Presentazione standard di PowerPoint - Jefferies 1040 5 DOC... · CONCLUSION Leading independent...

13

Introduction to DOC Generici Jefferies Conference November 19-20, 2014

Transcript of Presentazione standard di PowerPoint - Jefferies 1040 5 DOC... · CONCLUSION Leading independent...

Introduction to DOC GenericiJefferies Conference

November 19-20, 2014

INTRODUCTION TO DOC GENERICI

• The generics market in Italy

• DOC Generici: Leading Independent player

1

A LAND OF OPPORTUNITY

PENETRATION STILL SIGNIFICANTLY BEHIND EUROPEAN AVERAGE

Source: EGA European Generic Medicines Associations

2

Note: Represents retail sales to the pharmacy market. Source: IMS Health Sell-in

GENERICS: 19% PENETRATION OF ITALIAN RETAIL PHARMA MARKET IN 2014

3

ITALIAN GENERICS MARKET: KEY FEATURES

High concentration of players

High entry barriers

Company Branded

Reference pricing

Prescription by INN (International non-proprietary name) since 2012

Interchangeability with the originator and substitution among generics

Commercial discounts banned since 2009

National budget and repayment of overspending

(*) : source IMS Retail channel 2013 value

4

OUTLOOK: NEW WAVE OF PATENT EXPIRATIONS DRIVE GROWTH FROM 2017 IN ITALY

Ori

gin

ato

r m

arke

t va

lue

tod

ay

Year of Patent Expiration

5

2014-17 GROWTH DRIVEN BY PENETRATION AND PATENT EXPIRATIONS

Source: IMS Forecast 2014, prescription market

CAGR Value: +7,1%

CAGR Volume: +7,2%

6

INTRODUCTION TO DOC GENERICI

• The generics market in Italy

• DOC Generici: Leading independent player

7

DOC: THE LEADING INDEPENDENT GENERIC COMPANY IN ITALY

The only large independentplayer in Italian market

First sales in 2001 from theborn of the generic market

Acquired by Charterhouse in2013

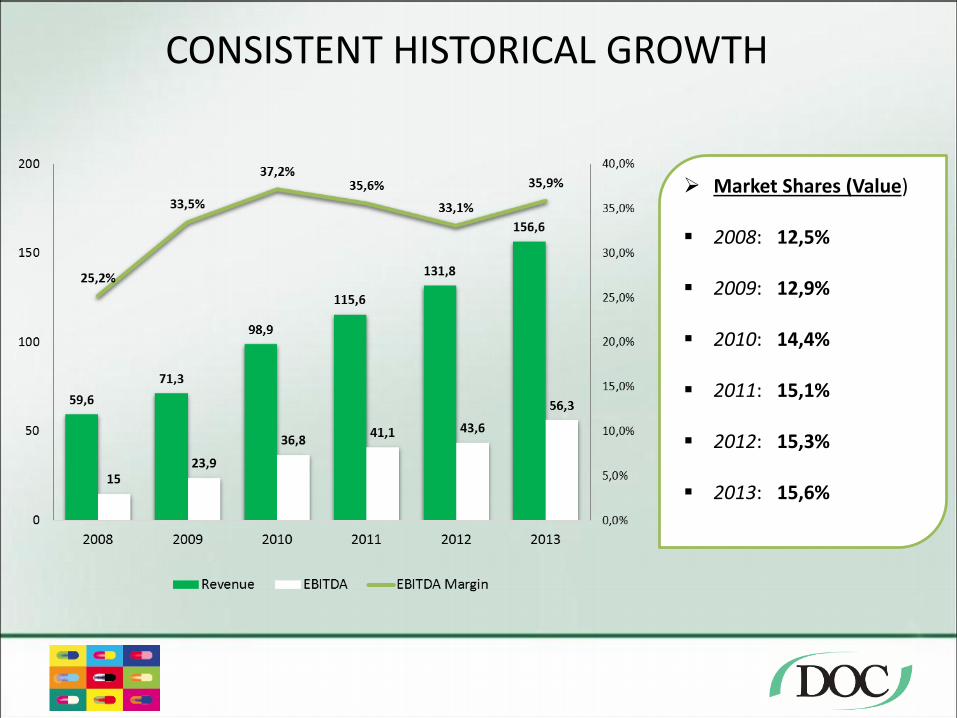

Sales 2013: 156,6 Mio/€(+18,9% vs. 2012)

EBITDA 2013: 56,3 Mio/€(+29% vs. 2012)

EBITDA MARGIN 2013: 36%(2012: 31%)

Market Share 2013: 15,6%(2012: 15,3%)

ORGANIZATION:• 63 employees• 94 exclusive agents

8

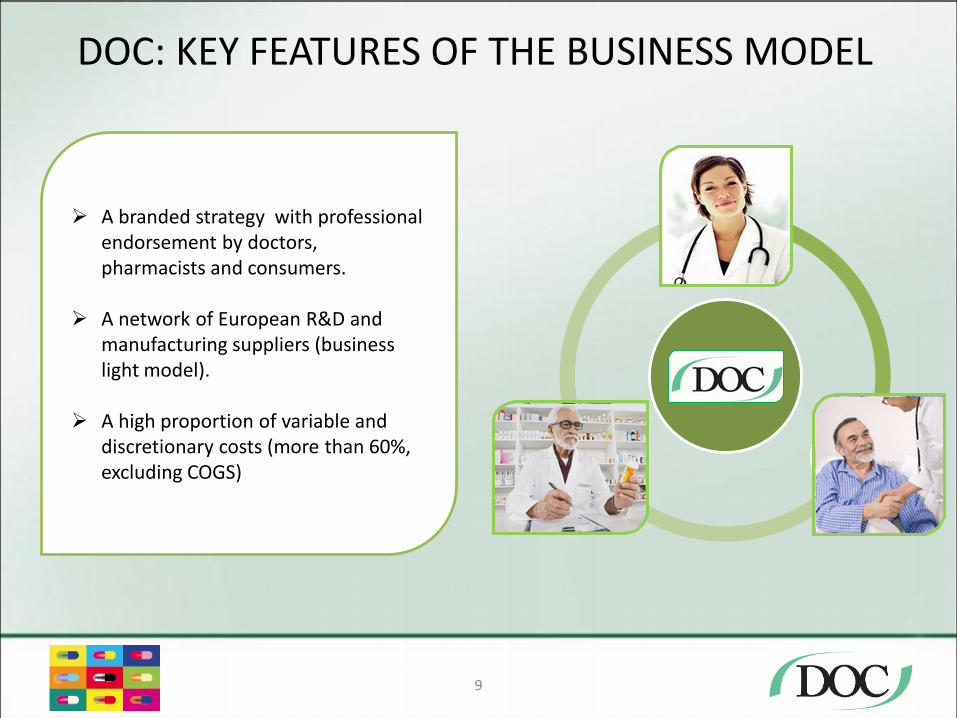

DOC: KEY FEATURES OF THE BUSINESS MODEL

A branded strategy with professional endorsement by doctors, pharmacists and consumers.

A network of European R&D and manufacturing suppliers (business light model).

A high proportion of variable and discretionary costs (more than 60%, excluding COGS)

9

A STRONG TRACK RECORD OF REVENUE GROWTH

0.3 4.3

23.1 29.3 30.5

39.0 39.1

53.5 59.2

71.3

98.9

115.5

131.8

156.6

0

20

40

60

80

100

120

140

160

180

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Net Sales Evolution (2000-13), EURm

2000-13 Revenue growth CAGR: 64%

CONSISTENT HISTORICAL GROWTH

Market Shares (Value)

2008: 12,5%

2009: 12,9%

2010: 14,4%

2011: 15,1%

2012: 15,3%

2013: 15,6%

CONCLUSION

Leading independent player in the Italian company-branded generics market

One of the most recognised generic brands in Italy

Flexible cost structure and asset light business model

Strong financial performance and cash generation

A market leading position….

….providing a compelling competitive position for future growth..

Uniquely positioned to exploit the growth of the Italian generics market

12