RENEWABLE ENERGY AND POWER GENERATION IN THE · PDF file12-06-2009 · Renewable...

21

RENEWABLE ENERGY AND POWER GENERATION IN THE PHILIPPINES: Legal Framework TREEDC – 1 ST ANNUAL INTERNATIONAL RENEWABLE ENERGY CONFERENCE Tennessee Tech University Cookeville, Tennessee October 13, 2014 Richard Anthony D. Alcazar Partner, Tan Acut Lopez & Pison

Transcript of RENEWABLE ENERGY AND POWER GENERATION IN THE · PDF file12-06-2009 · Renewable...

RENEWABLE ENERGY AND POWER GENERATION IN THE

PHILIPPINES: Legal Framework

TREEDC – 1ST ANNUAL INTERNATIONAL RENEWABLE ENERGY CONFERENCE

Tennessee Tech University

Cookeville, Tennessee

October 13, 2014

Richard Anthony D. AlcazarPartner, Tan Acut Lopez & Pison

Presentation Outline

I. Renewable Energy Act of 2008

II. Prior laws on RE as distinguished from RE Act

III. Policy Mechanisms under the RE Act1. Market Development Mechanism2. Consumer Incentives3. Production Incentives4. Commercialization Incentives

IV. Constitutional Requirements for Investments in RE

V. Foreign Equity Participation

Renewable Energy Act of 2008(RA No. 9513)

RE Act signed on December 16, 2008 and took effect on January 30, 2009

IRR of RE Act took effect on June 12, 2009

Coverage: Biomass, Geothermal, Solar, Hydro, Ocean, Wind

Accelerate the exploration and development of renewable energy resources to reduce country’s dependence on fossil fuel to reduce harmful emissions to achieve sustainable energy

development

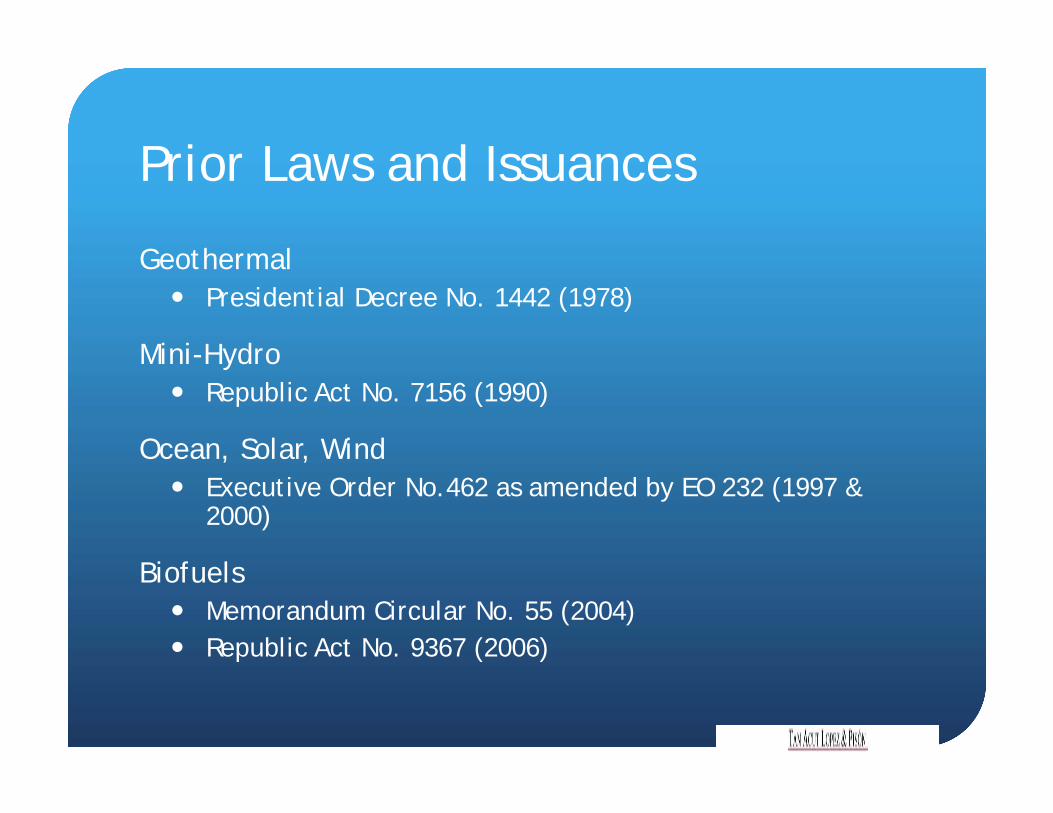

Prior Laws and Issuances

Geothermal Presidential Decree No. 1442 (1978)

Mini-Hydro Republic Act No. 7156 (1990)

Ocean, Solar, Wind Executive Order No.462 as amended by EO 232 (1997 &

2000)

Biofuels Memorandum Circular No. 55 (2004) Republic Act No. 9367 (2006)

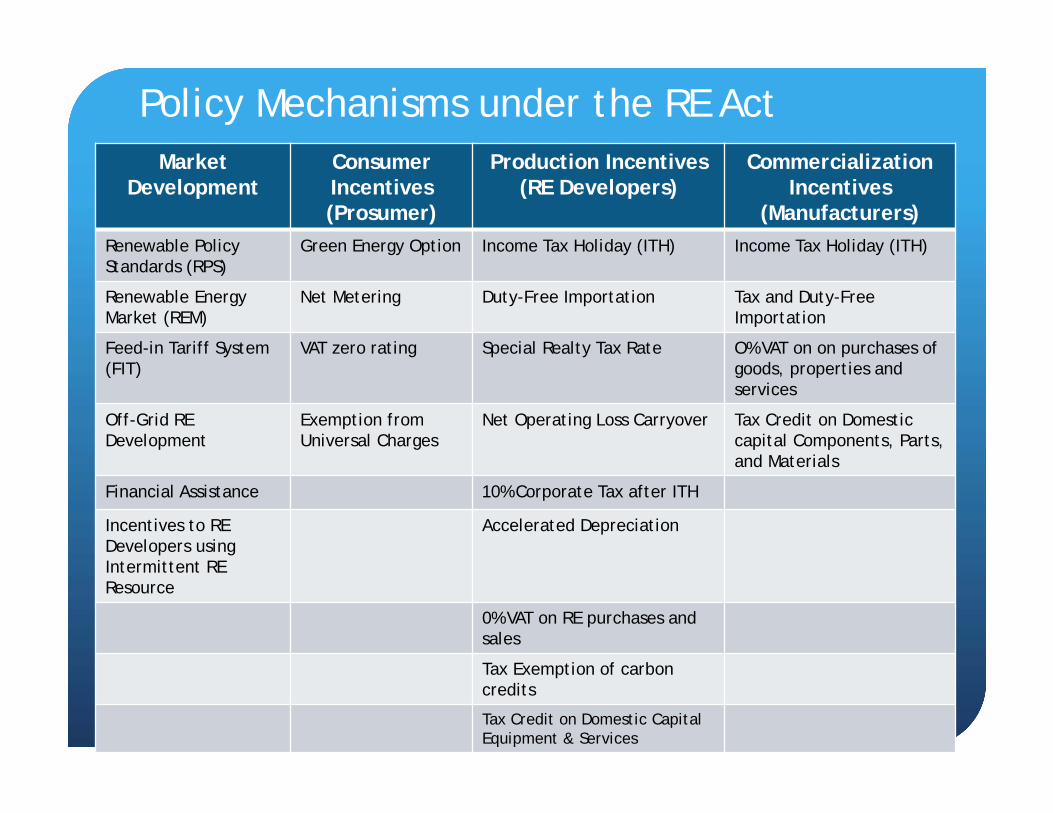

Policy Mechanisms under the RE ActMarket

DevelopmentConsumerIncentives(Prosumer)

Production Incentives(RE Developers)

CommercializationIncentives

(Manufacturers)Renewable Policy Standards (RPS)

Green Energy Option Income Tax Holiday (ITH) Income Tax Holiday (ITH)

Renewable Energy Market (REM)

Net Metering Duty-Free Importation Tax and Duty-Free Importation

Feed-in Tariff System (FIT)

VAT zero rating Special Realty Tax Rate O% VAT on on purchases of goods, properties and services

Off-Grid RE Development

Exemption from Universal Charges

Net Operating Loss Carryover Tax Credit on Domestic capital Components, Parts, and Materials

Financial Assistance 10% Corporate Tax after ITH

Incentives to RE Developers using Intermittent RE Resource

Accelerated Depreciation

0% VAT on RE purchases and sales

Tax Exemption of carbon credits

Tax Credit on Domestic Capital Equipment & Services

RE Act: Market Development

Renewable Portfolio Standard (RPS) Minimum percentage of electricity required to be sourced

or produced by electric power industry participants from eligible RE resources

Imposed on those serving on-grid areas, on a per grid basis Minimum percentage of generation from RE resources will

be based on: Sustainability of the RE Resources Available capacity of the relevant grid Available RE Resources within the specific grid

RE Certificates will be credited in compliance with any obligation under the RPS

Renewable Energy Registrar shall issue, keep, and verify RE Certificates corresponding to the energy generated from eligible RE facilities

RE Act: Market Development (Cont.)

Renewable Energy Market (REM) DOE shall establish the REM to facilitate compliance

with the RPS Submarket of Wholesale Electricity Spot Market

(WESM) where RE Certificates could be traded The rules on the operation of the REM has yet to be

established

RE Act: Market Development (Cont.) Feed-in Tariff System (FIT)

Guaranteed fixed price for at least 12 years for electricity produced from emerging RE resources.

Only electricity generated from wind, solar, ocean, run-of-river hydropower, and biomass power plants covered under the RPS shall enjoy the FIT

In July 27, 2012, the Energy Regulatory Commission approved the following FIT rates for a period 20 years for eligible RE developers:

/Assumed exchange rate is Php44.93 for every US Dollar

Computation of the FIT takes into account the cost of constructing and operating the representative plants for each RE technology, the generation output or capacity factors of the plants, and the reasonable return on investment for the RE developer.

Emerging RE Resources FIT Rate (Php/kWh)

FIT Rate(US$/kWh)

Wind 8.53 0.19

Biomass 6.63 0.15

Solar 9.68 0.22

Run-of-river hydro power 5.90 0.13

RE Act: Market Development (Cont.) Off-Grid RE Development Obligation to source minimum percentage of total annual

generation from available RE resources in the area concerned

Eligible RE generation in Off-Grid and missionary areas are entitled to RE Certificates

In case there is no viable RE resource in the off- grid and missionary areas, the relevant supplier in said areas are still obligated to comply with the RPS requirements.

Financial Assistance Program Government financial institutions to provide preferential

financial packages for the development, utilization and commercialization of RE projects duly recommended and endorsed by the DOE.

RE Act: Market Development (Cont.)

Incentives to RE Developers using intermittent RE Resources Priority and Must Dispatch Priority connection to the grid Priority purchase and transmission of, and payment for, RE

power by grid system operator RE Developer has the option to pay transmission and

wheeling charges on a per kw-hr basis at a cost equivalent to the average per kw-hr of all other electricity transmitted through the grid

RE Act: Consumption Incentives

Incentives given to end-users and consumers who are also encouraged to participate in distributed generation

Green Energy Option Mechanism that allows end-users the option to choose RE

Resources as their source of energy Transmission Company (NGCP) and the distribution utilities

are mandated to provide the mechanisms for physical connection and commercial arrangements necessary for the exercise of the option.

End-users to be informed by way of its monthly electric bill how much of the monthly energy consumption and generation charge is provided by RE facilities

RE Act: Consumption Incentives

Zero percent VAT on the sale of electricity generated from RE resources

Consumers are exempted from paying universal charges on electricity generated through RE System if: Electricity is consumed by the generators themselves

and/or Electricity is distributed free of charge to off-grid areas

• Tax rebates for all or part of the tax paid for the purchase of RE equipment for residential, industrial, or community use.

RE Act: Consumption Incentives (Cont.) Net Metering Allows end-users connected to a distribution utilities (DU)

to install an on-site RE facility not exceeding 100 kW in capacity so they can generate electricity for their own use and sell any excess electricity to the local distribution grid.

Customers of DU reduces the amount of electricity they buy and earn peso credits equivalent to the distribution utility’s (DU) blended generation cost for the excess electricity exported to the DU.

DU entitled to RE Certificate resulting from Net-Metering arrangements which shall be credited in compliance with its obligations under the RPS

Net Metering Rules was issued by the ERC on 27 May 2013

RE Act: Production IncentivesIncentives given to RE Developers

1. Income Tax Holiday (ITH) for existing, new or additional investments – 7 years

2. Accelerated depreciation of plant, machinery, and equipment in lieu of ITH Depreciation rate not exceeding twice the rate

prescribed in accordance with the Tax Code.

3. 10% corporate tax rate after availment of the ITH RE Developers shall pass on the savings to the end-users

in the form of lower power rates The ERC in coordination with the DOE shall determine

the appropriate mechanism for the power rate reduction.

RE Act: Production Incentives (Cont.)4. Net Operating Loss Carry-Over (NOLCO) during first 3

years to be carried over as deduction for the next 7 consecutive years

5. Duty free importation of machinery, equipment, materials and parts for the first 10 years

6. Zero percent VAT on:• sale of power generated from RE sources• Purchase of local goods, properties and services for the

development, construction, and installation of plant facilities

• The whole process of exploration and development of RE sources up to its conversion into power, including the services performed by subcontractors and/or contractors.

RE Act: Production Incentives (Cont.)7. Tax credit on domestic purchase of capital equipment,

machinery and spare parts equivalent to 100% of the VAT and customs duties that would have been paid on importation.

8. Realty tax on the civil works, equipment, machinery and other improvements shall not exceed 1.5% of their net book value.

9. Tax exemption of carbon credits

10. Incentives for farmers engaged in the plantation of biomass resources – Duty Free and VAT exemption on all types of agricultural inputs, equipment and machinery until 2019.

11. RE Developer servicing missionary areas are entitled to cash generation-based incentive for the power needed to service missionary areas.

RE Act: Commercialization Incentives Incentives given to manufacturers, fabricators, and

suppliers of locally produced RE equipment and components

1. Income Tax Holiday (ITH) for 7 years

2. Zero percent VAT on transactions with local suppliers of goods, properties, and services.

3. Tax and duty-free importation of components, parts, and materials that are not manufactured domestically in reasonable quantity and quality.

4. Tax credit on domestic purchase of components, parts, and materials

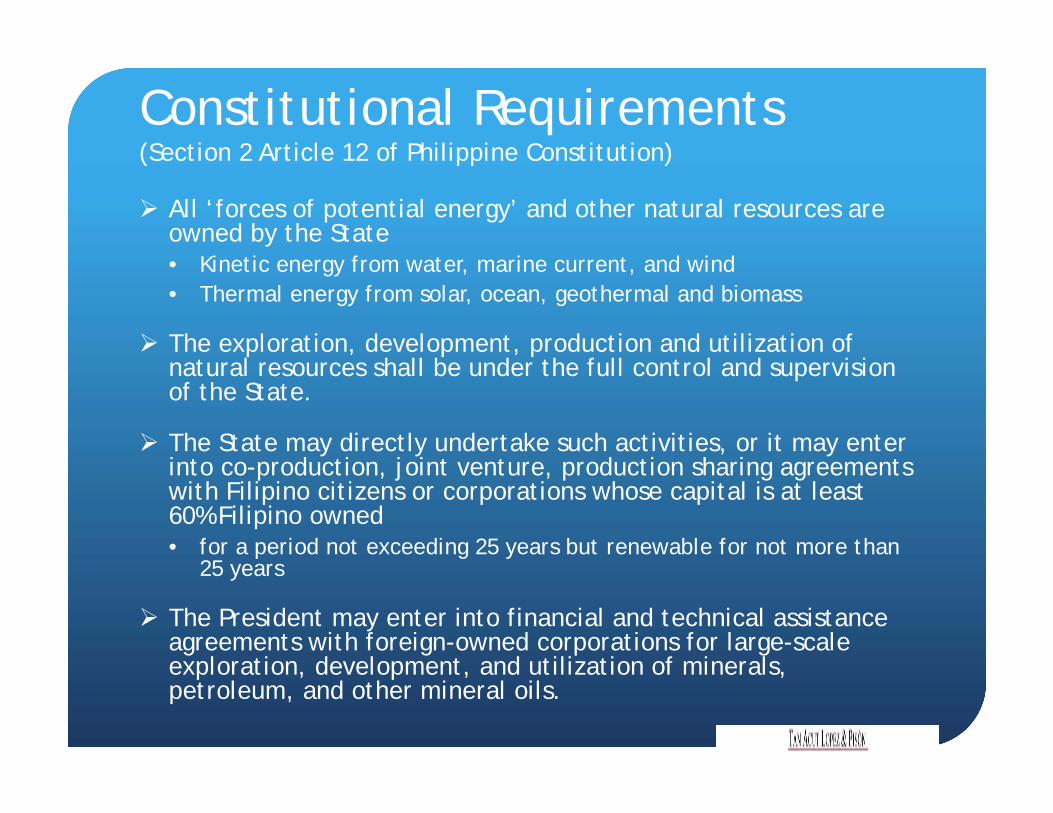

Constitutional Requirements(Section 2 Article 12 of Philippine Constitution)

All ‘forces of potential energy’ and other natural resources are owned by the State• Kinetic energy from water, marine current, and wind• Thermal energy from solar, ocean, geothermal and biomass

The exploration, development, production and utilization of natural resources shall be under the full control and supervision of the State.

The State may directly undertake such activities, or it may enter into co-production, joint venture, production sharing agreements with Filipino citizens or corporations whose capital is at least 60% Filipino owned • for a period not exceeding 25 years but renewable for not more than

25 years

The President may enter into financial and technical assistance agreements with foreign-owned corporations for large-scale exploration, development, and utilization of minerals, petroleum, and other mineral oils.

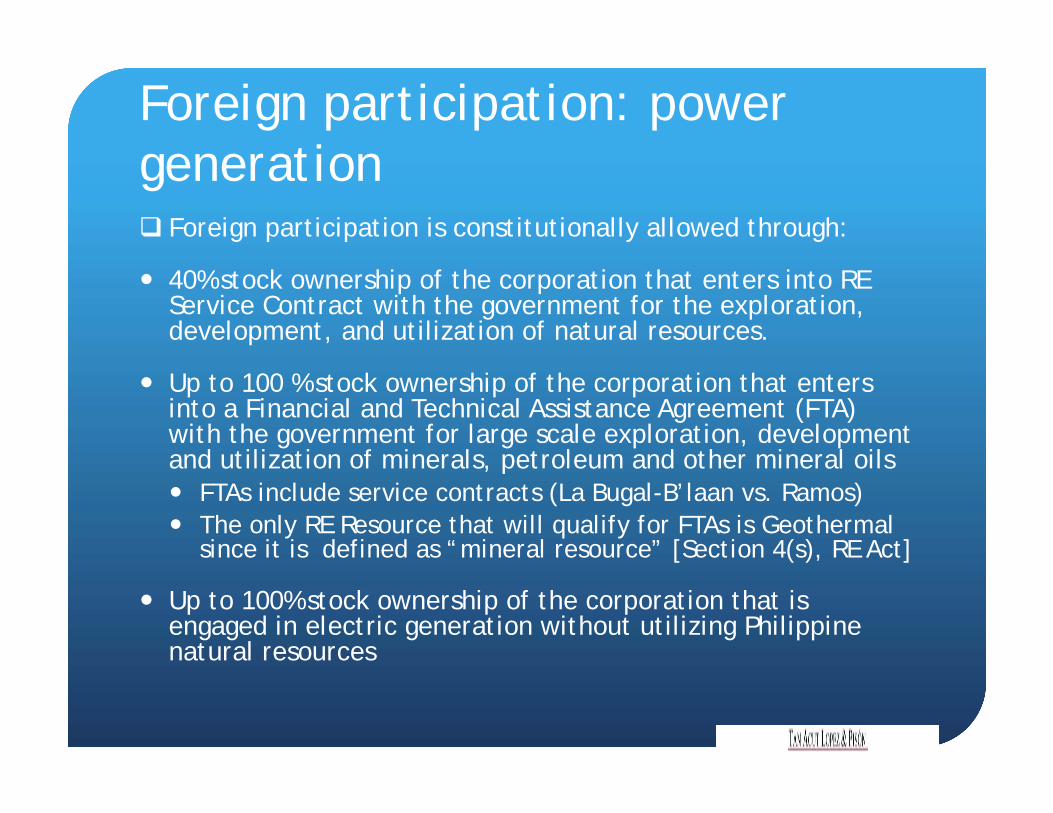

Foreign participation: power generation Foreign participation is constitutionally allowed through:

40% stock ownership of the corporation that enters into RE Service Contract with the government for the exploration, development, and utilization of natural resources.

Up to 100 % stock ownership of the corporation that enters into a Financial and Technical Assistance Agreement (FTA) with the government for large scale exploration, development and utilization of minerals, petroleum and other mineral oils FTAs include service contracts (La Bugal-B’laan vs. Ramos) The only RE Resource that will qualify for FTAs is Geothermal

since it is defined as “mineral resource” [Section 4(s), RE Act]

Up to 100% stock ownership of the corporation that is engaged in electric generation without utilizing Philippine natural resources

Foreign Participation: other RE activities (up to 100% foreign equity) Local manufacturers and fabricators of locally-produced

renewable energy equipment Export enterprises – no capitalization requirement Domestic enterprises – must have a minimum paid up capital of

US$200,000; otherwise, foreign equity will be limited to 40% Retail Trade - if manufacturer or fabricator will sell directly to the

general public (that is, retail trade) – must have a minimum paid-up capital of US$2,500,000, otherwise, foreign equity will be limited to 40%

RE Consultancy services Capitalization requirements for domestic enterprises apply

Installation and construction of RE facilities Capitalization requirements for domestic enterprises apply

Service and maintenance of RE facilities Capitalization requirements for domestic enterprises apply