Putting America’s Waterways to Work -...

53

Putting America’s Waterways to Work NYSE: KEX March 2018

Transcript of Putting America’s Waterways to Work -...

Putting America’s Waterways to Work NYSE: KEX

March 2018

Statements contained in this presentation with respect to the future are forward-looking

statements. These statements reflect management’s reasonable judgment with respect to

future events. Forward-looking statements involve risks and uncertainties. Actual results

could differ materially from those anticipated as a result of various factors, including cyclical

or other downturns in demand, significant pricing competition, unanticipated additions to

industry capacity, changes in the Jones Act or in U.S. maritime policy and practice, fuel

costs, interest rates, weather conditions and the timing, magnitude and the number of

acquisitions made by Kirby. Forward-looking statements are based on currently available

information and Kirby assumes no obligation to update such statements. A list of additional

risk factors can be found in Kirby’s annual report on Form 10-K for the year ended December

31, 2017.

Kirby reports its financial results in accordance with generally accepted accounting

principles (GAAP). However, Kirby believes that a certain Non-GAAP financial measure is

useful in managing Kirby’s businesses and evaluating Kirby’s performance. This

presentation contains a Non-GAAP financial measure, EBITDA. Please see the Appendix for

a reconciliation of GAAP to the Non-GAAP financial measure, EBITDA.

2

Forward Looking Statements

Non-GAAP Financial Measures

3

Business Segments

Marine Transportation

The largest inland and coastwise tank barge fleets in the United States

60% of 2017 Revenue

Distribution and Services

Nationwide service provider and distributor of engines, transmissions, parts, industrial equipment and oilfield service equipment

40% of 2017 Revenue

Public Market Information

4

NYSE: KEX

Share Price on February 26, 2018 $76.85

Shares Outstanding (as of February 26, 2018)

59.7MM

Market Capitalization $4,586MM

Net Debt $1,408MM

Enterprise Value $5,994MM

Company Overview

5

• Largest combined inland and coastal tank barge operator

– 998 inland tank barges and 302 towboats*

– 56 coastal tank barges and 53 tugboats*

– 75% of inland revenues under term contracts, of which approximately 51% are under time charters

– 80% of coastal revenues under term contracts, of which approximately 85% are under time charters

• Nationwide distributor and service provider for engines, transmissions, reduction gears, and related equipment used in oilfield services, marine, power generation, on-highway, and other industrial applications

• Manufacturer, remanufacturer and service provider of oilfield service equipment

• Provider of rental equipment including generators, material-handling equipment, pumps, and compressors for use in a variety of industrial markets

Successful integration of 34 marine and 19 distribution and services acquisitions

Marine Transportation

Distribution and Services

Return on Capital Driven Investment Decisions

Proven Acquisition Strategy

* As of February 26, 2018

6

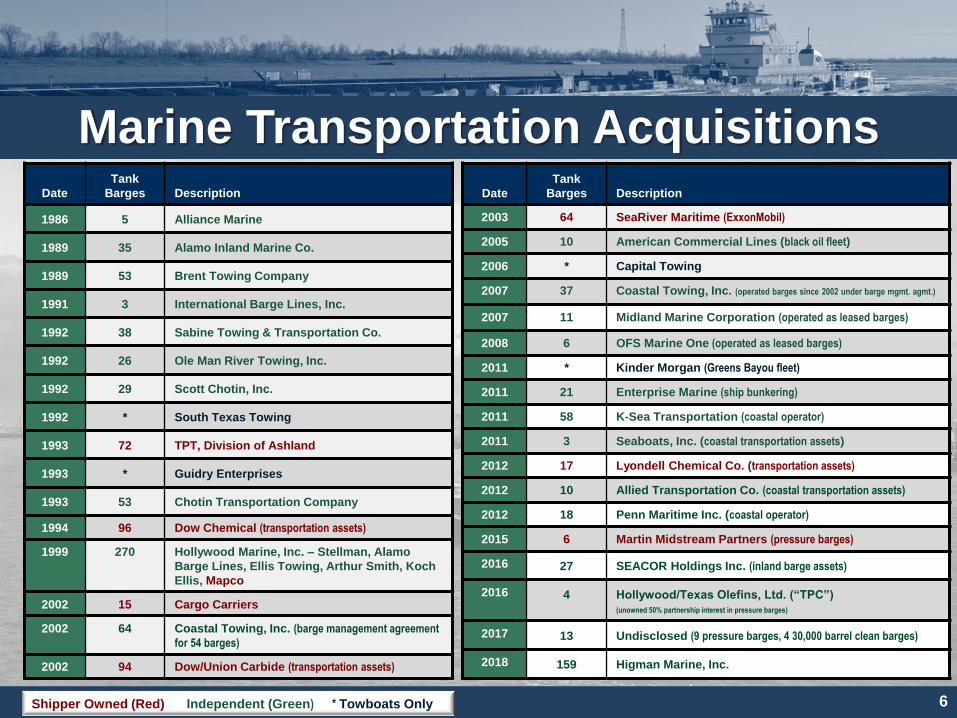

Date

Tank

Barges Description

2003 64 SeaRiver Maritime (ExxonMobil)

2005 10 American Commercial Lines (black oil fleet)

2006 * Capital Towing

2007 37 Coastal Towing, Inc. (operated barges since 2002 under barge mgmt. agmt.)

2007 11 Midland Marine Corporation (operated as leased barges)

2008 6 OFS Marine One (operated as leased barges)

2011 * Kinder Morgan (Greens Bayou fleet)

2011 21 Enterprise Marine (ship bunkering)

2011 58 K-Sea Transportation (coastal operator)

2011 3 Seaboats, Inc. (coastal transportation assets)

2012 17 Lyondell Chemical Co. (transportation assets)

2012 10 Allied Transportation Co. (coastal transportation assets)

2012 18 Penn Maritime Inc. (coastal operator)

2015 6 Martin Midstream Partners (pressure barges)

2016 27 SEACOR Holdings Inc. (inland barge assets)

2016 4 Hollywood/Texas Olefins, Ltd. (“TPC”)

(unowned 50% partnership interest in pressure barges)

2017 13 Undisclosed (9 pressure barges, 4 30,000 barrel clean barges)

2018 159 Higman Marine, Inc.

Shipper Owned (Red) Independent (Green) * Towboats Only

Date

Tank

Barges

Description

1986 5 Alliance Marine

1989 35 Alamo Inland Marine Co.

1989 53 Brent Towing Company

1991 3 International Barge Lines, Inc.

1992 38 Sabine Towing & Transportation Co.

1992 26 Ole Man River Towing, Inc.

1992 29 Scott Chotin, Inc.

1992 * South Texas Towing

1993 72 TPT, Division of Ashland

1993 * Guidry Enterprises

1993 53 Chotin Transportation Company

1994 96 Dow Chemical (transportation assets)

1999 270 Hollywood Marine, Inc. – Stellman, Alamo

Barge Lines, Ellis Towing, Arthur Smith, Koch

Ellis, Mapco

2002 15 Cargo Carriers

2002 64 Coastal Towing, Inc. (barge management agreement

for 54 barges)

2002 94 Dow/Union Carbide (transportation assets)

Marine Transportation Acquisitions

Distribution and Services Expansions

7

Acquisitions

1987 National Marine

1991 Ewing Diesel

1995 Percle Enterprises

1996 MKW Power Systems

1997 Crowley (Power Assembly Shop)

2000 West Kentucky Machine Shop

2000 Powerway

2004 Walker Paducah Corp.

2005 TECO (Diesel Services Division)

2006 Global Power Holding Company

2006 Marine Engine Specialists

2007 NAK Engineering (Nordberg Engines)

2007 P&S Diesel Service

2007 Saunders Engine & Equipment Company

2008 Lake Charles Diesel, Inc.

2011 United Holdings LLC

2012 Flag Services & Maintenance, Inc.

2016 Valley Power Systems, Inc.

2017 Stewart & Stevenson LLC

Internal Growth

1989 Midwest

1992 Seattle

2000 Cooper Nuclear

Historical Revenue Growth

8

$327 $366$513 $567 $535

$613$675

$796

$984

$1,173

$1,360

$1,082

$1,110

$1,850 $2,113

$2,242

$2,566

$2,148

$1,771

$2,214

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

In M

illi

on

s

Marine Transportation and Distribution and Services Revenue From Continuing Operations

10.6% compound

annual growth

1998-2017

$0.52 $0.63 $0.82 $0.94 $0.82 $0.83

$0.98

$1.33

$1.79

$2.29

$2.91

$2.34 $2.15

$3.35

$3.73

$4.44

$4.93

$4.11

$2.62

$1.99

$3.00

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

1

9

Historical EPS Growth

Earnings per share have been revised to reflect 2-for-1 stock split effective May 31, 2006

Earnings Per Share From Continuing Operations Excluding Non-Recurring Items

7.3% compound

annual growth

1998 - 2017

$2.50

2

2

(2) Based on Kirby's most recently published earnings guidance in the January 31, 2018 press release announcing Q4 2017 earnings. That guidance is shown for convenience only and does not constitute confirming or updating

the guidance, which will only be done by public disclosure.

(1) 2017 earnings per share exclude a one-time deferred tax revaluation benefit of $4.83 per share, and non-recurring after-tax charges including impairments of marine vessels of $1.20 per share.

Higman Marine Acquisition Overview

10

• $419 million in total consideration

• 6.5x – 7.5x multiple of 5-yr prior EBITDA average with synergies

Purchase Price

• EPS neutral in FY 2018

• Accretive in 2019 as inland barge market improves

• Anticipated cost synergies of $10-12 million over one year

Value Created

• All cash purchase

• To be financed through additional borrowings

Financing

• Signed purchase and sale agreement on February 4, 2018

• Closed on February 14, 2018 Timing

11

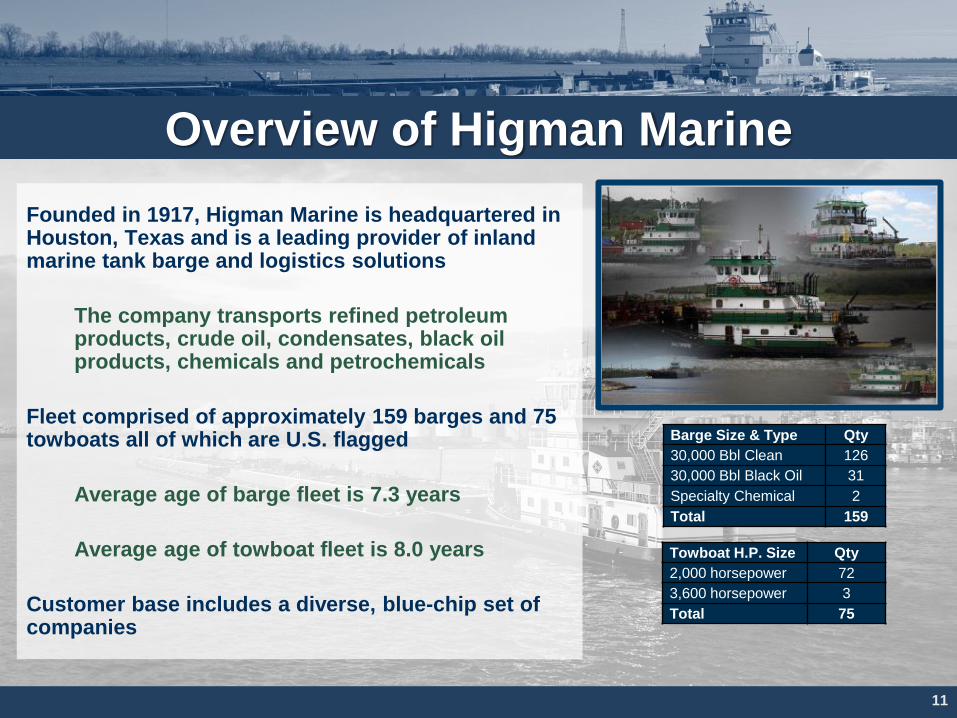

Overview of Higman Marine

Founded in 1917, Higman Marine is headquartered in Houston, Texas and is a leading provider of inland marine tank barge and logistics solutions

The company transports refined petroleum products, crude oil, condensates, black oil products, chemicals and petrochemicals

Fleet comprised of approximately 159 barges and 75 towboats all of which are U.S. flagged

Average age of barge fleet is 7.3 years

Average age of towboat fleet is 8.0 years

Customer base includes a diverse, blue-chip set of companies

Barge Size & Type Qty

30,000 Bbl Clean 126

30,000 Bbl Black Oil 31

Specialty Chemical 2

Total 159

Towboat H.P. Size Qty

2,000 horsepower 72

3,600 horsepower 3

Total 75

12

Rationale for Higman Acquisition

Adding scale in core business

Young, high-quality and well-maintained fleet

Expands business and relationships with existing customers

New capacity and flexibility to better serve customers

Ability to retain high-quality Higman personnel

Attractive time in cycle to acquire assets

Opportunities for cost synergies

Accretive to earnings as market recovers although first year will likely be neutral

13

MARINE TRANSPORTATION

14

U.S. Inland and Coastal Waterway Systems

Texas and Louisiana account for

80% of the total U.S. production of

chemicals and petrochemicals

12,000 miles of navigable

waterways link America’s

heartland to the world

Barge Industry Facts The U.S. barge industry serves the inland waterways, U.S. coastal ports, Alaska and Hawaii

– The inland barge fleet is comprised of approximately 18,000 dry cargo barges and 3,800 liquid tank barges

– The coastal market, including Alaska and Hawaii, encompasses approximately 290 tank barges that are 195,000 barrels or smaller

Kirby is principally in the liquid cargo transportation business

No competition from foreign companies due to a U.S. law known as the Jones Act

Equipment not subject to economic obsolescence because draft, lock and port restrictions limit the size of barges

Barges are mobile, carry wide range of cargoes and service different geographic markets

Water transportation plays a vital role in the U.S. economy

U.S. waterway systems are an environmentally friendly mode of transportation

15

Markets and Products Moved Products Drivers

Petrochemicals and Chemicals

Benzene, Styrene, Methanol, Naphtha,

Acrylonitrile, Xylene, Caustic Soda, Butadiene,

Propylene

Black Oil

Residual Fuel Oil, Coker Feedstock, Vacuum Gas

Oil, Asphalt, Carbon Black Feedstock, Crude Oil,

Natural Gas Condensate, Ship Bunkers Fuel for Power Plants and Ships, Feedstock for

Refineries, Road Construction

Refined Petroleum Products

Gasoline, No. 2 Oil, Jet Fuel, Heating Oil, Diesel

Fuel, Ethanol

Vehicle Usage, Air Travel, Weather, Refinery

Utilization

Agricultural Chemicals

Anhydrous Ammonia, Nitrogen-based Liquid

Fertilizer, Industrial Ammonia

Corn, Cotton, Wheat Production, Chemical

Feedstock Usage

16

Marine Transportation Demand Drivers

30%

70%

Consumer Durables

Consumer Non-Durables

56% 23%

17%

4% Petrochemicals and Chemicals

Black Oil

Refined Petroleum Products

Agricultural Chemicals

Revenue by Product1

1YTD as of December 31, 2017

17

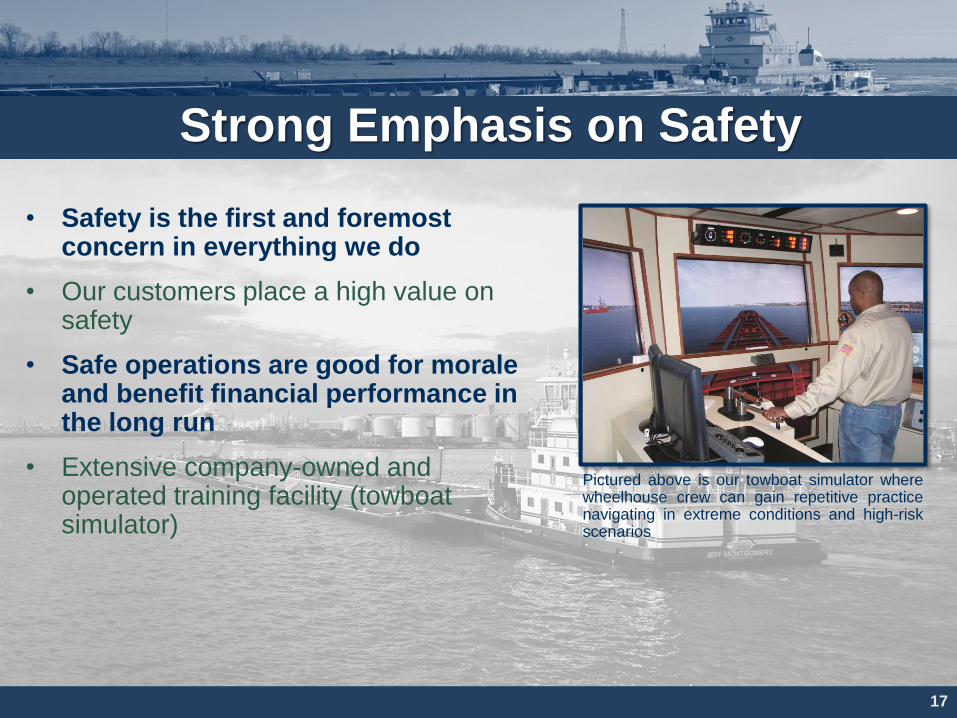

• Safety is the first and foremost concern in everything we do

• Our customers place a high value on safety

• Safe operations are good for morale and benefit financial performance in the long run

• Extensive company-owned and operated training facility (towboat simulator)

Strong Emphasis on Safety

Pictured above is our towboat simulator where wheelhouse crew can gain repetitive practice navigating in extreme conditions and high-risk scenarios

Inland Tank Barge Markets

18

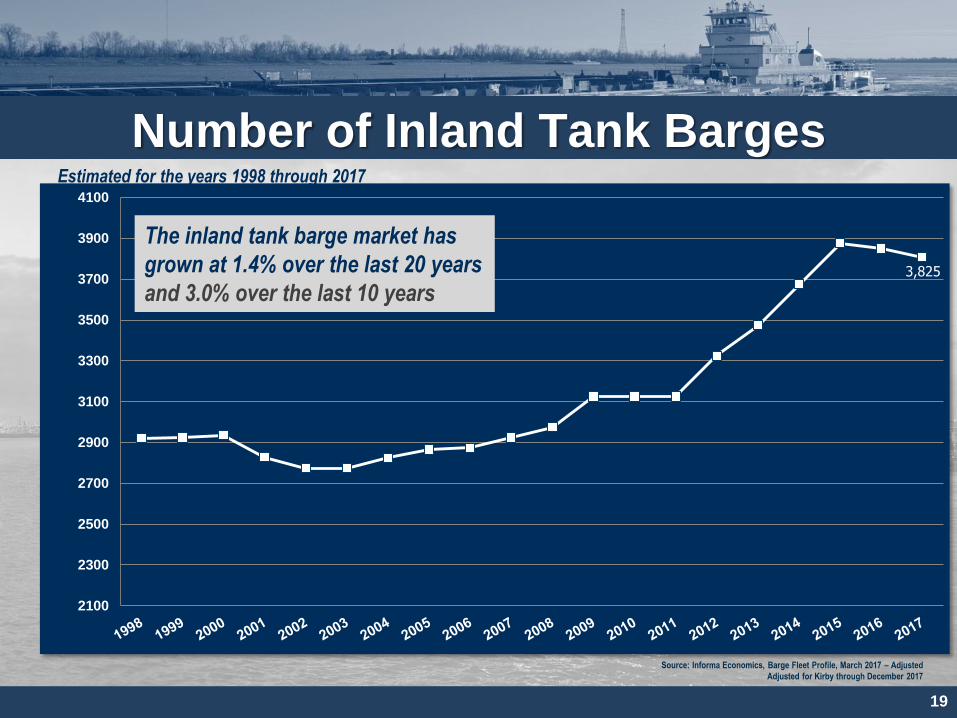

19

Number of Inland Tank Barges Estimated for the years 1998 through 2017

121 single hull tank

barges industry wide,

9 operated by Kirby

3,825

2100

2300

2500

2700

2900

3100

3300

3500

3700

3900

4100

Source: Informa Economics, Barge Fleet Profile, March 2017 – Adjusted

Adjusted for Kirby through December 2017

The inland tank barge market has

grown at 1.4% over the last 20 years

and 3.0% over the last 10 years

20

Inland Tank Barge Fleet Age Profile

1071

785

516

354 305

140

40

217 255

0

200

400

600

800

1000

1200

0 to 5 5 to 10 10 to 15 15 to 20 20 to 25 25 to 30 30 to 35 35 to 40 > 40

Inland Tank Barge Age Distribution1 (Number of barges by age in years)

Source: Informa Economics, Barge Fleet Profile, March 2017 (1) The total of 3,683 barges in this chart is unadjusted from the Informa Economics, Barge Fleet Profile

Inland Fleet Size and Flexibility

Towboat Fleet

• Operated an average of 227 towboats during

the 2017 fourth quarter of which 67 were

chartered

• Chartered towboats used to balance

horsepower with demand

21

Tank Barge Fleet

• Large fleet facilitates better asset utilization

• More backhaul opportunities

• Faster barge turnarounds

• Diversity of barge products and spot opportunities

• Less cleaning

Better Asset Utilization

Kirby Inland Fleet by Barge Type

* As of February 26, 2018 including barges from Higman acquisition 22

*

Petrochemicals / Refined Products -High capacity pumps -Specialty coated tanks

Black Oil & Bunkering -Self-contained heating systems

Pressure -Pressurized tanks

Anhydrous Ammonia -Refrigeration tanks

Specialty -Stainless steel tanks

783

139

61

10

5

23

Tank Barges

Operated

Dry Cargo Barges

Operated

John W. Stone Oil 37 -

Martin Midstream Partners 37 -

Buffalo Marine Service, Inc. 36 -

Accu Trans Marine 30 -

Targa 20 -

River City Towing Services 18 -

NGL Energy Partners 18 -

Rhodia, Inc. 18 -

Harley Marine Gulf 14 -

Progressive Barge Line 10 -

Apex Towing Company 9 -

Olin Corporation (Blue Cube) 9 -

Merichem Company 6 -

TW LaQuay Marine, LLC 4 -

Highland Marine 4 -

AgriChem Marine 2

Parker Towing Company 2 293

Oakley Barge Line 2 -

Campbell Transportation 1 698

Other 12 7,825

TOTAL 3,807 18,897

Informa Economics, Barge Fleet Profile, March 2017 – Adjusted

Tank Barges

Operated

Dry Cargo Barges

Operated

Kirby Corporation* 998 -

American Commercial Lines LLC 445 3,346

Canal Barge Company, Inc. 301 403

Ingram Barge Company 223 4,333

Florida Marine 219 218

MPLX (“Hardin St. Marine”) 215 -

Blessey Marine Services 169 -

Enterprise Products Partners 137 -

Magnolia Marine Transport Co. 88

American River Transportation Co. 82 1,781

LeBeouf Brothers Towing Co 81 -

Genesis Energy, L.P. 74

Southern Towing Company 69 -

Savage Inland Marine 63 -

PPG Industries, Inc. 56 -

Golding Barge Lines, Inc. 56 -

Devall Barge Line 53 -

Cenac Towing 52 -

Settoon Towing, LLC 51 -

Westlake Vinyl 44

Chem Carriers, Inc. 42

Shipper Owned Independent

Inland Barge Fleet by Operator

Shipper Owned Independent

* Kirby as of February 26, 2018 including barges from Higman acquisition

Coastal Tank Barge Markets

24

25

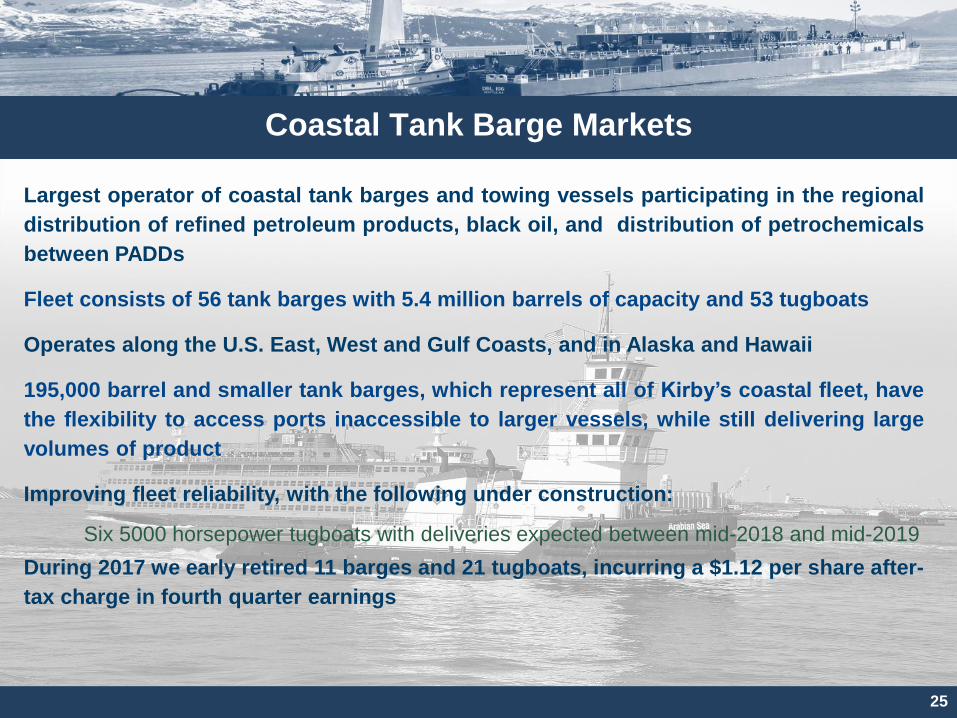

Coastal Tank Barge Markets

Largest operator of coastal tank barges and towing vessels participating in the regional

distribution of refined petroleum products, black oil, and distribution of petrochemicals

between PADDs

Fleet consists of 56 tank barges with 5.4 million barrels of capacity and 53 tugboats

Operates along the U.S. East, West and Gulf Coasts, and in Alaska and Hawaii

195,000 barrel and smaller tank barges, which represent all of Kirby’s coastal fleet, have

the flexibility to access ports inaccessible to larger vessels, while still delivering large

volumes of product

Improving fleet reliability, with the following under construction:

Six 5000 horsepower tugboats with deliveries expected between mid-2018 and mid-2019

During 2017 we early retired 11 barges and 21 tugboats, incurring a $1.12 per share after-

tax charge in fourth quarter earnings

40

61

112

34

19

6 2

19

0

20

40

60

80

100

120

0-5 Years 5-10 Years 10-15 Years 15-20 Years 20-25 Years 25-30 Years 30-35 Years 35+ Years

26

Coastal Tank Barge Age Profile

Nu

mb

er o

f B

arge

s

Coastal Barge Market Age Distribution* Number of barges by age

The average age of the

nation’s coastal tank barge

fleet is ~13 years

* Tank barges with 195,000 barrels capacity or less as of December 31, 2017

Coastal Tank Barge Owners

27

Coastal Tank

Barges Operated *

Estimated Barrel Capacity*

(MM)

Vane Brothers 78 2.8

Kirby Corporation 56 5.4

Harley Marine 42 1.9

Reinauer Transportation 25 2.1

Bouchard Transportation1 23 2.4

Crowley Marine2 15 2.5

Moran Towing 13 1.4

Genesis Energy, L.P. 9 0.9

Saltchuk Resources (Foss Maritime) 9 0.2

Sause Brothers 7 0.6

U.S. Shipping Corporation 4 0.6

Poling & Cutler 4 0.2

Martin Gas Marine 3 0.2

Overseas Shipholding Group3 1 0.2

Seacor 1 0.2

Wawa, Inc. 1 0.2

Occidental Chemical Corporation 1 0.1

Hyak Maritime 1 0.1

293 22.0

* Tank barges with 195,000 barrels capacity or less as of December 31, 2017

Kirby is Well-Positioned in U.S. Coastal Markets

(1) Excludes five vessels over 250,000 barrels (2) Excludes the “750 class”, three ATBs with capacity of 327,000 barrels/ea. (3) Excludes nine ATBs with capacity of 200,000 barrels or greater

28

DISTRIBUTION AND SERVICES

United Holdings Kirby Engine Systems

Stewart & Stevenson

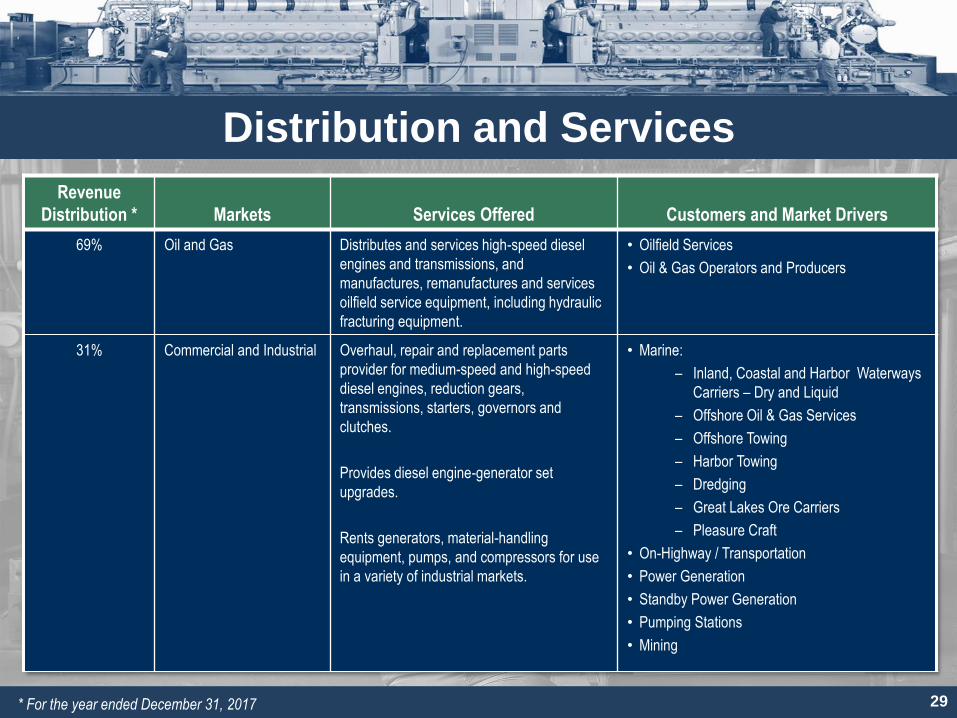

Distribution and Services

Revenue

Distribution *

Markets

Services Offered

Customers and Market Drivers

69% Oil and Gas Distributes and services high-speed diesel

engines and transmissions, and

manufactures, remanufactures and services

oilfield service equipment, including hydraulic

fracturing equipment.

• Oilfield Services

• Oil & Gas Operators and Producers

31% Commercial and Industrial Overhaul, repair and replacement parts

provider for medium-speed and high-speed

diesel engines, reduction gears,

transmissions, starters, governors and

clutches.

Provides diesel engine-generator set

upgrades.

Rents generators, material-handling

equipment, pumps, and compressors for use

in a variety of industrial markets.

• Marine:

– Inland, Coastal and Harbor Waterways

Carriers – Dry and Liquid

– Offshore Oil & Gas Services

– Offshore Towing

– Harbor Towing

– Dredging

– Great Lakes Ore Carriers

– Pleasure Craft

• On-Highway / Transportation

• Power Generation

• Standby Power Generation

• Pumping Stations

• Mining

* For the year ended December 31, 2017 29

Distribution and Services

30

Engines, Transmissions and Reduction Gears

Medium-Speed

– Electro-Motive Diesel (EMD)

– Cooper-Bessemer

– Nordberg

High-Speed

– Caterpillar

– Cummins

– MTU

– Detroit Diesel

– John Deere

– Isuzu

– Deutz

– Volvo Penta

Transmissions/

Reduction Gears

– Allison

– Falk

– Twin Disc

Oil and Gas Market

31

One of the largest distribution and services providers to the land-based

oil services market

Hydraulic fracturing technology has significantly expanded and reduced

the cost of producing U.S. natural gas and oil reserves

Manufacturer and remanufacturer of oilfield equipment used in the hydraulic

fracturing of shale formations

Approximate installed base of 13 million horsepower of frac equipment; most

require some form of major service every three to five years

Heavy duty cycle associated with fracturing drives need for service and parts

Kirby Distribution and Services Locations

32

Houston

Seattle

Chesapeake

Rocky Mount

Paducah

Tampa

Mobile Shreveport

Baton Rouge Lafayette / New Iberia

Belle Chasse/Harvey

Houma

Little Rock

Oklahoma City

Tulsa

Austin

San Antonio

Laredo

Pharr

Thorofare

Cotulla

Corpus Christi

Odessa

Marlborough

Middletown

Albany

NYC Piscataway

Fort Myers

Miami

Fort Lauderdale

West Palm Beach Fort Pierce

Orlando

Jacksonville

Ocala

Panama City

Stuttgart

Dallas Longview

Wichita Falls Lubbock

Great Bend

Liberal

Denver

Casper

Albuquerque

El Paso

Phoenix

Grand Junction

United Holdings Kirby Engine Systems Stewart & Stevenson

Locations / Branches

Allison / MTU / DTNA Territories

United Holdings Stewart & Stevenson

Kirby Engine Systems Stewart & Stevenson

EMD Territories

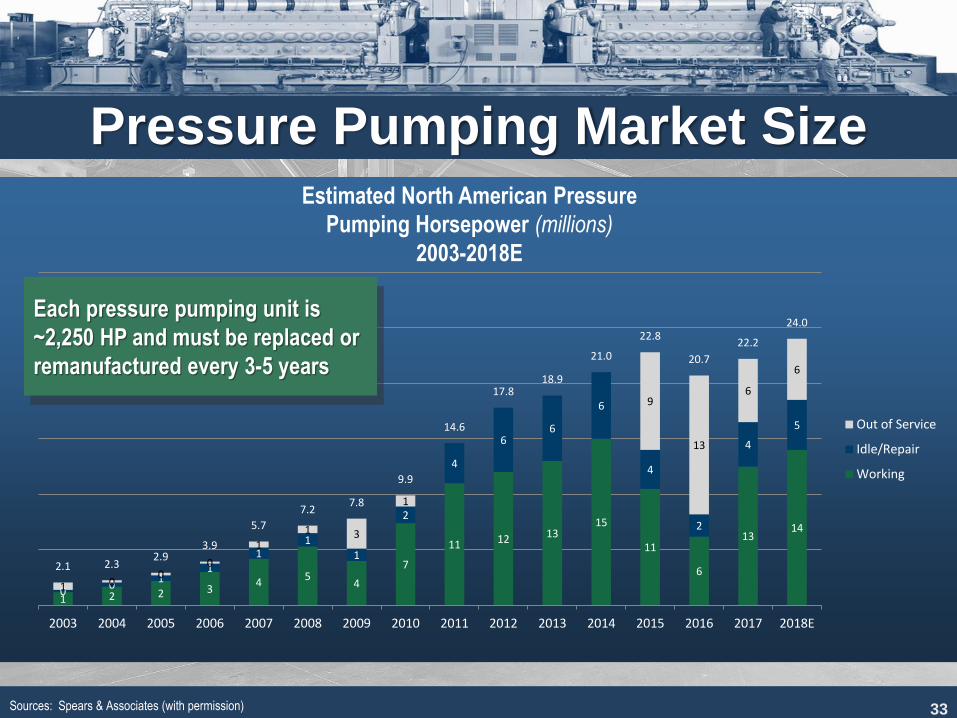

Pressure Pumping Market Size

33 Sources: Spears & Associates (with permission)

1 2 2 3 4

5 4

7

11 12 13 15

11

6

13 14

0 0

1 1

1 1

1

2

4

6 6

6

4

2

4

5

1 0 0

0

1

1 3

1

9

13

6

6

2.1 2.3 2.9

3.9

5.7

7.2 7.8

9.9

14.6

17.8 18.9

21.0

22.8

20.7

22.2

24.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018E

Out of Service

Idle/Repair

Working

Each pressure pumping unit is

~2,250 HP and must be replaced or

remanufactured every 3-5 years

Estimated North American Pressure

Pumping Horsepower (millions)

2003-2018E

OUTLOOK

34

35

2018 Guidance Published 2018 first quarter guidance of $0.45 to $0.65(1) per share versus $0.51 for the 2017 first quarter

- Includes $0.08 to $0.12 per share benefit from tax reform

Published 2018 full year guidance of $2.50 to $3.00(1) per share versus to $1.99(2) per share for 2017 excluding one-

time items in the fourth quarter

- Includes $0.40 to $0.50 per share benefit from tax reform

Marine Transportation:

- Inland utilization in the low-90% to mid-90% range

- Coastal utilization in the low-80% to mid-80% range

- Continued pricing pressure on inland and coastal tank barge term contract renewals

- Potential pricing inflection in inland markets in H2 2018

Distribution and Services:

For the land-based market, expect continued demand for pressure pumping remanufacturing and

transmission overhauls, as well as new equipment sales

In the marine market, expect results to improve as customers can no longer afford critical engine overhauls

previously deferred

Power generation is expected to be similar to 2017

(1) Based on Kirby's most recently published earnings guidance in the January 31, 2018 press release announcing Q4 2017 earnings. That guidance is shown for convenience only and does not

constitute confirming or updating the guidance, which will only be done by public disclosure.

(2) 2017 earnings per share exclude a one-time deferred tax revaluation benefit of $4.83 per share, and non-recurring after-tax charges including impairments of marine vessels of $1.20 per share.

FINANCIAL HIGHLIGHTS

36

37

Financial Summary

(1) 2017 earnings per share exclude a one-time deferred tax revaluation benefit and non-recurring after-tax charges including impairments of marine vessels.

Income Statement FY 2017 FY 2016 $ %

Revenues:

Marine transportation $ 1,324.1 $ 1,471.9 $ (147.8) -10%

Distribution and services 890.3 298.8 591.5 198%

Total $ 2,214.4 $ 1,770.7 $ 443.7 25%

Operating income (loss):

Marine transportation $ 136.0 $ 257.1 $ (121.1) -47%

Distribution and services 86.6 3.1 83.5 2694%

Corporate expenses (18.2) (15.0) (3.2) 21%

Total $ 204.4 $ 245.2 $ (40.8) -17%

Net earnings:

Net earnings (GAAP) $ 313.2 $ 141.4 $ 171.8 121%

US tax reform and deferred tax liability remeasurement (269.4) - (269.4)

Impairment of long-lived assets 66.9 - 66.9

Adjusted net earnings (Non-GAAP)1 $ 110.7 $ 141.4 $ (30.7) -22%

GAAP earnings per share $ 5.62 $ 2.62 $ 3.00 115%

Adjusted earnings per share (Non-GAAP)1 $ 1.99 $ 2.62 $ (0.63) -24%

Change

Operating Margins

38

18.9% 18.4%

16.6%

14.6% 15.7%

17.4%

19.0%

21.1%

22.4% 23.6%

21.1% 21.9% 22.1%

23.8% 24.3%

22.5%

17.5%

10.3% 10.0% 10.1% 10.1%

9.5% 9.7%

11.7%

14.9% 15.6%

15.0%

10.5% 10.6% 10.4% 9.4%

8.1% 7.5%

3.9%

1.1%

9.7%

0%

5%

10%

15%

20%

25%

30%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Marine Transportation Distribution and Services

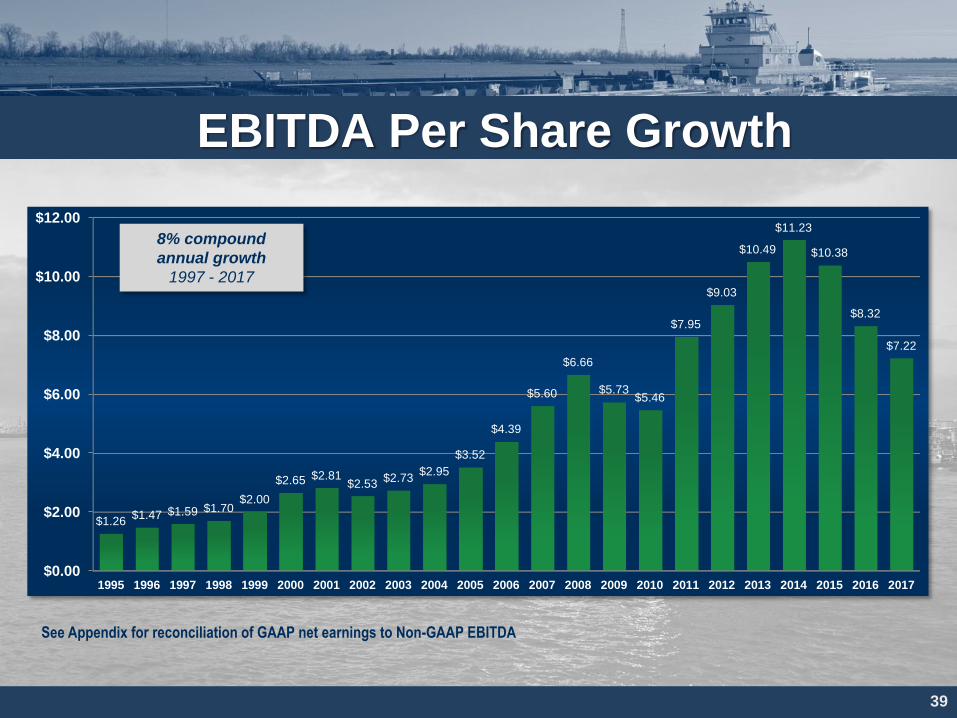

EBITDA Per Share Growth

39

See Appendix for reconciliation of GAAP net earnings to Non-GAAP EBITDA

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

$1.26 $1.47 $1.59 $1.70

$2.00

$2.65 $2.81 $2.53

$2.73 $2.95

$3.52

$4.39

$5.60

$6.66

$5.73 $5.46

$7.95

$9.03

$10.49

$11.23

$10.38

$8.32

$7.22

8% compound

annual growth

1997 - 2017

Cash Flows

40

Expansion Barges

$30

* Unaudited

$83 $97

$73

$112 $127

$142 $150

$236 $246

$319

$245

$312 $326

$601

$439

$524

$416

$353

$48 $59 $48

$72 $94

$122 $139

$164 $173 $193

$137

$226

$312

$253

$355 $345

$231

$177

$215

$0

$100

$200

$300

$400

$500

$600

$700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018E

In M

illio

ns

Last

Published

Guidance

1

$1951

Operating cash flow Capital expenditures (ex-acquisitions)

(1) Based on Kirby's most recently published earnings guidance in the January 31, 2018 press release announcing Q4 2017 earnings. That guidance is shown for convenience only and does not constitute confirming or updating

the guidance, which will only be done by public disclosure.

0%

10%

20%

30%

40%

50%

60%

Q12001

Q12002

Q12003

Q12004

Q12005

Q12006

Q12007

Q12008

Q12009

Q12010

Q12011

Q12012

Q12013

Q12014

Q12015

Q12016

Q12017

Debt-to-Capital Ratio

of 31.5% post

Higman Acquisition

Capital Structure

41

50.4%

24.2%

Debt-to-Total Capital 2001 – 2017

Financial Strength

42

• Investment grade rating

– Standard & Poor’s: BBB, stable (following Higman acquisition)

– Moody’s: Baa2, negative outlook (following Higman acquisition)

• $500 million unsecured Private Placement

– $150 million 7-year maturity at 2.72% due 2/27/2020

– $350 million 10-year maturity at 3.29% due 2/27/2023

• $850 million Bank Revolving Credit Facility

– Maturity date of June 26, 2022

– ~$408MM outstanding as of February 2018

• $500 million 4.200% Senior Notes

– Maturity date of March 1, 2028

– Used to fund Higman Marine acquisition

WHY INVEST IN KIRBY?

43

Why Invest in Kirby?

44

Long-term record of success

Experienced management teams in both core businesses

Marine Transportation

U.S. feedstock position puts our refinery, chemical, and integrated major customers in a globally competitive position and is driving volume growth

75% of inland revenue under term contracts, of which approximately 51% are under time charters

80% of coastal revenue under term contracts, of which approximately 85% are under time charters

Approximately 70% of petrochemicals moved produce consumer nondurable goods

Distribution and Services Provides essential service to marine, land-based, power generation, and other industrial sectors

Largest geographic footprint of any U.S. distribution and service provider

Strong financial discipline and cash flow

Thank You For Listening to Our Story

Kirby Corporation Putting America’s

Waterways to Work

46

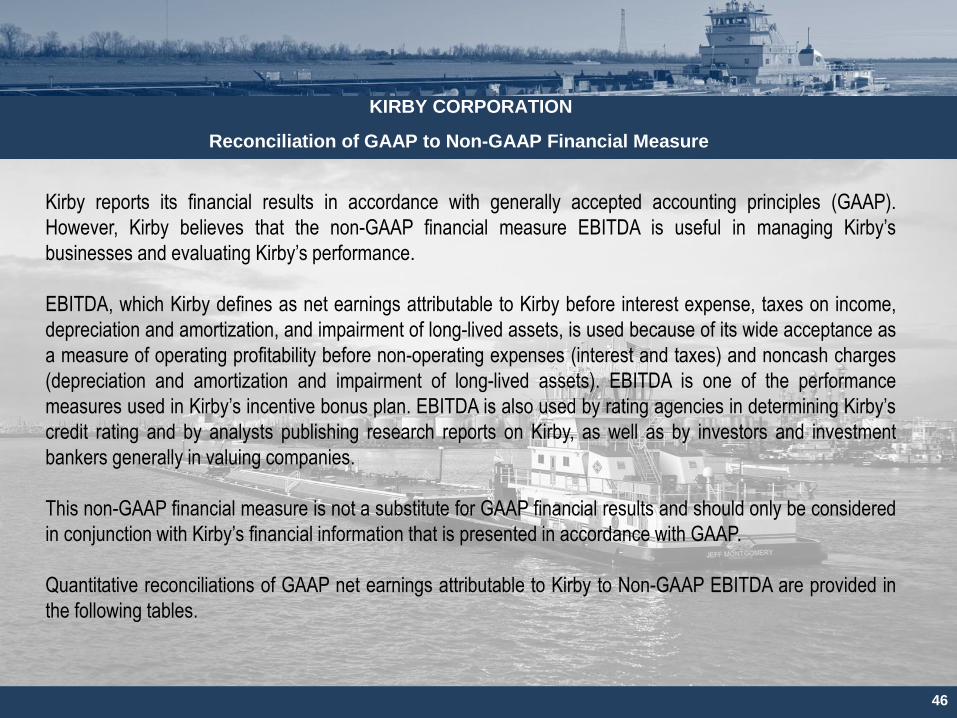

KIRBY CORPORATION

Reconciliation of GAAP to Non-GAAP Financial Measure

Kirby reports its financial results in accordance with generally accepted accounting principles (GAAP).

However, Kirby believes that the non-GAAP financial measure EBITDA is useful in managing Kirby’s

businesses and evaluating Kirby’s performance.

EBITDA, which Kirby defines as net earnings attributable to Kirby before interest expense, taxes on income,

depreciation and amortization, and impairment of long-lived assets, is used because of its wide acceptance as

a measure of operating profitability before non-operating expenses (interest and taxes) and noncash charges

(depreciation and amortization and impairment of long-lived assets). EBITDA is one of the performance

measures used in Kirby’s incentive bonus plan. EBITDA is also used by rating agencies in determining Kirby’s

credit rating and by analysts publishing research reports on Kirby, as well as by investors and investment

bankers generally in valuing companies.

This non-GAAP financial measure is not a substitute for GAAP financial results and should only be considered

in conjunction with Kirby’s financial information that is presented in accordance with GAAP.

Quantitative reconciliations of GAAP net earnings attributable to Kirby to Non-GAAP EBITDA are provided in

the following tables.

47

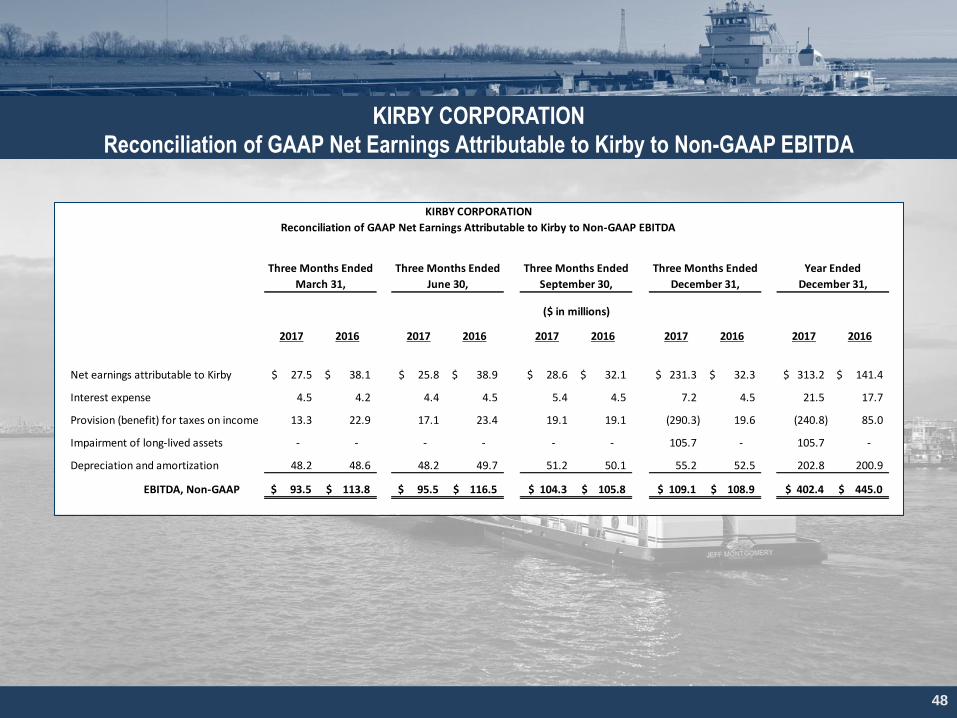

KIRBY CORPORATION

Reconciliation of GAAP Net Earnings Attributable to Kirby to Non-GAAP EBITDA

2017 2016 2015 2014 2013 2012 2011 2010 2009 2008

Net earnings attributable to Kirby 313.2$ 141.4$ 226.7$ 282.0$ 253.1$ 209.4$ 183.0$ 116.2$ 125.9$ 157.2$

Interest expense 21.5 17.7 18.8 21.5 27.9 24.4 17.9 11.0 11.1 14.1

Provision (benefit) for taxes on income (240.9) 85.0 133.7 169.8 152.3 127.9 109.3 72.3 78.0 97.4

Impairment of long-lived assets 105.7 - - - - - - - - -

Depreciation and amortization 202.9 200.9 192.2 169.3 164.4 145.2 126.0 95.3 94.0 91.2

EBITDA, Non-GAAP 402.4$ 445.0$ 571.4$ 642.6$ 597.7$ 506.9$ 436.2$ 294.8$ 309.0$ 359.9$

KIRBY CORPORATION

Reconciliation of GAAP Net Earnings Attributable to Kirby to Non-GAAP EBITDA

($ in millions)

48

KIRBY CORPORATION

Reconciliation of GAAP Net Earnings Attributable to Kirby to Non-GAAP EBITDA

2017 2016 2017 2016 2017 2016 2017 2016 2017 2016

Net earnings attributable to Kirby 27.5$ 38.1$ 25.8$ 38.9$ 28.6$ 32.1$ 231.3$ 32.3$ 313.2$ 141.4$

Interest expense 4.5 4.2 4.4 4.5 5.4 4.5 7.2 4.5 21.5 17.7

Provision (benefit) for taxes on income 13.3 22.9 17.1 23.4 19.1 19.1 (290.3) 19.6 (240.8) 85.0

Impairment of long-lived assets - - - - - - 105.7 - 105.7 -

Depreciation and amortization 48.2 48.6 48.2 49.7 51.2 50.1 55.2 52.5 202.8 200.9

EBITDA, Non-GAAP 93.5$ 113.8$ 95.5$ 116.5$ 104.3$ 105.8$ 109.1$ 108.9$ 402.4$ 445.0$

KIRBY CORPORATION

Reconciliation of GAAP Net Earnings Attributable to Kirby to Non-GAAP EBITDA

($ in millions)

Three Months Ended

December 31,

Year Ended

December 31,March 31,

Three Months Ended Three Months Ended

June 30,

Three Months Ended

September 30,

49

KIRBY CORPORATION

MARINE TRANSPORTATION PERFORMANCE MEASUREMENTS

(1) Ton miles indicate fleet productivity by measuring the distance (in miles) a loaded inland tank barge is moved. Example: A typical 30,000 barrel inland tank barge loaded with 3,300 tons of liquid cargo is moved 100 miles, thus generating 330,000 ton miles. (2) Inland marine transportation revenues divided by ton miles. Example: 4th quarter 2017 inland marine revenues of $241,951,000 divided by 2,971,000,000 ton miles = 8.1 cents. (3) Towboats operated, is the average number of owned and chartered inland towboats operated during the period. (4) Delay days measures the lost time incurred by an inland tow (inland towboat and one or more inland tank barges) during transit. The measure includes transit delays caused by weather, lock congestion and other navigational factors.

2009 2010 2011 2012 2013 2014 2015

Year Year Year Year Year Year Year 1st

Q 2nd

Q 3rd

Q 4th

Q Year 1st

Q 2nd

Q 3rd

Q 4th

Q Year

Inland Performance

Measurements:

Ton miles (in millions) (1)

11,977 12,957 13,414 12,224 11,754 13,088 12,502 2,748 2,792 2,648 2,973 11,161 2,977 2,818 2,753 2,971 11,519

Revenues/Ton mile (cents/tm) (2)

7.1 6.8 7.6 8.9 9.8 8.8 8.7 8.9 8.8 8.6 7.7 8.5 8.0 7.9 8.0 8.1 8.0

Towboats operated (3)

220 221 240 245 256 251 248 240 241 227 230 234 235 220 215 227 224

Delay days (4)

5,201 5,772 6,777 6,358 7,843 7,804 7,924 2,236 2,035 929 2,078 7,278 2,267 1,367 1,965 1,978 7,577

2016 2017

$135+ Billion of U.S. Petrochemical Investments*

Sources: ICIS, Company announcements, Kirby Corp. *Notes: Date reflects anticipated year in-service, red font reflects construction in progress, green online, unk=unknown

Corpus Christi/Point Comfort, TX Cost ($MM)

Celanese-Mitsui 2020 New methanol 800 Exxon-SABIC JV 2020 New ethylene/derivatives 9,300 Formosa 2018 New polyethylene / MEG 5,000

Formosa 2018 New ethylene 1,700 Formosa 2018 New LD polyethylene

Formosa 2020-21 New PDH

LyondellBasell 2017 Ethylene expansion 350

M&G Group 2018 New PET/PTA 1,000

Oxy/Mexichem J 2017 New ethylene (2 units) 1,500

Freeport – Old Ocean, TX Cost ($MM)

BASF-Yara 2018 New ammonia 600

CP Chemical 2018 New polyethylene 6,000

Dow 2016 New PDH 6,000

Dow 2017 New ethylene

Dow 2017 Polyethylene exp. Dow/MEGlobal JV 2019 Monoethylene Glycol 1,100

Iowa Cost ($MM)

Orascom (OCI) 2017 New fertilizer 3,000

CF Industries 2016 Ammonia expansion 1,900

Pacific Northwest Cost ($MM)

NW Innovation 2020 New methanol 3,600

Tesoro 2018-19 New xylene 400

Houston Ship Channel and surrounding TX Cost ($MM)

Celanese-Mitsui 2015 New methanol 800 Celanese-Mitsui TBD New methanol unk

Celanese 2018 Acetic /VAM expansion unk

Celanese 2018 New methanol unk

CP Chemical 2018 New ethylene (80% done) 5,000

CP Chemical 2017 PAO expansion unk

Enterprise 2017 New PDH unk

Enterprise 2019 New isobutylene 3,000 Exxon Mobil Exxon Mobil

2018

2017 New ethylene

New polyethylene 3,000

unk Flint Hills /Koch TBD New PDH unk

Fund Connell 2019 Methanol expansion 4,500

Ineos/Sasol JV 2018 New polyethylene unk Ineos 2017 Ethylene debottleneck unk

Ineos 2019 New Polyalphaolephin unk

LyondellBasell 2016 Tri-ethylene glycol exp. unk

LyondellBasell 2015 Propylene debottleneck 20 LyondellBasell 2021 Propylene oxide/TBA 2,400 LyondellBasell TBD Polypropylene/PDH 2,000 LyondellBasell 2019 New HDPE 700 LyondellBasell 2017 Ethylene expansion 170

TOTAL/Nova/ Borealis JV

2020 New polyethylene unk

Oklahoma Cost ($MM)

Koch Early -2018 Urea expansion 1,300

LSB Ind. 2016 New ammonia 275

Beaumont/Orange, TX Cost ($MM)

Exxon Mobil 2019 Polyethylene exp. unk

Flint Hills/Koch 2016 Ethylene expansion unk

Huntsman 2016 Ethylene oxide exp. 125

LANXESS 2016 Butadiene rubber unk

Natgasoline (OCI-G2X JV)

Early-2018 New methanol 1,000

TOTAL/Nova/ Borealis JV

2020 Ethylene expansion 1,700

Ohio Cost ($MM)

PTT Global Chem 2021 New ethylene 5,700

PBF 2015 Aromatics exp unk

50

Kentucky Cost ($MM)

Westlake 2017 Ethylene exp. unk

Indiana Cost ($MM)

Midwest Fert. 2022 New ammonia 2,800

Charleston, WV Cost ($MM)

US Methanol 2018 New methanol unk US Methanol TBD New methanol unk

Mobile, AL Cost ($MM)

Huntsman Chem. 2016 Epoxy expansion 65

Baton Rouge – New Orleans Corridor, LA Cost ($MM)

BASF Castleton

2016 2018

Butanediol exp. New methanol

Unk 1,200

CF Industries 2016 Ammonia expansion 1,900

CF Industries 2016 New UAN 1,900

Dow 2017 New polyolefin (2) 2,000 Dyno Nobel 2016 New ammonia 1,000

Eurochem 2018-19 New ammonia 1,500

Formosa 2021 New ethylene 9,400 IGP Methanol 2021 New methanol 4,600 Methanex 2015 Methanol migration 850

Methanex 2015 Methanol migration 550

Shell 2018 New alpha olefins 717

Shintech 2018-19 New EDC/ethylene 1,400

S. LA Methanol 2018-19 New methanol 1,300

Syngas Energy 2020 New methanol 360

Yuhuang Chem 2018 New methanol 1,850

Lake Charles, LA Cost ($MM)

WLK/Lotte JV 2019 New ethylene/MEG 3,000

Dow 2015 Ethylene expansion 1,060 LCM 2021 New methanol 3,800

Indorama 2018 Ethylene restart 175

G2X 2018 Methanol-to-gasoline 1,600

Sasol Sasol

2019

2019

New ethylene New polyethylene

11,000

Westlake 2016 Ethylene expansion 330

Monaca, PA

Cost ($MM)

Shell 2020 New ethylene 6,000

0

500

1,000

1,500

2,000

2,500

2016 2017 2018 2019 2020 2021 2022

51

U.S. Ethylene Feedslate Forecast

Source: Petral Consulting Company, Long Term Forecast to 2022, December 2017

Ethylene Feedstock Volume Thousands of Barrels per Day

Ethane Growth 43%

5-Year CAGR 7%

Product, 2017-2022 Growth and CAGR:

Propane Growth 4%

5-Year CAGR 1%

Butane Growth 8%

5-Year CAGR 1%

Naptha & Gasoil

Growth -7% 5-Year CAGR -1%

~70% of current ethylene

production is from ethane

0

10

20

30

40

50

60

70

2016 2017 2018 2019 2020 2021 2022

All of these Ethylene Plant Coproducts are Moved by Tank Barge

Xylenes & Heavy Aromatics

Growth 11% 5-Year CAGR 2%

52

U.S. Ethylene Plant Coproduct Output

Source: Petral Consulting Company, Long Term Forecast to 2022, December 2017

Ethylene Plant Coproduct Output Millions of Pounds per Day

Propylene Growth 10%

5-Year CAGR 2%

Product, 2017-2022 Growth and CAGR:

Toluene Growth 7%

5-Year CAGR 1%

Benzene Growth 13%

5-Year CAGR 3%

Butadiene & Other C4

Growth 19% 5-Year CAGR 4%

53

Near-Term U.S. Ethylene and Derivative Capacity Additions

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2016 2017 2018 2019 2020

mill

ion

to

ns

ann

ual

ly

Ethylene Capacity Derivative Capacity

Source: Bernstein Research (with permission) August 30, 2016

U.S. ethylene derivative capacity is expected to expand ~30% over the

next 5 years

~40% of new derivatives are products that are moved by water

Vinyl Acetate Monomer

1%

Polyethylene61%

Ethylene Oxide19%

Ethylene Dichloride

4%

Ethylbenzene0%

Alpha Olefins15%

Notes: Ethylbenzene – 99% used to make styrene; ethylene dichloride – a key feedstock in the production of PVC; ethylene oxide is a gas used as a raw material for innumerous applications, including cosmetics, fibers, lubricants, paint thinners and plasticizers and, while not carried by barge, the derivatives, such as ethylene glycol are; alpha olefins are building block chemicals; vinyl acetate monomer is used as a feedstock chemical for glues, fabrics, gels, insulation, paints, safety glass and certain plastics