Results Presentation Q2 2016 Results - ISOLUX · PDF fileare not entirely comparable to those...

21

Results Presentation Q2 2016 Results September 29, 2016

Transcript of Results Presentation Q2 2016 Results - ISOLUX · PDF fileare not entirely comparable to those...

Results Presentation

Q2 2016 Results September 29, 2016

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 2

Disclaimer

This presentation has been prepared by Grupo Isolux Corsán, S.A.; therefore no part of it may be published, disclosed or distributed in any form or by any means, nor used by any other person or entity, without the prior written consent of Grupo Isolux Corsán, S.A. For the purposes of this presentation and as the context requires, presentation means this document, its content or any part of it, any oral presentation, and any question and answer session during or in connection with this presentation. This presentation contains statements related to our future business and financial performance and future events or developments involving us that may constitute forward-looking statements. These statements may be identified by words such as “expects,” “looks forward to,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “will,” “project” or words of similar meaning. We may also make forward-looking statements in other reports, in presentations, in material delivered to shareholders and in press releases. In addition, our representatives may from time to time make oral forward-looking statements. Such forward-looking statements and information are based on the current expectations and assumptions, and are, therefore, subject to certain known or unknown risks and uncertainties. A variety of factors, which are beyond our control or may be difficult to predict, affect our operations, performance, business strategy and results and could cause our actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements or anticipated on the basis of historical trends. No representation or warranty is made than any forward-looking statement will come to pass. Should one or more risks or uncertainties materialize, or should underlying assumptions prove incorrect, our actual results, performance or achievements may vary materially from those described in the relevant forward-looking statement as being expected, anticipated, intended, planned, believed, sought, estimated or projected. We neither intend, nor assume any obligation, to publicly update or revise these forward-looking statements in light of developments which differ from those anticipated. The information contained in this presentation has not been verified or revised by the auditors of Grupo Isolux Corsán, S.A. and does not purport to be comprehensive. Certain data included in this presentation has been subject to rounding adjustments. Accordingly, in certain instances, the sum of the numbers in a column or a row in tables may not conform exactly to the total figure given for that column or row. This presentation does not constitute an offer to sale or a solicitation offer to buy or subscribe for any securities in any jurisdiction, including in the United States, form the basis for any investment decision and no specific recommendations are intended. Specifically, this presentation does not constitute a “prospectus” within the meaning of the U.S. Securities Act of 1933. This presentation is not, and shall not be deemed, an offer with respect to any securities, a solicitation to tender or exchange of any of the existing notes or existing shareholders equity or a solicitation of votes with respect to a plan filed under Chapter 11 of the U.S. Bankruptcy Code or any other type of reorganization. Any such offer or solicitation will comply with all applicable securities laws and/or, as applicable, provisions of the U.S. Bankruptcy Code and any other applicable law subject to U.S. Federal Rules of Evidence Rule 408 and its equivalents.

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 3

Results Presentation Q2 2016 | Table of Contents

Table of Contents 1. Main highlights

2. Q2 2016 Business and Financial Highlights

i. EPC

ii. Concessions

3. Appendix

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 4

1. Main Highlights

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 5

Results Presentation Q2 2016 | Main highlights

Spanish Group

Restructuring

Process

Corporate

Asset sales

Several processes in progress : T Solar, Transmission lines, Loma Blanca, Infinita and Tecna.

The Group is currently analyzing options for other non-core assets that could potentially be sold, in order to focus on EPC business

During the second half of July the financial creditors of the key Spanish entities of the Group voted the terms of the Restructuring Agreement

Financial creditors holding approx. 92%+ of the debt of each entity subject to the Restructuring Agreement supported. Thanks to this overwhelming support, the Group filed a petition in the Court of Madrid to request the “homologación judicial” on July 28, 2016.

At the beginning of September a judge was assigned to the file.

The judge has acknowledged the submission of the homologación petition and granted relief by suspending any foreclosures against the companies affected by the homologation

We are confident on the restructuring process success and homologation process is expected to be finalized ahead of the agreed deadline of 31 December 2016

In early September the Group announced a significant layoff program that will be carried out through a collective negotiation process with the employees’ representatives. Spanish labor law establishes a 1-month negotiation period, that starts on September 29th. The expected headcount reduction is over 500 people, nearly 30% of the staff in Spain.

Negotiations with our suppliers to agree modified payment terms are ongoing. We are already reaching agreements with a relevant number of them, that entail either a 3-year payment plan or an upfront payment with a haircut in the outstanding amounts.

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 6

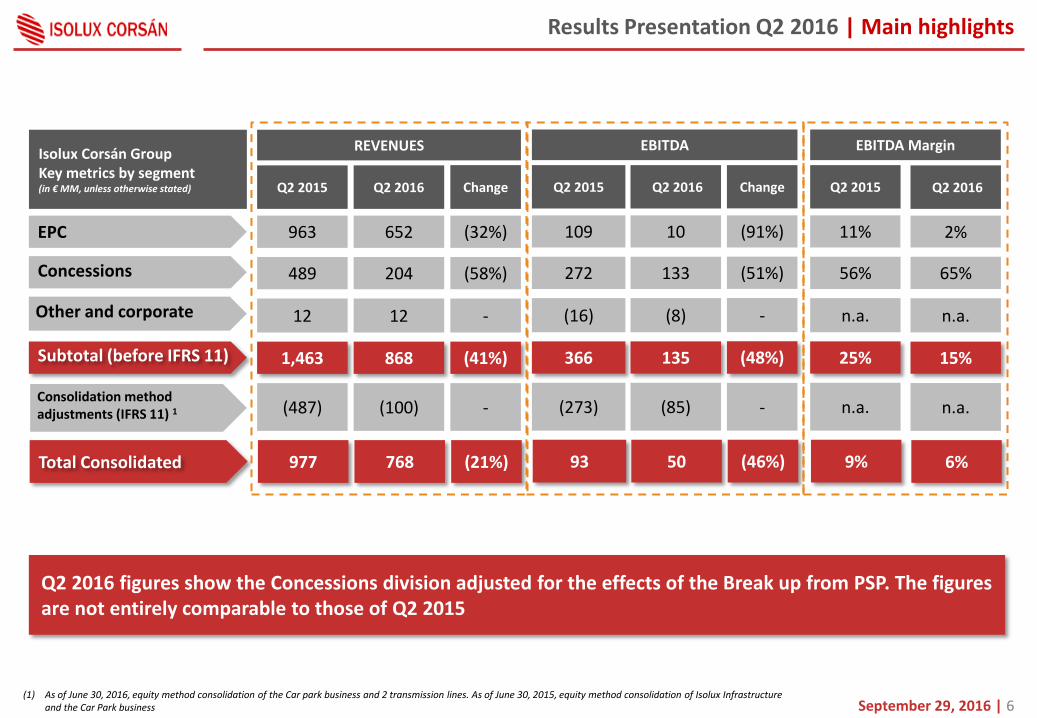

Isolux Corsán Group Key metrics by segment (in € MM, unless otherwise stated) Q2 2015 Q2 2016 Change

EPC 963 652 (32%)

Subtotal (before IFRS 11) 1,463 868 (41%)

Concessions 489 204 (58%)

Other and corporate 12 12 -

Consolidation method adjustments (IFRS 11) 1 (487) (100) -

REVENUES

Total Consolidated 977 768 (21%)

Q2 2015 Q2 2016 Change

109 10 (91%)

366 135 (48%)

272 133 (51%)

(16) (8) -

(273) (85) -

EBITDA

93 50 (46%)

Q2 2015

11%

25%

56%

n.a.

n.a.

EBITDA Margin

9%

Q2 2016

2%

15%

65%

n.a.

n.a.

6%

(1) As of June 30, 2016, equity method consolidation of the Car park business and 2 transmission lines. As of June 30, 2015, equity method consolidation of Isolux Infrastructure and the Car Park business

Q2 2016 figures show the Concessions division adjusted for the effects of the Break up from PSP. The figures are not entirely comparable to those of Q2 2015

Results Presentation Q2 2016 | Main highlights

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 7

170 (385)

379

(2)

172

6

Cash and cashequivalents Sep 2014

Cash and cashequivalents Dec 2015

Operating Cash Flow Q22016

Cash Flow from Investingactivities Q2 2016

Cash Flow from FinancingActivities Q2 2016

FX Cash and cashequivalents Jun 2016

Consolidated Cash Flow Bridge December 2015 to June 2016 (in € MM)

Cash Flow Bridge

STFI €13M

STFI €12M

Results Presentation Q2 2016 | Main highlights

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 8

2. Q2 2016 Business Highlights

i. EPC

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 9

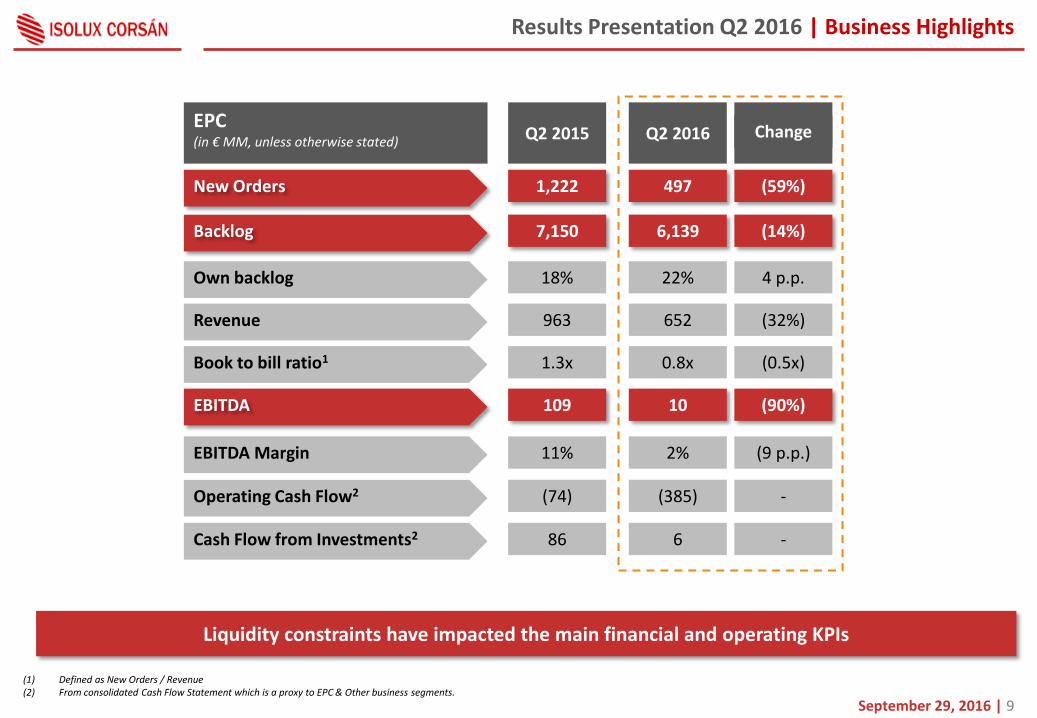

(1) Defined as New Orders / Revenue (2) From consolidated Cash Flow Statement which is a proxy to EPC & Other business segments.

EPC (in € MM, unless otherwise stated) Q2 2015 Q2 2016 Change

New Orders

Backlog

Own backlog

1,222 497 (59%)

7,150 6,139 (14%)

18% 22% 4 p.p.

Revenue 963 652 (32%)

Book to bill ratio1 1.3x 0.8x (0.5x)

EBITDA 109 10 (90%)

EBITDA Margin 11% 2% (9 p.p.)

Operating Cash Flow2 (74) (385) -

Cash Flow from Investments2 86 6 -

Liquidity constraints have impacted the main financial and operating KPIs

Results Presentation Q2 2016 | Business Highlights

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 10

12.550

18.165

7.946

6m 2014 6m 2015 6m 2016

EPC - Key Financial Highlights

Offers presented and under analysis Comments

Offers presented by Isolux (€m) Projects under analysis (€m)

22.940

20.029

18.249

FY2014 FY2015 6m2016

Lower contracting figures are driven by the numbers of offers in which Isolux has participated. In the first 6months of 2016 the amount of offers presented is down by 56% compared to the same period last year.

There are €1bn of offers that the Group has analyzed and worked on, but that could not be tendered for due to lack of bonding lines.

The amount of total projects under analysis has not declined in the same proportion. This means that infrastructure projects are out there, but that the liquidity situation prior to the injection of new funds at the end the of July, constrained the Group’s capacity to tender for these projects. The Group expects to become able to present offers to these projects as a result of the implementation of the refinancing.

Results Presentation Q2 2016 | Business Highlights

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 11

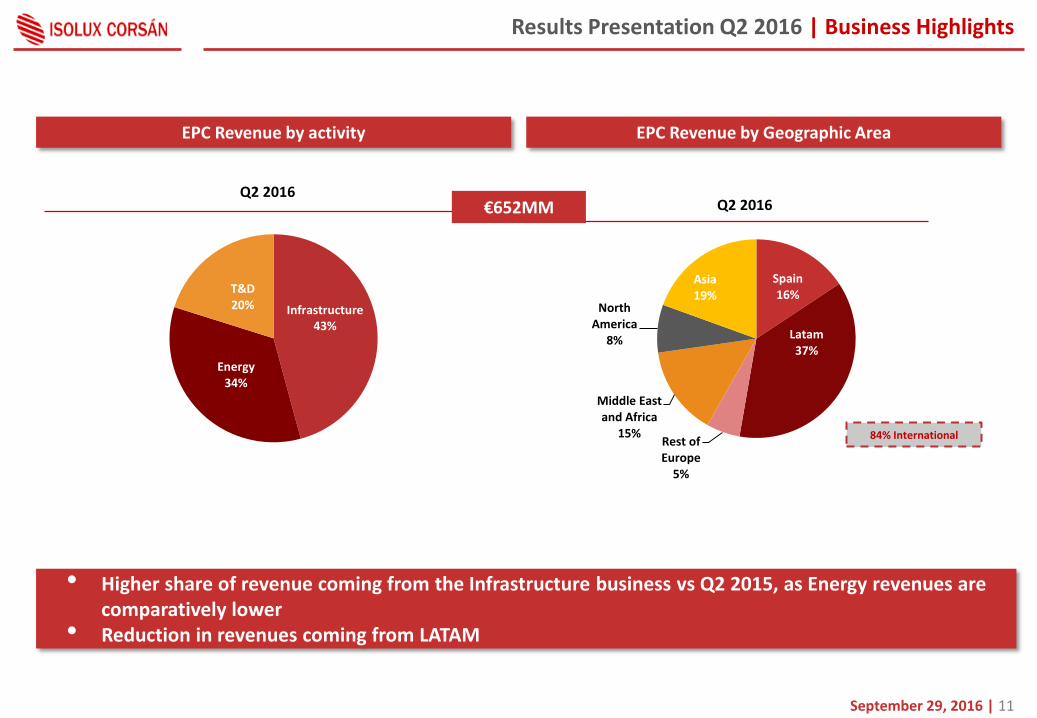

Spain 16%

Latam 37%

Rest of Europe

5%

Middle East and Africa

15%

North America

8%

Asia 19%

Energy 34%

T&D 20% Infrastructure

43%

EPC Revenue by activity

Q2 2016

EPC Revenue by Geographic Area

Q2 2016

84% International

€652MM

• Higher share of revenue coming from the Infrastructure business vs Q2 2015, as Energy revenues are comparatively lower

• Reduction in revenues coming from LATAM

Results Presentation Q2 2016 | Business Highlights

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 12

>250M 17%

100M-250M 35%

50M-100M 21%

10M-50M 20%

<10M 7% Middle

East and Africa 13%

Asia 19%

LATAM 48%

Rest of Europe

4%

Spain 10%

North America

6%

Energy 19%

T&D 33%

Infrastructure 48%

Q2 2016

EPC Backlog by Segment EPC Backlog by Geographic Area

Q2 2016

EPC Backlog Concentration

Q2 2016

90% International

• EPC backlog at the end of June stood at €6.1 bn • Concentration in mid size projects remains fairly stable • Exposure to Spain keeps decreasing with growth in ME&Africa as well as Asia

Results Presentation Q2 2016 | Business Highlights

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 13

2. Q2 2016 Business Highlights

ii. Concessions

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 14

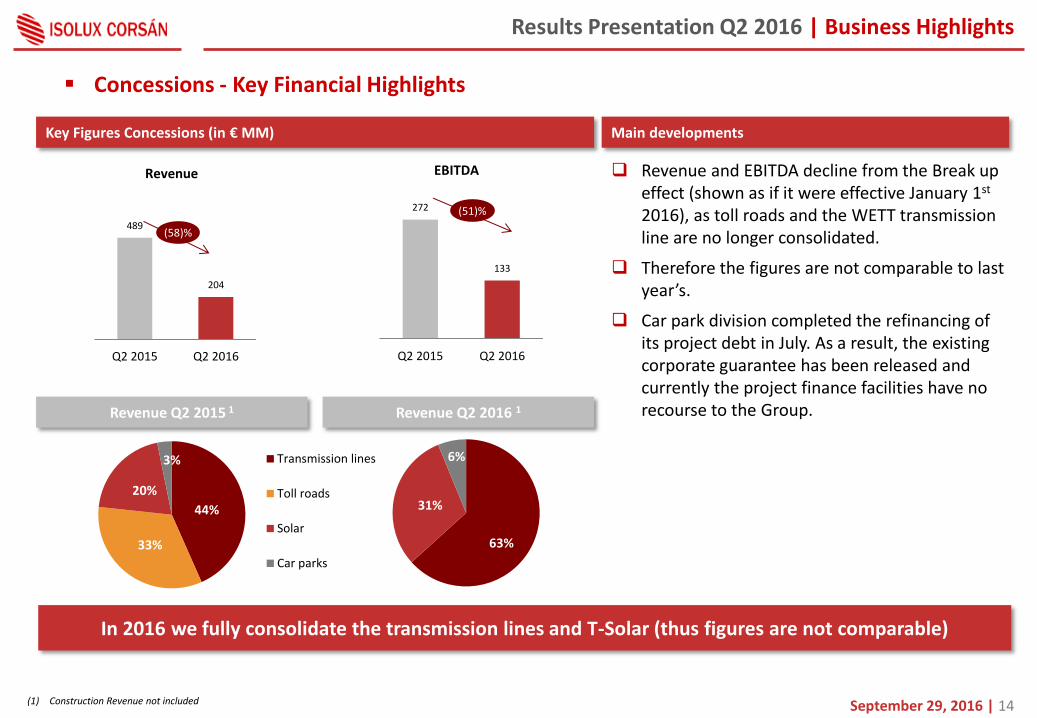

489

204

Q2 2015 Q2 2016

Concessions - Key Financial Highlights

Key Figures Concessions (in € MM) Main developments

Revenue and EBITDA decline from the Break up effect (shown as if it were effective January 1st 2016), as toll roads and the WETT transmission line are no longer consolidated.

Therefore the figures are not comparable to last year’s.

Car park division completed the refinancing of its project debt in July. As a result, the existing corporate guarantee has been released and currently the project finance facilities have no recourse to the Group.

In 2016 we fully consolidate the transmission lines and T-Solar (thus figures are not comparable)

(1) Construction Revenue not included

Revenue Q2 2016 1 Revenue Q2 2015 1

Revenue EBITDA

272

133

Q2 2015 Q2 2016

44%

33%

20%

3% Transmission lines

Toll roads

Solar

Car parks

(58)%

(51)%

63%

31%

6%

Results Presentation Q2 2016 | Business Highlights

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 15

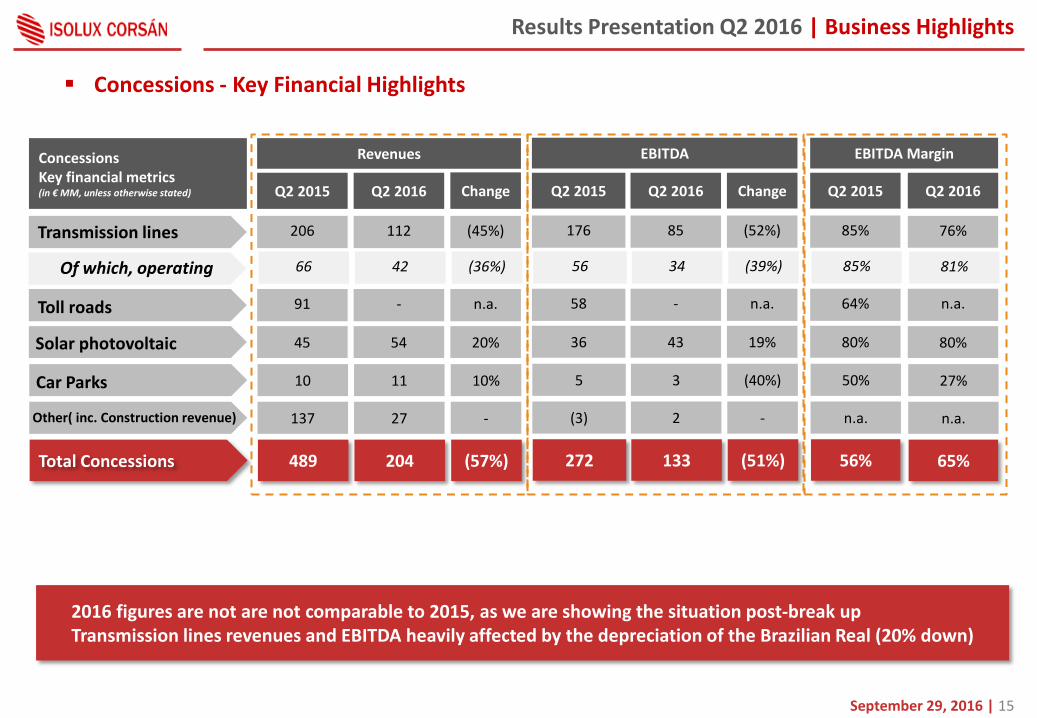

Concessions Key financial metrics (in € MM, unless otherwise stated) Q2 2015 Q2 2016 Change

Transmission lines 206 112 (45%)

Toll roads 91 - n.a.

Solar photovoltaic 45 54 20%

Revenues

Total Concessions 489 204 (57%)

Q2 2015 Q2 2016 Change

176 85 (52%)

58 - n.a.

36 43 19%

EBITDA

272 133 (51%)

Q2 2015

85%

64%

80%

EBITDA Margin

56%

Q2 2016

76%

n.a.

80%

65%

Car Parks 10 11 10% 5 3 (40%) 50% 27%

Other( inc. Construction revenue) 137 27 - (3) 2 - n.a. n.a.

Of which, operating 66 42 (36%) 56 34 (39%) 85% 81%

Concessions - Key Financial Highlights

2016 figures are not are not comparable to 2015, as we are showing the situation post-break up Transmission lines revenues and EBITDA heavily affected by the depreciation of the Brazilian Real (20% down)

Results Presentation Q2 2016 | Business Highlights

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 16

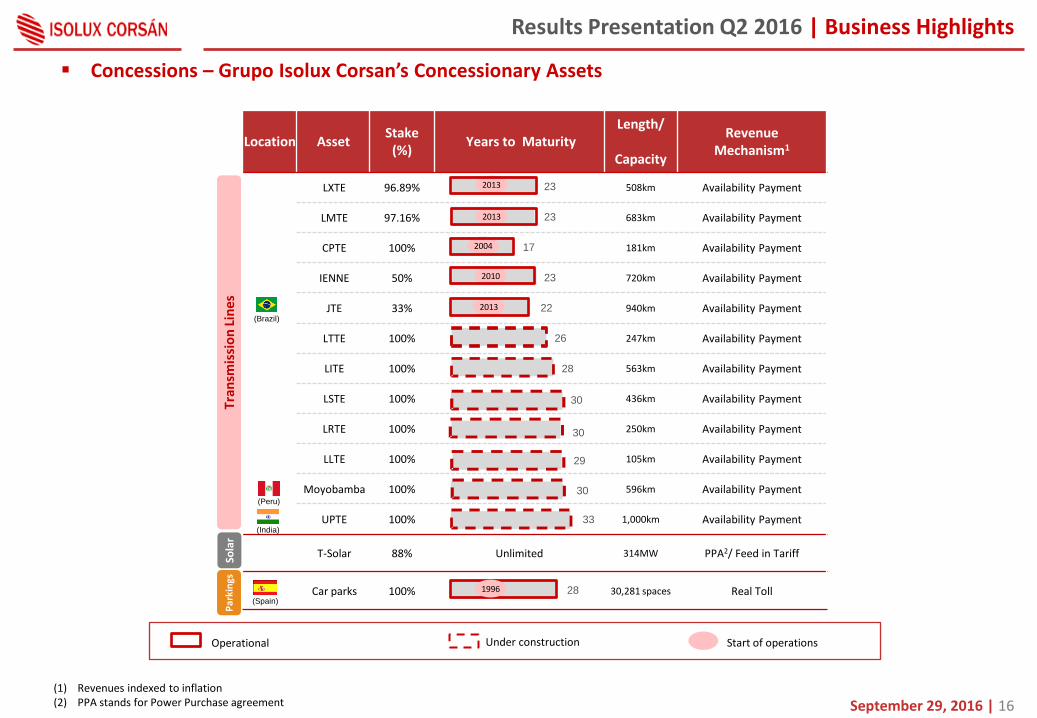

Location Asset Stake

(%) Years to Maturity

Length/

Capacity

Revenue Mechanism1

LXTE 96.89% 508km Availability Payment

LMTE 97.16% 683km Availability Payment

CPTE 100% 181km Availability Payment

IENNE 50% 720km Availability Payment

JTE 33% 940km Availability Payment

LTTE 100% 247km Availability Payment

LITE 100% 563km Availability Payment

LSTE 100% 436km Availability Payment

LRTE 100% 250km Availability Payment

LLTE 100% 105km Availability Payment

Moyobamba 100% 596km Availability Payment

UPTE 100% 1,000km Availability Payment

T-Solar 88% Unlimited 314MW PPA2/ Feed in Tariff

Car parks 100% 30,281 spaces Real Toll

Concessions – Grupo Isolux Corsan’s Concessionary Assets

Tran

smis

sio

n L

ine

s

(1) Revenues indexed to inflation (2) PPA stands for Power Purchase agreement

Sola

r

(Brazil)

(India)

2013

2004

2013

2013

2010

23

23

17

23

22

26

28

33

Operational Under construction Start of operations

(Peru)

30

30

29

30

(Spain)

Par

kin

gs

1996 28

Results Presentation Q2 2016 | Business Highlights

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 17

3. Appendix

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 18

Results Presentation Q2 2016 | Appendix

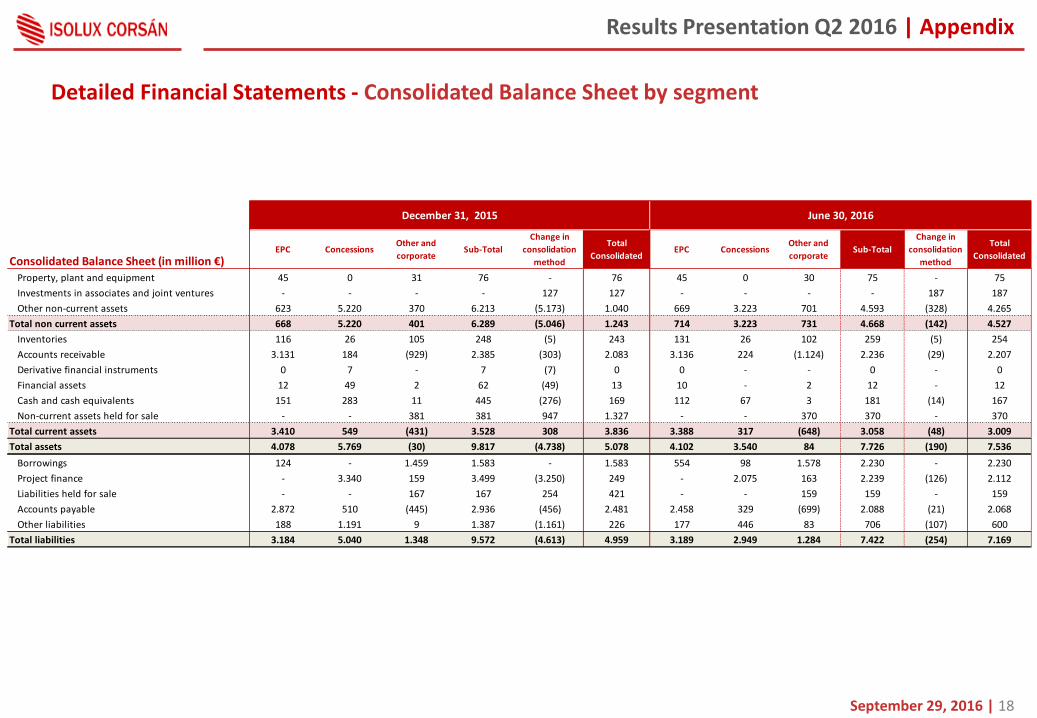

Detailed Financial Statements - Consolidated Balance Sheet by segment

Consolidated Balance Sheet (in million €)Property, plant and equipment 45 0 31 76 - 76 45 0 30 75 - 75

Investments in associates and joint ventures - - - - 127 127 - - - - 187 187

Other non-current assets 623 5.220 370 6.213 (5.173) 1.040 669 3.223 701 4.593 (328) 4.265

Total non current assets 668 5.220 401 6.289 (5.046) 1.243 714 3.223 731 4.668 (142) 4.527

Inventories 116 26 105 248 (5) 243 131 26 102 259 (5) 254

Accounts receivable 3.131 184 (929) 2.385 (303) 2.083 3.136 224 (1.124) 2.236 (29) 2.207

Derivative financial instruments 0 7 - 7 (7) 0 0 - - 0 - 0

Financial assets 12 49 2 62 (49) 13 10 - 2 12 - 12

Cash and cash equivalents 151 283 11 445 (276) 169 112 67 3 181 (14) 167

Non-current assets held for sale - - 381 381 947 1.327 - - 370 370 - 370

Total current assets 3.410 549 (431) 3.528 308 3.836 3.388 317 (648) 3.058 (48) 3.009

Total assets 4.078 5.769 (30) 9.817 (4.738) 5.078 4.102 3.540 84 7.726 (190) 7.536

Borrowings 124 - 1.459 1.583 - 1.583 554 98 1.578 2.230 - 2.230

Project finance - 3.340 159 3.499 (3.250) 249 - 2.075 163 2.239 (126) 2.112

Liabilities held for sale - - 167 167 254 421 - - 159 159 - 159

Accounts payable 2.872 510 (445) 2.936 (456) 2.481 2.458 329 (699) 2.088 (21) 2.068

Other liabilities 188 1.191 9 1.387 (1.161) 226 177 446 83 706 (107) 600

Total liabilities 3.184 5.040 1.348 9.572 (4.613) 4.959 3.189 2.949 1.284 7.422 (254) 7.169

June 30, 2016

EPC ConcessionsOther and

corporateSub-Total

Change in

consolidation

method

Total

ConsolidatedSub-Total

Change in

consolidation

method

Total

ConsolidatedEPC Concessions

Other and

corporate

December 31, 2015

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 19

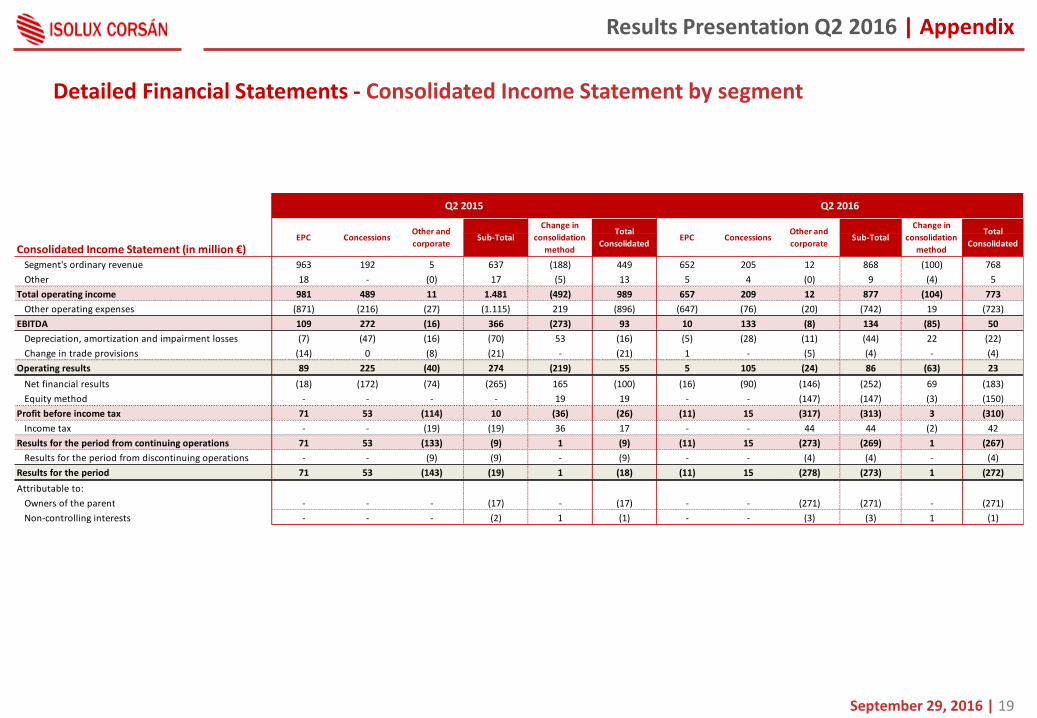

Detailed Financial Statements - Consolidated Income Statement by segment

Results Presentation Q2 2016 | Appendix

Consolidated Income Statement (in million €)Segment's ordinary revenue 963 192 5 637 (188) 449 652 205 12 868 (100) 768

Other 18 - (0) 17 (5) 13 5 4 (0) 9 (4) 5

Total operating income 981 489 11 1.481 (492) 989 657 209 12 877 (104) 773

Other operating expenses (871) (216) (27) (1.115) 219 (896) (647) (76) (20) (742) 19 (723)

EBITDA 109 272 (16) 366 (273) 93 10 133 (8) 134 (85) 50

Depreciation, amortization and impairment losses (7) (47) (16) (70) 53 (16) (5) (28) (11) (44) 22 (22)

Change in trade provisions (14) 0 (8) (21) - (21) 1 - (5) (4) - (4)

Operating results 89 225 (40) 274 (219) 55 5 105 (24) 86 (63) 23

Net financial results (18) (172) (74) (265) 165 (100) (16) (90) (146) (252) 69 (183)

Equity method - - - - 19 19 - - (147) (147) (3) (150)

Profit before income tax 71 53 (114) 10 (36) (26) (11) 15 (317) (313) 3 (310)

Income tax - - (19) (19) 36 17 - - 44 44 (2) 42

Results for the period from continuing operations 71 53 (133) (9) 1 (9) (11) 15 (273) (269) 1 (267)

Results for the period from discontinuing operations - - (9) (9) - (9) - - (4) (4) - (4)

Results for the period 71 53 (143) (19) 1 (18) (11) 15 (278) (273) 1 (272)

Attributable to:

Owners of the parent - - - (17) - (17) - - (271) (271) - (271)

Non-controlling interests - - - (2) 1 (1) - - (3) (3) 1 (1)

Q2 2015 Q2 2016

EPC ConcessionsOther and

corporateSub-Total

Change in

consolidation

method

Total

ConsolidatedEPC Concessions

Other and

corporateSub-Total

Change in

consolidation

method

Total

Consolidated

196 48 48

129 0 0

225 131 131

235 138 27

246 203

0

89 89 89

178 178 178

234 234 234

September 29, 2016 | 20

Detailed Financial Statements – Consolidated Cash Flow Statement

Results Presentation Q2 2016 | Appendix

Consolidated Cash Flow (in million €) Jan-Jun 2015 Jan-Jun 2016

Profit/(loss) for the period before taxes (38) (314)

Adjustments for non-cash items 128 319

Changes in working capital (157) (381)

Taxes paid (7) (9)

Net cash generated from /(used in) operating activities (74) (385)

Net change due to consolidation perimeter - 75

Purchase of PP&E and intangible assets (6) (6)

Sale of fixed and intangible assets - 1

Acquisition of concessionary assets and non-current assets assigned to projects (6) (65)

Net change in investments in associates and financial investments 96 1

Interests received and other financial income 1 1

Net cash used in investing activities 86 6

Proceeds /(Reimbursement) of Corporate debt, net (6) 505

Proceeds /(Reimbursement) of Project finance, net (7) (11)

Interest paid (102) (114)

Net cash flows generated from /(used in) financing activities (114) 379

March 5th 2015 | 21

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Thank you

© Isolux Corsán 2016

Isolux Corsán Investor Relations [email protected]