Published by Raymond James & Associates PESA Oil … · Published by Raymond James & Associates ......

60

U.S. Research September 2016 Please read disclosure/risk information and Analyst Certification beginning on slide 57. Published by Raymond James & Associates Raymond James Energy Group (800) 945-6275 Raymond James Energy Group (800) 945-6275 Energy Markets We are at the Tail End of a Supply Driven Downturn PESA Oil and Gas 101 [email protected] [email protected] © 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved. International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Transcript of Published by Raymond James & Associates PESA Oil … · Published by Raymond James & Associates ......

U.S. Research

September 2016

Please read disclosure/risk information and Analyst Certification beginning on slide 57.

Published by Raymond James & Associates

Raymond James Energy Group(800) 945-6275

Raymond James Energy Group(800) 945-6275

Energy Markets

We are at the Tail End of a Supply

Driven Downturn

PESA Oil and Gas 101

[email protected]@RaymondJames.com

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 2

We turned bearish on crude in mid-2012

Worried about surging U.S. supply

Numbers said $65 was correct

equilibrium oil price

We were wrong for two years as OPEC

supply fell by 2.5 million bpd

Oil prices fell when outages stabilized

Published by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

RJ Energy Outlook: Historical Perspective

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Supply Interruptions Important…

3

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 4

♦ OPEC flooding the market (Saudi, Iraq, Iran)

♦ U.S. supply posting huge growth

First time in 40 years

♦ Supply was the problem

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Why Did Energy Prices Collapse in 2014/15?

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 5

• Very bullish on oil prices relative to futures strip:

Crude prices move much higher in 2017

• Natural gas rebounds in in 2017: N.E. gas keeps a

lid long-term prices – volatile differentials

• Oilfield has overcorrected in 2015/16: Expect a

sharp rebound in 2017/18

Current Energy Overview

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

U.S. ResearchPublished by Raymond James & Associates

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 6

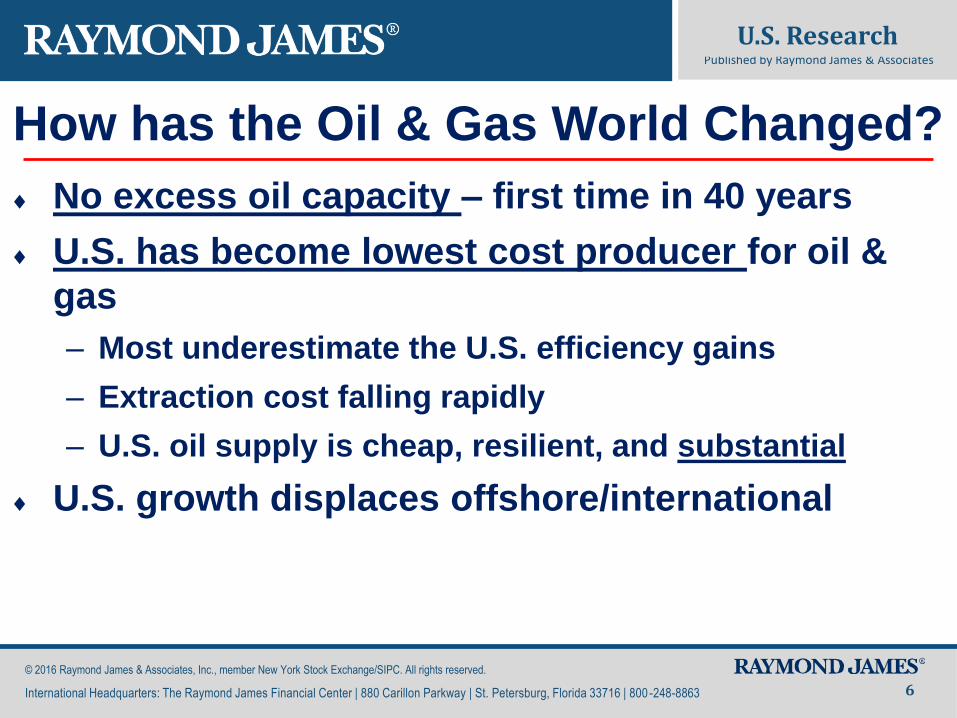

No excess oil capacity – first time in 40 years

U.S. has become lowest cost producer for oil &

gas

– Most underestimate the U.S. efficiency gains

– Extraction cost falling rapidly

– U.S. oil supply is cheap, resilient, and substantial

U.S. growth displaces offshore/international

Published by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

How has the Oil & Gas World Changed?

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 7

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Problem #1: Iraq’s Production Surge

2.69

2.92

3.073.12

3.03

3.16

3.043.08

3.293.33

3.22

3.48 3.5

3.94

4.25 4.28 4.28 4.294.35

4.404.45 4.45 4.45 4.45

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16E 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E

Iraq Crude Production, 2012-2017E (MMbpd)

IEA Reported Iraq Crude Production Raymond James ForecastSource: IEA, Bloomberg, Raymond James Research

Up ~1 million bpd!

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 8

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

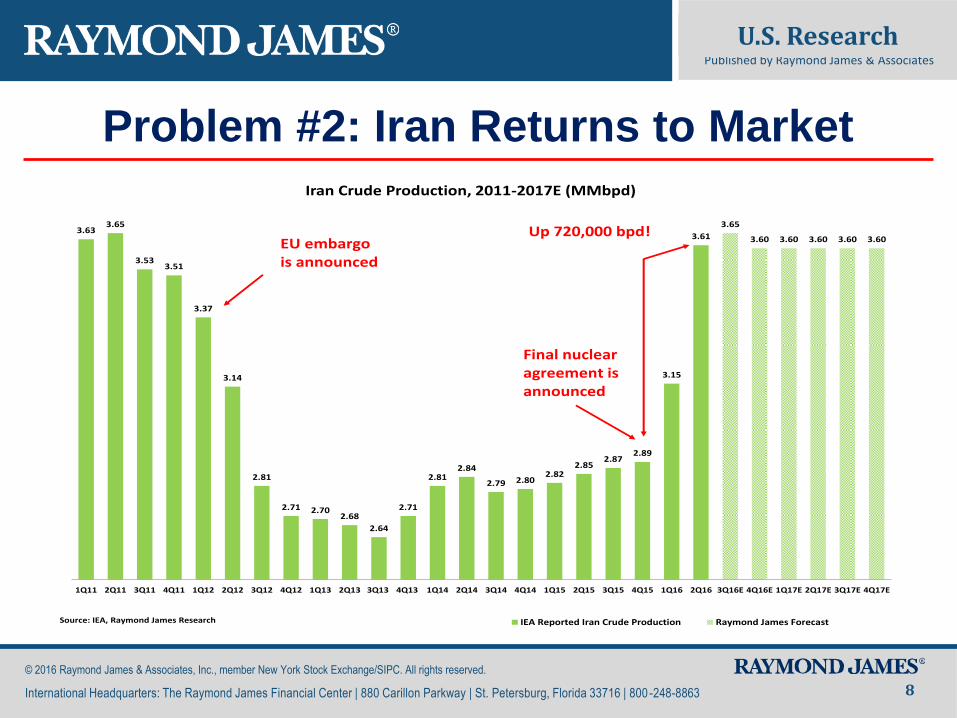

Problem #2: Iran Returns to Market

3.633.65

3.533.51

3.37

3.14

2.81

2.71 2.702.68

2.64

2.71

2.812.84

2.79 2.802.82

2.852.87

2.89

3.15

3.61

3.65

3.60 3.60 3.60 3.60 3.60

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16E 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E

Iran Crude Production, 2011-2017E (MMbpd)

IEA Reported Iran Crude Production Raymond James ForecastSource: IEA, Raymond James Research

EU embargois announced

Final nuclear agreement is announced

Up 720,000 bpd!

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 9

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Problem #3: Saudi Production Surged

8.55

8.9

9.34 9.37

9.65

9.77

9.6

9.23

8.99

9.27

9.82

9.49 9.469.5

9.629.53

9.77

10.29 10.2710.18 10.21

10.31

10.60

10.35

10.25

10.35

10.65

10.40

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16E 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E

Saudi Arabia Crude Production (excl. Neutral Zone), 2011-2017E (MMbpd)

IEA Reported Saudi Arabia Crude Production Raymond James ForecastSource: IEA, Raymond James ResearchSource: IEA, Raymond James ResearchSource: IEA, Raymond James Research

Up ~800,000 bpd!

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 10

If they have it, …

Why haven’t we seen it?

Published by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Does Saudi Really Have 2 MMbpd More?

275,000

285,000

295,000

305,000

315,000

325,000

335,000

Sau

di C

rud

e O

il In

ven

tori

es

(Mb

bls

)

Saudi Crude Oil Inventories

Source: JODI

Why Are Saudi OilInventories Falling?

Why are Saudi

inventories

falling?

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

The Oil Truck Has No Shock Absorbers

U.S. ResearchPublished by Raymond James & Associates

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 11

0

2

4

6

8

10

12

14

16

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016E

Excess C

ap

acit

y(M

Mb

ls/d

ay)

Excess OPEC Capacity

OPEC Excess CapacitySources: IEA, RJ&A, Bloomberg

16 MMBbls/d in '83 v.s. Almost None Today

15 Yr Bear Market For Oil

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 12

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Total OPEC and U.S. Production

6.00

8.00

10.00

12.00

14.00

16.00

18.00

30.00

32.00

34.00

36.00

38.00

40.00

42.00

Tota

l U.S

. Cru

de

Pro

du

ctio

n in

mm

bp

d

To

tal O

PEC

Cru

de

Pro

du

ctio

n in

mm

bp

d

OPEC and U.S. Total Oil Production

OPEC United States - total

Forecast

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 13

Efficiency Gains are Driving Growth

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

-

2,000

4,000

6,000

8,000

10,000

12,000

-

200

400

600

800

1,000

1,200

Mar

-07

Jul-

07

No

v-0

7

Mar

-08

Jul-

08

No

v-0

8

Mar

-09

Jul-

09

No

v-0

9

Mar

-10

Jul-

10

No

v-1

0

Mar

-11

Jul-

11

No

v-1

1

Mar

-12

Jul-

12

No

v-1

2

Mar

-13

Jul-

13

No

v-1

3

Mar

-14

Jul-

14

No

v-1

4

Mar

-15

Jul-

15

No

v-1

5

Mar

-16

Nat

ura

l gas

Pro

du

ctio

n (

Mcf

/day

)

Oil

Pro

du

ctio

n (

Bb

l/d

ay)

Production by Rig by PlayBakken

Eagle Ford

Niobrara

Permian

Marcellus*

Utica*

Haynesville*

Marcellus*

Bakken

Utica*

Eagle Ford

Niobrara

Haynesville*

Permian

* On Secondary AxisSources: EIA and Raymond James Research

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Well Productivity Growth Should Slow in 2017/18

14

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

37%

35%

31%

38%

36%

14%

7%

0

100

200

300

400

500

600

700

20

11

20

12

20

13

20

14

20

15

E

20

16

E

20

17

E

20

18

E

IP-3

0s

(Bp

d/w

ell)

U.S. Oil Productivity Gains

Sources: EIA, HPDI, and Raymond James Research

Moving up the Learning Curve:1. Shift from Verticals to Horizontals2. Longer Laterals3. More Stages

Accelerating Efficiencies:1. Continued Trends from Previous Years2. High-grading to Most Productive Portions of the Plays

Decelerating Efficiencies:1. Previous Trends Contribute Less Growth2. Low-grading to Fringe Portions of the Plays

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 15

U.S. Oil Growth Potential Still Staggering!

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

Source: HPDI, EIA, Raymond James Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

Jan

-19

85

May

-19

86

Sep

-19

87

Jan

-19

89

May

-19

90

Sep

-19

91

Jan

-19

93

May

-19

94

Sep

-19

95

Jan

-19

97

May

-19

98

Sep

-19

99

Jan

-20

01

May

-20

02

Sep

-20

03

Jan

-20

05

May

-20

06

Sep

-20

07

Jan

-20

09

May

-20

10

Sep

-20

11

Jan

-20

13

May

-20

14

Sep

-20

15

Jan

-201

7

May

-20

18

Sep

-20

19

Long-Term U.S. Crude Production Forecast

Forecast

MMBbl/d

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

8,500

9,000

9,500

10,000U.S. Oil Production (MBbl/d)

Total U.S. Crude

MBbl/d

Source: EIA, HPDI, Raymond James Research

U.S. Oil Supply Bottoms in Late-2016

16

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Estimates

* Assuming 500 Average

U.S. Rigs in 2016

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

What is U.S. Supply Sensitivity to Activity?

17

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

U.S. Rigs U.S. Oil Supply Growth

U.S. Rig Count Forecast Y/Y

Change

Rig Count Assumption Y/Y % ∆

0% -20% Base +20% Base

2014 1,858 6%

2015 976 -47%

2016E 406 507 608 -48%

2017E 640 800 960 58%

2018E 880 1,100 1,320 38%

Source: EIA, HPDI, Raymond James

U.S. Liquids Production Growth

(y/y growth in MBbl/d)

Impact from Rig Count Change

0% -20% Base +20%

2014 1,665

2015 966

2016E (426) (337) (234)

2017E (171) 222 631

2018E 767 1,127 1,490

Source: EIA, HPDI, Raymond James Research

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Rig Count Largest Driver of Production Changes

18

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Consensus?

Impossible Rig Count

-600

-400

-200

0

200

400

600

800

1000

400 500 600 700 800 900 1000 1100 12002017 Average Rig Count

2017 Y/Y U.S. Liquids Production Growth Under Various Rig Count Scenarios

Source: RJ Estimates, EIA, Drilling InfoAssumes 2016 rig count remains unchanged from current estimateAssumes oil rig percentage of 80%

MBbl/d

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 19

U.S. Oil Service Industry is Dying at “Strip” Prices

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

Cas

h F

low

in M

illio

ns

U.S. Oilfield Cash Flow and Capex

Operating Cash Flow Total Capex

Source: Raymond James Research; Spears & Associates; EIA; Company Reports; Bloomberg

U.S. E&P Capex

U.S. E&P Cash Flows

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 20

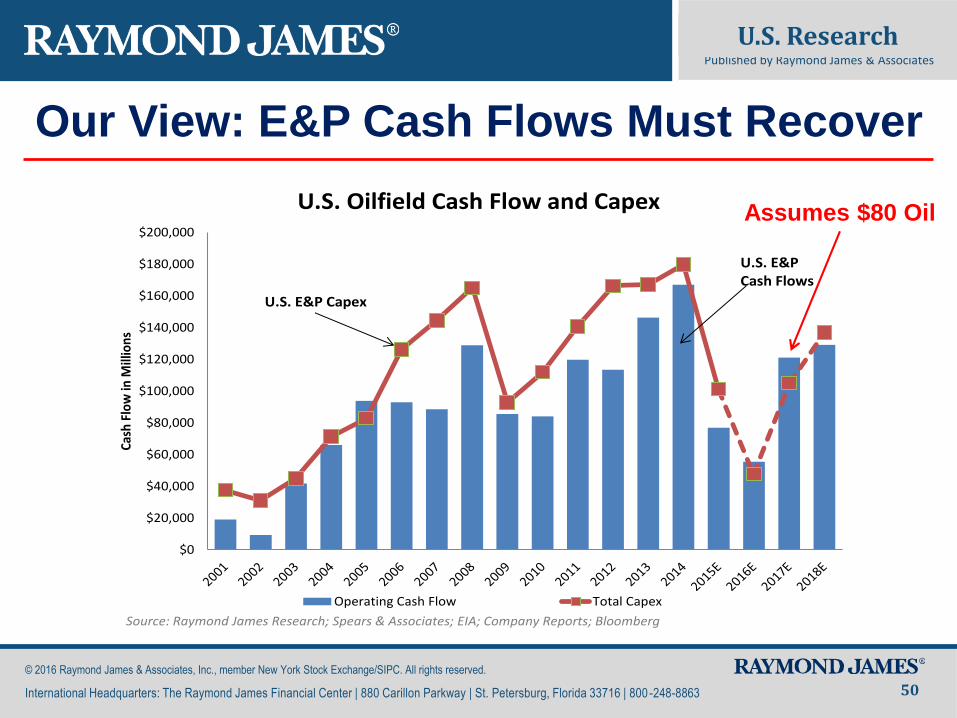

E&P Cash Flows Must Recover

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

Cash

Flo

w in

Mill

ion

s

U.S. Oilfield Cash Flow and Capex

Operating Cash Flow Total Capex

Source: Raymond James Research; Spears & Associates; EIA; Company Reports; Bloomberg

U.S. E&P Capex

U.S. E&P Cash Flows

Assumes $80 Oil

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

U.S. ResearchPublished by Raymond James & Associates

Non-U.S. Supply Assumptions Very Conservative

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 21

Sources: IEA, Raymond James Research

1,181 1,179

1,026

1,375

2016E 2017E 2018E 2019E

MB

bls

/d

Oil Project Delays and Cancellations, by Start Year

466

-739

-90

75

2015 2016E 2017E 2018E

MB

bls

/d

Non-OPEC/Non-U.S. Y/Y Oil Production Change

Source: IEA, Raymond James estimates

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 22

Global Capex Down 30+% Two Years in a Row ?

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Source: IEA, Raymond James Research

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

2010 2011 2012 2013 2014 2015 2016E

$ M

M

Capital Spending of Large-Cap Oil and Gas Companies

Based in the U.S.

Based Outside the U.S.

Source: Company filings, Raymond James research

Global Spending Down +/- 50%!

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 23

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Geopolitical Disruption

Nigeria Venezuela

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 24

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Structural Declines

China Colombia

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 25

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Structural Declines (Continued)

Angola Mexico

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

OIL DEMAND HAS

NOT BEEN THE PROBLEM

26

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 27

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

19

60

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15E

Oil Consumption Intensity - China vs. India

China India

Bb

ls o

f O

ilp

er

$1,0

00

GD

P

Source: EIA, IEA, IMF, World Bank

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

19

60

19

64

19

68

19

72

19

76

19

80

19

84

19

88

19

92

19

96

20

00

20

04

20

08

20

12E

Oil Consumption Intensity - Select Developed Countries

Germany Japan

U.S. UK

Bb

ls o

f O

ilp

er

$1,0

00 G

DP

(2000$)

Source: EIA, IEA, World Bank, CIA World Factbook

Japan

U.S.

UK

Germany

Long-Term Efficiency Trends Are Real, But…

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 28

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Cheap Gasoline is Slowing U.S. Efficiency Trend

22.5

23.0

23.5

24.0

24.5

25.0

25.5

26.0

Average MPG for New Vehicles Sold

Source: University of Michigan Transportation Research Institute

Downward trend after oil price crash

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 29

Driving Trends Are Changing

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

175

200

225

250

275

Ve

hic

le-m

ile

s (i

n b

illio

ns)

U.S. Vehicle-Miles Traveled (Monthly Average)

Source: U.S. Department of Transportation

Vehicle miles driven up3.5% in 2015, and up 3.3% YTD 2016!

Why the Stagnation?

- Urbanization?

- Demographics?

- Low Employment?

- High Gasoline Prices?

- Internet?

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

2016 Gasoline Prices Lower Than 2015

Published by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 30

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

2012 2013 2014 2015 2016E 2017E

Average Annual Gasoline Price

Source: EIA, RJ Research

Down ~28%

Down ~24%

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

-0.18%

2.70%2.57%

1.50%

2005-2014 Average 2015 Actual 2016 YTD Actual 2016 RJ Estimate

2016 U.S. Gasoline Demand (% Change)

Source: EIA

So, U.S. Gasoline Demand Is Responding!

Published by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 31

Too Low?

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 32

Gasoline Now “Driving” Chinese Demand

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Gasoline19%

Jet Fuel4%

Diesel36%

Fuel Oil13%

Other (Naphtha, Heating Oil, LPG,

Asphalt, Miscellaneous)

28%

2006 Chinese Oil Demand Breakdown

Total average annual oil demandwas 7.2 MMBbls/d

Middle class transportation accounts for ~23%

Source: Bloomberg, IEA, National Bureau of Statistics of China, Raymond

Gasoline26%

Jet Fuel6%

Diesel34%

Fuel Oil5%

Other (Naphtha,

Heating Oil, LPG, Asphalt,

Miscellaneous)29%

2015 Chinese Oil Demand Breakdown

Total average annual oil demand was 11.24 MMBbls/d

Middle classtransportation accounts for ~32%

Source: Bloomberg, IEA, National Bureau of Statistics of China, Raymond

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 33

China Oil Demand Problem Overstated !

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

0.89

0.48

0.59

0.44

0.36

0.63

0.37

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Chinese Demand Growth by Product (Million Bpd)

Other

Middle Class Transportation (Gas/Jet)

Estimates

Total

Source: Bloomberg, IEA, National Bureau of Statistics of China, RJ Research

0.29

Transportation accounts for 66% of 3 yr avg. growth

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Chinese SUV Sales Steadily Climbing

34

Published by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

China SUV Sales

Source: National Bureau of Statistics of China, Bloomberg

Average annual growth of almost 37% from 2011 through 2015.

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 35

Lower Oil Prices Have Stimulated Demand

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

Source: IEA, Raymond James Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

70

75

80

85

90

95

100

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

E

Global Oil Demand

"Old School"

1.0 MMBPD Y/Y Growth

$100 Oil

1.4 MMBPD Y/Y Growth

1.5 MMBPD Y/Y Growth

$55 Oil

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 36

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

We Think Global Oil Demand is Stout!

Region 2015 2016E 2017E 2018E

North America 0.9% 1.0% 0.0% 0.0%

Europe 1.9% 0.4% -1.0% -1.0%

Pacific (mainly Japan) -0.3% 0.0% -1.0% -1.0%

CIS (mainly Russia) -1.0% 1.8% 0.5% 0.5%

China 6.4% 3.2% 2.5% 2.5%

Other Asia 4.1% 4.9% 3.7% 3.7%

Latin America -0.7% -0.7% 1.0% 1.0%

Middle East 1.8% 0.8% 2.0% 2.0%

Africa 3.7% 2.6% 1.9% 1.9%

Total Demand Growth* (Jan. 2016) 1.8 MMbpd 1.4 MMbpd 1.2 MMbpd 1.2 MMbpd

Total Demand % Growth* (Jan. 2016) 2.0% 1.4% 1.2% 1.2%

Total Demand Growth* (Current) 1.8 MMbpd 1.7 MMbpd 0.9 MMbpd 1.0 MMbpd

Total Demand % Growth* (Current) 2.0% 1.8% 0.9% 1.0%

IEA Estimate (MMbpd) 1.9 MMbpd 1.2 MMbpd 1.2 MMbpd

IEA Estimate (%) 2.0% 1.3% 1.3%

Source: IEA, IMF, Raymond James research * After missing barrels

Oil Demand: Year-Over-Year Changes

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 37

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Where Does That Leave Our Global Oil Model?(Assumes No Additional Interruptions)

Source 2014A 2015A 2016E 2017E 2018E

Previous Year Build/Draw -0.7 0.4 1.4 -0.3 -0.6

U.S. Supply Growth 1.8 1.0 -0.3 0.3 1.2

Other Non-OPEC Non-U.S. -0.2 0.5 -0.6 -0.1 0.1OPEC Supply Growth 0.7 1.3 1.0 0.4 0.2

Saudi Arabia 0.1 0.6 0.2 0.0 0.0

Iraq 0.3 0.7 0.3 0.1 0.0

Iran 0.1 0.0 0.6 0.1 0.0

Total Global Supply 2.4 2.8 0.0 0.6 1.4

RJ Demand (incl. "Missing Bbls") 1.2 1.8 1.7 0.9 1.0

IEA Demand Estimate 1.3 1.6 1.4 1.3 N/A

Inventory Build Est. 0.4 1.4 -0.3 -0.6 -0.2

Source: IEA, Raymond James research

Current Model

Oil Supply-Demand: Year-Over-Year Changes

(MMbpd)

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

0.42

1.42

-0.28

-0.58

-0.25

-0.7

-0.4

-0.1

0.2

0.5

0.8

1.1

1.4

2014 2015 2016E 2017E 2018E

Impl

ied

Build

(Dra

w) -

Aft

er M

issi

ng B

arre

ls (M

Mbp

d)

Est. Quarterly Global Petroleum Inventory Builds (Draws)

CurrentBuild (Draw) Est.

Source: IEA, Raymond James research

38

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Supply Cycle’s Final Stages?

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Bearish:

• Will U.S. Efficiency Gains Continue?

• Does Saudi Have More Capacity?

• Hyperbolic U.S. $ Risk?

Bullish:

• Will OPEC Cut?

• Non-US, Non-OPEC Supply Decline?

• Middle East Production Risk Still Exists!

U.S. ResearchPublished by Raymond James & Associates

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Where Could We Be Wrong on Oil?

39

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 40

Gas Should Rally in 2017—

Plenty of U.S. Gas Sub-

$3.00 Long-Term

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

-2.1-2.6

-0.8-0.7-0.7

-0.3-0.2

0.10.5

1.51.4

-3.0 -2.5 -2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

TotalWeatherMexicoCanada

LNGLiquids

IndustrialBase Power

Nuke/HydroCswitching

Supply

Bcf/day

2017 Nov/Nov Theoretical Change in StorageTIGHTER LOOSER

BULLISH BEARISH

Ending Storage Estimates: Winter: 1,931 Bcf Summer: 3,761Bcf

Source: HPDI, EIA, Raymond James Estimates

2017 Gas Outlook Very Bullish

U.S. ResearchPublished by Raymond James & Associates

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 41

This assumes

$3.25 Gas

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Pipelines Are Key to U.S. Gas Supply

U.S. ResearchPublished by Raymond James & Associates

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 42

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

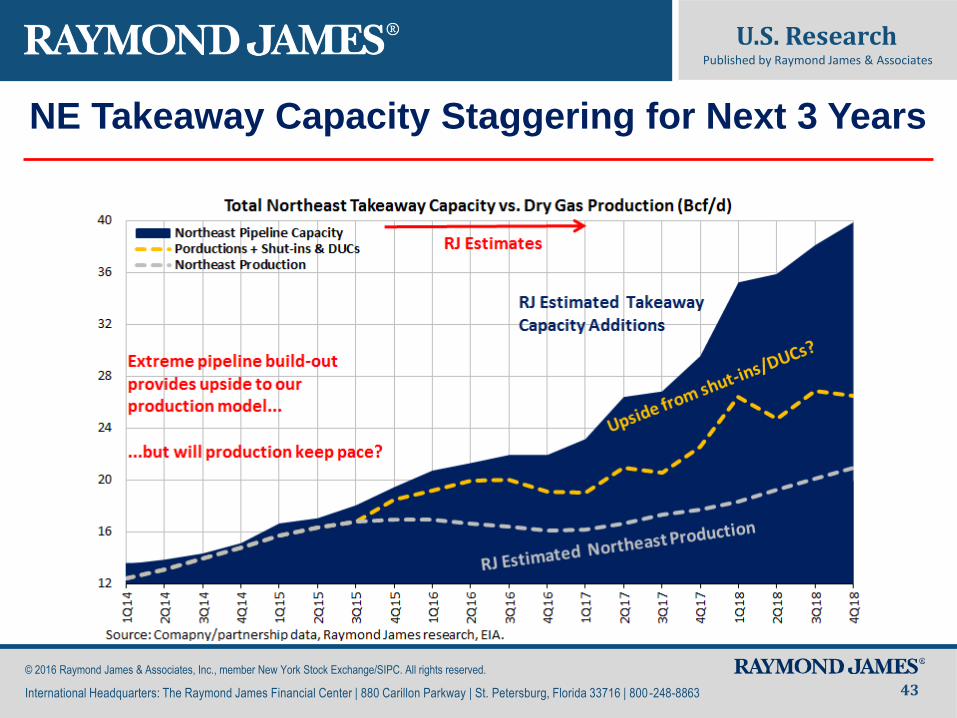

Total Dry Gas Production Y/Y Growth

Dry Gas Plays Wet Gas Plays Oil Plays Other NE Pipe Adds Total DUCs and Shut-ins

Source: HPDI, EIA, Raymond James Estimates

Bcf/d

Production from dry gas plays rolls over in mid-2016

Associated gas production

Planned Northeast pipeline additions are not incorporated into our model and help boost production in 2016 and 2017.

gas production from non-major plays

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

NE Takeaway Capacity Staggering for Next 3 Years

43

U.S. ResearchPublished by Raymond James & Associates

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 44

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Northeast Price Differentials Improve, For Now

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Demand Tailwinds Exist for Gas

45

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

LNG: 7+ Bcf/d of Potential Exports by 2020

46

U.S. ResearchPublished by Raymond James & Associates

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

0

2

4

6

8

3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Bcf

/d

U.S. LNG Export Forecast (Bcf/d)

Cameron LNG Corpus Christi Cove Point Elba Island Freeport Sabine PassSource: Company reports, Raymond James research

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 47

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Natural Gas Rally in 2017!

2016 Q1 16A Q2 16A Q3 16E Q4 16E 2016E

Bloomberg Consensus $2.01 $2.13 $2.33 $2.50 $2.24

NYMEX Futures $2.01 $2.13 $2.91 $3.12 $2.54

Old RJ Gas $2.01 $2.13 $2.05 $2.30 $2.12

New RJ Gas $2.01 $2.13 $2.75 $3.00 $2.47

2017 Q1 17E Q2 17E Q3 17E Q4 17E 2017E

Bloomberg Consensus $2.90 $2.80 $2.90 $3.05 $2.91

NYMEX Futures $3.41 $3.05 $3.08 $3.17 $3.18

Old RJ Gas $2.70 $2.60 $2.55 $2.75 $2.65

New RJ Gas $3.50 $3.25 $3.00 $3.25 $3.25

2018 Q1 18E Q2 18E Q3 18E Q4 18E 2018E

Bloomberg Consensus $3.00 $3.00 $3.00 $3.00 $3.00

NYMEX Futures $3.34 $2.86 $2.90 $3.00 $3.02

Old RJ Gas $2.50 $2.50 $2.50 $2.50 $2.50

New RJ Gas $3.25 $3.00 $2.75 $3.00 $3.00

2019 (+) Long-Term Forecast

Bloomberg Consensus $3.01

NYMEX Futures $3.24

Old RJ Gas $2.50

RJ Long-Term Gas $2.50

Source: Bloomberg, Thomson Reuters, Raymond James research

RJ&A Henry Hub Natural Gas Price Forecast (as of July 2016)

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

How Will Oilservice Cycle Unfold?

48

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 49

U.S. Oil Service Industry is Dying at “Strip” Prices

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

Cas

h F

low

in M

illio

ns

U.S. Oilfield Cash Flow and Capex

Operating Cash Flow Total Capex

Source: Raymond James Research; Spears & Associates; EIA; Company Reports; Bloomberg

U.S. E&P Capex

U.S. E&P Cash Flows

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 50

Our View: E&P Cash Flows Must Recover

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

Cash

Flo

w in

Mill

ion

s

U.S. Oilfield Cash Flow and Capex

Operating Cash Flow Total Capex

Source: Raymond James Research; Spears & Associates; EIA; Company Reports; Bloomberg

U.S. E&P Capex

U.S. E&P Cash Flows

Assumes $80 Oil

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 51

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

U.S. Supply Constraints

Balance Sheets, Labor, Frac Equipment

4%

5%

6%

7%

8%

9%

10%

U.S. Unemployment Rate, 2006-present

Source: Bureau of Labor Statistics, U.S. Department of Labor

High 2010 unemployment eased search for oil & gas workers in last downturn

This oil & gas downturn, U.S.

unemployment is only 5%

4

6

8

10

12

14

16

18

4Q141Q152Q153Q154Q151Q162Q163Q164Q161Q172Q173Q174Q171Q182Q183Q184Q18

Mil

lio

n H

ors

ep

ow

er

U.S. Pressure Pumping Fleet vs. Demand

Supply Denotes Active and Available HHP with Minimal Incremental CapexSource: Company Reports, IHS, Baker Hughes, Raymond James Research

Pressure Pumpers Regain Pricing Power in 2017 to Incentivize Restoration and Repair of Stacked

Equipment

Implied 2018 HP Shortfall

U.S. Horsepower Supply Range

Frac HP Demand

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 52

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

Legacy Equipment Must be Rebuilt

0

5

10

15

20

Mill

ion

Ho

rse

po

we

r

U.S. Pressure Pumping Fleet

Source: Company Reports, Raymond James Estimates

Marketable Legacy Equipment

Stacked, Refurbishable

Permanently Retired

Newbuilds

Refurbs

Black line designates total marketable equipment

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 53

Offshore Will Take Much Longer

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

0

50

100

150

200

250

300

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16E 2Q16E 3Q16E 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 1Q18E 2Q18E 3Q18E 4Q18E

Floater Supply vs. Demand

Sources: IHS Petrodata, RJ Estimates

Already Contracted Rigs

Idled Capacity and Potential Stacking

Contracted Newbuilds

Incremental Demand

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

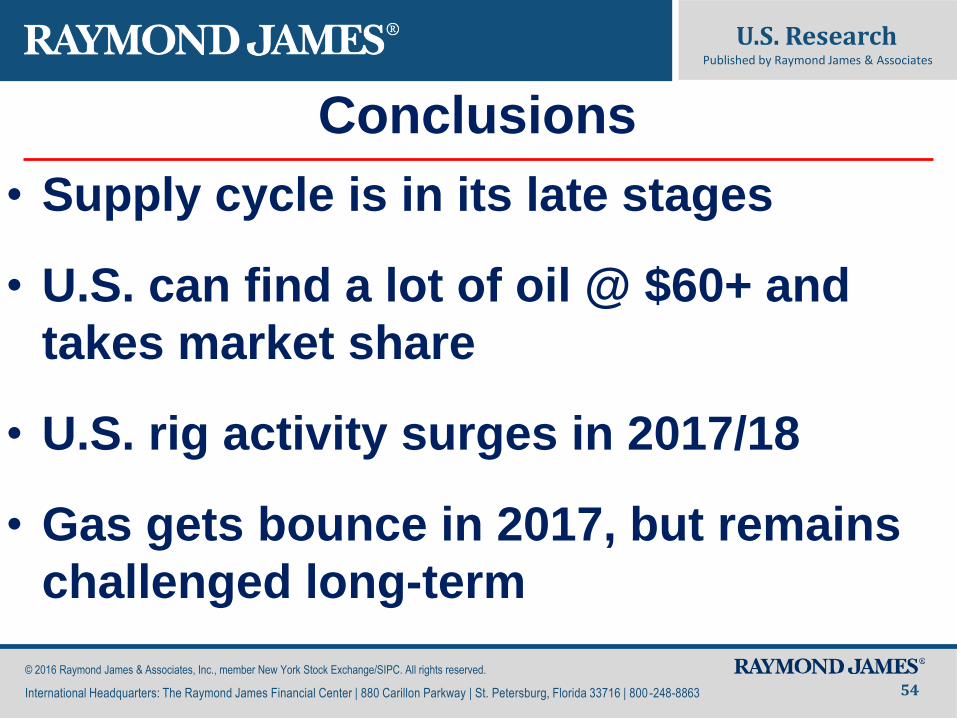

Conclusions

• Supply cycle is in its late stages

• U.S. can find a lot of oil @ $60+ and

takes market share

• U.S. rig activity surges in 2017/18

• Gas gets bounce in 2017, but remains

challenged long-term

54

U.S. ResearchPublished by Raymond James & Associates

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 55

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

World Oil Supply 365 365 90 91 92 92 365 90 91 92 92 365 365 (Mill ions of barrels per day)

SUPPLY 2014 YOY% 2015 YOY% 1Q16 2Q16E 3Q16E 4Q16E 2016E YOY% 1Q17E 2Q17E 3Q17E 4Q17E 2017E YOY% 2018E YOY%

United States - non-bio 11.99 17.2% 12.94 7.9% 12.77 12.62 12.33 12.25 12.49 -3.5% 12.36 12.57 12.85 13.23 12.75 2.1% 14.16 11.0%

United States - bio 1.02 2.8% 1.05 2.8% 1.05 1.11 1.11 1.12 1.10 4.8% 1.12 1.13 1.13 1.14 1.13 3.2% 1.13 0.0%

North America 20.09 10.9% 20.97 4.4% 20.94 20.16 20.49 20.45 20.51 -2.2% 20.67 20.32 21.05 21.48 20.88 1.8% 22.26 6.6%

Europe 3.33 0.3% 3.46 4.0% 3.62 3.35 3.17 3.44 3.39 -2.0% 3.47 3.22 3.05 3.31 3.26 -3.9% 3.12 -4.4%

Pacific 0.51 4.6% 0.47 -8.3% 0.45 0.45 0.51 0.48 0.47 1.1% 0.43 0.43 0.49 0.46 0.46 -3.5% 0.44 -3.5%

Total OECD 23.93 9.2% 24.90 4.1% 25.00 23.96 24.17 24.37 24.37 -2.1% 24.58 23.98 24.59 25.25 24.60 0.9% 25.82 5.0%

CIS 13.87 0.5% 14.00 0.9% 14.20 13.97 13.92 14.05 14.03 0.3% 14.17 14.06 14.15 14.30 14.17 1.0% 14.49 2.3%

Other Europe 0.14 0.0% 0.14 0.0% 0.14 0.14 0.14 0.14 0.14 0.0% 0.14 0.14 0.14 0.14 0.14 0.0% 0.14 0.0%

China 4.25 1.7% 4.33 1.8% 4.18 4.06 4.05 4.05 4.08 -5.6% 4.03 4.03 4.03 4.03 4.03 -1.4% 4.07 1.0%

Other Asia 2.63 -25.9% 2.73 3.8% 2.75 2.67 2.57 2.68 2.67 -2.3% 2.69 2.63 2.54 2.64 2.62 -1.7% 2.55 -2.6%

Latin America 4.96 6.4% 5.16 4.1% 4.50 5.03 5.19 4.93 4.91 -4.8% 4.39 4.96 5.17 4.93 4.86 -1.0% 4.87 0.1%

Middle East 1.32 -2.9% 1.25 -5.1% 1.27 1.27 1.27 1.27 1.27 1.6% 1.24 1.24 1.24 1.24 1.24 -2.6% 1.21 -2.6%

Africa 2.28 0.1% 2.26 -1.0% 2.17 2.16 2.15 2.13 2.15 -4.6% 2.13 2.11 2.10 2.09 2.11 -2.1% 2.08 -1.2%

Total NON-OECD 29.45 -1.7% 29.86 1.4% 29.21 29.29 29.29 29.25 29.26 -2.0% 28.78 29.17 29.35 29.36 29.17 -0.3% 29.41 0.8%

Other Biofuels 0.66 16.6% 0.67 1.5% 0.70 0.68 0.68 0.68 0.68 2.0% 0.71 0.70 0.70 0.70 0.70 2.0% 0.74 6.8%

Processing Gains 2.21 1.1% 2.24 1.4% 2.27 2.24 2.24 2.24 2.24 0.0% 2.27 2.24 2.24 2.24 2.24 0.0% 2.24 0.0%

Total Non-OPEC 56.25 3.0% 57.67 2.5% 57.18 56.17 56.38 56.54 56.56 -1.9% 56.34 56.08 56.87 57.54 56.70 0.3% 58.21 2.7%

Saudi Arabia 9.53 1.4% 10.13 6.3% 10.21 10.25 10.30 10.20 10.24 1.1% 10.21 10.25 10.30 10.20 10.24 0.0% 10.24 0.0%

Iran 2.81 4.8% 2.86 1.7% 3.15 3.60 3.60 3.60 3.49 22.2% 3.60 3.60 3.60 3.60 3.60 3.1% 3.63 0.8%

Venezuela 1.96 -1.8% 1.90 -3.2% 1.86 1.81 1.79 1.76 1.80 -5.1% 1.74 1.71 1.69 1.66 1.70 -5.9% 1.60 -5.9%

Iraq 3.33 8.2% 3.99 19.9% 4.28 4.30 4.35 4.40 4.33 8.5% 4.40 4.40 4.40 4.40 4.40 1.5% 4.40 0.0%

Nigeria 1.90 -2.7% 1.80 -5.2% 1.76 1.36 1.55 1.65 1.58 -12.3% 1.65 1.75 1.75 1.75 1.73 9.3% 1.63 -5.8%

United Arab Emirates 2.76 -0.1% 2.88 4.4% 2.81 2.81 2.81 2.81 2.81 -2.3% 2.81 2.81 2.81 2.81 2.81 0.0% 2.81 0.0%

Kuwait 2.61 2.3% 2.75 5.4% 2.83 2.70 2.80 2.80 2.78 1.3% 2.80 2.80 2.80 2.80 2.80 0.6% 2.80 0.0%

Libya 0.46 -48.7% 0.40 -12.7% 0.36 0.36 0.36 0.36 0.36 -11.8% 0.36 0.36 0.36 0.36 0.36 0.0% 0.36 0.0%

Angola 1.66 -3.4% 1.76 6.4% 1.77 1.76 1.75 1.74 1.76 -0.3% 1.72 1.70 1.68 1.66 1.69 -3.7% 1.61 -4.7%

Algeria 1.12 -2.8% 1.11 -0.9% 1.10 1.10 1.10 1.10 1.10 -1.1% 1.09 1.09 1.09 1.09 1.09 -1.0% 1.07 -2.0%

Qatar 0.71 -3.4% 0.66 -7.2% 0.66 0.66 0.66 0.66 0.66 0.6% 0.66 0.66 0.66 0.66 0.66 0.0% 0.66 0.0%

Neutral Zone 0.38 -26.1% 0.07 -81.6% 0.00 0.15 0.30 0.30 0.19 166.9% 0.30 0.30 0.30 0.30 0.30 59.0% 0.30 0.0%

Ecuador 0.55 5.7% 0.54 -1.8% 0.54 0.54 0.52 0.53 0.53 -1.8% 0.52 0.52 0.50 0.51 0.52 -3.0% 0.50 -3.0%

Indonesia 0.70 0.69 -1.0% 0.71 0.69 0.69 0.68 0.69 0.5% 0.68 0.68 0.68 0.68 0.68 -1.9% 0.68 0.0%

OPEC Crude 30.48 1.7% 31.55 3.5% 32.06 32.10 32.59 32.60 32.34 2.5% 32.55 32.64 32.62 32.49 32.58 0.7% 32.29 -0.9%

OPEC NGLs 6.50 3.9% 6.68 2.7% 6.77 6.81 6.81 6.81 6.81 2.0% 6.91 6.95 6.95 6.95 6.95 2.0% 7.08 2.0%

Total OPEC 36.98 2.1% 38.23 3.4% 38.83 38.91 39.39 39.41 39.15 2.4% 39.45 39.58 39.57 39.43 39.52 1.0% 39.37 -0.4%

TOTAL SUPPLY 93.23 2.6% 95.90 2.9% 96.01 95.08 95.78 95.95 95.70 -0.2% 95.80 95.66 96.44 96.98 96.22 0.5% 97.58 1.4%

Implied Inv. Build/(Draw)-RJ Est. 0.36 1.17 0.84 -0.64 -1.14 -1.41 -0.60 -0.25 -0.72 -1.62 -1.30 -0.98 -0.61

Implied Inv. Build/(Draw)-After Missing Bbl Adj. 0.22 0.99 0.43 -0.86 -1.36 -1.62 -0.81 -0.46 -0.94 -1.83 -1.51 -1.19 -0.83

Source: IEA, RJ&A Estimates

© 2013 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 56

U.S. ResearchPublished by Raymond James & Associates

U.S. Research

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863

World Oil Demand 365 365 90 91 92 92 365(Mill ions of barrels per day) 3.2%

DEMAND 2014 YOY% 2015 YOY% 1Q16 2Q16E 3Q16E 4Q16E 2016E YOY% 1Q17E 2Q17E 3Q17E 4Q17E 2017E YOY% 2018E YOY%

North America 24.14 0.2% 24.36 0.9% 24.21 24.41 24.85 24.93 24.61 1.0% 24.21 24.17 25.10 24.93 24.61 0.0% 24.61 0.0%

Europe 13.45 -1.2% 13.71 1.9% 13.47 13.63 14.21 13.75 13.77 0.4% 13.34 13.49 14.07 13.61 13.63 -1.0% 13.56 -0.5%

Pacific (mainly Japan) 8.13 -2.5% 8.10 -0.3% 8.57 7.65 7.78 8.42 8.10 0.0% 8.49 7.57 7.70 8.34 8.02 -1.0% 7.99 -0.4%

Total OECD 45.72 -0.7% 46.17 1.0% 46.26 45.69 46.84 47.10 46.48 0.7% 46.04 45.23 46.87 46.88 46.26 -0.5% 46.16 -0.2%

CIS (mainly Russia) 4.92 4.3% 4.87 -1.0% 4.85 4.91 5.08 4.99 4.96 1.8% 4.87 4.94 5.10 5.02 4.98 0.5% 5.01 0.5%

Other Europe 0.67 2.4% 0.70 3.7% 0.70 0.69 0.71 0.71 0.70 0.7% 0.70 0.69 0.71 0.71 0.70 0.0% 0.70 0.0%

China 10.70 3.4% 11.39 6.4% 11.54 11.79 11.83 11.87 11.76 3.2% 11.83 12.08 12.12 12.16 12.05 2.5% 12.35 2.5%

Other Asia 12.05 2.6% 12.54 4.1% 13.11 13.17 12.88 13.46 13.16 4.9% 13.60 13.65 13.36 13.96 13.64 3.7% 14.07 3.2%

Latin America 6.80 2.6% 6.76 -0.7% 6.53 6.74 6.82 6.76 6.71 -0.7% 6.59 6.80 6.88 6.82 6.78 1.0% 6.84 1.0%

Middle East 8.03 1.4% 8.17 1.8% 7.78 8.38 8.63 8.16 8.24 0.8% 7.93 8.55 8.81 8.32 8.40 2.0% 8.57 2.0%

Africa 3.97 2.2% 4.12 3.7% 4.25 4.22 4.13 4.31 4.23 2.6% 4.33 4.30 4.21 4.39 4.31 1.9% 4.42 2.5%

Total NON-OECD 47.15 2.7% 48.55 3.0% 48.75 49.90 50.07 50.25 49.75 2.5% 49.85 51.02 51.19 51.39 50.87 2.2% 51.97 2.2%

TOTAL DEMAND (RJ Est.) 92.87 1.0% 94.72 2.0% 95.01 95.59 96.91 97.35 96.22 1.6% 95.89 96.25 98.06 98.26 97.13 0.9% 98.12

Actual Missing Barrels 0.28 0.10 0.30 0.08

Missing Bbls Adjustment (1/2 actual) 0.14 0.19 0.23 0.23 0.23 0.23 0.23 0.23 0.23 0.23 0.23 0.23 0.23

TOTAL RJ DEMAND (inc. Miss. Bbls Adj) 93.01 1.2% 94.91 2.0% 95.54 95.81 97.14 97.58 96.45 1.6% 96.11 96.48 98.28 98.49 97.35 0.9% 98.35 1.0%

IEA DEMAND EST 92.88 1.1% 94.73 2.0% 95.01 95.29 96.67 96.79 95.94 1.3%

Y/Y bbl/day Change (IEA Est.) 0.97 1.85 1.41 1.17 1.00 1.31 1.21

Y/Y % Change (IEA Est.) 1.1% 2.0% 1.5% 1.2% 1.0% 1.4% 1.3%

Y/Y bbl/day Change (Before Missing Bbl Adj.) 0.94 1.85 1.41 1.46 1.25 1.88 1.50 0.88 0.66 1.15 0.91 0.90 1.00

Y/Y % Change 1.0% 2.0% 1.5% 1.6% 1.3% 2.0% 1.6% 0.9% 0.7% 1.2% 0.9% 0.9% 1.0%

Y/Y bbl/day Change (After Missing Bbl Adj.) 1.07 1.90 1.75 1.50 1.29 1.92 1.54 0.58 0.66 1.15 0.91 0.90 1.00

Y/Y % Change 1.2% 2.0% 1.9% 1.6% 1.3% 2.0% 1.6% 0.6% 0.7% 1.2% 0.9% 0.9% 1.0%

World Real GDP Growth 3.4% 3.1% 3.4% 3.6%

Source: IEA, RJ&A Estimates

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 57

Raymond James & Associates (RJA) is a FINRA member firm and is responsible for the preparation and distribution of research created in the United States. Raymond James & Associates is located at The Raymond James Financial Center, 880 Carillon Parkway, St. Petersburg, FL 33716, (727) 567-1000. Non-U.S. affiliates, which are not FINRA member firms, include the following entities that are responsible for the creation and distribution of research in their respective areas: in Canada, Raymond James Ltd. (RJL), Suite 2100, 925 West Georgia Street, Vancouver, BC V6C 3L2, (604) 659-8200; in Latin America, Raymond James Argentina S.A., San Martin 344, 22nd Floor, Buenos Aires, C10004AAH, Argentina, +54 11 4850 2500; in Europe, Raymond James Euro Equities SAS (also trading as Raymond James International), 40, rue La Boetie, 75008, Paris, France, +33 1 45 64 0500, and Raymond James Financial International Ltd., Broadwalk House, 5 Appold Street, London, England EC2A 2AG, +44 203 798 5600.

This document is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The securities discussed in this document may not be eligible for sale in some jurisdictions. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Investors should consider this report as only a single factor in making their investment decision.

For clients in the United States: Any foreign securities discussed in this report are generally not eligible for sale in the U.S. unless they are listed on a U.S. exchange. This report is being provided to you for informational purposes only and does not represent a solicitation for the purchase or sale of a security in any state where such a solicitation would be illegal. Investing in securities of issuers organized outside of the U.S., including ADRs, may entail certain risks. The securities of non-U.S. issuers may not be registered with, nor be subject to the reporting requirements of, the U.S. Securities and Exchange Commission. There may be limited information available on such securities. Investors who have received this report may be prohibited in certain states or other jurisdictions from purchasing the securities mentioned in this report. Please ask your Financial Advisor for additional details and to determine if a particular security is eligible for purchase in your state.

The information provided is as of the date above and subject to change, and it should not be deemed a recommendation to buy or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. Persons within the Raymond James family of companies may have information that is not available to the contributors of the information contained in this publication. Raymond James, including affiliates and employees, may execute transactions in the securities listed in this publication that may not be consistent with the ratings appearing in this publication.

Additional information is available on request.

Analyst Information

Registration of Non-U.S. Analysts: The analysts listed on the front of this report who are not employees of Raymond James & Associates, Inc., are not registered/qualified as research analysts under FINRA rules, are not associated persons of Raymond James & Associates, Inc., and are not subject to NASD Rule 2711 and NYSE Rule 472 restrictions on communications with covered companies, public companies, and trading securities held by a research analyst account.

Analyst Holdings and Compensation: Equity analysts and their staffs at Raymond James are compensated based on a salary and bonus system. Several factors enter into the bonus determination including quality and performance of research product, the analyst's success in rating stocks versus an industry index, and support effectiveness to trading and the retail and institutional sales forces. Other factors may include but are not limited to: overall ratings from internal (other than investment banking) or external parties and the general productivity and revenue generated in covered stocks.

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 58

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 59

© 2016 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. All rights reserved.

International Headquarters: The Raymond James Financial Center | 880 Carillon Parkway | St. Petersburg, Florida 33716 | 800 -248-8863 60

Additional Risk and Disclosure information, as well as more information on the Raymond James rating system and suitability categories, is available at rjcapitalmarkets.com/Disclosures/index. Copies of research or Raymond James’ summary policies relating to research analyst independence can be obtained by contacting any Raymond James & Associates or Raymond James Financial Services office (please see raymondjames.com for office locations) or by calling 727-567-1000, toll free 800-237-5643 or sending a written request to the Equity Research Library, Raymond James & Associates, Inc., Tower 3, 6

th Floor, 880 Carillon Parkway, St. Petersburg, FL 33716.

For clients in the United Kingdom:

For clients of Raymond James & Associates (London Branch) and Raymond James Financial International Limited (RJFI): This document and any investment to which this document relates is intended for the sole use of the persons to whom it is addressed, being persons who are Eligible Counterparties or Professional Clients as described in the FCA rules or persons described in Articles 19(5) (Investment professionals) or 49(2) (High net worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended) or any other person to whom this promotion may lawfully be directed. It is not intended to be distributed or passed on, directly or indirectly, to any other class of persons and may not be relied upon by such persons and is therefore not intended for private individuals or those who would be classified as Retail Clients.

For clients of Raymond James Investment Services, Ltd.: This report is for the use of professional investment advisers and managers and is not intended for use by clients.

For purposes of the Financial Conduct Authority requirements, this research report is classified as independent with respect to conflict of interest management. RJA, RJFI, and Raymond James Investment Services, Ltd. are authorised and regulated by the Financial Conduct Authority in the United Kingdom.

For clients in France:

This document and any investment to which this document relates is intended for the sole use of the persons to whom it is addressed, being persons who are Eligible Counterparties or Professional Clients as described in “Code Monétaire et Financier” and Règlement Général de l’Autorité des Marchés Financiers. It is not intended to be distributed or passed on, directly or indirectly, to any other class of persons and may not be relied upon by such persons and is therefore not intended for private individuals or those who would be classified as Retail Clients.

For institutional clients in the European Economic Area (EEA) outside of the United Kingdom:

This document (and any attachments or exhibits hereto) is intended only for EEA institutional clients or others to whom it may lawfully be submitted.

For Canadian clients:

This report is not prepared subject to Canadian disclosure requirements, unless a Canadian analyst has contributed to the content of the report. In the case where there is Canadian analyst contribution, the report meets all applicable IIROC disclosure requirements.

Proprietary Rights Notice: By accepting a copy of this report, you acknowledge and agree as follows:

This report is provided to clients of Raymond James only for your personal, noncommercial use. Except as expressly authorized by Raymond James, you may not copy, reproduce, transmit, sell, display, distribute, publish, broadcast, circulate, modify, disseminate or commercially exploit the information contained in this report, in printed, electronic or any other form, in any manner, without the prior express written consent of Raymond James. You also agree not to use the information provided in this report for any unlawful purpose. This is RJA client releasable research

This report and its contents are the property of Raymond James and are protected by applicable copyright, trade secret or other intellectual property laws (of the United States and other countries). United States law, 17 U.S.C. Sec.501 et seq, provides for civil and criminal penalties for copyright infringement. No copyright claimed in incorporated U.S. government works.