Getting the Best Advice for Your Nest-Egg: “Institutional vs. Retail”

Upload

kanan-guptaCategory

view

218download

0

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 1/21

Brands developed by the retailer and sold exclusively through

their stores.

PRIVATE LABELS

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 2/21

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 3/21

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 4/21

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 5/21

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 6/21

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 7/21

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 8/21

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 9/21

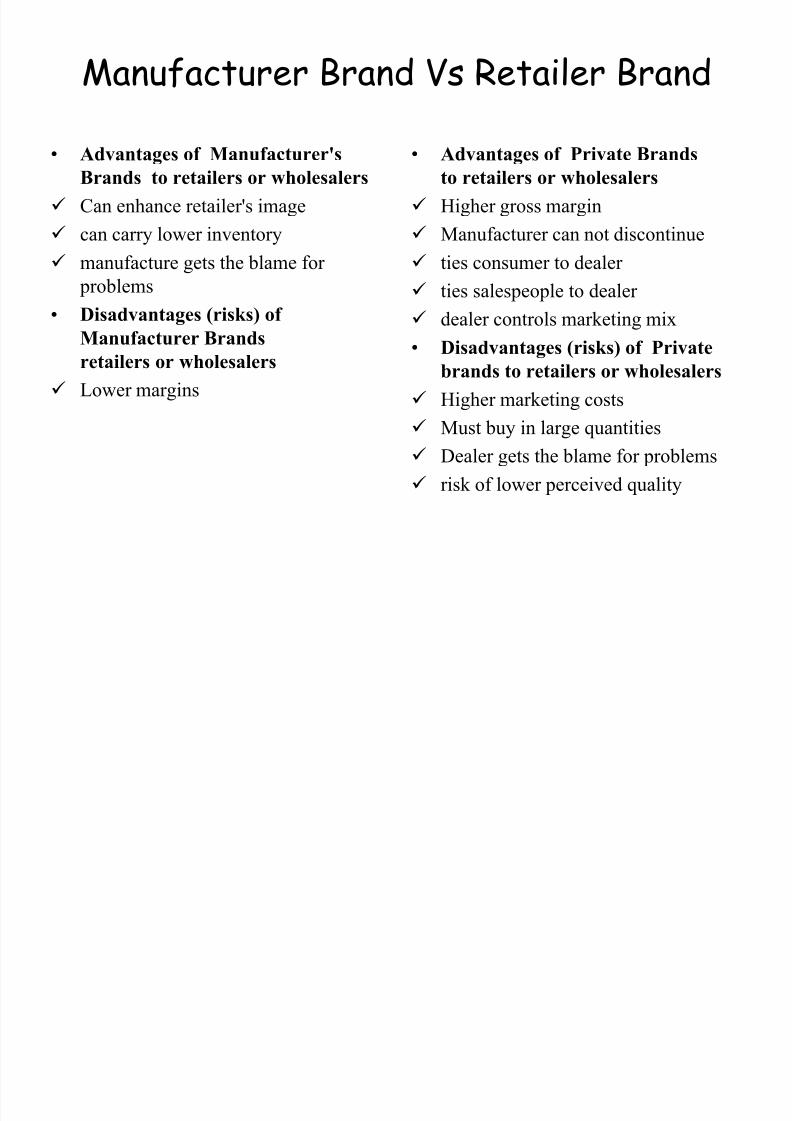

Manufacturer Brand Vs Retailer Brand

• Advantages of Manufacturer's

Brands to retailers or wholesalers

Can enhance retailer's image

can carry lower inventory

manufacture gets the blame for

problems

• Disadvantages (risks) of

Manufacturer Brands

retailers or wholesalers

Lower margins

• Advantages of Private Brands

to retailers or wholesalers

Higher gross margin

Manufacturer can not discontinue

ties consumer to dealer

ties salespeople to dealer

dealer controls marketing mix

• Disadvantages (risks) of Private

brands to retailers or wholesalers

Higher marketing costs

Must buy in large quantities

Dealer gets the blame for problems

risk of lower perceived quality

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 10/21

According to Kumar and Steenkamp (2007) there are four types of PL

strategies an organisation can adopt – Generic, Copycat, Premium and

Value Innovators.

Generic PL - products are cheap and undifferentiated and provide the

customer with a low-cost option.

Copycat labels - copy the offerings of the brand leader but offer them at

a slightly lower price.

Premium PLs - provide added value and differentiation; prices are either

close to or higher than the market leader.

Value Innovators - provide the best performance to price ratio, much

cheaper than the leader but provide exceptional value for money.

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 11/21

Generics

• A traditional retail brand • No name product or a sub-brand with poor quality at a very low price

• 3 strategies:

– Store brand + a sub-brand

(Tesco and Sainsbury)

– Stand-alone brand: “1” of Carrefour (“ premier prix ”)

– Consortium brand: Euroshopper (Ahold + 8 other European retailers)

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 12/21

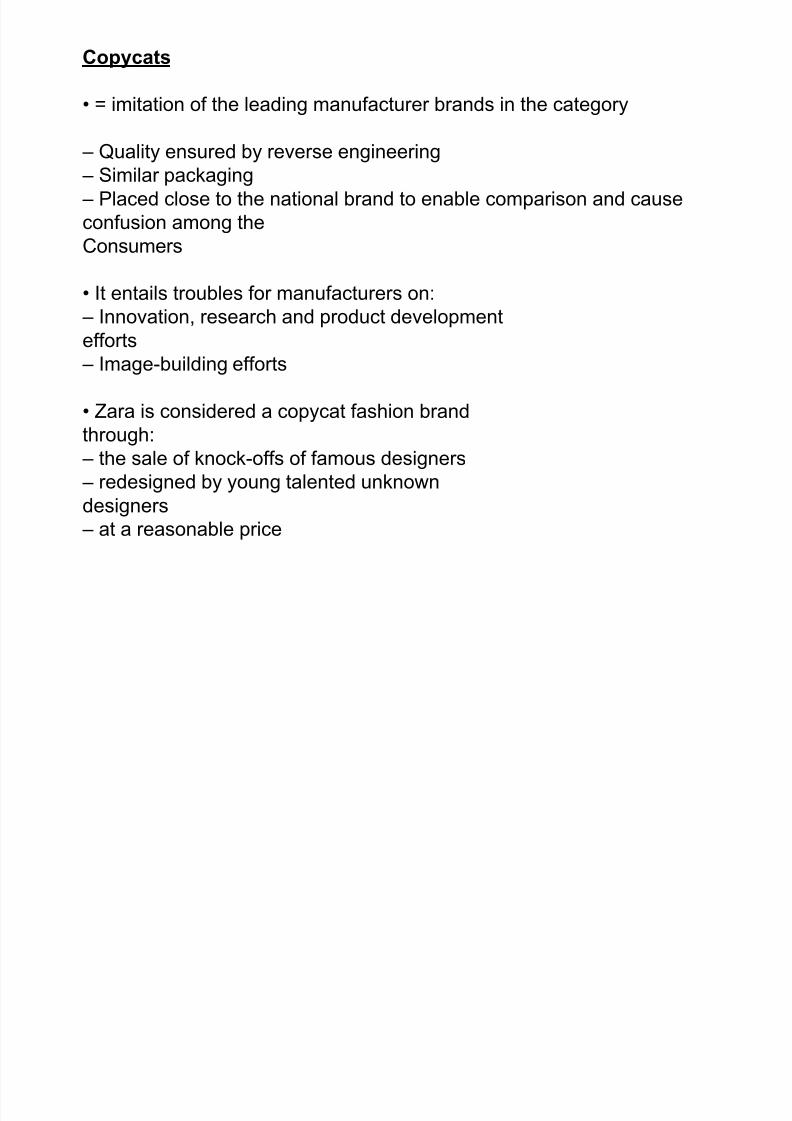

Copycats

• = imitation of the leading manufacturer brands in the category

– Quality ensured by reverse engineering

– Similar packaging

– Placed close to the national brand to enable comparison and cause

confusion among the

Consumers

• It entails troubles for manufacturers on:

– Innovation, research and product development

efforts

– Image-building efforts

• Zara is considered a copycat fashion brand through:

– the sale of knock-offs of famous designers

– redesigned by young talented unknown

designers

– at a reasonable price

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 13/21

Premium store brands

• Premium-lite store brands

– When a retailer makes a

superior product at a lower

price – Well-known ex.: Staples (US)

• Premium-price store brands

– Pioneered in the UK:

• Sainsbury • Marks and Spencer

• Tesco

– priced higher than

manufacturer brands

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 14/21

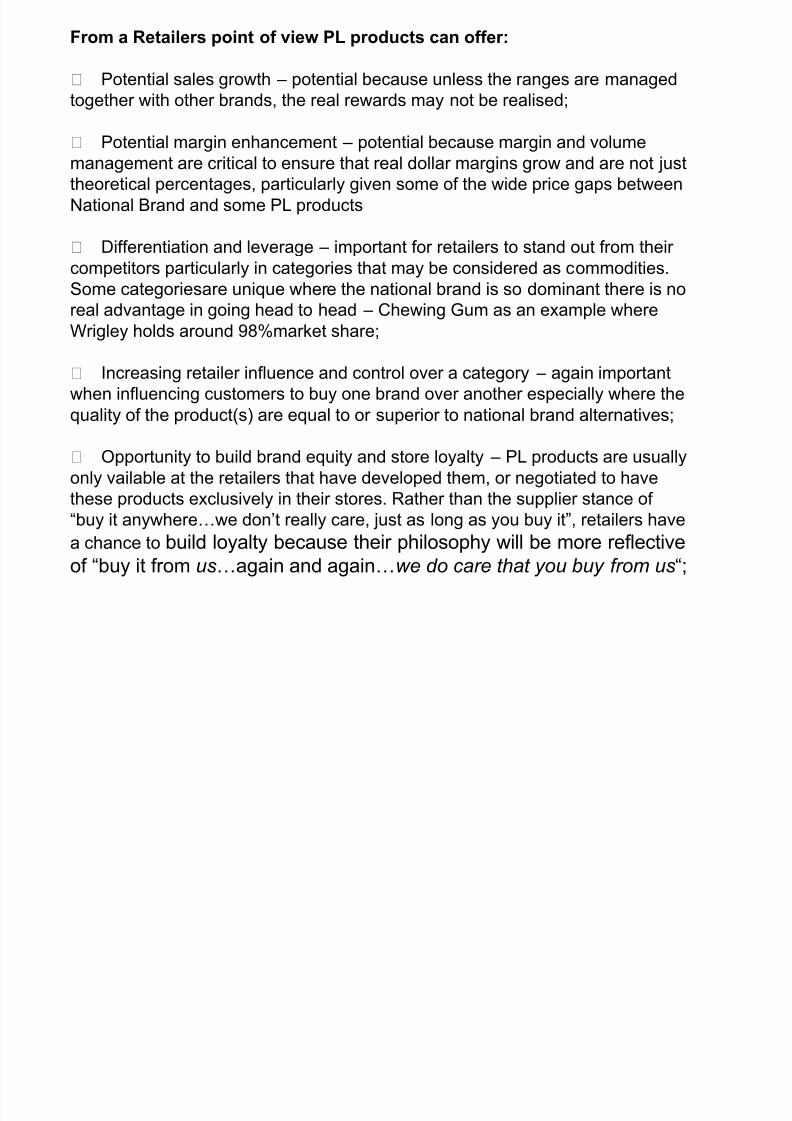

From a Retailers point of view PL products can offer:

Potential sales growth – potential because unless the ranges are managed

together with other brands, the real rewards may not be realised;

Potential margin enhancement – potential because margin and volumemanagement are critical to ensure that real dollar margins grow and are not just

theoretical percentages, particularly given some of the wide price gaps between

National Brand and some PL products

Differentiation and leverage – important for retailers to stand out from their

competitors particularly in categories that may be considered as commodities.

Some categoriesare unique where the national brand is so dominant there is no

real advantage in going head to head – Chewing Gum as an example where

Wrigley holds around 98%market share;

Increasing retailer influence and control over a category – again important

when influencing customers to buy one brand over another especially where the

quality of the product(s) are equal to or superior to national brand alternatives;

Opportunity to build brand equity and store loyalty – PL products are usually

only vailable at the retailers that have developed them, or negotiated to have

these products exclusively in their stores. Rather than the supplier stance of

“buy it anywhere…we don‟t really care, just as long as you buy it”, retailers have

a chance to build loyalty because their philosophy will be more reflective

of “buy it from us…again and again…we do care that you buy from us“;

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 15/21

The opportunity to create consumer value – very important when considering

the ranges of products to be developed; the greater the purchase frequency,

the moreoften customers will revert to those that offer „value‟

A downside in that customers may find their choices further diminished by

just having a National Brand and PL choice with no real newness or innovation

in range

An opportunity to create a value perception across the store a PL products

are generally perceived to offer good value

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 16/21

For the big national brands, private label brands present a unique set of

competitive challenges that also go beyond product comparison. For

example:

•Retailer‟s profit margins are generally higher for private label products

•Private label, in many cases, has more opportunity to gain exposure in the

Retailer‟s store, market and consumer‟s pantry.

•The retailer‟s relationship with manufacturers enables private label to

discover in advance what their competition is doing in media, trade

promotions and new product introductions.

•Retailers are investing more in developing and marketing their brands.

Consequently, they are not just the “me-too” brand anymore.

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 17/21

That is not to say that private label brands do not have their own

challenges. Retailers are ramping up capabilities in areas that their branded

competitors have been doing for a very long time. They include:

• As Private label grows, retailers have had to invest more in marketing and

servicing a brand that goes beyond the basic value brand they used to be.

•They have to invest in building equity like their branded competition.

•In many instances, the national branded manufacturer is making private

label.

•Retailers still rely on manufacturers to provide consumer and shopper

insights, beyond their walls, that enable innovation in building store traffic.

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 18/21

National brands generally bring customers to store, PL has to work harder at

point of purchase: price, visual appeal or „shelf awareness‟, credibility and clear

articulation of product benefits. Therefore they should:

•Ensure that there is a clearly articulated brand strategy

•Decide whether there is a brand vs. product line focus

•Establish agreed actions across the brand and category management team

•Define production parameters early – and clearly

•Bring partners together – ensure that there is a shared vision

•Consider the real opportunity costs of a PL vs. national brand•Decide if there is a manufacturing synergy between national brands and PLs

•Determine if there specialty PL suppliers who can provide innovation and

exclusivity

•Ensure that potential trading terms and marketing initiative sacrifices or gains

are clearly evaluated prior to embarking on the program

•Understand where innovation occurs, this is a real issue if your national brandmanufacturer is also your PL manufacture

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 19/21

The shifting competitive climate is forcing manufacturers of branded products to

get better at innovation and positioning for their brands while marketing budgets

are being cut. Manufacturers must find ways to develop innovations in product

development and reach their consumers more efficiently and effectively. Thebattleground is clear:

Marketers must be more rigorous in looking objectively at their business. The

ability to utilize real time cause and effect data to obtain lead indicators in order

to building and adjusting strategic direction and determine where they investtheir marketing, sales and operations dollars is critical.

When you consider 70 percent of purchase decisions are done in store, the

retailers pose both a tremendous threat as well as the key to the shopper.

Developing innovation in driving consumers to the centre of the store and finding

ways to get your products on the store‟s perimeter are imperative.

Finally, a tiered brand strategy is where the manufacturer wants to propose: a

core premium brand, a core mainstream brand and a value brand with the

correlating Private label as it fits. At a primal level it is a two brand strategy is

where the manufacturer wants to drive the retailer to.

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 20/21

For Suppliers…

Needless to say that it is the suppliers and manufacturers who have beenimpacted the most by the move to increase the presence of PLs in retail

outlets.

While PLs have always existed to some extent, what is most threatening to

manufacturers is that PL quality has improved. In some food taste tests, PL

products have in some cases even surpassed the quality and appeal of national brands. In all retail segments PLs now represent a real option for the

consumer.

And while PL have improved, manufacturers have, in some instances, been

increasing prices and in some cases investing less in their brands – this

creates a real opportunity for PL products to fill the void and in some cases

overtake weak National Brands through value positioning.

7/30/2019 Retail vs Manufactured

http://slidepdf.com/reader/full/retail-vs-manufactured 21/21

However, opportunities for manufacturers and suppliers outside traditional retail channels

to enter into supply are surfacing – an interesting development whereby manufacturers

whose own brands may have only been second or third tier, have the opportunity to

manufacture products under a specific retailers PL and compete with the top brands.

For suppliers, speed to market and innovation will be critical in order to compete effectively

and to ensure that brands remain market leaders.

Classic communication techniques such as 'above the line' advertising may help reinforce

brand strength while brand stretch may also provide opportunities for those suppliers

looking to step out of commoditised and/or mature categories.

In order to succeed suppliers and manufacturers can/should partner and „manage‟ the

relationship with their retailers. Innovate and differentiate to ensure that their brands are

those that customers prefer, and invest more in their brands. They need to also be more

proactive and understand the business, pricing and risk areas to a greater degree

and develop competitive tactics at store level.

![Indian Retail Models - Reliances vs Itc vs Future Group[Smallpdf.com]](https://static.fdocuments.in/doc/165x107/55cf98ea550346d0339a6cce/indian-retail-models-reliances-vs-itc-vs-future-groupsmallpdfcom.jpg)