Risk and Regulatory - Sia Partners...• BlockChain KYC making use of distributed ledger technology...

7

1 Risk and Regulatory Quarterly Newsletter (HK, JP and SG) Issue 9 – January 2017 Regulatory Focus RegTech – Leading To Paradigm Shift in Regulation New York | London | Hong Kong | Singapore | Japan |Dubai | Abu Dhabi | Riyadh | Casablanca | Brussels | Amsterdam | Roma | Milano | Paris | Lyon 1 CONFIDENTIAL © 2017 Sia Partners Website: http ://www.sia-partners.com | Blog: http ://en.finance.sia-partners.com/ page Overview of RegTech Since the financial crisis of 2008, regulations have been imposed on banks at an increasing pace in the following areas: • KYC/AML: Following the guidelines on the Financial Action Task Force (FATF), countries are strengthening their regulations on AML/CFT • Risk Management: Tighten control on capital reserve and higher expectation on risk models (e.g. Basel III, IFRS9, FRTB) • Data management: Data monitoring in active and granular level requesting high data quality (Data privacy acts, protection of biometric data) • Regulatory global tax reporting: International co-operation on combating tax evasion (e.g. FATCA, CRS) Complicated and demanding regulatory regimes have imposed great challenges to FIs in the following aspects: As a result, both the FIs and customers have suffered. Figures below indicate the increased compliance cost and client onboarding time over the years: Subject to the regulatory impacts, RegTech is considered as a magic key to resolve the compliance challenges in the short term. RegTech is also a core strategy changing the regulation landscape in the medium/long term. Some recent trends of RegTech are illustrated below: 1) Short Term (1-2 Year) • Digital KYC making use of mobile devices and biometrics • Big Data Analytics making use of data science • Technology on Cybersecurity control 2) Medium to Long Term (>3 years) • BlockChain KYC making use of distributed ledger technology • Smart Contract for automated data driven monitoring TECHNOLOGY • Legacy IT systems lack agility to keep up with fast-pace regulatory changes • Lack of data quality and robust systems for regulatory reporting DAILY OPERATIONS • Complicated and inefficient operating processes • Lack of smart automation and analytics capabilities COST & HUMAN CAPACITY • Lack of resources with the required knowledge • Lack of capacity to analyze and implement all regulations • The increasing cost of implementing the ever evolving regulatory requirements and recruiting talents in the market GOVERNANCE • Difficult to manage a comprehensive enterprise-wide governance program that meets regulatory expectations What is RegTech? RegTech, or otherwise known as “Regulatory Technology”, aims to apply the latest innovative technologies to better perform regulatory processes for the benefit of Financial Institutions (“FIs”)/Regulatory Authorities. It is composed of a broad range of industry players using such technology solutions to improve the existing methodology of risk remediation and regulatory compliance, and thus enhancing efficiency. Source: Financial Times Source: Thomson Reuters KYC Survey 2016

Transcript of Risk and Regulatory - Sia Partners...• BlockChain KYC making use of distributed ledger technology...

1

Risk and RegulatoryQuarterly Newsletter (HK, JP and SG)

Issue 9 – January 2017

Regulatory Focus

RegTech – Leading To Paradigm Shift in Regulation

New York | London | Hong Kong | Singapore | Japan |Dubai | Abu Dhabi | Riyadh | Casablanca | Brussels | Amsterdam | Roma | Milano | Paris | Lyon

1CONFIDENTIAL © 2017 SiaPartners Website: http://www.sia-partners.com | Blog: http://en.finance.sia-partners.com/

p a g e

Overview of RegTechSince the financial crisis of 2008, regulations have been imposed on banks at an increasing pace in the following areas: • KYC/AML: Following the guidelines on the Financial Action Task Force (FATF), countries are strengthening their regulations on AML/CFT• Risk Management: Tighten control on capital reserve and higher expectation on risk models (e.g. Basel III, IFRS9, FRTB)• Data management: Data monitoring in active and granular level requesting high data quality (Data privacy acts, protection of biometric data)• Regulatory global tax reporting: International co-operation on combating tax evasion (e.g. FATCA, CRS)

Complicated and demanding regulatory regimes have imposed great challenges to FIs in the following aspects:

As a result, both the FIs and customers have suffered. Figures below indicate the increased compliance cost and client onboarding time over the years:

Subject to the regulatory impacts, RegTech is considered as a magic key to resolve the compliance challenges in the short term. RegTech is also a core strategy changing the regulation landscape in the medium/long term. Some recent trends of RegTech are illustrated below:

1) Short Term (1-2 Year) • Digital KYC making use of mobile devices and biometrics • Big Data Analytics making use of data science • Technology on Cybersecurity control

2) Medium to Long Term (>3 years) • BlockChain KYC making use of distributed ledger technology• Smart Contract for automated data driven monitoring

TECHNOLOGY

• Legacy IT systems lack agility to keep up with fast-pace regulatory changes

• Lack of data quality and robust systems for regulatory reporting

DAILY OPERATIONS

• Complicated and inefficient operating processes• Lack of smart automation and analytics capabilities

COST & HUMAN CAPACITY

• Lack of resources with the required knowledge• Lack of capacity to analyze and implement all regulations• The increasing cost of implementing the ever evolving regulatory

requirements and recruiting talents in the market

GOVERNANCE

• Difficult to manage a comprehensive enterprise-wide governance program that meets regulatory expectations

What is RegTech?

RegTech, or otherwise known as “Regulatory Technology”, aims to apply the latest innovative technologies to better perform regulatory processes for the benefit of Financial Institutions (“FIs”)/Regulatory Authorities. It is composed of a broad range of industry players using such technology solutions to improve the existing methodology of risk remediation and regulatory compliance, and thus enhancing efficiency.

Source: Financial Times Source: Thomson Reuters KYC Survey 2016

1

Regulatory Focus

RegTech – Leading To Paradigm Shift in Regulation

RegTech Generation: Shifting to 3.0

While treating the technology approach before 2008 as RegTech 1.0, we are now in RegTech 2.0. Further exploration and adoption on RegTech is not only addressing the regulatory challenges, but also leading to a paradigm shift in the whole regulatory landscape in the long run.

RegTech Journey to Change Regulatory Landscape

The journey to RegTech 3.0 includes the following:

New York | London | Hong Kong | Singapore | Japan |Dubai | Abu Dhabi | Riyadh | Casablanca | Brussels | Amsterdam | Roma | Milano | Paris | Lyon

2CONFIDENTIAL © 2017 SiaPartners Website: http://www.sia-partners.com | Blog: http://en.finance.sia-partners.com/

p a g e

Risk and Regulatory Quarterly Newsletter (HK, JP, and SG)Issue 9 – January 2017

From single level of regulation to multiple levels of regulation

• Regulatory relaxation for the FinTech industry• Regulation based on firm’s size and market

contribution

From heterogenous to harmonized data reporting standard

• Harmonization data standards• Simplified data processing• Better customer experience

From Know your customer to Know your data• Granular data monitoring by using advanced

analytics, such as big data• Active compliance risk detection

From isolated data to connected data• Connect all structured and unstructured data

sources• Exploit the information uncovered by data

connection

Key Drivers Of RegTechFinancial institutions, regulators and technology start-ups are the main drivers of RegTech:

1

Regulatory Focus

RegTech – Leading To Paradigm Shift in Regulation

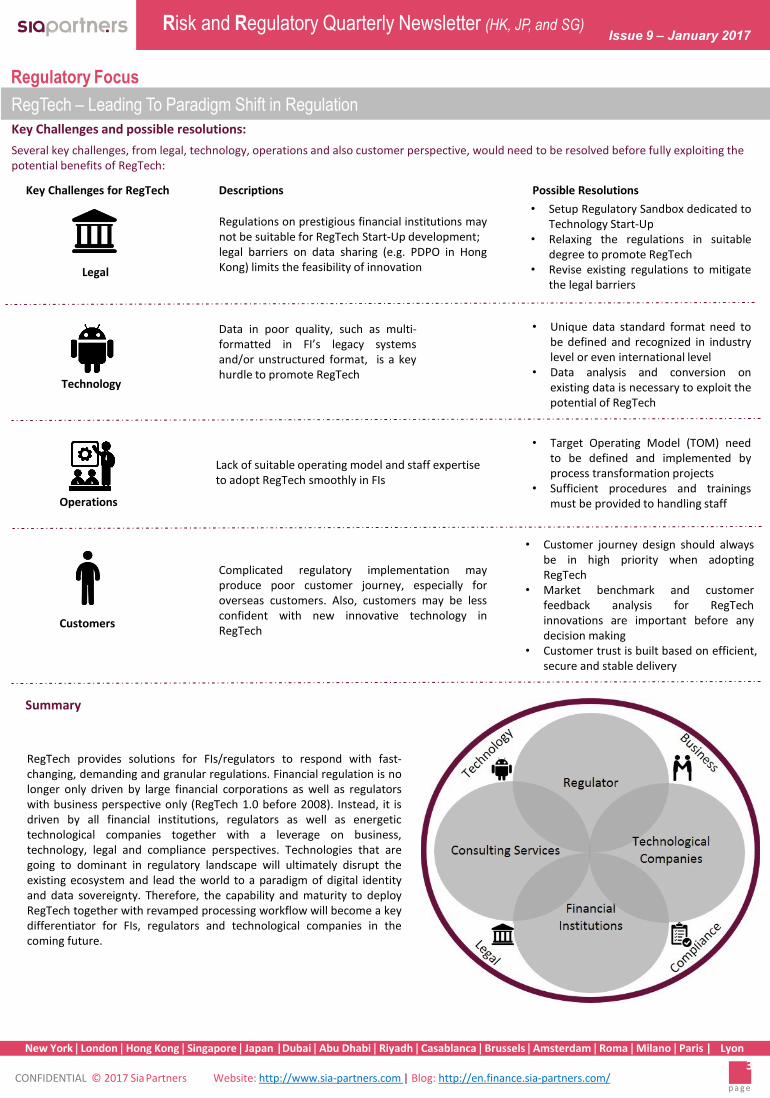

Key Challenges and possible resolutions:

Several key challenges, from legal, technology, operations and also customer perspective, would need to be resolved before fully exploiting the potential benefits of RegTech:

New York | London | Hong Kong | Singapore | Japan |Dubai | Abu Dhabi | Riyadh | Casablanca | Brussels | Amsterdam | Roma | Milano | Paris | Lyon

3CONFIDENTIAL © 2017 SiaPartners Website: http://www.sia-partners.com | Blog: http://en.finance.sia-partners.com/

p a g e

Risk and Regulatory Quarterly Newsletter (HK, JP, and SG)Issue 9 – January 2017

Key Challenges for RegTech Descriptions Possible Resolutions

Legal

Regulations on prestigious financial institutions maynot be suitable for RegTech Start-Up development;legal barriers on data sharing (e.g. PDPO in HongKong) limits the feasibility of innovation

• Setup Regulatory Sandbox dedicated toTechnology Start-Up

• Relaxing the regulations in suitabledegree to promote RegTech

• Revise existing regulations to mitigatethe legal barriers

Technology

Data in poor quality, such as multi-formatted in FI’s legacy systemsand/or unstructured format, is a keyhurdle to promote RegTech

• Unique data standard format need tobe defined and recognized in industrylevel or even international level

• Data analysis and conversion onexisting data is necessary to exploit thepotential of RegTech

Operations

Lack of suitable operating model and staff expertise to adopt RegTech smoothly in FIs

• Target Operating Model (TOM) needto be defined and implemented byprocess transformation projects

• Sufficient procedures and trainingsmust be provided to handling staff

Customers

Complicated regulatory implementation mayproduce poor customer journey, especially foroverseas customers. Also, customers may be lessconfident with new innovative technology inRegTech

• Customer journey design should alwaysbe in high priority when adoptingRegTech

• Market benchmark and customerfeedback analysis for RegTechinnovations are important before anydecision making

• Customer trust is built based on efficient,secure and stable delivery

Summary

RegTech provides solutions for FIs/regulators to respond with fast-changing, demanding and granular regulations. Financial regulation is nolonger only driven by large financial corporations as well as regulatorswith business perspective only (RegTech 1.0 before 2008). Instead, it isdriven by all financial institutions, regulators as well as energetictechnological companies together with a leverage on business,technology, legal and compliance perspectives. Technologies that aregoing to dominant in regulatory landscape will ultimately disrupt theexisting ecosystem and lead the world to a paradigm of digital identityand data sovereignty. Therefore, the capability and maturity to deployRegTech together with revamped processing workflow will become a keydifferentiator for FIs, regulators and technological companies in thecoming future.

1

New York | London | Hong Kong | Singapore | Japan |Dubai | Abu Dhabi | Riyadh | Casablanca | Brussels | Amsterdam | Roma | Milano | Paris | Lyon

4CONFIDENTIAL © 2017 SiaPartners Website: http://www.sia-partners.com | Blog: http://en.finance.sia-partners.com/

p a g e

Risk and Regulatory Quarterly Newsletter (HK, JP, and SG)Issue 9 – January 2017

Regulatory Updates

Global | Key BIS Regulatory Updates Source: BIS

Date

Published Title Regulator’s Purpose and Objectives

12-Oct-2016 TLAC Holdings Standard

This document is the final standard on the regulatory capital treatment of banks'investments in instruments that comprise total loss-absorbing capacity (TLAC) forglobal systemically important banks (G-SIBs). They take effect on 1 January 2019for most G-SIBs. The main elements of the prudential treatment are as follows:(i) Tier 2 deduction(ii) Threshold below which no deduction is required(iii) Instruments ranking pari passu with subordinated forms of TLAC must also bededucted

Global | Key FSB Regulatory Updates Source: FSB

Date

Published Title Regulator’s Purpose and Objectives

19-Oct-2016Key Attributes Assessment Methodology for the Banking Sector

FSB published a methodology for assessing the implementation of the KeyAttributes of Effective Resolution Regimes for Financial Institutions (KeyAttributes) in the banking sector. The Methodology sets out essential criteria toguide the assessment of the compliance of a jurisdiction’s bank resolutionframeworks with the FSB’s Key Attributes.

21-Nov-2016 FSB publishes 2016 G-SIB listThe Financial Stability Board (FSB), in consultation with the BCBS and nationalauthorities, published the 2016 list of G-SIBs.

Global | Key BIS Consultation Papers Source: BIS

Date

Published Title Regulator’s Purpose and Objectives

11-Oct-2016Regulatory treatment of accounting provisions - interim approach and transitional arrangements

The International Accounting Standards Board (IASB) and the US FinancialAccounting Standards Board (FASB) have adopted provisioning standards thatrequire use of expected credit loss (ECL) models rather than incurred loss models.The new accounting standards modify provisioning standards to incorporateforward-looking assessments in the estimation of credit losses. The consultativedocument sets out the proposal to retain, for an interim period, the currentregulatory treatment of provisions under the standardized and the internal ratings-based approaches.

23-Nov-2016Revisions to the annex on correspondent banking

The Basel Committee is consulting on proposed Revisions to the annex oncorrespondent banking. The proposed revisions guide the banks in theapplication of the risk-based approach for correspondent banking relationships.The proposed revisions also clarify supervisors' expectations regarding the qualityof payment messages as well as conditions for using Know Your Customer (KYC)utilities.

23-Nov-2016Proposals clarify rules on combating money laundering and terrorist financing in correspondent banking

Banks will have clearer guidance on how to best manage risks related to moneylaundering and the financing of terrorism under proposals issued today by theBasel Committee on Banking Supervision (BCBS). The draft revisions aim toensure that banks conduct correspondent banking business with the best possibleunderstanding of the applicable rules on anti-money laundering and countering thefinancing of terrorism.

Global | Key FSB Consultation Papers Source: FSB

Date

Published Title Regulator’s Purpose and Objectives

16-Dec-2016Guiding Principles on the Internal Total Loss-absorbing Capacity of G-SIBs (Internal TLAC)

FSB consults on principles for internal TLAC to assist home and host authorities inthe implementation of internal TLAC mechanisms consistent with the TLACstandard. The guiding principles cover:(i) Identification and composition of material sub-groups(ii) The size and composition of the requirement(iii) Design of the trigger mechanism for internal TLAC(iv) Cooperation and coordination between home and host authorities

1

New York | London | Hong Kong | Singapore | Japan |Dubai | Abu Dhabi | Riyadh | Casablanca | Brussels | Amsterdam | Roma | Milano | Paris | Lyon

5CONFIDENTIAL © 2017 SiaPartners Website: http://www.sia-partners.com | Blog: http://en.finance.sia-partners.com/

p a g e

Risk and Regulatory Quarterly Newsletter (HK, JP, and SG)Issue 9 – January 2017

Regulatory Updates

Global | Key BCBS Regulatory Updates Source: BCBS

Date

Published Title Regulator’s Purpose and Objectives

30-Nov-2016Risk weight for the International Development Association (IDA)

The BCBS has agreed that supervisors may allow banks to apply a 0% risk weightto claims on the IDA in accordance with paragraph 59 of the documentInternational Convergence of Capital Measurement and Capital Standards: aRevised Framework, June 2004 (Basel II Framework). IDA will be included in thelist of multi-lateral development banks as set out in footnote 24 to paragraph 59 ofthe Basel II Framework.

Hong Kong | Key HKMA Regulations Source: HKMA

Date

Published Title Regulator’s Purpose and Objectives

11-Oct-16Automatic Exchange of Financial Account Information in Tax Matters

This is a circular to remind FIs to carefully assess the Inland Revenue Ordinance2016, for its impact on their operations and put in place necessary processes andcontrols in order to ensure compliance with the due diligence and reportingobligations. FIs should also communicate effectively with customers the additionalinformation required.

18-Oct-16 TLAC Holdings Standard

This is a circular is about the standard on TLAC holdings issued by BCBS. Underthe new standard, the main elements of the prescribed regulatory capitaltreatment include:(i) Deduction(ii) Exemption thresholds(iii) Capital buffersIt also reminds FIs that HKMA is going to revise the treatment in accordance withthe BCBS timetable and FIs should prepare for any system change required.

25-Nov-16Supervisory Policy Manual (SPM): LM-2 “Sound Systems and Controls for Liquidity Risk Management”

This circular is on the revised version of the SPM module on Sound Systems andControls for Liquidity Risk Management. The following are the key highlights ofthe revision:(i) Greater degree of flexibility to determine liquidity risk governance andmanagement systems(ii) Provisions regarding the requirement of maintaining a “liquidity cushion” havebeen modified(iii) Removal of certain provision(iv) Combining similar or related provisions

6-Dec-16Implementation of margin and risk-mitigation standards for non-centrally cleared OTC derivatives

This is a circular on the implementation of initial margin (IM) requirements forphase 1 institutions and the exchange of variation margin (VM) for all coveredentities, starting from 1-March-2017. A six-month transitional period will be given,starting from 1-Mar-2017 to 31-Aug-2017.

19-Dec-16Enhanced Competency Framework (ECF) on Cybersecurity

The HKMA and the banking industry have worked together to develop an industry-wide ECF on Cybersecurity for the banking sector. This framework enablescybersecurity talent development and facilitates the building of professionalcompetencies and capabilities of those staff engaged in cybersecurity duties. AIsare advised to keep records of the relevant training and qualifications.

21-Dec-16 Cybersecurity Fortification Initiative

This is a circular to inform the implementation details of the CybersecurityFortification Initiative (CFI), stating that HKMA will adopt a phased approach:(i) First phase will cover around 30 AIs(ii) Under the first phase, the expected timeline for completing Inherent RiskAssessment and Maturity Assessment is end of Sep-2017 and end of Jun-2018for iCAST(iii) Second phase will cover all the remaining AIs and they are expected tocomplete the Inherent Risk Assessment and Maturity Assessment by the end of2018

30-Dec-16Supervisory Policy Manual (SPM): CR-G-14 “Margin and risk mitigation standards for non-centrally cleared OTC derivatives”

This is a circular on the final draft version of the SPM module on Margin and riskmitigation standards for non-centrally cleared OTC derivatives. The key sectionsof the module includes:(i) Cover margin standards including, inter alia, the exchange of VM and IM(ii) Cover risk mitigation standards such as trading relationship documentation,trade confirmation, valuation with counterparties, portfolio reconciliation, portfoliocompression, and dispute resolution(iii) Outline the Hong Kong Monetary Authority’s supervisory approach

1

New York | London | Hong Kong | Singapore | Japan |Dubai | Abu Dhabi | Riyadh | Casablanca | Brussels | Amsterdam | Roma | Milano | Paris | Lyon

6CONFIDENTIAL © 2017 SiaPartners Website: http://www.sia-partners.com | Blog: http://en.finance.sia-partners.com/

p a g e

Risk and Regulatory Quarterly Newsletter (HK, JP, and SG)Issue 9 – January 2017

Regulatory Updates

Hong Kong | Key HKMA Consultation Papers Source: HKMA

Date

Published Title Regulator’s Purpose and Objectives

4-Nov-16Consultation on Local Implementation of Net Stable Funding Ratio (NSFR)

This is a consultation paper on the local implementation of NSFR set out by theBasel Committee. The NSFR seeks to reduce banks’ funding risk over a longertime horizon by requiring banks to fund their activities with sufficiently stablesources of funding. HKMA proposes NSFR for category 1 institutions whilemodified NSFR for category 2 institutions. HKMA proposes to follow theimplementation timeline set by the BCBS, which is Jan-2018.

22-Nov-16Consultation on regulations for protected arrangements under Financial Institutions (Resolution) Ordinance

This is a consultation launched by HKMA, SFC and the Insurance Authority (IA)on a set of proposed regulations relating to protected arrangements under theFinancial Institutions (Resolution) Ordinance (Cap. 628). The proposedregulations seek to impose some suitably tailored constraints on the resolutionauthorities in the exercise of their resolution powers to safeguard the economiceffect of specific financial arrangements.

Hong Kong | Other Key HKMA Release Source: HKMA

Date

Published Title Regulator’s Purpose and Objectives

11-Nov-16White Paper On Distributed Ledger Technology

HKMA has commissioned the Hong Kong Applied Science and TechnologyResearch Institute (ASTRI) to conduct a research project on distributed ledgertechnology. This whitepaper lists out the research results.

Hong Kong | Key SFC Consultation Papers Source: SFC

Date

Published Title Regulator’s Purpose and Objectives

20-Sep-16

Consultation on Proposed Enhancements to the Position Limit Regime and the Associated Amendments to the Securities and Futures (Contracts Limits and Reportable Positions) Rules and Guidance Note on Position Limits and Large Open Position Reporting Require

This is a consultation paper on the SFC position limit regime. The key highlights ofthe proposal are as follow:(i) Raise the cap on the excess position limit that may be authorized by the SFCwould increase from 50% to 300% of the statutory position limit(ii) Proposed that the statutory position limit for stock options contracts will triple to150,000(iii) New excess position limits are proposed for index arbitrage activities, assetmanagers and market makers of exchange-traded funds

Hong Kong | Other Key SFC Release Source: SFC

Date

Published Title Regulator’s Purpose and Objectives

13-Oct-16SFC commences cybersecurity review on brokers’ internet and mobile trading systems

The SFC has launched a review to assess the cybersecurity preparedness,compliance and resilience of brokers’ internet and mobile trading systems. It findsthat in the past 12 months, 16 incidents were reported involving seven securitiesbrokers and total unauthorized trades in excess of $100 million.

Singapore | Key MAS Regulations Source: MAS

Date

Published Title Regulator’s Purpose and Objectives

6-Dec-16Guidelines on Margin Requirements for Non-Centrally Cleared OTC Derivatives Contracts

These Guidelines are issued by the Monetary Authority of Singapore (the“Authority”) pursuant to section 321 of the Securities and Futures Act (Cap. 289)(the “SFA”). The Guidelines set out the margin requirements for non-centrallycleared over-the-counter (“uncleared”) derivatives contracts.

8-Dec-16

Income tax act (chapter 134) income tax (international tax compliance agreements) (common reporting standard) regulations 2016

These Regulations implement the Standard for Automatic Exchange of FinancialAccount Information in Tax Matters (for the wider approach) developed andpublished by the Organisation for Economic Co-operation and Development,commonly known as the Common Reporting Standard (called in theseRegulations the CRS)

1

New York | London | Hong Kong | Singapore | Japan |Dubai | Abu Dhabi | Riyadh | Casablanca | Brussels | Amsterdam | Roma | Milano | Paris | Lyon

7CONFIDENTIAL © 2017 SiaPartners Website: http://www.sia-partners.com | Blog: http://en.finance.sia-partners.com/

p a g e

Risk and Regulatory Quarterly Newsletter (HK, JP, and SG)Issue 9 – January 2017

Regulatory Updates

Singapore | Key MAS Regulations (Con’t) Source: MAS

Date

Published Title Regulator’s Purpose and Objectives

10-Oct-16Guidelines on the Regulation of Clearing Facilities [Guideline No. SFA 03-G01]

The safe operation of a clearing facility requires a comprehensive identification ofrisks that arise within the clearing facility or through interdependencies with otherparticipants, as well as the ability to assess and effectively manage such risks. Ifthe clearing facility fails to properly manage its risks, it may seize up financialflows, undermine the fulfilment of obligations and transmit shocks from onefinancial institution to another. This would threaten the stability of the financialmarkets, and the broader economy. Given the importance of safety in preservingfinancial stability, MAS seeks to ensure the safe design and operation of clearingfacilities through regulation.

Singapore | Other Key MAS Release Source: MAS

Date

Published Title Regulator’s Purpose and Objectives

16-Nov-16MAS, R3 and Financial Institutions experimenting with Blockchain Technology

MAS announced that it is partnering R3, a Blockchain technology company, and aconsortium of financial institutions on a proof-of-concept project to conduct inter-bank payments using Blockchain technology. This project could potentially benefitpayment systems for participants to transact in different global markets round-the-clock that are today limited by time zone differences and office hours.

Standardized Approach For Counterparty Credit Risk Read More

Impact of the Trump Administration on the Banking Landscape Read More

PacNet Services: What you need to know Read More

GN17 Requirements will be enforced in January: Are You Ready? Read More

Regulations Pose New Challenges for Regulatory Report Production Processes Read More

Trending: biometrics for authentication Read More

Implementation of Third Party Risk Management Programs Read More

Anti-Money Laundering Risk in Trade Finance Read More

Life After Living Wills: How to Survive Dodd Frank’s Resolution Planning Requirement Read More

Latest Sia Partners’ Financial Blog Updates

About SiaPartners

Your Risk & RegulatoryContacts in Asia

Vincent KASBI

Head of Asia

David HOLLANDER

Head of Singapore

Makoto Suhara

Head of Japan

Helina LO

Project Director, Hong Kong

Victoria NG

Manager, Hong Kong

[email protected]@sia-partners.com