PUBLIC AUDIT ACT AMENDMENTS - National Treasury

15

PUBLIC AUDIT ACT AMENDMENTS

Transcript of PUBLIC AUDIT ACT AMENDMENTS - National Treasury

PUBLIC AUDIT ACT AMENDMENTS

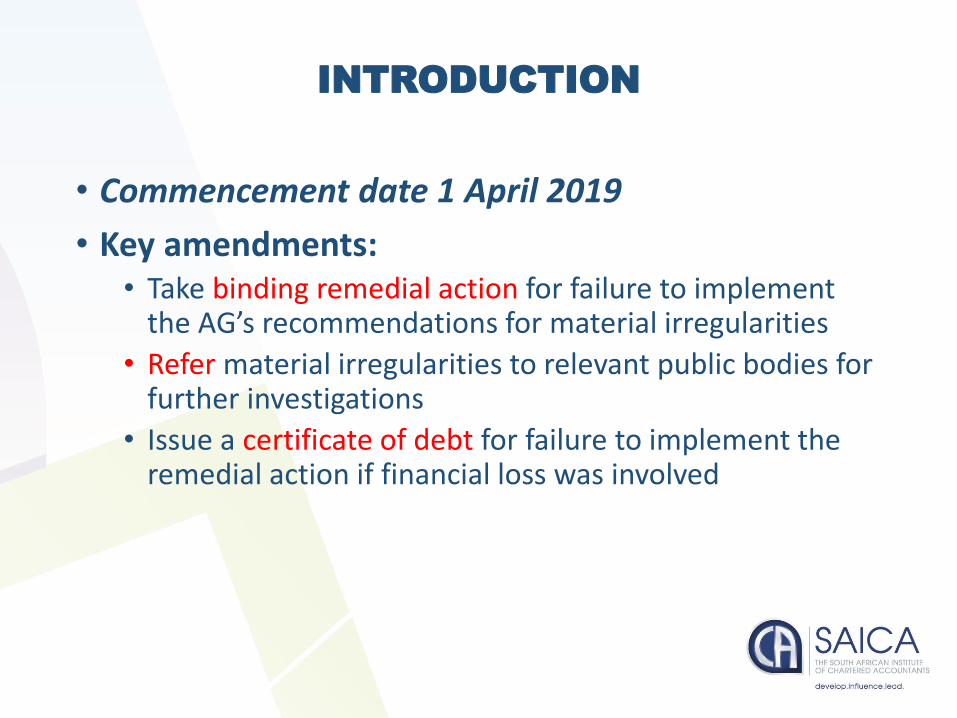

INTRODUCTION

• Commencement date 1 April 2019

• Key amendments:• Take binding remedial action for failure to implement

the AG’s recommendations for material irregularities

• Refer material irregularities to relevant public bodies for further investigations

• Issue a certificate of debt for failure to implement the remedial action if financial loss was involved

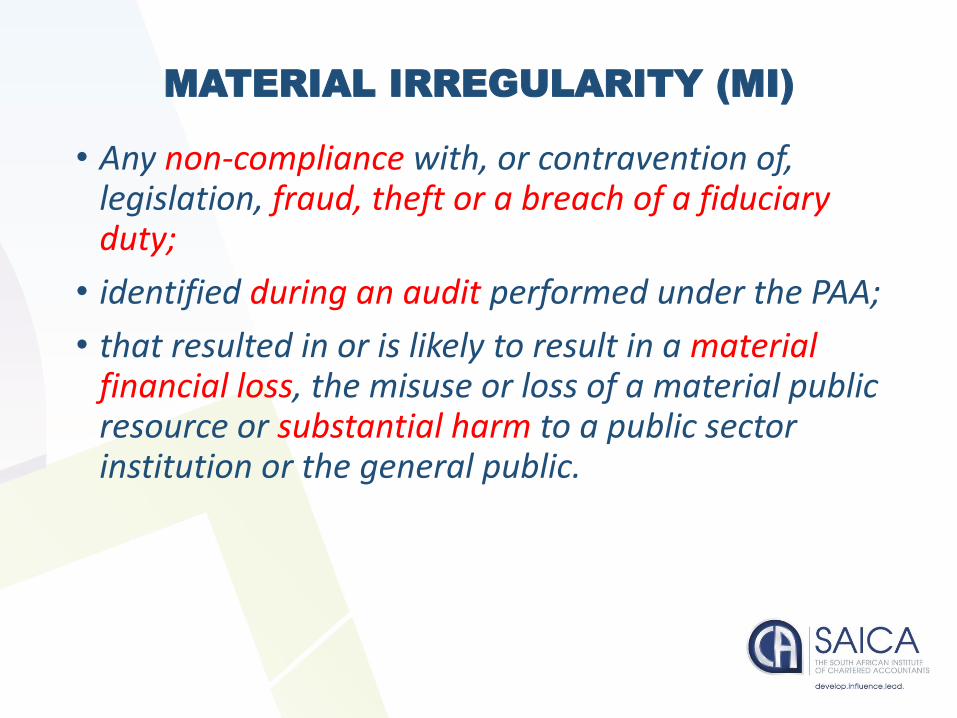

MATERIAL IRREGULARITY (MI)

• Any non-compliance with, or contravention of, legislation, fraud, theft or a breach of a fiduciary duty;

• identified during an audit performed under the PAA;

• that resulted in or is likely to result in a material financial loss, the misuse or loss of a material public resource or substantial harm to a public sector institution or the general public.

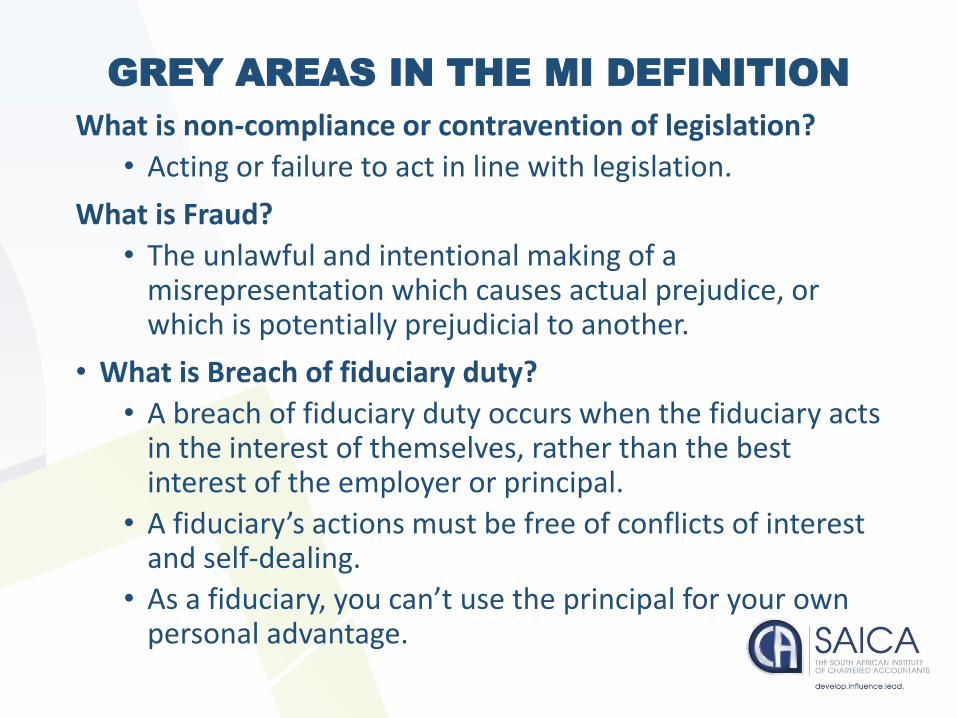

GREY AREAS IN THE MI DEFINITION

What is non-compliance or contravention of legislation?

• Acting or failure to act in line with legislation.

What is Fraud?

• The unlawful and intentional making of a misrepresentation which causes actual prejudice, or which is potentially prejudicial to another.

• What is Breach of fiduciary duty?

• A breach of fiduciary duty occurs when the fiduciary acts in the interest of themselves, rather than the best interest of the employer or principal.

• A fiduciary’s actions must be free of conflicts of interest and self-dealing.

• As a fiduciary, you can’t use the principal for your own personal advantage.

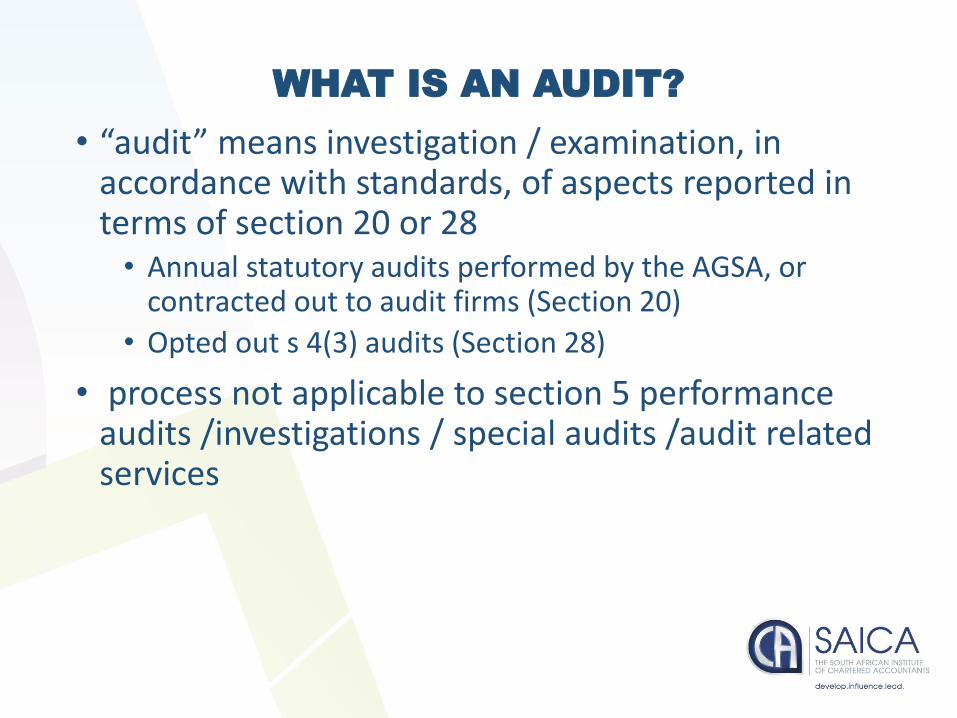

WHAT IS AN AUDIT?

• “audit” means investigation / examination, in accordance with standards, of aspects reported in terms of section 20 or 28• Annual statutory audits performed by the AGSA, or

contracted out to audit firms (Section 20)

• Opted out s 4(3) audits (Section 28)

• process not applicable to section 5 performance audits /investigations / special audits /audit related services

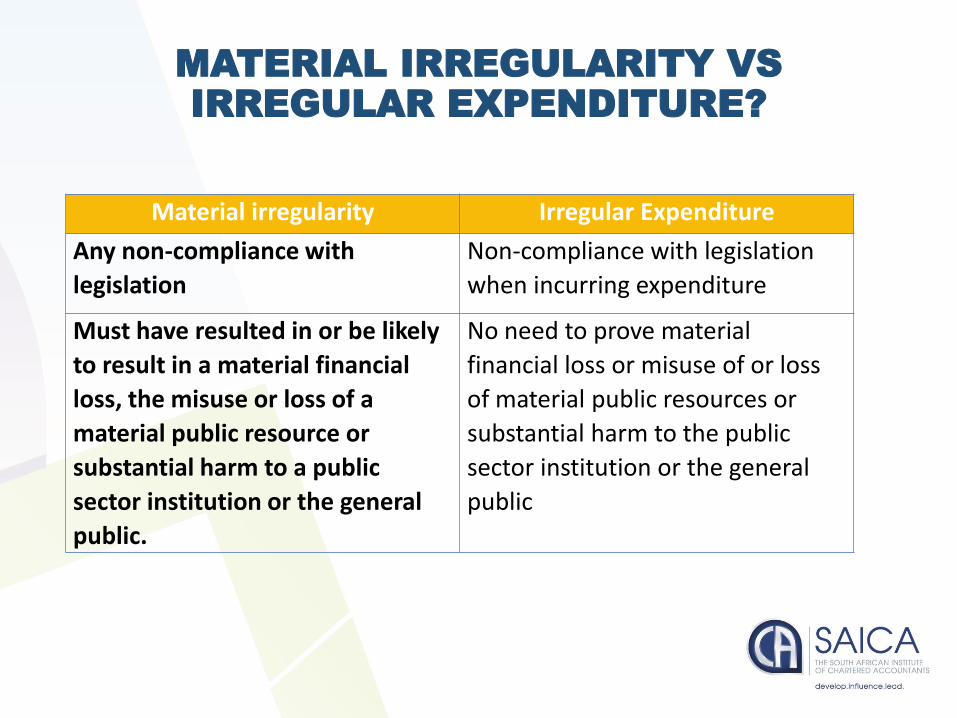

MATERIAL IRREGULARITY VS IRREGULAR EXPENDITURE?

Material irregularity Irregular Expenditure

Any non-compliance with

legislation

Non-compliance with legislation

when incurring expenditure

Must have resulted in or be likely

to result in a material financial

loss, the misuse or loss of a

material public resource or

substantial harm to a public

sector institution or the general

public.

No need to prove material

financial loss or misuse of or loss

of material public resources or

substantial harm to the public

sector institution or the general

public

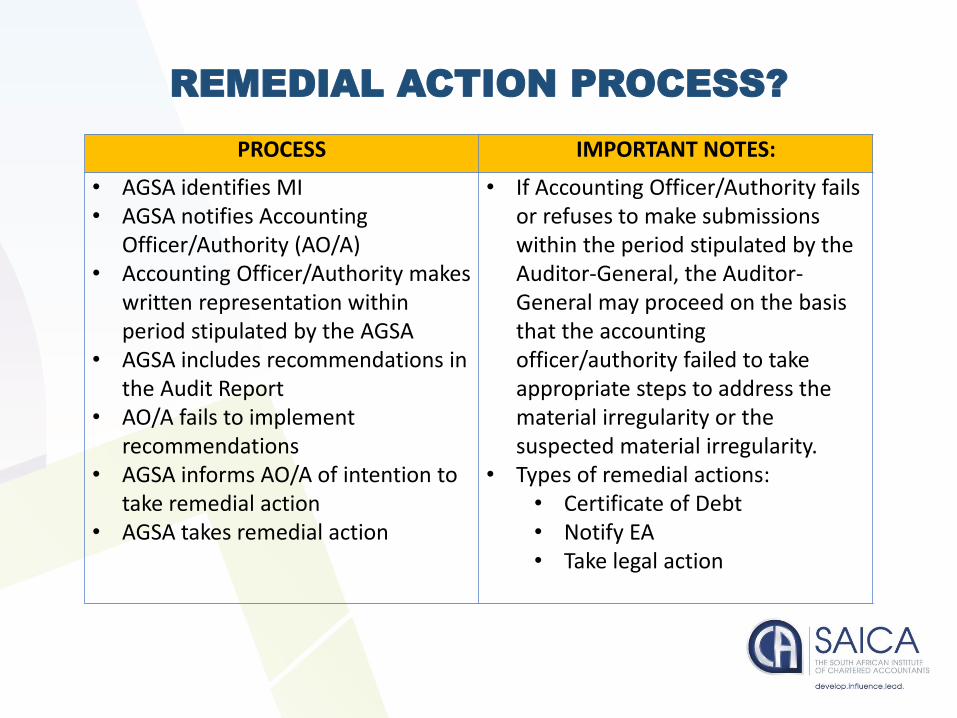

REMEDIAL ACTION PROCESS?

PROCESS IMPORTANT NOTES:

• AGSA identifies MI• AGSA notifies Accounting

Officer/Authority (AO/A)• Accounting Officer/Authority makes

written representation within period stipulated by the AGSA

• AGSA includes recommendations in the Audit Report

• AO/A fails to implement recommendations

• AGSA informs AO/A of intention to take remedial action

• AGSA takes remedial action

• If Accounting Officer/Authority fails or refuses to make submissions within the period stipulated by the Auditor-General, the Auditor-General may proceed on the basis that the accounting officer/authority failed to take appropriate steps to address the material irregularity or the suspected material irregularity.

• Types of remedial actions:• Certificate of Debt• Notify EA• Take legal action

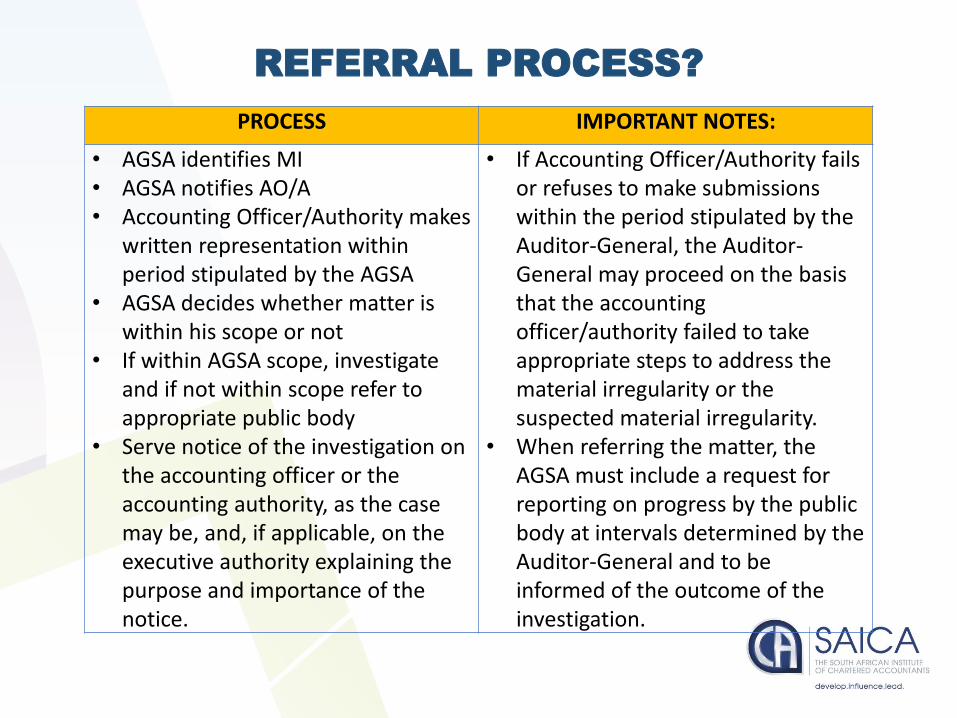

REFERRAL PROCESS?

PROCESS IMPORTANT NOTES:

• AGSA identifies MI• AGSA notifies AO/A• Accounting Officer/Authority makes

written representation within period stipulated by the AGSA

• AGSA decides whether matter is within his scope or not

• If within AGSA scope, investigate and if not within scope refer to appropriate public body

• Serve notice of the investigation on the accounting officer or the accounting authority, as the case may be, and, if applicable, on the executive authority explaining the purpose and importance of the notice.

• If Accounting Officer/Authority fails or refuses to make submissions within the period stipulated by the Auditor-General, the Auditor-General may proceed on the basis that the accounting officer/authority failed to take appropriate steps to address the material irregularity or the suspected material irregularity.

• When referring the matter, the AGSA must include a request for reporting on progress by the public body at intervals determined by the Auditor-General and to be informed of the outcome of the investigation.

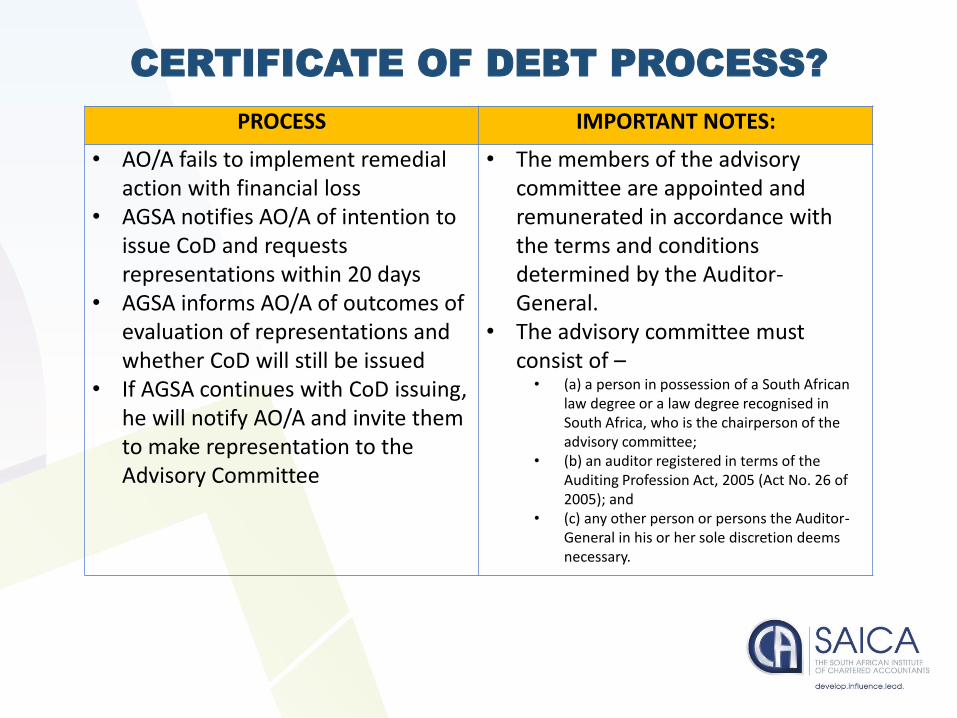

CERTIFICATE OF DEBT PROCESS?

PROCESS IMPORTANT NOTES:

• AO/A fails to implement remedial action with financial loss

• AGSA notifies AO/A of intention to issue CoD and requests representations within 20 days

• AGSA informs AO/A of outcomes of evaluation of representations and whether CoD will still be issued

• If AGSA continues with CoD issuing, he will notify AO/A and invite them to make representation to the Advisory Committee

• The members of the advisory committee are appointed and remunerated in accordance with the terms and conditions determined by the Auditor-General.

• The advisory committee must consist of –

• (a) a person in possession of a South African law degree or a law degree recognised in South Africa, who is the chairperson of the advisory committee;

• (b) an auditor registered in terms of the Auditing Profession Act, 2005 (Act No. 26 of 2005); and

• (c) any other person or persons the Auditor-General in his or her sole discretion deems necessary.

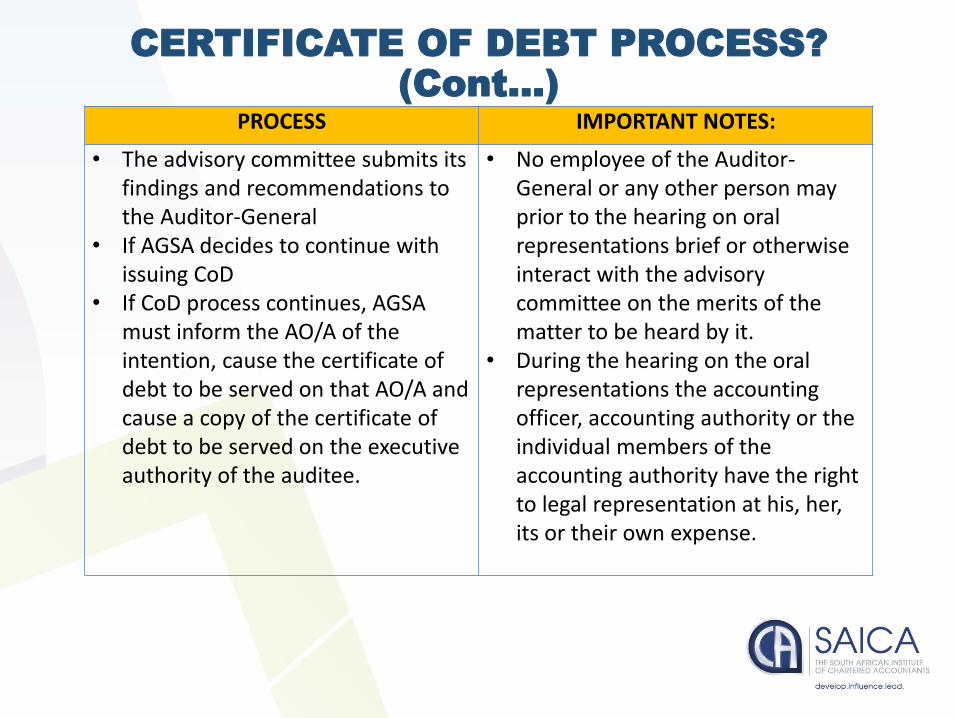

CERTIFICATE OF DEBT PROCESS? (Cont…)

PROCESS IMPORTANT NOTES:

• The advisory committee submits its findings and recommendations to the Auditor-General

• If AGSA decides to continue with issuing CoD

• If CoD process continues, AGSAmust inform the AO/A of the intention, cause the certificate of debt to be served on that AO/A and cause a copy of the certificate of debt to be served on the executive authority of the auditee.

• No employee of the Auditor-General or any other person may prior to the hearing on oral representations brief or otherwise interact with the advisory committee on the merits of the matter to be heard by it.

• During the hearing on the oral representations the accounting officer, accounting authority or the individual members of the accounting authority have the right to legal representation at his, her, its or their own expense.

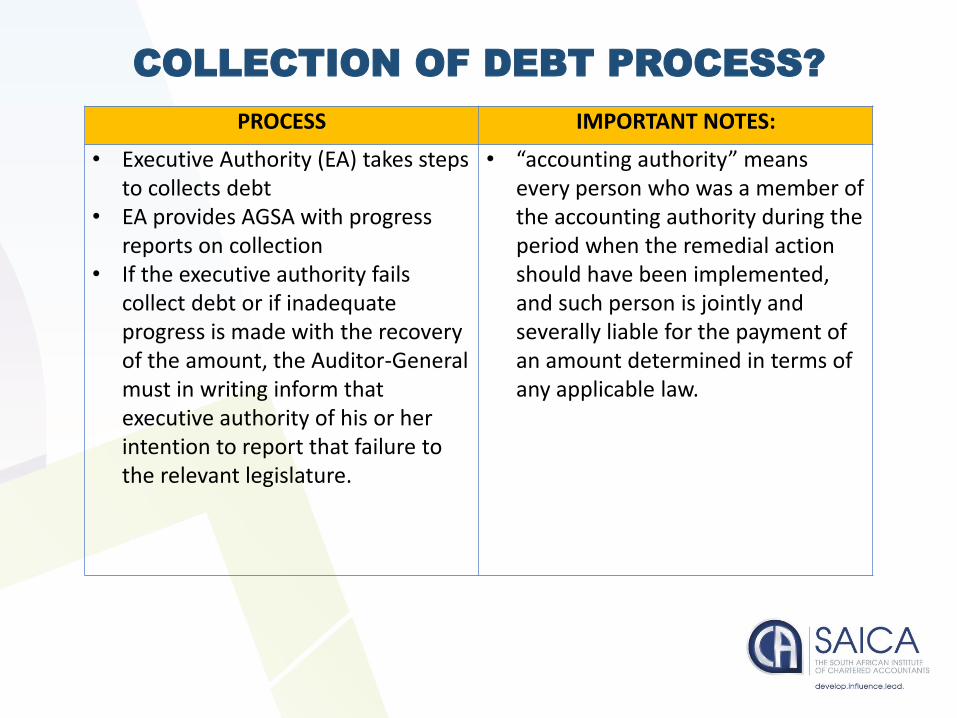

COLLECTION OF DEBT PROCESS?

PROCESS IMPORTANT NOTES:

• Executive Authority (EA) takes steps to collects debt

• EA provides AGSA with progress reports on collection

• If the executive authority fails collect debt or if inadequate progress is made with the recovery of the amount, the Auditor-General must in writing inform that executive authority of his or her intention to report that failure to the relevant legislature.

• “accounting authority” means every person who was a member of the accounting authority during the period when the remedial action should have been implemented, and such person is jointly and severally liable for the payment of an amount determined in terms of any applicable law.

IMPACT OF MI OG AG REPORTS?

Recommendations

MI is being investigated

MI referred to public body

Certificate of Debt issued

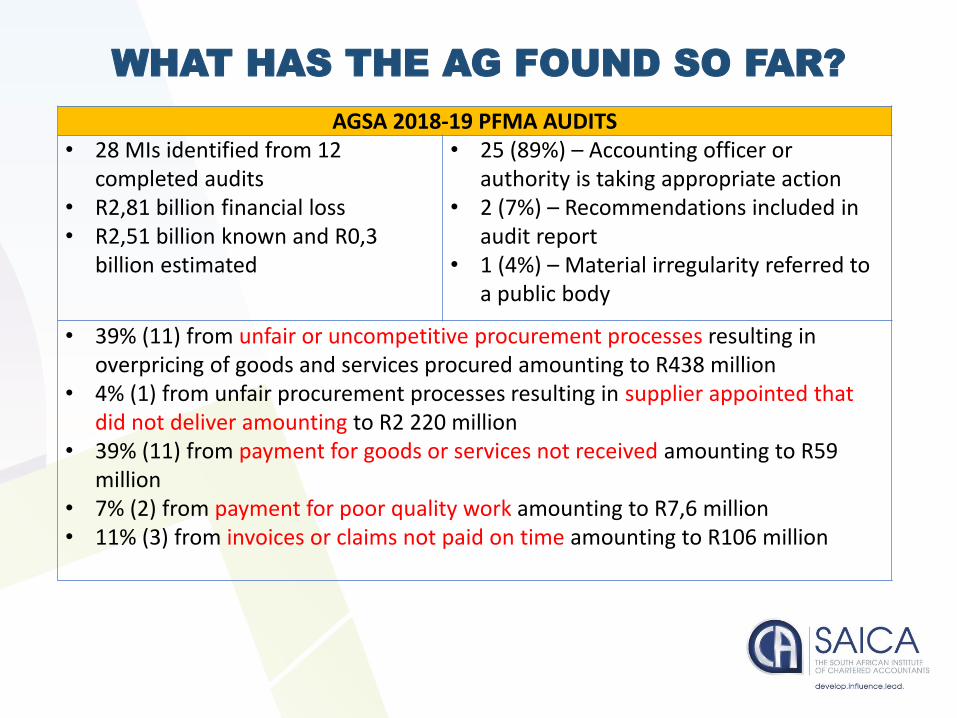

WHAT HAS THE AG FOUND SO FAR?

AGSA 2018-19 PFMA AUDITS• 28 MIs identified from 12

completed audits• R2,81 billion financial loss • R2,51 billion known and R0,3

billion estimated

• 25 (89%) – Accounting officer or authority is taking appropriate action

• 2 (7%) – Recommendations included in audit report

• 1 (4%) – Material irregularity referred to a public body

• 39% (11) from unfair or uncompetitive procurement processes resulting in overpricing of goods and services procured amounting to R438 million

• 4% (1) from unfair procurement processes resulting in supplier appointed that did not deliver amounting to R2 220 million

• 39% (11) from payment for goods or services not received amounting to R59 million

• 7% (2) from payment for poor quality work amounting to R7,6 million• 11% (3) from invoices or claims not paid on time amounting to R106 million

THANK YOU FOR YOUR ATTENTION!!

![UNHCR's Treasury Management [PeopleSoft] Module · PDF fileINTERNAL AUDIT DIVISION. AUDIT REPORT . UNHCR's Treasury Management (PeopleSoft) Module . Although the efficiency of the](https://static.fdocuments.in/doc/165x107/5aa005547f8b9a6c178d8a19/unhcrs-treasury-management-peoplesoft-module-audit-division-audit-report-unhcrs.jpg)