PwC Debt and Capital Advisory · 8 | 2016 Debt Market outlook and topical insights | PwC UK...

14

PwC Debt and Capital Advisory www.pwc.co.uk March 2016

Transcript of PwC Debt and Capital Advisory · 8 | 2016 Debt Market outlook and topical insights | PwC UK...

PwC Debt and Capital Advisory

www.pwc.co.uk

March 2016

2 | 2016 Debt Market outlook and topical insights | PwC

Welcome to PwC Debt & Capital Advisory’s update for March 2016.

Over the past 12 months our Debt & Capital Advisory practice has helped our clients raise over £1.5bn of debt, across the wide range of sources available from European debt markets, including High Yield bonds, Unitranche funds and Asset Backed Lending.

Our clients have included listed PLCs, private equity portfolio companies and privately-owned companies, both in the UK and abroad, helping them with financing requirements ranging from urgent acquisition funding through to a plentiful supply of recapitalisations for both privately-owned and private equity portfolio companies.

Later in this update we provide detailed analysis of the latest trends in European debt markets, split across the various markets that we cover. Over the last 12 months, across global debt markets we have seen increased bifurcation between ‘big ticket’ markets and the UK/European mid-market. Generally, the big ticket debt market is more susceptible to global macro-economic sentiment and, whilst you would expect a ‘trickle-down’ impact, the mid-market has generally held up well, bolstered by continuing levels of new liquidity from the prevalence of credit funds.

The final quarter of 2015 saw some volatility across sub-investment grade loan and bond markets and this uncertainty has extended into the first few months of 2016 with only very limited High Yield issuance to date. Institutional loan markets, used to fund the larger corporate and private equity deals, have also been more cautious with investors requiring higher yield and showing reduced documentation flexibility, making deals harder to deliver until the new market realities are accepted by borrowers. Differences have also been evident between US and European markets with the latter remaining relatively less sensitive than the US to global concerns around commodities and emerging markets.

During 2015, the UK/European mid-market was buoyant with strong demand for debt financing fuelled by CFO’s growing confidence in debt market deliverability overlaying generally positive sentiment in the UK. However, in the early weeks of 2016 there have been a few signs of widening pricing and tightening of covenant packages in the mid-market, so it is worth watching this space closely. The bias away from traditional bank lenders will continue with the now mature credit fund market providing an increasing number of options across the credit spectrum – to date credit funds have had to maintain a material pricing differentiation from the traditional bank market but this has reduced over time and we expect to see credit funds close this pricing gap further. The range of options available to the mid-market borrower will therefore continue to grow.

Furthermore, whilst the UK economy has recently fared better that most of its European counterparts, the European referendum now provides us with an extended period of potential uncertainty and it will be interesting to see how business and consumer confidence lasts through to the summer.

Against this regularly changing backdrop, PwC Debt & Capital Advisory has an experienced and well-resourced team that is available to help our clients assess, structure and execute the optimal financing package. If you would like to discuss your present or expected debt requirements, please see our contact details at the back of this update.

What’s happening in the Debt Markets?

PwC | 2016 Debt Market outlook and topical insights | 3

Using debt to enhance shareholder returns

In an environment where economic stability in the UK (EU Referendum permitting) is giving shareholders and businesses more confidence for the future, more are looking at ways of providing shareholders and/or management with ways to realise or enhance shareholder returns in what is, still, a relatively low growth climate.

The private equity-owned world regularly uses debt-funded recapitalisations to enhance and underpin equity returns and we have seen this trend extending to privately-owned businesses too. In the right circumstances, increased bank or credit fund financing can provide additional leverage to enable value to be realised; furthermore, the expanding credit fund market now provides ample appetite to fund transactions for privately-owned companies. In many circumstances, a blended bank/credit fund approach, or Unitranche, can serve both the core working capital debt requirements and fund a strip of more permanent capital.

For private company shareholders the regularly changing tax regulations mean choosing the right time to draw a dividend has become increasingly important and, with the Chancellor continually revising the tax system, many shareholders are regularly reviewing their options for realising value through either dividends or a return of capital.

In the public company arena, debt leverage has, generally, been very constrained since the financial crisis, driven by a combination of banks, shareholders and analysts all conspiring to historically low levels of leverage and gearing. This, overlaid with the low growth economy, has often resulted in a regression in shareholder returns from public equity markets, both from more cautious dividend strategies and lower overall capital growth.

One potential way to increase shareholder returns in the listed arena is to use debt to fund a share buyback programme; where current leverage allows, such an approach would enable companies to both return capital to selling shareholders and enhance Earnings Per Share for remaining investors. We think the jury is currently out amongst public company shareholders as to whether or not a debt-funded share repurchase programme is an appropriate strategy but, clearly, this will depend, in part, on whether one is a selling or longer-term investor, and their views on future growth in the particular company. On the assumption that investors buy into the concept of a share buyback, then we see appetite and capability within the banking arena to provide funding for such a programme. Adopting a debt funded approach may also benefit a company’s tax bill although the forthcoming interest deductibility changes will need to be considered carefully in any finance raising transaction.

PwC | 2016 Debt Market outlook and topical insights | 3

4 | 2016 Debt Market outlook and topical insights | PwC

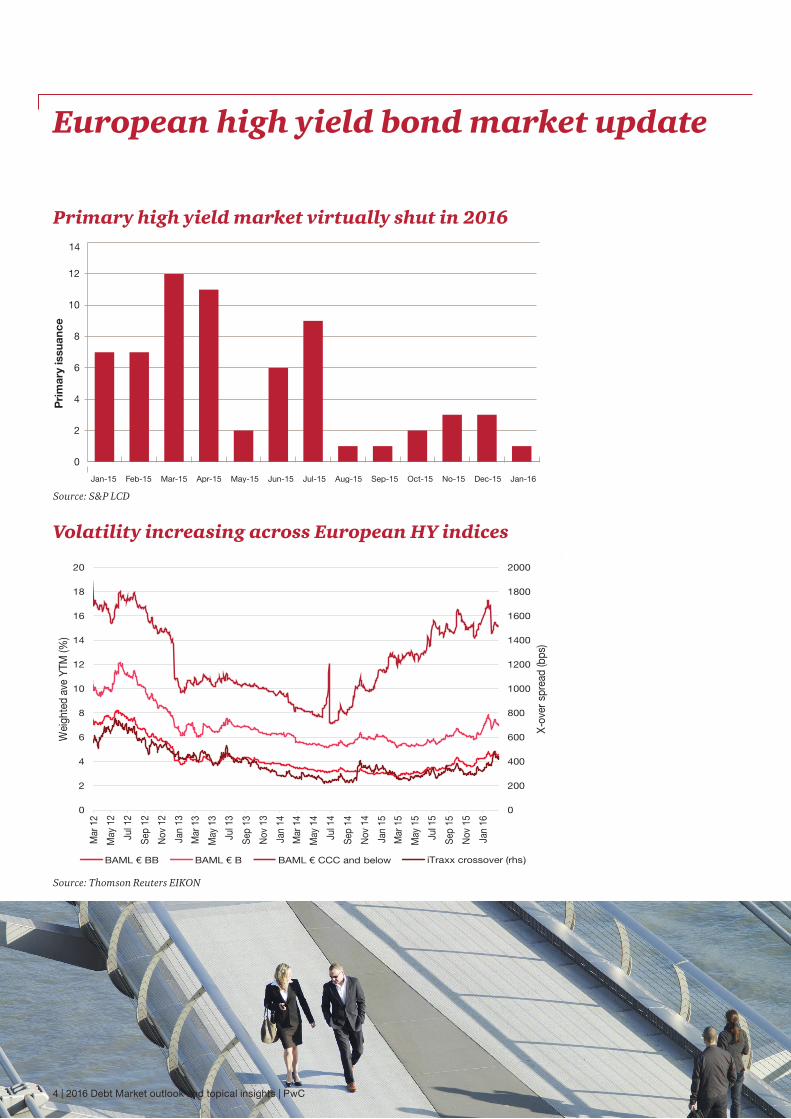

European high yield bond market update

Primary high yield market virtually shut in 2016

Source: S&P LCD

Volatility increasing across European HY indices

Source: Thomson Reuters EIKON

* The crossover index measures the CDS spread on an index of European high yield issuers

BAML €BB BAML €B BAML €CCC and below iTRAXX crossover (rhs)

0

2

4

6

8

10

12

14

Jan-15 Feb-15 Mar-15

Pri

mar

y is

suan

ce

Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 No-15 Dec-15 Jan-16

0

200

400

600

800

1000

1200

1400

1600

1800

2000

0

2

4

6

8

10

12

14

16

18

20

Mar

12

May

12

Jul 1

2

Sep

12

Nov

12

Jan

13

Mar

13

May

13

Jul 1

3

Sep

13

Nov

13

Jan

14

Mar

14

May

14

Jul 1

4

Sep

14

Nov

14

Jan

15

Mar

15

May

15

Jul 1

5

Sep

15

Nov

15

Jan

16

X-ov

er s

prea

d (b

ps)

Wei

ghte

d av

e YT

M (%

)

BAML € BB BAML € B BAML € CCC and below iTraxx crossover (rhs)

4 | 2016 Debt Market outlook and topical insights | PwC

PwC | 2016 Debt Market outlook and topical insights | 5

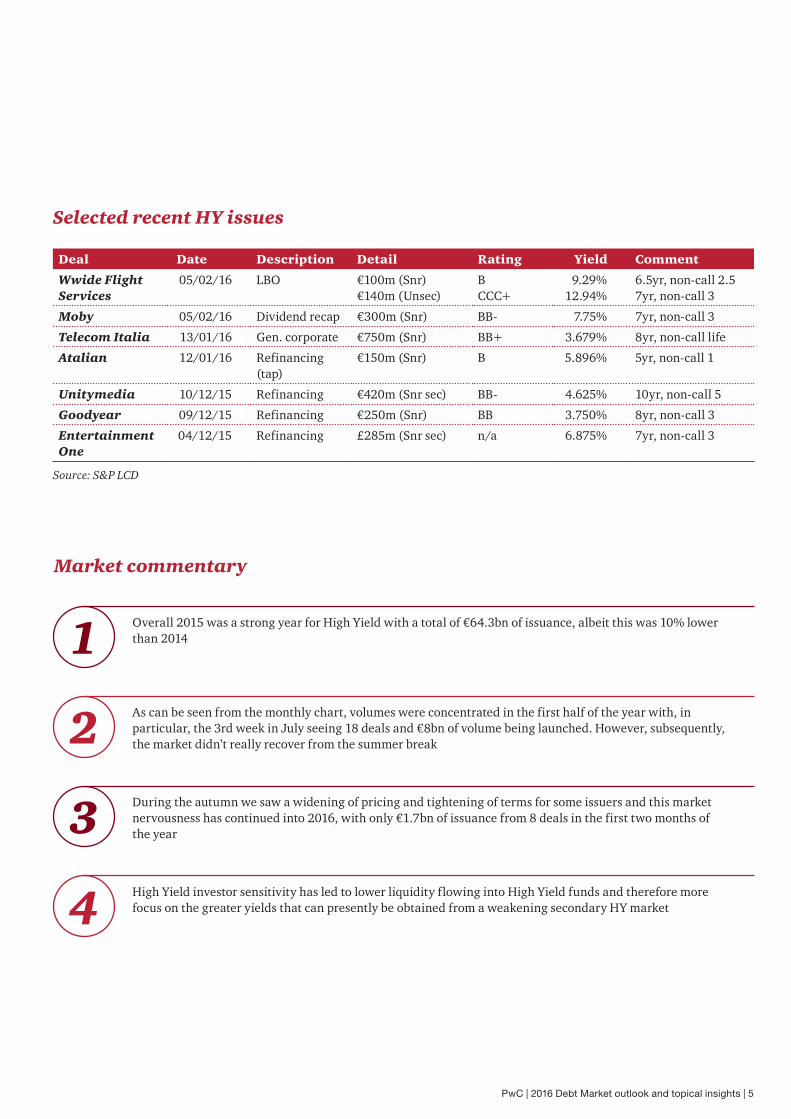

Selected recent HY issues

Market commentary

Deal Date Description Detail Rating Yield Comment

Wwide Flight Services

05/02/16 LBO €100m (Snr) €140m (Unsec)

B CCC+

9.29% 12.94%

6.5yr, non-call 2.5 7yr, non-call 3

Moby 05/02/16 Dividend recap €300m (Snr) BB- 7.75% 7yr, non-call 3

Telecom Italia 13/01/16 Gen. corporate €750m (Snr) BB+ 3.679% 8yr, non-call life

Atalian 12/01/16 Refinancing (tap)

€150m (Snr) B 5.896% 5yr, non-call 1

Unitymedia 10/12/15 Refinancing €420m (Snr sec) BB- 4.625% 10yr, non-call 5

Goodyear 09/12/15 Refinancing €250m (Snr) BB 3.750% 8yr, non-call 3

Entertainment One

04/12/15 Refinancing £285m (Snr sec) n/a 6.875% 7yr, non-call 3

Source: S&P LCD

1 Overall 2015 was a strong year for High Yield with a total of €64.3bn of issuance, albeit this was 10% lower than 2014

2 As can be seen from the monthly chart, volumes were concentrated in the first half of the year with, in particular, the 3rd week in July seeing 18 deals and €8bn of volume being launched. However, subsequently, the market didn’t really recover from the summer break

3 During the autumn we saw a widening of pricing and tightening of terms for some issuers and this market nervousness has continued into 2016, with only €1.7bn of issuance from 8 deals in the first two months of the year

4 High Yield investor sensitivity has led to lower liquidity flowing into High Yield funds and therefore more focus on the greater yields that can presently be obtained from a weakening secondary HY market

6 | 2016 Debt Market outlook and topical insights | PwC

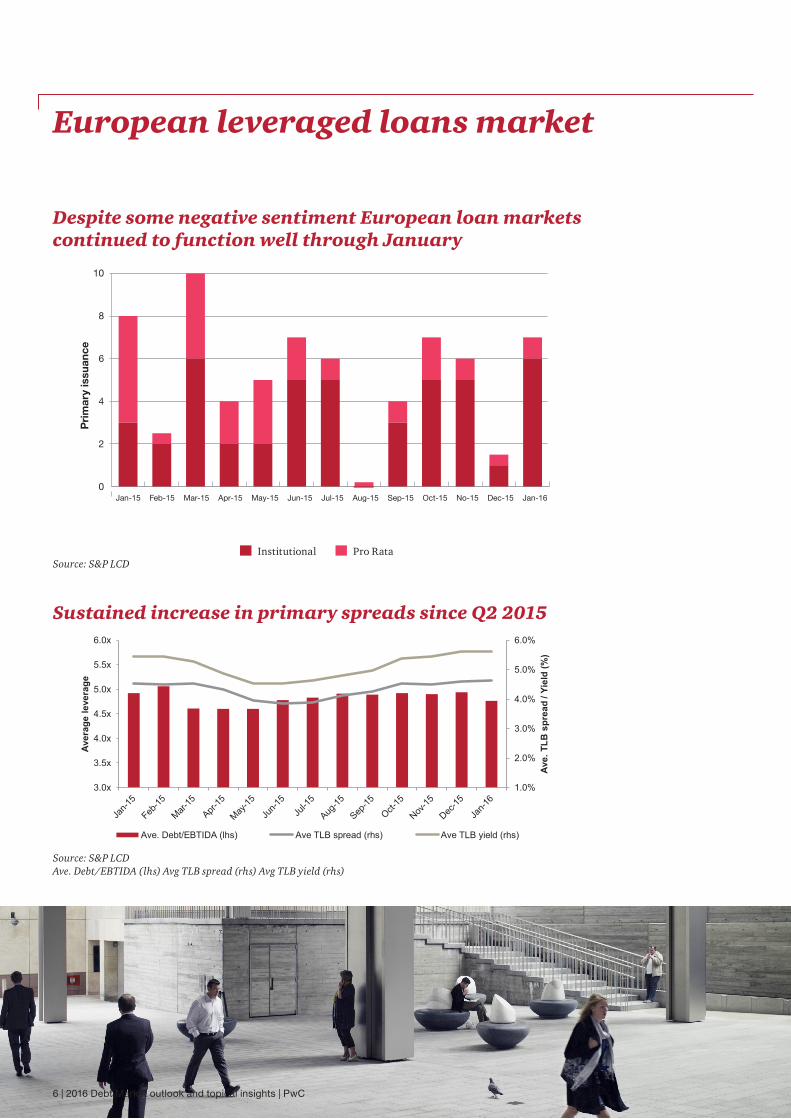

European leveraged loans market

Sustained increase in primary spreads since Q2 2015

Despite some negative sentiment European loan markets continued to function well through January

0

2

4

6

8

10

Jan-15 Feb-15 Mar-15

Pri

mar

y is

suan

ce

Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 No-15 Dec-15 Jan-16

Institutional Pro Rata

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

3.0x

3.5x

4.0x

4.5x

5.0x

5.5x

6.0x

Ave.

TLB

spr

ead

/ Yie

ld (%

)

Aver

age

leve

rage

Ave. Debt/EBTIDA (lhs) Ave TLB spread (rhs) Ave TLB yield (rhs)

Source: S&P LCDAve. Debt/EBTIDA (lhs) Avg TLB spread (rhs) Avg TLB yield (rhs)

Source: S&P LCD

6 | 2016 Debt Market outlook and topical insights | PwC

PwC | 2016 Debt Market outlook and topical insights | 7

1 Difficult conditions in the primary market mean that issuers have had to ‘pay up’ to get deals away in the last few months, although up until February the European loan market had remained somewhat insulated from both the US Oil & Gas and commodities fallout that has hit the US and High Yield markets

2 Macro concerns led to pricing widening with the average TLB clearing yield for February 2016 at 6.18% vs 90 day average of 4.5% at the end of Q2 2015

3 2016 YTD saw €10.0bn of issuance fuelled by a good pipeline of deals left over from 2015 successfully launched and cleared through syndication markets in January (€8.3bn) and February. However, a number of transactions were forced to widen pricing in January and February to clear syndication

4 There remains significant institutional capacity in the market, however current conditions for new CLO insurance remain challenging

Market commentary

8 | 2016 Debt Market outlook and topical insights | PwC

UK sponsored mid-market lending update

UK mid-market tracker

0

200

400

600

800

1,000

1,200

1,400

1,600

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

5.0x

UK

Mid

-mar

ket v

olu

me

(£m

)

3m. t

rail

ing

leve

rage

Source: Various, PwC analysis (tracking deals up to £300m debt funding in the sponsored market)

Deal volume 3M trailing average leverage

Dec-14

Jan-15

Feb-15

Mar-1

5

Apr-15

May-15

Jun-15

Jul-1

5

Aug-15

Sep-15

Oct-15

Nov-15

Dec-15

UK mid-market trends

1

2

3

December capped a busy year for the UK mid-market, a combination of competition between sponsors and highly liquid funding market conditions has driven valuations steadily upwards.

Average leverage levels remain around 4.5x, supported by the amount of capital that funds are looking to deploy, whilst pricing remains under pressure (particularly as banks seek to compete with funds).

As alternative lenders raise new and larger funds, they are increasingly able to fund and underwrite bigger deals (recent examples include the £150m refinancing of Universal Utilities and €250m buyout of Fintrax, both provided by Ares). The upper end of these deals would take market share away from the bank club/institutional markets where the ability of one lender to underwrite the capital structure could be a key competitive advantage for sponsors.

PwC | 2016 Debt Market outlook and topical insights | 9

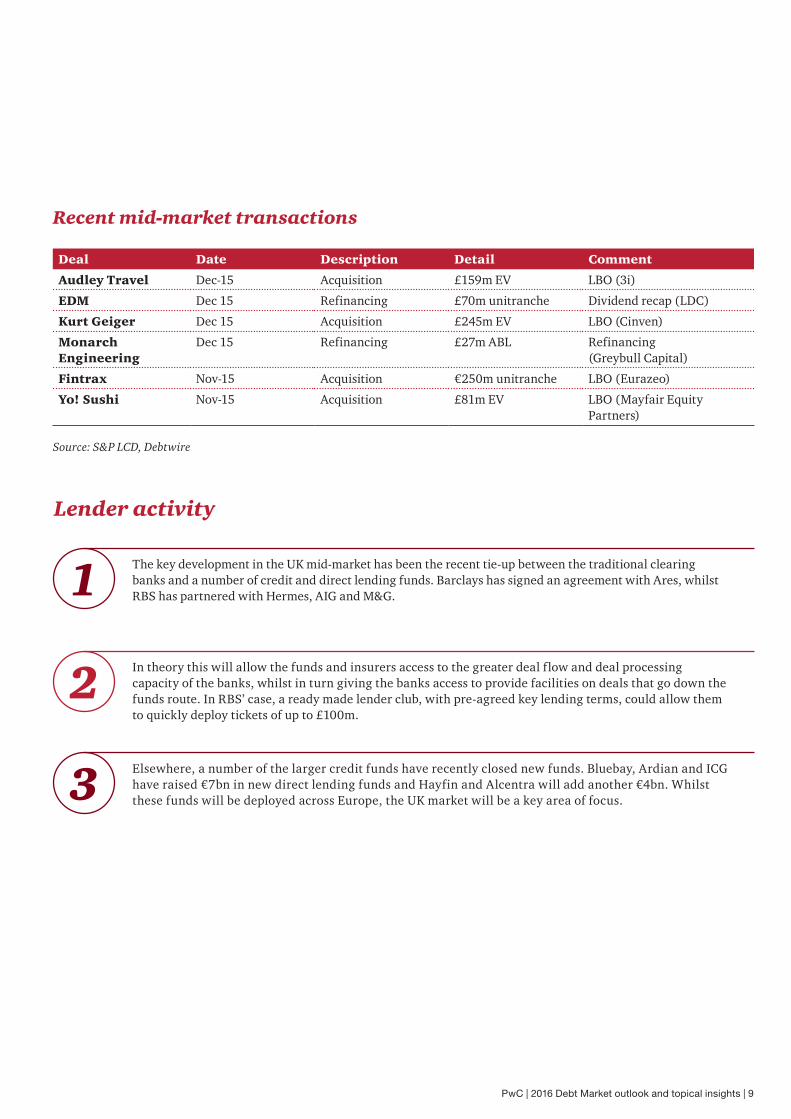

Recent mid-market transactions

Source: S&P LCD, Debtwire

Deal Date Description Detail Comment

Audley Travel Dec-15 Acquisition £159m EV LBO (3i)

EDM Dec 15 Refinancing £70m unitranche Dividend recap (LDC)

Kurt Geiger Dec 15 Acquisition £245m EV LBO (Cinven)

Monarch Engineering

Dec 15 Refinancing £27m ABL Refinancing (Greybull Capital)

Fintrax Nov-15 Acquisition €250m unitranche LBO (Eurazeo)

Yo! Sushi Nov-15 Acquisition £81m EV LBO (Mayfair Equity Partners)

Lender activity

1

2

3

The key development in the UK mid-market has been the recent tie-up between the traditional clearing banks and a number of credit and direct lending funds. Barclays has signed an agreement with Ares, whilst RBS has partnered with Hermes, AIG and M&G.

In theory this will allow the funds and insurers access to the greater deal flow and deal processing capacity of the banks, whilst in turn giving the banks access to provide facilities on deals that go down the funds route. In RBS’ case, a ready made lender club, with pre-agreed key lending terms, could allow them to quickly deploy tickets of up to £100m.

Elsewhere, a number of the larger credit funds have recently closed new funds. Bluebay, Ardian and ICG have raised €7bn in new direct lending funds and Hayfin and Alcentra will add another €4bn. Whilst these funds will be deployed across Europe, the UK market will be a key area of focus.

10 | 2016 Debt Market outlook and topical insights | PwC

Credentials

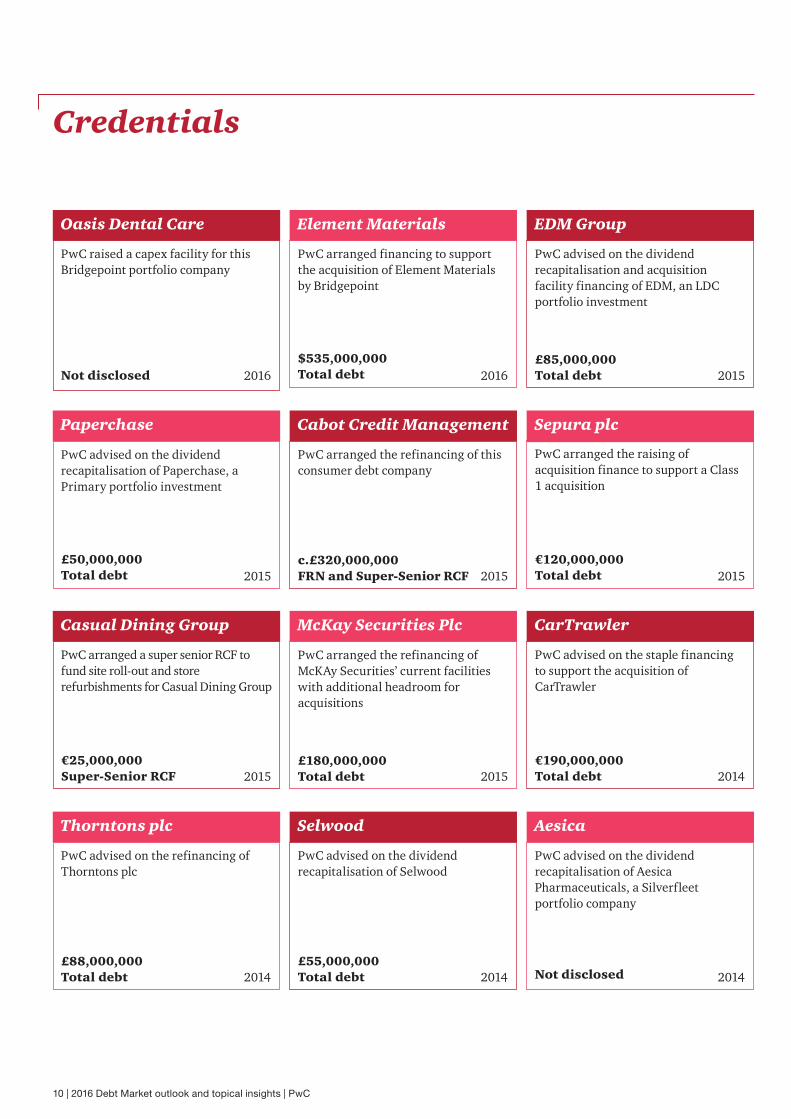

EDM Group

PwC advised on the dividend recapitalisation and acquisition facility financing of EDM, an LDC portfolio investment

£85,000,000 Total debt 2015

Cabot Credit Management

PwC arranged the refinancing of this consumer debt company

c.£320,000,000 FRN and Super-Senior RCF 2015

McKay Securities Plc

PwC arranged the refinancing of McKAy Securities’ current facilities with additional headroom for acquisitions

£180,000,000 Total debt 2015

Element Materials

PwC arranged financing to support the acquisition of Element Materials by Bridgepoint

$535,000,000 Total debt 2016

Thorntons plc

PwC advised on the refinancing of Thorntons plc

£88,000,000 Total debt 2014

CarTrawler

PwC advised on the staple financing to support the acquisition of CarTrawler

€190,000,000 Total debt 2014

Selwood

PwC advised on the dividend recapitalisation of Selwood

£55,000,000 Total debt 2014

Aesica

PwC advised on the dividend recapitalisation of Aesica Pharmaceuticals, a Silverfleet portfolio company

Not disclosed 2014

Oasis Dental Care

PwC raised a capex facility for this Bridgepoint portfolio company

Not disclosed 2016

Sepura plc

PwC arranged the raising of acquisition finance to support a Class 1 acquisition

€120,000,000 Total debt 2015

Paperchase

PwC advised on the dividend recapitalisation of Paperchase, a Primary portfolio investment

£50,000,000 Total debt 2015

Casual Dining Group

PwC arranged a super senior RCF to fund site roll-out and store refurbishments for Casual Dining Group

€25,000,000 Super-Senior RCF 2015

PwC | 2016 Debt Market outlook and topical insights | 11

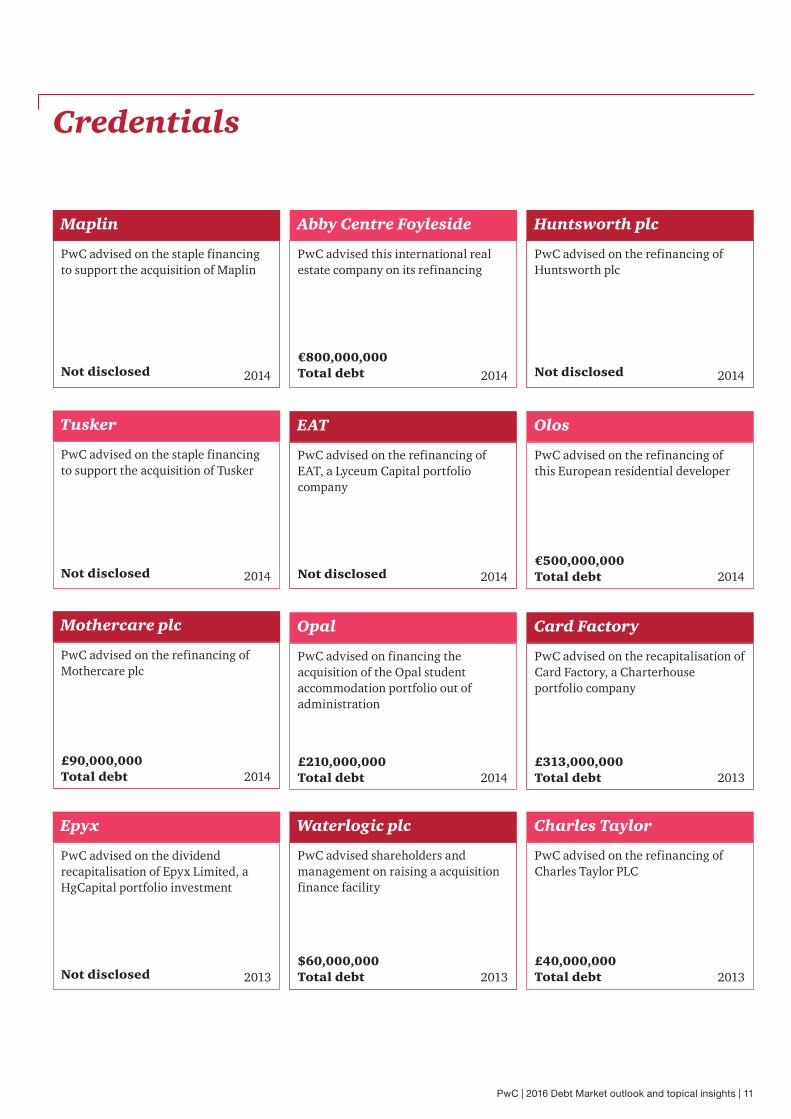

Maplin

PwC advised on the staple financing to support the acquisition of Maplin

Not disclosed 2014

Credentials

Abby Centre Foyleside

PwC advised this international real estate company on its refinancing

€800,000,000 Total debt 2014

Huntsworth plc

PwC advised on the refinancing of Huntsworth plc

Not disclosed 2014

Tusker

PwC advised on the staple financing to support the acquisition of Tusker

Not disclosed 2014

EAT

PwC advised on the refinancing of EAT, a Lyceum Capital portfolio company

Not disclosed 2014

Olos

PwC advised on the refinancing of this European residential developer

€500,000,000 Total debt 2014

Mothercare plc

PwC advised on the refinancing of Mothercare plc

£90,000,000 Total debt 2014

Opal

PwC advised on financing the acquisition of the Opal student accommodation portfolio out of administration

£210,000,000 Total debt 2014

Card Factory

PwC advised on the recapitalisation of Card Factory, a Charterhouse portfolio company

£313,000,000 Total debt 2013

Epyx

PwC advised on the dividend recapitalisation of Epyx Limited, a HgCapital portfolio investment

Not disclosed 2013

Waterlogic plc

PwC advised shareholders and management on raising a acquisition finance facility

$60,000,000 Total debt 2013

Charles Taylor

PwC advised on the refinancing of Charles Taylor PLC

£40,000,000 Total debt 2013

12 | 2016 Debt Market outlook and topical insights | PwC

Debt & Capital Advisory contacts

David GodbeePartner

M: +44 (0)7740 242013 T: + 44 (0)20 7213 4101 E: [email protected]

Sandra Kylassam-PillayDirector

M: +44 (0)7734 958510 T: + 44 (0)20 7213 4699 E: [email protected]

Paul AmbroseDirector

M: +44 (0)7841 569538 T: + 44 (0)20 7804 0737 E: [email protected]

Nicholas SternManager

M: +44 (0)7803 456041 T: + 44 (0)20 7804 5807 E: [email protected]

• Looking to make a strategic acquisition?

• Considering how to fund organic expansion (i.e. increased working capital, asset purchase etc.)?

• Refinancing current debt that is due to expire within 12-24 months?

• Thinking about how to fund a special dividend, shareholder loan repayment or share re-purchase programme?

Areas we can help you

• Strategic advice on all financing needs, including debt structuring and raising debt/equity

• Access to liquidity, through our relationships with over 200 banks and non-bank lenders

• Hands on support throughout your finance raising process, including running funding competition and managing negotiations with lenders

We are positioned to provide...

PwC’s Debt & Capital Advisory team provides both strategic advice and execution support to clients who are looking to raise or rearrange their debt capital structure.

The team has many years of financing experience across corporate, leveraged and investment banking, and would be delighted to discuss any of the topics mentioned in this newsletter or if any of the areas below resonate with you.

PwC | 2016 Debt Market outlook and topical insights | 13

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2016 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to the UK member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

160222-173611-SD-OS