Presentation: The Increasingly Important Role of Private ... · Hertz Semiconductor $15.0B Kinder...

21

© Copyright 2005 SunTrust Banks, Inc. The Increasingly Important Role of Private Equity Firms in M&A Private Equity 3Q 2006 Review Presentation for the University of Florida Finance Professional Speakers Series November 3, 2006 The data and interpretation in this review are not intended, nor implied to be a recommendation or advice of any form. Please seek the professional advice of a qualified accountant, financial advisor or attorney before making any investment or financial decisions as a result of reading this review. Duplication or transmission of this publication is strictly forbidden. Philip E. Marshall Managing Director – Investment Banking 407.237.5895 [email protected]

Transcript of Presentation: The Increasingly Important Role of Private ... · Hertz Semiconductor $15.0B Kinder...

© Copyright 2005 SunTrust Banks, Inc.

The Increasingly Important Role of Private Equity Firms in M&APrivate Equity 3Q 2006 ReviewPresentation for the University of Florida Finance Professional Speakers Series

November 3, 2006

The data and interpretation in this review are not intended, nor implied to be a recommendation or advice of any form. Please seek the professional advice of a qualified accountant, financial advisor or attorney before making any investment or financial decisions as a result of reading this review.

Duplication or transmission of this publication is strictly forbidden.

Philip E. MarshallManaging Director – Investment [email protected]

2

Biography

B.S. Food & Resource Economics – University of Florida - 1981

Focus on Economics, Accounting, and Finance

Sun Bank, N.A. (SunTrust Predecessor) 1981 - 1983

Management Training Program

Corporate Banking – Agribusiness

MBA - Wharton School – University of Pennsylvania – 1985

Emphasis on Finance

SunTrust Banks, Inc. 1985 – Present

Corporate Banking 1985 – 1988

SunTrust Capital Markets / SunTrust Robinson Humphrey – 1988 to Present

Vice President – Aircraft Leveraged Lease Finance Program

Director – Syndicated Finance Group

Managing Director – Capital Markets Origination

Managing Director – Investment Banking

Introduction

3

Introduction

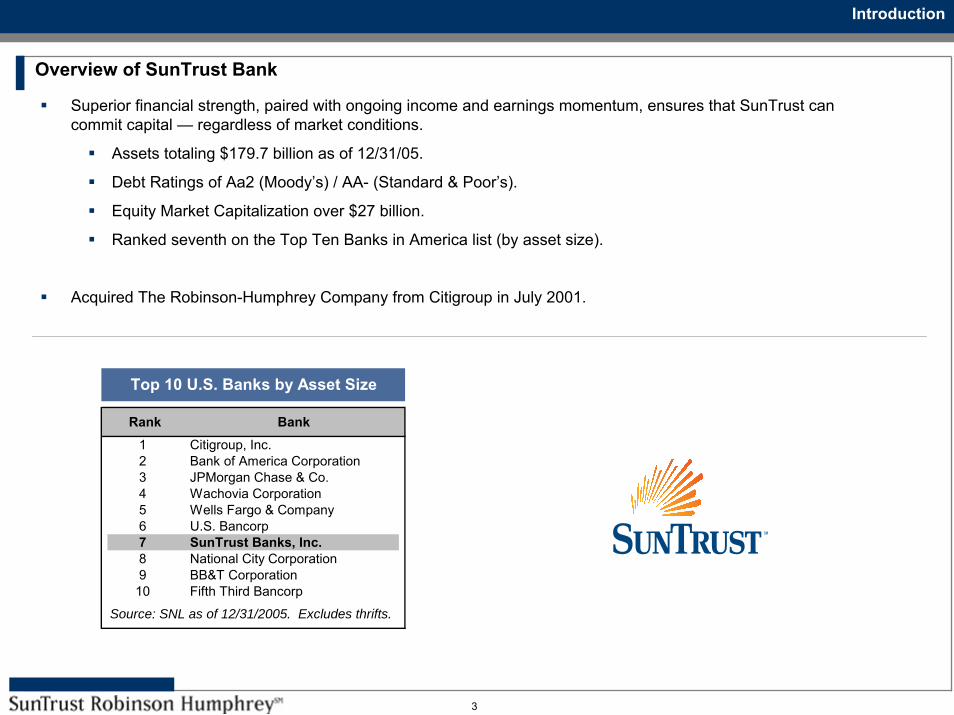

Overview of SunTrust Bank

Top 10 U.S. Banks by Asset Size

Rank Bank1 Citigroup, Inc.2 Bank of America Corporation3 JPMorgan Chase & Co.4 Wachovia Corporation5 Wells Fargo & Company6 U.S. Bancorp7 SunTrust Banks, Inc.8 National City Corporation9 BB&T Corporation

10 Fifth Third Bancorp

Source: SNL as of 12/31/2005. Excludes thrifts.

Superior financial strength, paired with ongoing income and earnings momentum, ensures that SunTrust can commit capital — regardless of market conditions.

Assets totaling $179.7 billion as of 12/31/05.

Debt Ratings of Aa2 (Moody’s) / AA- (Standard & Poor’s).

Equity Market Capitalization over $27 billion.

Ranked seventh on the Top Ten Banks in America list (by asset size).

Acquired The Robinson-Humphrey Company from Citigroup in July 2001.

4

Introduction

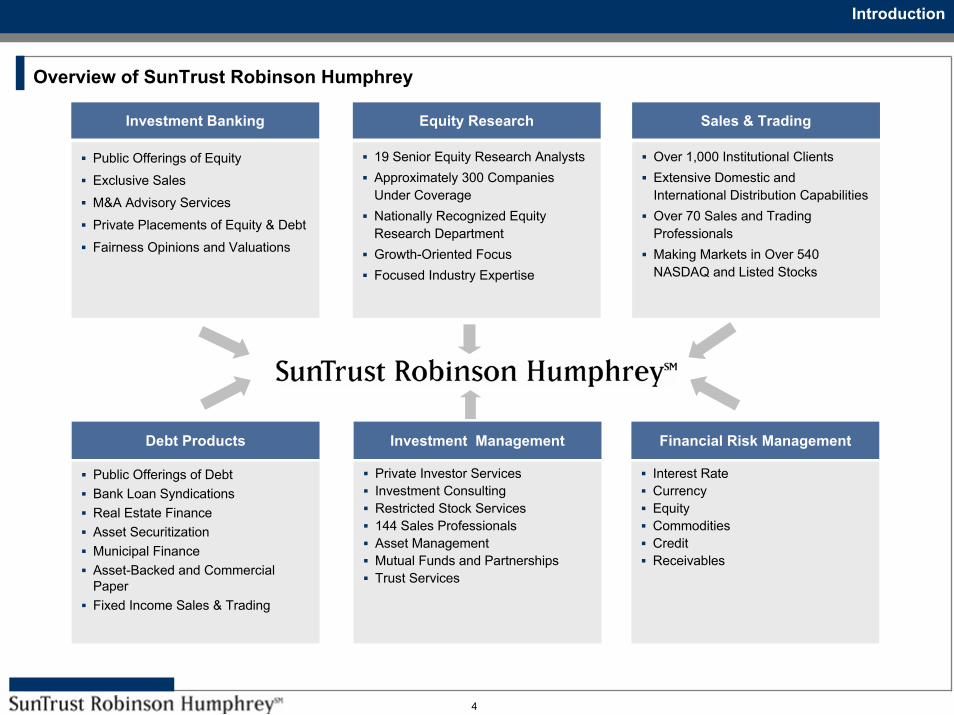

Overview of SunTrust Robinson Humphrey

Investment Banking

Public Offerings of Equity

Exclusive Sales

M&A Advisory Services

Private Placements of Equity & Debt

Fairness Opinions and Valuations

Equity Research

19 Senior Equity Research AnalystsApproximately 300 Companies Under CoverageNationally Recognized Equity Research DepartmentGrowth-Oriented FocusFocused Industry Expertise

Sales & Trading

Over 1,000 Institutional ClientsExtensive Domestic and International Distribution CapabilitiesOver 70 Sales and Trading ProfessionalsMaking Markets in Over 540 NASDAQ and Listed Stocks

Debt Products

Public Offerings of DebtBank Loan SyndicationsReal Estate FinanceAsset Securitization Municipal FinanceAsset-Backed and Commercial PaperFixed Income Sales & Trading

Investment Management

Private Investor ServicesInvestment ConsultingRestricted Stock Services144 Sales ProfessionalsAsset ManagementMutual Funds and PartnershipsTrust Services

Financial Risk Management

Interest RateCurrency Equity CommoditiesCredit Receivables

5

3Q 2006 Review

Private Equity (“PE”) has become one of the most important forces in the domestic and international M&A market

PE Buys One in Three Companies Sold 1

PE owned companies employ one in five people outside the public sector 2

Sponsor Activity Approached $200B in 2005

Strong 3Q 2006 Results 3

$57B in Disclosed Transactions

$5.6B in Sponsor Driven IPO Volume

Buyout firms raised $140B through 3Q 2006, compared to $112B in through 3Q 2005

Through 3Q 2006, 770 control-stake transactions were completed for an aggregate total of $182B

A recent survey by the Association for Corporate Growth and Thompson Financial reports that the private equity market is expecting continued exuberance through the end of 2006 4

Small and Middle Market Buyouts hold the Greatest Potential in Terms of Return

3Q 2006 REVIEW

1 BBC News, 6/20/20062 BBC News, 6/20/2006

3 Buyouts, 10/09/20064 Buyouts, 6/26/2006

6

2006 levels (volume / deals) on track to exceed 2005 levels

More than $150B in deals scheduled to close 4Q or 1Q 2007

On pace for a fifth straight year in terms of growth in annual deal volume

Sponsor-backed IPO volume totals $24.9B through 3Q 2006, down 2% from $25.5B in the same period last year 5

Sponsor-backed Secondary Offering volume totals $28B through 3Q 2006, up 17%, from $24B for the same period in 2005 6

Source: Buyouts, 10/09/20062005 1Q-3Q 2006

3Q 2006 Review

3Q 2006 REVIEW

5 Dealogic – Financial Sponsor Review, 10/05/20066 EBID

(in Billions)

U.S. BASED DEAL VOLUME (BY QUARTER)

12

4 4

20

16

40

52

10 11 8 12

38

42

73

11

5

12

20

37

57 57

9

4

17

42

46

59

$0

$10

$20

$30

$40

$50

$60

$70

$80

2000 2001 2002 2003 2004 2005 2006

(in Billions)

DEALS VOLUME AND FUNDRASING GROWTH2005 vs 1Q-3Q 2006

$182$198$140

$182

$0

$50

$100

$150

$200

$250

Deals Completed Buyout Funds Raised

7

The Rise of Private Equity

Last Year, All But Four Of the Largest Twenty Generators of Investment Banking Fees Were Private Equity Groups

3Q 2006 REVIEW

2005 2001

Rank Company Name Total Fees ($MM) Rank Company Name Total Fees ($MM)

1 Blackstone Group 305 1 Altria Group 257

2 KKR 304 2 France Telecom 250

3 Telefonica 296 3 Vodafone Group 230

4 Warburg Pincus & Co 295 4 Koninklijke KPN 224

5 Carlyle Group 264 5 BT Group 223

6 Goldman Sachs Merchant Banking 262 6 Nippon Telegraph & Telephone 216

7 Apax Partners 245 7 Tyco International 189

8 Thomas H Lee 240 8 KKR 174

9 Apollo Management 217 9 Agere Systems 168

10 EDF 201 10 Time Warner 166

11 Texas Pacific Group 197 11 Orange 162

12 Gazprom 194 12 AT&T Wireless 160

13 CVC Capital Partners 189 13 Charter Communications Hldgs 152

14 Permira Advisers 182 14 Deutsche Telekom 146

15 Cinven Limited 177 15 Calpine Corp 145

16 Suex 175 16 Adelphia Communications Corp 144

17 Ripplewood Holdings 165 17 Warburg Pincus & Co 140

18 3i Group 161 18 JP Morgan Partners 139

19 CSFB Private Equity 160 19 Telecom Italia 135

20 First Reserve Corporation 159 20 Sprint Corp 134

TOTAL $4,388 TOTAL $3,554

Source: Thompson Financial / Freeman & Co. Note: rankings exclude financial institutions and governmentsClosed end funds' ECM activity is excluded

INVESTMENT BANKING FEES - M&A, ECM, DCM, LOANS

8

Current Macro Trends in the Market

Growth of the Mega Deal

Convergence of Hedge Funds / Private Equity Funds

Trend to Long Term Outlook

Attractive Debt Markets Environment

Lower Return Expectations

3Q 2006 REVIEW

9

HCA$21.3B

FreescaleHertz Semiconductor

$15.0B Kinder Morgan $16.2BSunGardData Systems$11.3B

VNU$8.8B

Texas GencoToys 'R' Us $8.3B$6.6B Aramark Royal

$5.9B PhilipsSemiconductor

Dunkin' Brands Business$2.4B $5.5B

● ● ● ● ● ●Bain Capital ● ●

● ● ● ●● ● ● ● ●

Merrill Lynch ●● ● ●

● ● ●J F A M J J A S O N D J F M A J J A S O

2005 2006

Current Fund Size

CARLYLE GROUP BLACKSTONE GROUP **

Texas Pacific Group

AWASH IN CASH

Thomas H. LeeM M

Carlyle Group

Blackstone GroupKohlberg Kravis Roberts

TEXAS PACIFICGROUP

KOHLBERG KRAVIS ROBERTS*THOMAS H. LEE

$13.5B

$7.5B $8B$10B $14B $15.6B

Private Equity ActivityRecent high profile acquisitions involving some of the biggest private equity firms, and deal value excluding net debt, at announcement date

Mega Deals Successfully Completed

GROWTH OF THE MEGA DEAL

Source: Wall Street Journal / Weekend Edition – 6/03/2006, Capital IQ, 10/03/2006, Dow Jones 10/18/2006

* Does not include recent $5B IPO** Blackstone intends to add $5B to its $15.6B fund

10

(in Millions)

AVERAGE LBO SIZE (STRATEGIC AND FINANCIAL BUYERS)

$388.6

$973.3$1,043.4

$706.1$716.3

$972.4

$540.3

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

$1,100

2001 2002 2003 2004 2005 1Q-3Q06 3Q06

(in Billions)

U.S. FUNDRAISING (BY QUARTER)

12 12

1 3

9

35 35

10 9

1 1

12

44

48

11

7 6

1

12

33

57

21

8

2

16

9

70

$0

$10

$20

$30

$40

$50

$60

$70

$80

2000 2001 2002 2003 2004 2005 2006

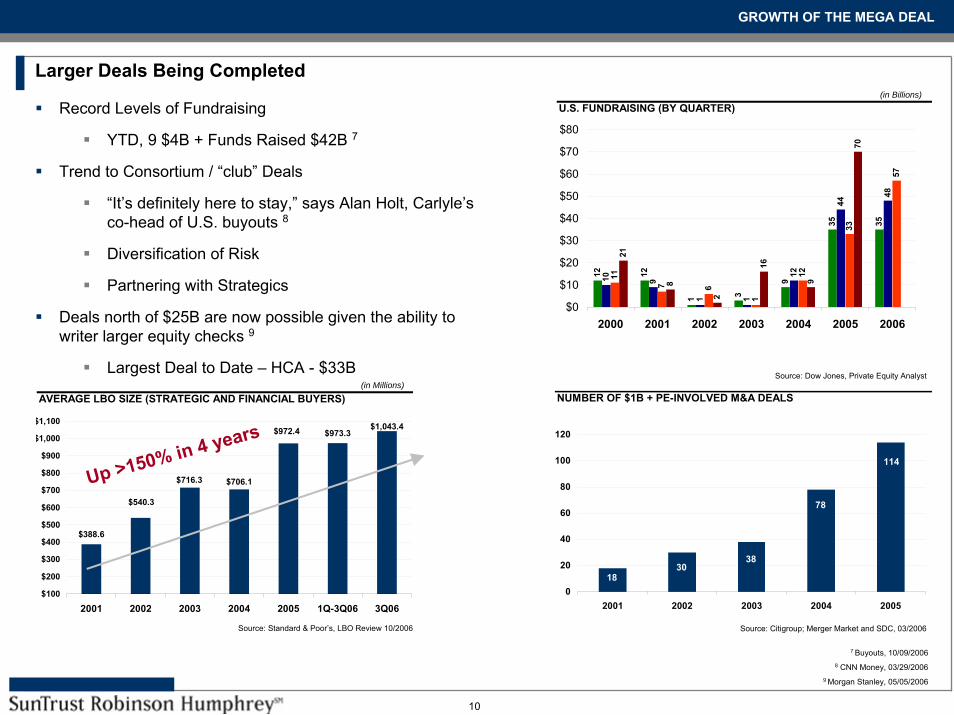

Larger Deals Being Completed

Up >150% in 4 years

Record Levels of Fundraising

YTD, 9 $4B + Funds Raised $42B 7

Trend to Consortium / “club” Deals

“It’s definitely here to stay,” says Alan Holt, Carlyle’s co-head of U.S. buyouts 8

Diversification of Risk

Partnering with Strategics

Deals north of $25B are now possible given the ability to writer larger equity checks 9

Largest Deal to Date – HCA - $33B

GROWTH OF THE MEGA DEAL

7 Buyouts, 10/09/20068 CNN Money, 03/29/2006

9 Morgan Stanley, 05/05/2006

Source: Standard & Poor’s, LBO Review 10/2006 Source: Citigroup; Merger Market and SDC, 03/2006

Source: Dow Jones, Private Equity Analyst

NUMBER OF $1B + PE-INVOLVED M&A DEALS

114

78

1830

38

0

20

40

60

80

100

120

2001 2002 2003 2004 2005

11

Its Getting Blurry in Here

2005 saw numerous high-profile examples of hedge funds taking on the long-term control investing due to overcrowding in its traditional short-term “trading” space, the influx of investor cash and recent regulatory amendments to lockup periods. 10

Hedge Funds Acting More like Buyout Funds:

In April, GMAC was acquired for $7.3B by a consortium led by Cerberus Capital Management, a NY-based hedge fund manager.

In February 2006, Harvard Business School reported that NY-based Freeman & Co. estimated “side-pocket”investments accounted for about 7% of hedge fund investments last year, a figure likely to go north of $100B in 2006. 11

In 2005, Circuit City was acquired for $3.25B by Boston-based hedge fund manager Highfields Capital Management.

In 2005, Beverly Enterprises, a US nursing home chain, rejected a bid worth $1.41B from an investor group that included hedge fund Appalossa Management.

Private Equity Funds Acting More like Hedge Funds:

The Carlyle Group launched two hedge funds earlier this year.

Blackstone Group, the world’s biggest buyout fund, has a hedge-fund unit with about $9B in assets.

Carl Ichan, legendary Wall Street raider, is launching his own hedge fund.

Over Time, the Ability to Distinguish the Two will be Blurred:

In February, at a conference in Frankfurt, David Rubenstein, a co-founder of Carlyle Group, said private equity and hedge funds may eventually converge. 12

In 2005, New York-based private equity firm AEA Investors, merged with Aetos Capital, a real estate and hedge fund firm. 13

10 Bank of America, Capital Eyes, 06/200511 Harvard Business School, Journal of Working Knowledge, 02/20/2006

12 Super Return Conference, Frankfurt, Germany, 02/23/200613 The Deal, 02/18/2005

CONVERGENCE OF PRIVATE FUNDS / HEDGE FUNDS

12

What to Expect in the Short Term

More Mergers Between Hedge and Private Equity Funds

More Private Equity Firms Launching Hedge Funds

More Hedge Funds Acting like Buyout Funds

A new breed of alternative investment that offers the investment flexibility of a hedge fund with a long-term investment profile of private equity

CONVERGENCE OF PRIVATE FUNDS / HEDGE FUNDS

13

Trend Towards Long Term Outlook

General Partners can no longer generate strong returns through financial engineering alone

Firms have shifted their strategy, increasing focus on “post acquisition” activities to add value:

Acquiring additional product lines through bolt-on acquisitions

In 1Q 2006, U.S. based PE firms completed at least 50 add-on acquisitions, one of every 4.5 deals closed 14

2005: One of Every 4.6 Deals; 2004: One of Every 6.5 Deals; 2003: One of Every 7 Deals 15

Enhancing Productivity / Growing Earnings

Roster of senior executives "on the bench" who work on specific projects

Specialization in sectors and partner with veterans to serve in executive management

Successful entrepreneurs can individually arrange financial backers

Longer Hold Periods are Now Needed to Actualize These Activities

Need for More “Patient Capital”

Public

KKR - $5B IPO / Apollo $1.5B – IPO

Apollo Failed to Raise its $2.5B Goal

Blackstone, Carlyle, Doughty Hanson have postponed plans for IPOs due to KKR’s poor performance 16

KKR Currently Trading Below Net Asset Value

Much of the capital invested in conservative instruments that return 2 – 3%, while charging a management fee that consumes almost as much as the return

Private

Lindsay Goldberg – Recently Closed New $3.1B, 20 Year Fund 1714 Buyouts, 04/05/2006 15 Buyouts, 04/05/2006

16 Wall Street Journal, 06/13/2006, Buyouts 10/06/200617 STRH Financial Sponsors Group, Capital IQ, 10/18/2006

TREND TO LONG TERM OUTLOOK

14

Perfect Storm of Circumstances

Historically Low Financing Costs

Substantial Liquidity

Flexible Debt Covenants

Robust Supply of Mezzanine Debt

Debt Market Receptive to Dividend Recapitalizations

ATTRACTIVE DEBT MARKETS ENVIRONMENT

15

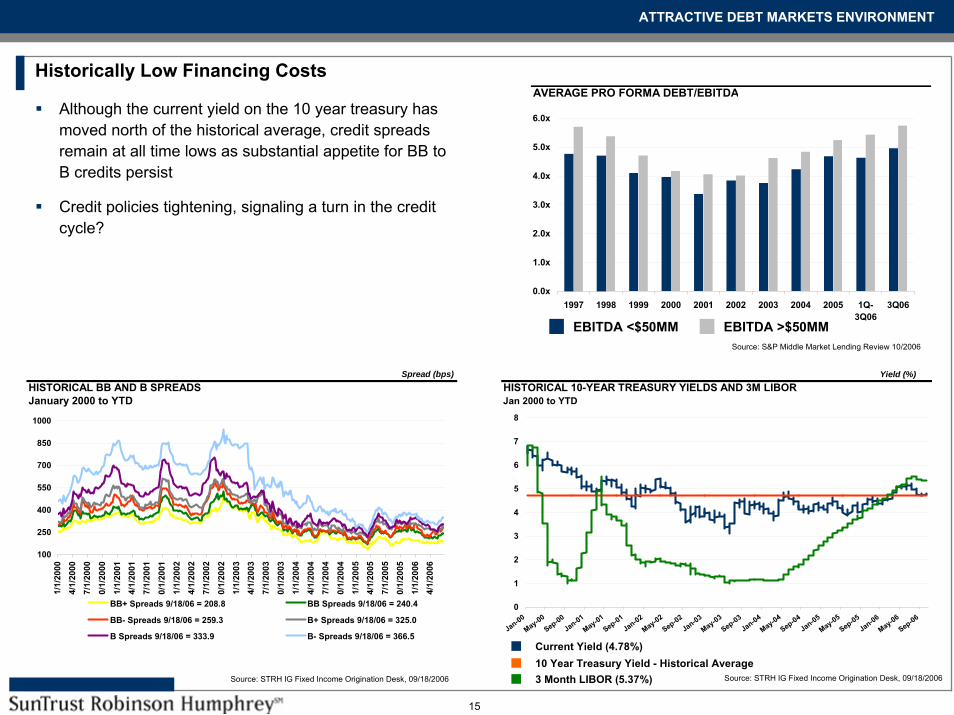

AVERAGE PRO FORMA DEBT/EBITDA

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

1997 1998 1999 2000 2001 2002 2003 2004 2005 1Q-3Q06

3Q06

Spread (bps)HISTORICAL BB AND B SPREADSJanuary 2000 to YTD

100

250

400

550

700

850

1000

1/1/

2000

4/1/

2000

7/1/

2000

10/1

/200

0

1/1/

2001

4/1/

2001

7/1/

2001

10/1

/200

1

1/1/

2002

4/1/

2002

7/1/

2002

10/1

/200

2

1/1/

2003

4/1/

2003

7/1/

2003

10/1

/200

3

1/1/

2004

4/1/

2004

7/1/

2004

10/1

/200

4

1/1/

2005

4/1/

2005

7/1/

2005

10/1

/200

5

1/1/

2006

4/1/

2006

BB+ Spreads 9/18/06 = 208.8 BB Spreads 9/18/06 = 240.4

BB- Spreads 9/18/06 = 259.3 B+ Spreads 9/18/06 = 325.0

B Spreads 9/18/06 = 333.9 B- Spreads 9/18/06 = 366.5

Yield (%)HISTORICAL 10-YEAR TREASURY YIELDS AND 3M LIBORJan 2000 to YTD

0

1

2

3

4

5

6

7

8

Jan-00May-00

Sep-00Jan-01

May-01Sep-01

Jan-02May-02

Sep-02Jan-03

May-03Sep-03

Jan-04May-04

Sep-04Jan-05

May-05Sep-05

Jan-06May-06

Sep-06

Historically Low Financing Costs

Although the current yield on the 10 year treasury has moved north of the historical average, credit spreads remain at all time lows as substantial appetite for BB to B credits persist

Credit policies tightening, signaling a turn in the credit cycle?

Source: STRH IG Fixed Income Origination Desk, 09/18/2006 Source: STRH IG Fixed Income Origination Desk, 09/18/2006

10 Year Treasury Yield - Historical AverageCurrent Yield (4.78%)

3 Month LIBOR (5.37%)

ATTRACTIVE DEBT MARKETS ENVIRONMENT

EBITDA >$50MMEBITDA <$50MMSource: S&P Middle Market Lending Review 10/2006

16

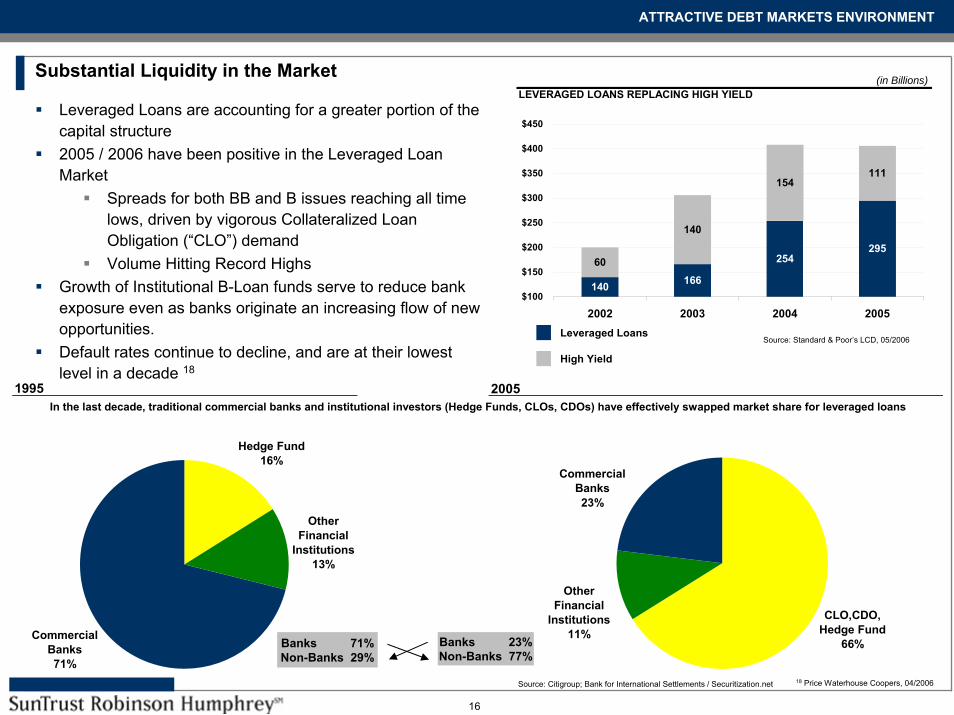

20051995In the last decade, traditional commercial banks and institutional investors (Hedge Funds, CLOs, CDOs) have effectively swapped market share for leveraged loans

Hedge Fund16%

Other Financial

Institutions13%

Commercial Banks71%

CLO,CDO, Hedge Fund

66%

Other Financial

Institutions11%

Commercial Banks23%

Leveraged Loans are accounting for a greater portion of the capital structure2005 / 2006 have been positive in the Leveraged Loan Market

Spreads for both BB and B issues reaching all time lows, driven by vigorous Collateralized Loan Obligation (“CLO”) demandVolume Hitting Record Highs

Growth of Institutional B-Loan funds serve to reduce bank exposure even as banks originate an increasing flow of new opportunities.Default rates continue to decline, and are at their lowest level in a decade 18

Substantial Liquidity in the Market

High Yield

Leveraged LoansSource: Standard & Poor’s LCD, 05/2006

Source: Citigroup; Bank for International Settlements / Securitization.net

Banks 71%Non-Banks 29%

Banks 23%Non-Banks 77%

ATTRACTIVE DEBT MARKETS ENVIRONMENT

18 Price Waterhouse Coopers, 04/2006

(in Billions)LEVERAGED LOANS REPLACING HIGH YIELD

140 166

254295

60

140

154111

$100

$150

$200

$250

$300

$350

$400

$450

2002 2003 2004 2005

17

Flexible Debt Covenants

Institutional and Pro Rata Loans

More borrowers are turning to the loan markets as they typically do not carry prepayment penalties 19

Explosive demand for CLO products has enabled less restrictive loan terms with fewer covenants and higher leverage levels

Quiznos Master LLC bypassed the HY market entirely

Quiznos sold a majority stake to JP Morgan Partners, debt financing provided ($925MM) entirely in first and second-lien debt

Public High Yield (“HY”)

Recent Public HY offerings during March and April (Nutro Products, AutoNation, Wood Resources and AngiotechPharmaceuticals) have all featured lower than normal call structures

Eight-year offerings by Angiotech, Nutro, and AutoNation had three year NC, while Wood Resources’ seven-year offering had a one-year NC

Issuers are getting the reduced NC provisions essentially for free

Bond investors are desperate enough for new paper to yield to the issuer’s demands without making them pay

19 Buyouts, 05/01/2006

ATTRACTIVE DEBT MARKETS ENVIRONMENT

18

Robust Supply of Mezzanine Debt

Three Month Libor has increased by almost 200 bps over the past 12 months, and has increased by about 90 bps since the beginning of 2006

2nd Lien no longer a more attractive option than fixed rate Mezzanine

Overall, the presence of 2nd Lien in middle market deals has declined dramatically from its peak

Economic Trends are Favorable for Mezzanine

Rising Interest Rates

Current Economic Cycle Drawing Closer to an End

Mezzanine lenders are reacting to the changing environment

Mezzanine Getting Cheaper

Three to four years ago, lenders were getting 18-20% interest rates inclusive of 6-7% warrants

Deals done today in the area of 14%, inclusive of 1-4% warrants.

Equity Co-Invest

ATTRACTIVE DEBT MARKETS ENVIRONMENT

Source: Merrill Lynch Middle Market Commentary, 09/2006

as % of Institutional Volume

SECOND-LIEN MIDDLE MARKET VOLUME($50MM EBITDA or Less)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 1Q-3Q06

3Q06

19

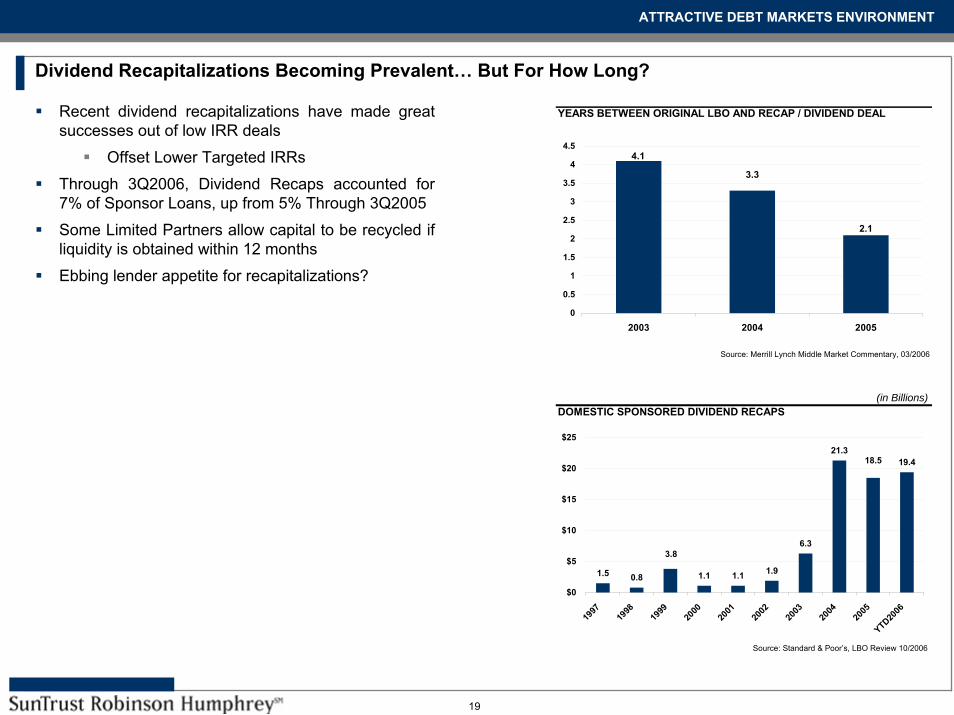

Recent dividend recapitalizations have made great successes out of low IRR deals

Offset Lower Targeted IRRs

Through 3Q2006, Dividend Recaps accounted for 7% of Sponsor Loans, up from 5% Through 3Q2005

Some Limited Partners allow capital to be recycled if liquidity is obtained within 12 months

Ebbing lender appetite for recapitalizations?

Dividend Recapitalizations Becoming Prevalent… But For How Long?

Source: Standard & Poor’s, LBO Review 10/2006

Source: Merrill Lynch Middle Market Commentary, 03/2006

ATTRACTIVE DEBT MARKETS ENVIRONMENT

(in Billions)DOMESTIC SPONSORED DIVIDEND RECAPS

1.5 0.8 1.1 1.1 1.9

6.3

21.319.4

3.8

18.5

$0

$5

$10

$15

$20

$25

1997

1998

1999

2000

2001

2002

2003

2004

2005

YTD2006

YEARS BETWEEN ORIGINAL LBO AND RECAP / DIVIDEND DEAL

2.1

4.1

3.3

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

2003 2004 2005

20

AVERAGE EQUITY CONTRIBUTION

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1997 1998 1999 2000 2001 2002 2003 2004 2005 1Q-3Q06

3Q06

Downward Pressure on Returns

20042003

LOWER RETURN EXPECTATIONS

Average EBITDA Multiples on the RiseLarger Deals More ExpensivePurchase price multiples for mid-market LBOs(<$50MM) remain at a 10 year high 20

Substantial LiquidityEstimates of $300B in funds available, $1T in purchasing powerEstimates of more than 100 funds with over $1B in management 21

Mega Funds Emerging ($10B +)Same Funds Chasing the Same Opportunities

Sponsor to Sponsor trades accounted for 16% of 1Q 2006 transactions 22

2005

20 Buyouts, 10/03/200621 Morgan Stanley, 05/05/200622 Buyouts, 04/03/2006

Source: Standard & Poor’s LBO Review 10/2006

Source: TA Associates, Annual LP Meeting, 2006

1Q-3Q 2006

Source: Standard & Poor’s LBO Review, 10/2006EBITDA >$50MMEBITDA <$50MM

TARGET RETURNS ON INVESTMENTS

0% 10% 20% 30% 40% 50% 60%

1998-2001

2001-2003

2004- Current

LBO PURCHASE PRICE / ADJUSTED EBITDA MULTIPLES

6.4

7.57.5

8.18.4

7.3

8.0

8.5

6.7 6.96.96.8

4x

5x

6x

7x

8x

9x

$100-$249MM $250-$499MM >$500MM

21

Expect Public Equities to Deliver 6-8% Returns

Expect Private Equity to Deliver 300-500 bps Over Public Equities

9-13% Returns

Big State Pension Funds and International Investors are Creating Overwhelming Demand

Good IRR Results and Distributions for 2005-2006

Will Sustain Demand for Several Years

Prefer Firms with Differentiated Strategies and Value Added

Target 18-22% Net Returns, will be Satisfied with 12-15%

LP Expectations

LOWER RETURN EXPECTATIONS