Internal Audit Manual - Ministry of Financeextranet.finance.gov.tt/content/Audit Manual- Very...

102

COMPTROLLER OF ACCOUNTS Ministry of Finance Government of the Republic of Trinidad Tobago Internal Audit Manual Prepared by the Financial Management Branch, Treasury Division, Ministry of Finance

-

Upload

phungquynh -

Category

Documents

-

view

215 -

download

0

Transcript of Internal Audit Manual - Ministry of Financeextranet.finance.gov.tt/content/Audit Manual- Very...

COMPTROLLER OF ACCOUNTS

Ministry of Finance

Government of the Republic of Trinidad Tobago

Internal Audit Manual

Prepared by the Financial Management Branch,

Treasury Division, Ministry of Finance

i

TABLE OF CONTENTS Pages

Introduction ……………………………………………………………………………… iii

1. The Internal Audit Environment

1.1 Legislative Framework – Specific to the Government of the Republic of

Trinidad and Tobago

1.1.1 Constitution of the Republic of Trinidad and Tobago………………… 3

1.1.2 Exchequer and Audit Act, Chapter 69:01……………………………. . 4

1.1.3 Financial Regulations to the Exchequer and Audit Act………….. …… 5

1.1.4 The Financial Instructions 1965………………………………………. 5

1.1.5 Ministry of Finance and Comptroller of Accounts Circulars………… 5

1.1.6 Manual of the Terms and Conditions of Employment……………….. 5

1.1.7 Chief Personnel Officer Circulars…………………………………….. 6

1.1.8 Commissions and Relevant Acts……………………………………… 6

1.1.9 Civil Service Act Chapter 23:01……………………………………… 7

1.1.10 Civil Service Regulations…………………………………………….. 7

1.1.11 Civil Service (External Affairs) Regulations…………………………. 8

1.1.12 Public Service Commission Regulation, 1966……………………….. 8

1.2 The Changing Environment of Internal Auditing

1.2.1 Compliance vs. Risk Management…………………………………… 10

1.2.2 Manual Environment vs. Information Technology Environment……. 11

1.2.3 Independence – Location vs. Mental Attitude……………………….. 12

1.2.4 Post Auditing vs. Ongoing Audits……………………………………. 13

1.3 International Standards

1.3.1 International Best Practice…………………………………………… 14

1.3.2 The Code of Ethics…………………………………………………… 15

1.3.2.1 Code of Ethics – Principles…………………………………………… 15

1.3.2.2 Rules of Conduct ……………………………………………………. 16

1.3.3 International Auditing Standards ……………………………………. 17

ii

1.4 The Committee of Sponsoring Organizations

1.4.1 Control Environment…………………………..……………………… 19

1.4.2. Risk Assessment…………………………………….………………… 19

1.4.3. Control Activities……………………………………………………… 20

1.4.4. Information and Communication……………………………………... 20

1.4.5 Monitoring…………………………………………………………..... 21

1.5 Criteria of Control Committee……………………………………………... 23

1.6 COBIT – Control Objectives for Information and Related Technology

1.6.1 What is COBIT………. ………………………………………............ 25

1.6.2 Benefits of implementing CobiT…………………………................... 25

1.6.3 COBIT Structure – Process Oriented…………………………………. 26

1.6.3.1 How does CobiT Work?……………………………………................ 28

1.6.3.2 Control Based …………………………………………….................... 29

1.6.3.3 Use of COBIT by the Internal Auditors………………………………. 29

1.7 Reporting Relationships

1.7.1 The Parliament of Trinidad and Tobago……………………………… 31

1.7.2 Minister of Finance …………………………………………………… 31

1.7.3 The Accounting Officer...……………………………………….......... 32

1.7.4 The Treasury Division……………..…………………………………. 33

1.7.5 Auditor General‟s Department ………………………………………. 34

1.7.6 The Public Accounts Committee and the Public Accounts Enterprises 35

Chapter 2

Treasury Statement on Corporate Governance

2.1 The Governance Structure of the Public Service – Legal Environment……38

Chapter 3

Management of the Internal Audit Unit

iii

3.1 The Corporate Planning Process……………………………………… 37

3.1.1 Government‟s overall Objectives & Policies…………………………. 38

3.1.2 The Ministry‟s Corporate Plan & Operational Plan…………………. 38

3.1.3 The Internal Audit Unit Corporate Plan……………………………… 38

3.1.3.1 Internal Audit Vision and Mission Statement ………………………. 39

3.1.3.2 Ministry‟s Priority Policies, Key Outcomes and Strategic Objectives 39

3.1.3.3 Strategies …………………….............................................................. 40

3.1.3.4 Key Output……………………………………..................................... 40

3.1.4 The Internal Audit Unit Operational Plan……………………………. 40

3.1.5 The Annual Audit Plan ………………………………………………. 41

3.2 Risk Assessment……………………………………............................ 42

3.2.1 Risk Assessment and Professional Judgement……………………….. 43

3.2.2 Information Sources……………………………………........................ 43

3.2.3 Setting Priorities…………………………………….............................. 43

3.3 Human Resource Management……………………………………....... 44

3.3.1 Training…………………………………………................................... 44

Chapter 4

Performance of Audit Work

4.1 Planning the Audit Assignment………………………………………. 46

4.1.1 Background Information……………………………………................ 47

4.1.2 Conducting Risk Assessment……………………………………......... 47

4.1.3 Establishing audit Objectives and Scope……………………………… 48

4.1.4 Ensure Subject Is Auditable……………………………………........... 49

4.1.5 Determining the necessary resources to perform the audit…………… 49

4.1.6 Communicate with the Relevant Stakeholder of the Audit…………… 50

4.1.7 Preliminary Survey……………………………………........................ 50

4.1.8 Development the Audit Programme…………………………………... 51

4.1.9 Define recipients of audit results……………………………………... 51

4.2 Audit Evidence……………………………………............................... 52

4.2.1 Nature of Evidence……………………………………........................ 52

4.2.2 Attributes of Evidence……………………………………................... 54

4.3 Documentation and Working Papers…………………………………. 55

4.3.1 Working Papers……………………………………............................. 55

iv

4.3.2 Purpose of the Working Papers………………………………………. 56

4.3.3 Documentation…………………………………….............................. 56

4.3.4 Supervisory Review…………………………………………............... 58

4.3.5 Control and Retention of Working Papers…………………………… 58

4.3.6 Permanent Files……………………………………............................. 59

4.4 Reporting……………………………………....................................... 59

4.4.1 Purpose of Report…………………………………….......................... 59

4.4.2 Elements of a Good Report……………………………………........... 60

4.4.3 Format of the Report……………………………………..................... 61

4.5 Interviews……………………………………...................................... 62

4.5.1 Identifying Availability of Evidence………………………………… 62

4.5.2 Exit Interview……………………………………................................ 63

4.6 Follow-up……………………………………...................................... 63

4.6.1 Timing of the follow-up……………………………………................. 63

Chapter 5

Value for Money Auditing

5.1 Background…………………………………….................................... 65

5.2 Economy, Efficiency and Effectiveness……………………………… 65

5.3 Approaches to VFM Auditing……………………………………....... 66

5.3.1 Procedures or Process-Oriented Approach…………………………… 67

5.3.2 Results-oriented Approach……………………………………............ 67

5.4 The Audit Process……………………………………......................... 68

5.4.1 The Planning Process…………………………………….................... 69

5.4.2 The Examination Phase…………………………………………......... 69

5.4.3 The Reporting Phase………………………………………….............. 70

5.4.4 The Follow-up Phase…………………………………………............. 71

5.5 Generic Questions for scope the audit……………………………….. 71

Chapter 6

Information Technology Audit

6.1 Background…………………………………….................................... 75

v

6.2 Computer-assisted audit Techniques (CAATS) ……………………… 76

6.2.1 Concept…………………………………….......................................... 76

6.2.2 Planning…………………………………………................................. 77

6.3 The Environment in which CAATS operate…………………………. 78

6.3.1 Understanding of the System………………………………………..... 78

6.3.2 Characteristics of the Data……………………………………............. 78

6.3.3 Audit Objectives………………………………………….................... 78

6.3.4 Audit Scope……………………………………................................... 79

6.4 Data Access……………………………………................................... 79

6.5 Application of CAATS……………………………………................. 79

6.6 Follow up Investigations……………………………………............... 80

6.7 Working Papers……………………………………............................ 81

6.8 Reporting……………………………………...................................... 81

Chapter 7

Role of Audit Committee……………………………………………………………………. 82

Glossary 83- 89

Appendices

vi

INTRODUCTION

(i) Purpose

This Internal Audit manual is designed to provide a comprehensive guidance for the

development and operations of internal auditing in the Public Service. It is intended to be used as

a source of reference and guidance for Internal Auditors in the daily performance of their duties.

Users of this manual are assumed to possess a basic knowledge and understanding of

management framework with practical guidance, tools and information for managing the Internal

Audit activity and for planning, coordinating and reporting to Management / the Accounting

Officer.

Against this background, this document aims to provide a standard set of guidelines regarding

Internal Auditing in the Public Service.

Internal Auditors must keep pace with current trends in their profession if they are to remain

effective in assisting management in the proper discharge of their duties

The Comptroller of Accounts believes that this manual will set the tone and will create the

necessary impetus for a sustainable and effective Internal Auditing mechanism in Government.

(ii) Definition of Internal Auditing

The Institute of Internal Auditors (IIA) (the world-wide professional organization for Internal

Auditing) defines internal audit as:-

„Internal Auditing is an independent, objective assurance and consulting activity designed to

add value and improve an organization’s operations. It helps an organization accomplish its

objectives by bringing a systematic, disciplined approach to evaluate and improve the

effectiveness of risk management, control and governance processes.’

In order to assist Accounting Officers in achieving their objectives in an intelligent manner,

Internal Auditors must be aware of the environment in which they operate and the rules which

govern their work activities.

vii

(iii) The Objective of Internal Auditing

The overall objective of Internal Auditing is to assist the Accounting Officer in the effective

discharge of his/her responsibilities by furnishing objective analyses, appraisals,

recommendations and pertinent comments on the activities reviewed.

The Internal Auditor must therefore be involved in any phase of activity in which he can be of

service to the Accounting Officer.

Activities include:-

appraising the soundness and application of accounting, financial and operating controls;

ascertaining the reliability of accounting and other data developed within the

organization;

ascertaining the extent of compliance with establish policies and procedures;

appraising the quality of performance in carrying out assigned responsibilities;

NB: Please note that this Auditing Manual is a work in progress. Inclusions will be inserted as

the various sections areas developed, reviewed and verified.

8

CHAPTER 1

INTERNAL AUDIT ENVIRONMENT

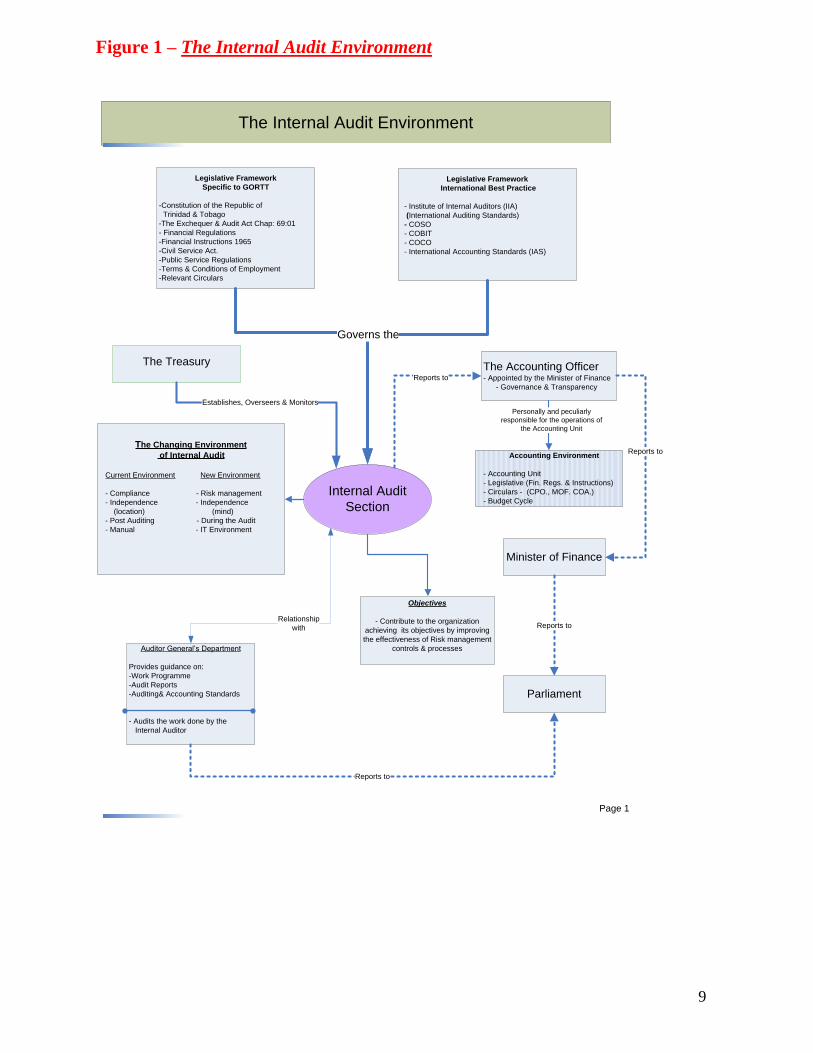

The Internal Audit Environment is shown on the flowchart at figure 1, page 2. The various

components are as follows:-

Legislative Framework- specific to the Government of Trinidad and Tobago;

Legislative Framework – International Best Practice;

The Treasury;

The Accounting Officer;

Minister of Finance;

The Auditor General Department;

The Parliament.

The ensuing sections give details of these areas.

9

Figure 1 – The Internal Audit Environment

Internal Audit

Section

The Treasury The Accounting Officer- Appointed by the Minister of Finance

- Governance & Transparency

Legislative Framework

Specific to GORTT

-Constitution of the Republic of

Trinidad & Tobago

-The Exchequer & Audit Act Chap: 69:01

- Financial Regulations

-Financial Instructions 1965

-Civil Service Act.

-Public Service Regulations

-Terms & Conditions of Employment

-Relevant Circulars

Establishes, Overseers & Monitors

Reports to

Auditor General’s Department

Provides guidance on:

-Work Programme

-Audit Reports

-Auditing& Accounting Standards

- Audits the work done by the

Internal Auditor

Minister of Finance

Reports to

Parliament

Reports to

The Internal Audit Environment

Page 1

Legislative Framework

International Best Practice

- Institute of Internal Auditors (IIA)

(International Auditing Standards)

- COSO

- COBIT

- COCO

- International Accounting Standards (IAS)

Governs the

Reports to

The Changing Environment

of Internal Audit

Current Environment New Environment

- Compliance - Risk management

- Independence - Independence

(location) (mind)

- Post Auditing - During the Audit

- Manual - IT Environment

Relationship

with

Objectives

- Contribute to the organization

achieving its objectives by improving

the effectiveness of Risk management

controls & processes

Accounting Environment

- Accounting Unit

- Legislative (Fin. Regs. & Instructions)

- Circulars - (CPO., MOF. COA.)

- Budget Cycle

Personally and peculiarly

responsible for the operations of

the Accounting Unit

10

1.1 THE LEGISLATIVE FRAMEWORK- SPECIFIC TO THE GOVERNMENT

OF THE REPUBLIC OF TRINIDAD AND TOBAGO

Internal Auditors in the operation and execution of their duties are governed by legal

provisions. These provisions are as follows:-

1.1.1 The Constitution of the Republic of Trinidad and Tobago Ch 1:01

Chapter 8 of the Constitution of the Republic of Trinidad and Tobago deals with Finance and

outlines the following requirements:-

The establishment of the Consolidated Fund

The authorization of expenditure from the Consolidated Fund

The responsibility of the Minister of Finance

The establishment of the Office and the functions of the Auditor General

The requirements for the appointment of the Auditor General and the setting up of the

Public Accounts Committee.

Chapter 8, Section 113 (1) of the Constitution of the Republic of Trinidad and Tobago states:-

(1) “The Minister responsible for Finance shall cause to be prepared and laid before the

House of Representatives before or not later than thirty days after the commencement

of each financial year estimates of revenues and expenditure of Trinidad and Tobago

for that year.”

Chapter 8, Section 116 (1-2) of the Constitution of the Republic of Trinidad and Tobago

states:-

(1) “There shall be an Auditor General for Trinidad and Tobago, whose office shall

be a public office.”

and

(2) “The public accounts of Trinidad and Tobago and of all officers, courts and authorities of

Trinidad and Tobago shall be audited and reported on annually by the Auditor General,

and for that purpose the Auditor General or any person authorized by him in that behalf

shall have access to all books, records, returns and other documents relating to those

accounts.”

In order to assist the Minister of Finance in complying with these provisions, Accounting

Officers are charged with the responsibility for preparing and submitting the estimates of

revenue and expenditure to the Minister of Finance and the Appropriation Accounts to the

Auditor General. Accounting Officers have the responsibility of ensuring that proper systems

of accounting as prescribed by the Treasury are establish and maintained within their

respective Ministry/Department.

The Auditor General is empowered by the Constitution to carry out audits of the accounts,

balance sheets and other financial statements of all enterprises that are owned or controlled by

or on behalf of the State. She shall submit reports annually to the Speaker, the President of the

11

Senate and the Minister of Finance. The Auditor General is also responsible for monitoring the

systems and records used in the preparation of these accounts to ascertain whether they are

functioning properly and are in compliance with the relevant laws and guidance.

Internal Auditors in Central Government are charged with the responsibility of assisting

Accounting Officers in the effective discharge of their duties as defined in the Exchequer and

Audit Act, Chapter 69:01. Internal Auditors must examine the records of their

Ministries/Departments in order to ascertain the extent of compliance with established policies

and procedures as established by the Treasury and must ensure that expenditure incurred and

revenue earned conform to the Estimates of Expenditure/Revenue approved by Parliament.

They must also ensure that expenditure incurred under the various votes, are made in

accordance with Budgeted Allocations and that expenditure does not exceed releases granted.

1.1.2 The Exchequer and Audit Act, Chapter 69:01

In the daily performance of their duties, Officers are guided by and operate under the rules as

enshrined in the Exchequer and Audit Act, Chap.69:01.

This Act provides for:-

- the control and management of the public finances in the Republic of Trinidad and Tobago;

- the duties and powers of the Auditor General;

- the collection of, issue and payment of public moneys;

- the audit of the Public Accounts and the protection and recovery of public property;

- the control of the powers of statutory bodies and for matters connected therewith.

The Act also interprets the title of the Accounting Officer in Part I Section 2 which states inter-

alia:-

“an accounting officer means any person appointed by the Treasury and charged with the duty

of accounting for any service in respect of which moneys have been appropriated by the

Constitution or by Parliament, or any person to whom issues are made from the Exchequer

Account.”

Internal Auditors are a valuable resource for Accounting Officers and as such must be aware of

the role of the Accounting Officer.

1.1.3 The Financial Regulations to the Exchequer and Audit Act, Chapter 69:01

In addition to the Exchequer and Audit Act which states and interprets the law, Internal

Auditors are also guided by the Financial Regulations in their daily operations. These

Regulations provide a more detailed guidance and makes provision for an independent Internal

Audit Unit.

Part II Section 13 (4) of the Regulations states:-

“Each Accounting Unit shall have a check staff and an independent internal audit

unit”

12

Part II Sections 4 (1) and (3) of the Exchequer and Audit Act makes provision for the control

and management of the accounts.

Part I Section 8 of the Regulations also states:

“It is the duty of an accounting officer to –

(a) ensure that the proper system of accounting as prescribed by the Treasury is

established and maintained.”

Guided by the Financial Regulations in their role and responsibilities, Internal Auditors will be

able to give assurance to Accounting Officers that records are accurate, systems of internal

controls are performing effectively, and there is compliance with systems laid down by the

Treasury.

1.1.4 The Financial Instructions 1965

The Financial Instructions 1965 was issued by the Treasury under Section 4 of the Exchequer

and Audit Ordinance 1959. These Instructions give details on accounting procedures to be

adopted by the various Ministries/Departments so as to promote reliance on the accuracy of

records and to ensure that systems are functioning as intended.

1.1.5 Ministry of Finance and Comptroller of Accounts Circulars

Circulars are issued from time to time by the Minister of Finance and the Comptroller of

Accounts.

Circulars from the Minister of Finance are issued when new accounting

systems/procedures are being introduced.

Circulars from the Comptroller of Accounts are issued for clarification/updating of

existing systems and procedures.

1.1.6 Manual of the Terms & Conditions of Employment

The terms and condition of employment for officers employed in the Public Service has been

compiled in a manual by the Chief Personnel Officer (CPO). Unlike the Financial Regulations

which deals with accounting matters within the Public Service and the treatment of such, the

Manual of the Terms and Conditions of Employment addresses the administration of rules,

regulations and circular instructions relating to the terms of employment of Officers in the

Public Service.

Section I of the manual embodies those rulings, guidelines, interpretations and classifications

that are most frequently sought from the CPO in respect of areas such as:

- hours of work,

- treatment of work in excess of normal working hours,

- different types of leave, traveling and subsistence allowance,

- transfers between Trinidad and Tobago,

- uniform and

- employment on contract.

13

Each area dealt with in the Manual is referenced to the relevant regulations from the Civil

Service, Public Service, CPO and Ministry of Finance Circulars.

Sections II and III of the manual contain circulars/circular memoranda mentioned in Section I.

The manual must be read in conjunction with the relevant provisions of the Civil Service

Regulation, Public Service Regulation or the Traveling Allowances Regulations as may be

appropriate.

This manual is one of the tools used by the Internal Auditor in interpreting and clarifying

issues on the terms and conditions of employment of officers employed in the Public Service.

1.1.7 Chief Personnel Officer Circulars

The Chief Personnel Officer issues circulars from time to time for the variation of officer‟s

terms and conditions of employment in relation to the terms and conditions, salaries and

allowances for all officers employed in the Civil Service as well as clarification of existing

circulars when necessary.

1.1.8 Commissions and Relevant Acts

Various Commissions established under the Constitution of the Republic of Trinidad and

Tobago are as follows:-

1. Public Service Commission

2. Police Service Commission

3. Teaching Service Commission

4. Judicial and Legal Service Commission

5. Statutory Authorities Commissions

These Commissions are followed by specific Acts and Regulations governing the relevant

service are as follows:-

- Public Service Commission:

Civil Service Act Chapter 35:50 - Civil Service

Fire Service Act Chapter 23:01 - Fire Service

Prison Service Act Chapter 13:02 - Prison Service

- Police Service Commission:

Police Service Act Chapter 15:01– Police Service

- Teaching Service Commission:

Education Act Chapter 39:01 – Teaching Service

- Judicial and Legal Service Commission:

Judicial & Legal Service Act Chapter 6:01 – Judicial and Legal Service

- Statutory Authorities Commission

Statutory Authorities Act Chapter 34:01 - Statutory Bodies

14

1.1.9 Civil Service Act Chapter 23:01

The Civil Service Act, Chapter 23:01 makes provision for the establishment and classification

of:

- the Civil Service,

- a Personnel Department,

- procedures for negotiations and consultation between the Government and members of

the Civil Service,

- the settlement of disputes,

- other matters concerning the relationship between the Government and the Civil Service.

The Act outlines the terms and conditions of employment of officers employed in the Civil

Service.

1.1.10 Civil Service Regulations

The Civil Service Regulations guided by the Civil Service Act, Chapter 23:01 defines the

various positions within the Civil Service and the details of the entitlements of these positions.

The Regulations also treats with various areas such as probation periods, secondment,

remuneration, increments, allowances, payment of pensions and gratuities and other matters

relating to officers.

An amendment to the Regulations in 1996 made provision for the Code of Conduct.

It is recommended that copies of the Regulations and Code of Conduct should be given to

every officer on their first appointment by the Public Service Commission by which he was

appointed together with his letter of appointment.

The Code of Conduct in the Civil Service Regulation deals with the conduct of an officer while

the Public Service Commission Regulations defines the method for dealing with an officer‟s

discipline and the relevant disciplinary action to be taken.

1.1.11 Civil Service (External Affairs) Regulations

The Civil Service (External Affairs) Regulations established under the Civil Service Act,

provides detailed requirements for Foreign Service Officers at the various Missions and the

entitlements to those Officers. Areas addressed under the Regulations are as follows:

Entry into the Foreign Service;

Postings to and from the Missions;

Allowances and other benefits;

Housing accommodations;

Leave and leave passage; and

Conduct of officers assigned to the Missions.

1.1.12 Public Service Commission Regulations, 1966

The Public Service Commission Regulations defines the following:

15

The “Public Service” includes the Civil Service, the Fire Service, the Prison Service, and for

the purposes of Section 53 of the Education Act, shall be deemed to include the Teaching

Service.

An “officer” means a person employed in that part of the Public Service established

respectively as the Civil Service, the Fire Service, the Prison Service, or any other service in

the Public Service who is subject to the jurisdiction of the Commission and, for the purposes of

Section 53 of the Education Act, shall be deemed to include all persons employed in the

Teaching Service.

A “Public Office” includes the Civil Service, the Fire Service, the Prison Service, and for the

purposes of Section 53 of the Education Act, shall be deemed to include the Teaching Service.

The Public Service Commission Regulations addresses the following areas within the Public

Service:

1. Appointments

2. Promotions

3. Transfers

4. Staff reports

5. Resignations

6. Retirement

7. Termination of appointments

The Civil Service Regulations also deals with the recruitment of officers as well as the terms

and conditions of these officers. The Public Service Regulations provides all officers and in

particular the Internal Auditor with the necessary guidance and knowledge in interpreting

matters listed above.

The Civil Service Act, Chapter 23:01 amended in 1966 provides for a Code of Conduct which

addresses the general conduct of a Civil Servant whereas the methods for dealing with Public

Officers‟ discipline and disciplinary actions are covered by the Public Service Commissions

Regulations.

The Internal Auditor in the conduct of the audit must be knowledgeable of the following laws

in relation to the various bodies:

1. The Civil Service Act, Chapter 23:01

2. The Fire Service Act, Chapter 23:01

3. The Prison Service Act, Chapter:13:02

4. The Police Service Act, Chapter: 15:01

5. The Education Act, Chapter 39:01

6. The Statutory Authorities Act, Chapter 34:01

The various Acts, Regulations, Instructions and Circulars are some of the main tools used by

Internal Auditors. The Internal Auditor must be knowledgeable of all aspects in order to

interpret and apply them to accounting transactions, verify compliance with the relevant laws

and provide advice and recommendations to his Accounting Officer.

The Internal Auditor, in assessing and reviewing the existing internal controls provides

Accounting Officers with an independent assessment of the Department‟s internal controls and

16

risk management framework and policies. This promotes reliability of information provided

and used in the decision-making process.

Summary to this Section- The legislative framework – specific to Government of the

Republic of Trinidad and Tobago provides guidance and

assists the internal auditors in their daily function and is

MANDATORY as tools to be used in all Internal Audit and

Accounting Units in the Public Service.

1.2 THE CHANGING ENVIORNMENT OF INTERNAL AUDITING

The increasing demand for good governance and transparency by the citizenry in the use of

taxpayer‟s dollars has impacted the way in which organizations conducted their businesses in

the past. In order to facilitate this demand for good governance and transparency and in

keeping with Government‟s mission and vision, the Public Service business processes,

communication techniques, and delivery services are continuously being upgraded and

transformed.

In this changing environment where the pace of Legislative Reform tends to lag behind, the

Internal Auditor is met with challenges in carrying out his responsibilities. In order to cope

with these challenges, the Internal Auditor must adopt relevant Standards and Tools from

internationally recognized Auditing and Accounting bodies in the conduct of their audits.

In the past the focus of Internal Audit activities within the Public Service was in the areas of

compliance, independence, post-auditing and auditing in a manual environment. This

traditional approach has continued in audit activities in the current environment. Internal

Auditors must now enhance their approach in order to fulfill their audit responsibilities in this

continuously evolving environment.

1.2.1 Compliance vs. Risk Management

Presently Internal Auditors are primarily concerned with checking accounting transactions

(historical) for compliance with financial laws. Checks are transaction based with a financial

focus in accordance with the relevant authorities and adherence to prescribed policies,

procedures and systems.

While compliance to relevant authorities, policies and procedures continues to be important,

the way in which compliance is currently being carried out must now change to compliance

with a risk focus. The Internal Auditor must be able to assess whether the existing controls are

adequate and relevant in addressing existing and potential risks which can prevent/delay the

organization achieving its objective.

The Committee of Sponsoring Organizations of the Treadway Commission (COSO), an

internationally recognized body gives guidance on monitoring internal controls systems. COSO

recognizes that risk changes over time and as such internal control systems need to be

reassessed for relevance and must address new risks as they emerge.

Ongoing assessment is recommended through the monitoring and evaluation of the

organization‟s internal control system and should be able to ascertain whether:

17

- management needs to reconsider the design of the existing controls when risk changes

and

- the controls which were designed to reduce risk at an acceptable level, continues to

operate effectively.

With ongoing assessments and the efficient and effective management of risks through strong

internal controls, the organization is able to have:

- more efficient , reliable and cost effective delivery of services to it‟s customers;

- more reliable decisions;

- innovation;

- minimal waste and fraud;

- better value for money through the efficient use of resources;

- improved project and programme management – better outputs and outcomes.

Once risks are mitigated, the organization‟s performance will improve and the likelihood of its

strategic and current objectives being achieved will increase.

1.2.2 Manual Environment vs. Information Technology Environment

Internal Auditors have traditionally operated in a paper based environment within the Public

Service. Checks for completeness, accuracy and verification of accounting transactions are

carried out against the relevant hard copy documents. A manual system provides an audit trail

which allows the Auditor to trace a transaction from its source to its completion. While manual

processing has its advantages it often operates at a slower pace and is prone to a higher degree

of errors.

Government, in improving its business processes with the aim of promoting the efficiency and

timeliness of its service delivery to its customers is engaged in ongoing development and

implementation of Information Technology (IT) related systems within the Public Service.

Internal Auditors must now be able to identify and assess the controls in this computerized

environment. Auditing software is now available for use by Internal Auditors in the form of

Computer Assisted Auditing Techniques (CAAT). With CAAT tools, an auditor can review,

test and analyze an entire population of data. Some areas of testing include testing in

compliance with standards, identifying control issues, verification of balances etc.

With the continuous development in new IT systems and the upgrading of existing ones,

business processes are constantly evolving with IT driven processes. Several accounting and

reporting processes within the Public Service are undergoing changes due to the incorporation

of either partially or wholly IT applications into its processes.

With the introduction and varying complexity of computerized systems, there exists a

corresponding loss of audit trail. The Internal Auditor must now tailor his audit activities in

order to give assurance on the integrity, accuracy, validity, timeliness and completeness of

outputs derived from such systems. He must assess the controls for adequacy and relevance

which will mitigate any risk which may prevent or delay the organization‟s ability in meeting

its objectives.

Some areas of risk in an IT environment that the Internal Auditors must consider in relation to

internal controls are:

18

- Data input

- Controls that are no longer relevant

- Hardware failure

- Threats /viruses

- System failure

- Fraud – human factor

- Resource management – efficient use of

COBiT, Control Objectives for Information and related Technology, is a framework which

addresses IT governance and gives guidance to management, IT professionals and auditors

on strategy and tactics that can best contribute to the achievement of the organization‟s

objectives

A methodology consisting of recognized and accepted standards and controls which is able

to assist IT professionals in implementation, reviewing, administrating and monitoring

various IT processes of the organization is available using COBiT. It is a tool that can be

used to assist them in linking Information Technology and control practices and addresses

the needs of IT governance and the integrity of information and information systems.

COBiT can be used by the Internal Auditor to:

- establish and review control baselines and standards:

- facilitate and creates performance metrics for risk assessments

- develop audit plan

- facilitate the audit

- manage residual risk

- issue control advisory and recommendations to IT groups.

While there is currently no legislation on auditing in an IT environment in the Public Service,

the Treasury advises that the principles with respect to COBiT be incorporated into the design

of their audit work programme. In this regard, the Internal Auditor must consult with the

Treasury Division for guidance on these matters.

1.2.3 Independence - Location vs. Mental Attitude

It is usual for Internal Audit Units within Ministries/Departments to be set up separately from

the Accounting Units for which most of its audit activities are carried out. This was seen to

promote the independence of the Internal Auditor. While independence is encouraged by

separate location, the need for independence must shift to one where it is more a state of mind.

In an era of new accountability and control there is a need for greater transparency and

accountability in the use of public funds.

The Internal Auditor, in meeting his responsibilities must conduct the audit in line with the

organization objectives for transparency and accountability. This will require the Internal

Auditor to develop a sound working relationship with management and relevant staff at all

levels. The internal auditor‟s knowledge and understanding of the organization will assist in

building effective relationships and in evaluating and improving the effectiveness of risk

management, internal controls and governance processes. Also, an effective and well run audit

team will be sought out for services, information and guidance.

19

The Internal Auditor must analyze the strengths and weaknesses of the organization‟s internal

controls, considering its governance, organizational culture, and related threats and opportunities

for improvement which can affect whether the organization is able to achieve its goals.

Internal Auditors may be called upon to advice on controls necessary in the development of

new systems for the organization and may also be involved in the auditing of those systems for

efficiency and effectiveness of the controls in place. In order to maintain independence in these

circumstances, Audit Committees within the Organizations can be set up to review the Audit

Report of the Internal Auditor.

Independence and objectivity continues to be required of the Internal Auditor in the

performance of his duties. He must have an unbiased mental attitude in the performance of his

engagements in such a manner that the quality and integrity of his work is not compromised in

any way.

1.2.4 Post-Auditing vs. Ongoing Audits

The work viewed by the Internal Auditor has been primarily historical in nature. Upon

completion of the transaction process, the Internal Auditor verifies the various accounting

transactions for compliance, accuracy and completeness. Errors and irregularities are often

discovered at this stage. With the emphasis on good governance and transparency this

continued approach to auditing will not mitigate impending risks. Risk-based auditing allows

the Internal Auditor to continuously assess new and emerging risk and to review existing

policies and procedures in order to strengthen where necessary. Reports from ongoing audits

may recommend new controls, where needed, in order to safeguard and use the resources of the

organization in an efficient manner, add value to and improve its operations.

1.3 INTERNATIONAL STANDARDS

Internal Auditing is conducted in a wide range of organizations diverse in their legal and

cultural environment. The complexity, size, structure and purpose are unique to each

organization. While differences may affect the practice of Internal Auditing in any given

environment, the Institute of Internal Auditors International Standards for Professional Practice

of Internal Auditing (Standards) is essential in providing guidelines with respect to the conduct

of the audit.

The purpose of the Standards is to:

Delineate basic principles that represent the practice of internal auditing;

Provide a framework for performing and promoting a broad range of value-added

internal auditing;

Establish the basis for the evaluation of internal audit performance;

Foster improved organizational processes and operations.

1.3.1 International Best Practice

The Institute of Internal Auditors (IIA) - Internal Auditing Standards

20

The Institute of Internal Auditors (IIA) is an international organization of internal auditing

professionals which sets guidance for Internal Auditors. Developed under the IIA is the

International Professional Practices Framework (IPPF) and its scope has been narrowed to

include only authoritative guidance which is categorized under the following two areas:

1. Mandatory:

i. The Definition of Internal Auditing; ( defined in the Introduction on page iii)

ii. The International Standards for the Professional Practice of Internal Auditing;

and

iii. The Code of Ethics.

2. Strongly Recommended:

i. Position Papers;

ii. Practice Advisories; and

iii. Practice Guides.

The Standards addressed under the International Professional Practices Framework are as

follows:

- Attribute Standards

- Performance Standards

- Practice Advisories to the Standards

- Assumption of Non-Audit Duties

- Assurance

- Board and Senior Management Reporting

- Chief Audit Executive Responsibilities

- Compliance with Standards

- Consulting

- Disclosures

- Engagement Communication

- Engagement Performance

- Engagement Planning and Scope

- Engagement Work papers

- Governance

- Independence & Objectivity

- Internal Control

- Outsourcing or Co-sourcing

- Proficiency and Due care

- Quality Assurance and improvement Program

- Resource Management

- Risked-based Planning

- Risk management and Assessment

1.3.2 The Code of Ethics

The Code of Ethics of the Institute of Internal Auditors (IIA) are principles relevant to the

profession and practice of internal auditing, and the rules of Conduct that describes behavior

expected of internal auditors. The Code of Ethics applies to both individuals and entities that

21

provide internal audit services. The purpose of the Code of Ethics is to promote an ethical

culture in the global profession of internal auditing.

Although it is not mandatory for Internal Auditors within the Public Service and State

enterprises to be members of the IIA, registered members in the Public Service are governed

by the Code of Ethics which include Principles that is relevant to the profession and practice of

internal auditors and the rules of conduct which are intended to guide the ethical conduct of

internal auditors.

Founded on the trust placed in its objectives assurance with respect to Governance, Risk

Management and Control, the Code of Ethics is appropriate and necessary in the Internal

Auditing profession.

1.3.2.1 Code of Ethics – Principles

Internal auditors are expected to apply and uphold the following principles:

i. Integrity

The integrity of internal auditors establishes trust and thus provides the basis

for reliance on their judgment.

ii. Objectivity

Internal auditors exhibit the highest level of professional objectivity in

gathering, evaluating, and communicating information about the activity or

process being examined. Internal auditors make a balanced assessment of

all the relevant circumstances and are not unduly influenced by their own

interests or by others in forming judgments.

iii. Confidentiality

Internal auditors respect the value and ownership of information they

receive and do not disclose information without appropriate authority

unless there is a legal or professional obligation to do so.

iv. Competency

Internal auditors apply the knowledge, skills, and experience needed in the

performance of internal audit services.

1.3.2.2 Rules of Conduct

i. Integrity

In demonstrating integrity, Internal auditors shall:

Perform their work with honesty, diligence, and responsibility;

Observe the law and make disclosures expected by the law and the profession;

22

Not knowingly be a party to any illegal activity, or engage in acts that are discreditable

to the profession of internal auditing or to the organization;

Respect and contribute to the legitimate and ethical objectives of the organization.

ii. Objectivity

Internal auditors shall:

Not participate in any activity or relationship that may impair or be presumed to impair

their unbiased assessment. This participation includes those activities or relationships

that may be in conflict with the interests of the organization;

Not accept anything that may impair or be presumed to impair their professional

judgment;

Disclose all material facts known to them that, if not disclosed, may distort the

reporting of activities under review.

iii. Confidentiality

Internal auditors shall:

Be prudent in the use and protection of information acquired in the course of their

duties;

Not use information for any personal gain or in any manner that would be contrary to

the law or detrimental to the legitimate and ethical objectives of the organization.

iv. Competency

Internal auditors shall:

Engage only in those services for which they have the necessary knowledge, skills, and

experience;

Perform internal audit services in accordance with the International Standards for the

Professional Practice of Internal Auditing;

Continually improve their proficiency and the effectiveness and quality of their

services.

Refer to Appendix 1.3.2A for the full list of the Code of Ethics.

1.3.3 International Auditing Standards

For more specific guidance, users of this manual should refer to Appendix 1.3.3A for the full

list of the relevant Standards. Where an appropriate standard was not developed to address an

area within the public sector environment, the Treasury Division will advise on the controls

to be used.

Refer to appendix 1.3.3A for relevant standards.

23

1.4 THE COMMITTEE OF SPONSORING ORGANIZATIONS (COSO) –

TREADWAY COMISSION

In 1992, five U.S. accounting and finance professional groups, in an alliance known as the

Committee of Sponsoring Organizations of the Treadway Commission (COSO) introduced the

Internal Control – Integrated Framework (the COSO Framework), a comprehensive report on

internal controls.

The motivation for the COSO report was the concern about the lack of uniform internal control

standards in organizations. The COSO framework is meant for managers and auditors to use in

developing and evaluating internal control systems.

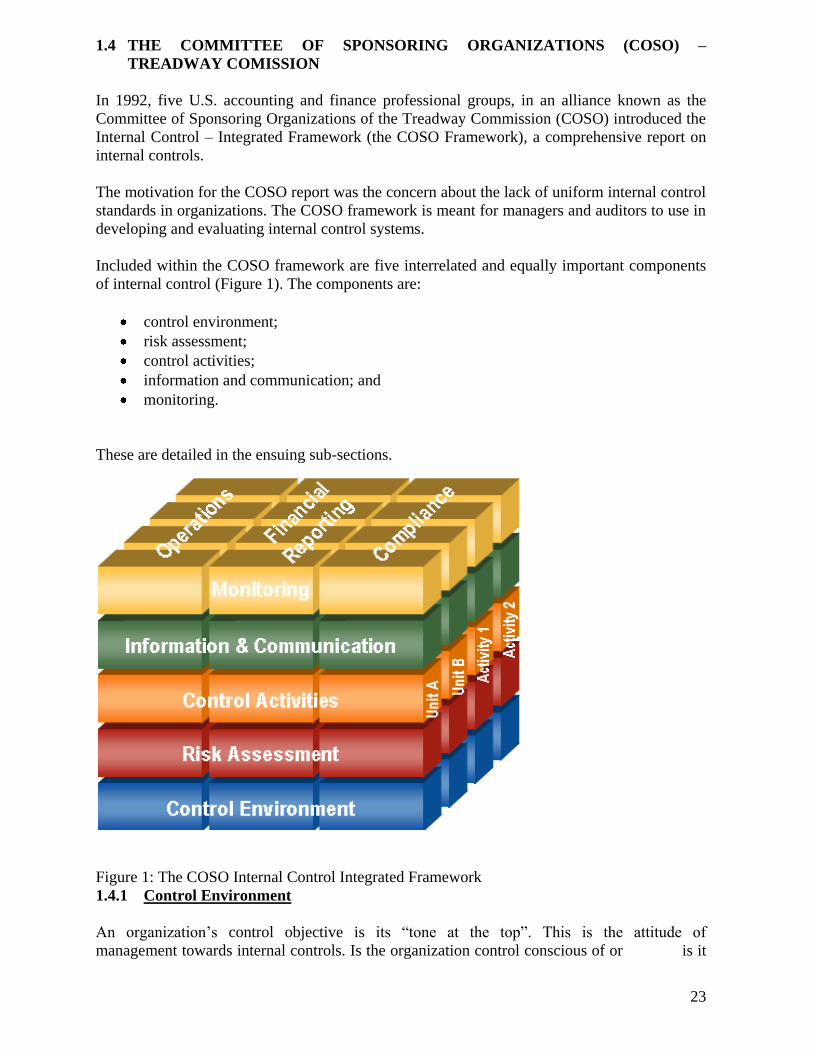

Included within the COSO framework are five interrelated and equally important components

of internal control (Figure 1). The components are:

control environment;

risk assessment;

control activities;

information and communication; and

monitoring.

These are detailed in the ensuing sub-sections.

Figure 1: The COSO Internal Control Integrated Framework

1.4.1 Control Environment

An organization‟s control objective is its “tone at the top”. This is the attitude of

management towards internal controls. Is the organization control conscious of or is it

24

relatively indifferent to internal controls? The components of the control environment

are as follows:

1. Integrity and Ethical Values - sound integrity and ethical values, particularly of top

management, are developed and understood and set the standard of conduct for

financial reporting.

2. Management - management understands and exercises oversight responsibility related

to financial reporting and related internal control.

3. Management‟s Philosophy and Operating Style - Management‟s philosophy and

operating style support achieving effective internal control over financial reporting.

4. Organizational Structure - the Company‟s organizational structure supports effective

internal control over financial reporting.

5. Financial Reporting Competencies - the Company retains individuals competent in

financial reporting and related oversight roles.

6. Authority and Responsibility - Management and employees are assigned appropriate

levels of authority and responsibility to facilitate effective internal control over

financial reporting.

7. Human Resources - Human resource policies and practices are designed and

implemented to facilitate effective internal control over financial reporting.

1.4.2 Risk assessment

The COSO report recognizes risk assessment as an important component of internal

control. The enterprise‟s risk framework will provide the organization with guidance

in developing plans to identify, measure, evaluate, and respond to risk. In assessing

risk internal auditors should consider the different types of risk as follows:

Financial Reporting Risks - the Company identifies and analyzes risks to the

achievement of financial reporting objectives as a basis for determining how the risks

should be managed.

Fraud Risk - the potential for material mis-statement due to fraud is explicitly

considered in assessing risks to the achievement of financial reporting

objectives.

1.4.3 Control activities

Control Activities are specific internal control procedures and policies. Examples are

authorizations, approvals, passwords, and segregation of duties. These are the heart of

internal controls. The activities are as follows:

1. Integration with Risk Assessment - Actions are taken to address risks to the

achievement of financial reporting objectives.

25

2. Selection and Development of Control Activities - Control activities are selected and

developed considering their cost and potential effectiveness in mitigating risks to the

achievement of financial reporting objectives.

3. Policies and Procedures - Policies related to reliable financial reporting are

established and communicated throughout the company, with corresponding

procedures resulting in management directives being carried out.

4. Information Technology - Information technology controls, where applicable, are

designed and implemented to support the achievement of financial reporting

objectives.

1.4.4 Information and Communication

Information and communication refers to the need for the organization to ensure that it

obtains and communicates the information needed to carry out management strategies and

objectives. The information may be internal or external to the organization. That is,

management must communicate internal control policies and procedures across the

organization, and to related parties outside the organization.

Types of information/communication are as follows:

1. Financial Reporting Information - Pertinent information is identified, captured, used at

all levels of the company, and distributed in a form and within a timeframe that

supports the achievement of financial reporting objectives.

2. Internal Control Information - Information needed to facilitate the functioning of other

control components is identified, captured, used and distributed in a form and within a

timeframe that enables personnel to carry out their internal control responsibilities.

3. Internal Communication - Communications enable and support understanding and

execution of internal control objectives, processes and individual responsibilities at all

levels of the organization.

4. External Communication - Matters affecting the achievement of financial reporting

objectives are communicated to outside parties.

1.4.5 Monitoring

COSO calls for continuous monitoring of an internal control system. This may be

accomplished by regular audits and evaluation, as well as by constant attention to

internal controls. Monitoring consists of:

1. Ongoing Monitoring and Separate Evaluations - Ongoing monitoring and/or separate

evaluations enable management to determine whether the other components of internal

control over financial reporting continue to function over time.

2. Reporting Deficiencies - Internal control deficiencies are identified and communicated

in a timely manner to those parties responsible for taking corrective action, and to

management and the Board as appropriate.

26

Four of the components of the COSO framework relate to the design and operation of the

system of internal control. These are:

control environment;

risk assessment;

control activities;

information and communication.

The fifth component- monitoring, is designed to ensure that internal control continues to

operate effectively.

The framework is designed to assist businesses and other organizations in assessing and

enhancing their internal control systems. IT provides a set of 20 basic principles drawn

directly from the five components mentioned above.

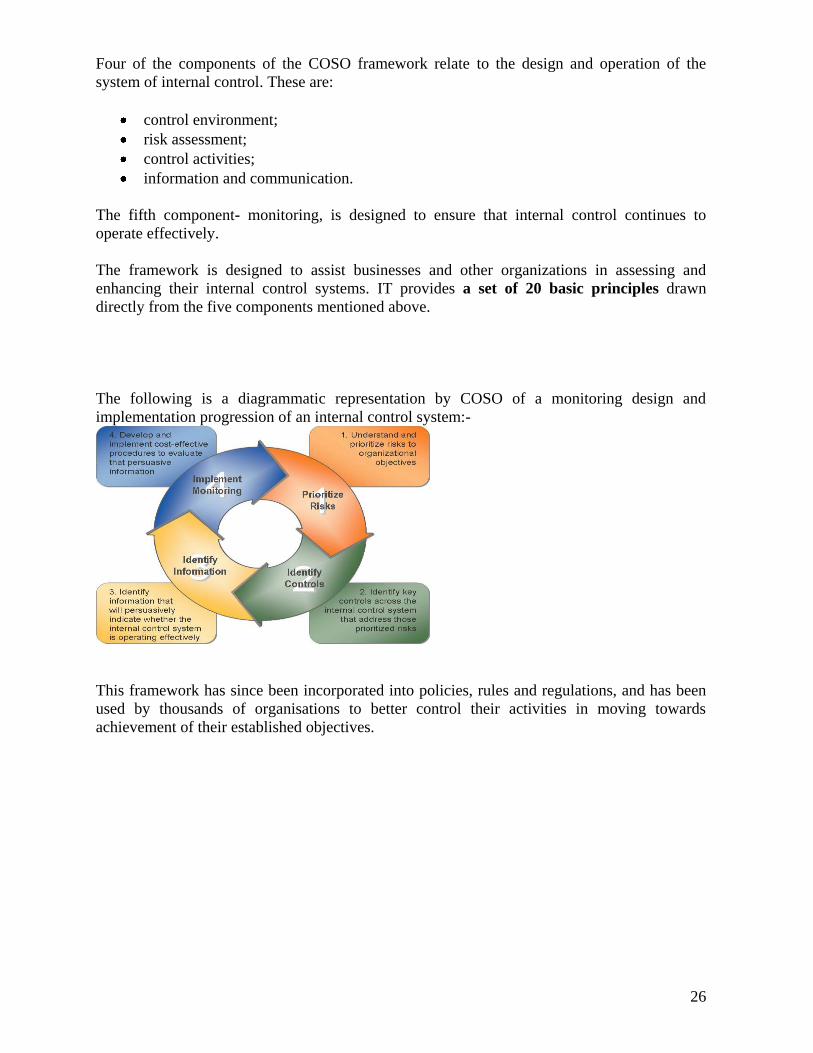

The following is a diagrammatic representation by COSO of a monitoring design and

implementation progression of an internal control system:-

This framework has since been incorporated into policies, rules and regulations, and has been

used by thousands of organisations to better control their activities in moving towards

achievement of their established objectives.

27

1.5 CRITERIA OF CONTROL COMMITTEE (COCO)

The Canadian Criteria of Control Committee (CoCo) was an initiative of the Canadian Institute

of Chartered Accountants to strengthen control and governance. According to CoCo the

essence of control in any organization is a combination of the organization‟s purpose,

commitment, and capability, monitoring and learning.

In CoCo, control entails all the elements of an organization which taken together, support

people in the achievement of the organization‟s objectives.

The elements include:

resources

systems

processes

culture

structure and

tasks

SUMMARY:

While it is management‟s responsibility to ensure that the organisation has a strong system of

internal controls, the Internal Auditor plays an important role in evaluating the effectiveness of

the internal control system and contributes to its ongoing effectiveness by significantly

monitoring internal controls in the organisation. Internal Auditors as well as the management

team can use the above framework as part of the process of improving the effectiveness and

efficiency of their internal control systems.

In order to have assurance that the controls are adequate, the Internal Auditor in the Public

Service can incorporate the above principles into their work programme. In so doing, they must

do the following:

i. Understand the organization‟s risks and prioritize in accordance with its objectives.

This process can influence management decisions regarding the type,

timing and extent of monitoring in relation to its internal controls. ii. Identify the controls which will address the existing and potential risk. With the

prioritization of risks, key controls can be identified within the organization‟s internal

control system. With key controls identified, monitoring resources of the organization

can be allocated where they can provide the most value. iii. Identify information which will indicate persuasively whether the controls selected are

operating effectively. This information is used by evaluators of the internal control system in

order to support a conclusion on whether or not the

system is operating effectively.

28

iv. Develop and implement cost effective procedures in order to evaluate persuasive

information supporting the conclusion that the internal control system is operating

effectively. Ongoing assessment of the monitoring procedures and/or evaluating and

analyzing information supporting conclusions on the effectiveness of the internal controls can

manage or mitigate identified risks.

1.6 COBIT – CONTROL OBJECTIVES FOR INFORMATION AND

RELATED TECHNOLOGY

1.6.1 What is COBIT

With the increasing reliance on Information Technology in business processes within

organizations, Managers need assurance that the information used satisfies business objectives.

Information must have and conform to characteristics which include – Effectiveness,

Efficiency, Confidentiality, Integrity, Availability, Compliance, and Reliability. This is critical

in influencing decisions made by managers and is useful for the organization‟s business

processes with the aim of achieving its objectives.

As a result of this increasing reliance on IT, the need for standards governing the IT processes

adopted by managers became necessary. The institute of IT Governance, established under the

Information Systems Audit and Control Association (ISACA) created the Control Objectives

for Information and Related Technology (CobiT).

CobiT, a tool primarily designed for use by Auditors has evolved into a management resource

due to the increasing need for IT governance in addressing current and future risks. It provides

management with a foundation upon which IT related decisions and investments can be based

and assists them in understanding their IT systems. It also assists managers in deciding on the

level of security and controls necessary to protect the organization‟s assets through the

development of an IT governance model. It includes internal and external stakeholders who

provide IT services and who have a control/risk responsibility.

The CobiT framework is based on the principle that the enterprise needs information for

decision making and therefore –

- requires information to achieve its objectives,

- needs information to invest in its IT resources and

- needs information to manage and control its IT resources.

29

This is best illustrated in the following diagram

1.6.2 Benefits of implementing CobiT

The use of CobiT as a governance framework over IT includes:

Better alignment, based on a business focus

A view, understandable to management, of what IT does

Clear ownership and responsibilities, based on process orientation

General acceptability with third parties and regulators

Shared understanding amongst all stakeholders, based on a common language

The use of COBIT as a tool must not be interpreted as any of the following and is therefore

not:

Audit Software

An IT audit plan

An IT Internal Audit work program

An IT Audit testing plan

Guide on how to Audit IT

The CobiT framework helps identify risks and the controls which have an impact on the

organization. It is divided into four distinct groups or domains which address these risks and

controls. Within each of these groups, guidelines are provided to analyze and understand

internal controls in the organization‟s IT resources. It provides its users with a set of generally

accepted measures, indicators, processes and best practices to assist them in analyzing and

evaluating IT governance. With the use of CobiT, Auditors are able to identify and assess IT

controls within the company‟s IT environment and to provide advice to management on these

matters. It also assists them in corroborating their audit findings and in substantiating their

opinions.

Business

Requirements which

responds to

Enterprise

Information

drive the

investments in

COBIT

IT Processes

IT Resources

to deliver that are

used by

30

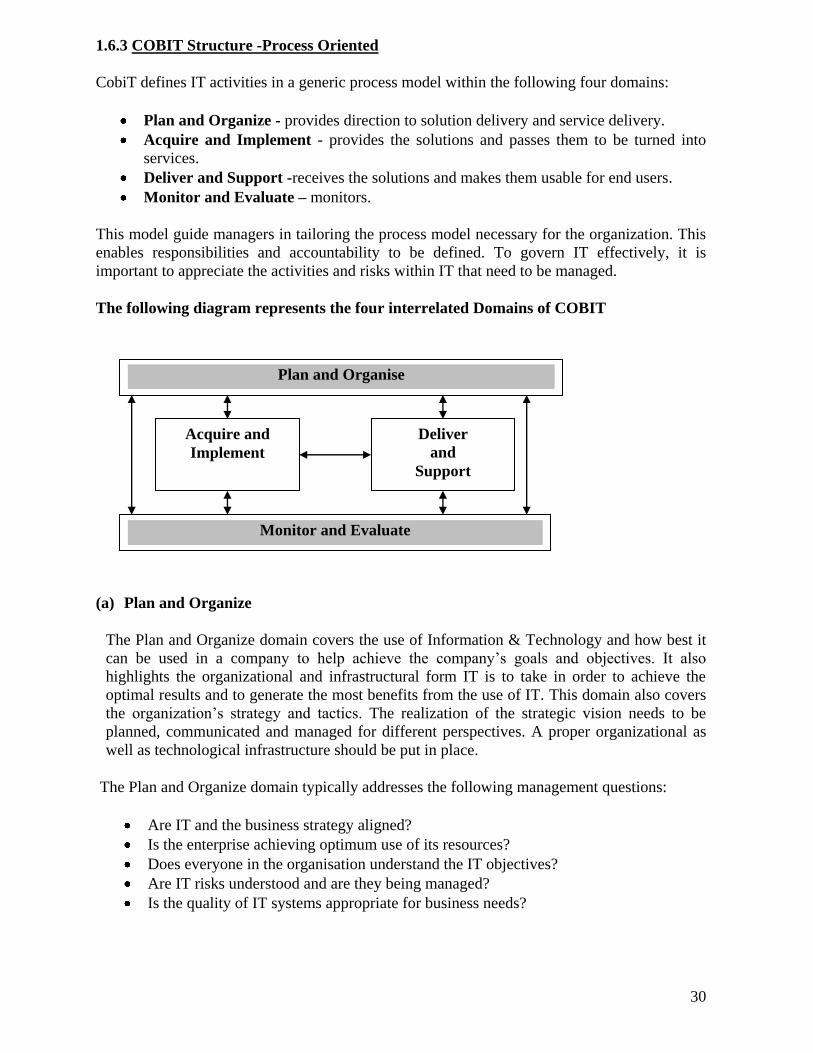

1.6.3 COBIT Structure -Process Oriented

CobiT defines IT activities in a generic process model within the following four domains:

Plan and Organize - provides direction to solution delivery and service delivery.

Acquire and Implement - provides the solutions and passes them to be turned into

services.

Deliver and Support -receives the solutions and makes them usable for end users.

Monitor and Evaluate – monitors.

This model guide managers in tailoring the process model necessary for the organization. This

enables responsibilities and accountability to be defined. To govern IT effectively, it is

important to appreciate the activities and risks within IT that need to be managed.

The following diagram represents the four interrelated Domains of COBIT

(a) Plan and Organize

The Plan and Organize domain covers the use of Information & Technology and how best it

can be used in a company to help achieve the company‟s goals and objectives. It also

highlights the organizational and infrastructural form IT is to take in order to achieve the

optimal results and to generate the most benefits from the use of IT. This domain also covers

the organization‟s strategy and tactics. The realization of the strategic vision needs to be

planned, communicated and managed for different perspectives. A proper organizational as

well as technological infrastructure should be put in place.

The Plan and Organize domain typically addresses the following management questions:

Are IT and the business strategy aligned?

Is the enterprise achieving optimum use of its resources?

Does everyone in the organisation understand the IT objectives?

Are IT risks understood and are they being managed?

Is the quality of IT systems appropriate for business needs?

Plan and Organise

Acquire and

Implement

Deliver

and

Support

Monitor and Evaluate

31

(b) Acquire and Implement

The Acquire and Implement domain covers identifying IT requirements, acquiring the

technology, and implementing it within the company‟s current business processes. This domain

also addresses the development of a maintenance plan that a company should adopt in order to

prolong the life of an IT system and its components. Changes in and maintenance of existing

systems are covered by this domain to ensure that the solutions continue to meet business

objectives.

The Acquire and Implement domain addresses the following management questions:

Are new projects likely to deliver solutions that meet business needs?

Are new projects likely to be delivered on time and within budget?

Will the new systems work properly when implemented?

Will changes be made without upsetting current business operations?

(c) Deliver and Support

The Deliver and Support domain focuses on the delivery aspects of the information

technology. It covers areas such as the execution of the applications within the IT system and

its results as well as the support processes that enable the effective and efficient execution of

these IT systems. These support processes includes service delivery, management of security

and continuity, service support for users, training, and management of data and operational

facilities.

The Deliver and Support domain addresses the following management questions:

Are IT services being delivered in line with business priorities?

Are IT costs optimised?

Is the workforce able to use the IT systems productively and safely?

Are adequate controls for confidentiality, integrity and availability of information in

place for information security?

(d) Monitor and Evaluate

The Monitor and Evaluate domain addresses a company‟s strategy in assessing the needs of the

company and whether or not the current system still meets the objectives for which it was

designed and the controls necessary to comply with regulatory requirements and governance. It

covers the independent assessment by auditors of the effectiveness of the IT System in its

ability to meet business objectives.

The Monitor and Evaluate domain addresses the following management questions:

Is IT performance measured to detect problems before it is too late?

Does management ensure that internal controls are effective and efficient?

Can IT performance be linked back to business goals?

Are adequate controls for confidentiality, integrity and availability of information in

place for information security?

32

1.6.3.1 How does CobiT Work?

Contained under the four groups or domains of the CobiT framework are 34 high level control

objectives. Each of these high level control objectives contains several detailed control

objectives. Each of the 34 IT process can be broken down into the following steps:

Process Description

Control Objectives

Management Guidelines

Maturity Model

1.6.3.2 Control Based

Control is defined as the policies, procedures, practices and organizational structures designed

to provide reasonable assurance that business objectives will be achieved and undesired events

will be prevented or detected and corrected.

IT control objectives provide a complete set of high-level requirements to be considered by

management for effective control of each IT process.

1.6.3.3 Use of COBIT by the Internal Auditors

COBIT can be used by the Internal Auditor in the following ways:

Assisting in the development of the audit plan.

Facilitating and creating performance metrics for Risk Assessments for managers.

Facilitating the audit.

Managing Residual Risk in the organisation.

Issuing effective controls advisory in order to reduce risk and making recommendations

to the IT Department for improved efficiency.

While CobiT targets control issues, it is not a replacement for the COSO internal control

framework (which focuses on internal controls in a manual environment) but addresses the

internal controls in today‟s Information Technology environment.

The Treasury Division advises that the principles with regard to the processes of CobiT can be

found in the CobiT 4.1 booklet which will be accessed through the Treasury Division. In this

regard, the Internal Auditor can consult with the Treasury Division for guidance.

SUMMARY:-

CobiT is an internationally accepted controls-based framework for IT governance that was first

released by ISACA in 1996. The framework provides guidance to an organisation on how to

use IT resources (i.e. applications, information, infrastructure and people) to manage IT

domains, processes and activities to respond to business requirements (i.e. compliance,

effectiveness, efficiency, confidentiality, integrity, availability and reliability). Well-governed

IT practices can assist businesses in complying with laws, regulations and contractual

arrangements.

33

1.7 REPORTING RELATIONSHIPS

1.7.1 The Parliament of Trinidad and Tobago

Chapter 4, Section 39 of the Constitution of the Republic of Trinidad and Tobago makes

provision for the establishment of the Parliament and states „There shall be a Parliament of

Trinidad and Tobago which shall consist of the President, the Senate and the House of

Representatives‟

The Minister of Finance reports to Parliament on the Public Accounts of the Republic of

Trinidad and Tobago. The Minister in pursuance of his statutory obligation also lays and

presents in the House of Representatives, the Budget Speech and the Appropriation Bill.

The Budget Speech is presented and the Appropriation Bill is debated and passed in the House

of Representatives. The Bill is then brought before the Senate where it is also debated and

passed after which it is forwarded to the President of the Republic of Trinidad and Tobago for

his assent. It then becomes the Appropriation Act for the particular year.

1.7.2 The Minister of Finance

(a) Control and Management of Public Finance

The Minister of Finance under Chapter 8, Section 113 (1) and (2) of the Constitution of the

Republic of Trinidad and Tobago and the provisions of the Exchequer and Audit Act Chapter

69:01 is responsible for the management of the Consolidated Fund and the supervision, control

and direction of all matters in relation to the financial affairs of the state which are not by law

assigned to any other Minister.

(b) Authorization of Expenditure from the Consolidated Fund

Chapter 8, Section 113 (1) and (2) of the Constitution states:

(1) “The Minister responsible for finance causes to be prepared and laid before the

House of Representatives before or not later than thirty days after the

commencement of each financial year, estimates of the revenues and

expenditure of Trinidad and Tobago for that year.”

(2) “The heads of expenditure contained in the estimates, other than expenditure

charged upon the Consolidated Fund by this Constitution or any Act, shall be

included in a Bill, to be known as an Appropriation Bill, providing for the

issue from the Consolidated Fund of the sums necessary to meet that

expenditure and the appropriation of those sums for the purposes specified

therein.”

After the Appropriation Act has been passed by Parliament (see 1.7.1 above) a General

Warrant is issued by the Minister of Finance to the Comptroller of Accounts authorizing him to

make withdrawals from the Consolidated Fund within the limits approved under the Act and in

accordance with Treasury directives.

34

Further, if within any financial year it is found that the sum appropriated may be insufficient,

or that there is need to expend on an item for which no appropriation was made, or that

money may have been over-expended on an appropriated item, a supplementary estimate,

showing the sum required or spent shall be laid before the House of Representatives and the

heads of any such expenditure shall be included in a Supplementary Appropriation Bill.

If the Appropriation Act in respect of any financial year does not come into operation by the

beginning of that financial year, the Minister of Finance may authorize the withdrawal of

moneys from the Consolidated Fund to meet the expenditure necessary to carry on the

services of the Government, until the expiration of thirty (30) days from the beginning of that

financial year of the coming into operation of the Act, whichever is the earlier.

Parliament may also provide for the establishment of a Contingencies Fund, and for

authorizing the Minister of Finance to make advances from that Fund, if he is satisfied that

there has arisen an urgent and unforeseen need for expenditure for which no other provision

exists.

1.7.3 The Accounting Officer

An Accounting Officer is defined in Section 2 Part 1 of the Exchequer and Audit Act Chapter

69:01 as:

„any person appointed by the Treasury and charged with the duty of

accounting for any service in respect of which moneys have been

appropriated by the Constitution or by Parliament, or any person to whom

issues are made from the Exchequer Account.‟

The duties and responsibilities of the Accounting Officer are as follows:

An accounting officer shall be appointed by a letter addressed personally to him by the

Treasury setting out in details his duties and responsibilities.

An accounting officer shall be responsible for ensuring –

a) that the financial business of the State for which he is responsible is properly

conducted; and

b) that public funds entrusted to his care are properly safe-guarded and are applied

only to the purposes intended by Parliament.

All accounting officers are personally and pecuniary responsible for –

c) the due performance of the financial duties of their departments;

d) the proper collection and custody of all public moneys receivable by them; and

e) for any accounts rendered by them or under their authority.

It is the duty of an accounting officer to –

a) ensure that the proper system of accounting as prescribed by the

Treasury is established and maintained.

To assist Accounting Officers in the efficient execution of their duties, the Internal Auditor is

provided as a management aid and reports directly to them. Prevention and detection of fraud

is management‟s responsibilities and the Internal Auditor must be alert to risks and exposures

that could allow for fraud.

35

The Internal Auditor‟s responsibility is therefore to the Accounting Officer. The scope of work

undertaken by the Internal Auditor is determined by his Accounting Officer to whom he is

responsible. The Audit Work programme of the Internal Auditor must be approved by the

Accounting Officer; consequently, the Accounting Officer can limit or expand the extent of the

Audit Work programme.

The Accounting Officer shall be answerable to the Public Accounts Committee and is required

to attend Public Accounts Committee (PAC) meetings on any matter relating the formal

regularity and propriety of accounts of all the expenditure out of the votes for which he is

responsible.

The Accounting Officer reports to the Minister of Finance on any irregularity connected with

the public accounts that may have been discovered.

1.7.4 The Treasury Division

In accordance with Section (2) Part I of the Exchequer and Audit Act Chapter 69:01:

“Treasury means the Minister, and includes such officer or officers in the Ministry of Finance

as may be deputed by the Minister to exercise powers and to perform duties under this act.”

The Minister of Finance is responsible for the control and management of the financial affairs

of the State. One of the core agencies through which this is accomplished is the Treasury

Division.

The Comptroller of Accounts is the Head of the Treasury Division as deputed by the Minister

of Finance and is charged with the responsibility of superintending the expenditure of public

moneys and ensuring that proper arrangements for accounting to the House of Representatives

are made.

Responsibilities

The core responsibilities of the Treasury Division are as follows:

to provide financial management and accounting services to Ministries and

Departments;

to produce the consolidated accounts of the Republic of Trinidad and Tobago;

to administer superannuation and/or terminal benefits to retired public

officers/beneficiaries;

to ensure that the appropriation account of the Republic of Trinidad and

Tobago are laid in Parliament on a timely basis.

To facilitate these operations the Treasury Division is divided into three broad functional areas

as follows:-

i. Financial Management;

ii. Treasury Management; and

iii. Pensions Management.

36

In the execution of its responsibilities for the management of the financial affairs of the State,

the Treasury Division develops implements and monitors financial management and

accounting systems throughout the Public Service. In addition, the Division is also responsible

for ensuring that the internal audit operates effectively. The Comptroller of Accounts is the

Head of the Treasury Division as deputed by the Minister of Finance and is charged with the

responsibility of superintending the expenditure of public moneys so and to ensure that proper

arrangements for accounting to the House of Representatives are made.

1.7.5 The Auditor General‟s Department

The Auditor General is appointed by the President after consultation with the Prime Minister

and The Leader of the Opposition. The office of the Auditor General is a public office, its staff

are public officers appointed in accordance with section 117 of the Constitution of the

Republic of Trinidad and Tobago. As stated in the Constitution the Auditor General, in the

exercise of his/her functions shall not be subject to the direction or control of any other person

or authority. This independence is necessary for an unbiased opinion on the accounts

examined.

The Auditor General reports annually to the Speaker, the President of the Senate and the

Minister of Finance on the Public Accounts of the Republic of Trinidad and Tobago.

In accordance with Section 25 (1) of the Exchequer and Audit Act, the Auditor General is

required to audit the accounts of Ministries, Departments and other Government Agencies to