Measure BB & Bond Oversight Committee Bond Oversight Committee April 30, 2012.

.

Merrill Lynch & Co. Market Risk Management

CONFIDENTIAL

Presentation to the Risk Oversight Committee

Market Risk Management Update

September 26, 2007

N .... o

"'" "'" o o o IT o c U

I

....I 2: U <C III

~ CI) CIl :::::I C" CIl

0:: -I: CIl E 10 ~ I-'iij '.;:::: I: CIl

"C ;;::::: I: o U

.

Merrill Lynch & Co, Market Risk Management

MRM Presentation to the Risk Oversight Committee VaR Backtesting

u

'" = 0 ,,.. --~ 0 rJl ~

300

200

100

0

(100)

(200)

(300)

Jan-01

Daily Backtesting P/L*

-I-day 99% specific risk VaK + add-on for specific issuer volatility

Jan- Jan- Feb- Feb- Mar- Mar-

15 29 12 26 12 26 Apr- Apr-

09 23

! :8/16 I

8/7 I 8/23

I

May- May- Jun- Jun- Jul- Jul- Jul- Aug- Aug- Sep-07 21 04 18 02 16 30 13 27 10

'Daily Backtesting PjL is intended to reflect profits or losses driven by market price changes on the day. The base PjL is Greensheets Principal Transactions, which excludes interest, dividends, fees and commissions. In some cases, Daily Backtesting PjL is also adjusted to eliminate material non-market driven accounting adjustments, new deal PjL, and in some cases intraday trading. The backtesting P&L does not include RPI and CD 0 Super Senior re-marking P&L due to the frequency of MTM.

CONFIDENTIAL

M .,... o

"'" "'" o o o IT o c U

I

....I 2: U <C III

~ CI) CIl :::::I C" CIl

0:: -I: CIl E 10 ~ I-'iij '.;:::: I: CIl

"C ;;::::: I: o U

.

Merrill Lynch & Co. Market Risk Management

ML & CO. VaR Backtesting VaR Backtesting (Cont'd)

n Highlight of PfL Movements ($Millions)

Aug-07 (144) Equity SRG

GSFI

Credit Trading

All Others

Aug-16 265 Currencies

Credit Trading

Global Rates

Aug-20 (112) Currencies

Credit Trading

All Others

Aug-23 (152) Credit Trading

Currencies

GSFI

Global Rates

CONFIDENTIAL

(53)

(39)

(19)

(33)

111

111

41

(71)

(17)

(24)

(51)

(48)

(35)

(20)

Proprietary trading losses in Statistical Arbitrage business

Losses on macro hedge due to tightening swap spreads and an equity market rally

Losses driven by CDX spread P / L and bond re-marks

Small losses in various businesses with $12mm from Principal Credit Group Americas

Gains driven by long volatility positions in JPY, CHF, NZD and MXN as well as from short positions in TRL and NZD and long positions in JPY.

Gains due to macro hedges in super-senior book, implemented by buying protection on monolines and through ABX index trades

Gains from long USD interest rate positions and long EUR and USD interest rate vega

Losses driven by lower volatility in JPY, AUD, NZD and TRY

Losses driven primarily by US proprietary trading

-$13mm from US. and Japan GELP

Losses in the super-senior book on ABX index hedges and long protection on monolines

Losses in options trading due to lower JPY, AUD and NZD volatilities

Losses due to adverse market movements causing losses in ABX positions

Drop in interest rate volatilities combined with are-mark ofFX volatilities in the Long Term Complex FX Option business

2

"'" .... o

"'" "'" o o o IT o c U

I

....I 2: U <C III

"C Qj -CI) Qj :::::I C" Qj

0:: -I: Qj

E -!II ~ I-'iij '.;:::: I: Qj

"C ;;::::: I: 0 U

.

Merrill Lynch & Co. Market Risk Management

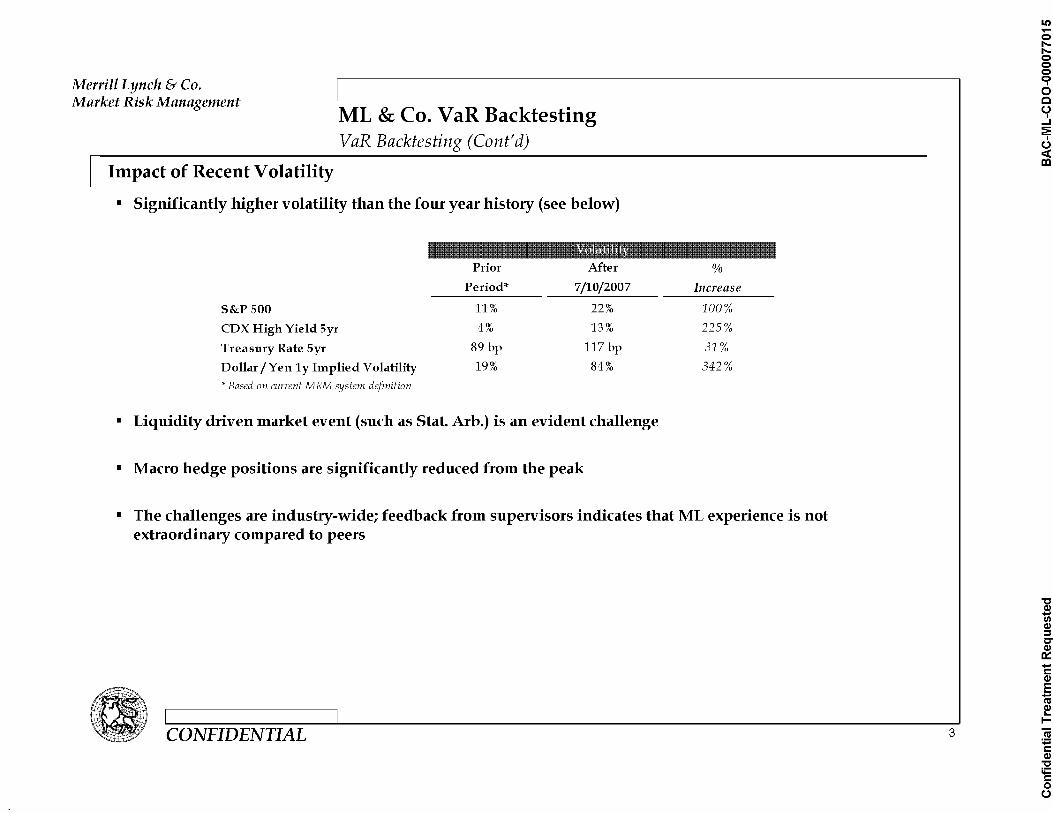

ML & CO. VaR Backtesting VaR Backtesting (Cont'd)

n Impact of Recent Volatility

• Significantly higher volatility than the four year history (see below)

Prior After

Period* 7/10/2007

S&P SOO 11% 22%

CDX High Yield Syr 4% 13%

Treasury Rate Syr 89 bp 117 bp

Dollar / Yen 1 y Implied Volatility 19% 84%

* Based on current MRM system definition

• Liquidity driven market event (such as Stat. Arb.) is an evident challenge

• Macro hedge positions are significantly reduced from the peak

%

Increase

100%

225%

31%

342%

• The challenges are industry-wide; feedback from supervisors indicates that ML experience is not extraordinary compared to peers

CONFIDENTIAL 3

II) .... o

"'" "'" o o o IT o c U

I

...I 2: U <C III

"C Qj -CI) Qj :::::I C" Qj

0:: -I: Qj

E -!II ~ I-'iij '.;:::: I: Qj

"C ;;::::: I: 0 U

.

Merrill Lynch & Co. Market Risk Management

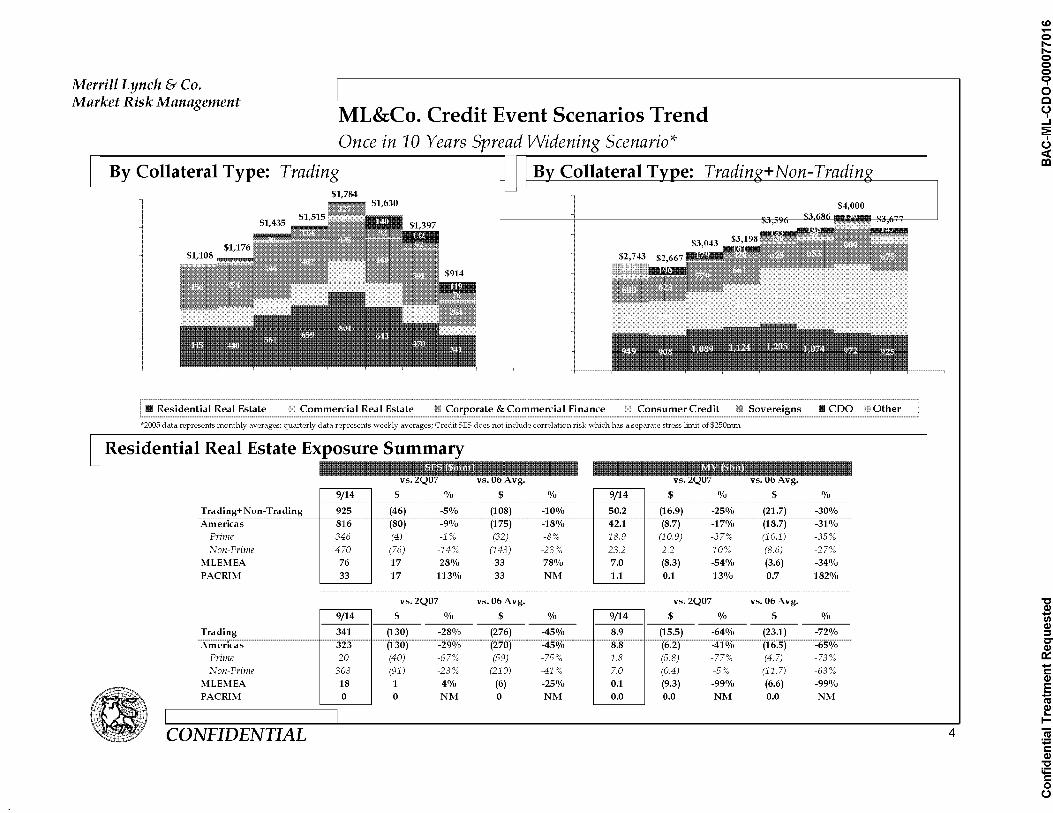

ML&Co. Credit Event Scenarios Trend Once in 10 Years Spread Widening Scenario*

By Collateral Type: T radin g f-=-.I-------"'C=--=o=l=la=t-=er=--=a=l---=-..~=-=---=-=--'-~_=_G_---'=--'-~--'=--'--~_'__=_G_--_

$4,000

Commercial Real Estate Corporate & Commercial Finance Consumer Credit Sovereigns • CDO Other

*2005 data represents monthly averages; quarterly data represents weekly averages; Credit SES does not include correlation risk which has a separate stress limit of $250mm

vs. vs. VS. VS.

9/14 $ % $ % 9/14 $ % $ %

Trading+ Non-Trading 925 (46) -5% (108) -10% 50.2 (16.9) -25% (21.7) -30% ~~~-~~~~~~~~-~~~~~~~~-~~~~~~~~-~~~~~~~~-~~~~~~~~

SI6 lso) ~~~~~~~:~9~o7o

('175) ~~~~~~~~~~::f8(Vo~~

42.1 (S:7) ~~~~~~-~~~~~~~~-~~~~~~~~-~~~~~~~~-~~~~~~~~-~~~~~~~~~~~~~~~~~~~

Americas -17% (18.7) -31% Prime 346 (4) -1% (32) -8% 18.9 (10.9) -37% (10.1) -35% Non~Prime 470 (76) -14% (143) -23% 23.2 2.2 10% (8.6) -27%

MLEMEA 76 17 28% 33 78% 7.0 (8.3) -54% (3.6) -34% PACRIM 33 17 113% 33 NM 1.1 0.1 13% 0.7 182%

vs.2Q07 vs.06Avg. vs.2Q07 vs.06Avg.

9/14 % % 9/14 % %

341 8.9 ~~~~~~323~~~~~~ ~~~~~S:S~~~~~~~

Prime 20 (40) -67% (59) -75% 1.8 (5.8) -77% (4.7) -73% Non~Prime 303 (91) -23% (210) -41% 7.0 (0.4) -5% (117) -63%

MLEMEA 18 1 4% (6) -25% 0.1 (9.3) -99% (6.6) -99% PACRIM 0 0 NM 0 NM 0.0 0.0 NM 0.0 NM

CONFIDENTIAL 4

CD .... o

"'" "'" o o o IT o c U

I

....I 2: U <C III

"C Qj -CI) Qj :::::I C" Qj

0:: -I: Qj

E -!II ~ I-'iij -.;:::: I: Qj

"C ;;::::: I: 0 U

.

Confidential Treatment Requested BAC-ML-CDO-000077017

.

Merrill Lynch & Co. Market Risk Management

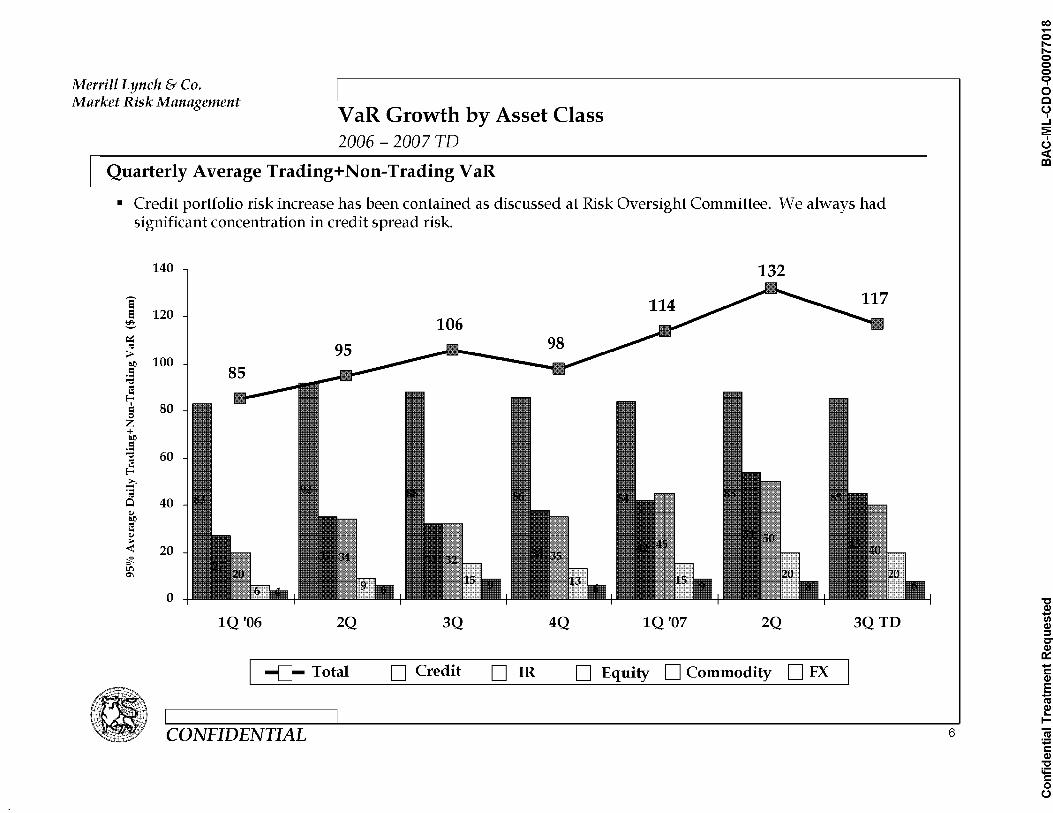

VaR Growth by Asset Class 2006 - 2007 TD

Quarterly Average Trading+ N on-Trading VaR

• Credit portfolio risk increase has been contained as discussed at Risk Oversight Committee. We always had significant concentration in credit spread risk.

140 132

'? IS 120 ~

~

" ~ 100 0.0

oS '"C is

E-< , 80 = 0 z

+ 0.0

oS '"C 60 " E!:: >. -or; 0 40

QJ 0.0

is QJ .. < 20 '2f-l!") C'I

0

lQ '06 2Q 3Q 4Q lQ '07 2Q 3QTD

-{]- Total D Credit D IR D Equity D Commodity D FX

CONFIDENTIAL 6

co .... e l"I"e e e IT o c U

I

....I 2: U <C III

"C .sl CI) CIl :::::I C" CIl

0:: -I: CIl E -1':1 ~ I-

~ -I: CIl

~ I: 0 U

.

Merrill Lynch & Co. Market Risk Management

ABS CDOs Risk Update

n · Issues • Until February 2007, we were able to buy protection to make the risk very far out-of-the-money, hence DV01

was modest. The real challenge started when monolines stopped selling protection on mezzanines.

• After the start of Subprime crisis, the first order focus was to reduce the junior tranche exposure.

• Underlying collateral analysis is extremely challenging due to the complexity of ABS asset combination

• The very low usage in Stress Event Scenario was due to the combination of the far out-of-the-money risk nature and the very low historical volatility of the Super AAA time series mapping.

• Desk-level DV01limits were set at a modest level for AAA risks.

• Current Status

• $5 billion reduction on 50%-100% High Grade risk, possibly more

• Business / Risk / Finance working on new valuation methodology based on fundamental analysis

• Infrastructure challenges in Credit Derivatives

• Exposure Update Retained Super Senior Spread DV01

($Millions) High Grade Mezzanines CD02 Total $ Limit

AUG-06 5,580 1,610 7,190 2.35 Stress $75mm

SEP-06 7,210 2,075 9,285 2.76 3.00

JAN-07 12,810 4,524 17,334 2.42 5.70

FEB 15,175 4,737 370 20,282 4.78 5.70

MAR 18,620 6,109 700 25,429 6.84 7.40

APR 23,220 6,192 1,340 30,752 6.01 7.40

MAY 22,310 6,117 440 28,867 5.98 7.40

JUN 22,310 6,423 1,620 30,353 6.79 7.40

JUL 24,120 6,438 1,505 32,158 6.60 7.40

AUG 18,286 6,228 1,201 25,715 5.40 7.40

SEP 18,158 6,173 1,201 25,532 5.30 7.40

CONFIDENTIAL 7

en .... o

"'" "'" o o o IT o c U

I

....I 2: U <C III

"C Qj -CI) Qj :::::I C" Qj

0:: -I: Qj

E -!II ~ I-'iij '.;:::: I: Qj

"C ;;::::: I: 0 U

.

Merrill Lynch & Co. Market Risk Management

U Follow-up for the Future

ABS CDOs Risk Update (Con t 'd)

• Revised methodology for Subprime stress scenarios based on fundamental analysis (see page on Real Estate Price Shock Scenario)

• Review of other large BjS or far out-of-the-money risk concentration with senior management

• Examples:

• GSFI lending ($40bn+)

• Investment Portfolio ($20bn+ and MLBUSA ABCP)

• Commercial Real Estate Lending ($25bn+ including ML Capital)

• Treasury Liquidity Portfolio ($20bn+ in CMO Floaters)

• Convertibility risk (Korea, India, Brazil, Turkey, etc.)

• GELP non-recourse financing and Hedge Fund derivatives

• OTM Derivative risk in GELP and CFXO (shorter Vega as markets sell off)

CONFIDENTIAL 8

o N o

"'" "'" o o o IT o c U

I

....I 2: U <C III

"C .sl CI) CIl :::::I C" CIl

0:: -I: CIl E -!II ~ I-

~ -I: CIl

~ I: 0 U

.

s;s; ;::, (t)

.... ~ ;:0;- ..... (t) -.... -~t:'""' ..... t..::: 'Jl ;:: ;:0;-('":>

n s;::::-;::, ~

0 ;:: n

~ ~ ?

(t)

~ s (t) ;::

~ ....

~ ~ ~

~ rc t-t t-t ~. --~

"<l = n

=-~ = r;rJ

s= t-t ~ = n rc CJ t-t 0 s= ~

CD

Confidential Treatment Requested BAC-ML-CDO-000077021

.

o

Confidential Treatment Requested BAC-ML-CDO-000077022

.

Confidential Treatment Requested BAC-ML-CDO-000077023

.

Merrill Lynch & Co. Market Risk Management

CONFIDENTIAL

Global Market Risk Management - Appendix Risk Profile Update

[12J

"'" N o

"'" "'" o o o IT o c U

I

....I 2: U <C III

"C Qj -CI) Qj :::::I C" Qj

0:: -I: Qj

E -!II ~ I-

~ -I: Qj

:'5! .... I: 0 U

.

Merrill Lynch & Co, Market Risk Management

MRM Presentation to the Risk Oversight Committee ABX HE 07-1

2007-to-Date Weekly Price Trend by Rating

4,000

3,500 l/ ~ ~ /'

3,000

2,500

~ QJ 2,000 <.I '': ~

1,500

1,000

500

0

/ I/' V ~ ""'-

/ VI /

II-""'"

/ J

L/ V - -

I' "--- /" '-V' , / /

VI' -I' V J ~ ~ ~ ../ ~ r--...

V ~l ~

I 1---+ I I I I I I I I I , I -1/26 2/9 2/23 3/9 3/23 4/6 4/20 5/4 5/18 6/1 6/15 6/29 7/13 7/27 8/10 8/24 9/7

-AAA AA A -BBB BBB-

CONFIDENTIAL

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

13

II) N o

"'" "'" o o o IT o c U

I

....I 2: U <C III

"C Qj -CI) Qj :::::I C" Qj

0:: -I: Qj

E -!II ~ I-'iij '.;:::: I: Qj

"C ;;::::: I: 0 U

.

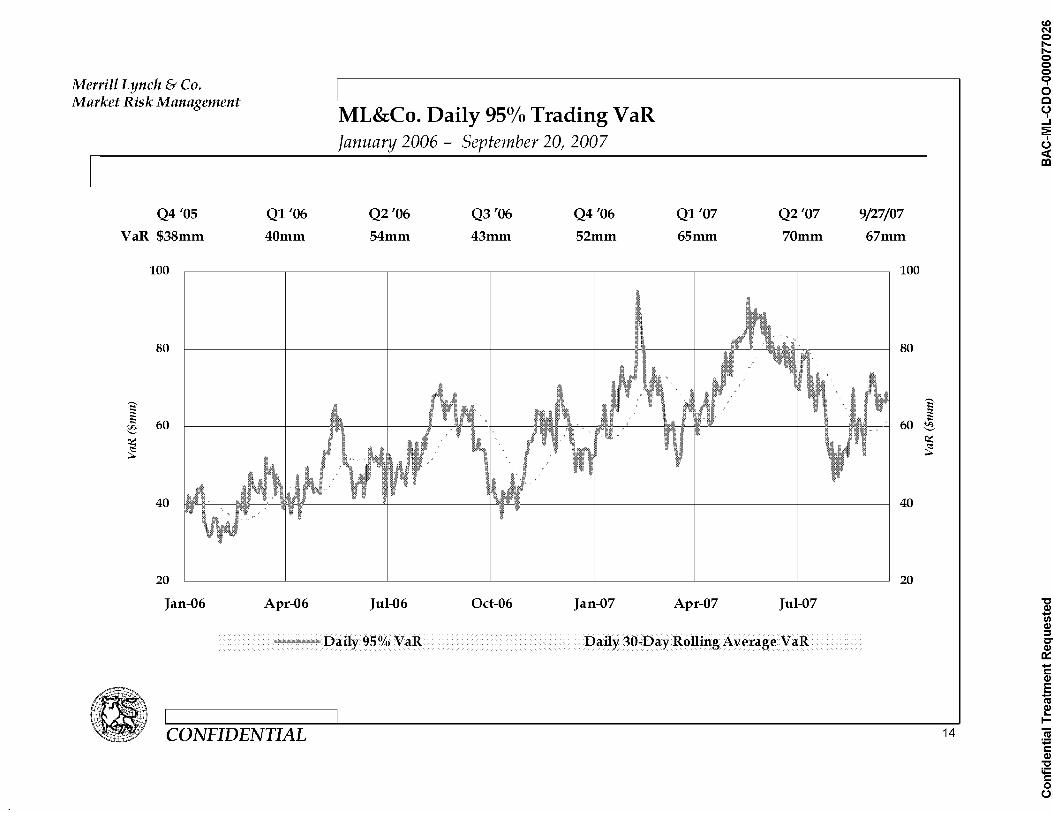

Merrill Lynch & Co. Market Risk Management

u Q4'05

VaR $38mm

E' ;: ~ ~

~

100

80

60

40

20

Jan-06

Ql '06

40mm

Apr-06

ML&Co. Daily 95% Trading VaR January 2006 - September 20, 2007

Q2'06

54mm

Jul-06

Q3'06

43mm

o ct-O 6

Q4'06

52mm

Jan-07

Ql '07

65mm

Apr-07

Q2'07

70mm

Jul-07

---Daily 95% VaR Daily 30-Day Rolling Average VaR

CONFIDENTIAL

9/27/07

67mm

100

80

60

40

20

E' ;: ~ ~ ~

14

CD N o

"'" "'" o o o IT o c U

I

....I 2: U <C III

"C .sl CI) CIl :::::I C" CIl

0:: -I: CIl E -!II ~ I-

~ -I: CIl

~ I: 0 U

.

Merrill Lynch & Co. Market Risk Management

u 100

80

60 1 !:: ~

~ 40

20

o Jan-06 Apr-06

ML&Co. Daily 95% Trading VaR Trend by Risk Factor January 2006 - September 20, 2007

Jul-06 Oct-06 Jan-07 Apr-07 Jul-07

I-TOTAL VAR -CREDIT COMMODITY EQUITY -IR FXI

Note: Credit Risk = Spread Volatility + Credit Product Spread + Credit Product Market Value

CONFIDENTIAL

100

80

60 1 !:: ~

40

~

~

20

0

15

"'" N o

"'" "'" o o o IT o c U

I

....I 2: U <C III

"C .sl CI) CIl :::::I C" CIl

0:: -I: CIl E -!II ~ I-

~ -I: CIl

:'5! .... I: 0 U

.

Merrill Lynch & Co. Market Risk Management

u 120

100

80

1 ::: ~ 60 ~

~

40

20

o

'\ I'" \~. ..

','

- "

ML&Co. Equity Specific Risk November 2006 - September 20, 2007

" ~' ..... .. ,;'~ .'~ ~ # :'.. ... ,.

" , ,~.l'\ '" I'

\ ,'.

'( ~# ~ •

g # ~ ~ \-

~

11/1/0611/26/0612/21/061/15/07 2/9/07 3/6/07 3/31/07 4/25/07 5/20/07 6/14/07 7/9/07 8/3/07 8/28/07

........ -Total VaR wi Eqty Sp. Risk Total VaR wi Gen. Mkt Risk

CONFIDENTIAL

- ........ -Equity VaR wi Eqty Sp. Risk - - - - - - - Equity VaR wi Gen. Mkt Risk

'.

16

co N o

"'" "'" o o o IT o c U

I

....I 2: U <C III

"C .sl CI) CIl :::::I C" CIl

0:: -I: CIl E -!II ~ I-

~ -I: CIl

~ I: 0 U

.

Merrill Lynch & Co. Market Risk Management

U By Risk Factor

180

160

140

120

1 100 !:: ~ ~ 80 ~

60

40

20

0

Jan-06 Apr-06

ML&Co. Daily 95% Stand-alone VaR: Trading+ N on-Trading January 2006 - September 20, 2007

180

160

140

120

100 1 !:: ~

80 ~

~

60

40

20

0

Jul-06 Oct-06 Jan-07 Apr-07 Jul-07

I-TOTAL VAR -CREDIT COMMODITY EQUITY -IR FXI

Note: Credit Risk = Spread Volatility + Credit Product Spread + Credit Product Market Value

CONFIDENTIAL 17

en N o

"'" "'" o o o IT o c U

I

....I 2: U <C III

"C .sl CI) CIl :::::I C" CIl

0:: -I: CIl E -!II ~ I-

~ -I: CIl

~ I: 0 U

.

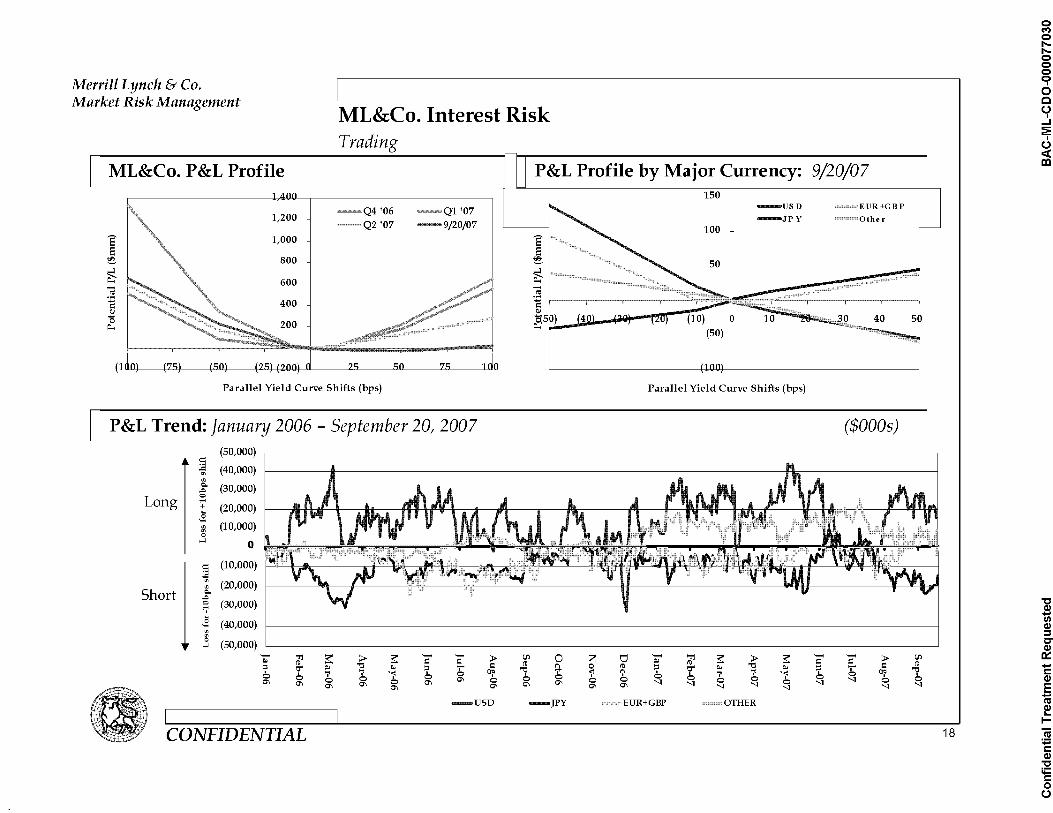

Merrill Lynch & Co. Market Risk Management

ML&Co. Interest Risk Trading

ML&Co. P&L Profile P&L Profile by Major Currency: 9/20/07

1 ~

~ r; .~ Q)

"0 Il.

1,200

1,000

800

600

-Q4'06 Q2 '07

'07 -9/20/07

(lUll) t"(')J t'JIIJ tl'JJ (2"11) II l'J "" "('1 I U

Parallel Yield Curve Shifts (bps)

U P&L Trend: January 2006 - September 20,2007

$: (50,000)

~ (40,000) '"

Long ::.. (30,000) ,.Q

<:> .... + (20,000) ~ '" (10,000) '" 0

""' 0

-USD

-JPY

100

II ~

50

Parallel Yield Curve Shifts (bps)

EUR+GBP

Other

($OOOs)

$: (10,000) ..= i (20,000)

Short

d' L~\7t'_1. .f'I.----... c- , rl~ , ....... • TI8'._/' r,"'"4.i.J .... , .. .... II

,.Q <:> (30,000) '-;' ~ (40,000) ""' '" ~

(50,000) ""' -~ ::s

6 0'>

'Tj a:: > a:: - - > CJl 0 Z tj - 'Tj a:: > a:: - - > CJl ro e e ro ~ ro e e ro OJ" ~ "0 ~ %, T' e

"9 " 0 ro ::s OJ" ~ "0 ~ %, T' e "9 6 7 7 b 0 Oil " -;: b 6 6 7 7 b 0 Oil

0 0 0'> 0 0 0 0 0 0 "I 0 0 0'> 0'> 0'> 0'> 0'> 0'> 0'> 0'> 0'> "I "I "I "I "I "I "I 0'> "I

-USD -JPY EUR+GBP OllIER

CONFIDENTIAL 18

o M o

"'" "'" o o o IT o c U

I

....I 2: U <C III

"C ,Sl CI) CIl :::::I C" CIl

0:: -I: CIl E -!II ~ I-

~ -I: CIl

~ I: 0 U

.

Merrill Lynch & Co. Market Risk Management

ML&Co. P&L Profile

e E ~

~ ";; .~

" "0 ~

-Q4'06 -Ql'07 Q2 '07 -9/20/07 800

600

400

200

(200)

Shift(%)

ML&Co. Equity Risk Trading

P&L Profile: 9/20/07

~ .........

";; '.0 I':

5 Ih ~ (T

U P&L Trend: January 2006 - September 20,2007

--;; (120)

" ] (90)

~ (60)

¢: (30) :a Vl

"if- 0 u;>

100; 30 ..e ~ 60

:3 "E 90

" "0 120 ~ -- ~ ~ ~ ~ -- -- ~

[JJ 0 Z tl -- ~ ~ ~ ~ = = i"t) ~

;: ~ ~ ~ ;: 7" "0 " ~ i"t) ;: ~ ~ , 'i' 'i' '1 0 iJj'I , 'i'" " , 'i' 'i' 0 0 0 , , 0

0"1 0 0 0 0 0"1 0"1 0 0 0"1 0 0 '1 0 0 0

0"1 0"1 0"1 0"1 0"1 0"1 0"1 0"1 '1 '1 '1

300

200

100

(100) (j 5

(200) ~ -AMR APR

Shifts (%)

~ -- -- ~ [JJ

= = i"t) ~ ;: 7" "0 '1 0 iJj'I ,

0 0 '1 '1 0 0 '1 '1 '1

- U.S. & Canada - EMEA APR Japan

CONFIDENTIAL

-EMEA Japan

(120) --;;

" (90) ~ (60) ~ (30)

¢:

:a Vl

0 "if-u;>

30 100;

..e 60 ~

";; 90 ~

" 120 "0 ~

1

19

.... M e l"I"e e e IT o c U

I

....I 2: U <C III

"C .sl CI) CIl :::::I C" CIl

0:: -I: CIl E -!II ~ I-

~ -I: CIl

~ I: 0 U

.

Merrill Lynch & Co. Market Risk Management

ML&Co. Currency Risk Trend Trading

n EUR 600 rn J~Y 1,000 I

1 ~

~ ~ (1W- (8) (6)

Q)

"0 Il.

(4)

-Q4'06 '07

400 Q2 '07 -9/20/07

200

(2)(200) 2

(400)

Shifts (%)

U Emerging Markets FX Loss for +/- 2% Shift Ql '06 Q2 '06 Q3 '06

(45)

'? " ~

Long <t: (30) :E [JJ

'if-";'

(15) '"' 0 ..... ill 0

,.J

'? 0

" ~ Short

<t: (15) :E [JJ

'if-N

(30) + '"' 0 .....

II II Asia IIEMEA II Latin America I 00 00 0

,.J (45)

CONFIDENTIAL

800 J E E 600 ~

~ I 400 ";; '.0 I': 200 Q)

"0 Il. r--

(8) (6) (4) (2)(200) g 2

Shifts (%)

Q4 '06 Ql '07 Q2 '07

-Q4 '06 -Ql '07

Q2 '07 -9/20/07

4 6 8

9/20/07

1

20

N M e l"I"e e e IT o c u , ....I 2: U <C III

"C .sl CI) CIl :::::I C" CIl

0:: -I: CIl E -1':1 ~ I-

~ -I: CIl :E .... I: 0 U

.

Merrill Lynch & Co. Market Risk Management

U Delta by Product

1,000

750

'? 500 E ~ 250 ~

I1J 0 0

(250)

(500)

Jan-06 Mar-06

ML&Co. Commodity Risk Analysis January 2006 - September 20, 2007

~-?-

J - I' .-r f"ti/' ~ ~ 'II .\ -.--- ----.-.----~ .•. -~~-~"'f-T.---.

\. "J'~~t+. l '\I'" v- " - V

May-06 Jul-06 Sep-06 Nov-06 Jan-07 Mar-07 May-07

Americas Power+Gas --EMEA Power+Gas Oil Coal

U Regional Delta by Product 2,000

1,500

1,000

1 500 .~ ..,..,."

~ 0 'If

~ (500) I1J 0

(1,000)

(1,500)

(2,000)

Jan-06 Mar-06 May-06 Jul-06 Sep-06 Nov-06 Jan-07 Mar-07 May-07

Jul-07

Jul-07

- Americas Power -- Americas Gas European Power -- European Gas

CONFIDENTIAL

Sep-07

Other

Sep-07

1,000

750

500 '? E

250 ~

~ 0 I1J

0

(250)

(500)

2,000

1,500

1,000

500 1 o ~

.a (500) Ql

o (1,000)

(1,500)

(2,000)

21

M M o

"'" "'" o o o IT o c U

I

....I 2: U <C III

~ CI) CIl :::::I C" CIl

0:: -I: CIl E 10 ~ I-'iij '.;:::: I: CIl

"C ;;::::: I: o U

.

Confidential Treatment Requested BAC-ML-CDO-000077034