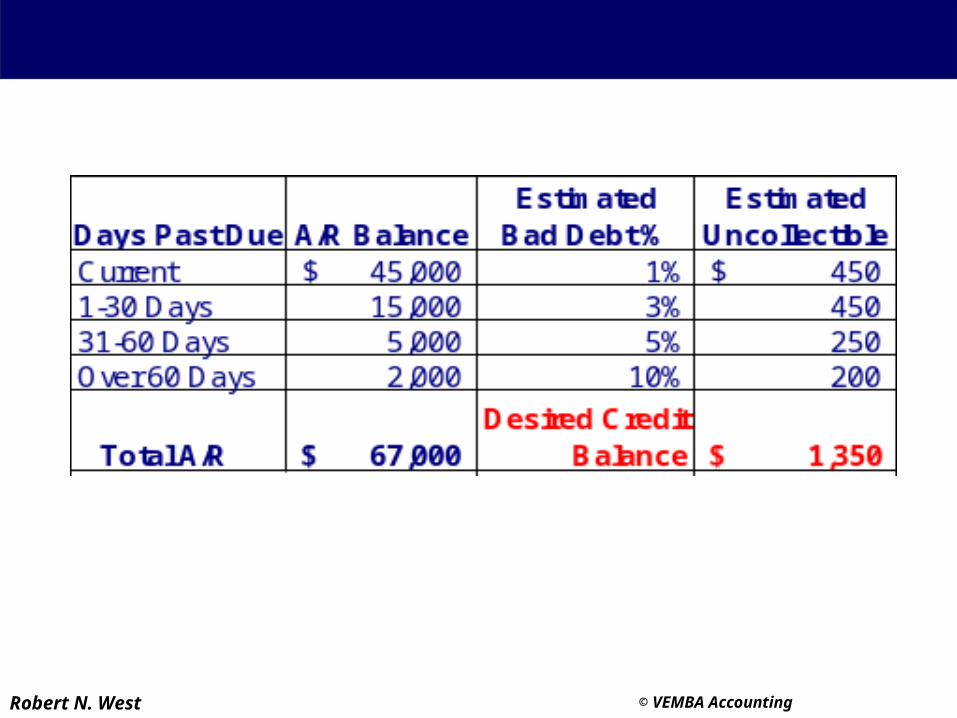

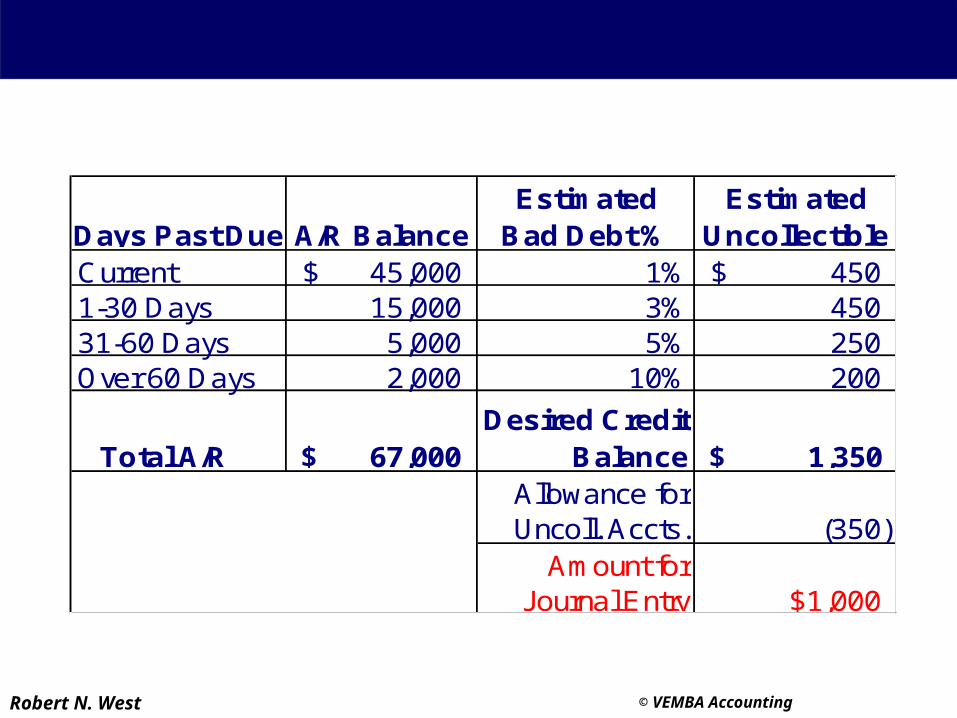

Percentage of Accounts Receivable

Days Past Due A/R BalanceEstimated

Bad Debt %Estimated

UncollectibleCurrent 45,000$ 1% 450$ 1-30 Days 15,000 3% 450 31-60 Days 5,000 5% 250 Over 60 Days 2,000 10% 200

Total A/R $ 67,000 Desired Credit

Balance $ 1,350 Allowance for Uncoll. Accts. (350)

Amount for Journal Entry $1,000

Robert N. West © VEMBA Accounting

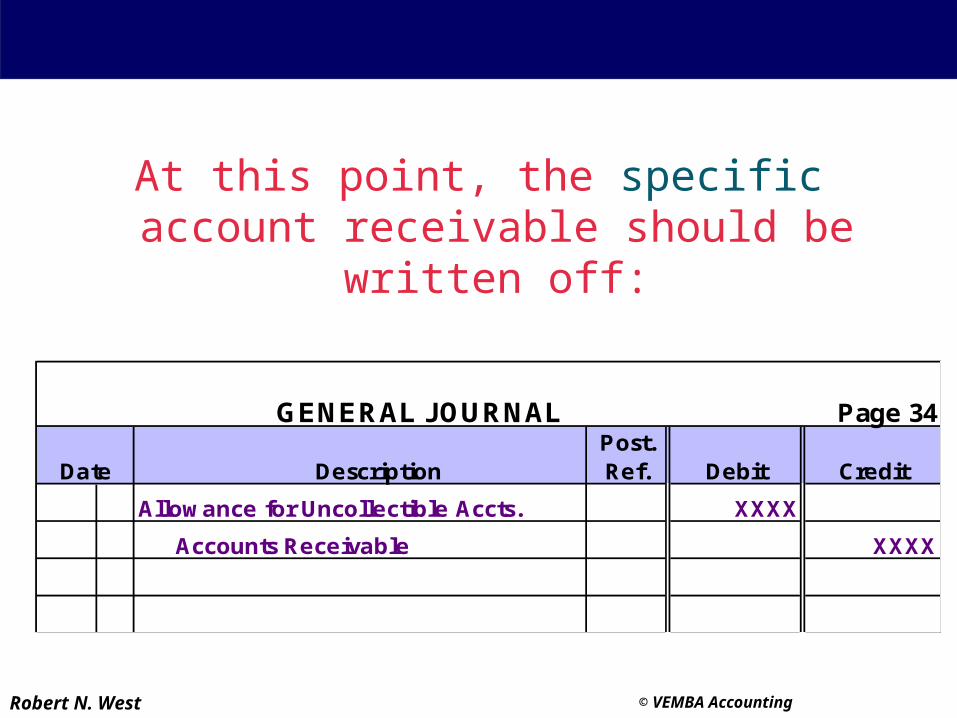

Write-off of Accounts ReceivableOccasionally it will become apparent that a

specific account receivable will not be collected.

Robert N. West © VEMBA Accounting

Write-off of Accounts ReceivableAt this point, the specific account receivable

should be written off:

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

Allowance for Uncollectible Accts. XXXX

Accounts Receivable XXXX

Robert N. West © VEMBA Accounting

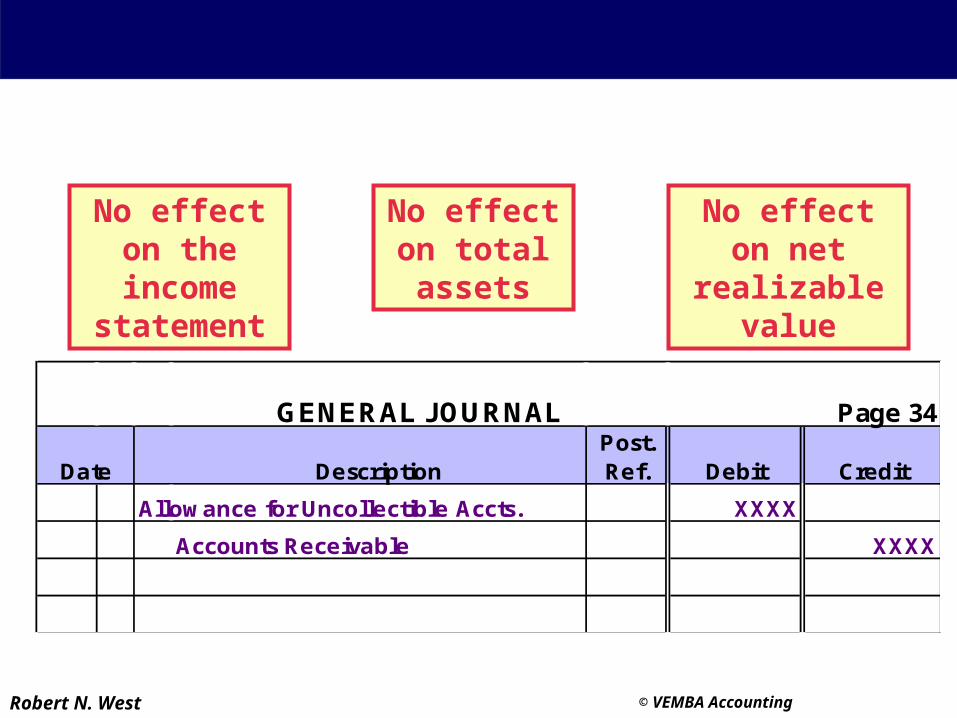

Write-off of Accounts Receivable

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

Allowance for Uncollectible Accts. XXXX

Accounts Receivable XXXX

No effect on the income statement

No effect on total assets

No effect on net realizable

value

Robert N. West © VEMBA Accounting

Recovery of Accounts Receivable Written Off

GENERAL JOURNAL Page 34

Date DescriptionPost. Ref. Debit Credit

Accounts Receivable XXXX

Allowance for Uncollectible Accts. XXXX

If an account that has been written off subsequently becomes collectible, simply

reverse the write-off entry.

Robert N. West © VEMBA Accounting

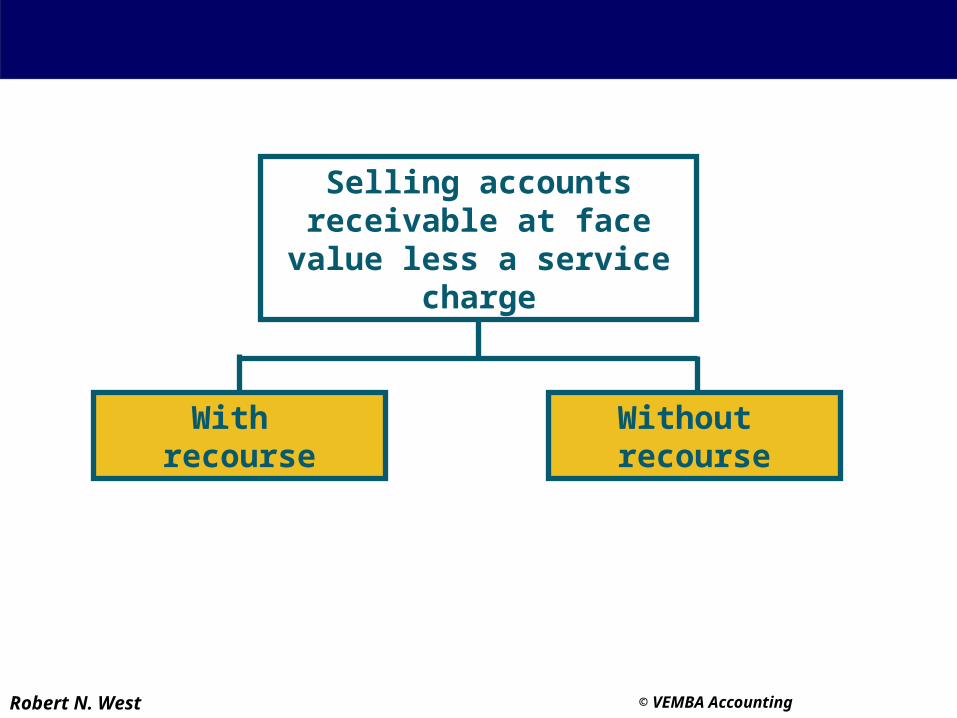

FactoringSelling accounts

receivable at face value less a service charge

With recourse

Without recourse

Robert N. West © VEMBA Accounting

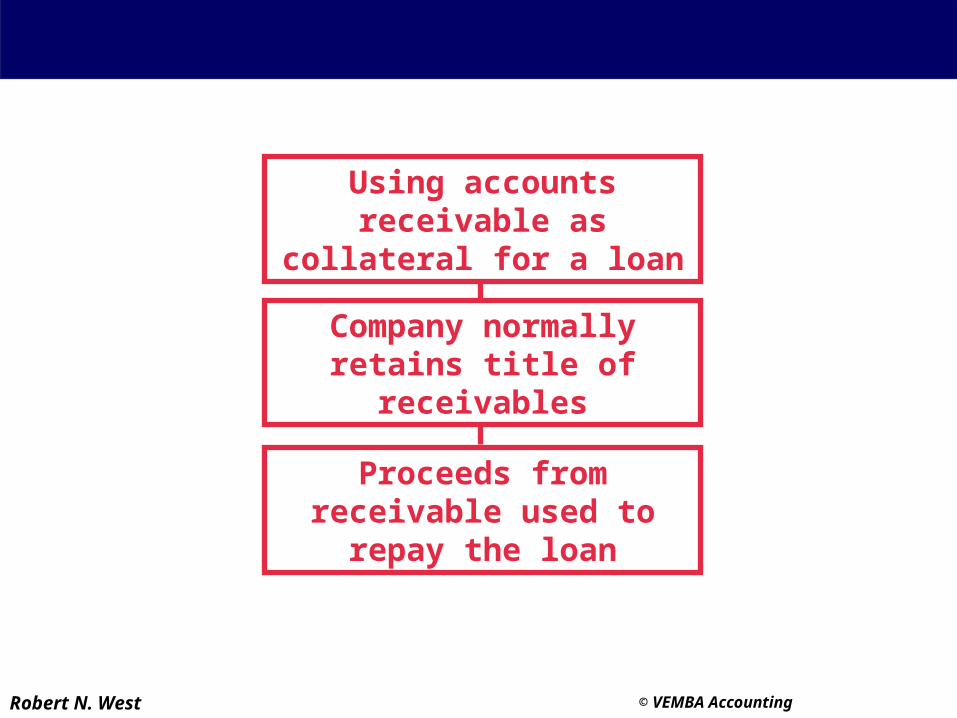

PledgingUsing accounts receivable

as collateral for a loan

Company normally retains title of receivables

Proceeds from receivable used to repay the loan

Robert N. West © VEMBA Accounting

Note Receivable

Promissory Notes

Maker

Payee

Principal

Interest

Maturity Date

Robert N. West © VEMBA Accounting

Analyzing Trade Receivables

Average receivable

collection period

Average accounts receivable balance

Total credit sales /365 days=

This ratio provides a rough measure of the length of time that a company’s accounts

receivable have been outstanding.