ABS VED дьяконов дмитрий оборотный капитал working capital inventory

Upload

swami-nathanCategory

view

218download

0

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 1/45

INDEX

SL NO. TOPIC PAGE NO.1 Introduction 72 Steel scenario 83 Company profile 124 Objective of study 225 Research methodology 236 Ratio analysis 247 Comparison of ratio 468 Inventory management 589 Receivables management 7010 Payables management 7711 Limitations 8012 Bibliography 81

IntroductionAfter preparation of the financial statement one may be interested in nowing the position of an enterprise from different points of view. This can be done byanalyzing the financial statements with the help of different tools of analysis

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 2/45

such as ratio analysis, funds flow analysis, cash flow analysis, comparative statement analysis, etc. in this process, a meaningful relationship is establishedbetween two or more accounting figures for comparison. I have learn about the analysis of ratio analysis.Inventories are assets of the firm and require investment and hence involve thecommitment of firm’s resources. The inventories need not be viewed as an idle asset rather these are an integral part of firm’s operations. But the question usuallyis as to how much inventories be maintained by a firm? If the inventories are too big, they become a strain on the resources, however, if they are too small, the firm may lose the sales. Therefore, the firm must have an optimum level of inventories. Inventory eeps changing, but the level may remain the same. The basic financial problem is to determine the proper level of investment in the inventories and to decide how much inventory must be acquired during each period to maintain that level.The receivables are assets as it represents a claim of the firm against its customers, expected to be realized in near future. Since a credit sale assumes a sizable proportion of total sales in any firm, the receivable management becomes anarea of attention. Every firm has to set of credit terms and policies under which goods are sold on credit, and every policy has a cost and benefit associatedwith it.When we are managing a growing company, we have to watch expenses carefully. Dont be lulled into complacency by seeing sales increase. Any time and any place we see expenses growing faster than sales, examine your costs carefully to find places to cut or control them.

Steel scenario

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 3/45

COMPANY PROFILE

Essar Steel is a global producer of steel with a footprint covering India, Canada, USA, and Asia. It is a fully integrated flat carbon steel manufacturer--fromiron ore to ready-to-mar et products. Its products find wide acceptance in highly discerning consumer sectors, such as automotive, white goods, construction, engineering and shipbuilding. It is India’s largest exporter of flat steel productsand aims to reach 25 MTPA capacities. Essar is an integrated steel producer, with operations all along the value chain. Essar Steel produces some of the world sbest steel at its state-of-the-art steel complex in Hazira, Gujarat. It is alsoIndia s largest exporter of flat products, sending half of its production abroad, mainly to the highly demanding mar ets of the West, and the growth mar ets ofSouth East Asia and the Middle East. Essar ensures excellent customer service t

hrough a modern distribution networ .

No wonder we are India s largest exporter of flat products, selling almost one-third of our production to the highly demanding US and European mar ets, and

to the growing mar ets of South East Asia and the Middle East. Anumber of major client companies have approved our steel for their use, including Caterpillar, Hyundai, Swaraj Mazda, the Kon an Railway and Maruti Suzu i. Essar Steel is among the 25 percentile of lowest cost producers world-wide and has acquired extensive quality accreditations. Our lean team gives us one of the highest productivities and lowest manpower costs among steel plants internationally.

Bailadilla ore benefication plant

At Bailadilla, where some of the world s richest and finest ore is available, Essar has set up a beneficiation plant of 8 million tonnes per annum (MTPA) capacity, which ensures the highest quality iron ore. The iron ore slurry is pumped through a 267 m. pipeline (the second longest in the world) to the pellet plant,yielding advantages of quality, cost and real time inventory management.

Visa hapatnam Pelletisation Plant

The slurry is received at our Pellet plant at Visa hapatnam, which has a capacity of 8 MTPA, providing vital raw material for the steel plant at Hazira.

Hazira Steel ComplexOur steel complex at Hazira, Gujarat, houses a 5.0 MTPA sponge iron plant, the world s largest gas-based HBI producer. The plant provides raw materials for ourstate-of-the-art 3.0 MTPA hot rolled coil (HRC) plant, the first and largest ofIndia s new generation steel mills. This plant, fed with inputs from three electric arc furnaces and three casters, increasing its capacity to 4.6 MTPA. The complex s sophisticated infrastructure includes independent water supply and power,oxygen and lime plants, a township and a captive port capable of handling up to

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 4/45

8 MTPA of cargo with modern handling equipment li e barges and floating cranes.Cold Rolling ComplexAt the other end of the value chain, the Company s downstream facilities includea 1.2 MTPA Cold Rolling Complex, adds further muscle to our steel ma ing facilities. The complex comprises two pic ling lines of 1.4 MTPA capacity, a reversingmill and a 1.2 MTPA Tandem Mill, two Galvanizing lines of 0.5 MTPA, Batch Annealing Furnace of 0.5 MTPA, a S in Pass Mill of 1.0 MTPA , Cold Rolling and Tandemmills and a Galvanizing plant. This enables Essar Steel to get into the genre of products that are tailor-made for automotive, white goods, shipbuilding, agriculture and construction industries - segments that were the exclusive domain ofa few international manufacturers.

P.T. Essar Indonesia - Our cold rolling complex in IndonesiaP T Essar is Indonesia s largest private sector flat products company, with a domestic mar et share of 35% and a history of process and product innovation. After a major expansion drive, its CR capacity has been enhanced to 400,000 TPA andits newly set up galvanising capacity is 1,50,000 TPA.

Customer-driven excellence

Customer delight drives everything we do at Essar Steel. To allow customers to consistently choose the best, we became the first Indian company to brand flat products, under the name 24-carat steel with a full range including hot and coldrolled coils, galvanized sheets and plates. From order boo ing to delivery, our

information technology systems are integrated between processes and with suppliers and customers. Our major customers can simply go online to place orders or chec details li e their order status, dispatch details, accounts and due payments. Our Systems Applications & Products (SAP R/3) installation is India s biggestand has been judged the best-implemented Indian SAP site by SAP AG Germany.

Product overview1) Hot rolled products

a) coilsb) platesc) sheetsd) Shot Blasted and Primed

2) Cold rolled products

3) Galvanized products

Hot Rolled CoilsEssar Steel is the largest steel producer in western India, with a current capacity of 4.6 MTPA at Hazira, Gujarat, and plans to increase this to 9 MTPA. The Indian operations also include an 8 MTPA beneficiation plant at Bailadilla, Chattisgarh, and an 8 MTPA pellet complex at Visa hapatnam.The complex also houses the steel plant. and the 1.4 MTPA cold rolling complex.The steel complex has a complete infrastructure setup, including a captive port,lime plant and oxygen plant.The dedicated infrastructure of Hazira Complex includes an independent water supply, power, lime & oxygen plant, a township and a captive port that can handle u

p to 6 MTPA of cargo, with modern handling equipment including barges and floating cranes.Cold Rolling ComplexEssar Steel adds substantial value to its world-class hot rolled coils through asophisticated Cold Rolling complex for further processing. The complex includestwo flying shear lines of capacity 0.2 MTPA each, and two slitting lines of capacity 0.2 MTPA each, catering to the mar et of plates and sheets. Essar is alsothe only Indian steel ma er with a 1.2 MTPA hot s in pass mill, from Clecim, theleading manufacturer from France. The mill allows it to enhance the steel s surface quality to match international standards. Its "service centre" concept, uni

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 5/45

que in India, reduces multiple handling costs for customers because it allows Essar Steel s plates and sheets to be used directly by the end-user.

Essar Steel produces highly customised value-added products catering to a variety of product segments and is India’s largest exporter of flat products, selling close to half of its production to the highly demanding US and European mar ets, and to the growing mar ets of South East Asia and the Middle East. The company’s products conform to quality specifications of international quality certificationagencies, li e ABS, API, TUV Rhine Land and Lloyd’s Register. Essar Steel is the first Indian steel company to receive an ISO 14001 certification for environmentmanagement practices.Essar Steel Algoma Inc.

Established in 1901, Essar Steel Algoma Inc. is an integrated steel producer based in Sault Ste. Marie, Ontario, Canada. Formerly operating as Algoma Steel, itwas acquired in June 2007 by Essar Steel Holdings Ltd (a wholly owned subsidiaryof Essar Global Ltd).Capacity: Essar Steel Algoma’s current production capacity is 2.4 million tonnes per annum (MTPA). Wor on expanding capacity to 4 MTPA is underway.

Facilities: Essar Steel Algoma is a fully integrated steelma ing operation thatfeatures a flexible manufacturing process and produces a mix of hot and cold rolled sheet and plate. Algoma’s cornerstone asset, the Direct Strip Production Complex (DSPC) is the newest continuous, thin slab caster in North America, positioni

ng Algoma as a leading supplier of high strength, light gauge steel. In addition, Algoma’s heat-treat plate facility provides a full range of quality steel gradesfor abrasion resistant, ballistic and other specialty plate applications. Other ey mills at the plant include a slabcaster, a 106-inch strip mill (one of thewidest in North America), a 166-inch plate mill, a cold mill, a just-in-time blan ing facility and a welded shapes and profiles division.Strengths: High-end, custom-made products, as well as proximity to the demand-driven North American mar et and Fortune 500 customers ma e Essar Steel Algoma a significant element of Essar’s global expansion plans.HistoryThe Essar Group was founded in 1969 by brothers Shri Shashi Ruia and Shri Ravi Ruia.

The Ruia family’s origins are in Rajasthan. Sometime in the 19th century, it movedto Mumbai and set up its own business. In 1956, Shri Nand ishore Ruia, father to Shri Shashi and Ravi Ruia, moved to Chennai, capital of the south Indian stateof Tamil Nadu, to begin independent business activities. He mentored his two sons in the intricacies of business. When Shri Nand ishore Ruia passed away in 1969, the brothers laid the foundation of the Group.The Essar Group began its operations with the construction of an outer brea wate

r in Chennai port. It quic ly moved to capitalise on every emerging business opportunity, becoming India’s first private company to buy a tan er in 1976. The Group also invested in a diverse shipping fleet and oil rigs, when the Government ofIndia opened up the shipping and drilling businesses to private players in the1980s.Then, in the 1990s, Essar began its steelma ing business by setting up India’s first sponge iron plant in Hazira, a coastal town in the western Indian state of Gujarat. The Group went on to build a pellet plant in Visa hapatnam and eventuallya fully integrated steel plant in Hazira.Through the 1990s, with the gradual liberalisation of the Indian economy, Essar

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 6/45

seized every opportunity that came its way. It diversified its shipping fleet, started oil & gas exploration and production, laid the foundation of its oil refinery at Vadinar, Gujarat, and set up a power plant near the steel complex in Hazira. The Construction business helped the Group build most of its business assets. Essar also entered the GSM telephony business, establishing India’s first mobile phone service in Delhi (branded Essar Cellphone) with Swiss PTT as the joint venture partner.The 21st century for the Essar Group has been all about consolidating and growing the businesses, with M&As, new revenue streams and strategic geographical expansion.

Vision

We will be a respected global entrepreneur,through the power of Positive Action.

Mission

We are committed to innovative growth,through our personal passion,reinforced by a professional mindset,creating value for all those we touch.

Management Team

Shashi Ruia, chairman, essar global ltd, is a first generation entrepreneur industrialist. Mr ruia began his career in the family business in1965 under the guidance of his father, the late nand ishore ruia, Along with his brother ravi .

Mr ruia is on several international bodies and industry associations. He was onthe managing committee of federation of Indian chambers of commerce and industry(FICCI), an apex body of India’s trade and business associations. He has also bee

n the chairman of the prestigious indo-us joint business council and is a formerpresident of Indian national shi powners association (INSA).

Ravi Ruia, Vice Chairman, Essar Global Limited, belongs to the generation of industrialists, who have played a significant role in leading India’s industrial renaissance. An engineer by training, his entrepreneurial abilities have enabled theEssar Group to become one of theleading names in global industry, Essar employsmore than 50,000 people across offices in Asia, Africa, Europe and the Americas.Mr Ravi Ruia has been the mastermind behind the Group’s globalisation plans, inclu

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 7/45

ding new ventures in Trinidad & Tobago, Vietnam and the Middle East, as well asthe recentacquisitions of Algoma Steel (now called Essar Steel Algoma), Canada, and Minnesota Steel, USA (now called Essar Steel Minnesota).

Prashant Ruia is the Promoter Director and Group Chief Executive of Essar GlobalLimited. He has been involved with the Group’s operation and management since 1985.Prashant Ruia is on the Board of the International Iron and Steel Institute. He is also a member of Confederation Indian Industry (CII) National Committee onSteel & Non Ferrous Metals and Chairman of CII National Committee on Hydro carbon and Petroleum. Mr. Ruia is also on the Board of Trade of the Ministry of Commerce and Industry, Government of India. He is also a member of the Young Presidents’ Organisation, Mumbai Chapter.Anshuman Ruia is a Director on the Board of major companies of Essar Global Limited. Essar Global Limited is a diversified business corporation operating in themanufacturing and services sectors of Steel, Energy, Power, Communications,Shipping Ports & Logistics, Construction and Mining & Minerals. Essar has an assetbase of USD 14.5 billion and employs more than 50,000 people across offices in Asia, Africa, Europe and the Americas.He currently oversees Essar’s Shipping Ports &Logistics, Telecom & BPO,and Power businesses. He is responsible for the expansion and diversification of the Power business into new, renewable energy sourcesand its entry into the transmission and distribution segment. Mr Ruia is also involved in new business ventures of the Group in India and overseas.

Scion of the Ruia family, Smiti Kanodia, promoter director, received her bachelor’s degree in Finance & Mar eting from New Yor University’s Stern School of Business. Ms Kanodia wor ed as a Mergers & Acquisitions analyst in the telecommunications sector at Lehman Brothers in New Yor , after which she pursued a postgraduatedegree in publishing at the London College of Printing.Ms Kanodia is involved in providing strategic direction to HR branding and communicationinitiatives at the Essar Group.

Rewant Ruia is the youngest member of the family of the Promoter Directors of Essar Global Limited. He began his career in the Essar Group with a short trainingstint in the Steel and Oil businesses.

His responsibilities include managing the aviation division and protocol functions for the Group. He is part of the management thin tan for new business development opportunities in Steel, Petroleum and Petrochemicals, and the pursuit ofglobal opportunities in all the businesses.Mr Ruia completed his schooling from the Hac ley School, New Yor , in 1999,and holds a degree in Business Management from Bentley College, Boston, USA. He has a een interest in music and sports.

Management Team - Steel Business

Mr. J Mehra Chief Executive Officer – Steel BusinessMr. Vi ram Amin Director, Sales & Mar etingMr. Alain Davezac EVP - Strategy & Business DevelopmentMr. Dilip Oommen Chief Executive Officer - Essar Steel (India)Mr. Armando Plastino Chief Executive Officer - Essar Steel AlgomaMr. K B Trivedi President Director & CEO - PT Essar IndonesiaMr. V Madhusudan President & CEO - Essar Steel MinnesotaMr. R K Zaroo Director – Project DevelopmentMr. M K Sampath Chief Executive Officer - Pellet Projects (India)Mr. H S Sethi Director – Projects (Orissa)

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 8/45

Mr. Mahadev Iyer Chief Financial OfficerMr. Kalyan Ghosh Sr. Vice President & Head – Supply Chain ManagementMr. Praneet Mehrish Sr. Vice President & Head – Human ResourcesMr. Anil Agarwal Sr. Vice President & Head - ProcurementMr. P C Panda Sr. Vice President & Head - LegalMr. Suresh Tanwar Vice President & Head – Health Safety & EnvironmentMr. Suneel Aradhye Chief Information Officer

OBJECTIVES OF THE STUDY

To study the ratio with other steel companies. To study the ways of monitoring receivables and analyze the trend of debtors. To study the spare management. To study the payable management.

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 9/45

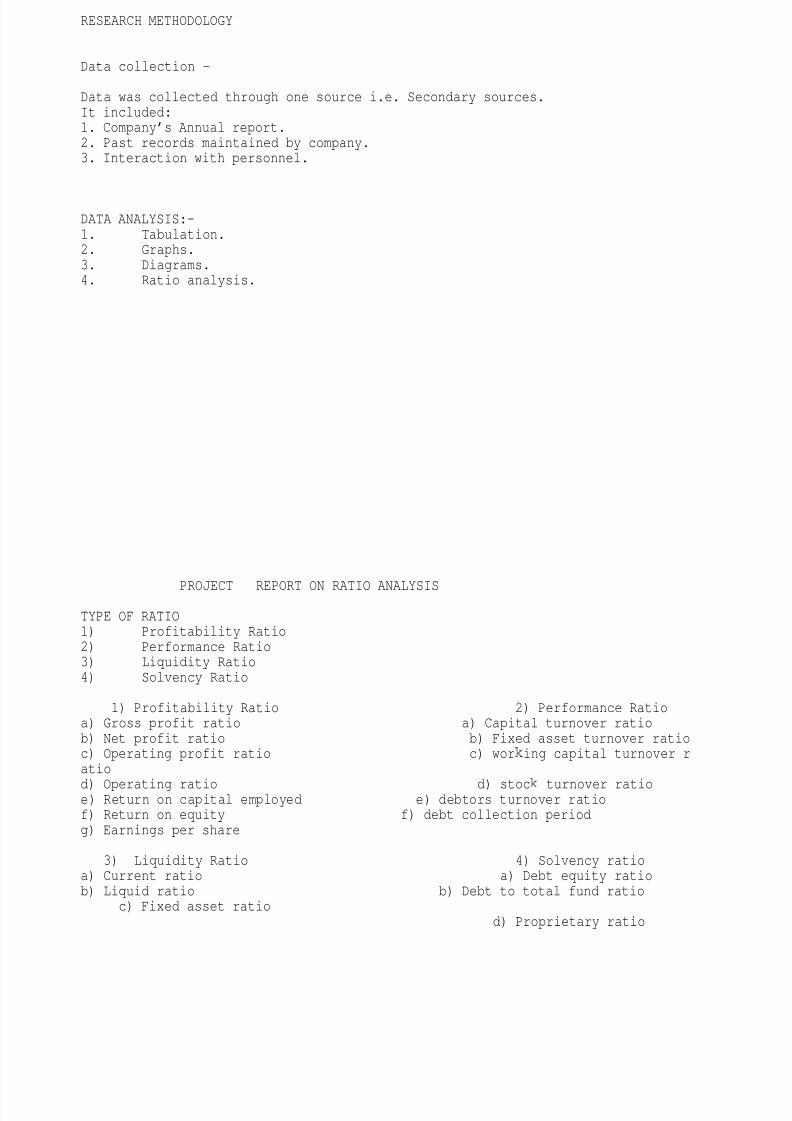

RESEARCH METHODOLOGY

Data collection –

Data was collected through one source i.e. Secondary sources.It included:1. Company’s Annual report.2. Past records maintained by company.3. Interaction with personnel.

DATA ANALYSIS:-1. Tabulation.2. Graphs.3. Diagrams.4. Ratio analysis.

PROJECT REPORT ON RATIO ANALYSIS

TYPE OF RATIO1) Profitability Ratio2) Performance Ratio3) Liquidity Ratio4) Solvency Ratio

1) Profitability Ratio 2) Performance Ratioa) Gross profit ratio a) Capital turnover ratiob) Net profit ratio b) Fixed asset turnover ratioc) Operating profit ratio c) wor ing capital turnover ratio

d) Operating ratio d) stoc turnover ratioe) Return on capital employed e) debtors turnover ratiof) Return on equity f) debt collection periodg) Earnings per share

3) Liquidity Ratio 4) Solvency ratioa) Current ratio a) Debt equity ratiob) Liquid ratio b) Debt to total fund ratio

c) Fixed asset ratiod) Proprietary ratio

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 10/45

e) Interest coverage ratio1) Profitability Ratio

a) Gross profit ratio-- Gross Profit Ratio shows the relationship between Gross Profit of the concern and its Net Sales. Gross Profit Ratio can be calculatedin the following manner:

Gross profitGross profit ratio = ------------------ * 100

Net saleWhere Gross Profit = Net Sales – Cost of Goods SoldCost of Goods Sold = Opening Stoc + Net Purchases + Direct Expenses – Closing

StocAnd Net Sales = Total Sales – Sales Return

Objective and Significance: Gross Profit Ratio provides guidelines to the concern whether it is earning sufficient profit to cover administration and mar etingexpenses and is able to cover its fixed expenses. The gross profit ratio of current year is compared to previous years’ ratios or it is compared with the ratios of the other concerns. The minor change in the ratio from year to year may be ignored but in case there is big change, it must be investigated. This investigation will be helpful to now about any departure from the standard mar -up and would indicate losses on account of theft, damage, bad stoc system, bad sales policies and other such reasons. It gives a good indication of financial health. Without an adequate gross margin, a company will be unable to pay its operating andother expenses. Firm that have a high gross profit margin are more liquid and thus have more cash flow to spend on research and development expenses.

07-0806-07Gross profit = Net income from operation -- 10743.32 8194.35

Material consumed -- -6750.84-5747.74

Increase/decrease in stoc -- -168.72 +872.66

Manufacturing & asset main-- -859.39-746.04

Gross profit = 2964.372573.23

2573.232964.37

Gross profit (06-07) = -------------- * 100 = 31.40% (07-08) = ------------- * 100 = 27.59%8194.35

10743.32Gross profit ratio analysis – gross profit for the year 07-08 is more as compare to 06-07. Even net turnover of 07-08 is more as compare to 06-07. But gross profit to turnover ratio of 07-08 is decline which is not good sign for the company &more over gross profit should not be much fluctuates. It shows 3.81% point difference. It may be because of recession, company may reduce the prices of their product in order to increase the demand of their product. As a result turnover isincreases but the margin which the company was earlier getting it is reduced.Suggestion for improvement – gross profit can be increase if the company efficiently utilize its resources and try to produce better quality of product and maximi

ze its output with low input. Because major direct expenditure is on material sothat must be efficiently utilize. Company should give more emphasis on enhancing its productivity and even try to get better return on that.b) Net profit ratio-- Net Profit Ratio shows the relationship between Net Profitof the concern and Its Net Sales.

Net profitNet profit ratio = --------------- * 100

Net sales

Where Net Profit = Gross Profit – operating expenses – Non Operating Expenses + Non

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 11/45

Operating Incomes.And Net Sales = Total Sales – Sales ReturnObjective and Significance: In order to wor out overall efficiency of the concern Net Profit ratio is calculated. This ratio is helpful to determine the operational ability of the concern. While comparing the ratio to previous years’ ratios,the increment shows the efficiency of the concern. Net profit includes all thefactors that influence profitability whether under management control or not. The higher the ratio, the more effective a company is at cost control.

436.49 428.62Net profit ratio (06-07) = -------------- * 100 = 5.33% (07-08) = -------------* 100 = 3.99%

8194.3510743.32Net profit ratio analysis -- Net profit for the year 07-08 is less as compare to06-07. But turnover is just the reverse. So decrease in net profit ratio indicates that the efficiency of the company decrease. As the ratio decrease the lesseffective a company is at cost control.Suggestion for improvement – the company have to put major control on all expenses. Reductions in expenses result in more profit. As a result the net profit ratioshows increment.c) Operating profit ratio-- Operating Profit means profit earned by the concernfrom its business operation and not from the other sources. While calculating the net profit of the concern all incomes either they are not part of the businessoperation li e Rent from tenants, Interest on Investment etc. are added and all

non-operating expenses are deducted. So, while calculating operating profits these all are ignored and the concern comes to now about its business income fromits business operations.

Operating profitOperating profit ratio = -----------------------------

* 100Net sales

Where Operating Profit = Gross Profit – Operating Expensesor Operating Profit = Net Profit + Non Operating Expenses – Non Operating Incomesand Net Sales = Total Sales – Sales ReturnObjective and Significance: Operating Profit Ratio indicates the earning capacity of the concern on the basis of its business operations and not from earning from the other sources. It shows whether the business is able to stand in the mar

et or not. Operating profit ratio measure a company’s operating efficiency with its successful cost control. The higher the ratio, the better the company is. A higher operating profit ratio means that a company has lower fixed cost and a better gross margin or increasing sales faster than costs.

07-08 06-07Operating profit = Gross profit -- 2964.37

2573.23Personnel expenses-- -225.80

-152.80Administrative expen-- -215.98 -146.14Selling & distribution-- -214.50 -3

38.26

2308.09 1936.03

1936.03Operating profit ratio (06-07) = ------------------- * 10

0 = 23.63%

8194.352308.09

(07-08) = ------------------* 100 = 21.48%

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 12/45

10743.32Operating profit ratio analysis – operating profit for the year 07-08 is more as compare to 06-07 but operating profit ratio is decrease by 2.15% point which is not good sign for the company. The higher the ratio, the better the company is. Here the net turnover is increase by 31.11% but the operating profit is increaseby 19.22% so that why operating profit ratio is decrease.Suggestion for improvement – the company has to control its operating expenses. Because less operating expenses will result in more net profit and more net profitwill create wealth of company and its shareholder’s. A higher operating profit put the company to stand in the mar et. This ratio can be improved by effective utilization of asset that is investment of company.d) Operating cost ratio- Operating Ratio matches the operating cost to the net sales of the business.

Operating costOperating cost ratio = -------------------- * 100

Net salesWhere Operating Cost = Cost of goods sold + Operating ExpensesCost of Goods Sold = Opening Stoc + Net Purchases + Direct Expenses – Closing StocOperating Expenses = Selling and Distribution Expenses, Office and Administration Expenses, Repair and Maintenance.

Objective and Significance: Operating Ratio is calculated in order to calculatethe operating efficiency of the concern. As this ratio indicates about the perce

ntage of operating cost to the net sales, so it is better for a concern to havethis ratio in less percentage. The less percentage of cost means higher margin to earn profit. Operating cost ratios are often used by production managers to monitor trends and identify problems. If a significant change occurs, the problemmust be identified as either internal (such as operations) or external (such aseconomic conditions). Since investors and other outsiders don t have access to operating information, operating ratios are rarely used outside the organization.

06-0707-08

Cost of goods sold = Net sale -- 8194.3510743.32

Gross profit-- -2573.23-2964.37

5621.127778.95Operating expenses = personnel expenses-- 152.80 22

5.80Administrative exp-- 146.14

215.98Selling & distribution -- 338.26

214.50637.20

656.28Operating cost = cost of goods sold + operating expensesOperating cost (06-07) = 5621.12 + 637.20 = 6258.32Operating cost (07-08) = 7778.95 + 656.28 = 8435.23

6258.32

Operating cost ratio (06-07) = ------------------ * 100 = 76.37%8194.35

8435.23Operating cost ratio (07-08) = ----------------- * 100 = 78.52%

10743.32Operating cost ratio analysis -- Operating ratio for the year 07-08 is higher than 06-07. Decrease in operating cost ratio represents good sign for the company

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 13/45

because the less percentage of cost means higher margin to earn profit. But herein the year 07-08 operating expenses is increase more than the turnover as a result the operating cost ratio increases.Suggestion for improvement – The Company has to put close loo on all operationalexpenses and try to control all these expenses where ever it is possible. A continuous increase in operating cost ratio is not good sign for the company as it is going to reduce it operating profit and net profit.e) Return on Investment or Return on Capital Employed: This ratio shows the relationship between the profit earned before interest and tax and the capital employed to earn such profit.

Net profit before interest, tax & dividendReturn on capital employed = ---------------------------------------------------- * 100

Capital employedWhere Capital Employed = Share Capital (Equity + Preference) + Reserves and Surplus + Long-term Loans – Fictitious Assetsor Capital Employed = Fixed Assets + Current Assets – Current LiabilitiesObjective and Significance: Return on capital employed measures the profit, which a firm earns on investing a unit of capital. The profit being the net result of all operations, the return on capital expresses all efficiencies and inefficiencies of a business. This ratio has a great importance to the shareholders and investors and also to management. To shareholders it indicates how much their cap

ital is earning and to the management as to how efficiently it has been wor ing.This ratio influences the mar et price of the shares. The higher the ratio, thebetter it is.

07-0806-07Capital employed = share capital (equity + preference) -- 1184.08

1387.00Reserve and surplus -- +3447.25

+3080.95Secured loan -- +5383.11

+6533.32Long term advance -- +144.56

+166.42

1015911167.69Net profit before interest & tax -- 1557

.78 1324.21

1324.21Return on capital employed (06-07) = ----------------- * 100 = 11.86%

11167.691557.78

Return on capital employed (07-08) = ------------ * 100 = 15.33%10159

Return on capital employed analysis – Return on capital employed for the year 07-0

8 is more than 06-07. Increase in return on capital employed is good sign for the investors and to the management. To shareholders it indicates how much their capital is earning and to the management as to how efficiently it has been wor ing.Suggestion for further improvement -- The Company has to increase its net profitand company has to reduce borrowing by paying through the internal accruals.f) Return on Equity: Return on equity is also nown as return on shareholders’ investment. The ratio establishes relationship between profit available to equity shareholders with equity shareholders’ funds.

Net profit after interest, tax & preference di

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 14/45

videndReturn on equity = ----------------------------------------------------------------------------- * 100

Equity share holder’s fundsWhere Equity Shareholders’ Funds = Equity Share Capital + Reserves and Surplus – Fictitious AssetsObjective and Significance:• Return on Equity judges the profitability from the point of view of equity sharholders.• This ratio has great interest to equity shareholders.• The return on equity measures the profitability of equity funds invested in thefirm.• The investors favor the company with higher ROE.

07-08 06-07Equity share holder’s fund = equity share capital -- 1140.481140.48

Reserve & surplus -- +3447.25+3080.95

4587.734221.43

Net profit after interest, tax & preference dividend = 423.28431.15

431.15Return on equity (06-07) = ------------- * 100 = 10.21%4221.43

423.28Return on equity (07-08) = ------------- * 100 = 9.23%

4587.73Return on equity analysis – return on equity for the year 07-08 is less as compareto 06-07. It is less by .98% point. ROE is referred to as Stoc holder s returnon investment, it tells the rate that shareholders are earning on their shares.So higher the rate represent the better return on investment which result in increase the shareholder’s wealth.Suggestion for improvement -- If new shares are issued then use the weighted average of the number of shares throughout the year. The company should try to incr

ease net profit.g) Earnings per Share: Earnings per share is calculated by dividing the net profit (after interest, tax and preference dividend) by the number of equity shares.

Net profit after interest, tax & preference dividend

Earnings per share = -------------------------------------------------------------------

No. of equity shareObjective and Significance: Earning per share helps in determining the mar et price of the equity share of the company. It also helps to now whether the company is able to use its equity share capital effectively with compare to other companies. It also tells about the capacity of the company to pay dividends to its equity shareholders. The higher the earnings per share, the higher each share sho

uld be worth. The earnings per share growth rate indicate the amount of growth for investors.

07-0806-07

No. of equity share -- 1,139,810,888985,041,908

Net profit after interest, tax & p.dividend-- Rs 4232800000 Rs 4,311,500,000

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 15/45

4,311,500,000Earnings per share (06-07) = ------------------- = Rs 4.38

985,041,908

4,232,800,000Earnings per share (07-08) = --------------------- = Rs 3.711,139,810,888Earnings per share analysis -- earnings per share (EPS) is one of the most important measure of a company’s strength. Obviously, the higher this number, the moremoney the company is ma ing. But in the year 07-08 earnings per share is decrease by .67 paisa. This is not good sign for the company even for shareholders.Suggestion for improvement – earning per share can be improve by increasing the net profit.2) Performance Ratioa) Capital turnover ratio-- Capital turnover ratio establishes a relationship between net sales and capital employed. The ratio indicates the times by which the capital employed is used to generate sales.

Net salesCapital turnover ratio = ---------------------

---------Capital employed

Where Net Sales = Sales – Sales ReturnCapital Employed = Share Capital (Equity + Preference) + Reserves and Surplus +

Long-term Loans – Fictitious Assets.Objective and Significance: The objective of capital turnover ratio is to calculate how efficiently the utilization of assets in the business is being used andhow many times the capital is turned into sales. Higher the ratio, better the efficiency of utilization of capital and it would lead to higher profitability.

07-08 06-07Net sales = sales -- 11910.66 9000.46

Excise duty -- -1167.34 -806.1110743.32 8194.35

Capital employed -- 10159.00 11167.69

8194.35 10743.32Capital turnover ratio (06-07) = -------------- = .73 (07-08) = --------------- = 1.06

11167.6910159.00

Capital turnover ratio analysis – capital turnover ratio for the year 07-08 is more as compare to 06-07 which is good sign for the company. As in the 07-08, 1.06times the capital is turn into sales. Higher the ratio, better the efficiency ofutilization of capital and it would lead to higher profitability.Suggestion for improvement – capital turnover ratio can be increase if we increasethe turnover by utilizing the best of available capital. We have to maximize the no. if times.

b) Fixed Assets Turnover Ratio: Fixed assets turnover ratio establishes a relationship between net sales and net fixed assets. This ratio indicates how well thefixed assets are being utilized.

Net salesFixed asset turnover ratio = -----------------------

Net fixed assetObjective and Significance: This ratio expresses the number to times the fixed assets are being turned over in a stated period. It measures the efficiency withwhich fixed assets are employed. A high ratio means a high rate of efficiency of

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 16/45

utilization of fixed asset and low ratio means improper use of the assets.07-08

06-07Net fixed asset = 9849.01

9997.37Net sales = 10743.32

8194.35

8194.3510743.32Fixed asset turnover ratio (06-07) = -------------- = .82 (07-08) = -------------- = 1.09

9997.379849.01

Fixed asset turnover ratio analysis – fixed asset turnover ratio for the year 07-08 is more as compare to 06-07 which is good sign for the company. The fixed-asset turnover ratio measures a company s ability to generate net sales from fixed-asset investments. A higher fixed-asset turnover ratio shows that the company hasbeen more effective in using the investment in fixed assets to generate revenues.Suggestion for improvement – fixed asset should be efficiently utilized up to itsmaximum capacity. Idle fixed asset should be dispose so that the amount which isrealize from that can be used in the operation.c) Wor ing Capital Turnover Ratio: Wor ing capital turnover ratio establishes a

relationship between net sales and wor ing capital. This ratio measures the efficiency of utilization of wor ing capital.Net

salesWor ing capital turnover ratio = ---------------------------

Net wor ing capitalWhere Net Wor ing Capital = Current Assets – Current LiabilitiesObjective and Significance: This ratio indicates the number of times the utilization of wor ing capital in the process of doing business. The higher is the ratio, the lower is the investment in wor ing capital and the greater are the profits. However, a very high turnover indicates a sign of over-trading and puts the firm in financial difficulties. The wor ing capital turnover ratio measures the efficiency with which the wor ing capital is being used by a firm. A high ratio i

ndicates efficient utilization of wor ing capital. A low wor ing capital turnover ratio indicates that the wor ing capital has not been used efficiently.07-08 06-07

Net wor ing capital = 557.98908.58

Net sales = 10743.32 8194.35

8194.3510743.32

Wor ing capital turnover ratio (06-07) = ------------- = 9.02 (07-08) = ---------------- = 19.25

908.58

557.98Wor ing capital turnover ratio analysis – wor ing capital turnover ratio for the year 07-08 is more as compare to 06-07. This shows that the wor ing capital is efficiently utilized. It is increase by 10.23% point.Suggestion for improvement – wor ing capital is based on various aspects li e debtor’s collection should be favorable and inventory turnover ratio, this shows thatmore frequently the stoc s are sold.d) Stoc Turnover Ratio: Stoc turnover ratio is a ratio between cost of goods sold and average stoc . This ratio is also nown as stoc velocity or inventory turnover ratio.

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 17/45

Cost of goods soldStoc turnover ratio = ------------------------

--------Average stoc

Where Average Stoc = [Opening Stoc + Closing Stoc ]/2Cost of Goods Sold = Net sales – gross profitObjective and Significance: Stoc is a most important component of wor ing capital. This ratio provides guidelines to the management while framing stoc policy.It measures how fast the stoc is moving through the firm and generating sales.It helps to maintain a proper amount of stoc to fulfill the requirements of the concern. A proper inventory turnover ma es the business to earn a reasonable margin of profit.

06-07 07-08Cost of goods sold = Net sale -- 8194.35 10743.32

Gross profit-- -2573.23 -2964.37

5621.12 7778.95Average stoc (06-07) = [341.78+528.84+332.16+1204.82]/2 = 120

3.80Average stoc (07-08) = [528.84+295.74+1204.82+1036.10]/2 = 15

32.75

5621.12

7778.95Stoc turnover ratio (06-07) = -------------- = 4.67 (07-08) = --------------- = 5.075

1203.80 1532.75Stoc turnover ratio analysis – stoc turnover ratio for the year 07-08 is more than 06-07. As it is increase it is good sign for the company. This shows that more frequently the stoc s are sold; the lesser amount of money is required to finance the inventory.Suggestion for improvement -- A low inventory turnover ratio indicates an inefficient management of inventory. A low inventory turnover implies over-investmentin inventories, dull business, poor quality of goods, stoc accumulation, accumulation of obsolete and slow moving goods and low profits as compared to total investment. So in order to increase this ratio company has to improve the entire t

hing in positive way. The inventory turnover ratio is also an index of profitability, where a high ratio signifies more profit; a low ratio signifies low profit.E) Debtors’ Turnover Ratio: Debtors turnover ratio indicates the relation betweennet credit sales and average accounts receivables of the year.

Net credit sales

Debtors turnover ratio = ----------------------------------------------

Average account receivablesWhere Average Accounts Receivables = [Opening Debtors and B/R + Closing Debtor

s and B/R]/2

Credit Sales = Total Sales – Cash SalesObjective and Significance: This ratio indicates the efficiency of the concern to collect the amount due from debtors. It determines the efficiency with which the trade debtors are managed. Higher the ratio, better it is as it proves that the debts are being collected very quic ly. Debtors’ turnover ratio indicates the number of times the debtors are turned over a year. The higher the value of debtors’ turnover the more efficient is the management of debtors or more liquid the debtors are. Similarly, low debtors turnover ratio implies inefficient managementof debtors or less liquid debtors.

06-07 07-08

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 18/45

Net credit sales = 8194.35 10743.32Average accounts receivables = 543.50 453.62

8194.35 10743.32Debtors turnover ratio (06-07) = ------------- = 15.077 (07-08) = ---------------- = 23.68

543.50 453.62Debtor’s turnover ratio analysis – Debtors’ turnover ratio for the year 07-08 is morethan 06-07 which is good sign for company. For the year 07-08 the debtors are efficiently manage as compare to 06-07. As increase in ratio shows that debtors are more liquid. Even we can say that liquidity of the debtors is increase.f) Debt Collection Period: Debt collection period is the period over which the debtors are collected on an average basis. It indicates the rapidity or slownesswith which the money is collected from debtors.

365 daysDebt collection period = -------------------------

---------Debtor’s turnover rat

ioObjective and Significance: This ratio measures the quality of debtors. This ratio indicates how quic ly and efficiently the debts are collected. The shorter the period the better it is and longer the period more the chances of bad debts. Although no standard period is prescribed anywhere, it depends on the nature of the industry.

06-07 07-08Debtors turnover ratio = 15.077 23.68365 365

Debt collection period (06-07) = ----------- = 24 days (07-08) = ----------- = 16days

15.077 23.68Debt collection period analysis – debt collection period for the year 07-08 is less as compare to 06-07. This is quite good for the company. Company efficiency isincrease in collecting the debts. A short collection period implies prompt payment by debtors. As per the ratio the no. of days is reduce by 8 days.Suggestion for improvement – the company has to sale the goods to those debtors who are ma ing the payment very frequently.3) Liquidity Ratio

a) Current Ratio -- Current ratio is calculated in order to wor out firm’s ability to pay off its short-term liabilities. This ratio is also called wor ing capital ratio. This ratio explains the relationship between current assets and current liabilities of a business. Where current assets are those assets which areeither in the form of cash or easily convertible into cash within a year. Similarly, liabilities, which are to be paid within an accounting year, are called current liabilities.

Current assetCurrent ratio = -----------------------

Current liabilityCurrent Assets include Cash in hand, Cash at Ban , Sundry Debtors, Bills Receivable, Stoc of Goods, Short-term Investments, Prepaid Expenses, Accrued Incomes etc.

Current Liabilities include Sundry Creditors, Bills Payable, Ban Overdraft, Outstanding Expenses etc.Objective and Significance: Current ratio shows the short-term financial position of the business. This ratio measures the ability of the business to pay its current liabilities. The ideal current ratio is supposed to be 2:1 i.e. current assets must be twice the current liabilities. In case, this ratio is less than 2:1, the short-term financial position is not supposed to be very sound and in case, it is more than 2:1, it indicates idleness of wor ing capital. Firms having less than 2 : 1 ratio may be having a better liquidity than even firms having morethan 2 : 1 ratio. This is because of the reason that current ratio measures the

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 19/45

quantity of the current assets and not the quality of the current assets. If afirm s current assets include debtors which are not recoverable or stoc s whichare slow-moving or obsolete, the current ratio may be high but it does not represent a good liquidity position.06-07 07-08

Current asset = 4397.41 3935.19

Current liability = 3488.83 3377.21

4397.413935.19

Current ratio (06-07) = -------------- = 1.26 (07-08) = --------------- = 1.165

3488.833377.21

Current ratio analysis – current ratio for the year 07-08 is less as compare to 06-07 this is because current asset is decrease more than current liabilities. A generally acceptable current ratio is 2 to 1. But whether or not a specific ratiois satisfactory depends on the nature of the business and the characteristics of its current assets and liabilities. The minimum acceptable current ratio is obviously 1:1.Suggestion for improvement –• Paying some debts.

• Increasing your current assets from loans or other borrowings with a maturity omore than one year.• Converting non-current assets into current assets.• Increasing your current assets from new equity contributions.

Limitation of current asset ratio –1. It is crude ratio because it measures only the quantity and not the quality of the current assets.2. Even if the ratio is favorable, the firm may be in financial trouble, because of more stoc and wor in process which is not easily convertible into cash, and, therefore firm may have less cash to pay off current liabilities.3. Valuation of current assets and window dressing is another problem. An equal increase in both current assets and current liabilities would decrease the

ratio and similarly equal decrease in current assets and current liabilities would increase current ratio.b) Liquid Ratio: Liquid ratio shows short-term solvency of a business in a truemanner. It is also called acid-test ratio and quic ratio. It is calculated in order to now how quic ly current liabilities can be paid with the help of quic assets. Quic assets mean those assets, which are quic ly convertible into cash.

Liquid assetLiquid ratio = -------------------------

Current liabilityWhere liquid assets include Cash in hand, Cash at Ban , Sundry Debtors, Bills Receivable, Short-term Investments etc. In other words, all current assets are liquid assets except stoc and prepaid expenses.

Current liabilities include Sundry Creditors, Bills Payable, Ban Overdraft, Outstanding Expenses etc.

Objective and Significance: Liquid ratio is calculated to wor out the liquidityof a business. This ratio measures the ability of the business to pay its current liabilities in a real way. The ideal liquid ratio is supposed to be 1:1 i.e.liquid assets must be equal to the current liabilities. In case, this ratio is less than 1:1, it shows a very wea short-term financial position and in case, itis more than 1:1, it shows a better short-term financial position.

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 20/45

Liquid asset (06-07) = current asset- inventory- prepaid expenses4397.41- 2328.77 = 2068.64

Liquid asset (07-08) = 3935.19- 2108.11 = 1827.08(06-07) (07-08)

Current liability = 3488.83 3377.212068.64 1827.08

Liquid ratio (06-07) = --------------- = .593 (07-08) = ---------------- = .54

3488.83 3377.21Liquid ratio analysis – liquid ratio for the year 07-08 is less as compare to 06-07 even liquid ratio of 06-07 is not good. It should be 1or more than that and for the year 07-08 it is further less so financial position is not good. The liquid ratio is decrease because liquid asset is decrease more than current liabilities. Current asset is decrease by 241.56 crores where as current liability is decrease by 111.62 crores.Suggestion for improvement – As 1:1 standard should not be used blindly. A liquidratio of 1:1 does not necEssarily mean satisfactory liquidity position of the firm if all the debtors cannot be realized and cash is needed immediately to meetthe current obligations. A firm having a high liquidity ratio may not have a satisfactory liquidity position if it has slow-paying debtors. On the other hand, afirm having a low liquid ratio may have a good liquidity position if it has fast moving inventories.4) Solvency ratio—

a) Debt equity ratio-- Debt equity ratio shows the relationship between long-term debts and shareholders funds’. It is also nown as ‘External-Internal’ equity ratio.Debt

Debt equity ratio = ----------------Equity

Where Debt includes Debentures, Mortgage Loan, Ban Loan, Public Deposits, Loanfrom financial institution etc.Equity (Shareholders’ Funds) = Share Capital (Equity + Preference) + Reserves andSurplus – Fictitious AssetsObjective and Significance: This ratio is a measure of owner’s stoc in the business. Proprietors are always een to have more funds from borrowings because:(i) Their sta e in the business is reduced and subsequently their ris too(ii) Interest on loans or borrowings is a deductible expenditure while computing

taxable profits. Dividend on shares is not so allowed by Income Tax Authorities.The owners want to do the business with maximum of outsider s funds in order tota e lesser ris of their investment and to increase their earnings (per share)by paying a lower fixed rate of interest to outsiders. The outsider creditors) on the other hand, want that shareholders (owners) should invest and ris their share of proportionate investments. A ratio of 2:1 is usually considered to be satisfactory ratio although there cannot be rule of thumb or standard norm for alltypes of businesses.

06-0707-08

Debt -- secured loan – 6533.325383.11

Long term advance -- +166.42+144.56

Unsecured loan -- +409.92+733.47

7109.666261.14

Equity share holder’s fund = equity share capital -- 1387.001184.08

Reserve & surplus -- +3080.95+3447.25

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 21/45

4467.954631.33

7109.66 6261.14Debt equity ratio (06-07) = ------------- = 1.59 (07-08) = --------------- = 1.35

4467.95 4631.33Debt equity ratio analysis – Debt equity ratio of both the year is not satisfactory because standard debt equity ratio is 2:1. Here it gives clear picture that company’s share capital is decreasing where as reserve and surplus is increasing. Itmeans that reserve & surplus is increasing at a high rate as compare to the rate at which share capital is decreasing so that’s why the overall figure in the year 07-08 is increasing.Suggestion for improvement – company should raise its fund by the combination of both equity and debt and try to maintain 2:1 ratio that is debt equity ratio.b) Debt to Total Funds Ratio: This ratio gives same indication as the debt-equity ratio as this is a variation of debt-equity ratio. This ratio is also nown assolvency ratio. This is a ratio between long-term debt and total long-term funds.

DebtDebt to total fund ratio = --------------------

TotalfundWhere Debt (long term loans) includes Debentures, Mortgage Loan, Ban Loan, Publ

ic Deposits, Loan from financial institution etc.Total Funds = Equity + DebtEquity (Shareholders’ Funds) = Share Capital (Equity + Preference) + Reserves andSurplus – Fictitious AssetsObjective and Significance: Debt to Total Funds Ratios shows the proportion of long-term funds, which have been raised by way of loans. This ratio measures thelong-term financial position and soundness of long-term financial policies. In India debt to total funds ratio of 2:3 or 0.67 is considered satisfactory. A higher proportion is not considered good and treated an indicator of ris y long-termfinancial position of the business. It indicates that the business depends toomuch upon outsiders’ loans.

06-0707-08

Equity share holder’s fund = equity share capital -- 1387.001184.08Reserve & surplus -- +3080.95

+3447.254467.95

4631.33Debt (long term) = secured loan – 6533.32

5383.11Long term advance -- +166.42

+144.566699.74

5527.67Total fund= equity + debt -- 11167.69

10159

6699.74 5527.67Debt to total fund ratio (06-07) = --------------- = .60 (07-08) = -------------- = .54

11167.6910159

Debt to total fund ratio analysis – debt to total fund ratio is for the both yearis quite satisfactory. A higher proportion is not considered good and treated an

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 22/45

indicator of ris y long-term financial position of the business.Suggestion for improvement – as company current debt to total fund ratio is satisfactory so in order to maintain this company has to maintain a proper balance between debt and equity.c) Fixed Assets Ratio: Fixed Assets Ratio establishes the relationship of FixedAssets to Long-term Funds.

Long term funds

Fixed asset ratio = ---------------------------

Net fixed assetWhere Long-term Funds = Share Capital (Equity + Preference) + Reserves and Surplus + Long-term Loans – Fictitious AssetsNet Fixed Assets means Fixed Assets at cost less depreciation. It will also include trade investments.Objective and Significance: This ratio indicates as to what extent fixed assetsare financed out of long-term funds. It is well established that fixed assets should be financed only out of long-term funds. This ratio wor out the proportionof investment of funds from the point of view of long-term financial soundness.This ratio should be equal to 1. If the ratio is less than 1, it means the firmhas adopted the impudent policy of using short-term funds for acquiring fixed assets. On the other hand, a very high ratio would indicate that long-term funds a

re being used for short-term purposes, i.e. for financing wor ing capital.06-0707-08Long term funds = share capital -- 1387.00 118

4.08Reserve & surplus -- +3080.95 +3447.

25Long term loans -- + 6533.32 +5383

.1111001.27 10014.

44Net fixed asset-- 9997.37

9849.01

11001.27 10014.44Fixed asset ratio (06-07) = ------------------ = 1.10 (07-08) =

---------------- = 1.029997.37

9849.01

Fixed asset ratio analysis -- fixed asset ratio for the 07-08 is less as compareto 06-07. Even it good sign for the company that fixed ratio for the year 07-08is very close 1 which is standard. This shows that fixed asset is financed outof long term fund.Suggestion for improvement – In order to maintain this ratio the company has to increase its long term fund equal to its fixed asset.

d) Proprietary Ratio: Proprietary Ratio establishes the relationship between proprietors’ funds and total tangible assets. This ratio is also termed as ‘Net Worth to Total Assets’ or ‘Equity-Assets Ratio’.

Proprietary fundsProprietary ratio = --------------------

----------Total assets

Where Proprietors’ Funds = Shareholders’ Funds = Share Capital (Equity + Preference)+ Reserves and Surplus – Fictitious AssetsTotal Assets include only Fixed Assets and Current Assets. Any intangible assets

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 23/45

without any mar et value and fictitious assets are not included.Objective and Significance: This ratio indicates the general financial positionof the business concern. This ratio has a particular importance for the creditors who can ascertain the proportion of shareholder’s funds in the total assets of the business. Higher the ratio, greater the satisfaction for creditors of all types.

06-07 07-08Equity share holder’s fund = equity share capital -- 1387.00

1184.08+Reserve & surplus -- +3080.95

+3447.254467.95

4631.33Total asset = fixed asset -- 9997.37 9849.01

+ Current asset -- + 4397.41 +3935.1914394.78 13784.20

4467.95 4631.33Proprietary ratio (06-07) = ----------------- = .31 (07-08) =

----------------- = .3414394.78 13784.20

Proprietary ratio analysis – proprietary ratio for the year 07-08 is more than the06-07. As the ratio is increase it is good sign for company. Higher the ratio b

etter is the long-term solvency position of the company. A low proprietary ratiowill include greater ris to the creditors.Suggestion for improvement – Idle fixed asset should be dispose so that the amountwhich is realize from that can be used in the operation.e) Interest Coverage Ratio: Interest Coverage Ratio is a ratio between ‘net profitbefore interest and tax’ and ‘interest on long-term loans’. This ratio is also termedas ‘Debt Service Ratio’.

Net profit before interest and tax

Interest coverage ratio = --------------------------------------------------

Interest on long term loans

Objective and Significance: This ratio expresses the satisfaction to the lendersof the concern whether the business will be able to earn sufficient profits topay interest on long-term loans. This ratio indicates that how many times the profit covers the interest. It measures the margin of safety for the lenders. Thehigher the number, more secure the lender is in respect of periodical interest.

06-0707-08

Net profit before interest & tax -- 1324.21 1557.78Interest on long term loan -- 563.62 609.89

1324.211557.78

Interest coverage ratio (06-07) = --------------- = 2.34 (07-08) = ---------------- = 2.55

563.62609.89

Interest coverage ratio analysis -- Interest coverage ratio for the year 07-08 is quite more than 06-07. Which is quite good sign for the company. For the 07-08, 2.55 times interests are covered by the profits. The wea ness of the ratio maycreate some problems to the financial manager in raising funds from debt sources.Suggestion for improvement – loan should be ta en at reasonable rate. Interest sho

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 24/45

uld be paid at fixed exchange rate. The exchange rate should be settle at the time of ta ing loan.

Comparison of Essar steel ratio with other steel companies

GROSS PROFIT RATIO

NAME OF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 12.6 25.49 16.42 31.4 27.59JINDAL STEEL 22.15 29.44 21.12 26.99 23.43TATA STEEL 26.63 36.41 33.76 34.91 37.7

Gross profit ratio interpretation –1) Gross profit ratio of Tata steel is increasing from the last 3 years.

2) Where as Essar and Jindal steel ratio shows upward and downward movement which means the ratio of both the company is not stable.3) Gross profit should not be much fluctuates.4) Tata steel has maintained a trend from last 4 years.

Suggestion for improvement – gross profit can be increase if the company efficiently utilize its raw material and try to produce better quality of product and maximize its output with low input. Because major direct expenditure is on materialso that must be efficiently utilize. Company should give more emphasis on enhancing its productivity and even try to get better return on that.

NET PROFIT RATIO

NAME OF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 1.61 9.67 8.54 5.33 3.99JINDAL STEEL 16.05 13 14.14 14.98 14.92TATA STEEL 16 23.72 22.78 23.53 23.43

Net profit ratio interpretation –1) Net profit ratio of Tata steel is best as compare to Jindal and Essar steel.

2) Net profit ratio of Jindal steel is better as compare to Essar steel.3) Both Jindal and Tata steel have maintained a good trend as it shown in the graph from the last four year.4) Essar steel net profit ratio is decline from last three years. This is not good sign for the company. As the ratio decrease the less effective a company is at cost control.5) This ratio is helpful to determine the operational ability of the concern. While comparing the ratio to previous years’ ratios, the increment shows the efficiency of the concern.6) Gross profit of Essar steel is increasing where as its net profit is decreasi

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 25/45

ng which means company’s indirect expenses is increasing.

Suggestion for improvement – the company have to put major control on all expenses. Reductions in expenses result in more profit. As a result the net profit ratioshows increment.OPERATING PROFIT RATIO

NAMEOF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 23.49 31.96 24.23 23.63 21.48JINDAL STEEL 31.69 34.83 27.79 32.79 29.46TATA STEEL 32.47 41.1 38.88 39.61 41.94

Operating profit ratio interpretation –1) Operating profit ratio of Essar steel is decreasing from the last 3 years2) Tata steel has maintained a incremental trend from last 3 years.3) Jindal steel ratio shows upward and downward movement.

4) Operating profit ratio measure a company’s operating efficiency with its successful cost control. The higher the ratio, the better the company is. So here thegraph shows that Tata steel has better control over cost.

Suggestion for improvement – the company has to control its operating expenses. Because less operating expenses will result in more net profit and more net profitwill create wealth of company and its shareholder’s. A higher operating profit put the company to stand in the mar et.

RETURN ON CAPITAL EMPLOYED

NAME OF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 8.41 26.28 10.37 11.86 15.33JINDAL STEEL 11.67 29 15.47 23.6 19.22TATA STEEL 39.43 56.78 43.93 28.11 17.16

Return on capital employed –1) Return on capital employed of Essar steel is continuously increasing from last 3 years which is good sign for the company.2) Where as Tata steel ratio is decreasing from last 3 years.3) Jindal steel shows upward and downward trend.4) Efficiency of Tata steel is decreasing where as Essar steel is increasing fro

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 26/45

m last 3 years.5) The higher the ratio, the better it is.

Suggestion for further improvement -- The Company has to increase its net profitand company has to reduce borrowing by paying through the internal accruals. The company has to maintain its increasing trends.

EARNING PER SHARE

NAME OF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 1.33 14.22 12.33 4.38 3.71JINDAL STEEL 0.79 63 26.17 70.85 86.07TATA STEEL 51.88 62.17 62.57 73.87 60.58

Earnings per share interpretation –1) Earnings per share of Jindal are increasing from last 3 years.2) Where as earning per share of Essar steel is decreasing from last 3 years.3) Tata steel & Essar steel earning per share for the year 07-08 is decrease ascompare to 06-07 but Tata steel EPS is decrease by 18% where as Essar is decrease by 15.30%.4) This shows that Tata and Essar have not effectively utilized their equity share capital for the year 07-08.5) Worth of share of Essar is continuously decreasing.

Suggestion for improvement – earning per share can be improve by increasing the net profit. Company is not able to use efficiently its equity share capital as compare to other companies.

NAME OF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 0.54 0.87 0.59 0.82 1.09JINDAL STEEL 0.52 0.88 0.72 0.81 0.81TATA STEEL 0.85 1.11 0.98 1.09 1.2FIXED ASSET TURNOVER RATIO

Fixed asset turnover ratio interpretation –1) Fixed asset turnover ratio of all the company is increasing from last 3 years. It is good sign for the company.2) The fixed-asset turnover ratio measures a company s ability to generate net s

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 27/45

ales from fixed-asset investments.3) A higher fixed-asset turnover ratio shows that the company has been more effective in using the investment in fixed assets to generate revenues.

Suggestion for improvement – fixed asset should be efficiently utilized up to itsmaximum capacity. Idle fixed asset should be dispose so that the amount which isrealize from that can be used in the operation.

INVENTORY TURNOVER RATIO

NAME OF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 8.73 11.33 6.96 4.67 5.08JINDAL STEEL 15.75 11.21 8.55 11.04 9.26TATA STEEL 12.91 10.42 9.89 10.81 10.84

Inventory turnover ratio interpretation –1) Inventory turnover ratio of all these companies shows ups and downs. There is no trend.2) But from last 2 years Essar steel ratio is just around 50% of Jindal and Tatasteel.3) From last 3 years all the companies have maintained its trends.

Suggestion for improvement -- A low inventory turnover ratio indicates an inefficient management of inventory. A low inventory turnover implies over-investmentin inventories, dull business, poor quality of goods, stoc accumulation, accumulation of obsolete and slow moving goods and low profits as compared to total in

vestment. So in order to increase this ratio companies have to improve the entire thing in positive way. The inventory turnover ratio is also an index of profitability, where a high ratio signifies more profit; a low ratio signifies low profit.

NAME OF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 0.61 0.83 0.89 0.59 0.54JINDAL STEEL 0.79 0.6 0.59 0.43 0.27

TATA STEEL 0.39 0.33 0.29 1.37 3.52LIQUID RATIO

Liquid ratio interpretation –1) Liquid ratio of all these company is not good because the ideal liquid ratiois supposed to be 1:1. This is not there from the year 03-04 to 05-06.

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 28/45

2) Jindal steel liquidity ratio is continuously decline which is not good sign for that company.3) Tata short term financial position is very good in the year 07-08 which showstheir liquid asset is around 3.5 times current liability. And it is increasingfrom last 2 years4) short term financial position of Jindal and Essar is not good.

Suggestion for improvement – As 1:1 standard should not be used blindly. A liquidratio of 1:1 does not necEssarily mean satisfactory liquidity position of the firm if all the debtors cannot be realized and cash is needed immediately to meetthe current obligations. A firm having a high liquidity ratio may not have a satisfactory liquidity position if it has slow-paying debtors. On the other hand, afirm having a low liquid ratio may have a good liquidity position if it has fast moving inventories.

NAME OF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 1.61 2.09 1.97 1.26 1.17JINDAL STEEL 1.45 0.98 0.89 0.76 0.58

TATA STEEL 0.68 0.71 0.72 1.77 3.92CURRENT RATIO

Current ratio interpretation –1) current ratio of Tata steel is continuously increasing from the year 03-04 to07-08.2) Essar steel current ratio is continuously decreasing from last 3 years whichis not good sign for the company. This shows that company’s ability to pay currentliability is decreasing.3) Jindal steel current ratio is decreasing continuously from the year 04-05 to

07-08. This shows that company’s ability to pay current liability is decreasing.4) Tata steel current ratio for the year 07-08 is around 4 which is also not good because it shows the idleness of wor ing capital.5) The minimum acceptable ratio is 1:1, Essar steel current ratio for all the year is acceptable as it is more then 1.

Suggestion for improvement –• Paying some debts.• Increasing your current assets from loans or other borrowings with a maturity omore than one year.• Converting non-current assets into current assets.• Increasing your current assets from new equity contributions.DEBT EQUITY RATIO

NAME OF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 7.69 3.96 4.55 1.5 1.19JINDAL STEEL 3.73 1.3 0.96 0.78 1.01TATA STEEL 0.72 0.37 0.25 0.67 1.07

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 29/45

Debt equity ratio interpretation –1) Debt equity ratio of Essar steel is very high in from the year 03-04 to 05-06which shows the their debt is very high as compare to equity in these years butgeneral acceptable ratio is 2:1 but there is no rule of thumb or stand norm forthe business.2) In the year 07-08 these company debt equity ratio is near to standard norm which is acceptable.3) Essar steel debt equity ratio is decreasing from last 3 year and but now company has to increase its debt to meet the standard norms.

Suggestion for improvement – company should raise its fund by the combination of both equity and debt and try to maintain 2:1 ratio that is debt equity ratio.

PROPRITORS RATIO

NAME OF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 11.12 18.27 15.18 31.03 33.6JINDAL STEEL 19.4 41.09 48.23 54.31 48.53TATA STEEL 57.24 72.04 79.49 59.12 48.15

Proprietor’s ratio interpretation –1) Higher the ratio better is the long-term solvency position of the company.2) A low proprietary ratio will include greater ris to the creditors.3) Jindal steel proprietors ratio shows increasing trend.4) From the last 3 years Essar steel ratio is increasing which good sign for company but whereas Tata steel ratio is decreasing which is not good sign for thatcompany.

Suggestion for improvement – Idle fixed asset should be dispose so that the amountwhich is realize from that can be used in the operation.

INTEREST COVERAGE RATIO

NAME OF COMPANY 2003-04 2004-05 2005-06 2006-07 2007-08ESSAR STEEL 1.87 2.73 3.3 2.34 2.55JINDAL STEEL 3.21 3.72 4.65 5.67 5.88

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 30/45

TATA STEEL 11.29 18.89 26.42 21.07 6.94

Interest coverage ratio interpretation --1) Essar steel has maintained its trend, they have to improve it means so increase the ratio.2) Jindal steel has maintained its increasing trend which is good sign for the company.3) Tata steel ratio from last 2 years it is decreasing which is not good sign for company it shows that company efficiency is decrease.

Suggestion for improvement – loan should be ta en at reasonable rate. Interest should be paid at fixed exchange rate. The exchange rate should be settle at the time of ta ing loan.

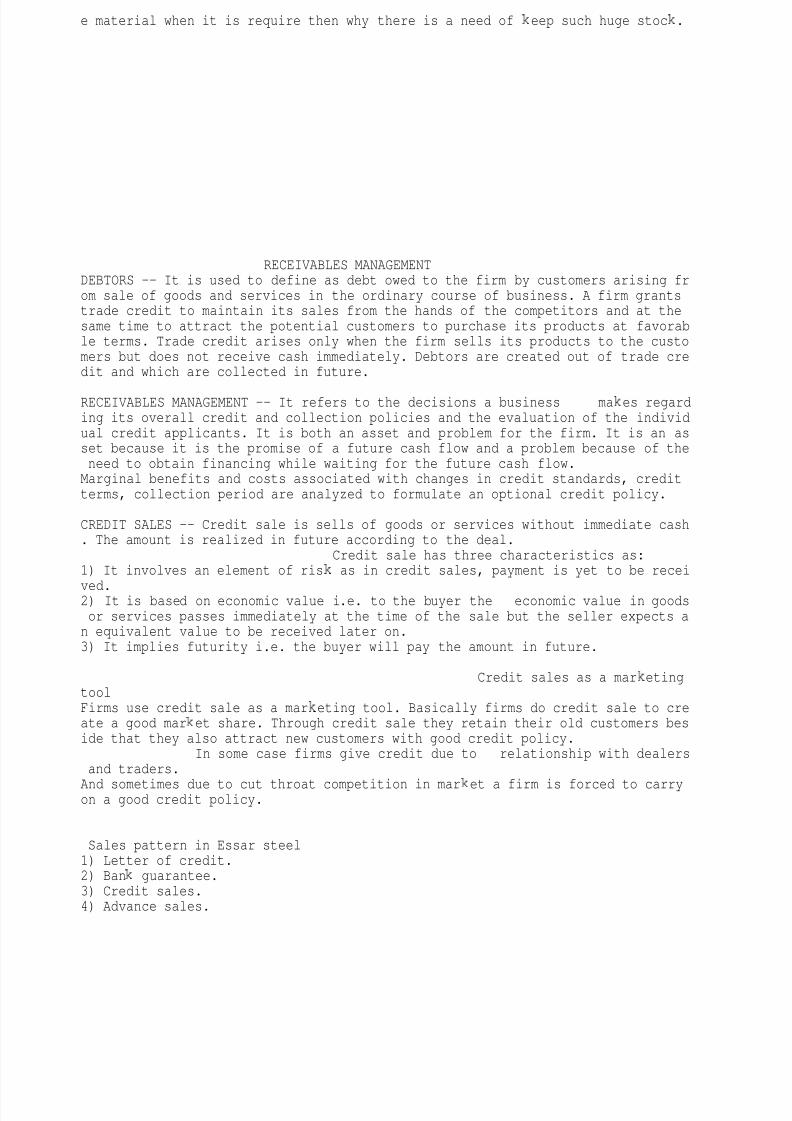

INVENTORY MANAGEMENT

TEAM MEMBERS OF STOREDEPARTMENT

SPARE MANAGEMENT AT STORE DEPARTMENTSpare is most important part of any ind of machinery or for production plant. Spare maintain the capacity of machinery. Non availability of any spare in right

time result in reduction in the performance of machinery or some time it may stop production result in huge loss to company , so proper management of spare isalso require.

INVENTORY PROCEDURE IN ESSAR STEEL1) In bond delivery number2) Receipt section3) Spare quality chec4) Goods receipt note5) Issue of spares

7/31/2019 projet report on working capital and inventory management

http://slidepdf.com/reader/full/projet-report-on-working-capital-and-inventory-management 31/45

6) Rejection of spares7) Codification8) Spare control technique

1) In bond delivery number—it is the number is allocated at gate when spare reach at gate. The authorized person see all the document which is presented by driver li e challen, invoice etc. there he also see the no. of items order and no. of item are there in invoice. Through SAP system. After that he put seal on document and write the vehicle number and other thing and put I.D no. that is called In bond number. After getting in bond no. then vehicle is allow to enter. There at gate the authority as the user that you want the spare now then if user say yes then they directly send the vehicle to concern department but if user sayno then they are sent to central store for unload . in case user want some spare then in that case also vehicle send to central store not send to user for partdelivery because to reduce the time and traffic.2) Receipt section—once the driver get the in bond no. it go to central store. There he shows the document to receipt authority. There he chec the seal andID no. & spare is physical chec .But some time spare is in wood box so to openat that time is not possible so it is chec in no. or box then gate pass is given to driver. If some time same vehicle is use to transport finish goods then ithas to go to gate for clearance and user send a mail for that vehicle then thatvehicle is allowed to particular location.3) Spare quality chec (321) — after the physical verification they inform the user that your spare is reach at store. Then user comes to central store and h

e sees the spare and its quality. If it according to right quality then he put (321) spare quality is chec and accepted. If he put (122) then spare is not according to right quality and rejected. so when he reject the spare that spare iseep away from other accepted spare. After 321 G.R.N is prepared and spare is taen into store and eep them in a particular location.4) Goods receipt note— goods receipt note is note prepare when user give (321) quality chec clearance. GRN shows that we have received this much of quantityof item. Once the GRN is done then the spare is eep into store at its defininglocation.5) Issue of spare— Essar steel has various departments. Various spare which is requires to various department most are available at one place that is at central store.User chec s through system all the spare which is of his department. If it is th

ere in store he through reservation slip put the order. If the require quantityis available then MRS is created and he send the reservation slip with concern person to collect the spare. Through MRS the store person now what spare the user want so they ta e out the spare eep that spare at issue location so that thespare can be easily handover when concern person come for spare. This is all incase of urgent. If it is not urgent then spare is send to concern department some other day as far as possible.When spare is send to concern department at that time issue note is given to security and they put control no. then after issue person collect the issue reservation slip and put spare document no. and post the transaction and file the issuerequisition note.If in case required quantity cannot be covered by issue in that case they issueall quantity but they send the available and rest t they send when spare availab

le at store.User through system he chec all the item what ind of all spare of his department is there in store. In case suppose the required quantity of spare is not at store in that case he order the spare through reservation slip. Spare as per available reserve to him and rest quantity PR is automatically prepare through SAPsystem. That PR is release by store as well as user department head. Once PR isrelease then purchase department place order for purchase of that particular spare.

6) Rejection of spare – when user is called for quality chec at that time u