LIFE INSURANCE – LIFE PROTECTION FLEXI COMBO – ADMIRE …

25

LIFE INSURANCE – LIFE PROTECTION FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT BUILD YOUR SUCCESSFUL FUTURE Flexi Combo combining Admire Life 2, which is a participating life insurance plan, and Wisdom / Expert Term Life Supplementary Contract, which is a non-participating term protection plan, underwritten by AIA International Limited (Incorporated in Bermuda with limited liability). Citibank (Hong Kong) Limited is an appointed insurance agent for AIA International Limited (Incorporated in Bermuda with limited liability). This product brochure is issued by AIA and is for distribution by Citibank (Hong Kong) Limited in Hong Kong only. AIA International Limited (Incorporated in Bermuda with limited liability)

Transcript of LIFE INSURANCE – LIFE PROTECTION FLEXI COMBO – ADMIRE …

LIFE INSURANCE – LIFE PROTECTIONFLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

BUILD YOUR SUCCESSFUL FUTUREFlexi Combo combining Admire Life 2, which is a participating life insurance plan, and Wisdom / Expert Term Life Supplementary Contract, which is a non-participating term protection plan, underwritten by AIA International Limited (Incorporated in Bermuda with limited liability). Citibank (Hong Kong) Limited is an appointed insurance agent for AIA International Limited (Incorporated in Bermuda with limited liability). This product brochure is issued by AIA and is for distribution by Citibank (Hong Kong) Limited in Hong Kong only.

AIA International Limited (Incorporated in Bermuda with limited liability)

1 LIFE INSURANCE – LIFE PROTECTION

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

Customisable 2-in-1 Flexi Combo combining customised protection and wealth accumulation

1. Protection that you can customise Flexi Combo combines Admire Life 2 and Wisdom /

Expert Term Life Supplementary Contract in one customisable insurance combo plan. By adjusting the protection proportion of these 2 plans, you are able to tailor your plans according to your personal needs, to provide your desired protection levels, for example, 200%, 300%, 400% or other percentage of your total premium paid up to your desired age, that suits you the best.

Regarding limitation of Flexi Combo, please refer to point 2 of Additional Important Information – Flexi Combo.

of your total premium paid up to your desired age, for customised security to support your personal needs.

Flexi Combo consists of Admire Life 2 (basic plan) and Wisdom / Expert Term Life Supplementary Contract (add-on plan). Together, this 2-in-1 insurance combo plan provides flexibility to optimise your preferred protection level according to your protection need up to desired age, so you can tailor-made your own personal life protection insurance combo plan to protect your loved ones.

“AIA”, “AIA Hong Kong”, “the Company”, “We”, “our”, or “us” herein refers to AIA International Limited (Incorporated in Bermuda with limited liability).

In this modern world of opportunity, every success story is uniqueBe the author of your own successful future with our Flexi Combo, which would provide protection and wealth accumulation in one customisable insurance combo plan that you can tailor according to your needs.Choose your preferred protection level, for example, 200%, 300%, 400% or other percentage

2. Cover that changes with you As your circumstances shift from one life stage to the

next, your protection can be adjusted to reflect your changing financial goals. Under Wisdom / Expert Term Life Supplementary Contract, Super Lifestage Option can enhance your protection level of your add-on plan, meanwhile Conversion Privilege allows you to convert the add-on plan to a whole life insurance protection plan before age 70 without any further medical underwriting.

For details, please refer to the “Super Lifestage Option” and “Conversion Privilege” sections of this brochure, under the heading Introduction to Wisdom Term Life Supplementary Contract (“Wisdom Term Life”) & Expert Term Life Supplementary Contract (“Expert Term Life”).

3. Long-term capital growth Admire Life 2 provides you with guaranteed cash value,

non-guaranteed Annual Dividends and non-guaranteed Terminal Dividend, all of which form your policy values to help you optimise your wealth accumulation, so you and your loved ones can embrace the future with confidence.

For details, please refer to the “Accumulate wealth for a lifetime of prosperity” section of this brochure, under the heading Introduction to Admire Life 2.

2

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACTLIFE INSURANCE – LIFE PROTECTION

Introduction to Admire Life 2

Lifelong protection for your loved ones

Admire Life 2 provides lifetime insurance with stable returns. If the insured, who is the person protected under the policy, passes away, we will pay the death benefit to the person whom you select in your policy as beneficiary. The death benefit will include:

i. the sum assured of the basic plan under this policy;

ii. a non-guaranteed cash amounts distributed on a yearly basis, called Annual Dividends, which have accumulated with interest under this policy; plus

iii. a one-off non-guaranteed cash payment, called a Terminal Dividend (if any), provided that the policy has been in force for 10 years.

We will deduct all outstanding debt under your policy before we make the payment to the beneficiary.

Accumulate wealth for a lifetime of prosperity

Admire Life 2 is a participating insurance plan that provides you with guaranteed cash value, enabling you to accumulate wealth and secure a prosperous future for yourself and your family. In addition, we will provide you with a non-guaranteed cash amount distributed on a yearly basis, called Annual Dividends (if any).

We will also provide you with the non-guaranteed Terminal Dividend if:

i. you surrender the policy; or

ii. the insured passes away.

where the above situation occurs after the policy has been in force for 10 years.

Payment of the Terminal Dividend is not guaranteed. We determine the amount at our sole discretion and may be zero. The Terminal Dividend (if any) does not form a permanent addition to the policy and it may be increased or decreased at subsequent declarations.

Flexible premium payment terms

With Admire Life 2, you can select from four premium payment terms according to your personal financial needs. Premium amounts are guaranteed to be fixed throughout the payment period, making it easy for you to budget flexibly. For 5-year, 10-year, 18-year or 25-year premium payment terms, the premium can be paid annually or monthly.

Premium Payment Term

Insured’s Age at Policy Issue

Benefit Term

5 years 15 days to age 65

Whole life10 years 15 days to age 60

18 years 15 days to age 60

25 years 15 days to age 55

Extra cover for more protection

To support you in unfortunate circumstances, we will waive the future premium for Admire Life 2 if the insured becomes totally and permanently disabled before the age of 60. If the insured is from the People’s Republic of China or is a juvenile, we shall waive the future premium in the event of presumptive disability. Please refer to point 9 of the Additional Important Information section of Admire Life 2 for definition of presumptive disability and juvenile. This benefit will be subject to our underwriting decision.

A currency that suits youFor your convenience, we offer the basic plan under this policy in US dollars and HK dollars.

4

3 LIFE INSURANCE – LIFE PROTECTION

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

AIA knows how hard you have worked, that is why we have specially designed Wisdom Term Life & Expert Term Life, each a life protection insurance add-on plan with sum assured starting from US$25,000 or HK$187,500 (Wisdom Term Life) and US$500,000 or HK$3,750,000 (Expert Term Life) that provides more protection with the flexibility you deserve. Premiums are affordable and guaranteed to remain unchanged within each renewal period. Both plans are also renewable at the end of each renewal period up to the age of 85. In addition, both plans provide you with flexibility to purchase additional cover at pivotal moments in life and, in the advent of a mishap, your wealth can be passed to future generations. You and your beloved ones will all be better prepared, protected for life’s uncertainties and free to indulge every priceless moment together.

Different options to suit your needs

Wisdom Term Life / Expert Term Life provides two renewal periods for you to choose from: 5 years and 20 years. Pick one that best suits your needs so that you can plan ahead.

Wisdom Term Life & Expert Term Life

Renewal Period 5 years 20 years

Insured’s Age at Application 15 days - 65 15 days - 65

Protection for your loved ones

If the insured, who is the person protected under the policy, passes away, we will pay the death benefit to the person whom you select in your policy as beneficiary. The death benefit will be equal to 100% of the sum assured of the add-on plan under this policy.

We will deduct all outstanding amount you owe to us under your policy before we make the payment to the beneficiary.

Introduction to Wisdom Term Life Plan Supplementary Contract (“Wisdom Term Life”) & Expert Term Life Supplementary Contract (“Expert Term Life”)

Super Lifestage OptionYou may need better life insurance protection when you enter another stage of life. Wisdom Term Life / Expert Term Life offers you an option to purchase an additional term life insurance plan in the form of an additional add-on plan without requiring further health information upon any of the following milestone events:

• the insured obtains a property mortgage and draw down the mortgage loan (new purchase of residential property); or

• the insured’s marriage; or• the birth of a natural child of the insured (excluding

adoption).

You may exercise the Super Lifestage Option:

• once per milestone event but not more than two milestone events for the same insured;

• each purchase of the additional add-on plan must be separated by at least 2 consecutive years;

• after Wisdom Term Life / Expert Term Life has been in force for 2 years;

• on or before the anniversary of cover immediately following the insured’s 60th birthday;

• within 180 days from the date of the milestone events; and

• provided that no claim is submitted to us or has been made under this add-on plan.

The sum assured of each new additional add-on plan cannot exceed:

• US$500,000 or HK$3,750,000; or• 50% of the sum assured of Wisdom Term Life / Expert

Term Life; or• the mortgage loan amount obtained by the insured for

the new purchase of residential property,

whichever is lower.

Eligibility of this benefit is subject to underwriting requirements determined by us from time to time.

Please refer to point 5 of Additional Important Information – Wisdom / Expert Term Life Supplementary Contract for more details.

4

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACTLIFE INSURANCE – LIFE PROTECTION

Guaranteed RenewalWisdom Term Life / Expert Term Life guarantees that your premium will not be increased because of any changes in your health condition within each renewal period. This cover is guaranteed to be renewable at the end of each renewal period up to the age of 85 of the insured. Renewal premium of next renewal period will be based on the prevailing premium rates for the age of the insured at the time of renewal (Please refer to the “Premium Adjustment” under Key Product Risk for Wisdom / Expert Term Life Supplementary Contract).

Conversion PrivilegeOn or before the anniversary of cover immediately following the insured’s 70th birthday, Wisdom Term Life / Expert Term Life can be converted into a whole life protection insurance plan without requiring additional health information, subject to increase in premium and choices of products then made available by us for the purpose of this privilege.

A currency that suits youFor your convenience, we offer the add-on plan under this policy in US dollars and HK dollars.

5 LIFE INSURANCE – LIFE PROTECTION

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

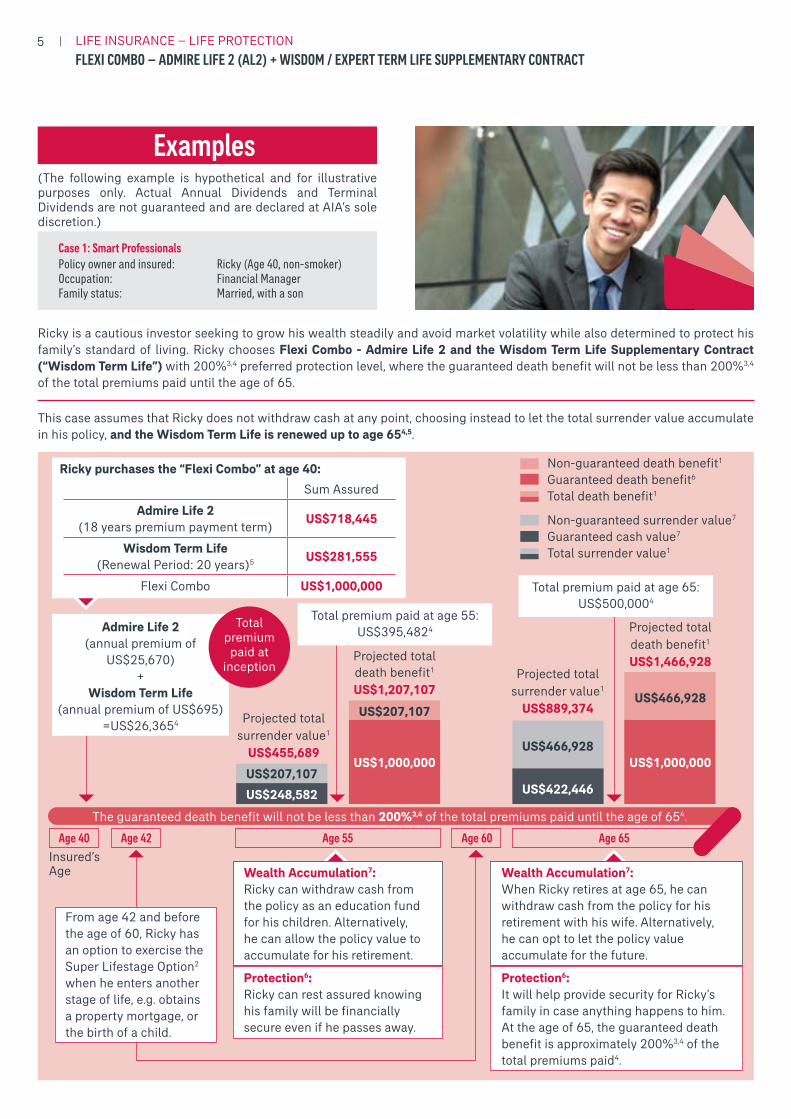

(The following example is hypothetical and for illustrative purposes only. Actual Annual Dividends and Terminal Dividends are not guaranteed and are declared at AIA’s sole discretion.)

Ricky is a cautious investor seeking to grow his wealth steadily and avoid market volatility while also determined to protect his family’s standard of living. Ricky chooses Flexi Combo - Admire Life 2 and the Wisdom Term Life Supplementary Contract (“Wisdom Term Life”) with 200%3,4 preferred protection level, where the guaranteed death benefit will not be less than 200%3,4 of the total premiums paid until the age of 65.

This case assumes that Ricky does not withdraw cash at any point, choosing instead to let the total surrender value accumulate in his policy, and the Wisdom Term Life is renewed up to age 654,5.

Examples

Case 1: Smart ProfessionalsPolicy owner and insured: Ricky (Age 40, non-smoker) Occupation: Financial Manager Family status: Married, with a son

Non-guaranteed death benefit1

Guaranteed death benefit6

Total death benefit1

Non-guaranteed surrender value7

Guaranteed cash value7

Total surrender value1

The guaranteed death benefit will not be less than 200%3,4 of the total premiums paid until the age of 654.

Sum Assured

Admire Life 2(18 years premium payment term)

US$718,445

Wisdom Term Life (Renewal Period: 20 years)5 US$281,555

Flexi Combo US$1,000,000

Ricky purchases the “Flexi Combo” at age 40:

From age 42 and before the age of 60, Ricky has an option to exercise the Super Lifestage Option2 when he enters another stage of life, e.g. obtains a property mortgage, or the birth of a child.

Wealth Accumulation7:Ricky can withdraw cash from the policy as an education fund for his children. Alternatively, he can allow the policy value to accumulate for his retirement.

Wealth Accumulation7:When Ricky retires at age 65, he can withdraw cash from the policy for his retirement with his wife. Alternatively, he can opt to let the policy value accumulate for the future.

Projected total death benefit1

US$1,207,107Projected total

surrender value1

US$889,374

Projected total death benefit1

US$1,466,928

US$207,107

US$466,928

US$207,107US$466,928

Age 40 Age 42 Age 55 Age 60 Age 65

US$422,446

US$1,000,000 US$1,000,000

Insured’s Age

Protection6:Ricky can rest assured knowing his family will be financially secure even if he passes away.

Protection6:It will help provide security for Ricky’s family in case anything happens to him. At the age of 65, the guaranteed death benefit is approximately 200%3,4 of the total premiums paid4.

Total premium paid at age 55:US$395,4824

Total premium paid at age 65:US$500,0004

Total premium

paid at inception

Admire Life 2(annual premium of

US$25,670)+

Wisdom Term Life(annual premium of US$695)

=US$26,3654 Projected totalsurrender value1

US$455,689

US$248,582

6

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACTLIFE INSURANCE – LIFE PROTECTION

1. The total surrender value of Flexi Combo illustrated is the sum of the policy’s guaranteed cash value plus accumulated non-guaranteed surrender value under Admire Life 2 (i.e. the non-guaranteed Annual Dividends with interest and the non-guaranteed Terminal Dividend); while the total death benefit of Flexi Combo illustrated is the sum of the sum assured of Admire Life 2 and Wisdom Term Life plus non-guaranteed death benefit under Admire Life 2 (i.e. the non-guaranteed Annual Dividends with interest and the non-guaranteed Terminal Dividend). The value is based on the current dividend scales and accumulation interest rate of 3.5% p.a. on Annual Dividends. The current dividend scales and interest rates are neither indicative of future performance nor guaranteed. Past performance or current performance of our business should not be interpreted as a guide for future performance. The actual Annual Dividends, accumulation interest rates and Terminal Dividend payable throughout the duration of the policy may vary at AIA’s sole discretion, which may be less or more favourable than those illustrated. The above example assumes that no cash withdrawal or policy loans are taken throughout the term of the policy and that all premiums are paid in full when due. To receive the amounts illustrated, the policy owner must surrender his policy at the end of the respective policy year. This policy will be terminated when the total surrender value has been withdrawn entirely.

2. The policy owner may exercise his right under the Super Lifestage Option within 180 days after each milestone event. The policy owner may purchase an additional add-on plan pursuant to the Super Lifestage Option for a maximum of two times. The sum assured of each additional term life add-on plan shall not exceed (i) US$500,000 or HK$3,750,000; (ii) 50% of the sum assured of the Wisdom Term Life; or (iii) the mortgage loan amount obtained by the insured for such new purchase of residential property, whichever is lower. Please refer to the “Super Lifestage Option” in the product brochure for details.

3. The ratio of total guaranteed death benefit to total premium paid varies over the policy term, please refer to the respective illustration for details.

4. The renewal premium of the Wisdom Term Life is not guaranteed. Please refer to the “Premium Adjustment” under Key Product Risk for Wisdom Term Life Supplementary Contract for details. As such, the actual total premium paid or protection level may be different from the values illustrated above.

5. The Wisdom Term Life is defaulted to be renewed up to age 85 by paying the renewal premium at each renewal period, to continue the protection. Renewal premium of each renewal period will be based on the prevailing premium rates for the insured’s age at the time of renewal. If you do not renew the Wisdom Term Life upon the end of renewal period, you will lose the protection.

6. The guaranteed death benefit of Flexi Combo includes both guaranteed death benefit of Admire Life 2 and Wisdom Term Life.

7. Wisdom Term Life is an insurance plan without any savings element. The total surrender value of Flexi Combo includes guaranteed cash value and non-guaranteed surrender value of Admire Life 2 only.

7 LIFE INSURANCE – LIFE PROTECTION

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

Having become a successful entrepreneur, Alan plans to accumulate sufficient wealth to enjoy a high-quality retirement at age 65 while also utilises his money to its full potential to help him fulfil various life goals. Alan chooses Flexi Combo - Admire Life 2 and the Expert Term Life Supplementary Contract (“Expert Term Life”) with 300%3,4 preferred protection level, where the guaranteed death benefit will not be less than 300%3,4 of the total premiums paid until the age of 65.

Case 2: Savvy AchieversPolicy owner and insured: Alan (Age 50, non-smoker) Occupation: Entrepreneur Family status: Married, with 2 sons

Non-guaranteed death benefit1

Guaranteed death benefit6

Total death benefit1

Non-guaranteed surrender value7

Guaranteed cash value7

Total surrender value1

Sum Assured

Admire Life 2(5 years premium payment term) US$851,621

Expert Term Life (Standard) (Renewal Period: 5 years)5 US$1,148,379

Flexi Combo US$2,000,000

Alan purchases the “Flexi Combo” at age 50:

Insured’s Age

The guaranteed death benefit will not be less than 300%3,4 of the total premiums paid until the age of 654.

The Customer has the flexibility to decide on the renewal of Expert Term Life every 5 years until the Age of 855.

On or before the age of 70, Alan has an option to exercise Conversion privilege2 to convert his Expert Term Life into a whole life plan, without the need to provide further health information.

Wealth Accumulation7:When Alan retires at age 65, he can withdraw cash from the policy for his retirement with his wife. Alternatively, he can opt to let the policy value accumulate for the future.

Wealth Accumulation7:At age 85, Alan can withdraw cash from the policy for his son to purchase property or develop his career.

Total premium paid at age 85:US$1,828,4824

Projected total death benefit1

US$2,373,797

Projected totalsurrender value1

US$2,364,470

Projected total death benefit1

US$3,632,076

US$1,632,076

US$373,797

US$1,632,076

Age 50 Age 65 Age 70 Age 85

US$732,394

US$2,000,000 US$2,000,000

Protection6:Alan can rest assured knowing his family will be financially secure even if he passes away.

Protection6:It will help provide security for Alan’s family in case anything happens to him.

Admire Life 2 (annual premium of US$111,767)+

Expert Term Life (annual premium of US$4,123)=US$115,8894

Total premium paid at age 65: US$666,6674

Projected totalsurrender value1

US$919,686

US$545,889US$373,797

Total premium

paid at inception

This case assumes that Alan does not withdraw cash at any point, choosing instead to let the total surrender value accumulate in his policy, and the Expert Term Life is renewed up to age 854.

8

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACTLIFE INSURANCE – LIFE PROTECTION

1. The total surrender value of Flexi Combo illustrated is the sum of the policy’s guaranteed cash value plus accumulated non-guaranteed surrender value under Admire Life 2 (i.e. the non-guaranteed Annual Dividends with interest and the non-guaranteed Terminal Dividend); while the total death benefit of Flexi Combo illustrated is the sum of the sum assured of Admire Life 2 and Expert Term Life plus non-guaranteed death benefit under Admire Life 2 (i.e. the non-guaranteed Annual Dividends with interest and the non-guaranteed Terminal Dividend). The value is based on the current dividend scales and accumulation interest rate of 3.5% p.a. on Annual Dividends. The current dividend scales and interest rates are neither indicative of future performance nor guaranteed. Past performance or current performance of our business should not be interpreted as a guide for future performance. The actual Annual Dividends, accumulation interest rates and Terminal Dividend payable throughout the duration of the policy may vary at AIA’s sole discretion, which may be less or more favourable than those illustrated. The above example assumes that no cash withdrawal or policy loans are taken throughout the term of the policy and that all premiums are paid in full when due. To receive the amounts illustrated, the policy owner must surrender his policy at the end of the respective policy year. This policy will be terminated when the total surrender value has been withdrawn entirely.

2. The policy owner can apply to exercise the conversion privilege on or before the age of 70.

3. The ratio of total guaranteed death benefit to total premium paid varies over the policy term, please refer to the respective illustration for details.

4. The renewal premium of the Expert Term Life is not guaranteed. Please refer to the “Premium Adjustment” under Key Product Risk for Expert Term Life Supplementary Contract for details. As such, the actual total premium paid or protection level may be different from the values illustrated above.

5. The Expert Term Life is defaulted to be renewed up to age 85 by paying the renewal premium at each renewal period, to continue the protection. Renewal premium of each renewal period will be based on the prevailing premium rates for the insured’s age at the time of renewal. If you do not renew the Expert Term Life upon the end of renewal period, you will lose the protection.

6. The guaranteed death benefit of Flexi Combo includes both guaranteed death benefit of Admire Life 2 and Expert Term Life.

7. Expert Term Life is an insurance plan without any savings element. The total surrender value of Flexi Combo includes guaranteed cash value and non-guaranteed surrender value of Admire Life 2 only.

9 LIFE INSURANCE – LIFE PROTECTION

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

Important Information of Flexi ComboThis brochure is for reference only. It is not, and does not form part of, a contract of insurance and is designed to provide an overview of the key features of these products. The precise terms and conditions of these plans are specified in the policy contract. Please refer to the policy contract for the definitions of capitalised terms, and the exact and complete terms and conditions of cover. This brochure should be read along with the illustrative document and other relevant marketing materials, which include additional information and important considerations about these products. We would like to remind you to review the relevant product materials provided to you and seek independent professional advice if necessary.

Wisdom Term Life / Expert Term Life is an insurance plan without any savings element. All premiums are paid for the insurance and related cost.

This brochure is for distribution in Hong Kong only.

Dividend Philosophy of Admire Life 2

This is a participating insurance plan designed to be held long term. Your premiums will be invested in a variety of assets according to our investment strategy, with the cost of policy benefits and expenses deducted as appropriate from premiums or assets. Your policy can share the divisible surplus (if any) from related product groups determined by us. We aim to ensure a fair sharing of profits between policy owners and shareholders, and among different groups of policy owners.

Future investment performance is unpredictable. Through our smoothing process, we aim to deliver more stable dividend payments by spreading out the gains and losses over a longer period of time. Stable dividend payments will ease your financial planning.

We will review and determine the dividend amounts to be payable to policy owners at least once per year. The actual dividends declared may be different from those illustrated in any product information provided (e.g. benefit illustrations). If there are any changes in the actual dividends against the illustration or in the projected future dividends, such changes will be reflected in the policy anniversary statement.

A committee has been set up to provide independent advice on the determination of the dividend amounts to the Board of the Company. The committee is comprised of members from different control functions or departments within the organisation both at AIA Group level as well as Hong Kong local level, such as office of the Chief Executive, legal, compliance, finance and risk management. Each member of the committee will exercise due care, diligence and skill in the performance of his or her duties as a member. The committee will utilise the knowledge, experience, and perspectives of each individual member to assist the Board in the discharge of its duty to make independent decision and to manage the risk of conflict of interests, in order to ensure fair treatment between policy owners and shareholders, and among different groups of policy owners. The actual dividends, which are recommended by the Appointed Actuary, will be decided upon the deliberation of the committee and finally approved by the Board of Directors of the Company, including one or more Independent Non-Executive Directors.

To determine the dividends of the policy, we consider both past experiences and the future outlook for all the factors including, but not limited to, the following:

Investment returns: include interest earnings, dividends and any changes in the market value of the product’s backing assets. Depending on the asset allocation adopted for the product, investment returns could be affected by fluctuations in interest income (both interest earnings and the outlook for interest rates) and various market risks, including credit spread and default risk, fluctuations in equity prices, property prices and foreign exchange currency fluctuation of the backing asset against the policy currency.

Claims: include the cost of providing death benefits and other insured benefits under the product(s).

Surrenders: include policy surrenders, partial surrenders and policy lapses; and the corresponding impact on the investments backing the product(s).

Expenses: include both expenses directly related to the policy (e.g. commission, underwriting, issue and premium collection expenses) and indirect expenses allocated to the product group (e.g. general administrative costs).

10

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACTLIFE INSURANCE – LIFE PROTECTION

For further information, please visit our website at http://www.aia.com.hk/en/dividend-philosophy.html

For the historical fulfillment ratio, please visit our website at http://www.aia.com.hk/en/fulfillment-ratio.html

Dividend and Bonus Philosophy

Historical Fulfillment Ratio

Investment Philosophy, Policy and Strategy of Admire Life 2

Our investment philosophy is to deliver stable returns in line with the product’s investment objectives and AIA’s business and financial objectives.

Our investment policy aims to achieve the targeted long-term investment results and minimise volatility in investment returns over time. It also aims to control and diversify risk exposures, maintain adequate liquidity and manage the assets with respect to the liabilities.

Our current long-term target strategy is to allocate assets attributed to this product as follows:

Asset Class Target Asset Mix (%)

Bonds and

other fixed income instruments60% - 80%

Equity-like assets 20% - 40%

Our investment strategy is to actively manage the investment portfolio i.e.: adjust the asset mix in response to the external market conditions. The proportion of equity-like assets would be lower when interest rate level is low and would be even lower than the long-term target strategy so to protect the guaranteed liability and to minimise volatility in investment returns over time, and vice versa when interest rate is high.

The bonds and other fixed income instruments predominantly include government and corporate bonds, and are mainly invested in the geographic region of the United States and Asia-Pacific (excluding Japan). Equity-like assets may include listed equity, mutual funds and direct / indirect investment in commercial / residential properties, and are mainly invested in Asia. Subject to our investment policy, derivatives may be utilised to manage our investment risk exposure and for matching between assets and liabilities.

Our currency strategy is to minimise currency mismatches. For bonds or other fixed income instruments, our current practice is to currency-match their bond purchases with the underlying policy denomination on best-efforts basis (i.e.: US Dollar assets will be used to support US Dollar liabilities and HK Dollar assets will be used to support HK Dollar liabilities). Subject to market availability and opportunity, bonds may be invested in currency other than the underlying policy denomination and currency swap will be used to minimise the currency risks. Currently assets are mainly invested in US Dollar. For equity-like assets, currency exposure depends on the geographic location of the underlying investment where the selection is done according to our investment philosophy, investment policy and mandate.

We will pool the investment returns from other long term insurance products (excluding investment linked assurance schemes and pension schemes) together with this participating insurance plan for determining the actual investment and the return will subsequently be allocated with reference to the target asset mix of the respective participating products. Actual investments (e.g. geographical mix, currency mix) would depend on market opportunities at the time of purchase. Hence it may differ from the target asset mix.

The investment strategy may be subject to change depending on the market conditions and economic outlook. Should there be any material changes in the investment strategy, we will inform policy owners of the changes, with underlying reasons and impact to the policies.

11 LIFE INSURANCE – LIFE PROTECTION

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

Key Product Risks

Admire Life 2

1. You should pay premium(s) on time and according to the selected premium payment schedule. If you stop paying the premium before completion of the premium payment term, you may elect one of the non-forfeiture options to surrender the basic plan or convert the basic plan to a non-participating insurance plan with life protection only. Compared with the original plan, such a plan will have less cover or a shorter term.

If no non-forfeiture option has been elected, the premium will be covered by a loan taken out on the policy automatically for one year so long as the sum of guaranteed cash value and accumulated Annual Dividends with interest (if any) of the basic plan is sufficient to cover the premium in default and any outstanding debt. Afterwards, we will use the remaining cash value to convert to a non-participating insurance plan with life protection only.

2. The savings component of the plan is subject to risks and possible loss. Should you surrender the policy early, you may receive an amount considerably less than the total amount of premiums paid.

3. We will terminate your policy and you / the insured will lose the cover when one of the following happens:

• the insured passes away;

• you do not pay the premium within 31 days of the due date and the policy has no cash value;

• the end of the benefit term if basic policy has been continued as a non-participating insurance plan; or

• the outstanding debt exceeds the guaranteed cash value of your policy. In the case of premium is covered by a loan taken out on the policy automatically, the outstanding debt exceeds the sum of guaranteed cash value and accumulated Annual Dividends with interest (if any) of your policy.

Wisdom / Expert Term Life Supplementary Contract

1. You need to pay the premium for this add-on plan as long as policy owner renews until age 85 or when the basic plan it is attached to is terminated, whichever is earlier. If you do not pay the premium within 31 days of the premium due date, the add-on plan will be terminated and you / the insured will lose the cover.

2. We will terminate your add-on plan and you / the insured will lose the cover when one of the following happens:

• the insured passes away;

• you do not pay the premium within 31 days of the premium due date;

• basic plan has been terminated or converted to a non-participating insurance plan; or

• anniversary of your cover immediately following the insured’s 85th birthday.

3. Total premiums payable may be greater than the sum assured.

4. Premium Adjustment

In order to provide you with continuous protection, we will review the premium of your add-on plan from time to time and adjust it accordingly at the end of each renewal period if necessary. During the review, we may consider factors including but not limited to the following:

• claim costs incurred from all policies under this add-on plan and the expected claim outgo in the future which reflects the impact of change in the incidence rate of death;

• historical investment returns and the future outlook of the product’s backing asset;

• policy surrenders and lapses expenses directly related to the add-on plan and indirect expenses allocated to this product.

12

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACTLIFE INSURANCE – LIFE PROTECTION

Flexi Combo

Credit Risk

We underwrite the plans and you are subject to our credit risk. If we are unable to satisfy the financial obligations of the policy, you may lose your premium paid and benefits.

Exchange Rate Risk

You are subject to exchange rate risks for plans denominated in currencies other than the local currency. Exchange rates fluctuate from time to time. You may suffer a loss of your benefit values and the subsequent premium payments (if any) may be higher than your initial premium payment as a result of exchange rate fluctuations. You should consider the exchange rate risks and decide whether to take such risks.

Inflation Risk

Your current planned benefit may not be sufficient to meet your future needs since the future cost of living may become higher than they are today due to inflation. Where the actual rate of inflation is higher than expected, you may receive less in real terms even if we meet all of our contractual obligations.

Suicide

If the insured commits suicide within one year from the date on which the policy takes effect, our liability will be limited to the refund of premiums paid (without interest) less any outstanding debt.

Incontestability

Except for fraud or non-payment of premiums, we will not contest the validity of this policy after it has been in force during the lifetime of the insured for a continuous period of two years from the date on which the policy takes effect. This provision does not apply to any add-on plan providing accident, hospitalisation or disability benefits.

Warning Statement

Admire Life 2 is an insurance plan with a savings element. Part of the premium pays for the insurance and related costs. On the other hand, Wisdom Term Life / Expert Term Life is a term life insurance plan without any savings element. All premiums are paid for the insurance and related costs. If you are not happy with your policy, you have a right to cancel it within the cooling-off period and obtain a refund of any premiums and any levy paid. A written notice signed by you should be received by AIA’s Hong Kong Main Office at 1/F, AIA Hong Kong Tower, 734 King’s Road, Quarry Bay, Hong Kong within the cooling-off period (that is, 21 calendar days immediately following either the day of delivery of the policy or the Cooling-off Notice to you or your nominated representative, whichever is earlier). After the expiration of the cooling-off period, if you cancel the policy before the end of the term, the projected total cash value may be less than the total premium you have paid.

13 LIFE INSURANCE – LIFE PROTECTION

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

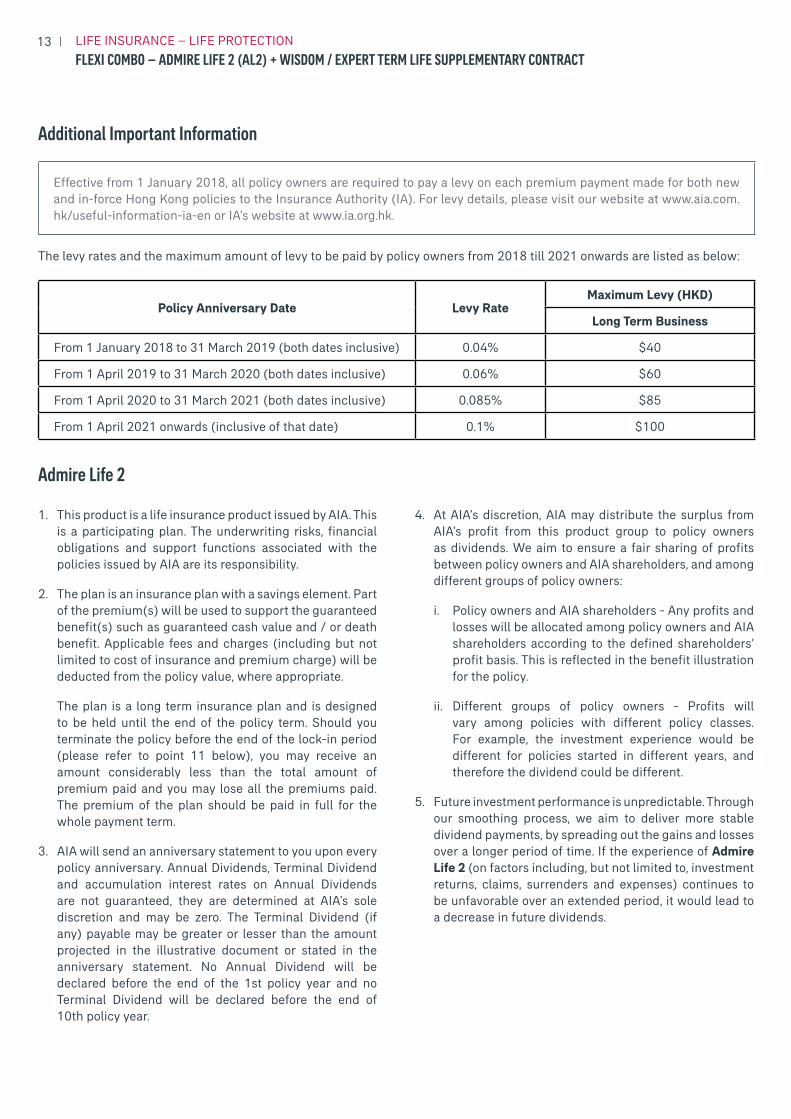

Additional Important Information

Effective from 1 January 2018, all policy owners are required to pay a levy on each premium payment made for both new and in-force Hong Kong policies to the Insurance Authority (IA). For levy details, please visit our website at www.aia.com.hk/useful-information-ia-en or IA’s website at www.ia.org.hk.

The levy rates and the maximum amount of levy to be paid by policy owners from 2018 till 2021 onwards are listed as below:

Policy Anniversary Date Levy RateMaximum Levy (HKD)

Long Term Business

From 1 January 2018 to 31 March 2019 (both dates inclusive) 0.04% $40

From 1 April 2019 to 31 March 2020 (both dates inclusive) 0.06% $60

From 1 April 2020 to 31 March 2021 (both dates inclusive) 0.085% $85

From 1 April 2021 onwards (inclusive of that date) 0.1% $100

Admire Life 2

1. This product is a life insurance product issued by AIA. This is a participating plan. The underwriting risks, financial obligations and support functions associated with the policies issued by AIA are its responsibility.

2. The plan is an insurance plan with a savings element. Part of the premium(s) will be used to support the guaranteed benefit(s) such as guaranteed cash value and / or death benefit. Applicable fees and charges (including but not limited to cost of insurance and premium charge) will be deducted from the policy value, where appropriate.

The plan is a long term insurance plan and is designed to be held until the end of the policy term. Should you terminate the policy before the end of the lock-in period (please refer to point 11 below), you may receive an amount considerably less than the total amount of premium paid and you may lose all the premiums paid. The premium of the plan should be paid in full for the whole payment term.

3. AIA will send an anniversary statement to you upon every policy anniversary. Annual Dividends, Terminal Dividend and accumulation interest rates on Annual Dividends are not guaranteed, they are determined at AIA’s sole discretion and may be zero. The Terminal Dividend (if any) payable may be greater or lesser than the amount projected in the illustrative document or stated in the anniversary statement. No Annual Dividend will be declared before the end of the 1st policy year and no Terminal Dividend will be declared before the end of 10th policy year.

4. At AIA’s discretion, AIA may distribute the surplus from AIA’s profit from this product group to policy owners as dividends. We aim to ensure a fair sharing of profits between policy owners and AIA shareholders, and among different groups of policy owners:

i. Policy owners and AIA shareholders - Any profits and losses will be allocated among policy owners and AIA shareholders according to the defined shareholders’ profit basis. This is reflected in the benefit illustration for the policy.

ii. Different groups of policy owners - Profits will vary among policies with different policy classes. For example, the investment experience would be different for policies started in different years, and therefore the dividend could be different.

5. Future investment performance is unpredictable. Through our smoothing process, we aim to deliver more stable dividend payments, by spreading out the gains and losses over a longer period of time. If the experience of Admire Life 2 (on factors including, but not limited to, investment returns, claims, surrenders and expenses) continues to be unfavorable over an extended period, it would lead to a decrease in future dividends.

14

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACTLIFE INSURANCE – LIFE PROTECTION

6. Cash withdrawals made will be deducted first from the accumulated Annual Dividends with interest (if any). Any further withdrawal which exceeds the remaining balance of the accumulated Annual Dividends with interest (if any) will be deemed as partial surrender of the basic plan and may lead to reduction of the sum assured of the basic plan. Such further withdrawal will be deducted from the guaranteed cash value and Terminal Dividend entitlement accrued (if any) (from and after the end of the 10th policy year), given upon such surrender. Therefore, the subsequent guaranteed cash value, Annual Dividends (if any) and Terminal Dividend (if any) will be adjusted accordingly based on the reduced sum assured.

7. The basic plan is subject to AIA’s minimum sum assured requirements as determined by AIA from time to time, and no withdrawal will be allowed which has the effect of reducing the sum assured of the basic plan below the minimum sum assured required.

8. All guaranteed and non-guaranteed elements (if any) and benefits of insurance policy are subject to the credit risk of AIA and the payments of such benefits and performance of the insurance policy are the obligations and liabilities of AIA. In the worst case, you may lose all the premium paid and benefit amount.

Policy benefits are not the obligation of any insurance agency or distributor selling or distributing the policy, or by any of their affiliates, and none of them makes any representation or guarantees regarding the claims-paying ability of AIA. AIA is responsible for its own financial condition and contractual obligations. Policy owners bear the default risk in the event that AIA is unable to satisfy its financial obligations under the insurance policy(ies).

9. Presumptive disability means the occurrence of any of the following: i) total and irrecoverable loss of sight of BOTH eyes; ii) severance of TWO limbs at or above wrist or ankle; or iii) total and irrecoverable loss of sight of ONE eye and loss by severance of ONE limb at or above the wrist or ankle. An insured ceases to be a juvenile when either after the age of 16 he / she becomes gainfully employed or self-employed; or he / she attains 18 years of age.

10. Add-on plans / riders means supplementary contracts as stated in the policy contract. Additional add-on plan means additional term life insurance purchased through Super Lifestage Option.

11. The reference to “Lock-in period” of basic plan (if any) is the breakeven policy year in which guaranteed cash value equals total premium paid under basic plan as illustrated in the illustrative document. The guaranteed breakeven policy year varies according to the plan currency, sum assured, premium payment term and the issue age, gender and smoking habits of the insured. Please refer to the illustration for the lock-in period applicable to your Admire Life 2 policy. Early surrender or termination of your policy before the end of the lock-in period may result in losses in that you may get back considerably less than your premiums paid.

12. Admire Life 2 does not provide single premium under Flexi Combo.

13. If premium remains unpaid 31 days after the premium due date, you may elect one of the non-forfeiture options to surrender the basic plan or convert the basic plan to a non-participating insurance plan with life protection only. Compared with the original plan, such a plan will have less cover or a shorter term.

If no non-forfeiture option has been elected, AIA will advance the premium due as an automatic loan for one year so long as the sum of guaranteed cash value and accumulated Annual Dividends with interest (if any) of the basic plan is sufficient to cover the premium in default and any outstanding debt. Afterwards, we will use the remaining cash value to convert to a non-participating insurance plan with life protection only.

You can also apply for a policy loan and borrow up to 100% of the guaranteed cash value of the policy. Where a policy loan is available and taken out, interest on the policy loan will be charged at a rate solely determined by us from time to time. Interest on loan amounts accrue on a daily basis and are due on each policy anniversary. Any interest unpaid when due will be added to the outstanding loan amount. The unpaid loan or policy debt (if any) on the policy will be deducted from the payment or proceeds (if any) under the policy. If the total outstanding loan amounts (including interest) owing to AIA under this policy (if any) exceed the guaranteed cash value of the policy, the policy will be terminated. In the case of premium is covered by a loan taken out on the policy automatically, if the outstanding loan amounts (including interest) exceed the sum of guaranteed cash value and accumulated Annual Dividends with interest (if any) of your policy, the policy will be terminated.

14. Total surrender value / total cash value refer to the same value and these terms are used interchangeably.

15. Benefit illustration / illustrative document / proposal refer to the same document and these terms are used interchangeably.

15 LIFE INSURANCE – LIFE PROTECTION

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

Wisdom / Expert Term Life Supplementary Contract

1. This product is a term life insurance product issued by AIA. This is a non-participating plan. The underwriting risks, financial obligation and support functions associated with the policies issued by AIA are its responsibility.

2. All guaranteed and non-guaranteed elements (if any) and benefits of insurance policy are subject to the credit risk of AIA and the payments of such benefits and performance of the insurance policy are the obligations and liabilities of AIA. In the worst case, you may lose all the premium and benefit amount.

Policy benefits are not the obligation of any insurance agency or distributor selling or distributing the policy, or by any of their affliates, and none of them makes any representation or guarantees regarding the claims-paying ability of AIA. AIA is responsible for its own financial condition and contractual obligations. Policy owners bear the default risk in the event that AIA is unable to satisfy its financial obligations under the insurance policy(ies).

3. Add-on plans / riders means supplementary contracts as stated in the policy contract. Additional add-on plan means additional term life insurance purchased through Super Lifestage Option.

4. Eligibility of Conversion Privilege and Guaranteed Renewal is subject to AIA’s underwriting requirement at policy inception, and such requirement is to be determined by AIA from time to time.

5. Super Lifestage Option is not available to Business Insurance or Wisdom / Expert Term Life Supplementary Contract with extra premium required due to insured’s nationality, medical or occupational rating. Eligibility of Super Lifestage Option is subject to AIA’s underwriting requirement at policy inception, and such requirement is to be determined by AIA from time to time.

Flexi Combo

1. The ratio of total guaranteed death benefit to total premium paid is varied over the policy term, please refer to the respective illustration for details.

2. The protection level under Flexi Combo will change throughout the policy term, please refer to the respective illustration for details. It may not be equal to the preferred protection level you chosen. The range of protection level you can choose under Flexi Combo varies according to the insured’s age at issue, gender, usual residence, health status, policy option, smoking status, occupation and desired age. Therefore, it may not exactly reflect 200%, 300% & 400% and might be higher or lower.

3. The add-on plan is defaulted to be renewed up to age 85 by paying the renewal premium at each renewal period, to continue the protection. Renewal premium of each renewal period will be based on the prevailing premium rates for the insured’s age at the time of renewal. If you do not renew the add-on plan upon the end of renewal period, you will lose the protection.

4. The policy currency of this plan offers in Hong Kong dollars (HKD) or in US dollars (USD). For USD, any exchange rate fluctuation will have a direct impact on the amount of premium required and the value of your benefit(s) in Hong Kong dollar terms.

Any transaction involving currencies involves risks including, but not limited to, the potential for changing political and / or economic conditions that may substantially affect the price or liquidity of a currency. Policy owner should pay heed to the presence of the potential currency risks and decide whether to take such risks.

5. The above product information should be used with the understanding that AIA is not rendering legal, accounting or tax advice. You are advised to check with your personal tax advisor for advice relevant to your circumstances.

6. AIA is the insurance underwriter of these insurance plans and is solely responsible for all approvals, coverage and compensations of their insurance plans. All insurance applications are subject to AIA’s underwriting and acceptance. AIA reserves the final right to approve any policy application. In case the policy application is declined, AIA will make full refund of the actual amount of premium and any levy paid by the customer without interest. AIA shall assume full responsibility for the contracts of respective insurance plans.

16

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACTLIFE INSURANCE – LIFE PROTECTION

7. If your application omits facts or contains materially incorrect or incomplete facts, AIA has the right to declare the policy void.

8. Whether to apply for insurance coverage is your own individual decision.

9. Claims under the plan must be made to AIA directly. You can get the appropriate claims forms by calling the AIA Customer Hotline (852) 2232 8808 in Hong Kong or by visiting www.aia.com.hk or any AIA Customer Service Centre. Please refer to the policy contract for details of claim procedure.

10. Citibank (Hong Kong) Limited’s role is limited to distributing the insurance product only and Citibank (Hong Kong) Limited shall not be responsible for any matters in relation to the products provided (including but not limited to account / policy maintenance matters).

Please contact the relevant licensed bank staff or call AIA Customer Hotline for details

AIA Hong Kong and Macau

AIA_HK_MACAUaia.com.hk

Hong Kong (852) 2232 8808

(on Hong Kong mobile network only)*1299

17 LIFE INSURANCE – LIFE PROTECTION

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

AIA Vitality is a wellness programme which aims to reward customers to live a healthy lifestyle.

Earn rewards for your healthy lifestylePurchase a selected AIA Vitality insurance product and be an AIA Vitality member1 to receive an instant 10% premium discount2 and an array of rewards and discounts offered by our partners. As long as you keep up a healthy lifestyle, you can even enjoy a minimum 10% premium discount each year3.

Simply being active in daily life and having a healthy diet, you can earn points and upgrade your status for more discounts and rewards.

18

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACTLIFE INSURANCE – LIFE PROTECTION

Remarks:1. The applicants for AIA Vitality must be aged 18 or above and must be the life insured of the in-force policy of an AIA Vitality selected

insurance product . 2. Premium discount is only applicable to the standard premiums of selected AIA Vitality insurance product and shall not apply to

any extra premiums due to loading. In all circumstances, the premium discount will be calculated in accordance with the insured’s AIA Vitality Status achieved on each policy anniversary. The policy anniversary of AIA Vitality selected insurance products and AIA Vitality membership anniversary may not be the same. For details and offers of AIA Vitality selected insurance products, please visit aia.com.hk/aiavitality.

3. To enjoy a 10% premium discount each year, members must become Gold Members during their first year and maintain Gold Status from then on.

4. Members will enjoy 15% premium discount in the subsequent year of policy renewal if they currently enjoy 10% premium discount and maintain the Platinum Status for 5 consecutive years.

5. AIA Vitality gives the member access to an array of rewards and discounts offered by our partners. For up-to-date information on each benefit, please visit aia.com.hk/aiavitality. Partners and benefits may vary at any time without prior notice.

6. An annual membership fee will be charged for AIA Vitality and a member has to renew the AIA Vitality membership annually on time in order to maintain the membership and enjoy premium discount (if any) in the subsequent policy years. The membership fee of AIA Vitality may vary at any time without prior notice. Likewise, programme benefits may be added or removed without prior notice.

Important note:Members must log in AIA Vitality through “AIA Connect” mobile application (“Platform”). The Platform is available to use under certain mobile phone operating systems. Please refer to App Store (iOS) and Google Play (Android) for the latest system requirements. AIA gives no warranty on the compatibility or reliability of the Platform, and accepts no responsibility in the event that you are not able to earn or record points due to incompatibility between Platform and / or mobile phone operating systems and fitness devices / fitness-tracking mobile apps.

Enjoy premium discount and lifestyle rewardsAIA Vitality rewards you to live healthy lives with premium discounts, enabling you to enjoy life with protection in a smart way.

• Enjoy an instant 10% premium discount for the first year by joining AIA Vitality

• Enjoy up to 15% premium discount if you can maintain your Platinum Status for 5 consecutive years4

• Premium discounts are not affected by claims history

You can also enjoy a wide range of rewards5 under AIA Vitality and you can refer to aia.com.hk/aiavitality for more details.

AIA Vitality is not an insurance product that falls under the jurisdiction of the insurance regulation. Annual membership fee is required for joining6. Moreover, the cover of the insured under the policy shall remain unchanged no matter whether the customer chooses to join AIA Vitality or not. For details and terms and conditions of the AIA Vitality membership and membership fee, please visit “How to join” section under aia.com.hk/aiavitality.

19 LIFE INSURANCE – LIFE PROTECTION

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

Example: Healthy journey of a Gold member

Earn more discounts and rewards with higher membership status

AIA Vitality Status

AIA Vitality Points

Members can enjoy a wide range of rewards with different reward levels depending on the membership status. For more details of the rewards, please visit aia.com.hk/en/aiavitalityrewards.

Discount adjustment

for the subsequent

year’s renewal7

Over 20,000 points in a year Upgrade to GOLD member

Know Your Health Improve Your Health9 Enjoy The Rewards

Complete 6 online assessments8

Earn 5,500 points (A)

Achieve 7,500 steps every day for 5 days in a week10

50 points/day x 5 daysx 52 weeks = 13,000 points

2 Partner gym visits in a week100 points/day x 2 daysx 52 weeks = 10,400 points

Complete health check• Blood pressure• BMI• Blood cholesterol• Blood glucoseEarn 750 points x 4 tests = 3,000 points (B) (Earn additional 750 points for each test if the result is within the healthy range) (i.e.1,500 points x 4 tests = 6,000 points (C))

Wide range of rewards available for members by keeping a healthy lifestyle.For more information of the rewards, please refer to aia.com.hk/aiavitality

Total: 8,500 (A) + (B) to 11,500 (A) + (C) points in a year Total: 10,400 to 13,000 points in a year

Remarks:7. If the insured joins (or has already joined) AIA Vitality as a member, he/she can enjoy an instant 10% premium discount

of first-year insurance premium when purchasing a selected AIA Vitality insurance product with premium discount. Upon subsequent AIA Vitality membership renewal, members can continue to enjoy the premium discount, this discount adjustment could increase or decrease according to the member’s AIA Vitality Status and the applicable insurance premium adjustment percentage. The higher the AIA Vitality Status, the greater the percentage of discount the member will enjoy. The AIA Vitality Insurance Premium Discount Percentage is capped at 15% and floored at 0%. Please refer to the policy contract for the exact and complete terms and conditions.

8. Members can earn a total of 5,500 points after completing the AIA Vitality Health Review, Stressor Assessment, Exercise Assessment, Online Nutrition Assessment, Non-smoker’s Declaration and Sleep Assessment. Online assessments may change from time to time without prior notice.

9. Members can earn up to 15,000 points a year for fitness activities including walking and visiting partner gym centres, etc.10. For the details of synchronising the step count with AIA Vitality, please visit aia.com.hk/aiavitality.Important note:For the relevant terms and conditions, and the latest details of all assessments, point-earning activities, rewards and offers, please visit aia.com.hk/aiavitality.

premium discount

20

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACTLIFE INSURANCE – LIFE PROTECTION

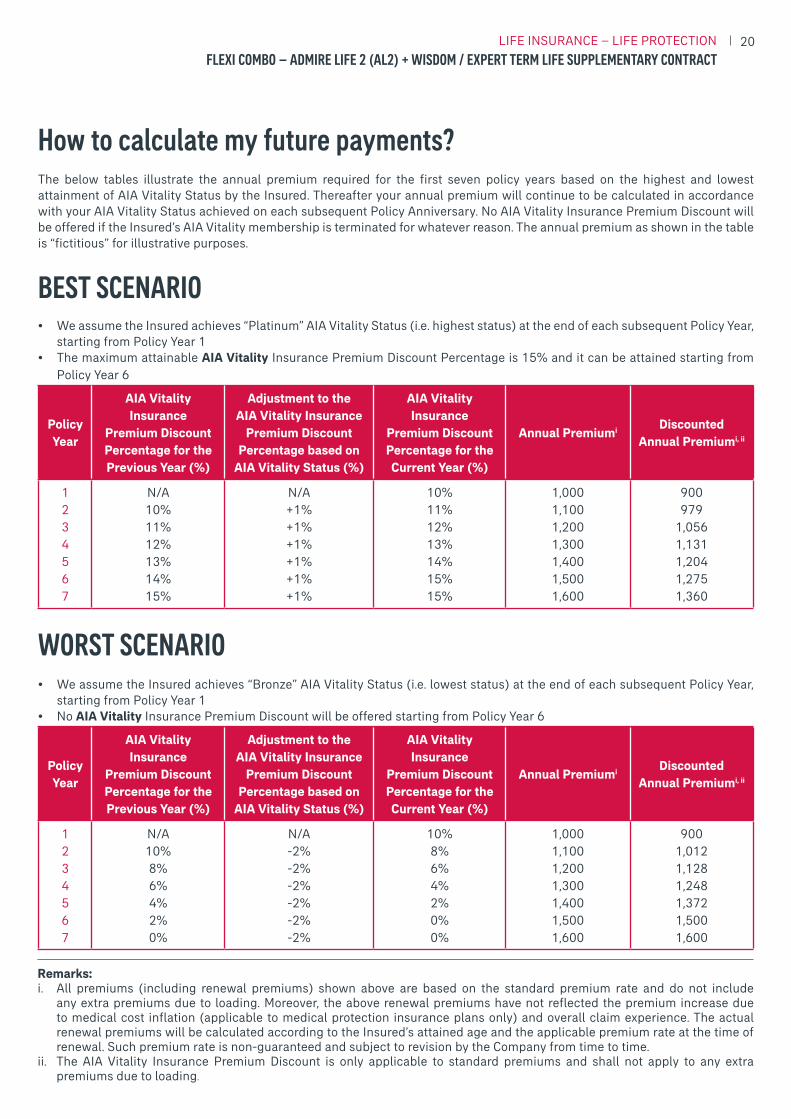

How to calculate my future payments?The below tables illustrate the annual premium required for the first seven policy years based on the highest and lowest attainment of AIA Vitality Status by the Insured. Thereafter your annual premium will continue to be calculated in accordance with your AIA Vitality Status achieved on each subsequent Policy Anniversary. No AIA Vitality Insurance Premium Discount will be offered if the Insured’s AIA Vitality membership is terminated for whatever reason. The annual premium as shown in the table is “fictitious” for illustrative purposes.

BEST SCENARIO• We assume the Insured achieves “Platinum” AIA Vitality Status (i.e. highest status) at the end of each subsequent Policy Year,

starting from Policy Year 1• The maximum attainable AIA Vitality Insurance Premium Discount Percentage is 15% and it can be attained starting from

Policy Year 6

PolicyYear

AIA Vitality Insurance

Premium Discount Percentage for the Previous Year (%)

Adjustment to the AIA Vitality Insurance

Premium Discount Percentage based on

AIA Vitality Status (%)

AIA Vitality Insurance

Premium Discount Percentage for the Current Year (%)

Annual Premiumi Discounted Annual Premiumi, ii

1234567

N/A10%11%12%13%14%15%

N/A+1%+1%+1%+1%+1%+1%

10%11%12%13%14%15%15%

1,0001,1001,2001,3001,4001,5001,600

900979

1,0561,1311,2041,2751,360

WORST SCENARIO• We assume the Insured achieves “Bronze” AIA Vitality Status (i.e. lowest status) at the end of each subsequent Policy Year,

starting from Policy Year 1• No AIA Vitality Insurance Premium Discount will be offered starting from Policy Year 6

PolicyYear

AIA Vitality Insurance

Premium Discount Percentage for the Previous Year (%)

Adjustment to the AIA Vitality Insurance

Premium Discount Percentage based on

AIA Vitality Status (%)

AIA Vitality Insurance

Premium Discount Percentage for the Current Year (%)

Annual Premiumi Discounted Annual Premiumi, ii

1234567

N/A10%8%6%4%2%0%

N/A-2%-2%-2%-2%-2%-2%

10%8%6%4%2%0%0%

1,0001,1001,2001,3001,4001,5001,600

9001,0121,1281,2481,3721,5001,600

Remarks: i. All premiums (including renewal premiums) shown above are based on the standard premium rate and do not include

any extra premiums due to loading. Moreover, the above renewal premiums have not reflected the premium increase due to medical cost inflation (applicable to medical protection insurance plans only) and overall claim experience. The actual renewal premiums will be calculated according to the Insured’s attained age and the applicable premium rate at the time of renewal. Such premium rate is non-guaranteed and subject to revision by the Company from time to time.

ii. The AIA Vitality Insurance Premium Discount is only applicable to standard premiums and shall not apply to any extra premiums due to loading.

21 LIFE INSURANCE – LIFE PROTECTION

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACT

Important note: 1. For up-to-date information on each benefit, please visit aia.com.hk/aiavitality. Partners and benefits may vary at any time

without prior notice. All representations within this document made on behalf of AIA International Ltd have been thoroughly researched, and are verifiable by documentary evidence. Representations within this document made on behalf of our AIA Vitality partners are based upon information that AIA International Ltd has received from them, and such information has been provided to us along with an assurance from our AIA Vitality partners that it is accurate.

2. The AIA Vitality Insurance Premium Discount is only applicable to the specific Basic Policy or Supplementary Contract named under this product brochure. The AIA Vitality Insurance Premium Discount is not extended to any other policies or supplementary contracts unless it is specifically stated otherwise.

3. The AIA Vitality Insurance Premium Discount Percentage is capped at 15% and floored at 0%.4. The Insured has to be an AIA Vitality member in order to enjoy the AIA Vitality Insurance Premium Discount.5. An annual membership fee will be charged for AIA Vitality and a member has to renew the AIA Vitality membership annually

on time in order to maintain the membership and enjoy AIA Vitality Insurance Premium Discount (if any) in the subsequent policy years.

6. If the AIA Vitality member is insured by more than one policy or supplementary contract under the AIA Vitality Series, the AIA Vitality Insurance Premium Discount or AIA Vitality Power Up Coverage applied, as the case may be, should be calculated independently for each policy or supplementary contract. For the avoidance of doubt, AIA Vitality Insurance Premium Discount and AIA Vitality Power Up Coverage are mutually exclusive. Please check the illustration of each policy or supplementary contract to find out which one applies.

7. Whether to apply for AIA Vitality is your/the insured’s own individual decision.8. Please note that any change/modification of structure or terms of AIA Vitality may possibly affect the accumulation of points,

and therefore the AIA Vitality status and also the benefits under a Vitality policy (including without limitation, premium discount).

9. Please note that if an AIA Vitality member is insured by more than one policy or supplementary contract under the AIA Vitality Series, you/the insured is only required to pay the Vitality membership fee once annually to enjoy the related benefits.

22

FLEXI COMBO – ADMIRE LIFE 2 (AL2) + WISDOM / EXPERT TERM LIFE SUPPLEMENTARY CONTRACTLIFE INSURANCE – LIFE PROTECTION

Flex

i_A

L2_C

iti_E

ng_2

020/

11

The more you engage with AIA Vitality,the more AIA Vitality Points you earn and the higher your AIA Vitality Status, leading to greater premium discount,lifestyle rewards and offers and a healthier you.

Contact us now

(852) 2232 [email protected]/aiavitality

Hong Kong

Citibank (Hong Kong) Limited - Important Notes from the insurance agent

1. Citibank (Hong Kong) Limited, being registered with the Insurance Authority as a licensed insurance agency, acts as an appointed licensed insurance agent for AIA International Limited (the "Insurance Company").

2. Citibank (Hong Kong) Limited's role is limited to distributing insurance products of the Insurance Company only and Citibank (Hong Kong) Limited shall not be responsible for any matters in relation to the provision of the products.

3. Insurance products are products and obligations of the Insurance Company and not of Citibank (Hong Kong) Limited. Insurance products are not bank deposits or obligations of, or guaranteed or insured by Citibank (Hong Kong) Limited, Citibank, N.A., Citigroup Inc. or any of their affiliates or subsidiaries, or any local governmental agency.

4. AIA Vitality (the "Programme") is not an insurance product. It is a membership programme and obligation of the Insurance Company and not of Citibank (Hong Kong) Limited. Citibank (Hong Kong) Limited’s role is limited to introducing the Programme only and you should obtain further details about the Programme directly from the Insurance Company. Citibank (Hong Kong) Limited shall not be responsible for any matters in relation to the Programme provided by the Insurance Company.

5. In respect of an eligible dispute (as defined in the Terms of Reference for the Financial Dispute Resolution Centre in relation to the Financial Dispute Resolution Scheme) arising between you and Citibank (Hong Kong) Limited out of the selling process of any insurance product conducted by Citibank (Hong Kong) Limited as agent for Insurance Company or the processing of the related transaction, you may enter into a financial dispute resolution scheme process with Citibank (Hong Kong) Limited in accordance with the applicable rules in Hong Kong. However any dispute over the contractual terms of insurance products should be resolved directly between you and the Insurance Company.

6. All insurance applications are subject to Insurance Company's underwriting and acceptance.

7. The Insurance Company is solely responsible for all approvals, coverage, compensations and account maintenance in connection with its insurance products.

8. Citibank (Hong Kong) Limited will not render you any legal, accounting or tax advice. You are advised to check with your own professional advisor for advice relevant to your circumstances.

9. You are reminded to carefully review the relevant product materials provided to you and seek independent advice if necessary.

10. For any policy service enquiries, please contact the relevant licensed bank staff or the Insurance Company.

© 2020 Citibank Citi and Arc Design is a registered service mark of Citibank, N.A. or Citigroup Inc. Citibank (Hong Kong) Limited

CIT

IIN

_ C

iti_

Vit

alit

y_E

ng_2

02

0/0

8