Presentación de PowerPoint - Bancóldex€¦ · · 2011-04-03• 2011 Colombian GDP’s forecast...

65

Bancóldex S.A. The Colombian Development Bank Figures as of December 31th 2010 March 2011

Transcript of Presentación de PowerPoint - Bancóldex€¦ · · 2011-04-03• 2011 Colombian GDP’s forecast...

Bancóldex S.A.The Colombian Development Bank

Figures as of December 31th 2010

March 2011

ColombiaEconomic Indicators

3

2007 2008 2009 2010* 2011f

GDP (USD bn) 207 243 235 273 313Real GDP growth (%) 6,3 2,7 0,8 4,2 4,6Annual Inflation (%) 5,7 7,7 2,0 3,2 3,6Fiscal Balance (% GDP) -0,6 -0,1 -2,7 -2,9 -3,0Current Account (%GDP -2,9 -2,8 -2,1 -2,5 -2,2

Exports f.o.b. (USD bn) 30,0 37,6 32,9 39,1 43,9

Imports f.o.b. (USD bn) 32,9 39,7 32,9 37,6 42,1

External Debt (USD bn) 44,6 46,4 53,7 59,6 63,8

External Debt (% GDP) 21,5 19,1 23,0 21,8 20,4

International Reserves (USD bn) 20,9 23,7 25,4 28,5 30,3

Sovereign rating :

Ba1 (Moody’s)

BB+ (Fitch & Duff & Phelps)

BB+ (Standard & Poor’s)

Outlook positive

Source: Banco de la República, Consensus Forecast, Dane , Bancoldex

Source: Ministerio de Hacienda

Colombia: general overview

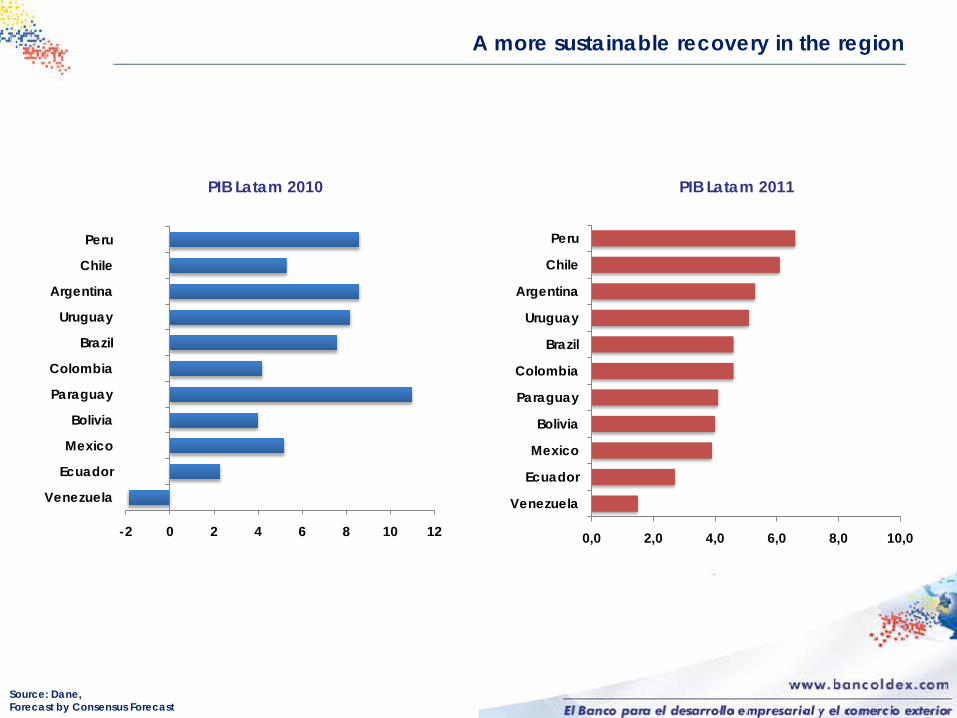

PIB Latam 2010 PIB Latam 2011

-2 0 2 4 6 8 10 12

Venezuela

Ecuador

Mexico

Bolivia

Paraguay

Colombia

Brazil

Uruguay

Argentina

Chile

Peru

0,0 2,0 4,0 6,0 8,0 10,0

Venezuela

Ecuador

Mexico

Bolivia

Paraguay

Colombia

Brazil

Uruguay

Argentina

Chile

Peru

A more sustainable recovery in the region

Source: Dane, Forecast by Consensus Forecast

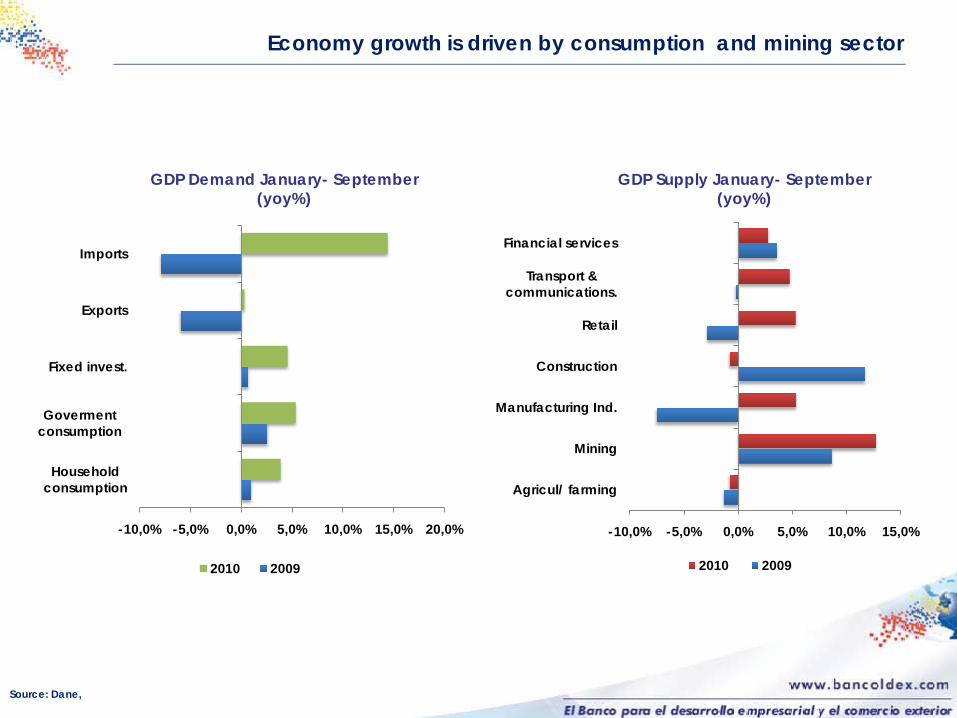

-10,0% -5,0% 0,0% 5,0% 10,0% 15,0%

Agricul/ farming

Mining

Manufacturing Ind.

Construction

Retail

Transport & communications.

Financial services

2010 2009

-10,0% -5,0% 0,0% 5,0% 10,0% 15,0% 20,0%

Household consumption

Goverment consumption

Fixed invest.

Exports

Imports

2010 2009

Economy growth is driven by consumption and mining sector

Source: Dane,

GDP Demand January- September(yoy%)

GDP Supply January- September(yoy%)

-20

-15

-10

-5

0

5

10

15

20

oct-

05

oct-

06

oct-

07

oct-

08

oct-

09

oct-

10-10

-5

0

5

10

15

20

25

oct-

05

oct-

06

oct-

07

oct-

08

oct-

09

oct-

10

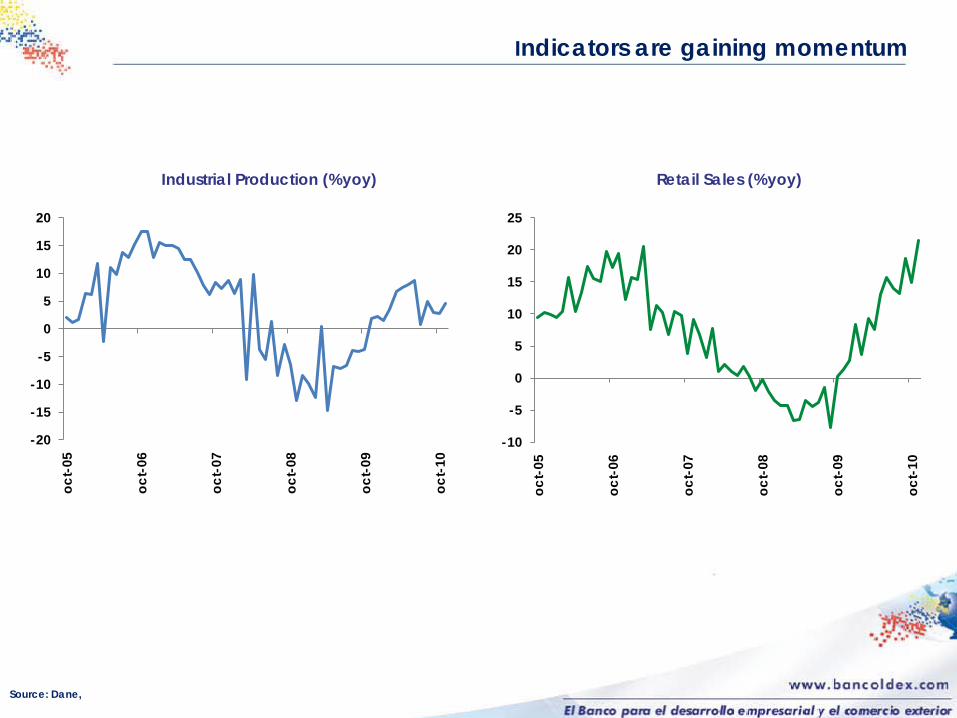

Source: Dane,

Indicators are gaining momentum

Industrial Production (%yoy) Retail Sales (%yoy)

35.974

22.904

13.070

29.663

16.06913.595

0

5000

10000

15000

20000

25000

30000

35000

40000

Total Traditional Non traditional

2010* 2009*

21,3%

42,5%

14,6%

63,4%

12,9%

36,8%

-3,9%

-20,0% 0,0% 20,0% 40,0% 60,0% 80,0%

Total

Traditional

Coffee

Oil & Derivates

Coal

Ferronickel

Non- Traditional

Source: Dane,

Foreign trade shows a better performance

ExportsJan – Nov (USD million)

ExportsJan – Nov 2010 (% yoy)

Expo

rtsIm

ports

By country By sector/ product

Trade structure

USA42,1%

Others 34,9%

China5,2%

Ecuador4,5%

Netherlands

4,1%

Venezuela3,6%

Peru2,9%

Brazil2,7%

USA25,8%

Others38,0%

China13,1%

Mexico9,5%

Brazil5,9%

Germany4,2% Argentina

3,5%

Consumption Goods

34%

Raw Materials

and Intermediate Products

30%

Capital Goods and Construction

Materials11%

Others6%

Coffee4,4%

Oil & Derivates

41,2%

Coal15,6%

Ferronickel2,4%

Non-Traditional

36,3%

Source: Dane,

4,5

5,7

7,7

2

3,173,57

2006 2007 2008 2009 2010 2011p

25,53

17,85

15,56

15,65

9,50

17,85

10,04

6,54

5,90

3,0

0 10 20 30

Consumption

Ordinary

Preferential

Treasury

Central Bank Jan-11

Source: Dane, Banco de la República

An effective monetary policy led to decrease interest rates.Inflation is according to Central Bank range target

Commercial Interest Rates(%)

Inflation(CPI annual variation %)

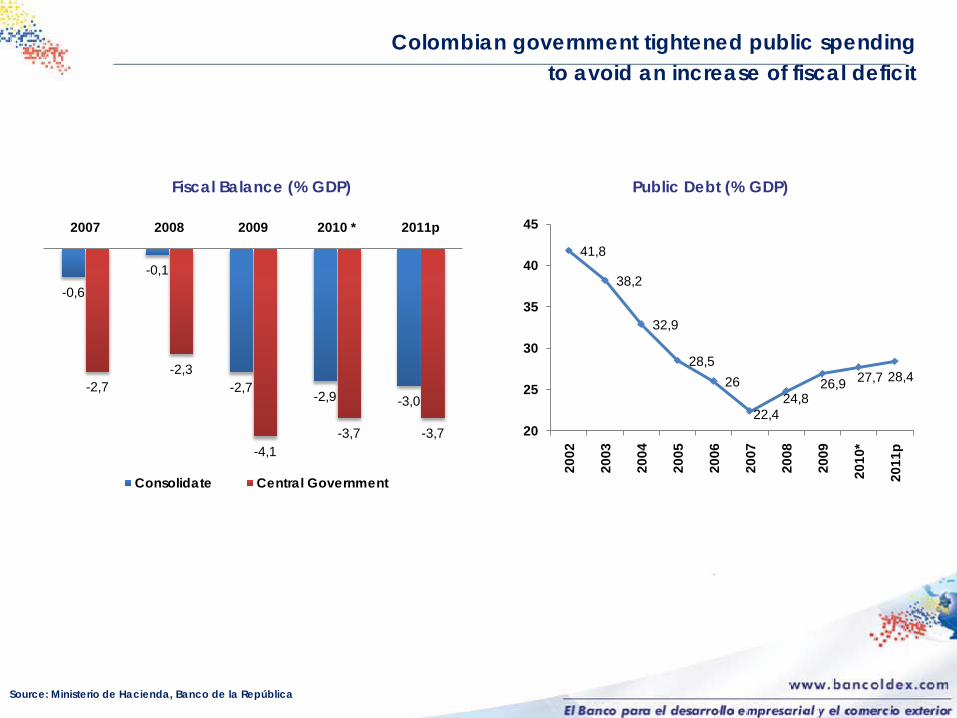

41,8

38,2

32,9

28,526

22,424,8

26,9 27,7 28,4

20

25

30

35

40

45

2002

2003

2004

2005

2006

2007

2008

2009

2010

*

2011

p

-0,6-0,1

-2,7-2,9 -3,0

-2,7-2,3

-4,1-3,7 -3,7

2007 2008 2009 2010 * 2011p

Consolidate Central Government

Source: Ministerio de Hacienda, Banco de la República

Colombian government tightened public spending to avoid an increase of fiscal deficit

Fiscal Balance (% GDP) Public Debt (% GDP)

0100200300400500600700

ene-

08ab

r-08

jul-0

8

oct-

08

ene-

09ab

r-09

jul-0

9

oct-

09

ene-

10ab

r-10

jul-1

0

oct-

10

ene-

11

Colombia

Brazil

Peru

Mexico

Chile

140

770

163

133

1010

518

125

0 200 400 600 800 1000 1200

Colombia

Ecuador

Brasil

Perú

Venezuela

Argentina

México

CDS

Source: Bloomberg Source: Bloomberg, JP Morgan. September 2010

EMBI Index

Easy of Doing Business

Low country risk and good business enviroment

172149

130127

124115

10643

393635

0 50 100 150 200

VenezuelaBolivia

EcuadorBrazil

UruguayArgentinaParaguay

Chile Colombia

PeruMexico

Source: Doing Business. position on 180 countries)

Colombia Financial System Indicators

12

Source: Superintendencia Financiera

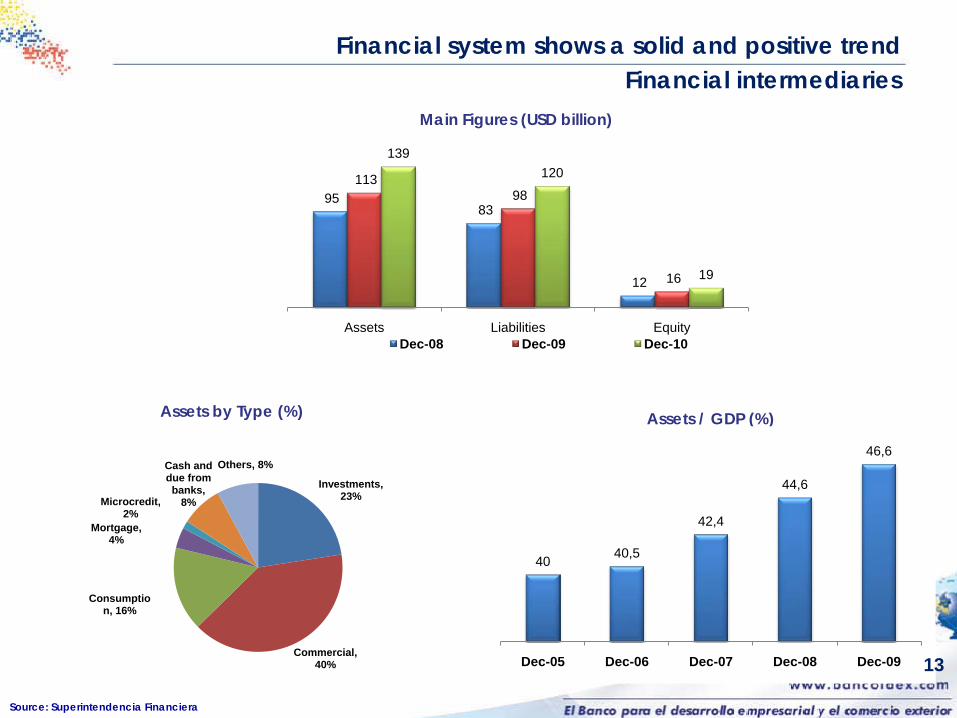

Financial system shows a solid and positive trendFinancial intermediaries

Assets by Type (%) Assets / GDP (%)

40 40,5

42,4

44,6

46,6

Dec-05 Dec-06 Dec-07 Dec-08 Dec-09

Main Figures (USD billion)

13

Investments, 23%

Commercial, 40%

Consumption, 16%

Mortgage, 4%

Microcredit, 2%

Cash and due from banks,

8%

Others, 8%

95 83

12

113 98

16

139120

19

Assets Liabilities EquityDec-08 Dec-09 Dec-10

Source: Superintendencia Financiera

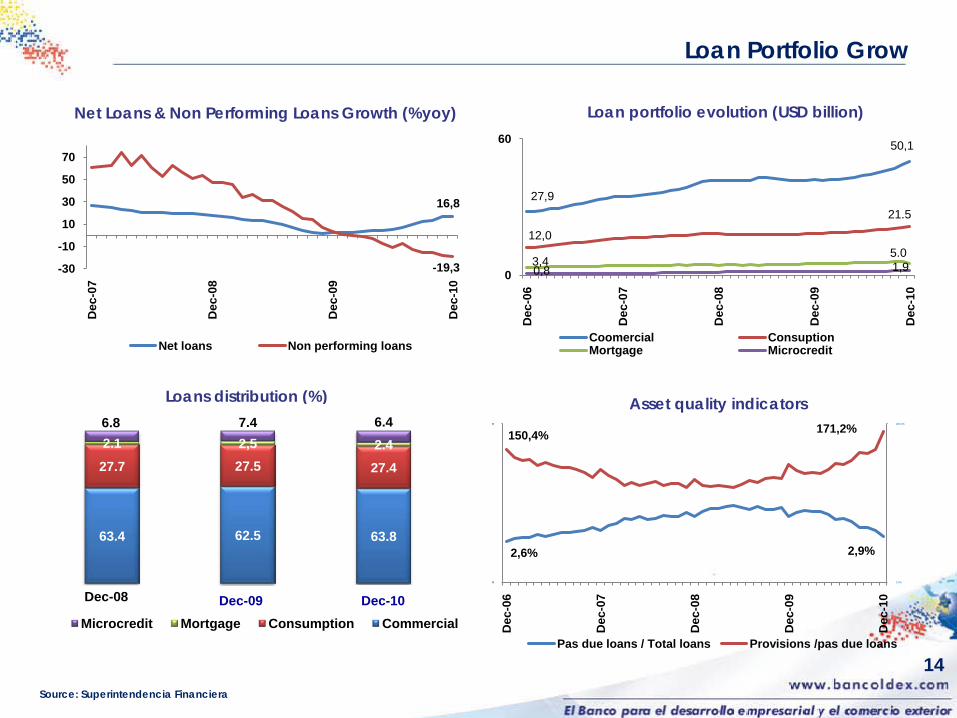

Loan Portfolio Grow

Asset quality indicatorsLoans distribution (%)

Loan portfolio evolution (USD billion) Net Loans & Non Performing Loans Growth (%yoy)

14

63.4 62.5 63.8

27.7 27.5 27.4

2.1 2,5 2.46.8 7.4 6.4

Microcredit Mortgage Consumption Commercial

Dec-08 Dec-09 Dec-10

27,9

50,1

12,0

21.5

3,45.0

0,8 1,90

60

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Coomercial ConsuptionMortgage Microcredit

2,6% 2,9%

150,4% 171,2%

0,0%

180,0%

0

0

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Pas due loans / Total loans Provisions /pas due loans

16,8

-19,3-30

-10

10

30

50

70

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Net loans Non performing loans

Source: Superintendencia Financiera

Despite the crisis, banks exhibited adequate indicatorsof liquidity and solvency

Solvency index evolution (%)

Liquidity ratio (%)

Profits (USD million)

* Profits between January 2010 – December 2010 15

Profitability (%)

6,60%7,90%

0%

12%de

c-06

dec-

07

dec-

08

dec-

09

dec-

10

1.488 1.563 1.836

2.139

2.642 3.062

-

500

1.000

1.500

2.000

2.500

3.000

3.500

dec-05 dec-06 dec-07 dec-08 dec-09 dec-10

2,5%

20,4%

7,2%

2,6%

18,6%

6,2%

0%

5%

10%

15%

20%

25%

ROAA ROAE Admon expenses / Assets

Dec-08 dec-09 dec-10

12,75

15,0

12

13

14

15

16

17

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

• 2011 Colombian GDP’s forecast will be between 3,5%- 5,5%

• Inflation expectation are trading well according of Central Bank’smedium target

• The current interest rates levels will help the economic growth

• The fiscal rule will lead to major stability in public finance

• Net loans show a recovery

• Lower risk aversion will lead to a local investment growth

• Financial system is solid and solvency will improve due to higher levelof retained earnings

• Financial institutions will remain with higher levels of liquidity

Conclusions

Table of Content1. Bancoldex

A. Nature of Bancóldex

B. Colombian law

C. Financial Structure

D. Organizational Structure

E. Strategic Action framework 2010-2015

F. Transformation Evolution Process

G. Bancoldex Special Programs• Futurex Microinsurance Program

• Bancoldex Entrepreneurial Center - CEB

• “aProgresar” Program• Bancóldex Capital Program

• Banca de las Oportunidades Program

Bancóldex

A. Nature of Bancóldex

Development Agency Of the Colombian Government

• State owned commercial bank

• Corporation by shares

• Incorporated as a mixed-capital

company

• It operates under the same legal

regime as private sector financial

institutions

Dec - 10 %

Ministry of Trade, Industry and Tourism 786.080.862 91,9%Ministry of Finance 67.177.642 7,9%Others 2.411.119 0,2%

Total 855.669.623 100%

Shareholders

N° Shares

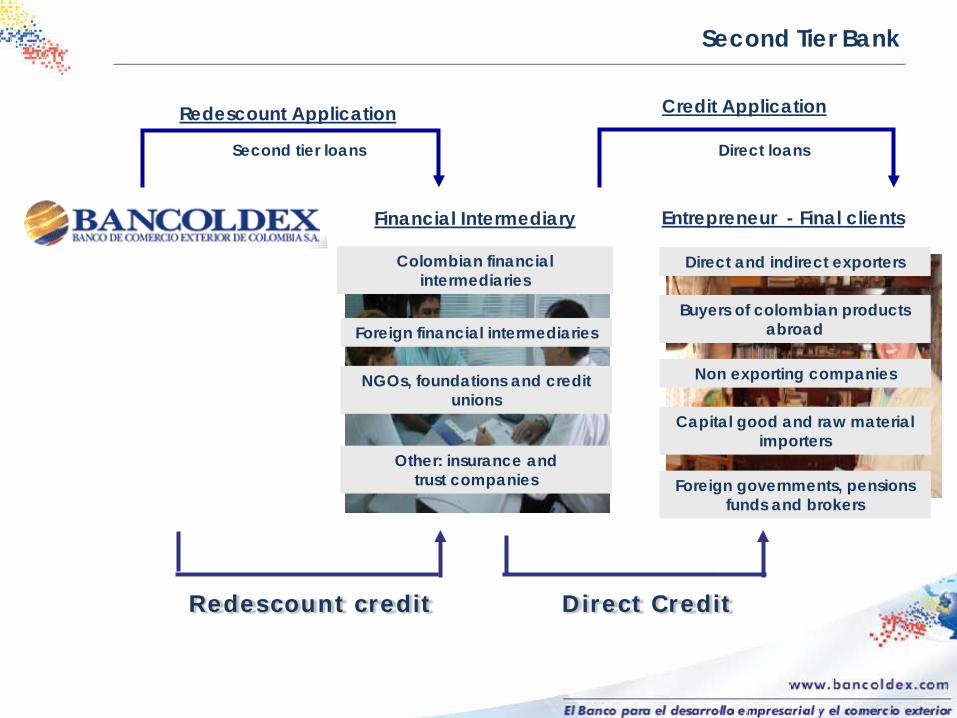

BANCÓLDEX

Colombian financialintermediaries

Entrepreneur - Final clients

Second tier loans Direct loans

Direct and indirect exporters

Buyers of colombian productsabroad

Non exporting companies

Capital good and raw material importers

Foreign governments, pensionsfunds and brokers

NGOs, foundations and creditunions

Other: insurance andtrust companies

Foreign financial intermediaries

Financial Intermediary

Second Tier Bank

Redescount Application

Redescount credit Direct Credit

Credit Application

B. Colombian Law

Colombian Law– Bills

• Bill N° 107/10C. Indemnification of victims of crimes against HumanRights and International Humanitarian Law.This Bill contemplates economical and welfare measures in favor ofvictims of crimes, against Human Rights and InternationalHumanitarian Law (state indemnification, land and assets restitution,etc).

• Bill N° 91/S. Financial services charges.This Bill grants to the Banking Superintendence the power to issueregulations about the maximum prices of financial services charges.In addition, the Bill contemplates the obligation of uploading thecharges on the financial institutions’ Web sites.

Colombian Law– Bills

• Bill N° 96/10S. Access to credit for poor people.This Bill contemplates a special obligation for Banks to offer microcreditloans to encourage formal creation of companies. In addition, the Billestablishes that the Banks must allocate a specific percentage of theirresources to the mentioned loans.

• Bill N° 179/11C The National Development Plan (2010-2014)

It contemplates a percentage from the profits of Bancoldex in orderto design and implement a Development Unit intended to performdifferent activities related to development banking; it also includesfinancing for projects and programs created by that Unit.

Colombian Law– Bills

• Bill N° 53/10C – 163/10S. It gives extraordinary faculties to thePresident to modify the structure of the national administration

This government bill gives extraordinary faculties to the ColombianPresident to split and to reorganize the Ministries of Interior andJustice, Social Protection and Environment, and Housing andTerritorial Development.

• Bill N° 178/11C allows financial consumers to make prepayments inany credit transaction

This bill allows financial consumers to make prepayments regardlessthe nature of the credit transaction, in whole or in part, along withinterests accrued until the date of payment, as well as otherapplicable charges.

• Act 1429 of 2010 “Formalization and First Job”

The objective of this act is to implement an economic and taxincentives to the creation and formalization of companies with lessthan 50 employees. It also provides incentives for the payment ofsocial security payments and fringe benefits for small businesses thatemploy people under 25 years.

• Act 1430 of 2010 promulgation of control and taxcompetitiveness rules

This act establishes a special tax deduction for investment in fixedassets; it includes incentives such as the exemption of the specialcontribution to the electricity industry; it also increases productivityFinancial Transactions Tax, by restricting certain practices speciallystructured to avoid the payment of such tax by the taxpayers. Finallyit implements some control measures aimed at better tax collection.

Colombian Law

• Act 1425 de 2010 abolishes two articles (39 and 40) of Act 472 of 1998- Class ActionThis act abolishes two articles of Act 472 of 1998 concerningeconomic incentives that were stated to the plaintiff in a classaction.

Colombian Law

C. Financial structure

98.821

0

30.000

60.000

90.000

120.000

Dec-07 Dec-08 Dec-09 Dec-10

CO

P M

illio

n

Net income

5.546.339

0

2.000.000

4.000.000

6.000.000

Dec-07 Dec-08 Dec-09 Dec-10

CO

P M

illio

n

Assets

4.164.001

0

1.500.000

3.000.000

4.500.000

Dec-07 Dec-08 Dec-09 Dec-10

CO

P M

illio

n

Liabilities

1.382.338

0

500.000

1.000.000

1.500.000

Dec-07 Dec-08 Dec-09 Dec-10

CO

P M

illio

n

Equity

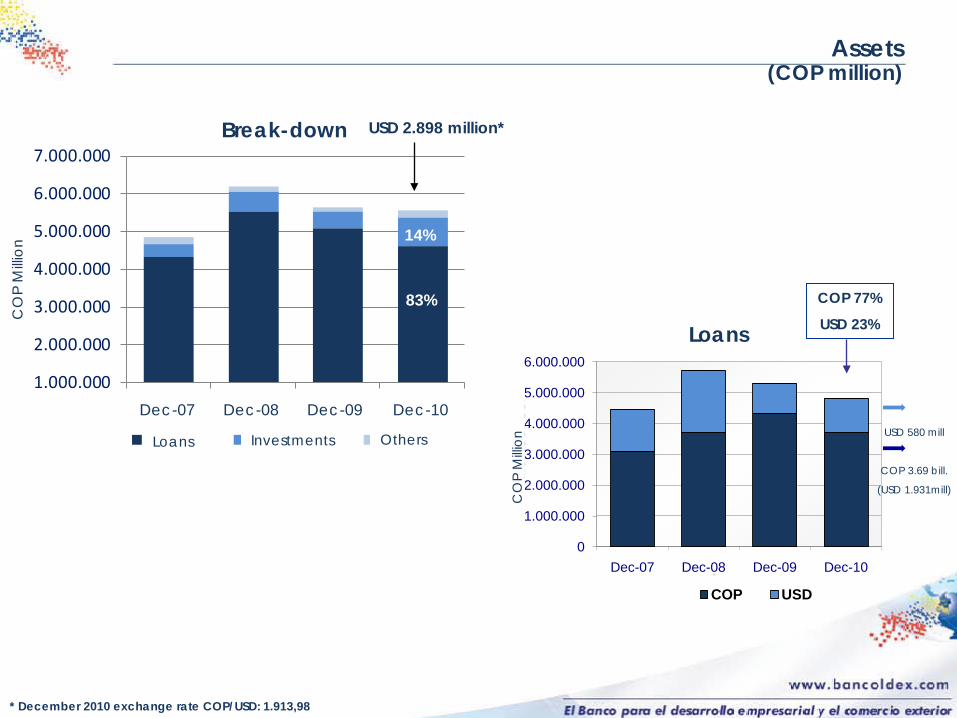

Financial StructureUSD 2.898 million* USD 2.176 million*

USD 52 million*USD 722 million*

* December 2010 exchange rate COP/USD: 1.913,98

1.000.000

2.000.000

3.000.000

4.000.000

5.000.000

6.000.000

7.000.000

Dic-07 Dic-08 Dic-09 Dic-10

Mill

ones

de

COP

Cartera Inversiones Otros

0

1.000.000

2.000.000

3.000.000

4.000.000

5.000.000

6.000.000

Dec-07 Dec-08 Dec-09 Dec-10

Millo

nes

de C

OP

COP USD

83% COP 77%

USD 23%

14%

Assets(COP million)

Break-down

Loans Investments Others

CO

P M

illion

Loans

CO

P M

illion

Dec-07 Dec-08 Dec-09 Dec-10

USD 2.898 million*

* December 2010 exchange rate COP/USD: 1.913,98

USD 580 mill

COP 3.69 bill.

(USD 1.931mill)

0

1.000.000

2.000.000

3.000.000

4.000.000

5.000.000

6.000.000

Dic-07 Dic-08 Dic-09 Dic-10

Mill

ones

de

COP

CDT's Bonos Otros Repos Corresp. y MultilatCDT's Bonds Others Repos Other banks

4.164.001

0

1.500.000

3.000.000

4.500.000

Dec-07 Dec-08 Dec-09 Dec-10

CO

P M

illio

n

Liabilities(COP million )

Evolution

27%

39%

31%

USD 2.176 million*

Break-down

CO

P M

illion

Dec-07 Dec-08 Dec-09 Dec-10

* December 2010 exchange rate COP/USD: 1.913,98

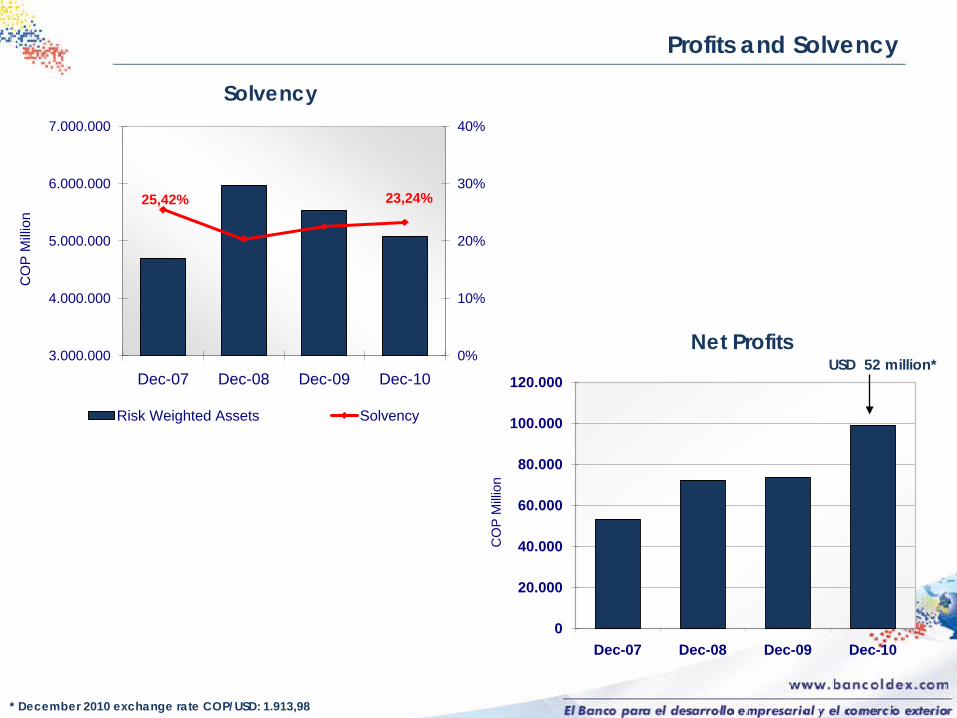

Profits and Solvency

0

20.000

40.000

60.000

80.000

100.000

120.000

Dec-07 Dec-08 Dec-09 Dec-10

CO

P M

illion

Net ProfitsUSD 52 million*

Solvency

25,42% 23,24%

0%

10%

20%

30%

40%

3.000.000

4.000.000

5.000.000

6.000.000

7.000.000

Dec-07 Dec-08 Dec-09 Dec-10

CO

P M

illio

n

Risk Weighted Assets Solvency

* December 2010 exchange rate COP/USD: 1.913,98

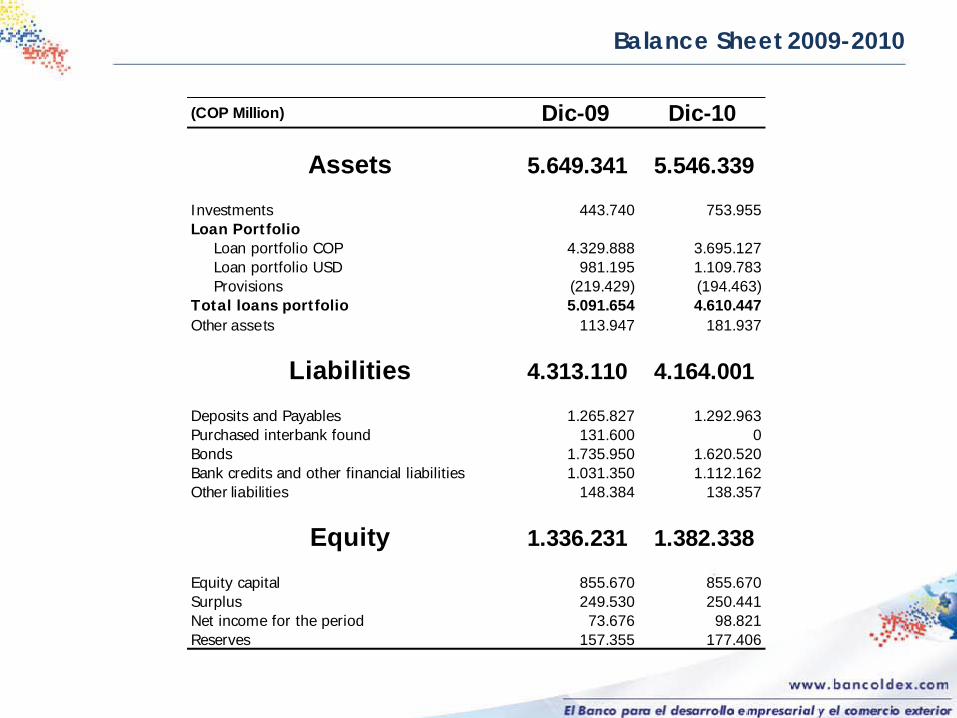

(COP Million) Dic-09 Dic-10

Assets 5.649.341 5.546.339

Investments 443.740 753.955Loan Portfolio

Loan portfolio COP 4.329.888 3.695.127Loan portfolio USD 981.195 1.109.783Provisions (219.429) (194.463)

Total loans portfolio 5.091.654 4.610.447Other assets 113.947 181.937

Liabilities 4.313.110 4.164.001

Deposits and Payables 1.265.827 1.292.963Purchased interbank found 131.600 0Bonds 1.735.950 1.620.520Bank credits and other financial liabilities 1.031.350 1.112.162Other liabilities 148.384 138.357

Equity 1.336.231 1.382.338

Equity capital 855.670 855.670Surplus 249.530 250.441Net income for the period 73.676 98.821Reserves 157.355 177.406

Balance Sheet 2009-2010

COP Million Dic-09 Dic-10

Financial income 494.843 349.455Financial expenses 299.913 197.960Forwards 6.483 9.662Net exchange gain/loss 1.103 (4.584)Financial margin before provisions 202.515 156.573Provisions 41.768 (19.748)Net financial margin 160.747 176.321 Other operational incomes 6.521 9.093 Operational expenses 81.288 83.197 Operational margin 85.980 102.217 Non operational incomes 2.022 12.256 Non operational expenses 583 1.420 Profit before taxes 87.419 113.052 Taxes 13.743 14.231 Net Profit 73.676 98.821

Income Statement 2009-2010

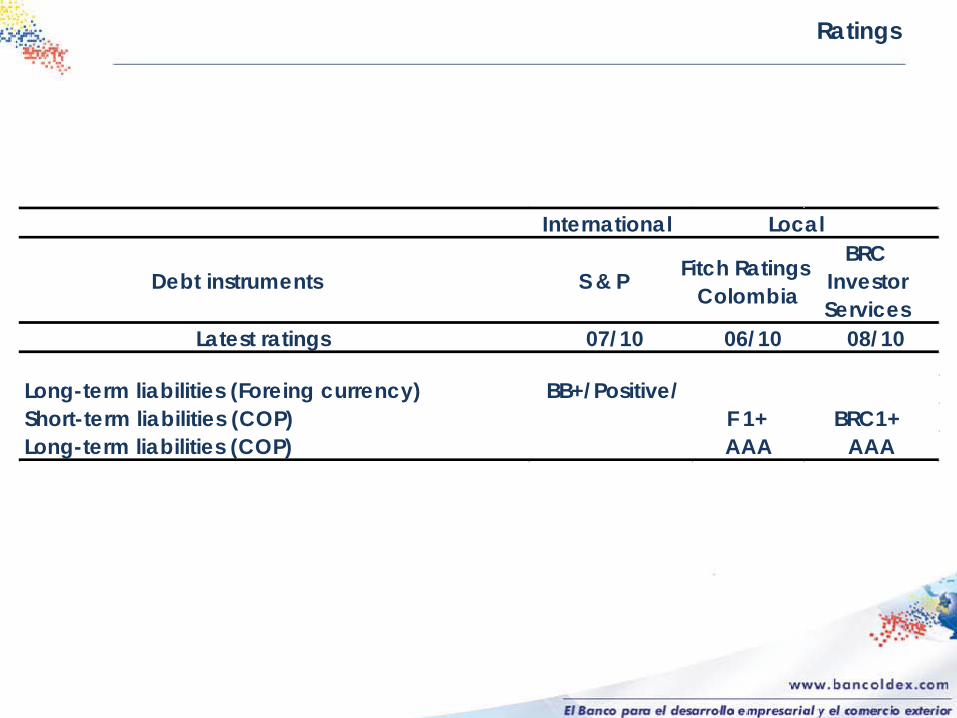

Ratings

International

Debt instruments S & P Fitch RatingsColombia

BRC Investor Services

Latest ratings 07/10 06/10 08/10

Long-term liabilities (Foreing currency) BB+/Positive/Short-term liabilities (COP) F 1+ BRC1+Long-term liabilities (COP) AAA AAA

Local

D. Organizational Chart

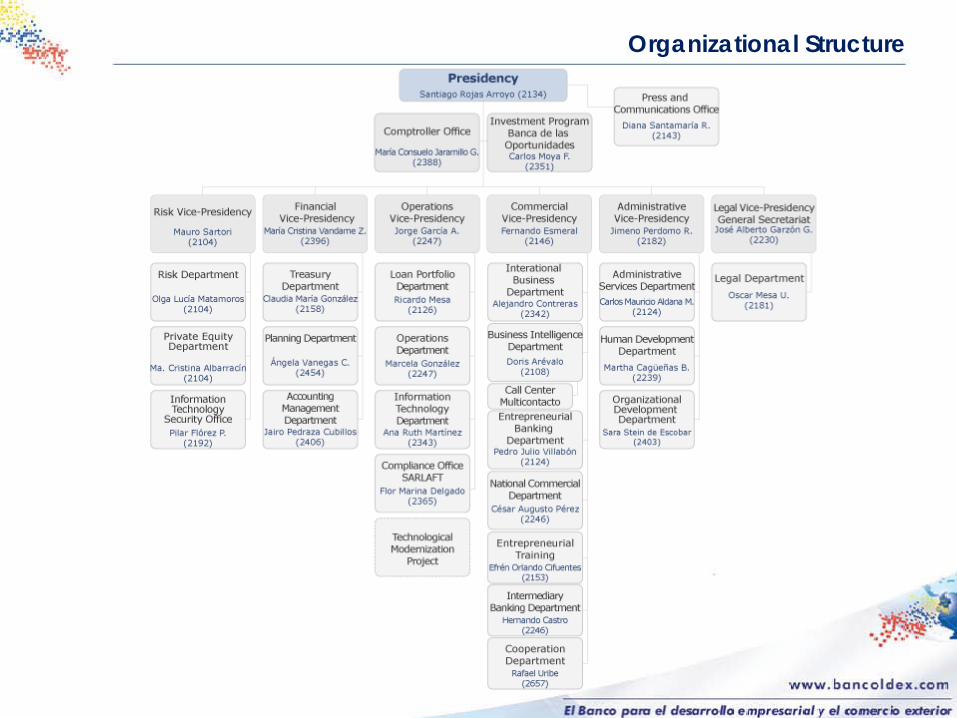

Organizational Structure

E. Strategic Action Framework2010-2015

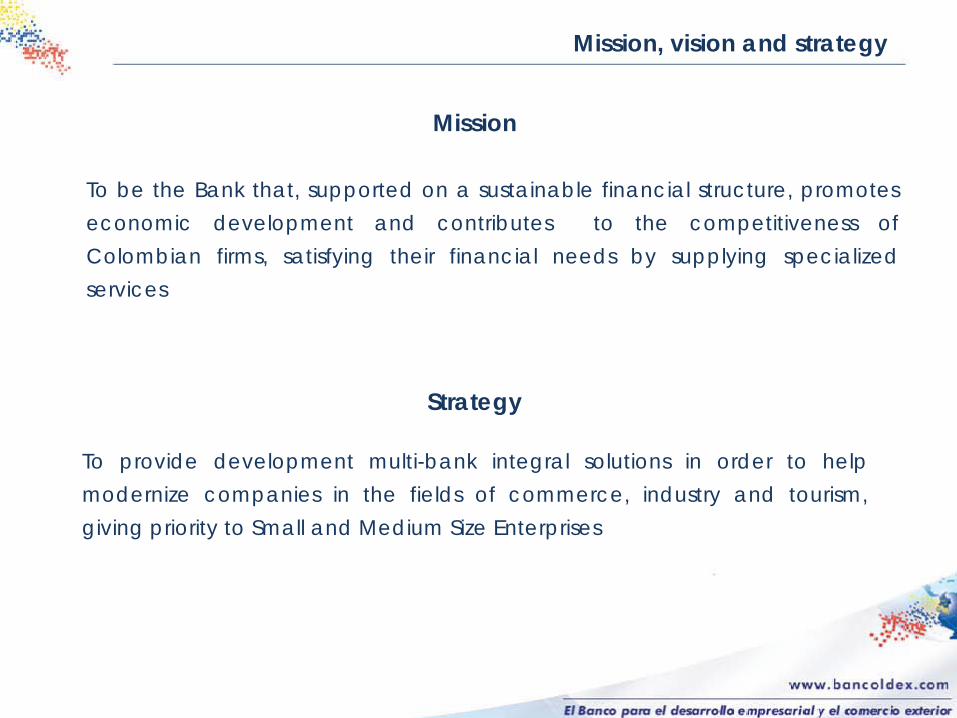

Mission

To be the Bank that, supported on a sustainable financial structure, promoteseconomic development and contributes to the competitiveness ofColombian firms, satisfying their financial needs by supplying specializedservices

Mission, vision and strategy

Strategy

To provide development multi-bank integral solutions in order to helpmodernize companies in the fields of commerce, industry and tourism,giving priority to Small and Medium Size Enterprises

Organizational Effectiveness

Financial SustainabilityGuarantee

ProductiveTransformation

and entrepreneurialdevelopment

Priorities and areas of action Inside actions

Internacionali-zation

Strategy

Bancóldex as a Government Agency

Environmental and social

strategy

Cooperation (resources from third parties)

Development Multi-Bank

Financial Instruments

Development AgencyNonfinancialinstruments

BankarizationSocial inclusion

and EntrepreneurFormalization

Entrepreneurial training Program

Strategic Action Framework 2010-2015

F. Transformation processFrom “Ex-Im Bank” to

“Entrepreneurial development and Ex-Im Bank”

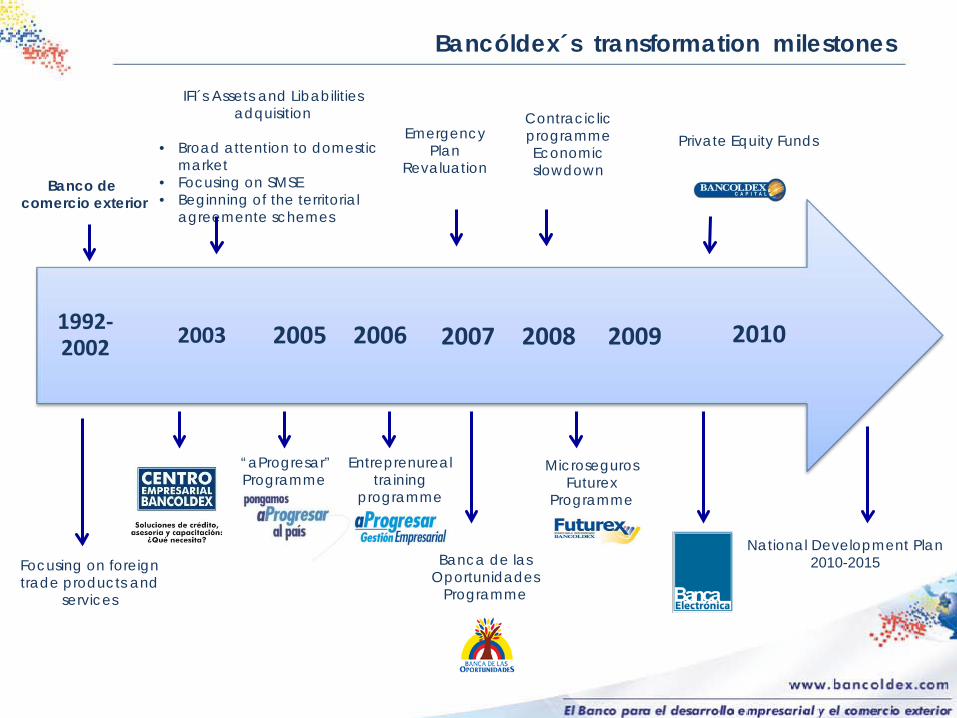

Bancóldex´s transformation milestones

2007 2010200920082006200520031992-2002

Banco de comercio exterior

IFI´s Assets and Libabilitiesadquisition

• Broad attention to domesticmarket

• Focusing on SMSE • Beginning of the territorial

agreemente schemes

“aProgresar” Programme

Banca de las Oportunidades

Programme

ContraciclicprogrammeEconomicslowdown

Private Equity Funds

MicrosegurosFuturex

Programme

National Development Plan 2010-2015

EmergencyPlan

Revaluation

Entreprenurealtraining

programme

Focusing on foreigntrade products and

services

Provide a wide portfolio of financial products and services (multi-banking), in order to support modernization of companies in the fields of commerce, industry and tourism, giving priority to Small and Medium Sized Enterprises(SMSE)

Specialized

banking

Development

banking

Development

Multi-banking

2002 2006 2010

Loans

Entrepreneurial training

Foreign trade and foreign banks

Factoring

Other

2006Loans

Collaterals

Entrepreneurial training

Foreign trade and foreign banks

Treasury products

Insurance services

Factoring

Development Agency and“Banca de las oportunidades”

Private equity

2010

Strategic Proposal

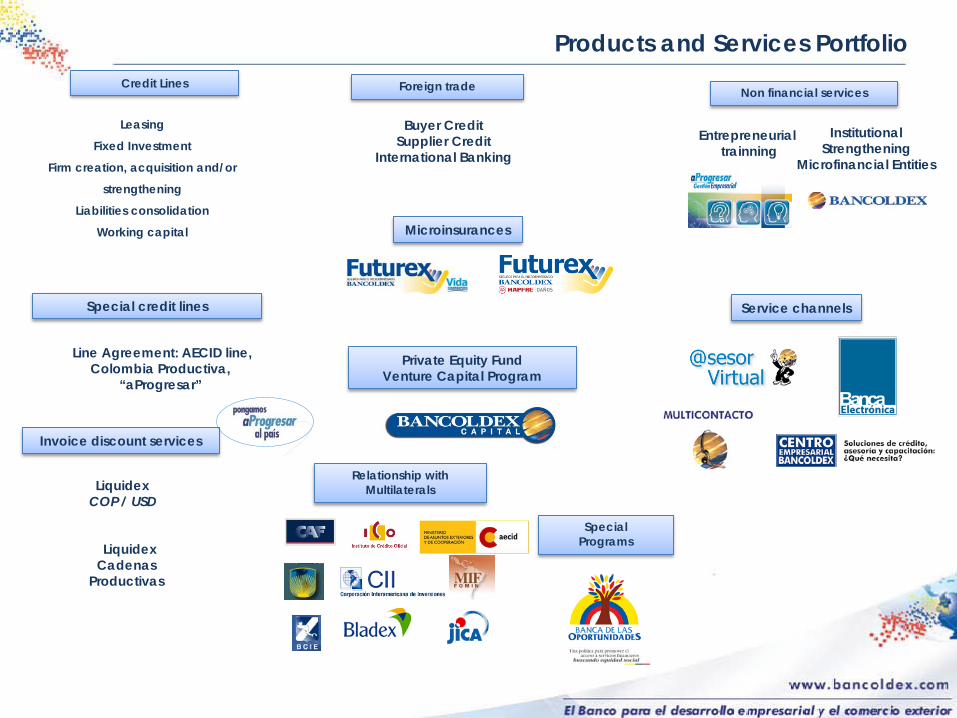

Entrepreneurial trainning

Line Agreement: AECID line, Colombia Productiva,

“aProgresar”

Buyer CreditSupplier Credit

International Banking

Leasing

Fixed Investment

Firm creation, acquisition and/or

strengthening

Liabilities consolidation

Working capital

Credit Lines

LiquidexCOP / USD

Liquidex Cadenas

Productivas

Special credit lines

Invoice discount services

Service channels

InstitutionalStrengthening

Microfinancial Entities

Non financial services

Microinsurances

Private Equity FundVenture Capital Program

Foreign trade

Products and Services Portfolio

Relationship withMultilaterals

Special Programs

Corporation74%

SMES8%

Microfirms0%

Others18%

2002

Transformation Process 2002 - 2010

Working capital

55%Modernizatio

n16%

Others29%

Short57%

Medium26%

Long17%

Long term financing

Enterprises modernization

SMSE´s focus Corporation29%

SMES36%

Microfirms16%

Others19%

2010

Working capital

68%

Modernization25%

Others7%

Short52%

Medium24%

Long24%

Disbursements as of Dec 2010: COP 3.543.511 mill.

Socioeconomic ImpactMicrofirms assisted

Regional coverage

SME assisted

112%

0

30000

60000

90000

120000

150000

63.481

107.580

110.021

141.694

130.213126.048

76%

0

1000

2000

3000

4000

5000

6000

7000

8000

6.374 6.397 6.745 6.701

7.596

6.616

109%

400

500

600

700

800

591

666 670 690

633

757

591

666 670690

633

757

Departaments No. Institutions

Dec-08 Dec-09 Dec-10Cundinamarca 21 27 23Antioquia 15 18 17Santander 14 15 14Valle/Cauca 8 9 8Tolima 6 6 5Atlántico 4 4 3Nariño 4 4 3Bolívar 4 4 3Caldas 3 3 2Huila 3 3 5Quindío 3 3 3Risaralda 3 2 2Guajira 2 2 -Nte Santander 2 2 2Meta 2 2 2Putumayo 2 2 1Arauca 2 2 2Boyacá 2 2 2Guainía 1 1 -Córdoba 1 - -Magdalena 1 1 1Casanare 1 1 2Cauca - - 1

Total 104 113 101

Microl-oans (regional coverage)

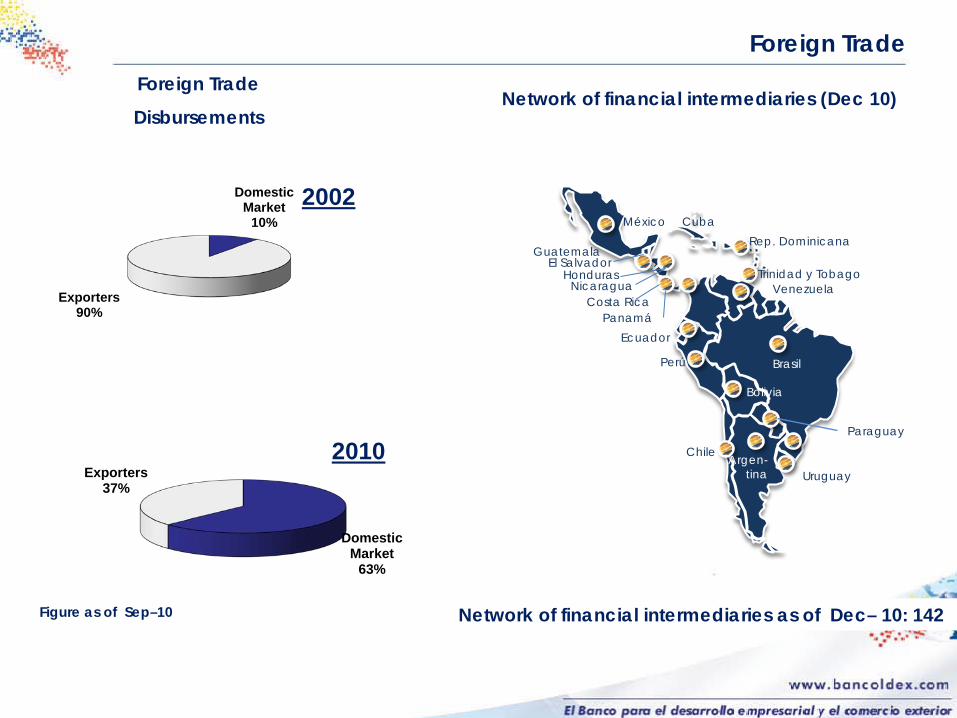

Foreign TradeForeign Trade

Disbursements

Domestic Market

10%

Exporters90%

Domestic Market

63%

Exporters37%

2002

2010

Network of financial intermediaries as of Dec– 10: 142

Network of financial intermediaries (Dec 10)

Figure as of Sep–10

Brasil

Bolivia

Ecuador

Perú

Chile

Venezuela

México

GuatemalaEl Salvador

HondurasNicaragua

Costa RicaPanamá

CubaRep. Dominicana

Trinidad y Tobago

Paraguay

UruguayArgen-

tina

• Futurex Microinsurance Program

• Bancoldex Entrepreneurial Centers- CEB

• “aProgresar” Program

• Bancoldex Capital Program

• Banca de las Oportunidades Program

G. Bancoldex Special Programs

Microinsurance

• Microinsurance Program FUTUREX – LIFE INSURANCE a joint effort of Government and private sector for low income micro entrepreneurs population.

• It is sold through Microfinancial Institutions – with credit line in Bancoldex. It is a low cost insurance policy that reduces the social vulnerability of microfirms and their families. The insurance also covers the loan portfolio of the Microfinancial Institution

Damages

• It offers coverage in case of death, incapability to work, critical illness, burial costs aid, and family ongoing living expenses aid.

• This insurance policy covers the microfirms premises and other property, including home if it is located in the same building, from damages caused by:

•Acts of Nature•Malicious damage or vandalism•Robbery•Loss of business income

Microinsurance

1. COOTREGUA-Puerto Inírida y

San José del Guaviare.

2. COOHOGARES-Pasto

3. COMFAMA-Medellín

4. F. San Jerónimo-Montería

5. FUNDEMICROMAG-Sta. Marta

6. Actuar Tolima

7. CORPROEM-Boyacá

8. F. Alcaraván-Arauca

9. ASOCOOP-Putumayo

10.COOPAC-Bogotá

11.ASOEMPRO-Bogotá

12.Coop. San Simon-Tolima

1. CORPROEM

2. F. Alcaraván

3. ASOCOOP

4. COOPAC

5. ASOEMPRO

6. Crezcamos

7. Contactar

8. F. Mario Santo Domingo

9. Coop. San Simón

10.F. Mundial de la Mujer

Bucaramanga

11.COOPFUTURO

12.FUNDESAN

• Insured*: 69.709*

• Insurable value: COP 249.800mill.• Insured*: 19.562*

• Insurable value: COP 94.500 mill.

* Figures as of December 2010 * Figures as of November 2010

CEB: Bogotá - Cali - Barranquilla - Bucaramanga - Pereira

TOTAL

Total Disbursements:COP 20.515 Milion

Number of transactions:1.647

Visitors:12.216 people

Trainned people:11.866

Average Credit: COP 12 Milion

Bancoldex Entrepreneurial Centers -CEBAs of Dec-10

The Entrepreneurial Centers – CEB are specialized offices created to provide financial, legal and managerial assistance to micro and small firms

COLLATERALSENTREPRENEURIAL SUPPORTCREDITS

Participating Institutions

aProgresar Program

Managerial and financial support program to spur productivity and

competitiveness

This training program was design to offer management tools to SME´s entrepreneurs, in order to improve the performance and competitiveness of the Colombian enterprises.

2007 -2010Trainned

entrepreneurs

GeographicalcoverageJan- Dec

2010

39.047

2007 - 31 cities2008 - 33 cities2009 - 37 cities2010 - 48 cities

12.871Trainned entrepreneurs

Entrepreneurial Training Program

Type of programs• Management training seminars• Conferences, workshops and short courses• Consultancy and assistance• Web courses• E-learning

Allies

Chambers of comerce Associations

Bancoldex Capital Program

Bancoldex Capital Program

Make available to Colombiancompanies new sources of long-termfinancing through capital fresh of theprivate equity funds

Promote private equity and venturecapital industry in the country

Attract new investors, local andforeign, to participate in the privateequity industry in the country

Bancoldex Capital Program promotes the private equity and venture capitalindustry in Colombia

Financial support

Investment in PrivateEquity and VentureCapital Funds

Bancóldex does notinvest directly incompanies

Non financial supportBancóldex willcontribute to theconstruction of theecosystem of theIndustry of PrivateEquity and VentureCapital. This in order toincorporate bestpractices in theindustry, throughactivities for investors,managers,companies and otherindustry players

Program Components Main objectives

Encourage access to financial services to the unbanked

colombian population, specially to the low-income

families, with the purpose of enhancing the country´s

development and promote social equity.

Mission – Banca de las Oportunidades

1. Macro-intervention or Environment and Regulation to promote access to financial services

It comprises the actions that aim to strengthen the environment in which the financial activities are developed and the regulatory framework of institutions that operate in it, in order to facilitate and promote access to financial services and microfinance.

2. Intermediate Intervention or Financial Services Support to Supply and Demand

It consists on activities that support services to the network entities in order to promote narrowing the gap between supply and demand. The role of the Banca de las Oportunidades involves the management and the allocation of resources for projects that have a cross-sectional impact, namely that they can benefit all suppliers of financial services allowing them to provide better services to the policy’s target population.

3. Micro-Intervention or Support to the Network of Banca de las Oportunidades

It includes the support activities to entities that belong to the network of Banca de las Oportunidades (credit institutions, credit unions and NGOs), providing incentives that motivate them to expand and make financial services massif. Banca de las Oportunidades designs and allocates incentives to: share the cost of the expansion of services when considered that its utility will not cover the costs, to decrease the risk perceived by these entities when entering into certain segments or to provide knowledge for the implementation of certain types of products.

Strategy

CORRESPONSALES NO BANCAROS

3.908

NON-BANKING AGENTS

9.458

No. DESEMBOLSOS A MICROEMPRESAS2.330.184 millones

LOANS TOMICROFIRMS

6.7 million

MICROEMPRESARIOSACCEDIENDO A

CREDITO POR 1a VEZ774.247

FIRST TIME LOANSTO MICROFIRMS

1.884.106

VALOR DESEMBOLSOSA MICROEMPRESAS

COP 7,2 billones

DISBURSEMENTSTO MICROFIRMS

COP 19 billion

Results

(September 30 de 2010) (August 2006 – September 2010)

(August 2006 – November 2010) (August 2006 – November 2010)

Contact us

Fernando EsmeralChief Commercial Officer(57-1) 382 15 15 ext [email protected] Cristina VandameChief Financial Officer(57-1) 382 15 15 ext [email protected] GarcíaChief Operations Officer(57-1) 382 15 15 ext [email protected]

Mauro SartoriRisk Chief Officer(57-1) 382 15 15 ext [email protected]

Cesar PérezNational Commercial Director(57-1) 382 15 15 ext [email protected]

Doris ArévaloBusiness Inteligence Director(57-1) 382 15 15 ext [email protected]

Alejandro ContrerasInternational Banking Director (57-1) 382 15 15 ext [email protected]

Pedro Julio VillabónLocal Banking Director(57-1) 382 15 15 ext [email protected]

Carlos Alberto MoyaBanca de las Oportunidades Program Director(57-1) 241 02 [email protected]

Hernando CastroMicrofirm Banking Director(57-1) 382 15 15 ext [email protected]

Jimeno PerdomoChief Administrative Officer(57-1) 382 15 15 ext [email protected]

José Alberto GarzónGeneral Secretary(57-1) 382 15 15 ext [email protected]

María Cristina AlbarracínPrivate Equity Director(57-1) 382 15 15 ext [email protected] GonzalezTreasury Director(57-1) 382 15 15 ext [email protected] UribeCooperation Director (57-1) 382 15 15 ext [email protected]

Bogotá :

Calle 28 No 13A-15, floors 38 to 42Phone: (57-1) 382 15 15Fax: (57-1)286 24 51 / (57-1)286 0237Working Hours (monday to friday): from 8:00 a.m. to 5:00 p.m.

E-mail web master: [email protected]_________________________________

SWIFT: BCEXCOBB_________________________________

Contact usCall Center Multicontacto Bancóldex Bogotá: (57-1) 6 49 71 00Toll free Number: (57-1) 01 8000 91 53 00

Contact us

![[Gokigenyou]_Creo the Crimson Crises_Cap.5,5](https://static.fdocuments.in/doc/165x107/577cd1391a28ab9e7893e9f7/gokigenyoucreo-the-crimson-crisescap55.jpg)