Presentation to investors 10-set-07 - Saras S.p.A. · Certain statements contained in this...

82

September 2007 SARAS S.p.A. 1 Presentation to investors Last update 10 th September 2007

Transcript of Presentation to investors 10-set-07 - Saras S.p.A. · Certain statements contained in this...

September 2007 SARAS S.p.A. 1

Presentation to investors

Last update 10th September 2007

September 2007 SARAS S.p.A. 2

Contents

• Saras in brief• Refining&Power margin• Competitive positioning• Refining context• Margins stability• Growth strategy• Maintenance schedule

SARAS IN A SNAPSHOT page 4

Historical data

• Supply-demand balance

• Stocks

• Commodity prices

• Cracks and differentials

• Oil market outlook

• Supply-demand balance

• Recent news

MARKET OVERVIEW page 19

• Refining

• IGCC Power generation

• Marketing

• Wind

BUSINESS SEGMENTS page 36

• Financial targets

• Group Financials

• Segment financials

• Key ratios

• Sensitivities

• Market multiples

• Analysts estimates

FINANCIALS page 61

• Board of Directors and Top management

• Management compensation

• Corporate governance

• Personnel

• HSE

OTHER page 75

September 2007 SARAS S.p.A. 3

Disclaimer

Certain statements contained in this presentation are based on the belief of the Company, as well as factual assumptions made by any information available to the Company. In particular, forward-looking statements concerning the Company’s future results of operations, financial condition, business strategies, plans and objectives, are forecasts and quantitative targets that involve known and unknown risks, uncertainties and other important factors that could cause the actual results and condition of the Company to differ materially from that expressed by such statements.

• Saras in a snapshot

••• Market overviewMarket overviewMarket overview

••• Business segments descriptionBusiness segments descriptionBusiness segments description

••• FinancialsFinancialsFinancials

••• OtherOtherOther

September 2007 SARAS S.p.A. 5

Saras in brief

ITALY

SPAIN

Ulassai

Sarroch

Sardinia

• 300,000 bl/day 2nd largest supersite* in

Europe integrated with petrochemical� Diesel oriented (diesel yield > 50%)

� Ability to run “unconventional” difficult crudes

� Strategically located in the middle of the Med

Cartagena

Arcola

Saras is a pure play refiner with stabilization of returns coming from Power generation

• Track record of superior site margins

• Marketing activities based in the high diesel demand regions of Italy and Spain

• Investing also in renewable energy� 84 MW wind farm in Sardinia

• Largest liquid fuel gasification plant in the world converting heavy bottoms into clean gas fed into a 560 MW CCGT

� fuel oil yield ~5%

* By complexity: source WoodMackenzie

Refinery&Power plant

Wind farm

Tank farm

Tank farm

September 2007 SARAS S.p.A. 6

Refining 57%Power

Generation 39%

Marketing 4% Ind.Serv&IT 0%

EBITDA by business segment

Saras in brief

568354Group Comparable1 EBITDA

2513MARKETING

324237REFINING

220106POWER GENERATION

-1-1OTHER

26

20062006

15

H1/07H1/07

WIND2 (100%)

EUR ml

% based on 2006 data

1. Calculated evaluating inventories at LIFO

2. Joint Venture Consolidated under the equity method (Saras share 70%)

September 2007 SARAS S.p.A. 7

Refining & Power Margin

* Q3/07 as at 7 September 2007

*

Track record of superior margins

1.9 1.9 5.6 7.1 6.2 5.6 7.7 6.5 5.6 6.7 9.9

2.22.8

3.5

3.9

3.7

3.94.0

4.5

3.6

3.6

3.7

4.4

2.6

1.52.1

4.5 4.7

2.8

1.9

4.7

2.8

1.6

3.0

5.4

2.2

4.14.7

6.1

9.5

10.710.1

9.6

12.2

10.1

9.2

10.4

0.6

14.3

0

2

4

6

8

10

12

14

16

2001 2002 2003 2004 2005 2006 Q1/06 Q2/06 Q3/06 Q4/06 Q1/07 Q2/07 Q3/07

$/b

l

Refinery Margin IGCC margin EMC Benchmark Totale

September 2007 SARAS S.p.A. 8

Ability to fully exploit the current trend in refining margins

• 300,000 bl/day supersite� high complexity (Nelson 9.6*)

� high conversion capacity (#1 in Europe)� integrated with petrochemical

• Diesel oriented (yield > 50%),

� total high value products yield greater that 80%

• Very low fuel oil production (~5%)

� Gasification plant converting the heavy bottoms into clean gas then used in a CCGT

• Marketing activities based in the high diesel demand regions of Italy and Spain

• Ability to run “unconventional” crudes that

normally trade below parity

• Strategically located in the middle of the Med

• Stabilization of returns through Power

generation and processing contracts

Saras’ competitive positioning

Ideal product yield to fully benefit from the projected evolution of products demand

Saras ideally placed to fully benefit from today’s context

Flexibility and geographical location allow a further optimization of crude oil slate

Electricity sold under long term contract with price linked to crude and oil products prices

* Site complexity: includes gasification and petrolchemical

September 2007 SARAS S.p.A. 9

0

2

4

6

8

10

12

14

16

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007 y

td

2008

2009

2010

60

64

68

72

76

80

84

88

92

Med crack spread (*)

Refining Capacity

World Oil Demand

million bbls/day$/bl

(*) 2/3 ULSD crack spread vs Brent + 1/3 Unleaded Gasoline crack spread vs Brent

Source: Saras elaboration on BP statistical review and EMC data for forecast

World Refining context

Strong mid-term margin prospect

• Soaring costs and delays in refinery new builds are supporting the duration of the tight supply/demand balance

• Need for sophisticated (and expensive) secondary units to be built alongside new distillation capacity in order to meet the severe product quality specifications

• Steady growth of demand, focused on light and middle distillates

September 2007 SARAS S.p.A. 10

World Refining context

Light product demand strength is key

• world diesel and gasoline demand steadily growing as high as 2.0-2.5% pa, while fuel oil consumption continues to decline (with benefits for complex refineries vs simple ones)

• the value of middle and light distillates boosted by growing demand and tightening of environmental specifications

• ongoing discussions for bunker fuel switch to gasoil could further boost demand of middle distillates in the next decade

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

Jan-9

9

Jul-9

9Ja

n-00

Jul-0

0Ja

n-01

Jul-0

1Ja

n-02

Jul-0

2Ja

n-03

Jul-0

3Ja

n-04

Jul-0

4Ja

n-05

Jul-0

5Ja

n-06

Jul-0

6Ja

n-07

Jul-0

7

$/b

l

0

10

20

30

40

50

60

70

80

90

$/b

l

Brent Dtd (RHs axis) ULSD crack vs Brent

Gasoline crack vs Brent HSFO crack vs Brent

September 2007 SARAS S.p.A. 11

Med refining context

CRUDE

• The Med crude slate is forecast to become sweeter and lighter, an exception to world average

• The Med is becoming a net crude exporter with a positive pressure on prices

0

10

20

30

40

50

1995 2005

Diesel car registrations trend

(% of total registrations)

Mediterranean Europe: crude demand and supply

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006M

illio

n b

arr

els

/da

y

Black Sea Lybia BTC Algeria South Europe imports

The Med : the ideal position for complex and diesel oriented refineries

PRODUCTS

• Diesel demand becoming more difficult to satisfy in Europe: new car registrations show a continuous growth of diesel-powered cars at the expense of gasoline-fuelled vehicles

• Deficit of diesel growing by about 2.5 million tons per year while surplus of gasoline growing by about 1.5 million tons per year

September 2007 SARAS S.p.A. 12

Margins stability: influence of Power

213 220 220

349445 457

0

100

200

300

400

500

600

700

800

2005 2006 2007E(*)

Eur million

Power Generation Refining&Marketing

(*) Bloomberg consensus

6.59

2.69

2.74

2.80 2.80

3.48

3.543.61 3.61

7.316.07 6.26

12.24

13.5912.67 13.00

0

2

4

6

8

10

12

14

16

2005 2006 Q1/07 Q2/07

Eur cent/KWhour

Fuel (indexed to Brent) Capex+operations (indexed to inflation)Incentive (up to 2009) Italian average electricity price

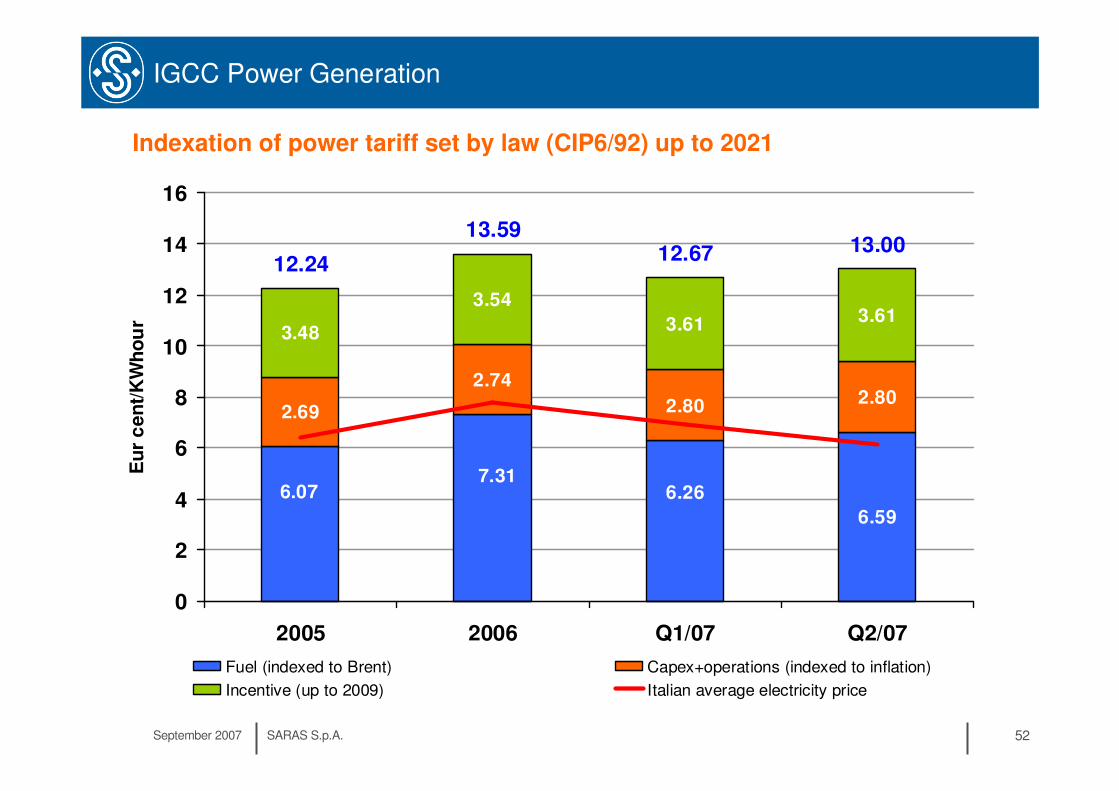

Power EBITDA essentially flat until 2021 Power tariff indexed to oil prices

• Power tariff set by law until 2021 and indexed to oil prices (CIP6/92 law)

• EBITDA substantially flat until 2021 due to the linearization procedure required by IFRS accounting rules

September 2007 SARAS S.p.A. 13

Saras is also a provider of refining services through processing contracts

A processing contract is an agreement to process third party crude oil under predetermined

conditions (i.e. product yields, processing fee, storage and delivery terms).

Saras’ processing contracts are grade specific and focused on certain families for which Saras

has specific need/interest.

Advantages of processing:

� Access to special crude oils otherwise

difficult to acquire

� Long term stability of supply

� Reduced working capital

� Stabilization of returns (equivalent to a put

option on the refining margins at fraction

of cost)

Approximate split of the value for third party runs

Profit Share

Optimization

Base Fee

Margins stability: Processing contracts

September 2007 SARAS S.p.A. 14

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

10,0

0,0 0,5 1,0 1,5 2,0 2,5 3,0 3,5 4,0 4,5 5,0

EMC benchmark, $/bl

Sara

s m

arg

in,

$/b

l

equivalent PUT Option

Processing

Saras' own crude

Efficient protection in case of margin downturn

Margins stability: Processing contracts

September 2007 SARAS S.p.A. 15

Growth strategy

High return and low risk organic growth strategy

Saras has a track record of “no regret” upgrading of the refinery

� lower investment risk (addition rather than step change)

� synergies with existing units, thanks to a long term view

CAPEX approx EUR 600 million in the period 2006-2009 (of which half is maintain capacity) with the following goals:

� Increase conversion capacity (+350,000 tons/year of diesel by end of 2007)

� additional runs thanks to increased time interval between major overhauls

� Increase capacity of running “unconventional” difficult crudes

Expected refining margin improvement of 1.8-2.4 $/bl by 2009 (1.2 $/bl already achieved in 2006/2007) with a positive impact on EBITDA of US$ 210-300 ml (US$ 120 million already achieved in 2006/2007)

After tax project IRR higher than 20%

September 2007 SARAS S.p.A. 16

Growth strategy

CAPEX forrefining

EUR 600 ml

2006 INCREASE CONVERSION CAPACITY

+ 200,000 TONS PER YEAR OF DIESEL + 0.5-0.7 $/bl

+ 150,000 TONS PER YEAR OF DIESEL (starting from Q3)

INCREASE REFINERY RUNS

+ 700,000 TONS

IMPROVE ENERGY EFFICIENCY

- 75,000 tons of C&L

HEAVY UP OF CRUDE SLATE

- 2 deg API

2007

2008

2009

Impact on refining margin

+ 0.5-0.6 $/bl

+ 0.6-0.8 $/bl

+ 0.2-0.3 $/bl

+ 1.8-2.4 $/bl

+ $ 50-70 ml

Impact on refining EBITDA

+ $ 60-80 ml

+ $ 20-30 ml

+ $ 210-300 ml

+ $ 50-60 ml

+ $ 30-50 ml

EUR

150 ml

EUR

150 ml

EUR

130 ml

EUR

170 ml

After tax project IRR > 20 %

TOTAL

organic growth strategy: further details

September 2007 SARAS S.p.A. 17

Growth strategy

Strong balance sheet sets the base of our external growth strategy

IN OUR CORE BUSINESSES

M&A opportunities in:

� Refining in Europe: assets and companies possibly available for sale are potential targets

� Marketing & Oil logistics: selective acquisitions to improve competitive position in specific areas (Spanish Med and Italy)

IN RELATED SECTORS

� WIND: pipeline of projects in the permitting phase

� BIODIESEL: 200,000 tons/year plant operational from 2008 (investment EUR 35 mil) to comply with new European regulations by 2010

� GAS EXPLORATION: committed about EUR 10 ml for seismic tests. Encouraging preliminary results, final results by end 2008.

BASIS FOR INVESTMENT: Stringent investment criteria:

• PROJECT IRR AFTER TAX 10-% 20% depending on business sector

• No growth for growth’s sake

• EPS accretive from day 1

September 2007 SARAS S.p.A. 18

Major maintenance schedule

• 2007 refinery maintenance schedule will affect refinery runs and also marginally conversion, no major maintenance in 2008

• Maintenance on IGCC power plant will have negligible impact on IFRS EBITDA since scheduled maintenance cycles and related production changes are included in the linearization procedure required by IFRS accounting principles

Impact of maintenance minimized by multi train configuration

IGCC

2 gasifier2 turbine

1 gasifier1 turbine

1 gasifier1 turbine

PLANT

4.2-4.64.2-4.61.0-1.11.1-1.20.9341.215Millions of

MWh

Estimated power production

1477USD millionAdditional loss on EBITDA due to lower conversion capacity

REFINERY

15.0-15.2110-111

14.3-14.5104-106

3.35-3.4524.5-25.2

3.70-3.8027.0-27.7

3.4124.9

3.8127.8

million tonsmillion bblEstimated runs

2 crude dist

1 vacuumMHC visbr

1 crude dist.

1 MHC1 crude dist.

1 vacuumvisbreaker

PLANT

2008expected

2007expected

Q4/07expected

Q3/07expected

Q2/07actual

Q1/07actual

••• Saras in a snapshotSaras in a snapshotSaras in a snapshot

• Market overview

••• Business segments descriptionBusiness segments descriptionBusiness segments description

••• FinancialsFinancialsFinancials

••• OtherOtherOther

September 2007 SARAS S.p.A. 20

Historical data

World Oil Demand and Refining Capacity

40.0

45.0

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

90.0

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

MM

bl

per

day

70%

75%

80%

85%

90%

95%

100%

Refinery utilization %

Oil demand

Distillation capacity

Refinery throughput

September 2007 SARAS S.p.A. 21

Historical data

US and Europe demand by productssource EMC World Refining Outlook, 2006

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

2002 2003 2004 2005 2006

Mil

lio

n b

/d

North America Gasoil EU Gasoil EU Gasoline North America Gasoline

USA and Europe: product demand pattern

September 2007 SARAS S.p.A. 22

Historical data

Crude prices

Source: Platt’s

0

10

20

30

40

50

60

70

80

Jan-

99Ju

l-99

Jan-

00

Jul-0

0Ja

n-01

Jul-0

1Ja

n-02

Jul-0

2Ja

n-03

Jul-0

3Ja

n-04

Jul-0

4Ja

n-05

Jul-0

5Ja

n-06

Jul-0

6Ja

n-07

Jul-0

7

$/bl

0

2

4

6

8

10

12

14

$/blBrent vs Arab Hvy (RHs axis) Brent dtd Urals Med Arabian Heavy Med

0

10

20

30

40

50

60

70

80

Jan-

99Ju

l-99

Jan-

00Ju

l-00

Jan-

01Ju

l-01

Jan-

02Ju

l-02

Jan-

03Ju

l-03

Jan-

04Ju

l-04

Jan-

05Ju

l-05

Jan-

06Ju

l-06

Jan-

07Ju

l-07

$/bl

02468101214161820

$/blWTI vs Maya (RHs axis) WTI Maya

September 2007 SARAS S.p.A. 23

Historical data

US market: gasoline crack spreads & stocks

Source: Platt’s & DOE

USA: Gasoline Crack spread vs WTI (Nymex)

0

5

10

15

20

25

30

35

40

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

Week n°

US

$/b

l

2007

2006

2001-2005 avg

2001-2005 range

USA: Gasoline stocks (demand fwd cover)

19

20

21

22

23

24

25

26

27

28

29

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

Week n°

day

s

2007

2006

2001-2005 avg

2001-2005 range

September 2007 SARAS S.p.A. 24

Historical data

US market: distillates crack spreads & stocks

Source: Platt’s & DOE

USA: Distillates stocks (demand fwd cover)

15

20

25

30

35

40

45

50

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

Week n°

day

s

2007 2006

2001-2005 avg

2001-2005 range

USA: Distillate Crack spread vs WTI (Nymex)

0

4

8

12

16

20

24

28

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

Week n°

US

$/b

l

2007

2006

2001-2005 avg

2001-2005 range

September 2007 SARAS S.p.A. 25

Historical data

US market: refinery utilization

Source: DOE

USA: Refinery utilization

65

70

75

80

85

90

95

100

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

Week n°

% u

tili

zati

on

2007

2006

2001-2005 avg

2001-2005 range

September 2007 SARAS S.p.A. 26

Historical data

Europe Med: Crude and Products prices

Source: Platt’s

0

10

20

30

40

50

60

70

80

Jan-

99Jul

-99

Jan-

00Ju

l-00

Jan-

01Ju

l-01

Jan-

02Ju

l-02

Jan-

03Ju

l-03

Jan-

04Ju

l-04

Jan-0

5Ju

l-05

Jan-

06Ju

l-06

Jan-

07Ju

l-07

Ura

ls M

ed

, $

/bl

0

100

200

300

400

500

600

700

800

Pro

du

cts

, $/t

on

Urals Med Gasoline ULSD Fuel Oil HS

September 2007 SARAS S.p.A. 27

Historical data

Med market: gasoline and diesel crack spreadsMonthly averages

Source: Platt’s

Med: Gasoline Crack spread vs Brent

0

2

4

6

8

10

12

14

16

18

20

22

24

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

US

$/b

l

2007

2006

2001-2005 avg

2001-2005 range

Med: Diesel Crack spread vs Brent

0

3

6

9

12

15

18

21

24

27

30

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

US

$/b

l

2007

2006

2001-2005 avg

2001-2005 range

September 2007 SARAS S.p.A. 28

Historical data

European market: refinery utilization

OECD Europe: Refinery utilization

75

77

79

81

83

85

87

89

91

93

95

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

% utilization

2007

2006

2001-2005 avg

2001-2005 range

September 2007 SARAS S.p.A. 29

Historical data

Europe Med: product differentials

Source: Platt’s

0

50

100

150

200

250

300

350

400

Jan-

99Ju

l-99

Jan-

00Ju

l-00

Jan-

01Ju

l-01

Jan-

02Ju

l-02

Jan-

03Ju

l-03

Jan-

04Ju

l-04

Jan-

05Ju

l-05

Jan-

06Ju

l-06

Jan-

07Ju

l-07

$/t

on

0

20

40

60

$/t

on

ULSD vs HSFO LSFO vs HSFO (rhs axis)

0

100

200

300

400

500

600

700

Jan-

99Ju

l-99

Jan-

00Ju

l-00

Jan-

01Ju

l-01

Jan-

02Ju

l-02

Jan-

03Ju

l-03

Jan-

04Ju

l-04

Jan-

05Ju

l-05

Jan-

06Ju

l-06

Jan-

07Ju

l-07

$/t

on

0

20

40

60

$/t

on

Delta (rhs axis) ULSD Gasoil 0,2%S

September 2007 SARAS S.p.A. 30

Oil Market Outlook

Middle Distillates demand forecast

source EMC World Refining Outlook, 2006

4.8 4.8 4.8 4.9

6.6 6.7 6.8 6.9

7.0 7.1 7.2 7.4

1.3 1.4 1.5 1.6

0

2

4

6

8

10

12

14

16

18

20

22

24

2007 2008 2009 2010

Mil

lio

n b

/d

North America Europe Asia Middle East

Gasoline demand forecast

source EMC World Refining Outlook, 2006

10.1 10.2 10.3 10.4

2.6 2.5 2.4 2.3

4.1 4.2 4.3 4.4

1.6 1.8 1.8 1.9

0

2

4

6

8

10

12

14

16

18

20

22

2007 2008 2009 2010M

illi

on

b/d

North America Europe Asia Middle East

2007-2010 Avg growth rate: 1.7% 2007-2010 Avg growth rate: 1.0%

Product demand forecast

September 2007 SARAS S.p.A. 31

Oil Market Outlook

Refining Industry: capital costs & investments

US PPI IRON&STEEL

1982=100

Source BLOOMBERG

Rising construction costs have made new projects unprofitable

September 2007 SARAS S.p.A. 32

Oil Market Outlook

Coker (20 kbd), Hydrocracker (40 kbd). Planned for 2010ELEFSIS (HELLENIC PETROLEUM)

Distillation (50 kbd). Planned for 2010SINES (GALP)

Sources: Purvin&Gertz, Emc (World Refining Outlook 2006)

Coker (20 kbd). Declared completion: 2009CASTELLON (BP)

Distillation (110 kbd), Hydrocracker (50 kbd), Coker (60 kbd).

Declared completion: 2009

CARTAGENA (REPSOL)

Hydrocracker (18 kbd). Declared completion: 2009TARANTO (ENI)

Coker (40 kbd). Declared completion: 2009BILBAO (REPSOL)

PROCESSING UNITS AND COMMENTSREFINERY

European Refining Industry: investments in distillation and conversion

September 2007 SARAS S.p.A. 33

Oil Market Outlook

ReutersPlans to build new refineries in Indonesia (with Aramco, KNPC, Petronas and Sinopec) cancelled as costs soared

Pertamina19 Feb ’07

Energy CompassExxonMobil and state Qatar Petroleum (QP) have shelved their Palm natural gas-to-liquids(GTL) project in the Mideast Gulf state. Qatari Energy Minister Abdullah al-Attiyah said high costs forced cancellation of the 154,000 b/d complex. Project inflation had pushed the price tag from an initial $7 billion in 2004 to more than $15 billion, according to industry sources.

ExxonMobil23 Feb ‘07

Kuwait’s Al-Zour refinery could be scrapped: rising costs could doom Kuwait’s proposed Al-Zour refinery, which may be scrapped after bids submitted in December were much higher than Kuwait National Petroleum Co. (KNPC) Envisaged

Oil refiner Sunoco Inc. is reviewing its expansion plans after the cost of a $300 million expansion project at its Philadelphia, Pennsylvania, refinery jumped by a third in less than a year

ConocoPhillips Corp. said it is re-evaluating the deep conversion expansion project at its 260,000 barrel per day refinery in Wilhelmshaven, Germany, due to shifting economics

NEWS

Al-Zour (Kuwait)

Sunoco

ConocoPhillips

REFINERY or COMPANY

Reuters2 Nov ‘06

Energy CompassDec ‘06

Reuters2 Nov ‘06

SOURCEDATE

Refining Industry: relevant news about investment plans

September 2007 SARAS S.p.A. 34

Oil Market Outlook

Energy CompassThe stalled 615,000 b/d project was relaunched with $12 billion budget and with new construction terms (cost-reimbursable basis). Planned statrup for 2011

Al-Zour (Kuwait)22 June ‘07

Middle east economic digest

State owned oil company, plans to build a 400,000 barrel-a-day refinery that will cost as much as $8 billion, The East Coast refinery will be built at Ras Tanura, Saudi Arabia, and is scheduled to be completed by January 2012 and will process Arabian heavy crude

Saudi Aramco15 June ‘07

Energy CompassRD Shell looks set to upgrade rather than expand its 110,000 b/d Tabangaorefinery; initial estimates for the upgrade have already risen above $300 ml from initial $100-200 ml

Philippines22 June ‘07

Energy CompassQatar agreed to build a 150,000 b/d refinery on Tunisia’s east cost. A joint committee will study technical specifications for the $2 billion plant over the next six months, with a start-up targeted for 2011

Qatar Petroleum22 June ‘07

Energy CompassFujairah refinery: Abu Dhabi’s International Petroleum Investment Co. may scale down a planned refinery in the UAE amid concerns that partner ConocoPhillips will pull out because of soaring costs. A pre-feasibility study for the Fujairah refinery came in recently with a cost of around $11 billion, up from original estimates of $5 billion- $6 billion

ConocoPhillipsApr’ 07

BloombergAngola’s state owned company is seeking to cut the cost of a new 200,000 b/d refinery, after the decision to end talks with Sinopec for a $3.7 billion project

Sonangol6 Mar ’07

NEWSREFINERY or COMPANY

SOURCEDATE

Refining Industry: relevant news about investment plans

September 2007 SARAS S.p.A. 35

Oil Market Outlook

BloombergTechnip Awarded a Front-End Engineering Design Contract for a 250,000 bbl/day Grassroots Refinery in Qatar + a crude oil pipeline from the Al Shaheenfield to Messaieed (90km offshore and 110km onshore), as well as other required import/export facilities. The facilities are scheduled to be operational by the end of 2011.

Qatar petroleum/ Techinp

27 Aug ‘07

ReutersTurkish fuel retailer Petrol Ofisi said it would invest $4.5 billion in building a refinery in the Mediterranean port city of Ceyhan for which it received permission late last month

Petrol Ofisi / Ceyhan4 Lug ’07

NEWSREFINERY or COMPANY

SOURCEDATE

Refining Industry: relevant news about investment plans

••• Saras in a snapshotSaras in a snapshotSaras in a snapshot

••• Market overviewMarket overviewMarket overview

• Business segments description

••• FinancialsFinancialsFinancials

••• OtherOtherOther

September 2007 SARAS S.p.A. 37

Refining

2,623,2508.7TOTAL with Gasification

180,00015.012,000BTX Plant

85,0005.017,000Semi-rigenerative Reformer

2,383,2507.9TOTAL COMPLEXITY

9.6

12.0

1.0

10.0

10.0

2.5

6.0

5.0

6.0

2.75

2.0

1.0

Nelson Complexity

Factor

240,00020,000Gasification

62,000

6,000

8,000

107,000

105,000

29,000

86,000

41,000

105,000

300,000

Capacity (barrels per

calendar day)

60,000Oxygenates (TAME)

62,000Hydrogen/PSA (MMcfd)

267,500Hydrotreating

80,000Alkylation

145,000Cat Reforming (CCR)

2,888,250TOTAL with Gasification & PetChem

630,000Distillate Hydrocracking

516,000Distillate Cracking (FCC)

112,750Visbreaking

210,000Vacuum Distillation

300,000Atmospheric Distillation

Complexity barrels

Process Unit

Sarroch refinery: structure and Nelson complexity index

September 2007 SARAS S.p.A. 38

Refining

Supersites and non-supersites ranking (source: WoodMackenzie)

All Data from WoodMac Downstream Online ( data available as of February 2007):

(*) Note for Saras: reported complexity by WoodMac is 7.9 but does not include full ownership of IGCC and is based on 313 kbcd capacity

We are restating Saras complexity (under WoodMac methodology) considering 100% IGCC ownership and a capacity of 300 kbcd

CAPACITIES (Mton/y)

8.6 8.6 8.47.9

7.0 6.9

6.1

9.28.7

8.3 8.2

6.3

Kar

lsru

he

(Sh

, Ex

x, C

on, B

P)

Sar

roch

(S

AR

AS

)

An

twer

p (

TOT

AL)

Pri

olo

(E

RG

)

Plo

ck (

PK

N)

Gel

sen

kirc

hen

(B

P)

Per

nis

(She

l l)

Mo

torO

il H

ella

s

Asp

ropy

rgo

s (H

EP)

Sza

zhal

om

batt

a (M

OL)

Po

rvo

o (

NE

ST

E)

Sch

wec

hat

(O

MV

)

WoodMackenzie: complexity indexes for the major European refineries (*)

14,9 15,0 17,4 14,6 8,016,9 12,6 6,720,7 5,3 10,0

SUPERSITES

9,4

NON SUPERSITES

September 2007 SARAS S.p.A. 39

Refining

24,122,800

375,500

5,541,490

4,365,260

713,900

5,012,500

8,114,100

barrels

3,835,100162TOTAL

59,700

881,000

694,000

113,500

796,900

1,290,000

Cubic metres

37

31

35

11

35

13

Nr. of tanks

FUEL OIL

LPG AND PENTANES

GASOIL

KEROSENE

GASOLINE

CRUDE OIL

• 11 BERTHS • 300,000 SDWT VESSELS (MAX)

Sarroch refinery: storage and marine terminal

September 2007 SARAS S.p.A. 40

Refining

Sarroch refinery: ranking by capacity

European Refineries

0

50

100

150

200

250

300

350

400

450

Ca

pa

cit

y,

kb

d

Average = 140 kbd

ERG coastal

SARAS

HEP Aspropyrgos

NESTE Porvoo

PKN Plock

MotorOilPetroplus Ingolstadt

September 2007 SARAS S.p.A. 41

Refining

Sarroch refinery: ranking by complexity

Nelson Index for European refineries with at least 140 kbd capacity (i.e. European average)

0

2

4

6

8

10

12

14

16

18

20

Ne

lso

n C

om

ple

xit

y In

de

x

ERG coastal

SARAS

HEP AspropyrgosNESTE Porvoo

PKN Plock

Petroplus Coryton

September 2007 SARAS S.p.A. 42

Refining

234,400

48,000

84,000

16,400

86,000

FCC Equivalent

barrels

240

80

40

100

FCC Equivalent

Factor %

16.020,000Gasification

105,000

41,000

86,000

Capacity (barrels per

calendar day)

78.1TOTAL

28.0Distillate Hydrocracking

5.5Visbreaking

28.6FCC

FCC Equivalent % on Distillation

Process Unit

Sarroch refinery: FCC equivalent index

Source: WoodMackenzie

September 2007 SARAS S.p.A. 43

Refining

Sarroch refinery: ranking by FCC equivalent conversion installed

Source: WoodMackenzie

Residue conversion capacity of European refineries

0

20

40

60

80

100

120

140

160

180

200

220

240

FC

C e

qu

ivale

nt

ba

rre

ls, k

bd

ERG coastal

SARAS

HEP Aspropyrgos

NESTE Porvoo

PKN Plock

MotorOil

Petroplus Ingolstadt

Conoco Killingholme

Petroplus Coryton

September 2007 SARAS S.p.A. 44

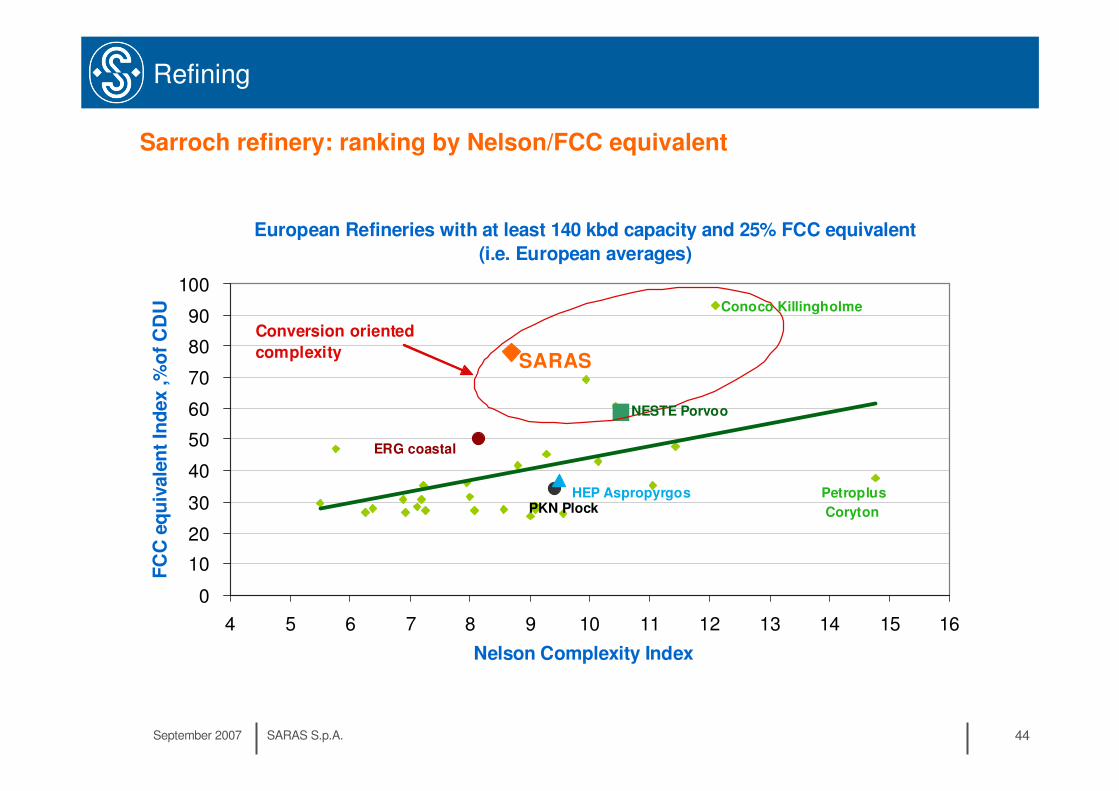

Refining

Sarroch refinery: ranking by Nelson/FCC equivalent

European Refineries with at least 140 kbd capacity and 25% FCC equivalent

(i.e. European averages)

0

10

20

30

40

50

60

70

80

90

100

4 5 6 7 8 9 10 11 12 13 14 15 16

Nelson Complexity Index

FC

C e

qu

ivale

nt

Ind

ex ,%

of

CD

U

Conversion oriented

complexity

ERG coastal

SARAS

HEP Aspropyrgos

NESTE Porvoo

PKN Plock

Conoco Killingholme

Petroplus

Coryton

September 2007 SARAS S.p.A. 45

1

3 CDU

(Crude DistillationUnit)

2 VDU

(VacuumDistillationUnit)

2 MHC

(MildHydrocracking)

1 FCC

(Fluid CatalyticCracker)

HeavydistillatesT1

T2

T3

V1

V2

Heavyresidue

MHC1

MHC2

FCC

2 REFORMERCCR1

CCR2(Polimeri)

TAR

1 VSB

(Visbreaker)VSB

3 GASIFIERS

G1G2

G3SYNGAS

3 GAS-STEAM TURBINES

POWER

1 ETHERIFICATION

1 ALKYLATION

5 DESULPHURIZATION UNITS

DIESEL

GASOLINE

Hydrogen

Hyd

rog

en

CRUDE OIL

Athmosferic and Vacuumdistillation

Conversion units Desulphurization & finishing

IGCC Power plant

Refining

Sarroch refinery: structure

September 2007 SARAS S.p.A. 46

Refining

Sarroch refinery reference capacity is 300,000 barrels per calendar day

Sarroch refinery: runs

14.0 14.2 14.0 14.4 14.3 14.515.1

14.5

106 106102 104 102

105 104110

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2002 2003 2004 2005 2006 2007E 2008E 2009E

million tons

80

85

90

95

100

105

110

115million bbl

Processing for third parties Own crude Total runs tot

September 2007 SARAS S.p.A. 47

Refining

Sarroch refinery: crude oil slate by grade and by origin (2006 data)

-1 0 1 2 3

%S

15

20

25

30

35

40

45

°AP

I

Brent

Ural

45 million

Barrel/year

28 million

Barrel/year

24 million

Barrel/year

Saras average

Light extra sweet

Light sweet

Medium Sour

Medium Sweet

Heavy Sour

-1 0 1 2 3

%S

15

20

25

30

35

40

45

°AP

I

Brent

Ural

45 million

Barrel/year

28 million

Barrel/year

24 million

Barrel/year

Saras average

Light extra sweet

Light sweet

Medium Sour

Medium Sweet

Heavy Sour

North Sea 20%

Middle East

13% FSU 6%

North Africa

61%

September 2007 SARAS S.p.A. 48

2006 data

Refining

Sarroch refinery: product yields

H1/07 data

C&L

6.1%LPG

2.3%

Naphtha&

Gasoline

27.8%

Middle

Distillates

52.0%

Fuel Oil&Other

4.2%

IGCC feed

7.6%

C&L 5.9%

Naphtha &

Gasoline

27.3%

LPG 2.2 %

Middle

Distillates

(mainly diesel)

51.4%

IGCC feed

8.1%

Fuel Oil&Other

5.1%

September 2007 SARAS S.p.A. 49

Refining

2.62.4 2.4

0.0

0.3

0.5

0.8

1.0

1.3

1.5

1.8

2.0

2.3

2.5

2.8

3.0

3.3

3.5

2005

2006

2007

2008

2009

2010

2011

2012

allocated emissions

Million tons

Sarroch refinery Co2 emissions

September 2007 SARAS S.p.A. 50

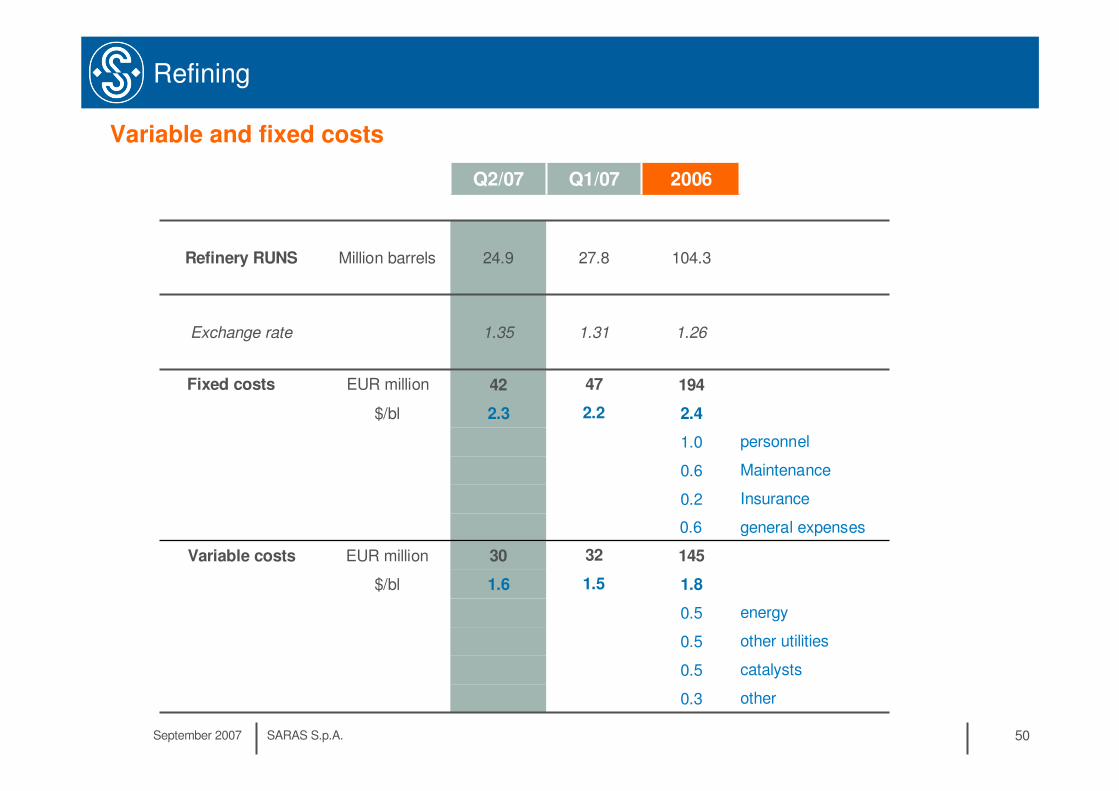

Refining

1.6

30

2.3

42

1.35

24.9

Q2/07

energy0.5

other utilities0.5

catalysts0.5

14532EUR millionVariable costs

0.3

1.8

0.6

0.2

0.6

1.0

2.4

194

1.26

104.3

2006

other

general expenses

Insurance

Maintenance

personnel

47EUR millionFixed costs

1.5$/bl

2.2$/bl

Million barrels

1.31Exchange rate

27.8

Q1/07

Refinery RUNS

Variable and fixed costs

September 2007 SARAS S.p.A. 51

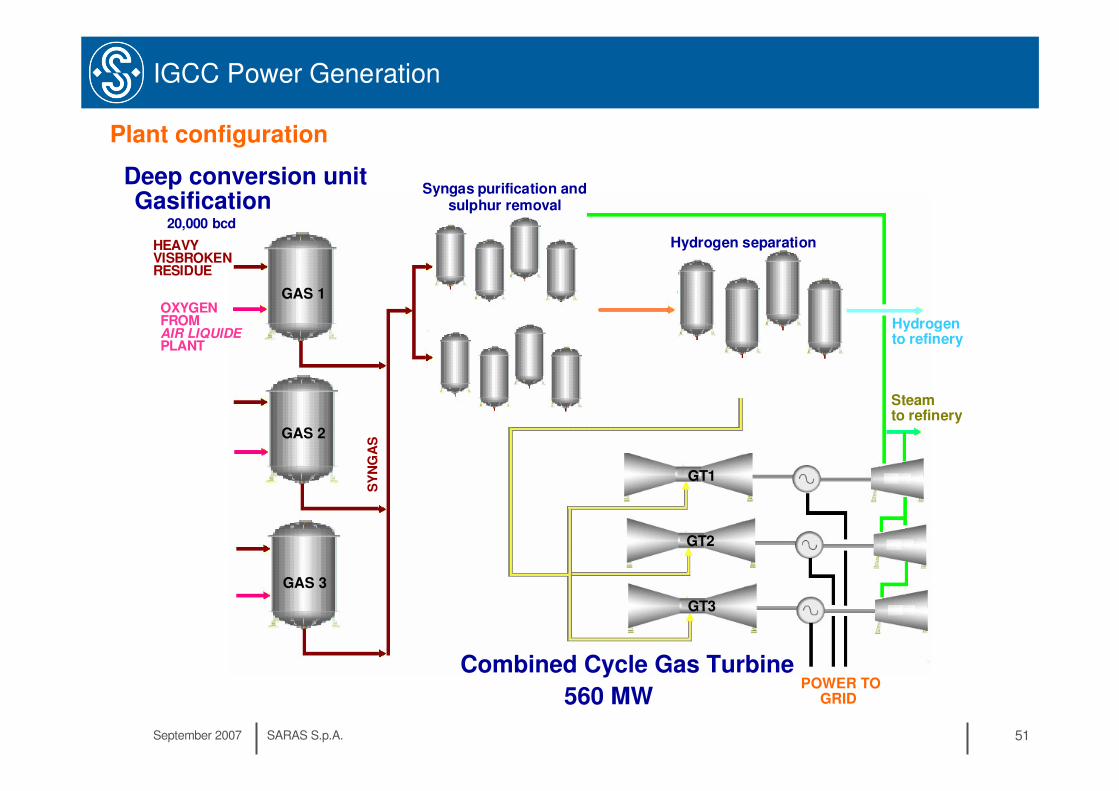

IGCC Power Generation

Plant configuration

HEAVY VISBROKEN RESIDUE

OXYGEN FROMAIR LIQUIDEPLANT

Hydrogento refinery

Deep conversion unitGasification

20,000 bcd

Combined Cycle Gas Turbine

560 MW

SY

NG

AS

Steamto refinery

GAS 1

POWER TO GRID

GT1

GAS 2

GAS 3

GT3

GT2

Syngas purification and sulphur removal

Hydrogen separation

September 2007 SARAS S.p.A. 52

IGCC Power Generation

6.59

2.69

2.74

2.80 2.80

3.48

3.54

3.61 3.61

7.316.07 6.26

12.24

13.5912.67 13.00

0

2

4

6

8

10

12

14

16

2005 2006 Q1/07 Q2/07

Eu

r c

en

t/K

Wh

ou

r

Fuel (indexed to Brent) Capex+operations (indexed to inflation)

Incentive (up to 2009) Italian average electricity price

Indexation of power tariff set by law (CIP6/92) up to 2021

September 2007 SARAS S.p.A. 53

IGCC Power Generation

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

2001 2002 2003 2004 2005 2006

Gasific

ation feed '000,0

00 tons

2.1

2.4

2.7

3.0

3.3

3.6

3.9

4.2

4.5

Ele

ctric

ity p

roduction, TW

h

Tar Gasoil Electricity

Production & feedstock consumptions

September 2007 SARAS S.p.A. 54

IGCC Power Generation

Million tons

CO2 emissions

3.7 3.9 3.9

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2005

2006

2007

2008

2009

2010

2011

2012

allocatedemissions

• Article 7bis of CIP6/92 law state: “the sale price of electricity will be updated in case of changes of regulations implying higher or additional costs for the producers”

• The guidelines of Italian energy authority, issued on 15th November 2006, confirm applicability of article 7bis to the CO2 related costs and also define reimbursement mechanism.

• Final resolution from the energy authority expected soon

September 2007 SARAS S.p.A. 55

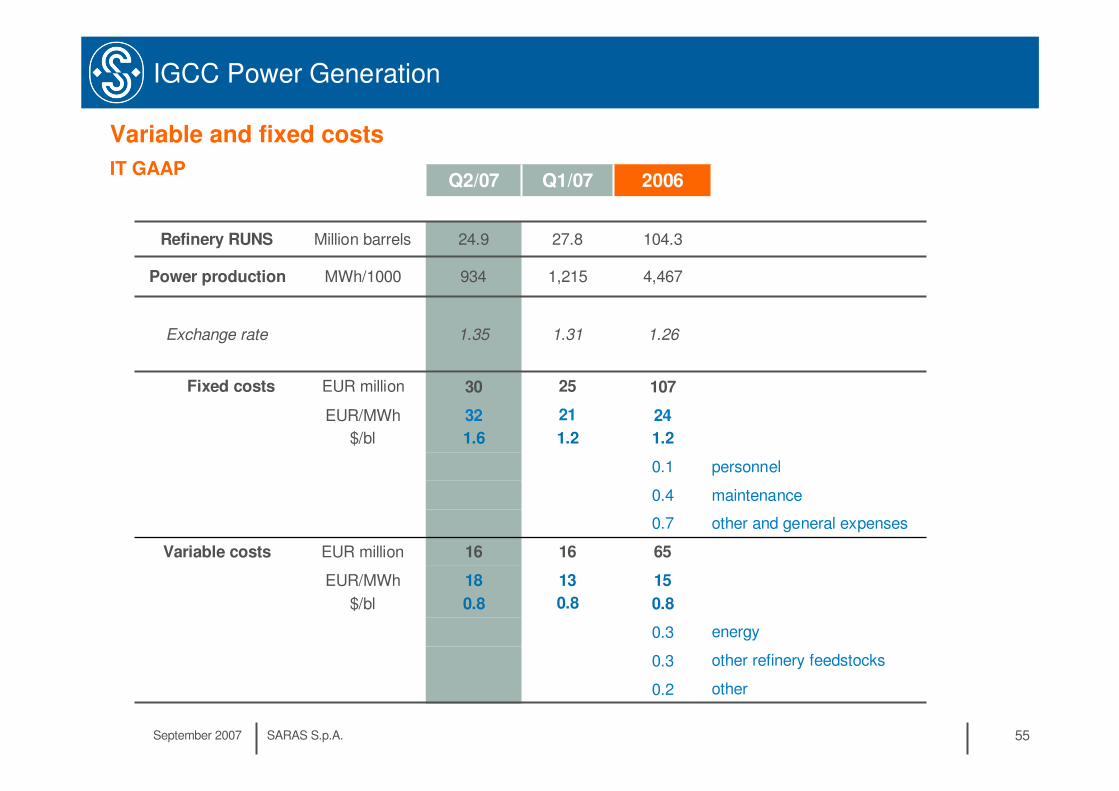

IGCC Power Generation

4,4671,215934MWh/1000Power production

energy0.3

other refinery feedstocks0.3

651616EUR millionVariable costs

0.2

15

0.8

0.7

0.4

0.1

24

1.2

107

1.26

104.3

2006

other

other and general expenses

maintenance

personnel

2530EUR millionFixed costs

13

0.8

18

0.8

EUR/MWh

$/bl

21

1.2

32

1.6

EUR/MWh

$/bl

Million barrels

1.311.35Exchange rate

24.9

Q2/07

27.8Refinery RUNS

Q1/07

Variable and fixed costs

IT GAAP

September 2007 SARAS S.p.A. 56

IGCC Power Generation

40.5

(14.5)

55.0

(32.0)

(18.0)

(38.7)

13.7

36.1

93.9

130.0

Q2/07

35.4

100.5

36.1

90.6

€ /MWh

€ /MWh

Incentive (up to 2009)

Other tariff components

13.711.7€ /MWhREVENUES FROM UTILITIES

(38.1)(33.9)€ /MWhFEEDSTOCKS FOR GASIFICATION

135.9126.7€/MWhREVENUES FROM POWER

(14.6)(13.0)€ /MWhVARIABLE COSTS

(24.0)(21.0)€ /MWhFIXED COSTS

73.070.5€ /MWhEBITDA

(12.1)(11.0)€ /MWhD&A

60.959.5€ /MWhEBIT

Q1/07 2006

Revenues and costs per Megawatt-hour (IT GAAP)

September 2007 SARAS S.p.A. 57

Marketing

Logistic of wholesale/retail operations in Italy and Spain

Owned depot

Third party depot

934

255

680

Q1/07

3,219

1,013

2,206

2006

803

263

540

Q1/06

771

236

535

Q2/06

2,957

1,037

1,920

2005

775

238

537

Q3/06

870

276

594

Q4/06

268ITALY

920TOTAL

652SPAIN

Q2/07Sales (thousand

tons)

37 service stations

other inland depot

wholesale market

share in Italy: ~5.5%

wholesale market share

in Spain: ~ 3.5%

Arcola Petrolifera

2 time chartered product vessels

September 2007 SARAS S.p.A. 58

Marketing

2 owned depots

Cartagena (Spain): 112,000 cubic meters

Arcola (Italy) : 200,000 cubic meters

A retail network of 37 high throughput service stations (abt 3.5 million litre per year) located in the Spanish med area

September 2007 SARAS S.p.A. 59

Wind

Wind in Italy

Sardinia347 MW

North Italy44 MW

Campania and Basilicata574 MW

Puglia, Abruzzo and Molise695 MW

Sicily451 MW

Capacity installed end 2006

Wind in Europe

3,136DENMARK

2,123ITALY

MW

48,416

11,615

20,622

SPAIN

TOTAL EU

GERMANY

Capacity installed end 2006

• Electric energy created by renewable energy plants are entitled to receive GC, related to the KWh produced, for the first 12 years of production since their last inspection.

• Said GC are issued by the Administrator with reference to the previous year´s effective production or in accordance with the foreseeable quantity of energy that will be produced the following year by the requesting operator.

• Specifically, all operators of the field, whether producers or traders, must possess and subsequently file a certain number of GC equal to 2% of the energy used/produced in the course of the previous year. GC are securities representing renewable energy whose purchase and filing with the Administrator must occur to avoid unlawful use of the energy by the operator. Also noteworthy is the

fact that the Administrator issues the GC and is then required to annul them, thus entitling the operators to comply with the above indicated Green Portfolio requirements.

• GC may be traded independently from the related renewable energy. Further, there is no legal

limitation on the possibility to freely and repeatedly trade GC before they are annulled by the Administrator. The only limit is given by the need of using certificates representing the past year´́́́s production. By way of example, if a GC is issued at the beginning of the year 2001, referring to energy that will be produced in the year 2002, its annulment must occur by March 31, 2003. Therefore,

throughout the entire period running from the date of issuance to the date of annulment, operators are entitled to trade GC, privately or within the Energy Stock Market, without any legal limitations whatsoever, except to the possibility of exporting the certificates abroad. In particular, as briefly mentioned above, GC do not necessarily have to be traded in connection with the energy they

represent, as long as the relative sale takes place in Italy. Contrarily, GC can be sold abroad only in conjunction with the sale of energy.

Green Certificates

September 2007 SARAS S.p.A. 60

Wind

Ulassai wind farm

Ulassai wind farm

Sardinia

• area of 6,500 acres

• 84 MW (42 Vestas aero generators x 2MW)

• upgradeable to 96 MW

• production of approx 150,000 MWh per year

• investment of EUR 100 million

• joint venture with Backcock&Brown (Saras 70%)

• project finance (equity 15%)

• equity IRR above 50%Sardeolica

11.9

7.6

54,910

Q1/07

12.1

7.4

157,292

2006

10.9

7.5

52,902

Q1/06

12.1

6.7

31,624

Q2/06

12.1

8.1

33,058

Q3/06

12.1

8.2

39,708

Q4/06

9.9Power tariff(€cent/MWh)

11.9Green certificates(€cent/MWh)

31,789Electricityproduction (MWh)

Q2/07

••• Saras in a snapshotSaras in a snapshotSaras in a snapshot

••• Market overviewMarket overviewMarket overview

••• Business segments descriptionBusiness segments descriptionBusiness segments description

• Financials

••• OtherOtherOther

September 2007 SARAS S.p.A. 62

Financial targets

17% 17%

0%

5%

10%

15%

20%

25%

2005 2006 2007

0.50

0.88

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2005 2006

ROACE – target between 10% to 15%

over the cycleNFP/EBITDA – less than 3.5

59%

0%

20%

40%

60%

80%

2005 2006 2007

Leverage - long term target 50%

18%

39%

0%

20%

40%

60%

2005 2006

Payout ratio - between 40% to 60%

ROACE: return on average capital employed after tax

Leverage: Net debt /(net debt + equity)

Payout: calculated on adjusted net income

September 2007 SARAS S.p.A. 63

48% 48% 46%39%

45%

20%13%

18%

9%

-1%-10%

0%

10%

20%

30%

40%

50%

60%

Q1/0

5Q

2/05

Q3/0

5Q

4/05

Q1/0

6Q

2/06

Q3/0

6Q

4/06

Q1/0

7Q

2/07

0.881.01

0.49

0.32

0.50

0.23

-0.02-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Q4/

05

Q1/

06

Q2/

06

Q3/

06

Q4/

06

Q1/0

7

Q2/

07

17% 18% 18% 18% 17% 18%21%

0%

5%

10%

15%

20%

25%

30%

2005

Q1/

06

Q2/

06

Q3/

06

2006

Q1/

07

Q2/

07

29%32%

25% 24%22% 23% 23%

0%

5%

10%

15%

20%

25%

30%

35%

2005

Q1/

06

Q2/

06

Q3/

06

2006

Q1/

07

Q2/

07

1,2 : quarterly figures are 1 year rolling

leverage , % NFP/EBITDA, %

ROAE2 , %ROACE1, %

Key Ratios

September 2007 SARAS S.p.A. 64

Group Financials

115.0

-0.533.44.2

77.9

105.3

40.0

0.620.31.3

17.8

155.00.1

53.75.5

95.7

145.3

Q1/07

225.9363.458.744.0161.898.9612.8EBIT

39.9162.843.740.539.439.2170.9Depreciation&amort.

159.4404.895.2120.085.2104.4482.7Comparable EBIT

-1.6-3.7-0.4-0.5-0.5-2.3-7.7Other activities

199.3567.5138.9160.5124.5143.6653.6Comparable EBITDA

17.668.418.317.217.815.173.3Refining1.23.42.20.60.30.31.2Marketing

20.588.322.122.122.022.193.0Power0.52.61.10.6-0.81.73.4Other activities

-1.1-1.10.70.1-1.3-0.6-4.3Other activities

123.2255.462.581.349.062.6348.2Refining6.021.43.28.76.43.121.8Marketing

31.8131.729.930.530.341.0120.4Power

213.423.0

421.5

783.7

2005

63.13.4

77.7

138.1

Q1/06

52.3220.052.052.652.3Power

140.8323.880.898.566.8Refining

24.8

526.2

2006

6.7

201.2

Q2/06

7.25.49.3Marketing

265.7102.484.5EBITDA

Q2/07Q4/06Q3/06

Comparable EBITDA : calculated evaluating inventories at LIFO

Comparable EBIT equal to comparable EBITDA less depreciation&amortization

Income statement (1) EUR million

September 2007 SARAS S.p.A. 65

Group Financials

20.1

14.0

0.0

6.1

0.07

71.020.1

50.9

40.9%

-33.5

84.40.0

2.6

-23.5-22.0

3.6-5.1

115.0

105.3

Q1/07

-46.533.730.335.4-35.53.5-75.9Adjustments

0.0-22.2-9.30.0-12.90.00.0Non recurring expenses

-3.514.76.60.08.10.00.0Non recurring items net of taxes

-4.3-6.90.8-12.34.50.15.7Change of derivatives fair value net of taxes

Detail of adjustments to net income-38.725.922.947.7-48.13.5-81.6(Invent. at LIFO- inv. at LIFO) net of taxes

1.36.52.50.51.12.4-0.4Equity interest

218.0338.257.856.4123.5100.5518.5Profit before taxes-82.1-130.1-22.1-22.6-47.7-37.7-212.1Taxes37.9%39.2%40.0%40.4%39.0%38.4%40.9%Tax rate

136.0208.135.733.875.862.8306.4Net income

89.5241.866.069.240.366.3230.5Adjusted net income

0.090.260.070.070.050.070.26Adjusted EPS

+5.910.1-2.619.5-6.7-0.1-8.6derivatives fair value

-3.2-22.0-0.8-4.6-9.3-7.3-25.3Interest expenses-11.82.19.3-3.2-10.66.6-60.0derivatives gains/losses

-9.2-9.95.911.7-26.6-0.8-93.9Net Financial expenses

159.4404.895.2120.085.2104.4482.7Comparable EBIT

225.9363.458.744.0161.898.9612.8EBIT

-46.533.730.335.4-35.53.5-75.9TOTAL adjustments

2005 Q1/06 2006Q2/06 Q2/07Q4/06Q3/06

Income statement (2) EUR million

September 2007 SARAS S.p.A. 66

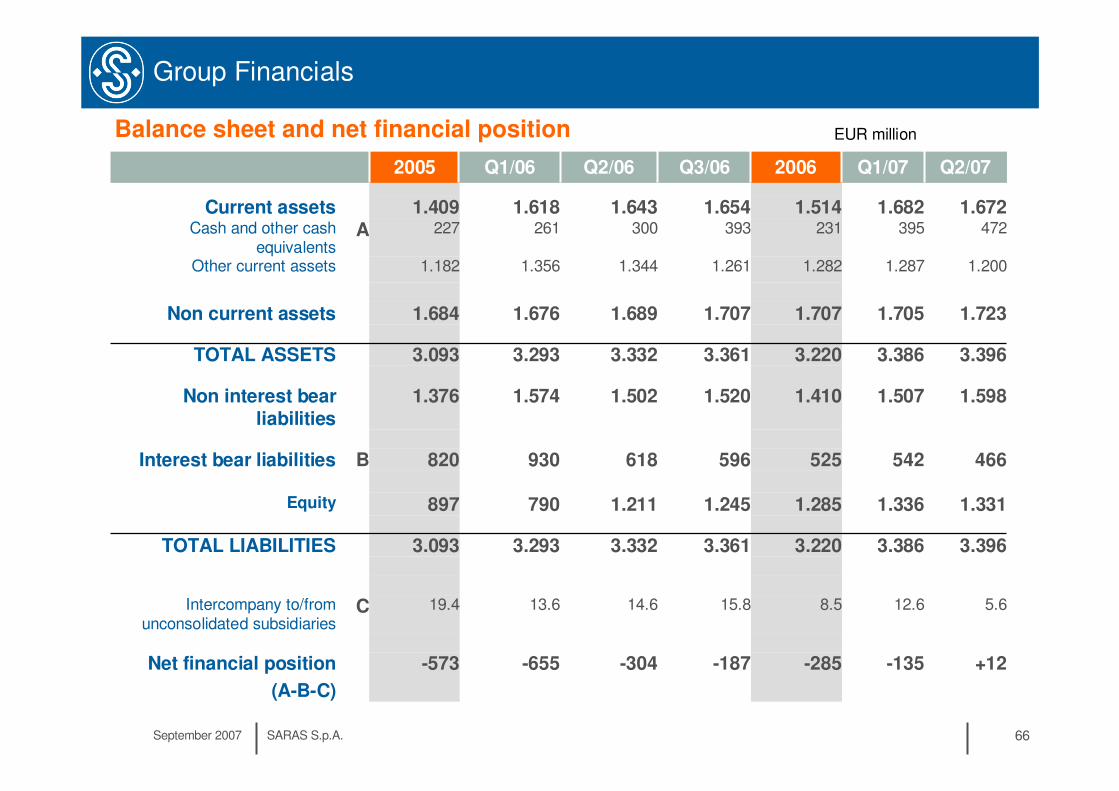

Group Financials

-135

12.6

3.386

1.336

542

1.507

3.386

1.705

1.287

395

1.682

Q1/07

C

B

A

466525596618930820Interest bear liabilities

1.5981.4101.5201.5021.5741.376Non interest bear liabilities

1.3311.2851.2451.211790897Equity

3.3963.2203.3613.3323.2933.093TOTAL LIABILITIES

5.68.515.814.613.619.4Intercompany to/from unconsolidated subsidiaries

+12-285-187-304-655-573Net financial position

(A-B-C)

3.3963.2203.3613.3323.2933.093TOTAL ASSETS

1.7231.7071.7071.6891.6761.684Non current assets

1.2001.2821.2611.3441.3561.182Other current assets

1.6721.5141.6541.6431.6181.409Current assets472231393300261227Cash and other cash

equivalents

2005 Q1/06 2006Q2/06 Q2/07Q3/06

Balance sheet and net financial position EUR million

September 2007 SARAS S.p.A. 67

Group Financials

-135

149

00

0

0-36

-36

78

185

-285

Q1/07

-57-133-41-19-46-27-86in tangible&intangible. assets

-285

-98

00

0

0

-41

-151

-57

-187

Q4/06

-143-17000-170-140dividends

-1431720342-170-140CF FROM FINANCING0342034200capital increase

147289117351-81152TOTAL CASHFLOW

+12-285-187-304-655-573Final net financial position

0-28-28000acquisitions

-57-161-47-46-27-86CF FROM INVESTMENTS

34727716454116379CF FROM OPERATIONS54-21671-104-32-320of which working capital

-135-573-304-655-573-726Initial net financial position

2005 Q1/06 2006Q2/06 Q2/07Q3/06

Cashflow EUR million

Capex by business segment EUR million

35.50.6

0.34.5

30.2

Q1/07

57.40.6

5.50.8

50.5

Q2/07

210011OTHER ACTIVITIES41

116

23

Q4/06

162211POWER GENERATION

13319462786TOTAL CAPEX

10815442670REFINING

710014MARKETING

2005 Q1/06 2006Q2/06 Q3/06

September 2007 SARAS S.p.A. 68

Segment Financials

Refining

40%36%48%46%47%55%46%Of which for third parties

5.43.02.81.62.84.71.9EMC benchmark

3.4153.80914.2863.8953.7642.9183.709Thousand tons

24.927.8104.328.427.521.327.1Million barrels

274309286309299234301Barrels/day

REFINERY RUNS

9.96.76.25.66.57.75.6Saras refining margin

513010823164423CAPEX

123.2

179.6

140.8

197.2

Q2/07

17.8

70.7

95.7

88.5

Q1/07

68.4

223.8

323.8

292.2

2006

18.317.217.815.1Comparable EBIT

36.813.8120.053.2EBIT

80.898.566.877.7Comparable EBITDA

55.131.0137.868.3EBITDA

Q4/06Q3/06Q2/06Q1/06EUR million

September 2007 SARAS S.p.A. 69

Segment Financials

Power generation

$/bl

€cent/Kwh

Mwh/1000

51.385.6323.868.888.786.879.5EBITDA ITALIAN GAAP37.972.4270.055.275.273.366.3EBIT ITALIAN GAAP

13.0012.6713.5913.4912.4613.7113.31POWER TARIFF

4.43.73.93.63.44.54.0POWER IGCC MARGIN

9341,2154,4679991,1471,1361,155ELECTRICITY PRODUCTION

64129120CAPEX

22.6

31.8

52.3

Q2/07

43.4

33.4

53.7

Q1/07

160.9

131.7

220.0

2006

32.445.244.039.3NET INCOME IT GAAP

29.930.530.341.0EBIT

52.052.652.363.1EBITDA

Q4/06Q3/06Q2/06Q1/06EUR million

September 2007 SARAS S.p.A. 70

Segment Financials

Marketing

2682551,013276238236263ITALY

6526802,204594537535540SPAIN

9209343,217870775771803TOTAL

SALES (THOUSAND TONS)

1098100CAPEX

6.0

16.1

7.2

17.3

Q2/07

4.2

1.7

5.5

3.0

Q1/07

21.5

11.7

24.8

15.1

2006

3.28.76.43.1Comparable EBIT

-7.60.212.17.0EBIT

5.49.36.73.4Comparable EBITDA

-5.40.812.47.3EBITDA

Q4/06Q3/06Q2/06Q1/06EUR million

September 2007 SARAS S.p.A. 71

Segment Financials

Other activities

1011001CAPEX

-1.6

-1.0

Q2/07

-0.5

0.1

Q1/07

-3.7

-1.1

2006

-0.4-0.5-0.5-2.3EBIT

0.70.1-1.3-0.6EBITDA

Q4/06Q3/06Q2/06Q1/06EUR million

Wind

Equity company – Saras share is 70%

€cent/Kwh

€cent/Kwh

Mwh

2.03.88.93.20.81.63.4NET INCOME

1.43.48.11.71.41.63.4Adjusted NET INCOME

9.97.67.48.28.16.77.4POWER TARIFF

11.911.912.112.112.112.112.1GREEN CERTIFICATES

31,78954,910157,29039,70833,05831,62452,902ELECTRICITY PRODUCTION

3.6

5.9

Q2/07

7.1

9.4

Q1/07

17.4

25.7

2006

5.63.32.85.8EBIT

7.95.44.77.7EBITDA

Q4/06Q3/06Q2/06Q1/06EUR million

September 2007 SARAS S.p.A. 72

Sensitivities

Refining

• 1 $/bbl of change on our refining margin affect refining annual EBITDA by roughly 100 USD million or 77 EUR million at 1.30

• +10 $/ton ULSD-HSFO, at constant overall margins, are +5 EUR million worth

• 0.05 change in the EUR/USD exchange rate affect annual refining EBITDA by roughly 25 EUR million (assuming a Saras refining margin of 7$/bl)

Power Generation

• +/- 10% of change of crude/product prices affect annual IT GAAP EBITDA by abt +/- 6.6%

• EUR/USD exchange rate from 1.30 to 1.20 affect annual IT GAAP EBITDA by roughly +10 EUR million

September 2007 SARAS S.p.A. 73

Market multiples

EV/EBITDA – PE – EV per complexity barrel

EV/EBITDA 2008source: Saras elaboration on Bloomberg data

5.05.5 5.8

6.6 6.6 6.97.8

8.7

4.7

0

2

4

6

8

10

12

14

LOTO

S

ERG

PKN

SAR

AS

PPHN

OIL

REF

NES

TE

HEP

MO

H

media= 6.4

PE 2008

source: Bloomberg

7.9

12.612.211.811.8

10.410.39.7

9.0

0

2

4

6

8

10

12

14

16

PPHN

OIL

RE

F

LOTO

S

NES

TE

PKN

MO

H

ERG

SARA

S

HEP

media= 10.6

EV per complexity barrel

984 1,036

1,391 1,442

1,702

1,938 1,922

2,1832,296

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

LOTO

S

ER

G

OIL

REF

SA

RA

S

PPH

N

PK

N

HE

P

NE

STE

MO

H

average= 1,656$

EV per complexity barrel

recent transactions

678

850

1,053

1,333

1,518

1,843 1,818

2,100

2,513

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

Coryton (UK)

2 Shell Ref (FR)

Wilmington (US)

Ashdod (ISR)

Mazeiku (LIT)

Houston (US)

Wilhelmshaven (GER)IES

TAMOIL

Last update 10th September 2007

September 2007 SARAS S.p.A. 74

Analyst estimates

Analyst recommendations and 2007 / 2008 / 2009 estimates (Bloomberg)

EBITDA Low Hi Mean

2007 659 695 6772008 597 784 717

2009 559 783 702

EBIT Low Hi Mean2007 374 534 486

2008 406 621 5252009 398 578 512

EPS Low Hi Mean

2007 0.31 0.33 0.332008 0.28 0.41 0.362009 0.35 0.41 0.38

Reported 2007Q1 Q2 Q3 Q4 TOTAL

EBITDA 155 199 354EBIT 115 159 274EPS 0.07 0.09 0.17

ANALYST RECCOMENDATIONS

BROKER DATE CONSENSUS TARGET

PRICE

JPMORGAN 05-Feb-07 OVERWEIGHT 5.00

MORGAN STANLEY 5-set-07 EQUALWEIGHT 4.70

UBS 1-ago-07 BUY 5.25

MERRILL LYNCH 02-Mar-07 NEUTRAL 4.40

CABOTO 15-May-07 ADD 5.00

INTERMONTE 10-ago-07 OUTPERFORM 5.20

BANCA AKROS 14-feb-07 BUY 5.00

UNICREDIT 8-mag-07 BUY 4.95

ACTINVEST 15-Dec-06 BUY 5.36

EUROMOBILIARE 6-lug-07 BUY 5.20

CA CHEUVREUX 31-ago-07 OUTPERFORM 5.30

IXIS 10-ago-07 ADD 4.85

LEHMAN BROTHERS 6-lug-07 OVERWEIGHT 5.20

GOLDMAN SACHS 22-giu-07 NEUTRAL 4.50

MEDIAN TARGET PRICE 5.00

source Thomson

Last update 10th September 2007

••• Saras in a snapshotSaras in a snapshotSaras in a snapshot

••• Market overviewMarket overviewMarket overview

••• Business segments descriptionBusiness segments descriptionBusiness segments description

••• FinancialsFinancialsFinancials

• Other

September 2007 SARAS S.p.A. 76

Board of Directors and Top Management

Board of Directors

Chairman Gianmarco MorattiCEO Massimo MorattiVice Chairman Angelo MorattiDirector Dario ScaffardiDirector Angelomario MorattiDirector Gabriele PreviatiIndep.Director Mario GrecoIndep. Director Gilberto Callera

General Manager

Dario Scaffardi

Chief Financial Officer

Corrado Costanzo

Internal audit

Ferruccio Bellelli

Public Affairs

Marco Ghiringhelli

September 2007 SARAS S.p.A. 77

Management compensation

Annual salary and fringe benefits

Annual incentive bonuses• based on both Company’s financial performance vs budget and individual

performance

Medium term Stock grant incentive plan• period 2007-2009• based on Saras’ stock performance vs peers and Company’s financial

performance

September 2007 SARAS S.p.A. 78

Corporate Governance

The Company is structured according to the traditional business administration and audit model as follows:

Board of Directors charged with overseeing business management within which various committees have been set up, namely

• remuneration committee• internal control committee

the Board includes two independent non-executive directors, Mr Mario Greco and Mr Gilberto Callera, who, together with another non-executive director, Mr Gabriele Previati, make up the above mentioned remuneration committee and the internal control committee.

Board of Statutory Auditors charged with supervising the compliance with laws and statutes, and monitoring the adequacy of the organisational structure, the internal control system and the Company’s accounting-administrative system.The Board has nominated the Chairman of the Board of Directors as the executive in charge of surveying internal control system functions.

September 2007 SARAS S.p.A. 79

Personnel

2006Male 80% 1,446Female 20% 352

Average age: 40 years

Average time at the company 11 years

The Saras Group has around 1,800 staff. Approximately 80% of these are employed in Sardinia, mostly at the Sarroch refinery. Some 230 people work overseas, in distribution and marketing.In over 40 years of activity, Saras has successfully built a reputation that has enabled it to attract the best employees, and to develop and retain talented and motivated personnel, who share the company’s values of honesty, respect, excellence and responsibility. Saras has promoted these values by creating and constantly improving a safe and stimulating work environment, which encourages respect for the individual and offers attractive opportunities for staff development.

September 2007 SARAS S.p.A. 80

HSE

2000-2001 2002-2003 2004-2005 2006-2008

Policy definition

EMS

Enviromentalreport

ISO14001

certification

The Eco-Management and Audit Scheme (EMAS) is the EU voluntary instrument which acknowledges organisations that improve their environmental performance on a continuous basis. EMAS registered organisations are legally compliant, run an environment management system and report on their environmental performance through the publication of an independently verified environmental statement. They are recognised by the EMAS logo, which guarantees the reliability of the information provided.

Saras certification pattern The Saras Group has always paid particular attention to the environmental issues connected with its activities.Investments in environmental and safety initiatives stood at EUR 17.6 million in 2006. This was approximately 16% of total investments made in the year

The Saras Group has a programme aimed at ensuring the safety of all its employees at work.The company introduced a specific safety policy in 1996, and since then has achieved positive results in safeguarding both its workers and the environment.

Saras’ environmental objectives include transparency of information. It has always made company data and the results of studies available to the authorities and the public. In keeping with this policy, Saras draws up an Environment and Safety Report each year.

The Group’s Safety Management System for the prevention of major accidents was developed pursuant to Legislative Decree 334/99. The main components ofthis system are a Safety Report, an Internal

Emergency Plan and an External Emergency Plan.

September 2007 SARAS S.p.A. 81

WEBSITE

www.saras.it

A comprehensive market section updated weekly including:

- EMC margin benchmark- Crude oil and products prices- Crack spreads

Saras Investor Relations

IR contacts

General email [email protected]

IR Manager- Marco Schiavetti +39 02 7737 301 [email protected]

IR Assistant- Giordano Serafini +39 02 7737 641

Financial communication- Rafaella Casula +39 02 7737 495

Assistant- Alessandra Gelmini +39 02 7737 642