Chapter Seven Accounting for Liabilities © 2015 McGraw-Hill Education.

23

Chapter Seven Accounting for Liabilitie s © 2015 McGraw-Hill Education.

-

Upload

ethel-bryant -

Category

Documents

-

view

222 -

download

0

Transcript of Chapter Seven Accounting for Liabilities © 2015 McGraw-Hill Education.

Chapter Seven

Accounting

for

Liabilities

© 2015 McGraw-Hill Education.

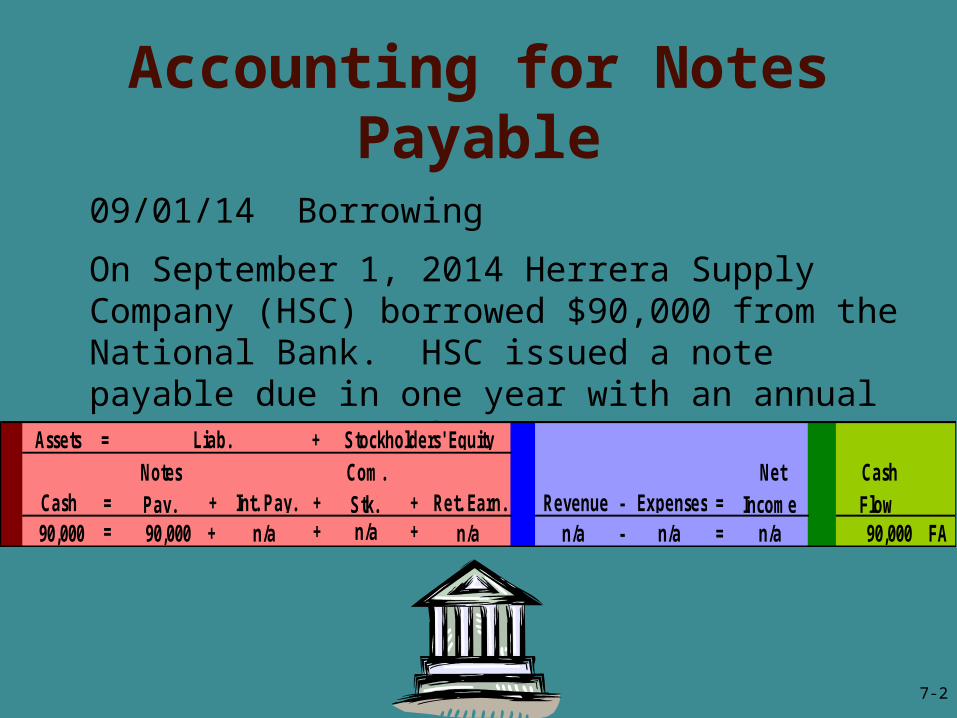

Accounting for Notes Payable

= +

Cash = Notes Pay. + Int. Pay. +

Com. Stk. + Ret. Earn. Revenue - Expenses =

Net Income

Cash Flow

90,000 = 90,000 + n/a + n/a + n/a n/a - n/a = n/a 90,000 FA

Assets Liab. Stockholders' Equity

09/01/14 Borrowing

On September 1, 2014 Herrera Supply Company (HSC) borrowed $90,000 from the National Bank. HSC issued a note payable due in one year with an annual interest rate of 9%.

7-2

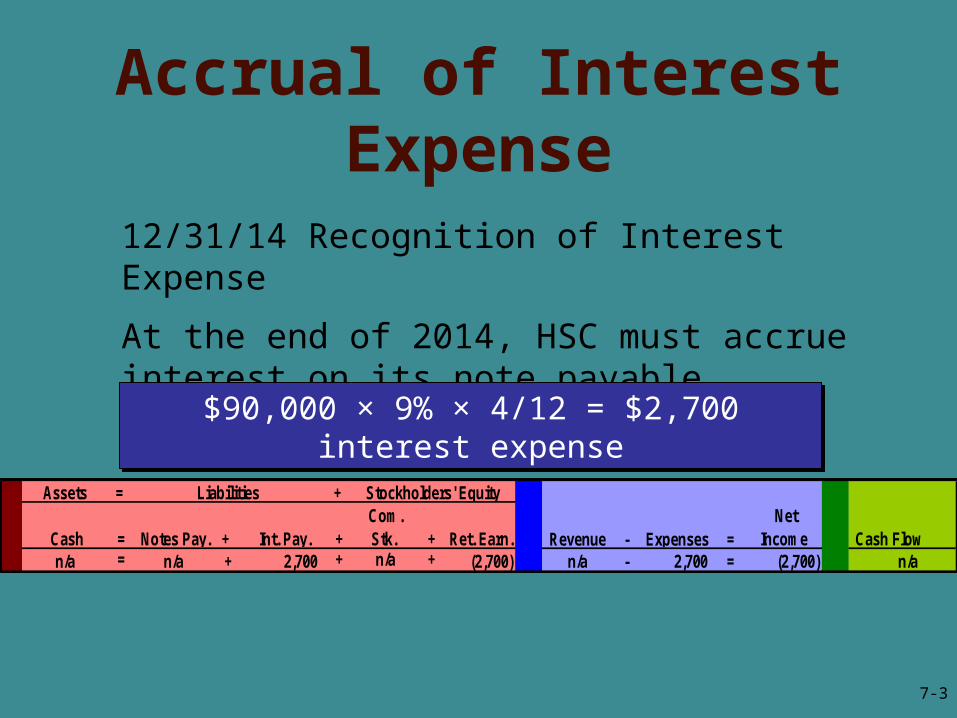

Accrual of Interest Expense

Assets = +

Cash = Notes Pay. + Int. Pay. + Com. Stk. + Ret. Earn. Revenue - Expenses =

Net Income Cash Flow

n/a = n/a + 2,700 + n/a + (2,700) n/a - 2,700 = (2,700) n/a

Stockholders' EquityLiabilities

12/31/14 Recognition of Interest Expense

At the end of 2014, HSC must accrue interest on its note payable.

$90,000 × 9% × 4/12 = $2,700 interest expense

$90,000 × 9% × 4/12 = $2,700 interest expense

7-3

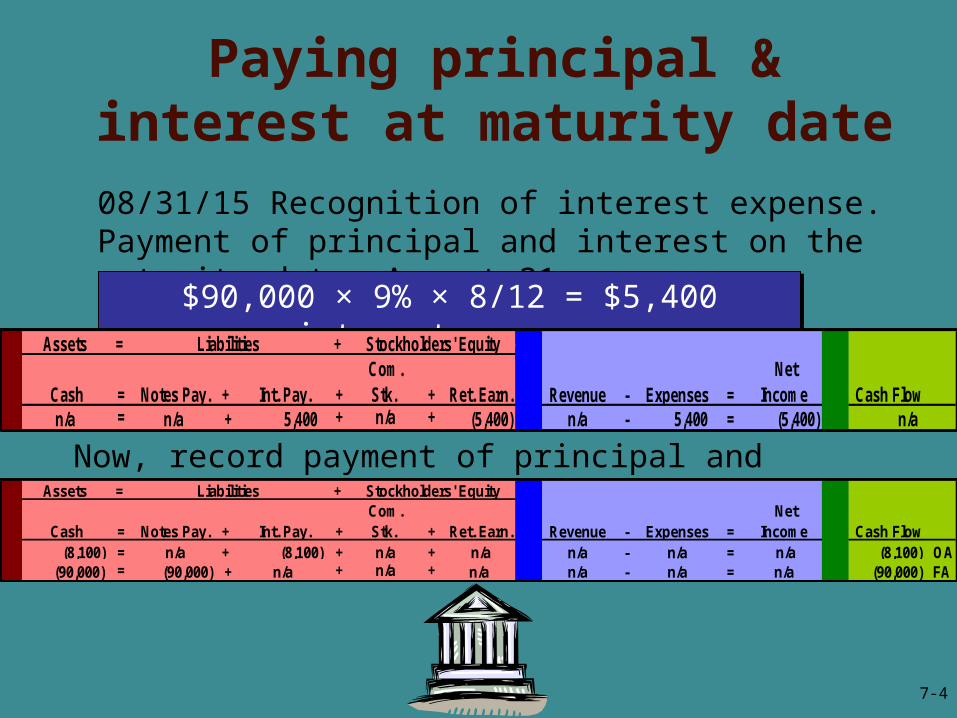

Paying principal & interest at maturity date

Assets = +

Cash = Notes Pay. + Int. Pay. + Com. Stk. + Ret. Earn. Revenue - Expenses =

Net Income Cash Flow

n/a = n/a + 5,400 + n/a + (5,400) n/a - 5,400 = (5,400) n/a

Stockholders' EquityLiabilities

Assets = +

Cash = Notes Pay. + Int. Pay. + Com. Stk. + Ret. Earn. Revenue - Expenses =

Net Income Cash Flow

(8,100) = n/a + (8,100) + n/a + n/a n/a - n/a = n/a (8,100) OA (90,000) = (90,000) + n/a + n/a + n/a n/a - n/a = n/a (90,000) FA

Stockholders' EquityLiabilities

08/31/15 Recognition of interest expense. Payment of principal and interest on the maturity date, August 31.

$90,000 × 9% × 8/12 = $5,400 interest expense

$90,000 × 9% × 8/12 = $5,400 interest expense

Now, record payment of principal and interest payable.

7-4

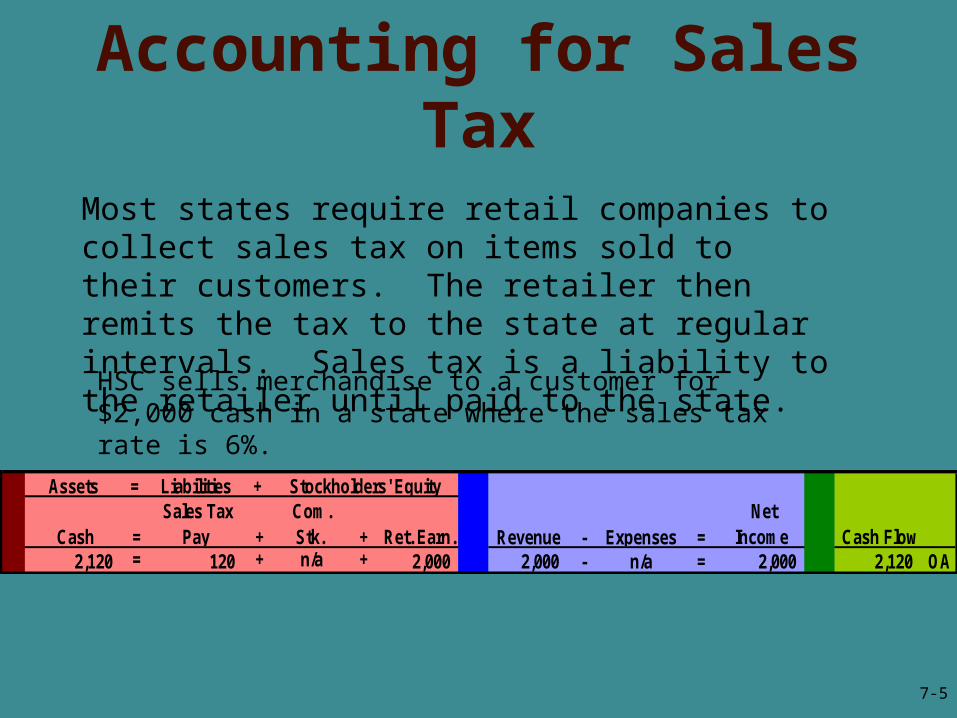

Accounting for Sales Tax

Assets = Liabilities +

Cash = Sales Tax

Pay + Com. Stk. + Ret. Earn. Revenue - Expenses =

Net Income Cash Flow

2,120 = 120 + n/a + 2,000 2,000 - n/a = 2,000 2,120 OA

Stockholders' Equity

Most states require retail companies to collect sales tax on items sold to their customers. The retailer then remits the tax to the state at regular intervals. Sales tax is a liability to the retailer until paid to the state.

HSC sells merchandise to a customer for $2,000 cash in a state where the sales tax rate is 6%.

7-5

Accounting for Sales Tax

Assets = Liabilities +

Cash = Sales Tax

Pay + Com.

Stk. + Ret. Earn. Revenue - Expenses =

Net Income

Cash Flow

(120) = (120) + n/a + n/a n/a - n/a = n/a (120) OA

Stockholders' Equity

Remitting the tax (paying cash to the state tax authority) is an asset use transaction.

7-6

Reporting Contingent Liabilities

7-7

Warranty Obligations

= Liab. + Equity

Cash + Inventory = + Ret. Earn. Rev. - Exp. = Net

Income Cash Flow

7,000 + n/a = n/a + 7,000 7,000 - n/a = 7,000 7,000 OA

n/a + (4,000) = n/a + (4,000) n/a - 4,000 = (4,000) n/a

Assets

To attract customers, many companies guarantee their products or services. Within the warranty period, the seller promises to replace or repair defective products without charge.

Event 1 Sale of MerchandiseHSC sells $7,000 of merchandise for cash. The merchandise had a cost of $4,000.

7-8

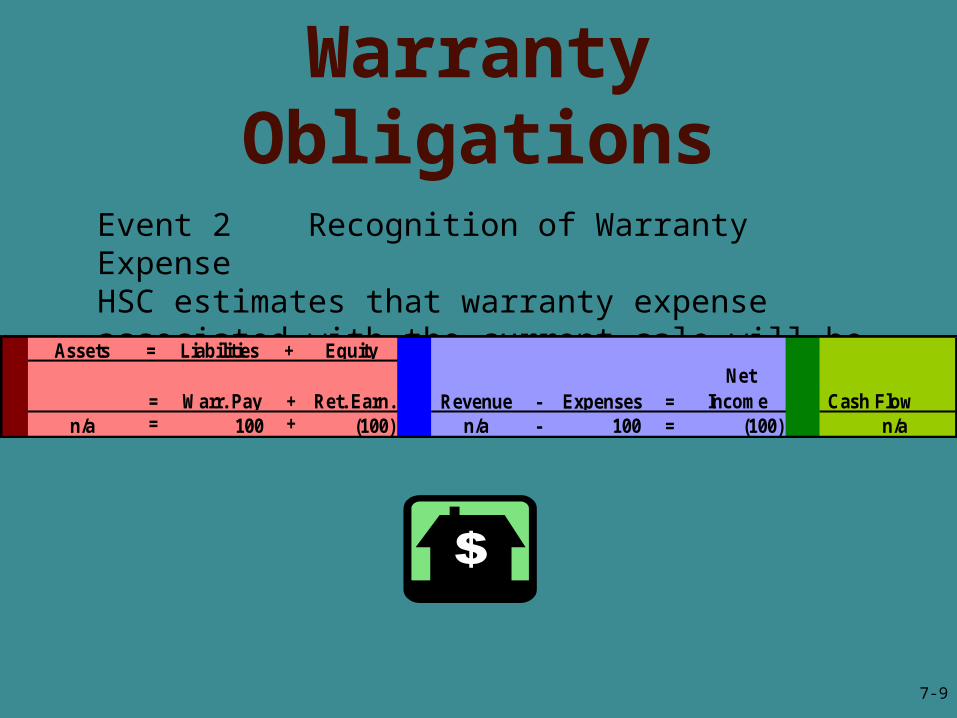

Warranty Obligations

Assets = Liabilities + Equity

= Warr. Pay + Ret. Earn. Revenue - Expenses = Net

Income Cash Flow n/a = 100 + (100) n/a - 100 = (100) n/a

Event 2 Recognition of Warranty ExpenseHSC estimates that warranty expense associated with the current sale will be $100.

7-9

Warranty Obligations

Assets = Liabilities + Equity

Cash = Warr. Pay + Ret. Earn. Revenue - Expenses = Net

Income Cash Flow (40) = (40) + n/a n/a - n/a = n/a (40) OA

Event 3 Settlement of Warranty ObligationHSC pays $40 cash to repair defective merchandise returned by a customer.

7-10

Financial Statements

Assets Cash 8,960$ Inventory 2,000 Total Assets 10,960$

Liabilities Warranties Payable 60 Stockholders' Equity Common Stock 5,000 Retained Earnings 5,900 Total Liab. & Stockholders' Equity 10,960$

Balance Sheet

Operating Activities Inflow from Customers 7,000$ Outflows for Warranty (40) Net Inflows From Oper. 6,960 Investing Activities 0Financing Activities 0 Beginning Cash Balance 2,000

Ending Cash Balance 8,960$

Statement of Cash Flows

Sales Revenue 7,000$ Cost of Goods Sold (4,000) Gross Margin 3,000 Warranty Expense (100) Net Income 2,900$

Income Statement

7-11

Installment Notes PayableCash payment determined using present valueconcepts presented in a later chapter.Cash payment determined using present valueconcepts presented in a later chapter.

All computations rounded to the nearest dollar; after the 2018 payment the loan balance is 0.

Accounting Period

Unpaid Principal

Balance on January 1

Cash Payment on

December 31

Amount Applied to

Interest

Amount Applied to Principal

2014 100,000$ 25,709$ 9,000$ 16,709$ 20152016

83,291 25,709 7,496 18,213 65,078 25,709 5,857 19,852

20172018

45,226 25,709 4,070 21,639 23,587 25,710 2,123 23,587

7-12

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Year 1 Year 2 Year 3 Year 4 Year 5

Interest

Principal

With each payment the amount applied to the principal increases and the amount applied to

interest decreases.

With each payment the amount applied to the principal increases and the amount applied to

interest decreases.

Annual payments

are constant.

Installment Notes Payable

7-13

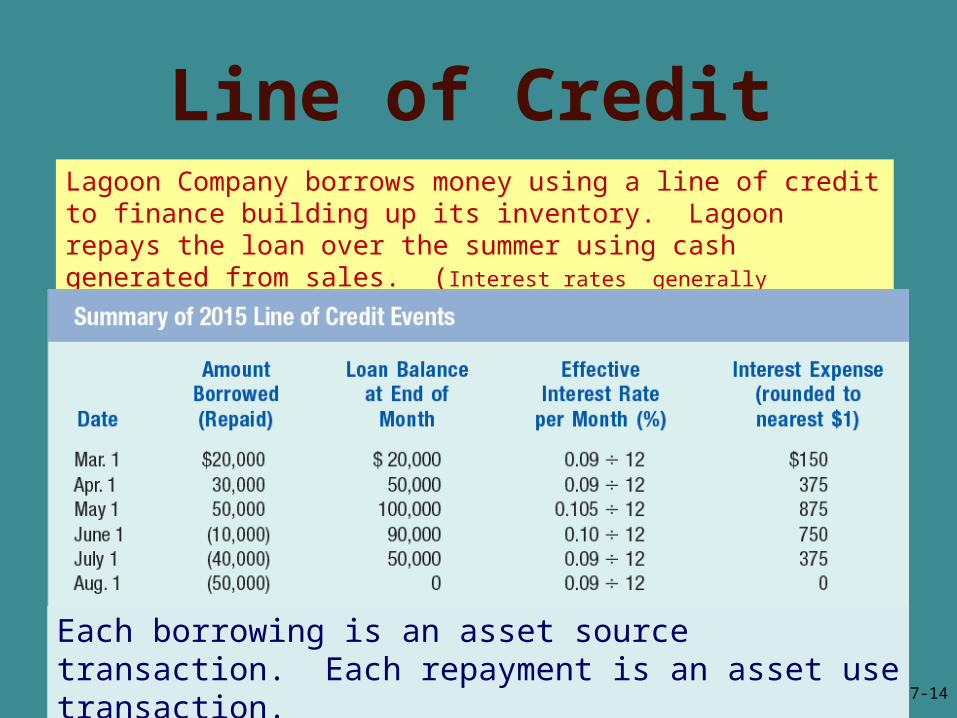

Line of CreditLagoon Company borrows money using a line of credit to finance building up its inventory. Lagoon repays the loan over the summer using cash generated from sales. (Interest rates generally fluctuate based on a designated interest rate benchmark.)

Each borrowing is an asset source transaction. Each repayment is an asset use transaction.

7-14

Mason Company issues bonds on January 1, 2011.Principal = $100,000Stated Interest Rate = 9%Interest Date = 12/31Maturity Date = Dec. 31, 2015 (5 years)

Mason Company issues bonds on January 1, 2011.Principal = $100,000Stated Interest Rate = 9%Interest Date = 12/31Maturity Date = Dec. 31, 2015 (5 years)

Bond Certificateat Face Value

Bond Certificateat Face Value

Bond Selling Price

Mason Company

Investors

Mason Company issues bonds on January 1, 2014.Principal = $100,000Stated Interest Rate = 9%Interest Date = 12/31Maturity Date = Dec. 31, 2018 (5 years)

Mason Company issues bonds on January 1, 2014.Principal = $100,000Stated Interest Rate = 9%Interest Date = 12/31Maturity Date = Dec. 31, 2018 (5 years)

Bond Certificateat Face Value

Bond Certificateat Face Value

Bond Selling Price

Mason Company

Investors

Bonds Issued at Face Value

7-15

Bonds Issued at Face Value

Event 1 Issue Bonds for CashIssuing the bonds has the following effect on Mason’s 2014 financial statements:

Event 1 Issue Bonds for CashIssuing the bonds has the following effect on Mason’s 2014 financial statements:

Assets = Liabilities + Equity

Cash = Bonds

Pay. + Revenue - Expenses = Net

Income Cash Flow

100,000 = 100,000 + n/a n/a - n/a = n/a 100,000 FA

Event 2 Investment in LandPaying $100,000 cash to purchase land is an asset exchange transaction.

Event 2 Investment in LandPaying $100,000 cash to purchase land is an asset exchange transaction.

Assets = Liabilities + Equity

Cash Land + Revenue - Expenses = Net

Income

Cash Flow

(100,000) + 100,000 = n/a n/a n/a - n/a = n/a (100,000) IA

7-16

Bonds Issued at Face Value

Event 3 Revenue RecognitionRecognizing $12,000 cash revenue from renting the property is an asset source transaction.

Event 3 Revenue RecognitionRecognizing $12,000 cash revenue from renting the property is an asset source transaction.

Assets = Liabilities + Equity

Cash = + Ret. Earn. Revenue - Expenses = Net

Income Cash Flow (9,000) = n/a + (9,000) n/a - 9,000 = (9,000) (9,000) OA

Event 4 Expense RecognitionMason’s $9,000 ($100,000 x 0.09) cash payment in each of the 5 years represents interest expense.

Event 4 Expense RecognitionMason’s $9,000 ($100,000 x 0.09) cash payment in each of the 5 years represents interest expense.

Assets = Liabilities + Equity

Cash = + Ret. Earn. Revenue - Expenses =

Net Income

Cash Flow

12,000 = n/a + 12,000 12,000 - n/a = 12,000 12,000 OA

7-17

Bonds Issued at Face Value

Event 6 Payoff of Bond LiabilityThe principal repayment on December 31, 2018 will have thefollowing effect on Mason’s 2018 financial statements:

Event 6 Payoff of Bond LiabilityThe principal repayment on December 31, 2018 will have thefollowing effect on Mason’s 2018 financial statements:

Assets = Liabilities + Equity

Cash = Bonds Pay. + Revenue - Expenses = Net

Income Cash Flow (100,000) = (100,000) + n/a n/a - n/a = n/a (100,000) FA

Assets = Liabilities + Equity

Cash Land + Revenue - Expenses = Net

Income

Cash Flow

100,000 + (100,000) = n/a n/a n/a - n/a = n/a 100,000 IA

Event 5 Sale of Investment in LandSelling the land for cash equal to its $100,000 book value is an asset exchange transaction.

Event 5 Sale of Investment in LandSelling the land for cash equal to its $100,000 book value is an asset exchange transaction.

7-18

Bond Certificateat Face Value

Bond Certificateat Face Value

Bond Selling Price

Mason Company

Investors

$100,000 face issued at 95:

Bonds Payable $100,000

Less: Discount on Bonds Payable (5,000)

Carrying Value $ 95,000

$100,000 face issued at 95:

Bonds Payable $100,000

Less: Discount on Bonds Payable (5,000)

Carrying Value $ 95,000

Bond Certificateat Face Value

Bond Certificateat Face Value

Bond Selling Price

Mason Company

Investors

Bonds Issued at a Discount

7-19

Mason Company issues bonds on January 1, 2011.Principal = $100,000Stated Interest Rate = 9%Interest Date = 12/31Maturity Date = Dec. 31, 2015 (5 years)

Mason Company issues bonds on January 1, 2011.Principal = $100,000Stated Interest Rate = 9%Interest Date = 12/31Maturity Date = Dec. 31, 2015 (5 years)

Bond Certificateat Face Value

Bond Certificateat Face Value

Bond Selling Price

Mason Company

Investors

$100,000 face issued at 105:

Bonds Payable $100,000

Plus: Premium on Bonds Payable 5,000

Carrying Value $ 105,000

$100,000 face issued at 105:

Bonds Payable $100,000

Plus: Premium on Bonds Payable 5,000

Carrying Value $ 105,000

Bond Certificateat Face Value

Bond Certificateat Face Value

Bond Selling Price

Mason Company

Investors

Bonds Issued at a Premium

7-20

Current Versus Noncurrent

Current assets are expected to be converted to cash or consumed within one year or an

operating cycle, whichever is longer. Current assets include:• Cash

• Marketable Securities• Accounts Receivable• Short-Term Notes Receivable• Interest Receivable• Inventory• Supplies• Prepaid Items

• Cash• Marketable Securities• Accounts Receivable• Short-Term Notes Receivable• Interest Receivable• Inventory• Supplies• Prepaid Items

7-21

Current Versus Noncurrent

Current liabilities are due within one year or an operating cycle, whichever is longer. Current

liabilities, also called short-term liabilities, include:

• Accounts Payable• Short-Term Notes Payable• Wages Payable• Taxes Payable• Interest Payable

• Accounts Payable• Short-Term Notes Payable• Wages Payable• Taxes Payable• Interest Payable

7-22

End of Chapter Seven

7-23