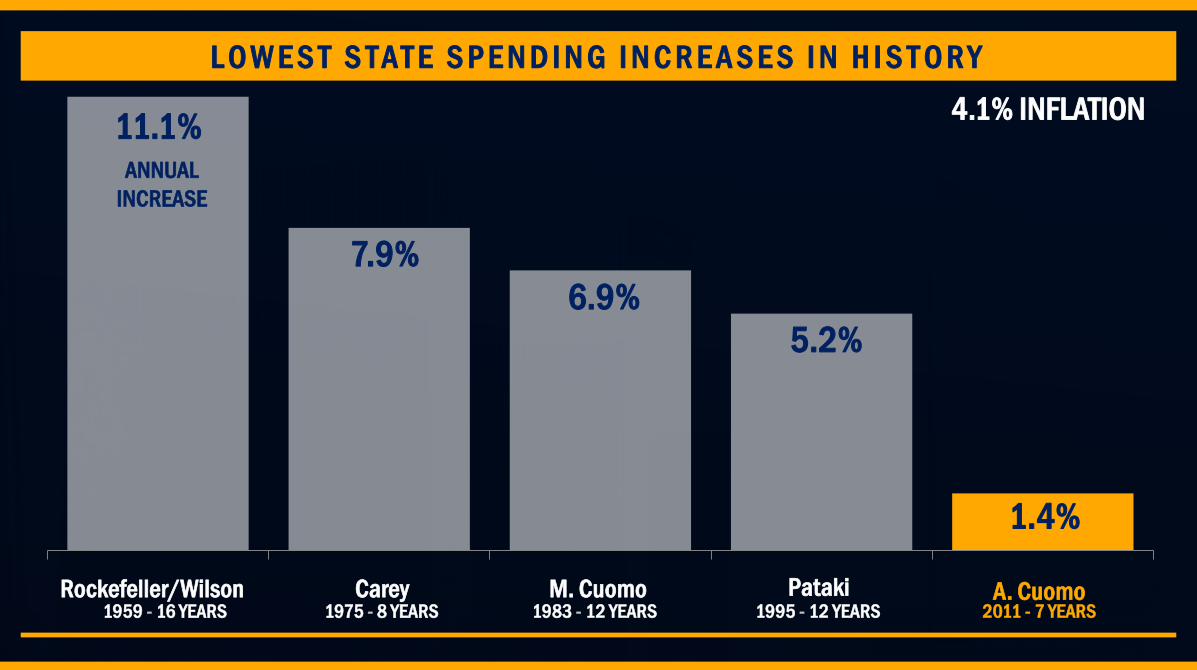

Robert F. Mujica, Jr. · 11.1% 6.9% 7.9% 1.4% carey m. cuomo pataki a. cuomo 1983 - 12 years 1995 -...

53

Robert F. Mujica, Jr. NEW YORK STATE DIVISION OF THE BUDGET

Transcript of Robert F. Mujica, Jr. · 11.1% 6.9% 7.9% 1.4% carey m. cuomo pataki a. cuomo 1983 - 12 years 1995 -...

Robert F. Mujica, Jr. NEW YORK STATE DIVISION OF THE BUDGET

11.1%

6.9%

7.9%

1.4%

Pataki M. Cuomo Carey A. Cuomo 1983 - 12 YEARS 1995 - 12 YEARS 2011 - 7 YEARS

ANNUAL

INCREASE

4.1% INFLATION

L O W E S T S T A T E S P E N D I N G I N C R E A S E S I N H I S T O R Y

Rockefeller/Wilson 1959 - 16 YEARS 1975 - 8 YEARS

5.2%

Because we controlled spending,

we were able to lower taxes.

Today every New Yorker pays a lower

tax rate than they did seven years ago.

• Corporate tax rates lowest since 1968

• Manufacturing tax rates lowest since 1917

• And middle class tax cut for the New Yorkers who

need it the most -- lowest since 1947

This year, we are giving the

average New Yorker a tax cut of $250.

When fully phased in,

the savings will rise to $698.

Our statewide unemployment is down

from 8.3% 7 years ago to 4.6% today.

-3.7 6.1%

-3.0 4.4%

-3.0 4.5%

-3.0 4.4% -5.2

4.0%

-2.9 5.5%

-2.8 5.1%

-3.2 5.1% -3.0

5.3% -2.8 5.3%

DEC. 2010 - 17

UNEMPLOYMENT DOWN ACROSS THE STATE

FY 2019 Executive Budget

By the numbers

NUMBERS OVERVIEW

General Fund Budget Gap – FY 2019

$4.4 billion

Baseline Spending Growth – 4.8%

$4.7 billion

Spending Reductions to Stay at 2%

$2.7 billion

Budget Gap Remaining After 2%

$1.7 billion

Surpluses/Gaps at 2 Percent Growth Dollars in millions

SURPLUSES/GAPS AT 2 PERCENT GROWTH

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

530

1,737

187

1,079

678

388

243 252

$78B

$64B

$70B

JAN-18

JAN-17

JAN-16

FY16 FY17 FY18 FY19

TWO YEARS OF REVENUE REDUCTIONS

ELIMINATES THE 2019 BUDGET GAP

• $2.7 billion in spending reductions

• $0.7 billion in new resources

• $1.0 billion in revenue actions

• Holds spending increase to 1.9% - lower than

2% growth cap

PROPOSED SENDING AT 1.9 PERCENT

$98.1

$102.8

$100.0

$90

$105

Current Year Estimate 2019 "Current Services"Before Actions

2019 Proposed Spending

+4.8%

$2.7 Billion

Spending Reduction

Needed to Achieve

2% Growth

$1.9 Billion

Proposed Spending

+1.9%

$ in billions

SUMMARY: STATE OPERATING & ALL FUNDS

FY 2018 FY 2019

Proposed

Change Percent

Change

State Operating $98.1B $100.0B $1.9B 1.9%

All Funds $164.4B $168.2B $3.8B 2.3%

Excludes extraordinary Federal aid and storm disaster relief.

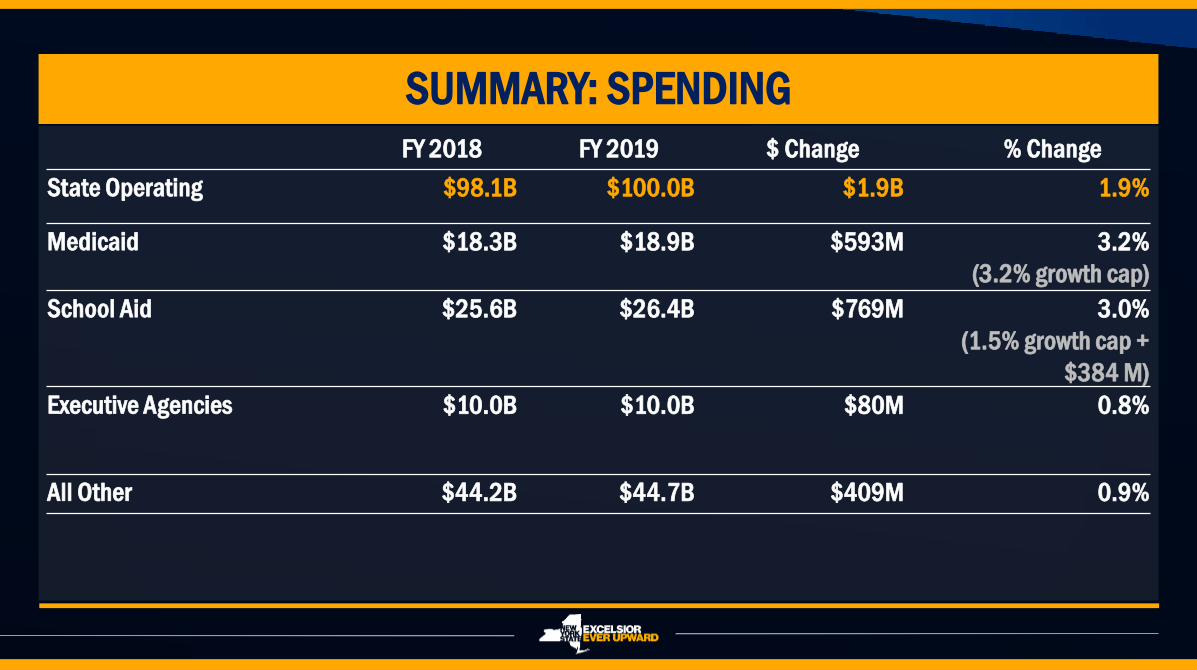

SUMMARY: SPENDING

FY 2018 FY 2019 $ Change % Change

State Operating $98.1B $100.0B $1.9B 1.9%

Medicaid $18.3B $18.9B $593M 3.2%

(3.2% growth cap)

School Aid $25.6B $26.4B $769M 3.0%

(1.5% growth cap +

$384 M)

Executive Agencies $10.0B $10.0B $80M 0.8%

All Other $44.2B $44.7B $409M 0.9%

WHERE IT GOES

ALL OTHER

23%

DEBT SERVICE

6%

OPERATIONS

27%

MEDICAID

19%

SCHOOL AID

25%

HOW IT GROWS

ALL OTHER

1.0%

DEBT SERVICE

0.3%

OPERATIONS

0.8%

MEDICAID

3.2%

SCHOOL AID

3.0%

CLOSING THE GAP

• Opioid Epidemic Surcharge: 2 cents per milligram

to fund the Opioid Prevention and Rehabilitation Fund.

• Health Tax on Vapor Products: 10 cents per fluid milliliter on vapor

products at the distributor level.

• Internet Fairness Conformity Tax: apply tax policy uniformly to online sellers by

requiring marketplace providers to collect a sales tax.

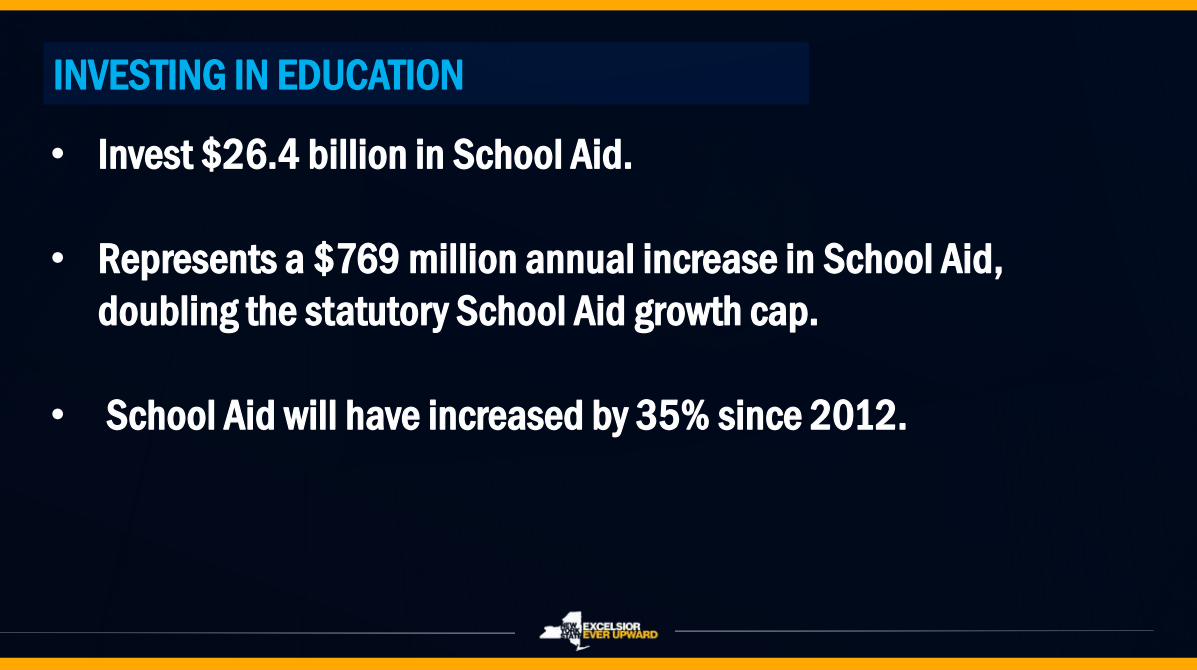

INVESTING IN EDUCATION

• Invest $26.4 billion in School Aid.

• Represents a $769 million annual increase in School Aid,

doubling the statutory School Aid growth cap.

• School Aid will have increased by 35% since 2012.

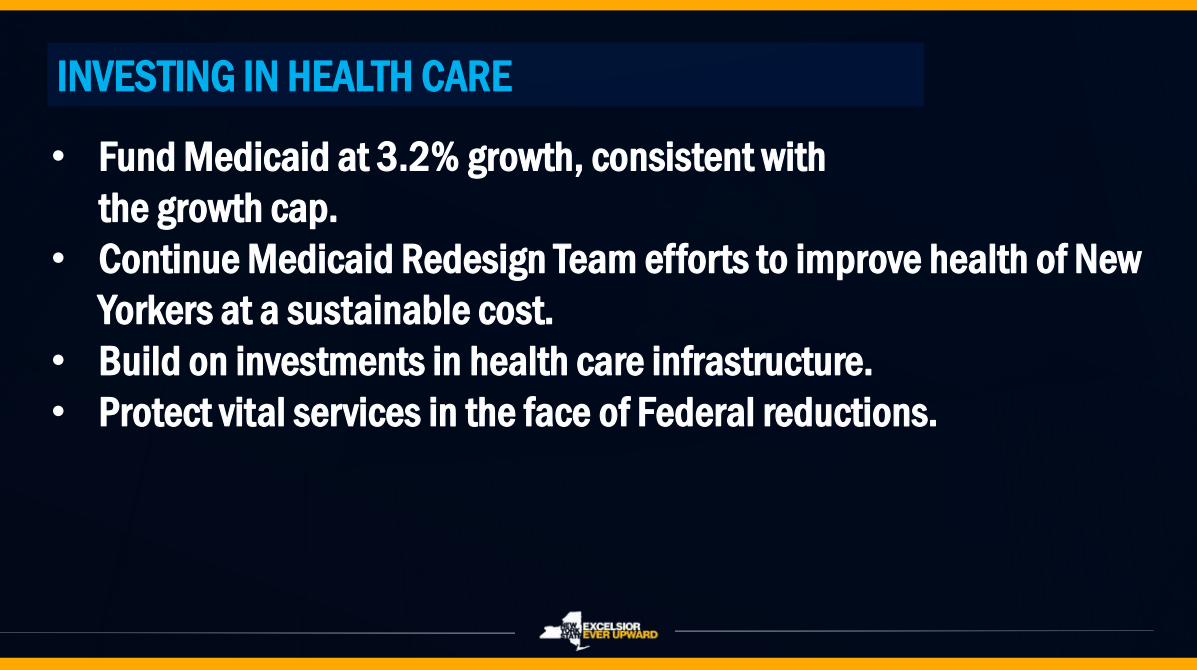

INVESTING IN HEALTH CARE

• Fund Medicaid at 3.2% growth, consistent with

the growth cap.

• Continue Medicaid Redesign Team efforts to improve health of New

Yorkers at a sustainable cost.

• Build on investments in health care infrastructure.

• Protect vital services in the face of Federal reductions.

STATEWIDE INVESTMENTS

MTA Capital Plan $29.9 billion Over 5 Years

Roads and Bridges Capital Plan $29.2 billion Over 5 Years

Subway Action Plan $836 million Over 2 Years

Housing and Homelessness $20 billion Over 5 Years

Clean Water Infrastructure Act $2.5 billion Over 5 Years

REDC Round VIII $750 million FY 2019

Upstate Revitalization Fund $1.7 billion Over 5 Years

Downtown Revitalization Initiative $100 million FY 2019

Environmental Protection Fund $300 million FY 2019

State Parks $90 million FY 2019

I ❤ NY/Taste NY $74 million FY 2019

Opioid Epidemic $200 million FY 2019

Raise the Age $100 million FY 2019

State Debt Outstanding (Millions of Dollars)

56,372 55,692 55,165 54,190

52,105 50,709

51,970

47,00048,00049,00050,00051,00052,00053,00054,00055,00056,00057,000

SY 2012 SY 2013 SY 2014 SY 2015 SY 2016 SY 2017 SY 2018

State debt declined for 5 consecutive years and is projected

to continue to be below when the Governor took office

AFFORDABLE DEBT LEVELS

State debt as percent of NYS personal income

Projected

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

19

69

19

71

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

20

21

20

23

LOWEST DEBT BURDEN SINCE THE 1960s

The main issue for 30-Day Amendments is to

Protect New Yorkers from the Federal

limitations on SALT

NY SENDS THE MOST TO WASHINGTON

NY Contributes more to the Federal Government than any other state – net $48B.

We are the #1 donor state.

Federal bill has New Yorkers picking up an even larger share.

Sen. Daniel Patrick Moynihan annually

published a report called the fisc on the

imbalance of finances that afflicts New

York

The cap on SALT deductions costs New

York

$14.3 billion.

Some New Yorkers have suggested that the Federal

changes will be good for them or their communities.

Elimination of full SALT harms

every New Yorker

W hy i s S A LT b a d f o r A L L N e w Yo r ker s ?

Re a s o n # 1 :

I t ’ s a s t a t e wi de p r o bl e m

A c c o r d i n g t o t h e S t a t e C o m p t r o l l e r, 5 2 o f N e w Yo r k ’ s

6 2 c o u n t i e s h a v e a v e r a g e S A LT a b o v e $ 10 , 0 0 0 . S A LT

i m p a c t s p e o p l e i n e v e r y c o m m u n i t y.

W hy i s S A LT b a d f o r A L L N e w Yo r ker s ?

Re a s o n # 2 :

St a t e wid e, a v e r a g e S A LT i s $ 2 2 ,16 8

A c c o r d i n g t o t h e S t a t e C o m p t r o l l e r, c i t i n g I R S d a t a ,

t h e a v e r a g e N e w Yo r k t a x p a y e r h a s S A LT d e d u c t i o n s

t h a t a r e m o r e t h a n t w i c e t h e $ 10 , 0 0 0 c a p .

W hy i s S A LT b a d f o r A L L N e w Yo r ker s ?

Re a s o n # 3 :

N e w Yo r k i s h a s a h i g h e r p e r c e n t a g e o f “ l o s er s ” t h a n

a ny o t h er s t a t e.

N e w Yo r k h a s t h e l a r g e s t p e r c e n t a g e o f t a x p a y e r s g e t t i n g a

t a x h i k e o f a n y s t a t e .

S o u r c e : I n s t i t u t e o f T a x a t i o n a n d E c o n o m i c P o l i c y

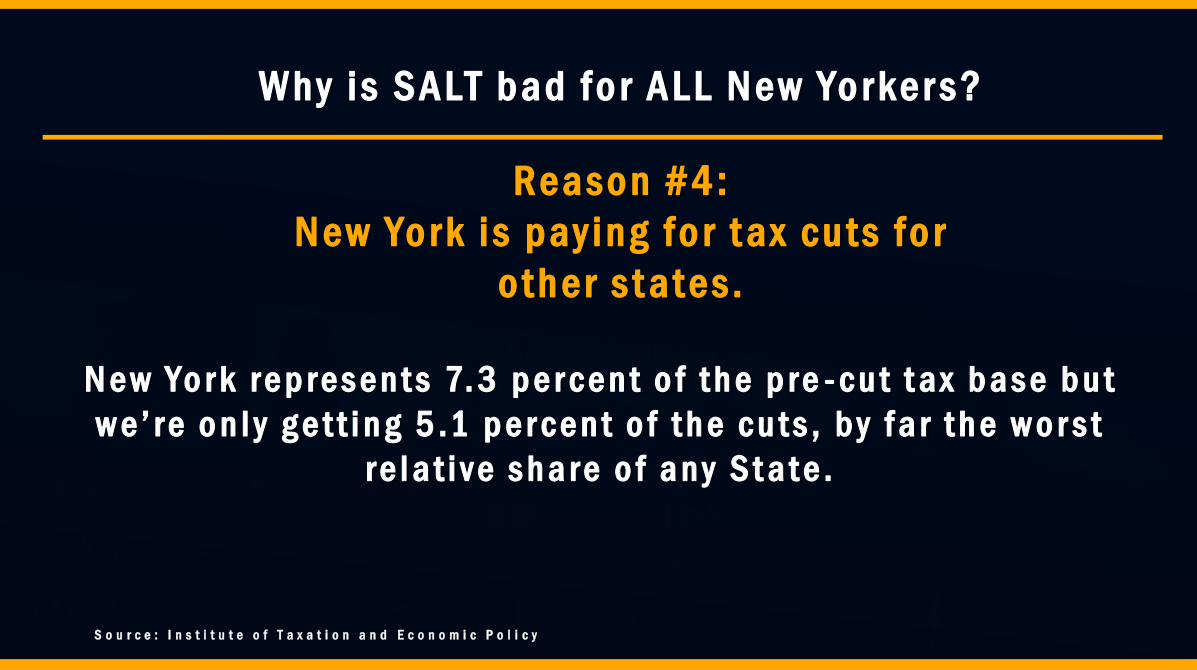

W hy i s S A LT b a d f o r A L L N e w Yo r ker s ?

Re a s on # 4 :

N e w Yo r k i s p ay ing f o r t a x c u t s f o r

o t h er s t a t e s .

N e w Yo r k r e p r e s e n t s 7. 3 p e r c e n t o f t h e p r e - c u t t a x b a s e b u t

w e ’ r e o n l y g e t t i n g 5 .1 p e r c e n t o f t h e c u t s , b y f a r t h e w o r s t

r e l a t i v e s h a r e o f a n y S t a t e .

S o u r c e : I n s t i t u t e o f T a x a t i o n a n d E c o n o m i c P o l i c y

Re a s o n # 5 :

F o r m o s t t a x payer s r e c e i v in g a f e d e r a l t a x c u t , i t ’ s

t e m p o r a r y.

T h e b e n e f i t s t h a t d o e x i s t f o r m i d d l e c l a s s t a x p a y e r s a r e

t e m p o r a r y, e x p i r i n g i n 2 0 2 5 . B y 2 0 27 , 5 3 p e r c e n t o f

t a x p a y e r s w i l l a c t u a l l y p a y m o r e t a x t h a n b e f o r e t h e l a w.

W hy i s S A LT b a d f o r A L L N e w Yo r ker s ?

S o u r c e : T a x P o l i c y C e n t e r

Re a s o n # 6 :

Re l a t i v e t o t h e w e a l t hy, m i d d l e c l a s s t a x payer s a r e

g e t t in g p o o r e r.

T h e l a r g e s t c u t s a r e g o i n g t o h i g h - i n c o m e t a x p a y e r s . A s a

s h a r e o f t o t a l w e a l t h , m i d d l e c l a s s t a x p a y e r s – e v e n t h o s e

g e t t i n g a t a x c u t – a r e g e t t i n g p o o r e r b e c a u s e o f t h e m o d e s t

s i z e o f t h e i r c u t .

W hy i s S A LT b a d f o r A L L N e w Yo r ker s ?

Re a s o n # 7:

S A LT i s d e c i m a t in g m i d d le c l a s s h o m e v a l u e s –

s t e a l in g a m a s s ed w e a l t h .

H o m e v a l u e s a r e t h e p r i n c i p l e s o u r c e o f w e a l t h f o r o u r

m i d d l e c l a s s . A c c o r d i n g t o M o o d y ’ s , h o m e v a l u e s i n m a n y

N e w Yo r k c o u n t i e s w i l l d r o p b y a s m u c h a s 10 p e r c e n t .

A l o n g w i t h N e w J e r s e y, t h i s i s t h e l a r g e s t i m p a c t o f a n y

S t a t e .

W hy i s S A LT b a d f o r A L L N e w Yo r ker s ?

Re a s on # 8 :

S A LT t h r eat ens t h e s t a t e b u d g e t .

S A LT e n c o u r a g e s h i g h - i n c o m e N e w Yo r k e r s t o m o v e t o o t h e r

s t a t e s . I f e v e n a s m a l l n u m b e r o f h i g h - i n c o m e t a x p a y e r s

l e a v e t h e s t a t e i t w o u l d c r i p p l e o u r r e v e n u e s , l e a d i n g t o

l a r g e b u d g e t d e f i c i t s .

W hy i s S A LT b a d f o r A L L N e w Yo r ker s ?

Re a s o n # 9 :

I t t h r e a t e n s p r o g r a ms p e o p le d e p e n d o n .

B y s h r i n k i n g t h e S t a t e t a x b a s e , S A LT w i l l i m p a c t f u n d i n g f o r

m a n y p r o g r a m s t h a t N e w Yo r k e r s d e p e n d o n , i n c l u d i n g

S c h o o l A i d , M e d i c a i d a n d a w i d e r a n g e o f s e r v i c e s .

W hy i s S A LT b a d f o r A L L N e w Yo r ker s ?

Re a s o n # 10 :

I t t h r e a t e n s j o b s by m a k i n g N e w Yo r k l e s s c o m pe t i t iv e.

C a p p i n g S A LT m a k e s N Y S a n d N Y C r e l a t i v e l y m o r e e x p e n s i v e

p l a c e s t o l i v e , e f f e c t i v e l y i n c r e a s i n g t h e S t a t e a n d C i t y

i n c o m e t a x r a t e . A n y o n e ’ s j o b c o u l d b e t i e d t o s o m e o n e w h o

i s n o w r e c o n s i d e r i n g N e w Yo r k .

W hy i s S A LT b a d f o r A L L N e w Yo r ker s ?

30-Day Amendments to the FY

2019 Executive Budget

TODAY

30-DAY AMENDMENT

Create a new employer compensation

expense tax

EMPLOYER COMPENSATION EXPENSE TAX

• Federal Law limits deductions for individuals – employer side taxes on

payroll remain deductible.

• To maximize deductibility, provide an option for employers to protect

their employees.

EMPLOYER COMPENSATION EXPENSE TAX

• Employers could opt-in, annually, with the first enrollment deadline

October 1, 2018.

• Employers would be subject to a 5% tax on all annual payroll expenses

in excess of $40,000 per employee.

• Program is phased in over three years beginning on January 1, 2019.

• 1.5% in first year, 3% in second year, 5% in third year.

EMPLOYER COMPENSATION EXPENSE TAX

• Employees receive a tax cut on their wages via new tax credit to

ensure no decline in take-home pay.

• Progressive personal income tax system remains in place.

• Designed to be revenue neutral for the state.

• Gives employers the opportunity to reduce their employees’ federal

taxes while keeping overall business expenses unchanged.

It costs employers nothing.

Their employees are protected from federal

tax increases.

30-DAY AMENDMENT

Expand Charitable Contribution

Options

EXPAND CHARITABLE CONTRIBUTION OPTIONS

• Legislation creates two new Charitable Contribution Funds to accept

donations to fund health care and education programs.

• Taxpayers who itemize deductions could claim these charitable

contributions as deductions on their Federal and State tax returns.

• Any taxpayer making a donation could also claim a State tax credit equal

to 85 percent of the donation amount for the tax year after the donation

is made.

Contributions offer federal deduction

and an offsetting state tax credit

PUBLIC

EDUCATION FUND HEALTHCARE FUND

CHARITABLE CONTRIBUTIONS

TO BENEFIT NEW YORKERS

EXPAND CHARITABLE CONTRIBUTION OPTIONS

LOCAL OPTION:

• The amendment authorizes school districts and local governments to

create charitable funds for education and health care, respectively.

• Donations to these funds would provide a reduction in local property tax

bills (via a local credit) equal to a percent of the donation.

30-DAY AMENDMENT

Decouple from

Federal Tax Law

DECOUPLE FROM FEDERAL TAX LAW

Avoid more than $1.5 billion in State tax increases brought solely by increases

in Federal taxes.

• Decouple from the Federal $10,000 cap SALT ($441M).

• Decouple from other Federal deduction changes ($269M).

• Decouple to maintain the State single filer standard deduction. Without

this change, single filers would not be able to take the standard deduction

on their State return ($840M).

Robert F. Mujica, Jr. NEW YORK STATE DIVISION OF THE BUDGET

![Uruguay election: How will next president stack up …Mujica],” says Daniel Buquet, a political scientist here. “He is unrepeatable.” Mujica, popularly known as Pepe, has an](https://static.fdocuments.in/doc/165x107/5ece149076ae9231b56f4641/uruguay-election-how-will-next-president-stack-up-mujicaa-says-daniel-buquet.jpg)