Presentation Title - LBCG€¦ · Presentation Title ... Reports and Current Reports for a more...

31

Presentation Title Presentation Subtitle Crestwood Midstream Partners LP Crestwood Equity Partners LP Connections for America’s Energy ™ ™ Presentation Title Presentation Subtitle Crestwood Midstream Partners LP Crestwood Equity Partners LP Connections for America’s Energy ™ ™ Presentation Title Presentation Subtitle Crestwood Midstream Partners LP Crestwood Equity Partners LP Connections for America’s Energy ™ ™ 30/07/2015 Connections for America’s Energy ™ ™ ™ ™ Connections for America’s Energy ™ ™ Connections for America’s Energy Crestwood Midstream Partners LP Darrel Hagerman- VP-Commercial & Business Development Permian Midstream Congress July 29 th and 30 th , 2015

Transcript of Presentation Title - LBCG€¦ · Presentation Title ... Reports and Current Reports for a more...

Presentation Title Presentation Subtitle

Crestwood Midstream Partners LP Crestwood Equity Partners LP

Connections for America’s Energy ™

™

Presentation Title Presentation Subtitle

Crestwood Midstream Partners LP Crestwood Equity Partners LP

Connections for America’s Energy ™

™

Presentation Title Presentation Subtitle

Crestwood Midstream Partners LP Crestwood Equity Partners LP

Connections for America’s Energy ™

™

30/07/2015

Connections for America’s Energy ™

™

™

™ Connections for America’s Energy ™

™ Connections for America’s Energy

Crestwood Midstream Partners LP Darrel Hagerman- VP-Commercial & Business Development Permian Midstream Congress July 29th and 30th, 2015

Connections for America’s Energy ™ ™ ™ ™ ™ ™

2

The statements in this communication regarding future events, occurrences, circumstances, activities, performance, outcomes and results are forward-looking statements. Although these statements reflect the current views, assumptions and expectations of Crestwood’s management, the matters addressed herein are subject to numerous risks and uncertainties which could cause actual activities, performance, outcomes and results to differ materially from those indicated. Such forward-looking statements include, but are not limited to, statements about the benefits that may result from the merger and statements about the future financial and operating results, objectives, expectations and intentions and other statements that are not historical facts. Factors that could result in such differences or otherwise materially affect Crestwood’s financial condition, results of operations and cash flows include, without limitation, the possibility that expected cost reductions will not be realized, or will not be realized within the expected timeframe; fluctuations in crude oil, natural gas and NGL prices (including, without limitation, lower commodity prices for sustained periods of time); the extent and success of drilling efforts, as well as the extent and quality of natural gas and crude oil volumes produced within proximity of Crestwood assets; failure or delays by customers in achieving expected production in their oil and gas projects; competitive conditions in the industry and their impact on our ability to connect supplies to Crestwood gathering, processing and transportation assets or systems; actions or inactions taken or non-performance by third parties, including suppliers, contractors, operators, processors, transporters and customers; the ability of Crestwood to consummate acquisitions, successfully integrate the acquired businesses, realize any cost savings and other synergies from any acquisition; changes in the availability and cost of capital; operating hazards, natural disasters, weather-related delays, casualty losses and other matters beyond Crestwood’s control; timely receipt of necessary government approvals and permits, the ability of Crestwood to control the costs of construction, including costs of materials, labor and right-of-way and other factors that may impact Crestwood’s ability to complete projects within budget and on schedule; the effects of existing and future laws and governmental regulations, including environmental and climate change requirements; the effects of existing and future litigation; and risks related to the substantial indebtedness, of either company, as well as other factors disclosed in Crestwood’s filings with the U.S. Securities and Exchange Commission. You should read filings made by Crestwood with the U.S. Securities and Exchange Commission, including Annual Reports on Form 10-K and the most recent Quarterly Reports and Current Reports for a more extensive list of factors that could affect results. Readers are cautioned not to place undue reliance on forward-looking statements, which reflect management’s view only as of the date made. Crestwood does not assume any obligation to update these forward-looking statements.

Forward Looking Statements

2

Connections for America’s Energy ™ ™ ™ ™ ™ ™

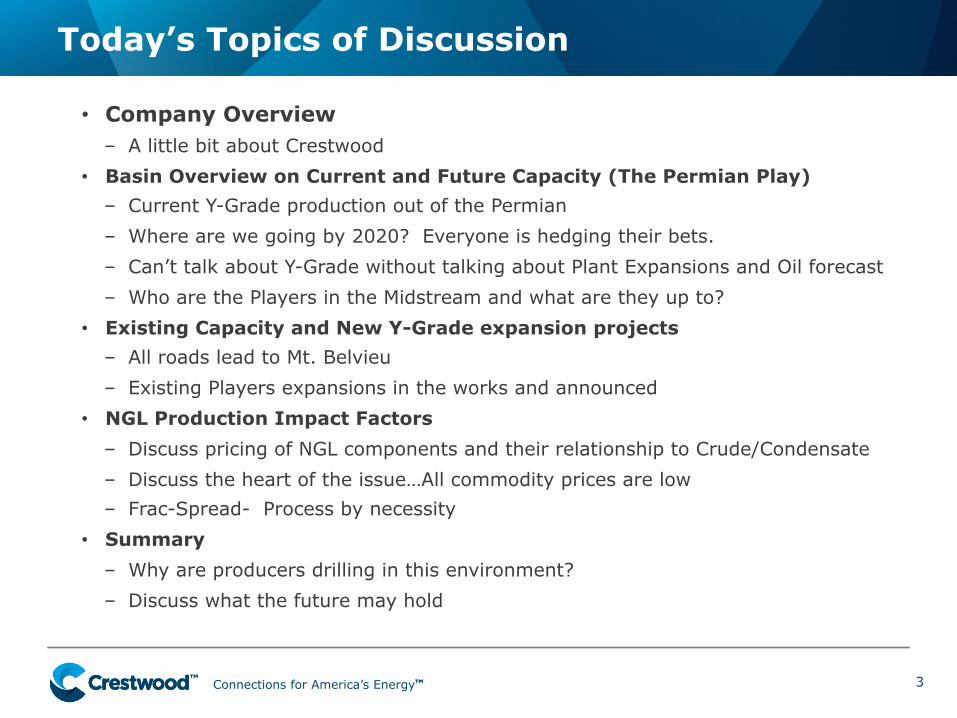

Today’s Topics of Discussion

3

• Company Overview – A little bit about Crestwood

• Basin Overview on Current and Future Capacity (The Permian Play)

– Current Y-Grade production out of the Permian

– Where are we going by 2020? Everyone is hedging their bets.

– Can’t talk about Y-Grade without talking about Plant Expansions and Oil forecast

– Who are the Players in the Midstream and what are they up to?

• Existing Capacity and New Y-Grade expansion projects

– All roads lead to Mt. Belvieu

– Existing Players expansions in the works and announced

• NGL Production Impact Factors

– Discuss pricing of NGL components and their relationship to Crude/Condensate

– Discuss the heart of the issue…All commodity prices are low

– Frac-Spread- Process by necessity

• Summary

– Why are producers drilling in this environment?

– Discuss what the future may hold

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Crestwood’s Mission

4

Crestwood connects fundamental energy supply with energy demand across North America through a best-in-class midstream network. Our diversified asset base and integrated services provide flow assurance across the value chain for producers and consumers of natural gas, natural gas liquids and crude oil. Building on our history of strong customer services, operational safety as the top priority and long term value creation for our investors, Crestwood is committed to achieving sustainable growth through expansions and acquisitions which increase our connections to America’s midstream energy infrastructure.

Connections - Create Flow Assurance • Linking supply and demand across midstream value chain • Increased visibility for producers to end users • End-to-end solutions for best path to demand centers • Scale to complete major infrastructure growth projects

Operations - Maximize Value to Customers • Critical midstream infrastructure in premier shale plays and

market centers • Comprehensive services, leveraging relationships to link supply

with demand • Through expertise in gathering, processing, transportation,

storage and logistics • Improving customer options through control of product from

wellhead to burner tip

Execution - Deliver on Disciplined Strategy • Best-in-class operations and customer service • Completing infrastructure projects on time, on budget • Optimize the asset portfolio through organic project and

acquisition growth • Experienced management and dedicated employees focused on

creating investor value

Integrity - Embody Core Principles • Focus on operational safety as our top priority • Responsible care for environmental compliance and

sustainability • Commitment to communities where we operate and our

employees live • Valuing relationships with our, customers, employees, vendors

and the public

Connections for America’s Energy ™ ™ ™ ™ ™ ™

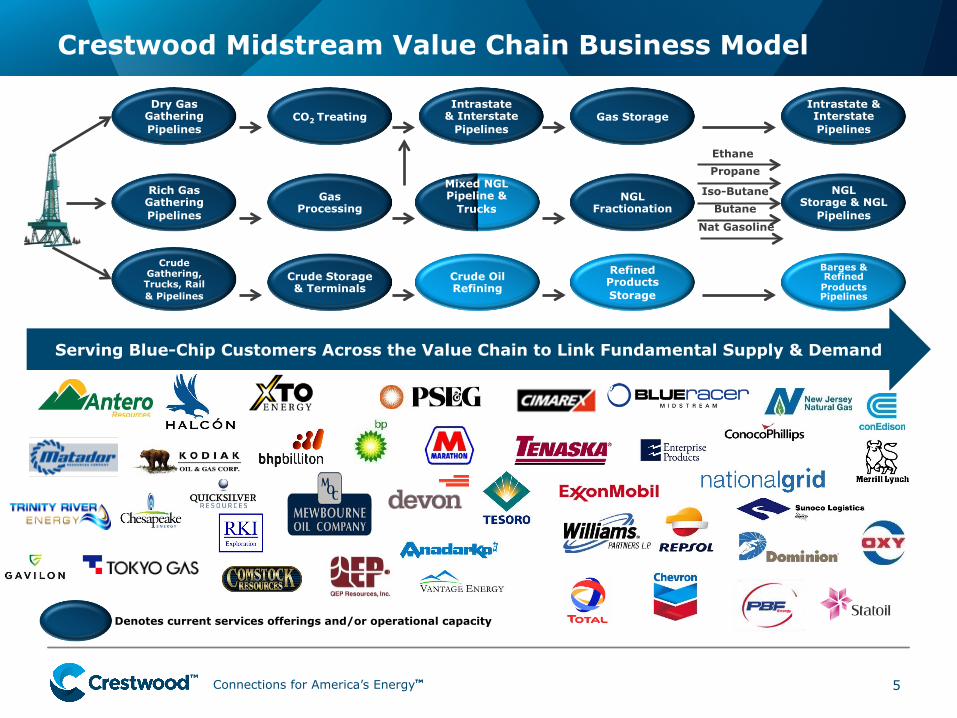

Crestwood Midstream Value Chain Business Model

Denotes current services offerings and/or operational capacity

Nat Gasoline

Iso-Butane

Butane

Propane

Ethane

Gas Storage

NGL Fractionation

NGL Storage & NGL

Pipelines

Crude Gathering, Trucks, Rail & Pipelines

Crude Storage & Terminals

Crude Oil Refining

Refined Products Storage

Barges & Refined Products Pipelines

Mixed NGL Pipeline &

Trucks

CO2 Treating

Rich Gas Gathering Pipelines

Gas Processing

Dry Gas Gathering Pipelines

Intrastate & Interstate

Pipelines

Intrastate & Interstate Pipelines

Serving Blue-Chip Customers Across the Value Chain to Link Fundamental Supply & Demand

5 5

Connections for America’s Energy ™ ™ ™ ™ ™ ™

6

Diversified US Midstream Portfolio

6

Key Statistics: • 1.4 Bcf/d

transportation • 2.6+ Bcf/d

gathering • 1,350 miles of

pipeline • 79 Bcf storage

• 481 MMcf/d processing

• 180 MBPD crude oil rail terminalling

• 125 MBPD crude oil gathering

• 294 MBPD nationwide NGL logistics business; 543 trucking units and 1840 Rail Cars

Existing platform in every premier shale play in North America creates significant opportunity for optimization, organic expansion, and strategic M&A

Connections for America’s Energy ™ ™ ™ ™ ™ ™

80,000 Square Mile Playground “Larger than Oklahoma”

7

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Spraberry/Wolfcamp – A view in 2014

Spraberry/Wolfcamp is the world’s second largest oil field and the largest US oil field. Other

stacked formations in the Midland Basin add additional resource to recoverable estimates.

0 20 40

Total Recoverable Resource (BBoe)

60

Cantarell, Mexico

Zuluf, Saudi Arabia

ADCO, UAE

Romashkinskoye, Russia

Shaybah, Saudi Arabia

Samotlorskoye, Russia

Safaniyah, Saudi Arabia

Burgan, Kuwait

Spraberry/Wolfcamp, USA

0 20 40

Total Recoverable Resource (BBoe)

60

Thunder Horse, GoM

Kuparuk River, AK

Wilmington, CA

Midway-Sunset, CA

East Texas Basin

Delaware Basin

Bakken Shale

2nd Largest Oil Field Worldwide

Largest Oil Field in the US

Ghawar, Saudi Arabia1

Prudhoe Bay, AK

Eagle Ford Shale

Spraberry/Wolfcamp

Source: Pioneer Natural Resources, Investor Presentations. (1) Ghawar scaled down for illustrative purposes. Its total recoverable resource is ~157 BBoe.

8

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Here we are in 2015

9

Permian is still King

Source- Pioneer Investor Presentation

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Yes…Flaring is still going on in the Permian Basin

10

Connections for America’s Energy ™ ™ ™ ™ ™ ™

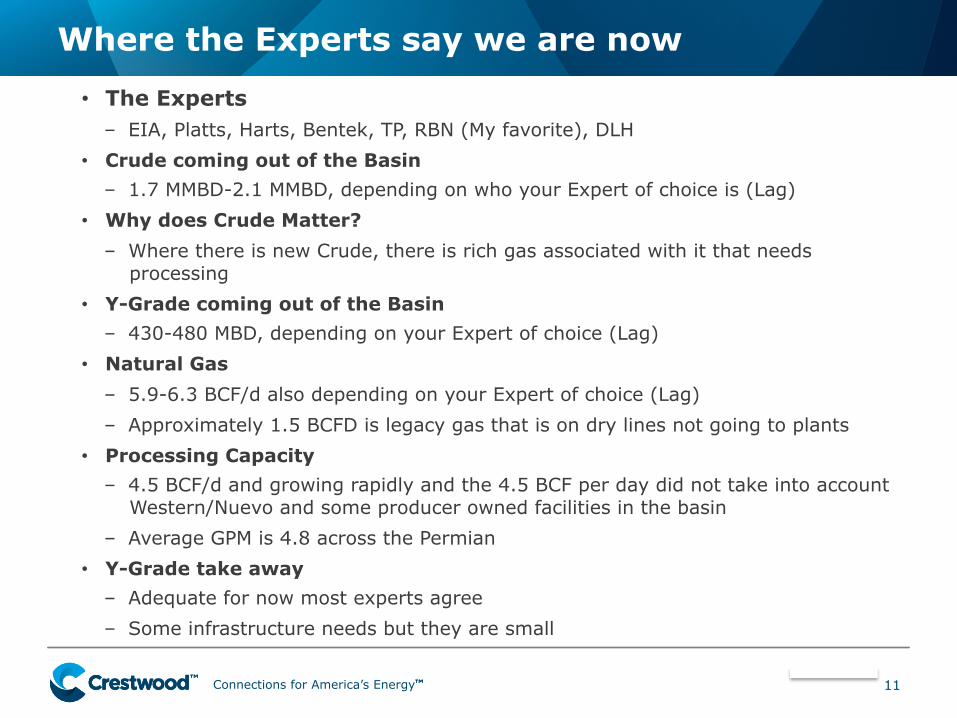

Where the Experts say we are now

11 Source: Zillow

• The Experts – EIA, Platts, Harts, Bentek, TP, RBN (My favorite), DLH

• Crude coming out of the Basin

– 1.7 MMBD-2.1 MMBD, depending on who your Expert of choice is (Lag)

• Why does Crude Matter?

– Where there is new Crude, there is rich gas associated with it that needs processing

• Y-Grade coming out of the Basin

– 430-480 MBD, depending on your Expert of choice (Lag)

• Natural Gas

– 5.9-6.3 BCF/d also depending on your Expert of choice (Lag)

– Approximately 1.5 BCFD is legacy gas that is on dry lines not going to plants

• Processing Capacity

– 4.5 BCF/d and growing rapidly and the 4.5 BCF per day did not take into account Western/Nuevo and some producer owned facilities in the basin

– Average GPM is 4.8 across the Permian

• Y-Grade take away

– Adequate for now most experts agree

– Some infrastructure needs but they are small

Connections for America’s Energy ™ ™ ™ ™ ™ ™

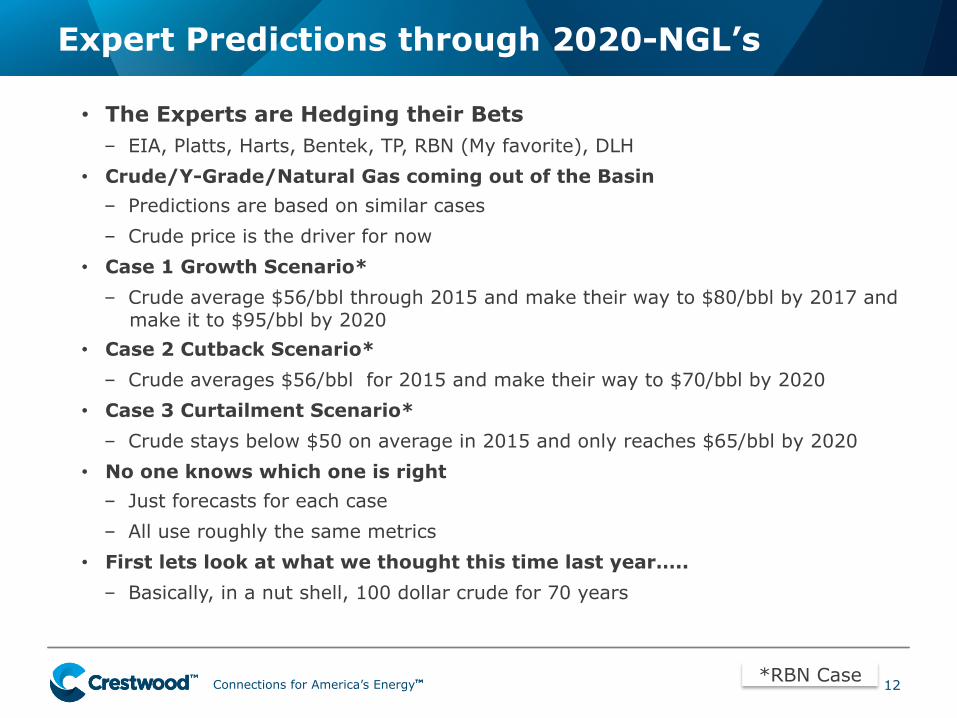

Expert Predictions through 2020-NGL’s

12 Source: Zillow

• The Experts are Hedging their Bets – EIA, Platts, Harts, Bentek, TP, RBN (My favorite), DLH

• Crude/Y-Grade/Natural Gas coming out of the Basin

– Predictions are based on similar cases

– Crude price is the driver for now

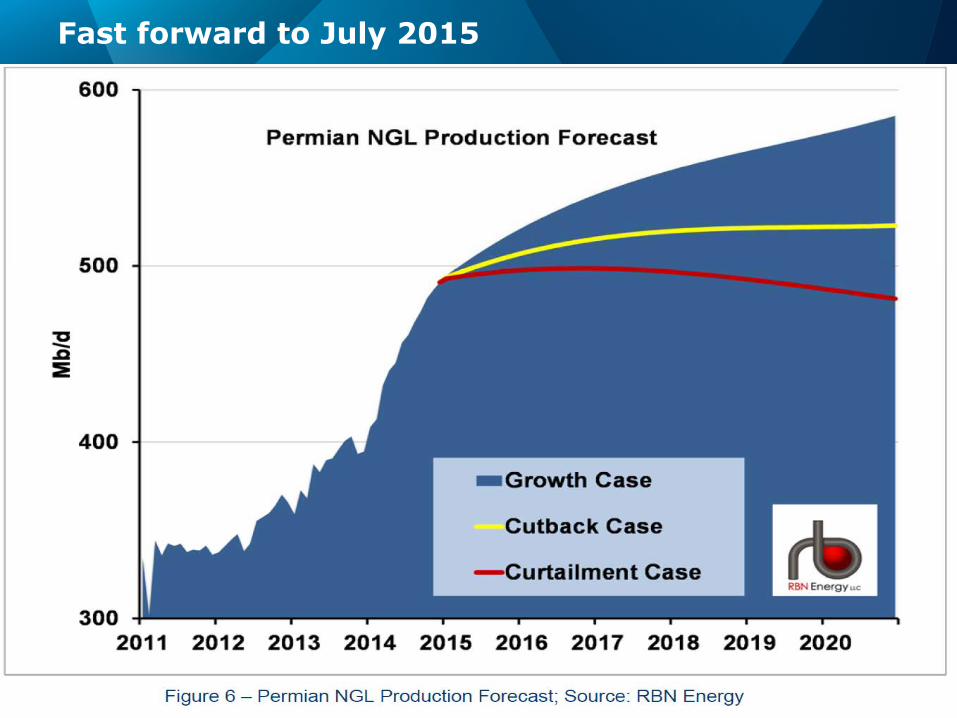

• Case 1 Growth Scenario*

– Crude average $56/bbl through 2015 and make their way to $80/bbl by 2017 and make it to $95/bbl by 2020

• Case 2 Cutback Scenario*

– Crude averages $56/bbl for 2015 and make their way to $70/bbl by 2020

• Case 3 Curtailment Scenario*

– Crude stays below $50 on average in 2015 and only reaches $65/bbl by 2020

• No one knows which one is right

– Just forecasts for each case

– All use roughly the same metrics

• First lets look at what we thought this time last year…..

– Basically, in a nut shell, 100 dollar crude for 70 years

*RBN Case

Connections for America’s Energy ™ ™ ™ ™ ™ ™

What we thought our world would look like in 2014

Source: RBN Energy 13

By 2020: • Gas was expected to reach over 8 Bcf/d

• NGLs were expected to approach 1 MMBls/d

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Fast forward to July 2015

Source: RBN Energy 14

Connections for America’s Energy ™ ™ ™ ™ ™ ™

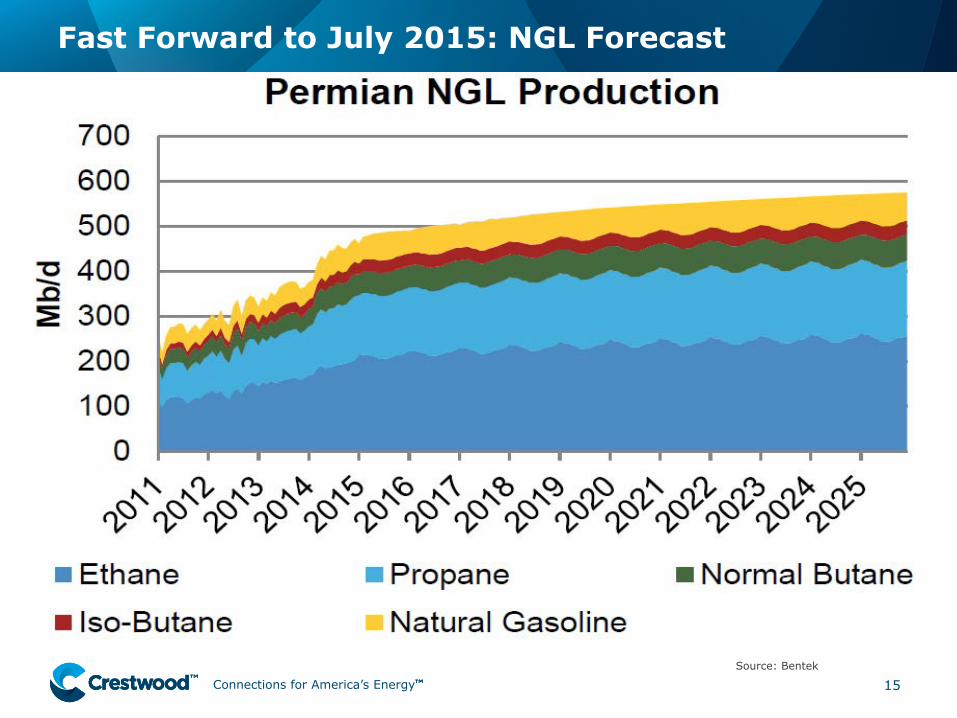

Fast Forward to July 2015: NGL Forecast

15

Source: Bentek

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Fast Forward to July 2015: Gas Forecast

16

Source: Bentek

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Production Outlooks from the Permian by Quality

Source: EIA 17

Connections for America’s Energy ™ ™ ™ ™ ™ ™

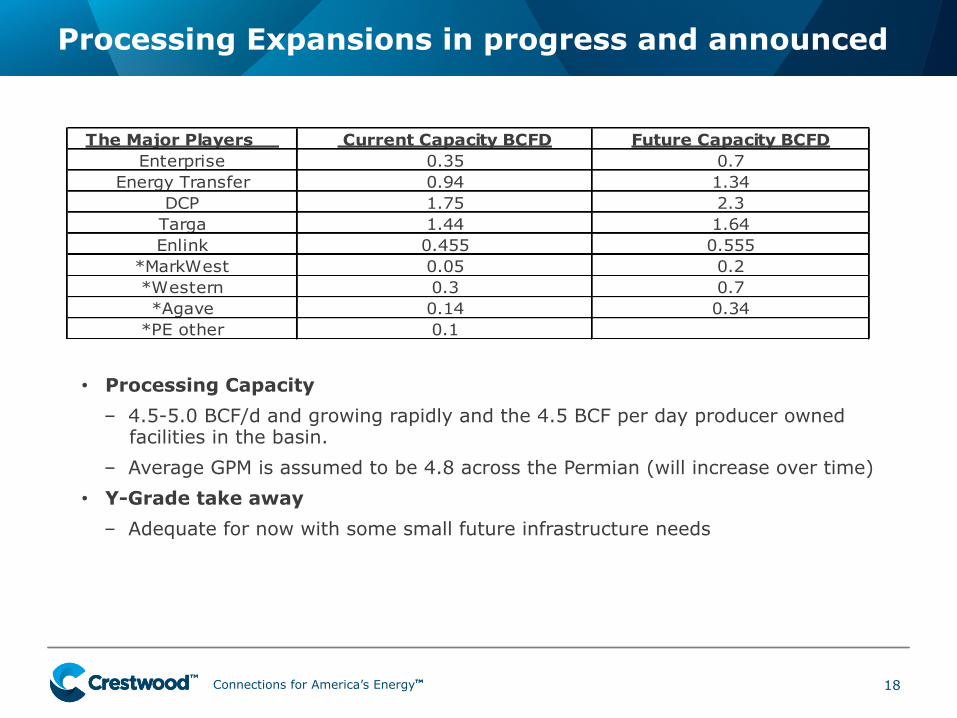

Processing Expansions in progress and announced

18

• Processing Capacity

– 4.5-5.0 BCF/d and growing rapidly and the 4.5 BCF per day producer owned facilities in the basin.

– Average GPM is assumed to be 4.8 across the Permian (will increase over time)

• Y-Grade take away

– Adequate for now with some small future infrastructure needs

The Major Players Current Capacity BCFD Future Capacity BCFDEnterprise 0.35 0.7

Energy Transfer 0.94 1.34DCP 1.75 2.3

Targa 1.44 1.64Enlink 0.455 0.555

*MarkWest 0.05 0.2*Western 0.3 0.7*Agave 0.14 0.34

*PE other 0.1

Connections for America’s Energy ™ ™ ™ ™ ™ ™

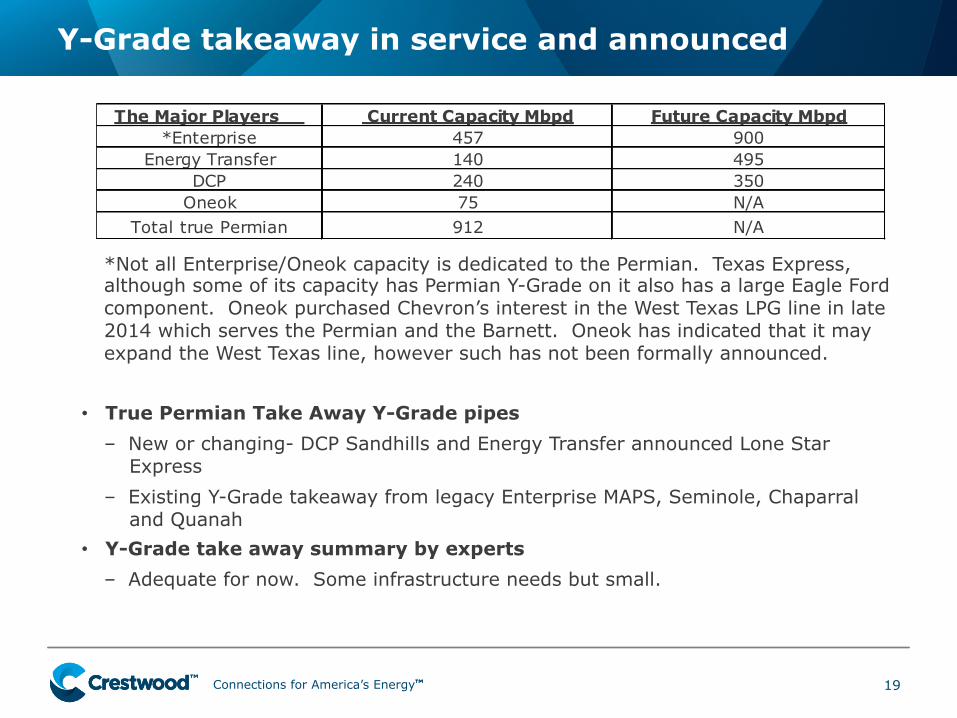

Y-Grade takeaway in service and announced

19

*Not all Enterprise/Oneok capacity is dedicated to the Permian. Texas Express, although some of its capacity has Permian Y-Grade on it also has a large Eagle Ford component. Oneok purchased Chevron’s interest in the West Texas LPG line in late 2014 which serves the Permian and the Barnett. Oneok has indicated that it may expand the West Texas line, however such has not been formally announced.

• True Permian Take Away Y-Grade pipes

– New or changing- DCP Sandhills and Energy Transfer announced Lone Star Express

– Existing Y-Grade takeaway from legacy Enterprise MAPS, Seminole, Chaparral and Quanah

• Y-Grade take away summary by experts

– Adequate for now. Some infrastructure needs but small.

The Major Players Current Capacity Mbpd Future Capacity Mbpd*Enterprise 457 900

Energy Transfer 140 495DCP 240 350

Oneok 75 N/ATotal true Permian 912 N/A

Connections for America’s Energy ™ ™ ™ ™ ™ ™

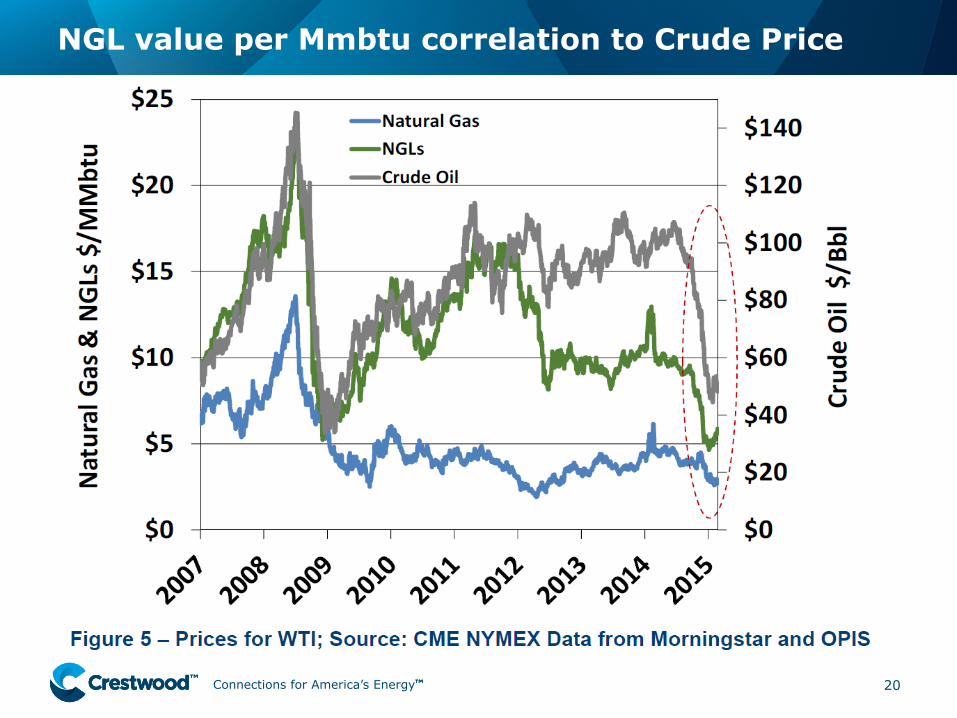

NGL value per Mmbtu correlation to Crude Price

20

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Summary

21 Source: Zillow

• Y-Grade and Processing Infrastructure – Appear to be in-line with current environment

– Fractionation, which will be discussed later, appears to be in-line with today’s market conditions as well

– The Y-Grade take away players and Midstream providers each have an incentive to adapt quickly to changing market conditions

• Price uncertainty

– Some producers will drill to hold acreage even if economics are not acceptable

– Regardless, if commodity prices remain depressed, drilling will slow and oil, gas and Y-Grade outputs will fall

• Frac-Spread

– In most areas, depending on a producers contract with its Midstream provider, someone is losing money as the frac-spread has disappeared

• Propane

– The US is now the world’s largest exporter of Propane. Propane is now under water in most areas as an NGL

– Despite being the world’s largest Propane exporter, US supply is at record levels with no demand growth

• The remainder of 2105 should be very interesting……

• Investor Slides for the projects we discussed are attached

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Questions and Answers

22

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Y-Grade DCP

23

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Y-Grade Enterprise

24

Connections for America’s Energy ™ ™ ™ ™ ™ ™

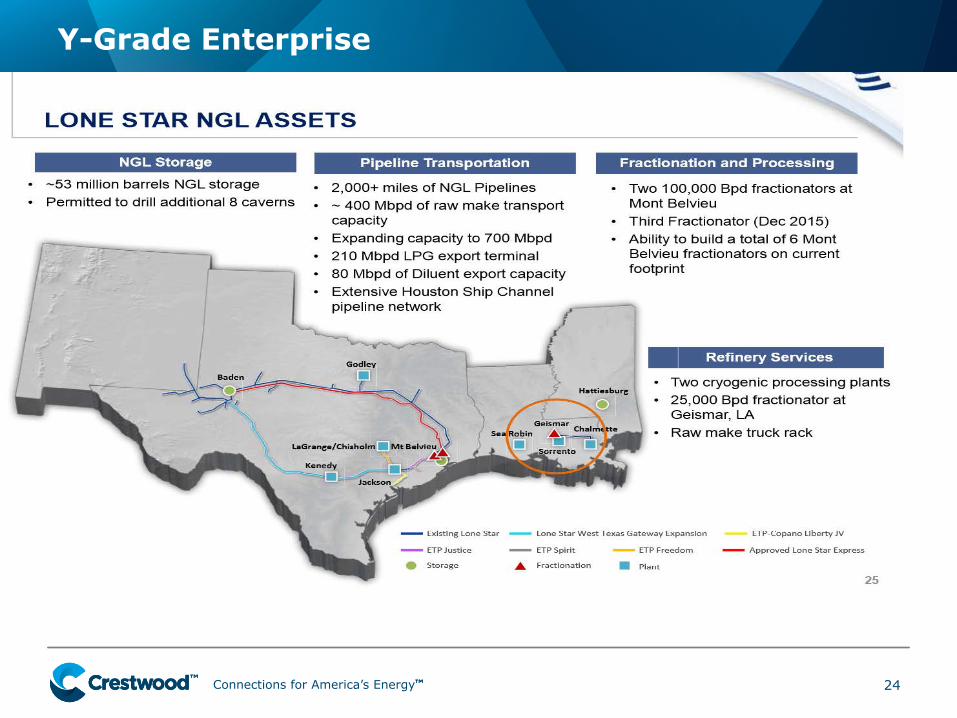

Lone Star Investor Presentation LS Express

25

Willow Lake - Phase 2 Cryogenic Gas Plant

Connections for America’s Energy ™ ™ ™ ™ ™ ™

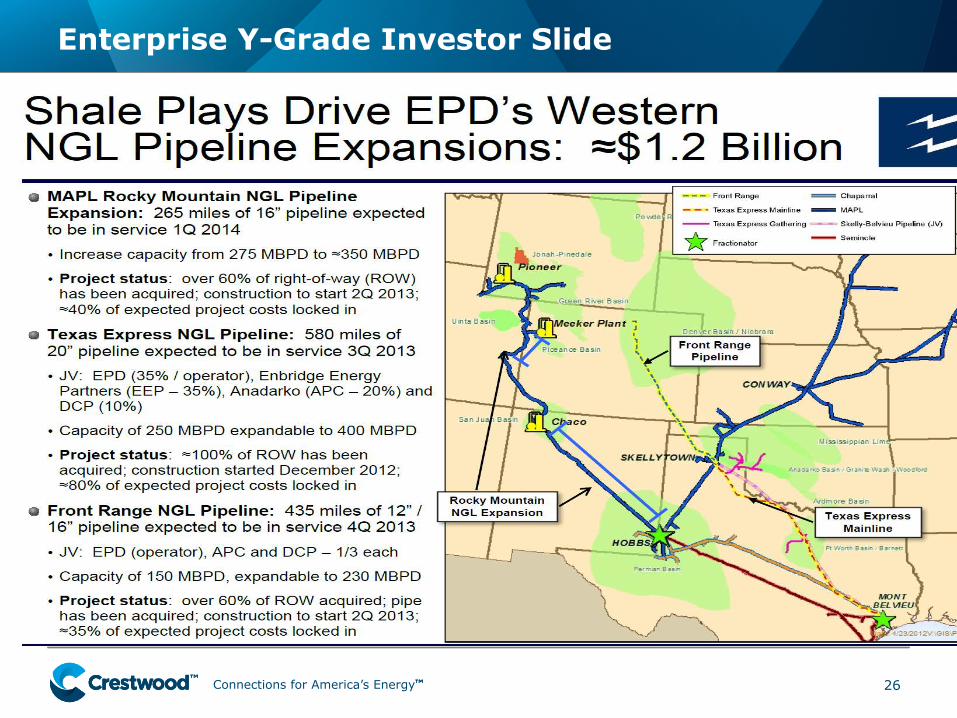

Enterprise Y-Grade Investor Slide

26

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Enlink Investor Presentation Slide

27

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Enterprise Midstream Expansions

28

Connections for America’s Energy ™ ™ ™ ™ ™ ™

ETC Investor Slide

29

Connections for America’s Energy ™ ™ ™ ™ ™ ™

Targa Investor Presentation Slide

30

Connections for America’s Energy ™ ™ ™ ™ ™ ™

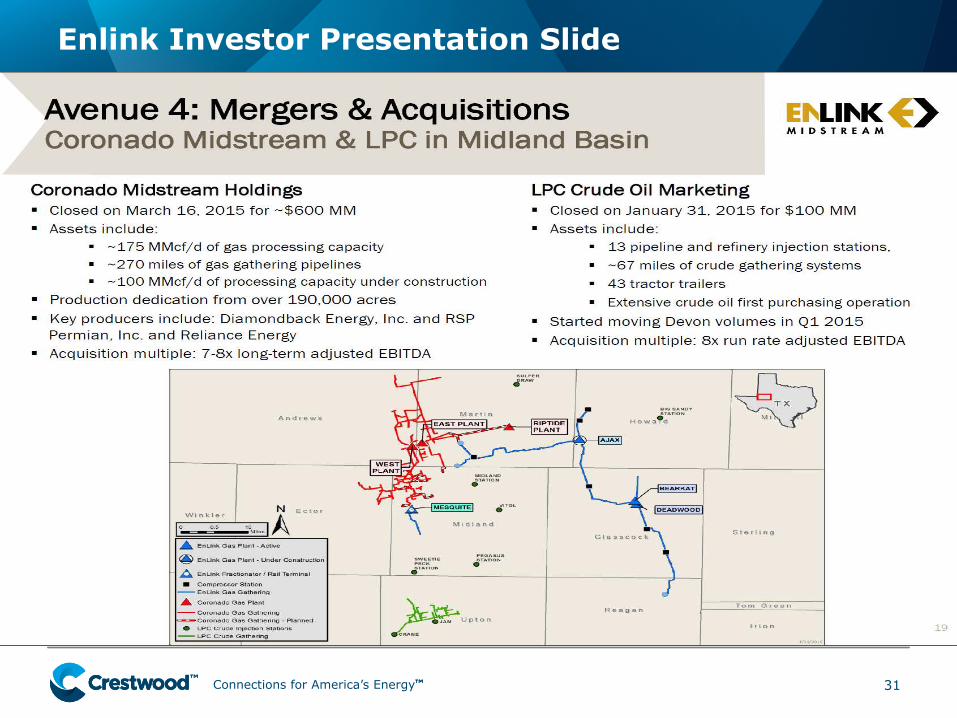

Enlink Investor Presentation Slide

31