Quarterly outlook and model portfolio allocations...Short-term government bond yields are...

6

AGF ASSET ALLOCATION COMMITTEE Q3 2020 Quarterly outlook and model portfolio allocations Asset allocation The AGF Asset Allocation Committee is positioned modestly overweight equities as global markets recover with the help of fiscal and monetary stimulus. Some economies have begun reopening with little disruption thus far, however other a resurgence of COVID-19 cases in other key markets may trigger bouts of volatility along the way. We expect the direction of the virus will ultimately define the strength of financial markets in the upcoming quarter. The AAC’s overweight position towards equities is slightly increased to 63.0% with assets reallocated from cash. The underweight to fixed income remains as well as a modest allocation to cash to soften the impact of volatility. 0% 10% 20% 30% 40% 50% 60% 70% Cash Fixed Income Equity 62.5 35.0 2.5 63.0 35.0 2.0 60.0 40.0 0.0 FIGURE 1: Asset allocations Q2-2020 Model Q3-2020 Model Benchmark Source: AGF Asset Allocation Committee, as of July 2020. Benchmark: 10% Bloomberg Barclays Canada Aggregate Bond Index / 25% Bloomberg Barclays Global Aggregate Bond Index / 2.5% Bank of America/Merrill Lynch U.S. High Yield Master II Total Return Index / 2.5% JPMorgan EMBI Global Total Return Index / 16.5% S&P/TSX Capped Composite Total Return Index / 24.2% S&P 500 Total Return Index / 9.3% MSCI Europe / 3.5% MSCI Japan / 1.7% MSCI Pacific ex-Japan / 4.8% MSCI Emerging Markets

Transcript of Quarterly outlook and model portfolio allocations...Short-term government bond yields are...

A G F A S S E T ALLOCATION COMMIT TEE

Q3 2020

Quarterly outlook and model portfolio allocations

Asset allocation

The AGF Asset Allocation Committee is positioned modestly

overweight equities as global markets recover with the help

of fiscal and monetary stimulus. Some economies have

begun reopening with little disruption thus far, however

other a resurgence of COVID-19 cases in other key markets

may trigger bouts of volatility along the way. We expect the

direction of the virus will ultimately define the strength of

financial markets in the upcoming quarter.

The AAC’s overweight position towards equities is slightly

increased to 63.0% with assets reallocated from cash. The

underweight to fixed income remains as well as a modest

allocation to cash to soften the impact of volatility.

0%

10%

20%

30%

40%

50%

60%

70%

CashFixed IncomeEquity

0%

10%

20%

30%

40%

50%

60%

70%

CashFixed IncomeEquity

62.5

35.0

2.5

63.0

35.0

2.0

60.0

40.0

0.0

FIGURE 1: Asset allocations

Q2-2020 Model Q3-2020 Model Benchmark

Source: AGF Asset Allocation Committee, as of July 2020.

Benchmark: 10% Bloomberg Barclays Canada Aggregate Bond Index / 25% Bloomberg Barclays Global Aggregate Bond Index / 2.5% Bank of America/Merrill Lynch U.S. High Yield Master II Total Return Index / 2.5% JPMorgan EMBI Global Total Return Index / 16.5% S&P/TSX Capped Composite Total Return Index / 24.2% S&P 500 Total Return Index / 9.3% MSCI Europe / 3.5% MSCI Japan / 1.7% MSCI Pacifi c ex-Japan / 4.8% MSCI Emerging Markets

AAC OUTLOOK Q3 2020

2

Source: AGF Asset Allocation Committee, as of July 2020. Benchmark: 16.5% S&P/TSX Capped Composite Total Return Index / 24.2% S&P 500 Total Return Index / 9.3% MSCI Europe / 3.5% MSCI Japan / 1.7% MSCI Pacific ex-Japan / 4.8% MSCI Emerging Markets

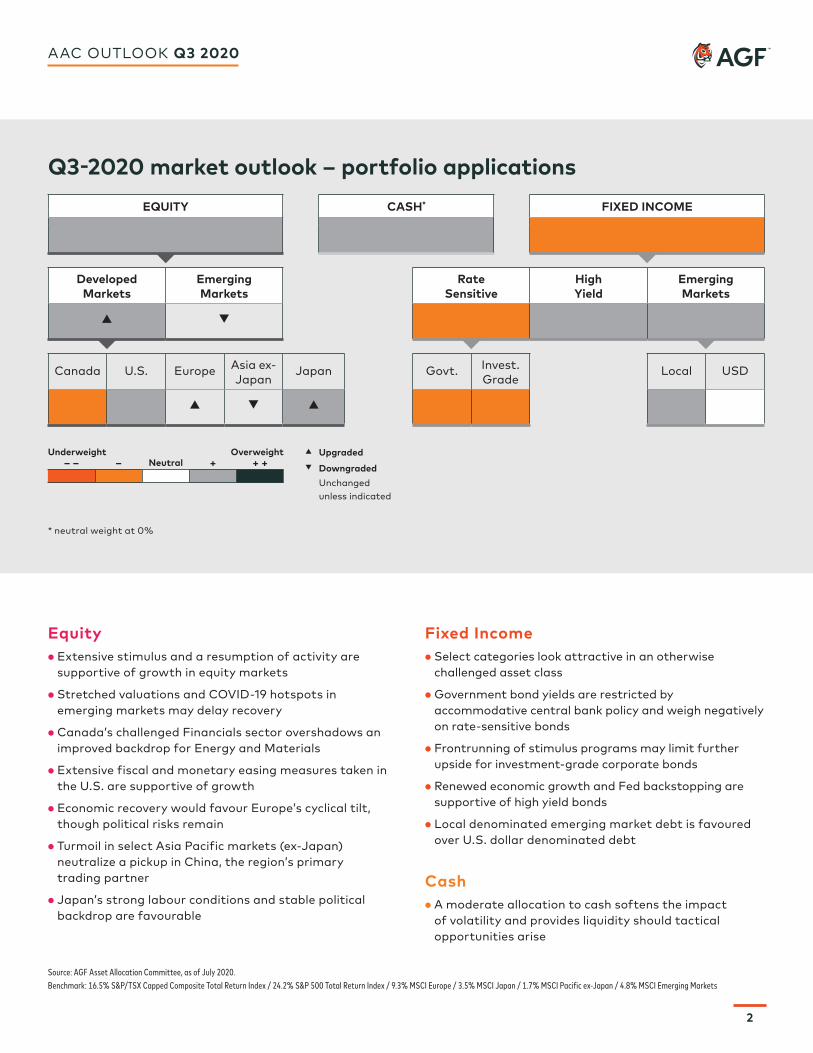

Equity• Extensive stimulus and a resumption of activity are

supportive of growth in equity markets

• Stretched valuations and COVID-19 hotspots in emerging markets may delay recovery

• Canada’s challenged Financials sector overshadows an improved backdrop for Energy and Materials

• Extensive fiscal and monetary easing measures taken in the U.S. are supportive of growth

• Economic recovery would favour Europe’s cyclical tilt, though political risks remain

• Turmoil in select Asia Pacific markets (ex-Japan) neutralize a pickup in China, the region’s primary trading partner

• Japan’s strong labour conditions and stable political backdrop are favourable

Fixed Income• Select categories look attractive in an otherwise

challenged asset class

• Government bond yields are restricted by accommodative central bank policy and weigh negatively on rate-sensitive bonds

• Frontrunning of stimulus programs may limit further upside for investment-grade corporate bonds

• Renewed economic growth and Fed backstopping are supportive of high yield bonds

• Local denominated emerging market debt is favoured over U.S. dollar denominated debt

Cash• A moderate allocation to cash softens the impact

of volatility and provides liquidity should tactical opportunities arise

Q3-2020 market outlook – portfolio applications

Underweight Overweight– – – Neutral + + +

▴ Upgraded

▾ Downgraded

Unchanged unless indicated

EQUITY CASH** FIXED INCOME

Canada U.S. Europe Asia ex-Japan

Japan Govt. Invest. Grade

Local USD

▴ ▾ ▴

Developed Markets

Emerging Markets

Rate Sensitive

High Yield

Emerging Markets

▴ ▾

* neutral weight at 0%

AAC OUTLOOK Q3 2020

3

Equity allocationThe small overweight to equities is increased as monetary

and fiscal stimulus are supportive of continued recovery

into the second half of 2020. Beyond government

stimulus, however, a lack of near-term catalysts may

limit upside potential. Equity market growth may be

bifurcated between those able to maintain a pace of

reopening without a resurgence in cases versus those

who suffer setbacks.

The Committee prefers developed markets (DM) over

emerging markets (EM) for the upcoming quarter. A

restart in manufacturing activity and inflating DM

central bank balance sheets should positively impact

EM countries over the longer term, however stretched

fundamentals and COVID-19 hotspots lead to a neutral

view at this time.

Developed market equities remain attractive, though

the Committee’s constructive view is generally focused

towards select countries.

Canada’s dependence on its challenged Financials sector

overshadows improved near-term conditions for Energy

and Materials. The Committee has further increased their

underweight position for the upcoming quarter.

Extensive fiscal aid and monetary easing measures

implemented in the U.S. are supportive of growth.

Company fundamentals remain constructive and leading

efforts towards a COVID-vaccine reflect positively on

equities. The U.S. is experiencing a resurgence in virus

cases, however, which may lead to elevated volatility and

disrupt the resumption in business activity.

The Committee’s outlook for Europe is improved to a

neutral position. A global economic recovery would favour

the region’s tilt towards cyclicals and manufacturing

industries, also helped by monetary stimulus. Political

overhang may limit upside, however, in regards to Brexit

proceedings and U.S. trade tariffs.

Asia Pacific Markets (ex-Japan) are supported by a pickup

in Chinese activity, however geopolitical risk in Hong Kong

and a challenged backdrop in Australia weigh negatively

on the group. The Committee has reduced its overweight

to a neutral position for the upcoming quarter.

Japan is among the most favoured developed markets.

The country has been less impacted by the COVID-19 virus

as compared to other regions, causing fewer disruptions

in employment and economic activity. Room for further

fiscal stimulus remains as well, if required.

FIGURE 2: Equity allocations

0%

5%

10%

15%

20%

25%

30%

Emerging marketsJapanAsia Pacific (ex-Japan)EuropeUnited StatesCanada

0%

5%

10%

15%

20%

25%

30%

Emerging marketsJapanAsia Pacific (ex-Japan)EuropeUnited StatesCanada

12.0 11.5

16.5

27.029.0

24.2

7.09.0 9.3

3.0 2.0 1.74.5

6.5

3.5

9.0

5.0 4.8

Q2-2020 Model Q3-2020 Model Benchmark

Source: AGF Asset Allocation Committee, as of July 2020.Benchmark: 16.5% S&P/TSX Capped Composite Total Return Index / 24.2% S&P 500 Total Return Index / 9.3% MSCI Europe / 3.5% MSCI Japan / 1.7% MSCI Pacific ex-Japan / 4.8% MSCI Emerging Markets

4

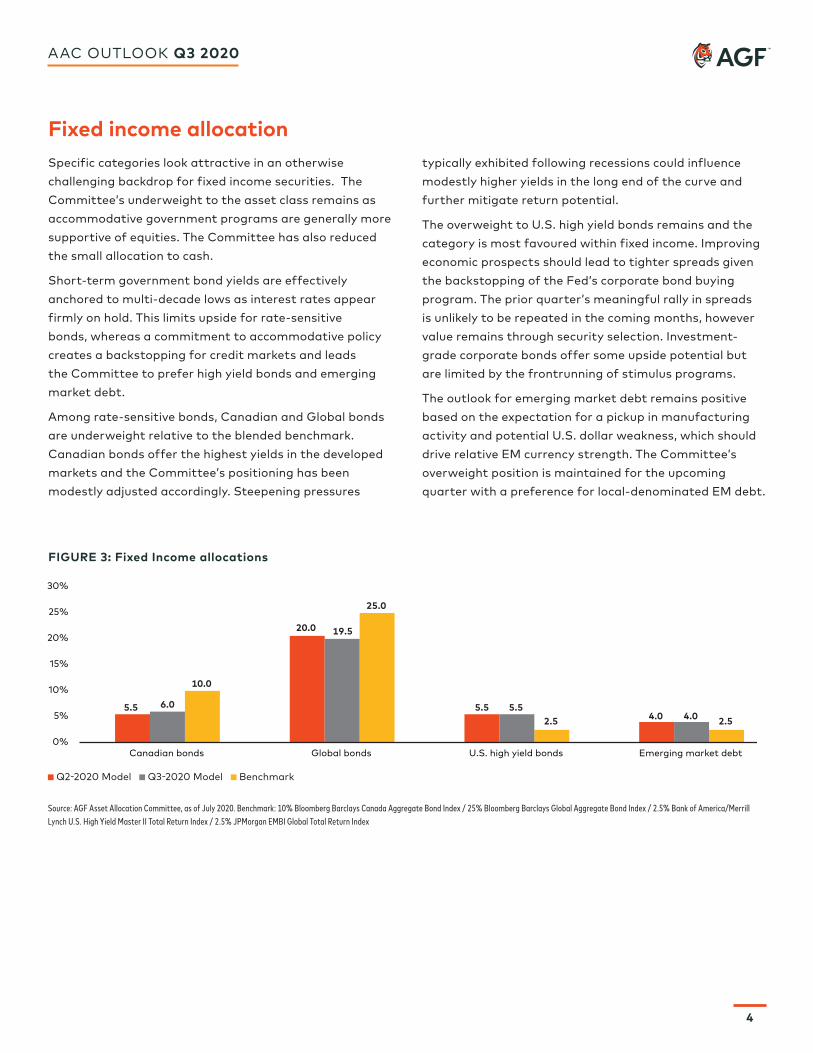

Fixed income allocationSpecific categories look attractive in an otherwise

challenging backdrop for fixed income securities. The

Committee’s underweight to the asset class remains as

accommodative government programs are generally more

supportive of equities. The Committee has also reduced

the small allocation to cash.

Short-term government bond yields are effectively

anchored to multi-decade lows as interest rates appear

firmly on hold. This limits upside for rate-sensitive

bonds, whereas a commitment to accommodative policy

creates a backstopping for credit markets and leads

the Committee to prefer high yield bonds and emerging

market debt.

Among rate-sensitive bonds, Canadian and Global bonds

are underweight relative to the blended benchmark.

Canadian bonds offer the highest yields in the developed

markets and the Committee’s positioning has been

modestly adjusted accordingly. Steepening pressures

typically exhibited following recessions could influence

modestly higher yields in the long end of the curve and

further mitigate return potential.

The overweight to U.S. high yield bonds remains and the

category is most favoured within fixed income. Improving

economic prospects should lead to tighter spreads given

the backstopping of the Fed’s corporate bond buying

program. The prior quarter’s meaningful rally in spreads

is unlikely to be repeated in the coming months, however

value remains through security selection. Investment-

grade corporate bonds offer some upside potential but

are limited by the frontrunning of stimulus programs.

The outlook for emerging market debt remains positive

based on the expectation for a pickup in manufacturing

activity and potential U.S. dollar weakness, which should

drive relative EM currency strength. The Committee’s

overweight position is maintained for the upcoming

quarter with a preference for local-denominated EM debt.

6.0

10.0

5.5

19.5

25.0

20.0

5.52.5

5.54.0 2.54.0

0%

5%

10%

15%

20%

25%

30%

Emerging market debtU.S. high yield bondsGlobal bondsCanadian bonds

FIGURE 3: Fixed Income allocations

Q2-2020 Model Q3-2020 Model Benchmark

Source: AGF Asset Allocation Committee, as of July 2020. Benchmark: 10% Bloomberg Barclays Canada Aggregate Bond Index / 25% Bloomberg Barclays Global Aggregate Bond Index / 2.5% Bank of America/Merrill Lynch U.S. High Yield Master II Total Return Index / 2.5% JPMorgan EMBI Global Total Return Index

AAC OUTLOOK Q3 2020

AAC OUTLOOK Q3 2020

5

Q2-2020 economic recap

Global financial markets recovered strongly in the

second quarter of 2020 with the backing of monetary

and fiscal policy as well as advancement in the fight

against COVID-19. The spread of cases slowed in select

major economies which allowed for partial resumption of

manufacturing and other business activity, while hopes

of progress towards a vaccine led to improved consumer

confidence. Elevated levels of volatility carried into the

second quarter, however, as a global response to racial

injustices and an uptick of COVID-19 cases in the U.S.

contributed to investor angst.

The U.S. Federal Reserve (Fed) led major central banks in

efforts to support the global economy by inflating their

balance sheet to over US$7 trillion, while policymakers in

Congress enacted the US$2 trillion CARES act. Lagged

effects of the shutdown were rampant in reported

economic data during the quarter as the U.S. lost over 20

million jobs in April and the unemployment rate reached a

post-war high of 14.7% before partially improving towards

the end of the quarter. After falling to decade-lows of 41.5

in April, the ISM Manufacturing PMI returned to modest

expansionary levels of 52.6 in June.

The Bank of Canada expanded its newly introduced

quantitative easing program with up to $50 billion of

provincial bonds and up to $10 billion of investment

grade corporate bonds in addition to weekly government

bond buying already in place. The gradual reopening

of manufacturing and vehicle mobility led to increased

Energy demand and thus higher crude oil prices, though

at around $40 by the mid-year point, held well below

levels entering 2020. The path of Canada’s labour market

resembled that of the U.S., with historic losses to begin

the quarter followed by remarkable gains announced for

May, yet with only a fraction of losses recouped, risk of

permanent job losses continued to grow.

Eurozone manufacturing rebounded close to pre-virus

levels in June though remained in contraction territory

for the 17th straight month to end the quarter. The

European Central Bank maintained its €1.1 trillion easing

programme which supported a strong equity rebound. The

recovery was also helped by the quelling of virus cases in

Italy and Spain, two of Europe’s hardest hit countries.

Japan’s stable political backdrop and social cohesion in

general continued in the second quarter, though ongoing

deflation challenges were exacerbated by the COVID-19

pandemic.

U.S. dollar strength weighed negatively on emerging

markets in general, as did elevated case counts in

Brazil and India. However, partial reopening of China’s

economy supported market growth as the China Caixin

Manufacturing PMI returned to expansionary territory

during the quarter.

AAC OUTLOOK Q3 2020

™ The ‘AGF’ logo and ‘Invested in Discipline’ are trademarks of AGF Management Limited and used under licence. The commentaries contained herein are provided as a general source of information based on information available as of June 30, 2020 and should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities. Every effort has been made to ensure accuracy in these commentaries at the time of publication, however accuracy cannot be guaranteed. Market conditions may change and the manager accepts no responsibility for individual investment decision arising from the use or reliance on the information contained herein. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed; their values change frequently and past performance may not be repeated. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com). AGF Investments is a group of wholly owned subsidiaries of AGF Management Limited, a Canadian reporting issuer. The subsidiaries included in AGF Investments are AGF Investments Inc. (AGFI), Highstreet Asset Management Inc. (Highstreet), AGF Investments America Inc. (AGFA), AGF Asset Management (Asia) Limited (AGF AM Asia) and AGF International Advisors Company Limited (AGFIA). AGFA is a registered advisor in the U.S. AGFI and Highstreet are registered as portfolio managers across Canadian securities commissions. AGFIA is regulated by the Central Bank of Ireland and registered with the Australian Securities & Investments Commission. AGF AM Asia is registered as a portfolio manager in Singapore. The subsidiaries that form AGF Investments manage a variety of mandates comprised of equity, fixed income and balanced assets. Publication date: July 20, 2020

For more information on the AGF Asset Allocation Committee visit AGF.com.

FU

ND

98

6 0

7-20

-E

AGF Asset Allocation Committee The AGF Asset Allocation Committee is comprised of experienced investment professionals, specializing in various areas

of the global bond and equity markets. Members provide insight into risks and opportunities, shaping the outlook of their

respective asset class, which leads to an optimized asset allocation view. This top-down view guides the allocations for all

funds managed by the Committee.