Applied Techniques for Conversion Rate Optimisation - Paul Rouke from PRWD

27/10/2016

1

Price Optimisation: A case study of new pricing techniquesAlan Clarkson, Royal LondonAlastair Black, Willis Towers Watson

4 November 2016

Agenda

• What is price optimisation?

• Price optimisation in the life market – benefits and practicalities

• Conclusions and questions

27 October 2016 2

27/10/2016

2

What is price optimisation?

27 October 2016

What is price optimisation?

• Any movement away from a “technical” price is price optimisation, and it happens all the time:

27 October 2016 4

Brand value

Strategic pricingCustomer demand

Competitive pricing

27/10/2016

3

Price optimisation in insuranceInsurance is different!

• Customers are used to providing lots of information

• Fewer “physical” constraints

• …. but stronger TCF requirements

Use of customer demand to set prices

• Analyse the likelihood of different segments to purchase

• … and use this as a quantitative input

• Traditionally done only at a very high level

• Separate “risk” and “demand and elasticity” components

27 October 2016 5

Risk modelling

• The underlying cost of providing the insurance policy

• Covering commission, benefits, expenses, cost of capital

• Typical cashflow model, with assumptions

• Nothing new!

• But an opportunity to improve risk modelling

27 October 2016 6

27/10/2016

4

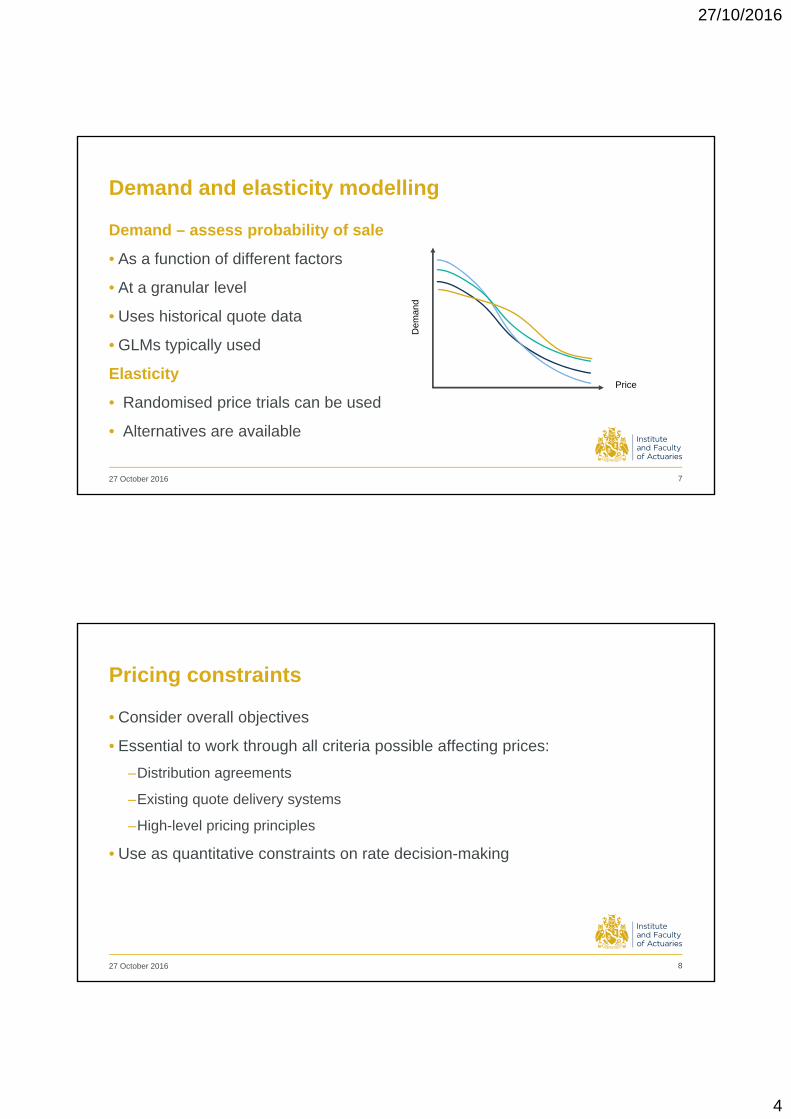

Demand and elasticity modelling

Demand – assess probability of sale

• As a function of different factors

• At a granular level

• Uses historical quote data

• GLMs typically used

Elasticity

• Randomised price trials can be used

• Alternatives are available

27 October 2016 7

Price

Dem

and

Pricing constraints

• Consider overall objectives

• Essential to work through all criteria possible affecting prices:

–Distribution agreements

–Existing quote delivery systems

–High-level pricing principles

• Use as quantitative constraints on rate decision-making

27 October 2016 8

27/10/2016

5

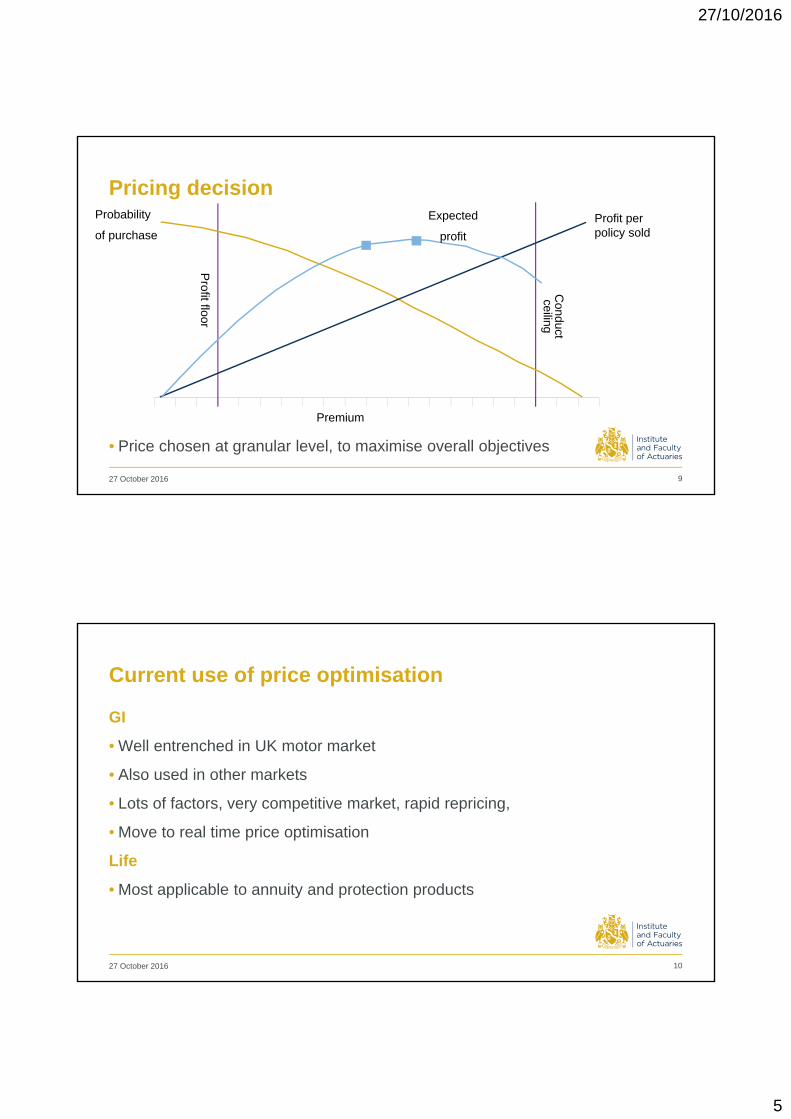

Pricing decision

• Price chosen at granular level, to maximise overall objectives

27 October 2016 9

Conductceiling

Profit floor

Probability

of purchase

Expected

profit

Premium

Profit per policy sold

Current use of price optimisation

GI

• Well entrenched in UK motor market

• Also used in other markets

• Lots of factors, very competitive market, rapid repricing,

• Move to real time price optimisation

Life

• Most applicable to annuity and protection products

27 October 2016 10

27/10/2016

6

Price optimisation in the Life marketBenefits and practicalities

27 October 2016

The Protection Market

27 October 2016 12

“Standard” Price Other FactorsPrice Is Important

Flat MarketAdvised ChannelLife & Sickness

27/10/2016

7

Opportunity for life insurers?

27 October 2016 13

Risk Factors

Term of Contracts

Flat Market

Regulatory Pressure

Volume of Data

Key Reasons used in GI Opportunities in Life

Risk Factors

Aggregators Aggregators

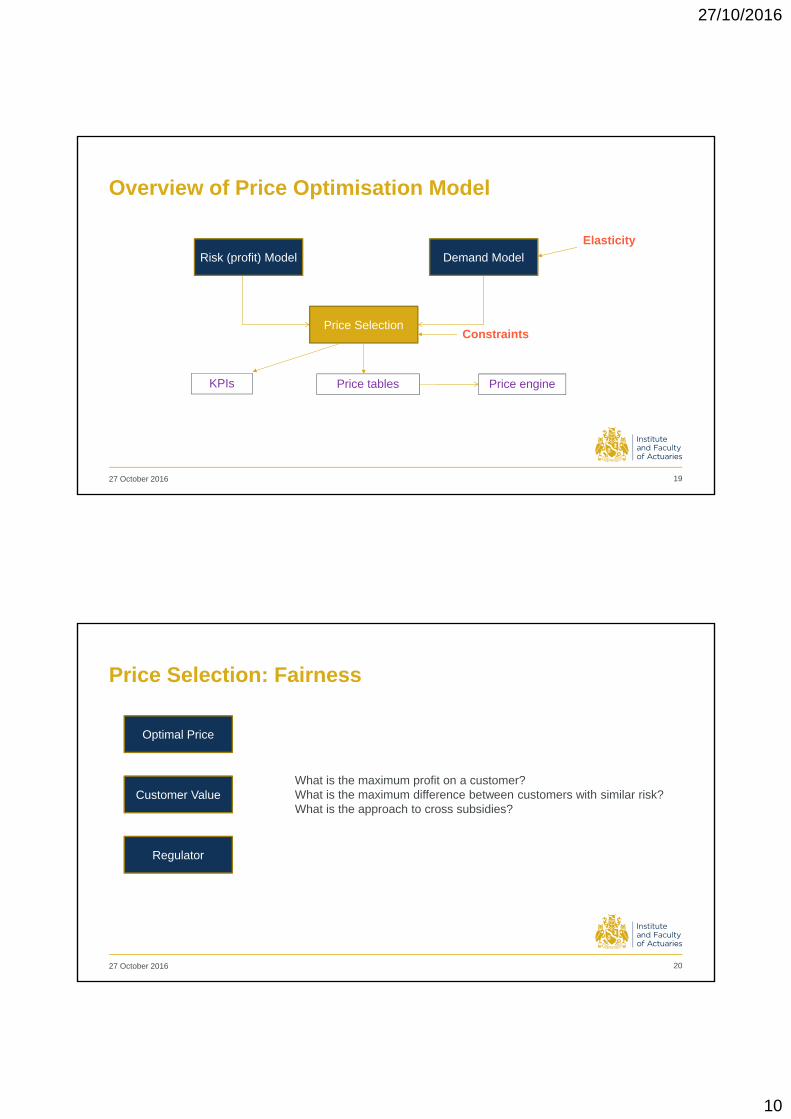

Overview of Price Optimisation Model

27 October 2016 14

Price tablesKPIs Price engine

Risk (profit) Model Demand Model

Price SelectionConstraints

Focus on “Demand Model” and “Price Selection”

Elasticity

27/10/2016

8

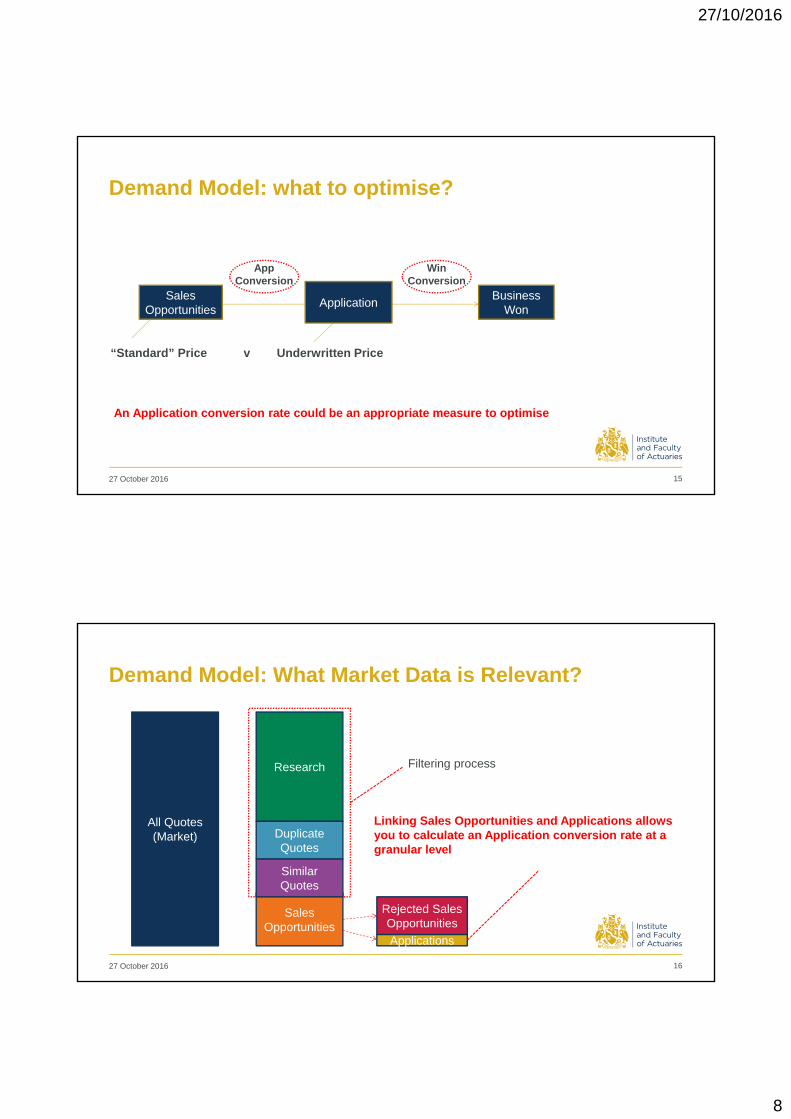

Demand Model: what to optimise?

27 October 2016 15

Sales Opportunities

Business Won

App Conversion

An Application conversion rate could be an appropriate measure to optimise

Win Conversion

Application

“Standard” Price v Underwritten Price

Demand Model: What Market Data is Relevant?

27 October 2016 16

All Quotes(Market)

Research

Duplicate Quotes

Sales Opportunities

Rejected Sales Opportunities

Applications

Filtering process

Linking Sales Opportunities and Applications allows you to calculate an Application conversion rate at a granular level

Similar Quotes

27/10/2016

9

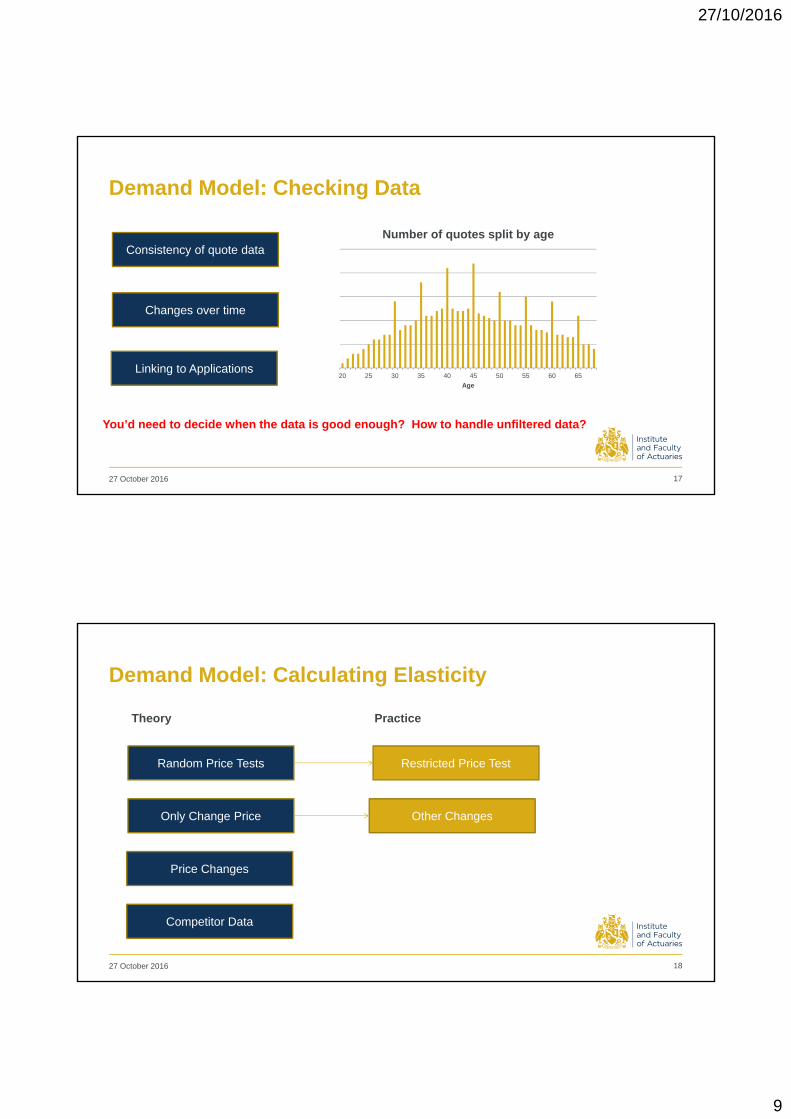

Demand Model: Checking Data

27 October 2016 17

20 25 30 35 40 45 50 55 60 65

Age

Number of quotes split by age

Linking to Applications

Consistency of quote data

Changes over time

You’d need to decide when the data is good enough? How to handle unfiltered data?

Demand Model: Calculating Elasticity

27 October 2016 18

Random Price Tests Restricted Price Test

Price Changes

Competitor Data

Other ChangesOnly Change Price

Theory Practice

27/10/2016

10

Overview of Price Optimisation Model

27 October 2016 19

Price tablesKPIs Price engine

Risk (profit) Model Demand Model

Price SelectionConstraints

Elasticity

Price Selection: Fairness

27 October 2016 20

Optimal Price

Customer Value

Regulator

What is the maximum profit on a customer?What is the maximum difference between customers with similar risk?What is the approach to cross subsidies?

27/10/2016

11

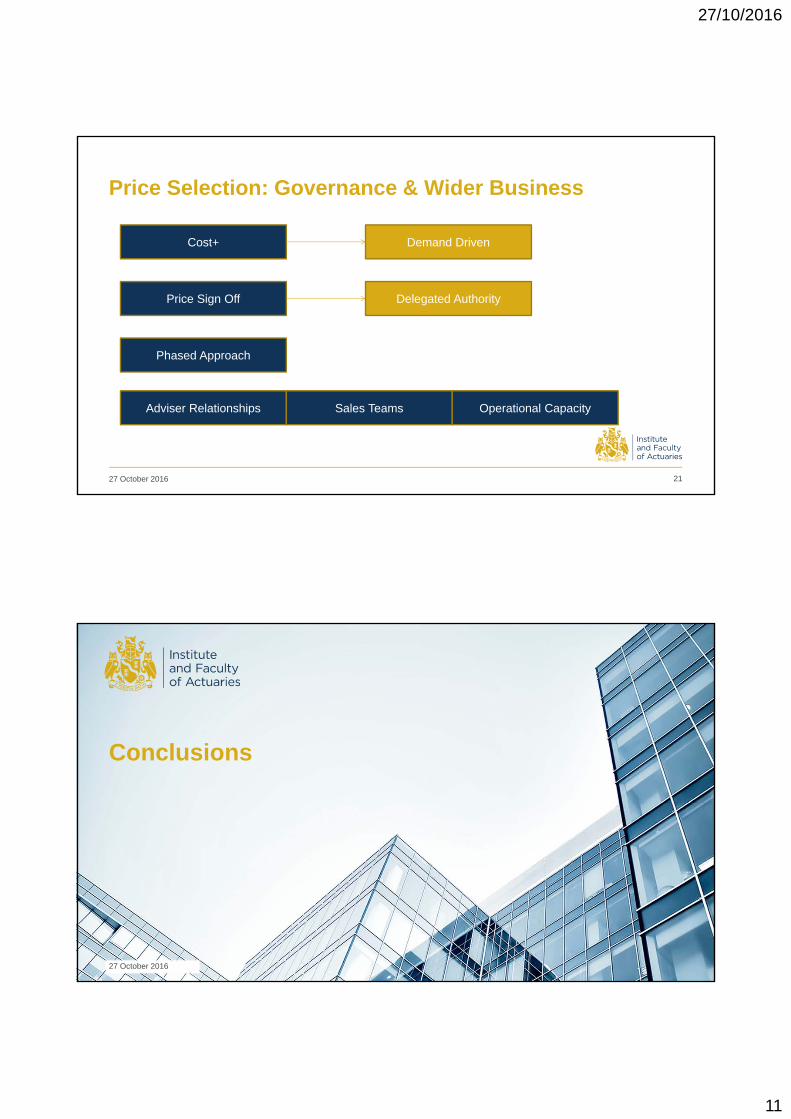

Price Selection: Governance & Wider Business

27 October 2016 21

Adviser Relationships Sales Teams Operational Capacity

Cost+ Demand Driven

Price Sign Off Delegated Authority

Phased Approach

Conclusions

27 October 2016

27/10/2016

12

Price optimisation has arrived in Life insurance!

• Well proven techniques that add significant business value

• Additional challenges in Life insurance

• Enhanced understanding of customers

• Already being used in the market

• Will become a necessity to compete

27 October 2016 23

27 October 2016 24

The views expressed in this presentation are those of invited contributors and not necessarily those of the IFoA. The IFoA do not endorse any of the views stated, nor any claims or representations made in this presentation and accept no responsibility or liability to any person for loss or damage suffered as a consequence of their placing reliance upon any view, claim or representation made in this presentation.

The information and expressions of opinion contained in this publication are not intended to be a comprehensive study, nor to provide actuarial advice or advice of any nature and should not be treated as a substitute for specific advice concerning individual situations. On no account may any part of this presentation be reproduced without the written permission of authors.

Questions Comments