RETIREMENT INVESTMENTS INSURANCE Accumulation and Protection Planning Combo A Protection and...

20

RETIREMENT • INVESTMENTS • INSURANCE Accumulation and Protection Planning Combo A Protection and Retirement Strategy All In One.

-

Upload

everett-hutchinson -

Category

Documents

-

view

215 -

download

0

Transcript of RETIREMENT INVESTMENTS INSURANCE Accumulation and Protection Planning Combo A Protection and...

RETIREMENT • INVESTMENTS • INSURANCE

Accumulation and Protection Planning Combo

A Protection and Retirement Strategy All In One.

Important Disclosures

Accumulation and Protection Planning Combo is, first and foremost, a concept. It is not a product or contract.

These materials are not intended to and cannot be used to avoid tax penalties and they were prepared to support the promotion or marketing of the matters addressed in this document. Each taxpayer should seek advice from an independent tax advisor.

The ING Life Companies and their agents and representatives do not give tax or legal advice. This information is general in nature and not comprehensive; the applicable laws change frequently and the strategies suggested may not be suitable for everyone. Each taxpayer should seek advice from his or her tax and legal advisors regarding their individual situation.

CN0404-9224-0515

Are You Protecting Your Financial Future?

CN0404-9224-0515

The Realities We Face: Social Security and Federal Spending

CN0404-9224-0515

Additional Challenges – “The Need to Protect”

Premature Death: If your income stopped at your death, how would your family cope? A comprehensive financial strategy helps plan for these events and provides peace of mind.

Disability: Disability is something most people do not like to think about. However, the chances that you will become disabled are probably greater than you realize. Studies show that a 20-year-old worker has a 3-in-10 chance of becoming disabled before reaching full retirement age.

Longevity: For many, the time spent in retirement is longer than ever. With today’s medical advancements and healthier lifestyles, many Americans can expect to live much longer.

Health Care: Advances in medical research and technology have helped to create one of the world’s most modern health care systems. As the dialogue for how to pay for it all plays across the front pages of our newspapers and over the network airwaves, one thing is certain: as the chart notes, we will pay more and more for our healthcare costs.

CN0404-9224-0515

Additional Challenges – “The Need to Save”

Social Security

Personal Assets: Faced with the turbulent economy of recent years, millions of Americans the past few years have followed this financial strategy: “duck and cover.” That works well inside a boxing ring. Not so much when planning for a future that starts with a retirement you deserve.

Employer Sponsored Plans: Pension, Profit Sharing, 401(k), 403(b), SEP, SIMPLE

You Need to Avoid: Short-term decisions that lead to long-term financial mediocrity.

Retirement that leaves you wanting for more while living on less.

Planning that accounts for the expected while ignoring the potential for the unexpected.

CN0404-9224-0515

Possible Solutions

Work Longer - Retire Later

Increase Qualified Plan Contributions

Save More in Personal Assets

Work Longer - Retire Later

Increase Qualified Plan Contributions

Save More in Personal Assets

CN0404-9224-0515

Plus: Premature Death Can Devastate Your Financial Plans

If your income stopped because of your death, what would be the impact on your family?

Life insurance coverage on you may provide a “safety net”

ING’s Accumulation and Protection Planning Combo provides death benefit protection in an efficient manner, and may provide tax advantaged dollar, growing to give

you a supplemental income at retirement.

ING’s Accumulation and Protection Planning Combo provides death benefit protection in an efficient manner, and may provide tax advantaged dollar, growing to give

you a supplemental income at retirement.

CN0404-9224-0515

What IS Accumulation and Protection Planning Combo?

The Accumulation and Protection Planning Combo combines term life insurance and cash value life insurance to provide:

Death Benefit Protection for your family

Tax Advantaged Accumulation for your retirement

Death Benefit Protection for your family

Tax Advantaged Accumulation for your retirement

CN0404-9224-0515

Key Benefits of Life Insurance

Income Tax-free Death Benefit

Income Tax-deferred Growth Potential

Tax-free Supplemental Income

Flexible Premium Contributions

No IRS Distribution Requirements or Penalties

CN0404-9224-0515

Accumulation and Protection Planning Combo

CN0404-9224-0515

CN0404-9224-0515

Accumulation and Protection Planning Combo

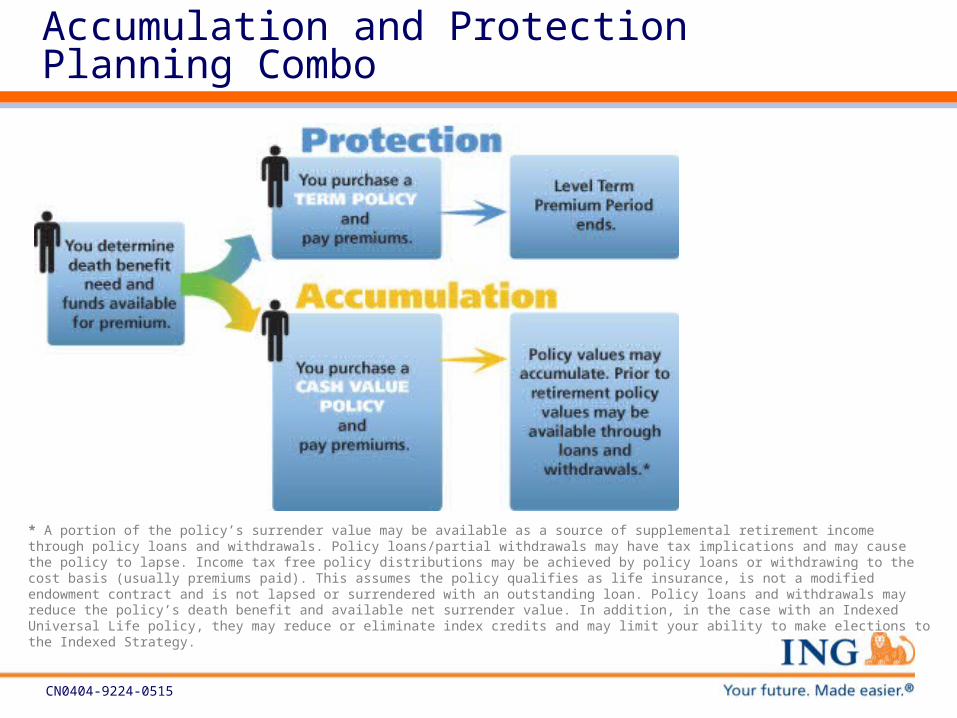

CN0404-9224-0515

Accumulation and Protection Planning Combo

* A portion of the policy’s surrender value may be available as a source of supplemental retirement income through policy loans and withdrawals. Policy loans/partial withdrawals may have tax implications and may cause the policy to lapse. Income tax free policy distributions may be achieved by policy loans or withdrawing to the cost basis (usually premiums paid). This assumes the policy qualifies as life insurance, is not a modified endowment contract and is not lapsed or surrendered with an outstanding loan. Policy loans and withdrawals may reduce the policy’s death benefit and available net surrender value. In addition, in the case with an Indexed Universal Life policy, they may reduce or eliminate index credits and may limit your ability to make elections to the Indexed Strategy.

* A portion of the policy’s surrender value may be available as a source of supplemental retirement income through policy loans and withdrawals. Policy loans/partial withdrawals may have tax implications and may cause the policy to lapse. Income tax free policy distributions may be achieved by policy loans or withdrawing to the cost basis (usually premiums paid). This assumes the policy qualifies as life insurance, is not a modified endowment contract and is not lapsed or surrendered with an outstanding loan. Policy loans and withdrawals may reduce the policy’s death benefit and available net surrender value. In addition, in the case with an Indexed Universal Life policy, they may reduce or eliminate index credits and may limit your ability to make elections to the Indexed Strategy.

CN0404-9224-0515

Accumulation and Protection Planning Combo

* A portion of the policy’s surrender value may be available as a source of supplemental retirement income through policy loans and withdrawals. Policy loans/partial withdrawals may have tax implications and may cause the policy to lapse. Income tax free policy distributions may be achieved by policy loans or withdrawing to the cost basis (usually premiums paid). This assumes the policy qualifies as life insurance, is not a modified endowment contract and is not lapsed or surrendered with an outstanding loan. Policy loans and withdrawals may reduce the policy’s death benefit and available net surrender value. In addition, in the case with an Indexed Universal Life policy, they may reduce or eliminate index credits and may limit your ability to make elections to the Indexed Strategy.

** Death proceeds from a life insurance policy are generally income tax-free and if properly structured, may be free from estate tax.

CN0404-9224-0515

Accumulation and Protection Planning Combo

How Does It Work – A Sample Situation

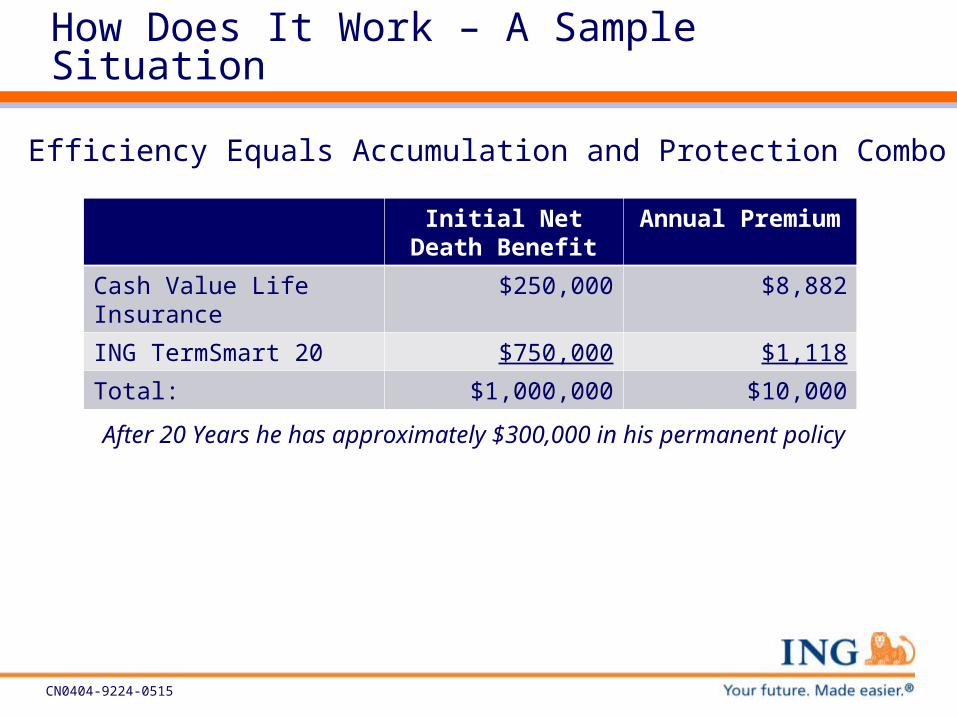

Male, Age 45

$1,000,000 death benefit need

$10,000 available to:• Purchase life insurance• Save for retirement

CN0404-9224-0515

How Does It Work – A Sample Situation

Efficiency Equals Accumulation and Protection Combo

After 20 Years he has approximately $300,000 in his permanent policy

Initial Net Death Benefit

Annual Premium

Cash Value Life Insurance $250,000 $8,882

ING TermSmart 20 $750,000 $1,118

Total: $1,000,000 $10,000

CN0404-9224-0515

How Does It Work – A Sample Situation

What if he put the $10,000 in a $1,000,000 permanent policy?

Efficiency Equals Accumulation and Protection Combo

Initial Net Death Benefit

Annual Premium

Cash Value Life Insurance $250,000 $8,882

ING TermSmart 20 $750,000 $1,118

Total: $1,000,000 $10,000

After 20 Years he has approximately $300,000 in his permanent policy

CN0404-9224-0515

How Does It Work – A Sample Situation

After 20 years he would have approximately $200,000 in his permanent policy

Efficiency Equals Accumulation and Protection Combo

Initial Net Death Benefit

Annual Premium

Cash Value Life Insurance $250,000 $8,882

ING TermSmart 20 $750,000 $1,118

Total: $1,000,000 $10,000

After 20 Years he has approximately $300,000 in his permanent policy

CN0404-9224-0515

What if he put the $10,000 in a $1,000,000 permanent policy?

ING Accumulation and Protection Combo

• You may need to accumulate more funds in order to retire

• You may also want your family to be secure if you die unexpectedly

• It may make sense to accomplish both goals in the same financial tool

CN0404-9224-0515