Pulse Crop Market Outlook

61

Pulse Crop Market Outlook February 2015 Presented by: Chuck Penner

Transcript of Pulse Crop Market Outlook

Pulse Crop Market Outlook

February 2015

Presented by:

Chuck Penner

PRESENTATION OUTLINE

Key consumption market overview

Key competitor overview

Field pea situation & outlook

Lentil situation & outlook

Chickpea situation & outlook

Dry bean situation & outlook

1

KEY CONSUMPTION MARKETS

India

World’s largest producer, consumer and importer

Peas and lentils of most interest

Turkey

Large consumer and re-exporter

Mostly lentils and a few chickpeas

China

Peas are the main interest

Other South Asia

Opportunistic buyers of red lentils and yellow peas

2

INDIA

3

Kharif pulse crop (Jun-Oct)

Pigeon peas, urd beans, mung beans, others

Indirect impact on Cdn pulses

2014 was dry, causing low yields

Rabi pulse crop (Nov-Mar)

Chickpeas, lentils, peas, others

Direct impact on Cdn pulse export potential

Acreage likely lower, esp for chickpeas

Mostly dry so far

INDIAN RABI PULSE PLANTING – LATE JAN

4

Large shortfall for chickpeas

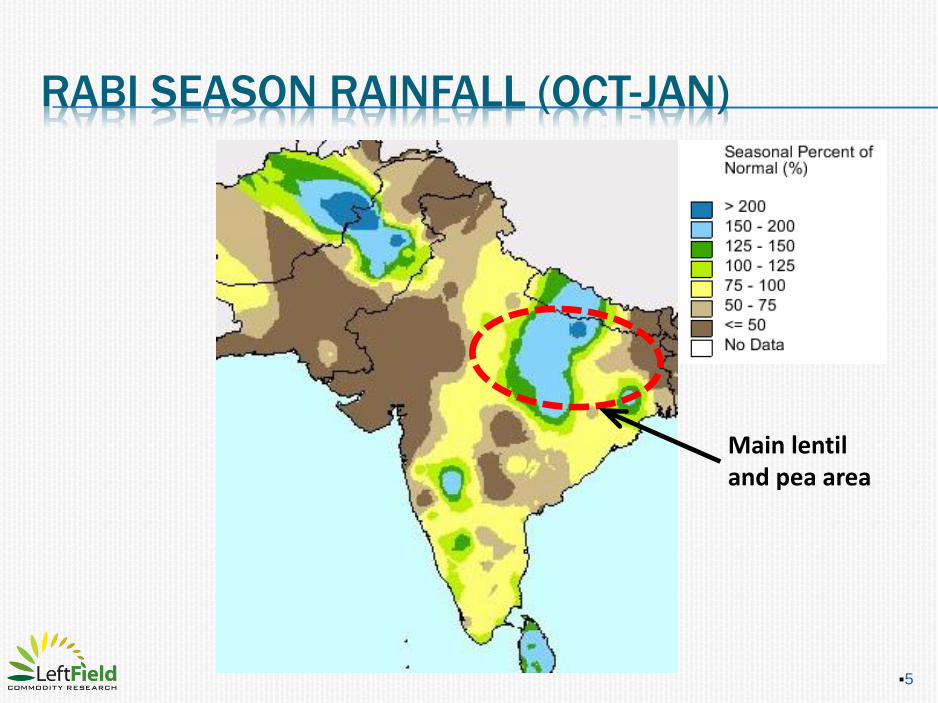

RABI SEASON RAINFALL (OCT-JAN)

5

Main lentil and pea area

INDIAN PULSE PRODUCTION & IMPORTS

6

??

TURKEY

7

Grows mostly kabuli chickpeas and red lentils

Red lentils are winter crop

Large consumer but also trading hub for MENA

Re-export a lot of product to surrounding countries

Lentil crop is receiving decent rains

Acreage likely expanded in response to prices

TURKISH LENTIL PRODUCTION

8

Long term decline

TURKISH SEASONAL RAINFALL

9

CHINA

10

Imports mainly yellow peas (some greens)

Fractionates for food ingredients

Increase in import demand in response to

declining domestic production

Govt emphasis on corn, wheat and rice production

More consumption forecast by USDA

Slower start for 2014/15 exports a small

concern, likely won’t catch up

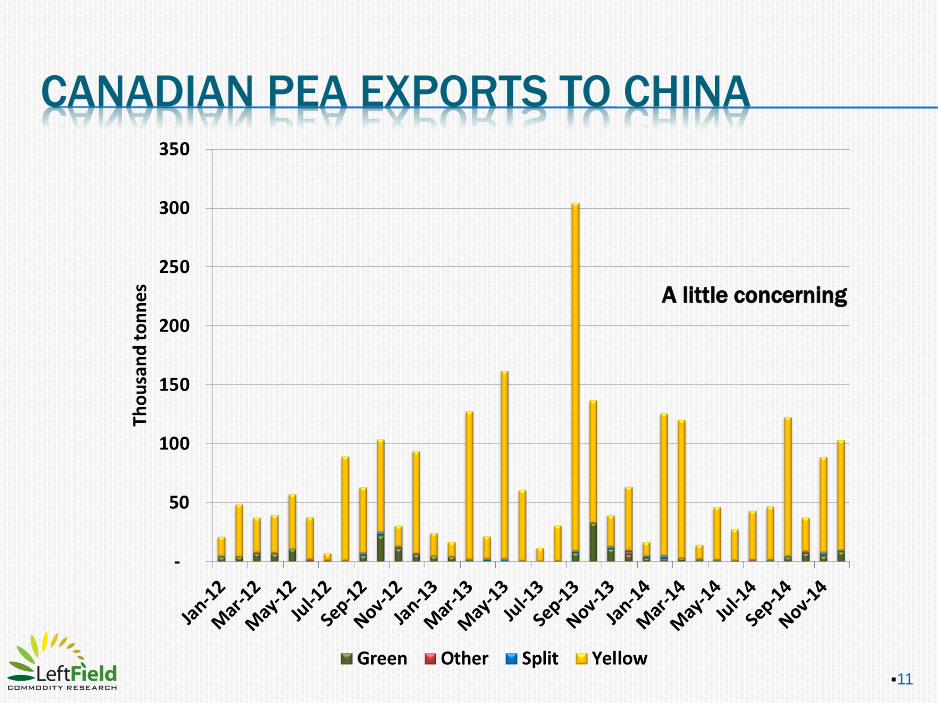

CANADIAN PEA EXPORTS TO CHINA

11

A little concerning

CHINA PEA PRODUCTION & IMPORTS

12

Fewer imports

KEY COMPETITOR MARKETS

Australia

Key export competitor with freight advantage

Reduced crops due to dry conditions in SE

Black Sea

Mostly peas and chickpeas (so far)

Average crop this year

Export surge is already past

US

Peas and green lentils

In 2014, more peas and less lentils

13

AUSTRALIAN PULSE PRODUCTION

BLACK SEA PEA PRODUCTION

US PULSE PRODUCTION

CANADIAN PEA PRODUCTION BY TYPE

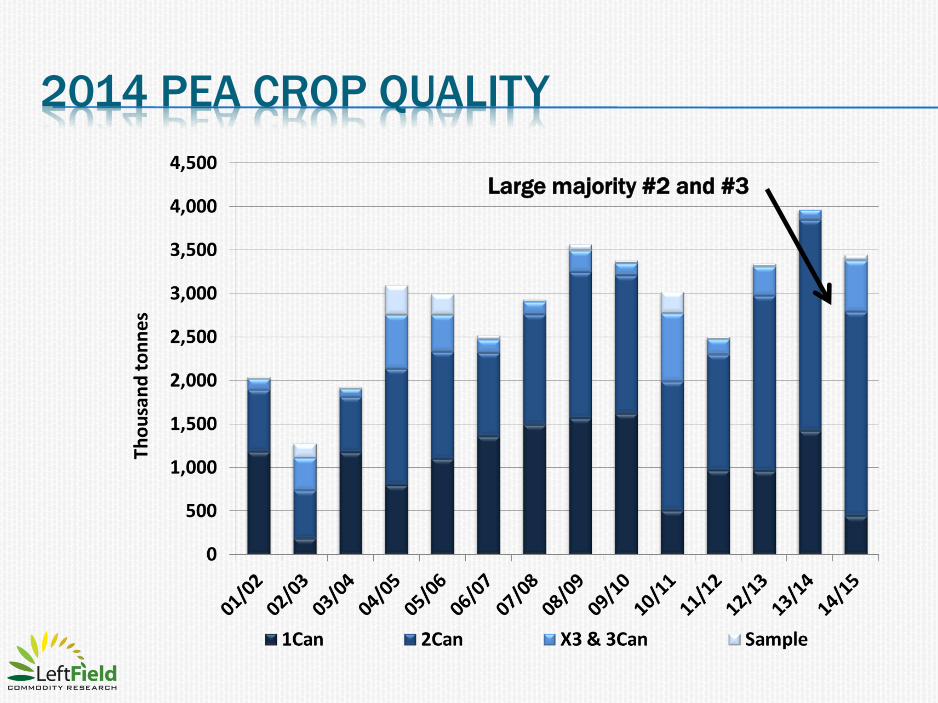

2014 PEA CROP QUALITY

Large majority #2 and #3

CANADIAN 2014/15 PEA EXPORTS

Record exports in Sep

INDIAN CHANA PRODUCTION

Fewer acres, lower yields

INDIAN PEA & DESI CHICKPEA PRICES

Prices reacting to poor

crop outlook, then rains

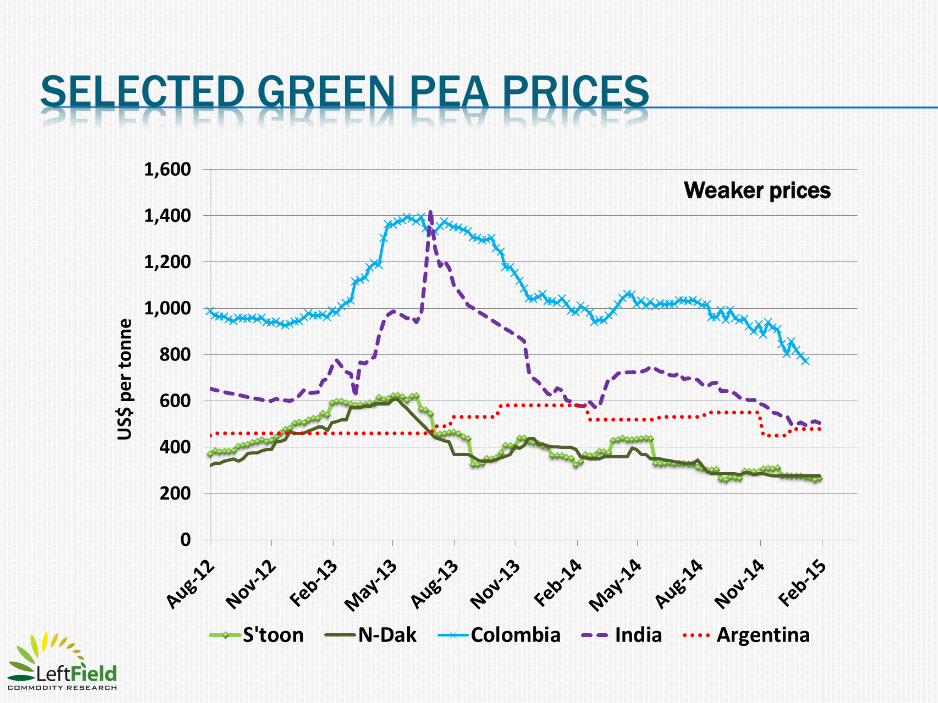

SELECTED GREEN PEA PRICES

Weaker prices

SASKATCHEWAN PEA BIDS

Yellows showing

more strength

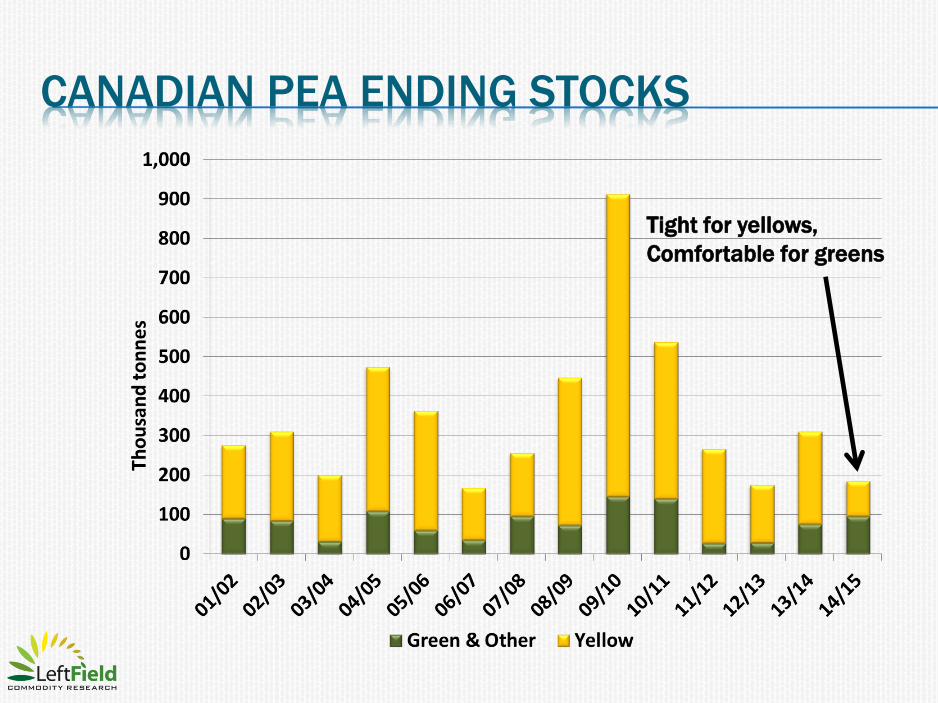

CANADIAN PEA ENDING STOCKS

Tight for yellows,

Comfortable for greens

PEAS – REST OF 2014/15

Yellows

Smaller Canadian crop with heavy South Asian demand

Supplies will run low later in 2014/15

More gains ahead

Greens

Bigger Canadian crop with flat demand (at current prices)

Can substitute for yellows in China if price is right

Limited upside potential

Feeds

Strong as long as meal markets are supported

25

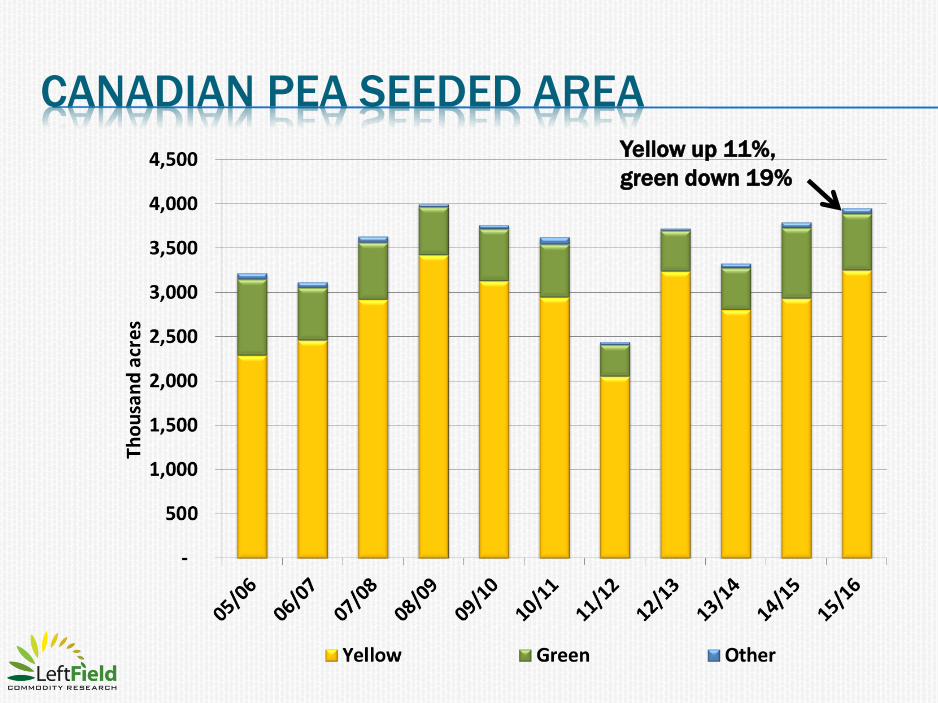

CANADIAN PEA SEEDED AREA Yellow up 11%,

green down 19%

CANADIAN PEA SUPPLIES

Not heavy supplies

PEAS – 2015/16

Cdn acreage up 4%, just under 4.0 million acres

Shift back to yellows as price spread shrinks

Other countries will also respond with acres

Strong demand from India for 1st half, at least

China is key unknown

Yellow prices likely stronger into 2015/16

Greens steady in 2015

Less support for feeds

28

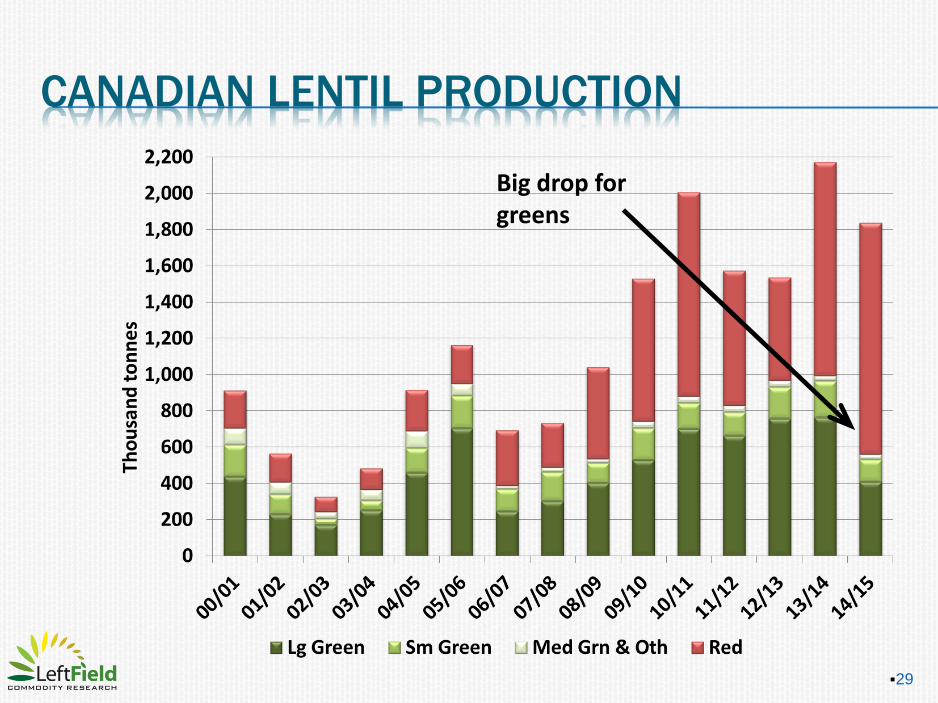

CANADIAN LENTIL PRODUCTION

29

Big drop for greens

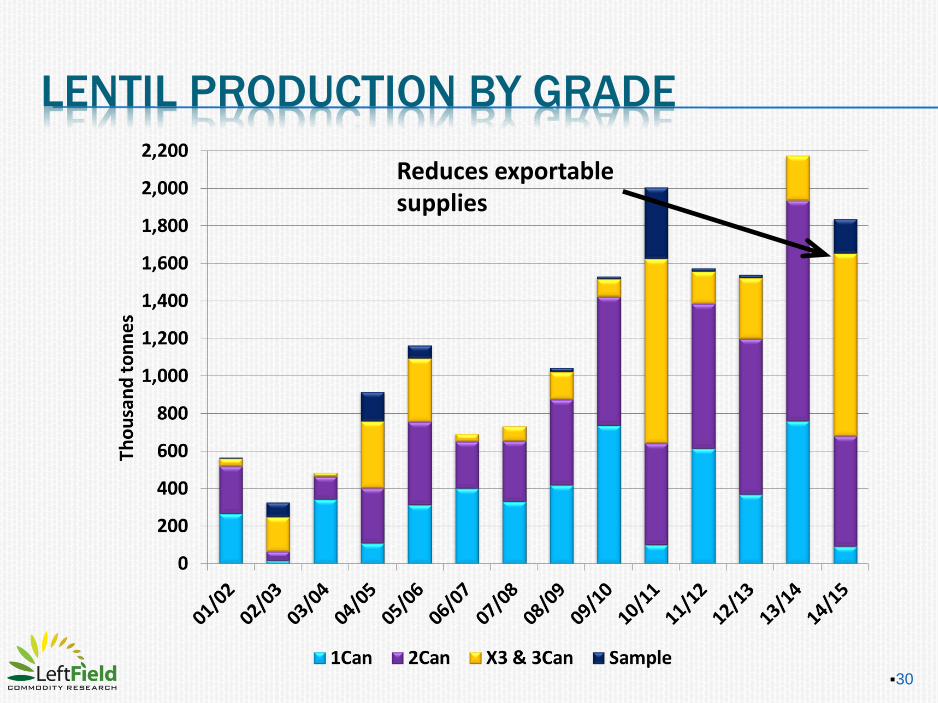

LENTIL PRODUCTION BY GRADE

30

Reduces exportable supplies

CANADIAN 2014/15 LENTIL EXPORTS

31

Record month in October

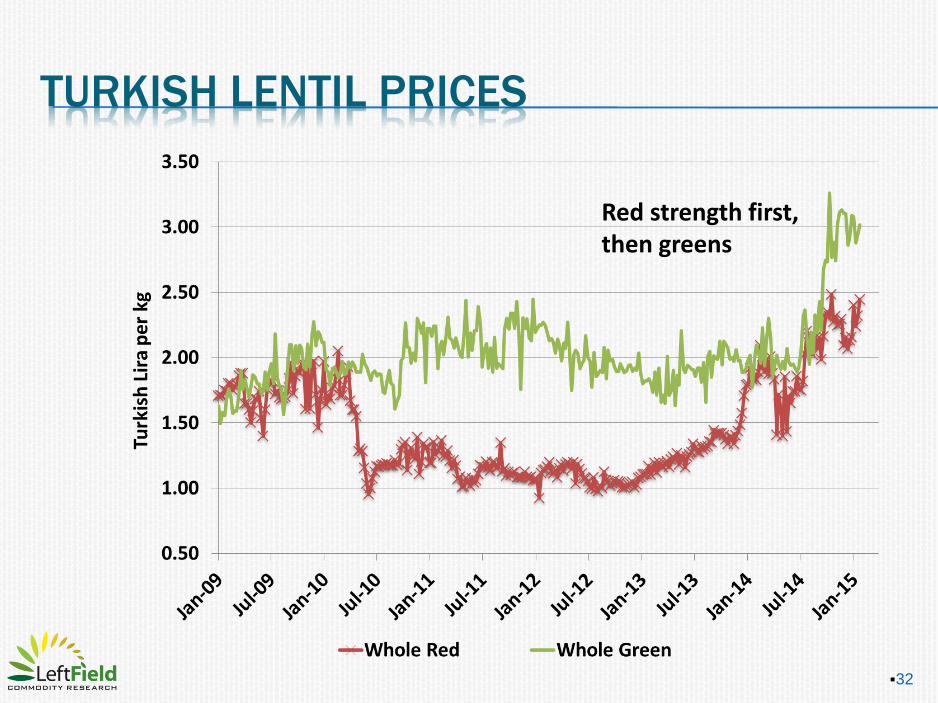

TURKISH LENTIL PRICES

32

Red strength first, then greens

INDIAN LENTIL & PIGEON PEA PRICES

33

Record highs

AVERAGE SASKATCHEWAN LENTIL BIDS

34

Trying to find the highs

CANADIAN LENTIL ENDING STOCKS

35

Very limited supplies

LENTILS – REST OF 2014/15

Reds

Reduced Canadian supplies

Strong demand from India and Turkey

New-crop harvests coming – India and Turkey

Could soften market a bit (Feb and following)

Greens

Small poor quality crop with limited carryover

Firm prices through 14/15

No new harvest till next fall, but more Canadian acres

expected (seed?)

36

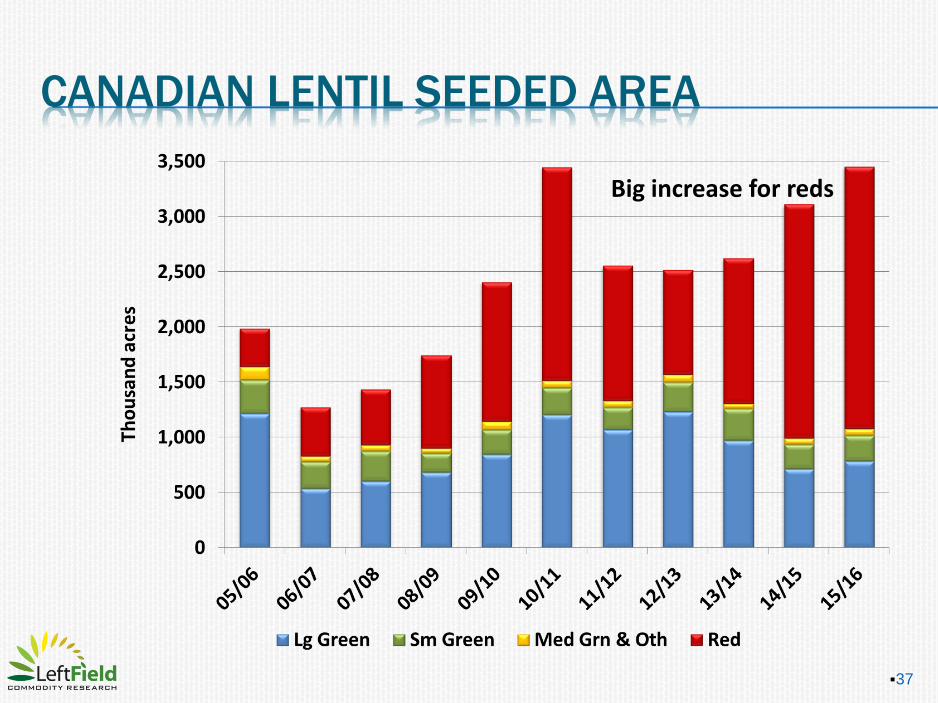

CANADIAN LENTIL SEEDED AREA

37

Big increase for reds

CANADIAN LENTIL SUPPLIES

38

Comfortable but not heavy

LENTILS – 2015/16

Expect 11% more Canadian acres in 2015

Seed supplies, root rot caution

Other countries will also respond with acres

Need all that production to replenish supplies

Especially large and small greens

Red lentil demand firm, at least first half of 15/16

Turkey could slip depending on crop

Prices off the highs but historically strong

39

CANADIAN CHICKPEA SUPPLIES

40

Lots of carryover

TURKISH CHICKPEA PRICES

41

Smaller calibre weaker

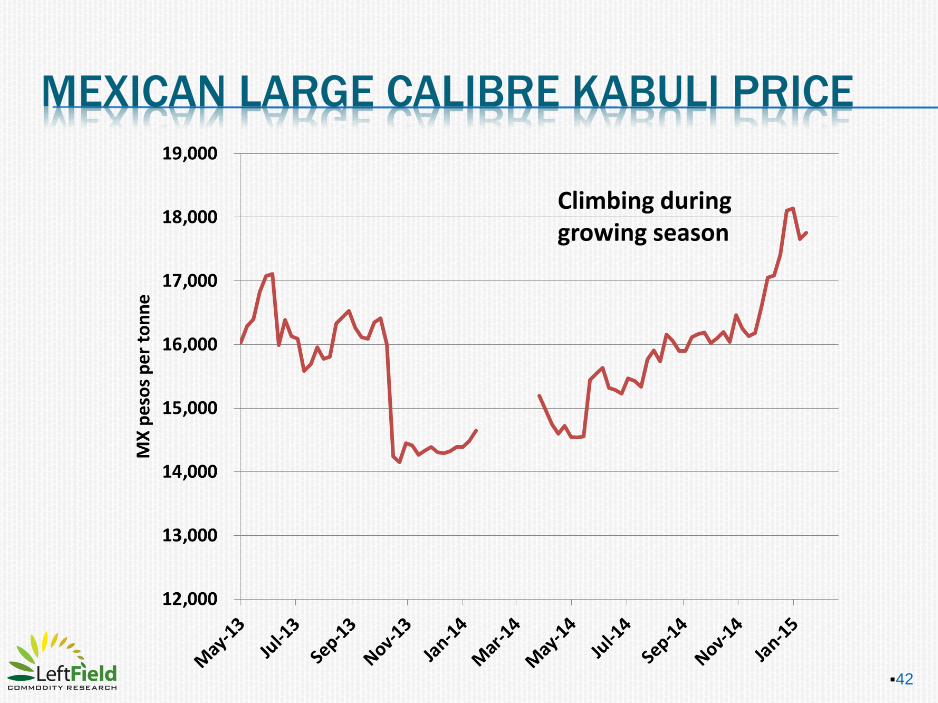

MEXICAN LARGE CALIBRE KABULI PRICE

42

Climbing during growing season

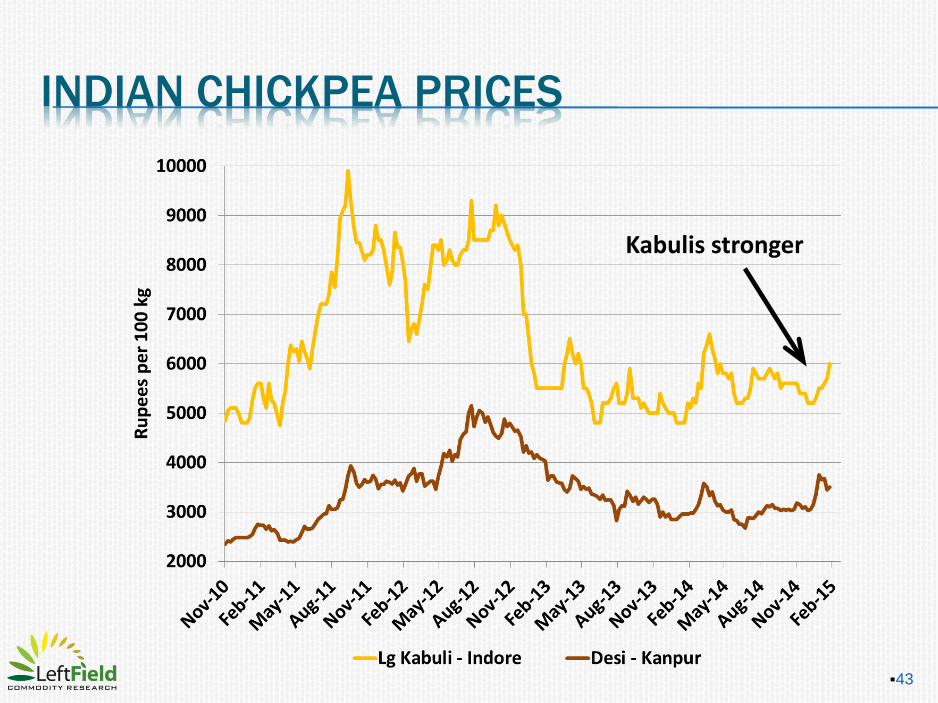

INDIAN CHICKPEA PRICES

43

Kabulis stronger

CHICKPEAS – REST OF 2014/15

Bullish factors

Fewer acres in India

Smaller crop in Australia

More North American consumption

Bearish factors

Mexican crop still uncertain

Heavy North American supplies

Slow export pace

44

CHICKPEAS – 2015/16

Cdn acreage down 10%

Large N Am supplies will hang over the market

Smaller Indian crop will help export demand

Steady to higher prices but no windfall

45

CANADIAN DRY BEAN PRODUCTION

46

Small recovery in crop

US DRY BEAN PRODUCTION

47

Solid bounce in production

US BEAN EXPORTS TO MEXICO

48

Two years of good Mexican crops

US DRY BEAN BIDS

49

Blacks showing a bit of bounce

DRY BEANS – REST OF 2014/15

Bullish factors

Stronger demand from MENA

Quality problems elsewhere

Questions about Brazilian crop

Bearish factors

Larger North American crops

Reduced Mexican demand

Rebound in S American crops

50

DRY BEANS –2015/16

Reduced North American acres (down ~ 5%)

Response to lower prices

Tighter supplies

More competition in export markets

Steady to slightly higher with variability between

classes

51

CANADIAN FABABEAN ACREAGE

52

A “small” increase

CANADIAN FABABEAN EXPORTS

53

Early response

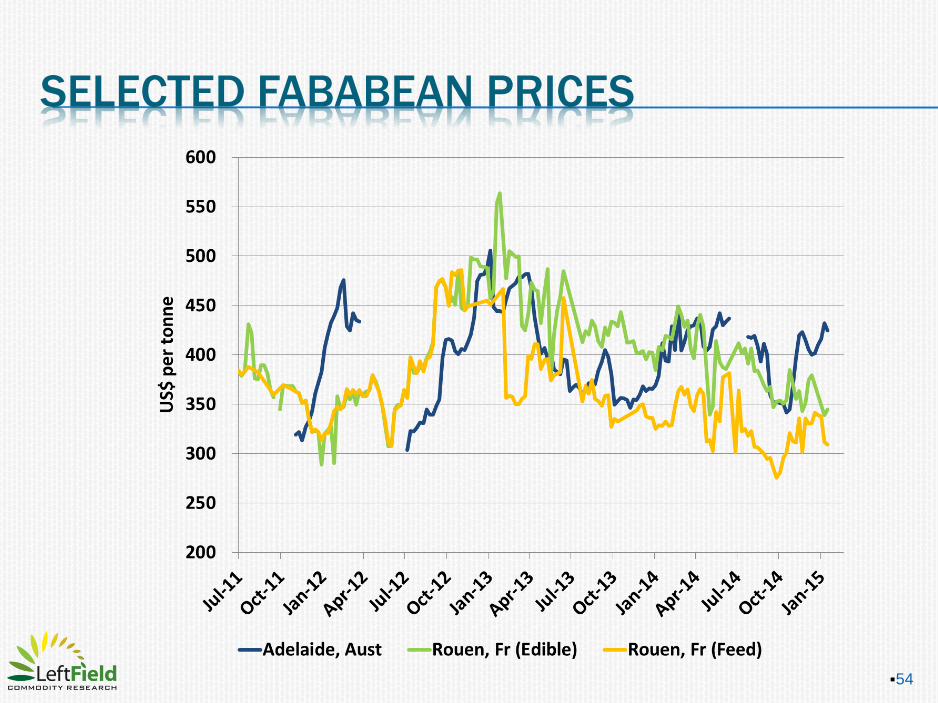

SELECTED FABABEAN PRICES

54

FABABEAN OUTLOOK

Bullish factors

Growing demand from MENA

Solid feed demand

Weaker Canadian dollar

Support from pea market

Bearish factors

Increased acres in Canada, Australia and Europe

Production subsidies in France

Vulnerable soymeal markets

55

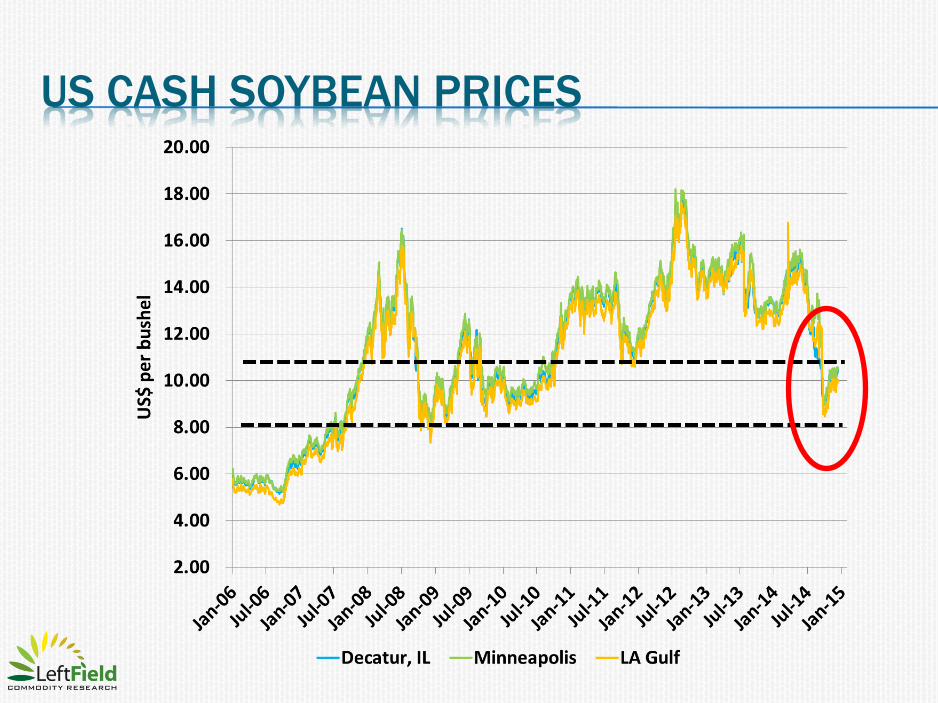

US CASH SOYBEAN PRICES

GLOBAL SOYBEAN PRODUCTION & USE

GLOBAL SOYBEAN ENDING STOCKS

US SOYBEAN ENDING STKS & FARM PRICE

THANK YOU!

www.leftfieldcr.com