Princeton University Financial Overview · Princeton University Financial Overview ... Princeton...

21

Princeton University Financial Overview Carolyn Ainslie Vice President for Finance and Treasurer October 16, 2013

Transcript of Princeton University Financial Overview · Princeton University Financial Overview ... Princeton...

Princeton University Financial OverviewCarolyn AinslieVice President for Finance and TreasurerOctober 16, 2013

Princeton Finance Facts• Endowment Driven: Princeton has one of the highest endowments per

student in the country, providing almost half of the operating budget.

• Every Student is Subsidized: Educational expenditures are approximately double Princeton’s tuition.

• Robust Financial Aid: 60% of our entering freshman class receive institutional financial aid and all doctoral students are guaranteed tuition and stipend support while fully enrolled.

• Superb Investment Performance: Over 25 years, the average annual growth rate has been 12%; despite big hit in 2009.

• Strong Research Program: Princeton researchers compete effectively for federal dollars, but the government over time has required an increasingly large co‐investment from the University.

2

Princeton Finance Facts • Labor‐Centered: Human capital accounts for more than 40% of

Princeton’s overall operating expenditures.

• Strategic Planning for Capital: The University has a multi‐year capital plan that focuses on priorities and incorporates the use of reserves to fund projects; re‐pay debt; and to endow the cost of on‐going operations and maintenance costs.

• Prudent Cash Management: Accumulated balances and strategic borrowing have positioned the University to address liquidity issues effectively.

• The Long View: Decisions today are carefully considered for their impact on the University in the long view

3

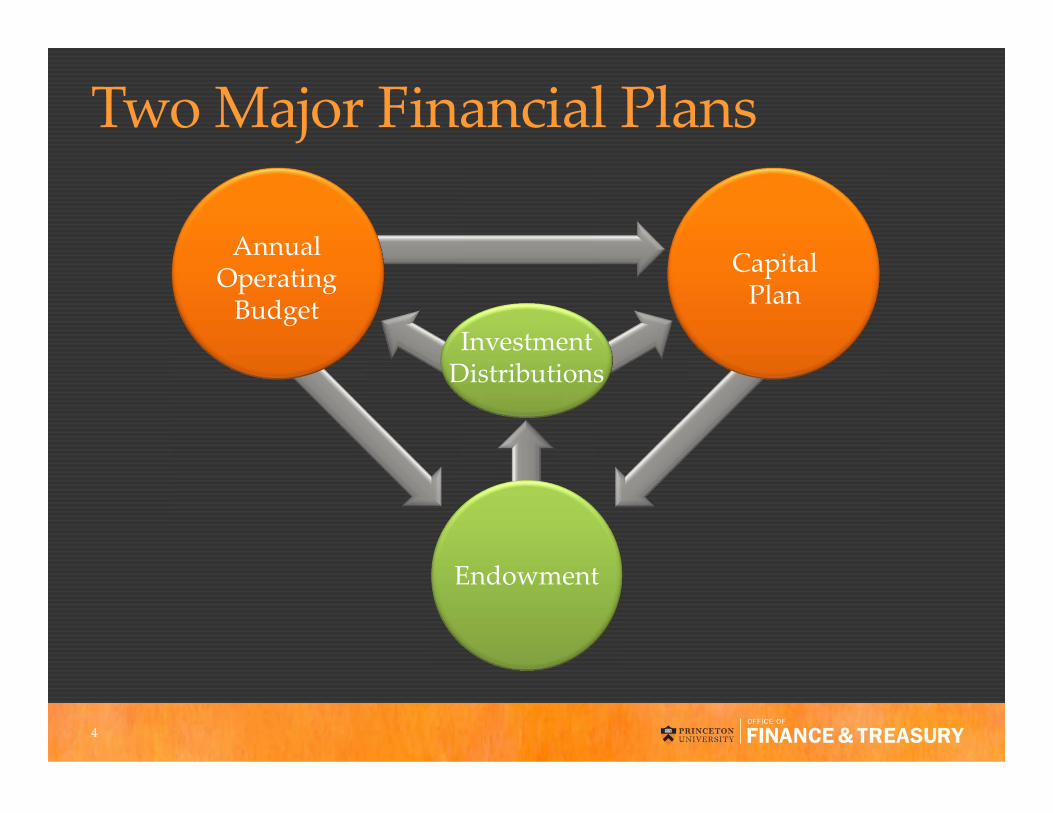

Two Major Financial Plans

Endowment

Capital Plan

Annual Operating Budget

InvestmentDistributions

4

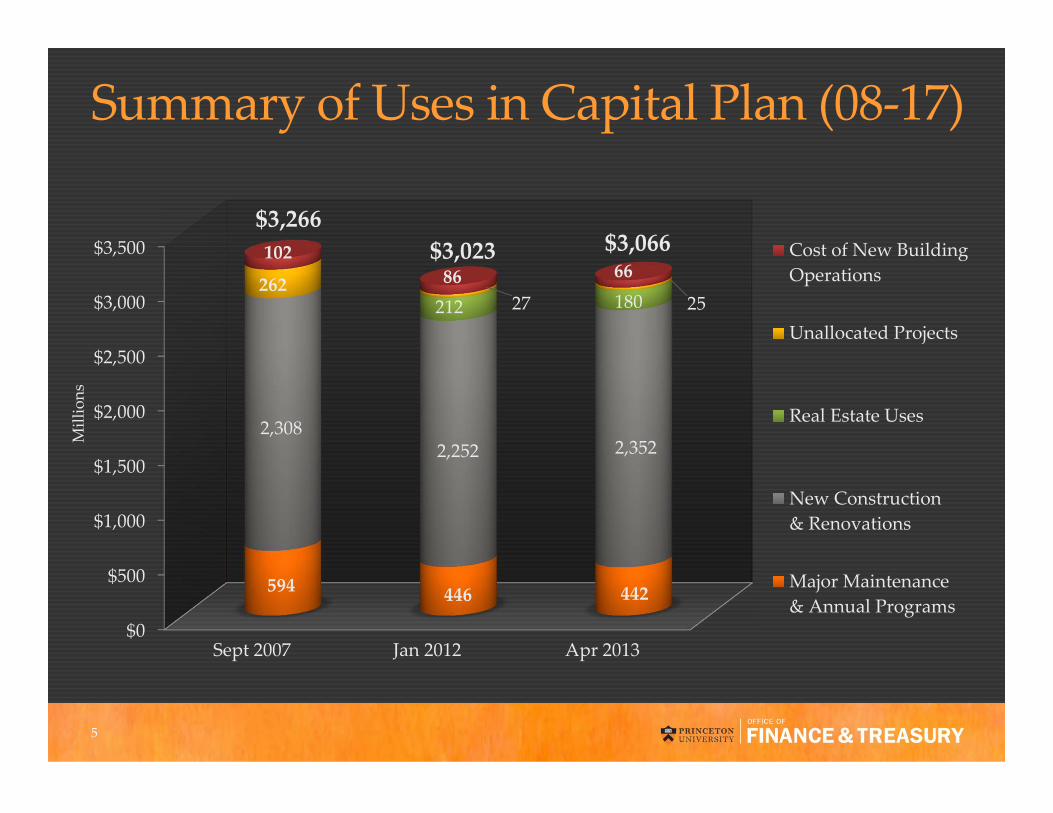

Summary of Uses in Capital Plan (08‐17)

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Sept 2007 Jan 2012 Apr 2013

594 446 442

2,308 2,252 2,352

212 180 262

27 25

102 86 66

Cost of New BuildingOperations

Unallocated Projects

Real Estate Uses

New Construction& Renovations

Major Maintenance& Annual Programs

$3,266$3,023 $3,066

Millions

5

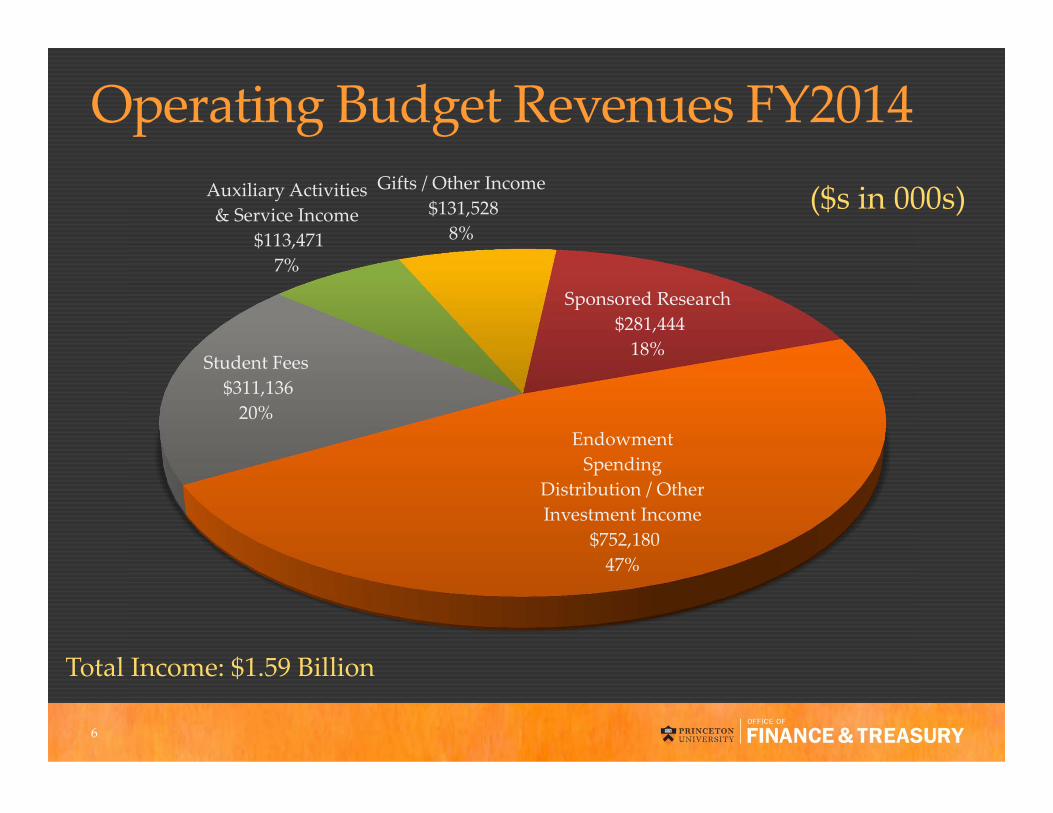

Endowment Spending

Distribution / Other Investment Income

$752,180 47%

Student Fees$311,136 20%

Auxiliary Activities & Service Income

$113,471 7%

Gifts / Other Income$131,528

8%

Sponsored Research$281,444 18%

Operating Budget Revenues FY2014

Total Income: $1.59 Billion

($s in 000s)

6

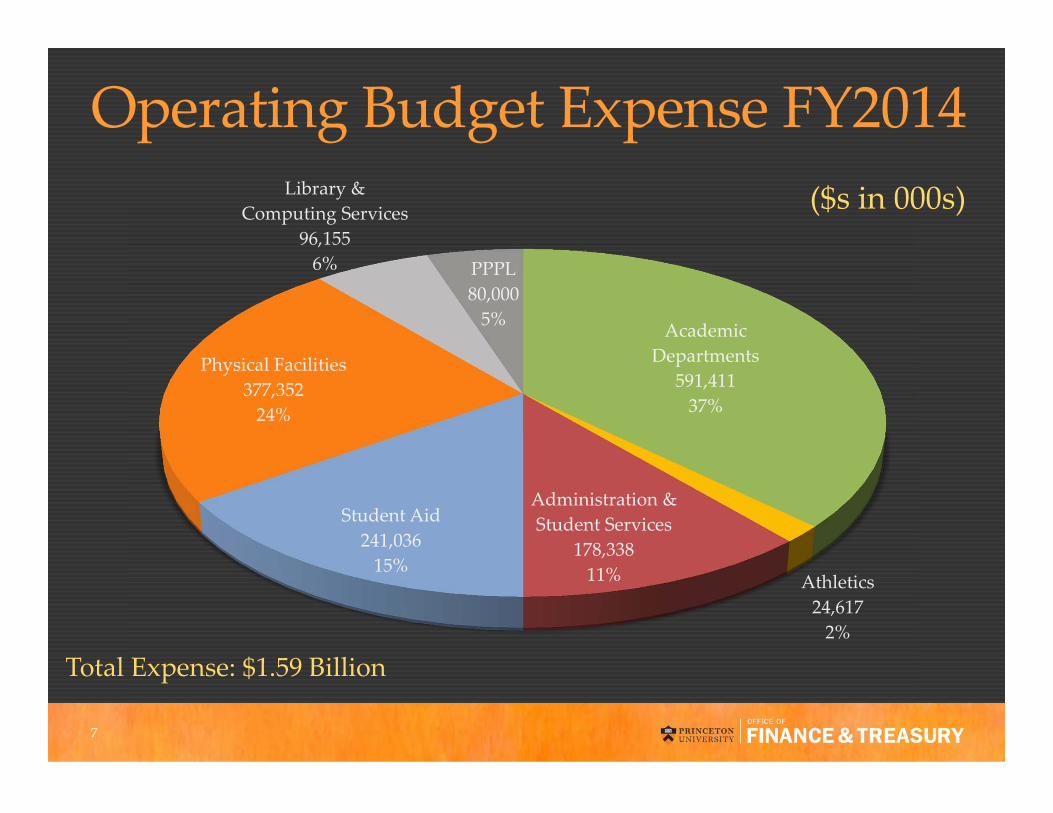

Academic Departments

591,41137%

Athletics24,6172%

Administration & Student Services

178,33811%

Student Aid241,03615%

Physical Facilities377,35224%

Library & Computing Services

96,1556% PPPL

80,0005%

Operating Budget Expense FY2014

Total Expense: $1.59 Billion

($s in 000s)

7

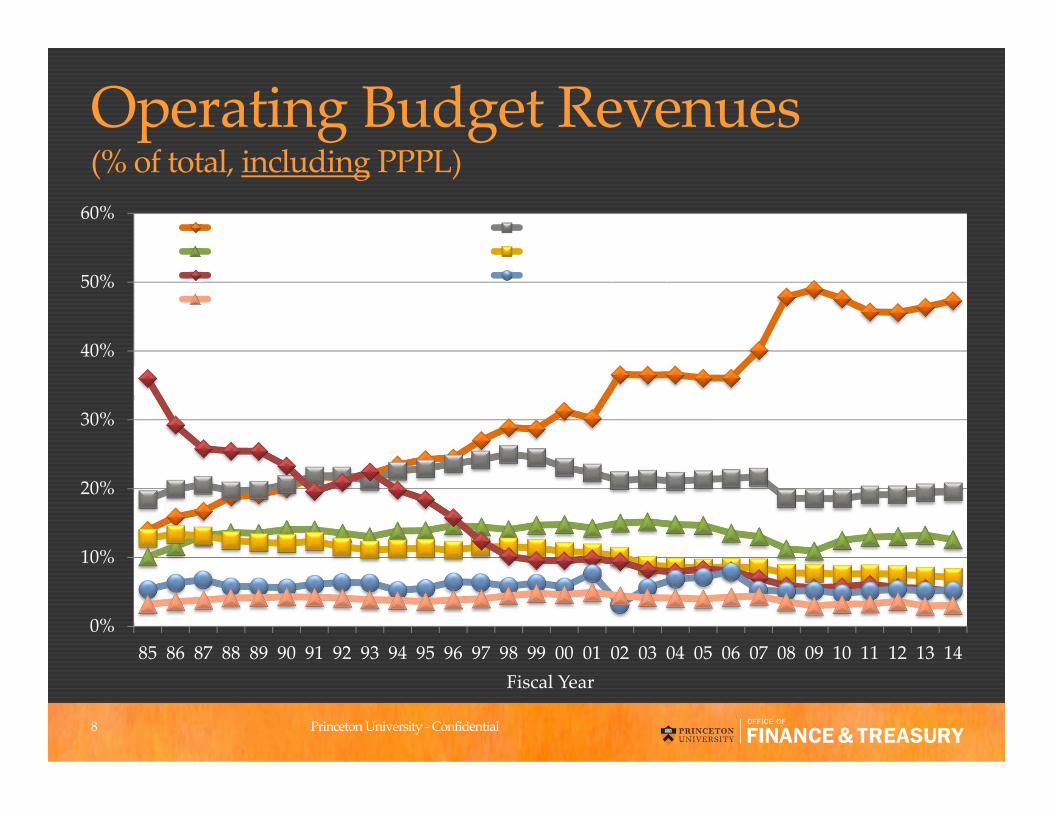

Operating Budget Revenues (% of total, including PPPL)

0%

10%

20%

30%

40%

50%

60%

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14Fiscal Year

Invest. Income Student FeesSpons Res (no PPPL) Aux Activ. & Service DeptsPPPL Private Gifts, Grants, and Other Inc.Annual Giving

8 Princeton University ‐Confidential

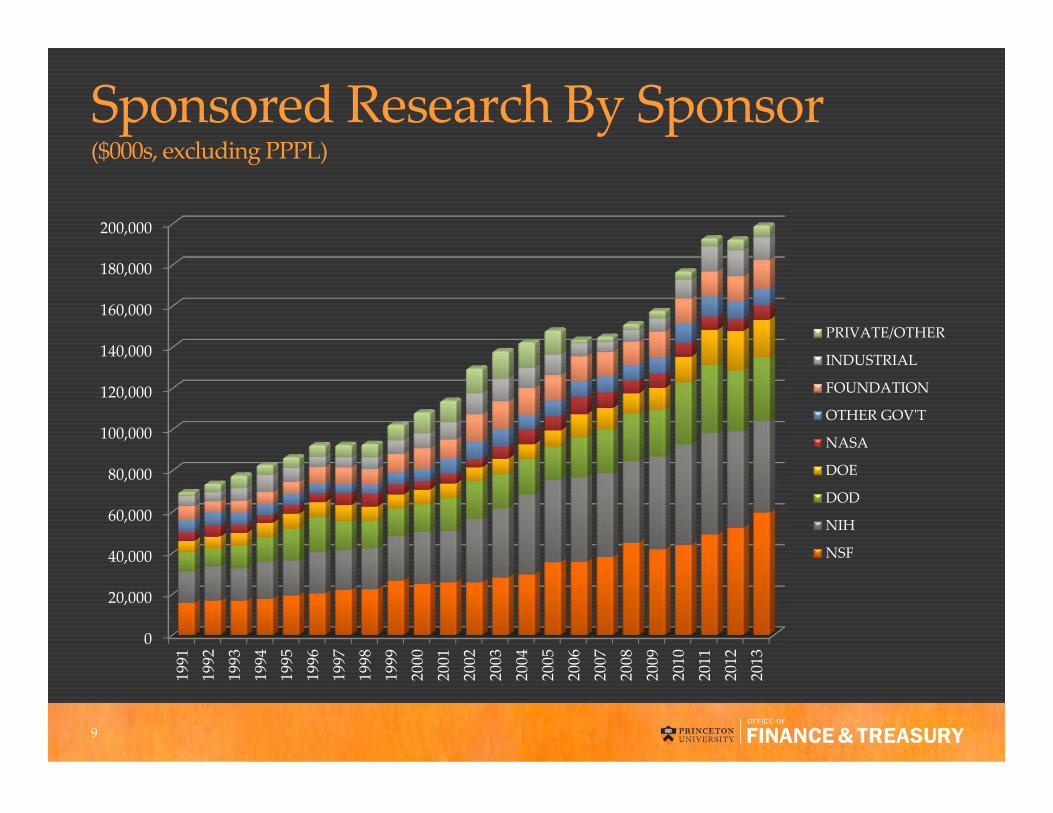

Sponsored Research By Sponsor ($000s, excluding PPPL)

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

PRIVATE/OTHER

INDUSTRIAL

FOUNDATION

OTHER GOVʹT

NASA

DOE

DOD

NIH

NSF

9

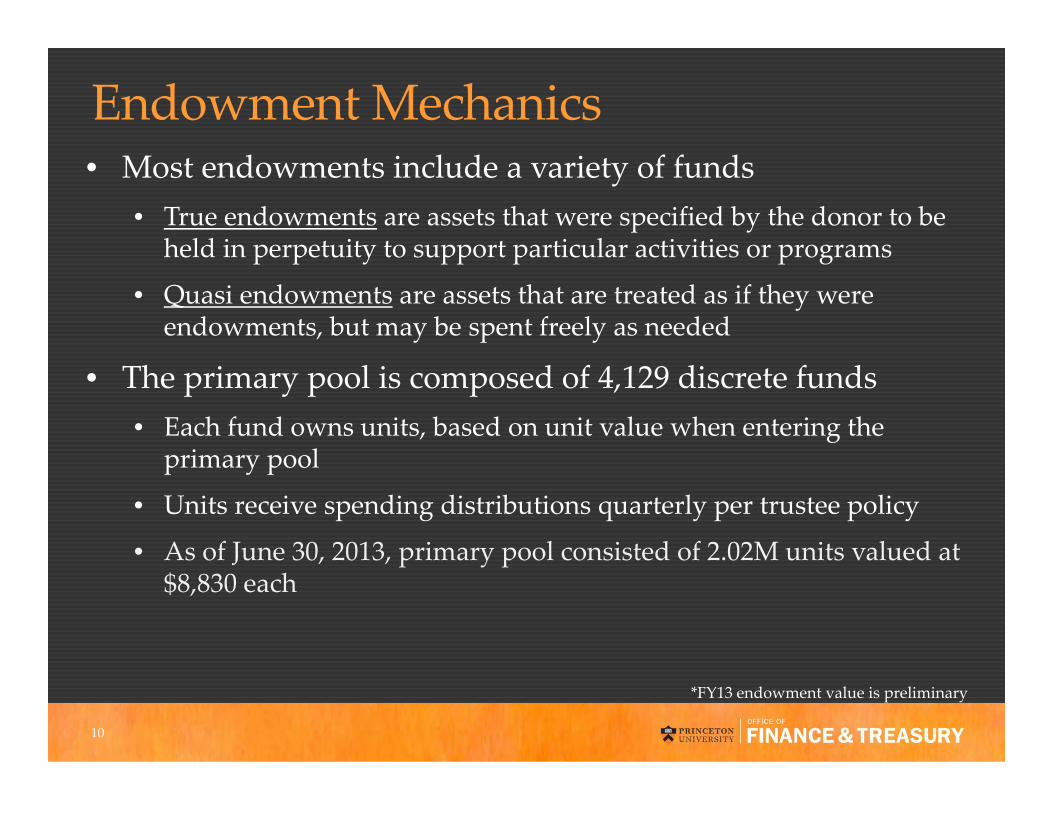

Endowment Mechanics• Most endowments include a variety of funds

• True endowments are assets that were specified by the donor to be held in perpetuity to support particular activities or programs

• Quasi endowments are assets that are treated as if they were endowments, but may be spent freely as needed

• The primary pool is composed of 4,129 discrete funds• Each fund owns units, based on unit value when entering the

primary pool

• Units receive spending distributions quarterly per trustee policy

• As of June 30, 2013, primary pool consisted of 2.02M units valued at $8,830 each

*FY13 endowment value is preliminary

10

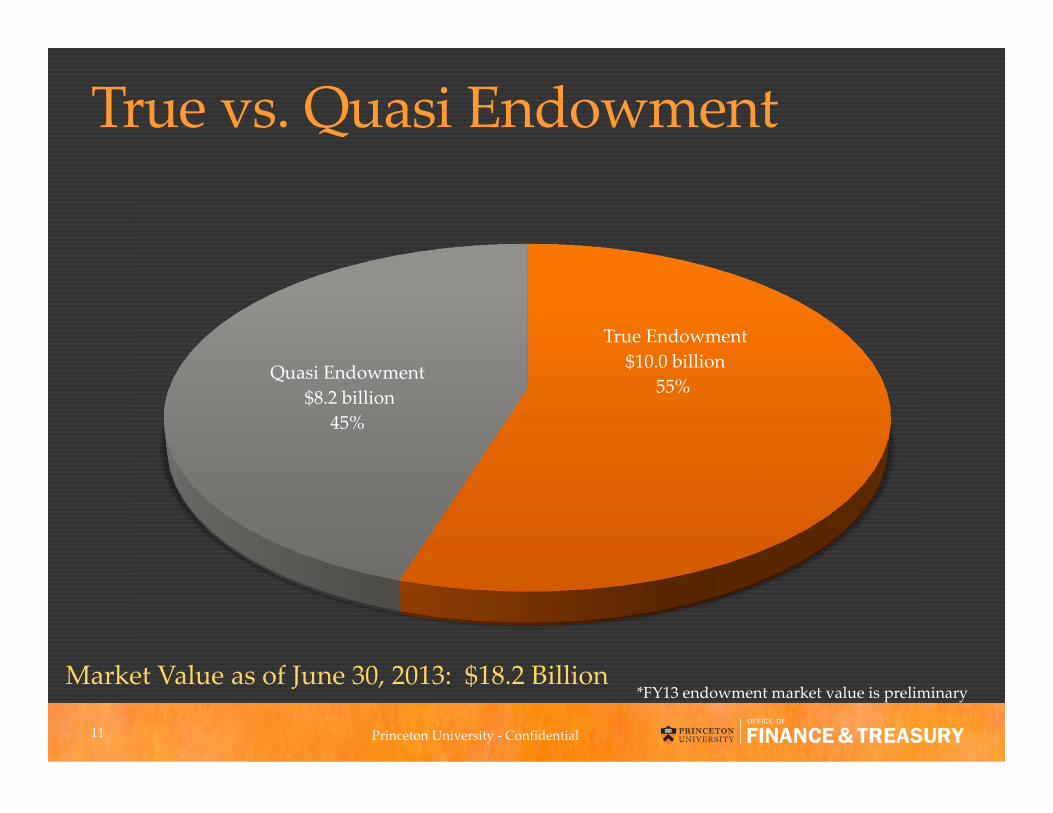

True Endowment$10.0 billion

55%Quasi Endowment

$8.2 billion 45%

True vs. Quasi Endowment

Market Value as of June 30, 2013: $18.2 Billion

Princeton University ‐ Confidential

*FY13 endowment market value is preliminary

11

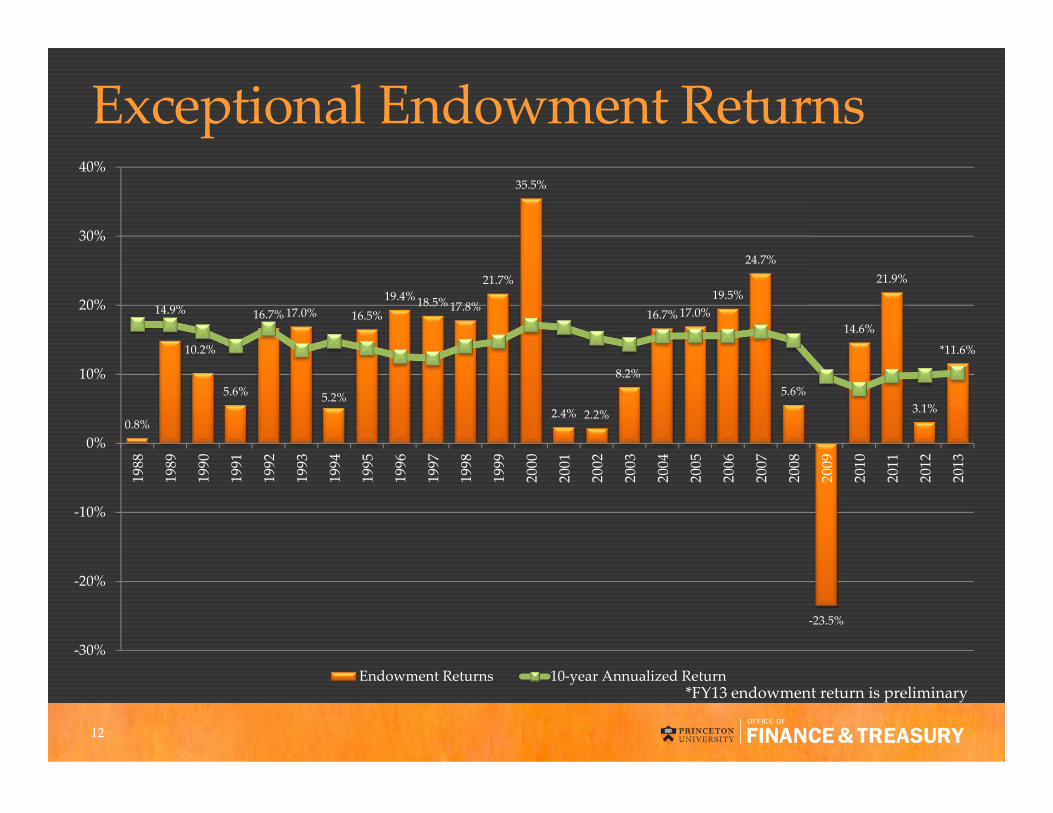

Exceptional Endowment Returns

0.8%

14.9%

10.2%

5.6%

16.7%17.0%

5.2%

16.5%19.4%18.5%17.8%

21.7%

35.5%

2.4% 2.2%

8.2%

16.7%17.0%19.5%

24.7%

5.6%

‐23.5%

14.6%

21.9%

3.1%

*11.6%

‐30%

‐20%

‐10%

0%

10%

20%

30%

40%

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Endowment Returns 10‐year Annualized Return*FY13 endowment return is preliminary

12

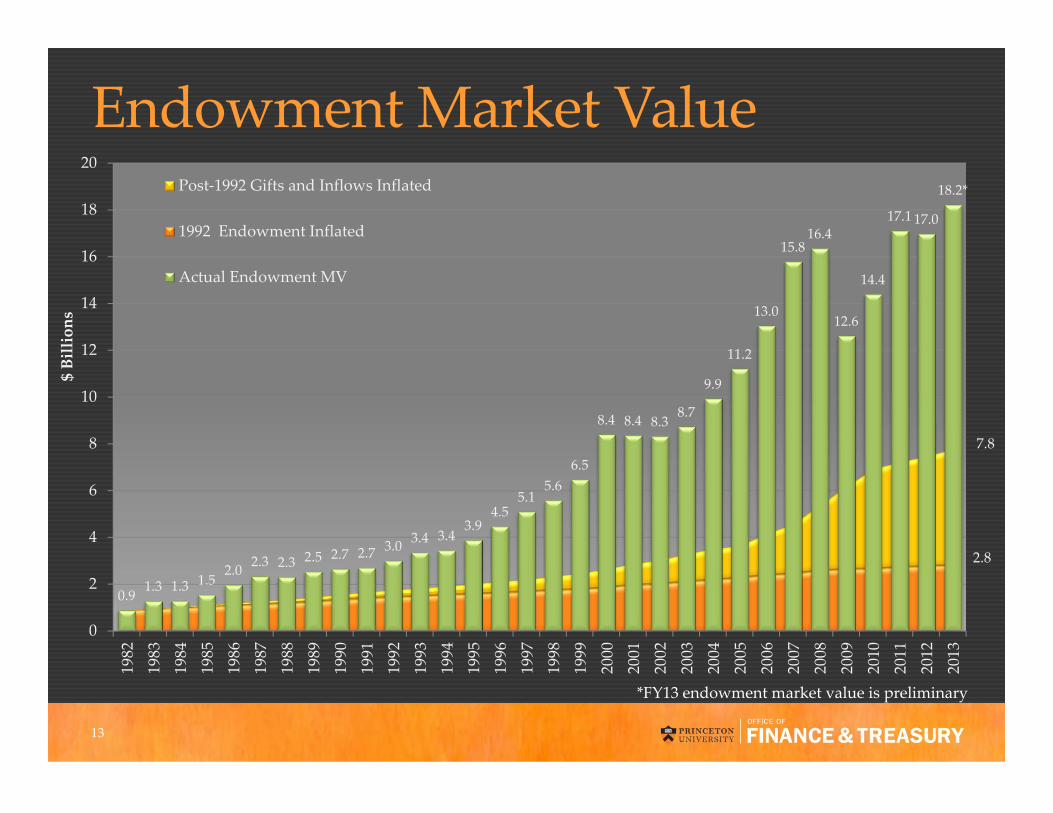

Endowment Market Value

0.9 1.3 1.3 1.52.0 2.3 2.3 2.5 2.7 2.7 3.0 3.4 3.4

3.94.5

5.15.6

6.5

8.4 8.4 8.38.7

9.9

11.2

13.0

15.816.4

12.6

14.4

17.1 17.0

18.2*

0

2

4

6

8

10

12

14

16

18

20

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

$ Billions

Post‐1992 Gifts and Inflows Inflated

1992 Endowment Inflated

Actual Endowment MV

7.8

2.8

*FY13 endowment market value is preliminary

13

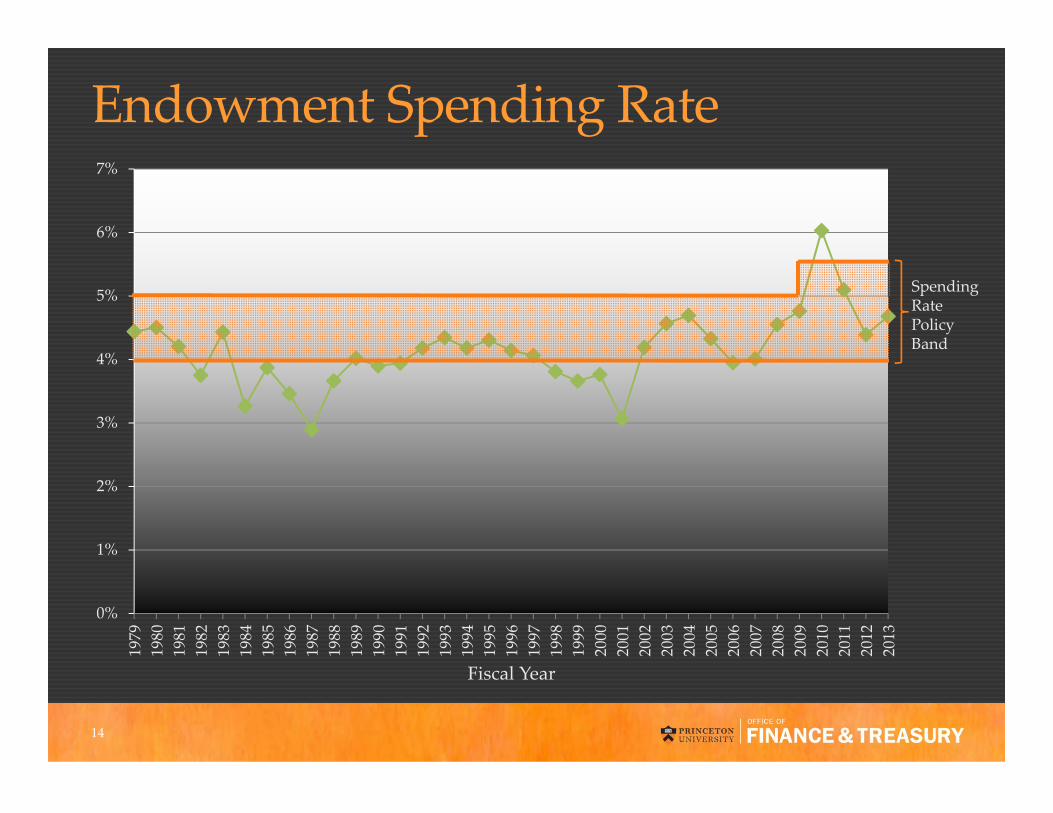

Endowment Spending Rate

0%

1%

2%

3%

4%

5%

6%

7%

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

SpendingRate Policy Band

Fiscal Year

14

PRINCETON PRIME

15

Princeton Prime –Areas of Focus 1. Replace existing accounting structure and redesign

financial reports.

2. Upgrade financial system to latest, supported release.

3. Automate key business processes, reducing paper use.

4. Support budgeting processes with better tools for planning and forecasting.

5. Introduce new Travel and Expense management program.

16

Implications for Departments• Account and Department codes will change.• Less effort for financial managers to answer basic financial

management questions. For example:• How much has Department A spent on travel, recruiting, etc. ?• How much funding does Professor Smith have available, including

gifts, grants and contracts?• Were funds spent in compliance with their restrictions?

• PIs and Grants Managers will have financial reports by award that map to their award budgets.

• Easier to manage and track interdisciplinary activities (e.g. a shared conference).

17

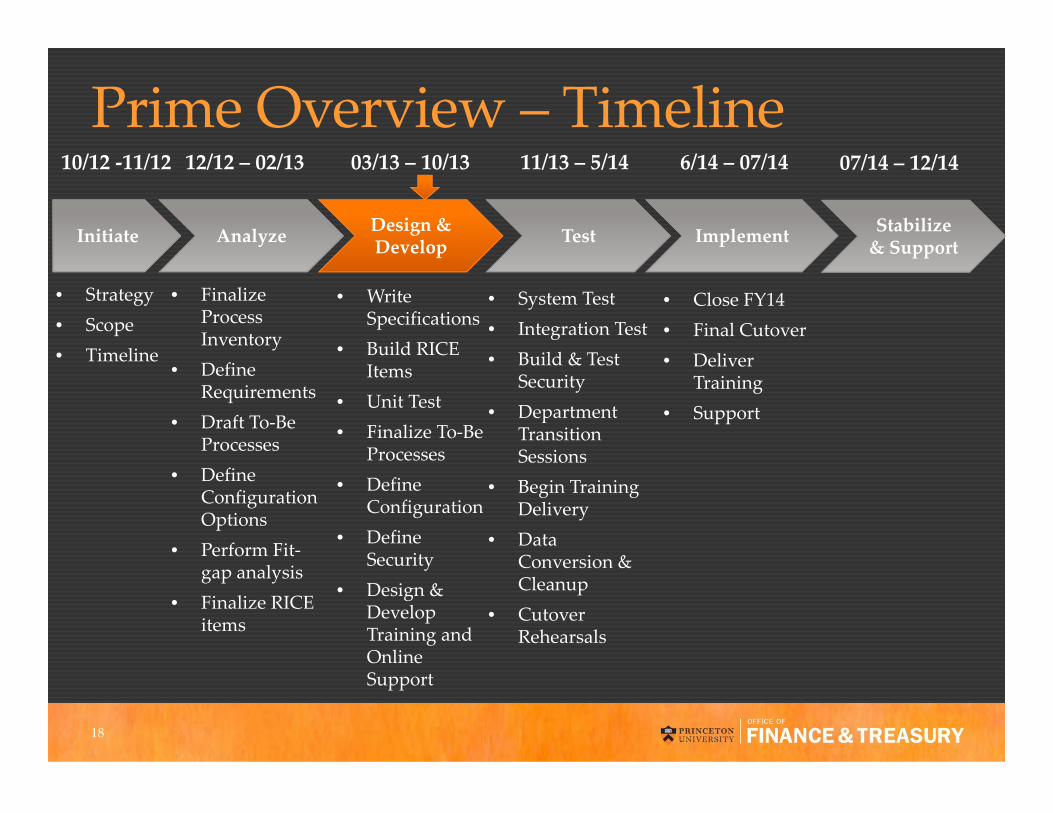

Prime Overview – Timeline

Initiate Analyze Design & Develop Test Implement

• System Test• Integration Test• Build & Test

Security• Department

Transition Sessions

• Begin Training Delivery

• Data Conversion & Cleanup

• Cutover Rehearsals

03/13 – 10/13

• Write Specifications

• Build RICE Items

• Unit Test• Finalize To‐Be

Processes• Define

Configuration• Define

Security• Design &

Develop Training and Online Support

12/12 – 02/13 11/13 – 5/14 6/14 – 07/14

• Close FY14• Final Cutover• Deliver

Training• Support

• Finalize Process Inventory

• Define Requirements

• Draft To‐Be Processes

• Define Configuration Options

• Perform Fit‐gap analysis

• Finalize RICE items

• Strategy• Scope• Timeline

Stabilize & Support

07/14 – 12/1410/12 ‐11/12

18

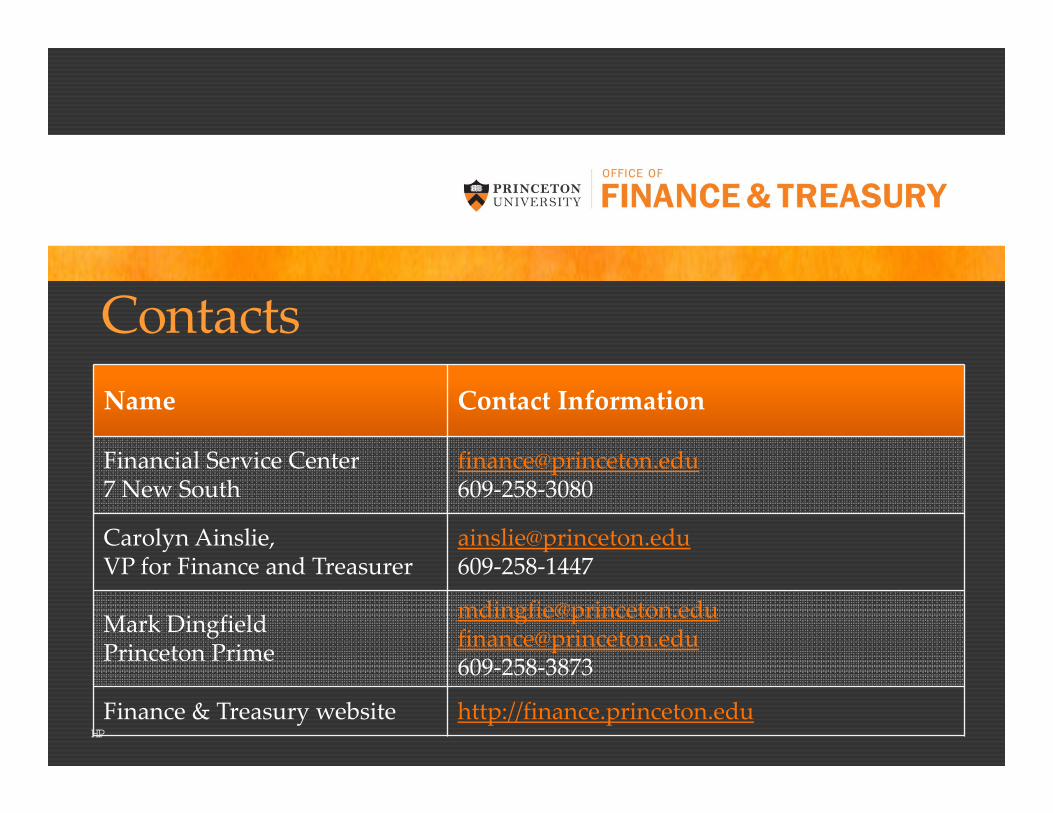

ContactsName Contact Information

Financial Service Center7 New South

[email protected]‐258‐3080

Carolyn Ainslie, VP for Finance and Treasurer

[email protected]‐258‐1447

Mark DingfieldPrinceton Prime

[email protected]@princeton.edu609‐258‐3873

Finance & Treasury website http://finance.princeton.edu19

Thank you!