QUIC RESEARCH REPORT · QUIC Research Report June 22, 2015 CCL Industries Research Report June 22,...

12

The information in this document is for EDUCATIONAL and NON-COMMERCIAL use only and is not intended to constitute specific legal, accounting, financial or tax advice for any individual. In no event will QUIC, its members or directors, or Queen’s University be liable to you or anyone else for any loss or damages whatsoever (including direct, indirect, special, incidental, consequential, exemplary or punitive damages) resulting from the use of this document, or reliance on the information or content found within this document. The information may not be reproduced or republished in any part without the prior written consent of QUIC and Queen’s University. QUIC is not in the business of advising or holding themselves out as being in the business of advising. Many factors may affect the applicability of any statement or comment that appear in our documents to an individual's particular circumstances. © Queen’s University 2015 QUIC RESEARCH REPORT QUIC Research Reports focus on emerging investment themes that affect current portfolio companies and companies under coverage. Metals & Mining Summary: CCL Industries is a Canadian-based manufacturer of labels and aluminum containers for a wide range of end markets. With over 65 years of industry experience, and a mid-range market cap compared with is peers, CCL is in a favorable position to continue pursuing successful acquisitions, while it ventures into the “high-tech” labeling industry. New company operations will rely more heavily on design services, premium market customers (luxury car and wine companies), and professional graphic arts. With this new strategy, CCL can develop new business segments in new markets—serving traditional label products to emerging markets, while innovating in mature North American, European, and Australian markets. Through this research report, we examine CCL’s present business operations, development-based investment theses, valuation metrics, and analyses behind our target price. CCL Industries (TSX:CCL.B) Consumer goods, pharma, office, food and beverage all in one stock June 22, 2015 Anson Kwok Carmen Chen Tracy Li

-

Upload

phungkhanh -

Category

Documents

-

view

223 -

download

0

Transcript of QUIC RESEARCH REPORT · QUIC Research Report June 22, 2015 CCL Industries Research Report June 22,...

The information in this document is for EDUCATIONAL and NON-COMMERCIAL use only and is not intended to constitute specific legal, accounting,

financial or tax advice for any individual. In no event will QUIC, its members or directors, or Queen’s University be liable to you or anyone else for any loss

or damages whatsoever (including direct, indirect, special, incidental, consequential, exemplary or punitive damages) resulting from the use of this

document, or reliance on the information or content found within this document. The information may not be reproduced or republished in any part

without the prior written consent of QUIC and Queen’s University.

QUIC is not in the business of advising or holding themselves out as being in the business of advising. Many factors may affect the applicability of any

statement or comment that appear in our documents to an individual's particular circumstances.

© Queen’s University 2015

QUIC RESEARCH REPORT

QUIC Research Reports focus on

emerging investment themes that

affect current portfolio companies

and companies under coverage.

Metals & Mining

Summary:

CCL Industries is a Canadian-based manufacturer of labels and aluminum

containers for a wide range of end markets. With over 65 years of

industry experience, and a mid-range market cap compared with is

peers, CCL is in a favorable position to continue pursuing successful

acquisitions, while it ventures into the “high-tech” labeling industry. New

company operations will rely more heavily on design services, premium

market customers (luxury car and wine companies), and professional

graphic arts. With this new strategy, CCL can develop new business

segments in new markets—serving traditional label products to

emerging markets, while innovating in mature North American,

European, and Australian markets.

Through this research report, we examine CCL’s present business

operations, development-based investment theses, valuation metrics,

and analyses behind our target price.

CCL Industries (TSX:CCL.B)

Consumer goods, pharma, office, food and beverage all in

one stock

June 22, 2015

Anson Kwok

Carmen Chen

Tracy Li

QUIC Research Report

June 22, 2015

CCL Industries Research Report

June 22, 2015

Table of Contents

Key Industry Characteristics 3

Business Description and History 3

Investment Theses 5

Risks and Catalysts 7

Financials and Valuation 8

References 11

Appendix 12

QUIC Research Report

June 22, 2015

CCL Industries Research Report

June 22, 2015 3

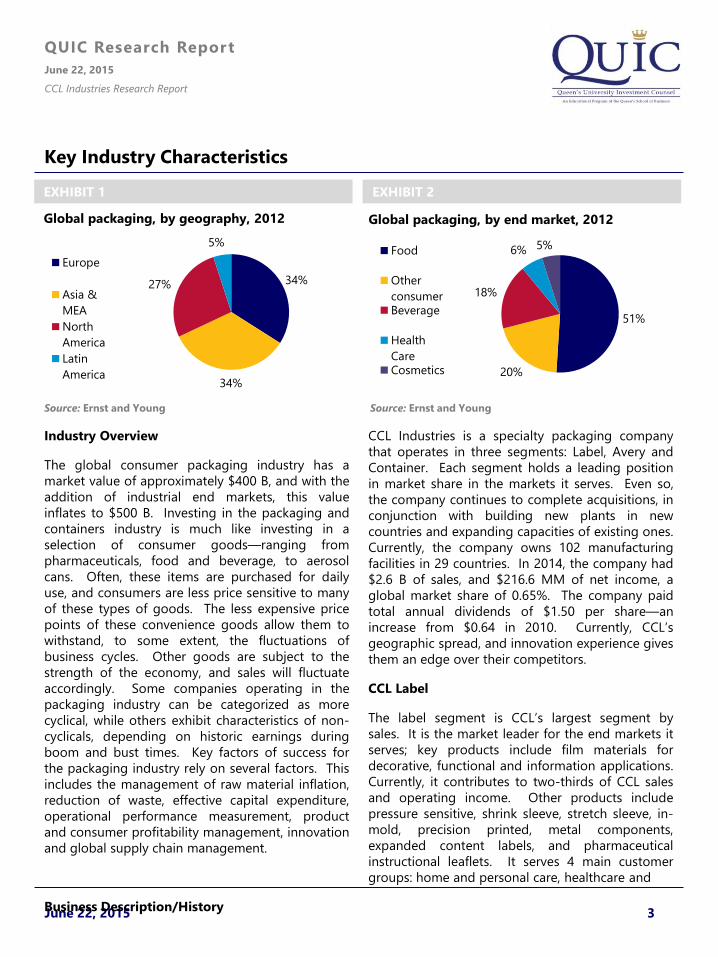

Industry Overview

The global consumer packaging industry has a

market value of approximately $400 B, and with the

addition of industrial end markets, this value

inflates to $500 B. Investing in the packaging and

containers industry is much like investing in a

selection of consumer goods—ranging from

pharmaceuticals, food and beverage, to aerosol

cans. Often, these items are purchased for daily

use, and consumers are less price sensitive to many

of these types of goods. The less expensive price

points of these convenience goods allow them to

withstand, to some extent, the fluctuations of

business cycles. Other goods are subject to the

strength of the economy, and sales will fluctuate

accordingly. Some companies operating in the

packaging industry can be categorized as more

cyclical, while others exhibit characteristics of non-

cyclicals, depending on historic earnings during

boom and bust times. Key factors of success for

the packaging industry rely on several factors. This

includes the management of raw material inflation,

reduction of waste, effective capital expenditure,

operational performance measurement, product

and consumer profitability management, innovation

and global supply chain management.

Business Description/History

CCL Industries is a specialty packaging company

that operates in three segments: Label, Avery and

Container. Each segment holds a leading position

in market share in the markets it serves. Even so,

the company continues to complete acquisitions, in

conjunction with building new plants in new

countries and expanding capacities of existing ones.

Currently, the company owns 102 manufacturing

facilities in 29 countries. In 2014, the company had

$2.6 B of sales, and $216.6 MM of net income, a

global market share of 0.65%. The company paid

total annual dividends of $1.50 per share—an

increase from $0.64 in 2010. Currently, CCL’s

geographic spread, and innovation experience gives

them an edge over their competitors.

CCL Label

The label segment is CCL’s largest segment by

sales. It is the market leader for the end markets it

serves; key products include film materials for

decorative, functional and information applications.

Currently, it contributes to two-thirds of CCL sales

and operating income. Other products include

pressure sensitive, shrink sleeve, stretch sleeve, in-

mold, precision printed, metal components,

expanded content labels, and pharmaceutical

instructional leaflets. It serves 4 main customer

groups: home and personal care, healthcare and

Key Industry Characteristics

Source: Ernst and Young

Global packaging, by geography, 2012

EXHIBIT 2EXHIBIT 1

Global packaging, by end market, 2012

34%

34%

27%

5%

Europe

Asia &

MEA

North

America

Latin

America

51%

20%

18%

6% 5%Food

Other

consumerBeverage

Health

CareCosmetics

Source: Ernst and Young

QUIC Research Report

June 22, 2015

CCL Industries Research Report

June 22, 2015 4

specialty, food and beverage, and a new CCL

Design sector.

The home and personal care sector recently

completed significant capacity expansion projects

at two North American tube plants. A successful

acquisition of Sancoa and TubeDec—companies

producing labelled and laminated products helped

boost sales in 2013.

The healthcare and specialty line is CCL’s highest-

margin sector. Food and beverage has experienced

years of improved sales. CCL design is the newest

addition to the Label sector, seeking to invest in

facilities, find new markets and develop advanced

technologies.

CCL Avery

Avery Dennison Corporation was acquired by CCL

Industries in 2013, for $500 MM. Avery operates

two major product lines—printable media and

BOPWI. Its printable media line manufactures and

sells labels, marketing and product identification

labels, dividers, business cards, name badges and

specialty media labels. Its BOPWI segment includes

binders, dividers, sheet protectors and writing

instruments. While it sells ready-to-go supplies, its

“web-to-print” services have grown in popularity as

well, as consumers look for more customization and

e-retailing becomes more integral to sales. Pro

Media is another important service, offering a range

of pre-die cut labels used by large format

professional digital printers.

CCL Container

The container product line includes recyclable

aluminum aerosol cans and bottles for personal

use, home care, cosmetic industries, and aluminum

bottles for the beverage market. In 2014, a joint

venture with Reinfelden from Germany, a specialty

chemicals group, was announced to build a new

aluminum slug plant in the US. The aluminum

aerosol industry has only one credible source of

supply in NAFTA countries. This project will thus

serve as a great alternative to North American

producers.

Business Description and History

EXHIBIT 3

Source: Company Reports

Revenue $MM, 2010-14

EXHIBIT 4

EBITDA, 2010-14

Source: Company Reports

$75 $81 $83

$190

$201

$0

$1,000

$2,000

$3,000

2010 2011 2012 2013 2014

Label Avery Container

$221

$239 $255

$339

$482

$200

$300

$400

$500

2010 2011 2012 2013 2014

EBITDA, $MM

QUIC Research Report

June 22, 2015

CCL Industries Research Report

June 22, 2015 5

Investment Thesis I – New growth opportunities

Historically, CCL’s revenue stemmed primarily from

consumer staples companies, which provided the

company with consistent streams of revenue.

However, the issue with the traditional labeling

market are its lower-yielding margins from

traditional single-ply adhesive labels that are placed

on price-taking consumer goods. From CCL’s

investments and their recent acquisitions, it is

evident that the company aims to shift itself into

higher-margin industries where there is more space

for product innovation, design service offerings,

and consequently, customers with higher

willingness to pay.

CCL Label’s new CCL Design sub-segment targets

companies in automotive, security, and other

specialty sectors. Auto industry labeling in

particular is a new initiative that CCL Design

established in 2014. Currently, it has a fresh

presence in Germany, where customers include

luxury auto brands like Mercedez-Benz, Mercedez-

AMG, Maybach, and BMW. CCL can thus penetrate

the European luxury car market, and expand into

China and other areas of Southeast Asia, where

luxury car sales make up a bigger segment of total

car sales than in Europe or the US.

CCL Design’s other area of emphasis is automotive

safety, which falls in line with its existing security

label product line. Auto safety is an inalterable

need—car manufacturers will take increased

precautions to market more in-car features, and

consumers will become more safety-conscious.

External influences such as government regulations

and increased consumer purchasing power in

emerging markets will boost market supply of such

goods. CCL Design captures traditional safety

features labeling, such as airbag labels, but also has

new design services for telematics support. This

includes plastic and aluminum holders for GPS

navigation systems, smartphones and charging

devices. These parts will become more integral for

vehicles and will fit consumer needs in the US

market especially, where sales to cash flow growth

will be quick.

To support its ambitions, CCL Design’s expansion is

met with a $30 MM investment package for Design-

related greenfield plants and equipment upgrades.

Part of this included the 2015 acquisition of INT

America in Detroit, Michigan, a private company

that manufactures metal tread plates for domestic

automotive equipment manufacturers. Mirroring its

operations in Germany, CCL will likely target luxury

makers like Fiat-Chrysler and Jaguar for its interior

décor design services, but the acquisition of INT

America also implies a focus on functional parts

manufacturing. We are optimistic about this

strategic shift. We also see a possible

discontinuation of CCL Container, or little

acquisition activity in this segment as a result in the

future. Margins in this sector have been historically

lower than Label and Avery—only 8%, compared to

16% Avery, and 14% Label in 2014.

Investment Theses

EXHIBIT 5

Source: Company Reports

New Products and Markets

Segment Products Applications

Auto Protective Film, Sill

design, Machine &

Equipment

Displays

Custom car

design;

functional

protection;

safety-labelling

Security Tamper-evident;

track-and trace;

security pigment

Pharmaceuticals;

electronics

Specialty Plastics for

coloured LED

lights; expanded

content labels for

regulatory

information

Industry; office;

specialty

chemicals; multi-

lingual product

descriptions

QUIC Research Report

June 22, 2015

CCL Industries Research Report

June 22, 2015 6

Investment Thesis II – Product Development in

CCL Label and Avery

Following the company’s shift towards higher-

margin industries, traditional labeling products for

CCL Label and Avery are offering more innovative

varieties to satisfy customer preferences for

premium-quality, environmental friendly, personal

safety, and customization features.

CCL Label’s frontier innovations for the beverage

market include super stretch sleeves that decorate

PET beverage containers without adhesives, and

“wash-off” labels for reusable bottles. With

beverage labels, there is growing emphasis on

aesthetic quality, and other premium features such

as dual-ply labels, where the top layer can rip away

to reveal more information underneath. Super

stretch sleeves are able to mold into the shape of

the bottle itself—offering more grocery-shelf

differentiation. Other innovations include

“intelligent” packaging and radio-frequency

identification labels, which use electromagnetic

fields to transmit data and store information. These

intelligent labels are sensitive to environmental

changes such as exposures to certain gases, or

unwanted manipulation. This gives a nod to

higher-tech product development for use in the

pharmaceutical or food packaging fields.

Applications of these innovations will sustain the

strong demand that CCL has seen from its food,

beverage and pharmaceutical markets, and provide

CCL with a stronger competitive edge against its

competitors.

The Avery segment is positioned to provide

customers with more customization options, after

its success with CCL so far in more traditional

labeling products. In 2014, Avery launched a new

customer arm named “We Print” targeting North

American small businesses and individuals that is

easy to use, quick and affordable. It offers clients

customization options online, and home/business

deliveries of custom orders. A complementary 2014

acquisition of German e-commerce company Nilles

for $17.3 MM targets larger European businesses

wishing to purchase custom designed labels. Avery

also launched a new high-margin “Printable Media”

product line that targets the graphic arts market,

and looks to enter into the software/printing

market with new copier, ink-jet and laser printer

labels and corresponding computer software. As

such, Avery is able to offer product suites, in which

design, materials, and software can be purchased at

once. This gives the company space to develop

further business contracts with larger retailers, while

satisfying demands of individual consumers.

Investment Theses

QUIC Research Report

June 22, 2015

CCL Industries Research Report

June 22, 2015 7

Investment Thesis III – Noncyclical

characteristics in a cyclical industry

As a company operating in a cyclical industry,

strong global macroeconomic outlook should

benefit CCL and provide a good environment

conducive to growth. US consumer spending and

GDP growth looks strong, as do numbers across

Southeast Asia, where sales experienced double-

digit growth in 2014 from 2013 in CCL’s Label

segment. 2007 was an especially good year for the

company, as EPS rose by 90.8% to $4.58. CCL

positioned itself for accelerated growth, with extra

cash on hand to pursue acquisitions or plant

expansion. However, the 2008 financial crisis

erased much of the momentum created in 2007,

and was reflected in a drop in CCL’s share price

from end 2007 highs. In 2014, CCL re-invested in

accelerated growth through bolt-on acquisitions,

and seeks to continue down this path with no

supply or demand side impediments. The last 5

years have demonstrated steady growth for the

company with no indicators of negative effects

from a sluggish post-recession global economy.

The price of raw material inputs, such as plastics,

resins, papers, specialty chemicals, and aluminum

are typically of concern for companies in packaging

and labelling. However, as a company with

geographic diversification of its plants, and over 60

years of operations, CCL has the ability to mitigate

this volatility through long-term contracts with

most of its suppliers.

Investment Theses, Catalysts, and Risks

Catalysts

1. US auto-sector growth: In February 2015, CCL acquired INT America LLC, a private company in Detroit,

Michigan. Unlike other acquisitions completed previously, INT manufactures metal tread plates for

domestic automotive equipment manufacturers. The US auto and durable goods markets have seen good

post-recession recoveries, as the US economy strengthens.

2. Plant extensions and equipment purchases in the US: Investments totaling $30 MM (including the

$4.75 MM purchase of INT America), will be made into extending and upgrading US manufacturing

divisions that focus on the Electronics and Home Appliance markets.

Risks

1. Rise in internet-based digital communication and data storage: The rise in digital communication

and data storage is a risk for CCL label and Avery segments. The move of documents from paper to

computer and cloud-based storage systems decreases consumer demand for paper labels, which could

negatively affect long term sales growth. CCL has a very diversified portfolio, with 95% of revenue coming

from countries outside Canada, thus this trend should not materially impact results in the near-term.

However, product innovation in traditional label segments will have to cater to design, price or quality

trends to compete with digitalization. The increased targeting of new markets is another option for CCL.

2. Decline in traditional mail: Traditional mail volumes have declined significantly in recent years in the

North American and European markets. Email swiftly replace mailed letters for personal and business use;

banks offer digital account statements to clients; home mail delivery is decreasing, and will likely be phased

out altogether in the next 5 years. This trend directly impacts address label sales volumes in the markets

that Avery operates in.

QUIC Research Report

June 22, 2015

CCL Industries Research Report

June 22, 2015 8

Historically, CCL has demonstrated sound revenue

growth, successful acquisition completion, and fiscal

responsibility. Market cap increased more than 6

fold since 2005, with the most explosive growth

occurring in 2013-14, during which it had its highest

historic ROE and ROTC ratios. Looking at a 10-year

cycle of ROE and ROTC, the company demonstrates

robust operating efficiency. 2005-07 growth

dropped off with the natural business cycle

recession, and since 2010, the ratios suggest a good

recovery. Going forwards, expected expansions in

CCL Design and Avery, specialty industries growth,

and product innovation will require greater R&D

and capex expenses.

CCL pays close attention to sustaining its margins,

regardless of the business activities mix it pursues.

From the past 5 years of operations, EBITDA

margins have remained steady at 19%. In light of

more expansions, and a business segment focus

shift, the company ‘s strong FCF and additional

$300 MM line of credit will likely keep margins at

19%, while we should see an increase with a change

in strategic focus to boost margins.

Depreciation has been slightly above capex for the

past 5 years, suggesting that the company has been

underinvesting its capital. This implies that there is

more space in the future to pursue higher-tech PPE

expansion—particularly in the United States, which

CCL plants are not as widespread compared to

Europe.

Unlevered cash flow growth has exceeded EBITDA

growth over the last 5 years (with the exception of

2011, in which CCL experienced a decline in FCF

over 2012). Capex growth has not exceeded EBITDA

either—in absolute terms or yearly growth. It has

also been in-line with annual depreciation figures—

thus FCF has been able to grow at a favourable rate,

giving financial flexibility for capex spending and

other expenses. All in all, this implies that CCL has

the ability to save cash at a higher rate than what it

spends.

This kind of fiscal conservatism is well reflected in

company debt levels as well. Looking at net debt to

total book capitalization, CCL currently has a ratio

of 26.4%, while higher than historic levels, is still fair

given the 2013 Avery acquisition (costing more than

double of net income), and a doubling of market

cap within 3 years. Furthermore, leverage to

EBITDA fell to 0.9x, despite 5 strategic acquisitions

since Avery, debt repayments and restructuring

expenses. With a low accumulation of debt

obligations, even during post-recession years of

2010-12, CCL can likely deliver on its future

commitments to increase dividend growth, as it has

in the past.

CCL is poised to post steady increases in EPS

growth as ROC and ROE have been increasing

steadily. Not only does this imply greater returns

per share (should P/E be sustained or increased),

but also further dividend growth. CCL’s board of

directors recently declared a 25% increase in the

dividend, $0.075 more per Class B share per quarter

to $0.38. In 2014, the payout ratio was 17%. In

2010, quarterly dividends were less than half, at

$0.175 per share in 2010.

P/B rests on the higher side, at 3.93 currently,

relative to its peers. However, PEG looks

favorable—at 0.26x. The low PEG offsets some

concern with a slightly higher P/E of 22.6x. As long

as growth looks favorable, management should be

able to successfully complete further acquisitions as

it has historically, and sustain its operating margins.

Financials and Valuation

QUIC Research Report

June 22, 2015

CCL Industries Research Report

June 22, 2015 9

Financials and Valuation

EXHIBIT 7

Source: Company Reports

EBITDA, Levered FCF Growth YoY, 2010-14

$95 $100 $103

$120

$146

$86$81

$94

$116

$154

$0

$60

$120

$180

2010 2011 2012 2013 2014

Depreciation Capex

EXHIBIT 8

Depreciation v. capex, $MM, 2010-14

Source: Company Reports

2009.5 2010 2010.5 2011 2011.5 2012 2012.5 2013 2013.5 2014 2014.5

(60%)

(20%)

20%

60%

100%

140%

$200

$300

$400

$500

2010 2011 2012 2013 2014

EBITDA, $MM, LHS Levered FCF Growth YoY, RHS

EXHIBIT 6

10%11%

14%

7%6%

10%11% 11%

16%

20%

7% 7%7% 7%

5%7%

8%10%

12%

14%

0%

5%

10%

15%

20%

25%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Return on equity Return on total capital

ROE, ROTC, 2005-14

Source: Company Reports

QUIC Research Report

June 22, 2015

CCL Industries Research Report

June 22, 2015 10

Comparables Analysis

Chemicals Market Enterprise EV / EBITDA P/CF Dividend Price / Earnings Net Debt/EBITDA

Cap ($MM) Value ($MM) LTM 2014E 2015E LTM Yield 2014E 2015E 2014E 2015E

E. I. du Pont de Nemours and Company* $63,222 $70,156 11.8x 10.3x 9.8x 19.0x 2.8% 17.7x 15.8x 1.0x 0.9x

The Dow Chemical Company* $61,425 $80,361 8.7x 8.9x 8.3x 8.8x 3.2% 17.6x 15.0x 1.5x 1.4x

Monsanto Company* $53,623 $59,227 13.8x 11.8x 10.9x 21.6x 1.7% 19.1x 16.2x nmf 1.0x

Methanex $6,182 $7,691 9.7x 10.4x 7.2x 6.4x 2.0% 18.9x 10.6x 1.5x 1.1x

Winpak Ltd $2,479 $2,297 11.4x 10.0x 9.0x nmf 0.3% 19.7x 17.5x nmf nmf

Chemtrade Logistics Income Fund $1,404 $2,308 10.5x 9.4x 9.1x 13.1x 5.9% 31.7x 23.5x 3.7x 3.6x

Intertape Polymer Group $1,072 $1,244 10.7x 8.6x 7.3x 12.1x 3.3% 14.5x 11.6x 1.2x 1.0x

Canexus $285 $921 10.0x 8.8x 8.0x 13.1x 2.6% nmf 12.0x 6.1x 5.5x

Richards Packaging Income Fund $186 $236 9.6x nmf nmf nmf 5.5% nmf nmf nmf nmf

Mean $19,687 $23,197 10.8x 9.8x 8.7x 13.4x 2.8% 20.1x 16.2x 2.1x 2.1x

Median $3,774 $3,951 10.7x 9.7x 8.6x 13.1x 2.5% 19.0x 16.3x 1.3x 1.1x

CCL Industries $5,167 $5,703 11.2x 10.2x 9.6x 13.0x 1.0% 19.8x 17.9x 1.0x 0.9x

Comparable Companies

The two companies offering very similar products to CCL are Winpak Ltd, and Richards Packaging Income

Fund. CCL’s EV/EBITDA, P/CF and P/E multiples trade fairly—slightly above the subsector averages, at 9.6x,

13.0x and 17.9x. Across the peer group, CCL compares favourably for its net debt/EBITDA multiple, trading

at 0.9x, well below the mean of 2.1x. Multiples for Winpak and CCL are very close, suggesting that both

companies are valued similarly in their industry.

$172

$172

$173

$180

$193

Laurentian Bank Securities

BMO

QUIC

TD

Industrial Alliance

Securities

Target Price

Target Return

Current Share Price $149.65

Target Share Price $173.62

Dividend Yield 1.00%

12-Month Return 17.02%

Based on a terminal EBITDA multiple of 18.5x and a discount rate of 8.3%, our DCF model (Appendix)

results in a target price of $173.62.

QUIC Research Report

June 22, 2015

CCL Industries Research Report

June 22, 2015 11

1. World Packaging Association

2. Capital IQ

3. Bloomberg

4. Ernst and Young

5. TD Securities

6. Thomson ONE

7. Globe and Mail

References

QUIC Research Report

June 22, 2015

CCL Industries Research Report

June 22, 2015 12

Appendix: DCF Valuation

Historical Projected

FY2010 FY2011 FY2012 FY2013 FY2014 2015 2016 2017 2018 2019

Revenue: $1,192 $1,268 $1,309 $1,889 $2,586 $3,103 $3,475 $3,788 $4,053 $4,256

YoY Growth % 6% 3% 44% 37% 20% 12% 9% 7% 5%

Cost of Goods Sold: $916 $975 $996 $1,414 $1,892 $2,327 $2,641 $2,917 $3,040 $3,192

% Total Revenue 77% 77% 76% 75% 73% 75% 76% 77% 75% 75%

Gross Profit: $276 $294 $312 $475 $694 $776 $834 $871 $1,013 $1,064

Margin % 23% 23% 24% 25% 27% 27% 27% 27% 27% 27%

Operating Expneses: 55 55 58 137 213 255 286 312 333 350

% Total Revenue 5% 4% 4% 7% 8% 8% 8% 8% 8% 8%

EBITDA 221 239 255 339 481 578 647 705 755 792

% Total Revenue 19% 19% 19% 18% 19% 19% 19% 19% 19% 19%

YoY Growth % 2% 3% (8%) 4% 20% 12% 9% 7% 5%

Less: Depreciation and Amortization 95 100 103 120 146 176 197 214 229 241

% Total Revenue 8% 8% 8% 6% 6% 6% 6% 6% 6% 6%

EBIT 125 139 152 219 335 402 450 491 525 552

% Total Revenue 11% 11% 12% 12% 13% 13% 13% 13% 13% 13%

% YoY Growth 11% 9% 44% 53% 20% 12% 9% 7% 5%

Less: Interest Expense 28 23 22 24 24 29 32 35 38 40

% Total Revenue 2% 2% 2% 1% 1% 1% 1% 1% 1% 1%

Less: Income Taxes 28 34 36 46 88 117 131 142 152 160

Effective Tax Rate % 28% 29% 27% 31% 29% 29% 29% 29% 29% 29%

Net Operating Profit After Tax $71 $84 $97 $104 $217 $257 $288 $313 $335 $352

YoY Growth % 18% 16% 6% 109% 19% 12% 9% 7% 5%

Plus: Depreciation and Amortization 95 100 103 120 146 176 197 214 229 241

Less: Capital Expenditures 86 81 94 116 154 184 207 225 241 253

% Total Revenue 7% 6% 7% 6% 6% 6% 6% 6% 6% 6%

Less: Change in Net Working Capital 39 (16) 71 (4) 6 17 10 43 15

UFCF $81 $64 $122 $37 $213 $242 $261 $292 $281 $325

Discount Period 0.5 1.5 2.5 3.5 4.5

Discount Factor 96% 89% 82% 75% 70%

Present Value of UFCF $233 $231 $239 $212 $226

Share Price Calculation

Multiples Method Yes

Discount Rate 8.37%

Terminal EBITDA Multiple 18.6x

Terminal Year Growth Rate 2.00%

Terminal Value $14,735

PV of Terminal Value $10,261

Sum of PV of Cash Flows $1,283

Enterprise Value $11,543

Enterprise Value $11,543

Less: Total Debt $7,761

Plus: Cash and cash equivalents $2,297

Less: Other liabilities $0

Implied Equity Value $6,079

FDSO 35

Implied Share Price $173.62

$173.62 6.8% 7.3% 7.8% 8.3% 8.8% 9.3% 9.8%

17.0x 166.74$ 160.79$ 154.99$ 149.33$ 143.82$ 138.44$ 133.20$

17.5x 175.15$ 169.03$ 163.06$ 157.23$ 151.56$ 146.03$ 140.63$

18.0x 183.57$ 177.27$ 171.13$ 165.14$ 159.30$ 153.61$ 148.06$

18.5x 191.99$ 185.51$ 179.20$ 173.04$ 167.04$ 161.19$ 155.49$

19.0x 200.40$ 193.75$ 187.27$ 180.95$ 174.79$ 168.78$ 162.92$

19.5x 208.82$ 201.99$ 195.34$ 188.85$ 182.53$ 176.36$ 170.35$

20.0x 217.24$ 210.23$ 203.41$ 196.76$ 190.27$ 183.95$ 177.78$

Discount Rate

Term

inal

EB

ITD

A M

ult

iple