PT Prodia Widyahusada Tbkprodia.co.id/Assets/img/Upload/Hub Investor/PRDA - 9M2017 Results...

33

PT Prodia Widyahusada Tbk 9M2017 Results Update 26 October 2017

Transcript of PT Prodia Widyahusada Tbkprodia.co.id/Assets/img/Upload/Hub Investor/PRDA - 9M2017 Results...

PT ProdiaWidyahusada Tbk

9M2017 Results Update26 October 2017

2

This presentation has been prepared by PT Prodia Widyahusada (the "Company") solely for use in connection with the analyst presentation relating to theCompany. The information contained in this presentation is strictly confidential and is provided to you solely for your reference. By viewing all or part of thispresentation, you agree to maintain confidentiality regarding the information disclosed in this presentation as set out in the confidentiality agreement signed byyou and to be bound by the limitations set forth herein. Any failure to comply with these restrictions may constitute a violation of applicable securities laws.

This presentation is for information purposes only and does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe forany securities, nor should it or any part of it from the basis of, or be relied in any connection with, any contract or commitment whatsoever. Any such purchaseshould be made solely on the basis of the information contained in the final offering memorandum relating to such securities.

Neither this presentation nor any copy of portion of it may be sent or taken, transmitted or distributed, directly or indirectly, in or into Japan,Australia, Canada or the United States or any other jurisdiction which prohibits the same. The securities have not been, and will not be registeredunder the U.S. Securities Act of 1933, as amended (the "Securities Act"), or the securities laws of any state of the United States or any otherjurisdictions and the securities may not be offered or sold within the United States except pursuant to an exemption from, or in a transaction notsubject to, the registration requirements of the Securities Act and applicable state or local securities laws. This presentation is not for distribution in,nor does it constitute an offer for sale of the securities in the United States. The Company does not intend to offer or sell the securities of theCompany to the public in the United States. Any public offering of securities to be made in the United States would be made by means of a prospectusthat could be obtained from the Company and that would contain detailed information about the Company and management as well as financialstatements.

This presentation may not be forwarded or distributed to any other person and may not be copied or reproduced in any manner. Failure to comply with thisdirective may violate applicable laws.

This presentation includes forward-looking statements. These statements contain the words "anticipate", believe", "intend", "estimate", "expect", "plan" andwords of similar meaning. All statements other than statements of historical facts included in this presentation, including, without limitation, those regarding theCompany's financial position, business strategy, plans and objectives of management for future operations (including development plans and objectives relatingto the Company's business and services) are forward-looking statements. Such forward looking statements involve known and unknown risks, uncertainties andother important factors that could cause the actual results, performance or achievements of the Company to be materially different from results, performance orachievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on the numerous assumptions regardingthe Company's present and future business strategies and the environment in which the Company will operate, and must be read together with thoseassumptions. These forward-looking statements speak only as at the date of this presentation. Predictions, projections or forecasts of the economy or economictrends of the markets are not necessarily indicative of the future or likely performance of the Company. Past performance is not necessarily indicative of futureperformance.

The information and opinions contained in this presentation noted above are subject to change without notice.

Disclaimer

3

Contents

Investment Highlights

9M2017 Business Update

Growth Strategies

Financial Highlights

4

Contents

Investment Highlights

9M2017 Business Update

Growth Strategies

Financial Highlights

5

Contents

Investment Highlights

1. The Forefront of a Significant Indonesian Healthcare Opportunity

2. Pioneer & Market Leader in the Indonesian Independent Clinical Lab Industry

3. Largest Nation-wide Lab Network, with the Largest National Reference Lab, and a

Wholly-operated and scalable “Hub-and-Spoke” Model

4. Most-recognized Clinical Lab Brand in the Country Supported by Consistent Focus

on Quality

5. Comprehensive Service Offering that Targets Multiple Customer Segments

Supported by Strong Relationships with Healthcare Practitioners and Institutions

6. Proven track record of strong growth and financial performance

7. Experienced senior leadership and management team with deep experience in

clinical lab services and healthcare

6

Investment Highlights

The Forefront of a Significant Indonesian Healthcare Opportunity

1.1

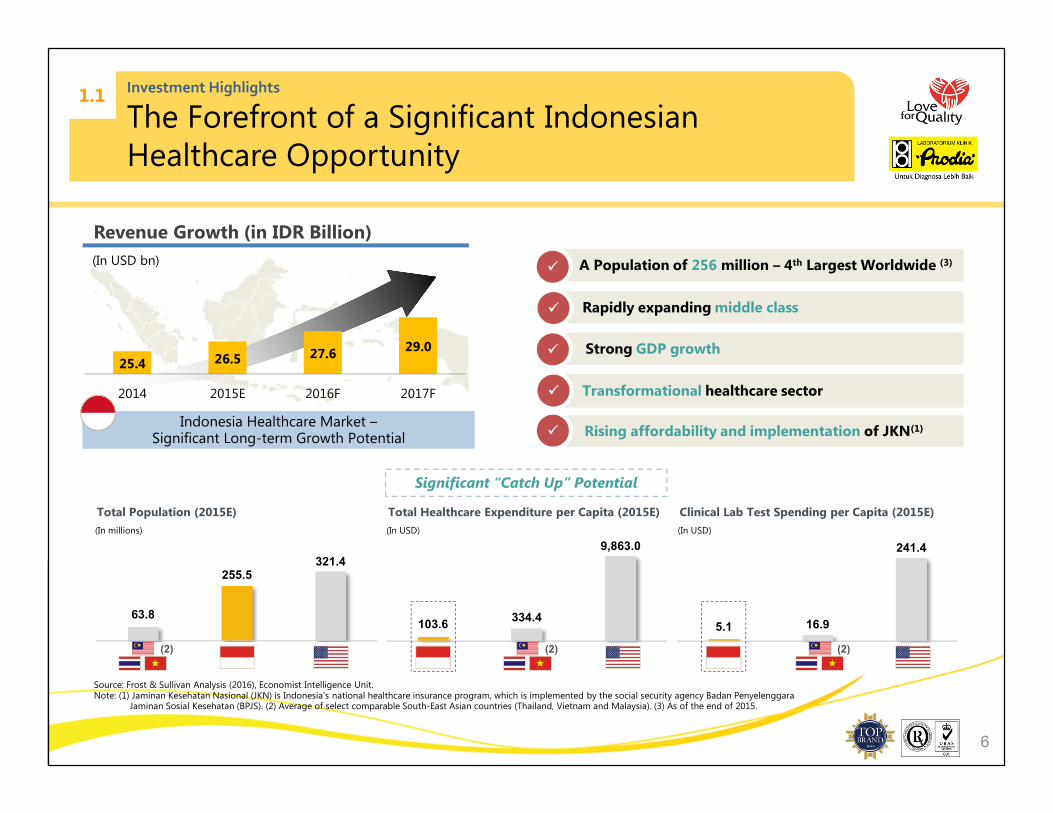

25.4 26.5 27.629.0

2014 2015E 2016F 2017F

Indonesia Healthcare Market –Significant Long-term Growth Potential

Indonesia Healthcare Market –Significant Long-term Growth Potential

Revenue Growth (in IDR Billion)

(In USD bn)

Rising affordability and implementation of JKN(1)�

Transformational healthcare sector�

Strong GDP growth�

Rapidly expanding middle class�

A Population of 256 million – 4th Largest Worldwide (3)�

103.6334.4

9,863.0

Total Healthcare Expenditure per Capita (2015E)

Source: Frost & Sullivan Analysis (2016), Economist Intelligence Unit.Note: (1) Jaminan Kesehatan Nasional (JKN) is Indonesia's national healthcare insurance program, which is implemented by the social security agency Badan Penyelenggara

Jaminan Sosial Kesehatan (BPJS). (2) Average of select comparable South-East Asian countries (Thailand, Vietnam and Malaysia). (3) As of the end of 2015.

(In USD)

Total Population (2015E) Clinical Lab Test Spending per Capita (2015E)

5.1 16.9

241.4

63.8

255.5321.4

Significant “Catch Up” Potential

(In USD)

(2) (2) (2)

(In millions)

7

Investment Highlights

Significant Growth Potential for Private Laboratories in Indonesia

1.2

2427 27 25 26 28 29

2011 2012 2013 2014 2015E 2016F 2017F

Source: Frost & Sullivan Analysis (2016).

13A-15E CAGR 0.3%

Indonesian Healthcare Market is Growing

(Market size by revenue; In USD bn)

Private Laboratory Testing Market is Growing Faster

(Market size by revenue; In USD mn)

386 435492

558615

706

817

2011 2012 2013 2014 2015E 2016F 2017F

8

2.1

No. of Labs

7th May 1973

1975 1990

1999

20102011

2012

7th Dec 2016 – IPO

7

132 labs(1)

(274 outlets, 31 provinces,

116 cities)

2017

20051990

32 38 90

1992 1996–97

� Established in Jakarta and Bandung

� Founded in Solo, Central Java

� Established Prodia ChildLab

� Became the firstlab in Indonesiato receiveNGSP certification for HbA1c diagnostic service

� Received Service Excellence Award

� First Top Brand Award

� Establishment of Prodia National Reference Lab, the first Indonesian lab clinic to receiveSNI ISO 15189international accreditation

� Became the first and only lab in Indonesia to receivedaccreditationfrom the College of American Pathologists ("CAP")

� Received SMK3 accreditation and OHSAS 2015, along with the Award as "Diagnostic Services Company of the Year 2015" from Frost & Sullivan

� Opened the first green building used for laboratories in Indonesia, Graha Prodia, in Surabaya

� In progress of opening Prodia Health Care outlets to offer wellness services

1

19732010

107

2007

99

Note: (1) Includes PNRL.

2016

� Partnerships with National University Hospital-Singapore & Specialty Lab

� Established professional management team

� Scholarships given to employees for Masters and PhD programs in biomedical sciences

� Received BNSP (Badan Nasional Sertifikasi Profesi) certification for lab technologist competency

� Became the firstclinical laboratory in Indonesia to receive international certification (ISO 9002)

2008

2009

2001–05

Investment Highlights

Pioneer in Clinical Laboratory Testing

9

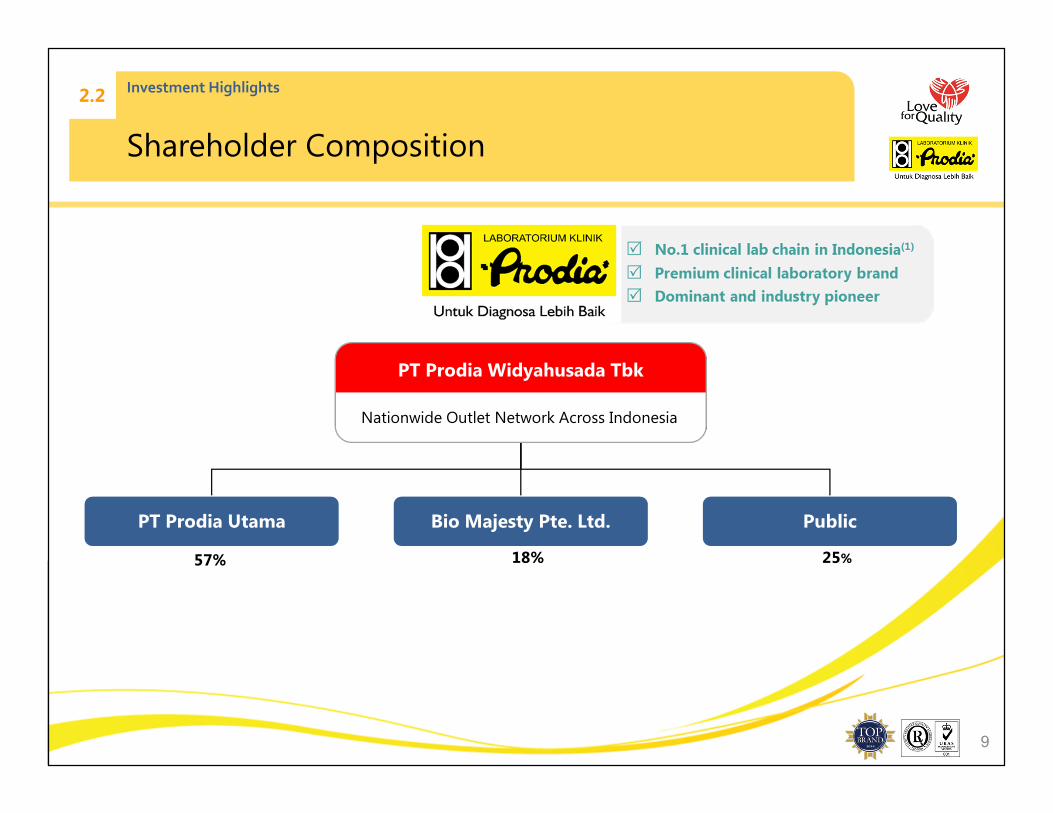

Investment Highlights

Shareholder Composition

2.2

PT Prodia Widyahusada Tbk

PT Prodia Utama Bio Majesty Pte. Ltd. Public

57% 18% 25%

Nationwide Outlet Network Across Indonesia

10

Clinical Labs

Specialty Clinic

POCOutlet

HospitalLab

20 0 23 1

Clinical Labs

Specialty Clinic

POCOutlet

HospitalLab

22 0 23 1

Investment Highlights

Largest Nationwide Network

3.1

II

I

IV

V

VI

VIIVIIISumatera

Kalimantan

Sulawesi

PapuaIII

Clinical Labs

and 1 PHC

(Upgrade PHC : 10)

Clinical Labs

and 1 PHC

(Upgrade PHC : 10)

132

and 1

132

and 1

Specialty ClinicSpecialty Clinic33

POC OutletsPOC Outlets126126

Hospital LabsHospital Labs1212

= Referral lab in Jakarta, Surabaya, Makassar and Medan

Java

Clinical

Labs

Specialty

Clinic

POC

Outlet

Hospital

Lab

33 2 33 5

III IV V

Clinical Labs

Specialty Clinic

POCOutlet

HospitalLab

15 0 5 1

Clinical Labs

Specialty Clinic

POCOutlet

HospitalLab

7 0 6 1

Clinical

Labs

Specialty

Clinic

POC

Outlet

Hospital

Lab

16 1 16 2

VI

Clinical Labs

Specialty Clinic

POCOutlet

HospitalLab

7 0 2 0

I II VII

Clinical Labs

Specialty Clinic

POCOutlet

HospitalLab

12 0 18 1

VIII

11

Investment Highlights

Scalable Hub and Spoke Model

3.2

POC Center

or POC

Collection Center

Collection / Testing Testing

� Centralized information with

integrated IT platform that

connects each lab to PNRL

Prodia National

Reference Lab

(PNRL)

� Prodia Clinical Labs,

Hospital and Other Clinics

refer tests to PNRL

Walk-in Customers

Doctor Referrals

Corporate Clients

External Referrals

Doctor

Referrals

PNRL Serves Around

2.5 Million Referral Tests

Annually. 24/7 Operation to

Fully Accommodate

Reference Needs from All

Prodia Outlets

Clinical Labs

Prodia’s National Reference Lab as the only private national reference laboratory in Indonesia accredited by the College of American Pathologists,accommodating international researches, referrals from hospitals, medical centers, and both Prodia clinical labs as well as external clinical labs.

Clinical Labs

� “Hub and spoke” model offers scalableplatform reducing turnaround time andcost

� Spokes facilitate deeper penetrationwithin region strengthening brand anddriving higher volumes

� Efficiency of a clinical laboratoryimproves with increasing test volumesmaking automated tests less expensiveand labs more cost efficient

Significant Economies of Scale Achieved

12

Investment Highlights

Most Recognized Clinical Lab Brand in Indonesia

4

Note: (1) NGSP stands for the National Glycohemoglobin Standardization Program. (2) HbA1c, also known as the haemoglobin A1c or glycated haemoglobin, is an important blood test that gives a good indication of how well your diabetes is being controlled. (3) CAP is considered the highest accreditation in the clinical lab industry worldwide.

� The only clinical lab in Indonesia accredited by College of American Pathologists (“CAP”(3))

� Received 56% of the votes from a sample of Indonesian consumers in the 2015 Top-Brand Survey

� 1st clinical laboratory in Indonesia that received international certification

� 1st and the only clinical lab in Indonesia to receive NGSP(1) certification for HbA1c(2)

diagnostic service

� 1st Indonesian clinical laboratory that received SNI ISO 15189

� All labs are owned and operated by Prodia to maintain better control and ensure consistency in quality standards

Pioneer in Indonesian Laboratory Services

Center of Excellence

Largest Lab Network and Service Offering

Leading National Reference Laboratory

Customer Focused

Quality as a Way of Life

Awards

13

Investment Highlights

Comprehensive Service Offering Targets Multiple Customer Segments

5.1

14

Most Reputable Brand

2014-2015

Investment Highlights

PRODIAMost Recognized Clinical Lab Brand

5.2

Top Brand Award

2009 - 2017

Indonesia Original Brand 2012 - 2016

Indonesia Best Brand Award (IBBA)2013 - 2016

Corporate ImageAward (IMAC)2012 - 2017

Service Quality Award 2013, 2015 - 2017

2015 - 2017

Satria Brand Award

2011 - 2017

SEA Service Excellence Award

2010-2013

Rekor Bisnis2013

Brand Champion Consumer

Awards 2015

Master Service Award

2012 - 2017

Wow Brand Award

2015 & 2017

Best E Mark2016

Frost & Sullivan Award 2015

Indonesia Most Creative Companies

2017

15

Investment Highlights

Senior Leadership and Management Team

7

Experienced, Professional Management Team with a Track Record in Delivering Superior Growth and Innovation

Diagnostic ServicesCompany of the Year 2015

- Frost & Sullivan

Top Brand Award 2017

16

Investment Highlights

Pioneer and Leader in Indonesian Independent Clinical Lab Industry

8

Key Private Independent Lab Players

No. of Clinical Laboratories

Java Outside Java

Total

Prodia 70 58 128

Kimia Farma 29 14 43

Pramita 18 5 23

Cito 19 2 21

Parahita 14 1 15

Biomedika 13 1 14

Total Clinical Labs for Next 5 Players

116

Prodia

35%

Next 5

Players

Combined

33%

Others

(786 Private

Stand-

alone Labs)

32%

Source: Frost & Sullivan analysis (2016)

No.1 Independent Clinical Lab Chain

Market Share by Revenue of Key Players (2015)

Largest and Most Diversified Laboratory Network

Number of Labs of 6 Key Players in Indonesia (2015)

17

Contents

Investment Highlights

9M2017 Business Update

Growth Strategies

Financial Highlights

18

2017 Network Developments

Clinical Lab

5-7

1

Referral Lab

& Next Gen Lab (Jakarta)

1

Specialty Clinic

2

POC Outlets

20

Hospital Laboratories

3-5

Upgrade Clinical Lab to PHC

8-10

Wilayah

3 : 73

Wilayah

1 : 21

Wilayah

4 : 44

Wilayah

6 : 35

Wilayah

7 : 9

Wilayah

8 : 31

Wilayah

2 : 14

Wilayah

5 : 46

19

Revenue Growth (in IDR Billion)

9M 2017 Revenue

986 1,081

1,198 1,359

946 1,042

2013 2014 2015 2016 9M 2016 9M 2017

� Revenue increased by 10.2% driven by double-digit sales growth from External Referral and Corporate Client customers

20

9M 2017 Number of Visit and Revenue per Visit

Number of Visits (in ‘000) Revenue per Visit (in IDR ‘000)

2,236 2,305 2,3832,482

1,742 1,790

2013 2014 2015 2016 9M 2016 9M 2017

441469

503547 543

582

2013 2014 2015 2016 9M 2016 9M 2017

� Number of visits grew year-on-year by 2.8% as check-up volume rebounds post-Ramadhanseason

� Revenue per visit continues to increase along with the introduction of new test types, as well

as double digit sales growth of External Referral and Corporate Client customers

21

Routine (~214 Tests) 90.8%

9M 2017 Customer Segments & Testing Types

Diversified Customer Base

(9M 2017 Revenue Split)

� Patients referred by doctors

� Out-of-pocket cash payment

� Individual walk-in patients

� Out-of-pocket cash payment

� Primarily samples referred by hospitals and labs

� Funded by referring Institutions on credit

� Corporate check-ups

� Funded by corporates on credit

13.7%Corporate clients

18.6%External Referral

Walk-in Customers

33.6%

Doctor Referrals

34.1%

Comprehensive Test Offering

(9M 2017 Test Volume Breakdown by Service Type)

Esoteric (~130 Tests) 3.4%

Non-Laboratory5.9%

Complementary Service Package

General Medical Check-Up Services

� Pre and post

test doctor

consultation

services

� Home

collection

services

Specialty

Clinics

� Specialized

clinical facilities

tailored to

specific

customer needs

� Include children

& women

Referral

Lab Services

� Includes both

routine and

esoteric testing

� Employs

advanced

testing

equipment

10.4 Million

Tests Performedper 9M 2017

22

9M 2017 New Testing Types

Molecular

• CT/NG RT PCR

• Warfarin Indiv Test (CYP2C & VCORC1 genotype)

• MTB/MOTT-DNA

• Telomere Analysis

• Mutation of JAK2 V617

Immunology

• Aldosteron

• ProALD Panel

• AMA M2

Others

• Fragmentation of DNA Sperm

• CBC (Complete Blood Count), Sedimentation rate, Leukocyte Count

Screening Package

• Wellness Basic/Medium/Premium Package

23

Technology to Increase Customer Satisfaction

Launched e-Pay and e-Reg

to increase distribution channel and provide easier way to register and payment system

Payment can be made through ATM Transfer and Credit Card

Customers can access their laboratory results through PRODIA apps and email

24

Contents

Investment Highlights

9M2017 Business Update

Growth Strategies

Financial Highlights

25

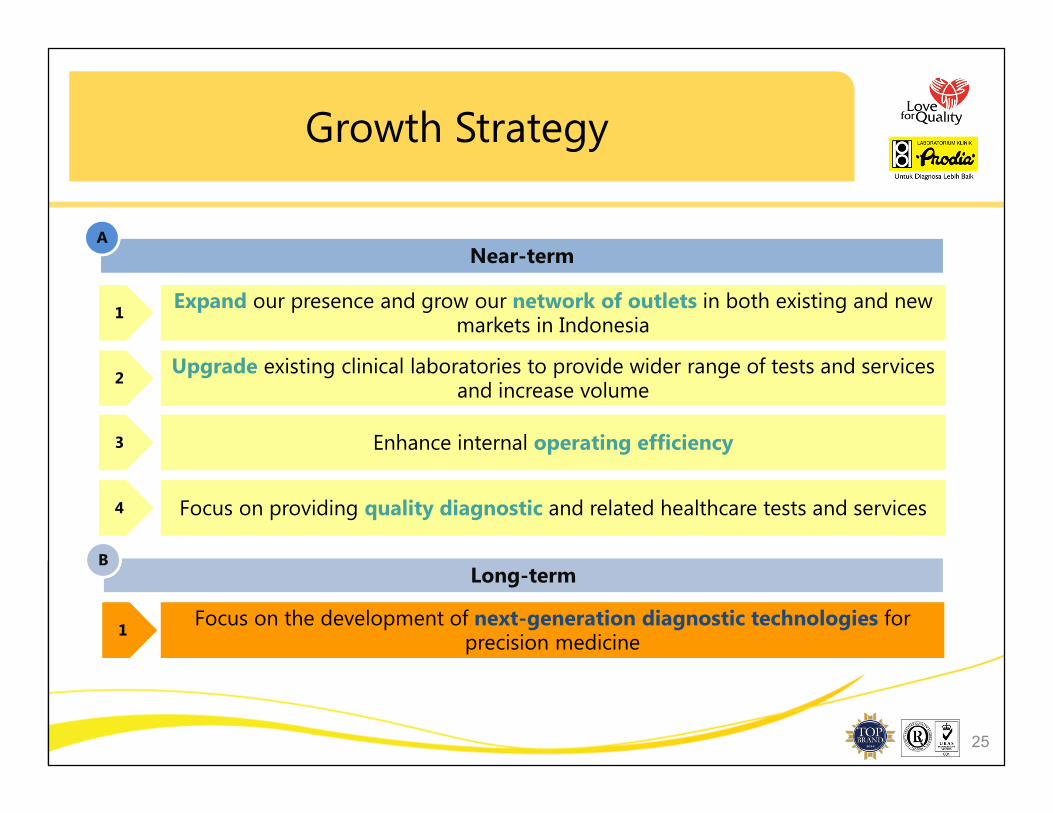

Growth Strategy

Near-term

33 Enhance internal operating efficiencyEnhance internal operating efficiency

22Upgrade existing clinical laboratories to provide wider range of tests and services

and increase volumeUpgrade existing clinical laboratories to provide wider range of tests and services

and increase volume

11Expand our presence and grow our network of outlets in both existing and new

markets in IndonesiaExpand our presence and grow our network of outlets in both existing and new

markets in Indonesia

44 Focus on providing quality diagnostic and related healthcare tests and servicesFocus on providing quality diagnostic and related healthcare tests and services

Focus on the development of next-generation diagnostic technologies for precision medicine

Focus on the development of next-generation diagnostic technologies for precision medicine

11

Long-term

A

B

26

Near Term Growth Plan

Enhance Operating Efficiency

Focus on Quality

3

4

4 regional referral labs(1)

Up to 33 additional clinical labs over next five years

Up to 20 new POC collection centers per year

13 new specialty clinics over next five years(2)

Upgrade up to 39 additional clinical labs to PHC Clinics(3)

Note: (1) Three out of Four Regional Referral Labs already opened in 2017(2) Two specialty clinics already opened in 2016 and 2017(3) Eleven PHC Clinics already added at clinical labs in 2017

5 new hospital labs per year

Expand Network of Outlets Upgrade Clinical Labs

1 2

24 Clinical Lab Improvements

Prodia’s Network Expansion Plan by 2021

27

Long-Term Strategy

Leader in Next Generation Technology

Molecular Diagnostics

The Concept of Precision Medicine

Chromatography-Mass Spectrometry

Advanced Pathology Lab

Laboratory Platforms Innovation

Immunology (Flow Cytometry) Lab

Targeted Therapy

Personalized Treatment and Prevention

� Global initiative to move towards personalized treatment and prevention

� Leverages genomics, proteomics, and metabolomics analysis

� Key to the successful offering of precision medicine is the availability of diagnostic information

Diversified Clinical Diagnostics Platform

+Scientific Talent

28

Contents

Investment Highlights

9M2017 Business Update

Growth Strategies

Financial Highlights

29

132148

175

209

111

156

13.4% 13.7% 14.6% 15.4%

11.8%

15.0%

2013 2014 2015 2016 9M 2016 9M 2017

EBITDA EBITDA Margin

EBITDA (in IDR Billion)

Financial Highlights

9M 2017 Revenue & EBITDA (Unaudited)

� EBITDA margin climbed 317 bps driven by double-digit revenue growth and improvement of raw material cost as a proportion to sales

30

Gross Profit (in IDR Billion)

Financial Highlights

9M 2017 Gross Profit & Net Income (Unaudited)

Net Income (in IDR Billion)

� Gross Profit increased by 20 bps as volume catches up and raw material cost as a proportion to sales declined

� Improvements on COGS and Operating Cost (Marketing and SG&A) management, as well as increased Financial Income supported the gain in Net Income

545

602

57.6%

57.8%

9M 2016 9M 2017

Gross Profit Margin

29

99

3.1%

9.5%

9M 2016 9M 2017

Net Income Margin

31

469 506

571 637

473 496 31

33 36

39

26 27

501 539

607 676

499 522

50.8% 49.9% 50.6% 49.7%52.7%

50.2%

2013 2014 2015 2016 9M 2016 9M 2017

Marketing Expenses

General and Administrative

Expenses (G&A)

Total

Operating Expense as % of

Total Revenue

Cost of Revenue (in IDR Billion)

Operating Expense (in IDR Billion)

337 382

429 475

333 365

47

72 82

90

68 74

384

454

511 565

401 440

38.9%42.0% 42.7% 41.6% 42.4% 42.2%

2013 2014 2015 2016 9M 2016 9M 2017

Indirect Cost

Direct Cost

Total

Cost of Revenues as % of

Total Revenue

Financial Highlights

9M 2017 Cost Structure (Unaudited)

32

Financial Highlights

Financial Summary 9M 2017 (Unaudited)

(in IDR Bn) 9M 2016 9M 2017 /

Revenue 945.65 1,041.79 10.2 %

Gross Profit 545.05 602.18 10.5 %

Earnings Before Tax 42.45 119.32 181.1 %

Net Profit 29.22 98.91 238.5 %

EBITDA 111.42 155.79 39.8 %

EBITDA % 11.8 % 15.0 % 317 BPS

Debt to Equity 10.95 0.42 - 10.53

Debt to Asset 0.92 0.30 - 0.62

Thank you