Projects of Common Interest 2018 - 2019 Regional Meetings... · Energy Projects of Common Interest...

111

Energy Projects of Common Interest 2018 - 2019 Meeting of TEN-E Gas cross - Regional Groups and networks thematic group 7 November 2018, Brussels DG ENER, Networks & Regional Initiatives https://webcast.ec.europa.eu/pci-gas-meeting

Transcript of Projects of Common Interest 2018 - 2019 Regional Meetings... · Energy Projects of Common Interest...

Energy

Projects of Common Interest 2018 - 2019

Meeting of TEN-E Gas cross - Regional Groups and 𝐂𝐂𝐂𝐂𝟐𝟐 networks thematic group

7 November 2018, Brussels

DG ENER, Networks & Regional Initiatives

https://webcast.ec.europa.eu/pci-gas-meeting

Energy

10:00-10:15 Introductionby Catharina Sikow-Magny, Head of Unit Networks & Regional Initiatives, DG ENER

10:15-10:35 Projects of Common Interest (PCI) legal framework: brief overview by Milosz Momot, DG ENER

10:35-11:20 PCI process (2018 – 2019) in view of preparing the 4th Union listTimeline and interventions by Regional Groups and Thematic areas leadersJane Amilhat Deputy Head of Unit Networks & Regional Initiatives, DG ENERRaphael Sauter, RG NSI West leaderAdam Szolyak, RG NSI East leaderMilosz Momot, RG SGC leaderSebastian Gras, RG BEMIP leaderKatrien Prins, Thematic area – CO2 network leader

11:20-12:20 The role of monitoring of PCIs in the overall PCI process:

ACER 2018 monitoring outcomesby Boyko Nitzov, Agency for the Cooperation of Energy Regulators

The inclusion of monitoring results in the 2018- 2019 PCI process-principles by Irina Mihaela Minciuna, DG ENER

Agenda

Energy

Agenda

12:20-14:00 Lunch break

14:00-14:45 The Ten-Year Network Development Plan for gas (TYNDP 2018) : process, scenarios and European needs identificationby Stefano Astorri, European Network of Transmission System Operators for Gas (ENTSOG)

14:45-15:45 Working together: roles and responsibilities in the PCI processby Irina Mihaela Minciuna, DG ENER

15:45-16:00 Next steps by Catharina Sikow-Magny, Head of Unit Networks & Regional Initiatives, DG ENER

Energy

Projects of Common Interest

Legal framework

Energy

COMPETITIVE-NESS

SECURITY OF SUPPLY SUSTAINABILITY

TEN-E Regulation

(347/2013) -addressing

infrastructure needs in a

comprehensive way

Trans-European energy networks are at the heart of the European energy policy

Energy

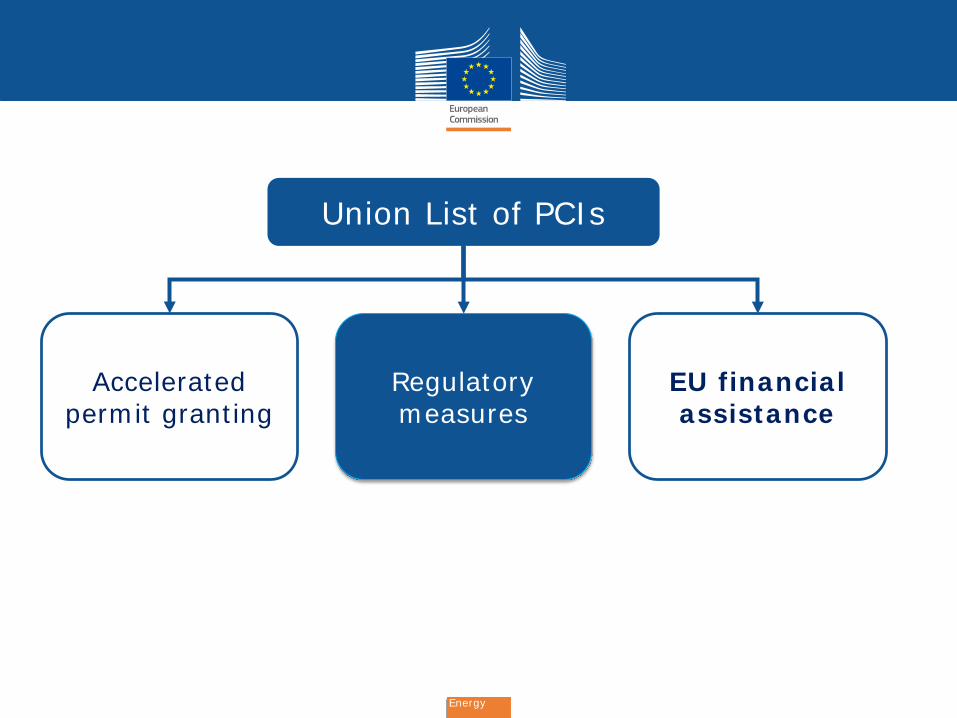

Union List of PCIs

Acceleratedpermit

granting

Regulatory measures

EU financialassistance

Criteria / CBA

CO2 transportE-highwaysSmart grids

Project of Common Interest Benefits

Regional cooperation &

High Level Groups

Energy

Gas infrastructure consist of:Tr

ansm

issi

on • for gas transmission, the project concerns investment in reverse flow capacities or changes the capability to transmit gas across the borders of the Member States concerned by at least 10 % compared to the situation prior to the commissioning of the project;Sto

rage

and

LN

G

• for gas storage or liquefied/compressed natural gas, the project aims at supplying directly or indirectly at least two Member States or at fulfilling the infrastructure standard (N-1 rule) at regional level in accordance with Article 6(3) of Regulation (EU) No 994/2010 of the European Parliament and of the Council

Energy

Union List of PCIs

Acceleratedpermit

granting

Regulatory measures

EU financialassistance

Energy

Permit granting – Regime of common interest

Competent Authority to

manage permit granting process

3,5 years time limit for

the permit granting decision

Increased transparencyand enhanced

public participation

Priority status for PCIs

• Most preferential treatment in Member States

• Streaming of Environmentalassessment procedures

Energy

Union List of PCIs

Acceleratedpermit granting

Regulatorymeasures

EU financialassistance

Energy

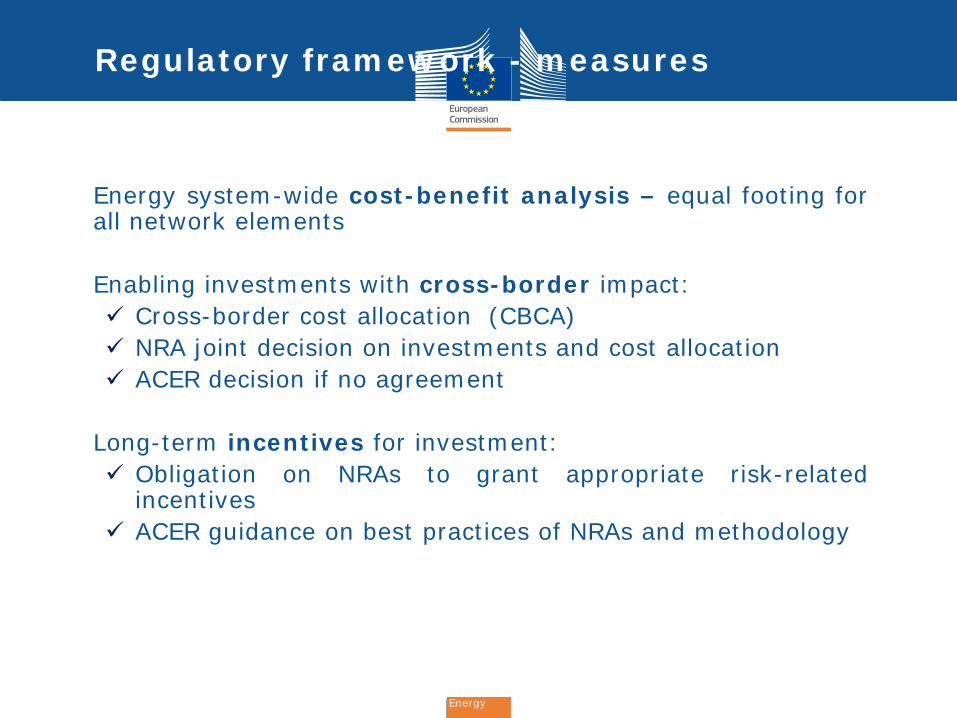

Regulatory framework - measures

• Energy system-wide cost-benefit analysis – equal footing forall network elements

• Enabling investments with cross-border impact: Cross-border cost allocation (CBCA) NRA joint decision on investments and cost allocation ACER decision if no agreement

• Long-term incentives for investment: Obligation on NRAs to grant appropriate risk-related

incentives ACER guidance on best practices of NRAs and methodology

Energy

Union List of PCIs

Acceleratedpermit granting

Regulatorymeasures

EU financialassistance

Structural Funds, EIB, EFSI, Marguerite Fund, EBRD

CEF Regulation 1361/2013 with 5.35bn;

Energy

TEN-E Regulation introducesBENEFITS for PCIs but alsocertain obligations on PCIpromoters

Your project (indeed)But part of a (common)network

Delays may trigger call forproposals for an alternativeproject promoterArt 5(7)(d)

Submit an annual report onprogress achieved, delaysregistered – to ACER(reporting by 31 March)

Draw up an implementationplan including a timetablefor the major milestones ofa project (Art 5(1)) -Transparency platform

Keep project websites up-to-date (Art 9(7))

Share information withinRegional Groups

Promoters obligation

Energy

Projects of Common Interest2018 - 2019 Process

Energy

2018-2019 PCI process gas

Cross regional meeting

Regional meeting

Technical and High Level Decision Making Body meeting

Energy

Step 1: Identification of system needs

• Objective: identify the most relevant needs within the region for which further infrastructure development is necessary

• Input: largely based on the ENTSOG TYNDP data

• Regional groups are responsible for defining the needs of the priority corridors

• Output: agreed needs of the priority corridors.

Energy

Step 2: Projects submission

• Objective: collect the candidate PCI projects

• Input: TYNDP 2018 projects can apply

• Project promoters submit their project/s for the PCI selection in line with the Commission guidance.

• Submission tool: ENTSOG tool developed in line with the Commission requirements.

Note: The Commission is in charge of the submission process, not ENTSOG

• Output: list of candidate PCI projects

Submission window:

20 November 2018 -10 January 2019

Energy

Step 3.1: Public consultation on candidate projects

• Objective: collect public views on the candidate PCI projects

• Input: TYNDP 2018 project sheets + ACER monitoring outcomes + information submitted in the PCI submission window

• Stakeholders & citizens are invited to submit their views on the projects.

• Consultation tool: The EUSurvey tool will be used for this purpose.

• Output: public views per projects summed up in the report on public consultation. These views will be considered by the Regional Groups.

Energy

Step 3.2: National Regulatory Authorities projects consultation

• Objective: collect the NRAs views on the candidate PCI projects

• Input: TYNDP 2018 project sheets + ACER monitoring outcomes + information submitted in the PCI submission window

• NRAs submit their views on all the projects from their national territory.

• Consultation tool: ACER survey tool will be used for this purpose.

• Output: NRAs view per projects, views that will be used by the Regional Groups.

Energy

Step 4: Define methodology and assess the candidate PCI projects

• Objective: define the assessment methodology and based on it assess all the PCI candidate projects

• Input: TYNDP 2018 project data and project monitoring information

• RG members are responsible to agree on the assessment methodology and prepare the Decision Making Body decision.

• Output: Assessment methodology and outcome of the methodology implementation per priority corridor.

Energy

Step 5. PCI list adoption and ACER opinion

• Objective: Technical and High Level Decision Making Body PCI lists per corridor adoption

• Input: RGs assessment resultsand ACER opinion

• Technical and High Level Decision Making Body are responsible to adopt the list.

• Output: 4th PCI list to be formally adopted by the Commission [Delegated Act]

Energy

Projects of Common Interest

Gas Regional Groups & Thematic Group Cross-border carbon dioxide network

Energy

• Electricity regional group leaders:NSI West leader: Raphael SauterRG NSI East leader - Adam SzolyakRG SGC leader: Milosz MomotRG BEMIP leader: Sebastian Gras

•Thematic area CO2 network: Katrien Prins

Energy

North-South gas interconnections in Western Europe

North-South gas interconnections in Western Europe (‘NSI West Gas’): gas infrastructure for North-South gas flows in Western Europe to further diversify routes of supply and for increasing short-term gas deliverability

Member States concerned: Belgium, Denmark, France, Germany, Ireland, Italy, Luxembourg, Malta, the Netherlands, Portugal, Spain, the United Kingdom;

Energy

North-South gas interconnections in Central Eastern and South Eastern Europe

North-South gas interconnections in Central Eastern and South Eastern Europe (‘NSI East Gas’): gas infrastructure for regional connections between and in the Baltic Sea region, the Adriatic and Aegean Seas, the Eastern Mediterranean Sea and the Black Sea, and for enhancing diversification and security of gas supply.

Member States concerned: Austria, Bulgaria, Croatia, Cyprus, Czech Republic, Germany, Greece, Hungary, Italy, Poland, Romania, Slovakia, Slovenia;

Energy

Southern Gas Corridor

Southern Gas Corridor (‘SGC’): infrastructure for the transmission of gas from the Caspian Basin, Central Asia, the Middle East and the Eastern Mediterranean Basin to the Union to enhance diversification of gas supply.

Member States concerned: Austria, Bulgaria, Croatia, Czech Republic, Cyprus, France, Germany, Hungary, Greece, Italy, Poland, Romania, Slovakia, Slovenia;

Energy

Baltic Energy Market Interconnection Plan in gas

Baltic Energy Market Interconnection Plan in gas (‘BEMIP Gas’): gas infrastructure to end the isolation of the three Baltic States and Finland and their dependency on a single supplier, to reinforce internal grid infrastructures accordingly, and to increase diversification and security of supplies in the Baltic Sea region.

Member States concerned: Denmark, Estonia, Finland, Germany, Latvia, Lithuania, Poland, Sweden.

Energy

PRIORITY THEMATIC AREA: Cross-border carbon dioxide network

Cross-border carbon dioxide network: development of carbon dioxide transport infrastructure between Member States and with neighbouring third countries in view of the deployment of carbon dioxide capture and storage.

Member States concerned: All

Energy

ACER monitoring

2018 report outcomes

Energy

Inclusion of monitoring in the PCI process

Energy

The Projects of Common Interest are chosen due to their high benefit to the Energy Union

In order to bring the benefits to citizens and businesses the PCIs need to be implemented on time

Monitoring by the Regional and High Level Groups is necessary to check and support the timely implementation of PCIs

Energy

Copenhagen Forum conclusion

• “The Forum asks the Regional Groups members to increase their involvement in the project implementation in line with the legal requirements. In addition, the Forum asks the Regional Groups to include the monitoring in the process of defining the future PCI lists.”

Energy

Regional Group members:

• 1. acknowledge the importance of monitoring for the PCIs implementation

• 2. agree to include the PCI monitoring outcomes in the PCI assessment methodology

• 3. follow and support the PCIs implementation under the Regional and High Level Groups fora

Energy

Working together: roles and responsibilities

Energy

Overview of roles & responsibilities

Energy

Cooperation Platform

Members: ENTSOG, ACER and European Commission

Regular meetings: Feb2018 until March/April 2019

Tasks: 1. Makes sure that TYNDP

material fulfills the PCI process needs

2. Makes checks on data necessary for the PCI process

3. Supports in the drafting of the PCI assessment methodology

4. Continuous support to the Regional Groups in the PCI process

Energy

Regional Groups

Members: Member States, National Regulatory Authorities, ENTSOs, ACER, promoters and European Commission

Regular meetings: Q3/2018-Q2/2019

Tasks: 1. Identifies and agrees on

the Regional infrastructure needs/ gaps

2. Agree on the PCI assessment methodology

3. Discusses and makes recommendations to facilitate implementation of PCIs

Energy

Regional Groups –NRAs

1. Annex III.2.(7) For proposed projects falling under the categories set out in Annex II.1 and 2, national regulatory authorities, and if necessary the Agency, shall, where possible in the context of regional cooperation (Article 6 of Directive 2009/72/EC, Article 7 of Directive 2009/73/EC), check the consistent application of the criteria/ cost-benefit analysis methodology and evaluate their cross-border relevance. They shall present their assessment to the Group.

2. Within the context of the Regional groups discusses and makes recommendations to facilitate implementation of PCIs

Energy

Regional Groups – Stakeholders

Stakeholders are invited to participate in meetings throughout the process [where appropriate] and engage in discussions, especially regarding the needs identification in the regions.

Stakeholders and the general public are also consulted on the list of the candidate projects at the beginning of the process through an open consultation.

Energy

Decision Making Body

Members: Member States and European Commission

Meeting: June-Sept 2019

Tasks: • Following Regional Groups

recommendation discusses and adopts the regional PCI lists

Energy

The Ten-Year Network Development Plan for gas (TYNDP 2018)

- process, - scenarios- European needs identification

Energy

Projects of Common InterestNext steps

Energy

PCI submission

• Period: 20 November 2018 – 10 January 2019

• Submission through online tool

• All the data available in the TYNDP will be automatically considered (including costs)

• For a cross-border infrastructure to be considered eligible to enter the PCI process all of its projects must be submitted (e.g. Interconnector A-B= [country A to border] + [border to country B]). Failure to comply with this requirement will result in project elimination. The cross-border project promoters are advised to discuss with their counterpart before submitting their part of the project.

Energy

Regional system needs assessment

• Next meetings will be hold in the regional format:

• 2nd week December

• The meetings are also open to the public

• For the meetings preparation the RGs member will receive:

• End November – the draft ENTSOG System needs report

Energy

Public PCI candidate consultation

• Period: mid-January – mid March

• Open to all the interested public

• Similar with the past PCI consultation

Energy

NRAs consultation

• Period: mid-January – mid March

• Based on an online questionnaire

• NRAs will be asked to check the consistent application of the criteria/ cost-benefit analysis methodology and evaluate their cross-border relevance

Energy

European Commission contacts – PCI process:

For general inquiries: [email protected]

Regional group leaders:

NSI West leader: Raphael SauterEmail: [email protected] Phone: +32 229-92827

RG NSI East leader - Adam SzolyakEmail: [email protected] Phone: +32 229-84032

RG SGC leader: Milosz MomotEmail: [email protected] Phone: +32 229-80750

RG BEMIP leader: Sebastian GrasEmail: [email protected] Phone: +32 229-83127

Thematic area – CO2 network: Katrien PrinsEmail: [email protected] Phone: +32 229-60353

THE ROLE OF MONITORING OF PCIS IN THE OVERALLPCI PROCESS:

ACER 2018 MONITORING OUTCOMES

Meeting of the TEN-E Cross-Regional Group on Gas Brussels, 7 November 2018

The views expressed in this presentation are those of the presenter and not necessarily of the Agency, any of its Boards, or any NRA.

1

Needs, gaps, assessment tools

A Look Back to 2017 PCIs

Source: This slide is based on the Agency’s Opinion on the Draft 2017 Gas PCI List, http://www.acer.europa.eu/Official_documents/Acts_of_the_Agency/Opinions/Opinions/ACER%20Opinion%2013-2017.pdf

• Clear link between the infrastructure needs and the assessed features of the projects:

• Infrastructure gap or may introduce redundant capacities? Most IPs currently do not show signs of congestion

• Bottom-up approach - involve stakeholder views about problems and needs• Still… gap between projects supported by the market and proposed for the PCI

list was significant• Define minimum mandatory information to be provided by project

promoters in their application• ENTSOG to make the TYNDP better for the purpose of the PCI selection:

• PS-CBA should be available as an output of the TYNDP• Update of the PCI assessment methodology should start as soon as the format

of the output of the TYNDP 2018 is developed• The most pressing deficiency in 2017 was the CBA methodology: limited

availability of benefit and cost data, esp. in monetary terms in the TYNDP• The updated CBA methodology to be communicated by ENTSOG to the

European Commission before the process starts (done!)

2

PCI Monitoring Results 2017

A Look Back to 2017 PCI Progress

Source: This slide is based on the Agency’s Consolidated Report on the progress of electricity and gas Projects of Common Interest for the year 2016, Vol. 2 – Gas http://www.acer.europa.eu/Official_documents/Acts_of_the_Agency/Publication/Consolidated%20Report%20on%20the%20progress%20of%20electricity%20and%20gas%20projects%20of%20Common%20Interest%20for%20the%20year%202016.pdf

• Transmission dominates planned investments… only in 2 cases would bring gas by pipeline from new sources;

• About €6 billion invested since 2013 (€3.2 billion in 2016 alone);• Investment bulk went into just 2 PCIs in SGC. Investment levels do not correlate well

with reported commissioning dates;• 21 PCIs filed investment requests incl. CBCA, 13 intend to apply;• 8 applied for specific incentives, 35 not decided yet, 42 do not plan to apply;• 4 applied for exemptions, 15 not decided yet, 61 do not plan to apply.

3

Refined Monitoring Tools, Looking for Trends

New in 2018 PCI Monitoring

Source: This slide and the next ones are based on the Agency’s PCI Monitoring Report 2018, available from: https://www.acer.europa.eu/Official_documents/Publications/Pages/Publication.aspx

• New information support system (“VALVE”), remotely accessible:• Pre-filled with TYNDP 2017 data, promoters could confirm that the information

is still valid or provide an update (53 PCIs, 98 investment items)• Information at the level of each investment item, then converted and

aggregated (if applicable) to PCI level• Reports for 52 out of the 53 PCIs by the legal deadline, 1 PCI after the deadline

• Project life-cycle cost data missing or incomplete for 66% of the PCIs• Only 6 PCIs were able to indicate the value of benefits• PCIs are subject to CBA already at the stage of preparing the PCI list, so

the lack of any estimate of the value of a project’s expected lifecycle costs and benefits casts fundamental doubts on the projects merits’ level.

• Recommended by the Agency:• Foresee in the CBA methodology ways and means to allow project promoters

to assess / update the lifecycle value of the costs and the monetised benefits• Promoters to evaluate the costs and the benefits of their projects from the

inception of the project and to track the progress of the costs and benefits over the entire project cycle

4

PCIs and NDPs (1/2)

New in 2018 PCI Monitoring

• NDPs typically include the national sections of cross-border gas transmission projects, but – as a rule – do not consider the cross-border effects of LNG or UGS projects located outside their geographical scope

• 12 PCIs are entirely absent from the NDP of their hosting countries (6 transmission, 5 UGS and 1 LNG project)

• 11 investment items of PCIs are missing from the NDP of at least one of the hosting countries

• Reasons for the absence of a PCI in the NDP (as reported):• No NDP exists in the country or the operators are not required to prepare and

publish an NDP (8 instances);• The project is not developed by the TSO, but by an independent developer (6

instances);• The NDP was prepared at an earlier date compared to the date of the adoption

of the PCI list, the PCI will be proposed for the next NDP (4 instances);• The promoter has not yet applied for a connection to the national transmission

system and thus is out of the scope of the NDP (3 instances).

5

PCIs and NDPs (2/2)

New in 2018 PCI Monitoring

• TYNDP should build on NDPs, so PCIs should build on NDPs• Promoters should always first apply for inclusion in the relevant NDPs (where

applicable)• If a valid reason exists which prevents a promoter from first applying for

inclusion of a project in the relevant NDPs (e.g. no NDP exists), then promoters should first consult the relevant NRAs and other relevant offices in the concerned MS, before applying to the PCI list

• Greater consistency is recommended in the assessment of the cross-border impacts of gas transmission (pipelines, compressor stations), LNG, and UGS projects

• Each investment item should exist only in one instance on the PCI list:• Avoid having the same investment item or project component as a part of

several PCIs (to avoid double counting the project characteristics and potential confusion in the treatment of investment requests under Article 12 of R. No 347/2013 and also in subsequent requests for grants

• Make sure that the scope of the investment associated with the relevant PCI and its costs and benefits is clearly defined and uniquely attributable to the PCI

6

Advancement

PCI Monitoring Results 2018

• 25 PCIs in the current list were on the 2015 PCI list in the same form• 5 of these PCIs made progress (2 moved from permitting to construction and 3

advanced into the permitting phase), 13 PCIs remained unchanged, 7 PCIs registered since 2015 a setback or “reverse progress”, i.e. they are currently in a less advanced status than before

• Decreasing number of PCIs for which no work was reported• However, in many cases no work was carried out, but the PCI is still reported to be

“on time”, which looks inconsistent• Only 5 PCIs advanced from one stage to the next one in 2017

Status as of31 January 2018:

PCI Monitoring Results 2018

Cost• Total investment costs for all projects in the 2017 PCI list amounts to €43.5

billion, €9 billion less than in 2015• Up variations mostly due to technical changes and/or more precise budget• Down variations mostly due to a more precise budget or revised calculations

• Promoters plan to invest €15 billion and €10 billion in 2022 and 2023 respectively, i.e. about 60% of the total investment costs within 5 years, 57% in just two years (2022-2023)

• At the same time, promoters indicated that the costs actually incurred since the first PCI list (October 2013, i.e. over >4 years), amount to €9.65 billion (about €2.5 billion p.a.)

• For the investment plans actually to be carried out by 2023 as indicated by the promoters, the pace of investment would have to accelerate in the next few years by almost 300% p.a. compared to the observed levels since 2013

• 54% of total investment costs for pipelines (incl. CS) is in the SGC (up from 42% in 2017), 51% of total CS power also occurs in the SGC

7

PCI Monitoring Results 2018

Planned Pipeline Infrastructure, Cost Factors• More than 17,000 km of planned PCI pipelines, 1,000 km less than in 2017 - approx.

2x the estimated length of pipelines to be constructed in Europe over the next few years as reported by industry sources (“probable pipeline projects in Europe”) -9,613 km. Moreover, industry assessment covers all Europe to the Urals

• Reasonably good correlation of reported cost to pipe diameter, length, max operating pressure, terrain, population density, onshore/offshore

• Considering UIC, promoters “prima facie” may overestimate investment costs. Reported cost >UIC by 46%, up from 33% in 2017. Still, in the majority of instances reported costs appear to remain within a reasonable range

8

PCI Monitoring Results 2018

Benefits

• Benefits assessment was provided in just 6 cases• The results of this and of all the previous monitoring round carried out by

the Agency repeatedly demonstrate that promoters are not in a position to provide clear and easily understandable quantified (monetised) data about the benefits of their projects, or have no intention of calculating monetised benefits

• The Agency hopes that the 2nd CBA methodology will enable promoters to properly assess the benefits of their projects, as repeatedly recommended by the Agency in its Opinions

• The Agency calls on project promoters to evaluate the monetised benefits of their projects and provide the result in their annual reports to the Agency

9

PCI Monitoring Results 2018

Commissioning• If past reported implementation patterns continue in the future, the commissioning

dates of some projects are likely to be postponed• High peak of investment in the few coming years, if commissioning is to take place

according to schedule… but few projects are reported to be under construction• A bit less than half of the PCIs are reported to be on time and the other half is

reported to have fallen behind schedule – in one year…• No PCIs were planned to be commissioned in the lifetime of the 2015 PCI list• Only 7 PCIs are planned to be commissioned during the lifetime of the current PCI

list, i.e. in 2018 and 2019

Expected year of commissioning by corridor:

10

PCI Monitoring Results 2018

Rescheduling, Delays• Rescheduling in most cases is the result of one or more of these:

• Re-prioritisation of the project’s implementation against other investments of the project promoter

• Changes due to complementarity with the rescheduled infrastructure investments of another project promoter

• Gas market uncertainties, changes in the gas demand/supply balance• Delay is most likely to occur due to one or more of these:

• Environmental issues (including re-routing and/or re-siting, problems with cultural heritage or other authority involved in the environmental procedure)

• Financing reasons• Permit granting process

• To resolve the issues that caused difficulties, promoters typically resort to:• Requests for government support for permitting and regulatory decisions• Entering into new commercial contracts with suppliers/shareholders• Undertaking risk management activities• Grants

11

PCI Monitoring Results 2018

Facilitating Project Advancement and Continuity

• Define a consistent set of key project milestones and use aligned lists of project description items by key stakeholders (NRAs / Agency, ENTSOG, the European Commission, and INEA)

• The 2-year period of validity of the PCI lists represents a much shorter timeframe than the typical life cycle duration of a PCI

• The Agency sees value in re-evaluating regularly the PCI status granted to projects, to ensure that they still make sense in an ever evolving context. The Agency sees the 2-year frequency for this exercise as appropriate

• However, the Agency recommends that consideration is also given to better reconciling the duration of the PCI list validity with the observed duration of the typical PCI life cycle

• The Agency recommends using the results of the monitoring of the progress of projects already on the PCI list in the selection for future PCI lists, to make sure that the continuous relevance and progress of projects over longer period of time are properly considered

12

Thank you for your

attention

Thank you for your attention

The views expressed in this presentation are those of the presenter and not necessarily of the Agency, any of its Boards, or any NRA.

Ten-Year Network Development Plan for gas (TYNDP 2018)

Stefano AstorriInvestment Subject Manager, System Development

Process, scenarios and European needs identification

Brussels, 7 November 20184th PCI Regional Groups

<Code>_Rev_0

2

1234

TYNDP 2018 Process

TYNDP 2018 Scenarios

ENTSOG 2nd CBA Methodology

Infrastructure gaps

3

1234

TYNDP 2018 Process

TYNDP 2018 Scenarios

ENTSOG 2nd CBA Methodology

Infrastructure gaps

4

TYNDP 2018 Report Main elements

Demand Scenarios

Supply Scenarios

PS-CBA

CBA 2.0

ProjectFiche

Part of TYNDP 2018

Adapted version applied to TYNDP 2018

Infrastruct.gaps

System Assessment

Infra. data& Map

PRJ Name PRJ Status Code Project Name

Physical Reverse Flow

at Moffat interconnection

point (IE/UK)

Less-Advanced TRA-N-829PCI 5.1.1 Physical Reverse Flow at Moffat inter point (IE/UK)

Physical Reverse Flow

at Moffat interconnection

point (IE/UK)

Less-Advanced TRA-N-1064 Moffat Physical Reverse Flow

Bidirectional Austrian -

Czech Interconnection

(BACI)

Advanced TRA-N-21 Bidirectional Austrian-Czech Interconnector (B

Project Main Information

TYNDP 2018 project draft list

5

TYNDP 2018 process: main steps

Gas and Elect. ENTSOs Scenario Development

Gas CBA Methodology 2.0

Inclusion of projects in TYNDP

System & needs assessment

Projects assessment**

Final TYNDPReportDraft TYNDP Report *

Public workshop, webinar, SJWS or Prime Mover WS

Consultation with the member statesPublic consultationSubmission of projects in TYNDP

Mar’16 Dec’16 Dec’17 Jul’18 Dec’18 Jun’19

Adapted CBAM (Oct)

CBAM EC approval (?)

ACER Opinion (2 months)

Sep’18

June-18: publication of TYNDP projects

Mid-Dec-18: publication identification of gaps

End Jun-19: publication of Final TYNDP

End Jan-19: publication PS-CBA

fiches

ENTSOG TYNDP 2018 will support European Commission 4th PCI process• Or after CBAM approval by Commission** For PCI applicants

6

TYNDP 2018 Project Collection> 207 investment submitted for TYNDP 2018 (link)for ~ 165 overall projects.> Concerning 37 countries> Of which 10 countries not being part of EU

7

1234

TYNDP 2018 Process

TYNDP 2018 Scenarios

ENTSOG 2nd CBA Methodology

Infrastructure gaps

8

TYNDP 2018 Scenario Building ProcessDec ’16 Dec ’17

Gas and electricity ENTSOs Scenario Building

Draft scenario storylines

25/04/2016

Public WebConsultation

12/06/2016

Workshop

Workshop

Scenario storylines

Workshop

02/06/2016 05/07/2016 10/10/2016

Public WebConsultation

Data collection

Scenario building process

Draft Scen.

Report

Final Scen.

Report

Public WebConsultation

Workshop

09/10/2017

02/10/2017 10/11/2017

Workshop

30/03/2018

A 2-year process with thorough stakeholder engagement

from TYNDP 2017….

9

Towards a joint scenarios development

To create a common framework on which assess consistently System and Infrastructure Projects

… to TYNDP 2018

10

What Regulation states..

> Annex V of Regulation (EU) No 347/2013, covering the methodology for a harmonized energysystem-wide cost-benefit analysis for projects of common interest, specifies that:(1) The methodology shall be based on a common input data set representing the Union’s electricity and

gas systems in the years n+5, n+10, n+15, and n+20, where n is the year in which the analysis isperformed.

> Art. 11.8 of Regulation (EU) No 347/2013,(1) By 31 December 2016, the ENTSO for Electricity and the ENTSO for Gas shall jointly submit to the

Commission and the Agency a consistent and interlinked electricity and gas market and networkmodel including both electricity and gas transmission infrastructure as well as storage and LNGfacilities, covering the energy infrastructure priority corridors and areas and drawn up in line with theprinciples laid down in Annex V. After approval of this model by the Commission according to theprocedure set out in paragraphs 2 to 4, it shall be included in the methodologies.

Why a joint exercise?

11

Scenarios overview

3 storylines reflecting future increasing uncertainty

All scenarios have been built as realistic and technically sound, aiming at reducing emissions by 80 to 95% in line with EU targets for 2050

Decarbonisation and energy efficiency reshape energy demand, with gas having a role in all demand sectors.Gas demand decrease in some scenarios. Natural gas partially compensated by renewable gas.

Gas to power stems from modelling power generation mix

Gas and electricity demand

Coordinated approach on heating and transport sectors

Coordinated approach on heating and transport sectors

Electricity demand Gas demandTwh/y

Twh/y

13

Decarbonisation of gas supply

Different scenarios foreseeing different levels of renewable gas penetration. Future infrastructure projects will more and more focus on integration of renewable and decarbonized gases.

14

Peak gas demand

Peak demand is a key element of infrastructure design. Gas peak demand is mostly maintained over time especially for power generation.

Gas peak demand TYNDP 2018 Historic gas and electricity consumption

Gas Peak Winter 17/18

GW

h/d

Electricity demand

Gas demand

15

Reaching EU’s climate targets with the gas infra

Hybrid system allows high CO2 reductions at low cost. Gas infrastructure can cope with increasing shares of renewable gas. Additional infrastructure could further support renewable gas integration and CO2 reduction.

0

500

1.000

1.500

2.000

2.500m

t CO

2 eq

uiva

lent

CO2 reductions in gas and electricity system

40% Reduction 60% Redution 80% Redution

16

TYNDP 2018 scenarios evolution

TYNDP 2018 scenarios on a narrower range compared to TYNDP 2017 while still ensuring to capture a big envelope of future development and ensure a robust infrastructure assessment.

For TYNDP 2017 the values for 2040 have been interpolated since available only until year 2035.

TWh/y Max TYNDP 2017

17

1234

TYNDP 2018 Process

TYNDP 2018 Scenarios

ENTSOG 2nd CBA Methodology(and its application to TYNDP 2018)

Infrastructure gapd

18

2nd ENTSOG CBA Methodology

ENTSOG has released its Adapted CBA Methodology forEuropean Commission approval> Main improvements:

more streamlined methodology

increased transparency

refined supply and supply price methodology

refined market modelling assumptions

indicators simplification

project grouping guidelines

compulsory cost provision

improved sensitivity analysisclickhere

19

TYNDP assesses the gas infrastructure against the Union energy policies

Is further infrastructure needed? (1)

Sustaina-bility

Security of supply

Market integration

Compe-tition

Are they achieved with the existing infrastructure and FID projects?

Yes

No further infrastructure needs

No

TYNDP assesses further infrastructure development

> FID projects + advanced projects> FID projects + 3rd PCI list projects> Single PS-CBAs

Existing + FID = Low infra level

Exist.+FID + Advanced= Advanced infra level

Exist.+FID + PCI 2nd list= PCI infra level

CBA Methodology as common metrics to system and project assessment

20

Is further infrastructure needed? (2)

System Assessment PS-CBA

Infrastructure Gaps ?

Does ADVANCED

projects solve the needs?

Does 3rd PCI projects solve

the needs?

Infrastructure Levels (assessed grid)

Existing + FID* projects

* before TYNDP 2018 project data collection ended

Existing + FID* + Advanced

projects

Existing + FID* + 3rd PCI projects

v

benefits of projects measured through INCREMENTAL

APPROACH against :

Existing + FID* projects

Existing + FID* + Advanced

projects

Infrastructure Levels

21

1234

TYNDP 2018 Process

TYNDP 2018 Scenarios

ENTSOG 2nd CBA Methodology

Infrastructure gaps

22

Security of supply

• Resilience to extreme temperature• Resilience to many supply and infrastructure disruptions

Market integration and competition• Most of Europe has access to diversified supply sources• Hub prices converge most of the time – especially in Western Europe

Sustainability• The existing EU gas infrastructure is generally already able to

complement renewable generation and integrate renewable gases

In specific areas further infrastructure needs remain

What the EU gas infrastructure already achieves

23

Competition

24

Supply Source Access (SSA)> Infrastructure perspective to the share of countries’ demand able to benefit from decrease of price of a given supply source> If 20%* of the demand can benefit from this decrease, the country is considered accessing the source> Tariffs pancaking effect allows for more realistic source spread among countries

2020 2030 (DG) 2040 (GCA)

* Given a certain threshold, supplies with a limited potential may not appear as an additional source for countries with large demand. Results are shown for selected scenarios

HR, GR, FY, RO showing limited number of sources in ST

BG, HR, DK, EE, GR, HU, PT, SI, ES, SE, showing limited number of sources in ST

BG, FY, EE, FI, LV, LT, RO, PT, ES show limited source differentiation.MT and CY isolated.

25

> Unreducible share of this source necessary for a country to cover its demand on a yearly basis> Cooperative approach: countries will align their dependence level as long as infrastructures allow for it> Dependence > 25% indicates that at least one quarter of the demand need to be supplied from this source

Supply Source Dependence (SSD) - Russia

Countries with SSD > 25% in other scenarios: AT, BE, SI, SE

Countries with SSD > 25% in other scenarios: DE and NL

Future situations improves for BH, BG, FY and RS thanks to FID projects

2020 2030 DG 2040 GCA

Results are shown for selected scenarios

26

> At EU level, limited dependence on LNG> Some country limitations still exist> LNG dependence considers LNG as single source (but tested also as multisource)

Supply Source Dependence (SSD) – Global LNG

Iberian peninsula showing even higher dependence in ST scenarios

Iberian peninsula showing limited dependence but increasing over time

2020 2025 (DG) 2030 (GCA)

Results are shown for selected scenarios

27

Supply needs over time

Access to new supply sources – indigenous or extra-EU - would contribute to maintain supply diversification and flexibility

TWh

max potential

min potential

28

> A country is better diversified from an infrastructure perspective if its entry are sufficiently balanced between its borders.

> Countries with LICD < 5000 considered sufficiently diversified in terms of capacity.

LNG and Interconnection Capacity diversification (LICD)

2020 2030 (DG) 2040 (GCA)

Results are shown for selected scenarios

Some SEE countries improves due to commissioning of FID projects

29

Market Integration

30

Price convergence

Marginal price can generally converge even in case of high price variation of Russian and LNG supply, with a rather Central-Western / Eastern Europe discrepancy in case of significantly high Russian or LNG price

2020

2040

RU max RU min LNG max LNG min

RU max

Results are shown for selected scenarios

> Refined supply methodology and tariffs inclusion allow to better identify price differentials> Projects may contribute to further price convergence

RU min LNG max LNG min

31

Security of Supply

32

Assessment of the resilience of the European gas system to cope with various stressful events>Climatic stressPeak day demand2-week cold spell

>Supply route disruptions in case of climatic stress*1. Ukraine route2. Belarus route3. Imports to Baltic states and Finland4. Algerian import pipelines

>Infrastructure disruptionSingle Largest Infrastructure disruption of each country, during a peak day

Risk of demand curtailment (CD)

*Based on risk groups defined by SoS regulation 2017/1938 (Annex I)

33

Climatic Stress – Peak day> The assessment shows that most of the EU gas system is resilient to Peak and 2-Week demand

situations> Only Croatia presents demand curtailment from 2025 onwards and FYROM only in 2025.

2020 2030 (DG) 2040 (GCA)

Results are shown for selected scenarios

34

2020

> Some countries (SEE) showing risk of curtailed demand in all scenarios due to infrastructure limitations> In ST Europe has not sufficient capacities of alternative import routes from Russian supply, impacting also

Western European countries

2030 – 2040 (DG/GCA) 2030 – 2040 (ST)

Supply Route Disruption - Ukraine

Results are shown for selected scenarios

Commissioning of FID projects allows more countries to share the risk.

2020

> Under Belarus transit disruption most of the gas system is resilient but Lithuania in all scenarios from 2030 onward Poland in ST

Supply Route Disruption - Belarus

2030 (DG) 2040 (ST)

Results are shown for selected scenarios

36

> Finland and Estonia exposed to a high risk of demand curtailment from 2020 onwards> Lithuania exposed from 2025 due to decommissioning of Klaipeda LNG

Supply Route Disruption - Baltic States and Finland

2020 2030 2040

Results are shown for selected scenarios

37

> Until 2030 European gas system is resilient to a disruption of all import pipelines from Algeria.> From 2030, whilst the EU is generally resilient, the Iberian Peninsula may be exposed to a limited risk of

demand curtailment in all scenarios resulting from an increasing peak demand in all scenarios.

Supply Route Disruption – Algeria pipelines

2020 2030 2040

Results are shown for selected scenarios

38

> It considers the disruption of the Single Largest Infrastructure disruption > The indicator is simulated and takes into account possible bottlenecks before the disrupted infrastructure

Largest Infrastructure Disruption

DK faces risk of curtailment in EUCO and ST while PL in EUCO but limited

More countries facing curtailment in DG and ST

Most exposed: SE, FI, EE, RO, GR, IE with BG and RS only in 2020

Results are shown for selected scenarios

> In ST (2030-2040), SLI disruption in Slovakia can expose all Europe to an overall gas shortage (≈400 GWh on a peak day)

2020 2030 2040

Adaptation of L-gas to H-gasNetherlands, Germany, Belgium and France markets are partly supplied with L-gas.

> Starting from 2020, part of the local gas demand in BE, FR and DE will be converted from L-gas to H-gas> L-H gas conversion is already considered in the Low assessment> ENTSOG will run Ps-CBAs for L-H gas projects

40

Next steps

41

Project-specific assessment process in TYNDP 2018

PS-CBA only on projects for which promoters have stated the intention to apply to PCI in point 1

>ENTSOG is currently running PS-CBA on project groups>List of project groups published by ENTSOG here>Promoters will be delivered with all main PS-CBA results

Thank You for Your Attention

ENTSOG -- European Network of Transmission System Operators for GasAvenue de Cortenbergh 100, B-1000 Brussels

EML:

WWW: www.entsog.eu

Stefano AstorriInvestment Subject Manager, System Development

43

Global Climate Action

44

Sustainable Transition

45

Distributed Generation

46

Peak Demand

Electricity peak demand TYNDP 2018 Gas peak demand TYNDP 2018

47

Ensuring the consistent assessment of the two key energynetworks of Europe against the same futures> The ENTSOs joint scenario building process for TYNDP 2020 has started,

after it was applied for the first time for TYNDP 2018.

> Scenarios cover all energy use, in Transport, Heating and Industry, andaddress the role of the energy carriers gas and electricity.

> Carbon emissions and RES integration are key features in the scenariodevelopment.

Joint ENTSOs Scenario Development

TYNDP 2020 scenario development has startedCarbon emissions and level of de-/centralisation are key features

48

Infrastructure level composition

49

CBA 2.0 Indicators

> For indicators in benefits from projects can be verified in terms ofmitigating/solving the identified infrastructure gaps up to a certainthreshold

> For all other indicators, any improvement from the current situation canbe considered as benefit from projects assessed in the PS-CBA phase

50

Limited Supply Source Access

2020 Shares per source for each country