Public Expose 2020 - ir-bri.com

30

Public Expose 2020 PT BANK RAKYAT INDONESIA (PERSERO) Tbk.

Transcript of Public Expose 2020 - ir-bri.com

Public Expose 2020PT BANK RAKYAT INDONESIA (PERSERO) Tbk.

2

BRI AT A GLANCE

3

Corporate Plan (2018 – 2022)

The Most Valuable Bank in SEA& Home to The Best Talent

Micro SME Consumer Corporate SubsidiariesGrowing and

developing the micro business

Maintaining market

leadership in salary based loan & other

consumer loans

Becoming leading

SME Bank in Indonesia

Improving

profitability of the corporate banking

unit

Increasing

contributions from subsidiary

companies

Human CapitalImplementing

Performance Driven Culture

ITImproving IT

Capacity, and IT Governance

ChannelIncreasing efficiency

and productivity

RiskStrengthening risk

management culture

4

BRI Senantiasa Menciptakan “Success Stories”

SimpedesKupedes

1984

4 Jutadebitur Kupedes

71 Jutanasabah Simpedes

BRIGUNA

1989

1,7 Jutanasabah Briguna

Rp100 T

KUR

2009

5,6 Jutanasabah KUR

Rp73 T

BRILINK

2014

±400 ribu Agen> Rp500T Trx

AsuransiMikro

2014

± 4,8JutaPemegang Polis

BRISPOT

2018

MikroSmall Comm

Consumer

..nextsuccess stories ..

2019

Digital Loan Products dan

Digital Paymet Ecosystem

Digital Initiatives

2020 onwards..

•Ultra Micro Loans

•Micro payment ecosystem

2016 - 2017

BRIVolution

Journey begins here..

BRIVolutionTransformasi digital dan culture BRI menuju

The Most Valuable Bank in SEA di tahun 2022 dan Home to the Talent

Transformasi digital dan

culture

..tetap fokus pada UMKM khususnya Mikro “Go Smaller, Go Shorter, Go Faster” melalui digitalisasi..

2003 2007 2011 2015 2020

Kinerja Saham BBRI

5

Harga Saham BBRI & Kapitalisasi Pasar

* Setelah stock split 1: 2 (Jan’11) dan 1 : 5 (Nov’17)

Rp 3.80025 Agustus 2020

Market Cap

Rp 468,7 TRp 87,5*

15 Jan 2003

Total Investor’s Value 69x

2015 2016

2017 2018

2019 Agustus 20205 5

4 43 3

Peringkat Market Cap BBRIdi Asia Tenggara

6

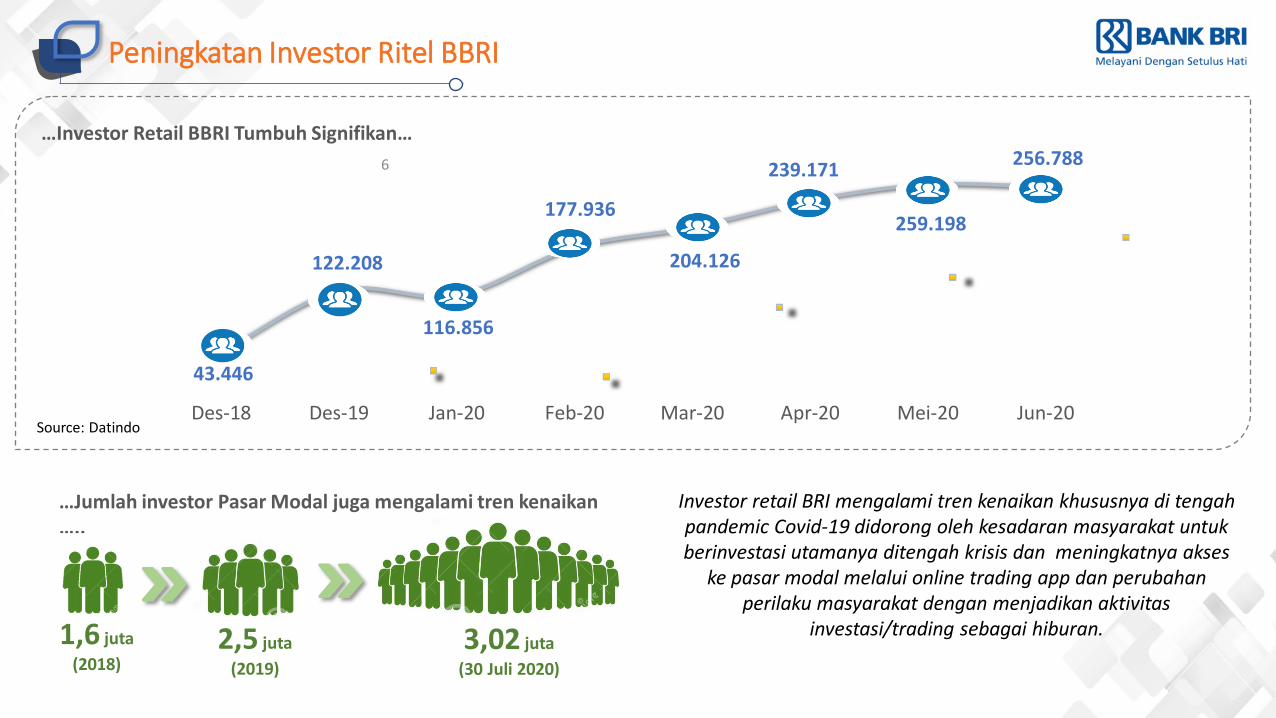

Peningkatan Investor Ritel BBRI

43.446

122.208

116.856

177.936

204.126

239.171

259.198

256.788

Des-18 Des-19 Jan-20 Feb-20 Mar-20 Apr-20 Mei-20 Jun-20

Investor retail BRI mengalami tren kenaikan khususnya di tengah pandemic Covid-19 didorong oleh kesadaran masyarakat untuk berinvestasi utamanya ditengah krisis dan meningkatnya akses

ke pasar modal melalui online trading app dan perubahan perilaku masyarakat dengan menjadikan aktivitas

investasi/trading sebagai hiburan.

…Investor Retail BBRI Tumbuh Signifikan…

2,5 juta

(2019)

…Jumlah investor Pasar Modal juga mengalami tren kenaikan …..

1,6 juta

(2018)3,02 juta

(30 Juli 2020)

Source: Datindo

7

Mengapa Investasi di BBRI?

PertimbanganInvestor

berinvestasidi BBRI

Fokus Pada Segmen UMKM

Digital Transformation

Customer Base, Networks dan Permodalan yang Kuat

• Sesuai Core Competency bisnis BRI• Potensi pertumbuhan yang masih sangat tinggi

• Sebagai sumber baru pertumbuhan bisnis• Digitasi proses bisnis untuk meningkatkan efisiensi

Implementasi ESG (Environment, Social & Governance) Terdepan • Memastikan sustainability bisnis perusahaan

8

STRATEGI BRI DI MASA PANDEMI & PROGRAM PEMULIHAN EKONOMI NASIONAL (PEN)

9

Fokus dan Strategi BRI

PEOPLE’S FIRST

SUSTAINABLEBUSINESS GROWTH

GOOD CORPORATE GOVERNANCE

Protokol Kesehatan

Work From Home

Optimalisasi Digital

• Sterilisasi seluruh premis • Vaksin untuk pekerja• Produk dan alat kesehatan untuk pekerja

(masker, hand-sanitizers, dan vitamins)

• Work From Home• Ruang kerja yang fleksible

• BRIStars: Digital office application• BRISpot: Digital loan processing• BRISIM: Daily monitoring Dashboard

Portofolio Kredit

• Pertumbuhan yang Selektif• Program restrukturisasi kredit

Aktivitas Market

• Menjaga reserve requirement, SR, LDR, RIM • Menjaga long position pada Net Foreign

Position• Menjaga Cash Ratio

GCG Implementation

Memastikan prinsip Good Corporate Governance tetap terimplementasi dengan baik

Restrukturisasi KreditBerdasarkan Segmen

46%

1%

6%

2%

45%

Micro Corp&SOE ConsumerMedium Small Comm.

18%

42%

15%

25%

Jakarta Java Ex. JakartaSumatra Mid & East

Restrukturisasi KreditBerdasarkan Wilayah

10

Dukungan BRI kepada Nasabah Selama Masa PandemiMelalui Restrukturisasi Kredit

Restrukturisasi Kredit dalam Rp Triliun

Jumlah Nasabah Restrukturisasi dalam Jutaan

Posisi JULY 31st 2020

14,9

101,2

160,5 171,9 183,7

14,9

86,3

59,3 11,4 11,8 1,7%

11,7%

18,6%19,8%

21,3%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

-

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

180,0

200,0

Mar Apr May Jun Jul

Total Monthly % to Total Loan

0,13

1,41

2,642,82 2,95

0,13

1,28 1,22 0,19 0,13 1,1%

11,1%

20,7%22,2% 23,2%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

0,00

0,50

1,00

1,50

2,00

2,50

3,00

3,50

Mar Apr May Jun Jul

Total Monthly % to Total Loan

“Tren restrukturisasi menurun seiring dengan pelonggaran PSBB dan kembalinya aktivitas ekonomi masyarakat”

11

Dukungan BRI untuk Pemulihan Usaha UMKM

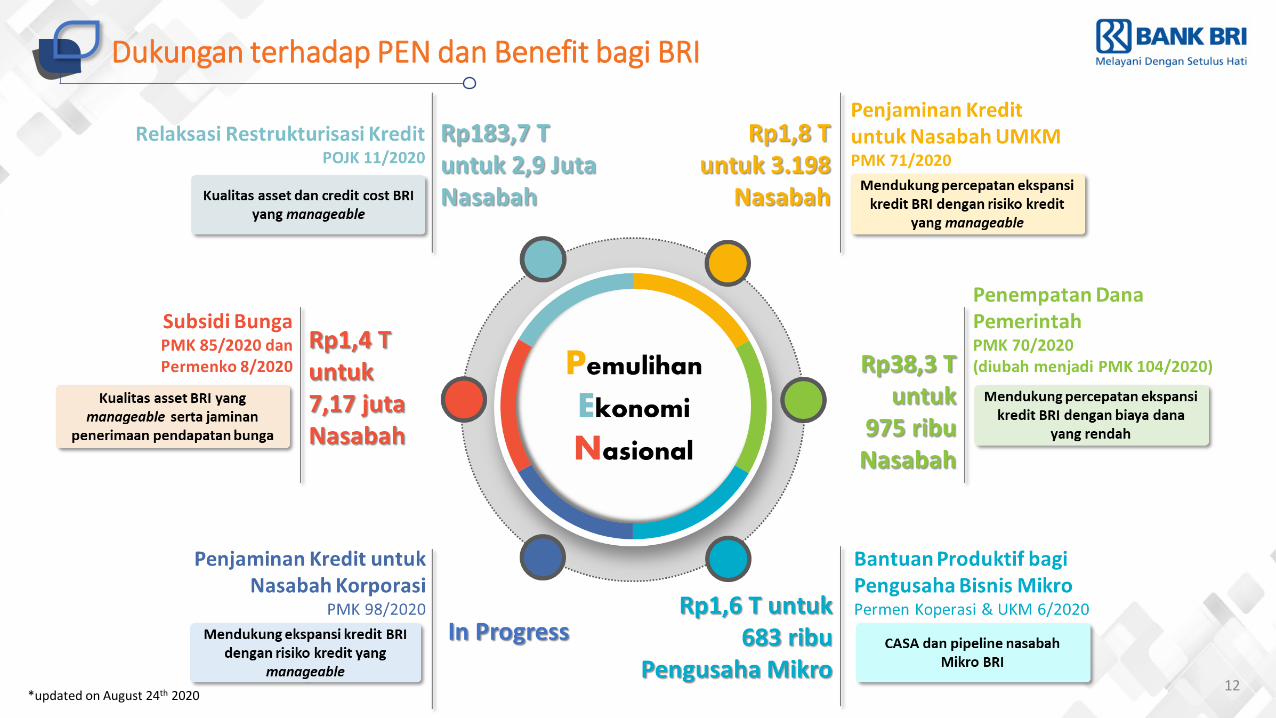

Dukungan terhadap PEN dan Benefit bagi BRI

*updated on August 24th 202012

13

BUSINESS UPDATE

14

Update Makro Ekonomi Indonesia

Source: BI

15

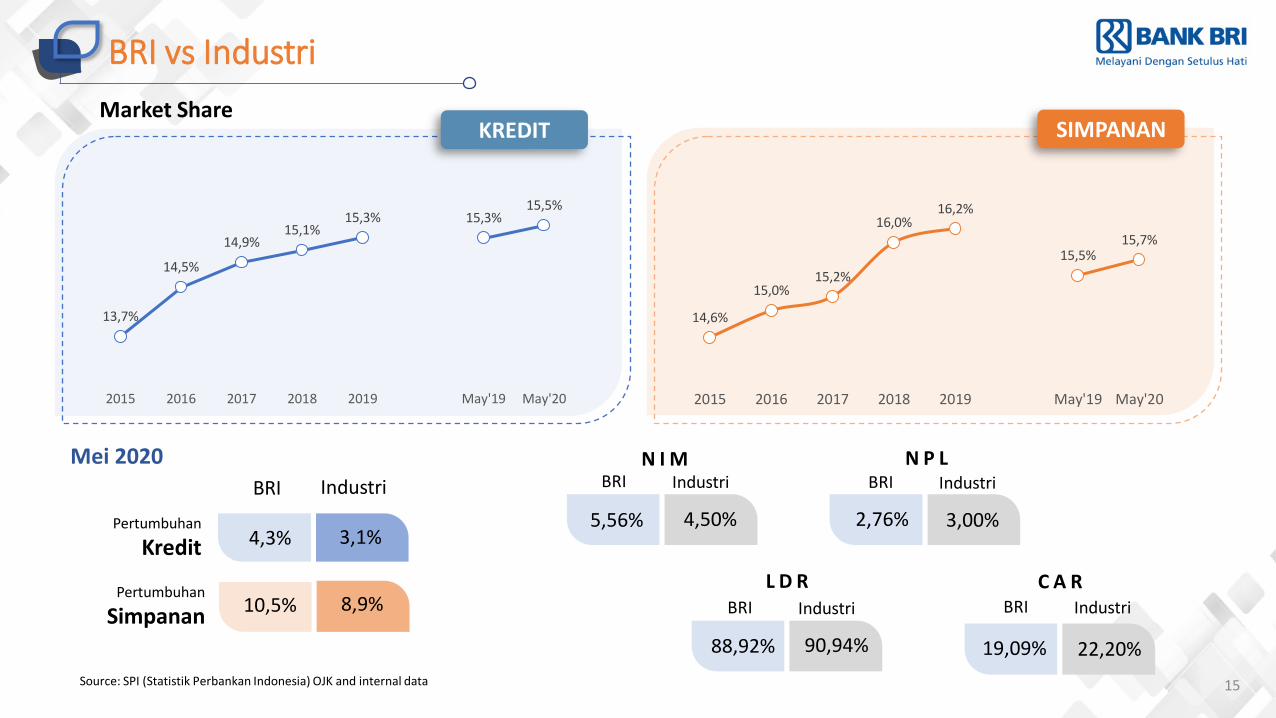

BRI vs Industri

Market Share

Source: SPI (Statistik Perbankan Indonesia) OJK and internal data

KREDIT SIMPANAN

Pertumbuhan

Kredit

BRI Industri

4,3% 3,1%

8,9%10,5%

N I M N P L

L D R

5,56% 2,76%

88,92%

C A R

19,09%

BRI Industri BRI Industri

BRI Industri BRI Industri

4,50% 3,00%

90,94% 22,20%

13,7%

14,5%

14,9%15,1%

15,3% 15,3%15,5%

13,0%

13,5%

14,0%

14,5%

15,0%

15,5%

16,0%

16,5%

2015 2016 2017 2018 2019 May'19 May'20

14,6%

15,0%15,2%

16,0%16,2%

15,5%15,7%

14,0%

14,5%

15,0%

15,5%

16,0%

16,5%

17,0%

2015 2016 2017 2018 2019 May'19 May'20

Mei 2020

Pertumbuhan

Simpanan

16

Financial Highlights (Bank Only)

√ NPL (net) is after provision for impaired loan

√ Started in 2018, Loan has been adjusted due to reclassification of Trade Finance/LC Related Receivables from Loan to Other Earning Assets-Other Receivables

2015 2016 2017 2018 2019 1H'19 1H'20 g YoY

Asset/Liabilities

Total Assets (IDR Billion) 845.998 964.001 1.076.438 1.234.200 1.343.078 1.224.398 1.309.321 6,9%

Total Loans (Gross) (IDR Billion) 558.436 635.291 702.395 798.881 859.558 837.193 869.042 3,8%

Total Deposits (IDR Billion) 642.774 723.845 803.327 898.033 969.750 899.393 1.013.156 12,6%

Asset Quality

NPL (gross) 2,02% 2,03% 2,12% 2,16% 2,62% 2,35% 2,98%

NPL (nett) 1,22% 1,09% 0,88% 0,92% 1,04% 1,12% 0,77%

Liquidity

CASA 59,21% 60,57% 60,65% 61,84% 59,01% 58,72% 56,64%

LDR 86,88% 87,77% 87,44% 88,96% 88,64% 93,09% 85,78%

RIM/MIR (Macroprudential Intermediary Ratio) 88,51% 85,31% 92,17% 82,3%

LCR 201,29% 229,98% 201,76% 243,57%

NSFR 133,50% 136,17% 128,69% 138,10%

Profitability

Net Profit (IDR Billion) 25.204 25.753 28.469 31.702 34.029 16.203 10.201 -37,0%

Cost of Fund (CoF) 4,24% 3,83% 3,27% 3,47% 3,58% 3,64% 3,54%

NIM 7,85% 8,00% 7,92% 7,45% 6,98% 7,02% 5,72%

Cost Efficiency Ratio (CER) 41,28% 41,26% 41,15% 41,02% 40,26% 41,35% 50,23%

Operating Expense to Operating Income 66,69% 68,69% 69,14% 68,40% 70,10% 71,12% 77,49%

ROA before tax 4,19% 3,84% 3,69% 3,68% 3,50% 3,31% 2,41%

ROE Tier 1 29,89% 23,08% 20,03% 20,49% 19,41% 19,02% 12,62%

ROE B/S 24,39% 19,98% 18,72% 18,87% 17,77% 17,40% 11,33%

Capital

Tier1 CAR 16,76% 21,91% 21,95% 20,15% 21,52% 19,73% 18,81%

Total CAR 20,59% 22,91% 22,96% 21,21% 22,55% 20,77% 19,83%

IDR Billion

17

Fokus Tumbuh di Segmen UMKM

178,9 211,5 239,5 274,3 307,7 292,6 313,4

88,5100,2

114,6130,8

140,5 135,1 141,0

120,0

135,5

153,9

183,0

198,7190,3

195,6

21,2

18,1

19,9

18,3

21,519,5

20,0

68,5

77,2

77,4

91,0

93,891,3

97,4

81,2

92,8

97,1

101,4

97,4108,4

101,6

558,4

635,3

702,4

798,9

859,6837,2

869,0

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

800,0

900,0

1000,0

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

800,0

900,0

1000,0

2015 2016 2017 2018 2019 1H'19 1H'20

32,0 33,3 34,1 34,3 35,8 35,0 36,1

15,8 15,8 16,3 16,4 16,3 16,1 16,2

21,5 21,3 21,9 22,9 23,1 22,7 22,5

3,8 2,9 2,8 2,3 2,5 2,3 2,312,3 12,1 11,0 11,4 10,9 10,9 11,2

14,5 14,6 13,8 12,7 11,3 12,9 11,7

-

20,0

40,0

60,0

80,0

100,0

120,0

2015 2016 2017 2018 2019 1H'19 1H'20

7,1YoY Growth ( % ) 4,3 2,8 3,0 6,6 -6,2 3,8(Rp Tn) 20,8 5,9 5,3 0,6 6,1 -6,7 31,8

Outstanding Kredit – berdasarkan segmen bisnis (Rp Triliun)

Komposisi – berdasarkan segmen bisnis (%)

Micro Consumer Small Comm. Medium Corporate Non SOE SOE Total

28,0%

30,0%

32,0%

34,0%

36,0%

38,0%

40,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

18

Penyaluran Kredit secara Bulanan

... Loans disbursement in Micro, Consumer & Medium Segment is increasing …

Micro Consumer

Small Commercial

18,7

22,1 21,9

10,4

8,2

15,8

18,3

Jan Feb Mar Apr May Jun Jul

4,7

7,1

6,4 5,9

5,0

5,8 6,4

Jan Feb Mar Apr May Jun Jul

4,1

5,3

3,9

2,5

1,8

3,2 3,3

Jan Feb Mar Apr May Jun Jul

IDR Trillion

19

Kualitas Kredit

NPL Coverage Ratio

17,0 21,9 29,1 34,6 37,5 38,3 51,8

11,3 12,9 14,9 17,2 22,5 19,7 25,9

151,1%170,3%

195,5% 200,6%166,6%

194,6% 200,3%

0,0%

50,0%

100,0%

150,0%

200,0%

250,0%

-

10,0

20,0

30,0

40,0

50,0

60,0

2015 2016 2017 2018 2019 1H'19 1H'20

Provision NPL NPL Coverage

20

Pertumbuhan dan Komposisi Simpanan

Deposits Composition, COFDeposits Growth: Trend

(IDR Trillion)

113,0 140,8 144,4 176,4 167,8 162,3 172,8

267,6 297,6

342,8 378,9 404,4 365,8

401,1

262,2

285,4

316,1

342,7 397,5

371,3

439,3

642,8

723,8

803,3

898,0

969,8

899,4

1.013,2

0,0

200,0

400,0

600,0

800,0

1.000, 0

1.200, 0

0,0

200,0

400,0

600,0

800,0

1.000, 0

1.200, 0

2015 2016 2017 2018 2019 1H'19 1H'20

Demand Deposit Saving Time Deposit TOTAL

59,2% 60,6% 60,6% 61,8% 59,0% 58,7% 56,6%

40,8% 39,4% 39,4% 38,2%41,0% 41,3% 43,4%

4,24%

3,83%

3,27%3,47% 3,58% 3,64% 3,54%

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

3,50%

4,00%

4,50%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018 2019 1H'19 1H'20

Low Cost High Cost COF Liabilities

Inisiatif Simpanan

Optimalisasi value chain transaction untuk nasabah korporasi

Konsep baru tabungan mikro – Teman Simpedes

New BRI Mobile (penambahan fitur pembukaan rekening online)

Optimialisasi Agen BRILink (branchless banking)Ekosistem Pembayaran Digital, khususnya Micro

Payment Ecosystem melalui Pasar.id dan Stroberi

21

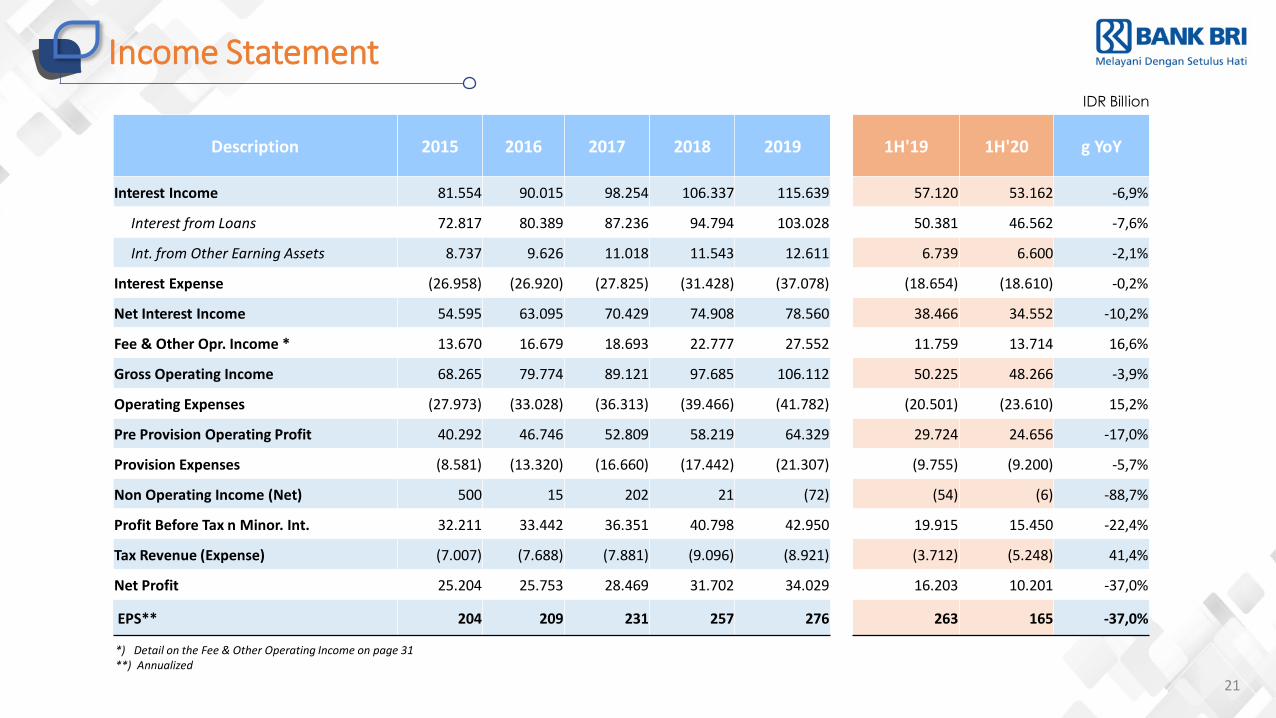

Income Statement

*) Detail on the Fee & Other Operating Income on page 31**) Annualized

IDR Billion

Description 2015 2016 2017 2018 2019 1H'19 1H'20 g YoY

Interest Income 81.554 90.015 98.254 106.337 115.639 57.120 53.162 -6,9%

Interest from Loans 72.817 80.389 87.236 94.794 103.028 50.381 46.562 -7,6%

Int. from Other Earning Assets 8.737 9.626 11.018 11.543 12.611 6.739 6.600 -2,1%

Interest Expense (26.958) (26.920) (27.825) (31.428) (37.078) (18.654) (18.610) -0,2%

Net Interest Income 54.595 63.095 70.429 74.908 78.560 38.466 34.552 -10,2%

Fee & Other Opr. Income * 13.670 16.679 18.693 22.777 27.552 11.759 13.714 16,6%

Gross Operating Income 68.265 79.774 89.121 97.685 106.112 50.225 48.266 -3,9%

Operating Expenses (27.973) (33.028) (36.313) (39.466) (41.782) (20.501) (23.610) 15,2%

Pre Provision Operating Profit 40.292 46.746 52.809 58.219 64.329 29.724 24.656 -17,0%

Provision Expenses (8.581) (13.320) (16.660) (17.442) (21.307) (9.755) (9.200) -5,7%

Non Operating Income (Net) 500 15 202 21 (72) (54) (6) -88,7%

Profit Before Tax n Minor. Int. 32.211 33.442 36.351 40.798 42.950 19.915 15.450 -22,4%

Tax Revenue (Expense) (7.007) (7.688) (7.881) (9.096) (8.921) (3.712) (5.248) 41,4%

Net Profit 25.204 25.753 28.469 31.702 34.029 16.203 10.201 -37,0%

EPS** 204 209 231 257 276 263 165 -37,0%

22

Trend Pendapatan Bunga Bersih & NIM

INTEREST INCOME

IDR Trillion

INTEREST EXPENSE

NII NIM

“Tren pendapatan bunga bulanan membaik sejak April 2020”

3,11

3,19

3,32

3,053,02

2,92

Jan Feb Mar Apr May Jun

10,289,95

10,44

6,21

7,62

8,65

5,00

6,00

7,00

8,00

9,00

10,00

11,00

Jan Feb Mar Apr May Jun

7,176,75

7,12

3,16

4,60

5,73

Jan Feb Mar Apr May Jun

NII

7,20%6,76%

7,08%

3,19%

4,62%

5,59%

7,20% 6,97% 7,00%

6,07%5,56% 5,72%

Jan Feb Mar Apr May Jun

NIM Marginal NIM

23

Pertumbuhan Fee Based Income

7.352

9.21010.303

11.900

14.293

6.201

7.430

7,7%

8,6%8,8%

9,2%

10,0%

9,0%

11,1%

7,0%

7,5%

8,0%

8,5%

9,0%

9,5%

10,0%

10,5%

11,0%

11,5%

2000

4000

6000

8000

10000

12000

14000

16000

2015 2016 2017 2018 2019 1H'19 1H'20

Fee Based Income % FBI to Total Operating Income

g (yoy):19,8%Fee Based Income (Rp Miliar)

Komposisi Fee Based Income

….Komposisi Fee Based Income terhadap Pendapatan Operasional terus meningkat seiring dengan pertumbuhan FBI yang kuat, disumbang Fee dari E-Channel dan E-

Banking….

24

BRILink

Bank account is not required

Money transfer

Bill payment

Loan installment

Cash deposit & withdrawal

Mobile phone voucher

SERVICES PROVIDED

360.00 0

370.00 0

380.00 0

390.00 0

400.00 0

410.00 0

420.00 0

430.00 0

440.00 0

1H'19 1H'20

391.348

434.364

# of Agents

-

50

100

150

200

250

300

350

1H'19 1H'20

234

321

# of Transaction(In Million)

300

310

320

330

340

350

360

370

380

1H'19 1H'20

Transaction Volume(IDR Trillion)

330,67

375,59

-

100,00

200,00

300,00

400,00

500,00

600,00

1H'19 1H'20

358,89

478,57

(IDR Billion)FBI

A branchless banking initiatives performed by BRI’s customer through fee income sharing scheme..

Cash pickup

70,8 Ribu saving referrals ( )

60,6 Ribu loan referrals ( )

Rp9,45 T CASA ( )

180,1% YoY

608,1% YoY

78,3% YoY

52,6 Ribu (70% dari total) akuisisi desa

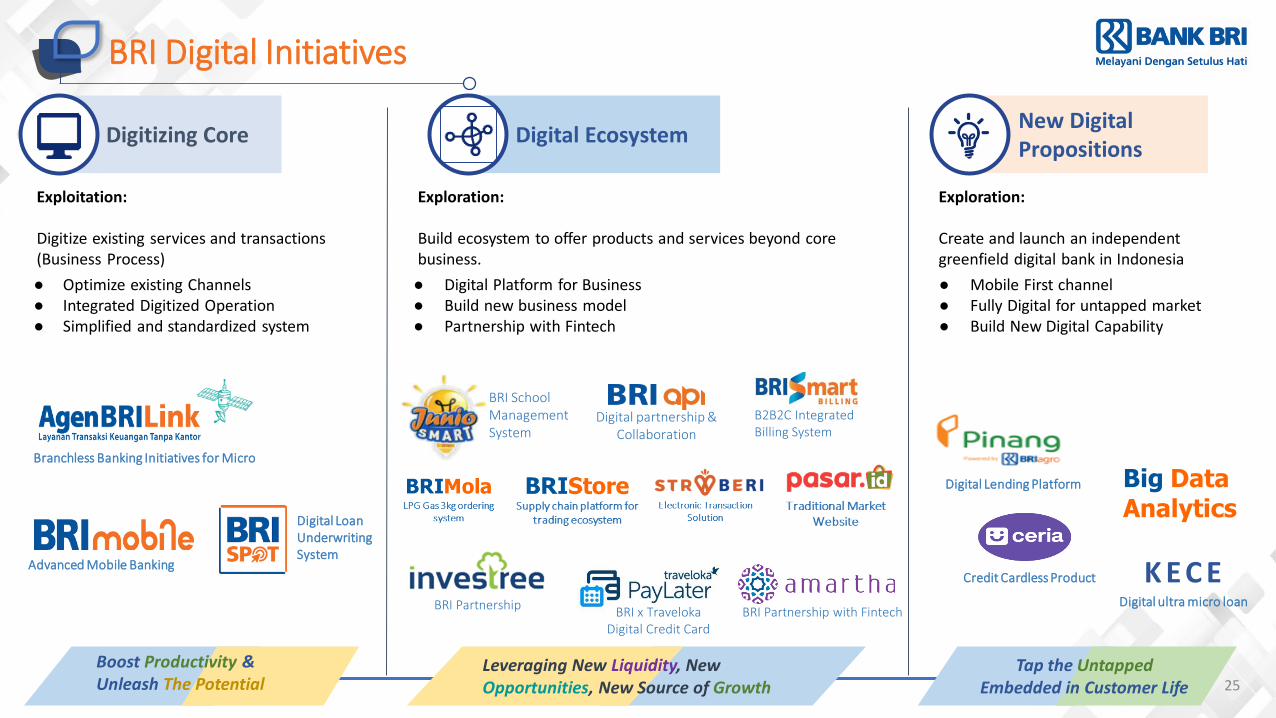

Digitizing Core Digital EcosystemNew Digital Propositions

Exploration:

Build ecosystem to offer products and services beyond core business.

Exploration:

Create and launch an independent greenfield digital bank in Indonesia

Exploitation:

Digitize existing services and transactions (Business Process)

● Optimize existing Channels● Integrated Digitized Operation● Simplified and standardized system

Big Data Analytics

Branchless Banking Initiatives for Micro

Digital LoanUnderwriting System

Advanced Mobile Banking

Digital partnership & Collaboration

B2B2C Integrated Billing System

BRI School Management System

● Digital Platform for Business● Build new business model● Partnership with Fintech

Digital Lending Platform

● Mobile First channel● Fully Digital for untapped market● Build New Digital Capability

Boost Productivity &Unleash The Potential

Tap the UntappedEmbedded in Customer Life

Leveraging New Liquidity, NewOpportunities, New Source of Growth

BRI Partnership

Credit Cardless Product

25

BRI Digital Initiatives

K E C EBRI Partnership with FintechBRI x Traveloka

Digital Credit Card

Digital ultra micro loan

26

Meningkatkan Kapabilitas Digital BRI

Digital Loan Products*Data as of July 2020

Digital Loan Partnership*Data as of July 2020

Rp64,8 Billion

disbursed to 9,950 borrowers

BRI senantiasa mengeksplorasi potensi bisnis baru dengan

mengembangkan produk digital lending serta menjalin partnership dengan fintechs dan digital start-ups untuk mewujudkan aspiration“Go Smaller, Go Shorter, Go Faster”

Rp88,6 Billion

disbursed to 29,766 borrowers

Rp21 Billion (June 2020)

disbursed to 8,804 borrowers

Rp321 Billion

disbursed to 87 borrowers

Rp381 Million

disbursed to 95 borrowers

Rp215,7 Billion

disbursed to 28,646 borrowers

27

BRI Initiatives On ESG

28

KEY TAKEAWAYS

Key Takeaways

29

• Manageable liquidity

• Loan restructuring pace slows down

• Loan disbursement start to recover

• Net interest income has bottomed out

• Fee income grew double digit supported by E-Channel & E-Banking Transaction

• Adequate provision provide cushion to anticipate Covid-19 impact

• Digital initiatives accelerates during pandemic

• Capital condition maintained at optimum level

PT BANK RAKYAT INDONESIA (Persero) Tbk.Investor Relations7th floor BRI II BuildingJl. Jenderal Sudirman No. 44-46 Jakarta 10210Indonesia

Phone : 62 21 5752006/09, 5751952/79Fax : 62 21 5752010Website : www.ir-bri.com Email : [email protected]

Disclaimer ; this report has been prepared by PT bank Rakyat Indonesia (Persero) Tbk (Bank BRI) independently and is circulated for the purpose of general information only. It is not intended to the specific person who may receive this report.The information in this report has been obtained from sources which we deem reliable. No warranty (expressed or implied) is made to the accuracy or completeness of the information. All opinions and estimations included in this reportconstitute our judgment as of this date and are subject to change without prior notice. We disclaim any responsibility or liability without prior notice of Bank BRI and/or their respective employees and/or agents whatsoever arising which maybe brought against or suffered by any person as a result of acting in reliance upon the whole or any part of the contents of this report and neither Bank BRI and/or its affiliated companies and/or their respective employees and/or agentsaccepts liability for any errors, omissions, negligent or otherwise. In this report and any inaccuracy herein or omission here from which might otherwise arise