Project Report Of Ratio Analysis

78

1 1 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.) A PROJECT REPORT ON WORKING CAPITAL & RATIO ANALYSIS UNDERTAKEN AT HINDUSTAN NATIONAL GLASS & INDUSTRIES LTD. VIRBHADRA, RISHIKESH (UTTARAKHAND) SUBMITTED BY RAHUL KUNDLIYA REG.NO: 11001882 OF LOVELY PROFESSIONAL UNIVERSITY JALANDHAR NEW DELHI GT ROAD, PHAGWARA PUNJAB

-

Upload

shreyagomez -

Category

Documents

-

view

607 -

download

35

description

Ratio Analysis Project file of companies

Transcript of Project Report Of Ratio Analysis

1

1 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

A PROJECT REPORT

ON

WORKING CAPITAL & RATIO ANALYSIS

UNDERTAKEN AT

HINDUSTAN NATIONAL GLASS & INDUSTRIES LTD.

VIRBHADRA, RISHIKESH (UTTARAKHAND)

SUBMITTED BY

RAHUL KUNDLIYA

REG.NO: 11001882

OF

LOVELY PROFESSIONAL UNIVERSITY JALANDHAR

NEW DELHI GT ROAD, PHAGWARA PUNJAB

2

2 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

CONTENTS

CERTIFICATE ………………………………………………………………………….6

DECLARATION………………………………………………………………………..7

ACKNOWLEDGEMENT……………………………………………………………….8

COMPANY PROFILE………………………………………………………………….9

HISTORY OF THE COMPANY………………………………………………………..10

DIVERSIFIED PRODUCTIVE CAPABILITIES……………………………………..10

FUTURE PLANS………………………………………………………………………..10

FUTURE SUCCESS…………………………………………………………………….11

HNGIL GROUP PROFILE……………………………………………………………...11-13

VISION………………………………………………………………………………….14

COMPANY POLICY…………………………………………………………………...17-20

EXPORT & IMPORT

PURCHASE POLICY

SALES PLOICY

WELFARE ACTIVITIES

SAFTEEY MEASURES

SWOT ANALYSIS OF THE COMPANY……………………………………………...21-22

BOARD OF DIRECTORS………………………………………………………………23-24

IMPORTANT DEPARTMENTS & DESIGNATIONS…………………………………25-26

EXECUTIVE SUMMARY………………………………………………………………27

MANUFACTURING PROCESS OF GLASS…………………………………………...27-31

GLASS CONTAINER FACTORIE

BATCH HOUSE

HOT END

FURNACE

FORMING PROCESS

FORMING MACHINES

INTERNAL TREATMENT

3

3 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

ANNEALING

COLD END

INSPECTIO EQUIPMENT

SECONDRY PROCESSING……………………………………………………………31-32

PACAKAGING

COATINGS

ANCILLARY PROCESSES- COMPRESSORS

INTRODUCTION (FINACIAL MANAGEMENT)…………………………………….33-39

PROBLEM STATEMENT……………………………………………………………….40

NEED OF THE STUDY………………………………………………………………….40

OBJECTIVE OF THE STUDY…………………………………………………………..40

RESEARCH DESIGN & DATA COLLECTION……………………………………….41

METHODOLOGY…………………………………………………………………….....42

LITERATURE REVIEW………………………………………………………………..43-44

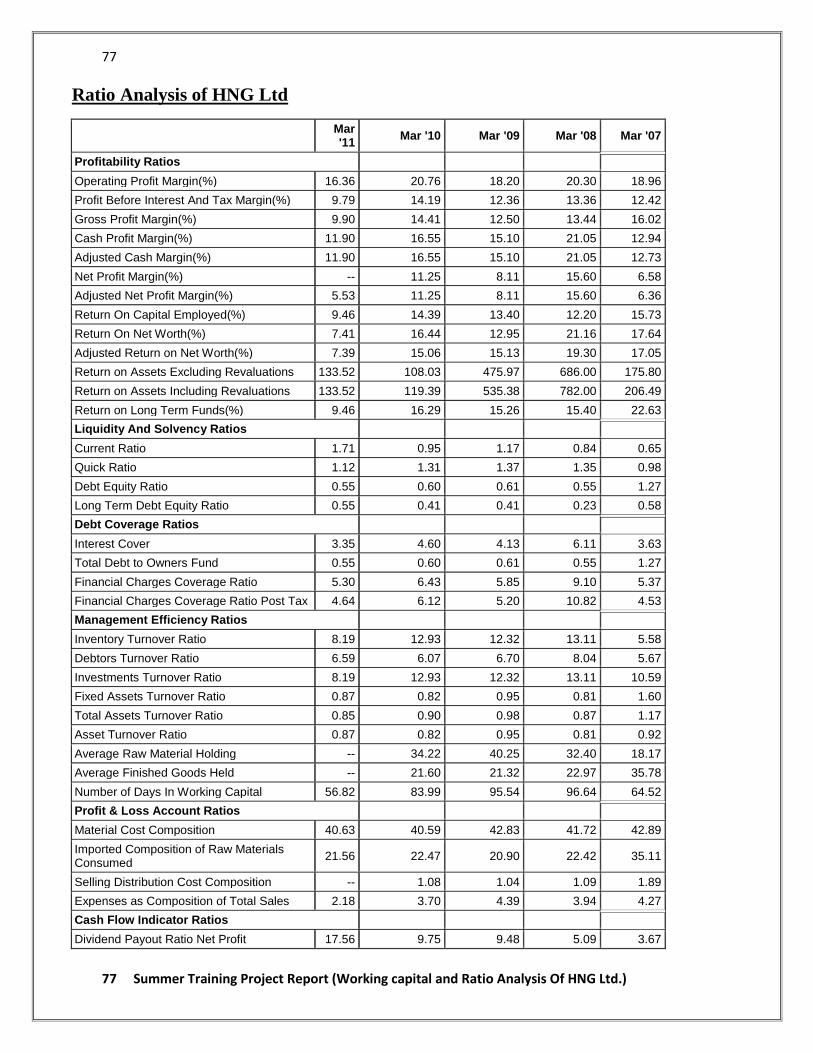

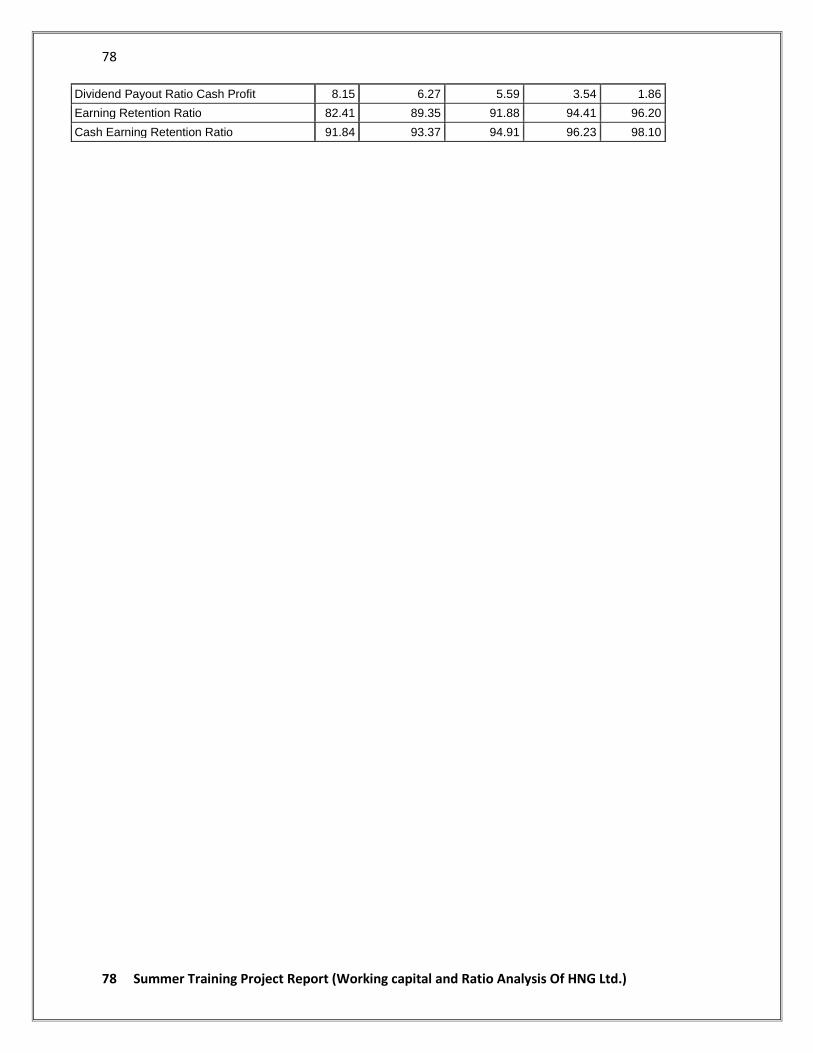

RATIO ANALYSIS……………………………………………………………………..45-59

MEANING

STEPS IN RATIO ANALYSIS

BASIS OR STANDARDS OF COMPARISON

NATURE OF RATIO ANALYSIS

GUIDELINES OR PRECAUTIONS FOR USE OF RATIOS

IMPORTANCE OF RATIO ANALYSIS

LIMITATIONS OF RATIO ANALYSIS

CLASSIFICATIONS OF RATIOS

DATA ANALYSIS AND INTERPRETATION OF RATIOS……………………….....60-66

DATA ANALYSIS OF BALANCE SHEET…………………………………………….67-68

OBSERVATIONS AND FINDINGS……………………………………………………69

LIMITATIONS OF THE STUDY………………………………………………………...70

SUGGESTIONS…………………………………………………………………………...70

4

4 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

CONCLUSION…………………………………………………………………………… 71

REFERENCES…………………………………………………………………………….72

ANNEXTURE……………………………………………………………………………..74-78

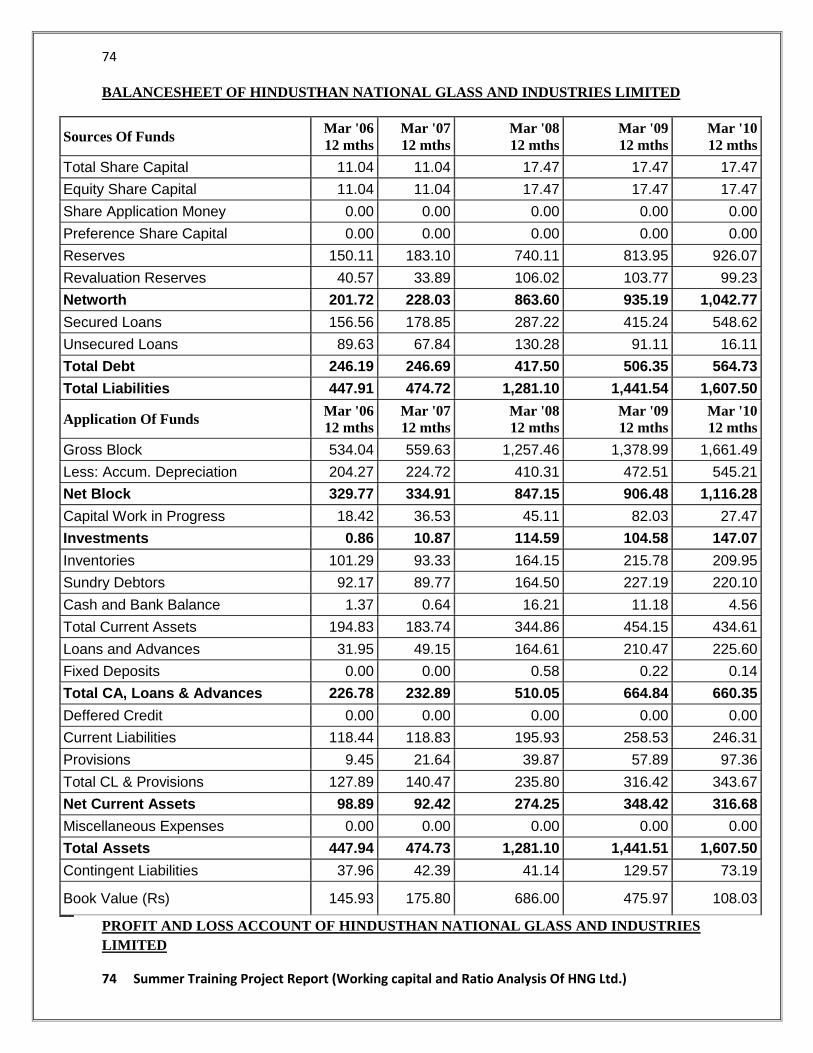

BALANCESHEET OF THE COMPANY

PROFIT AND LOSS A/C

5

5 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

6

6 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

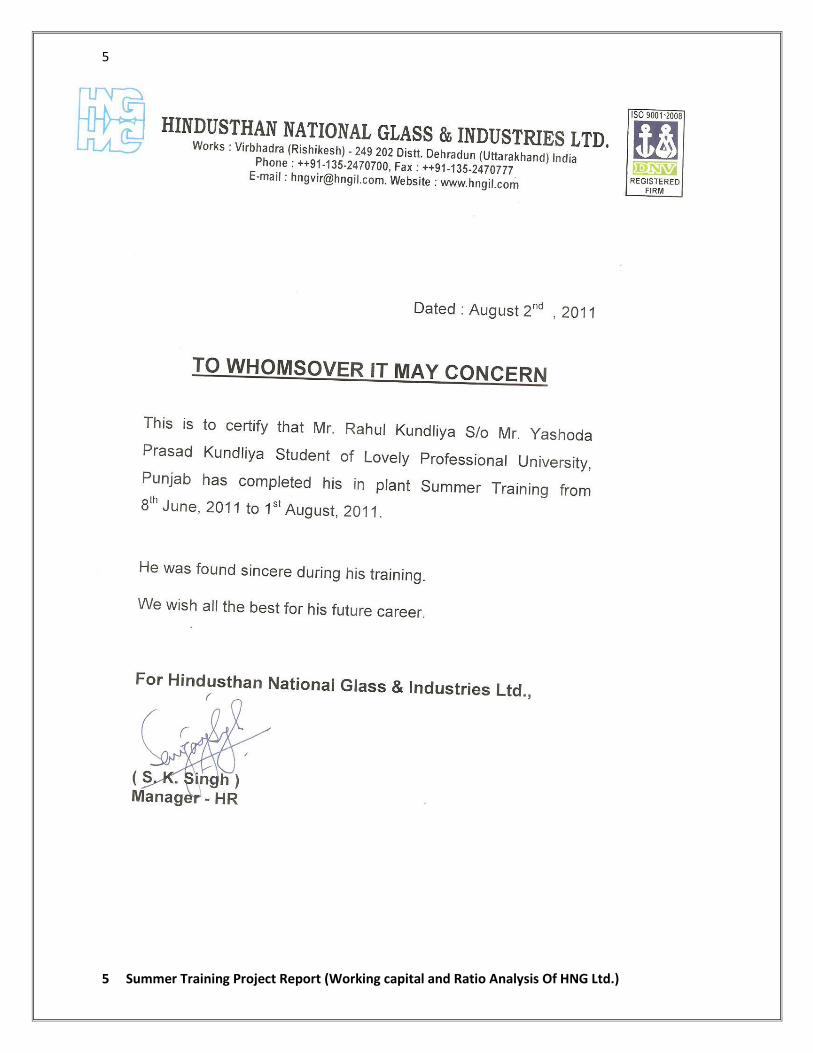

CERTIFICATE

This is to certify that Mr. Rahul Kundliya of Lovely Institute of

Management, Phagwara has successfully completed the project work

titled “WORKING CAPITAL AND RATIO ANALYSIS OF HNG Ltd.” in

partial fulfillment of requirement for the award of POST

GRADUATION DEGREE IN BUSINESS MANAGEMENT prescribed by the Lovely

Professional University. This project is the record of authentic

work carried out during the academic year (2010 – 2012).

7

7 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

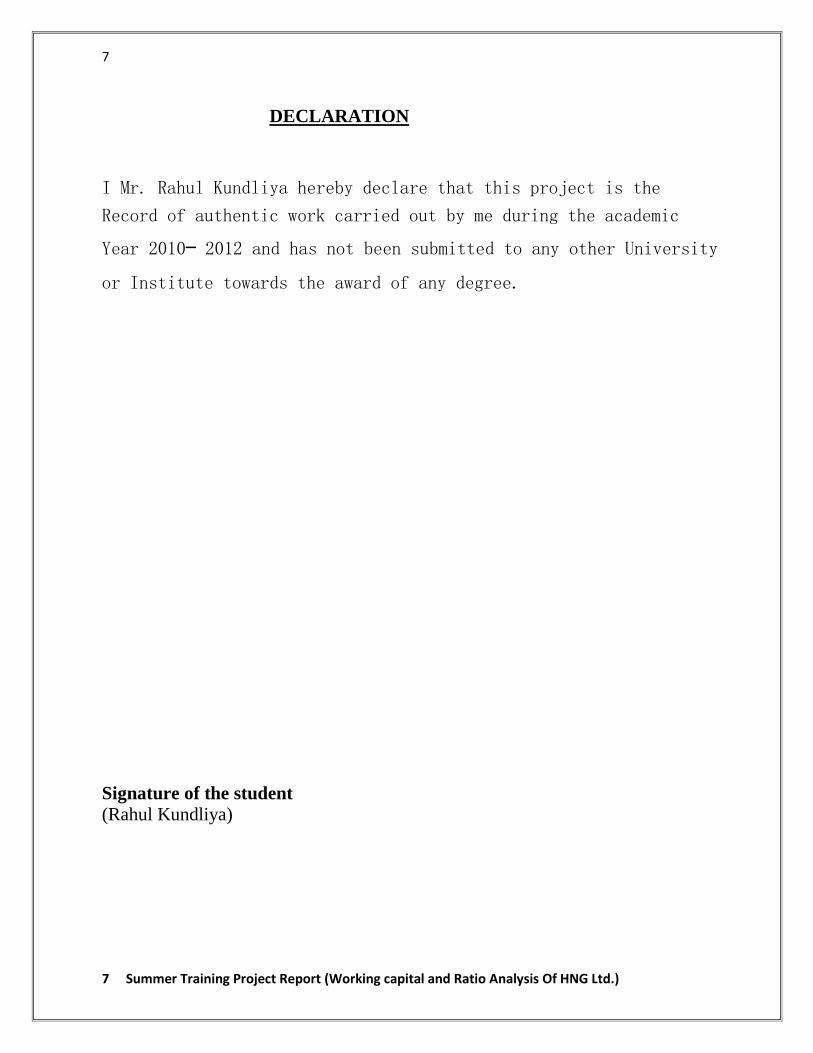

DECLARATION

I Mr. Rahul Kundliya hereby declare that this project is the

Record of authentic work carried out by me during the academic

Year 2010– 2012 and has not been submitted to any other University or Institute towards the award of any degree.

Signature of the student

(Rahul Kundliya)

8

8 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

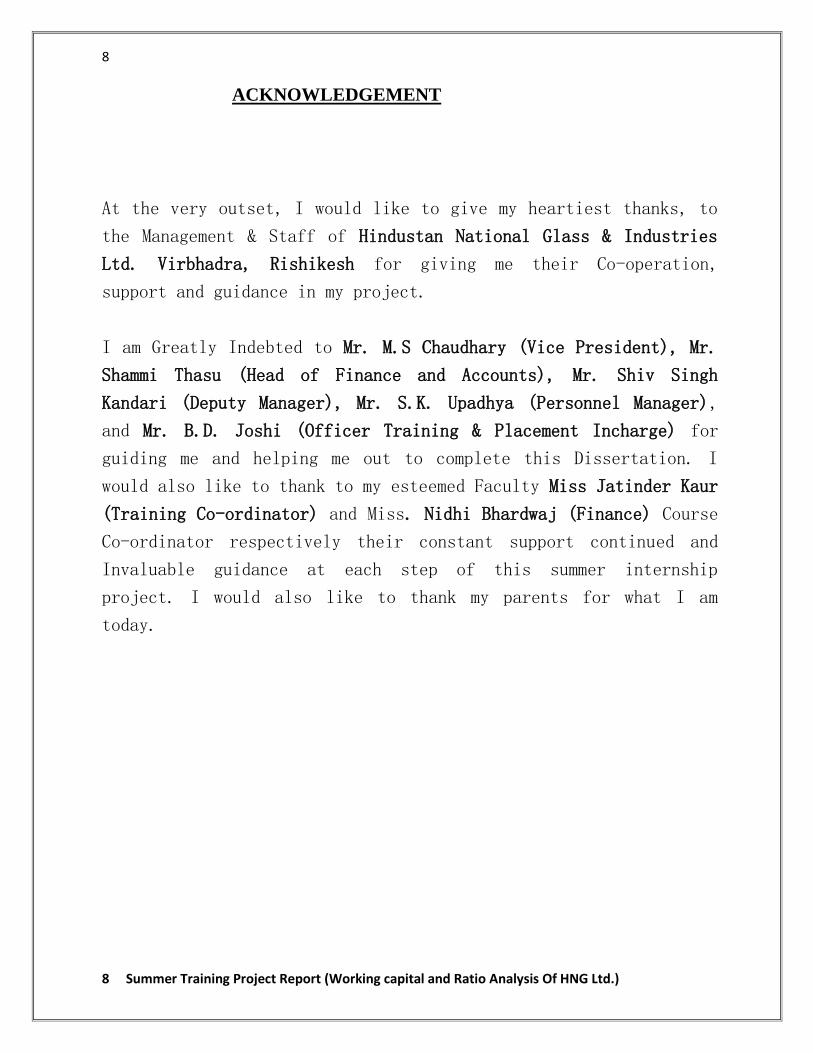

ACKNOWLEDGEMENT

At the very outset, I would like to give my heartiest thanks, to

the Management & Staff of Hindustan National Glass & Industries

Ltd. Virbhadra, Rishikesh for giving me their Co-operation,

support and guidance in my project.

I am Greatly Indebted to Mr. M.S Chaudhary (Vice President), Mr.

Shammi Thasu (Head of Finance and Accounts), Mr. Shiv Singh

Kandari (Deputy Manager), Mr. S.K. Upadhya (Personnel Manager),

and Mr. B.D. Joshi (Officer Training & Placement Incharge) for

guiding me and helping me out to complete this Dissertation. I

would also like to thank to my esteemed Faculty Miss Jatinder Kaur

(Training Co-ordinator) and Miss. Nidhi Bhardwaj (Finance) Course

Co-ordinator respectively their constant support continued and

Invaluable guidance at each step of this summer internship

project. I would also like to thank my parents for what I am

today.

9

9 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

COMPANY PROFILE -

The unit was originally incorporated by the name of M/S J/G glass limited in the

year 1972 with a Furnace capacity of 60 MT a an ancillary to IDPL

VIRBHADRA. Due to technical and other reasons the unit could not perform

well and landed into financial crunch and as such was taken over by the THAPAR

GROUP as subsidiary unit, however in the year 1994 the company was

incorporated as a joint venture with ACI INTERNATIONAL a USA based MNC.

It was named as OWENS BILTLTD. Later on in the year 1998, the share holding

of THAPAR GROUP was taken over by OI INC an AMETICAN MND and it has

OWENS BROCKWAY (I) LTD. on 7th

January 2002, Hindustan national Glass &

Industries along with its associate company Ceramic Decorators LTD. Has taken

over the management and ownership of the company and the name of the

company was changed to ACE GLASS CONTAINERS LIMITED. With the

approval of Humble High Court the unit stands merged with patent company M/S

HINDUSTAN NATIONAL GLASS & INDUSTRIES LIMITED, and is

known accordingly.

HINDUSTAN NATIONAL GLASS & INDUSTRIES LIMITED is a

manufacturer of all varieties of glass bottles/vials. Manufacturing facilities are

strategically located at Rishra near Calcutta since (1952) and Bahadurgarh near

Delhi since (1964), Rishikesh, Pondicherry and Nasik With state - of - art -

induction furnace for manufacturing of castings in its own foundary. HNGIL has

incorporated its technology from the best suppliers in Europe and USA. HNIL

Group operates 10 furnaces and 42 production lines with fully automatic IS

(Individual Section) machines up to 12 Sections operating on Double and Triple

Gob.

All the plants have thorough electronic inspection system right from the batch

mixing till the final packing. Quality control and R&D Sections are well equipped

with sophisticated instruments enabling production of international quality

10

10 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

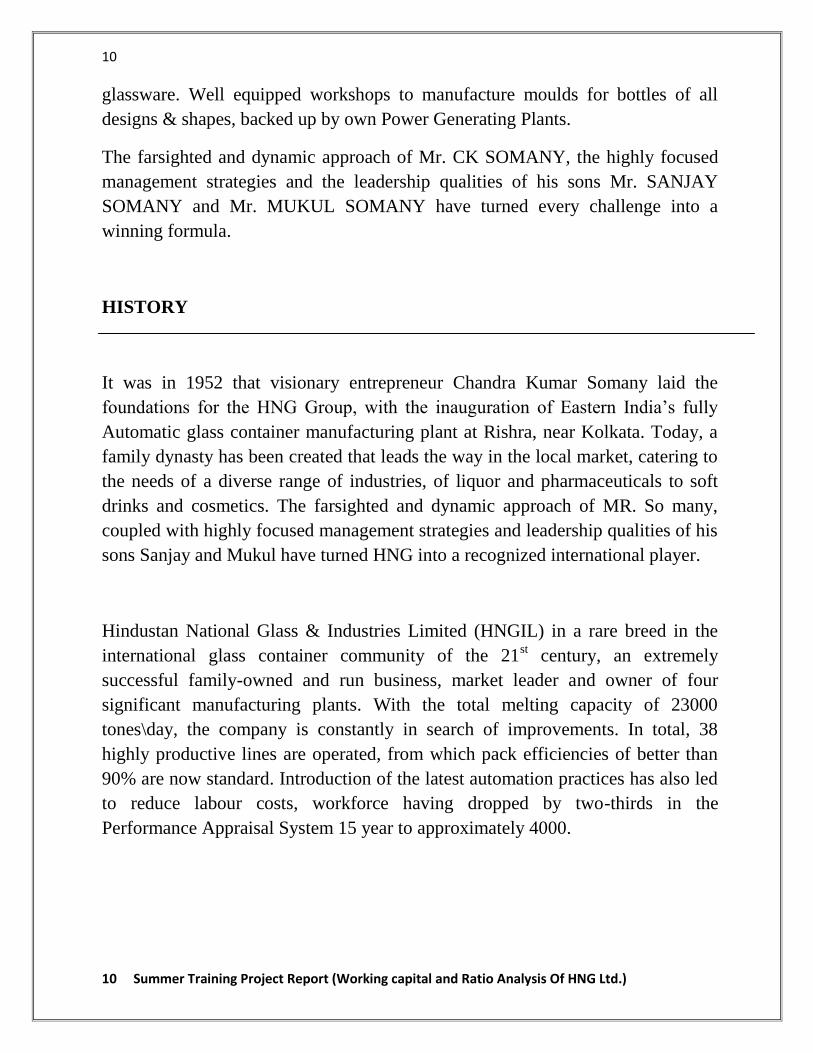

glassware. Well equipped workshops to manufacture moulds for bottles of all

designs & shapes, backed up by own Power Generating Plants.

The farsighted and dynamic approach of Mr. CK SOMANY, the highly focused

management strategies and the leadership qualities of his sons Mr. SANJAY

SOMANY and Mr. MUKUL SOMANY have turned every challenge into a

winning formula.

HISTORY

It was in 1952 that visionary entrepreneur Chandra Kumar Somany laid the

foundations for the HNG Group, with the inauguration of Eastern India’s fully

Automatic glass container manufacturing plant at Rishra, near Kolkata. Today, a

family dynasty has been created that leads the way in the local market, catering to

the needs of a diverse range of industries, of liquor and pharmaceuticals to soft

drinks and cosmetics. The farsighted and dynamic approach of MR. So many,

coupled with highly focused management strategies and leadership qualities of his

sons Sanjay and Mukul have turned HNG into a recognized international player.

Hindustan National Glass & Industries Limited (HNGIL) in a rare breed in the

international glass container community of the 21st century, an extremely

successful family-owned and run business, market leader and owner of four

significant manufacturing plants. With the total melting capacity of 23000

tones\day, the company is constantly in search of improvements. In total, 38

highly productive lines are operated, from which pack efficiencies of better than

90% are now standard. Introduction of the latest automation practices has also led

to reduce labour costs, workforce having dropped by two-thirds in the

Performance Appraisal System 15 year to approximately 4000.

11

11 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Diversified Productive Capabilities

Alongside the original Rishra factory near kolkata since 1964 HNG has operated a

plant at Bahadurgarh, close to New Delhi .Flint, amber and green colors are

produced on 13 lines at Rishra, while the larger Bahadurgarh Facility melts flints

amber and cosmetic-grade compositions, operating a total of 15 lines.

Associate company Ace Glass Containers Ltd has manufacturing capacity at

Rishikesh (flint and green, six lines) and Pondicherry (flint, four lines). Formerly

a 100% subsidiary of USA- based Owens- Illinois Inc; Ace was acquired in 2002,

when 0-1 took the unexpected decision to exit the Indian market. Prior to the

HNG takeover, production at a third factory in Pune had ceased.

With the recent acquisition of the glass container unit of Larsen & turbo, situated

at Nasik in Western India, HNG has now established its presence in all the four

zones of India. The Nasik plant has a melting capacity of 300 tons per day,

operating a total of four lines (flint).

FUTURE PLANS

HNG’s endeavor to cater for the entire Indian market has been successful but the

quest for further expansion has not ended as plans for a new facility between

Mumbai and Baroda are expected to be progressed within the for next two years.

When operational, this plant will be larger than any of HNG’s existing facilities,

although precise details are still under wraps.

The origin of this collaborative approach stem from CK Somany’s plans to

develop the business in the 1950’s, Alongside HNG’s expansion of glass

manufacturing expertise is a commitment to maximize the capabilities and

efficiencies if its support service .Apart from owning and quarries, the company

operates a state –of-the-art induction furnace to make castings in its own foundry

located at Bahadurgarh this operation complements a well - equipped mould

production shop and the latest CAD/CAM facility to design articles in a variety of

shapes .

12

12 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Also situated at Bahadurgarh is subsidiary company glass Equipment (India) led.

GEIL was created in 1974 and specializes in the manufacture of glass forming

equipment. Currently operating at full capacity to keep pace with HNG’s own

requirements as well as satisfying orders from other glassmakers, GEIL produces

complete IS machines as well as conversions, electronic timing systems, feeders;

conveyors ware transfers, stackers, motor- driven presses and spare parts

FUTURE SUCCESS

IN recent years, the HNG group has emerged as India’s leading glass container

manufacturer, expanding and modernizing its production expertise to keep pace

with growth in the local market. Demand is expected to grow by a further 8% in

the next 12 months and while smaller players become increasingly regionalized

and unable to compete on an effective level, there can be little doubt that HNG-led

by Somany family- can look forward to continuing success in the future.

HNGIL GROUP PROFILE

HNGIL, the largest and most prolific producer of glass containers, operating at

present 10 furnaces at giver location (Rishra, Bhahadurgarh, Pondicherry, Nasik,

& Rishikesh) and production lines, In addition HNG has acquired a glass

container manufacturing unit of M/S Haryana sheet Glass Limited at Neemrana,

Rajastan. A fully integrated group having its own foundary for casting, well

equipped workshop for moulds and spare parts captive power plants and quarries

for sand with fleet for finished goods movement has given competitive advantage

to its customers.

A MARKET LEADER

In the 5ml – 3200 ml segment, HNG Group is the undisputed market leader

catering to 70% of the Domestic Market in the pharmaceutical, beverage,

processed food, cosmetic and liquor sectors covering industry majors like coca-

13

13 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

cola Dabur, Glaxo Smith Kline Beecham, Nestle, Pepsi, Reckitt Benckiser (India)

Ltd., Smith Kline Beecham UB Group etc. Exports to south east, Middle East,

Africa and First world countries on Europe & North America

ON SUPER FAST GROWTH TRACK

Its spirit to ascend newer parameters remains as insatiable as ever. The days ahead

are gleaming with promise. With modernizations, up gradation and foresight to

meet the emerging and more distinctive demands of the customers, the group is all

set for unprecedented achievements. With projected planned investment of

Rs 3000 million in the next three years, touching life in more ways than one tune

the harmony of nature

MILESTONES

It order to keep with changing technology and demands, the group has acquired

the glass division of L & T at Nasik in October 2005, having one furnace of 320

TPD melting capacity. HNGIL has also entered into a scheme of amalgamation

with ACE GLASS CONTAINERS (ACE) which scheme has been sanctioned by

the Honorable High Courts of Kolkata and Delhi. Post amalgamation HNGIL’ un-

audited turnover as on 31.03.2008 stands at a figure more than Rs. 1100 crore.

RISHIKESH PLANT

2 furnaces; combined melting capacity of 340 MT per day.

Furnace ii used for manufacturing of green glass.

6 lines of glass making IS machines.

Off – site printing facility with 3 decorating lines

14

14 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

VISION

“To strive to be a major International producer of

quality Containers glass by consistently following

And adopting the most modern Methods and

techniques in an environment Friendly manner

with active involvement of its Employees to meet

the needs of its Customers and stakeholders so

as to achieve Sustainable development and long

term growth.”

15

15 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

RAW MATERIAL USED FOR FORMATION OF GLASS & ITS

SOURCES

Raw Materials required in the organization are ore obtained from various mines

and other places or areas:

Silica sand (mineral) - Former material (main agent) >SiO2 from

Allahabad, Ghaziabad, Faridabad and Jaipur;

Soda ash (chemical) – Flux Material to lower down melting >Al2 O2,

Fe2, O3 from Jaipur and other places also;

Limestone + dolomite (mineral): Both are used as stabilizers (stability)>

CaO + MgO from jaipur & Dehradun;

Feldspar- used for durability>Na, K2O from Jaipur;

Fine chemicals- De Colorizes> Selenium from special markets; and

Broken glass from local market.

16

16 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

MAIN CUSTOMERS OR CLIENTS OF THE COMPANY

The clientele includes leading companies like:

Pepsi Company

Coca-Cola company

Cadbury Company

Nestle India Ltd.

Raun Pollack

Dabur India Ltd.

Lakme Lever

Glaxo Welcome

Pfizer

Reckitt & Coleman

Shaw-Wallace

Mith Kline Beecham

UB Group

Hamdard Wakf Laboratories

Mount Shivalik Ltd.

Albert David Ltd

Mc- Dowell Group

Kedia Group

Bayer Group and

Other leading companies.

17

17 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

EXPORT IMPORT POLICY

HNG Industries Limited exports their glass product to South East, Middle East,

Africa and First World Countries in Europe & North America.

It follows the EXIM Policy which has some Principal objects.

To accelerate the country’s transition to a globally vibrant economy with a

view to derives maximum benefit from expanding global market

opportunities.

To stimulated sustained economic growth by providing access to essential

raw materials, components, consumable and capital goods required for

augmented production.

To enhance the technological strength and efficiency of Indian industry

and services, thereby improving their competitive strength while

generating new employment opportunities and encourage the attainment of

internationally accepted standard of quality.

To provide consumer with good quality product at reasonable price.

18

18 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

PURCHASE POLICY -

The purchase policy of the HNG Industries Limited includes the following:

Company maintains the goodwill of approval vendors.

Purchase preference is given to those who have adopted internationally

known quality management system.

There are continuous checks on inventory levels so as to avoid the situation

of over stocks.

Purchases are done keeping the quality aspect in view.

The company aims at producing the higher quality of glass to satisfy his

customers. This is achieved by:

Adoption and implement of quality utilization of requirement of ISO:

Continuous up gradation of technology for optimum utilization of resources and

manufacturing products in cost effective manner, Imbibing the culture of

continuous quality improvement through motivation and plant training of all

employees.

Specimen of various standardizes forms being used in this company for carrying

out the various functions of purchase department as describe is enclosed at the

end.

19

19 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

SALES POLICY -

The sales policy of HNG Industries Limited includes the following:

Company maintains the goodwill of all the customers.

Sales preference is given to those who have adopted internationally known

quality management system.

There is continuous check on inventory levels so as to avoid the situation

of overstocks.

Sales are done keeping the quality aspects in view.

WELFARE ACTIVITIES

HNG Industries limited provides various welfare facilities for the employees

which are enumerated as follows:

Provide uniform and shoes to the employees according to their department

as per the term of general agreement.

Provide canteen and mess facility.

Provide medical coverage to the employees.

20

20 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Club facility.

Providing ambulance and first aid facility.

Time to time various awards and rewards given to employees.

SAFETY MEASURES

HNG Industries Limited lays utmost care towards health and safety of all

personnel. Central safety committee at the apex level and the department safety

committee at the shop floor are formed to review and monitor the safety activity.

Training on safety, fire fighting is given to all level of employees at the regular

intervals. The company is generally providing Personal Productive Equipments

like helmets, ear plugs, safety shoes, googles etc. to their employees.

21

21 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

SWOT ANALYSIS OF THE COMPANY

Every organization has some strength and weakness, opportunities and threats:

HNG Industries Limited have some strength, weakness, opportunities and threats.

These are as follows:

STRENGTHS –

The company is strong and well established company.

The company is customer oriented company.

It exists from 30 years.

Company produces good quality of glass bottles.

It has dynamic and forward looking management.

Up gradation & modernization of existing machine resulted in higher speed

& efficiencies.

Company has attained ISO- 9001 certificate for quality.

Goodwill in the eyes of the public.

WEAKNESS –

At present the factory business strategies are not driven by Core

competency.

Absence of long term planning.

Absence of raw material near the factory place

Locus of control is absent.

Less space and less number of godowns.

Financial weakness (Lack of working capital).

Overstaffing

Lack of good marketing strategies.

22

22 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

OPPORTUNITIES –

Suitable glass factory norms of government.

Increase in demand in existing line of business.

Only one of its kinds in the new state called Uttaranchal.

THREATS –

Emergence of new competitive pressure example L & T.

Due to the introduction of plastic and disposable cold drinks and beer

bottles, glass product demand somewhat decreases.

Companies based on single product (Bottles) only.

Import of finished product to India due to less government regulations.

23

23 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

BOARD OF DIRECTORS

1. Chairman : Mr. C.K Somany

Mr. C.K Somany is acknowledged expert in a glass technology and is

providing policy guidelines for the Management and administration for the

company. He holds an F.B.I.MC (London) Degree and a degree in glass

Plant Instrumentation from Honeywell brown, Minneapolis, U.S.A.

2. Managing Director: Mr. Sanjay Somany

Mr. Sanjay Somany is a commerce graduate and he has obtained a Diploma

in Diesel Engineering and vast knowledge of the glass manufacturing

Technology. At the Present he is the Managing director of the company.

3. Joint Managing Director : Mr. Mukul Somany

Mr. Mukul Somany is commerce Graduate. He is a noted Industrialist in the

glass manufacturing Industry.

24

24 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

OTHER MEMBERS

Senior President Mr. J.P Kasera

Senior President Mr. R.R Soni

President Mr. R.L Khandelia

President Mr. C.K Jain

Vice President Mr. S. Chaudhary

Vice President (Marketing) Mr. S. Bhende

Vice President (Marketing) Mr. V. Sharan

Vice President (Glass & Ceramics) Mr. A.C Jain

Vice President (Material) Mr. N.K Kabra

Vice President (Exports) Mr. Devdutta Hoare

25

25 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

IMPORTANT DEPARTMENT & DESIGNATIONS

1. Stores :

Commercial Senior Manager Mr. Rajeev Gaur

Executive Stores Mr. Ramesh Sharma

Office Store Mr. Umesh Gupta

2. Production :

DGM Production Mr. D.K Nawani

Managing Production Mr. Ratan Singh

Machine Manager Production Mr. Vikas Jain

Assistant Manager Mr. R.P Dimri

Executive Mr. B.N Purohit

Officer Mr. H.S. Rawat &

Mr. Balswaroop

26

26 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

3. Finance / Accounts :

General Manger Mr. Shammi Thusi

Deputy Manager Mr. Shiv Singh Kandari

Assistant Manger Mr. A.K Saxena

Officers Mr. Rakesh Joshi &

Mr. Alam Singh Negi

Clerical Assistant Mr. Ramesh Bisht

Mr. Vinay Saklani

Mr. Manoj Semwal

Mr. Anil Negi

4. Personal Department :

Personal Manger Mr. S.K Upadhya

Officer (Training & Placement Incharge) Mr. I.S. Bisht

Mr. B.D Joshi

Safety Officer

(Sanitation & Gardening Incharge) Mr. Rajeev Sharma

27

27 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Executive Summary

Cash is the lifeline of a company. Understanding a company’s cash flow health is

essential to making Investment decision. A Good way to judge a company cash

flow prospects is to look at its working capital management. Working capital is

also known as operating capital, it represents the day by day operating liquidity

available to business.

The goal of Working capital management is to ensure that a firm is able to

continue its operations and that it has sufficient ability to satisfy both maturing

short-term debt and upcoming expenses.

Manufacturing Process of glass

Glass is common in everyday life, from glass windows to glass containers. The

Manufacturing of glass for every day process may be complex process. The

process of mass production of glass is given below.

Glass Container Factories

Modern glass container factory are broadly divided into three parts – Batch house,

the hot end and the cold end. The batch houses are concerned with the raw

material. In hot end are the furnaces, machines that produce containers (forming)

and annealing ovens. In cold end there are inspection and packaging equipments.

28

28 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

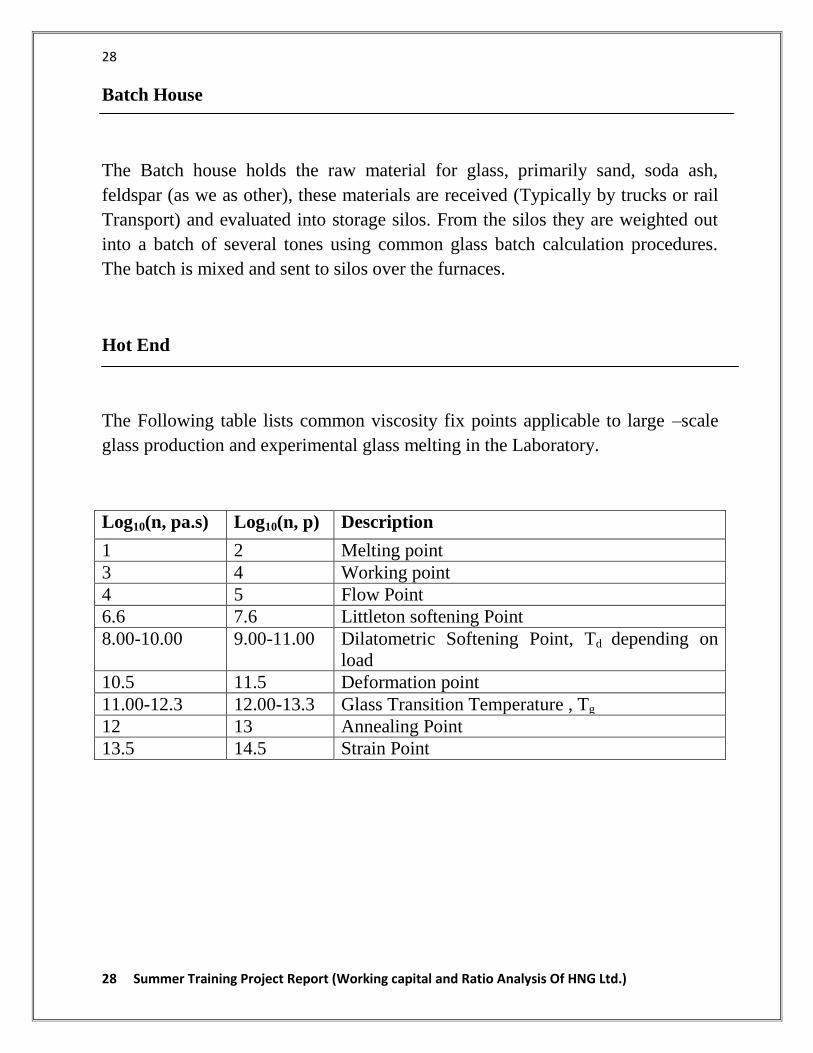

Batch House

The Batch house holds the raw material for glass, primarily sand, soda ash,

feldspar (as we as other), these materials are received (Typically by trucks or rail

Transport) and evaluated into storage silos. From the silos they are weighted out

into a batch of several tones using common glass batch calculation procedures.

The batch is mixed and sent to silos over the furnaces.

Hot End

The Following table lists common viscosity fix points applicable to large –scale

glass production and experimental glass melting in the Laboratory.

Log10(n, pa.s) Log10(n, p) Description

1 2 Melting point

3 4 Working point

4 5 Flow Point

6.6 7.6 Littleton softening Point

8.00-10.00 9.00-11.00 Dilatometric Softening Point, Td depending on

load

10.5 11.5 Deformation point

11.00-12.3 12.00-13.3 Glass Transition Temperature , Tg

12 13 Annealing Point

13.5 14.5 Strain Point

29

29 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Furnace

The hot end of a glassworks is where the molten glass is formed into containers,

begning when the batch is fed at a slow controlled rate into the furnace. The

furnaces are natural gas or fuel oil fired and operates at a temperature up to 1650c.

The temperature is limited by the quality of the furnace superstructure material

and by the glass composition. Glass Furnaces typically operates and energy

recovery scheme known as regeneration. The hot exhaust gas flow back over one

of two piles of loosely packed bricks, called regenerators. These bricks schemes

known as regeneration. These bricks become hot and every 20-30 minutes the

flow of the combustion system is changed over so that the combustion air, which

is mixed with the gas, is drawn through the heated bricks and combustion exhaust

flows through the other pile of bricks.

The batch melts inside the furnace which is maintained as a pool of molten glass,

perhaps 1200mm deep by 50 to 150m2. The molten glass flow from a sub ducted

channel known as the furnace throat into the refiner and fore hearth channels,

these channels cool the glass very precisely so that the glass forming machine is of

a uniform and exact temperature.

Forming Process

There are currently two primary methods of making a glass container the blow

and the blow method and the press and blow method. In all cases a stream of

molten glass at its plastic temperature (10500c-1200

0c) is cut by a shearing blade

to form a cylinder of glass called a gob. Both of the processes start with this job

falling by gravity and guided by through and chute into the bank moulds. In the

blow and blow process, the glass first is bow from blow into the blank moulds to

create a parison and pre container. The parison is the flipped over into a final

mould, where a final blow the glass out into the mould to make the final container

shape. In the case of press and blow, the parison is formed by a metal plunger

which pushes the glass out into the blank mould. The process then continues as

before, with the parison being transferred to the mould and the glass being blow

out into the mould.

30

30 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Forming Machines

The forming machines hold and move the container. Generally powered by

compressed air, the mechanisms are timed to coordinate the movement of all these

parts so that containers are made.

The most widely used forming machines arrangement in the individual section

machines invented in 1903 by Michael J Owens in Illinois. This machine has a

bank of 5-16 identical sections each of which contains one complete set of

Mechanisms to make containers. The sections are in a row and the gobs feed into

each section via a moving chute, called the gob distributor. Section makes either

one, two, three or four containers simultaneously. In the cases of multiple gobs,

the shears cut the gobs simultaneously, and they fall into the blank moulds in

parallel.

Internal Treatment

After the forming process, some containers- Particularly those intended for

alcoholic spirits – undergo a treatment to improve the chemical resistance of the

Inside, called internal treatment or dealkalization. This is usually accomplished

through the injection of suffer or fluorine containing gas mixture into bottles at

high temperatures. The gas is typically delivered to the container either in the air

used in the forming process or through a nozzle directing a stream of the gas into

the mouth of the bottle after forming. The treatment renders the container more

resistant to alkali extraction which can cause increased in product PH and in some

cases container degradation.

31

31 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Annealing

As a glass cools it shrinks and solidified. Uneven cooling causes weak glass due

to stress. Even cooling is achieved by annealing. An annealing oven (Known in

the industry as a Lehr) Heats the container to about 5800C then cools it, depending

on the glass thickness, over a 20-60 minute period.

Cold End

The role of the cold end is to inspect the container for defects, package the

container for shipment and label the containers.

Inspection Equipment

Glass container are 100% inspected, every container is inspected. Automatic

machines inspect for a variety of faults. Typical faults include small cracks in the

glass called checks, foreign inclusions called stones, bubbles in the glass called

blisters and excessively thin walls. In addition to rejecting faulty containers,

inspection equipment gathers statistical information and relays it to the forming

machine operators in the hot end. Computer systems collect faults information to

the mould that produced the container. This is done by reading the mould number

on the container by the mould that made it. Operators carry out a range of checks

manually on samples of containers, usually visuals and dimensional checks.

Secondary Processing

Sometimes containers factories will offer service such as labeling, labeling,

technologies are available. Unique to glass is the Applied Ceramic Labeling

process (ACL). This is screen – Printing of the decoration into the container with

vitreous enamel paint, which is then backed on. Bottles have various added

services such as Etching (Absolute Raspberry/Ruby Red) and applied Ceramic

Labeling (Absolute Blue/Pears/Red/Black).

32

32 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Packaging

Glass containers are packaged in various ways; popular in Europe are bulk pallets

with between 1000 and 4000 containers each. This is out by automatic machines

(palletizes) which arrange and stack containers separated by layer sheets. Others

possibilities include boxes and even hand sewn sacks. Once packed the new

―stock units‖ are labeled and warehoused.

Coatings

Glass containers typically receive two surface coatings, one at the hot end, just

before annealing and at the cold end just after annealing. At the hot end a very

thin layer of tin oxide is applied either using a safe organic compound or inorganic

stannic chloride. Tin based system are not the only once used, although the most

popular. Titanium tetrachloride or organo-titanates can also be used. In all the

cases the coating renders the surface of the glass more adhesive to the cold end

coating. At the cold end the layer of typically, polythene wax is applied via a

water based emulsion. This makes the glass more adhesive to the cold end

coating. This makes the glass slippery, protecting it from scratching and stopping

and stopping containers from sticking together when they are moved on a

conveyor. The resultant invisible combined coatings give a virtually uncatchable

surface to the glass. Due to reduction of in- service surface damage the coating

often is described as strengtheners, however a more correct definition might be

strength retaining coatings.

Ancillary Processes – Compressors

Forming Machines are largely powered by compressed air and typical glass work

will have several large compressors (totaling 30k-60Kcfm) to provide the needed

compressed air. Furnaces, Compressors and forming machines generate quantities

of waste heat which generally is cooled water. Hot glass which is not used in the

forming machine is diverted glass (called cullet) is generally cooled by water,

some time even processed and crushed in a water bath arrangements. Often

cooling requirements are shared.

33

33 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Introduction (Financial Management)

Financial Management is the specific area of finance dealing with the financial

decision corporations make, and the tools and analysis used to make the decisions.

The discipline as a whole may be divided between long-term and short-term

decisions and techniques. Both share the same goal of enhancing firm value by

ensuring that return on capital exceeds cost of capital, without taking excessive

financial risks.

Capital investment decisions comprise the long-term choices about which

projects receive investment, whether to finance that investment with equity or

debt, and when or whether to pay dividends to shareholders.

Short-term corporate finance decisions are called working capital management

and deal with balance of current assets and current liabilities by managing cash,

inventories, and short-term borrowings and lending (e.g., the credit terms

extended to customers). Corporate finance is closely related to managerial finance,

which is slightly broader in scope, describing the financial techniques available to

all forms of business enterprise, corporate or not.

Role of Financial Managers:

The role of a financial manager can be discussed under the following heads:

1. Nature of work

2. Working conditions

3. Employment

4. Training, Other qualifications and Advancement

5. Job outlook

6. Earnings

7. Related occupations

Let us discuss each of these in a detailed manner.

34

34 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

1. Nature of work

Almost every firm, government agency and organization has one or more financial

managers who oversee the preparation of financial reports, direct investment

activities, and implement cash management strategies. As computers are

increasingly used to record and organize data, many financial managers are

spending more time developing strategies and implementing the long-term goals

of their organization.

The duties of financial managers vary with their specific titles, which include

controller, treasurer or finance officer, credit manager, cash manager, and risk and

insurance manager. Controllers direct the preparation of financial reports that

summarize and forecast the organization’s financial position, such as income

statements, balance sheets, and analyses of future earnings or expenses.

Regulatory authorities also in charge of preparing special reports require

controllers. Often, controllers oversee the accounting, audit, and budget

departments. Treasurers and finance officers direct the organization’s financial

goals, objectives, and budgets. They oversee the investment of funds and manage

associated risks, supervise cash management activities, execute capital-raising

strategies to support a firm’s expansion, and deal with mergers and acquisitions.

Credit managers oversee the firm’s issuance of credit. They establish credit-rating

criteria, determine credit ceilings, and monitor the collections of past-due

accounts. Managers specializing in international finance develop financial and

accounting systems for the banking transactions of multinational organizations.

Cash managers monitor and control the flow of cash receipts and disbursements

to meet the business and investment needs of the firm. For example, cash flow

projections are needed to determine whether loans must be obtained to meet cash

requirements or whether surplus cash should be invested in interest-bearing

instruments. Risk and insurance managers oversee programs to minimize risks

and losses that might arise from financial transactions and business operations

undertaken by the institution. They also manage the organization’s insurance

budget. Financial institutions, such as commercial banks, savings and loan

associations, credit unions, and mortgage and finance companies, employ

additional financial managers who oversee various functions, such as lending,

trusts, mortgages, and investments, or programs, including sales, operations, or

electronic financial services. These managers may be required to solicit business,

authorize loans, and direct the investment of funds, always adhering to State laws

and regulations.

35

35 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Branch managers of financial institutions administer and manage all of the

functions of a branch office, which may include hiring personnel, approving loans

and lines of credit, establishing a rapport with the community to attract business,

and assisting customers with account problems. Financial managers who work for

financial institutions must keep abreast of the rapidly growing array of financial

services and products.

In addition to the general duties described above, all financial managers perform

tasks unique to their organization or industry. For example, government financial

managers must be experts on the government appropriations and budgeting

processes, whereas healthcare financial managers must be knowledgeable about

issues surrounding healthcare financing. Moreover, financial managers must be

aware of special tax laws and regulations that affect their industry. Financial

managers play an increasingly important role in mergers and consolidations and in

global expansion and related financing. These areas require extensive, specialized

knowledge on the part of the financial manager to reduce risks and maximize

profit. Financial managers increasingly are hired on a temporary basis to advise

senior managers on these and other matters. In fact, some small firms contract out

all accounting and financial functions to companies that provide these services.

The role of the financial manager, particularly in business, is changing in response

to technological advances that have significantly reduced the amount of time it

takes to produce financial reports. Financial managers now perform more data

analysis and use it to offer senior managers ideas on how to maximize profits.

They often work on teams, acting as business advisors to top management.

Financial managers need to keep abreast of the latest computer technology in

order to increase the efficiency of their firm’s financial operations.

2. Working conditions

Financial managers work in comfortable offices, often close to top managers and

to departments that develop the financial data these managers need. They typically

have direct access to state-of-the-art computer systems and information services.

Financial managers commonly work long hours, often up to 50 or 60 per week.

They generally are required to attend meetings of financial and economic

associations and may travel to visit subsidiary firms or to meet customers.

36

36 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

3. Employment

While the vast majority is employed in private industry, nearly 1 in 10 works for

the different branches of government. In addition, although they can be found in

every industry, approximately 1 out of 4 are employed by insurance and finance

establishments, such as banks, savings institutions, finance companies, credit

unions, and securities dealers.

4. Training, Other qualifications and Advancement

A bachelor’s degree in finance, accounting, economics, or business administration

is the minimum academic preparation for financial managers. However, many

employers now seek graduates with a master’s degree, preferably in business

administration, economics, finance, or risk management. These academic

programs develop analytical skills and provide knowledge of the latest financial

analysis methods and technology.

Experience may be more important than formal education for some financial

manager positions—notably, branch managers in banks. Banks typically fill

branch manager positions by promoting experienced loan officers and other

professionals who excel at their jobs. Other financial managers may enter the

profession through formal management training programs offered by the

company. Continuing education is vital for financial managers, who must cope

with the growing complexity of global trade, changes in State laws and

regulations, and the proliferation of new and complex financial instruments.

Firms often provide opportunities for workers to broaden their knowledge and

skills by encouraging employees to take graduate courses at colleges and

universities or attend conferences related to their specialty. Financial

management, banking, and credit union associations, often in cooperation with

colleges and universities, sponsor numerous national and local training programs.

Persons enrolled prepare extensively at home and then attend sessions on subjects

such as accounting management, budget management, corporate cash

management, financial analysis, international banking, and information systems.

Many firms pay all or part of the costs for employees who successfully complete

courses. Although experience, ability, and leadership are emphasized for

promotion, this type of special study may accelerate advancement.

37

37 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

In some cases, financial managers also may broaden their skills and exhibit their

competency by attaining professional certification. There are many different

associations that offer professional certification programs. For example, the

Association for Investment Management and Research confers the Chartered

Financial Analyst designation on investment professionals who have a bachelor’s

degree, pass three sequential

Examinations, and meet work experience requirements. The Association for

Financial Professionals (AFP) confers the Certified Cash Manager credential to

those who pass a computer-based exam and have a minimum of 2 years of

relevant experience. The Institute of Management Accountants offers a Certified

in Financial Management designation to members with a BA and at least 2 years

of work experience who pass the institute’s four-part examination and fulfill

continuing education requirements. Also, financial managers who specialize in

accounting may earn the Certified Public Accountant (CPA) or Certified

Management Accountant (CMA) designations.

Candidates for financial management positions need a broad range of skills.

Interpersonal skills are important because these jobs involve managing people and

working as part of a team to solve problems. Financial managers must have

excellent communication skills to explain complex financial data. Because

financial managers work extensively with various departments in their firm, a

broad overview of the business is essential.

Financial managers should be creative thinkers and problem solvers, applying

their analytical skills to business. They must be comfortable with the latest

computer technology. As financial operations increasingly are affected by the

global economy, financial managers must have knowledge of international

finance. Proficiency in a foreign language also may be important. Because

financial management is critical for efficient business operations, well-trained,

experienced financial managers who display a strong grasp of the operations of

various departments within their organization are prime candidates for promotion

to top management positions. Some financial managers transfer to closely related

positions in other industries. Those with extensive experience and access to

sufficient capital may start their own consulting firms.

38

38 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

5. Job outlook

Some companies may hire financial managers on a temporary basis, to see the

organization through a short-term crisis or to offer suggestions for boosting

profits. Other companies may contract out all accounting and financial operations.

Even in these cases, however, financial managers may be needed to oversee the

contracts. Computer technology has reduced the time and staff required to produce

financial reports. As a result, forecasting earnings, profits, and costs, and

generating ideas and creative ways to increase profitability will become a major

role of corporate financial managers over the next decade. Financial managers

who are familiar with computer software that can assist them in this role will be

needed.

6. Earnings

The Association for Financial Professionals’ 16th annual compensation survey

showed that financial officers’ average total compensation in 2006, including

bonuses and deferred compensation, was $261,800. Selected financial manager

positions had average total compensation as follows:

Vice president of finance 367,000 US$

Treasurer 301,200

Assistant vice president-finance 282,600

Controller/comptroller 268,600

Director 227,200

Assistant treasurer 223,800

Assistant controller/comptroller 231,000

Manager 167,000

Cash manager 129,400

Large organizations often pay more than small ones, and salary levels also can

depend on the type of industry and location. Many financial managers in both

39

39 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

public and private industry receive additional compensation in the form of

bonuses, which also vary substantially by size of firm. Deferred compensation in

the form of stock options is becoming more common, especially for senior level

executives.

7. Related occupations

Financial managers combine formal education with experience in one or more

areas of finance, such as asset management, lending, credit operations, securities

investment, or insurance risk and loss control. Workers in other occupations

requiring similar training and skills include accountants and auditors; budget

analysts; financial analysts and personal financial advisors; insurance

underwriters; loan counselors and officers; securities, commodities, and financial

services sales agents; and real estate brokers and sales agents.

40

40 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

PROBLEM STATEMENT

How to measure the financial position of the company with the help of ratio analysis?

NEED FOR THE STUDY

1. The study has great significance and provides benefits to various parties whom

directly or indirectly interact with the company.

2. It is beneficial to management of the company by providing crystal clear picture

regarding important aspects like liquidity, leverage, activity and profitability.

3. The study is also beneficial to employees and offers motivation by showing

how actively they are contributing for company’s growth.

4. The investors who are interested in investing in the company’s shares will also

get benefited by going through the study and can easily take a decision whether to

invest or not to invest in the company’s shares.

OBJECTIVES OF STUDY

The major objectives of the resent study are to know about financial strengths and

weakness of HNG Ltd through FINANCIAL RATIO ANALYSIS.

The main objectives of resent study aimed as:

1. To study the present financial system at HNG Ltd

2. To know the financial condition of the company.

3. Interpret the financial statement so that the strength and weakness of a firm

Historical performance and current financial condition can be determined.

4. To analyze the liquidity position of the company.

41

41 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

5. Throw light on a long term solvency of a firm.

6. To offer appropriate suggestions for the better performance of the

organization

RESEARCH DESIGN

A research design is the specification of method and procedure for accruing the

information needed. It is overall operational pattern of frame work of project that

stipulates what information is to be collected for source by that procedures

Descriptive Research design is appropriate for this study.

Descriptive study is used to study the situation. This study helps to describe the

situation. A detail descriptive about present and past situation can be found out by

the descriptive study. In this involves the analysis of the situation using the

secondary data.

DATA COLLECTION

This research study is based on secondary data, means data that are already

available i.e. the data which have been already collected and analyzed by someone

else.

Secondary data are used for the study of Ratio analysis of this company. To

collect the data I have refer – Company annual report, annual magazine, last 5

year balance sheet, and cash flow statements.

42

42 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

METHODOLOGY

The information is collected through secondary sources during the project. That

information was utilized for calculating performance evaluation and based on that,

interpretations were made.

Sources of secondary data:

1. Most of the calculations are made on the financial statements of the company

provided statements.

2. Referring standard texts and referred books collected some of the information

regarding theoretical aspects.

3. Method- to assess the performance of the company method of observation of

the work in finance department in followed.

FINANCIAL ANALYSIS

Financial analysis is the process of identifying the financial strengths and

weaknesses of the firm and establishing relationship between the items of the

balance sheet and profit & loss account. Financial ratio analysis is the calculation

and comparison of ratios, which are derived from the information in a company’s

financial statements. The level and historical trends of these ratios can be used to

make inferences about a company’s financial condition, its operations and

attractiveness as an investment. The information in the statements is used by

Trade creditors, to identify the firm’s ability to meet their claims i.e.

liquidity position of the company.

Investors, to know about the present and future profitability of the company

and its financial structure.

Management, in every aspect of the financial analysis. It is the

responsibility of the management to maintain sound financial condition in

the company.

43

43 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

LITERATURE REVIEW -

Many researchers have studied financial ratios as a part of working capital

Management; however, very few of them have discussed the working capital

Policies in specific. Some earlier work by Gupta and Heffner (1972) examined

the differences in financial ratio averages between industries. The Conclusion of

both the studies was that differences do exist in mean profitability, Activity,

leverage and liquidity ratios amongst industry groups. Pinches et al. (1973) used

factor analysis to develop seven classifications of ratios, and found that the

classifications were stable over the 1951-1969 time periods. In a regional study,

Pandey and Parera (1997) provided an empirical evidence of working capital

management policies and practices of the private sector manufacturing companies

in Sri Lanka. The information and data for the study were gathered through

questionnaires and interviews with chief financial officers of a sample of

manufacturing companies listed on the Colombo Stock Exchange. They found that

most companies in Sri Lanka have informal working capital policy and company

size has an influence on the overall working capital policy (formal or informal)

and approach (conservative, moderate or aggressive). Moreover, company

profitability has an influence on the methods of working capital planning and

control.

Chu et al. (1991) analyzed the hospital sectors to observe the differences of

financial ratios groups between hospital sectors and industrial firms sectors. Their

study concluded that financial ratios groups were significantly different from

those of industrial firms’ ratios as well these ratios were relatively stable over the

five years period. A significance relationship for about half of industries studied

indicated that results might vary from industry to industry. Another aspect of

working capital management has been analyzed by Lamberson (1995) who

studied how small firms respond to changes in economic activities by changing

their working capital positions and level of current assets and liabilities. Current

ratio, current assets to total assets ratio and inventory to total assets ratio were

used as measure of working capital while index of annual average coincident

economic indicator was used as a measure of economic activity. Contrary to the

expectations, the study found that there is very small relationship between charges

44

44 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

in economic conditions and changes in working capital. However, Weinraub and

Visscher (1998) have discussed the issue of aggressive and conservative working

capital management policies by using quarterly data for a period of 1984 to 1993

of US firms. Their study looked at ten diverse industry groups to examine the

relative relationship between their aggressive/conservative working capital

policies. The authors have concluded that the industries had distinctive and

significantly different working capital management policies. Moreover, the

relative nature of the working capital management policies exhibited remarkable

stability over the ten-year study period. The study also showed a high and

significant negative correlation between industry asset and liability policies and

found that when relatively aggressive working capital asset policies are followed

they are balanced by relatively conservative working capital financial policies.

Sathyamoorthi (2002) focused on good corporate governance and in turn effective

management of business assets. He observed that more emphasis is given to

investment in fixed assets both in management area and research. However,

effective management working capital has been receiving little attention and

yielding more significant results. He analyzed selected Co-operatives in Botswana

for a period of 1993-1997 and concluded that an aggressive approach has been

followed by these firms during all the four years of study. Filbeck and Krueger

(2005) highlighted the importance of efficient working capital management by

analyzing the working capital management policies of 32 non-financial industries

in USA. According to their findings significant differences exist between

industries in working capital practices over time.

45

45 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

RATIO ANALYSIS -

The term ―Ratio‖ refers to the numerical and quantitative relationship between

two items or variables. This relationship can be exposed as

Percentages

Fractions

Proportion of numbers

Ratio analysis is defined as the systematic use of the ratio to interpret the financial

statements. So that the strengths and weaknesses of a firm, as well as its historical

performance and current financial condition can be determined Ratio reflects a

quantitative relationship helps to form a quantitative judgment.

STEPS IN RATIO ANALYSIS

The first task of the financial analysis is to select the information relevant to

the decision under consideration from the statements and calculates

appropriate ratios.

To compare the calculated ratios with the ratios of the same firm relating to

the past or with the industry ratios. It facilitates in assessing success or

failure of the firm.

Third step is to interpretation, drawing of inferences and report writing

conclusions are drawn after comparison in the shape of report or

recommended courses of action.

BASIS OR STANDARDS OF COMPARISON

Ratios are relative figures reflecting the relation between variables. They enable

analyst to draw conclusions regarding financial operations. They use of ratios as a

tool of financial analysis involves the comparison with related facts. This is the

basis of ratio analysis. The basis of ratio analysis is of four types.

Past ratios, calculated from past financial statements of the firm.

Competitor’s ratio, of the sum most progressive and successful competitor

firm at the same point of time.

46

46 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Industry ratio, the industry ratios to which the firm belongs to Projected

ratios, ratios of the future developed from the projected or pro forma

financial statements

NATURE OF RATIO ANALYSIS

Ratio analysis is a technique of analysis and interpretation of financial statements.

It is the process of establishing and interpreting various ratios for helping in

making certain decisions. It is only a means of understanding of financial

strengths and weaknesses of a firm. There are a number of ratios which can be

calculated from the information given in the financial statements, but the analyst

has to select the appropriate data and calculate only a few appropriate ratios. The

following are the four steps involved in the ratio analysis.

Selection of relevant data from the financial statements depending upon the

objective of the analysis.

Calculation of appropriate ratios from the above data.

Comparison of the calculated ratios with the ratios of the same firm in the

past, or the ratios developed from projected financial statements or the

ratios of some other firms or the comparison with ratios of the industry to

which the firm belongs.

INTERPRETATION OF THE RATIOS

The interpretation of ratios is an important factor. The inherent limitations of ratio

analysis should be kept in mind while interpreting them. The impact of factors

such as price level changes, change in accounting policies, window dressing etc.,

should also be kept in mind when attempting to interpret ratios. The interpretation

of ratios can be made in the following ways.

Single absolute ratio

Group of ratios

Historical comparison

Projected ratios

Inter-firm comparison

47

47 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

GUIDELINES OR PRECAUTIONS FOR USE OF RATIOS

The calculation of ratios may not be a difficult task but their use is not easy.

Following guidelines or factors may be kept in mind while interpreting various

ratios is

Accuracy of financial statements

Objective or purpose of analysis

Selection of ratios

Use of standards

Caliber of the analysis

IMPORTANCE OF RATIO ANALYSIS

Aid to measure general efficiency

Aid to measure financial solvency

Aid in forecasting and planning

Facilitate decision making

Aid in corrective action

Aid in intra-firm comparison

Act as a good communication

Evaluation of efficiency

Effective tool

LIMITATIONS OF RATIO ANALYSIS

Differences in definitions

Limitations of accounting records

Lack of proper standards

No allowances for price level changes

Changes in accounting procedures

Quantitative factors are ignored

Limited use of single ratio

Background is over looked

Limited use

Personal bias

48

48 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

CLASSIFICATIONS OF RATIOS

The use of ratio analysis is not confined to financial manager only. There are

different parties interested in the ratio analysis for knowing the financial position

of a firm for different purposes. Various accounting ratios can be classified as

follows:

1. Traditional Classification

2. Functional Classification

3. Significance ratios

1. Traditional Classification

It includes the following.

Balance sheet (or) position statement ratio: They deal with the

relationship between two balance sheet items, e.g. the ratio of current assets

to current liabilities etc., both the items must, however, pertain to the same

balance sheet.

Profit & loss account (or) revenue statement ratios: These ratios deal

with the relationship between two profit & loss account items, e.g. the ratio

of gross profit to sales etc.,

Composite (or) inter statement ratios: These ratios exhibit the relation

between a profit & loss account or income statement item and a balance

sheet items, e.g. stock turnover ratio, or the ratio of total assets to sales.

2. Functional Classification

These include liquidity ratios, long term solvency and leverage ratios, activity

ratios and profitability ratios.

3. Significance ratios

Some ratios are important than others and the firm may classify them as primary

and secondary ratios. The primary ratio is one, which is of the prime importance

to a concern. The other ratios that support the primary ratio are called secondary

ratios.

49

49 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

IN THE VIEW OF FUNCTIONAL CLASSIFICATION THE RATIOS

ANALYSES ARE:

Liquidity ratio

Leverage ratio

Activity ratio

Profitability ratio

1. LIQUIDITY RATIOS

Liquidity refers to the ability of a concern to meet its current obligations as &

when there becomes due. The short term obligations of a firm can be met only

when there are sufficient liquid assets. The short term obligations are met by

realizing amounts from current, floating (or) circulating assets The current assets

should either be calculated liquid (or) near liquidity. They should be convertible

into cash for paying obligations of short term nature. The sufficiency (or)

insufficiency of current assets should be assessed by comparing them with short-

term current liabilities. If current assets can pay off current liabilities, then

liquidity position will be satisfactory.

To measure the liquidity of a firm the following ratios can be calculated

Current ratio

Quick (or) Acid-test (or) Liquid ratio

Absolute liquid ratio (or) Cash position ratio

(a) CURRENT RATIO:

Current ratio may be defined as the relationship between current assets and current

liabilities. This ratio also known as Working capital ratio is a measure of general

liquidity and is most widely used to make the analysis of a short-term financial

position (or) liquidity of a firm.

Current Ratio =

Current Assets

Current Liabilities

50

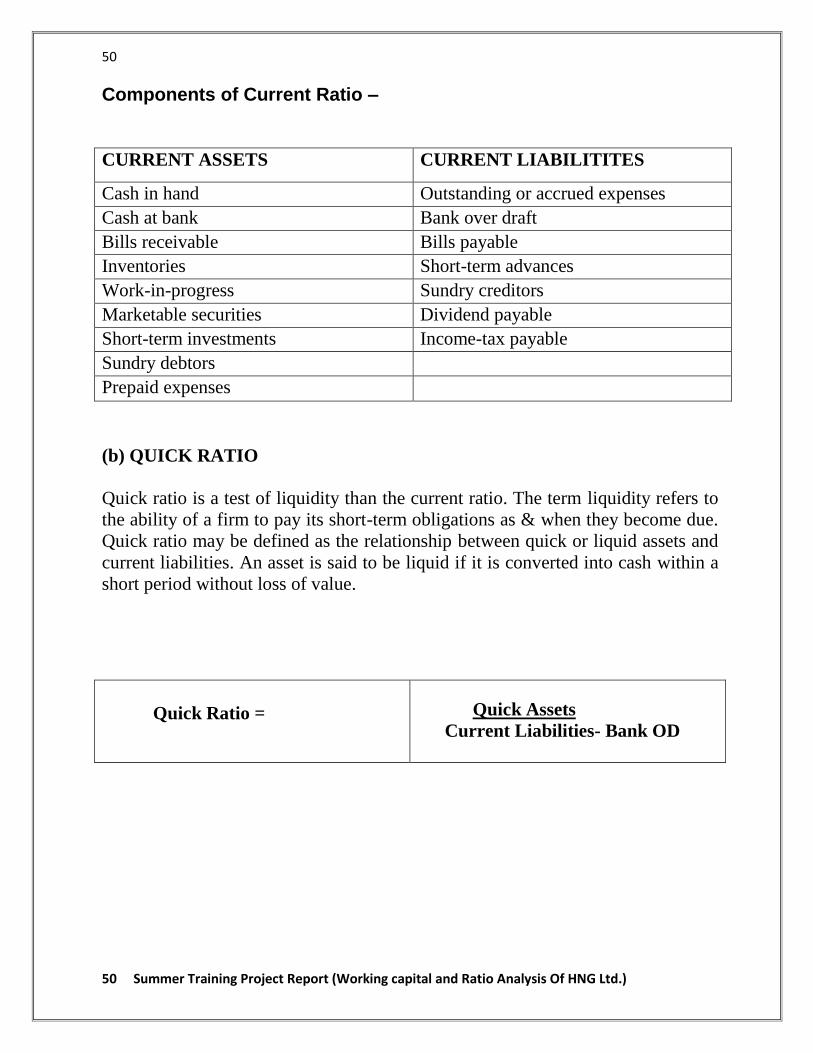

50 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Components of Current Ratio –

CURRENT ASSETS CURRENT LIABILITITES

Cash in hand Outstanding or accrued expenses

Cash at bank Bank over draft

Bills receivable Bills payable

Inventories Short-term advances

Work-in-progress Sundry creditors

Marketable securities Dividend payable

Short-term investments Income-tax payable

Sundry debtors

Prepaid expenses

(b) QUICK RATIO

Quick ratio is a test of liquidity than the current ratio. The term liquidity refers to

the ability of a firm to pay its short-term obligations as & when they become due.

Quick ratio may be defined as the relationship between quick or liquid assets and

current liabilities. An asset is said to be liquid if it is converted into cash within a

short period without loss of value.

Quick Ratio =

Quick Assets

Current Liabilities- Bank OD

51

51 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

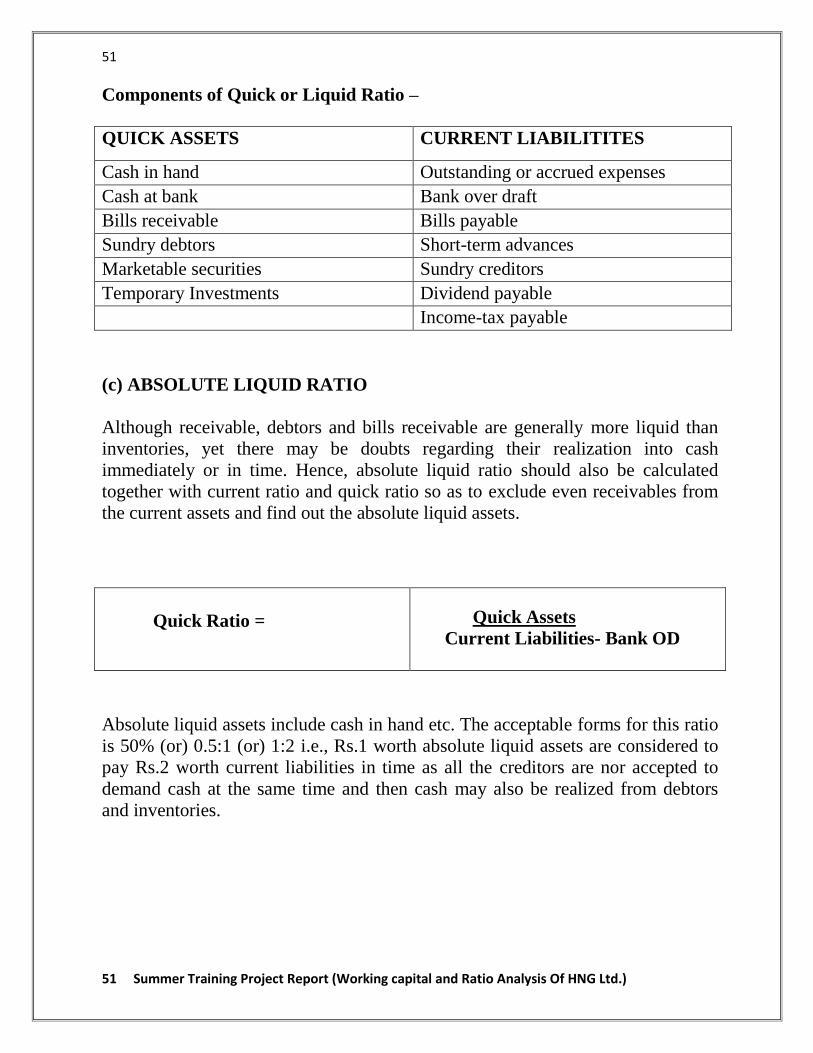

Components of Quick or Liquid Ratio –

QUICK ASSETS CURRENT LIABILITITES

Cash in hand Outstanding or accrued expenses

Cash at bank Bank over draft

Bills receivable Bills payable

Sundry debtors Short-term advances

Marketable securities Sundry creditors

Temporary Investments Dividend payable

Income-tax payable

(c) ABSOLUTE LIQUID RATIO

Although receivable, debtors and bills receivable are generally more liquid than

inventories, yet there may be doubts regarding their realization into cash

immediately or in time. Hence, absolute liquid ratio should also be calculated

together with current ratio and quick ratio so as to exclude even receivables from

the current assets and find out the absolute liquid assets.

Quick Ratio =

Quick Assets

Current Liabilities- Bank OD

Absolute liquid assets include cash in hand etc. The acceptable forms for this ratio

is 50% (or) 0.5:1 (or) 1:2 i.e., Rs.1 worth absolute liquid assets are considered to

pay Rs.2 worth current liabilities in time as all the creditors are nor accepted to

demand cash at the same time and then cash may also be realized from debtors

and inventories.

52

52 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Components of Absolute Liquid Ratio –

ABSOLUTE LIQUID ASSETS CURRENT LIABILITITES

Cash in hand Outstanding or accrued expenses

Cash at bank Bank over draft

Interest on Fixed Deposit Bills payable

Short-term advances

Sundry creditors

Dividend payable

Income-tax payable

2. LEVERAGE RATIOS

The leverage or solvency ratio refers to the ability of a concern to meet its long

term obligations. Accordingly, long term solvency ratios indicate firm’s ability to

meet the fixed interest and costs and repayment schedules associated with its long

term borrowings.

The following ratio serves the purpose of determining the solvency of the concern.

(a) PROPRIETORY RATIO

A variant to the debt-equity ratio is the proprietary ratio which is also known as

equity ratio. This ratio establishes relationship between share holder’s funds to

total assets of the firm.

Proprietory ratio=

Shareholders fund

Total Assets

53

53 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

Components of Proprietory Ratio –

SHARE HOLDERS FUND TOTAL ASSETS

Share Capital Fixed Assets

Reserves & Surplus Current Assets - Cash in hand & at bank

Bills receivable

Inventories

Marketable securities

Short-term investments

Sundry debtors

Prepaid Expenses

3. ACTIVITY RATIOS

Funds are invested in various assets in business to make sales and earn profits.

The efficiency with which assets are managed directly affect the volume of sales.

Activity ratios measure the efficiency (or) effectiveness with which a firm

manages its resources (or) assets. These ratios are also called ―Turn over ratios‖

because they indicate the speed with which assets are converted or turned over

into sales.

Working capital turnover ratio

Fixed assets turnover ratio

Capital turnover ratio

Current assets to fixed assets ratio

(a) WORKING CAPITAL TURNOVER RATIO

Working capital of a concern is directly related to sales.

Working capital = Current assets - Current liabilities

54

54 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

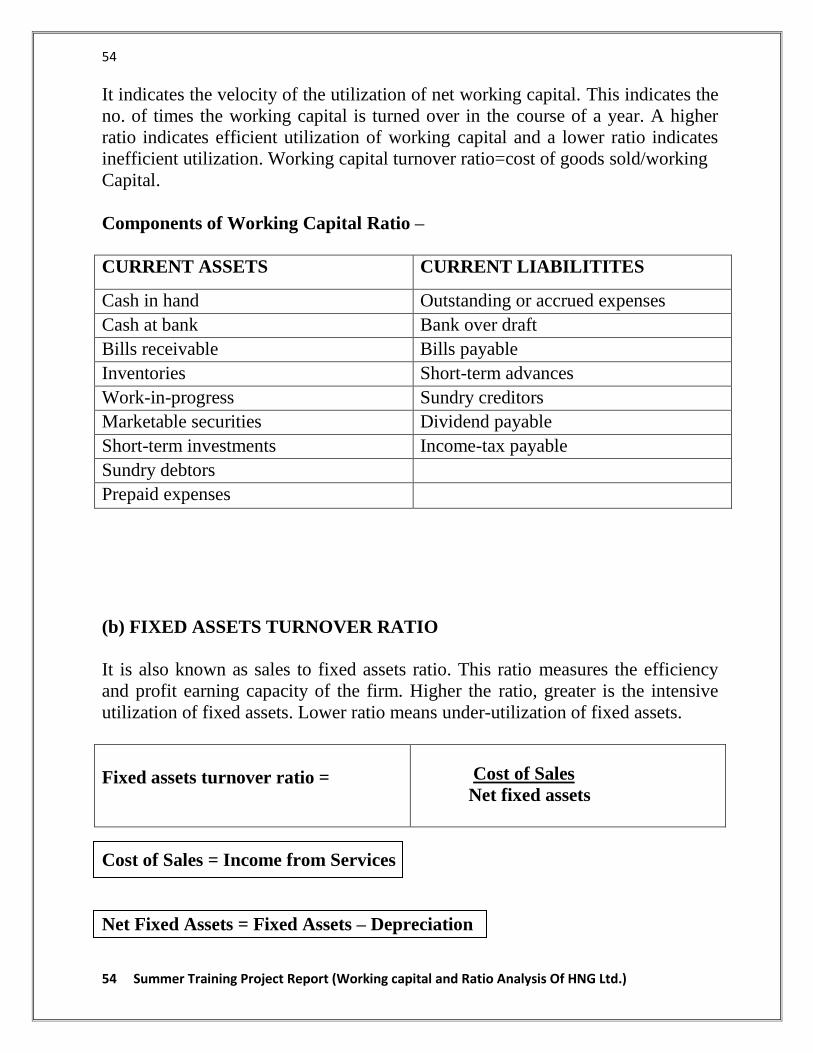

It indicates the velocity of the utilization of net working capital. This indicates the

no. of times the working capital is turned over in the course of a year. A higher

ratio indicates efficient utilization of working capital and a lower ratio indicates

inefficient utilization. Working capital turnover ratio=cost of goods sold/working

Capital.

Components of Working Capital Ratio –

CURRENT ASSETS CURRENT LIABILITITES

Cash in hand Outstanding or accrued expenses

Cash at bank Bank over draft

Bills receivable Bills payable

Inventories Short-term advances

Work-in-progress Sundry creditors

Marketable securities Dividend payable

Short-term investments Income-tax payable

Sundry debtors

Prepaid expenses

(b) FIXED ASSETS TURNOVER RATIO

It is also known as sales to fixed assets ratio. This ratio measures the efficiency

and profit earning capacity of the firm. Higher the ratio, greater is the intensive

utilization of fixed assets. Lower ratio means under-utilization of fixed assets.

Fixed assets turnover ratio =

Cost of Sales

Net fixed assets

Cost of Sales = Income from Services

Net Fixed Assets = Fixed Assets – Depreciation

55

55 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

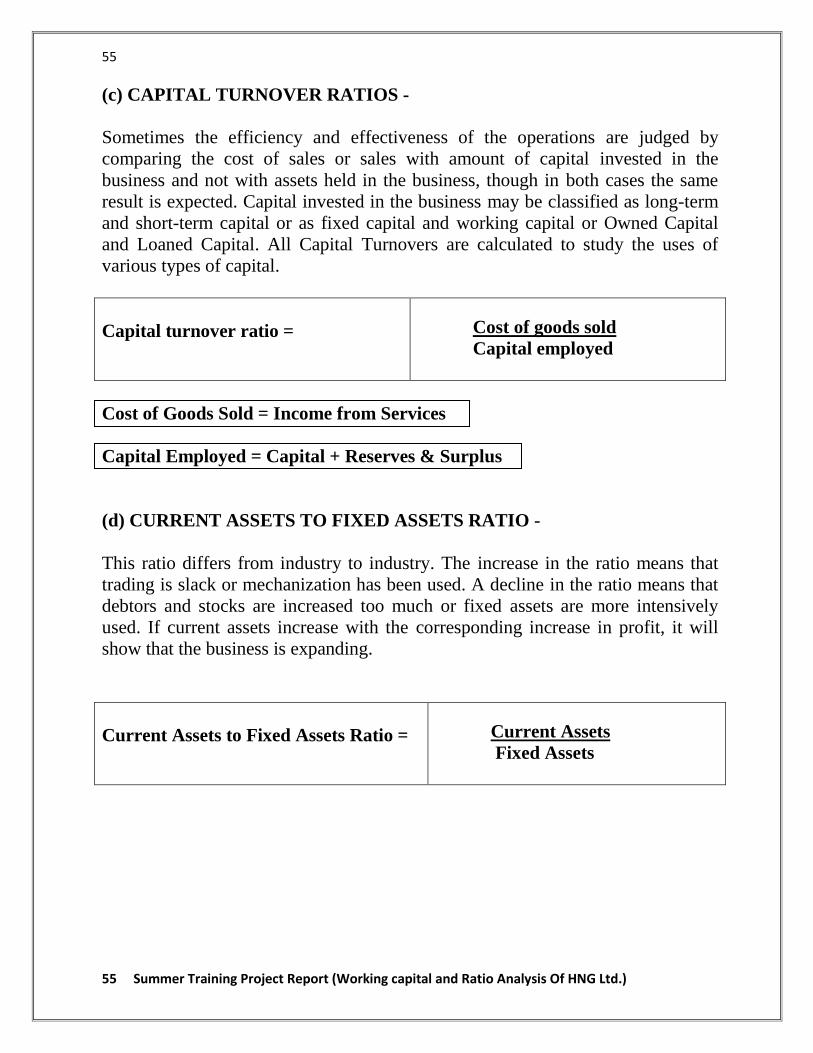

(c) CAPITAL TURNOVER RATIOS -

Sometimes the efficiency and effectiveness of the operations are judged by

comparing the cost of sales or sales with amount of capital invested in the

business and not with assets held in the business, though in both cases the same

result is expected. Capital invested in the business may be classified as long-term

and short-term capital or as fixed capital and working capital or Owned Capital

and Loaned Capital. All Capital Turnovers are calculated to study the uses of

various types of capital.

Capital turnover ratio =

Cost of goods sold

Capital employed

Cost of Goods Sold = Income from Services

Capital Employed = Capital + Reserves & Surplus

(d) CURRENT ASSETS TO FIXED ASSETS RATIO -

This ratio differs from industry to industry. The increase in the ratio means that

trading is slack or mechanization has been used. A decline in the ratio means that

debtors and stocks are increased too much or fixed assets are more intensively

used. If current assets increase with the corresponding increase in profit, it will

show that the business is expanding.

Current Assets to Fixed Assets Ratio =

Current Assets

Fixed Assets

56

56 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

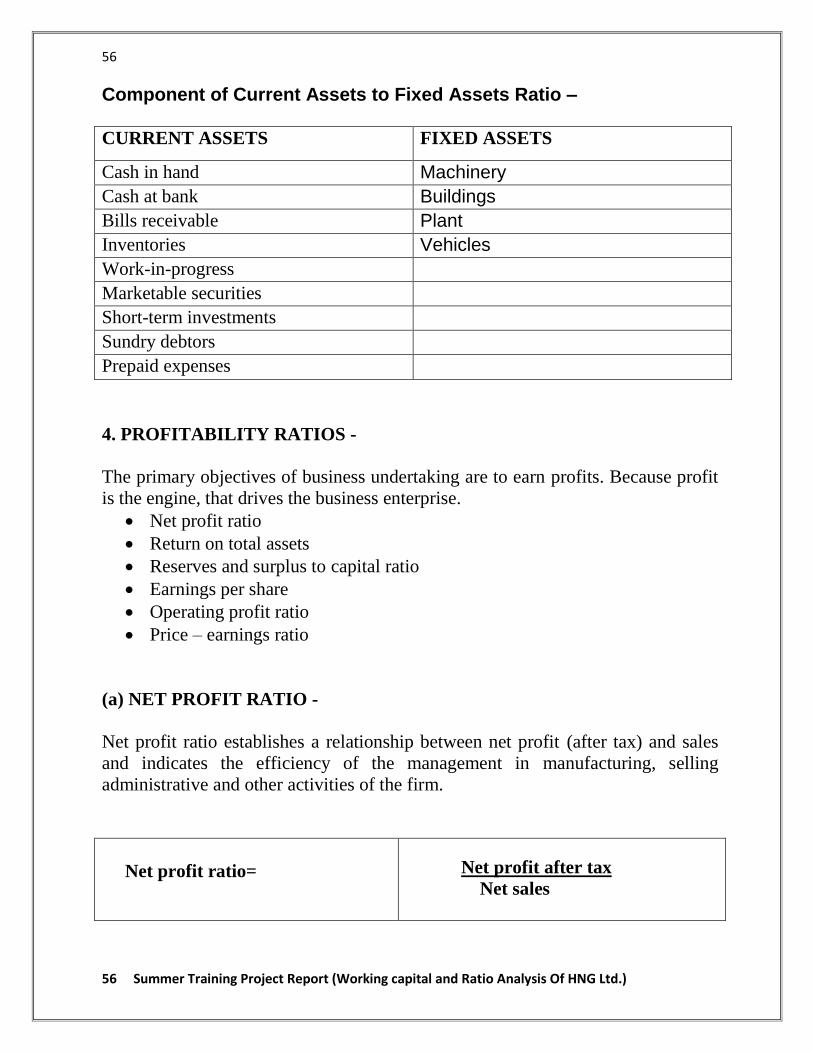

Component of Current Assets to Fixed Assets Ratio –

CURRENT ASSETS FIXED ASSETS

Cash in hand Machinery

Cash at bank Buildings

Bills receivable Plant

Inventories Vehicles

Work-in-progress

Marketable securities

Short-term investments

Sundry debtors

Prepaid expenses

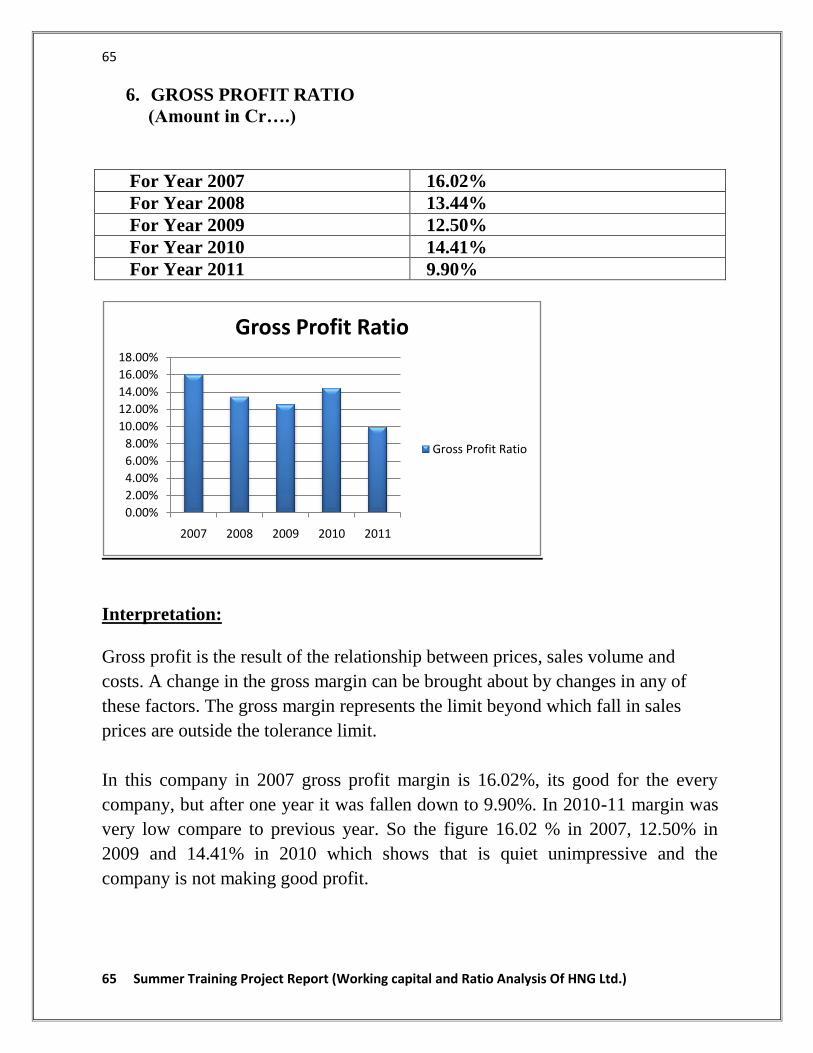

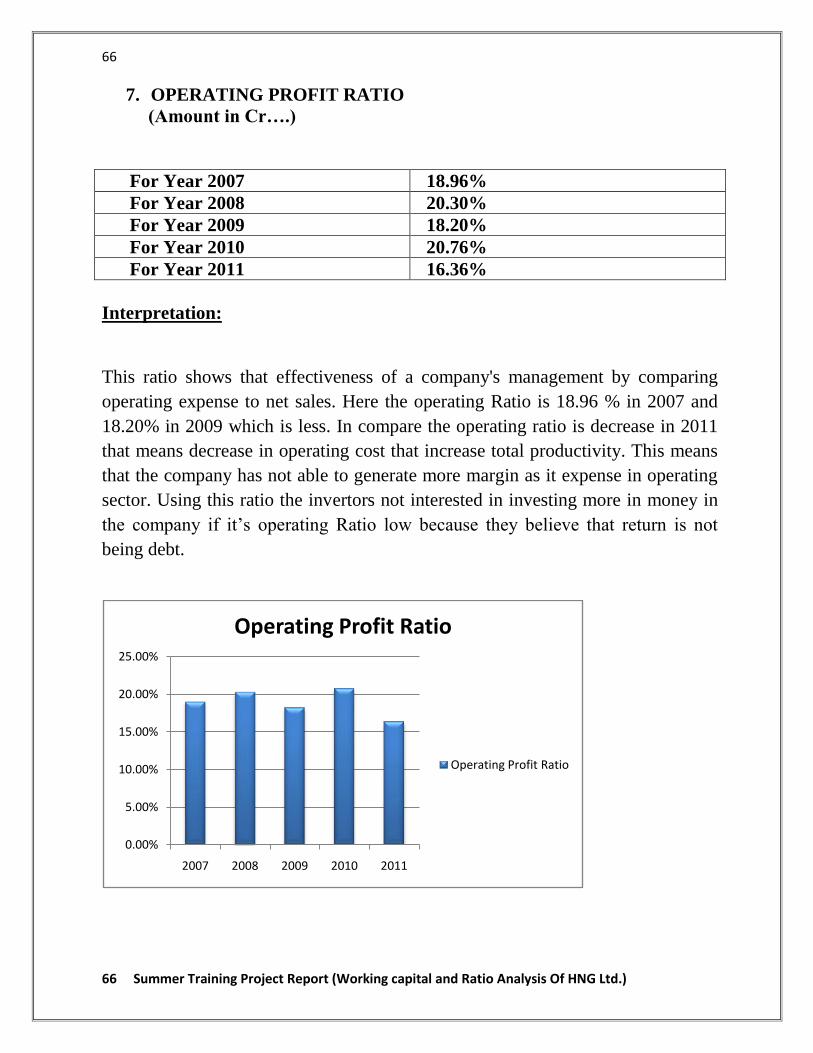

4. PROFITABILITY RATIOS -

The primary objectives of business undertaking are to earn profits. Because profit

is the engine, that drives the business enterprise.

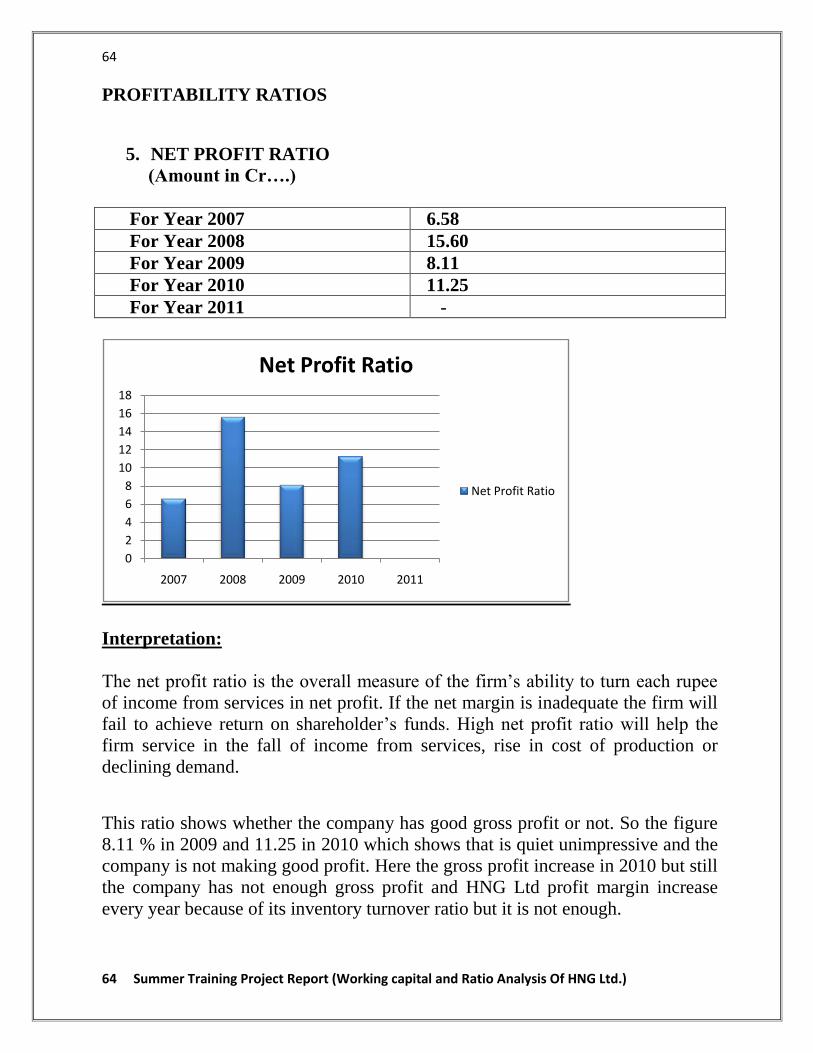

Net profit ratio

Return on total assets

Reserves and surplus to capital ratio

Earnings per share

Operating profit ratio

Price – earnings ratio

(a) NET PROFIT RATIO -

Net profit ratio establishes a relationship between net profit (after tax) and sales

and indicates the efficiency of the management in manufacturing, selling

administrative and other activities of the firm.

Net profit ratio=

Net profit after tax

Net sales

57

57 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

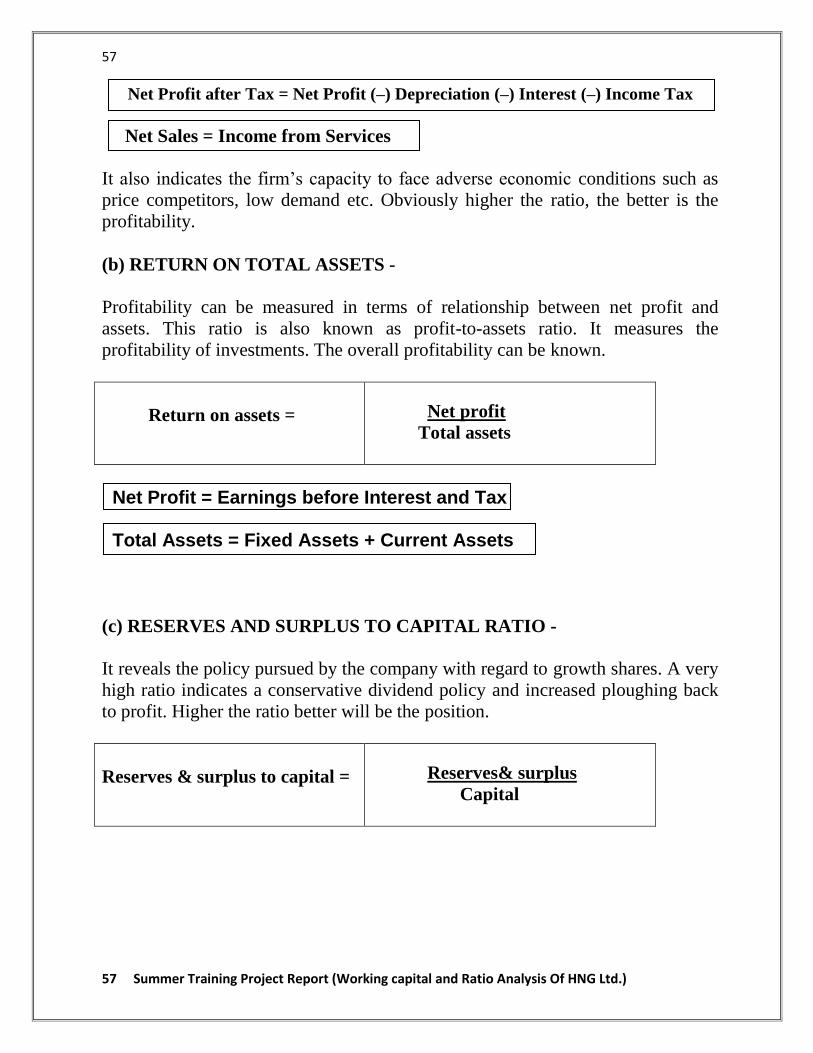

Net Profit after Tax = Net Profit (–) Depreciation (–) Interest (–) Income Tax

Net Sales = Income from Services

It also indicates the firm’s capacity to face adverse economic conditions such as

price competitors, low demand etc. Obviously higher the ratio, the better is the

profitability.

(b) RETURN ON TOTAL ASSETS -

Profitability can be measured in terms of relationship between net profit and

assets. This ratio is also known as profit-to-assets ratio. It measures the

profitability of investments. The overall profitability can be known.

Return on assets =

Net profit

Total assets

Net Profit = Earnings before Interest and Tax Total Assets = Fixed Assets + Current Assets

(c) RESERVES AND SURPLUS TO CAPITAL RATIO -

It reveals the policy pursued by the company with regard to growth shares. A very

high ratio indicates a conservative dividend policy and increased ploughing back

to profit. Higher the ratio better will be the position.

Reserves & surplus to capital =

Reserves& surplus

Capital

58

58 Summer Training Project Report (Working capital and Ratio Analysis Of HNG Ltd.)

(d) EARNINGS PER SHARE -

Earnings per share is a small verification of return of equity and is calculated by