ROADSHOW - Danske Bank

57

Financial results for Q3 2012 New strategy 30 October 2012 ROADSHOW

Transcript of ROADSHOW - Danske Bank

Financial results for Q3 2012 New strategy

30 October 2012

ROADSHOW

2

Financial results for Q3 2012 New strategy

Agenda

Financial results

Capital, funding and liquidity

Outlook for 2012

Q&A session

Appendix: Trends in focus areas & business units

New strategy

3

Financial results for Q3 2012 New strategy

3

New Standards

for Danske Bank

4

Financial results for Q3 2012 New strategy

Recognised as the most

trusted financial partner

New vision for 2015

4

Setting new standards

in financial services

New mission

5

Financial results for Q3 2012 New strategy

Lithuania

Strategic units

• Danica

• Danske Capital

• Nordania

Estonia

Latvia

Finland

Nordic relationship bank with expertise

Sweden

Norway

Northern Ireland

Denmark

Ireland

6

Financial results for Q3 2012 New strategy

The most trusted financial partner

Customer satisfaction 2015

We want to be in the top two in customer satisfaction among our prioritised customer segments

Financial results 2015

We want to be in the top three among Nordic peers measured by return on equity (ROE)

6

7

Financial results for Q3 2012 New strategy

Financial targets

ROE 3.8% Above 12% in 2015

Dividend payments

Nil for 2012 About 40% of annual net profit, but lower until we have reached capital and rating targets

Core tier 1 Total capital Liquidity

12.7% Minimum 13% by the end of 2013 19.4% Minimum 17% by the end of 2013 Meet EU 2015 LCR requirement by the end of 2012

Ratings S&P/Moody’s/Fitch Improve ratings at least one notch A-/Baa1/A

Nominal cost FTE C/I ratio

2012 guidance at 27bn Below DKK 26 bn in 2015 20,651 To be reduced by 2,000 in 2013-2015 55% Below 48% in 2015

Q3 2012 Ambitions

8

Financial results for Q3 2012 New strategy

ROE above 12% in 2015

ROE development from 2012 to 2015

2015E (after tax) ROE above 12% in 2015

Capital, regulation, inflation, tax 6–7% points

Short term rates (pre-tax) 4–5% points

Declining loan losses (pre-tax) 5–6% points

Management actions (pre-tax) 4–6% points

9M 2012 annualised (after tax) 3.8%

9

Financial results for Q3 2012 New strategy

Financial results: 9M 2012 shows strong improvement, Q3 showed stable development Income statement & key figures (DKK m) Key points for the first nine months

• Strong improvement in net profit

• Improvement driven by strong income growth

• Expenses flat despite restructuring charges

• Impairments higher than 9M 2011 owing to deterioration of the macroeconomic climate

Key points Q3

• Flat net interest income despite lower short-term rates

• Solid trading income within guidance

• Declining expenses, mainly seasonal effect

• Lower impairments, drop in Denmark but increase in CIB

• Lower RWA and higher CT1 ratio

9M 2012 9M 2011 Index Q3 2012 Q2 2012 Index

Net interest income 18,588 17,355 107 6,198 6,218 100

Net fee income 6,129 6,080 101 2,116 2,026 104

Net trading income 7,469 5,687 131 1,785 2,462 73

Other income 2,323 2,799 83 689 846 81

Net income from insurance business 1,310 -407 - 427 699 61

Total income 35,819 31,514 114 11,215 12,251 92

Expenses 19,598 19,528 100 6,116 6,632 92

Profit bef. loan imp. charges 16,221 11,986 135 5,099 5,619 91

Loan impairment charges 9,910 8,396 118 2,879 3,109 93

Profit before tax 6,311 3,590 176 2,220 2,510 88

Tax 2,708 2,067 131 903 1,007 90

Net profit 3,603 1,523 237 1,317 1,503 88

Net profit ex non-core Ireland 7,216 - - 2,645 2,840 93

Return on avg. shareholders' equity (%) 3.8 1.7 222 4.1 4.7 87

C/I ratio (%) 54.7 62.0 88 54.5 54.1 101

Core tier 1 capital ratio (%) 12.7 11.8 108 12.7 12.1 105

Risk-weighted assets (bn) 851 895 95 851 893 95

Total loans ex repos (bn) 1,700 1,694 100 1,700 1,704 100

Deposits (ex repos) & RD bonds (bn) 1,471 1,505 98 1,471 1,460 101

Total assets (bn) 3,599 3,381 106 3,599 3,481 103

Loan loss ratio (bp) 68 58 117 56 62 90

10

Financial results for Q3 2012 New strategy

Net interest income: Headwind from lower short-term rates neutralised by higher lending margins Quarterly net interest income (DKK m) Net interest income drivers

Positive

• Increased lending rates, mainly in Denmark

Negative

• Low and declining central bank rates

Sensitivity

Short-term interest rate sensitivity across all currencies

+ 25 bp = DKK +800 m

– 25 bp = DKK – 800 m

Q312

6,218 6,172

6,198

Q212

6,182

Q112 Q411 Q311

6,016

11

Financial results for Q3 2012 New strategy

Net fee income: Growth in financing fees because of repayment of state-guaranteed bonds Quarterly net fee income (DKK m)

640

Q312 Q112

688

1,386

2,026 2,116

Q212

659

1,457

1,987

1,299

Q411

2,218

719

1,499

Q311

1,938

564

1,374

Portfolio fees

Activity fees

Fee income drivers

• Activity levels remain stable

• Increase in portfolio-based fees driven by repayment of bonds issued with state guarantee (quarterly effect of DKK 70 m)

• Activity-based fees stable despite summer season

Fee income split, Q3 2012 (%)

20

71

9

Banking Activities ex CIB

CIB

Danske Capital

12

Financial results for Q3 2012 New strategy

Quarterly trading income (DKK m)

Trading income: Q3 2012 within expectations, strong improvement over Q3 2011

267

Q312

1,785

Q212

2,462

Q112

3,222

Q411

1,638

Q311

• Solid trading income, mainly from bond and derivatives activities

• Q3 includes DKK 124 m realised loss from AFS portfolio off set in total income

Interest rate sensitivity (Group) • 1 pp increase in yield curve: DKK -316 m

Trading income drivers

Trading income split, Q3 2012 (%)

42

95

43

Equities

Bonds & DCM

Repos & derivatives

FX & money market

13

Financial results for Q3 2012 New strategy

Quarterly insurance income (DKK m)

Insurance: Result closer to normal, boosted by good investment returns

427

699

184

976

-735

Q212 Q411 Q112 Q311 Q312

Key points

• Risk allowance booked for three out of four groups

• Strong result for unit-linked products

• Danish and German interest rate spread declined in Q3, increasing liabilities by DKK 700 m

• Shadow account of DKK 1.3 bn

• Expect risk allowance for three groups for the full year

• Premiums declining because of intensified price competition in Denmark and Sweden

14

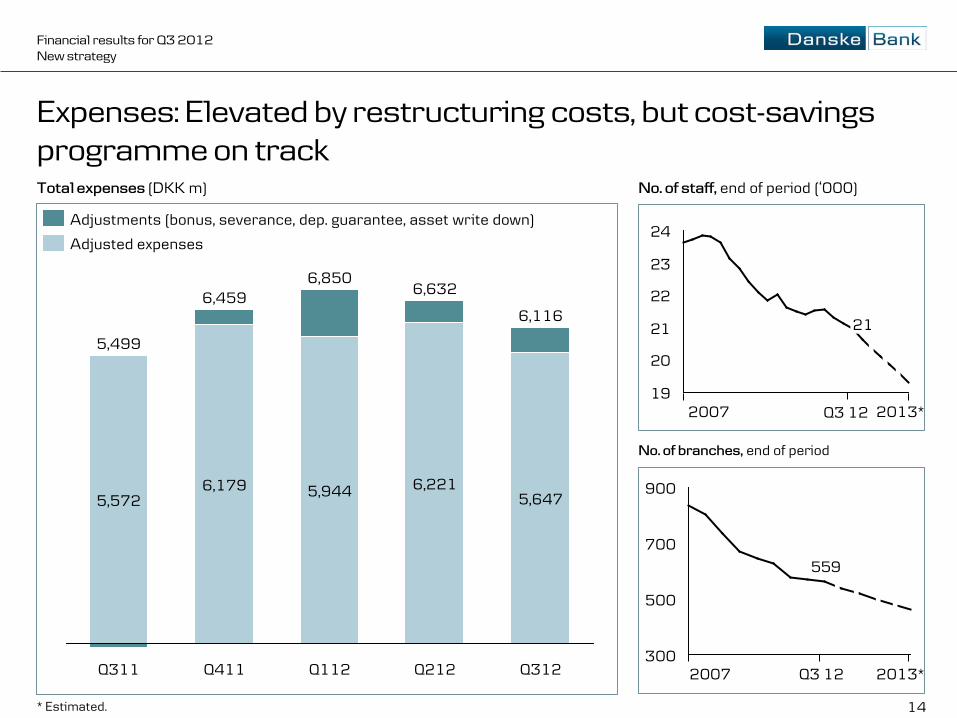

Financial results for Q3 2012 New strategy

Expenses: Elevated by restructuring costs, but cost-savings programme on track Total expenses (DKK m)

No. of staff, end of period (‘000)

No. of branches, end of period

559

900

700

500

300

19

20

21

22

23

24

21

Q312

6,116

5,647

Q212

6,632

6,221

Q112

6,850

5,944

Q411

6,459

6,179

Q311

5,499

5,572

2007

2007 2013* Q3 12

* Estimated.

2013*

Adjustments (bonus, severance, dep. guarantee, asset write down)

Adjusted expenses

Q3 12

15

Financial results for Q3 2012 New strategy

Impairments by customer segment (DKK bn)

Impairments: Declining trend continues, mainly among personal customers and financials

Impairment drivers

Q212

3.1

Q112

3.9

Q411

4.8

Q311

2.8

Q312

2.9

Personal

Large corp.

SMEs

Financials • Decline in impairments of DKK 230 m in Q3

• Drop in impairments in Denmark and Finland; increase at CIB

• Lower impairments for personal and financial customers

• Some increases for large corporates and SMEs

• Q3 impairments related primarily to

• CRE in Non-core Ireland

• Shipping in CIB

• Impaired loans declined because of write-offs and new definition, which excludes loans with no impairments

16

Financial results for Q3 2012 New strategy

Impairments (DKK m)

Impairments: Lower impairments in Denmark, Finland and Northern Ireland

Loan loss ratio (bp, annualised)

960

260

206

1,374

-91

84

7

61

151

-138

39

34

44

48

Group 2,879 3,109

Non-core Ireland 1,350

CIB 630

Baltics

Ireland

Northern Ireland 214

Norway

Sweden

Finland

Denmark 737 Q312

Q212 Q312 Q212

Denmark 30 40

Finland 12 39

Sweden 9 13

Norway 9 2

Northern Ireland 186 225

Ireland 65 137

Baltics -303 -195

CIB 189 63

Non-core Ireland 2,477 2,329

Group 56 62

17

Financial results for Q3 2012 New strategy

Capital: Earnings, tier 2 issue and sale of securitisation assets boost capital ratios

Capital drivers Capital ratios, under CRD/Basel II (%)

---- Solvency need

17.0

19.4

Q4 11

11.8

16.0

17.9

Q3 12

12.7

Core tier 1

Tier 1 (including state hybrid)

Total capital

----------- 10.8 ----------

• State hybrid represents 2.8 percentage points of the tier 1 and total capital ratios

• Issuance of tier 2 capital in September 2012 raised total capital ratio by 0.7 of a percentage point

• Risk Adjusted Capital (RAC) ratio from S&P rose from 6.3% YE-11 to estimated 6.9%*

RWA (DKK bn)

13

29

851

Q2 12

Market risk

893

Securitisation etc.

Q3 12

* Assuming unchanged S&P RWA.

18

Financial results for Q3 2012 New strategy

18

Details on the equity issue 5-years senior bond spread vs. peers; 6M ASW-Spread (bp)*

Raised DKK 7.1 bn through an accelerated book-building; significant tightening in spreads since September Amount: DKK 7,150 m

Price: DKK 93 per new share

Method: Accelerated book-building without pre-emption rights to current shareholders

Why: To accelerate rating improvements and achievement of our capital targets, strengthen our funding position and better align us with our Nordic peers

Outcome: A outlook change from Stable to Positive from S&P and a positive reaction from Moody’s

New shares: 76.9 m shares

Total number of shares: 1,008.6 m shares

200

150

100

50

0 Jun

2012

-96bp

Jul 2012

Aug 2012

Sep 2012

Oct 2012

Nov 2012

* Outstanding senior benchmark issues with maturity in February 2017 (SHB in July 2017).

Handelsbanken

Danske Bank Nordea

Swedbank

29/10 -5/11: -21bp

19

Financial results for Q3 2012 New strategy

Deposits and funding: Small improvement in deposits after rating downgrade, 2013 funding plan started

Long term funding (DKK bn)

Long term funding Deposits, end of period (DKK bn)

73

2013

40-70

2012*

85

2011

97 97 8659 52

Q3 12

743

623

68

Q2 12

736

620

57

Q1 12

774

616

72

Q4 11

795

629

69

Q3 11

789

624

68

BA, other

CIB

Markets

* End of Q3 2012.

• Funding raised by end of Q3 2012:

• 43 % covered bonds

• 48 % senior debt

• 9 % tier 2 capital

• DKK 25 bn of 2013 plan pre-funded

• Funding plan for 2013 reflects large redemptions in 2014

• Goal: LCR compliant end 2012

2013 pre-funded

2013 funding plan

Completed

20

Financial results for Q3 2012 New strategy

Liquidity: Strong liquidity buffer despite deposit outflow

Bond portfolio rating, DKK 502 bn (%)

Key points

3 mos 6 mos 9 mos 12 mos

300

200

100

0

Q3 2012 Q2 2012 Q3 2011

12-month liquidity*, end of period (DKK bn)

84

5 12 Other

AAA

≥A

• 12-month liquidity of more than DKK 150 bn

• 12-month liquidity curve remains positive for more than 2½ years

• Eligible liquidity buffer of more than DKK 300 bn

* Moody’s Financial Strength. Main assumptions: No access to capital markets; no refinancing of debt to credit institutions, issued bonds or subordinated capital; moderate reduction of business activities.

21

Financial results for Q3 2012 New strategy

Outlook for 2012 as a whole: Earnings remain low but are moving in the right direction

Macro Economic growth to remain low in most markets

Expenses Expected to increase 4% above 2011 level, including restructuring costs

Loan losses In line with 2011 level, around DKK 13 bn

Net profit Results remain low but represent a step in the right direction

Dividend No dividend payment is expected for 2012

Income Improvement of income is an ongoing process

22

Financial results for Q3 2012 New strategy

www.danskebank.com/ir

23

Financial results for Q3 2012 New strategy

Appendix

Macro 24

NII and margin developments 26

Credit 31

Funding and rating 40

Business units 44

Expenses 29

Tax 30

24

Financial results for Q3 2012 New strategy

Macro trends

Bankruptcies (index 1996 = 100)

Property prices, Nordic countries (index 1996 = 100) Rating upgrades*, corporates, 12-month rolling average (%)

Business confidence indicator (index 1996 = 100)

400

300

200

100

2012 2008 2004 2000 1996

Sweden Norway Finland Denmark

60

80

100

120

140

160

2012 2008 2004 2000 1996

Denmark Finland Sweden

100

50

0 2012 2011 2010 2009

CIB Finland Sweden Norway Denmark

Upgrades > downgrades

Downgrades > upgrades

100

200

300

400

2012 2008 2004 2000 1996

Finland Sweden Norway Denmark

* Relation between upgrades and total rating changes. From Q4 2011, ratings are affected by recalibration.

25

Financial results for Q3 2012 New strategy

Denmark: Stabilisation of house prices

Danish house price by region (%)

Unemployment and foreclosures (%)

* Leading indicator, based on monthly statistics from “home” (Danske Bank’s real estate agency) that cover about one-third of the market. Sources: Danske Research, Danmarks Statistik, Association of Danish Mortgage Banks, “home”, Adam, Danish Central Bank, Skat and own calculations.

0

5

10

0

200

400

600

2012 2004 1996

No. of forced sales (rha) Unemployment 10Y swap rate

16

14

12

10

80

70

60

50

40

30

Danish housing market (000’s)

House price per sq m (rhs) No. housing units for sale

2010 2009 2008 2007 2012

Affordability index, quarterly data from1985 – 2011

140

120

100

80

60

40

2012 2008 2004 2000 1996 1992 1988

Below average = cheap

Above average = expensive

Region Prices Change Change in Preview*

peaked since peak Q2 12 Q3 12

Copenhagen Q3 2006 -27,0 0,7

Zealand Q2 2007 -29,1 0,3

South Denmark Q2 2008 -18,8 -1,4

Central Jutland Q2 2008 -14,5 1,7

Northern Jutland Q1 2008 -12,2 1,6

Nationwide Q3 2007 -19,7 0,6 0,5

Mixed rate Fixed rate Average

26

Financial results for Q3 2012 New strategy

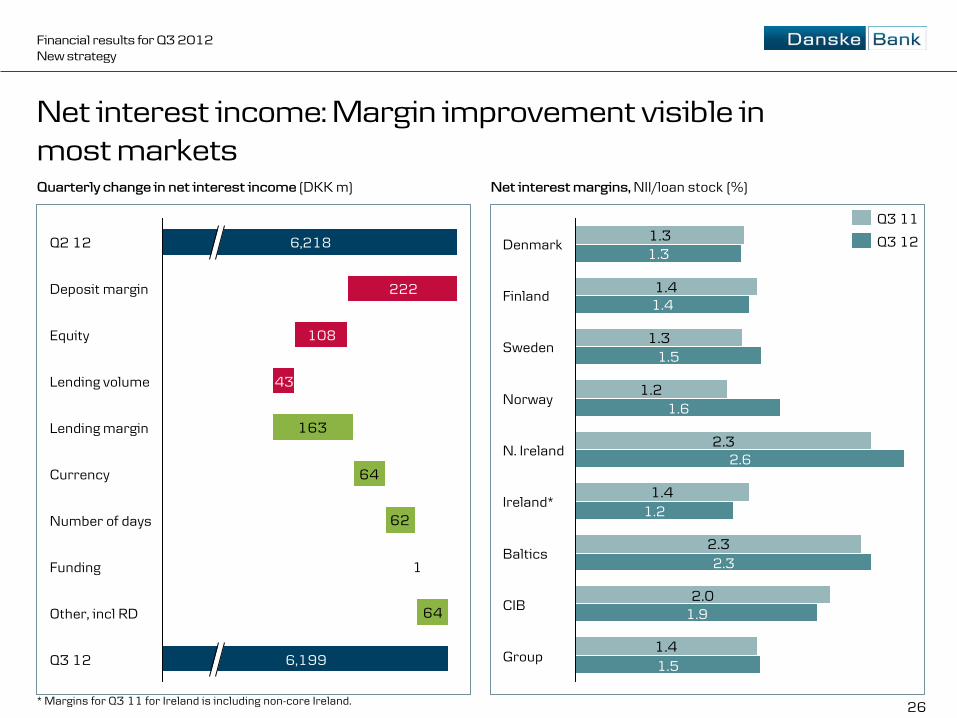

Net interest income: Margin improvement visible in most markets Quarterly change in net interest income (DKK m) Net interest margins, NII/loan stock (%)

1.3

1.4

1.3

1.2

2.3

1.4

2.3

2.0

1.4Group

1.5

CIB 1.9

Baltics 2.3

Ireland* 1.2

N. Ireland 2.6

Norway 1.6

Sweden

Finland 1.4

Denmark

1.5

1.3

Q3 11

Q3 12

163

64

62

64

Q3 12

Number of days

6,199

Other, incl RD

Currency

Funding

Lending margin

1

Lending volume 43

Equity 108

Deposit margin 222

Q2 12 6,218

* Margins for Q3 11 for Ireland is including non-core Ireland.

27

Financial results for Q3 2012 New strategy

* Includes Realkredit Danmark. ** Non-core Ireland is included in margins for Ireland prior to Q112.

Quarterly lending margins (%)

0.60 0.69

0.55

0.65

0.68 0.73

0.67 0.75

0.06 0.16

0.05 0.19

0.84 0.86

0.75 0.77

0.63 0.65

0.77 1.05

0.72 0.72

0.57 0.75

0.36 0.38

0.16 0.36

0.09 0.33

0.29 0.60

Q3 12

Q2 12

Q1 12

Q4 11

Quarterly deposit margins (%)

Higher lending margins are beginning to feed through

Denmark*

Sweden

Norway

Northern Ireland

Ireland**

Baltics

CIB

Finland

1.90 1.61

1.58

1.27 1.23

1.11 1.09

1.18 1.18 1.18

1.29

1.35 1.38

1.17

1.32 1.20 1.19

0.61

0.64

1.17

0.66

0.91 1.09

1.24

2.11

1.31

0.68

2.18 2.09

2.16

1.60

0.77

28

Financial results for Q3 2012 New strategy

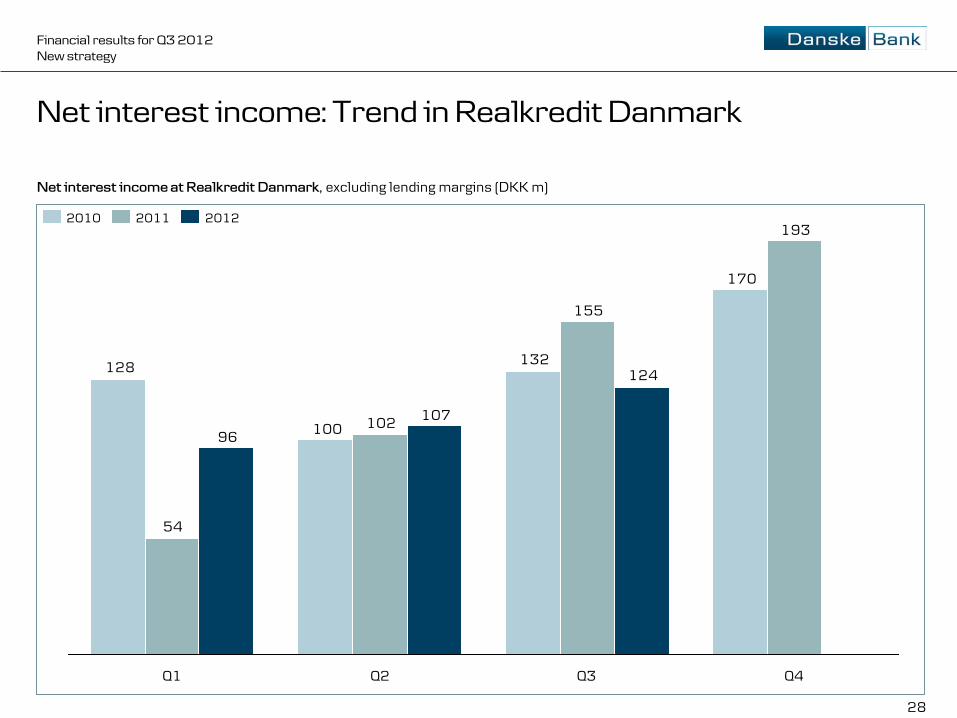

Net interest income: Trend in Realkredit Danmark

170

132

100

128

193

155

102

54

124

107

96

Q2 Q1 Q4 Q3

2011 2012 2010

Net interest income at Realkredit Danmark, excluding lending margins (DKK m)

29

Financial results for Q3 2012 New strategy

Expenses: Cost-savings programme on track

Expenses (DKK m) Quarterly change in expenses (DKK m)

Sales of leasing assets

Q3 12 6,116

Others

154

105

Holiday payments 257

Q2 12 6,632

Employees (number of FTEs)

20,651

21,32021,522

22,093

23,624

2011 2010 2008

-669

Q3 12 2009

9M 2012 9M 2011 Index Q3 2012 Q2 2012 Index

Expenses 19,598 19,528 100 6,116 6,632 92

Perf. based compensation 656 446 147 199 172 116

Severance payments etc. 590 209 282 227 303 75

Deposit guarantee scheme 77 962 - 43 -64 -

Asset write-down 463 113 410 0 0 -

Adjusted expenses 17,812 17,798 100 5,647 6,221 91

30

Financial results for Q3 2012 New strategy

Adjusted tax rate at 25%, but actual tax rate remains high owing to Ireland Actual and adjusted tax rates (DKK m)

* Permanent non-taxable differences are due primarily to value adjustments and the dividend from Nets. ** Taxes from previous years are due primarily to a reduction of the tax rate in the UK.

Q3 2012 Q2 2012 Q1 2012 Q4 2011 Q3 2011

Pre-tax profit 2,220 2,510 1,581 615 10

Pre-tax loss, Ireland core and non-core 1,374 1,616 1,371 1,524 1,490

Permanent non-taxable difference* -25 -93 34 -69 -8

Adjusted pre-tax profit, Group 3,569 4,034 2,986 2,070 1,492

Tax according to P&L 903 1,007 798 415 394

Taxes from previous years** -10 -22 -85 2 2

Adjusted tax 894 984 713 417 396

Adjusted tax rate 25.0% 24.4% 23.9% 20.1% 26.5%

Actual tax rate 40.7% 40.1% 50.5% 67.5% NM

31

Financial results for Q3 2012 New strategy

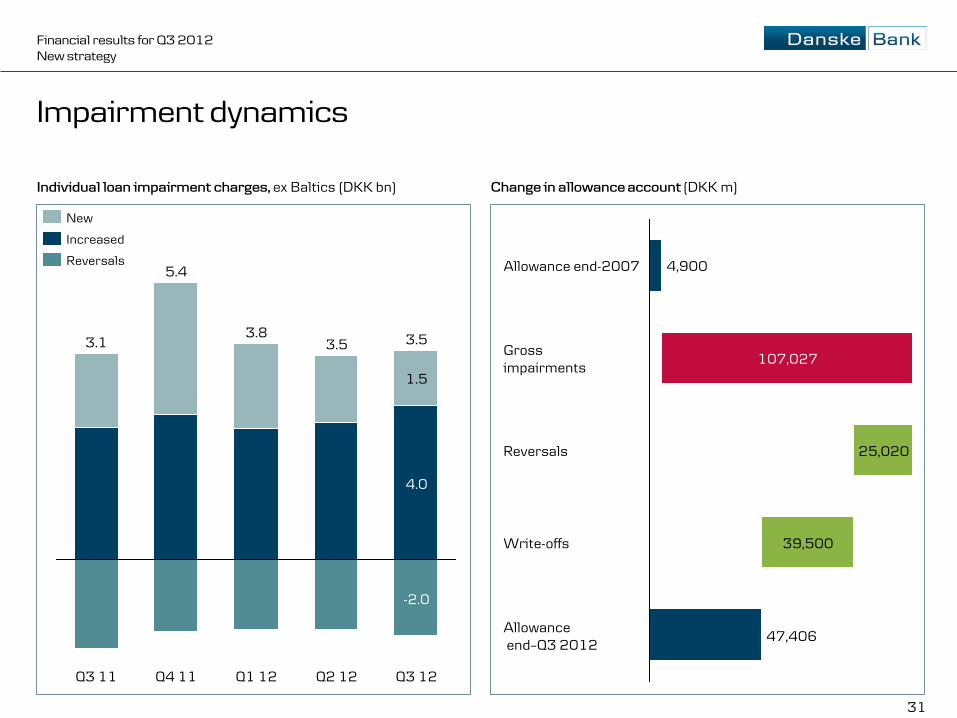

Impairment dynamics

Individual loan impairment charges, ex Baltics (DKK bn) Change in allowance account (DKK m)

Allowance end–Q3 2012

47,406

Write-offs 39,500

Reversals 25,020

Gross impairments

107,027

Allowance end-2007 4,900

Q3 12

3.5

-2.0

4.0

1.5

Q2 12

3.5

Q1 12

3.8

Q4 11

5.4

Q3 11

3.1

Increased

Reversals

New

32

Financial results for Q3 2012 New strategy

Loan quality

Coverage, individual allowance /impairment-tested loans (%) Impairment-tested loans (%)

7.0 Group 5.7

Non-core Ireland 64.1 68.1

CIB 5.1 4.8

Baltics 17.1 19.1

Ireland 9.2 13.9

Northern Ireland 18.4 18.9

Norway 2.6 3.2

Sweden 1.8 2.0

Finland 3.3 3.8

Denmark 4.9 5.8

Q3 12

Q2 12

31

31

34

33

63

52

47

35

56

40Group 37

Non-core Ireland 47

CIB 44

Baltics 48

Ireland 59

Northern Ireland 65

Norway 35

Sweden 32

Finland 30

Denmark 28

Q3 12

Q2 12

Note: Loans in rating categories 10 and 11 are subject to individual impairment testing. Q3 12 is excluding impaired portion. Rating category 10 contains exposures to customers which are not in default but for which evidence of impairment exists; rating category 11 contains exposures to customers in default.

33

Financial results for Q3 2012 New strategy

Retail Banking Denmark, including Realkredit Danmark

Loans by LTV and rating, Realkredit Danmark, end-Q3 2012 (%)

Portfolio facts, Realkredit Danmark, end-Q3 2012

398,045 loans (residential and commercial)

3,031 loans in 3- and 6-month arrears (0.8%)

157 repossessed properties

DKK 13 bn of loans with LTV > 100%, including DKK 3bn with

public guarantee

Average LTV ratio of 71%

LTV ratio on origination (legal requirement)

Residential: max. 80%

Commercial: max. 60%

Impairments at Retail Banking Denmark, Q3 2012 (DKK m)

Q310 Q111 Q311 Q112

1.0

0.8

0.6

0.4

0.6

Q312

1-month arrears, Realkredit Danmark (% of stock)

Rating 1-3 4-7 8-11 Total Public LTV ratio guarantee

0-20 7.5 22.0 3.8 33.3 0.4

20-40 5.2 18.7 3.4 27.4 0.4

40-60 3.4 14.5 2.9 20.7 0.4

60-80 1.8 8.9 1.9 12.6 0.4

80-100 0.7 2.9 0.7 4.3 0.4

>100 0.4 1.0 0.3 1.8 0.4

Total (DKK bn) 139 497 95 731 17

Individual Collective Total

Bank Personal customers 245 -4 241

Agriculture 44 -3 41

Commercial property 174 -154 21

Other 89 -19 71

Total 552 -179 373

RD Personal customers 119 -41 78

Commercial 294 -8 286

Total 413 -49 364

Retail Banking Denmark 965 -228 737

34

Financial results for Q3 2012 New strategy

Denmark, mortgage margins, 80 % LTV, owner occupied, (basis points)

Mortgages: More risk-sensitive pricing is the name of the game

52

73

81

98

106

All products Adjustable rate Fixed rate

+ 2

0 b

p pe

r re

finan

cing

+ 2

0 b

p pe

r re

finan

cing

Oct ‘12: with amortisation Oct ‘12: interest only 2011

2011-12 • Margin increase on personal

customers (Q1 12) • Refinancing fee of 5 bp at each

refinancing (introduced in Q4 11, booked as trading income)

July 2012 • Margin increase on loans with

LTV > 60% • Refinancing fee increased to

10 bp at each refinancing

October 2012 • Margin increase on loans with

LTV > 60% • Margin increase on interest only

loans with LTV > 60% • Refinancing fee increased to

20 bp at each refinancing

Margin increases

35

Financial results for Q3 2012 New strategy

Limited exposure to agriculture and shipping

Agriculture: breakdown of loan portfolio, Q3 2012 (%)

Agricultural exposure and allowance, Q3 2012 (DKK bn) Shipping exposure and allowance, Q3 2012 (DKK bn)

Shipping: breakdown of loan portfolio, Q3 2012 (%)

6

16

25

14

21

Pig farming 19

Cattle breeding

Agriculture Other

Mixed operations

Grocery trade

11

10

9

77 9

10

15

7

8

5

Other

Ro-Ro 2 Product tanker

Offshore supply

Offshore rig

Gas tanker

Dry bulk Cruise/Ferry

Crude tanker

Container

Chemical tanker Car carriers

Business unit Gross exposure

Allowance Coverage

CIB 43.7 1.6 3.8%

-portion from Danish customers 11.8 1.1 9.3%

-portion from Norwegian customers 13.1 0.2 1.4%

-portion from other customers 18.8 0.4 2.0%

Other business units 2.7 0.5 20.4%

Total exposure 46.3 2.2 4.7%

Business unit Allowance Coverage

Realkredit Danmark 45.7 0.4 0.9%

Retail Banking Denmark 11.1 2.5 22.2%

- portion from pig farmers 3.0 1.1 35.5%

Other business units 16.8 0.5 3.1%

Total exposure 73.6 3.4 4.6%

Gross exposure

36

Financial results for Q3 2012 New strategy

Denmark and Northern Ireland: Loan exposure

Note: Value of collateral is capped by size of loan and reflects a haircut of at least 20%. Impaired loans are individually impairment tested (rating categories 10 and 11). Rating category 10 contains exposures to customers which are not in default but for which evidence of impairment exists; rating category 11 contains exposures to customers in default.

Impaired loans

10.1

5.9

1.4

2.9

Gross exposure

519.0

Impaired loans

0.6

0.4

0.2

Gross exposure

16.6

Value of collateral

Individual impairments

Dividend

Denmark (DKK bn) Northern Ireland (DKK bn) Denmark (DKK bn) Northern Ireland (DKK bn)

Collective impairments 0.5 bn Impaired 2%

Collective impairments 0.0 bn Impaired 3%

Collective impairments 0.1 bn Impaired 14%

Collective impairments 0.2 bn Impaired 43%

Commercial property exposure Residential mortgage exposure

Impaired loans

4.8

1.9

3.0

Gross exposure

10.2

Impaired loans

16.7

8.4

3.4

4.9

Gross exposure

121.7

37

Financial results for Q3 2012 New strategy

Note: Value of collateral is capped by size of loan and reflects a haircut of at least 20%. Impaired loans are individually impairment tested (rating categories 10 and 11). Rating category 10 contains exposures to customers which are not in default but for which evidence of impairment exists; rating category 11 contains exposures to customers in default. *Number of arrears, excluding buy-to-let financing.

Collective impairments 0.1 bn Impaired 5%

Personal mortgages (DKK bn)

Collective impairments 0.4bn Impaired 12%

Ireland: Breakdown of loan portfolio

Arrears*, private customers (%)

Q2

12

3.4

10.9

Q4

11

Q2

11

Q4

10

Q2

10

Market

180+ days

91-180 days

Impaired loans

1.8

0.9

0.7

0.2

Gross exposure

15.6

Other (DKK bn)

Impaired loans

0.5

0.1

0.6

-0.2

Gross exposure

11.6

Collective impairments 0.4 bn Impaired 9%

-0.1

Impaired loans

2.3

1.1

1.3

Gross exposure

27.1

Total (DKK bn)

Value of collateral

Individual impairments

Dividend

38

Financial results for Q3 2012 New strategy

Non-core Ireland

Note: Value of collateral is capped by size of loan and reflects a haircut of at least 20%. Impaired loans are individually impairment tested (rating categories 10 and 11). Rating category 10 contains exposures to customers which are not in default but for which evidence of impairment exists; rating category 11 contains exposures to customers in default. * Consists primarily of consumer related industries.

Impaired loans

12.0

4.5

6.0

1.5

Gross exposure

14.4

Impaired loans

1.8

0.8

1.0

Gross exposure

8.9

Impaired loans

5.8

2.0

2.3

1.5

Gross exposure

7.8

Dividend

Value of collateral

Individual impairments

CRE (DKK bn) Personal mortgages (DKK bn) Other* (DKK bn)

Collective impairments 0.1 bn Impaired 83%

Collective impairments 0.3 bn Impaired 20%

Collective impairments 0.0 bn Impaired 75%

Collective impairments 0.4 bn Impaired 63%

Impaired loans

19.6

7.3

9.3

3.0

Gross exposure

31.1

Total (DKK bn)

39

Financial results for Q3 2012 New strategy

Update on conduits: Exposure and risk reduced in 2012

Credit exposure, rating categories, Q3 2012 (DKK bn)

Credit exposure, mortgages, Q3 2012 (DKK bn)

Gross credit exposure 2007-12 (DKK bn)

Credit exposure underlying asset class, Q3 2012 (DKK bn)

Q3 12

20

Q2 12

28

Q1 12

28

2011

31

2010

40

2009

48

2008

56

2007

62

Rating category 1-9

Rating category 10-11

011

1

23

2

4

6

111

23

2

4

6

1 9 8 7 6 5 4 3 2 11 10

Net Credit Exposure Gross Credit Exposure

6%

55%

7%

12%

20%

Non-prime residential mortgages

Corporate risk

Commercial mortgages

Other

Prime residential mortgages

5%

70%

1% 13%

11% Other, non-prime

NL, non-prime

NL, prime

UK, prime

UK, non-prime

Total: DKK 10.1 bn Total: DKK 19.7 bn

40

Financial results for Q3 2012 New strategy

Solid funding structure and liquidity position

Loan portfolio and long-term funding, Q3 2012 (DKK bn)

167

374

743

597

1211,700

729 Issued RD bonds RD mortgages

Covered bonds

Bank mortgages

Deposits

Bank loans

Senior debt

Funding

1,760

729

Loans 2031

2 1

2021

10

4

24

2018

26

41

52

2015

58

70

48

2012

3 1

9

2024

2 1 0

2027

1 0

Senior

Hybrid T1*

Subordinated T2*

Covered bonds

Maturing funding (DKK bn)

* Maturity calculated to first possible call.

41

Financial results for Q3 2012 New strategy

Well-diversified funding position

Funding sources (%)

57

12

7

6

6 25

293

Equity Central banks

Subordinated debt

Repos

Banks

S-T bonds 1

L-T bonds

Covered bonds Match-funded

DK mortgage bonds

Deposits

Funding position Q3 12(%)

30

20

10

0

Sha

reho

lder

s’ e

q.

Sub

ord.

deb

t

Long

-ter

m b

onds

Cov

. bon

ds

Mor

tgag

e fin

ance

(m

atch

fund

ed)

Dep

osit

s

Sho

rt-t

erm

bon

ds

Rep

os

Due

to c

redi

t in

st.

(ex

CIB

)

Cen

tral

ban

ks

40

Q4 11

Q3 12

Short-term funding Long-term funding

42

Financial results for Q3 2012 New strategy

Danske Bank’s long term issuer rating

Danske Bank’s ratings

Rating agency issues

Moody’s S&P Fitch

Aaa AAA AAA

Aa1 AA+ AA+

Aa2 AA AA

Aa3 AA- AA-

A1 A+ A+

A2 A A

A3 A- A-

Baa1 BBB+ BBB+

Baa2 BBB BBB

Baa3 BBB- BBB-

… … …

Ca D D

General focus

• Profitability: a sustainable improvement in net profit will be positive

• Asset quality: a significant decrease in non-performing loans, impairments and actual losses will be positive

• Macroeconomic environment: an improvement of the economic conditions in Denmark and Ireland will be positive

Standard & Poor’s

• Capital strength: quality of current capital is good, but a RAC ratio sustainable above 7 % will have a positive effect on the rating (Q4 2011 level of 6.3%)

Moody’s

• Liquidity: refinancing risks in the Danish mortgage system creates an instability in the Danish housing market

• Systemic support: only 1 notch uplift for Danske Bank, Swedish peers have 3 notches of uplift

43

Financial results for Q3 2012 New strategy

Three different methods to rate banks

+ + = =

Bank Financial Strength

Rating

Baseline Credit

Assess- ment (BCA)

Parental and Cooperative

support

Adjusted

BCA

Systemic Support

Issuer Rating

Anchor SACP*

Business position

Capital & Earnings

Risk position

Funding & Liquidity

SACP Extraord. Support

Issuer rating

+ = + = + + +

C- Baa2 0 notches Baa2 1 notch Baa1

BBB+ +1 notch -1 notch -1 notch 0 notches

BBB 2

notches A-

Individual rating/Viability rating

Support rating/support rating floor

Issuer Default Rating (IDR)

IDR is the higher of the Viability Rating and the support floor

a

A-

A

Rating method Danske Bank’s rating

* Stand-alone credit profile (SACP)

44

Financial results for Q3 2012 New strategy

Retail Banking Denmark: Higher NII owing to several margin increases, but higher impairments reduce the result Income statement (DKK m) Trend in lending volume, average (DKK bn)

Margin trends, ex RD (%) Market shares, incl. CIB and repo lending*, ex RD (%)

* Danske Markets.

20

24

28

32

36

Q312 Q212 Q112 Q411 Q311

Deposits Lending

0

1

2

3

4

Q312 Q212 Q112 Q411 Q311

Deposits Lending

548550555558559

383385386390391

Q312 Q212 Q112 Q411 Q311

-2%

-2%

Corporate Retail 9M 2012 9M 2011 Index

Net interest income 9,387 9,097 103

Net fee income 2,408 2,400 100

Other income 695 808 86

Total income 12,490 12,305 102

Total expenses 6,813 6,523 104

Profit bef. loan imp. charges 5,677 5,782 98

Loan impairment charges 3,027 2,649 114

Profit before tax 2,650 3,133 85

ROE before loan imp. charges 16.9 18.3

45

Financial results for Q3 2012 New strategy

Retail Banking Finland: Visible increase in net interest income, but low result because of low margins and higher loan losses

Trend in lending volume, average (DKK bn)

Margin trends (%) Market shares, incl. CIB (%)

10

12

14

Q312 Q212 Q112 Q411 Q311

0.9

0.6

0.3

0.0 Q312 Q212 Q112 Q411 Q311

Deposits Lending Deposits Lending

1011001009896

5151505050

+3%

+5%

Q312 Q212 Q112 Q411 Q311

Corporate Retail

Income statement (DKK m)

9M 2012 9M 2011 Index

Net interest income 1,650 1,531 108 Net fee income 815 741 110 Other income 240 385 62 Total income 2,705 2,657 102 Total integration expenses 315 395 80 Expenses ex total intgr. exp. 1,902 1,976 96 Profit bef. loan imp. charges 488 286 171 Loan impairment charges 309 57 -Profit before tax 179 229 78

325,809 ROE before loan imp. charges 9.2 6.1

46

Financial results for Q3 2012 New strategy

Retail Banking Sweden: High return held up by 19 % increase in net interest income partly due to stronger SEK

6.0

5.5

5.0

4.5

4.0 Q312 Q212 Q112 Q411 Q311

1.5

1.0

0.5

0.0 Q312 Q212 Q112 Q411 Q311

Deposits Lending Deposits Lending

928686838210399100101100

+3%

+12%

Q312 Q212 Q112 Q411 Q311

Corporate Retail

Trend in lending volume, average (DKK bn)

Margin trends (%) Market shares, incl. CIB (%)

Income statement (DKK m)

9M 2012 9M 2011 Index

Net interest income 2,082 1,754 119

Net fee income 415 452 92

Other income 140 159 88

Total income 2,637 2,365 112

Expenses 1,260 1,256 100

Profit bef. loan imp. charges 1,377 1,109 124

Loan impairment charges 315 47 -

Profit before tax 1,062 1,062 100

ROE before loan imp. charges 17.1 15.0

47

Financial results for Q3 2012 New strategy

Retail Banking Norway: Solid increase in total income; pre-tax profit more than doubles as impairments losses decline

6

5

4 Q312 Q212 Q112 Q411 Q311

1.5

1.0

0.5

0.0 Q312 Q212 Q112 Q411 Q311

81787774716160585860

Q312 Q212 Q112 Q411 Q311

+1%

+13%

Corporate Retail

Deposits Lending Deposits Lending

Trend in lending volume, average (DKK bn)

Margin trends (%) Market shares, incl. CIB (%)

Income statement (DKK m)

9M 2012 9M 2011 Index

Net interest income 1.544 1.149 134

Net fee income 226 187 121

Other income 538 554 97

Total income 2.308 1.890 122

Expenses 1.365 1.358 101

Profit bef. loan imp. charges 943 532 177

Loan impairment charges 155 271 57

Profit before tax 788 261 302

ROE before loan imp. charges 16,1 10,4

48

Financial results for Q3 2012 New strategy

Banking Activities Northern Ireland: Moving in the right direction with higher income and lower impairments

* Corporate lending volume excludes lending to public sector. Volume positive affected by currency change

Q212 Q112 10

Q312

40

30

20

Q411 Q311

3

2

1

0 Q312 Q212 Q112 Q411 Q311

1817171616

25252525 25

-2%

+14%

Q311 Q112 Q312 Q212 Q411

Corporate Retail

Deposits Lending Corporate Retail

Trend in lending volume*, average (DKK bn)

Margin trends (%) Market shares (%)

Income statement (DKK m)

9M 2012 9M 2011 Index

Net interest income 916 845 108

Net fee income 277 231 120

Other income 92 103 89

Total income 1,285 1,179 109

Expenses 807 842 96

Profit bef. loan imp. charges 478 337 142

Loan impairment charges 1,120 1,654 68

Profit before tax -642 -1,317 -

ROE before loan imp. charges 31.0 21.2

49

Financial results for Q3 2012 New strategy

Banking Activities Ireland: Still higher expenses owing to restructuring of the continuing business

181717

2727

799

3740

Q312 Q212 Q112 Q411 Q311

-82%

-33%

Corporate Retail

2

1

0 Q312 Q212 Q112 Q411 Q311

4

3

2

1 Q312 Q212 Q112 Q411 Q311

Deposits Lending Deposits Lending

Trend in lending volume, end of period (DKK bn)

Margin trends (%) Market shares (%)

Income statement (DKK m)

Note: Figures from Q4 2011 and back are not restated after non-core split-up from Banking Activities Ireland.

9M 2012 9M 2011 Index

Net interest income 300 686 44

Net fee income 62 48 129

Other income 31 35 89

Total income 393 769 51

Expenses 583 532 110

Profit bef. loan imp. charges -190 237 -

Loan impairment charges 559 4,711 12

Profit before tax -749 -4,474 -

ROE before loan imp. charges -17.0 10.0

50

Financial results for Q3 2012 New strategy

Non-core Ireland: Dominated by high impairments

899

222727

-19%

-17%

Q312 Q212 Q112 Q411 Q311

Corporate

Retail

Trend in lending volume, end-of-period (DKK bn)

Margin trends (%) Portfolio breakdown, Q3 2012(%)

Income statement (DKK m)

Note: Figures from Q4 2011 and back are not restated after non-core split-up from Banking Activities Ireland.

Q312

0.1

1.4

Q212

0.6

1.5

Q112

0.5

1.6

Q411 Q311

Deposits

Lending

Included in BA Ireland

25%

29%

46%

Other

Personal mortgages

CRE

Included in BA Ireland

9M 2012 9M 2011 IndexNet interest income 298 - -Net fee income 2 - -Other income 3 - -Total income 303 - -Expenses 176 - -Profit bef. loan imp. charges 127 - -Loan impairment charges 3,740 - -Profit before tax -3,613 - -

51

Financial results for Q3 2012 New strategy

Banking Activities Baltics: Higher income and impairment reversals raise pre-tax profit by 60 %

Market shares, lending (%)

1111121212

78889

-10%

-19%

Q312 Q212 Q112 Q411 Q311

Corporate Retail

0

1

2

3

Q312 Q212 Q112 Q411 Q311

12

9

6

3

0 Q312 Q212 Q112 Q411 Q311

Deposits Lending Lithuania Latvia Estonia

Trend in lending volume, average (DKK bn)

Margin trends (%)

Income statement (DKK m)

9M 2012 9M 2011 Index

Net interest income 357 363 98

Net fee income 114 109 105

Other income 103 72 143

Total income 574 544 106

Expenses 267 264 101

Profit bef. loan imp. charges 307 280 110

Loan impairment charges -395 -156 -

Profit before tax 702 436 161

ROE before loan imp. charges 31.8 28.7

52

Financial results for Q3 2012 New strategy

CIB: Solid NII growth but significantly higher loan losses, mainly from shipping

Trend in lending volume, average (DKK bn)

Geographical breakdown of lending, Q3 2012 (%)

110109108107103

Q312 Q212 Q112 Q411 Q311

1.6

Q312

1.2

0.8

0.4

0.0 Q212 Q112 Q411 Q311

Deposits Lending

20

15

36

30

Sweden

Finland

Norway

Denmark

Margin trends (%)

Income statement (DKK m)

9M 2012 9M 2011 Index

Net interest income 1,584 1,483 107 Net fee income 573 604 95 Other income 78 127 61 Total income 2,235 2,214 101 Total integration expenses 18 92 20 Expenses ex total intgr. exp. 766 721 106 Profit bef. loan imp. charges 1,451 1,401 104 Loan impairment charges 1,054 95 -Profit before tax 397 1,306 30

ROE before loan imp. charges 15.5 16.8

53

Financial results for Q3 2012 New strategy

Danske Markets & Treasury: Solid earnings due to high activity including Q3

Impairments (DKK m)

-750

-65

52

-27

Q112 Q411

-52

Q311 Q312 Q212

Trading income split, Q3 2012 Income statement (DKK m)

Trading activities , accumulated income (DKK bn)

8,000

6,000

4,000

2,000

0

2012 2011 2010

Q4 Q3 Q2 Q1

42

95

43

Equities

Bonds & DCM

Repos & derivatives

FX & money market 9M 2012 9M 2011 IndexDanske Markets 6,775 3,877 175 Group Treasury -220 593 -Total income 6,555 4,470 147 Expenses 2,297 1,968 117 Profit bef. loan imp. charges 4,258 2,502 170 Loan impairment charges -40 -981 -Profit before tax 4,298 3,483 123

ROE before loan imp. charges 45.5 40.3

54

Financial results for Q3 2012 New strategy

Danske Capital: Lower fee income owing to change in asset mix and one-offs; margins remain flattish

AuM – customer breakdown (DKK bn)

AuM – asset breakdown (%)

* Retail includes Danske Invest. ** Margin for asset management is adjusted income, including performance fees, divided by business volume, end of period.

30

Q212 Q112 Q411 Q311

4

Q312

66

Bonds Equities Cash

201

Q212 Q112 Q411 Q311

191

Q312

16

258

Life insurance Retail* Institutional Private equity

0.4

0.3

0.2

0.1

0.0 Q312 Q212 Q112 Q411 Q311

Margin trends** (%)

Income statement (DKK m)

9M 2012 9M 2011 Index

Net interest income 87 88 99

Net fee income 1.208 1.229 98

- portion from performance fees 10 17 -

Other income 30 49 61

Total income 1.325 1.366 97

Expenses 774 780 99

Profit bef. loan imp. charges 551 586 94

Loan impairment charges 8 -47 -

Profit before tax 543 633 86

55

Financial results for Q3 2012 New strategy

-100%

-50%

0%

50%

100%

-2.00% -1.00% 0.00% 1.00% 2.00%

Danica Pension: Strong investment result and partially booked risk allowance

48 70 68 73

19

6 6

High

10

14

3

Medium

9

17

Low

10

14

New schemes

12

21

Investment allocation for Danica Traditionel, end-Q3 2012 (%) Income statement (DKK m)

Possibility of booking risk allowance in 2012*, end-Q3 2012 (%)

No risk allowance

Partial risk allowance

Full risk allowance

% c

hang

e in

equ

itie

s

% point change in interest rate

* Under assumption of a rolling yield spread of 0 between Danish and German government bonds at the end of 2012.

Credit bonds Bonds Equities Property 9M 2012 9M 2011 Index

Premiums (bn) 18.4 20.0 92

Danica Traditionel (insurance result) 950 822 116

Unit-linked (insurance result) 267 245 109

Health and accident (ins. result) -94 33 -

Investment result 435 345 126

Financing result -73 -126 -

Special allotments -69 -150 -

Net income bef. postp. risk allow. 1,416 1,169 121

Change in shadow account -106 -1,576 -

Net income 1,310 -407 -

56

Financial results for Q3 2012 New strategy

Danica Pension’s profit model

Profit model Condition/ sensitivity Q1-Q3 2012 DKK m

Danica Traditionel. Mainly risk allowance 69 bp of technical provisions (DKK 173 bn)

Can be booked only if investment return is high enough and if no use of bonus potential of paid-up policies

Risk allowance Other

1,008 -58

Unit-linked business. Long-term: approximately 0.4% of AuM

Prices and volume Solid income base but also price competition

267

Health and accident business Combined ratio Price competition -94

Return on investment portfolio at shareholders’ risk

Equity markets, interest rates Annualised investment return: 3.6%

435

Financing result

S-T interest rate (equity – allocated capital)

Low short-term interest rate -73

Special allotments, depending on profit and business volume

Expected to be around DKK 0.1 billion in 2012 if investment return is at normal level

-69

Shadow account Uncertainty because of dependency on investment return for the rest of the year

-106

Total 1,310

+

1

2

3

4

5

6

+

+

+

=

+

7

+

∑

57

Financial results for Q3 2012 New strategy

Disclaimer

Important Notice

• This presentation does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of

an offer to buy or acquire securities of Danske Bank A/S in any jurisdiction, including the United States, or an inducement to enter into investment activity. No part of this presentation, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever. The securities referred to herein have not been, and will not be, registered under the Securities Act of 1933, as amended (“Securities Act”), and may not be offered or sold in the United States absent registration or an applicable exemption from the registration requirements of the Securities Act.

• This presentation contains forward-looking statements that reflect management’s current views with respect to certain future events and potential financial performance. Although Danske Bank believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those set out in the forward-looking statements as a result of various factors many of which are beyond Danske Bank’s control.

• This presentation does not imply that Danske Bank has undertaken to revise these forward-looking statements, beyond what is required by applicable law or applicable stock exchange regulations if and when circumstances arise that will lead to changes compared to the date when these statements were provided.